China y América Latina: hacia una relación estratégica UDUAL...China y América Latina: hacia una...

40

China y América Latina: hacia una relación estratégica Osvaldo Rosales Director International Trade and Integration Division ECLAC I Seminario Internacional China y A. Latina y el Caribe UNAM, Ciudad de México, México 28 th May, 2012

Transcript of China y América Latina: hacia una relación estratégica UDUAL...China y América Latina: hacia una...

China y América Latina: hacia una relación

estratégica Osvaldo Rosales

Director International Trade and Integration Division

ECLAC

I Seminario Internacional

China y A. Latina y el Caribe

UNAM, Ciudad de México, México

28th May, 2012

I. Emergent Economies: The New Geography of Economic Growth

The South has driven much of the upturn in international trade

GROWTH IN WORLD TRADE AND

CONTRIBUTION OF DEVELOPING COUNTRIES,

2003-2010 (Percentages)

Source: ECLAC, on the basis of data

from CPB Netherlands Bureau for

Economic Policy Analysis.

3

WORLD: DISTRIBUTION OF EXPORTS,

1985 AND 2010 (Percentages of world trade)

1985 2010 a

S-S From 6% to 24%

N-N : From 63% to 38%

Source: ECLAC, on the basis of United

Nations Commodity Trade Database

(COMTRADE).

a Estimate on the basis of 90% of world

exports.

South-South trade has become more significant within world trade in the wake of the crisis

and could exceed North-North trade by 2017

EXPORTS BY REGION, 1985-2020 (Percentages of the total)

Source: ECLAC, on the basis of official figures

Nota Figures for 2011-2020 are projections on the basis of the

long-term linear trend.

4

Regions / Countries 2008 2009 2010 2011

Developed Economies 0,12 -1,79 1,55 1,22

United States 0,00 -0,53 0,56 0,53

European Union 0,15 -0,87 0,36 0,35

Japan -0,07 -0,37 0,23 0,08

Others 0,04 -0,02 0,40 0,25

Developing Countries 2,74 1,27 3,46 3,18

Sub-Saharan Africa 0,13 0,07 0,12 0,14

Latin America and the Caribbean 0,37 -0,15 0,52 0,40

Developing Asia 1,64 1,66 2,29 2,10

China 1,13 1,19 1,40 1,37

Middle East and North Africa 0,25 0,09 0,19 0,20

Central and Eastern Europe 0,11 -0,12 0,15 0,12

World 2,87 -0,52 5,01 4,40

CONTRIBUTION TO WORDL GDP GROWTH, 2008-2011 (Growth rates)

The South led the recovery of world economy in 2010, with Developing Asia and Latin America and the Caribbean playing a protagonist role

Fuente: ECLAC based on IMF data

LAC and DA (2.8 combined)

accounting for 56% of world growth of 5.0 % in 2010. LAC’s

contribution was similar to that of the

US that year

5

In 2010, developing countries received 50% of global FDI flows

Source: ECLAC, on the basis of figures from World Investment Report 2011 (UNCTAD).

FDI FLOWS BY RECIPIENT REGION, 1990-2010

(Billions of dollars and percentages of the total)

The crisis hastened the reduction of the per capita income gap between the developing countries and the advanced economies

WORLD: PER CAPITA INCOME GAP, 1980-2016

(Index of difference in per capita GDP with respect to the developed economies,

in logarithms and 1980=100)

Source: ECLAC, on the basis of IMF (2011), “World Economic Outlook Database,” and World Economic and Financial Surveys. Note: the lines correspond the evolution of the gap. A positive trend denotes a widening of the gap, while a negative trend denotes a narrowing of the gap (convergence).

