CITIZEN ENGAGEMENT AND LOCAL … Capstone Final...CITIZEN ENGAGEMENT AND LOCAL GOVERNMENT REVENUE...

29

CITIZEN ENGAGEMENT AND LOCAL GOVERNMENT REVENUE GENERATION IN UGANDA Advanced Project in International Management and Policy May 2009 Catherine Nagutta Lutaya Nina Sharma West

Transcript of CITIZEN ENGAGEMENT AND LOCAL … Capstone Final...CITIZEN ENGAGEMENT AND LOCAL GOVERNMENT REVENUE...

CITIZEN ENGAGEMENT AND LOCAL GOVERNMENT REVENUE GENERATION

IN UGANDA

Advanced Project in International Management and Policy

May 2009

Catherine Nagutta Lutaya Nina Sharma West

TABLE OF CONTENTS Summary 1 Introduction 1 Grounding the Study 2 Methodology 3 Uganda Country Context 4 What Should Be Happening 5 What Is Happening 8 What Could Be Happening 19 Conclusion 21 Appendix 23 References 27

SUMMARY Local governments are potentially very important for Uganda as they can play a significant role in generating revenue and encouraging civic involvement, as well as creating a visible link between taxes and service delivery. However, local government revenue generation has deteriorated since the abolition of the graduated personal tax (GPT). In order to understand the challenges faced by local governments, a series of interviews were conducted to gather information about the national policies that impact local governments, how those policies work on the ground, and what non-regulated innovations exist to overcome revenue challenges. While national policies regarding revenue generation are extensive, their fulfillment at the local level is weak. In the field, many interviewees shared anecdotes to highlight shortcomings in policy implementation and vast challenges faced by inadequate revenue. There are several small-scale innovations that generate revenue through civic engagement. In some cases, citizens work directly with local governments to raise funds for specific projects. In other cases, citizens work alone or with NGOs in order to raise revenue and provide services to citizens. Central government can play a significant role in improving local government efficiency and reducing local government dependency on fiscal transfers by promoting civic engagement in revenue generation. In order to gain a more complete understanding, empirical research should be conducted that that explores citizen attitudes towards taxation and service delivery, as well as the potential for small-scale innovations to be regulated. INTRODUCTION “Good governance is good money.”1 The recent abolition of the graduated personal tax (GPT), once the most important source of revenue for many local governments, compounded by limited fiscal autonomy, has resulted in a lack of own-source revenue in local governments in Uganda. Some part of the revenue deficiency seems to be attributable to a lack of citizen confidence in local governments—people may not pay local taxes because they do not see local services being delivered. Could greater citizen engagement help increase revenue? Studies on citizen engagement and fiscal decentralization processes in Uganda have typically focused on participatory budgeting and the expenditure side of the budget. For this study, we sought to understand citizen engagement in terms of revenue generation. The study was commissioned and executed in partnership with the World Bank and the Municipal Development Partnership for Eastern and Southern Africa (MDP-ESA), an organization dedicated to capacity building that works in 25 eastern and southern African countries to promote civic engagement and ensure effective self-governance. MDP-ESA encourages stakeholders to participate in central and local government processes as a way of improving accountability and influencing effective service delivery in their communities. Background This report builds directly on the recommendations from a study exploring the effects of participatory budgeting on revenue generation in Uganda, which suggested exploring how citizen participation specifically focused on revenue generation (rather than expenditure) could improve the local government

1 Mobezyi, Olivia Acting Senior Finance Officer, Bugembe Town Council, Jinja District, January 12 2009

1

resource base and guarantee sustainable local service delivery.2 We sought to gain an informal understanding of general citizen attitudes towards tax and fee payment; to understand the perceived link between taxes and service delivery; to explore the impact of key national policies such as the Fiscal Decentralization Strategy and new district creation on revenue mobilization; and to look for productive innovations relevant for local revenue generation. Given time and resource limits, our approach was exploratory; based on our findings, we tentatively assess the importance of citizen participation in local revenue generation. The first section of this paper will discuss our research methodology and provide a limited literature review of case studies on citizen engagement and revenue generation in Africa. The next section will present our findings in expected, actual, and prospective contexts. First, we discuss what should be happening based on the existing legal framework and policies. Second, we assess what is happening based on field interviews seeking to understand the implementation of policies affecting revenue generation and citizen engagement. And third, we consider what could ideally be happening, based on the small-scale innovations already in place that have potential for replication and regulation to potentially enhance revenue generation. The final section will suggest potential areas for further exploration. GROUNDING THE STUDY: PREVIOUS WORK ON REVENUE GENERATION We conducted a selective literature review of work that considered the nature and importance of local government own-source revenues, the extent to which citizens are engaged in revenue generation, and any lessons from other cases that can be applied to Uganda. Overall, our review found that most studies available focused on the relationship between participatory budgeting and expenditure, and not revenue generation. Studies by MDP-ESA and the World Bank (including some conducted by previous NYU Capstones) on citizen participation in revenue generation provide some information on small-scale, localized innovations, practical approaches and informal mechanisms that exist within local governments. Each study highlights the general lack of local revenue sources and a dependency on central government transfers, thus underscoring the need to understand how citizen participation can enhance revenue generation. A few examples are briefly summarized below. Rwanda Study A study in Rwanda on citizen engagement in revenue generation in post conflict settings is one of the few papers that showed positive revenue mobilization results from citizen participation. Rather than wait for government to fix the public service delivery system after the Rwandan genocide, citizens mobilized to fill the gaps and to meet their own needs. Citizens were involved in two projects: an Education fund and a Mutual Health Insurance Scheme. The Education fund collects financial contributions from citizens and civil society organizations to support deserving students that are unable to fund their own education. The health insurance scheme began as an ambulance cooperative, in which every household contributed money for hospital transport costs. Driven by community willingness to contribute, the Ministry of Health introduced a subsidized health insurance scheme in the districts. Local governments are responsible for mobilizing and sensitizing their own communities to the scheme.3

2 Babcock, Brannan, Gupta, and Shah, “The Right to Participate: Participatory Budgeting & Revenue Generation in Uganda” March 2008 3 Kiessel, Tumukunde, Khawar (2008), Government-Citizen Partnership for Public Service Delivery in Post- Conflict Situations: Rwanda case study prepared for UNDESA.

2

In both schemes central government plays an active role in encouraging innovations through recognizing members of the community at innovation days and in published bulletins. Government support for community schemes encourages citizen participation and community mobilization towards improving service delivery in local governments.

Malawi, Tanzania and Zambia Study A study conducted by MDP-ESA in Malawi, Zambia and Tanzania exploring the link between participatory budgeting and local revenue generation4 made the following revenue-specific observations. Malawi citizens were significantly aware of the sources of local revenue compared to citizens in Tanzania. While the study revealed that willingness to pay for services varied by country, overall citizens were more inclined to pay their taxes and fees if they felt assured that their quality of life would increase. Regarding whether to pay government or a private provider to provide a service, responses varied across the countries. Malawi citizens trusted their local governments to provide services while Tanzania citizens preferred private providers implying that the level of mistrust in government is high. Notably, citizens in all three countries were aware that they could not demand services from their local governments if they did not make their payments. Overall, the major obstacle of abject poverty permeated the ability of citizens to pay taxes and fees in all three countries. METHODOLOGY We began the work with the intention of developing an initial understanding of the opportunities and potential for citizen participation in revenue generation. To do this, we preliminarily explored the revenue generation constraints faced by local governments, citizen perceptions of local governments, the importance of citizen participation, and the perceived connection between revenue generation and service delivery. We actively looked for positive innovations in revenue generation that could inform both Uganda local governments and other African nations, with a focus on citizen engagement. We conducted exploratory field research through more than 40 relatively informal discussions and interviews over three-weeks from December 2008 to January 2009. We focused on Bamunanika sub-county and Makulubita sub-county in Luwero district; in Mafubira sub-county and Bugembe town council in Jinja district; and in Kapeeka sub-county in Nakaseke district. We obtained financial records and program documents to supplement the interviews when available. We held informal interviews and convened focus groups with various sub-groups such as market vendors, school administrators and other community members. Additionally, we interviewed key central government agencies focused on decentralization and revenue generation policies, local government association and NGO representatives, local government political leadership and technical officers (Annex 1). Interviews were conducted primarily in English, and in Luganda when necessary. Due to the time constraints, our research was conducted only in sub-counties with close proximity to Kampala. Despite our physical limitations, the findings seem to have relevance for what is happening in other districts in Uganda based on interviewee responses and other similar case studies. Overall, we found that while reasonably clear policies exist, what is happening on the ground does not necessarily reflect those policies. Furthermore, several innovations have resulted in the development of

