Constraint Propagation influenced by Dr. Rina Dechter, “Constraint Processing”

1

CONSTRAINT TO TECHNOLOGY ADOPTION- ROLE OF

CREDIT AND FINANCIAL INCLUSION

Report Submitted to

INTERNATIONAL CROPS RESEARCH INSTITUTE FOR THE SEMI-ARID TROPICS,

PATANCHERU, INDIA.

By

AMIT KUMAR

International Crops Research Institute for the Semi-Arid Tropics

Patancheru, 502 324

Andhra Pradesh, India

July 2012

2

Declaration

I do hereby declare that the dissertation entitled upon” constraint to technology

adoption- role of credit and financial inclusion” is an original and independent

record of project work undertaken by me under the supervision of Dr. MCS

Bantilan, Director, MIP (Market, Institutions and Policies) and Dr. D Kumara

Charyulu, Scientist. MIP (Market, Institutions and Policies) at International

crops research institute for the semi arid tropics (ICRISAT), Patancheru, India,

during the period of my study as a part of masters in Agri-Business Economics.

Hyderabad By

Date: - 12/07/12 Amit Kumar

3

Abstract

This paper makes a successful attempt to check the impact of credit on technology adoption.

Presently, Indian Agriculture is facing an economic condition of constant returns to scale but

its dependency is at its peak, thanks to the ever-rising population of this country. Use of

modern technology can help in boosting the growth and production but technology has a cost

attach to it, which most of the Indian farmers are unable to bear. Timely and efficient supply

of credit to all the cultivators especially the poorest of them is the only feasible solution we

have but this could only be possible if the rate of financial inclusion is increased. Financial

inclusion refers to providing banking solutions to the poorest of poor’s. Beside these, the

present study assessed the state of financial inclusion in Maharashtra as well as in ICRISAT

VLS villages through secondary as well as primary information. Finally, this study has

brought out the various real time problems faced by the farmers of Kinkheda and kanzara

villages and have provided with some solutions for immediate relief.

Title : CONSTRAINT TO TECHNOLOGY ADOPTION- ROLE OF CREDIT

AND FINANCIAL INCLUSION

Name : AMIT KUMAR

Institute : GOKHALE INSTITUTE OF POLITICS AND ECONOMICS, PUNE, INDIA

Supervisors : Dr. MCS BANTILAN and Dr. D KUMARA CHARYULU

Submitted : 12th

July 2012

4

ACKNOWLEDGEMENTS

I am highly grateful to Dr. MCS Bantilan, Director, Market Institutions and Policy (MIP),

ICRISAT for kindly giving me this opportunity to do my project as a part of my academic

schedule. Her constant supervision and timely advice will always be remembered with a deep

sense of gratitude.

I express my heartfelt gratitude and indebtedness to Dr. Kumara Charyulu, Scientist, Market

Institutions and policies (MIP), ICRISAT for his constant encouragement to all. He regulates

healthy research environment and interactivity. I am grateful to the learning system unit

(LSU) at ICRISAT, for providing me an opportunity to join an institute of international repute

and excellence in research.

I wish to express my thankfulness to officers of Bank of Maharashtra for providing me with

timely and acute data on financial inclusion. I pay my gratitude to Mr. Chopde (Senior

Scientific officer), who accompanied me all the way throughout my work and for his constant

help and support.

My special thanks to Mr. Ajay (Assistant field supervisor, Kanzara) and Mr. Sachin (Assistant

field supervisor, Kinkheda) for their help and support during my field visit. I would also like

to thank Mr. Anand, Mr. Likhitihkar and all the scientists at ICRISAT for their appreciable

help and support.

I would like to thank all my fellow interns for their coordination and for sharing knowledge

with me during my internship.

I also take this opportunity to thank my parents, god and everyone who had been a great help

and support throughout my dissertation.

5

Table of Contents Introduction ................................................................................................................................. 6 Recent scenario in rural indebtedness and agricultural credit ................................ 7 RBI initiatives for financial inclusion ................................................................................. 9 Present Scenario ....................................................................................................................... 10 Macro level Picture- A pan India study............................................................................. 11 Literature Review .................................................................................................................... 14 Research objective ................................................................................................................... 15 Methodology .............................................................................................................................. 15 State level study- Maharashtra............................................................................................ 16 Results and Discussions ......................................................................................................... 17 Impact of Credit on technology adoption ........................................................................ 19 Regression Analysis ................................................................................................................ 22 Constraints ................................................................................................................................. 24 Special Recommendation ...................................................................................................... 29 Replace Insurance with future market ............................................................................ 29 Working of the co-operatives .............................................................................................. 30 Conclusion................................................................................................................................... 30

Bibliography ..................................................................................................................... 32

Annexure ........................................................................................................................... 33

6

Introduction

Technology as defined is the application of scientific knowledge for practical purposes. The

first use of technology way backs to the period when man converted the natural resources into

simple tools. Since then, technology has seen a many fold change and development. Nearly

70 percent of India’s population (National Sample Survey Organization, 2005) is dependent

upon Agriculture sector. Agricultural technology has been a primary factor contributing to the

increase in farm productivity over the past half-century but we are still far behind our

potential. Stagnation and a negative return to scale are the key features of present Agriculture.

One important reason for the present pitiful condition is the non-acceptability of technology

and lack of credit for the farmers. Rural credit has a very important function of minimizing

the domain of in-equality. Credit is the soul of any business or enterprise. Timely availability

of credit can uplift the condition and take the growth to the next level. Meeting the credit

demand and increasing the acceptability of the new technologies can uplift the Indian

Agriculture as it has done in the past during the Green Revolution.

Agriculture in India has always been dependent on monsoons and thus it’s a risky activity.

The credit provision to agriculture sector started when the government started extending

credit in the times of drought. According to the studies done in 1936 and 1937, the

moneylenders disbursed the entire credit to agriculture and the cooperatives and other

institutional sources contributed very little. Nationalization of major commercial banks took

place in 1969, which acted as a step to increase the credit to agriculture from the commercial

banks. Later, Agriculture became a ‘priority sector’ and it became mandatory for banks to

extend credit to it. It was also felt that there is a need for separate banking in the agriculture

sector and thus Regional Rural Banks were set up in 1977 and National Bank for Agriculture

and Rural Development (NABARD) was set up in 1982. The scenario improved after this and

share of institutional credit increased from 7% in 1951 to 66% in 1991.

The main objective of this research is to study the role of credit and financial inclusion in

enhancing the acceptability of technology in Agriculture. Secondarily the study would like to

know the Constraints in the availability of finance and rural credit in my selected sample.

With time the availability of finance is improving, Public and Private player are working

7

together for this purpose but still there are many in the societies, who are deprived of this.

Women’s especially faces a constraint while making use of the formal loans. In rural India,

Women’s are responsible for enhancing the standard of living of the family. They are an

important part of the society and optimal growth of SAT Agriculture is greatly dependent on

their growth. With all these, I would like to give an overview and work toward providing a

credit plus solution for improving the availability of credit for the farmers and enhancing the

agriculture in Semi Arid Tropics.

Recent scenario in rural indebtedness and agricultural credit

Despite the increase in the number of rural branches of commercial banks, rural cooperative

banks and regional rural banks, the problem of rural indebtedness is still very severe and it

can be confirmed by the alarming increase in the number of farmer suicides in India.

According to the Report of ‘Expert group on agricultural indebtedness, 2007’, the share of

non-institutional sources in debt of cultivator households has increased from 30.6% in 1991 to

36.8% in 2002(Expert group on agriculture indebtness, 2007). One key reason for this fate is

the large dependency of farmers on monsoon for agriculture production. Beside this, most of

the farmers depend on non-institutional sources of credit where the cost of borrowing is very

high. The farmers don’t prefer to borrow from the formal sources because the banking

services are poor and there’s always a delay in disbursement of loan i.e. around 33 weeks is

required for loan approval in commercial banks. The commercial banks are also reluctant to

lend to small and marginal farmers because of their low credit worthiness and high risk of

default.

A recent policy initiative of doubling of agricultural credit policy (DACP) was introduced in

2004-05 in which it targeted to double the agricultural credit in 3 years. According to the

report of the ‘Task force on credit related issues of farmers’ published by NABARD in 2010,

the target had been achieved in 2 years but the credit allocations were not balanced in terms of

regions and size of farmers (Task force on credit related issues of farmers, 2010). Small and

marginal farmers were neglected and southern states got most of the share. The report also

suggested that most of the credit disbursement was in the month of March. Ideally, it should

have been before beginning of ‘rabi’ and ‘kharif’ seasons. Thus we can doubt if the

agricultural credit is being used for the correct purposes.

8

Another policy initiative was the introduction of Kisan Credit Card (KCC) in 1998-99. This

was supposed to increase the flexibility of credit for the farmers. According to the report,

which has reviewed the working of KCC and was published by NABARD in 2010, the KCC

hasn’t been working in the desired direction because 19% of the sample of farmers taken

weren’t aware of the benefits and utilities of the card (Working of KCC, 2010). 68% of the

farmers thought it to be a ‘one-shot operation’ and didn’t know that it can be used for a

number of withdrawals within the credit limit, and 48% of the farmers said that the credit

received under KCC was inadequate. Thus, it can be concluded from the review that KCC

hasn’t been operating in accordance with the purpose for which it was created.

