Collaboration The Butterfly Effect -...

23

Survey conceptualised and initiated by Global Supply Chain Dynamics – Measuring the Butterfly Effect for South Africa supplychainforesight 2009 Collaboration Network Integration Planning Forecasting Visibility Agility Strategic alignment Optimisation FMCG/Retail Report www.supplychainforesight.co.za

Transcript of Collaboration The Butterfly Effect -...

Survey conceptualised and initiated by

Global Supply Chain Dynamics – Measuring the Butterfly Effect

for South Africa

supplychainforesight

2009

CollaborationNetwork

IntegrationPlanning

Forecasting

Visibility

Agility

Strategic alignment

Optimisation

FMCG/Retail Report

www.supplychainforesight.co.za

1

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

The supplychainforesight report for 2009, true to tradition for this benchmark piece of South African strategic supply chain research, is right up to the minute in offering insights into supply chain strategy and operations in the global recession and economic crisis.

Last year’s research focused on those companies that were earning competitive advantage from their supply chains in a global context of economic growth and market diversity. However, the macro-economic situation in which the research takes place this year could not be more different. The global growth boom was enabled by the building out of global supply chains into an intricately intertwined network of supply and demand all over the world. Now, the global recession means that an industry decision on the other side of the world to put the brakes on growth plans could mean serious consequences for suppliers in South Africa. We’ve called this the Butterfly Effect – the phenomenon where a small change at one place in a complex system can have large effects elsewhere.

The 2009 supplychainforesight survey has been conducted by respected international research company Frost and Sullivan, and continues to be conceived and sponsored by Barloworld Logistics.

In this year’s overall report we delved into the impact of the Butterfly Effect in different areas of urgent relevance for SA’s supply chains, including the move to localisation, the relationship between business strategy and supply chain strategy, and the latest views of the industry on outsourcing and environmental agendas – all with the trenchant comment and insight the market has come to expect from the research.

Also true to tradition is the quality and depth of the response to the questionnaire with around 250 senior executives and supply chain managers in most of SA’s major companies across key industries taking part. This maintains the focus of the research, established over the past six years, on large multinational companies whose strategies shape much of the country’s economy.

Each year the research is taken from these key industries and presented back as a focused insight into the industry concerned. As part of this exercise, each key SA industry is compared to the overall view of supply chain management and senior executive viewpoints given in the main report. For the FMCG/Retail supply chain this year, different responses were measured from both the supply side and the retail side. Throughout the report, these are compared and contrasted.

Apart from this, the 2009 edition of supplychainforesight for the FMCG/Retail industry is structured according to many of the key themes and findings that appeared in the main report, but focuses specifically on the following ways in which South Africa’s major FMCG supply chains are responding to the global economic meltdown:

• Short-termFMCGsupplychainobjectivesandchallenges: Tracking industry trends and strategies, including responses to the economic crisis and the focus on aligning the supply chain strategy with the business strategy. Since supplychainforesight has been tracking the FMCG/Retail industry since the inception of the research six years ago, we also draw some comparative conclusions about the strategic trend in the sector.

The Butterfly Effect

supplychainforesight

20092

• Outsourcingrevisited: an in-depth look at the outsourcing question in the FMCG/Retail sector reveals a characteristic maturity about the reasons for and the value of outsourcing – in accordance with the picture in the overall research this year.• Industryinvestment:where the senior supply chain executives in FMCG are planning to invest, and why. • Speakingthesamelanguage–PrivateandPublicsectorco-operation: This section addresses a perennially difficult issue for the FMCG/Retail industry, which is often dependent on complex physical distribution networks – the challenges presented to the private sector by the public sector’s supply chain and logistics initiatives, especially the physical logistics infrastructure of the country. • TheRealGreenissues: An in-depth look at the levels of awareness and business thinking in SA around sustainable environmentally-friendly business practices reveals that South Africa Inc has a long way to go on the issue. This is, surprisingly, especially true for the FMCG/Retail sector, which, despite indirectly or directly servicing the consumer market, is fairly non-committal about the value of investment in environmental sustainability.

FMCGObjectivesandChallenges

In this section we present the trend-tracking section of the survey, which takes place every year and provides our findings with some context – how senior executives and supply chain managers in the sector view their supply chain objectives and challenges for the coming year.

The short term (1-2 years) objectives of the FMCG sector have become realigned to the restrictive market conditions in a very interesting way. A graphic depiction of these objectives can be seen here.

High Significant Medium LowCritical

ImportanceLevels

Legend

16% 14% 16%

11% 11%3% 6%14%

5% 12% 5% 9% 9%

5% 16% 23% 12% 5%

30% 9% 12% 5%

2%

Fig1:KeyShort-termObjectivesofFMCGSector

60%0% 40%20%

Alignment with business objectives

Demand driven production

Procurement optimisation

Vertical Integration of ERP and P&F tools

Inventory management

3

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

As can be seen, the top 5 leading short term objectives of the FMCG industry sector, in order of first-rank importance, are:

• Aligningthesupplychainwithbusinessstrategy• Demand-drivenproduction• Procurementoptimisation• Inventorymanagement• VerticalintegrationofERPandPlanning&Forecasting(P&F)tools.

Over the last five years of the supplychainforesight study, some of these same objectives, crucial cornerstones for effective supply chains in the sector, have appeared time and time again.

Improve service offered to customers

Reduce investment in inventory

Increase flexibility and responsiveness

of manufacturing

Improve cooperation/ collaboration in the

supply chain

Improve information visibility

0% 10% 20%

37%

37%

42%

47%

59%

30% 40% 60%50% 70%

Fig2B:FMCGObjectives2005

Reduce investment in inventory

Increase effectiveness of procurement

processes

Reduce out of stocks

Improve services offered to customers

Reduce costs of transportation

0% 10% 40%20% 50% 70%

63%

63%

58%

57%

50%

30% 60%

Fig2A:FMCGObjectives2004

20%

24%

26%

31%

60%Improve service offered to customers

Increase shelf availability/ reduce

out of stocks

Improve cooperation/ collaboration in the

supply chain

Reduce supply chain costs

Reduce investment in

industry

0% 10% 40% 60%20% 50% 70%30%

Fig2C:FMCGObjectives2006

Reduce out-of-stocks/ increase shelf availability

Improve services offered to customers

Lower warehousing and distribution costs

on-time deliveries

Lower the costs of manufacturing

0%

7%

8%

11%

15%

21%

15% 25%5% 10% 20%

Fig2D:FMCGObjectives2007

16% 12% 16% 7%16%

30% 14% 14% 14%

2%

12% 9% 12% 14% 7%

supplychainforesight

20094

81%

94%

100%

77%

74%

Lower sourcing/ procurement

costs

Reduce out-of-stocks/increase shelf

availability

Improve service offered to customers

Reduce investment in inventory

Lower warehousing and distribution costs

0% 90% 100%30%10% 20% 40% 50% 60% 80%70%

Fig2E:FMCGObjectives2008

In almost every instance, the FMCG focus in previous years has been on supplying the right kind of stock at the right service levels to the retail trade – service delivery has been paramount, as has the focus on improving collaboration with their downstream retail customers.