4 World Bank/ MDP-ESA (2008), Enhancing Local Governments’ Capacity for Increased Revenue Generation through Participatory Budgeting in Eastern and Southern Africa

3

alternative sources of revenue and enhanced mechanisms for mobilization that can be models for replication. UGANDA COUNTRY CONTEXT

Uganda’s local government structure has evolved overtime through the various regimes in power. The first significant change in the way lower level structures functioned began with the introduction of Resistance councils at the village level after the National Resistance Movement came to power in 1986. Resistance councils encouraged citizen participation in decision-making, acted as a platform for popular democracy, and provided the foundation for the decentralization policy.5 Based on the recommendations of a national commission of inquiry into the local government system6, Uganda adopted a decentralization policy in 1993, giving local governments autonomy over a portion of locally generated revenue and expanding their decision-making powers. In 1995, a new constitution laid out the local government governance structure7 and further expanded the decentralization policy to apply to all levels of local government in order to ensure citizen participation in decision-making. 8 The Constitution clearly states that, “decentralization shall be a principle applying to all levels of local government and, in particular, from higher to lower local government units to ensure peoples’ participation and democratic control in decision making.”9 The decentralization policy has the following objectives: (a) transfer real power to local governments to enable them handle local priorities; (b) transfer revenue from the central government to local governments; (c) improve accountability and effectiveness by bringing political and administrative controls over services to the communities were they are delivered; (d) empower local communities and local officials to free them from constraints imposed by central government; (e) provide a clear link between payment of taxes and service provision; and (f) empower councils to plan, finance and provide services to their residents. 10 Additionally, the central government recently adopted a seventh objective focused on local economic development in order to enhance the management of fiscal resources and to improve economic and tax bases in all local areas.11 The Local Government Act (LGA) of 1997 elaborated on the constitutional objectives of the decentralization policy, laying out the political and administrative structure of local governments, local government powers and responsibilities, local revenue sharing arrangements and the local election system.12 Since 2001, the LGA has been amended to strengthen decentralization by increasing citizen participation in local councils. Through policy objectives and LGA enhancements, Uganda has emerged as having one of the most ambitious decentralization policies in Africa. As other studies have highlighted, however, what happens on the ground is not always reflective of the policy in place.13 We sought to explore how the overall legal

5 Resistance Council Statute 1993 laid out the functioning of Resistance Councils 6 Uganda, GOU 1987. Report of the Commission of Inquiry into the Local Government System, quoted in Elliot Green (2008) District Creation and Decentralization in Uganda, Working Paper NO. 24 “Development as State Making.” 7 See Annex 3 8 Constitution of the Republic of Uganda, 1995 Article 176 9 Ibid. 10 Local Government Finance Commission (2005), A Study on the Implications of the proposed Suspension of Graduated Tax (GT) on Local Governments’ Financing and Decentralization process in Uganda (p.2) 11 LGFC (2008), The Experience of Uganda: Local Government’s Role as a Partner in the Decentralization Process to Strengthen Local Development 12 Onyach Olaa (2003), The challenges of implementing decentralization: recent experiences in Uganda 13 LGFC (2000) Local Revenue Enhancement Study

4

and policy context affects participation and revenue generation to determine whether what is happening on the ground is reflective of Uganda’s constitutional principles and guidelines. WHAT SHOULD BE HAPPENING: POLICY AND CIVIC ENGAGEMENT MECHANISMS THAT AFFECT REVENUE GENERATION In order to fully understand the reality of local government revenue generation in Uganda, it is important to know what should be happening according to established policies and legal framework as they relate to citizen engagement and revenue generation. After detailing the de facto, or legal, aspects of revenue generation in Uganda, we will explore the de facto, or actual, implementation of the legal framework, highlighting successes and discrepancies in order to suggest further areas for study. Policies and Legal Framework Revenue-Specific Policy Uganda’s National Constitution provides the basic structure and powers of local governments under the decentralization policy framework. With regard to the local government system, the Constitution provides that decentralization will “ensure that functions, powers and responsibilities are devolved and transferred from the [central] government to local government units in a coordinated manner.”14 To ensure this devolution and transfer of power and responsibilities, the Constitution states that “there shall be established for each local government unit a sound financial base with reliable sources of revenue.”15 Through these statements, the Constitution provides the basis for revenue sources available to local governments, revenue collection and participation of citizens in revenue mobilization. Other laws and policies complement the Constitution to guide implementation of the three aspects. Available Revenue Sources Based on existing laws and policies, there are two main categories of revenue available to local governments – own-source revenues and central government transfers. While it should be noted that direct access to donor funding may also be available to local governments, this happens only in exceptional cases and did not factor into our study. Own-source Revenue Own-source revenue comprises of a variety of fees taxes and user charges and is governed by various laws specific to the businesses or trade. 16 For example, the there are specific Local Government Act Caps that address local government taxes within their respective areas,17 regulating market fees, levying license fees on trade-specific businesses.18 Other laws address permit fees, regulate tourist agents, regulate the manufacture and sale of liquor, and regulate activities related to cattle transportation and sale. Additionally, property falls under own-source revenue and includes rates levied on commercial properties, as well as ground rent, rental fees, building inspection fees and plan approval fees.

14 Constitution of the Republic of Uganda 2005, Article 176 (2) (a) 15 Ibid Article 176 (2) (d) 16 See Annex 2 17 Local Government Act Cap 243, Section 81 and Schedule five 18 See section 8 of the Trading licensing Act, 2007 (adopted from MOLD Local Revenue Hand book 2007)

5

In 2005, amendments to the LGA suspended the Graduated Personal Tax (GPT), a direct tax previously paid by every able-bodied adult man and women who were in paid employment. Although GPT was productive, the tax had complexities in its administration as well as severe efficiency and equity effects.19 The abolition of the GPT effectively left local governments without a main source of their local revenue. In 2008, amendments to the LGA introduced two new taxes – the Hotel Tax and the Local Service Tax – to supplement local governments after the abolition of GPT. The Hotel Tax is levied on hotel customers for room occupancy. Hotels are mandated to remit collections on a monthly basis to the local government where the hotel is situated. The Local Service Tax is levied on all persons in gainful employment.20 In addition to enhancing revenue, the payment of regulatory taxes acts a means of enforcing controls and discipline among local governments. Government Transfer Revenue In the fiscal year 2008-2009, Uganda’s national budget is SHS 3.889 trillion (US $2.36 billion).21 Of this, 30% SHS 1.17 trillion (US $708 million) is used for grants to local governments. There are several different types of central government revenue transfers. Conditional grants earmark resources for specific activities and constitute 11% of transfers to local governments. Unconditional grants are freely programmable by local government and constitute 88% of transfers. Capital grants are earmarked for building purposes alone. Equalization grants constitute 0.5% of transfers and allow for local government make special provisions for the least developed parishes.22 Revenue Administration The National Constitution guides revenue collection and states that, “local governments shall have power to levy, charge, collect and appropriate fees and taxes in accordance with any law enacted by Parliament.”23 Additionally, local governments are allowed to retain a proportion of the revenue collected on behalf of government for carrying out their functions.24 The Local Government Act lays out the percents retained by local governments as follows. In city and municipal councils, revenue is collected by division councils. Division councils retain 50% of all revenue collected in its area of jurisdiction, and remit 50% back to the city or municipal council. In rural areas, revenue is collected by sub-county councils. Sub-county councils retain 65% of all revenue collected under their jurisdiction (or a higher percentage if approved by the district council). The remaining 35% (or other amount) is remitted back to the district25 In order to ensure transparency in fee assessment, collection and payment, the Constitution provides that, “Parliament shall by law make provision for tax appeals in relation to taxes to which this article applies.”26 Additionally, the LGA requires the establishment of tax assessment appeal tribunals at the sub-county level.27