6

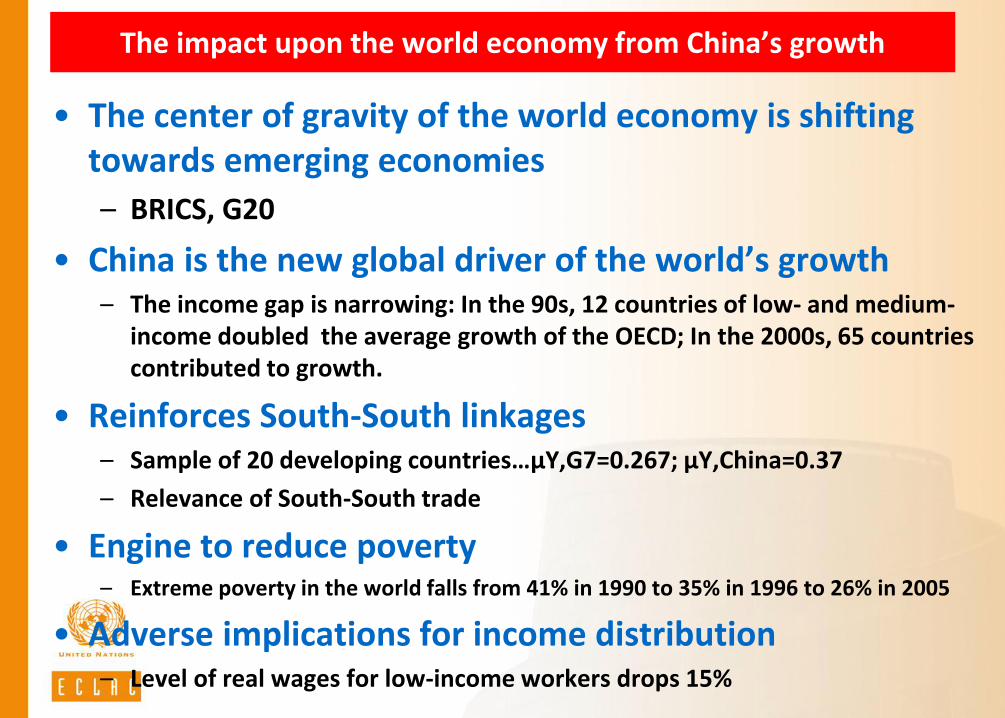

The impact upon the world economy from China’s growth

• The center of gravity of the world economy is shifting towards emerging economies

– BRICS, G20

• China is the new global driver of the world’s growth – The income gap is narrowing: In the 90s, 12 countries of low- and medium-

income doubled the average growth of the OECD; In the 2000s, 65 countries contributed to growth.

• Reinforces South-South linkages – Sample of 20 developing countries…µY,G7=0.267; µY,China=0.37

– Relevance of South-South trade

• Engine to reduce poverty – Extreme poverty in the world falls from 41% in 1990 to 35% in 1996 to 26% in 2005

• Adverse implications for income distribution – Level of real wages for low-income workers drops 15%

8

En 2030, 2/3 of the world middle- class will be in East Asia.

This region will explain 60% of the world consumption

expenditure

POBLACIÓN Y GASTOS DE CONSUMO DE LA CLASE MEDIA,

POR REGIONES, 2009, 2020 Y 2030 a

Fuente: CEPAL, sobre la base de Homi Kharas, “The Emerging Middle Class in Developing Countries”, enero de 2010.

a Las cifras de 2020 y 2030 son proyecciones.

b Los gastos de consumo se calcularon sobre la base de la paridad del poder adquisitivo (PPA).

Población

(En porcentajes del total mundial)

Gastos de consumo b

(En porcentajes del total mundial)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2020* 2030*

América del Norte

Europa

Africa sub-sahara

Oriente Medio yAfrica del Norte

América Latina y elCaribe

Asia y Oceania

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2020* 2030*

Developing Asia and Latin America and the Caribbean will be leading world growth Contribution to World Economic Growth by Region,

2011-2021 (In percentages)

BBVA. “Economic Outlook, Eagles”, Annual Report 2012, Economic Analysis

II. Main features of trade between Latin America and East

Asia

FEALAC-LAC trade with Asia Pacific has been growing fast

A. Exports B. Imports

6,4

1,3

4,2

21,6

33,4

13,7

8,9

10,8

- 10 20 30 40

World

United States

European Union

Asia Pacific

China

Other Asia

Latin America and the Caribbean

Rest of the World

9,2

5,9

9,2

14,8

22,6

9,1

8,1

9,5

- 05 10 15 20 25

World

United States

European Union

Asia Pacific

China

Other Asia

Latin America and the Caribbean

Rest of the World

LATIN AMERICA AND THE CARIBBEAN, INTERNATIONAL TRADE, BY MAJOR PARTNER, 2006-2010 (Annualised growth rates)

Source: Economic Commission for Latin America and the Caribbean

Asia-Pacific, and especially China, has been a key factor in diversifying markets for the region. However, the dynamism of AP

does not lie solely in China

A. Exports B. Imports

0

10

20

30

40

50

60

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Latin America and the Caribbean China

Other Asia United States

European Union

0

10

20

30

40

50

60

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

LATIN AMERICA AND THE CARIBBEAN, INTERNATIONAL TRADE, BY MAJOR PARTNER, 1990-2010 (Share in regional total)

Source: ECLAC based on COMTRADE.

