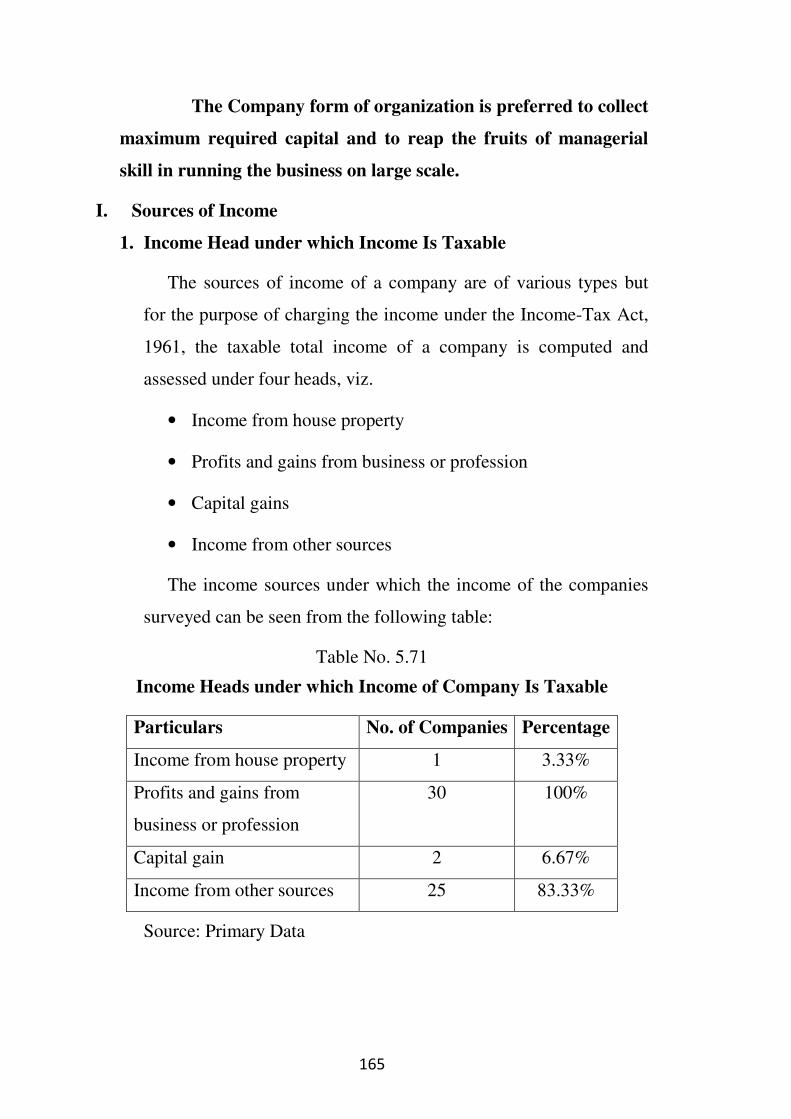

CHAPTER - V PRESENTATION OF THE DATA AND ANALYSIS...

136

66 CHAPTER - V PRESENTATION OF THE DATA AND ANALYSIS 5.1 Introduction: The present study is being carried out with the objectives to study overall growth of income-tax consultancy as a profession, to discuss various services provided by tax consultants to the assessees, the difficulties faced by them in providing such services and the difficulties of various types of assessees (i.e. individual, firm and company only) in getting the services from income-tax consultants. In view of these objectives the researcher has collected huge amount of primary data by presenting and circulating separate questionnaire for each type of assessees i.e. individual, firm and company. The tax authorities directly and indirectly related with income-tax consultancy services are contacted, the formal and informal discussions are held with them and relevant data is elicited. The secondary data is collected by using available secondary sources. In this chapter an attempt is being made to present, analyze and interpret the data under the following two main parts- I. Income-Tax Consultants, their Services and Difficulties II. Different types of assessees and their difficulties in getting tax services. This part is again divided into three sections, viz. 1. Individual Assessees 2. Partnership Firm Assessees and 3. Company

Transcript of CHAPTER - V PRESENTATION OF THE DATA AND ANALYSIS...

66

CHAPTER - V

PRESENTATION OF THE DATA AND ANALYSIS

5.1 Introduction:

The present study is being carried out with the objectives to study

overall growth of income-tax consultancy as a profession, to discuss

various services provided by tax consultants to the assessees, the

difficulties faced by them in providing such services and the difficulties

of various types of assessees (i.e. individual, firm and company only) in

getting the services from income-tax consultants. In view of these

objectives the researcher has collected huge amount of primary data by

presenting and circulating separate questionnaire for each type of

assessees i.e. individual, firm and company. The tax authorities directly

and indirectly related with income-tax consultancy services are contacted,

the formal and informal discussions are held with them and relevant data

is elicited. The secondary data is collected by using available secondary

sources.

In this chapter an attempt is being made to present, analyze and

interpret the data under the following two main parts-

I. Income-Tax Consultants, their Services and Difficulties

II. Different types of assessees and their difficulties in getting tax

services.

This part is again divided into three sections, viz.

1. Individual Assessees

2. Partnership Firm Assessees and

3. Company

67

PART-A

Income-Tax Consultants, their Services and Difficulties

In India, income-tax services are mainly provided by the

professional Chartered Accountants, who are the members of their

professional body, the Institute of Chartered Accountants of India and

abide by their professional code of conduct. Some law professionals and

those who have completed their degrees or diplomas in taxation,

accountancy or commerce also provide such services. All these services

providers provide their various types of services according to their

professionals’ rules and regulations, code of conduct, rules and

regulations provided by the Government under various taxation acts, rules

and customs followed in this regard. The professional charges vary from

case to case depending on number of services provided, volume of

transactions etc. generally per case lump sum or on percentage basis.

They mainly face their professional difficulties such as their staff,

location of office, time management etc. Difficulties on the part of clients

arise because of various tax collection departments, their official practices

and the implementation of the rules and regulations framed under the

Income-Tax Act, 1961 by them.

5.A.I General Information:

As far the income-tax consultants are concerned they differ from

each other as to their qualification, seniority in the profession, age,

strength of their staff, training to them, their social status, public

relations, office location, other infrastructural facilities provided by them,

service promptness etc., which affect their client base, quality of services

provided by them and their efficiency and difficulties in providing

68

services. As such a detailed enquiry is held in this regard which revealed

following things:

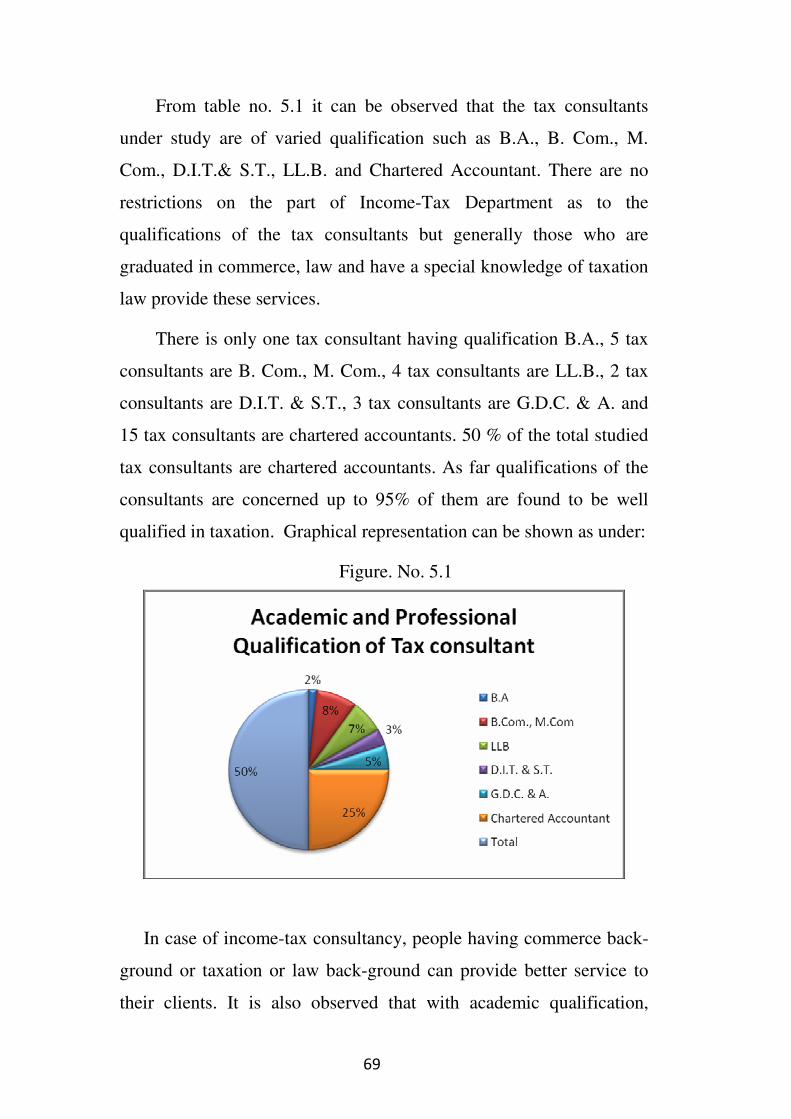

5.A.I.(1) Academic and Professional Qualifications

Academic and professional qualification plays very important role

in service providing task. It mainly affects the quality and performance of

the service provided. The highly qualified and professionalized

consultants can provide maximum tax services under one roof. Naturally

the clients prefer such consultants. The academic and professional

qualifications of the studied tax consultants are as under:

Table No. 5.1

Academic and Professional Qualifications

Qualification No. of Tax Consultants Percentage

B.A 1 3.33%

B.Com., M.Com 5 16.67%

LL.B 4 13.33%

D.I.T. & S.T. (Diploma in

Income-tax & Sales Tax)

2 6.67%

G.D.C. & A. 3 10%

Chartered Accountant 15 50%

Total 30 100%

Source: Primary Data

69

From table no. 5.1 it can be observed that the tax consultants

under study are of varied qualification such as B.A., B. Com., M.

Com., D.I.T.& S.T., LL.B. and Chartered Accountant. There are no

restrictions on the part of Income-Tax Department as to the

qualifications of the tax consultants but generally those who are

graduated in commerce, law and have a special knowledge of taxation

law provide these services.

There is only one tax consultant having qualification B.A., 5 tax

consultants are B. Com., M. Com., 4 tax consultants are LL.B., 2 tax

consultants are D.I.T. & S.T., 3 tax consultants are G.D.C. & A. and

15 tax consultants are chartered accountants. 50 % of the total studied

tax consultants are chartered accountants. As far qualifications of the

consultants are concerned up to 95% of them are found to be well

qualified in taxation. Graphical representation can be shown as under:

Figure. No. 5.1

In case of income-tax consultancy, people having commerce back-

ground or taxation or law back-ground can provide better service to

their clients. It is also observed that with academic qualification,

70

experience in this field is also equally important. Some well-known

tax consultants in the studied area are not from commerce or taxation

background yet with experience and devotional work they are

providing better quality services to their clients.

