CONSERVATION EASEMENTS – LEGAL ASPECTS AGRICULTURE MEETING HON. PHILLIP PELLETIER HENDRY COUNTY...

52

CONSERVATION CONSERVATION EASEMENTS – EASEMENTS – LEGAL ASPECTS LEGAL ASPECTS AGRICULTURE MEETING AGRICULTURE MEETING HON. PHILLIP PELLETIER HON. PHILLIP PELLETIER HENDRY COUNTY PROPERTY APPRAISER HENDRY COUNTY PROPERTY APPRAISER JANUARY 21, 2010 JANUARY 21, 2010

-

Upload

isabela-waring -

Category

Documents

-

view

215 -

download

1

Transcript of CONSERVATION EASEMENTS – LEGAL ASPECTS AGRICULTURE MEETING HON. PHILLIP PELLETIER HENDRY COUNTY...

CONSERVATIONCONSERVATIONEASEMENTS – EASEMENTS –

LEGAL ASPECTSLEGAL ASPECTS

AGRICULTURE MEETINGAGRICULTURE MEETING

HON. PHILLIP PELLETIERHON. PHILLIP PELLETIER

HENDRY COUNTY PROPERTY APPRAISERHENDRY COUNTY PROPERTY APPRAISER

JANUARY 21, 2010JANUARY 21, 2010

Gaylord A. Wood, Jr.Gaylord A. Wood, Jr.Wood & Stuart, P.A.Wood & Stuart, P.A.

Bunnell FL 32110Bunnell FL 32110

© 2010 All Rights Reserved© 2010 All Rights Reserved

Gaylord A. Wood, Jr.Gaylord A. Wood, Jr.

Limited practice principally to ad Limited practice principally to ad valorem tax cases since 1968valorem tax cases since 1968

Firm exclusively represents Property Firm exclusively represents Property Appraisers in 14 counties including Appraisers in 14 counties including Hendry County since 1979 or soHendry County since 1979 or so

Regular Member of International Regular Member of International Association of Assessing Officers and Association of Assessing Officers and Member of the Legal CommitteeMember of the Legal Committee

WHAT IS PROPERTY?WHAT IS PROPERTY?

A House and Lot?A House and Lot? A Diamond ring?A Diamond ring? Water Rights?Water Rights? A Pet Boar Hog?A Pet Boar Hog?

WHAT IS PROPERTY?WHAT IS PROPERTY?Answer:Answer:

A House and Lot?A House and Lot? A Diamond ring?A Diamond ring? Water RightsWater Rights!! A Pet Boar Hog?A Pet Boar Hog?

PROPERTY is the rights flowing PROPERTY is the rights flowing out of the ownership of an out of the ownership of an

object. If you can see it, smell object. If you can see it, smell it, touch it, hear it or taste it, it is it, touch it, hear it or taste it, it is

not property.not property.

What are conservation easements?What are conservation easements?

Conservation easements are, in Conservation easements are, in principle, voluntary legal agreements principle, voluntary legal agreements between landowners and a land trust between landowners and a land trust or government agency that or government agency that permanently limit land uses in order permanently limit land uses in order to protect wildlife habitat and other to protect wildlife habitat and other natural resources, while allowing natural resources, while allowing certain carefully planned activities certain carefully planned activities that will not damage these that will not damage these conservation values. conservation values.

