CHOICE SERIES VERSION

8

The one who works for you! ® ® Income. Guaranteed. Lifetime Income Benefit Rider American Equity’s CHOICE SERIES VERSION

Transcript of CHOICE SERIES VERSION

The one who works for you!®

®

Income. Guaranteed.

Lifetime Income Benefit RiderAmerican Equity’s

CHOICE SERIES VERSION

Fixed index annuities are designed to guarantee income down the road and provide principal protection along the way, while allowing for growth opportunities. These are important benefits for Americans who are enjoying longer lives and retirements.

For retirees who want to secure a revenue stream that cannot be outlived, we offer the optional Lifetime Income Benefit Rider which provides flexible income payments through a guaranteed income source.

Lifetime Income Benefit Rider

For over 20 years, American Equity has been committed to quality annuity products backed by superior service. Today, as the number three all-time fixed index annuity provider1, we remain focused on the business principles that have served our contract owners from the beginning. Through our financial strength and ongoing stability, we help fund more than half-a-million contract owners’ retirements across the country.

$48 Billion in Assets2

23,000 Active Agents567,000 Active Contract Owners

A- (Excellent) rating from A.M. Best3

A- (Strong) rating from S&P 500®4

American-owned and operated

What is a fixed index annuity? A fixed index annuity is a contract backed by the financial strength and claims paying ability of the issuing company. This guarantees contract owners a retirement vehicle designed to protect assets while allowing for growth opportunities. It does this through a combination of powerful benefits:

• Principal Protection

• Guaranteed Income

• Tax-Deferred Growth

• Liquidity

• May Avoid Probate

How a fixed index annuity works The long-term retirement product is purchased with an insurance provider that, in turn, guarantees principal protection, tax-deferred growth on assets

and a reliable income stream. Throughout the course of the contract, the fixed index annuity can earn additional interest credits based, in part, on equity index increases. As an insurance product, the fixed index annuity is not directly tied to any index. So, there are none of the exposure risks associated with direct stock or share ownership. The annuity cannot lose money due to volatility and the interest credited will never be less than zero.

What is the LIBR?The optional LIBR can help secure a guaranteed lifelong income source. It offers a set accumulation period where money is able to grow tax-deferred up to when the first income payment is received. A rider fee is deducted from the Contract Value each year as long as the rider is active.

Why choose American Equity?

Lifetime Income Benefit Rider Income. Guaranteed. 3

Fixed Index Annuity with Lifetime Income Benefit Rider (LIBR) The fixed annuity and income rider work together to provide a lifetime of benefits.

4

Key Terms In order to understand how the Lifetime Income Benefit Rider works, it is important to know the product’s key terms and features.

Annuitization Conversion of accumulated value of your annuity into regular guaranteed income payments.

Surrender Termination of the contract in exchange for Cash Surrender Value.

Surrender Charge

Fee charged, when applicable, for full or partial distribution over the Penalty-Free Withdrawal amount.

Contract Value

Value of the funds in the Base Contract.

Income Account Value (IAV)

This value is used solely to determine the amount of income to be received under this Rider. It is not a traditionally accessible value. This serves as a measuring value tool for purposes of the Rider only.

IAV Period The period of time during which the Income Account Value is credited the Income Account Value Rate.

IAV Rate Annual effective interest rate that is applied to the Income Account Value.

Lifetime Income Benefit (LIB)

The amount of income received for elected payments. It is based on IAV and age at the time of election.

Rider Fee The fee charged for this rider is deducted from the Contract Value each year as long as the LIBR is active.

Joint Life Payout

A legal spouse, as defined under federal law and at least 50 years old, payment is based on the age of the younger joint payee. Payments are made through the life of the last surviving spouse.

Single Life Payout

For the owner and sole annuitant, payouts are based on age at election.

Interest Crediting Strategies

Contract owners choose from several Index or Fixed Value Crediting Strategies, each offering different opportunities for growth.

Guaranteed Income This rider option offers a set IAV Rate, declared at issue and guaranteed for up to 14 years. The income payments may begin at any time after the first contract year and are available without a Surrender Charge or having to Annuitize the contract.

LIB and Wellbeing Rider The Wellbeing Rider is designed to help address financial concerns related to significant health issues.

The income payment amount can be double, for up to five years, if a contract owners becomes unable to perform multiple Activities of Daily Living (ADLs) outlined in the contract. This benefit is not confinement driven, so it is available for those receiving home care.

There is a two year waiting period before the rider can be turned on.

Indexing Income The IAV is based on the rate of return on the contract from the previous anniversary. The Contract Value rate of return is then multipled by the IAV Multiplier to determine the IAV Credit for the year. Every anniversary, the IAV Credit is applied to the IAV. If there are no interest credits for the year, the IAV will not increase.

LIBR OptionsThere are three income rider options available. These are designed to help individuals reach their income goals and meet their lifestyle needs.