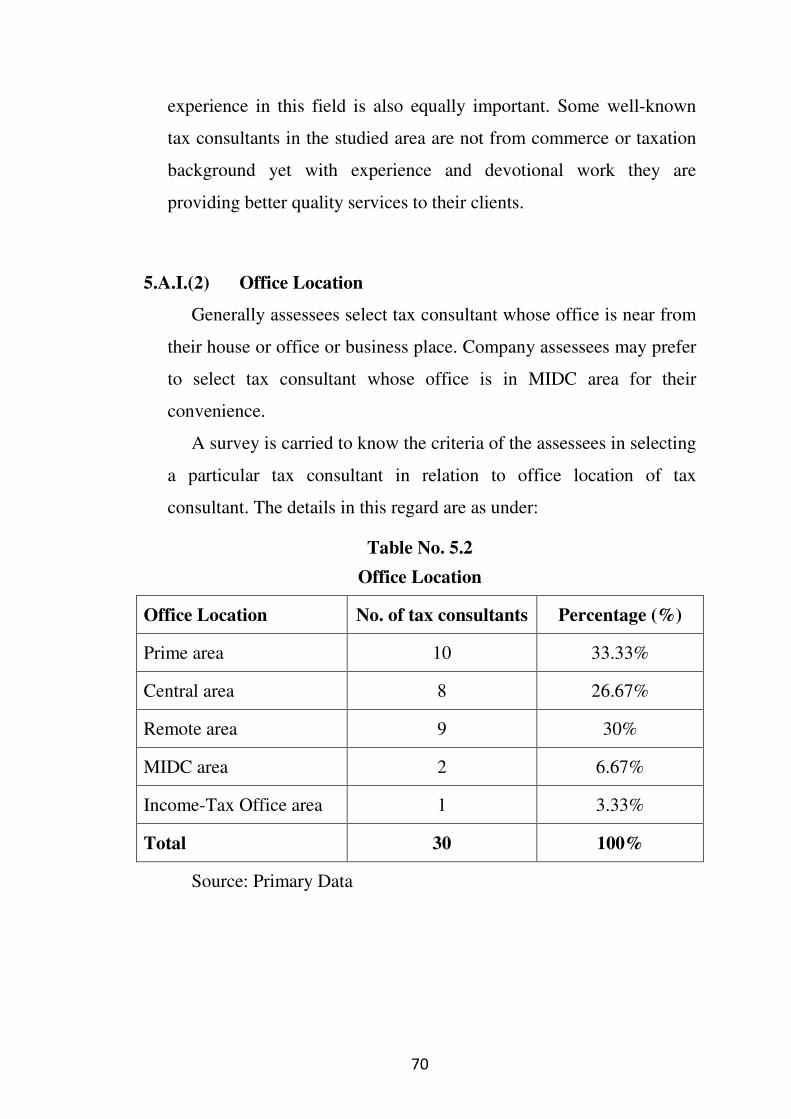

5.A.I.(2) Office Location

Generally assessees select tax consultant whose office is near from

their house or office or business place. Company assessees may prefer

to select tax consultant whose office is in MIDC area for their

convenience.

A survey is carried to know the criteria of the assessees in selecting

a particular tax consultant in relation to office location of tax

consultant. The details in this regard are as under:

Table No. 5.2

Office Location

Office Location No. of tax consultants Percentage (%)

Prime area 10 33.33%

Central area 8 26.67%

Remote area 9 30%

MIDC area 2 6.67%

Income-Tax Office area 1 3.33%

Total 30 100%

Source: Primary Data

71

Figure 5.2

Office Location

Central area,

26.67%

Prime area,

33.33%

Income-Tax

Office area,

3.33%

MIDC area,

6.67%

Remote area,

30%

From the table no. 5.2 it can be observed that office places of 10

(33.33%) tax consultants are in prime area, 8 (26.67%) tax consultants

are in central area, while offices of 9 (30%) tax consultants are in

remote area. 2 (6.67%) tax consultants have selected MIDC area for

their office. One tax consultant’s office is in Income-Tax Office area.

Though the above table gives statistical data, it is observed that it is

not necessary for the assessees that the office place of tax consultant

must be in prime area or in central area. It is also observed that ‘trust

of assessees on tax consultant’ and ‘services provided by them’ are

only important things in selecting tax consultant, office place is not so

important for assessees.

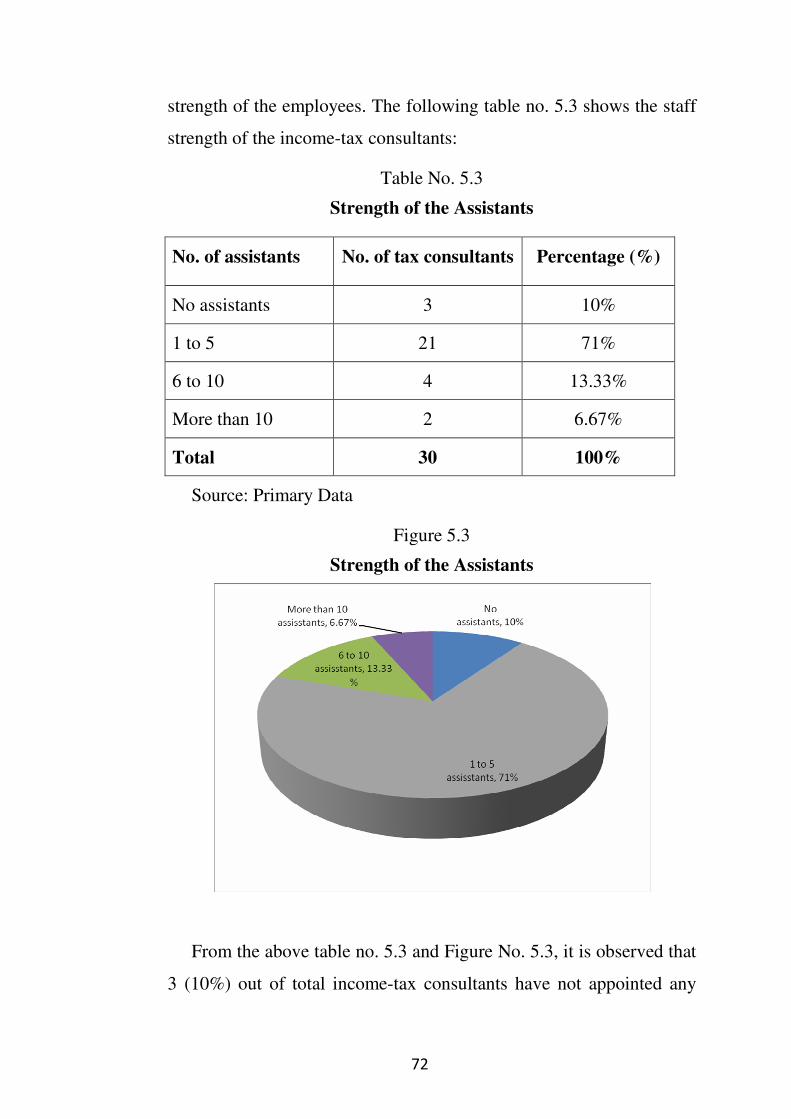

5.A.I.(3) Assistants’ Strength:

Assistants or office staff of the tax consultants play vital role in tax

consultancy services. They assist tax consultants by performing

majority of clerical work required for assessees. An enquiry is made to

review the size of the income-tax consultancy firms based on their

72

strength of the employees. The following table no. 5.3 shows the staff

strength of the income-tax consultants:

Table No. 5.3

Strength of the Assistants

No. of assistants No. of tax consultants Percentage (%)

No assistants 3 10%

1 to 5 21 71%

6 to 10 4 13.33%

More than 10 2 6.67%

Total 30 100%

Source: Primary Data

Figure 5.3

Strength of the Assistants

From the above table no. 5.3 and Figure No. 5.3, it is observed that

3 (10%) out of total income-tax consultants have not appointed any

73

assistant. These income-tax consultants are doing all the work

themselves.

21 (70%) income-tax consultants have appointed less than 5

assistants. Table no. 5.3 shows that majority of the income-tax

consultants require maximum 5 assistants. 4 (i.e. 13.33%) income-tax

consultants have appointed assistants in the range of 6 to 10. Only 2

income-tax consultants have appointed more than 10 assistants. One of

them has appointed 18 assistants. This shows that the most of the

income-tax consultants in this area are small sized and operate on a

small scale.

5.A.I.(4) Selection of Assistants / Staff

Well qualified and experienced assistant is the asset to the

tax consultancy firm. He can provide quality service efficiently to

the clients. In tax consultancy service, assistants who are from

commerce and/or law faculty are preferred to provide service

efficiently. As such every tax consultant takes maximum care in

selection of these assistants.

A survey is conducted to know the selection criteria by the

income-tax consultants in selecting the assistants. The following

table shows different criteria used for selecting the assistants.

74

Table No.5.4

Selection Criteria for Assistants

Particulars No. of Tax consultants Percentage (%)

Educational qualification

(at least B.Com.)

19 63.33%

Computer education

(especially Tally)

10 33.33%

Knowledge of accounting

& auditing

6 20%

Experience 4 13.33%

Loyalty to organizations 2 6.67%

Source: Primary Data

The table no. 5.4 shows that the tax consultants in selecting

their staff have given maximum 63.33% emphasis on their

educational qualifications while only 33.33% and 20% emphasis is

given to their skill oriented education i.e. computer literacy and

knowledge of accounting and auditing respectively. Much

importance has not been given to experience (13.33%) and loyalty

(6.67%) of the candidate. Majority of the consultants expect that

their assistant should be a commerce graduate.

However, the informal discussion by the researcher with the

income-tax consultants revealed that the group of friends and

relatives of tax consultants are also playing important role in the

selection of staff by the tax consultants.

75

5.A.I.(5) Training to Assistants / Staff

Business environment is ever changing. It requires up to date

knowledge and information. The services rendered by tax

consultants are technical by nature. Technical service requires

constant and regular training to the staff. Assistants should up

dated with current tax matters by providing training to them.

A survey is taken to enquire the adequacy of the training

given to the staffs by the income-tax consultants in this area. The

following table shows the details relating to training given to the

assistants:

Table No.5.5

Training to Assistants

Particulars No. of tax consultants Percentage (%)

Training Provided 25 83.33%

Training Not Provided 2 6.67%

Not applicable 3 10%

Total 30 100%

Source: Primary Data

It is expected that the professional service provider should render

satisfactory services to his clients. Tax consultant is a professional and

therefore his services to his clients must be satisfactory. For this

purpose, tax consultant must be with well equipped office and with

trained staff.

76

Figure No.5.4

Training to Assistants

Training Not

Provided,

6.67%

Training

Provided,

83.33%

Not

applicable,

10%

The issue of training to staff is discussed with the tax consultants

interviewed by the researcher. From the table 5.5 it is noticed that out

of 30 tax consultants interviewed 25 (83.33%) tax consultants provide

training to staff and only 2 tax consultants in the selected area have

not provided training to their staff and 3 tax consultants are rendering

services to the clients without the help of assistants.

