Competitiveness and Business Environment in Finland...

84

Competitiveness and Business Environment in Finland – An International Benchmarking MTI Publications 7/2004 Industries Department

Transcript of Competitiveness and Business Environment in Finland...

Competitiveness and Business

Environment in Finland –

An International Benchmarking

MTI Publications

7/2004

Industries Department

Series title and number of the publication Aleksanterinkatu 4

P.O. Box 32 Tel. +358 9 16001 MTI Publications FIN-00170 Helsinki FINLAND

FIN-00023 GOVERNMENT Helsinki FINLAND

Telefax +358 9 1606 3666 7/2004

Date March 2004

Commissioned by Ministry of Trade and Industry

Authors Industries Department Hannu Lipponen Esa Viitamo

Date of appointment

Title Competitiveness and Business Environment in Finland - An International Benchmarking

Abstract Competitiveness and Business Environment in Finland - An International Benchmarking reviews the interaction between competitiveness, production structures, and the business environment. The survey sets out to analyse Finnish competitiveness in an international context. The economic performance is outlined thorough an analysis of standard of living, productivity and industrial structures. The analysis of business environment is narrowed down to innovation environment and labour and product markets. These are areas that have been highlighted in recent international competitiveness analyses, too. Finnish competitiveness is of a high standard. In recent years, productivity has increased rapidly and production has been developing towards knowledge-intensive structures. Finnish innovation environment is globally advanced and the innovation activities and support systems are efficient. Maintaining competitiveness requires that the base of productivity growth be extended to include more industrial activities. The percentages of gross domestic product are rather high in the sectors with lower growth rates in productivity. Moreover, their output is heavily dependent upon demand in the domestic market. These sectors include construction, transport, real estate, business-related services, social and health services, as well as education. To foster productivity growth and to further open up the economy, it is important to increase deregulation in product and labour markets. Moreover, there is a need to strengthen research and development inputs in the services sector. Finally, a great potential for improvement is found within public welfare services, where productivity can be raised through utilising the services of private enterprises. MTI contact: Industries Department/Senior Researcher Hannu Lipponen, tel. +358 9 1606 3606

Key words Industrial policy, competitiveness, markets, structural change, business environment, productivity, employment

ISSN 1459-9376

ISBN 951-739-764-X

Pages 82

Language English

Price € 17

Published by Ministry of Trade and Industry

Sold by Edita Publishing Ltd

Foreword

Competitiveness and Business Environment in Finland – An International

Benchmarking is a review drawn up by the Ministry of Trade and Industry. It aims

to outline the interaction between competitiveness, industrial structure and the

business environment of enterprises in Finland.

The review is a tool for the Ministry, to support the design and implementation of

Finland’s business environment policy. Our objective is also to discuss competi-

tiveness and its determinants. For this purpose, a section has been added to the Min-

istry’s website at the address www.ktm.fi/competitiveness. This section monitors

the development of competitiveness and the business environment in Finland.

The starting point of this review is benchmarking Finnish competitiveness in an in-

ternational context. Economic performance is examined through an analysis of the

standard of living, productivity and industrial structure. As for the business envi-

ronment, the focus is on the innovation environment, as well as on the labour and

commodity markets. The role of these factors has been emphasised in recent inter-

national studies, too. Taxation and macroeconomic factors are excluded from this

review. The purpose of the forthcoming reviews is to deepen and expand the analy-

sis of the business environment.

This review, compiled by the Industrial Policy Division of the Ministry’s Industries

Department, is also available at the web address mentioned above.

Erkki Virtanen

Permanent Secretary

Contents

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Summary and Conclusions . . . . . . . . . . . . . . . . . . . . . . . 9

1 National competitiveness . . . . . . . . . . . . . . . . . . . . . 12

1.1 Competitiveness consists of several levels . . . . . . . . . . . . 12

1.2 Finland ranks well in international evaluations . . . . . . . . . . 13

2 Well-being . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

2.1 Finnish well-being is among the highest in the world . . . . . . 16

2.2 Economic growth has been among the fastest in the world. . . . 20

2.3 The structure of productivity growth has changed . . . . . . . . 24

3 Industrial structure . . . . . . . . . . . . . . . . . . . . . . . . 27

3.1 The market sector is expanding . . . . . . . . . . . . . . . . . . 27

3.2 Productivity growth is driven by manufacturing . . . . . . . . . 28

3.3 Information and communications technology shows the way . . 32

3.4 Technology- and knowledge-intensity is increasing . . . . . . . 37

3.5 Industry restructuring reflects the dynamics of company

demography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4 Innovation environment . . . . . . . . . . . . . . . . . . . . . 48