Guaranteed IncomeOption 1

Issue Age: 50-80

IAV Rate: 6.0% Compounding

IAV Period: Up to 14 years

IAV Reset: Years 3-7

Fee: 0.90% of Contract Value, annually

Issue Age: 50-80

IAV Rate: 6.0% Compounding

IAV Period: Up to 14 years

IAV Reset: Years 3-7

Fee: 1.00% of Contract Value, annually

Wellbeing BenefitOption 2

Lifetime Income Benefit Rider Income. Guaranteed. 5

Issue Age: 50-80

IAV Multiplier5: Set at issue, guaranteed for first contract year.

IAV Period: Until the LIB payments are elected

IAV Reset: N/A

Fee: 0.90% of Contract Value, annually

Indexing Income Option 3

There are three income rider options available. The rider is optional and if one is not selected it will not be added to the contract.

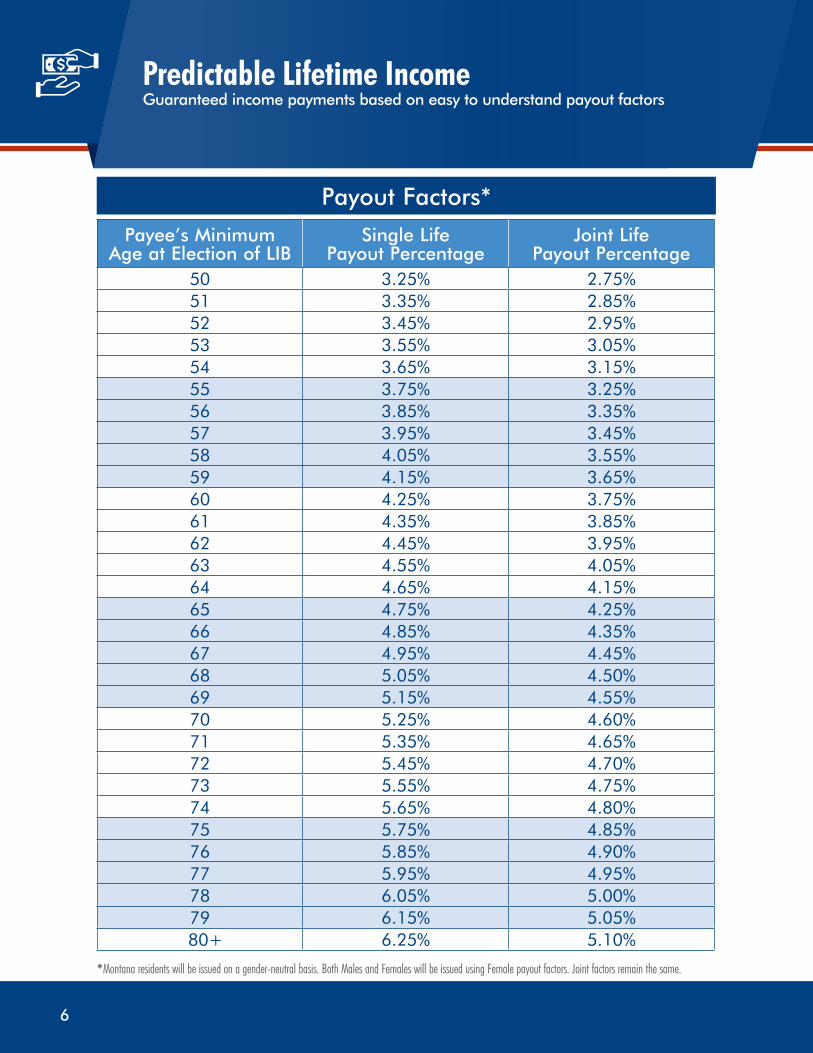

Predictable Lifetime IncomeGuaranteed income payments based on easy to understand payout factors

Payout Factors*

6

Payee’s MinimumAge at Election of LIB

Single LifePayout Percentage

Joint Life Payout Percentage

50 3.25% 2.75%51 3.35% 2.85%52 3.45% 2.95%53 3.55% 3.05%54 3.65% 3.15%55 3.75% 3.25%56 3.85% 3.35%57 3.95% 3.45%58 4.05% 3.55%59 4.15% 3.65%60 4.25% 3.75%61 4.35% 3.85%62 4.45% 3.95%63 4.55% 4.05%64 4.65% 4.15%65 4.75% 4.25%66 4.85% 4.35%67 4.95% 4.45%68 5.05% 4.50%69 5.15% 4.55%70 5.25% 4.60%71 5.35% 4.65%72 5.45% 4.70%73 5.55% 4.75%74 5.65% 4.80%75 5.75% 4.85%76 5.85% 4.90%77 5.95% 4.95%78 6.05% 5.00%79 6.15% 5.05%

80+ 6.25% 5.10%

*Montana residents will be issued on a gender-neutral basis. Both Males and Females will be issued using Female payout factors. Joint factors remain the same.