For the first time since the survey began six years ago, the FMCG sector shows a major shift in their strategic thinking. The top-ranked objective of strategic alignment was in fact ranked as important only by 9% of FMCG respondents last year, as opposed to the 46% of the retail response who rated it as significant. Now, almost a third of the respondents rate it as their first priority, with the traditional areas of inventory management (even though this remains the most widely-ranked factor) and planning and forecasting slipping down the rankings. The fact that demand-driven production and procurement optimisation have moved up in importance as objectives points to a more collaborative attitude with retailers, and a more holistic approach to cost containment and supply chain planning.

As far as challenges in the FMCG sector are concerned, the picture is somewhat more practical and tactically oriented.

Growing severity of economic slowdown

Making supply chain demand-driven

Making the supply chain lean

Oil price volatility

Efficient P&F tools

90%0% 60%30%

Fig3:WhatChallengesareShapingtheStrategiesofFMCG?

High Significant Medium LowCritical

ImportanceLevels

Legend

19% 16% 12%19%

21% 12% 12%19%

2%

5%

5

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility The growing severity of the economic slowdown is first on the agenda, though it is regarded slightly less seriously than by the general sample – perhaps because the true extent of the slowdown was yet to hit the sector at the time the data was collected – followed by the ongoing struggle to make the supply chain demand-driven, and lean. These factors, demand-led and lean supply chains, appear in reverse order of importance in the Retail picture. Finally, the oil price volatility for the FMCG sector also features as a challenge, since it is dependent on fuel-heavy manufacturing and transport operations.

The differences between this year’s picture and previous years’ research are again instructive. Without fail the major challenges in the past were related to planning and forecasting accuracy, closely followed by skills shortages and the means to collaborate effectively.

42%

43%

43%

50%

68%Improve planning

and forecasting capabilities

Create supply chain collaboration

opportunities

Benchmark our supply chain performance and improve

our use of existing IT systems

Improve the core capabilities of our supply chain staff

Change our physical logistics/

distribution network

0% 10% 40% 60%20% 50% 70%30%

Fig4A:FMCGChallenges2004

33%

35%

35%

44%

58%Our planning

and forecasting abilities

Aligning our skills to meet the supply

chain strategy

The capabilities of our existing IT systems

The physical distribution network

The skills/ capabilities of our supply chain staff

0% 10% 40% 60%20% 50% 70%30%

Fig4C:FMCGChallenges2005

24%

26%

26%

26%

35%Our planning

and forecasting abilities

The specialised needs of customers

Skills and capabilities of our SC staff

Benchmarking our supply chain

performance

Creating SC collaboration opportunities

0% 5% 20% 30%10% 25% 35%15%

Fig4B:FMCGChallenges2006

14% 16% 18%

7%

9%

7%

9%

17%

The increased complexity of our

supply chain

Our planning and forecasting

capabilities

Skills and capabilities of supply chain staff

The diverse needs of our customers

The increased volume in our supply chain

0% 6%2% 4% 8% 10% 12%

Fig4D:FMCGChallenges2007

supplychainforesight

20096

92%

78%

78%

98%

100%

Our planning and forecasting

abilities

The increased volume in our

supply chain

Capabilities of our existing IT systems

Skills and capabilities of our supply chain staff

Our distribution network

0% 30%10% 20% 40% 50% 60% 80%70% 90% 100%

Fig4E:FMCGChallenges2008

We might conclude from the shift in the challenges picture that the FMCG industry has found a more focused and strategic means of working with the retail sector to move to a demand-driven supply chain as a means to address planning and forecasting accuracy. Outsourcing of supply chain functions may also be assisting in addressing the skills shortages that previously presented a consistent challenge in the sector.

RetailObjectivesandChallenges

For the retail side, a more traditional picture for industry short-term objectives is seen. Inventory management remains the number one priority, with strategic alignment a distant second, and far less of a priority than the FMCG sector. With procurement optimisation appearing in third place, it’s clear that the business focus remains on stock availability and cost containment.

High Significant Medium LowCritical

ImportanceLevels

Legend

25% 11% 6% 11% 6%

6% 22% 11% 17% 3%

11% 11% 8% 6%

9% 6% 6% 6% 3%

6% 3% 6%

Fig5:KeyShort-termObjectivesoftheRetailSector2009

Inventory Management

Alignment with business objectives

Procurement optimisation

Demand-driven production

Improved collaboration

0% 40% 60%20%

7

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

While the picture in previous years focused on planning and forecasting and collaboration opportunities, the current focus on inventory management and procurement optimisation might be seen as progress on the collaboration front with the FMCG sector, even if the optimisation of procurement may represent a rationalisation of the supplier base.