Florida Statutes define Florida Statutes define conservation easements:conservation easements:

Section 704.06, F.S.Section 704.06, F.S. “… “…a right or interest in real property a right or interest in real property

which is appropriate to retaining land or which is appropriate to retaining land or water areas predominantly in their natural, water areas predominantly in their natural, scenic, open, agricultural, or wooded scenic, open, agricultural, or wooded condition; retaining such areas as suitable condition; retaining such areas as suitable habitat for fish, plants, or wildlife; habitat for fish, plants, or wildlife; retaining the structural integrity or retaining the structural integrity or physical appearance of sites or properties physical appearance of sites or properties of historical, architectural, archaeological, of historical, architectural, archaeological, or cultural significance….” A N D or cultural significance….” A N D

Section 704.06 Prohibits:Section 704.06 Prohibits:

Construction or placing of buildings, Construction or placing of buildings, roads, signs, billboards or other roads, signs, billboards or other advertising, utilities, or other advertising, utilities, or other structures on or above the ground structures on or above the ground

Dumping or placing of soil or other Dumping or placing of soil or other substance or material as landfill or substance or material as landfill or dumping or placing of trash, waste, dumping or placing of trash, waste, or unsightly or offensive materials or unsightly or offensive materials

Section 704.06 ProhibitsSection 704.06 Prohibits

Removal or destruction of trees, shrubs, Removal or destruction of trees, shrubs, or other vegetation or other vegetation

Excavation, dredging, or removal of Excavation, dredging, or removal of loam, peat, gravel, soil, rock, or other loam, peat, gravel, soil, rock, or other material substance in such manner as to material substance in such manner as to affect the surface affect the surface

Surface use except for purposes that Surface use except for purposes that permit the land or water area to remain permit the land or water area to remain predominantly in its natural condition predominantly in its natural condition

Section 704.06 Prohibits:Section 704.06 Prohibits:

Activities detrimental to drainage, flood Activities detrimental to drainage, flood control, water conservation, erosion control, water conservation, erosion control, soil conservation, or fish and control, soil conservation, or fish and wildlife habitat preservation wildlife habitat preservation

Acts or uses detrimental to such Acts or uses detrimental to such retention of land or water areas retention of land or water areas

Acts or uses detrimental to the Acts or uses detrimental to the preservation of the structural integrity or preservation of the structural integrity or physical appearance of sites or properties physical appearance of sites or properties of historical, architectural, archaeological, of historical, architectural, archaeological, or cultural significance or cultural significance

Section 2 – How created?Section 2 – How created?

By restriction, easement, covenant, By restriction, easement, covenant, or condition in any deed, will, or or condition in any deed, will, or other instrument executed by or on other instrument executed by or on behalf of the owner of the property, behalf of the owner of the property, or in any order of taking or in any order of taking

Property Owner Incentives:Property Owner Incentives:Owner receives a huge tax Owner receives a huge tax

deduction!deduction!Up to 50% of Adjusted Gross Up to 50% of Adjusted Gross

Income for 15 yearsIncome for 15 yearsFarm property – 100% through Farm property – 100% through

end of 2009end of 2009

Landowner IncentivesLandowner Incentives

Section 170, Internal Revenue CodeSection 170, Internal Revenue Code Preservation of land areas for outdoor recreation by, or the education of, the general public,

Protection of a relatively natural habitat of fish, wildlife, or plants, or similar ecosystem,

Preservation of an historically important land area or a certified historic structure, or

Landowner Incentives (Cont’d)Landowner Incentives (Cont’d) the preservation of open space (including farmland and forest land) where such preservation is either: for the scenic enjoyment of the general public and will yield a significant public benefit or Pursuant to a clearly delineated federal, state, or local governmental conservation policy and will yield a significant public benefit.