In 1992, NABARD introduced the SHG-bank linkage project under the microfinance

institutions. But the distribution of SHGs has been skewed across the states and more than

50% of them have been concentrated in the southern states. According to a report published

by NABARD in 2010 on the evaluation of SHGs, there has been a problem of insufficient

backward linkages in the micro-enterprises (MEs), which are very important for the running

of the MEs (Evaluation of self help gropus, 2010). The Agricultural Debt Waiver and Debt

Relief Scheme (ADWDRS) was launched in 2008 in which the government promised that

agricultural loans, which were given to small farmers after 1st of April 1997 and were

outstanding on March 31 2007, should be written-off. According to the report of the task

force by NABARD, a number of farmers haven’t benefited from the scheme because their

agricultural loans were counted as ‘other’ loans and thus weren’t written-off. The farmers

who had taken loans prior to 1 April 1997 didn’t benefit and felt cheated and are also not

eligible to take fresh loans. Another reason for low benefits of the scheme is the fact that a

majority of small defaulters depend on non-institutional sources of credit and such loans

weren’t included in the scheme.

Thus the conclusion that can be drawn from reviewing the policy initiatives taken by the

government is that a lot needs to be done for achieving equitable credit disbursement to the

agricultural sector in India. Also, strong emphasis should be laid on mitigating the risk

involved in agriculture and reducing the dependence of small farmers on non-institutional

sources of credit.

9

RBI initiatives for financial inclusion

Providing banking facility to the poorest of poor is the latest goal of RBI. The Central bank of

India in collaboration with NABARD has brought in few initiatives to improve the inclusion.

The following are few of them:

No-Frill accounts: In November 2005, RBI asked banks to offer no-frills savings

account, which enables excluded people to open a savings account. Normally, the

savings account requires people to maintain a minimum balance but No-frills account

requires no balance. The number of no-frills account has increased mainly in public

sector banks from about 0.4 million to 6 million between March 2006 and March

2007. The number of No-frill accounts in private sector banks also increased from 0.2

million to 1 million in the same period.(Agarwal, 2008)

Usage of Regional language: The Banks were required to provide all the material

related to opening accounts, disclosures etc. in the regional languages.

Simple KYC Norms: In order to ensure that persons belonging to low income group

both in urban and rural areas do not face difficulty in opening the bank accounts due to

the procedural hassles, the Know Your Customer procedure for opening accounts has

been simplified for those persons who intend to keep balances not exceeding rupees

fifty thousand in a year.

Easier Credit facilities: Banks have been asked to consider introducing General

purpose Credit Card (GCC) facility up to Rs. 25,000/- at their rural and semi urban

branches.

Other rural intermediaries: Banks were permitted in January 2006, to use other rural

organizations like Non- governmental organizations, self-help groups, micro-finance

institutions etc. for furthering the cause of financial inclusion.

Using Information Technology: A few Pilot projects have been initiated to test how

technology can be used to increase financial inclusion. UshaThorat in her speech (June

19, 2007) pointed to a few measures:-

1. Smart cards for opening bank accounts with biometric identification.

2. Link to mobile or hand held connectivity devices ensure that the transactions

are recorded in the bank's books on real time basis.

3. The use of IT also enables banks to handle the enormous increase in the

volume of transactions for millions of households.

10

Financial Education: RBI has taken number of measures to increase financial literacy

in the country. It has set up a multilingual website in 13 languages explaining about

banking, money etc. It has started putting up comic strips to explain various difficult

subjects like importance of saving, RBI's functions etc.

Present Scenario

Despite all the efforts, the present scenario in the Indian economy is not good. Policies are

there but their efficient working is a big question mark. To provide the poorest of poor with

banking facility, first we need to reach them. Infrastructure bottlenecks are the biggest hurdle

in this path. The following are some key highlights of Indian economy-

51.4% of farmer households are financially excluded from both formal / informal

sources. (Agarwal, 2008)

Of the total farmer households, only 27% access formal sources of credit; one third of

this group also borrows from non-formal sources.(Agarwal, 2008)

Overall, 73% of farmer households have no access to formal sources of credit.

(Agarwal, 2008)

Exclusion is most acute in Central, Eastern and Northeastern regions - having a

concentration of 64% of all financially excluded farmer households in the country.

Marginal farmer households constitute 66% of total farm households. Only 45% of

these households are indebted to either formal or non-formal sources of

finance.(Agarwal, 2008)

About 20% of indebted marginal farmer households have access to formal sources of

credit.

Among non-cultivator households nearly 80% do not access credit from any source.

36% of ST Farmer households are indebted (SCs and Other Backward Classes - OBC

- 51%) mostly to informal sources.

Source:- (Agarwal, 2008)

11

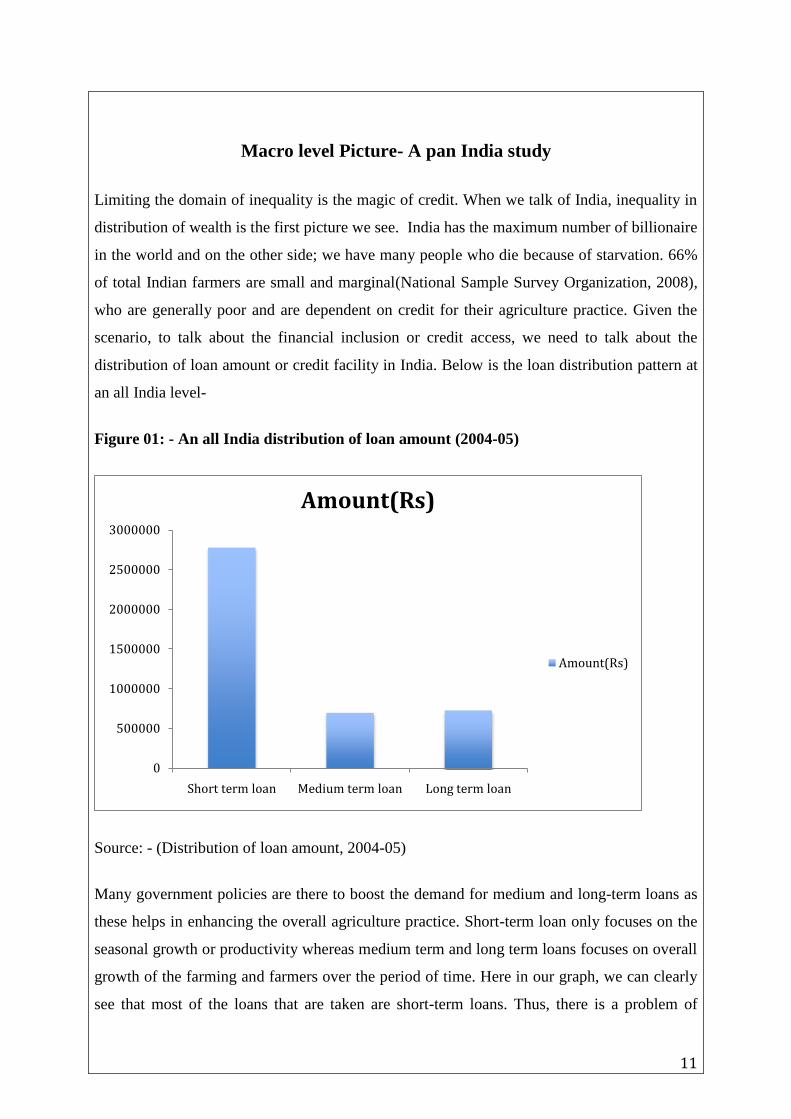

Macro level Picture- A pan India study

Limiting the domain of inequality is the magic of credit. When we talk of India, inequality in

distribution of wealth is the first picture we see. India has the maximum number of billionaire

in the world and on the other side; we have many people who die because of starvation. 66%

of total Indian farmers are small and marginal(National Sample Survey Organization, 2008),

who are generally poor and are dependent on credit for their agriculture practice. Given the

scenario, to talk about the financial inclusion or credit access, we need to talk about the

distribution of loan amount or credit facility in India. Below is the loan distribution pattern at

an all India level-

Figure 01: - An all India distribution of loan amount (2004-05)

Source: - (Distribution of loan amount, 2004-05)

Many government policies are there to boost the demand for medium and long-term loans as

these helps in enhancing the overall agriculture practice. Short-term loan only focuses on the

seasonal growth or productivity whereas medium term and long term loans focuses on overall

growth of the farming and farmers over the period of time. Here in our graph, we can clearly

see that most of the loans that are taken are short-term loans. Thus, there is a problem of

0

500000

1000000

1500000

2000000

2500000

3000000

Short term loan Medium term loan Long term loan

Amount(Rs)

Amount(Rs)