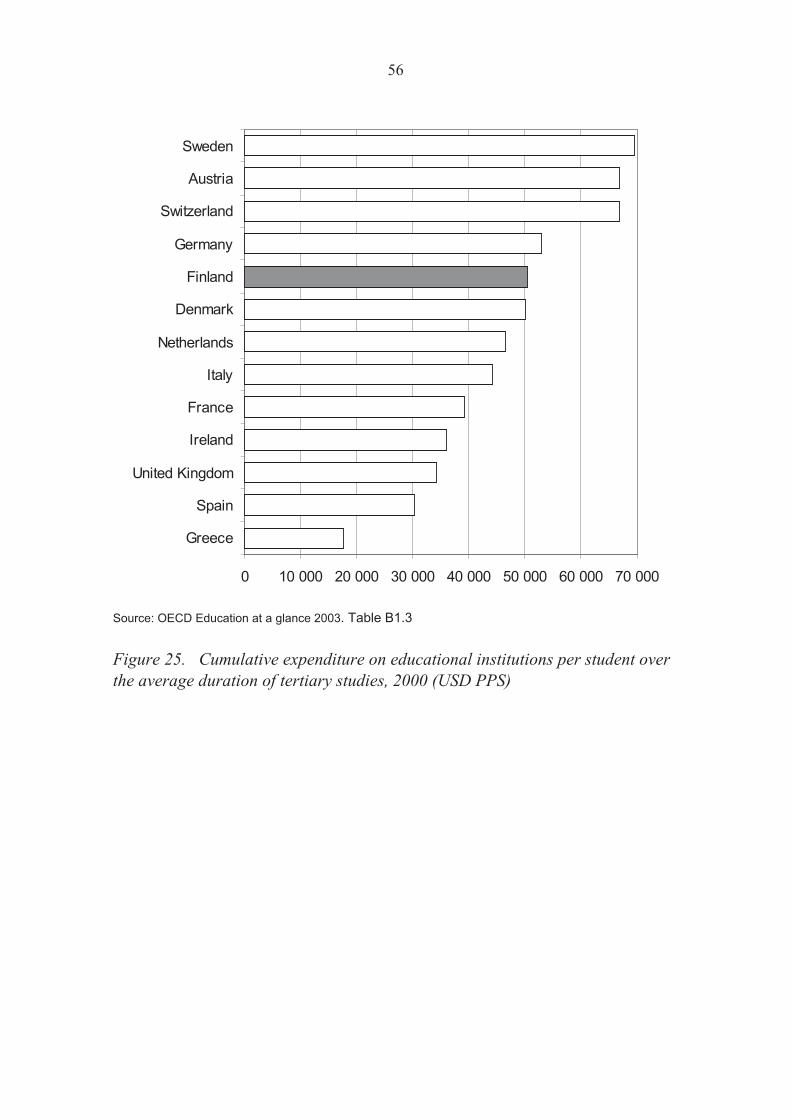

4.1 High educational level of population . . . . . . . . . . . . . . . 48

4.2 Many top-skilled workers . . . . . . . . . . . . . . . . . . . . . 52

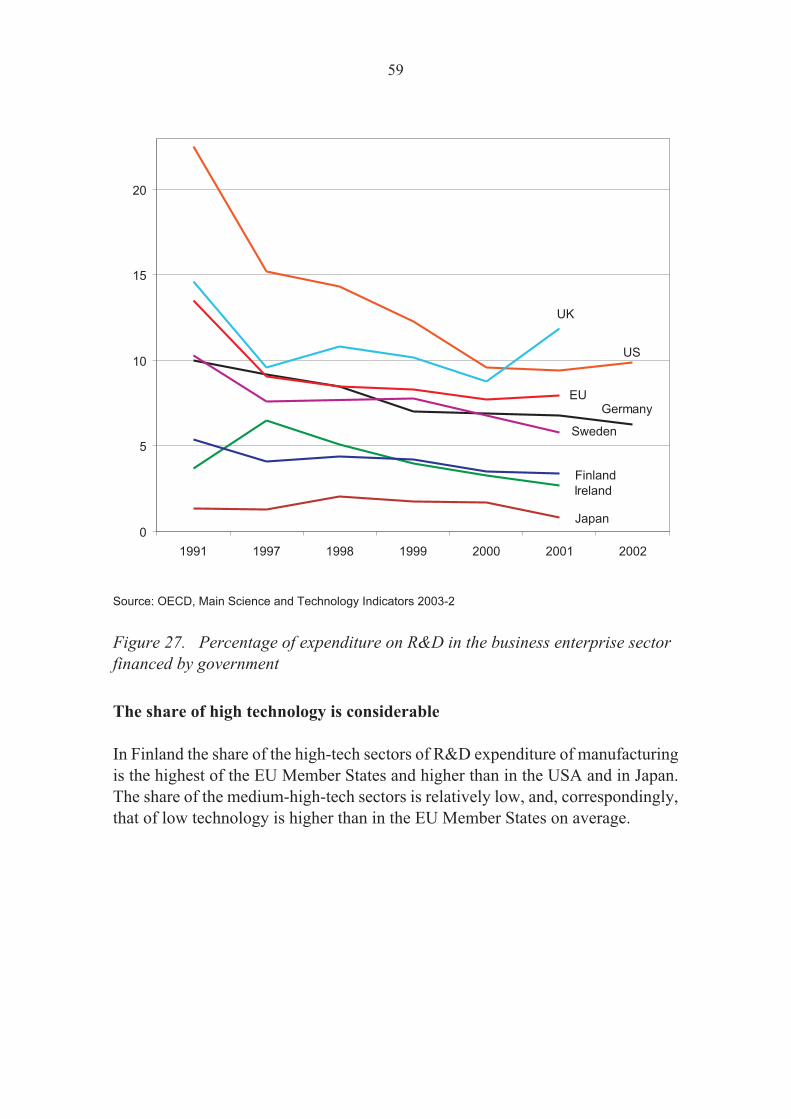

4.3 R&D investment is top-class . . . . . . . . . . . . . . . . . . . 57

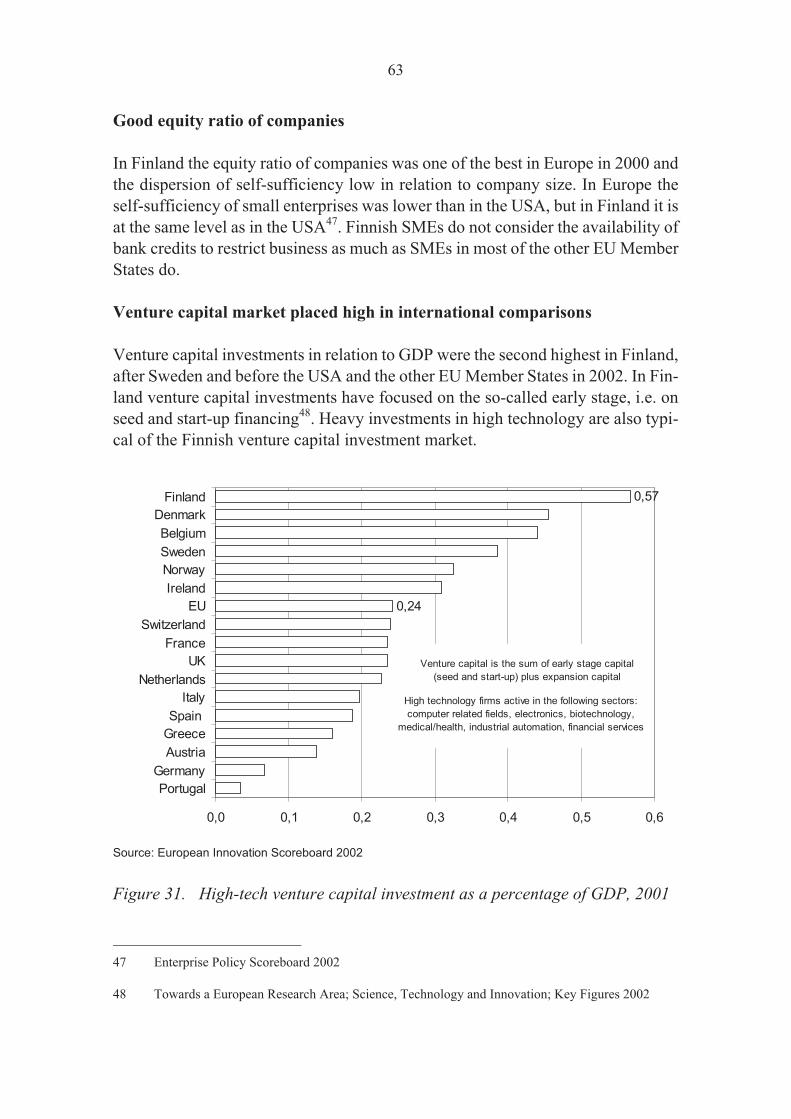

4.4 Availability of risk financing is good . . . . . . . . . . . . . . . 62

4.5 Innovation activities are fruitful . . . . . . . . . . . . . . . . . 64

5 Functioning of the market . . . . . . . . . . . . . . . . . . . . 68

5.1 Unemployment turning into lack of labour . . . . . . . . . . . . 68

5.2 The educational attainment level and demand for labour are ill

matched . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

5.3 Deficiencies in the flexibility of the labour market . . . . . . . . 73

5.4 The openness of economy is relatively low. . . . . . . . . . . . 74

5.5 Regulation restricts competition on the home market . . . . . . 76

Sources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

Summary and Conclusions

Business environment is excellent, whereas the standard of living is only

average

Finland is doing well in the global competition. Productivity has grown rapidly and

the industrial structure has been upgraded. Welfare, measured by economic, social

and environmental indicators, is among the highest in the world, as in the other

Nordic countries.

Finland places remarkably high in international rankings of competitiveness, too.

The results of these rankings are, however, mixed from the Finnish point of view.

The competitiveness of the business environment gets an excellent score, whereas

for the standard of living the position has remained around the 15th for years. This

contradiction needs an explanation.

This explanation has been sought for by assessing competitiveness on three interde-

pendent levels. Standard of living depicts economic performance, with labour in-

puts and labour productivity as its components. Performance is influenced by the

industrial structure, which is a key determinant for the growth potential of econ-

omy. The third level is the business environment, which determines the industrial

structure and which business environment policy directs.

Restructuring of industry has been prominent

The growth of labour productivity has been strong for more than two decades. This

has mainly been attributed to the manufacturing sector, with productivity growth

second fastest after Ireland. For the service sector and construction in particular,

productivity growth has been markedly slower, at times even negative. By the inter-

national standard, however, productivity has grown rapidly in the service sector,

too. In general, industries producing information and communication technologies

and utilising them extensively show the highest productivity growth.

There has been a marked shift in the sources of the productivity growth towards the

end of the 1990s. Total factor productivity, reflecting technological development

and improvement in skills and know-how, has increasingly replaced productivity

growth based on capital deepening. This indicates a growing knowledge-intensity

of the industrial structure.

9

The change in the industrial structure has been profound and one of the fastest in the

world. Increase in technology-intensity of the manufacturing sector has been

strong, driven mainly by the manufacture of communications equipment. For the

service sector the structural change has been slower, though in international com-

parison the GDP share of the knowledge-intensive services has been growing rap-

idly as well. The enterprise volatility rate has also been high, boosting productivity

growth in several industries.

The growth rate of labour input and the standard of living have a strong interdepen-

dence. During the past ten years, employment has picked up dynamically, but there

are still some 130,000 jobs less than before the depression at the beginning of the

1990s.

Innovation environment is favourable, while the functioning of the markets

is deficient

Numerous indicators show that the Finnish innovation environment is excellent;

the level of educational attainment of the workforce is high and the research re-

sources are top-class, cooperation between businesses and research institutions is

intensive and innovation activities are productive and internationally oriented.

Moreover, the financial market functions efficiently, and the availability of venture

capital is good by the international standard.

The causality between the quality of the innovation environment and the rapid

growth of labour productivity is straightforward. Favourable innovation environ-

ment has promoted restructuring of the economy and the growth of the technol-

ogy-intensity of production processes as well.

Competition encourages firms to maintain and improve efficiency and develop new

products. The openness of economy, i.e. the extent it is internationally integrated,

determines the functioning of competition. The openness of the Finnish economy is

lower compared to that of the other small EU Member States. The share of foreign

trade of GDP and the number of foreign investments channelled to Finland are rela-

tively low, and the price level is one of the highest in the world.

The gradual deregulation of the product market, initiated in the 1980s, has pro-

moted the growth of productivity and restructuring. Still, in OECD estimates, Fin-

land figures among the countries where regulation has been proved to hinder com-

petition. Construction, water and natural gas resources management, retail trade

and transportation are among the sectors subjected to detrimental regulation. The

exposure of these industries to international competition has been low, too. The ris-

10

ing price level and weak productivity growth are characteristic of industries pro-

tected from international competition.

There is evidence of malfunctioning of the labour market, too. Problems occur in

matching the educational structure and the demand for labour, although the educa-

tional level, labour participation rate and participation in adult training are the high-

est in the world. The long duration of academic studies weakens the employment

rate. The greatest problem of the labour market is, however, high unemployment,

which results e.g. from the rapid industrial restructuring and ageing of the popula-

tion. Within the next few years, the ageing of the population and the increasing lack

of qualified labour will be factors that restrict economic growth.

The greatest potential for productivity growth lies in the service sector

Maintaining competitiveness calls for strengthening productivity growth and ex-

tending the growth base. Except for the manufacture of communications equip-

ment, the industries with the highest growth of productivity are relatively narrow.

Conversely, productivity growth is lowest in industries with considerable GDP

shares. Among these are construction and specific service industries: transporta-

tion, real-estate activities, business services, health care and social services, as well

as education and training.

The greatest potential for productivity growth is in the service sectors and in con-

struction. Productivity growth and increased openness of the economy necessitate

abolishing the detrimental regulation of the product and labour markets. R&D ac-

tivities in the service sectors should also be boosted. The greatest potential lies in

raising the productivity of public health care services by fostering market-based ac-

tivities in particular. Provision of services has been gradually opened to private en-

terprises. Still, lack of procurement skills is one of the factors putting the brakes on

the change.

11

1 National competitiveness

Starting point

Improvement of economic performance and recognition of the factors explaining it

have been raised as the core of business environment policy. This is influenced by

two development trends in particular, which became increasingly stronger in the

1990s.

The integration of world economy and deregulation of the markets have strength-

ened competition between firms and countries and subjected new, previously pro-

tected economic sectors to competition. Globalisation and the related rapid techno-

logical change have at the same time added to the volatility of international eco-

nomic development. Unanticipated changes in the business environment may

change, even rapidly, the relative competitive positions of countries.

1.1 Competitiveness consists of several levels

By definition, national competitiveness refers to a country’s economic perfor-

mance in relation to other countries or groups of countries1. On the methodological

side, the internal dynamics of economy is increasingly stressed. The characteristics

of the business environment and the resource base of a country pave the way for the

growth of production and productivity. This is further reflected in the development

of the standard of living and welfare, respectively.

In this review, too, analysis follows the successive stages mentioned above. The

competitiveness of the business environment is primarily determined by microeco-

nomic factors, of which the most important ones are the innovation environment

and functioning of markets. These factors are examined here, too. The purpose of

business environment policy is to improve the microeconomic environment2.

12

1 Competitiveness is related to a narrower concept, competitive advantage, which refers to resources or

assets that competitiveness of countries is based on (most often a factor of the business environment).