FEALAC-AP is already a significant export market for some Latin American countries. From the AP viewpoint, Latin America has not been a major trading

partner, which results in a highly asymmetrical relationship

A. FEALAC-AP Exports B. FEALAC-LAC Exports

99.282

99.710

93.072

10.483

64.314

55.028

58.492

52.455

50.943

44.066

52.417

55.053

39.134

42.485

23.286

44.031

.007

.029

.161

1.209

1.403

1.682

1.862

1.979

2.530

2.595

2.741

3.270

4.332

4.974

5.077

6.493

0 50 100

Brunei Darussalam

Lao P.D.R.

Myanmar

Cambodia

Australia

Malaysia

Indonesia

Philippines

Thailand

Viet Nam

Singapore

New Zealand

FEALAC-AP

Japan

China

Koorea, Rep. of

FEALAC-AP

FEALAC-LAC

1.067

1.619

2.554

2.716

3.462

3.678

3.844

4.034

5.225

6.060

9.784

12.077

12.400

15.893

17.199

21.574

23.415

39.219

39.953

29.559

26.761

6.520

65.664

4.382

33.866

33.284

4.259

70.047

29.624

21.959

18.052

45.778

41.554

62.193

22.264

17.545

17.648

7.175

0 20 40 60 80 100

El Salvador

Nicaragua

Mexico

Panama

Venezuela, R. B.

Guatemala

Ecuador

Paraguay

Colombia

Costa Rica

FEALAC-LAC

Uruguay

Argentina

Bolivia (E.P.)

Brazil

Peru

Chile

Cuba

FEALAC-AP

FEALAC-LAC

SHARE OF FEALAC-AP AND FEALAC-LAC TRADE IN TOTAL TRADE 2008-2010 (percentages)

ECLAC based on COMTRADE and official national statistics.

Trade between AP and LAC is almost entirely inter-industrial, though with some differences among AP countries

LATIN AMERICA AND THE CARIBBEAN : EXPORT STRUCTURE BY TECHNOLOGICAL INTENSITY

(Percentage) A. MAJOR EXPORT MARKETS, 2008-2010

24%

62%

28%

52%

23%

25%

12%

24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Latin Americaand the

Caribbean

Asia Pacific United States EuropeanUnion

High tech manufactures Medium tech manufacturesLow tech manufactures Natural Resource-based ManufacturesPrimary Products

B. SELECTED ASIAN MARKETS, 2007-2009

0%10%20%30%40%50%60%70%80%90%

100%

ASEAN Aus+NZl China Japan Korea, Rep. of

Others World

Source: ECLAC based on COMTRADE.