Reduce investment in

inventory

Increase effectiveness of procurement

processes

Reduce out of stocks

Improve services offered to customers

Reduce costs of transportation

0% 10% 40%20% 50% 70%

63%

63%

58%

57%

50%

30% 60%

Fig6A:RetailObjectives2004

35%

30%

30%

39%

43%

Improve services offered to customers

Increase shelf availability/reduce

out of stocks

Reduce investment in inventory

Improve co-operation/ collaboration in

supply chain

Reduce warehouse operating costs

0% 15%5% 10% 20% 25% 30% 40%35% 45%

Fig6C:RetailObjectives2006

10%

8%

8%

10%

12%

Reduce out-of-stocks/increase

shelf availability

Improve service offered to customers

Improve co-operation/ collaboration in the

supply chain

Redefine our supply chain strategy

Improve flexibility and agility of supply chain

0% 4%2% 6% 8% 10% 14%12%

Fig6D:RetailObjectives2007

80%

33%

63%

59%

48%

68%

Reduce investment in inventory

Improve collaboration/ co-operation in

the supply chain

Increase shelf availability/ reduce

out of-stocks

Improve information visibility

Improve service offered to customers

0% 30%10% 20% 40% 50% 70%60%

Fig6B:RetailObjectives2005

31%

25%

17%

3%

6%

11%

14%

6%

11%

28%

14%

8%

11%

3%

8%

14%

11%

8%

6%

17%

8%

3%

14%

6%

supplychainforesight

20098

82%

80%

60%

89%

100%

Improve services offered to customers

Reduce investment in

inventory

Reduce out-of-stocks/ increase shelf

availability

Improve co-operation/ collaboration in

supply chain

Decreased lead times

0% 30%10% 20% 40% 50% 60% 80%70% 90% 100%

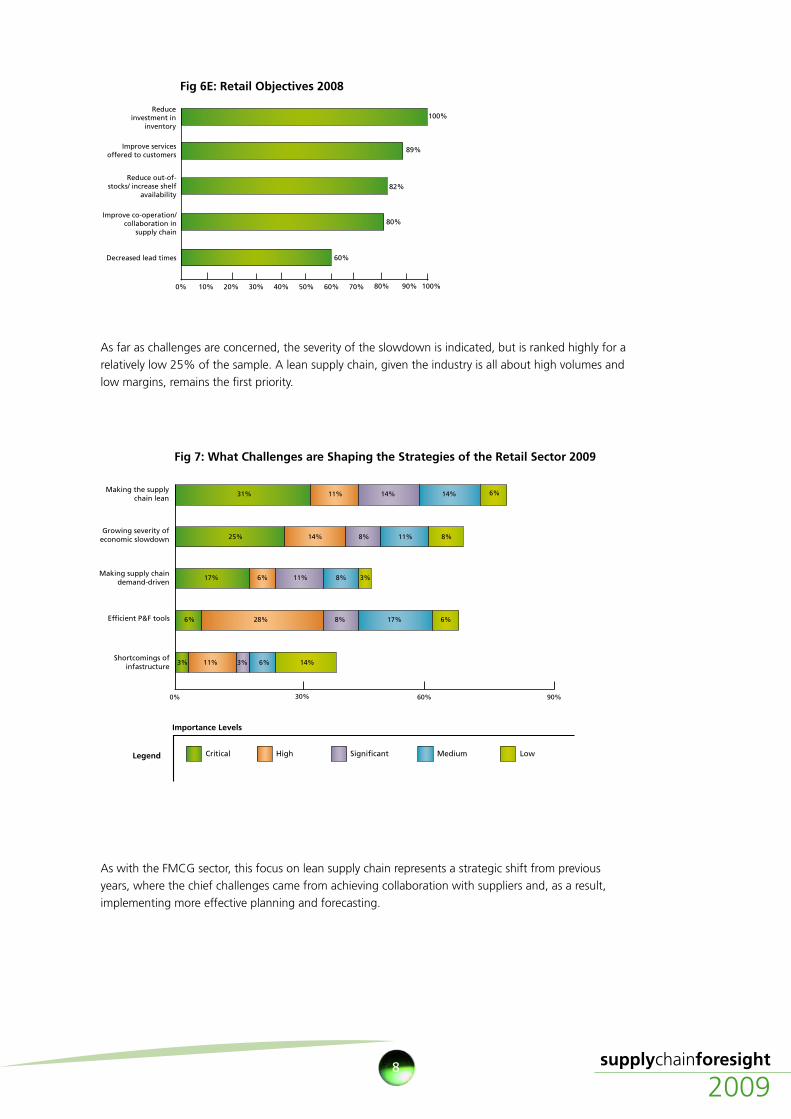

Fig6E:RetailObjectives2008

As far as challenges are concerned, the severity of the slowdown is indicated, but is ranked highly for a relatively low 25% of the sample. A lean supply chain, given the industry is all about high volumes and low margins, remains the first priority.

Growing severity of economic slowdown

Making the supply chain lean

Making supply chain demand-driven

Efficient P&F tools

Shortcomings of infastructure

0% 30% 60% 90%

Fig7:WhatChallengesareShapingtheStrategiesoftheRetailSector2009

High Significant Medium LowCritical

ImportanceLevels

Legend

6%

As with the FMCG sector, this focus on lean supply chain represents a strategic shift from previous years, where the chief challenges came from achieving collaboration with suppliers and, as a result, implementing more effective planning and forecasting.

9

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

42%

43%

43%

50%

68%Improve planning

and forecasting capabilities

Create supply chain collaboration

opportunities

Benchmark our supply chain performance and improve our

use of existing IT systems

Improve the core capabilities of our supply chain staff

Change our physical logistics/distribution

network

0% 10% 40% 60%20% 50% 70%30%

Fig8A:RetailChallenges2004

33%

52%

36%

36%

68%

Creating supply chain collaboration

opportunities

Our planning and forecasting abilities

The logistics channel

Benchmarking our supply chain

preformance

Our sourcing and procurement practices

0% 30%10% 20% 40% 50% 70%60% 80%

Fig8B:RetailChallenges2005

88%

88%

100%

62%

59%

Integration of IT system

Capabilities of IT systems

Achieving a common supply chain vision

Warehouse management

capabilities

Creating supply chain collaboration

opportunities

0% 30%10% 20% 40% 50% 60% 80%70% 90% 100%

Fig8E:RetailChallenges2008

12%

13%

14%

7%

11%

8%

Our planning and forecasting

capabilities

Achieving a common supply chain vision

The increased volume in our supply chain

Capabilities of our existing IT systems

Creating supply chain collaboration

opportunities

0% 6%2% 4% 8% 10% 12%

Fig8D:RetailChallenges2007

35%

25%

21%

43%

46%

Creating supply chain collaboration

opportunities

Planning and forecasting

abilities

Integration of our IT systems

Benchmarking and auditing our supply chain performance

Capabilities of our existing IT systems

0% 30%10% 20% 40% 50% 60%

Fig8C:RetailChallenges2006

50% 7% 36% 7%

11% 28% 39% 22%

11% 11% 22% 11% 44%

6% 17% 17% 39% 22%

33% 28% 17% 22%

22% 17% 22% 28% 11%

supplychainforesight

200910

Fig8D:RetailChallenges2007

Overall, the objectives and challenges of SA’s FMCG and Retail sectors are less focused than most of the sample on the economic slowdown, although this remains an urgent issue. This may be because the consumer impact and falling demand had not yet properly filtered through to the market at the time of the study being done. More pertinently, the objectives and challenges of both sides of the supply chain seem much more aligned with each other than in previous years, which seems to indicate a more effective collaborative approach to planning and inventory management in particular.

OutsourcingRevisited One noteworthy aspect of last year’s overall national research was the growing realisation in large SA companies that the lack of available skills to provide resources to service the growth and diversity in supply chains was harming productivity and profitability. Once more, the most successful companies in the 2008 study were those who were early adopters of ‘smart outsourcing’, that is, working with supply chain partners who could provide more sophisticated skills and resource for the management of complex global supply chain operations.