This resource is not freely available to other countries.

2 The other component of the business environment, macroeconomic factors, are excluded from this

review.

Figure 1. Levels and dynamics of competitiveness

The business environment provides the preconditions for the competitiveness of

firms, industries and production activities, which is measured by productivity and

change in the industrial structure. The competitiveness of the industrial structure

further determines the overall performance, i.e. the standard of living (GDP/popu-

lation). The standard of living again is an integral element of welfare, which is mea-

sured by such qualitative factors as education and training, health and the state of

the environment.

In Figure 1, the competitiveness effects are mainly directed from below upwards. In

reality, firms and industries also influence their business environment and its com-

petitiveness in many ways. This also applies to welfare, which through social capi-

tal affects labour productivity. However, examination of these feedbacks is ex-

cluded from the scope of this review.

1.2 Finland ranks well in international evaluations

The Swiss institutes, World Economic Forum (WEF) and International Institute for

Management Development (IMD), draw up annually evaluations of the competi-

tiveness of developed and less developed economies. Competitiveness is measured

by composite indexes that are derived from statistics describing the state of econo-

mies and the views of business executives of various countries. In the evaluations

of both institutes, Finland has ranked high in recent years.

13

Competitiveness of

the business environment

• Innovation environment

• Labour market

• Commodities market

Competitiveness of

the industrial structure

• Productivity of sectors

• Change in the industrial structure

• Enterprise turnover rate

Business

environment

policy

Welfare and standard of living

• Human and environmental well-being

• Labour input

• Productivity

Competitiveness of

the business environment

• Innovation environment

• Labour market

• Commodities market

Competitiveness of

the industrial structure

• Productivity of sectors

• Change in the industrial structure

• Enterprise turnover rate

Business

environment

policy

Welfare and standard of living

• Human and environmental well-being

• Labour input

• Productivity

However, Finland’s overall performance is mixed. In the latest ranking of IMD,

Finland tops the comparison in terms of the business environment depicting the fu-

ture competitiveness potential, but as to performance realised it is ranked at 18

only. The business environment indexes are based on questionnaire material,

whereas performance has mainly been measured by statistics.

WEF’s Growth Competitiveness Index, which in 2001 was the second highest in

Finland after the United States, measures the growth potential of economy and

thereby future competitiveness potential, too. Finland is well placed by indicators

of technological development and functioning of public institutions, but our macro-

economic competitiveness is relatively low, respectively3. As in the results of IMD,

Finland is ranked high by indexes based on the views of business executives.

The Finnish paradox

WEF’s growth competitiveness analysis is complemented with a comparison of the

microeconomic business environment, which aims to map out the factors explain-

ing the differences in the standard of living. Here the analytical framework is a clus-

ter model by Michael Porter4, in which the competitiveness of the various industries

is created as a joint effect of the strategies and business environment of firms. The

total microeconomic index is obtained as a weighted average of the indicators mea-

suring these determinants.

Based on this cluster approach, too, the Finnish business environment turns out to

be excellent. The competitiveness of the microeconomic business environment cor-

relates positively with the standard of living, i.e. countries with high competitive-

ness also have a high GDP per capita. Deviations are, however, big, and Finland, to-

gether with the UK, belongs to countries where the standard of living is clearly

lower than what the quality of the business environment statistically predicts.

In general, there are two explanations for this performance deficit. According to

WEF, Finland’s competitiveness lies on a solid ground, and the deficit can be attrib-

14

3 The Global Competitiveness Report 2002–2003, WEF. According to the latest report by WEF, Fin-

land also ranks on the top in terms of macroeconomy as well: at the second position. The main ex-

planation for this leap is that the index depicting public expenditure has been replaced by indexes

measuring the efficiency of the public sector.

4 Cf. Porter, 1990.

uted to a slow upward adaptation of the standard of living5. An opposite explana-

tion is based on the measurement method of the indicators; namely, the microeco-

nomic competitiveness index is also derived from the questionnaire material. Thus

there would not be any performance deficit, if the evaluations of the business envi-

ronment were oversized. The results of IMD also support this conclusion. One of

the aims of this review is to find the possible reasons for this contradiction.

Source: Global Competitiveness Report 2003–2004, WEF.

Figure 2. Standard of living and microeconomic business environment.

15

Standard of living

(GDP/population)

1. United States

2. Ireland 3. Norway

15. Finland

Business environment

1. Finland

2. United States

3. Great Britain

Corporate strategies

1. United States

2. Germany

3. Great Britain

4. Finland

Microeconomic

(business)

competitiveness

1. Finland

2. United States

3. Great Britain

Standard of living

(GDP/population)

1. United States

2. Ireland 3. Norway

15. Finland

Business environment

1. Finland

2. United States

3. Great Britain

Corporate strategies

1. United States

2. Germany

3. Great Britain

4. Finland

Microeconomic

(business)

competitiveness

1. Finland

2. United States

3. Great Britain

5 According to this explanation, the improvement of the quality of the business environment is not im-

mediately reflected in higher performance.

2 Well-being

Interrelation between well-being, the environment and technology

Well-being can be divided into human and environmental well-being, which are

mutually dependent. Economic growth and the state of the environment have tradi-

tionally had a negative interdependence: if one is to be increased, the other has to be

cut. Technological change is, however, reducing this juxtaposition. The growth of

production based on research and intangibles allows increasing material well-being

without impairing the state of the environment6.

2.1 Finnish well-being is among the highest in the

world

According to a narrower definition, Finnish well-being is at 11th place in the

global ranking. Our educational level tops the rankings, but health and the stan-

dard of living represent the average level of the most developed countries.

With a broader definition (quality of living), Finland belongs to the top ten rank-

ing together with the other Nordic countries. The same applies to the well-being of

the environment and eco-competitiveness.

Health and the standard of living drop Finland off the leading scores

The Human Development Report, published annually by the United Nations, eval-

uates the socio-economic development of countries with a combined indicator HDI

(Human Development Index). The index is calculated as an average of life expec-

tancy, educational level and the standard of living (GDP/population). According to

the UN definition, human development is about creating an environment in which

people can develop their full potential and lead productive, creative lives in accord

with their needs and interests.

16

6 The state of the environment may even improve, if the production share of industries that heavily

strain the environment decreases at the same time.

Norway, Iceland and Sweden of the Nordic countries are countries with the highest

human development, which, except for Sweden, rank on top by all the three indica-

tors. In relation to the overall ranking, Sweden scores relatively low by the GDP per

capita. In the 2001 human development comparison, Finland shared the 11th place

together with Denmark, Ireland, the UK and Luxembourg. In terms of educational

attainment, Finland heads the world rankings (shared first place), but our overall

score declines owing to lower standard of living (15th position) and life expectancy

(16th position).

Quality of living and sustainable development are the world’s best

Despite its usability, the UN’s human development indicator omits some central

sub-sectors of well-being. The World Conservation Union (IUCN) uses a well-be-

ing index that is broader than HDI7. This index measuring sustainable development

distinguishes between human well-being (HWI8) and environmental well-being

(EWI9).

Table 1. Sustainable Development Index

Human Well-being Index (HWI) Ecosystem Well-being Index (EWI)

Health and stability of family size Biodiversity, state of the eco-system

Income level, nutrition, hygiene and national

economy

Quality of waterways and potable water

Educational level, communications system Air protection and quality of urban atmo-

sphere

Society, freedom, administration, crime Animal protection, diversity of species

Distribution of income and equality between

the genders

Consumption of natural resources and bur-

dens on the environment

Source: Wellbeing of Nations (2001).

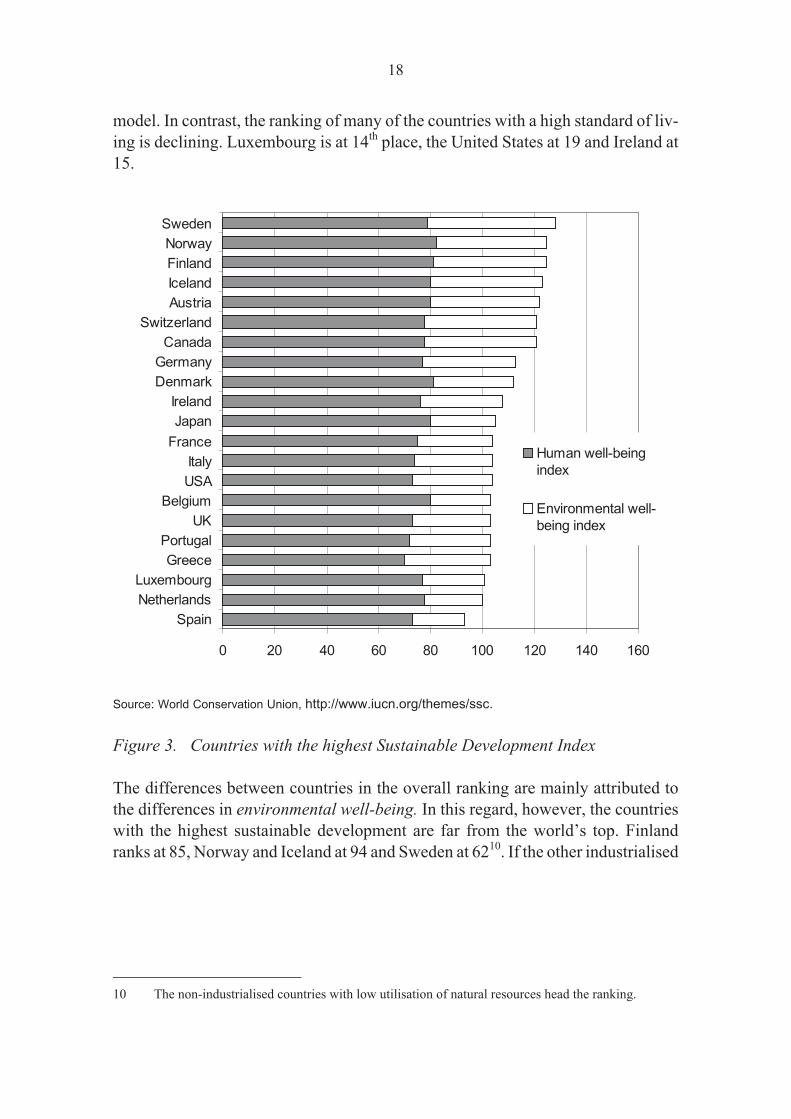

The countries with the highest score in sustainable development are Sweden, Fin-

land, Norway and Iceland of the Nordic countries, together with Austria (cf. Figure

3). Thus Finland’s ranking is considerably higher, as well-being is expanded to in-

stitutional factors and when indicators of basic human needs are included in the

standard of living (prosperity). HWI, too, clearly favours the Nordic well-being

17

7 Wellbeing of Nations (2001).

8 HWI = Human Well-being Index.

9 EWI = Ecosystem Well-being Index.

model. In contrast, the ranking of many of the countries with a high standard of liv-

ing is declining. Luxembourg is at 14th place, the United States at 19 and Ireland at

15.