19 Smoke (2001), Fiscal Decentralization in Developing Countries: A Review of Current Concepts and Practice 20 MOLG Local Revenue Enhancement Initiatives, Local Service Tax and Local Hotel Tax, Position Paper for the Local Governments Budget Framework Paper, December 2008 21 LGFC (2008), The Experience of Uganda: Local Government’s Role as a Partner in the Decentralization Process to Strengthen Local Development. 22 Article 193 of the Constitution of the Republic of Uganda, 2005. 23 Article 191 (1) Constitution of the Republic of Uganda, Republic of Uganda, September 30th 2005 24 Article 192 (b) Constitution of the Republic of Uganda, Republic of Uganda, September 30th 2005 25 Section 85, Local Government Act Cap 243 26 Article 191(4) Constitution of the Republic of Uganda, Republic of Uganda, September 30th 2005 2005 27 Local Government Act, Regulation 7, Schedule five

6

While the finance department in a district or urban council is responsible for local revenue administration such as supervising and collecting revenue, enforcement of revenue collection varies.28 Such variations include issuance of demand notices for payment of license fees, interest charges, fines, and seizing of market stalls. As a last resort, non-compliance can result in prosecution in court. Citizen Engagement-Specific Policy Policies affecting citizen engagement in planning, budgeting and development processes are clearly defined. The Constitution guarantees that “every Uganda citizen has the right to participate in the affairs of government, individually or through his or her representatives in accordance with law”29 Local government planning and budget conferences are held at the end of each fiscal year. Prior to these conferences, the Ministry of Finance, Planning and Economic Development (MOFPED) convenes a national budget conference that brings various stakeholders including local government officials, donors, NGOs and private sector representatives together to inform them about the performance of the economy and resource allocations. The stakeholders set goals and review sector performance. After the national conference, a local government conference convenes local stakeholders such as government officials and civil society representatives to discuss sector working group reports and resource allocation and transfers. Additionally, they update district development plans30 which local government budget committees approve at a later stage. (See Annex 4) This process ensures that the opinions of local representatives are used to inform community budget priorities. The process aims to determine how resources should be mobilized in line with local government priorities. The ‘General Guide to the Local Government Budget Process’ details the tools to guide local governments in the budget cycle.31 Additionally, there are policies for ensuring participation and inclusion of marginalized groups. For example, at least thirty-percent of local council representatives must be women and each local council must have a secretary representing persons with disabilities. Policy Weaknesses There are a number of weaknesses and problems with policies governing revenue generation and citizen engagement in Uganda. First, local governments have limited autonomy over revenues, and the revenue sharing structure is complex and constraining. Second, government transfers are formula based but do not account for good measures of need. Third, since the abolition of the GPT, not enough new revenue sources have been assigned to local governments. Fourth, the policy framework does not provide for an incentive structure for taxpayers or collectors as a way to encourage participation and transparency. Fifth, property tax encourages differential treatment because it is paid by commercial properties and not individual properties that benefit from service delivery. Finally, the Hotel Tax benefits urban and tourist areas, and thus cannot deliver the same benefits everywhere.

28 Local Government Act Cap 243, Regulation18(3) and 19 Schedule five 29 Article 38(1) Constitution of the Republic of Uganda, Republic of Uganda, September 30th 2005 2005 30 Uganda Debt Network (2002), The Uganda Budget Process and How it Relates to the PRSP/PEAP 31 Babcock, Brannan, Gupta, and Shah, “The Right to Participate: Participatory Budgeting & Revenue Generation in Uganda” March 2008 (p.3)

7

Overall Observations on Revenue Generation Policy Generally, Uganda’s laws and policies on revenue generation are relatively clear and strong in certain respects. In addition, a number of institutions such as the Ministry of Local Government (MLG), the Local Government Finance Commission (LGFC), the Urban Authorities Association of Uganda (UAAU), and the Uganda Local Government Association (ULGA), are charged with or have assumed the task of coordinating and monitoring the implementation of these policies and as well as conducting studies to improve them. On the other hand, there are some weaknesses in the framework, as noted above. Moving beyond the existing policy framework, we now consider the degree to which these laws and policies have been implemented and how they have influenced revenue enhancement. WHAT IS HAPPENING: OBSERVATIONS ON REVENUE GENERATION AND CIVIC ENGAGEMENT FROM FIELDWORK

This section discusses the current state of revenue generation and civic engagement in Luwero and Jinja districts, highlighting a number of the problems that undermine policy implementation specific to revenue and civic engagement as well as general problems that affect revenue and civic engagement. This discussion is divided into three sections on revenue problems, citizen engagement problems, and positive innovations. Problem Area: Revenue Generation Overall, we found that revenue generation is weak in both Luwero and Jinja districts. In general, revenue collected from taxes and fees is substantially lower than what was collected prior to the abolition of the GPT. This deficiency has reduced local government capacity to generate adequate own-source revenue for local service delivery. Despite the problems in GPT administration, its abolition coupled with the limitations of recently adopted taxes meant to compensate for its loss suggest that local governments will remain primarily dependent on central government transfers for service delivery. In order to address this deficiency, central government instituted a compensation plan to assist local governments after the loss of the GPT. However, GPT compensation still does not suffice. In Bamunanika sub-county, Luwero district, the difference between local revenue during the last year of GPT and recent local revenue plus GPT compensation amounted to a revenue shortfall of SHS 29.5 million. As illustrated in the table below, in Luwero district, there was a steady decline in revenue collected by the district since 2006; one year after the GPT was abolished. Luwero District Revenue Performance 2003-2008 (amounts in Uganda shillings)32

Year Own-source revenue Estimate Actual

2003/2004 Total revenue 657,670,853 588,532,892 Portion from G- tax 333,184,250 209,601,027

2004/2005 Total Revenue 751,491,153 598,249,305 Portion from G-Tax 300,821,548 241,882,761 2006/2007 Total Revenue 184,478,680 127,730,948 2007/2008 Total Revenue 184,478,680 252,962,948

Source: Luwero District Final Accounts. GPT portion amounts reflect change in revenue collection. Total revenue is inclusive of GPT. 32 The amounts are stated in Uganda currency equivalent to SHS 2,000 to $1 USD

8

Further demonstrating this revenue deficiency, in Jinja district council, local revenue in 2007 amounted to approximately SHS 100 million lower than the amount collected during the GPT period. (see Table below). Jinja District Council Revenue 2003-2008 (amounts in Uganda Shillings)

Year Own-source Revenue Estimate Actual

2003/2004 Total revenue 560,213,000 538,183,781 Portion from GT 389,000,000 389,683,829 2004/2005 Total Revenue 880,732,000 821,369,323 Portion from GT 344,657,000 368,427,311 2005/2006 Total Revenue 752,545,000 744,013,614 Portion from GT 16,387,233 2006/2007 Total Revenue inclusive of

GT compensation 790,975,246 826,967,527

GT compensation 467,800,007 2007/2008 Total Revenue 375,039,000 373,864,327

Source: Revenue performance for Jinja District Council. GPT portion amounts reflect change in revenue collection. Total revenue is inclusive of GPT Additionally, in Mafubira sub-county, local revenue during GPT period was higher than revenue post-GPT. Without GPT compensation, Makulubita collects an average of SHS 18.7 million from local revenue sources. This represents a decline in revenue from the GPT period. (See Table below) Revenue Performance for Mafubira Sub-county 2003- 2007 (amounts in Uganda Shillings)

Year Own-source Revenue Estimate Actual

2003/2004 Total revenue 180,652,981 126,429,385 Portion from G- tax 83,834,750 2004/2005 Total Revenue 115,020,000 102,939,375

Portion from G-Tax 81,201,375 2005/2006 Total Revenue with compensation 71,789,300 65,084,300 G-Tax compensation 47,531,300 2006/2007 Total Revenue with compensation 70,830,000 70,117,881 G-Tax Compensation 50,221,181

Source: Jinja District Final Accounts. GPT portion amounts reflect change in revenue collection. Total revenue is inclusive of GPT. As illustrated above, it is evident that local governments still rely heavily on central government transfers to finance service delivery. However, community and local government officials expressed concern that government grants are insufficient and that GPT compensation is inadequate to cover the revenue shortfall, as noted.