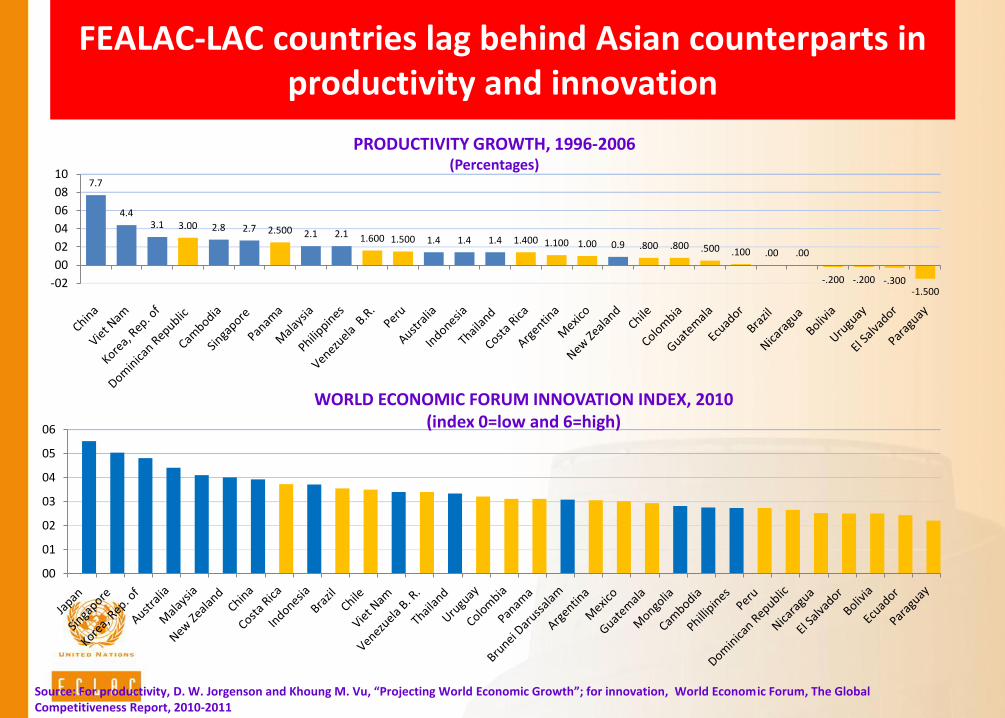

FEALAC-LAC countries lag behind Asian counterparts in productivity and innovation

7.7

4.4 3.1 3.00 2.8 2.7 2.500 2.1 2.1 1.600 1.500 1.4 1.4 1.4 1.400 1.100 1.00 0.9 .800 .800 .500 .100 .00 .00

-.200 -.200 -.300 -1.500

-02

00

02

04

06

08

10

00

01

02

03

04

05

06

PRODUCTIVITY GROWTH, 1996-2006 (Percentages)

WORLD ECONOMIC FORUM INNOVATION INDEX, 2010 (index 0=low and 6=high)

Source: For productivity, D. W. Jorgenson and Khoung M. Vu, “Projecting World Economic Growth”; for innovation, World Econom ic Forum, The Global Competitiveness Report, 2010-2011

FEALAC-AP countries perform much better in poverty reduction and income distribution than FEALAC-LAC counterparts. This presents

formidable challenges for the latter

AUS

CHN

IDN

JPN

KHM

KOR LAO

MNG MYS

NZL

PHL SGP THA

VTM

ARG

BOL

BRA

CHI

COL

CRI

DOM

ECU GTM

MEX

NIC PAN

PER PRY

SLV UGY

VEN

20

25

30

35

40

45

50

55

60

0 5000 10000 15000 20000 25000 30000 35000 40000 45000 50000

GN

I In

dex

GDP per capita

INCOME DISTRIBUTION OF FEALAC COUNTRIES IN RELATION TO GDP PER CAPITA, 2009 (Dollars and GNI Index)

Source: ECLAC based on World Bank World Economic Development Indicators, 2010.

III. Main features of trade between Latin America and China

China has become a very important trading partner for some countries in LAC particularly with respect to imports.

A. Exports B. Imports

Source: ECLAC based on data from COMTRADE

LATIN AMERICA AND THE CARIBBEAN: ASIA-PACIFIC AND CHINA’S PARTICIPATION IN TRADE, 2010

(In percentages of total imports and exports of each country)

0 10 20 30 40 50 60

NicaraguaBahamasGrenada

St. Vincent and the GrenadinesBelize

El SalvadorSaint Lucia

Saint Kitts & NevisJamaica

GuatemalaMexico

Trinidad and TobagoParaguaySuriname

HaitiBarbadosDominica

GuyanaEcuador

HondurasDominican Republic

Bolivia, Plur. St. ofCosta RicaColombia

PanamaUruguay

Venezuela, Bol. Rep. ofArgentina

Lat. Am. & CaribbeanBrazilPeruChileCuba

China Others Asia /a

9.1

0 10 20 30 40 50 60

NicaraguaSaint Lucia

Saint Kitts & NevisGrenada

HondurasTrinidad and Tobago

BarbadosBahamas

JamaicaBelize

El SalvadorPanama

Costa RicaGuatemala

MexicoGuyana

HaitiDominica

EcuadorSuriname

Bolivia, Plur. St. ofVenezuela, Bol. Rep. of

Dominican RepublicLat. Am. & Caribbean

CubaUruguay

St. Vincent & the GrenadinesColombiaArgentina

BrazilChilePeru

Paraguay

China

Others Asia /a

13.0

In eight short years, China’s importance as a trading partner for Latin America has increased significantly.