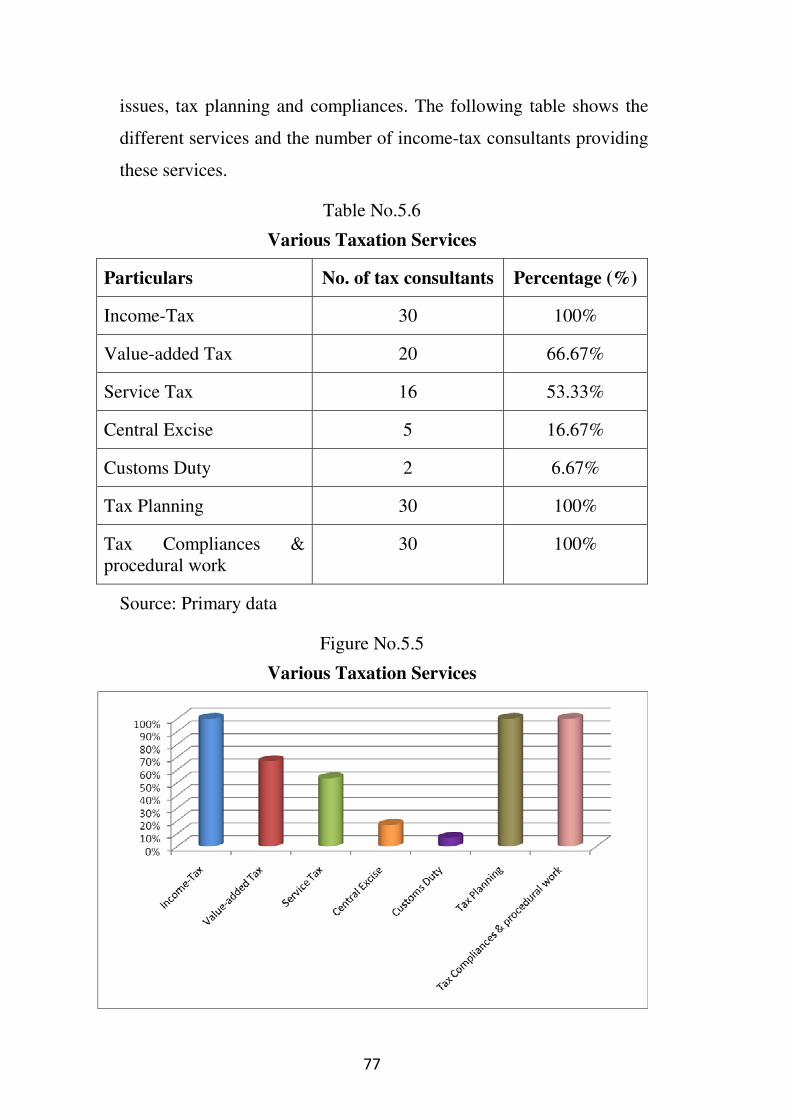

5.A.II Services Provided by Income-Tax Consultants

Income-tax consultants provide various types of services to their

clients, which mainly include book-keeping, taxation, cost accounting,

auditing etc. The quality of service provided mainly depends on the

infrastructural facility available as well as qualification of the

consultants and the number of services provided by them.

5.A.II.(1) Taxation Services

The study of different services provided by the income-tax

consultants revealed that the major services pertain to income-tax

77

issues, tax planning and compliances. The following table shows the

different services and the number of income-tax consultants providing

these services.

Table No.5.6

Various Taxation Services

Particulars No. of tax consultants Percentage (%)

Income-Tax 30 100%

Value-added Tax 20 66.67%

Service Tax 16 53.33%

Central Excise 5 16.67%

Customs Duty 2 6.67%

Tax Planning 30 100%

Tax Compliances &

procedural work

30 100%

Source: Primary data

Figure No.5.5

Various Taxation Services

78

The table no. 5.6 shows that all the income-tax consultants

provide the services of income-tax issues, tax planning and tax

compliances and procedural work. Tax planning is the service which

tries to ensure that the tax liability is minimum. It is different from

evasion of tax. In tax planning due care is taken to get the benefit of

exemptions and deductions allowed by the Income-Tax Act, 1961.

The compliances and procedural work aims at making sure that all

necessary forms and payments are appropriately submitted.

Apart from the core areas of practice, approximately 20 (66.67%)

and 16 (53.33%) of the income-tax consultants provide the Value

Added Tax consultancy and Service Tax consultancy services to their

clients respectively. Other taxation services such as Central Excise and

Customs are not provided by most of the income-tax consultants. Only

5 (16.67%) and 2 (6.67%) of the income-tax consultants provide these

services respectively.

5.A.II.(2) Book-keeping Services

Maintaining of accounts according to the legal provisions of the

law is prime necessity in taxation. This requires specialized staff.

Many small scale businesses, individuals do not afford to employ such

staff. They take the help of their tax consultants in this regard. As such

most of the income-tax consultants provide such book-keeping

services to their clients. The following table no. 5.7 shows the details

of the book keeping services provided by the income-tax consultants:

79

Table No.5.7

Book-keeping Services

Particulars No. of Tax consultants Percentage (%)

Service Provider 24 80%

Service Not-

provider

6 20%

Total 30 100%

Source: Primary data

The above table shows that the 24 (80%) of the income-tax

consultants provide the services of book keeping to the clients. Only 6

(20%) of the income-tax consultants do not provide this service to

their clients.

5.A.II.(3) Cost Accounting Services

Cost accounting services are not so common in this area. Generally

cost accounting services are availed by manufacturing companies

which are less in number in this area. The following table no. 5.8

shows the details of the cost accountancy service provided by the

income-tax consultants:

Table No.5.8

Cost Accounting Services

Particulars No. of Tax consultants Percentage (%)

Service Provider 5 16.67%

Service Not-provider 25 83.33%

Total 30 100%

Source: Primary Data

80

The above table shows that only 5 (16.67%) of the income-tax

consultants provide the services of cost accountancy. Other 25

(83.33%) of the income-tax consultants do not provide this service to

their clients. Informal discussion with the income-tax consultants

revealed that this service is not generally demanded by the clients and

hence are not provided.

5.A.II (4) Audit Services

Audit is another service provided by the chartered accountants’

firms and certified auditors along with taxation services to their

clients. Under Companies Act, Trust Act and many other Acts, it is

mandatory to the business to get their accounts audited by a competent

authority. Cost audit, Tax audit, VAT audit, Financial audit etc. are

various audits required under various Acts.

Audit services are provided only by the income-tax consultants

who are chartered accountants and who are competent to conduct such

audits under the respective law (certified auditors). A study of ‘the

income-tax consultants who can conduct the audits for assessees’ is

done to understand the different types of audits conducted by them.

Table no. 5.9 reveals the different types of audits and income-tax

consultants providing these audit services to their clients:

81

Table No.5.9

Audit Services

Particulars No. of Tax consultants Percentage (%)

Statutory Audit 16 53.33%

Cost Audit -- --

Tax Audit 19 63.33%

VAT Audit 17 56.67%

Internal Audit 16 53.33%

Financial Audit 4 13.33%

Environmental Audit 2 6.67%

Information System

Audit

6 20%

Source: Primary Data

The table no. 5.9 shows that maximum tax consultants 63.33% are

providing tax audit services to their clients while 53.33% (16), 56.67%

(17) are providing statutory audit and VAT audit services to their

clients. Only 4 out of 30 are providing, financial audit services while 6

(20%) are providing information system audit facilities to their clients.

Except 2 (6.67%) none of the consultant provides environmental audit

service to their clients. Cost audit services are not provided by the

income-tax consultants in this area.

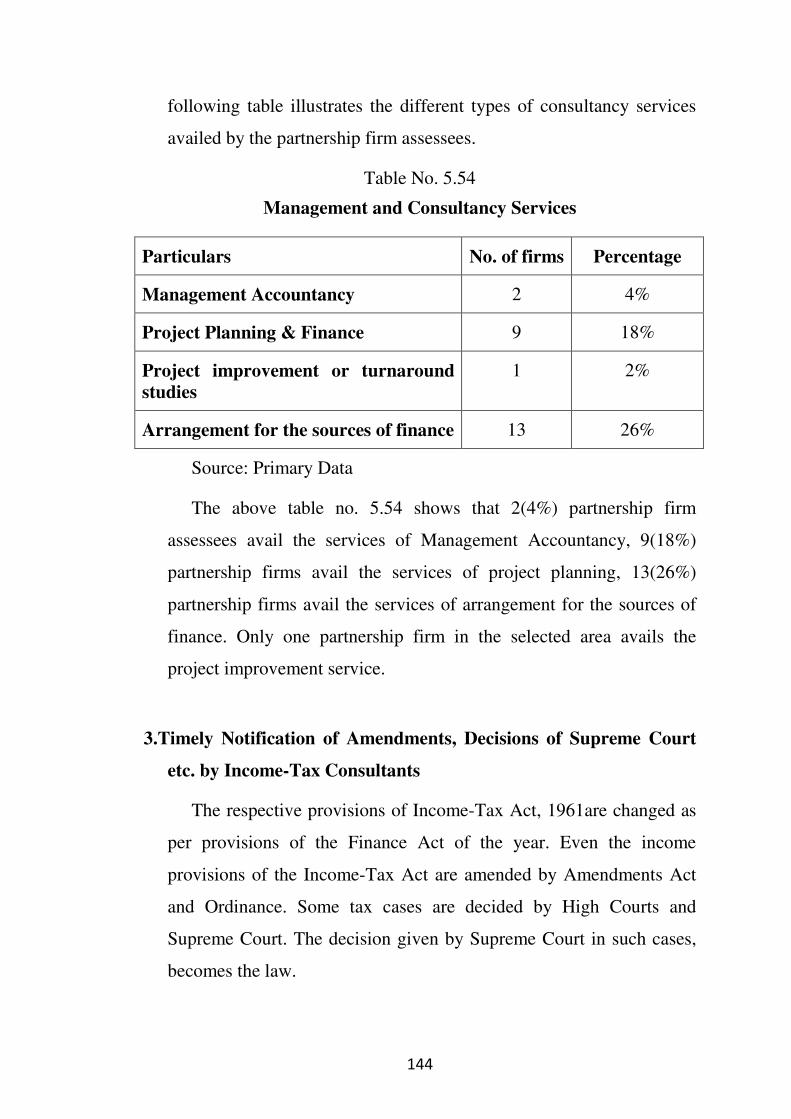

5.A.II.(5) Consultancy Services

The income-tax consultants also provide the consultancy services

to their clients. Such consultancy services include the management

accountancy, project planning and financing, project improvement or

82

turnaround studies, arrangement for the sources of finance, etc. The

following table no. 5.10 illustrates the different types of consultancy

services provided by the income-tax consultants:

Table No.5.10

Consultancy Services

Particulars No. of tax consultants Percentage (%)

Management

Accountancy/Internal Audit

16 53.33%

Project Planning & Finance 20 66.67%

Project improvement or

turnaround studies

4 13.33%

Arrangement for the sources of

finance

11 36.67%

Source: Primary Data

The above table shows that most of the income-tax consultants, i.e.

20 (66.67%) provide the project planning and financing services. Other

major consultancy services include management accountancy / internal

audits and arrangement for the sources of finance that are provided by

approximately 16 (53.33%) and 11 (36.67%) of the income-tax

consultants. Only 4 (13.33%) income-tax consultants provide these

services. The services of project improvement or turnaround studies are

not provided by the most of the income-tax consultants as there is no

demand from clients for these services.