9

Undermining Policy Implementation As mentioned, weaknesses in the policy framework such as limited assignment, limited autonomy, complex sharing structure, and coverage problems with property and hotel tax affect revenue collection and civic engagement. The following problems are specific to revenue and add to the undermining of policy implementation. Uneven Knowledge of Laws and Policies and Varying Capacity Through our conversations, we learned that district officials had better access to and understanding of laws and policies than did officials at lower levels. Several officials offered the opinion that parish leaders and councilors are often illiterate and are less likely to interpret the laws and policies accurately, thus indirectly limiting the number of revenue sources that can be exploited locally. Anecdotes from the field suggested that the levels of capacity among local officials seems to vary considerably. Differences in Resources, Economic Bases, and Revenue Administration Despite having the same legal framework and policies governing own-source revenue, the local governments that we observed had variations in the diversification and administration of own-source revenue. We found that revenue sources vary across sub-counties and town councils (see Annex 2). Interviews from the field suggested that Jinja has diverse sources of taxes and fees, while Luwero had relatively few revenue sources. Bugembe town council and Jinja district had more revenue sources including trading licenses, market dues, property tax, parking fees, hotel taxes, land fees from a sugar factory and royalties from a power-generating firm. On the other hand, the main revenue sources in Bamunanika and Makulubita were trading licenses issued to small petrol station dealers, small restaurants and license fees from private schools. Other revenue sources such as fees from butcheries, traditional healers and charcoal lorries are seasonal by nature, making it difficult to implement officially designated rates. We also found that revenue administration varies within sub-counties. For instance, while Makulubita sub-county uses teams to conduct participatory revenue assessments, other sub-counties do not. The participatory mechanisms of local governments, including some positive efforts, will be explored further in the next section of this paper. (See Annex 2) Centralization of Some Revenues that Could be Shared Centralization of some types of revenue without sharing arrangements has stripped local governments of revenue generated within their borders. Several local and central officials were concerned that motor vehicle license fees collected by the Uganda Revenue Authority are not shared with local governments. Additionally, we learned that the Jinja local government does not receive a share of revenue collected from Nile River fishing licenses. On the one hand, there may be valid reasons for keeping some of these revenues centralized in Uganda. On the other hand, some sharing of these revenues may be considered appropriate. It is important that local governments maintain a degree of fiscal autonomy over a share of revenues that can create a connection in the minds of citizens between the revenue generation and service delivery.33

33 Smoke (2007) Local Revenues under Fiscal Decentralization in Developing Countries: Linking Policy Reform, Governance and Capacity (P.11)

10

Non Revenue-Specific Policy Problems As mentioned, there are several policy issues that are not directly related to revenue generation but nevertheless impact efficiency, such as technology and district splitting. Limited use of Technology The local governments that we visited lack adequate technology to effectively administer revenue assessment and collection. Additionally, we learned that sub-counties have on average one computer in their offices and have no system to map potential tax sources, nor track collections from these sources. Most of the tracking was done manually using lists compiled by the collectors and making door-to-door checks to identify those that had not paid, a system that is time consuming, costly and leaves room for human error. All of this contributes to a general lack of knowing the tax base, making assessment and collection of fees and taxes inadequate, and thus negatively impacting revenue generation. District Splitting While district splitting – often referred to as the ‘creation’ of new districts – has created problems with local government financial viability and citizen engagement, some local governments end up better off while others end up worse off. New districts such as Nakaseke (which was subdivided from its mother district Luwero) were performing well in revenue collection and mobilization, despite the fact that this division had a negative revenue impact on the mother district. For example, councilors explained during an interview that after the Nakaseke split, Luwero was left with the burden of financing previous debts that had been incurred in the territory that is now Nakaseke. We also learned that new districts can potentially create positive connections between politicians and citizens. In some instances, districts split due to poor representation and governance in the mother district. When a new district is formed, the new administration strives to improve accountability and participation of the community to mobilize resources. A government official described a number of new districts that are performing better than their mother districts in revenue mobilization because of good leadership and the willingness of citizens to help their district succeed.34 A government official stated that, “Kyenjonjo district that was recently created has never experienced infancy because of good leadership. Therefore, the key to engaging citizens in raising revenue is good leadership. All districts can raise revenue but have to be focused.”35 Several community members and NGO representatives, however, were concerned that aside from a financial hindrance, district splitting can also be a used to consolidate political power. We heard anecdotes in which locally elected representatives from the party in power recruiting their supporters for positions in the expanding government bureaucracy. This is relevant to local governments’ ability to generate revenue because local government employees, elected officials and councilors are able to use their positions and local government resources to mobilize support for their party.36

34 Interview with Assumpta Tibamwenda Ikiriza, Ministry of Local Government 35 Interview with Patrick Mutabwire, Commissioner Ministry of Local Government 36 Larock (2008), Deepening Decentralization or Regime Consolidation: What explains the unprecendented creation of new districts in Uganda?

11

Problem Area: Citizen Engagement Through our fieldwork, we found that citizen engagement is affected by several different factors, including attitudes, civic awareness, political influence, corruption, and feedback mechanisms each of which can affect the ability of local governments to engage their citizens in participatory governance, thus negatively impacting local revenue generation. Attitudes Through our interviews, we heard reports that attitudes towards tax and fee payment vary across age, gender and local governments. Local government officials in each sub-county acknowledged that tax compliance increases with age; elderly people in the villages regarded tax payment as prestigious. One local government official acknowledged that, “during the graduated tax period, elderly male citizens used to pay their taxes on time and were known to go boasting around that whoever didn’t pay taxes wasn’t ‘man enough.’ However, collectors always experienced problems getting money from younger male citizens.”37 We also learned that in some instances, tax compliance has been shown to increase with the level of education. For example, local officials noted that businesses owners more widely understood the importance of taxes and fees, while those who were uneducated or illiterate did not. Attitudes towards payment were also reported to vary with gender. Local government officials in Bamunanika and Mafubira expressed that women were more resistant to tax payment than men, and often sought sympathy from tax collectors to avoid payment. We were told that resistance to payment commonly stems from the belief that government and donors should provide services to the people, but that individuals should not have to pay for those services. Citizens are focused on receiving services but not focused on how services are funded or how they personally can contribute. Officials offered opinions and stories that suggested a primary cause of non-payment is citizen apathy, not high tax rates. For example, in Bamunanika, a group of approximately forty motorbike drivers is required to pay SHS 30,000 per month in parking fees collectively. Sub-county officers informed us that the drivers have complained that the rate is too high; yet, during the assessment phase, the rate was reduced from SHS 50,000 to the current SHS 30,000 rate. Several local government officials felt that citizens made excuses about rates being too high, when their real impetus for non-payment was apathy. Often the negative attitudes of citizens towards tax payment are influenced by other factors such as general civic awareness, political influence, and corruption. Civic Awareness Anecdotal evidence from each sub-county suggests that citizen satisfaction with service delivery—and presumably attitudes towards paying taxes—is dependent on personal benefit. Community members only saw a visible link between tax payment and service delivery when they directly benefitted from the service. For instance, local officials noted that women are more likely than men to appreciate a borehole or health clinic constructed with tax funding, since women are the primary water gatherers and clinic users.