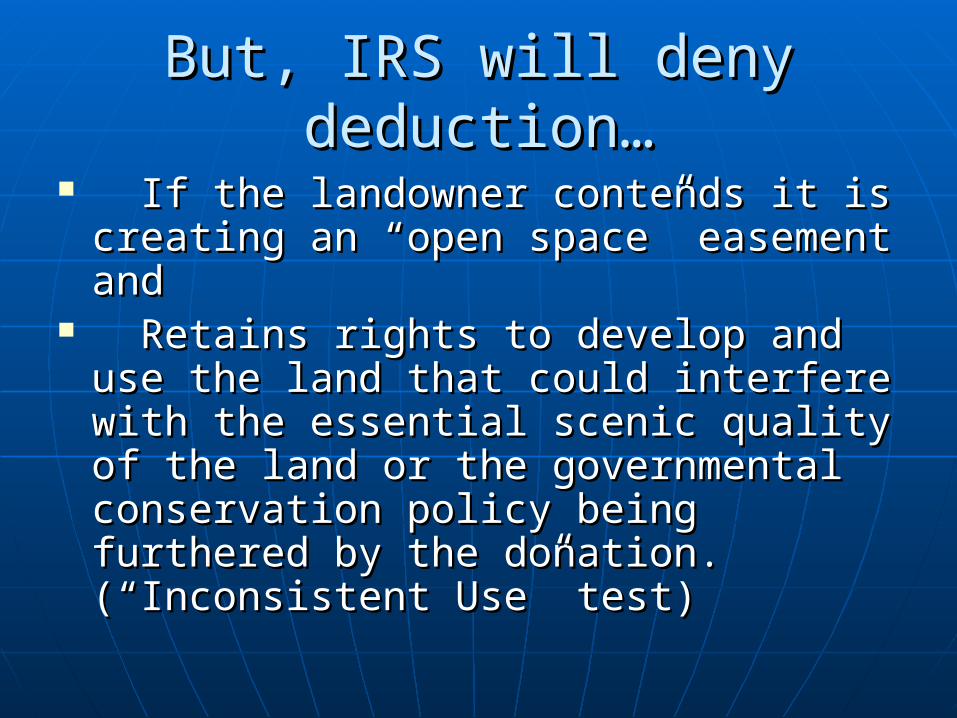

But, IRS will deny deduction…But, IRS will deny deduction…

If the landowner contends it is If the landowner contends it is creating an “open space” easement creating an “open space” easement andand

Retains rights to develop and use Retains rights to develop and use the land that could interfere with the the land that could interfere with the essential scenic quality of the land or essential scenic quality of the land or the governmental conservation the governmental conservation policy being furthered by the policy being furthered by the donation. (“Inconsistent Use” test)donation. (“Inconsistent Use” test)

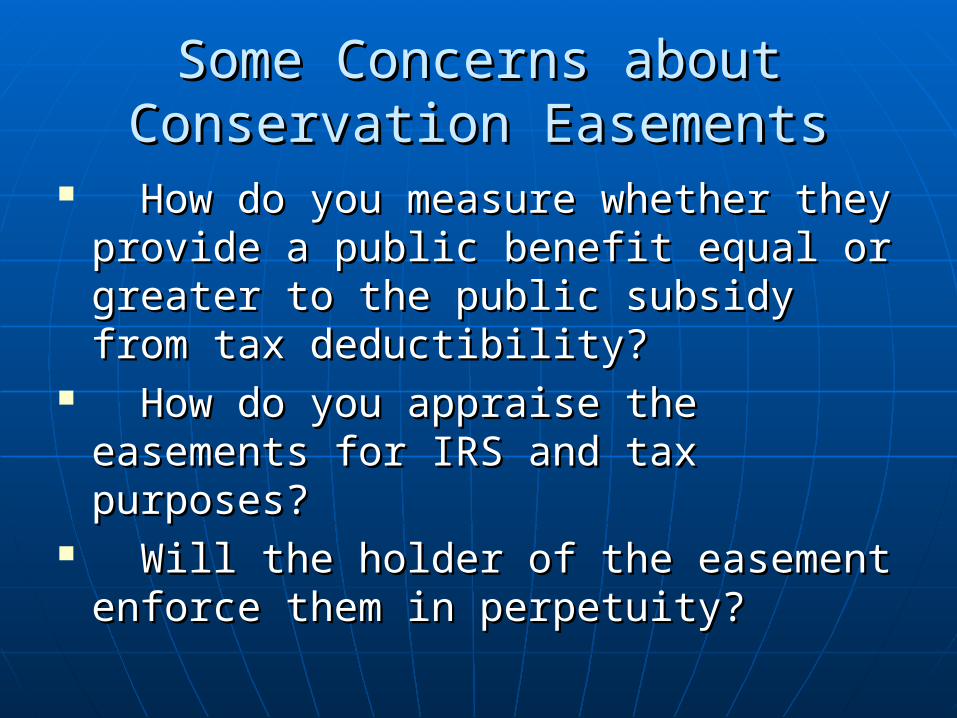

Some Concerns about Some Concerns about Conservation EasementsConservation Easements