5.A.II.(6) Timely Notification of Amendments, Decisions of

Supreme Court to the Assessees

Timely intimation of amendments in Income-Tax Act and decisions of

various courts, save the time, money and efforts of the assessees. They

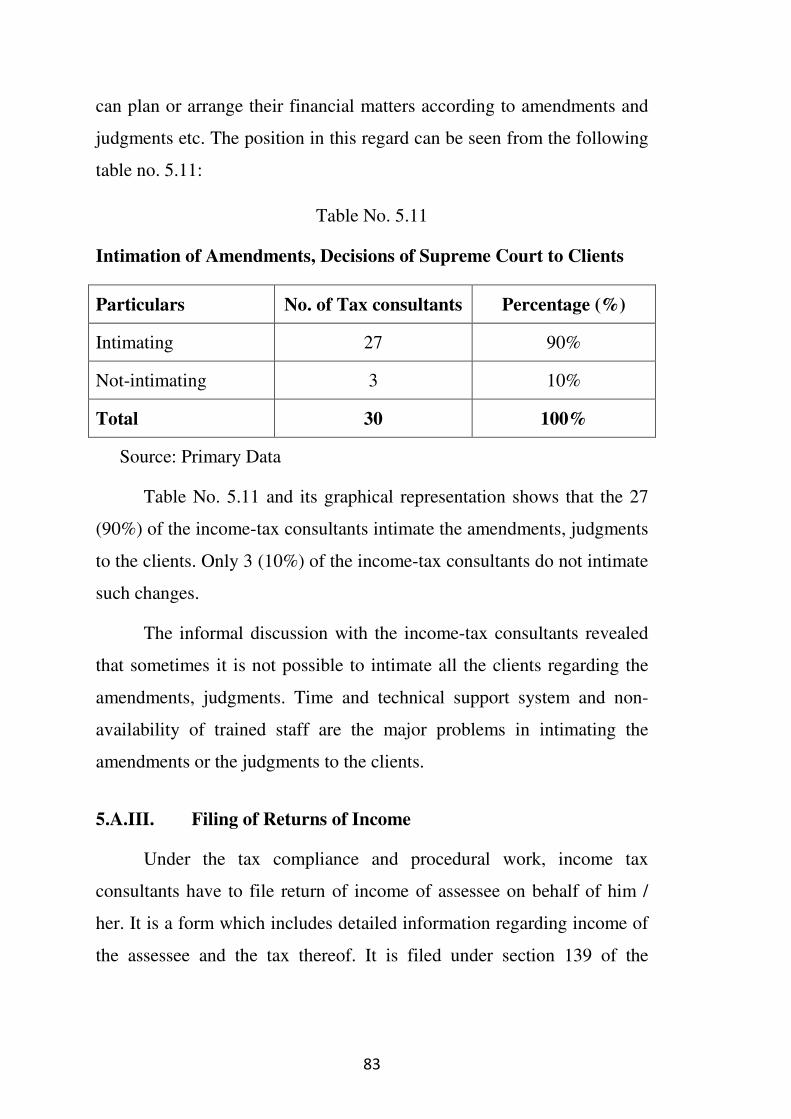

83

can plan or arrange their financial matters according to amendments and

judgments etc. The position in this regard can be seen from the following

table no. 5.11:

Table No. 5.11

Intimation of Amendments, Decisions of Supreme Court to Clients

Particulars No. of Tax consultants Percentage (%)

Intimating 27 90%

Not-intimating 3 10%

Total 30 100%

Source: Primary Data

Table No. 5.11 and its graphical representation shows that the 27

(90%) of the income-tax consultants intimate the amendments, judgments

to the clients. Only 3 (10%) of the income-tax consultants do not intimate

such changes.

The informal discussion with the income-tax consultants revealed

that sometimes it is not possible to intimate all the clients regarding the

amendments, judgments. Time and technical support system and non-

availability of trained staff are the major problems in intimating the

amendments or the judgments to the clients.

5.A.III. Filing of Returns of Income

Under the tax compliance and procedural work, income tax

consultants have to file return of income of assessee on behalf of him /

her. It is a form which includes detailed information regarding income of

the assessee and the tax thereof. It is filed under section 139 of the

84

Income-Tax Act, 1961. All the documentary evidences are required to

attach with it.

5.A.III.(1) Mode of Filing the Returns of Income

Previously returns of income were filed in paper form only. Now-

a-days Online Tax Accounting System has been introduced. It has

made e-filing of returns and e-payment mandatory for the assessees

who are tax audited. In case of other assessees it is on tax consultant to

select the mode for filing the return of income. A study is conducted to

know the mode of filing the return of income selected by different

income-tax consultants. The following table shows the details in this

regard:

Table No. 5.12

Modes of Filing the Return of Income

Particulars No. of Tax consultants Percentage (%)

E-filing 4 13.33%

On paper 3 10%

Both 23 76.67%

Total 30 100%

Source: Primary Data

From the table no.5.12 it can be observed that 4 (i.e. 13.33%)

income-tax consultants use only e-filing mode for filing the returns of

income. On the contrary 3 (i.e. 10%) income-tax consultants file the

returns of income in paper form only. 23 (i.e. 76.67%) income-tax

consultants use both the modes i.e. electronically and in paper form

for filing the returns of income.

85

It is observed that income tax consultants from new generation use

e-filing mode comfortably. On the contrary senior tax consultants are

not so comfortable with such electronic devises. They need to take

help of their assistants in e-filing the returns.

There are some benefits of e-filing of returns of income and some

technical problems too. These benefits and difficulties discussed as:

5.A.III.(2) Benefits of Electronically Filing the Returns of Income

The study is conducted to know the benefits enjoyed by the

income-tax consultants in electronically filing the returns of income. It

is observed by the researcher from the total 27 income-tax consultants

who file the returns of income electronically that the most common

benefit is quick and time saving. It is possible to file return any time

and from any where. Less paper work is required.

The following table shows the details of different benefits enjoyed

by the income-tax consultants:

Table No. 5.13

Benefits of Electronically Filing the Return of Income

Particulars No. of Tax consultants Percentage (%)

Quick-time saving 15 50%

Paperless-Paper saving 10 33.33%

Anytime submission 8 26.67%

Easy automation calculation 7 23.33%

Accurate 6 20%

Money saving 1 3.33%

Source: Primary Data

86

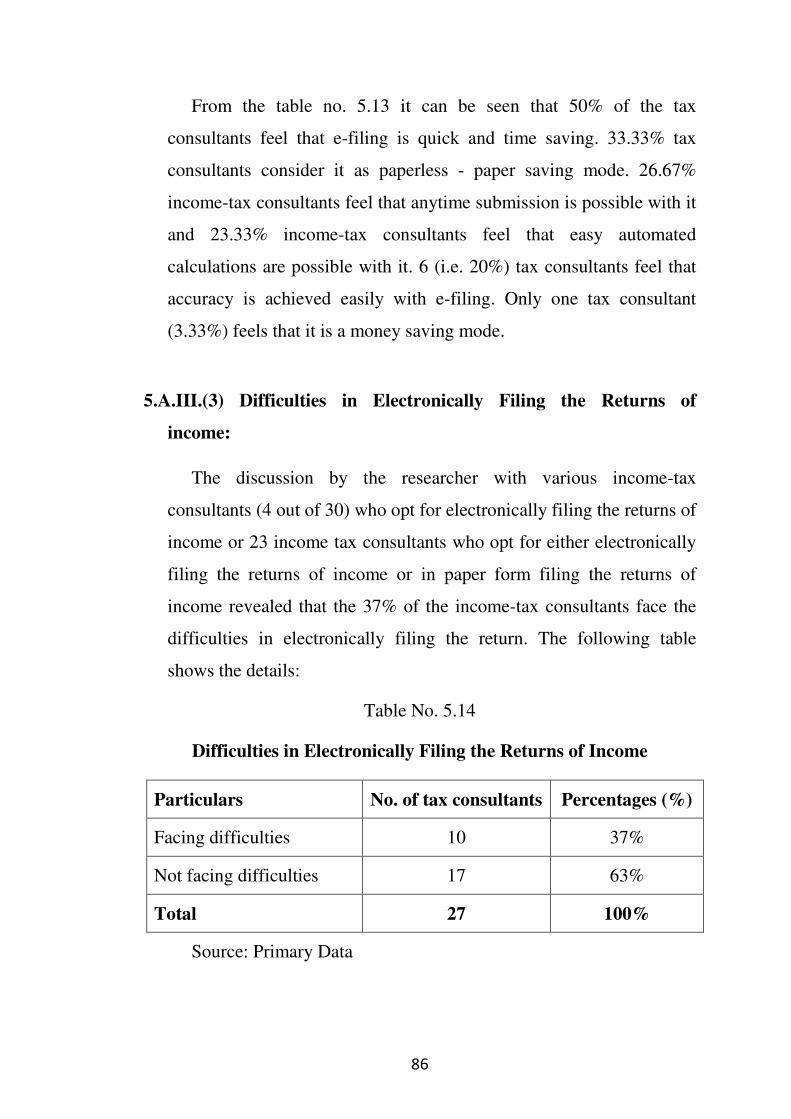

From the table no. 5.13 it can be seen that 50% of the tax

consultants feel that e-filing is quick and time saving. 33.33% tax

consultants consider it as paperless - paper saving mode. 26.67%

income-tax consultants feel that anytime submission is possible with it

and 23.33% income-tax consultants feel that easy automated

calculations are possible with it. 6 (i.e. 20%) tax consultants feel that

accuracy is achieved easily with e-filing. Only one tax consultant

(3.33%) feels that it is a money saving mode.

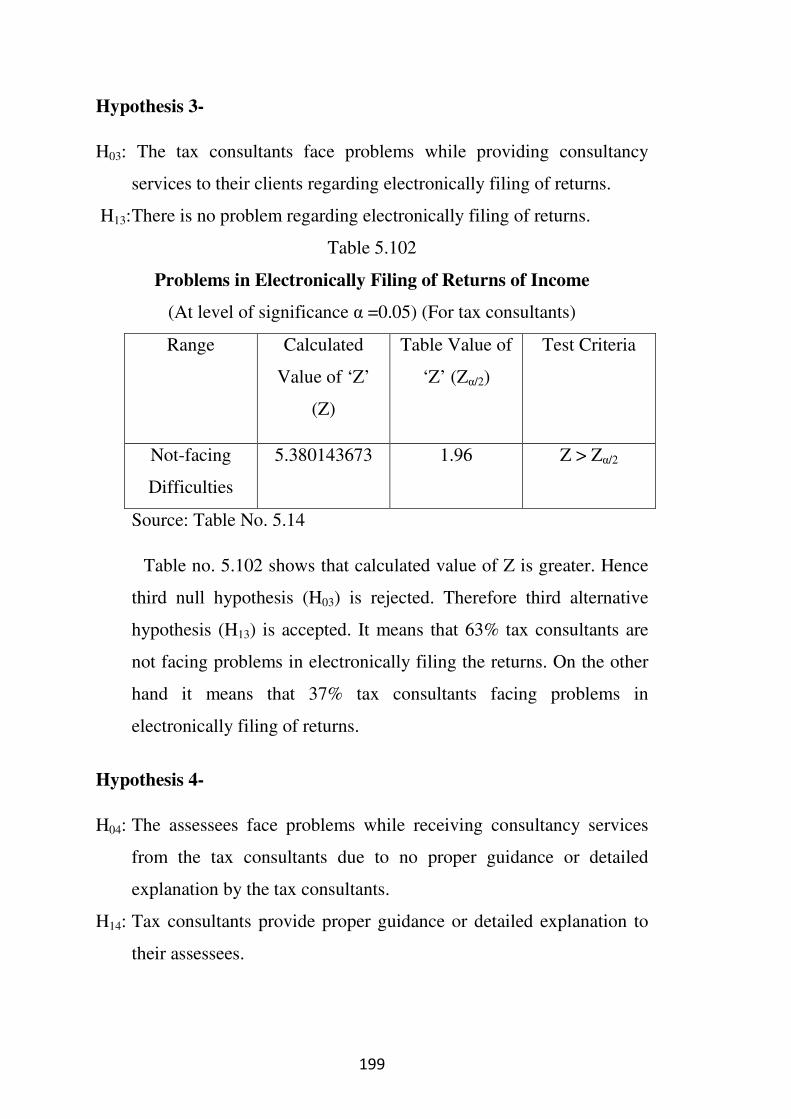

5.A.III.(3) Difficulties in Electronically Filing the Returns of

income:

The discussion by the researcher with various income-tax

consultants (4 out of 30) who opt for electronically filing the returns of

income or 23 income tax consultants who opt for either electronically

filing the returns of income or in paper form filing the returns of

income revealed that the 37% of the income-tax consultants face the

difficulties in electronically filing the return. The following table

shows the details:

Table No. 5.14

Difficulties in Electronically Filing the Returns of Income

Particulars No. of tax consultants Percentages (%)

Facing difficulties 10 37%

Not facing difficulties 17 63%

Total 27 100%

Source: Primary Data

87

Figure 5.6

Difficulties in Electronically Filing the Returns of Income

Not facing

difficulties ,

63%

Facing

difficulties,

37%

From the table no. 5.14 it is clear that 63 % tax consultants have no

problem in e-filing the returns. But e-filing return creates some

technical problems.