FMCGviewsonoutsourcing

In the FMCG sector, the pattern follows that of the general research sample – however, with a significantly higher proportion giving as their reason for outsourcing most of their supply chains that they wish to focus on core competencies (83% versus 57% in the general sample), and also a higher proportion giving cost reduction as a reason (63% versus 39% in the general sample).

Fig9A:FMCGOutsourcingRevisited

19% Do not outsource

37% Outsource most of SCM

44% Minimal outsourcing

0% 20% 40% 60% 80% 100%

Keeping up with competition

Strong internal SCM skills

Source of competitive advantage

Low cost-efficiency

Lack of suitable supplier

Sceptical outlook on information sharing

High Significant Medium LowCritical

ImportanceLevels

Legend

17%

31%

31%

25%

8%

13%

25%

13%

13%

31%

50%

25%

19%

25%

31%

6%

25%

2%

63%

56%

31% 31%

31%

25%

17% 8%

25%

38%

11

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

Also in common with the overall sample, areas which are kept in-house and not outsourced relate to customer demands and inventory management, the two key areas in which the sector relates directly to their retail customers. Warehousing is notable for the extent of its outsourcing, understandable in the context of the way in which retail demand controls the flow of inventory.

19% Do not outsource

37% Outsource most of SCM

44% Minimal outsourcing

Fig9B:FMCGOutsourcingRevisited

80% 100%

Gaining competitive advantage

Reducing logistics costs

Focusing on core competencies

Not a source of competitive advantage

Lack of inhouse skills

Keeping up with competition

0% 20% 40% 60%

High Significant Medium LowCritical

ImportanceLevels

Legend

supplychainforesight

200912

7%

73%

13%

7%

Lack of qualified personnel/resources

Availability of strong capability among current partners

Lack of visibility across supply chain

Dependence on downstream participants(distributors/customers)

Dependance on upstream participants(suppliers)

Other

ImportanceLevels

Legend

Supplierselection

Inventory management

DistributionTransportation & shipping

Warehouse management

Manufacturing & production

Customer demands

100%

80%

60%

40%

20%

0%Sourcing

demographics

50%

17% 14%21%

4%8%

29%

25%

33%43%

43%

57%56% 14%

25%

17%

29%17%

14%17%

7%4%

29%

17%

9%

9%

12%

14%

12%

14%

12%

29%

Fig10:FMCGMainReasonsforOutsourcing

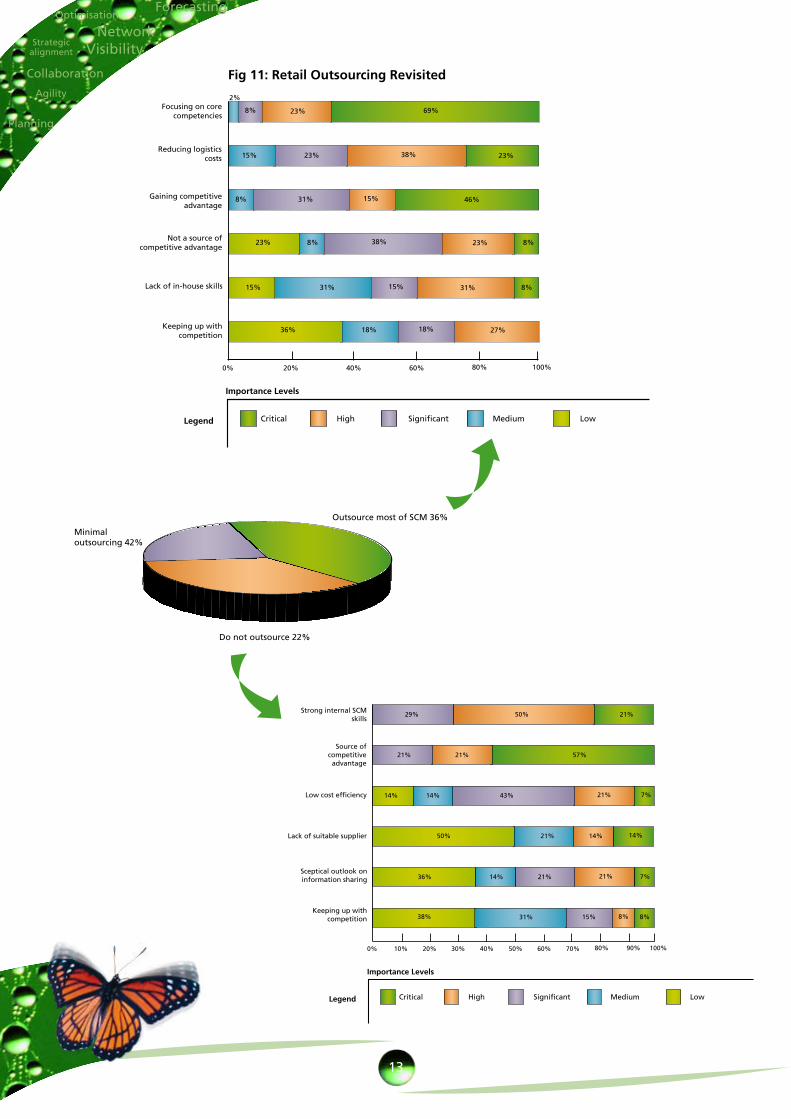

Retailoutsourcingrevisited

For the retail sector the picture is also the same as the general report, but the differences in emphasis are instructive. For those who outsource most of their supply chain functions, the overwhelming reason is to focus on core competencies. Also notable is the much lesser degree to which cost reduction is given as a key reason for outsourcing (23% versus 39% in the general sample), and how much more of the retail response see outsourcing offering competitive advantage (48% versus 35% in the general sample).

29%

21%

14%

50%

36%

38%

21%

14%

21% 7%

50%

21%

14%

21%

14%

7%

21%

57%

43%

14%

21%

8% 8%31% 15%

2%

15%

8%

23%

15%

36%

69%

38%

15%

38%

15%

18%

23%

46%

23%

31%

27%

8%

8%

23%8%

23%

31%

8%

31%

18%

1013

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

Minimal outsourcing 42%

Do not outsource 22%

Outsource most of SCM 36%

Gaining competitive advantage

Reducing logistics costs

Focusing on core competencies

Not a source of competitive advantage

Lack of in-house skills

Keeping up with competition

0% 20% 40% 60% 80% 100%

High Significant Medium LowCritical

ImportanceLevels

Legend

Fig11:RetailOutsourcingRevisited

Low cost efficiency

Source of competitive advantage

Strong internal SCM skills

Lack of suitable supplier

Sceptical outlook on information sharing

Keeping up with competition

0% 30%10% 20% 40% 50% 60% 80%70% 90% 100%

High Significant Medium LowCritical

ImportanceLevels

Legend

9%

5%26%

44%

27%

23%

14%

30%

19%

26%

23%

16%

3%

48%

30% 5%

9% 14%

47%

16%

21%

40%

28%

6%

23%

12%

14% 21%

19%

28%

12%

23%

39%

28%

2%

16%

2%

30%

supplychainforesight

200914

What this may indicate, again, is the extent to which collaboration with manufacturers and distributors has improved – and the extent to which, in the retail trade, the control of inventory itself is a core competency.