Income and WithdrawalsThe LIBR offers control of distribution options and the ability to access funds for unexpected circumstances.

Lifetime Income Benefit (LIB) Election LIB payments can begin any time after the first contract anniversary. At the time of election, contract owners select either single life or joint life payouts. Once LIB payments begin these choices are locked in and may not be changed.

• Single Life – payout is based on the contract owner age at the time of payout election.

• Joint Life – payout is based on the youngest age of the contract owner or spouse, and income payments are guaranteed until the death of the surviving spouse.

Excess WithdrawalsAny partial withdrawals taken from the Contract Value after LIB payments have started are considered excess withdrawals and will reduce future LIB payment amounts and your IAV on a pro-rata basis. For example an additional withdrawal of 5% of your Contract Value reduces your future LIB payments by 5%. If an Excess Withdrawal plus LIB payment exceeds the Penalty-Free Withdrawal amount allowed in any contract year; Surrender Charges will be applied to any amount in excess of the Penalty-Free Withdrawal amount. Should Excess Withdrawals reduce the Contract to below the minimum value, as outlined in your contract, the rider terminates and LIB payments stop.

Required Minimum Distributions (RMD) The LIBR is RMD friendly. If the LIB payment does not satisfy the RMD amount in your contract for that year, then we will increase the payment to meet the required amount. This will not be considered an Excess Withdrawal.

Death of Owner American Equity’s annuities have a Death Benefit that allows the beneficiaries immediate access to contract value at the time of death. This can help avoid a costly prolonged probate process.

If the owner’s spouse is sole primary beneficiary of the contract, elects spousal continuation, and is at least age 50, then income benefits may continue. Details and available options are detailed in the contract.

The rider terminates and income payments stop upon the earliest of either the owner’s written request, the date the contract terminates, the date the contract is annuitized or the date the owners of the contract changes. Once the rider terminates, it may not be reinstated.

Tax Treatment All LIB payments are considered a withdrawal from the Contract Value, and any part of the withdrawal that is deferred interest is taxable as income. If the contract is in a qualified plan the entire amount of the withdrawal may be taxable. The taxation is a calculation of income payments as outlined in the Internal Revenue Code.

In addition, the taxable portion of any withdrawal taken before age 59½ may be subject to an additional penalty of 10% by the Internal Revenue Service. Please contract a tax professional for additional information.

Lifetime Income Benefit Rider Income. Guaranteed. 7

1158-SB 04.03.17 ©2017 American Equity. All Rights Reserved.

life.american-equity.com 888-221-1234Call us at6000 Westown Pkwy, West Des Moines, IA 50266

®

Service Our contract owners are why we are here, and we do our best to provide service, second to none, every day.

Integrity Our values of honesty, fairness and truthfulness have been central to our past success and will continue to be for generations to come.

ExcellenceOur dedication to going above and beyond in every facet of our business has established us as a top-tier fixed index annuity provider.

Safety Our products provide Sleep Insurance® for contract owners that can trust their principal is protected and their income is guaranteed for life.

American Equity Commitment to Values

Annuity Contract and 5Rider issued under form series ICC14 IDX8, ICC14 R-LIBR, ICC16 R-LIBR-IDX and 14 R-LIBR-W and state variations thereof. Availability may vary by state.1 Source: http://www.looktowink.com/2016/03/30418/. If you cannot access this article online, you may call 888-647-1371 to request a copy.2 As of 12/31/16 - Assets $48 billion, Liabilities $45 billion.3 A.M. Best has assigned American Equity an “A-” (Excellent) rating, reflecting their current opinion of American Equity’s financial strength and its ability to meet its ongoing contractual

obligations relative to the norms of the life/health insurance industry. A.M. Best utilizes 15 rating categories ranging from A++ to F. An “A-” rating from A.M. Best is its fourth highest rating. For the latest rating, access www.ambest.com. Rating effective 8/2/2006, affirmed 4/14/2016.

4 Standard and Poor’s rating service has recognized American Equity Investment Life Insurance Company with an “A-” rating. An insurer rated “A” has strong financial security characteristics, but is somewhat more likely to be affected by adverse effects of changing circumstances or economic conditions than are insurers with higher ratings. Ratings from ‘AA’ to ‘CCC’ may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Rating effective 8/5/15.

5 During the Initial Period, currently 10 years, the minimum IAV multiplier is 100%. After the Initial Period, the minimum IAV Multiplier is 50% until the LIB payments are elected.Annuity contracts are products of the insurance industry and are not guaranteed by any bank or insured by the FDIC. Guarantees are based on the financial strength and claims paying ability of American Equity.American Equity Investment Life Insurance Company® does not offer legal, investment, or tax advice. Please consult a qualified professional.