In case the return is digitally signed, on successful uploading of e-

Return, ITR-V Form would be generated which needs to be printed by

the tax-payer. This is an acknowledgement. Tax-payer has to fill-up

this ITR-V Form, duly verify and mail to Income-Tax Department,

Bangalore within prescribed time limit by ordinary post only. If

assessee fails to do so, it will deem that the return in respect of which

the Form ITR-V has been failed was never furnished.

Submission of Form ITR-V is not acknowledged by the concerned

office at Bangalore. Therefore tax consultants can not make it sure

whether Form ITR-V submitted is received by the Income-Tax

Department or not. There is also chance of miscarriage of it in transit

or misplacement in the office. This procedure makes the funky

position of income-tax consultant.

88

The other difficulties faced by the income-tax consultants are

summarized as under:

- Electricity failure.

- On-line system failure / site block.

- No access to proper sites.

- Technological knowledge and updating of information.

- No access of data due to server problem.

- The uploading system does not give the list of errors. Returns of

income are accepted with errors.

- Acknowledgements are not received in time.

- Slow working on web-sites.

- No verification of e-payments through cross check.

Further it is observed that the most of the senior income-tax

consultants in this area are not updated with the computer system and

are dependent on the assistants for electronically filing the returns of

income.

5.A.IV Other Difficulties Faced by Income-Tax Consultants

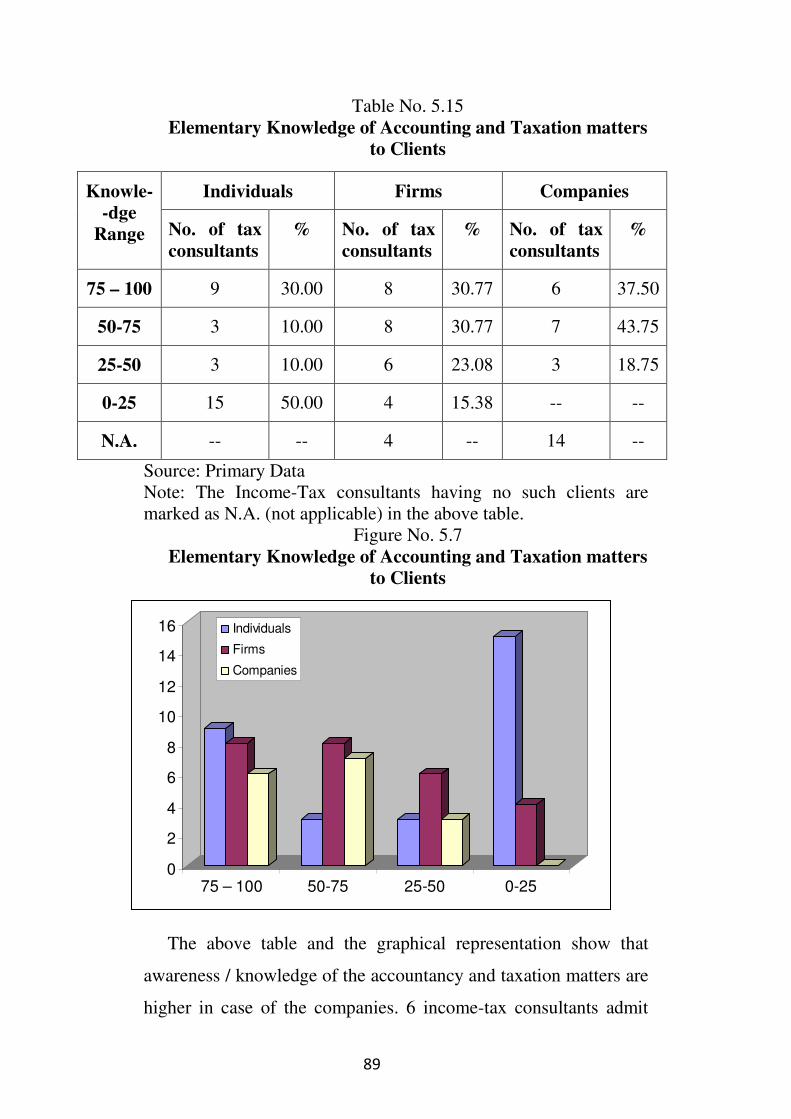

5.A.IV.(1) A study is conducted to assess the overall knowledge of

accountancy and taxation matters to the clients. The study is

restricted only to the individuals, firms and the companies. It is

observed that the knowledge of the accountancy and taxation

matters is higher with companies in the area of research work

followed by firms and then individual assessees. The following

table shows relative opinion of the income-tax consultants about

the awareness / knowledge of the accountancy and taxation matters

to their clients:

89

Table No. 5.15

Elementary Knowledge of Accounting and Taxation matters

to Clients

Individuals Firms Companies Knowle-

-dge

Range No. of tax

consultants

% No. of tax

consultants

% No. of tax

consultants

%

75 – 100 9 30.00 8 30.77 6 37.50

50-75 3 10.00 8 30.77 7 43.75

25-50 3 10.00 6 23.08 3 18.75

0-25 15 50.00 4 15.38 -- --

N.A. -- -- 4 -- 14 --

Source: Primary Data

Note: The Income-Tax consultants having no such clients are

marked as N.A. (not applicable) in the above table.

Figure No. 5.7

Elementary Knowledge of Accounting and Taxation matters

to Clients

0

2

4

6

8

10

12

14

16

75 – 100 50-75 25-50 0-25

Individuals

Firms

Companies

The above table and the graphical representation show that

awareness / knowledge of the accountancy and taxation matters are

higher in case of the companies. 6 income-tax consultants admit

90

that 75-100 % company clients have knowledge of accountancy

and taxation matters. Approximately 31% (8) income-tax

consultants believe that knowledge of the subject is adequate with

partnership firms. The percentage is further lower to 30 % in case

of individuals. 50 % Tax consultants believe that individual

assessees are unaware about accountancy and taxation matter. This

reveals the fact that the awareness / knowledge of the subject

matter are lower with individuals.

Assessees are required to be aware of some tax provisions at

least relating to their business or profession, tax obligations, due

dates regarding tax compliances etc. If they are unaware of this

basic knowledge, it creates problem for tax consultants. In such

cases tax consultants have to call / remind these assessees

frequently.

5.A.IV.(2) Further study is conducted to understand the availability of

the trained staff with the clients. Untrained staff or assessees who

are unaware of book-keeping and accountancy may make errors in

book-keeping or may use wrong methods for book-keeping, etc.

which creates problem in service providing task by tax consultants.

The following table gives the details of clients having trained

staffs:

91

Table No. 5.16

Trained Staff with Assesseess

Individuals Firms Companies Range

No. of tax

consultants

% No. of tax

consultants

% No. of tax

consultants

%

75 – 100 7 23.33 13 50 14 87.5

50 – 75 4 13.33 5 19.23 1 6.25

25 – 50 -- -- -- -- -- --

0 – 25 19 63.33 8 30.77 1 6.25

Total 30 100 26 100 16 100

N.A. 4 14

Source: Primary Data

Note: The income-tax consultants having no such clients are marked

as N.A. (not applicable) in the above table.

Figure No. 5.8

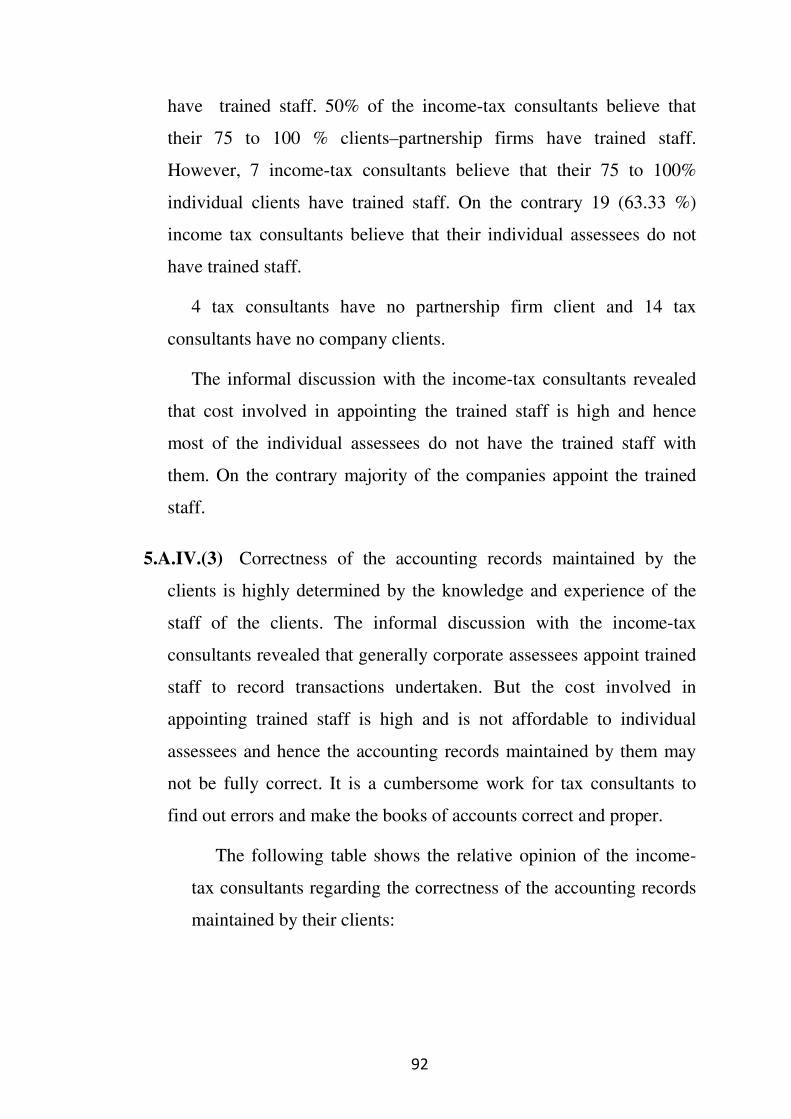

The table no. 5.16 and figure no. 5.8 shows that 14 (ie.87.5%)

income-tax consultants believe that their 75 to 100 % corporate clients

92

have trained staff. 50% of the income-tax consultants believe that

their 75 to 100 % clients–partnership firms have trained staff.

However, 7 income-tax consultants believe that their 75 to 100%

individual clients have trained staff. On the contrary 19 (63.33 %)

income tax consultants believe that their individual assessees do not

have trained staff.

4 tax consultants have no partnership firm client and 14 tax

consultants have no company clients.

The informal discussion with the income-tax consultants revealed

that cost involved in appointing the trained staff is high and hence

most of the individual assessees do not have the trained staff with

them. On the contrary majority of the companies appoint the trained

staff.

5.A.IV.(3) Correctness of the accounting records maintained by the

clients is highly determined by the knowledge and experience of the

staff of the clients. The informal discussion with the income-tax

consultants revealed that generally corporate assessees appoint trained

staff to record transactions undertaken. But the cost involved in

appointing trained staff is high and is not affordable to individual

assessees and hence the accounting records maintained by them may

not be fully correct. It is a cumbersome work for tax consultants to

find out errors and make the books of accounts correct and proper.