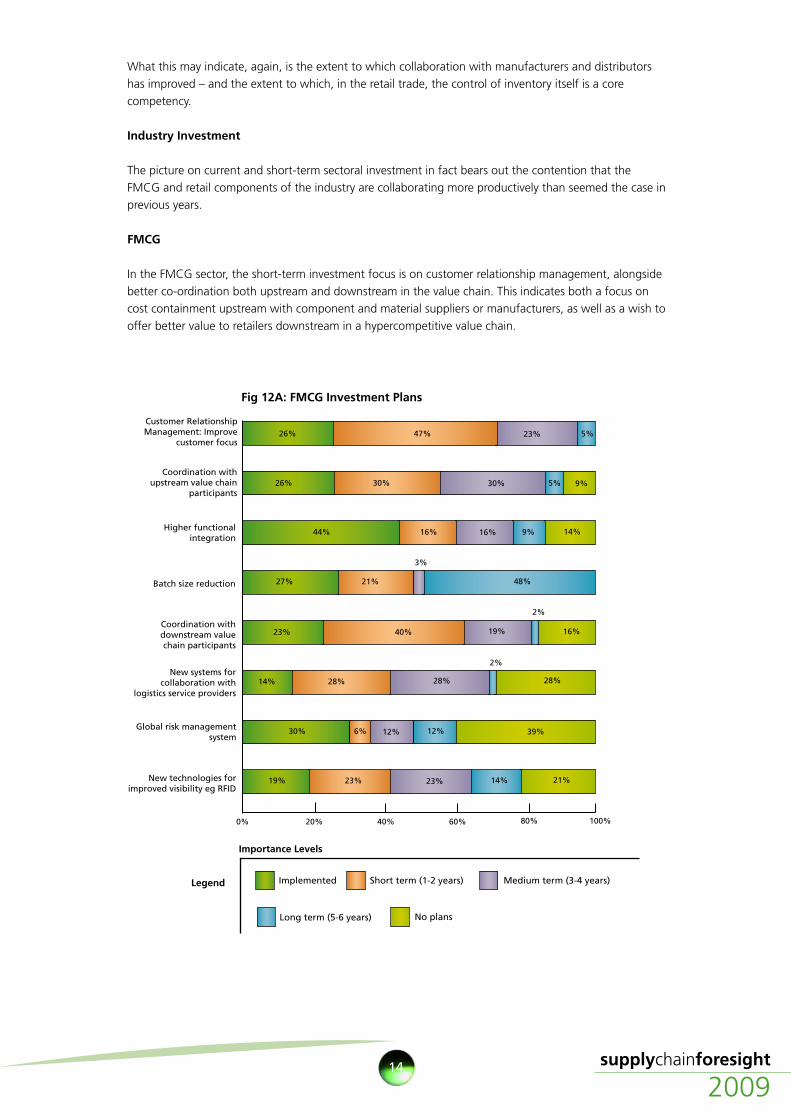

IndustryInvestment

The picture on current and short-term sectoral investment in fact bears out the contention that the FMCG and retail components of the industry are collaborating more productively than seemed the case in previous years.

FMCG

In the FMCG sector, the short-term investment focus is on customer relationship management, alongside better co-ordination both upstream and downstream in the value chain. This indicates both a focus on cost containment upstream with component and material suppliers or manufacturers, as well as a wish to offer better value to retailers downstream in a hypercompetitive value chain.

100%

Fig12A:FMCGInvestmentPlans

Coordination with downstream value chain participants

Batch size reduction

Coordination with upstream value chain

participants

Higher functional integration

Customer Relationship Management: Improve

customer focus

New systems for collaboration with

logistics service providers

Global risk management system

New technologies for improved visibility eg RFID

0% 20% 40% 60% 80%

Short term (1-2 years) Medium term (3-4 years)Implemented

Long term (5-6 years) No plans

ImportanceLevels

Legend

22%

17%

36%

16%

17%

17%

16%

19%

8%

22%

22%

13%

28%

22%

11%

14%

53%

8%

11%

17% 11%

63%

17%

19%

8%

14%

8%

6%56%

47%

19%

19%

31%

31%

16%

42%

6%

15

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

Retail

For the retail sector the picture is focused on upstream value chain participants, the FMCG sector, as well as on the consumers, with plans to invest in customer relationship in the short term leaping to 78% of the sample. With the crucial focus on inventory management in the sector, much focus is also placed on investment in improved supply chain visibility, with 61% of the sample planning investment in new technologies in this area.

Speakingthesamelanguage:PublicandPrivateSectorCo-operation

FMCG

In the FMCG sector there was a surprisingly high degree of lack of awareness of Transnet’s investments in SA logistics infrastructure, with 27% of the sample saying they were unaware. This may indicate the extent to which the sector deals with transportation and import/export issues directly, and the extent to which their value chain is regionally or domestically located. In common with the general sample, however, there is agreement among those who are aware that investment and private sector involvement in logistics planning and execution will improve matters.