How do you measure whether they How do you measure whether they provide a public benefit equal or provide a public benefit equal or greater to the public subsidy from greater to the public subsidy from tax deductibility?tax deductibility?

How do you appraise the How do you appraise the easements for IRS and tax purposes?easements for IRS and tax purposes?

Will the holder of the easement Will the holder of the easement enforce them in perpetuity?enforce them in perpetuity?

Conservation Easements come Conservation Easements come in two flavors:in two flavors:

Public EasementsPublic Easements Private EasementsPrivate Easements

Private Easements (704.06)Private Easements (704.06)

May be acquired by “a charitable May be acquired by “a charitable corporation or trust whose purposes corporation or trust whose purposes include protecting natural, scenic, or open include protecting natural, scenic, or open space values of real property, assuring its space values of real property, assuring its availability for agricultural, forest, availability for agricultural, forest, recreational, or open space use, protecting recreational, or open space use, protecting natural resources, maintaining or natural resources, maintaining or enhancing air or water quality, or enhancing air or water quality, or preserving sites or properties of historical, preserving sites or properties of historical, architectural, archaeological, or cultural architectural, archaeological, or cultural significance.”significance.”

HUGE LOOPHOLE:HUGE LOOPHOLE:

“ “A conservation easement may be A conservation easement may be released by the holder of the released by the holder of the easement to the holder of the fee easement to the holder of the fee even though the holder of the fee even though the holder of the fee may not be a governmental body or may not be a governmental body or a charitable corporation or trust.”a charitable corporation or trust.”

Washington Post 2003 – “Nonprofit Washington Post 2003 – “Nonprofit sells scenic acreage to allies at a sells scenic acreage to allies at a loss” (Nature Conservancy)loss” (Nature Conservancy)

PUBLIC EASEMENTSPUBLIC EASEMENTS

“ “Conservation easements may be Conservation easements may be acquired by any governmental body acquired by any governmental body or agency.” (704.06)or agency.” (704.06)

No central registry from which one No central registry from which one can determine which governmental can determine which governmental body holds which easements.body holds which easements.

Nationally, believed that 1,700 Nationally, believed that 1,700 trusts hold 37,000,000 acres of land trusts hold 37,000,000 acres of land in fee and conservation easements.in fee and conservation easements.

Is there a “Standard Is there a “Standard Conservation Conservation Easement?”Easement?”

Is there a “Standard Is there a “Standard Conservation Conservation Easement?”Easement?”

Short answer – “No!”Short answer – “No!”

FISHEATING CREEK – GLADES COUNTY

FISHEATING CREEKFISHEATING CREEK

Lykes Bros. owns 320,000 acres in Lykes Bros. owns 320,000 acres in Glades and Highlands Counties.Glades and Highlands Counties.

Creek: “Place Where Fish are Eaten”Creek: “Place Where Fish are Eaten” Lykes Bros. had two concessions for Lykes Bros. had two concessions for

canoeing and public accesscanoeing and public access Closed the waterway when faced with Closed the waterway when faced with

poaching and vandalismpoaching and vandalism State of Florida sued to declare State of Florida sued to declare

Fisheating Creek a public navigable Fisheating Creek a public navigable waterway.waterway.