12

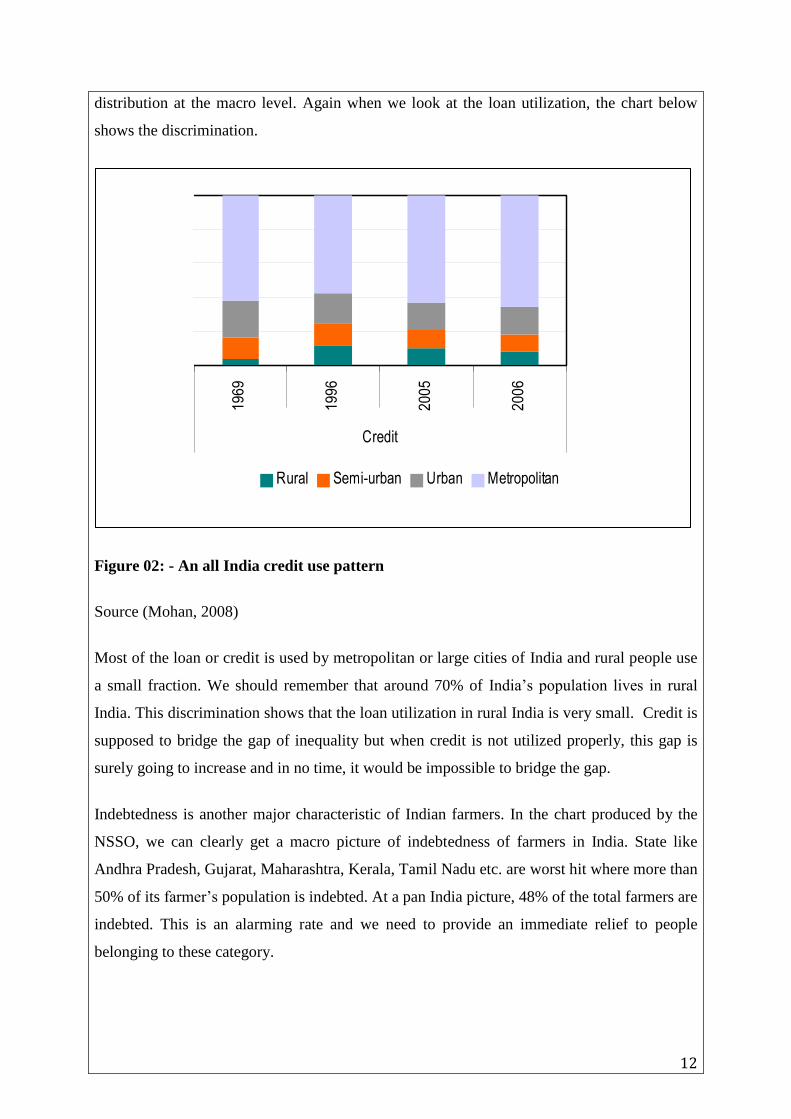

distribution at the macro level. Again when we look at the loan utilization, the chart below

shows the discrimination.

Figure 02: - An all India credit use pattern

Source (Mohan, 2008)

Most of the loan or credit is used by metropolitan or large cities of India and rural people use

a small fraction. We should remember that around 70% of India’s population lives in rural

India. This discrimination shows that the loan utilization in rural India is very small. Credit is

supposed to bridge the gap of inequality but when credit is not utilized properly, this gap is

surely going to increase and in no time, it would be impossible to bridge the gap.

Indebtedness is another major characteristic of Indian farmers. In the chart produced by the

NSSO, we can clearly get a macro picture of indebtedness of farmers in India. State like

Andhra Pradesh, Gujarat, Maharashtra, Kerala, Tamil Nadu etc. are worst hit where more than

50% of its farmer’s population is indebted. At a pan India picture, 48% of the total farmers are

indebted. This is an alarming rate and we need to provide an immediate relief to people

belonging to these category.

13

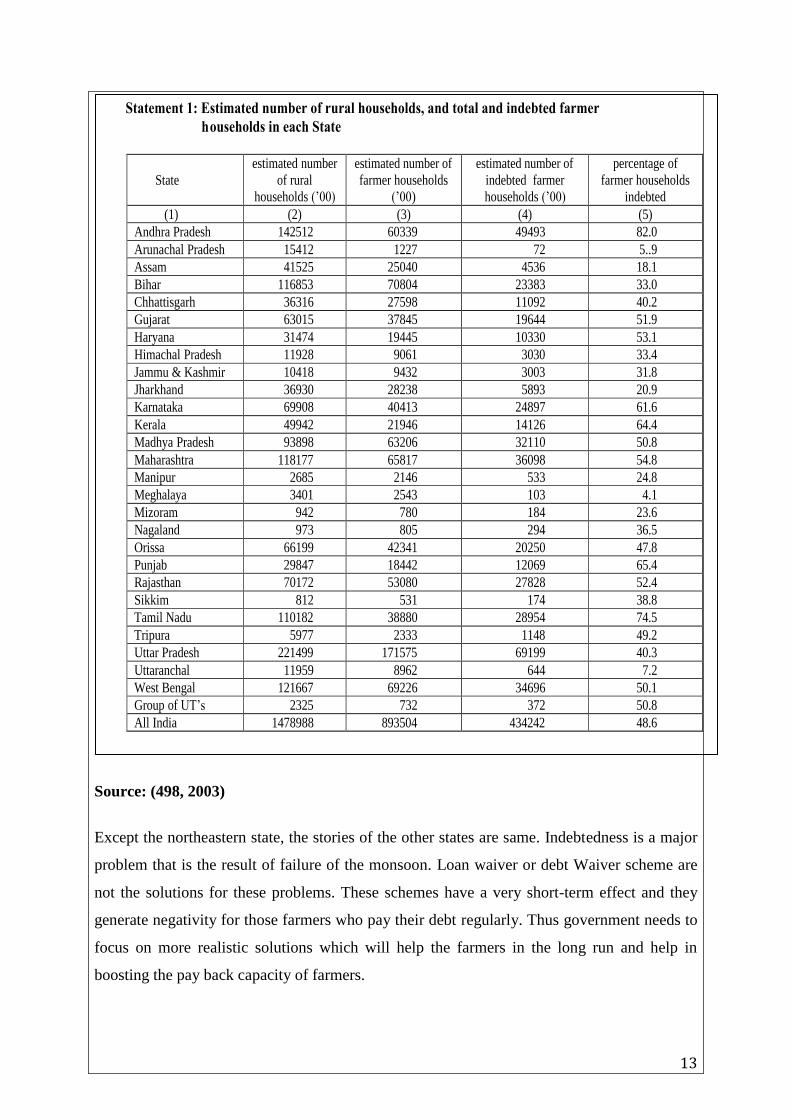

Source: (498, 2003)

Except the northeastern state, the stories of the other states are same. Indebtedness is a major

problem that is the result of failure of the monsoon. Loan waiver or debt Waiver scheme are

not the solutions for these problems. These schemes have a very short-term effect and they

generate negativity for those farmers who pay their debt regularly. Thus government needs to

focus on more realistic solutions which will help the farmers in the long run and help in

boosting the pay back capacity of farmers.

NSS Report no. 498: Indebtedness of Farmer Households, 2003

10

3.1 Geographical distribution of total and indebted farmer households: Statement1

shows estimated number of rural households, farmer households, indebted farmer households

and percentage of farmer households indebted in each of the states. At all-India level, an

estimated 60.4% of rural households were farmer households and of them 48.6% were

reported to be indebted. The incidence of indebtedness was highest in Andhra Pradesh

(82.0%), followed by Tamil Nadu (74.5%), Punjab (65.4%), Kerala (64.4%), Karnataka

(61.6%) and Maharashtra (54.8%). Moreover, Haryana, Rajasthan, Gujarat, Madhya Pradesh

and West Bengal each had about 50 to 53% farmer households indebted. States with very low

proportion of indebted farmer households were Meghalaya, Arunachal Pradesh and

Uttaranchal. In each of these States less than 10% farmer households were indebted.

In absolute terms, out of an estimated 43.4 million indebted farmer households, 6.9

million belonged to Uttar Pradesh, 4.9 million to Andhra Pradesh, 3.6 million to Maharashtra,

3.5 million to West Bengal and 3.2 million to Madhya Pradesh. More than half of the

indebted farmer households belonged to th ese five States.

Statement 1: Estimated number of rural households, and total and indebted farmer

households in each State

State

estimated number

of rural

households (’00)

estimated number of

farmer households

(’00)

estimated number of

indebted farmer

households (’00)

percentage of

farmer households

indebted

(1) (2) (3) (4) (5)

Andhra Pradesh 142512 60339 49493 82.0

Arunachal Pradesh 15412 1227 72 5..9

Assam 41525 25040 4536 18.1

Bihar 116853 70804 23383 33.0

Chhattisgarh 36316 27598 11092 40.2

Gujarat 63015 37845 19644 51.9

Haryana 31474 19445 10330 53.1

Himachal Pradesh 11928 9061 3030 33.4

Jammu & Kashmir 10418 9432 3003 31.8

Jharkhand 36930 28238 5893 20.9

Karnataka 69908 40413 24897 61.6

Kerala 49942 21946 14126 64.4

Madhya Pradesh 93898 63206 32110 50.8

Maharashtra 118177 65817 36098 54.8

Manipur 2685 2146 533 24.8

Meghalaya 3401 2543 103 4.1

Mizoram 942 780 184 23.6

Nagaland 973 805 294 36.5

Orissa 66199 42341 20250 47.8

Punjab 29847 18442 12069 65.4

Rajasthan 70172 53080 27828 52.4

Sikkim 812 531 174 38.8

Tamil Nadu 110182 38880 28954 74.5

Tripura 5977 2333 1148 49.2

Uttar Pradesh 221499 171575 69199 40.3

Uttaranchal 11959 8962 644 7.2

West Bengal 121667 69226 34696 50.1

Group of UT’s 2325 732 372 50.8

All India 1478988 893504 434242 48.6

14

Review of Literature

Credit is one of the most common topics of the present times. Whether it’s the newspaper,

textbooks or magazines, credit and its problems are the favorite topics of everyone. My basic

understanding of the topic can be credited to my formal course work at the masters

programmed in GIPE. Beside that, the following are some other sources, which helped me

getting a wider knowledge of the topic and finding my research objectives for the two months

at ICRISAT-

State of Indian Farmer- Surjit Singh &VidyaSagar (2004): -This book helped in

developing the basic insight upon the credit system of India. It talked about evolution

of credit institutions and delivery mechanism. Changes in government policies toward

agriculture credit and evolution of credit system in India. This book also talked on the

performance of Present Credit Delivery mechanism whereby they brought in the

recent performance of Commercial banks, RRB’s, etc. At the conclusion it shed some

light on topics like Crop Insurance, MSP reforms, and Agriculture Credit through

Micro-Finance.