The following table shows the relative opinion of the income-

tax consultants regarding the correctness of the accounting records

maintained by their clients:

93

Table No.5.17

Details of Correctness of the Accounting Records

Maintained by the Clients

Individuals Firms Companies Range

No. of tax

consultants

% No. of tax

consultants

% No. of tax

consultants

%

75 – 100 12 40 15 57.70 14 87.5

50 – 75 8 26.67 1 3.85 1 6.25

25 – 50 3 10 4 15.38 -- --

0 – 25 7 23.33 6 23.07 1 6.25

N.A. 4 14

Total 30 100 26 100 16 100

Source: Primary Data

Note: The income-tax consultants having no such clients are marked as

N.A. (not applicable) in the above table

The table no. 5.17 shows that 14 (i.e. 87.5 %) income-tax

consultants believe that the accounting records maintained by their

75-100% corporate clients are correct. 15 (i.e. 57.70 %) income-tax

consultants believe that the accounting records maintained by their

75-100% partnership firm clients, are correct. In case of individual

clients, however, only 40% of the income-tax consultants are

confident of their accounting records.

Table No. 5.17 shows only the most of the corporate clients

have the trained staff and accordingly, the accounting records

maintained by these clients are most correct.

94

PART - B

Different Types of Assessees and Their Difficulties in Getting Tax

Consultancy Services.

As discussed earlier there are seven types of ‘person’. Every

person can become an assessee if he comes under the situation as

mentioned in the definition of assessee. The present study deal with only

three assessees i.e. individual, firm and company. The data collected and

analyzed is grouped under three headings:

I. Individual Assessees

II. Partnership Firm Assessees

III. Company Assessees

5.B.I INDIVIDUAL ASSESSEES

An ‘individual’ means a natural person i.e. human being.

Individual includes a male, female, minor child and insane. The details of

information collected from individual assessees are discussed as under:

5.B.I.(i) Sources of Income

Any economic activity which earns a surplus is a source of income.

The term ‘income’ is discussed earlier. For study purpose all the

income activities can be classified as under:

1. Classification of Income Activities

Under Income-Tax Act all types of income of an assessee is

taxable. As considered to be the income of an individual, there is

variety of economic activities that lead to income which mainly

includes business, profession, employment and vocation. The

95

following table no.5.18 shows the sources of income of individual

assessees under study.

Table No.5.18

Sources of Income

Particulars No. of Individuals Percentage (%)

Business 112 37.33%

Profession 96 32.00%

Employment 71 23.67%

Vocation 21 7.00%

Total 300 100%

Source: Primary Data

Above table shows that out of randomly selected 300

assessees 112 individuals are doing business, the activities mainly

include any trade, commerce or manufacture or any adventure or

concern in the nature of trade, commerce or manufacture.

Percentage of individual assessees engaged in doing business in

selected area, is 37.33%. 96 (32%) individuals are professionals

like doctors, lawyers, auditors, engineers, etc. and are engaged in

the field of professions. 71 (i.e. 23.67%) individuals are employees

serving in government, semi-government and non government

organizations. 21 Individuals are engaged in vocational activities

like, brokerage, insurance agency, music, dancing etc. Percentage

of individual assessees engaged in vocational activities is 7%.

96

Figure No. 5.9

The study of the table no. 5.18 and graphical representation

shows that out of total sample surveyed, majority individual

assessees 208 (69.33%) are dependent on either business or

profession for their income, while rest 30.67 % are dependent

either employment or vocation for their income source analysis

shows highest 112 (37.33%) have shown business income as their

source of income while 96 (32%) showed profession as their

income source. 71 (23.67%) have shown employment and 21 (7%)

shown vocation as their income source.

It’s a good sign for economic development that numbers of

individuals are engaged in business or profession.

2. Income Heads under which Income of Individual

Assessee is Taxable

Under the Income-Tax Act, 1961, the taxable total income is

computed and assessed under five heads viz.

97

• Income from salary

• Income from house property

• Profits and gains from business or profession

• Capital gains

• Income from other sources

Income of an assessee is assessed under that income head which

is his main source of income head when he or she earns income

under more than one head. Accordingly he or she will have to file

his or her return of income in Form 'Saral D' for salary income

while Form No. ITR-4 for profits and gains from business. Income

from remaining heads are computed and assessed under appropriate

heads of income.

Table No.5.19

Income Heads wise Taxability of Assessees

Sr. No. Main Source of Income No. of Individuals

1 Income from salary 71

2 Income from house property 7

3 Profits and gains from business or

profession

208

4 Capital gain 5

5 Income from other sources 9

Source: Primary Data

It is observed that the individual assessees falling under

category ‘Income from Salary’ or profits and gains from business

and profession have other sources of income such as income from

house property, income from other sources and capital gains.

98

The above table shows that 208 (69.33%) assessees’ main

source of income is ‘profit and gain from business and profession’.

71 (23.67%) assessees’ main source of income is ‘salary income’.

Very few i.e. 9, 7 and 5 persons earn income through ‘income from

other sources’, ‘income from house property’ and ‘capital gain’

respectively.

As majority of individuals are engaged in doing business or

profession, their main source of income is ‘profit and gain from

business and profession’. Individuals who are employees earn

income under the head ‘Income from Salary’.

‘Income from other sources’ includes income which is not

exempt from income-tax under the Act and which does not fall

under any other head e.g. interest on bank deposits, dividend

received, winning from lottery etc.

3. Income Range

Every person whose total income exceeds the maximum amount

not liable to the income-tax, shall be taxed under the Income-Tax

Act at the rate or rates prescribed under the Finance Act relevant to

the assessment year, considering his residential status. Such

maximum amount not liable to tax changes every year according to

the provisions in finance bill of each year. This maximum amount

not liable to tax is different for women, men and senior citizens.

Presently the tax rates for A.Y. 2009-10 are as follows:

99

---------------------------------------------------------------------------------

Income Range Slab Rates

---------------------------------------------------------------------------------

Income from NIL to Rs.1,50,000/- NIL

Rs. 1,50,000/- to Rs. 3,00,000/- , 10%

Rs. 3,00,000/- to Rs. 5,00,000/- and 20%

more than Rs. 5,00,000/- 30%

----------------------------------------------------------------------------------

For each slab, percentage of tax is different. Tax is calculated at

the rate applicable to income range of assessee. The following table

No. 5.20 shows income range of the individual assessees under

study.

Table No. 5.20

Income Range

Income Range (Rs.) No. of Individuals Percentage (%)

Less than Rs. 3 lakhs 163 54.33

Rs. 3 lakhs to 5 lakhs 83 27.67

More than Rs. 5 lakhs 54 18.00

Source: Primary Data

100

Figure 5.10

Above table no. 5.20 and its graphical representation shows that

163 (i.e. 54.33%) individual assessees examined fall under the first

income group i.e. who earns income above Rs.1,50,000/- but below

Rs. 3,00,000/-. 83 (i.e. 27.67%) individual assessees are earning

income more than Rs. 3,00,000/- but below Rs. 5,00,000/-.

Remaining 54 (18%) individuals earn income more than Rs.

5,00,000/- .

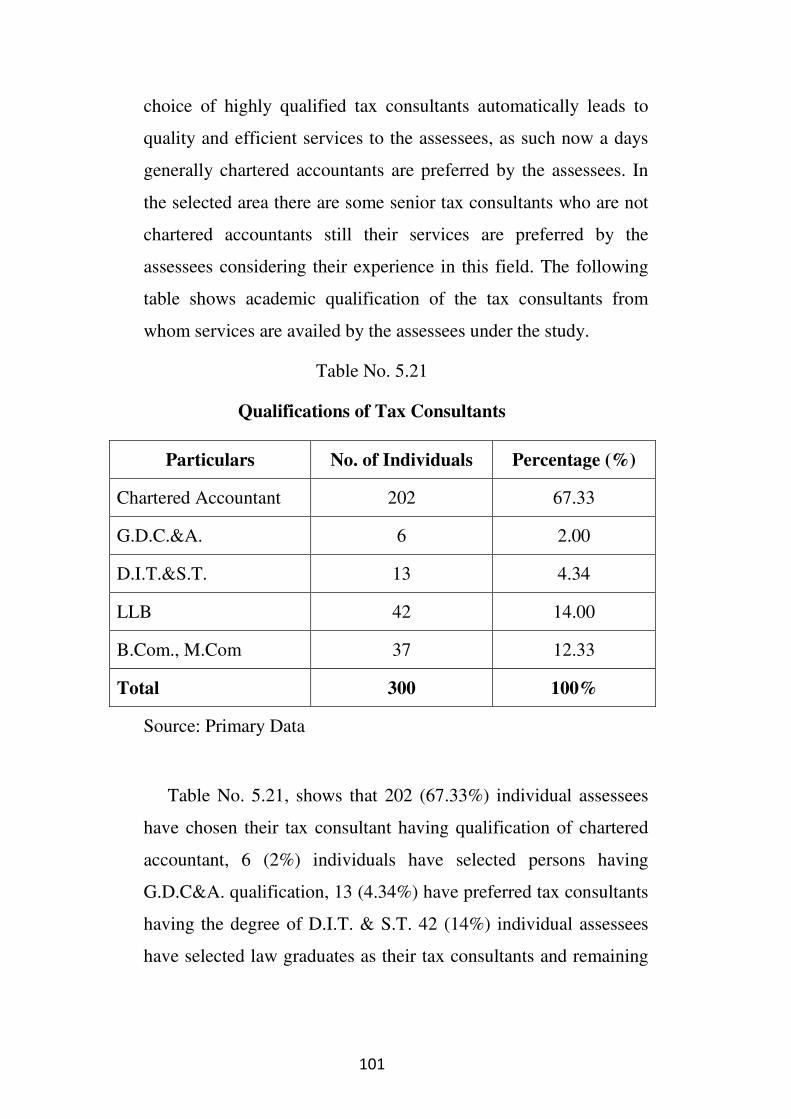

5.B.I.(ii) Qualification and Services Availed from Tax Consultant

1. Qualifications of Tax Consultants

In the early stage of the tax consultancy profession any person

having basic knowledge of taxation, can start tax consultancy

profession. Now-a-days frequent changes in tax laws, amendments

to it and the competition in the profession have lead to acquire

minimum competency in it. As such only graduates from

commerce, law faculty, D.I.T. & S.T, G.D.C. & A. diploma holders

and mostly Chartered Accountants are in the profession. The

101

choice of highly qualified tax consultants automatically leads to

quality and efficient services to the assessees, as such now a days

generally chartered accountants are preferred by the assessees. In

the selected area there are some senior tax consultants who are not

chartered accountants still their services are preferred by the

assessees considering their experience in this field. The following

table shows academic qualification of the tax consultants from

whom services are availed by the assessees under the study.

Table No. 5.21

Qualifications of Tax Consultants

Particulars No. of Individuals Percentage (%)

Chartered Accountant 202 67.33

G.D.C.&A. 6 2.00

D.I.T.&S.T. 13 4.34

LLB 42 14.00

B.Com., M.Com 37 12.33

Total 300 100%

Source: Primary Data

Table No. 5.21, shows that 202 (67.33%) individual assessees

have chosen their tax consultant having qualification of chartered

accountant, 6 (2%) individuals have selected persons having

G.D.C&A. qualification, 13 (4.34%) have preferred tax consultants

having the degree of D.I.T. & S.T. 42 (14%) individual assessees

have selected law graduates as their tax consultants and remaining

102

37 (i.e. 12.33%) individual assessees have selected B.Com.,

M.Com. degree holders as their tax consultants.

Majority of the individual assessees have selected C.A.s as their

tax consultants as they can provide maximum tax services at single

window. The degree of chartered accountant from Institute of

Chartered Accountants of India is itself a landmark in this

profession.