Source: World Conservation Union, http://www.iucn.org/themes/ssc.

Figure 3. Countries with the highest Sustainable Development Index

The differences between countries in the overall ranking are mainly attributed to

the differences in environmental well-being. In this regard, however, the countries

with the highest sustainable development are far from the world’s top. Finland

ranks at 85, Norway and Iceland at 94 and Sweden at 6210. If the other industrialised

18

0 20 40 60 80 100 120 140 160

Spain

Netherlands

Luxembourg

Greece

Portugal

UK

Belgium

USA

Italy

France

Japan

Ireland

Denmark

Germany

Canada

Switzerland

Austria

Iceland

Finland

Norway

Sweden

Human well-being

index

Environmental well-

being index

10 The non-industrialised countries with low utilisation of natural resources head the ranking.

countries are taken as points of reference, the Nordic countries retake the leading

positions11.

The ranking of the countries remains almost the same for eco-efficiency, which is

measured by the ratio between HWI and EWI (cf. Figure 4). The index value shows

roughly to what extent human well-being has been achieved at the expense of

straining the environment at the different levels of HWI. For instance, Greece,

where the HWI index gets a relatively low value, ranks high in terms of eco-effi-

ciency. Norway drops to the 7th place. As can be seen in the Figure, the standard of

living of the countries with the highest eco-efficiency represent the average level of

the OECD countries12.

Source: World Conservation Union, http://www.iucn.org/themes/ssc.

Figure 4. Eco-efficiency (HWI/EWI) and standard of living (GDP/population)

19

0

0,5

1

1,5

2

2,5

3

3,5

4

Sw

eden

Canada

Sw

itzerland

Fin

land

Icela

nd

Austr

ia

Norw

ay

Gre

ece

Germ

any

Port

ugal

US

A

Irela

nd

UK

Italy

Fra

nce

Denm

ark

Japan

Luxem

bourg

Belg

ium

Neth

erlands

Spain

0

10000

20000

30000

40000

50000

60000

Eco-efficiency

GDP/population

HWI/EWI GDP/population

11 Interestingly, the countries where the forest industry plays a key role (Finland, Sweden, Austria and

Canada) top the ranking of both sustainable development and eco-system well-being.

12 The index is calculated with the current PPP in US$ in 2000.

2.2 Economic growth has been among the fastest in

the world

Finland’s standard of living has for long occupied the 15th position. Of the factors

constituting the standard of living, productivity and labour participation rate are

the most important ones.

Economic growth in Finland has been among the fastest in the world. This has re-

sulted mainly from the dynamic growth of productivity and the relatively rapid

growth of employment.

The standard of living, which measures the performance of national economy, is

determined by the number of production inputs and the output yielded by the in-

puts. In its simplest form, the standard of living can be expressed by the identity be-

low:

The first term at the right hand side of the identity, labour productivity, depicts the

efficiency of total production. The second term denotes the average annual working

time, and the third one labour participation. Thus growth in labour productivity, an

increase in the number of working hours and an increase in the number of the em-

ployed in relation to the population affect the standard of living.

Labour participation is more important than working time

As for the standard-of-living, Finland’s ranking at the 15th position is about the

same as the score for its components. Compared e.g. to Ireland, the share of the em-

ployed population is higher in Finland, but Ireland has more working hours per em-

ployee, and productivity is also clearly higher. Similarly, in comparison to the sec-

ond ranking, Norway, Finland has clearly more working hours, but in Norway pro-

ductivity, as well as the proportion of the employed of the population, is higher. In

Finland the employment rate is higher than in the EU on average, but distinctly

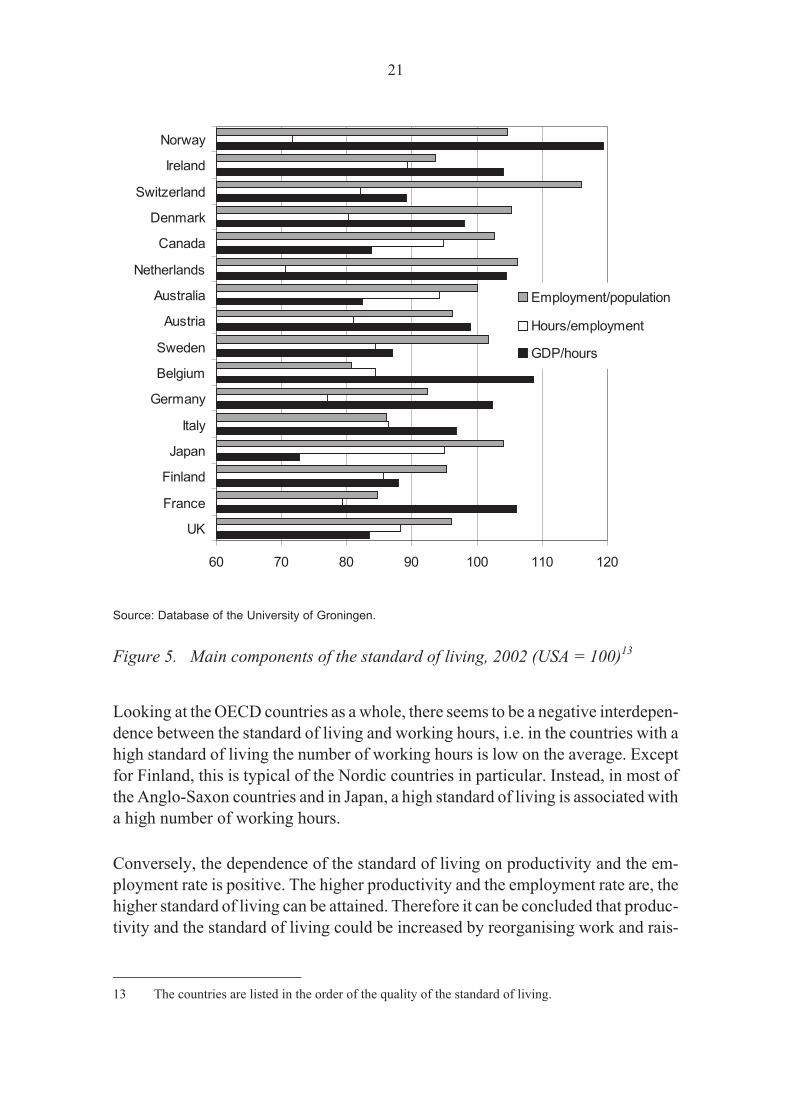

lower than in the other Nordic countries. (cf. Figure 5).

20

population

employment

employment

rsworkinghou

rsworkinghou

GDP

population

GDP���

Source: Database of the University of Groningen.

Figure 5. Main components of the standard of living, 2002 (USA = 100)13

Looking at the OECD countries as a whole, there seems to be a negative interdepen-

dence between the standard of living and working hours, i.e. in the countries with a

high standard of living the number of working hours is low on the average. Except

for Finland, this is typical of the Nordic countries in particular. Instead, in most of

the Anglo-Saxon countries and in Japan, a high standard of living is associated with

a high number of working hours.

Conversely, the dependence of the standard of living on productivity and the em-

ployment rate is positive. The higher productivity and the employment rate are, the

higher standard of living can be attained. Therefore it can be concluded that produc-

tivity and the standard of living could be increased by reorganising work and rais-

21

60 70 80 90 100 110 120

UK

France

Finland

Japan

Italy

Germany

Belgium

Sweden

Austria

Australia

Netherlands

Canada

Denmark

Switzerland

Ireland

Norway

Employment/population

Hours/employment

GDP/hours

13 The countries are listed in the order of the quality of the standard of living.

ing the labour participation rate. These effects are transmitted through an increased

and more efficient use of labour inputs. Figure 6 illustrating an increase in the stan-

dard of living 614 also supports this conclusion.