Presidential Address by Shri. Y.S.P. Thorat- on ‘Rural Credit in India; Issues and

Concern: - This article by Mr. Thorat gave an insight on the real present situation in

India. All the major issues related to disbursement of credit were clearly mentioned in

this article. Some major problems mentioned by him were Inadequacy of credit,

Constraints on timely availability of credit, High interest rates, Neglect of small and

marginal farmers, Low credit-deposit ratios in several states, Continued presence of

informal markets.

Rural Credit in India (Microfinance and self help Groups) - An Overview of History

and Perspective May 2011 by Deva raja: - The objective of this study was to examine

the overview of rural credit in India and to finds a remarkable continuity in the

problems faced by the poor throughout this period. With controversial results, both

supporting and not the assumption that microfinance can promote income generating

activities, this paper attempts to demonstrate the role of microfinance in rural credit in

India. These include dependence on usurious moneylenders and the operation of a

deeply exploitative grid of interlocked, imperfect markets. This did increase bank

15

profitability but at the cost of the poor and of backward regions. While the MFI model

of microfinance is unsustainable, the SHG-Bank Linkage approach can make a

positive impact on security and empowerment of the disadvantaged. Much more than

microfinance is needed to overcome the problems that have persisted over the last 100

years.

Research objectives

Based upon my readings of the literature, I felt that credit plays a very important role in

purchase and adoption of improved inputs. There was a clear picture that shows that when

credit is available a farmer has a better capacity to make use of new variety and technologies

and work toward enhancing his farm activities. One important thing, which I saw was that

there were many constraints in the path of optimal distribution of credit. Another key thing

which I found was that private players and self-help groups over the time has been working

toward enhancing the availability of credit and that women’s were discriminated by formal

sources for distribution of credit. But as I had a time constraint, I focused on two main

objectives-

Impact of credit on technology adoption.:- as my research has a primary focus on

technology, my first part of the research deals with Impact of credit on technology

adoption. Here technology is defined as new and high yielding variety of seeds.

Constraints in credit and financial inclusion: - when we talk about credit in

agriculture, no project can be complete without the inclusion of constraints. There are

many and I have tried to find some of them through my primary survey. These are the

real time constraints faced by the farmers.

Methodology

This research will be mainly based upon primary data collected from the selected villages of

Maharashtra. I plan to choose two ICRISAT villages to collect my primary data for the

research, as it’s the most feasible resource I could get given the time constraints. I will try to

divide the farmers into two categories whereby I would be looking at farmers who have

access to credit and at those, who have no access. Based upon the difference in characteristics,

I would like to prove my hypothesis using statistical tools and other available secondary data.

16

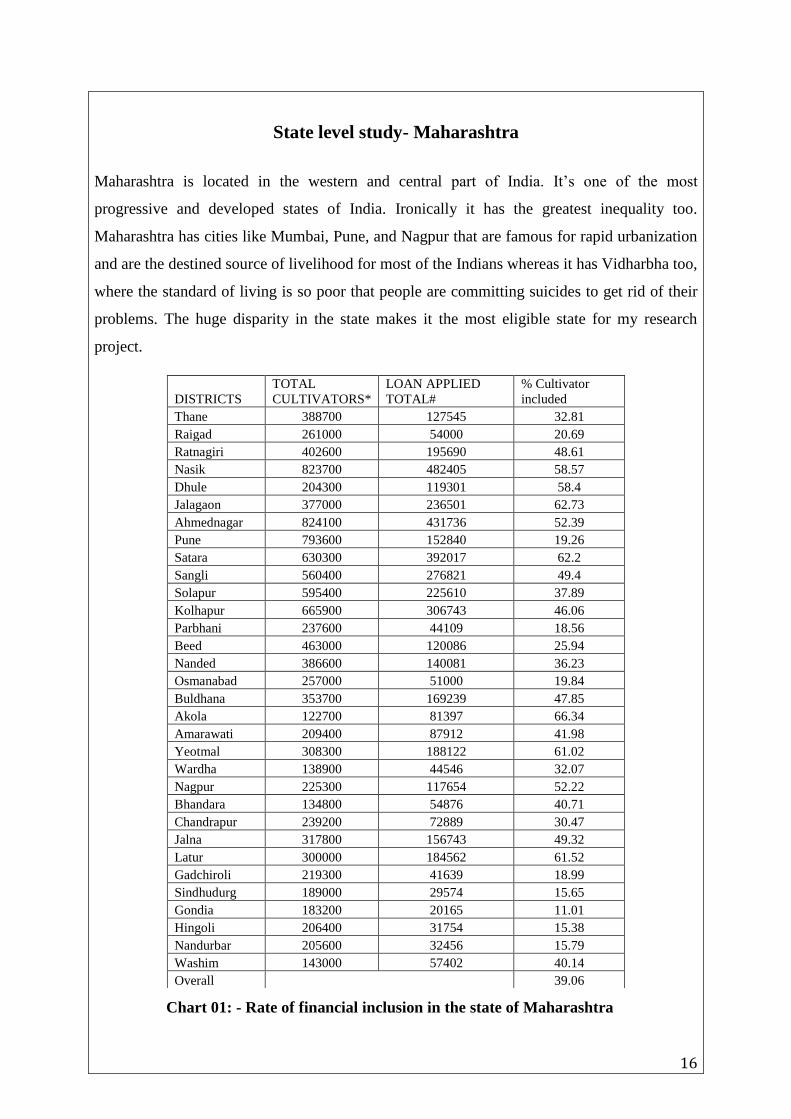

State level study- Maharashtra

Maharashtra is located in the western and central part of India. It’s one of the most

progressive and developed states of India. Ironically it has the greatest inequality too.

Maharashtra has cities like Mumbai, Pune, and Nagpur that are famous for rapid urbanization

and are the destined source of livelihood for most of the Indians whereas it has Vidharbha too,

where the standard of living is so poor that people are committing suicides to get rid of their

problems. The huge disparity in the state makes it the most eligible state for my research

project.

Chart 01: - Rate of financial inclusion in the state of Maharashtra

DISTRICTS

TOTAL

CULTIVATORS*

LOAN APPLIED

TOTAL#

% Cultivator

included

Thane 388700 127545 32.81

Raigad 261000 54000 20.69

Ratnagiri 402600 195690 48.61

Nasik 823700 482405 58.57

Dhule 204300 119301 58.4

Jalagaon 377000 236501 62.73

Ahmednagar 824100 431736 52.39

Pune 793600 152840 19.26

Satara 630300 392017 62.2

Sangli 560400 276821 49.4

Solapur 595400 225610 37.89

Kolhapur 665900 306743 46.06

Parbhani 237600 44109 18.56

Beed 463000 120086 25.94

Nanded 386600 140081 36.23

Osmanabad 257000 51000 19.84

Buldhana 353700 169239 47.85

Akola 122700 81397 66.34

Amarawati 209400 87912 41.98

Yeotmal 308300 188122 61.02

Wardha 138900 44546 32.07

Nagpur 225300 117654 52.22

Bhandara 134800 54876 40.71

Chandrapur 239200 72889 30.47

Jalna 317800 156743 49.32

Latur 300000 184562 61.52

Gadchiroli 219300 41639 18.99

Sindhudurg 189000 29574 15.65

Gondia 183200 20165 11.01

Hingoli 206400 31754 15.38

Nandurbar 205600 32456 15.79

Washim 143000 57402 40.14

Overall 39.06

17

Distribution of formal credit in India is a state subject. As already mentioned credit is the soul

of good agriculture practice therefore Indian government initiated a successful Lead bank

scheme to check efficient and sufficient distribution of formal credit in India. Under this

scheme, a single bank was selected as a lead bank in every district headquarters. This bank

was supposed to issue crop loans to the farmer and also check the functioning of other public

banks in the locality. Bank of Maharashtra is the lead bank in the state of Maharashtra and is

suppose to take care of distribution of credit in all the 35 districts. The data here is the

inclusion rate according to the state lead bank committee (SLBC) in the year 2011-12. Here

we have taken the number of farmers who have taken the loan in the past year and the number

of total cultivators in the area according to the census 2011. Based upon the data, we have

done few calculations to bring a macro level picture of distribution of credit in the state of

Maharashtra.

From the chart 01, we can see the coverage of formal financial institutes in the state of

Maharashtra. The state average is 39.06%, which means out of the total, 39.06% of the

farmers are covered under formal source of credit or made available with formal loan. Akola

is the best district where nearly 66% of its farmer population is covered under formal source

of credit and Gondia is the most excluded district where only 11% of its population is

included or covered under formal source of credit(State lead bank committee, 2012). The

inequality about which I have mentioned in the beginning can easily be seen here through this

data. For my research I was supposed to take Akola and Gondia as my sample but due to the

time constraint, I choose Akola as my sample district as the inclusion here is the greatest and

the impact on technology adoption could be easily deduced.