Destination of Exports Source of Imports

2000 2008 2000 2008

Argentina 6 2 4 3

Brazil 12 1 11 2

Chile 5 1 4 2

Colombia 35 4 15 2

Peru 4 2 13 2

Venezuela 37 3 18 3

Costa Rica 26 2 16 3

Mexico 25 5 6 3

Cuba 5 2 5 2

China has a presence in 21 Latin American nations

• Top 5 in 10 countries

• Top 1-2- in 6 countries

… in almost 32 markets

• Top 5 in 23 countries

• Top 2 in 5 countries

LAC (16 countries): Share of the main destinations in total exports, 2000-2020 (In %)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on data from the COMTRADE database and national sources. Notes: The 16 countries are: Argentina, Bolivia (Plurinational State of), Brazil, Chile, Colombia, Costa Rica, Ecuador, El Salvador, Guatemala, Honduras, Mexico, Panama, Paraguay, Peru, Uruguay, Venezuela (Bolivarian Republic of). Estimates and projections based on GDP growth rates for the years 2000-2009 in the United States, European Union, China, Latin America and the Caribbean, Asia-Pacific, and the Rest of World. A growth rate of trade which converges to the economies' long-term growth rate is expected.

LAC (16 countries): Share of the Main Sources of Total Imports, 2000-2020. (In %)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on data from the COMTRADE database and national sources. Notes: the 16 countries are: Argentina, Bolivia (Plurinational State of), Brazil, Chile, Colombia, Costa Rica, Ecuador, El Salvador, Guatemala, Honduras, Mexico, Panama, Paraguay, Peru, Uruguay, Venezuela (Bolivarian Republic of). Estimates and projections based on GDP growth rates for the years 2000-2009 in the United States, European Union, China, Latin America and the Caribbean, Asia-Pacific, and Rest of World. It is expected a growth rate of trade which converges to the economies' long-term growth rate.

China is displacing EU as the second largest trading partner of LAC

Recent features of trade between China and Latin America

• Trade is concentrated in few countries and few products

– Brazil, Chile and Argentina account for 77% of exports

– Copper (30%) and Soy (12%)

• In each country, few products (2-3) make up 80-90% of exports to China (with the exception of Brazil and Mexico)

• They are basic products that are not technologically intensive or knowledge-based (with the exception of Mexico and Costa Rica)

Recent features of trade between LAC-AP

• Trade ties with China and Asia-Pacific are different among the regions.

– In South America they are of a complementary nature and South America has a slight surplus.

– Competition and deficits in Mexico and Central America

• High asymmetries between elevated trade flows and low reciprocal investment

• Trade with China is excessively of an inter-industrial nature.

– Lat. Am. exports raw materials and imports manufactures.

– Less room for diversifying exports

– Productive and technological alliances are more difficult.

Exports, imports and trade balance with China (In millions of dollars)

Source: ECLAC on the basis of COMTRADE data, official data and DOTs (IMF).

Trade pattern of LAC with China is

different among South America and

Mexico and Central America

IV. Conocer los desafíos de China para aprovechar oportunidades

29

Los desafíos de China

• Apoyarse más en el mercado interno y en el consumo doméstico

• Equilibrar la costa con el interior

– Reducir las desigualdades

– Mejorar la distribución del ingreso

• Construir una red de apoyo social

30

Osvaldo Rosales 31 6/5/2012

Agenda interna de negociaciones en China

• Política del “Go West” busca reducir diferencias campo ciudad y entre la costa y zonas rurales

• El delta del Yangtze –Shangai es el más dinámico

• La zona de Guangdong – en torno al delta Pearl River- busca competir con Shangai, creando una amplia zona de LC hasta la frontera con India

Osvaldo Rosales 32 6/5/2012

El 9+2, un TLC inédito

• Area integrada de comercio que incluye 9 provincias más Hong Kong y Macao – 1/3 de la población china

– 30% de las X chinas

– 40% del PIB de China

– Objetivo: llevar el dinamismo de la costa a las provincias más pobres del interior

– 9 provincias: Guangdong, Fujian, Jiangxi, Hunan, Guangxi, Hainan, Guizhou, Yunnan, Sichuan

– 9+2 vía Yunnan conduce a la India !!!!!!