37 Interview with Wamala Victo, Councilor Makulubita sub-county.

12

One area of general concern expressed by local officials is the extent to which citizens understand both the importance of taxation and the need to raise revenue locally. While sensitization for elections happens on a widespread national level, sensitization on taxation is limited. A Makulubita focus group participant indicated that the community in the sub-county is largely illiterate, so posting documents and messages at the sub-county headquarters – a common practice – is not effective.38 One central government official expressed concern that policy documents are sent to districts in large, difficult to read volumes. Without an executive brief or summary, the issues and policies may get lost in translation.39 This highlights the fact that inadequate local government capacity can negatively impact citizen engagement. Political Influence Several of our interviewees expressed concern that political interference in local government activities affected citizen participation in revenue generation. We found that political influence can have both positive and negative effects. For instance, good political leadership can play a role in increasing citizen participation in revenue generation such as the case in Bushenyi district, where elected leaders successfully mobilized citizens to contribute to construction of the district headquarters.40 More often, however, our interviews suggest that political interference can have a negative impact on citizen engagement, specifically due to the multiparty political system. Candidates have apparently encouraged citizens not to pay taxes in an effort to win votes, promising that they will provide free services if only citizens vote for that candidate. Consequently, citizens vote based on political party affiliation, rather than merit. This affects both revenue alone and citizen engagement. For example, in Jinja, we heard that two citizen contributory schemes existed prior to the multiparty system – the education fund and the health users fund – to which citizens made financial contributions in order to receive services from the district. Since multiparty elections, however, political candidates have purported that under their leadership, citizens would not need to contribute to these funds to receive services. Without citizen funding, however, these schemes have ceased to exist. Additionally, we were told that because Chief Administrative Officers (CAOs) are appointed centrally rather than through local elections, citizen engagement is diminished. A focus group member in Makulubita expressed concern that CAOs are accountable to the politicians that appointed them rather than to the people. Conflicting accountability leads to a lack of citizen trust in CAOs, thus negatively affecting their ability to mobilize citizens. In general, the extent to which political influence affects citizen participation seems to depend largely on the degree to which political leaders and officers work together to implement policy and mobilize citizens. Corruption Some of our interviewees noted that corruption at the technical officer level affects citizen trust in government. In some sub-counties, citizens were concerned that roads were poorly constructed because tenders for construction were awarded to contractors with connections to the administration, rather than through an open bidding process. Sub-county chiefs felt that they lacked the power to confront poor-performing contractors because the tender came from the district administration level.

38 January 9 2009 39 Interview with Mr. Patrick Mutabwire, Commissioner MOLG 40 Ibid.

13

We learned, however, that citizen dissatisfaction with service provision varied across sub-counties. A focus-group member stated that “the people prefer government to provide services than to private people doing so. Leaders at the sub-county are left out in making decisions on tender awards which creates a situation were the sub-county chief cannot do much against a contractor that provides poor services.”41 Despite the obvious lack of contractor accountability, citizens did prefer to have government provide a service for them rather than a private provider, due to the inconsistent results of private contractors. For example, in Makulubita, citizens had noticed faulty borehole construction from a private provider, and expressed preference for government to provide services instead. 42 Feedback Mechanisms We found a general absence of citizen complaint or feedback mechanisms at the sub-county level. Feedback mechanisms can encourage citizen engagement because they act as a form of accountability between leaders and citizens. The only exception to this was Luwero Client Charter, which will be discussed in the “Positive Innovations” section below. Positive Innovations with Citizen Engagement in Revenue Issues Despite many problems surrounding revenue generation and citizen engagement, we learned of a number of innovations in each sub-county that seem to have resulted in positive changes in the community. As a general summation, in each district, local government officials informed us that citizens make personal contributions to community projects such as the construction of roads and health centers, through labor, as will be discussed in the next chapter. Because revenue generation cannot be the responsibility of the community alone, we found many central actors that influence citizen engagement and revenue generation. For instance, the Uganda Local Government Association (ULGA) works to promote democracy, good governance and better services to local governments; the Urban Authorities Association of Uganda (UAAU) promotes and protects the interests of member urban authorities on behalf of its members; and the Uganda National NGO Forum acts as a collective voice for civil society by bringing together NGOs to engage on public policies in order to reflect the views and concerns of the poor.43 These actors, coupled with local, up-country actors, have helped inform the community about the importance of generating revenue and the connection between tax payment and services. Encouraging citizen engagement, government transparency, and finding alternative own-source revenue are paramount to the success of increasing local government fiscal autonomy. Several of our field interviews exemplified these ideas, as they involved the community in raising funds, creating accountability, and mobilizing informal groups to ultimately enhance the overall quality of life. These innovations fall into three distinct categories: Process Innovations, Financing Innovations, and Sensitization Innovations. Process Innovations Process innovations that we learned about through our field work directly address barriers or hindrances in local governance by increasing transparency through feedback mechanisms or other citizen engagement mechanisms.

41 Focus group discussion with Haji Kigozi Ali, Makulubita sub-county 42 Makulubita Sub-county focus group, January 9 2009 43 Uganda National NGO Forum website, http://www.ngoforum.or.ug/index.php

14

The Luwero Client Charter In 2007, the Luwero produced its first Client Charter, a document that “specifies the standard for the delivery of services and sets our feedback and complaint handling mechanisms.”44 The district’s mission is to “serve the community through the coordinated delivery of services which focus on national and local priorities for sustainable development.”45 It outlines values and principles, as well as the district’s principal services and commitments to its clients, including central government, politicians, religious leaders, donors, civic and cultural leaders, and the general public.46 What sets the Luwero Client Charter apart from a simple list of promises is that it specifies detailed processes related to client rights, feedback mechanisms, and complaint management. Additionally, the Charter clearly states that government must respond to complaints immediately, and that feedback can be expected within two weeks of the complaint. While the Client Charter does not directly impact revenue generation, it has the potential to empower citizens and local government officials to do so. By creating and widely communicating a solid structure through which citizen clients can work with government officials, hierarchical barriers are effectively broken down, and effective governance can happen. Participatory Assessment & Complaint Systems Makulubita sub-county in Luwero uses a participatory team to conduct tax assessments. A group of assessors including the sub-county chief, parish chief, extension staff, sub-accountant, and village-level officials visit businesses to determine an appropriate fee.47 Having more than one official present at the assessment leaves less room for corruption; additionally, more assessors allow for different forms of communication and negotiation, and fewer opportunities to claim that an assessment was unfair. Coupled with participatory assessment is a system for making formal complaints or seeking fee adjustments. Business owners can appeal at the village level through to the sub-county level. Because there is a hierarchical structure in place, there is little room for illegal renegotiations, and citizens are able to make complaints to people with power to make a change. This policy allows citizens to confront local government officials and break down societal barriers. Mafubira sub-county in Jinja district uses team assessments as well. While their system does not include a complaint hierarchy or an incentive system, they have begun the process of creating transparency in assessment.48 Incentive systems and complain mechanisms encourage citizen engagement, as “prompt redress of complaints may help convince people that the municipality means business.”49 Public Recognition as a Tax Incentive Makulubita recognizes its tax collectors publicly which provides an incentive for efficient and non-corrupt collection. In addition to public recognition, certificates, bonus payments, and other low-cost benefits act as an incentive for tax collectors to fulfill their duties in a timely and comprehensive manner. We learned that some towns have considered instituting public recognition for taxpayers, acting as an incentive for timely payment of assessed fees. 44 Luwero District Client Charter July 2007 45 Luwero District Client Charter July 2007 46 ibid. 47 Interview with S. Sibihwana, January 9 2009 48 Interview with Charles Wansagi, Mafubira Sub-county Vice Chief January 12 2009. 49 Fjeldstad, Odd-Helge, “Local Revenue Mobilization in Urban Settings in Africa, 2006