Results and Discussions

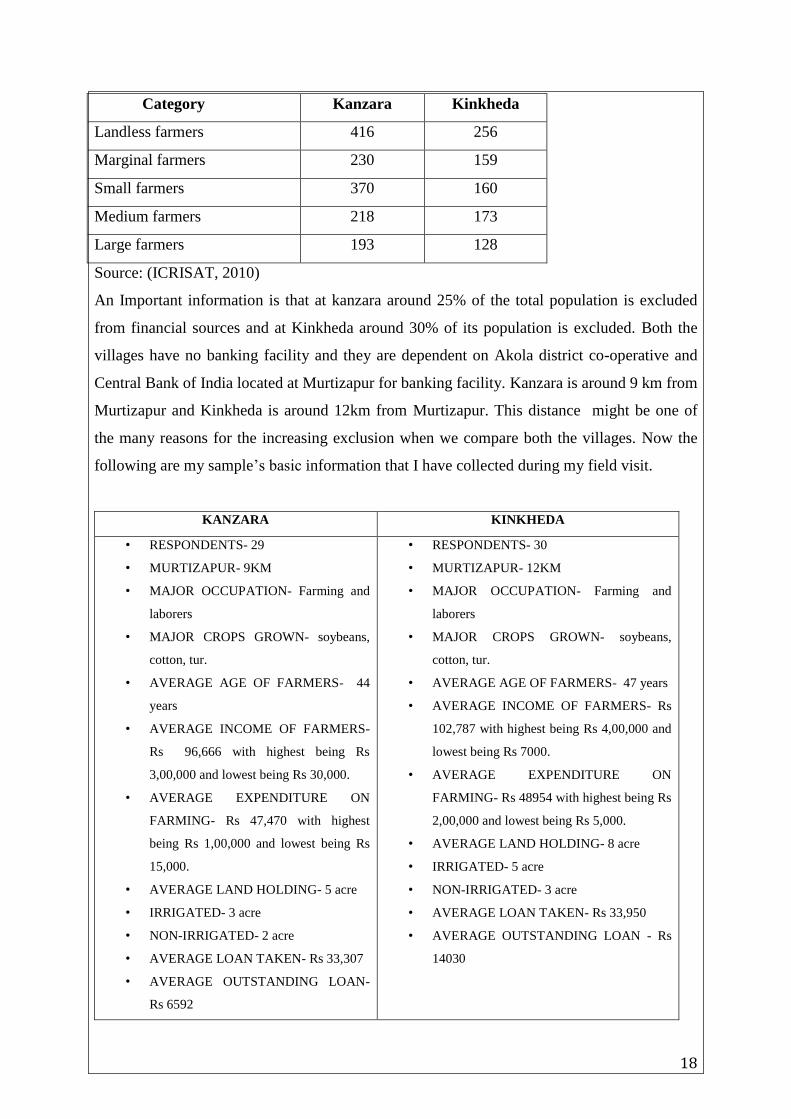

Kanzara and Kinkheda are the two villages in Akola that I have taken as my sample village.

Based upon my real time experience, I could conclude that Kanzara is a slightly better village

than kinkheda in term of availability of resources, standard of living and connectivity to the

nearest town. The following is the basic profile of farmers in the area-

18

Category Kanzara Kinkheda

Landless farmers 416 256

Marginal farmers 230 159

Small farmers 370 160

Medium farmers 218 173

Large farmers 193 128

Source: (ICRISAT, 2010)

An Important information is that at kanzara around 25% of the total population is excluded

from financial sources and at Kinkheda around 30% of its population is excluded. Both the

villages have no banking facility and they are dependent on Akola district co-operative and

Central Bank of India located at Murtizapur for banking facility. Kanzara is around 9 km from

Murtizapur and Kinkheda is around 12km from Murtizapur. This distance might be one of

the many reasons for the increasing exclusion when we compare both the villages. Now the

following are my sample’s basic information that I have collected during my field visit.

KANZARA KINKHEDA

• RESPONDENTS- 29

• MURTIZAPUR- 9KM

• MAJOR OCCUPATION- Farming and

laborers

• MAJOR CROPS GROWN- soybeans,

cotton, tur.

• AVERAGE AGE OF FARMERS- 44

years

• AVERAGE INCOME OF FARMERS-

Rs 96,666 with highest being Rs

3,00,000 and lowest being Rs 30,000.

• AVERAGE EXPENDITURE ON

FARMING- Rs 47,470 with highest

being Rs 1,00,000 and lowest being Rs

15,000.

• AVERAGE LAND HOLDING- 5 acre

• IRRIGATED- 3 acre

• NON-IRRIGATED- 2 acre

• AVERAGE LOAN TAKEN- Rs 33,307

• AVERAGE OUTSTANDING LOAN-

Rs 6592

• RESPONDENTS- 30

• MURTIZAPUR- 12KM

• MAJOR OCCUPATION- Farming and

laborers

• MAJOR CROPS GROWN- soybeans,

cotton, tur.

• AVERAGE AGE OF FARMERS- 47 years

• AVERAGE INCOME OF FARMERS- Rs

102,787 with highest being Rs 4,00,000 and

lowest being Rs 7000.

• AVERAGE EXPENDITURE ON

FARMING- Rs 48954 with highest being Rs

2,00,000 and lowest being Rs 5,000.

• AVERAGE LAND HOLDING- 8 acre

• IRRIGATED- 5 acre

• NON-IRRIGATED- 3 acre

• AVERAGE LOAN TAKEN- Rs 33,950

• AVERAGE OUTSTANDING LOAN - Rs

14030

19

As I have already mentioned that kanzara is slightly a better village, it can be seen from the

fact that the average outstanding loan for kinkheda is Rs 14,030 that is much greater than that

of kanzara, which is Rs 6592. Outstanding loans results in default and farmers artificially get

excluded from the formal source of credit ultimately resulting in financial exclusion. Again,

irrigated land is preferred over non-irrigated in terms of loan disbursement as there’s a higher

chance of recovery in irrigated area. Given my sample of 29 people who were using formal

source to borrow credit, 65% of the total were farmers having majority of their land holdings

in irrigated area. Beside this, most of the crop loan was used for crops like soybean and

Cotton.

Impact of Credit on technology adoption

The literature review that I followed and my discussions with my mentor and other scientists

at ICRISAT brought to me a single picture that credit has a positive impact on technology

adoption, which means given a timely and sufficient amount of credit supply, a farmer is able

to make use of better technology available for a particular crop. In my study, I have regarded

technology as new and high yielding variety of seed. The following were few key findings-

Importance of credit can easily be felt from the fact that on asking my 59 respondents that

what would they do, if no credit is available to them. It was surprising to see that only 27% of

the total farmers told me that they would continue farming. Rest would quit farming and lease

out their land, work as a laborer or migrate to some other place.

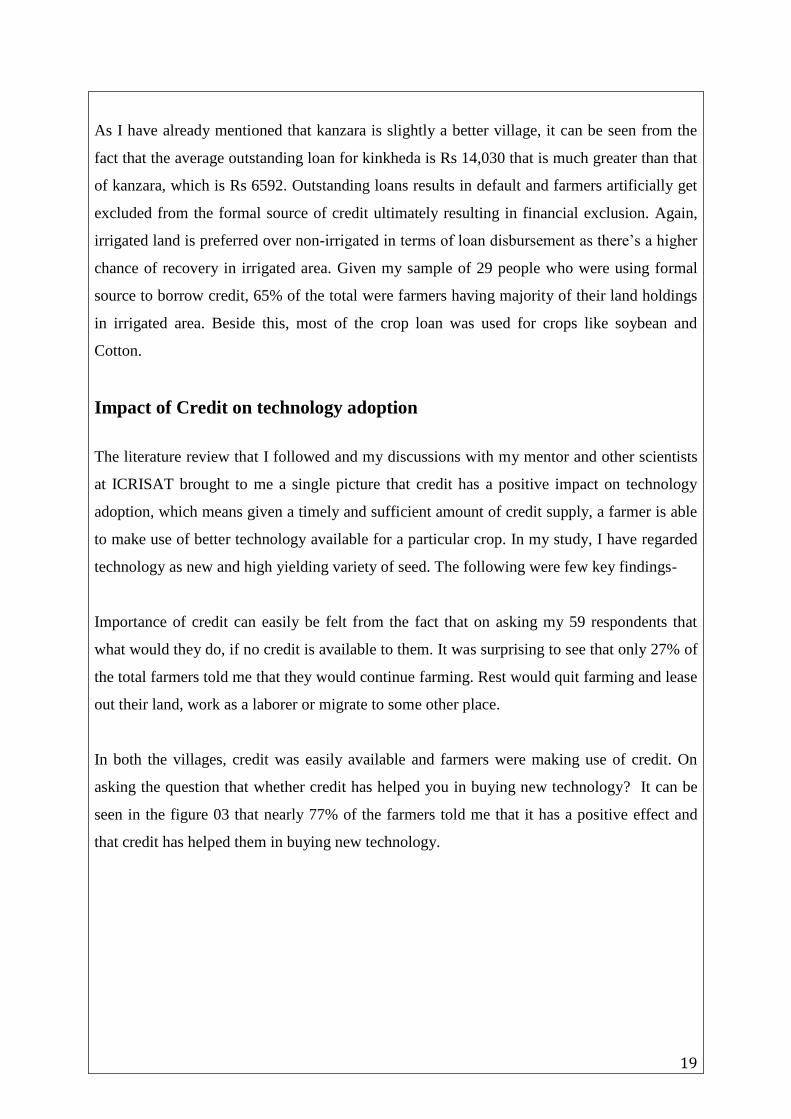

In both the villages, credit was easily available and farmers were making use of credit. On

asking the question that whether credit has helped you in buying new technology? It can be

seen in the figure 03 that nearly 77% of the farmers told me that it has a positive effect and

that credit has helped them in buying new technology.

20

Figure 03: - Results of farmers use of new variety of seeds

23% of the farmers who told me that they were not using new technology were mainly small

landless farmers and defaulters with no source of credit.