This can be presented graphically as under.

Figure No. 5.11

2. Services Availed

The services that can be demanded by the individual assessees

from their tax consultants can be divided in to two i.e. i) Taxation

services and Non-tax (allied) services, which are as follows.

103

Table No. 5.22

Availing of Different Types of Services

Taxation Services No. of Individuals Percentage (%)

Taxation Services 300 100

Allied Services 91 30.33

Source: Primary Data

Individual assessees avail only taxation services from tax

consultants. Small traders, professionals, vocational etc. generally

avail both types of services i.e. tax services for all types of taxes

and non-tax services like book-keeping, various types of audits,

consultancy services regarding profit maximization, cost control

etc.

a. Taxation Services

Each and every assessee tries to minimize his/her tax burden by

proper tax planning, as such they demand tax planning services

from their tax consultants. The tax planning tries to ensure that the

tax liability borne is (within the frame-work of law of course)

minimum. Other service provided by tax consultants is the tax

compliance and procedural work which aims at making sure that all

necessary forms and payments are appropriately submitted. This

service saves the client from lot of headache and helps to make the

whole ‘deal’ more attractive to the client.

The individual assessees avail mostly income-tax consultancy

services from income-tax consultants but some assessees may avail

104

consultancy services for other taxes too. These taxes include VAT,

Service tax, Central Excise, Customs duty etc.

The following table shows the number of individual assessees

availing different services provided by the tax consultants.

Table No.5.23

Taxation Services Availed

Particulars No. of Individuals Percentage (%)

Tax issues

Income-Tax 300 100

Value added Tax 40 13.33

Service Tax 11 3.37

Central Excise 3 1

Custom Duty 3 1

Tax Planning 282 94

Tax Compliances &

procedural work

296 98.67

Source: Primary Data

Above table shows that all (100%) individual assessees avail the

services of income-tax issues, 282 (94%) individual assessees avail

tax planning service and 296 individual assessees avail the service

of tax compliances and procedural work from income-tax

consultants. Apart from the core areas of income-tax consultancy

services, approximately 13.33% and 3.67% of the individual

assessees avail the Value Added Tax consultancy and Service Tax

consultancy services respectively. VAT is paid on inter-state sale

or purchase of goods and Service Tax is paid on services provided,

105

covered under the Finance Act. Other taxation services of Central

Excise and Customs are availed by 3 (1%) individual assessees.

Central Excise Duty is paid on manufacturing of goods and

Custom Duty is paid on import and export of goods. Only 1% of

the individual assessees avail these services.

b. Allied Services

Along with taxation services, assessees avail services like

book-keeping services, cost accounting services, internal audit,

management consultancy and financial consultancy services etc.

from tax consultants. For study purpose these services are grouped

under the heading ‘allied services’. Table No. 5.24 provides the

data in this regard.

Table No. 5.24

Allied Services Availed

No. of Individuals

Services Availed

services

(%) Not availed

services

(%)

Book-keeping 21 7% 279 93%

Cost Accountancy 3 1% 297 99%

Audit 14 4.67% 286 95.33%

Consultancy services 53 17.67% 247 82.33%

Source: Primary Data

106

Figure No. 5.12

Allied Services Availed

The above table 5.24 and figure no. 5.12 depicts that only 21 i.e. 7

% individual assessees avail book-keeping services while 279 i.e. 93%

individual assessees are maintaining required books of accounts

themselves. Only 1% individual assessees avail cost accountancy

services. 286 i.e. 95.33% assessees get their accounts audited from

their tax consultants. 82.33 % assessees avail consultancy services too.

The audit and consultancy services are varied in nature. The following

data clears the picture in this regard.

� Audit

Audit is a systematic examination of books of accounts and records

carried on in order to ascertain whether the financial statements give

true and fair view of the financial position as at the year end and of the

financial results for that year. Tax audit is mandatory for the assessees

having business turnover in excess of Rs.40,00,000/- (for A.Y.2011-

12 Rs.60,00,000/- ) or gross receipts from profession in excess of Rs.

10,00,000/- (for A.Y. 2011-12 Rs.12,00,000/-). VAT audits are

107

mandatory in cases of sales in excess of Rs. 40,00,000/-. The

following table explains the different types of audits conducted by the

individual assessees.

Table No. 5.25

Auditing Services Availed

Particulars No. of Individuals Percentage (%)

Cost Audit --- ---

Tax Audit 1 0.33

VAT Audit --- ---

Internal Audit 8 2.67

Financial Audit 2 0.67

Environmental Audit --- ---

Information System Audit 3 1

Total 14 4.67

Source: Primary Data

The above table shows that out of 14 (4.67%) assessees availed audit

services, 8 (2.67%) assessees availed internal audit service, 3 (1%)

information system audit, 2 (0.67%) financial audit and 1 (0.33%) tax

audit services respectively from their tax consultant. Generally

manufacturing companies requires ‘cost audit’. None of the individual

assessees availed cost audit service.

� Consultancy Services

Individual assessees also avail the consultancy services from their

tax consultants. Such consultancy includes management accountancy,

project planning and financing, project improvement or turnaround

studies, arrangement for the sources of finance, etc. The following table

illustrates the different types of consultancy services availed by the

individual assessees.

108

Table No. 5.26

Consultancy Services Availed

Particulars No. of Individuals Percentage (%)

Management Accountancy 4 1.33%

Project Planning & Finance 17 5.67%

Project improvement or

turnaround studies

5 1.67%

Arrangement for the sources of

finance

27 9%

Total 53 17.67%

Source: Primary Data

The above table shows that out of total 53 assessees availing

consultancy services maximum 27 (9%) assessees availed financial

services, 17 (5.67%) project planning services, 5 (1.67%) project

improvement services and 4 (1.33%) management accountancy

services.

3.Behavior of Staff

General behavior of staff of the income-tax consultants is

polite with the clients. They are courteous and helpful to clients.

They avoid behave rudely with them. The details in this regard are

as follows:

109

Table No. 5.27

Behavior of staff

Particulars No. of Individuals Percentage (%)

Polite 144 48%

Co-operative / Helpful 143 47.67%

Non-cooperative 10 3.33%

Irresponsible 2 0.67%

Rude 1 0.33%

Total 300 100%

Source: Primary Data

From the table no. 5.27 it can be observed that 144 (48%)

individual assessees stated that behavior of the staff of the tax

consultants is polite, 143 (47.67%) individual assessees stated that

its co-operative while 10 (3.33%) individuals stated that staff of tax

consultants are non-cooperative. 2 (.67%) individual assessees

complained that they are irresponsible and 1 (0.33%) individual

assessee complained that they are rude.

4. Timely Notification of amendments, decisions of Supreme

court etc. by Income-Tax consultants

Every year budget proposals in the form of finance bill are

presented to Parliament for consideration and approval. When the

bill is passed by the Parliament and the President of India gives his

/ her consent, it becomes Finance Act of the Financial Year. The

respective provisions of Income-Tax Act are also change with

changes in the Finance Act of the year.

110

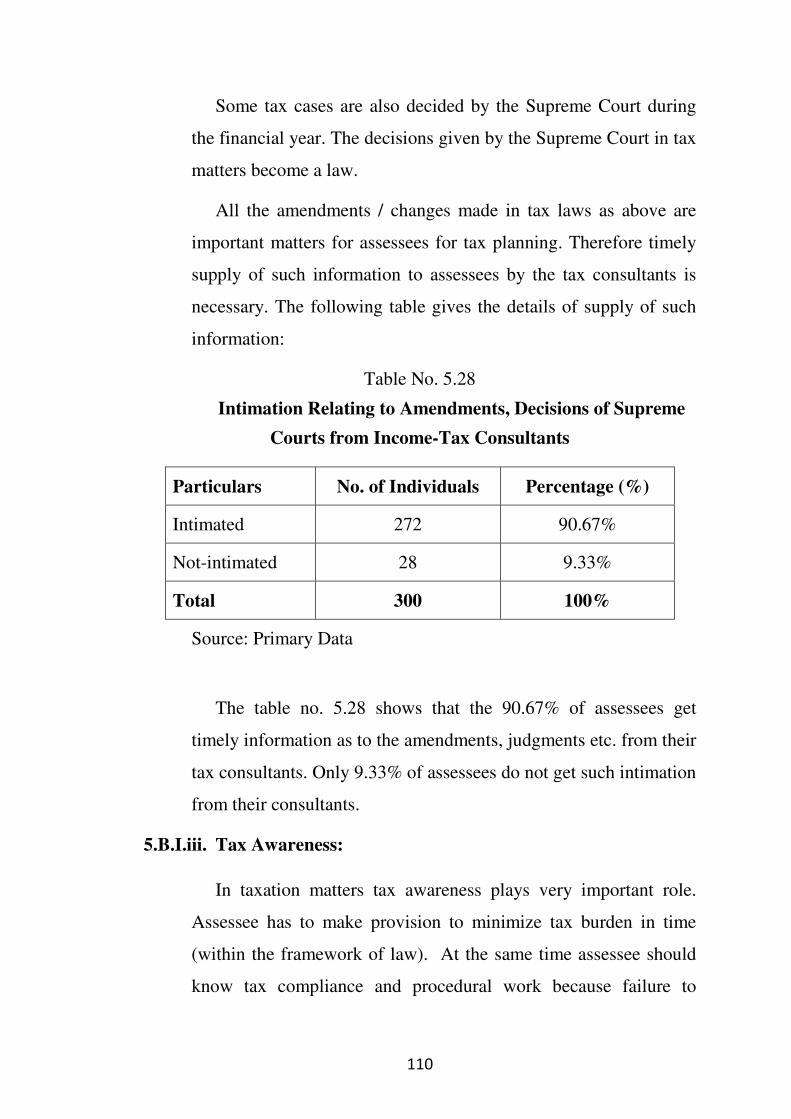

Some tax cases are also decided by the Supreme Court during

the financial year. The decisions given by the Supreme Court in tax

matters become a law.

All the amendments / changes made in tax laws as above are

important matters for assessees for tax planning. Therefore timely

supply of such information to assessees by the tax consultants is

necessary. The following table gives the details of supply of such

information:

Table No. 5.28

Intimation Relating to Amendments, Decisions of Supreme

Courts from Income-Tax Consultants

Particulars No. of Individuals Percentage (%)

Intimated 272 90.67%

Not-intimated 28 9.33%

Total 300 100%

Source: Primary Data

The table no. 5.28 shows that the 90.67% of assessees get

timely information as to the amendments, judgments etc. from their

tax consultants. Only 9.33% of assessees do not get such intimation

from their consultants.

5.B.I.iii. Tax Awareness:

In taxation matters tax awareness plays very important role.

Assessee has to make provision to minimize tax burden in time

(within the framework of law). At the same time assessee should

know tax compliance and procedural work because failure to

111

comply with the statutory provisions of the Act attracts some kind

of penalties.