To settle the case (1999) --- To settle the case (1999) ---

Fisheating Creek Ecosystem ProjectFisheating Creek Ecosystem Project State of Florida acquired WHIP – State of Florida acquired WHIP –

Wildlife Habitat Incentive Program Wildlife Habitat Incentive Program easements and some ownership of easements and some ownership of 59,910 acres59,910 acres

Cost of $55,628,563Cost of $55,628,563 On the list: State seeks to acquire On the list: State seeks to acquire

an additional 116,966 acresan additional 116,966 acres 2003 assessed value: $15,326,6512003 assessed value: $15,326,651

2003 Proposed Acquisition2003 Proposed Acquisition

24,000 acres – proposed agreement 24,000 acres – proposed agreement with State of Florida for $24,000,000with State of Florida for $24,000,000

Stated Purpose: To protect delicate Stated Purpose: To protect delicate wetlands, forest and native range wetlands, forest and native range ecosystems.ecosystems.

Limit some of Lykes’ agricultural Limit some of Lykes’ agricultural usesuses

Limit the number of times the land Limit the number of times the land could be subdivided and sold….could be subdivided and sold….

B U T – Also permitted:B U T – Also permitted:

Developing commercial wellfields Developing commercial wellfields that could dry up the wetlands that could dry up the wetlands ecosystemecosystem

Drill oil and gas wells, build roads Drill oil and gas wells, build roads and pipelines over 71% of the landand pipelines over 71% of the land

Cover the land with deep resevoirs Cover the land with deep resevoirs for water storagefor water storage

Conduct “Water Management Conduct “Water Management Activities” like deep well injection…Activities” like deep well injection…

Conclusion of Florida Department Conclusion of Florida Department of Environmental Protection (2003):of Environmental Protection (2003):

"This proposal wasn't a conservation easement, it "This proposal wasn't a conservation easement, it was a development permit, with taxpayers was a development permit, with taxpayers footing the bill," said Nina Baliga of the Florida footing the bill," said Nina Baliga of the Florida Public Interest Research Group. "Allowing this Public Interest Research Group. "Allowing this proposal to go forward would have undermined proposal to go forward would have undermined the very concept of the conservation easement, the very concept of the conservation easement, and opened the door to all sorts of shady deals and opened the door to all sorts of shady deals aimed at exploiting our natural heritage." aimed at exploiting our natural heritage."

Property Tax Property Tax Ramifications:Ramifications:

ExemptionExemption

AssessmentAssessment

Florida ConstitutionFlorida Constitution

2008 Tax and Budget Reform 2008 Tax and Budget Reform Commission, Amendment 4Commission, Amendment 4

Art. VII, Sec. 3 – Provides exemption Art. VII, Sec. 3 – Provides exemption for real property dedicated in for real property dedicated in perpetuity for conservation purposes, perpetuity for conservation purposes, including property encumbered by including property encumbered by perpetual conservation easements, perpetual conservation easements, as defined by general law.as defined by general law.

Florida ConstitutionFlorida Constitution

Article VII, Section 4(b)Article VII, Section 4(b) “ “As provided by general law and As provided by general law and

subject to conditions, limitations, and subject to conditions, limitations, and reasonable definitions specified reasonable definitions specified therein, land therein, land used for conservation used for conservation purposespurposes shall be classified by shall be classified by general law and assessed solely on general law and assessed solely on the basis of character or use.”the basis of character or use.”

Article VII, Sec. 4(b)Article VII, Sec. 4(b)

Implemented by Section 193.501, Implemented by Section 193.501, Florida StatutesFlorida Statutes

Land qualified as environmentally Land qualified as environmentally endangered pursuant to paragraph endangered pursuant to paragraph (6)(i) and so designated by formal (6)(i) and so designated by formal resolution of the governing board of resolution of the governing board of the municipality or county within the municipality or county within which such land is located; which such land is located;