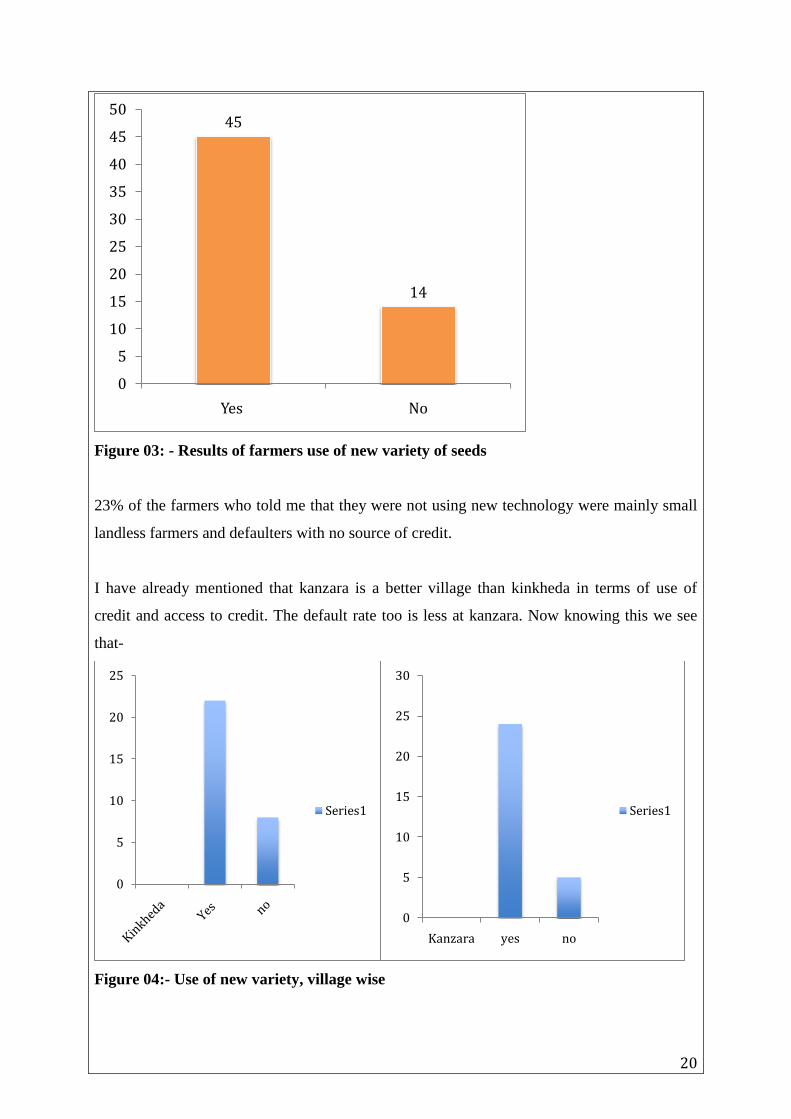

I have already mentioned that kanzara is a better village than kinkheda in terms of use of

credit and access to credit. The default rate too is less at kanzara. Now knowing this we see

that-

Figure 04:- Use of new variety, village wise

45

14

0

5

10

15

20

25

30

35

40

45

50

Yes No

0

5

10

15

20

25

Series1

0

5

10

15

20

25

30

Kanzara yes no

Series1

21

It’s clear from figure 04 that in kanzara, 83% of the farmers were using new technolgy and

only 17% said that they weren’t aware or using the new technology. Similarly at Kinkheda, it

was seen that 73.3% of the farmers used new variety and the rest said that they were not using

the new technology. Here we can see that at kanzara a propotionate more farmers were using

new variety of seeds compare to that in kinkheda. My sample size was very low due to the

time constraints but still we can get a micro level picture where it shows that credit has a

positive impact on adoption of technology. We can clearly see that at kinkheda more farmers

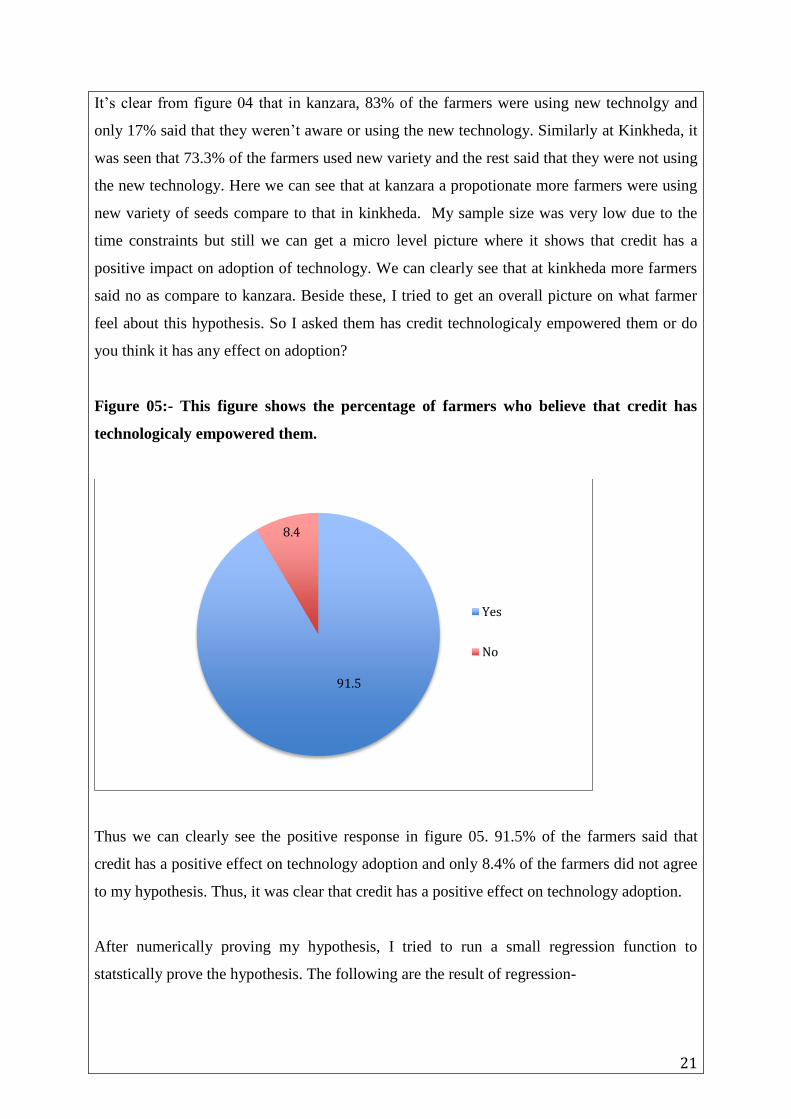

said no as compare to kanzara. Beside these, I tried to get an overall picture on what farmer

feel about this hypothesis. So I asked them has credit technologicaly empowered them or do

you think it has any effect on adoption?

Figure 05:- This figure shows the percentage of farmers who believe that credit has

technologicaly empowered them.

Thus we can clearly see the positive response in figure 05. 91.5% of the farmers said that

credit has a positive effect on technology adoption and only 8.4% of the farmers did not agree

to my hypothesis. Thus, it was clear that credit has a positive effect on technology adoption.

After numerically proving my hypothesis, I tried to run a small regression function to

statstically prove the hypothesis. The following are the result of regression-

91.5

8.4

Yes

No

22

Regression Analysis

Here, we have taken adoption as a function of many variables. Adoption is a dummy variable

and the function looks like-

A= F( x1,x2,x3,x4,x5,x6,x7)

Where,

A- Technology Adoption

X1- Farmer’s Age

X2- Land Holding

X3- Rainfed Holding

X4- Household Income

X5- Household Profit

X6- Amount Borrowed last year

X7- Outstanding Loan

Running the simple regression using Ordinary Least Square method, we get results as

follow-

R R SQUARE ADJUSTED R SQUARE

0.499 0.249 0.147

VARIABLE NAME COEFFICIENT T VALUE SIGNIFICANCE

AGE -0.267 -2.135 0.037

LANDHOLDING 0.142 0.526 0.601

DRY HOLDING -0.188 -1.147 0.257

AVERAGE

INCOME

0.161 0.212 0.833

NET PROFIT -0.118 -0.202 0.833

CREDIT 0.369 1.918 0.061

OUTSTANDING

LOAN

0.060 0.459 0.648

23

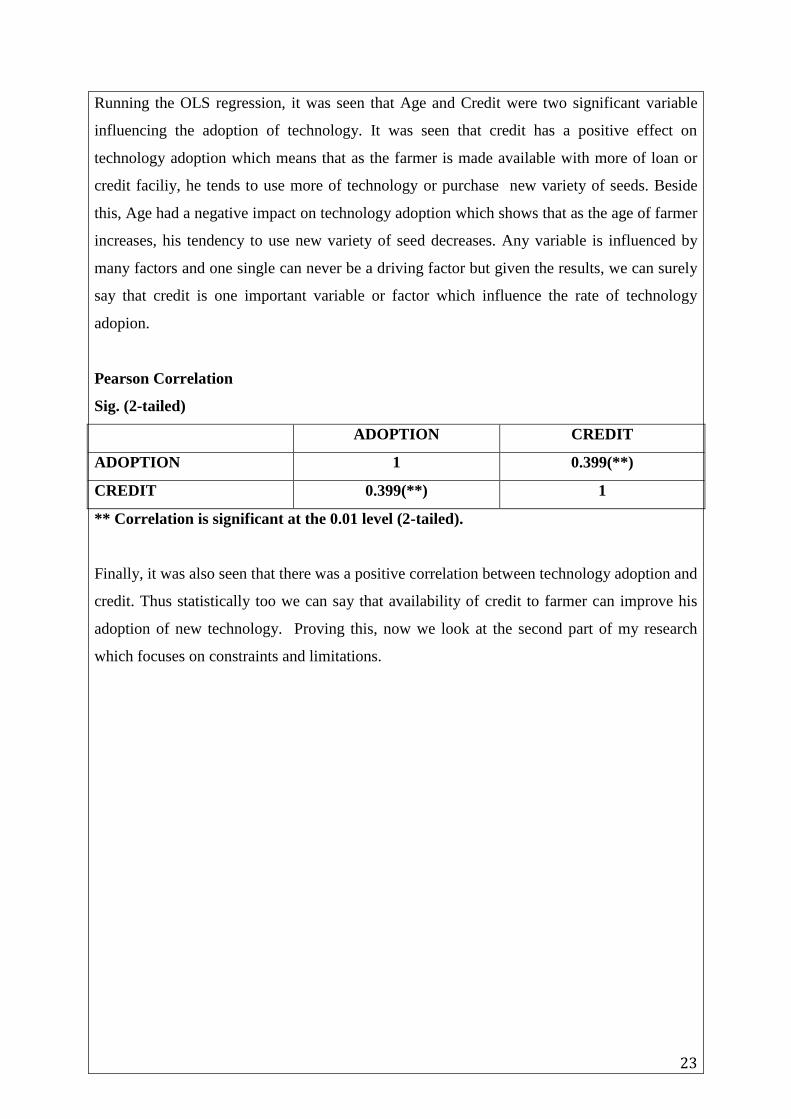

Running the OLS regression, it was seen that Age and Credit were two significant variable