15

Financing Innovations While process innovations are vital to the future success of local governments, without funding, processes will fall flat. We found several instances in sub-counties where community groups worked together to raise funds or contribute their own funds and skills to enhance services. Each of these financing innovations involved a partnership in some form, whether between government and citizens, or citizens and NGOs. Namulesa Market Co-Funding During our interviews in Mafubira Sub-county, we learned that the local district administration had worked in partnership with vendors at the Namulesa Market to build a new market. Prior to its reconstruction, the Namulesa Market consisted of a series of poorly constructed wooden stalls (Figure 1). When the local government chose to rebuild the market, it did not have enough funds to do so. Ultimately, the market was built through co-funding by the local government and market vendors. This partnership enabled vendors to hold government accountable for its expenditures because vendors had a personal stake in the service delivered, and because their funds were being matched. Despite this process, the vendors noted that a private contractor poorly constructed the market sewage system. To prevent such an oversight in future endeavors, market vendors are interested in organizing a formal market association which will better equip them to lobby local government to support their interests and address their concerns, as well as to make personal contributions and to maintain and manage the future of the market.50 Standard High School Kapeeka Resource Generation Kapeeka sub-county is in Nakaseke district, a newly formed district carved out of Luwero in 2008. Standard High School is housed in a repurposed German factory in the center of the sub-county. Over several years, the headmaster of Standard High School mobilized the local community to contribute their own materials, labor, and funds to enhance the school. Through this community involvement, the school has constructed a chicken coop, a piggery, and a cabbage garden, all of which provide school lunches for students. Extra pigs, chickens, eggs, and cabbage are sold at the local market, providing additional funds that help to sustain the school and its lunch program.51 In turn, enrollment at the school is up because parents no longer have to shoulder the cost of feeding their children. Additionally, the school has developed a partnership with an American faith-based NGO that funds the school and enhances the community through vocational training and health services.52 The major asset of Kapeeka is its people and their willingness to provide their own labor, skills, materials and funds to support the school. Through alternative funding sources, Standard High School purchased several acres of land – including a fresh water source – on which to build a new boarding school. By seeking alternative revenue sources to provide educational services, Kapeeka stands out as a success that could be replicated across other sub-counties.

50 Namulesa Market Focus Group January 13, 2009 51 Interview with Silvano, Standard High School Kapeeka, January 9 2009. 52 www.covealliance.org/aboutus.htm

16

Bushenyi Community Group A central government official informed us that community members in Bushenyi had banded together to provide services and increase their collective voice.53 First, a group worked together to collect food waste and form a composting association as an alternative to burning garbage. Another group started as an informal burial group. Seeing their efforts of working together pay off, the group formalized itself into a market association that could represent vendors and regulate stalls, prices, and market amenities. Yet another group formed when a district headquarters needed rebuilding. Community members contributed labor and materials to construct the building when central government transfers would not suffice. While creating a market association or a composting group and working together to build an office may be simple projects, they are forms of partnership that can provide services where funds are insufficient, or provide a platform for community needs to be collectively heard. Sensitization and Education Innovations In addition to process and financing innovations, citizen engagement regarding revenue generation would not be possible without extensive sensitization and education innovations. As mentioned, there is a national emphasis on sensitization regarding elections, but not on sensitization for taxation. We encountered several innovative organizations and sub-counties that have used alternative sensitization schemes to impart the importance of taxation. Additionally, several of the innovations described below address not only sensitization but are experiments in process innovations as well. Bamunanika and CODI Bamunanika sub-county in Luwero district worked with the Community Development and Welfare Initiative (CODI), an NGO that advocates for good governance through sensitization and priority setting. In partnership with Oxfam, CODI conducted a survey in Bamunanika Sub-county in an effort to improve governance, service delivery, and accountability, and to empower citizens at the village level.54 Through these meetings, CODI helped villages identify their most pressing needs and presented them to parish development committees who in turn used them to “prioritize issues for integration into the sub-county development plan and budgeting for the financial year 2009/2010.”55 CODI also engaged citizens through an alternative sensitization program, understanding that a major barrier to efficient governance was the disconnect between citizens and elected officials. In order to break down this barrier, CODI filmed interviews with elected officials and replayed the interviews for citizens to help them understand that officials are ordinary people who are approachable and sympathetic. In another instance, CODI enlisted a celebrity to gather citizens at a public location where they had arranged for a local government official to be as well. CODI insisted that the official mingle with the people, thus making him a more approachable public figure. Additionally, CODI sought to reach citizens in a more effective manner and used puppetry56 to explain the taxation and assessment process. As an NGO, CODI does not have to answer to nor receive funding from the government, so while sub-county chiefs may not be able to confront government officials, CODI has nothing to lose by doing so. 53 Interview with Patrick Mutabwire, Ministry of Local Government, January 6 2009 54 Community Development Initiative (2008), A Social Audit Report on Citizen Empowerment for Good Governance in Bamunanika Sub-county, Luwero District. 55 CODI Report on Village Participatory Planning Exercise 56 CODI presentation – use of puppetry

17

While there are policies that exist around sensitization and information sharing, CODI and Bamunanika recognized that alternative, creative means were necessary to break down barriers, conduct localized sensitization, instigate change and ultimately encourage citizen engagement. Priority Setting We learned that in Bugembe, the most populated area in Jinja sub-county, not every local interest group has yet registered with the town council because it is still a newly created area. Noticing a lack of citizen engagement, Bugembe worked with the UN Habitat program to identify 20 community stakeholders to represent community opinions. Stakeholders were interviewed to determine the major priorities in the community, and these interviews informed the Council’s development plan and acted as benchmarks to help assess the Council’s performance in the future. While priority setting is an effective way to gauge community needs, it does not necessarily mean that priorities will be met. Yet, several sub-counties still found this practice to be worthwhile because “the cooperation between local government officials, councilors, and community leaders in setting common goals”57 is crucial to encouraging accountability and increasing trust. And, through increased trust, citizens may be more willing to pay taxes. Improving and Using Lower Level Development Plans Makulubita sub-county in Luwero district has nine parishes, each with a parish development committee that is consulted for guidance on how and where to spend its funds. According to the sub-county chief, the parish development committee guides all projects and involves citizens before implementation.58 Parish development committees also conduct a SWOT analysis to create a development plan for their parish that includes alternative sources of revenue. By compiling all development plans into forecasting, Makulubita has developed a 3-year development plan, which sets benchmarks for progress and encourages citizen engagement in seeing the plan fulfilled. While development plans do not directly tie into increased revenue, they do directly engage citizens in the goals and priorities of the sub-county as a whole. As engagement and awareness increase, there is potential for citizens to feel more connected to their sub-county and more willing to pay taxes because they see how they will be used. Overall Observation The innovations briefly outlined above are simple, low-cost, and effective means to engage citizens in the taxation process as well as the expenditure planning process. In many cases, innovations simply involve attempts at more effective implementation of existing frameworks, such as the Parish Development Committee. By inviting citizens to participate and understand that their priorities can and should guide elected officials, citizens will become more aware of the process and less apathetic to it. Too often, a lack of sensitization keeps citizens from understanding their right to participate in their own governance. By reaching citizens in alternative ways, breaking down barriers, and encouraging citizen involvement in prioritizing and planning, revenue generation has the potential to increase. In each interview and focus group, we were informed that poverty is typically the most significant impediment to citizen participation in revenue generation and mobilization. Abject poverty permeates