Section 193.501Section 193.501

“ “land designated as conservation land designated as conservation land in a comprehensive plan land in a comprehensive plan adopted by the appropriate adopted by the appropriate municipal or county governing body; municipal or county governing body; or any land which is utilized for or any land which is utilized for outdoor recreational or park outdoor recreational or park purposes may, by appropriate purposes may, by appropriate instrument, for a term of not less instrument, for a term of not less than 10 years… ”than 10 years… ”

Section 193.501Section 193.501

“ “or any land which is utilized for or any land which is utilized for outdoor recreational or park outdoor recreational or park purposes ”purposes ”

Where the development right is Where the development right is conveyed to a public agency or conveyed to a public agency or private trust,private trust,

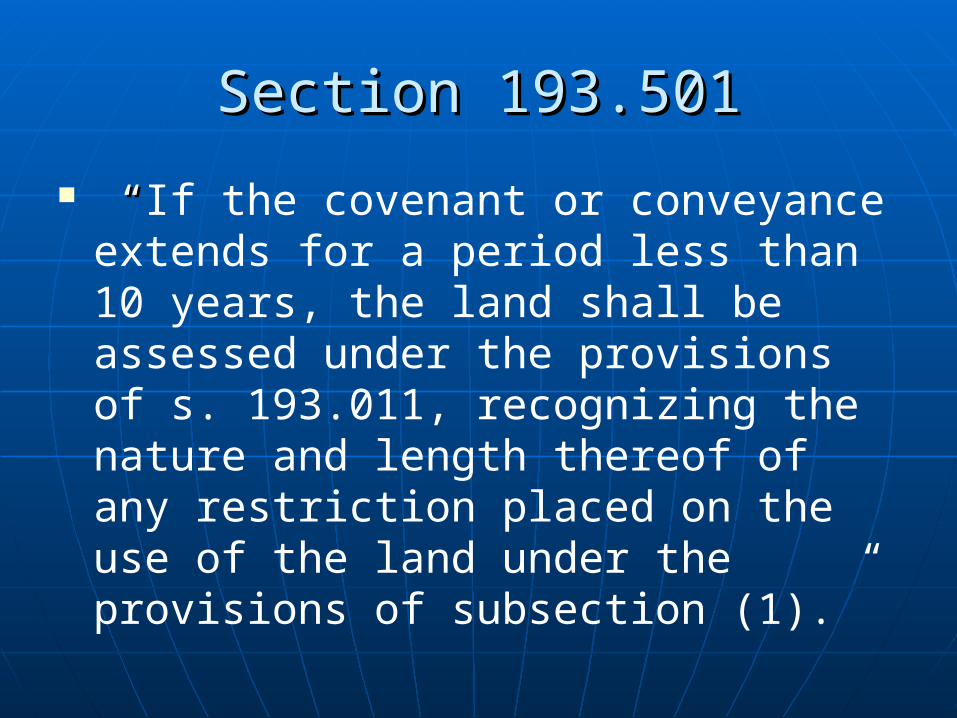

Section 193.501, F.S.Section 193.501, F.S.

“ “If the covenant or conveyance If the covenant or conveyance extends for a period of not less than extends for a period of not less than 10 years from January 1 in the year 10 years from January 1 in the year such assessment is made, the such assessment is made, the property appraiser, in valuing such property appraiser, in valuing such land for tax purposes, shall consider land for tax purposes, shall consider no factors other than those relative no factors other than those relative to its value for the present use, as to its value for the present use, as restricted by any conveyance or restricted by any conveyance or covenant under this section. ”covenant under this section. ”

Section 193.501Section 193.501

“ “If the covenant or conveyance extends for a period less than 10 years, the land shall be assessed under the provisions of s. 193.011, recognizing the nature and length thereof of any restriction placed on the use of the land under the provisions of subsection (1).”