influencing the adoption of technology. It was seen that credit has a positive effect on

technology adoption which means that as the farmer is made available with more of loan or

credit faciliy, he tends to use more of technology or purchase new variety of seeds. Beside

this, Age had a negative impact on technology adoption which shows that as the age of farmer

increases, his tendency to use new variety of seed decreases. Any variable is influenced by

many factors and one single can never be a driving factor but given the results, we can surely

say that credit is one important variable or factor which influence the rate of technology

adopion.

Pearson Correlation

Sig. (2-tailed)

ADOPTION CREDIT

ADOPTION 1 0.399(**)

CREDIT 0.399(**) 1

** Correlation is significant at the 0.01 level (2-tailed).

Finally, it was also seen that there was a positive correlation between technology adoption and

credit. Thus statistically too we can say that availability of credit to farmer can improve his

adoption of new technology. Proving this, now we look at the second part of my research

which focuses on constraints and limitations.

24

Constraints in Accessing Credit

When we talk about constraints, the list can be never ending. Literature,books, articles or let it

be any major findings on credit, there is always a special mention about constraints and

limitation. Credit being a state and sensitive subject, there are a lot of problems in its

distribution. The following are few important of them, which I think is worth mentioning.

Here I have divided the constraints into two . The first one are the problems which the farmers

say they have faced real time while taking the loans and the second part deals with problems

that I have deduced from my primary research findings.

Constraints faced by farmers-

Borrowing Credit from formal sources are lengthy and time taking process. It was

seen that on an average it took 15-30 days to take a loan. It’s almost impossible to get

the loan on time and this is then reflected by the fall in production and productivity.

Many farmers complained of delay in disbursement of loan. After a loan is being

sanctioned, it takes another week for disbursement.

Documentation process is large. To take a formal loan, n numbers of documents are

needed to be presented to the banker. No objection certificate and nodules are to be

collected by the farmer from all the other banks in the area, which is time consuming.

A farmers has to travel a lot for a formal loan to be sanctioned. His opportunity cost is

wasted. He could have used this time for cultivation but its wasted and not accounted.

Many farmers complained of bribe being asked by the officials for loan.

Many farmers complained of Amount of loan ibeing too low to make any long term

changes in farming practices. The amount alloted merely meet the basic input cost.

Credit is not at par with need. At least Rs 10,000 per acre must be provided which is

way higher than the present allotment of Rs 6000 per hectare.

Sources of credit are not enough and at the time of need, the demand is higher than

supply. Generally loan is required just before the kharif and rabi season. Thus at these

times, there is a sharp incraese in number of applications and the formal sources in the

area are not able to meet the rise in the demand.

25

Other limitation out of my research findings-

Awarness about the government programs and facilities. It was found that 42.3% of

the total farmers were not aware about the various government programs and schemes

and those who knew only a few had a experience of using their rights or making use of

the facility.

Another limitation arises in form of loan utilization pattern. Crop loan is issued for the

sole purpose of culivation of new crops. Most of the farmers being poor it was seen

that a part of the loan amount is used for household consumption too. This ultimately

results in fall in productivity and production as the alloted sum is not used to buy the

optimal amount of inputs. Another important thing that was seen in case of utilization

pattern was that when a farmer took a crop loan from formal sources, he used a part of

the sum for agriculture and other for household consumption but when a farmer took a

crop loan from non-formal sources, he used the whole sum for the agriculture itself.

Thus there was a disparity in the use of funds alloted from formal and informal

sources. One important fact for this situation is that the formal loan cost a farmer only

7% per annum whereas the same loan through informal sources cost a farmer anything

between 66% to 100% per annum.

Whenever we think of formal loan, nobody talks about the cost of loan or the cost that

is to be borne by the farmer in order to make use of this loan. Many will think that

there are no cost and if it exist, it would be negligible. To everyone’s surprise, it was

seen that 33% of the farmers had to pay from their pocket in order to make use of the

loan. Nearly every farmer in my sample has incurred some cost but these 33% of the

farmers had to pay more than 10% of the loan amount as cost to loan. Given the

condition of farmers, this 10% is a surprisingly great sum. For a loan of Rs 7000, in

monetary terms a farmer had to pay from Rs 750 to Rs 5000 as cost to loan. These

cost include many charges like travel,documents and bribe.

Womens are an important part of any society. Nearly 50% of the total population

consist of them. When we talk about formal loans to women, it was seen that no

women farmers were making use of the formal loan. Surprisingly, this was true

because by the nature of Indian law on land ownership, they were permenantly

disqualified. We already know that to make use of formal loan, the farmer has to keep

his land as a collateral. Here, when they have no land on their name, they have no

collateral and thus they are non-eligible for the formal loan.

26

Land is the true wealth of a farmer. Land values have appreciated in recent times and

are at the all time high. But inefficiency in government mechanism and illegal

registration of the land at lower price to avoid taxes have kept the prices of land lower

in government books and records. It was seen that many farmers were not happy with

the amount they are being offered against their collateral. They feel that the land value

is high and once the land papers are kept with the bank, the farmers couldn’t sell them

or use them to take other loans on it. Thus, they feel true value of the land must be

realised and loan or money should be given at par with the true market value.

Another important constraint which I found was artificial exclusion existing in the

village. I have used these term to define a situation, where banking facility is provided

but farmers aren’t able to make use of the facility. In my sample, 46% of the total

farmers were atificialy excluded from formal source of credit. Reasons for this

exclusion are default or outstanding loans, no colateral or landless farmers and land

not being registered on name of the farmers. Nearly 75% of the excluded farmers were

defaultes and thus were not eligible for new loans. It was followed by landless farmers

and land being not on the name of farmer. The worst hit of this scenario are the female

farmers, where hindu family law doesnot allow the land to be registered in the name of

females. Therefore they are by default excluded.

Again in case of defaulters it was seen that out of the total of 55% of the farmers belonged to

the category of farmers whose income were less than Rs 75000 per annum followed by high

income groups and in another category, 70% of the defaulters belonged to the category of

farmers whose landholdings were less than 8 acre. Thus we can see that small and poor

farmers are the most affected.

Lastly, it was found that the amount of loan or credit which is issued is not enough.

70% out of the total who were still making use of formal sources said that the loan

amount is not enough. Few important reasons for this unsatisfaction was the rising

prices of inputs over the time, black marketing of seeds in the open market and

inflated prices of fertilizers at the retail store.

Suggestions/ solutions: When there are problems,there are ought to be solutions to them.

I have found few solutions, of which some were listed by the farmers and some have been

deduced through my research. The following are the solutions-

27

Suggestions by the farmers

• There should not be disparity in allocation of fund between the irrigated and non-

irrigated land. It’s a common practice that irrigated land are preferred over non

irrigated during loan sanctioning practice. We should note that 55% of India’s

agriculture land is non-irrigated or rainfed. This discrimination would lead to

worsening of the agriculture situation in the coming times.

• The amount of loan in share per acre of land should be increased. At present it is Rs

6000 per acre. This sum as I have already mentioned is not sufficient for most of the

farmers. This sum need to increased to atleast Rs 10,000 per acre.

• Accessibility should be improved. There are many farmers who are artificialy

excluded. We should know that if this artificial exclusion rate is not checked, it could

lead to a crisis whereby most of the farmers could be in this cateogary and then the

government would have to waive of their loan at the cost of the tax payers money,

which is indeed unethical. There should be a special provisions for defaulters.

• Payments of loans in installment should be allowed and new loans should be issued

once certain part of the previous loan is paid. It was found that most of the farmers

have defaulted because at the stipulated time they lacked the total amount of money

that is to be paid to the bank. Banks should allow customized installments, whereby

farmer could choose his own slab depending upon his ability and there should be a

provision to give new loans once a certain pre-fixed part of the outstanding loan is

paid. Defaulting the farmer leads to his non access to formal credit and thus hampers

his agriculture gowth.

• Private banks should have more of participation. 18% priority sector lending is

mandatory for all the banks but its seen that most of the private and foreign banks

have failed to do so. Making a check on their efficient working could enhance the

supply of rural credit and would be definitely for the betterment of farmers in india.

• It was seen that most of the farmers faced a problem whereby they were not aware

about various government programs and their rights. Information center must be set up

at every district headquarter if not at every taluka where all the relevant information

must be provided to farmers free of cost. This would improve the farmers knowledge

and could also help in curbing the malpractices of bank officials.

28

• Lastly, Landless farmers should be provided with a source of Credit. A major portion

of Indian farmers belong to this category. Their condition will not improve until they

are provided with a formal source of credit.