100%

Fig12B:RetailInvestmentPlans

Coordination with downstream value chain participants

Batch size reduction

Coordination with upstream value chain

participants

Higher functional integration

Customer Relationship Management: Improve

customer focus

New systems for collaboration with

logistics service providers

Global risk management system

New technologies for improved visibility eg RFID

0% 20% 40% 60% 80%

Medium term (3-4 years)Short term (1-2 years)Implemented

ImportanceLevels

Legend

Long term (5-6 years) No plans

17%

8%

17%

21%

13%

8%

21%

71%

33% 8%46%

8%

13%

13%

71%

71%

50% 13%

supplychainforesight

200916

Retail

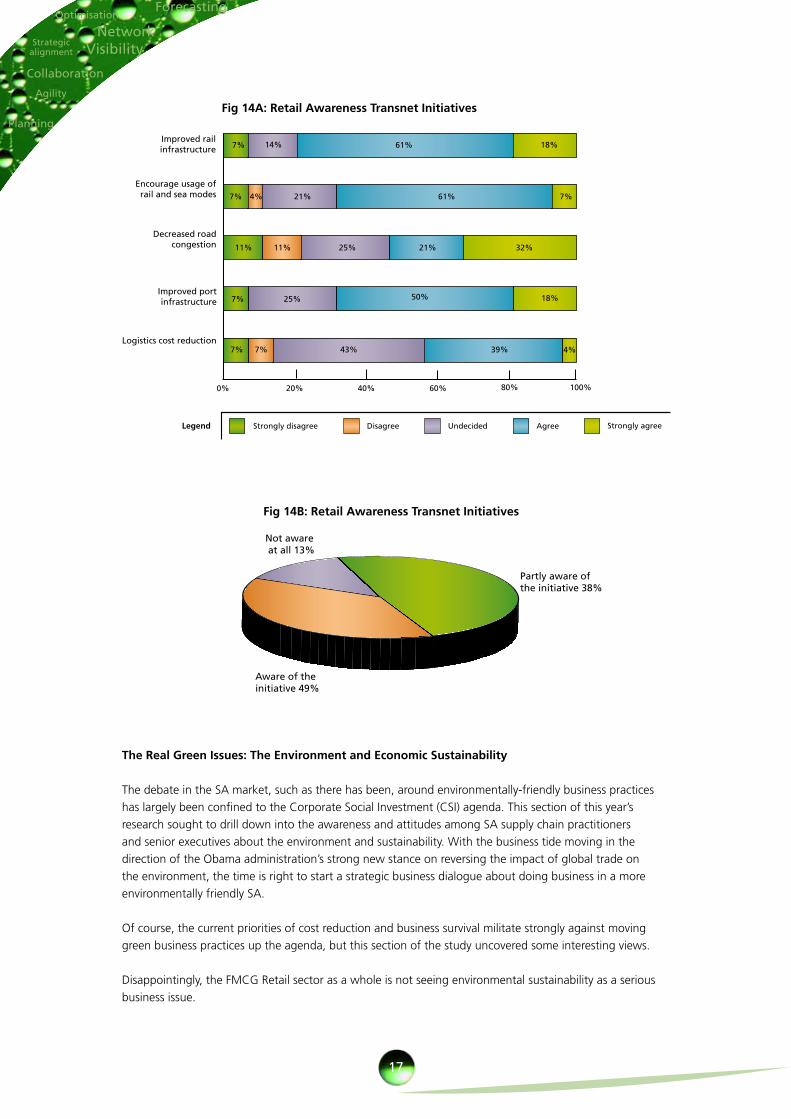

For the retail sector, the lack of awareness of the Transnet investment plans is less, and more in line with the general sample. Interestingly, there is less confidence here that the investments will have an impact on improved rail and port traffic, again perhaps because there is a more domestic focus for the industry. Where there is a difference is in the much greater conviction, with 32% of the sample strongly agreeing (compared to 14% for the general sample) that the investment will decrease road congestion. This is a particularly troublesome area for the management of inventory for retailers, since it affects deliveries both on the roads and as congestion at delivery bays and distribution centres.

100%

Encourage usage of rail and sea modes

Improved rail infastructure

Decreased road congestion

Improved port infastructure

Logistics cost reduction

0% 20% 40% 60% 80%

Fig13A:FMCGAwarenessTransnetInitiatives

Disagree Undecided Agree Strongly agreeStrongly disagreeLegend

Aware of the initiative 30%

Partly aware of the initiative 43%

Not aware at all 27%

Fig13B:FMCGAwarenessTransnetInitiatives

7%

7%

11%

7%

7%

21%

25%

43%

14%

4%

11%

7%

25%

61%

21%

39% 4%

50%

61% 18%

7%

32%

18%

17

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

Encourage usage of rail and sea modes

Improved rail infrastructure

Decreased road congestion

Improved port infrastructure

Logistics cost reduction

0% 20% 40% 60% 80% 100%

Fig14A:RetailAwarenessTransnetInitiatives

Disagree Undecided Agree Strongly agreeStrongly disagreeLegend

Fig14B:RetailAwarenessTransnetInitiatives

Aware of the initiative 49%

Partly aware of the initiative 38%

Not aware at all 13%

TheRealGreenIssues:TheEnvironmentandEconomicSustainability

The debate in the SA market, such as there has been, around environmentally-friendly business practices has largely been confined to the Corporate Social Investment (CSI) agenda. This section of this year’s research sought to drill down into the awareness and attitudes among SA supply chain practitioners and senior executives about the environment and sustainability. With the business tide moving in the direction of the Obama administration’s strong new stance on reversing the impact of global trade on the environment, the time is right to start a strategic business dialogue about doing business in a more environmentally friendly SA.

Of course, the current priorities of cost reduction and business survival militate strongly against moving green business practices up the agenda, but this section of the study uncovered some interesting views.

Disappointingly, the FMCG Retail sector as a whole is not seeing environmental sustainability as a serious business issue.