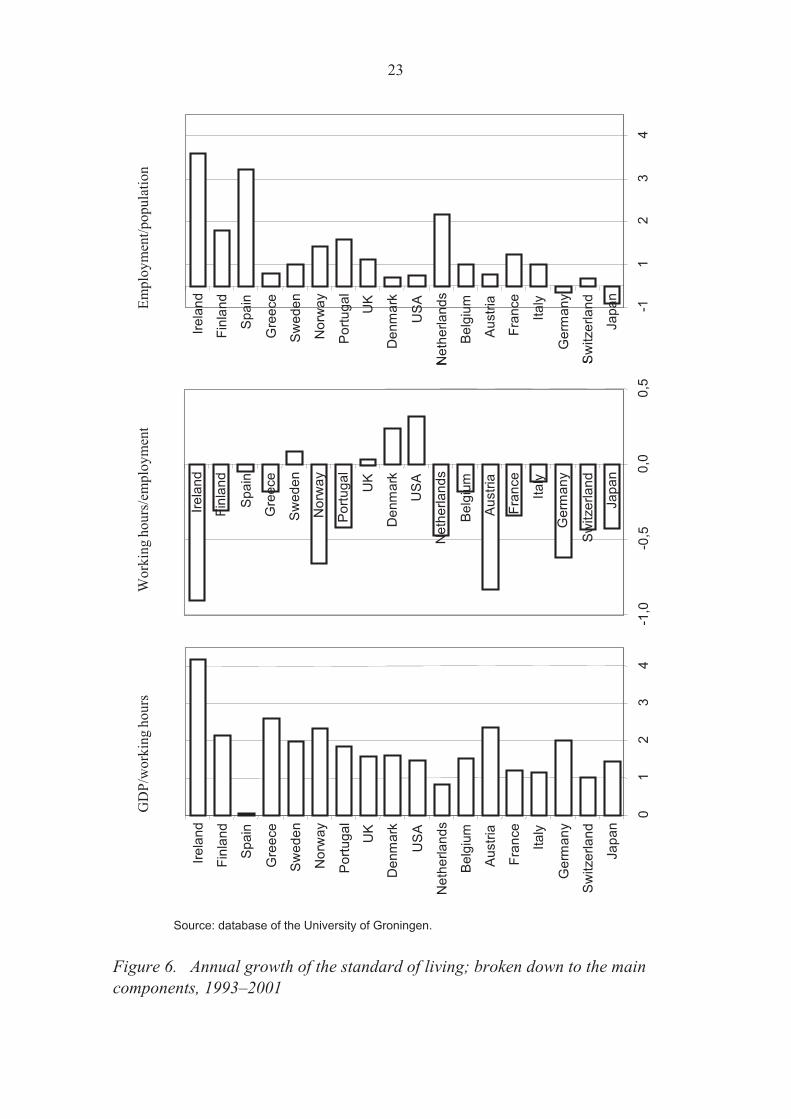

Growth of the standard of living is based on labour productivity

Of the OECD countries, growth of the standard of living has been clearly fastest in

Ireland – 6.4% on average – followed by Finland with a growth rate of over 3%. As

in most industrialised countries, the most important factor of economic growth in

Finland has been labour productivity. The growth of the employment rate has also

played a significant role. In this respect Ireland, Spain and the Netherlands stand as

the best examples. In the countries with the fastest growth of employment, how-

ever, the number of working hours per employee has fallen. This has occurred in

Finland, too, especially towards the latter half of the 1990s. In contrast, in countries

like the United States and Denmark, where the number of working hours has risen,

growth of employment and also of the standard of living has been slower.

22

14 The countries are organised by the growth rate of the standard of living.

Source: database of the University of Groningen.

Figure 6. Annual growth of the standard of living; broken down to the main

components, 1993–2001

23

01

23

4

Ja

pa

n

Sw

itze

rla

nd

Ge

rma

ny

Ita

ly

Fra

nce

Au

str

ia

Be

lgiu

m

Ne

the

rla

nd

s

US

A

De

nm

ark

UK

Po

rtu

ga

l

No

rwa

y

Sw

ed

en

Gre

ece

Sp

ain

Fin

lan

d

Ire

lan

d

-11

23

4

Ja

pa

n

Sw

itze

rla

nd

Ge

rma

ny

Ita

ly

Fra

nce

Au

str

ia

Be

lgiu

m

Ne

the

rla

nd

s

US

A

De

nm

ark

UK

Po

rtu

ga

l

No

rwa

y

Sw

ed

en

Gre

ece

Sp

ain

Fin

lan

d

Ire

lan

d

-1,0

-0,5

0,0

0,5

Ja

pa

n

Sw

itze

rla

nd

Ge

rma

ny

Ita

ly

Fra

nce

Au

str

ia

Be

lgiu

m

Ne

the

rla

nd

s

US

A

De

nm

ark

UK

Po

rtu

ga

l

No

rwa

y

Sw

ed

en

Gre

ece

Sp

ain

Fin

lan

d

Ire

lan

d

01

23

4

Ja

pa

n

Sw

itze

rla

nd

Ge

rma

ny

Ita

ly

Fra

nce

Au

str

ia

Be

lgiu

m

Ne

the

rla

nd

s

US

A

De

nm

ark

UK

Po

rtu

ga

l

No

rwa

y

Sw

ed

en

Gre

ece

Sp

ain

Fin

lan

d

Ire

lan

d

-11

23

4

Ja

pa

n

Sw

itze

rla

nd

Ge

rma

ny

Ita

ly

Fra

nce

Au

str

ia

Be

lgiu

m

Ne

the

rla

nd

s

US

A

De

nm

ark

UK

Po

rtu

ga

l

No

rwa

y

Sw

ed

en

Gre

ece

Sp

ain

Fin

lan

d

Ire

lan

d

-1,0

-0,5

01

23

4

Ja

pa

n

Sw

itze

rla

nd

Ge

rma

ny

Ita

ly

Fra

nce

Au

str

ia

Be

lgiu

m

Ne

the

rla

nd

s

US

A

De

nm

ark

UK

Po

rtu

ga

l

No

rwa

y

Sw

ed

en

Gre

ece

Sp

ain

Fin

lan

d

Ire

lan

d

-11

23

4

Ja

pa

n

Sw

itze

rla

nd

Ge

rma

ny

Ita

ly

Fra

nce

Au

str

ia

Be

lgiu

m

Ne

the

rla

nd

s

US

A

De

nm

ark

UK

Po

rtu

ga

l

No

rwa

y

Sw

ed

en

Gre

ece

Sp

ain

Fin

lan

d

Ire

lan

d

-1,0

-0,5

0,0

0,5

Ja

pa

n

Sw

itze

rla

nd

Ge

rma

ny

Ita

ly

Fra

nce

Au

str

ia

Be

lgiu

m

Ne

the

rla

nd

s

US

A

De

nm

ark

UK

Po

rtu

ga

l

No

rwa

y

Sw

ed

en

Gre

ece

Sp

ain

Fin

lan

d

Ire

lan

d

GD

P/w

ork

ing

ho

urs

Wo

rkin

gh

ou

rs/e

mp

loy

men

tE

mp

loy

men

t/p

op

ula

tio

n

2.3 The structure of productivity growth has

changed

The basis of labour productivity growth has shifted over to total factor productiv-

ity. This has been connected with a decreased impact of capital deepening arising

from the decline in the investment rate. This change reflects a decline in the invest-

ment rate and improved efficiency in use of production resources.

Labour productivity depends on two factors, total factor productivity (TFP15) and

capital deepening16. Total factor productivity refers to all residual effects of pro-

ductivity growth outside the increase in labour and capital. Among these are tech-

nological development, organisational innovations, dissemination of technological

information, and improved skills of the workforce. Total factor productivity is con-

sidered to be the most important indicator of growth, because it depicts the overall

efficiency of the use of production resources of economy.

Capital deepening of production refers to a growing substitution of capital for la-

bour. In the Western industrialised countries, and Finland in particular, capital

deepening has been boosted by favourable macroeconomic factors and labour

costs, which are considered high.

In Finland the main long-term source of growth of labour productivity has been to-

tal factor productivity with the average growth effect of around 1.8 percentage

points per year. The effect of capital deepening has varied between 1.2% and 1.8%,

respectively. In the early 1990s – before the fastest stage of the restructuring – Fin-

land showed one of the highest growth rates in total factor productivity (cf. Figure

7).

24

Labour

CapitalTFP

Labour

GDP�����

15 TFP = Total Factor Productivity.

16 The analysis of the components of labour productivity based on the hypotheses of the standard pro-

duction theory on the production possibilities and substitutability of inputs. The basic assumption is

constant returns to scale, i.e. an increase of inputs by one unit, increases the ouput by one unit. Then

growth of labour production can be expressed as a sum of total factor productivity and capital dee-

pening as follows:.

Source: European Competitiveness Report 2001.

Figure 7. Average annual contribution of total factor productivity to labour

productivity growth in the 1990s, %

Restructuring has increased the relative importance of total factor

productivity

The structure of total factor productivity changed essentially towards the end of the

past decade. The effect of total factor productivity rose to over three per cent, while

the impact of capital deepening diminished and turned even negative (cf. Figure 8).

This change resulted, above all, from the dynamic growth of the technology-inten-

sive electronics and ICT industries, which has boosted the total factor productivity

growth of manufacturing. The influence of total factor productivity has increased in

the traditional industries and in the private service sectors, too.

25

-1 0 1 2 3 4

Japan

Spain

Italy

Germany

EU-15

France

Netherlands

Belgium

UK

Denmark

Austria

USA

Luxembourg

Portugal

Greece

Sweden

Finalnd

Ireland

1995-2001

1990-1995

Along with the change in the industrial structure, the decrease in the investment rate

in the traditional manufacturing in particular has brought down the relative impor-

tance of physical capital17. Although developments in the majority of industrialised

countries have gone in the same direction, in Finland the change has been excep-

tionally drastic.

Source: European Competitiveness Report 2001.

Figure 8. Average annual contribution of capital deepening to labour produc-

tivity growth in the 1990s, %

26

-0,5 0 0,5 1 1,5

Finland

Ireland

Netherlands

Sweden

Italy

Spain

France

Belgium

UK

Luxembourg

Denmark

EU-15

Germany

Austria

USA

Greece

Japan

Portugal

1995-2001

1990-1995

17 Physical capital is increasingly being replaced by immaterial capital.

3 Industrial structure

Regeneration is the driving force of competitiveness

Renewal of production activities enhances productivity in three different ways.

Development of business activities and innovativeness within companies are re-

flected in industry-specific efficiency and thereby in productivity of economy. A

change in the industrial structure strengthens this effect, if the proportion of indus-

tries with rapid productivity growth increases. The third effect is brought about

through the transaction relations between industries18. The innovativeness of the

subcontracted industries, such as services, may raise the productivity of economy,

even if their productivity remained unchanged.

3.1 The market sector is expanding

The industrial structure in Finland resembles in broad outline the average of the

OECD countries and the EU Member States. The share of the service sector is

around two thirds, that of industry and construction less than one third, and the

share of primary production close to 5%. Compared with the United States and the

leading European countries, the share of the service sector of total production is,

however, about 10% lower in Finland, and the share has even decreased in recent

years.