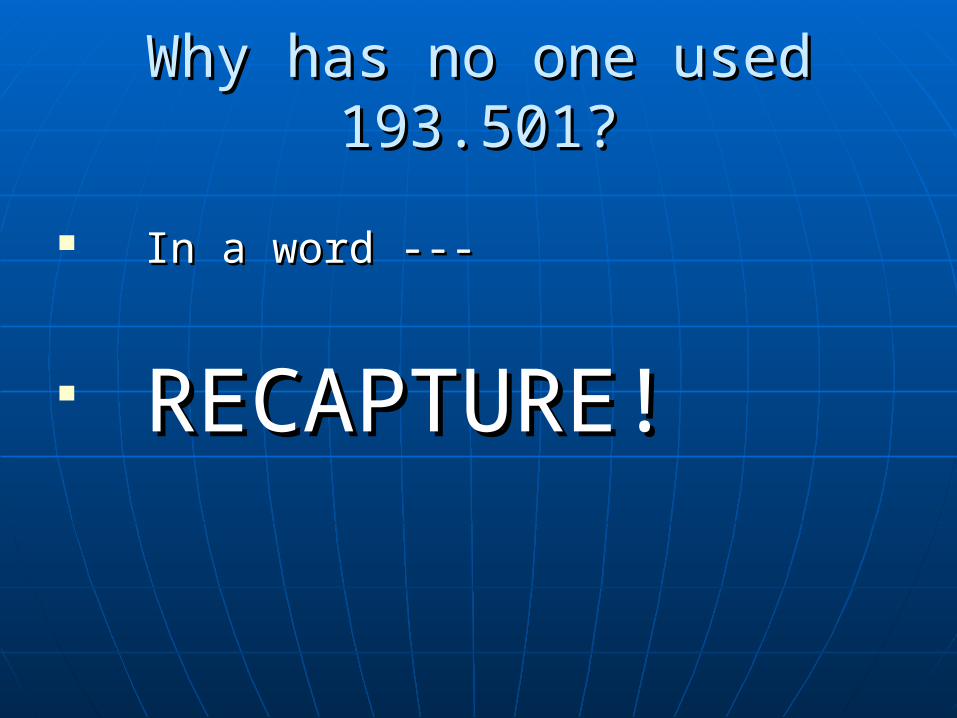

Why has no one used 193.501?Why has no one used 193.501?

In a word ---In a word ---

RECAPTURE!RECAPTURE!

Section 193.501Section 193.501

Also, “Also, “A person or organization that, on January 1, has the legal title to land that is entitled by law to assessment under this section shall, on or before March 1 of each year, file an application for assessment under this section with the county property appraiser.””

No application, no problem.No application, no problem.

EXEMPTIONEXEMPTION

2009 Legislature Issues were:2009 Legislature Issues were:

What form of easement required?What form of easement required? Who permitted to hold the easement?Who permitted to hold the easement? Minimum size of land?Minimum size of land? What environmental values?What environmental values? What Best Management Practices if other What Best Management Practices if other

uses also permitted?uses also permitted? What Payments in Lieu of Taxes?What Payments in Lieu of Taxes? What other uses also permitted?What other uses also permitted?