supplychainforesight

200918

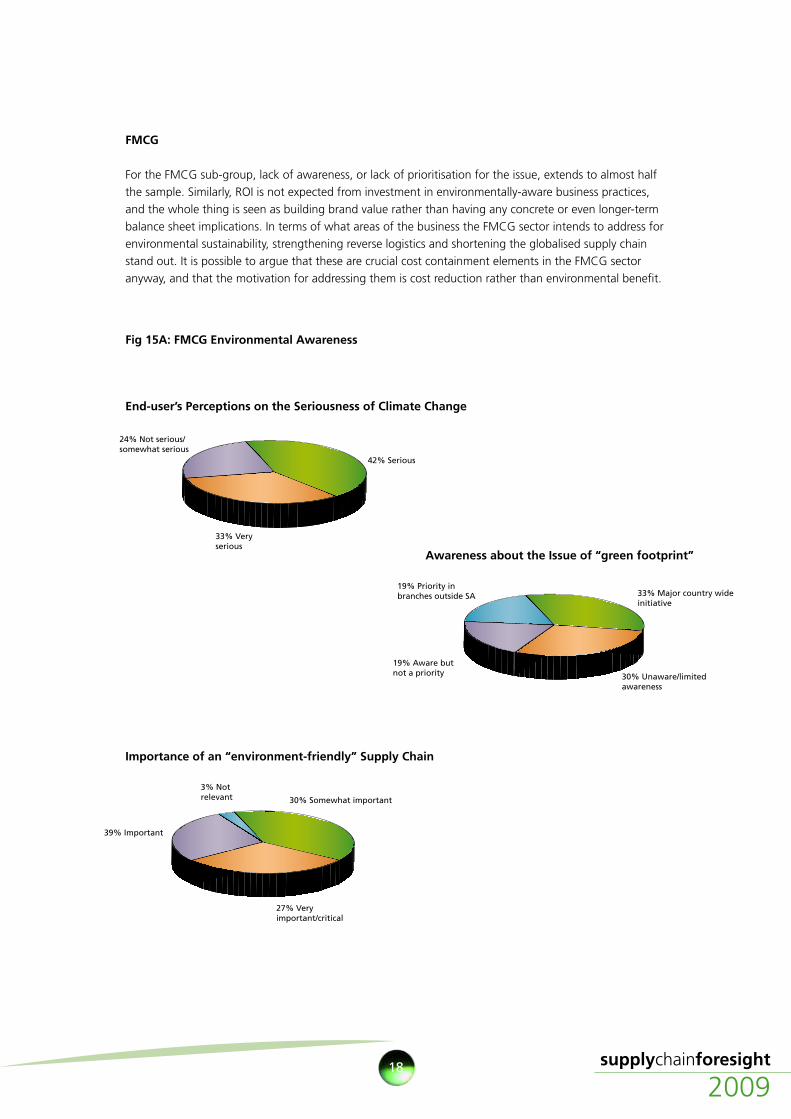

FMCG

For the FMCG sub-group, lack of awareness, or lack of prioritisation for the issue, extends to almost half the sample. Similarly, ROI is not expected from investment in environmentally-aware business practices, and the whole thing is seen as building brand value rather than having any concrete or even longer-term balance sheet implications. In terms of what areas of the business the FMCG sector intends to address for environmental sustainability, strengthening reverse logistics and shortening the globalised supply chain stand out. It is possible to argue that these are crucial cost containment elements in the FMCG sector anyway, and that the motivation for addressing them is cost reduction rather than environmental benefit.

Fig15A:FMCGEnvironmentalAwareness

33% Very serious

42% Serious

24% Not serious/somewhat serious

19% Aware but not a priority

33% Major country wide initiative

30% Unaware/limited awareness

19% Priority in branches outside SA

30% Somewhat important

3% Not relevant

27% Very important/critical

39% Important

AwarenessabouttheIssueof“greenfootprint”