As in the other Nordic countries, the public sector in Finland is mainly responsible

for the provision of welfare services. Consequently, the share of the public sector of

service production is internationally high. A look at the share of the so-called busi-

ness services19 in the whole service sector reveals that Finland and the other Nordic

countries are, nevertheless, going their separate ways. With the growing share of

business services, Finland is converging the USA and the leading European coun-

tries (cf. Figure 9).

27

18 Viitamo (2003).

19 This ratio also broadly illustrates the size of the public sector, as the services outside the business ser-

vice sector mainly consist of welfare services.

Source: OECD, STAN database.

Figure 9. Business services; share of the value added of the service sector

The growth of the demand for business services and gradual outsourcing of the ser-

vice activities of business enterprises have mainly influenced the development. As

a result of outsourcing, market-based production may increase even without any

growth in total production. The recent increase of business activities in provision of

welfare services has had similar effects.

3.2 Productivity growth is driven by

manufacturing

In Finland growth of labour productivity has ranked on the world’s top during the

past 20 years. The growth has mainly been driven by manufacturing, with the pro-

ductivity level already higher than in the USA.

Compared to manufacturing, the productivity level of services is distinctly lower

and growth slower. Nevertheless, the growth of productivity in the service sector

and in market-based services has been faster than in the OECD countries on aver-

age.

28

58

60

62

64

66

68

70

72

74

US

A

UK

Germ

any

Fra

nce

Neth

erlands

Fin

land

Norw

ay

Denm

ark

Sw

eden

-1

-0,5

0

0,5

1

1,5

2

2,5

3

3,5Share 2000

Change 1995 - 2000

% %

Productivity of manufacturing already higher than in the USA

By long-term productivity growth, Finland figures among the most competitive

countries in the world. During 1980–1999 the aggregate labour productivity rose

80%20, while in most of the OECD countries growth remained below 50% during

the same period. Productivity growth has been driven by manufacturing, where

productivity increased as much as 180%. At the end of the past decade, the produc-

tivity level of manufacturing was higher than in the United States (cf. Figure 10)21.

Measured by the number of employees, however, the difference is still around 10%

between the USA and Finland22.

Source: Database of the University of Groningen.

Figure 10. Development of productivity levels in manufacturing; measured by

working hours (USA = 100)

29

0 20 40 60 80 100 120

Australia

UK

Canada

Japan

Germany

France

Sweden

Netherlands

Belgium

USA

Finland

2000

1980

1960

20 Measured by working hours.

21 The method of calculating value added is based here on the unit values of industrial products. From

these the values and volume data are derived for product groups (University of Groningen;

http://www.eco.rug.nl/GGDC/icop.html)

22 Ireland, where productivity level is one of the highest in the world, is missing from the reference

countries.

While productivity of services and construction has increased slower than in manu-

facturing, the long-term growth of private services in particular ranks on the

world’s top. Of the most developed countries, Japan has experienced the fastest

productivity growth, around 70% during 1980–1999, but Finland is placed second

with the growth rate of 60%23.

This is also reflected in the narrowing down of Finland’s productivity gap with re-

spect to the USA. In 1980 the productivity level of private services was 40% lower

than the U.S. level, but in 1999 the difference was no more than about 20%. Al-

though Finland has during the same period outstripped e.g. Sweden and Denmark,

productivity level of services as a whole represents the average level of the indus-

trialised countries.

Ireland dominates in manufacturing, the USA in services; Finland is well

placed in both

The effect of manufacturing on the aggregate productivity growth is significant in

most countries, especially in countries with highest productivity growth rates (cf.

Figure 11). Of the EU Member States, Finland ranks second after Ireland, where

productivity growth in the service sector has been modest. Productivity growth

rates in services that are lower than the average are typical of many Central Euro-

pean countries as well, whereas in the Anglo-Saxon countries productivity growth

has been rapid.

In most developed countries productivity of business services has increased faster

than productivity in the service sector as a whole. This implies that productivity of

welfare services has increased slowly, if at all. While productivity of the service

sector in Finland has increased faster than in the OECD countries on average, the

difference with respect to the leading USA still remains considerable.

30

23 Mankinen, Rouvinen, Ylä-Anttila (2002)

Source: OECD, STAN database.

Figure 11. Annual productivity growth by main industrial sector, 1995–2000,

%24

31

Ind

ust

ryS

erv

ice

sect

or

Bu

sin

ess

serv

ices

00

,51

1,5

22

,5

Sp

ain

Ita

ly

Ne

the

rla

nd

s

Ja

pa

n

Fra

nce

No

rwa

y

Be

lgiu

m

Ge

rma

ny

De

nm

ark

UK

Au

str

alia

US

A

Ca

na

da

Au

str

ia

Sw

ed

en

Gre

ece

Fin

lan

d

Ire

lan

d

02

46

81

0

Sp

ain

Ita

ly

Ne

the

rla

nd

s

Ja

pa

n

Fra

nce

No

rwa

y

Be

lgiu

m

Ge

rma

ny

De

nm

ark

UK

Au

str

alia

US

A

Ca

na

da

Au

str

ia

Sw

ed

en

Gre

ece

Fin

lan

d

Ire

lan

d

00

,51

1,5

22

,53

Sp

ain

Ita

ly

Ne

the

rla

nd

s

Ja

pa

n

Fra

nce

No

rwa

y

Be

lgiu

m

Ge

rma

ny

De

nm

ark

UK

Au

str

alia

US

A

Ca

na

da

Au

str

ia

Sw

ed

en

Gre

ece

Fin

lan

d

Ire

lan

d

00

,51

1,5

22

,5

Sp

ain

Ita

ly

Ne

the

rla

nd

s

Ja

pa

n

Fra

nce

No

rwa

y

Be

lgiu

m

Ge

rma

ny

De

nm

ark

UK

Au

str

alia

US

A

Ca

na

da

Au

str

ia

Sw

ed

en

Gre

ece

Fin

lan

d

Ire

lan

d

02

46

81

0

Sp

ain

Ita

ly

Ne

the

rla

nd

s

Ja

pa

n

Fra

nce

No

rwa

y

Be

lgiu

m

Ge

rma

ny

De

nm

ark

UK

Au

str

alia

US

A

Ca

na

da

Au

str

ia

Sw

ed

en

Gre

ece

Fin

lan

d

Ire

lan

d

00

,51

1,5

22

,5

Sp

ain

Ita

ly

Ne

the

rla

nd

s

Ja

pa

n

Fra

nce

No

rwa

y

Be

lgiu

m

Ge

rma

ny

De

nm

ark

UK

Au

str

alia

US

A

Ca

na

da

Au

str

ia

Sw

ed

en

Gre

ece

Fin

lan

d

Ire

lan

d

02

46

81

0

Sp

ain

Ita

ly

Ne

the

rla

nd

s

Ja

pa

n

Fra

nce

No

rwa

y

Be

lgiu

m

Ge

rma

ny

De

nm

ark

UK

Au

str

alia

US

A

Ca

na

da

Au

str

ia

Sw

ed

en

Gre

ece

Fin

lan

d

Ire

lan

d

00

,51

1,5

22

,53

Sp

ain

Ita

ly

Ne

the

rla

nd

s

Ja

pa

n

Fra

nce

No

rwa

y

Be

lgiu

m

Ge

rma

ny

De

nm

ark

UK

Au

str

alia

US

A

Ca

na

da

Au

str

ia

Sw

ed

en

Gre

ece

Fin

lan

d

Ire

lan

d

24 Productivity has been calculated as an annual change of fixed value added (base year 1995) in relati-

on to the number of the employed. The order of the countries is based on the aggregate productivity

growth.

3.3 Information and communications technology

shows the way

Productivity growth has been fastest in the industries producing ICT, in which the

growth is among the highest in the world. Of the industries utilising ICT exten-

sively, productivity growth has been strong in financing and in manufacturing of

electrical machinery. In general, there remains much to improve in utilisation of

ICT across industries.

Except for manufacture of communications equipment, high productivity growth

is concentrated on relatively narrow groups of industries. In contrast, productivity

growth in the industries with the highest GDP share has been slack. Among these

are construction, public services and some of the central private services. This im-

balance partly explains the Finnish paradox of why the aggregate productivity

and standard of living are only of the international average.

As conveyed by the recent studies, information and communications technology

(ICT) has become one of the major factors explaining the productivity differences

across industries. In its international benchmarking studies on productivity, the

University of Groningen applies an ICT-based industry taxonomy. It divides indus-

tries into those producing and utilising ICT extensively and into industries that uti-

lise ICT only little or not at all (other sectors)25. The classification is based on an

empirical finding that productivity growth in the ICT industries is faster on average

than in other sectors.

32

25 The classification is based on the ICT investments statistics by industry in the USA, which reflects

the utilisation potential of ICT in other developed countries (Bart van Ark & al. 2002). Note that there

may be sector-specific differences across countries. For instance, in Finland transportation and logis-

tic services utilise extensively ICT-based applications (Viitamo, 2003).