Osvaldo Rosales 33 6/5/2012

EL TLC 9+2

Los desafíos de China

• Apoyarse más en el mercado interno y en el consumo doméstico

• Equilibrar la costa con el interior

• Construir una red de apoyo social

• Reducir drásticamente la contaminación

34

35

36

Los desafíos de China

• Apoyarse más en el mercado interno y en el consumo doméstico

• Equilibrar la costa con el interior

• Construir una red de apoyo social

• Reducir drásticamente la contaminación

• Asegurar un desarrollo bajo en carbono

• Asegurar una adecuada oferta agrícola y de materias primas

• Compatibilizar lo anterior con su nuevo rol en Asia y en la economía global

– Convertibilidad del yuan

– Apertura de su cuenta de capitales

– Internacionalización de empresas

37

V. Building a strategic economic and trade relationship with

China/Asia.

Main Issues • China is more important for South America’s growth

than the United States.

• Positive cycle for international prices for commodities for the remainder of the decade (relevant for South America)

– Possibility of a “super cycle”

– Risk: excessive support for commodities with low value added, exchange rate appreciation, obstacles for export diversification and productive transformation

– Challenge: Take advantage of the opportunities

• “Dutch Disease?” The curse of natural resources?

• New central-peripheral cycle in the XXI century?

Improving relationships between China and Latin America: challenges for L. America

• Privilege multinational approaches. Less emphasis to unilateral approaching initiatives to China and Asia Pacific

– Scale matters: more coverage initiatives capable of attracting resources in larger

– Larger scale of initiatives

• Coordinate efforts between LatAm countries

• Define regional priorities in an agreed agenda

– Export diversification

– Attracting Chinese FDI: investing in Asian value-chains

– Business and technology Sino-Lat Am alliances

– Advancing on trade and investment operations in renminbi

Improving relationships between China and Latin America: challenges for China

• Increase and diversify its FDI in Lat Am

• Understand the political and institutional features of Lat Am

– Separation of powers; legislation on visas; labor and environment legislation; role of civil society

• Funds to support export diversification of Lat AM SMEs

– Traceability in natural resources exports

– Quality certification

– Technical standards

– Reducing carbon footprint in exports

– Joint promotion in China

Joint challenges for China and Lat Am

• Increase levels of bilateral trade and investment

– Improve dialogue on trade remedies.

– Transparency on SPS issues and health protocols

– NTB in line with WTO provisions

– Mechanisms for consultation, negotiation, mediation and arbitration to resolve commercial disputes

• Cooperation on the global agenda

– Reform the international monetary system and international financial regulation

– Climate change

– Early warning and policy coordination against threats of international economic crisis

– South-South cooperation mechanisms in preventing financial impacts, preventing contagion and preserving trade flows.

Advancing an agenda for China-Latam cooperation

• Strengthening S-S dialogue on issues of the global agenda

– International monetary system reform

– Climate Change

• Increasing Trade

– Transparency on SPs and sanitary protocols

– NTB in line with WTO provisions

– Arbitrations and negotiated settlements to avoid excessive AD accusations

• Fostering reciprocal investments

• Diversifying Trade (Chinese fund for LA X diversification)

– Traceability in natural resource exports

– Food safety and sustainable agriculture

– Reducing carbon in exports

– Tech standards, quality certifications

• Fostering reciprocal investments

– Regional portal on Investment opportunities

– Attract Chinese investors to invest in LA infrastructures

– Support LA investment in China and Asia Pacific (CCPIT may help)

• Working for a China-Latin America Summit

Latin America’s Challenges

• Diversify Exports

• Invest in China

• Participate in Asian supply value

chains

• Coordinated policy on China

• Work towards a China-Latin America

Summit.

China’s Challenges

• Increase FDI in Latin America

• Funds to support SMEs exporters

• Technological Cooperation

• Understand political-institutional

aspects of Latin America

Joint Challenges

• Improve dialogue between ministries of

trade (trade remedies)

• Identify joint opportunites in China, Asia

and Latin America

• Trade, investment and technological

business partnerships

• Create a forum for an ongoing dialogue

• Cooperation on issues of the global

agenda

45

How to deal with these challenges?

Please, read it.