57 Ibid. 58 Interview with Sibihwana, Sylvia Makulubita Sub-county Chief, January 9, 2009

18

every attempt by local governments to raise revenue. Put simply, the need to put food on the table outweighs the importance of paying taxes. WHAT COULD BE HAPPENING: OPPORTUNITIES AND AREAS FOR FURTHER RESEARCH As demonstrated, despite the problems of policy implementation and a general lack of local government funding, small-scale revenue generation and citizen engagement innovations are happening. While each innovation exists on a local level, they all have the potential to be replicated and scaled up, and in some instances, could be regulated within a new policy. The following section will outline the opportunities for central and local government actors, as well as areas for further research to enhance revenue generation and citizen engagement. Opportunities As we highlighted through the innovations witnessed on the ground, there are many opportunities for central and local government to take steps designed to help increase citizen engagement and potentially enhance local revenue generation through changes in process, financing, and sensitization. Regarding process, central government actors may wish to use the Luwero Client Charter as an example of good fulfillment of the decentralization policy, as it improves accountability and empowers communities. Additionally, while the practices of CODI are unconventional, Central government may want to reevaluate the relationship between political leaders and technical officers. Because technical officers have the responsibility to fulfill policies on the ground, yet political leaders have the power to influence their ability to carry out technical duties. As a key player in enhancing local revenue and based on the financing innovations witnessed, central government may wish to explore alternative ways to increase local government autonomy and decrease their dependency on central government transfers, thus creating a “connection in the minds of local voters between the revenue generation and service delivery actions of local elected officials.”59 Aside from property and vehicle registration taxes mentioned by central government actors, the redistribution of other centrally collected taxes to local governments may help to create more autonomy and strengthen accountability. Other opportunities for central government to enhance revenue and citizen engagement are reviewing the remittance process for the VAT or the distribution process for the Hotel Tax, potentially resulting in increased revenues for rural areas. Finally, regarding sensitization, central government can play a significant role in publicizing local government innovations to encourage replication in other Sub-counties. As demonstrated through the Rwanda case study, central government learned from local government innovations and helped to create policies that benefitted local governments, helping them become more independent. Local Government By adopting some of the process, financing and educational innovations mentioned above, local governments can slowly build citizen engagement, which should in turn lead to enhanced revenue

59 Smoke, Paul Local Revenues under Fiscal Decentralization in Developing Countries: Linking Policy Reform, Governance and Capacity, August 2008

19

generation. In cases such as the Luwero Client Charter, Namulesa Market co-funding and Kapeeka resource mobilization, local governments have used their power to act on their own without additional resources from central government. By being innovative and proactive in encouraging citizen engagement to improve revenue, local governments can accomplish much on their own. Additionally, local governments can look to organizations like the ULGA, NGO Forum, and UAAU to learn about innovations in other areas that are replicable. Regarding process innovations, local governments need to innovate to enhance revenue and participation. For example, local governments may want to look to Luwero for suggestions on creating and implementing a Client Charter to engage citizens in their own governance. Additionally, local governments may look to Makulubita as a guide in using parish development committees to inform the sub-county development plan. Without mechanisms to promote accountability, and without the willingness or ability for citizens to engage in the process, “local revenue generation is likely to remain limited.”60 Regarding financing innovations, there is opportunity for local governments to improve tax administration – from assessment to collection. Because poor tax revenue can be based on myriad factors (negative attitudes towards payment, incorrect assessments, size of tax base, corruption, transportation, etc.) local governments may want to determine which point in the administration process hinders the process most. By focusing on the weak links in tax administration, local governments will be able to better understand the opportunities and constraints to raising revenue from their existing tax base. Regarding sensitization, as witnessed in both Uganda and Tanzania, citizens lack the understanding that taxes are vital to the ability of a local government to provide services.61 There are many opportunities for increased revenue generation through enhancing the sensitization process and through engaging stakeholders who can influence citizens to participate. Alternative, grassroots opportunities for sensitization such as those that CODI conducted in Bamunanika, can enhance both citizen engagement and revenue generation. Additionally, while the law forbids traditional leaders from participating in political or civil society activities, local governments may wish to explore ways that traditional leaders could be engaged in influencing constituents to their benefit. Anecdotes from the field suggested that traditional leaders and local governments are often in a power struggle, trying to raise funds and loyalty from the same base. There is potential for traditional and government institutions to cooperate without explicitly involving traditional leaders in governance. As in Rwanda, in Uganda “people identify with and understand traditional models” which make them a prime “foundation in order to connect with local people.”62 In each sub-county visited, local government acknowledged that traditional leaders had influence over the population, but they were not actively engaged in the revenue generation due to legal constraints. In this vein, local governments may also wish to explore the potential for Churches and other religious organizations to mobilize people to contribute to local revenue. For example, during a service at the New Life Church in Kabalagala, Kampala, the pastor read aloud – in English and Luganda – the Church’s annual budget and expenditures.63 While this practice pertains more to participatory budgeting, local governments may wish to explore how churches can help in mobilizing people to participate in governance.

60 Smoke, Paul 2008 61 Fjeldstad, Odd-Helge, “To Pay or Not to Pay? Citizens’ Views on Taxation by Local Authorities in Tanzania, 2006 62 Kiessel, et al. 2008 63 January 11 2009

20

Areas for Further Research As we learned through our research, there are many weaknesses to the current decentralization, but also many positive innovations on the ground. We found that first and foremost, local governments need alternative own-source revenues and enhanced collection mechanisms in order to decrease their dependency on central government transfers. Second, we found that civic engagement on the importance of taxation is lacking. Third, each Sub-county struggles with combating both citizen apathy and abject poverty, two major obstacles in enhancing citizen engagement and revenue generation. As such, we feel that going deeper into some of the cases covered here and looking for additional cases of innovation could benefit local government processes and inform central government policy. Because ours and other studies have been conducted on a local level with severe time constraints, a deeper study should be conducted that can determine if the similar small-scale issues and innovations are happening in other districts further out from Kampala. MDP-ESA and LGFC may want to explore ways to connect taxes with service delivery in the minds of citizens.64 For example, we learned that if a health clinic is constructed through locally collected funds, only those who visit the clinic see it as a community service – namely, women and children, not the men who pay the taxes.65 Research could explore how superficial these connections are, as well as what would help citizens better understand how their taxes help the community. In that vein, local governments could benefit from research on alternative civic education programs, such as CODI. As we learned, alternative education can engage citizens, encourage citizen leaders, and create a community that participated regularly in their own governance. When mobilized and educated, citizens can then be empowered to demand services, thus increasing the visibility between payment and service delivery.66 CONCLUSION Our limited exploratory study confirmed the need for more expansive research focused on the potential for citizen engagement to enhance revenue in Ugandan local governments. Since the abolition of the GPT, local governments in Uganda lack fiscal autonomy and are heavily dependent on central government funding. As such, local governments are unable to raise adequate funds through own-source revenues and thus cannot provide adequate services for their constituents. This, compounded with a general lack of tax sensitization has resulted in a deficiency in local government revenue generation. Despite the general lack of funding and citizen engagement across the sub-counties visited, there are small-scale initiatives that directly and indirectly impact revenue and civic engagement and can be used to enhance participation across the board. In several instances, these innovations build upon existing policy frameworks, suggesting that the problem is one of implementation, as the infrastructure to support civic engagement in revenue generation already exists. Further studies that consider improving existing policies will help to create a framework for local governments to increase revenue. Emphasis should be placed on publicizing existing small-scale initiatives and innovations through top-down information sharing, technical assistance and incentives. Working in partnership with the MLG and ULGA, rather than dependency, will help local governments increase their efficiency and effectiveness in raising revenue and eventually close the gap between existing policies and what is happing on the ground.