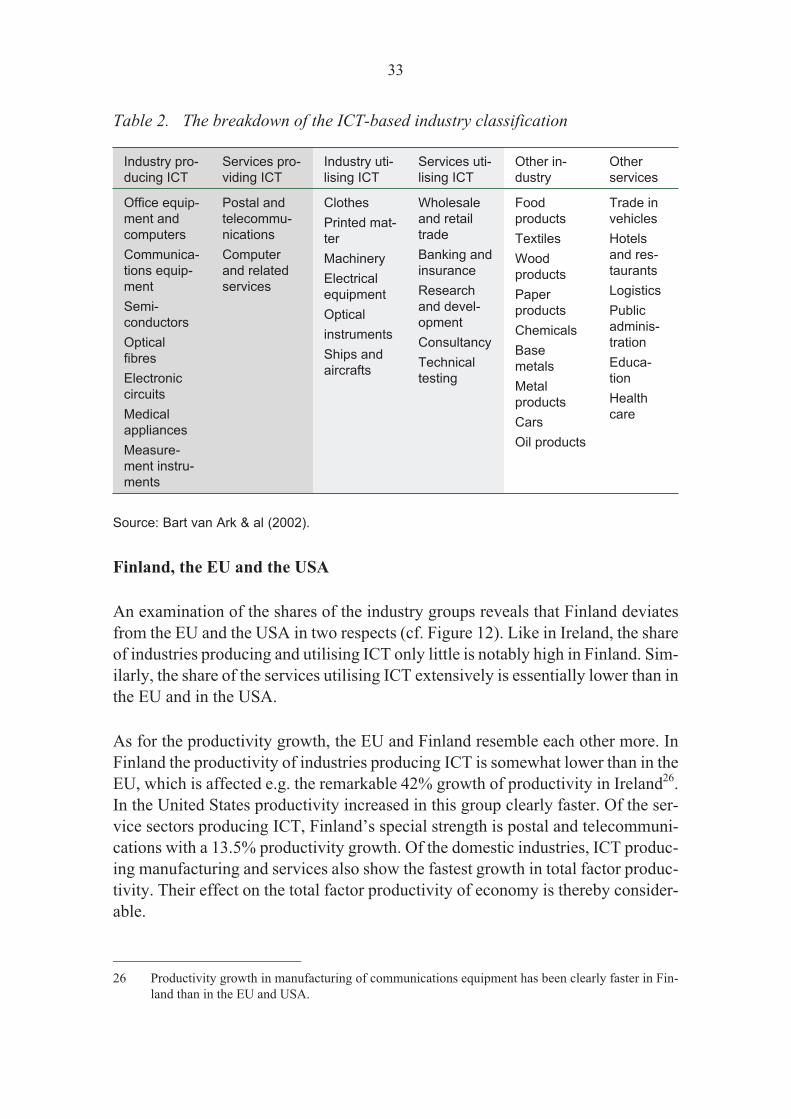

Table 2. The breakdown of the ICT-based industry classification

Industry pro-

ducing ICT

Services pro-

viding ICT

Industry uti-

lising ICT

Services uti-

lising ICT

Other in-

dustry

Other

services

Office equip-

ment and

computers

Communica-

tions equip-

ment

Semi-

conductors

Optical

fibres

Electronic

circuits

Medical

appliances

Measure-

ment instru-

ments

Postal and

telecommu-

nications

Computer

and related

services

Clothes

Printed mat-

ter

Machinery

Electrical

equipment

Optical

instruments

Ships and

aircrafts

Wholesale

and retail

trade

Banking and

insurance

Research

and devel-

opment

Consultancy

Technical

testing

Food

products

Textiles

Wood

products

Paper

products

Chemicals

Base

metals

Metal

products

Cars

Oil products

Trade in

vehicles

Hotels

and res-

taurants

Logistics

Public

adminis-

tration

Educa-

tion

Health

care

Source: Bart van Ark & al (2002).

Finland, the EU and the USA

An examination of the shares of the industry groups reveals that Finland deviates

from the EU and the USA in two respects (cf. Figure 12). Like in Ireland, the share

of industries producing and utilising ICT only little is notably high in Finland. Sim-

ilarly, the share of the services utilising ICT extensively is essentially lower than in

the EU and in the USA.

As for the productivity growth, the EU and Finland resemble each other more. In

Finland the productivity of industries producing ICT is somewhat lower than in the

EU, which is affected e.g. the remarkable 42% growth of productivity in Ireland26.

In the United States productivity increased in this group clearly faster. Of the ser-

vice sectors producing ICT, Finland’s special strength is postal and telecommuni-

cations with a 13.5% productivity growth. Of the domestic industries, ICT produc-

ing manufacturing and services also show the fastest growth in total factor produc-

tivity. Their effect on the total factor productivity of economy is thereby consider-

able.

33

26 Productivity growth in manufacturing of communications equipment has been clearly faster in Fin-

land than in the EU and USA.

Source: Bart van Ark & al (2002).

Figure 12. ICT industries; size and annual productivity growth, 1995–2000

34

010

20

30

40

50

ICT

pro

du

cin

g

ma

nu

factu

rin

g

ICT

pro

du

cin

g

se

rvic

es

ICT

usin

g

ma

nu

factu

rin

g

ICT

usin

g

se

rvic

es

Oth

er

ma

nu

factu

rin

g

Oth

er

se

rvic

es

Fin

lan

d

US

A

EU

05

10

15

20

25

ICT

pro

du

cin

g

ma

nu

factu

rin

g

ICT

pro

du

cin

g

se

rvic

es

ICT

usin

g

ma

nu

factu

rin

g

ICT

usin

g

se

rvic

es

Oth

er

ma

nu

factu

rin

g

Oth

er

se

rvic

es

Fin

lan

d

US

A

EU

010

20

30

40

50

ICT

pro

du

cin

g

ma

nu

factu

rin

g

ICT

pro

du

cin

g

se

rvic

es

ICT

usin

g

ma

nu

factu

rin

g

ICT

usin

g

se

rvic

es

Oth

er

ma

nu

factu

rin

g

Oth

er

se

rvic

es

Fin

lan

d

US

A

EU

05

10

15

20

25

ICT

pro

du

cin

g

ma

nu

factu

rin

g

ICT

pro

du

cin

g

se

rvic

es

ICT

usin

g

ma

nu

factu

rin

g

ICT

usin

g

se

rvic

es

Oth

er

ma

nu

factu

rin

g

Oth

er

se

rvic

es

Fin

lan

d

US

A

EU

Sh

are

of

the

GD

Pin

20

00

%P

rod

uct

ivit

yg

row

th%

Although in Finland, too, the productivity of sectors utilising ICT extensively is

higher than in the other sectors, the case of manufacturing is the opposite. For in-

stance, the forest industries, belonging to the non-ICT group, a faster productivity

growth than in the EU and USA. In terms of services utilising ICT, the ranking of

Finland is good, with only the USA, Norway and Sweden ahead of us. Here the

spearhead industries are financial intermediation and other activities auxiliary to fi-

nancing.

The spear is sharp but thin-pointed

A more detailed examination confirms that the ICT industries are on top of produc-

tivity development in Finland. Table 3 presents a compilation of the industries with

productivity growth during 1995–2000 at least as rapid as in economy as a whole

(2.4%). In 1998 the share of this group of total production was 41%, productivity

growth 5.1% and production growth 7.1%.

Table 3. Sectors with fastest production growth, 1993–2001

Industry Percentage

(GDP)

1998

Annual growth of

productivity %

(working hours)

Annual growth

of production %

(value added)

ICT producer Radio- and communications equip-

ment

3.5 15.3 35.1

ICT user Activities auxiliary to financing 0.2 10.5 22.0

ICT producer Postal and telecommunications 2.7 9.6 10.9

ICT user Financial intermediation 2.7 6.1 1.8

Electricity, gas and water supply 2.3 5.2 1.7

ICT user/

producer

Electrical machinery and equip-

ment

0.9 4.7 7.7

Agriculture and forestry 3.7 4.7 1.7

Chemicals 1.5 4.2 4.8

Base metals 1.1 4.1 5.0

Other vehicles 0.3 3.7 8.9

ICT user Publishing and printing business 1.5 3.4 3.2

Wood products 1.2 3.3 5.9

Food products 1.9 3.1 1.5

Pulp and paper 4.1 3.1 3.9

ICT user Other machinery and equipment 2.9 3.0 6.4

ICT user Wholesale and retail trade 10.5 3.0 4.8

Mining 0.2 2.8 2.8

Total 41.4 5.1 7.1

Source: OECD, STAN database.

35

The share of the ICT industries of the productivity growth of the industries listed

under Table 3 is around 70 % and over 80 % of production growth. The impact of

the ICT sectors on the growth of the entire economy is also high on average, with

the most significant exception financial intermediation, in which productivity

growth is based on capital deepening.

Large sectors and services utilising ICT only little are the weak points

In a similar way, the most problematic areas of productivity growth can be illus-

trated by examining the development of the largest industries (cf. Table 427). In

1998 the GDP share of this sector of was 48%, total productivity growth 0.5% and

production growth 2.5% during 1993–2001.

The largest industries consist of public services, real-estate services, transportation

and construction. The proportion of public services of GDP is nearly 18% and their

productivity and growth is among the lowest of this group. Other industries with

low performance are construction, business services and other societal and personal

services. Thus Finland’s average ranking in productivity and standard of living

can be explained by the high GDP share of sectors with low productivity growth.

Table 4. Development of the productivity and production of the largest indust-

ries, 1993–2001

Sector Percentage

(GDP)

1998

Annual

productivity

growth %

(working hours)

Annual

production

growth %

(value added)

Real-estate services 11.0 2.1 3.0

Health care and social services 7.8 -0.5 1.1

Transportation and storage 7.3 1.7 3.6

Construction 5.0 -2.2 1.5

Public administration and defence 5.0 0.7 1.0

Education and training 4.9 -0.6 1.7

ICT user Business services 3.7 0.1 6.4

Other societal and personal services 3.5 0.3 2.9

Total 48.2 0.5 2.5

Source: OECD, STAN database.

36

27 Of the largest sectors, retail and wholesale trade (2.), pulp and paper industry (8.) and agriculture and

forestry (10.) have been excluded here.

3.4 Technology- and knowledge-intensity is

increasing

In Finland the change in the industrial structure has been biggest in manufactur-

ing, where the share of technology-intensive sectors of total production is one of

the highest in the world. This restructuring has, above all, resulted from the dy-

namic growth of the ICT manufacturing. Restructuring has, at the same time,

strongly contributed to the aggregate productivity growth.

The restructuring of manufacturing is also reflected in the rapid increase in the

technology-intensity of goods exports. The technology-intensity of exports has

reached the average level of the OECD countries.

In Finland the GDP share of knowledge-intensive services is lower than in indus-

trialised countries on average. The growth of their GDP has, however, been

among the fastest in the OECD countries.

The growth of the technology-intensiveness of manufacturing has been

among the fastest in the world

Measured by the production structure of the manufacturing sector, Finland is one of

world’s most technology-intensive countries. After the leading countries, Ireland

and Korea, the differences between Hungary, Germany and Finland are small. This

can be seen when examining the proportion of high and medium-high technology

industries of total production (cf. Figure 13). In Finland the impact of high technol-

ogy, mainly communications technology, is remarkable, and its relative share is the

highest of the OECD countries. In Finland the share of medium-high technology

sectors is lower than on average. This is influenced e.g. by the high GDP share of

the forest industry, which belongs to low technology industries.