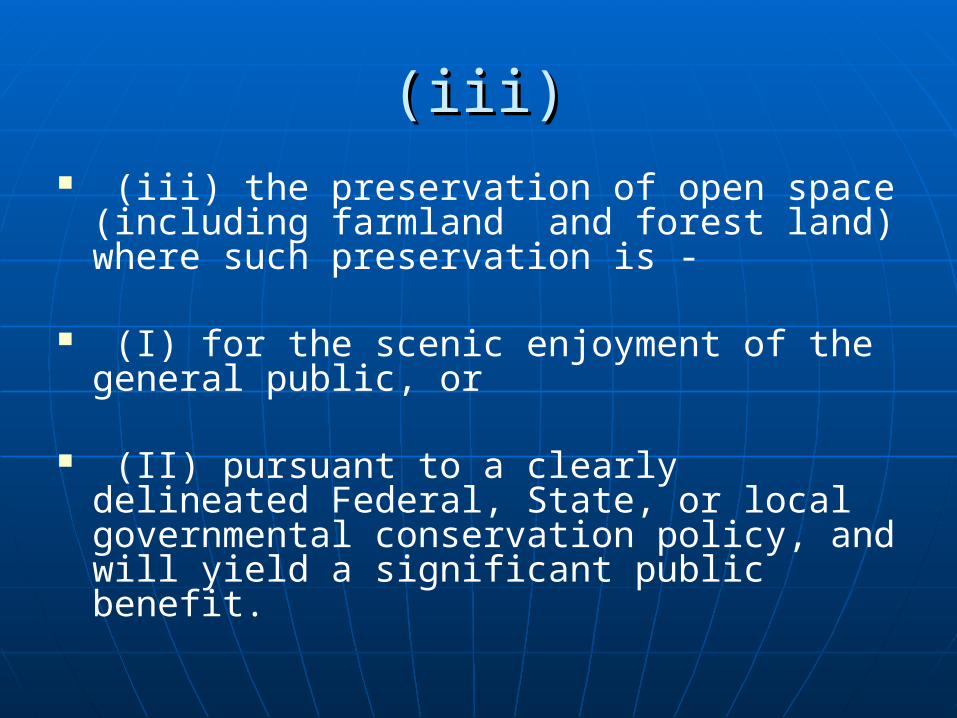

“conservation purpose, as defined in 26 U.S.C. s. 170(h)(4)(A)(i)-(iii)”

(i) the preservation of land areas for outdoor recreation by, or the education of, the general public,

(ii) the protection of a relatively natural habitat of fish, wildlife, or plants, or similar ecosystem,

(iii)(iii) (iii) the preservation of open space

(including farmland and forest land) where such preservation is -

(I) for the scenic enjoyment of the general public, or

(II) pursuant to a clearly delineated Federal, State, or local governmental conservation policy, and will yield a significant public benefit.

TOTAL EXEMPTIONTOTAL EXEMPTION

“ “(2) Land that is dedicated in perpetuity for conservation purposes and that is used exclusively for conservation purposes is exempt from ad valorem taxation. Such exclusive use does not preclude the receipt of income from activities that are consistent with a management plan when the income is used to implement, maintain, and manage the management plan. ” Also: > 40 acres. ” Also: > 40 acres.

PARTIAL EXEMPTIONPARTIAL EXEMPTION

“ “(3) Land that is dedicated in perpetuity for conservation purposes and that is used for allowed commercial uses is exempt from ad valorem taxation to the extent of 50 percent of the assessed value of the land.””

40 ACRE WEASEL40 ACRE WEASEL

“ “(4) Land that comprises less than 40 contiguous acres does not qualify for the exemption provided in this section unless, in addition to meeting the other requirements of this section, the use of the land for conservation purposes is determined by the Acquisition and Restoration Council created in s. 259.035 to fulfill a clearly delineated state conservation policy and yield a significant public benefit. ” ”

Buildings and ImprovementsBuildings and Improvements

““Buildings, structures, and other improvements situated on land receiving the exemption provided in this section and the land area immediately surrounding the buildings, structures, and improvements must be assessed separately pursuant to chapter 193. However, structures and other improvements that are auxiliary to the use of the land for conservation purposes are exempt to the same extent as the underlying land.”

ENFORCEMENTENFORCEMENT

“ “WWater management districts with jurisdiction over lands receiving the exemption provided in this section have a third-party right of enforcement to enforce the terms of the applicable conservation easement for any easement that is not enforceable by a federal or state agency, county, municipality, or water management district when the holder of the easement is unable or unwilling to enforce the terms of the easement. ” ”

Fiscally Constrained CountiesFiscally Constrained Counties

After November 1, 2010After November 1, 2010 May apply for grants to replace May apply for grants to replace

taxes lost as a result of Amendment taxes lost as a result of Amendment 4.4.

QUESTIONS?QUESTIONS?