64 Mentioned first by Raphael Magyezi, Secretary General of the Uganda Local Government Association, January 6 2009 65 Interview with Charles Wansangi, Mafubira Sub-county January 12 2009 66 this was demonstrated by the women of the Namulesa market – now that they understand their collective power as market vendors, they are interested in creating a formal association to lobby for their needs 21

ANNEX 1: LIST OF INTERVIEWS

Interviewee Position Organization Location Date Yasin Sendaula Assistant Commissioner Ministry of Local

Government Kampala January 5, 2009

Tom Matte Permanent Secretary Ministry of Local Government

Kampala January 5, 2009

Patrick Mutabwire Commissioner Ministry of Local Government

Kampala January 6, 2009

John Bahengana Secretary General Urban Authority Association of Uganda (UAAU)

Kampala January 6, 2009

Assumpta Tibamweda Ikiria

Ministry of Local Government

Kampala January 6, 2009

Raphael Magyezi Secretary General Uganda Local Government Association

Kampala January 6, 2009

Martin Onyach-Olaa

World Bank Kampala January 7, 2009

Bernard Ogwang Okutta, James Ogwang, Adam Babae

Director of Local revenues and central grants, senior economist, principal economist

Local Government Finance Commission

Kampala January 7, 2009

Amos Kalema Client Service Officer Luwero District Luwero January 8, 2009 Robert Kabaale Sub-county Chief Bamunanika Sub-

county Luwero January 8, 2009

Community Development and Child Welfare Initiative (CODI)

Wobelenzi, Luwero District

January 8, 2009

Syvia Sibihwana Sub-county Chief Makulubita Sub-county

Makulubita, Luwero District

January 9, 2009

David Serwaniko Vice Chairman Makulubita Sub-county

Makulubita, Luwero District

January 9, 2009

Victo Wamala, Hajji Kigozi Ali, and Paul Kiyimba

Focus Group Makulubita Sub-county

Makulubita, Luwero District

January 9, 2009

Paul Mubiiwa Principal Financial Officer Jinja District Jinja January 12, 2009 Charles Wansagi Vice Chief Mafubira Sub-

county Mafubira, Jinja District

January 12, 2009

Bugembe Town Council

Bugembe, Jinja District

January 12, 2009

Namulesa Market Group

Focus Group Mafubira Sub-county

Mafubira, Jinja District

January 12, 2009

Arthur Larok NGO Forum Kampala January 14, 2009

23

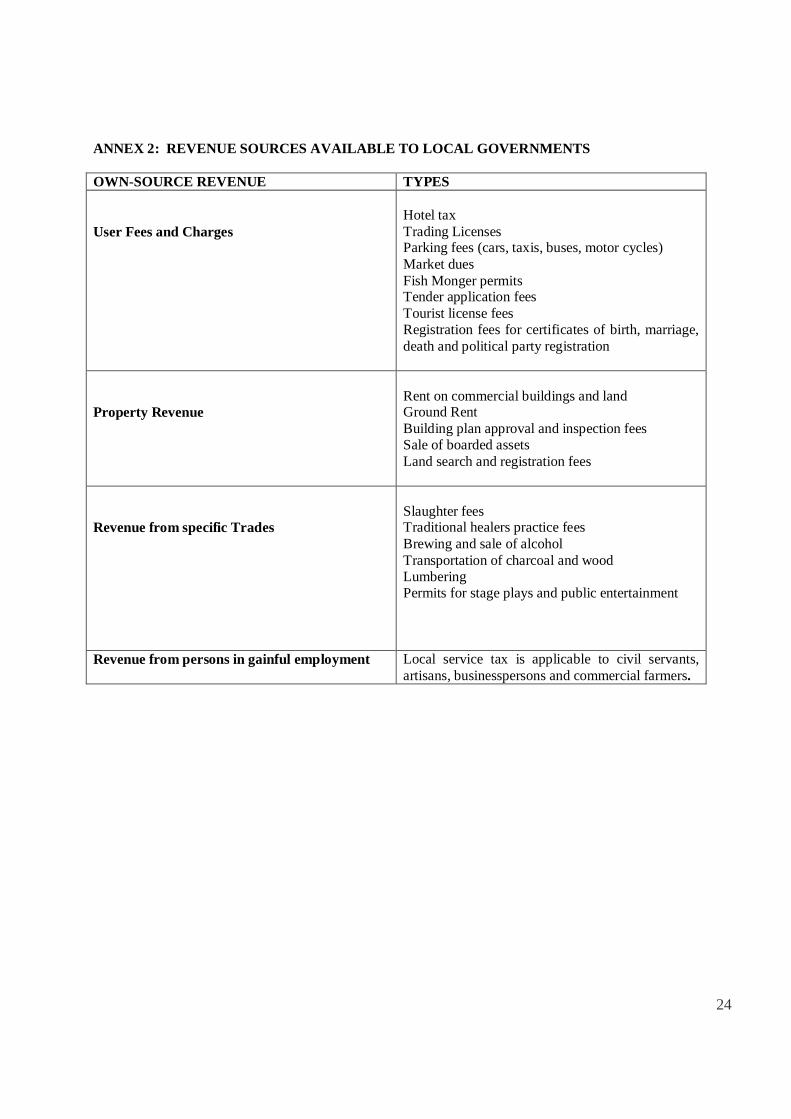

ANNEX 2: REVENUE SOURCES AVAILABLE TO LOCAL GOVERNMENTS OWN-SOURCE REVENUE TYPES User Fees and Charges

Hotel tax Trading Licenses Parking fees (cars, taxis, buses, motor cycles) Market dues Fish Monger permits Tender application fees Tourist license fees Registration fees for certificates of birth, marriage, death and political party registration

Property Revenue

Rent on commercial buildings and land Ground Rent Building plan approval and inspection fees Sale of boarded assets Land search and registration fees

Revenue from specific Trades

Slaughter fees Traditional healers practice fees Brewing and sale of alcohol Transportation of charcoal and wood Lumbering Permits for stage plays and public entertainment

Revenue from persons in gainful employment Local service tax is applicable to civil servants, artisans, businesspersons and commercial farmers.

24

ANNEX 3: STRUCTURE OF LOCAL GOVERNMENT SYSTEM

Source: LGFC (2008), The Experience of Uganda: Local Government’s Role as a Partner in the Decentralization Process to Strengthen Local Development

25

ANNEX 4: UGANDA BUDGET CYCLE Source: Holmes M. and Evans A. (2003), “A review of Experience in Implementing Medium Term Expenditure Frameworks in a PRSP context: A synthesis of Eight Country Studies”, London: ODI,

26

REFERENCES Babcock, Brannan, Gupta, and Shah, “The Right to Participate: Participatory Budgeting & Revenue Generation in Uganda” March 2008 Community Development Initiative, A Social Audit Report on Citizen Empowerment for Good Governance in Bamunanika Sub-county, Luwero District. 2008. Constitution of the Republic of Uganda Article, 1995/2000 COVE Alliance for Uganda www.covealliance.org/aboutus.htm Fiscal Decentralization in Uganda, Draft strategy paper, 2004 Fjeldstad, Odd-Helge, “To Pay or Not to Pay? Citizens’ Views on Taxation by Local Authorities in Tanzania, 2006 Fjeldstad, Odd-Helge, “Local Revenue Mobilization in Urban Settings in Africa, 2006 Namulesa Market Focus Group January 13, 2009 Kiessel, Tumukunde, Khawar (2008), Government-Citizen Partnership for Public Service Delivery in Post- Conflict Situations: Rwanda case study prepared for UNDESA. Larock, Arthur Deepening Decentralization or Regime Consolidation: What explains the Unprecendented creation of new districts in Uganda? 2008 Local Government Act Local Government Accounting Manual Local Government Finance Commission, Local Revenue Enhancement Study, 2000 Local Government Finance Commission, A Study on the Implications of the proposed Suspension of Graduated Tax (GT) on Local Governments’ Financing and Decentralization process in Uganda 2005, p.2 Luwero District Client Charter July 2007 Magyezi, Raphael, Secretary General of the Uganda Local Government Association, January 6 2009 Makulubita Sub-county focus group, January 9 2009 Ministry of Local Government, Local Revenue Hand book 2007 Ministry of Local Government, Local Revenue Enhancement Initiatives, Local Service Tax and Local Hotel Tax, Position Paper for the Local Governments Budget Framework Paper, December 2008 Mobezyi, Olivia Acting Senior Finance Officer, Bugembe Town Council, Jinja District, January 12 2009 Mutabwire, Patrick Interview, Commissioner MOLG January 9 2009

27