37

Source: OECD, STAN database.

Figure 13. Technology-intensive manufacturing; the share of the GDP, %

Restructuring has boosted productivity growth

In regard to the restructuring of manufacturing and growth of technology-intensity

(cf. Figure 14), the OECD countries can be divided into three groups; countries

where the overall change has been negative, countries where the increase in the

shares of technology groups have balanced, and countries where the change has

been driven by high-tech manufacturing. Finland, which belongs to the latter

group, ranks first in terms of the growth of the share of high-tech manufacturing

and thereby specialisation.

When Figure 14 is compared with Figure 11 illustrating productivity growth, the

dependence between restructuring and productivity growth becomes obvious.

Countries where the share of high-tech industries has increased the most are also

positioned high with regard to productivity growth in manufacturing. The most ob-

vious exception is the USA, where technology-intensiveness has, in fact, de-

creased. Nonetheless, productivity has increased in the USA, too, and faster than on

average. For the USA productivity growth is more induced by internal renewal of

industries and wide-scoped utilisation of ICT.

38

0

5

10

15

20

25

Irela

nd

Kore

a

Hungary

Germ

any

Fin

land

Japan

Sw

eden

Belg

ium

Canada

Mexic

o

US

A

Fra

nce

Italy

Austr

ia

UK

Denm

ark

Spain

Neth

erl

ands

Austr

alia

Norw

ay

Gre

ece

Medium-hightech

Hightech

Source: OECD, STAN database.

Figure 14. The share of technology-intensive manufacturing; annual change of

the GDP, 1992–2001

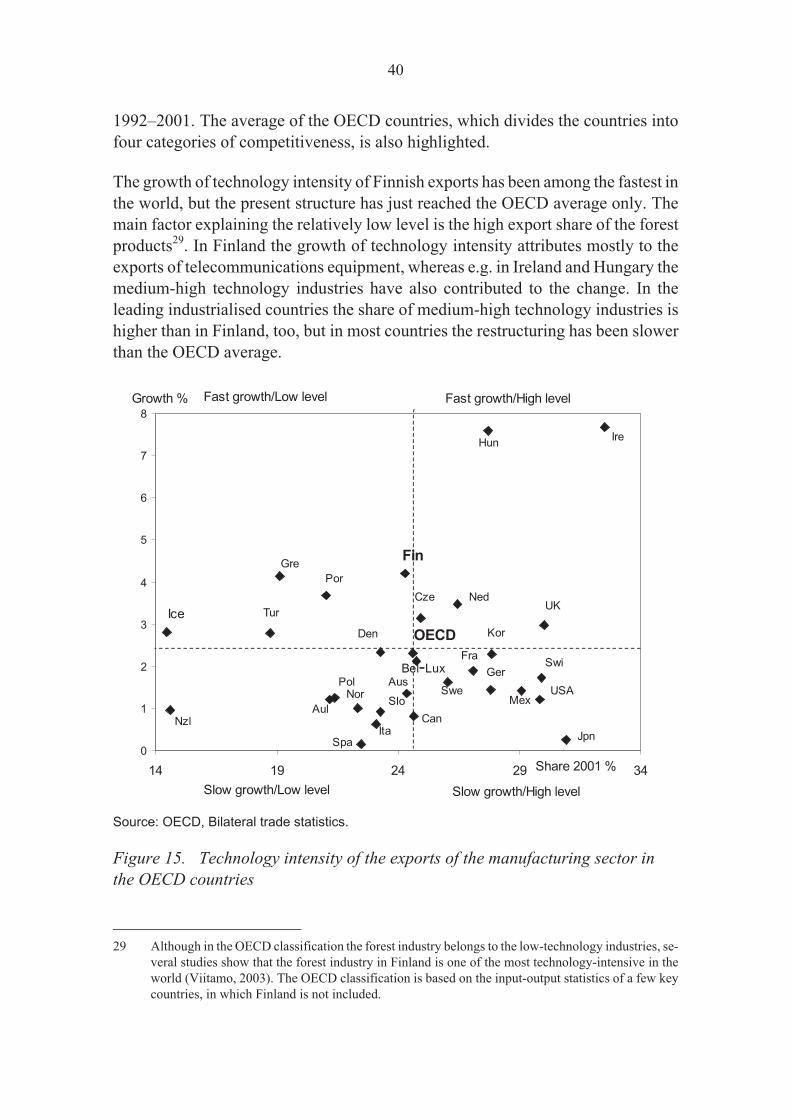

The technology-intensiveness of goods exports has reached the average

OECD level

The restructuring of manufacturing is reflected in the technology-intensity of goods

exports as well. This is measured by the weighted average of the export shares of

the four technology categories.28 The horizontal axis of Figure 15 measures the

value of the indicator in 2001 and the vertical one the absolute change during

39

-10 -5 0 5 10 15 20

Greece

Spain

Italy

Germany

Netherlands

Australia

Japan

USA

UK

France

Belgium

Norway

Austria

Canada

Denmark

Sweden

Korea

Ireland

Mexico

Hungary

Finland

Medium-hightech

Hightech

28 The weightings have been given as follows: high technology (0.4), medium-high technology(0.3),

medium-low technology (0.2) and low technology (0.1).

1992–2001. The average of the OECD countries, which divides the countries into

four categories of competitiveness, is also highlighted.

The growth of technology intensity of Finnish exports has been among the fastest in

the world, but the present structure has just reached the OECD average only. The

main factor explaining the relatively low level is the high export share of the forest

products29. In Finland the growth of technology intensity attributes mostly to the

exports of telecommunications equipment, whereas e.g. in Ireland and Hungary the

medium-high technology industries have also contributed to the change. In the

leading industrialised countries the share of medium-high technology industries is

higher than in Finland, too, but in most countries the restructuring has been slower

than the OECD average.

Source: OECD, Bilateral trade statistics.

Figure 15. Technology intensity of the exports of the manufacturing sector in

the OECD countries

40

0

1

2

3

4

5

6

7

8

14 19 24 29 34

IreHun

FinGre

Por

NedCzeUK

Ice Tur

Den OECD

Bel-Lux

Kor

Fra

Swe

Swi

NzlAul

Nor

GerPol

USA

JpnSpa

Aus

ItaCan

Slo Mex

Fast growth/Low level Fast growth/High level

Slow growth/Low level Slow growth/High level

Share 2001 %

Growth %

29 Although in the OECD classification the forest industry belongs to the low-technology industries, se-

veral studies show that the forest industry in Finland is one of the most technology-intensive in the

world (Viitamo, 2003). The OECD classification is based on the input-output statistics of a few key

countries, in which Finland is not included.

The growth of the knowledge-intensiveness in the service sector ranks on the

world’s top

The so-called knowledge-intensive business services30, which belong to business

services, play a central role with respect to growth of competitiveness. According

to an ICT-based industry classification, the knowledge-intensive service sector in-

cludes services producing ICT, i.e. postal and telecommunications, computer ser-

vices and services utilising ICT (excluding the sectors of trade).

High knowledge-intensity of services or extensive use of ICT are not necessarily

associated with high growth of productivity. For instance, in many business service

sectors value added has increased on a par with the labour input (cf. Table 3). More

often, the competitiveness effects of knowledge-intensive services manifest them-

selves in indirect productivity impacts in client industries.

In most of the OECD countries, the proportion of knowledge-intensive services of

total production and the service sector is increasing (cf. Figure 16). A positive dif-

ference between these indicators implies that the proportion of the service sector of

total production is increasing. As indicated by Figure 16, the trend in Finland, Can-

ada, Norway and Ireland have been the opposite in recent years. That is, the GDP

share of the service sector is diminishing31.

In Finland the growth of the share of the knowledge-intensive services has been

rapid by the international standard, and fastest, if the change in this share is viewed

within the service sector. The fastest-growing industries in Finland are computer

services and postal and telecommunications. Among the factors that have contrib-

uted to this are the dynamic growth of the ICT manufacturing, outsourcing of ser-

vice activities and liberalisation of the telecommunications market at the beginning

of the 1990s.

41

30 KIBS = Knowledge Intensive Business Services.

31 Unlike the GDP share, the proportion of the service sector of total employment has been on a con-

tinuous increase in Finland, which partly reflects the relative decline in productivity in the service

sector with respect to other sectors. However, this is not characteristic of Finland only. In many

OECD countries employment has increased faster than the GDP share.

Source: OECD STAN database32.

Figure 16. Knowledge-intensive business services; annual growth 1996–2001,

%

42

-0,5 0,5 1,5 2,5 3,5 4,5

Spain

France

Norway

Canada

Austalia

Belgium

Denmark

Austria

Sweden

Germany

Italy

UK

Korea

Ireland

Japan

Mexico

USA

Greece

Finland

Netherlands

Hungary

Luxembourg

Share of the service sector

Share of the GDP

(44,5)

(16,3)

(21,0)

(10,5)

(22,5)

(15,1)

(13,5)

(13,5)

(15,4)

(20,5)

(16,5)

(16,9)

(20,0)

(15,6)

(17,6)

(20,9)

(12,2)

(15,8)

(23,4)

(13,0)

(28,6)

(22,2)

32 The share of knowledge-intensive services of total production in the latest year available 1999–2001

is given in brackets.

3.5 Industry restructuring reflects the dynamics of

company demography

In contrast to the EU, production and employment in manufacturing have centred

on large companies in Finland. The majority of new firms are enterprises with one

employee only. Therefore the employment effect of new firms is among the lowest

of the developed countries.

In Finland the enterprise volatility rate has been of the international average, but

the growth of the number of enterprises is slow. In manufacturing the enterprise

volatility rate is lower than in the service sectors, where the costs of entries and ex-

its are lower. The volatility rate is also influenced by the rapidity of technological

change and the knowledge-intensity of industries. The enterprise volatility has in-

creased productivity of industries.

Enterprise volatility is restructuring on the micro level

Change in the industrial structure is ultimately determined by the differences in the