Importanceofan“environment-friendly”SupplyChain

End-user’sPerceptionsontheSeriousnessofClimateChange

26%

25%

50%

14%

18%

33%

9%

29%

5%

42%

14%

15%

33%

3%

22%

50%

56%

17%

29%

55%

27%

27%

14%

20%

21%

7%

9%

19%

45% 30%

29% 10%

55%

5% 5% 26%

41%

15%

9%

33%

43%

9%

19%

9%

6%

3%

11%7%

19

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

Retail

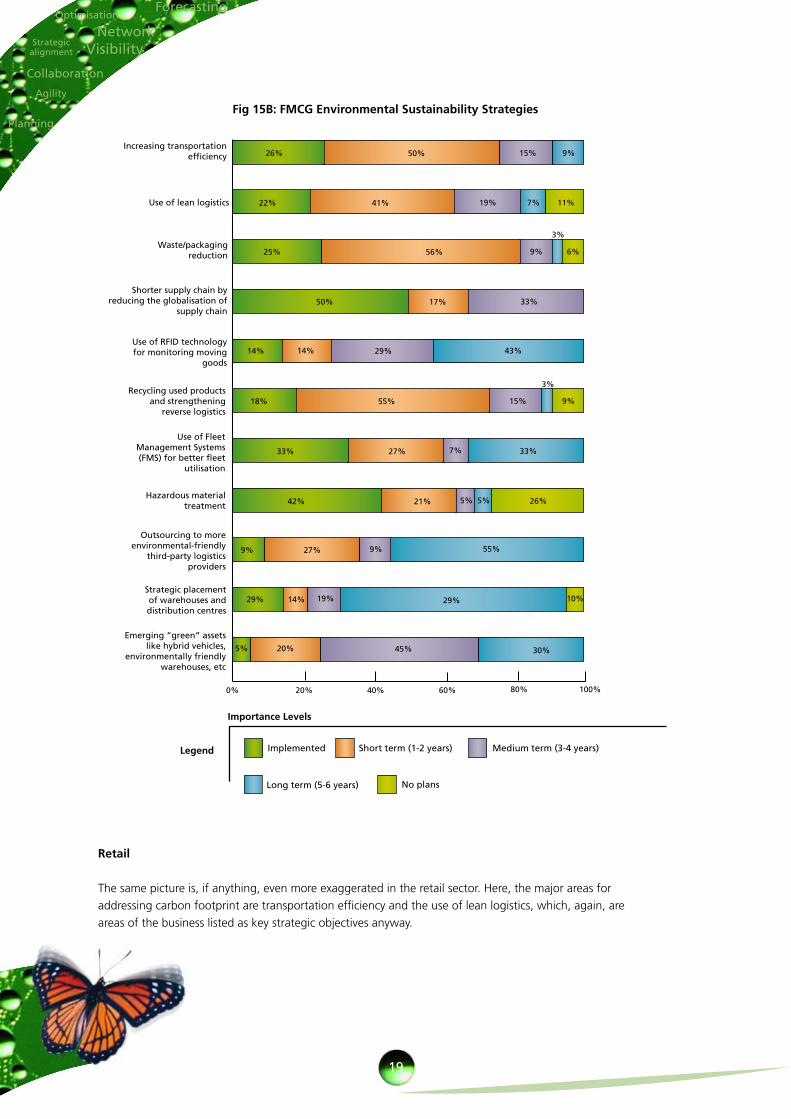

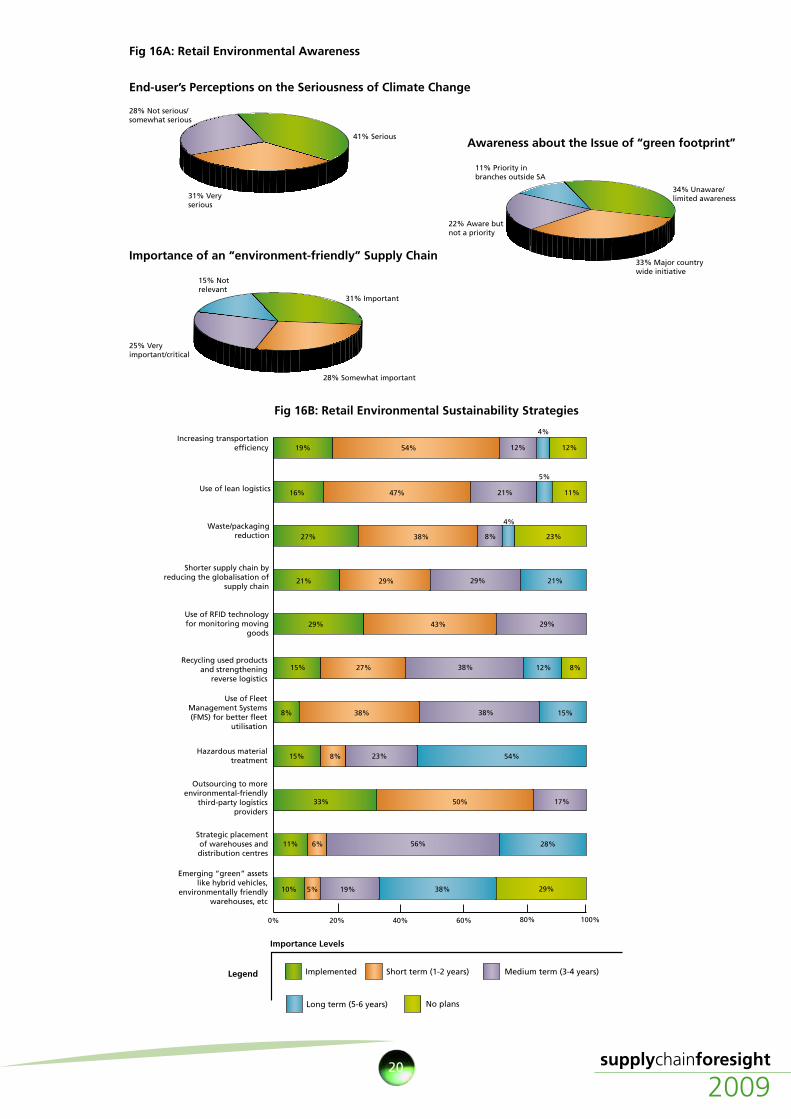

The same picture is, if anything, even more exaggerated in the retail sector. Here, the major areas for addressing carbon footprint are transportation efficiency and the use of lean logistics, which, again, are areas of the business listed as key strategic objectives anyway.

Fig15B:FMCGEnvironmentalSustainabilityStrategies

Hazardous material treatment

Use of Fleet Management Systems (FMS) for better fleet

utilisation

Use of RFID technology for monitoring moving

goods

Use of lean logistics

Recycling used products and strengthening

reverse logistics

Waste/packaging reduction

Shorter supply chain by reducing the globalisation of

supply chain

Increasing transportation efficiency

Outsourcing to more environmental-friendly

third-party logistics providers

Strategic placement of warehouses and distribution centres

Emerging “green” assets like hybrid vehicles,

environmentally friendly warehouses, etc

0% 20% 40% 60% 80% 100%

Short term (1-2 years) Medium term (3-4 years)

Long term (5-6 years) No plans

Implemented

ImportanceLevels

Legend

19%

16%

27%

21%

29%

15%

8%

15%

11%

10%

33%

54%

47%

38%

29%

43%

27%

38%

8%

6%

5%

50%

12%

21%

8%

29% 21%

29%

38%

38%

23%

56%

38%19% 29%

17%

12%

15%

54%

28%

8%

12%

11%

23%

4%

5%

4%

supplychainforesight

200920

Fig16B:RetailEnvironmentalSustainabilityStrategies

Hazardous material treatment

Use of Fleet Management Systems (FMS) for better fleet

utilisation

Use of RFID technology for monitoring moving

goods

Use of lean logistics

Recycling used products and strengthening

reverse logistics

Waste/packaging reduction

Shorter supply chain by reducing the globalisation of

supply chain

Increasing transportation efficiency

Outsourcing to more environmental-friendly

third-party logistics providers

Strategic placement of warehouses and distribution centres

Emerging “green” assets like hybrid vehicles,

environmentally friendly warehouses, etc

0% 20% 40% 60% 80% 100%

Short term (1-2 years) Medium term (3-4 years)

Long term (5-6 years) No plans

Implemented

ImportanceLevels

Legend

Fig16A:RetailEnvironmentalAwareness

31% Very serious

41% Serious

28% Not serious/somewhat serious

22% Aware but not a priority

33% Major country wide initiative

34% Unaware/limited awareness

11% Priority in branches outside SA

15% Not relevant

25% Very important/critical

28% Somewhat important

31% Important

AwarenessabouttheIssueof“greenfootprint”

Importanceofan“environment-friendly”SupplyChain

End-user’sPerceptionsontheSeriousnessofClimateChange

21

Collaboration

Network

Planning

Forecasting

VisibilityStrategic alignment

Optimisation

Agility

The FMCG and Retail sector’s current strategic supply chain trajectory looks something like this. Achieving a ‘responsible’ supply chain balance in the upper right quadrant, between profitability and sustainability in a world where most resources are thinly stretched _ is no mean feat, and currently the industry, like many others, is focused on cost containment and on efficiency in a tight economic environment. For the sector that means inventory management and demand-driven production, components of the combined supply chain that require strong and effective collaboration between suppliers and retailers. By and large the sector seems to be achieving this smart collaboration, which puts it in good stead for seeing out the recessionary conditions the market is currently experiencing.

It is far more difficult in an environment like today’s, where survival is the watchword and the potential for failure is the compelling event that drives most businesses on. The world’s explosion in cross border and international trade and consistent growth over the past few years has been shown to be fragile at its heart. And yet, the Butterfly Effect – say, for example, the sub-prime housing crisis in the US bringing down a global financial network intricately linked by information-based supply chains - can be combated and contextualised.

For the FMCG and Retail sectors a positive outcome of the crisis may be a more long-term view of strategic alignment between the business and its supply chains. The more collaborative attitude demonstrated this year will help in further reducing costs, and managing and optimising inventory in an even more volatile global economy.

The industry’s relative lack of emphasis and importance given to environmental issues in its supply chain operations is puzzling for a sector that is centrally concerned with consumers. Brand value apart, one would assume that sustainable environmentally-friendly business practices in the consumer goods sector might be a smart long-term investment.

Conclusion–OutofCrisis,Opportunity

Low High

Low

Hig

h

SupplyChainSophistication

BusinessCompetitiven

ess

Fig17:SupplyChainButterflyEffect

Industries Focusing on Efficiency

& Cost

Effective Planning & Forecasting

Leverage Modal Advantages

Industries Focusing on Efficiency

& Cost

Effective Planning & Forecasting

Leverage Modal Advantages

Research conducted by

Survey conceptualised and initiated by

www.barloworld-logistics.com