Study recommendations:

• Small and medium size business must be promoted and loans for the same must be

issued. Farming alone cannot help the farmers as it’s a seasonal employment. In my

survey,I have seen that most of the farmers have a very low income and their standard

of living is poor. Providing them SME loans can improve the farmers livelihood.

• Farmers have a share in co-operatives. As a share holder, he should be given his

dividends on time and the working of the co-operative should be made transparent to

all the farmers or at least the member farmers.

• Credit plus approach must be used by the bank officials. This means the bank should

not only disburse the loan amount but also take care of the optimal and efficient

utilization of the loan. Once this method is applied, the amount of loan default and

defaulters will decrease and it will be a beneficial situation for both the bankers and

the farmers.

• Technology specific loans i.e. loans for tractors, seeds, micro irrigation etc must be

introduced. This will help a farmers in buying the much needed echnology which he’s

unable to use as the crop loan amount is barely enough to meet the tradition

requirements of farming.

• Most of the default is due to failure of monsoon. Banks can hedge this risk by linking

the production to future’s market. This will be beneficial for both the farmers and the

banks.

• Almost all the farmers have mobile phones. Therefore all the relevant information can

be send to them through a voice mail in the local language. This service would be free

of cost to the farmer and it won’t cost the government much. Nearly all the service

providers would be more than happy to provide this help under their CSR( Corporate

social resposibility) or on payment of small fee.

29

Special Recommendation

Based upon my primary survey and study, I have found few key things worth mentioning and

are listed here. Co-operatives and Crop insurance schemes are two critical things that are

supposed to uplift the condition of Indian farmers but sadly none of them are working to the

level they should. Co-operatives have a very high default rate whereas none of the farmers

have been benefited out of the mandatory crop loan scheme. There’s cost attached to all the

policies and this cost is borne by the taxpayers of this country. Inefficiency and failure at the

cost of billions of taxpayers is a serious problem and we need to do something to bring in an

optimal solution. I have tried listing some, which I feel can be beneficial to all stakeholders.

Replace Insurance with future market

Outstanding loans or defaults are the highest risk involved in rural credit. Many banks fail to

provide efficient supply of rural credit because they are worried about the recovery of loans.

Most of the default is due to failure of monsoon. Given a chance a farmer would always like

to pay back his outstanding loans because non payments leads to his non eligibility for new

loans and informal loans are very costly. Banks alone cant be blamed for rejecting the loan

applications because increasing number of defaults could lead to the bankruptsy of the bank.

At present when a farmer takes a loan, a certain part of his loan amount is taken back as a

premium to his crop insurance which is mandatory. But hardly, any farmer get compensated

due to the area approach followed by most of the insurance companies. So, what should be

done?

One solution to this problem can be hedging this risk by linking the production to future’s

market instead of the insurance. When the bank officials sanctions a loan to the farmer, they

should make an assumption of the profitable production. Now, the banker should buy the

subsequent production amount’s contract in the future market to be delivered in the future

date i.e. the date on which the farmer is suppose to reap his own production and for all this the

banker will have to pay a small premium. Now suppose the production fails due to the failure

of monsoon,then the banker can take the delivery of the production hedged and thus save the

farmer and bank both from the crisis and if the monsoon and production are normal then the

banker can breach the contract and he would loose the small premium which he has paid at

the beginning of the contract. This premium would be more or less equal to the insurance

30

premium amount. The only benefit is that here the farmer would be actually compensated for

the loss, he has incurred. This would definitely be a win-win situation for both the farmers

and the bankers.

Working of the co-operatives

During my field visit, I was surprised to know that most of the financial inclusion was not by

the National Banks but was by the Co-operatives in the area. Co-operative is a formal institute

wherein a farmer has to be a menber to make use of the loan or financial services. Once a

farmer takes a loan from the co-operative, 10% of his loan amount is taken back by the co-

operative and he’s been offered with a share in the co-operative of the equal worth. Again,

when a farmer default or if he’s not able to pay back the loan, he is termed as a defaulter and

is not made avaialble with any new credit.

Now, being a member of the co-operative a farmer has a right to sell back his old share in the

co-operative and from the money thus received, he should be able to convert his default

account into a regular by paying back the old sum which he has borrowed and defaulted.

Atleast that’s what a common person do,when he takes a share in a private company. He buys

during his golden times and sell them at the time of credit crunch. But the same doesnot hold

true for a member of the co-operative. He has no right to do so or if there is one, no farmer is

aware of this. Beside this, being a member, the farmer should be made available with all the

workings of the committee and if not all the members, regular farmers or members should be

provided with timely dividends.

Co-operatives are government organizations for the betterment of farmers. There efficient

working should be checked and they should work toward uplifting the status of farmer and

not act as a bottleneck in the path of success. Their efficient working and timely help could

help in smooth flow of rural credit and can improve the financial inclusion too.

Conclusion

Agriculture in India is a state subject and its enhancement is greately dependent upon the

functioning of the government. Credit as we have seen is the soul of agriculture. Timely and

sufficient supply of credit could do wonders for the agriculture and can take the agriculture to

the highest equilibrium of growth and development.

31

Policy makers at the centre and state are always worried about the impact of increasing the

supply of credit. It’s seen that an increase in supply of credit tends to bring in inflation, which

is a topic of concern for the policy makers. Through this research, we have seen that credit has

a positive impact upon the technology adoption. If the supply of rural agricultural credit

increases, it would be certainly reflected back by an increase in technology adoption at the

field. We should know that using more of technology will ease the farmer’s work load and

will ultimately increase the production and productivity. Thus there’s a great scope of

increasing the supply of rural agricultural credit and it would be beneficial for both the policy

makers and the farmers.

But it was seen that there are many constraints and bottlenecks in the path of credit and

agricultural growth. Providing banking facility to the poorest of poor will only be possible

once we are able to reach them. Problems have been the same since ages and no effective

solutions have been provided till date. It should be noted that Indian agriculture is suffering

but its dependency is at its peak. Solutions with immediate effects are the need of hour and

they should be brought in and implemented soon.

32

Bibliography

498, N. S. (2003). Indebtness of Indian farmers. Government of India.

Agarwal, A. (2008 йил 3-March). Economic Research. From

http://www.oecd.org/dataoecd/16/55/40339652.pdf

Distribution of loan amount. (2004-05). New delhi: Academic foundation. Department of

Agriculture and co-operation.

(2010). Evaluation of self help gropus. NABARD.

(2007). Expert group on agriculture indebtness.

ICRISAT. (2010). Know your village profile. Patancheru.

Mohan, R. (2008 йил March). Distribution of credit in India. IDBI Gilts limited.

(2005). National Sample Survey Organization. GOI.

(2008). National Sample Survey Organization. Government of India.

(2012). State lead bank committee. Bank of Maharashtra.

(2010). Task force on credit related issues of farmers. NABARD.

(2010). Working of KCC. NABARD.

33

Annexure

Questionnaire for the field survey Constraint to technological Adaptation- Role of Rural Credit and Financial Inclusion

Name of respondent:/--------------------------------------------------------------------------------- Sex:/ ------------- Age: /------

---------

Village: /_____________________________District: /_________________________________

Land holding:/_______________ (acres) --------------------------- Irrigated -------------------------------- Rain fed

Major crops growing: ------------------------------------- -------------------------------- --------------------------------- Are you member of cooperative society: --------------------------------- (yes/no) Annual Income:/ ___________________ Gross expenditure:/ ---------------------------------------------------

Major sources of credit: (Pl. tick them)

Formal Informal Money lenders Others if any

National Banks DCCBs/PACs Others

Farmer Cooperatives /SHGs Friends/Relatives Micro-finance institutions

Village money lenders Other if any

Have you applied for credit in recent times (last year)? (yes/No) If yes, How many times you have applied for credit in the last one year? ----------------------- In that how many times approved ------------------------------------ In total, how much you have borrowed: ------------------------------------- (Rs) From where Inst ---------------------------------- Amt -------------------------------------- Int rate-----------------

Inst -----------------------------------Amt --------------------------------------Int rate-----------------

Inst -----------------------------------Amt --------------------------------------Int rate-----------------

Inst -----------------------------------Amt --------------------------------------Int rate-----------------

EA ENA NE

34

How you utilized the loan money:

Purpose Amt

Seed (Improved)

Fertilizer

Pesticides

Consumption

Health

Household expenditure

Others if any

Are you getting enough credit for cultivation of crops? (yes/no)

If no what are the reasons: ----------------------------------- -------------------------------------------- -------------------------------

--------------

What are problems in borrowing credit (institution-wise)

1.

2.

3.

4.

If Not accessible to credit, what are the reasons:

o Not member in cooperative o Not have collaterals / security o Defaulter /having outstanding loans o Self sufficient o Time taking process o Others________________________

Are you aware about the various government schemes that are prevailing related to credit and crop loans? (yes / No) If yes, Pl. explains: ----------------------------------------- ------------------------------------------------ ----------------------------- Are you aware about the new variety of seeds in the market?(yes/ No)

If yes, Pl. explain about ------------------------------------ ------------------------------------------ ---------------------------------

Where you prefer to borrow more in future and Why? (Formal and Informal)

Why: ------------------------------------------ ------------------------------------------------- --------------------------------------------- How much outstanding loans do you have --------------------------- (Rs.) when you borrowed ------------------------ Reasons for outstanding: -------------------------------------- -------------------------------------- --------------------------------- How much money did you incurred in obtaining the loans (Rs)--------------------------------------- If you are NE, what are the reasons: ------------------------------------ -------------------------------------- ------------------------

35

In your opinion, the overall proportions of money borrowing from different sources in the village: Formal ------------------------------(%) In-formal -------------------------------- (%) Others ----------------------------- (%) *EA- Eligible and accessible ENA- Eligible but don’t have access NE- Non- Eligible