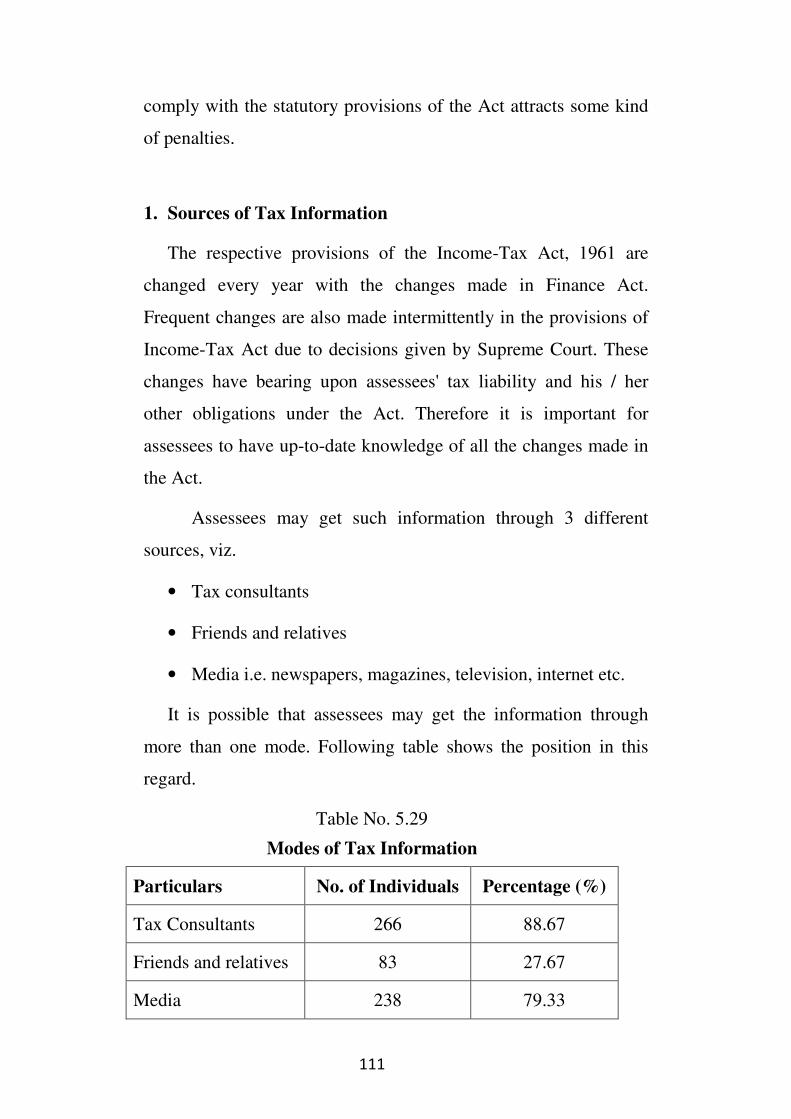

1. Sources of Tax Information

The respective provisions of the Income-Tax Act, 1961 are

changed every year with the changes made in Finance Act.

Frequent changes are also made intermittently in the provisions of

Income-Tax Act due to decisions given by Supreme Court. These

changes have bearing upon assessees' tax liability and his / her

other obligations under the Act. Therefore it is important for

assessees to have up-to-date knowledge of all the changes made in

the Act.

Assessees may get such information through 3 different

sources, viz.

• Tax consultants

• Friends and relatives

• Media i.e. newspapers, magazines, television, internet etc.

It is possible that assessees may get the information through

more than one mode. Following table shows the position in this

regard.

Table No. 5.29

Modes of Tax Information

Particulars No. of Individuals Percentage (%)

Tax Consultants 266 88.67

Friends and relatives 83 27.67

Media 238 79.33

112

Source: Primary Data

The assessees generally use multiple sources for getting tax

information. They consult their tax consultants. Media also

provides such information through news, advertisement in

newspapers, articles in ‘taxation and commerce’ journals,

advertisement and discussions on television channels etc. The

friends, relatives also provide such information to each other. The

table no. 5.29 shows that maximum assessees 266 (88.67%) got the

information from tax consultants and also 238 (79.33%) from

media. Only 83 (27.67%) assessees got the information through

friends and relatives. Majority of them used multiple sources for

the purpose.

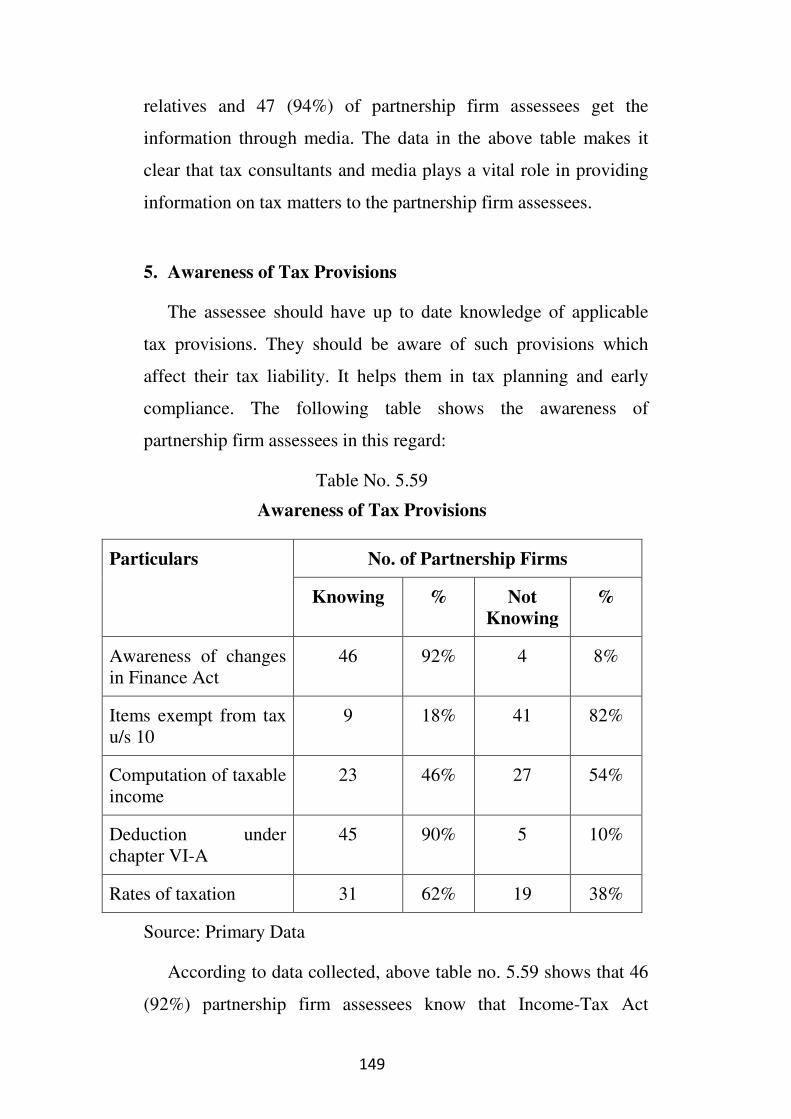

2. Awareness of Tax Provisions

For minimizing tax burden and taking benefit of the changing

provisions, clauses of Income-Tax Act, the assessee must be aware

about it. Generally the provisions regarding incomes exempted

from tax, clubbing of income, various deductions allowed from

income, tax rates, change in minimum taxable income etc.,

assessee must know for his benefit. Assessees’ awareness in this

regard can be seen from following table:

113

Table No. 5.30

Awareness of Tax Provisions

No. of Individuals Particulars

Knowing

Provisions

% not-knowing

Provisions

%

Awareness of changes in

Finance Act

275 91.67 25 8.33

Items exempt from tax 75 25 225 75

Computation of taxable

income

196 65.33 104 34.67

Clubbing of income 54 18 246 82

Deduction under chapter

VI-A

199 66.33 101 33.67

Charging procedure of

Income-Tax

232 77.33 68 22.67

Rates of taxation 235 78.33 65 21.67

Source: Primary Data

According to data collected, table no. 5.30 shows that 275

(91.67%) individual assessees know that Income-Tax Act

undergoes changes every year with the changes in Finance Act.

Remaining 25 (8.33%) assessees are unaware of changes in

Finance Act and impact of it on their tax liability.

75 (25%) individual assessees know various items exempt from

tax under section 10. In this category some assessees are advocates

and some are professors of commerce faculty. 225 (75%)

individual assessees are ignorant about it.

114

Assessees have tendency to minimize their tax liability. If they

can reduce their tax liability, even by Re. 1/-, they try to minimize.

For that purpose they are interested in knowing the computation of

taxable income. They try to verify whether the tax consultants have

computed their taxable income properly or not. Above table no.

5.30 indicates that 196 (65.33%) individual assessees are aware of

computation of taxable income and 104(34.67%) assessees are

unaware.

Sections from 60 to 65 of the Income-Tax Act, 1961 are the

sections dealing with the provisions of clubbing of income of

another person with the income of assessee. If there is a case of

transfer of income of the property without the transfer of asset to

another person receiving the income, the income of transferee is

clubbed with the income of the transferor. Only 54 (18%)

individual assessees know these provisions of clubbing of income.

Other 246 (82%) assessees are unaware of these provisions. On the

contrary, they are under wrong impression and ask the question,"

Why should I pay tax on income of other person?" However under

the following cases clubbing of income provisions of the Act are

attracted:

i. Transfer of income where there is no transfer of asset

ii. Revocable transfer of asset

iii. Remuneration of spouse from a concern in which the other

spouse has substantial interest

iv. Income of asset transferred to the spouse

v. Income from asset transferred to son's wife

vi. Income of a minor child etc.

115

These are some examples where income of another person is to

be clubbed with the total income of assessees.

The aggregate of income computed under each head after giving

effect to the provisions of clubbing of income and set off of losses

is known as "gross total income". In computing the total income of

an assessee certain deductions from Gross Total Income are

permissible (under chapter VI-A) under sections 80 C to 80 U of

Income-Tax Act, 1961. The table no. 5.30 shows 199 (66.33%)

individual assessees know these deductions and 101 (33.67%) are

unaware of these provisions.

Without the authority of law, tax can not be levied and collected

in India. Section 4 of Income-Tax Act gives such authority to levy

and collect income-tax. It is a charging section. Where any Central

Act enacts that income-tax shall be charged for any assessment

year at any rate or rates, income-tax at that rate or those rates shall

be charged for that year, in accordance with and subject to the

provisions (including provisions for the levy of additional income-

tax) of this Act, in respect of the total income of the previous year

of every person. The base for levy of tax in any assessment is

normally the income of previous year. However, in some cases,

income-tax may be charged in respect of the income of a period

other than the previous year. Though the income of the previous

year is assessed in the relevant assessment year and tax is levied,

the tax is deducted at source or paid in advance wherever it is

deductible or payable.

As the table no. 5.30 shows that 232 (77.33%) individual

assessees are aware of charging of income-tax and other 68

(22.67%) assessees don't.

116

On total income, tax is calculated according to the rates

prescribed under the relevant Finance Act. Rates of income-tax are

different for female assessees and senior citizen. According to

above table, it is clear that 235 (78.33%) individual assessees know

these rates of income-tax and 65 (21.67%) assessees have no

knowledge of these rates of income-tax.

It is observed that some assessees try to know each and every

provision relating to calculation of their income and all the details

about calculations made by tax consultants, on the other hand some

assessees blindly signs the returns of income filled by the tax

consultants.

3. Discussion of Annual Budget

Annual Budget presented in the Parliament contains various tax

proposals. Some of the proposals may be relating to the individual

assessees. It is expected that the assessee should study these

proposals. It helps them in tax planning. Generally they alone are

unable to understand these provisions. In this matter tax

consultants guide them properly and explain provisions in detail, if

assessees discuss with them.

Table No. 5.31

Discussion of Annual Budget

Particulars No. of

Individuals

Percentage

Discussion with Tax consultants 90 30%

No discussion with tax consultants 210 70%

Total 300 100%

Source: Primary Data

117

Above table no. 5.31 shows that 90(30%) individual

assessees discuss the annual budget provisions with the tax

consultants before hand. And 210 (70%) individuals don't hold

such discussions regarding provisions of annual budget with tax

consultant, but they explained that whenever they do so, their tax

consultants help them in understanding such provisions. But they

do not explain until assessees ask.

In personal interview it is observed that majority of

individuals (out of 70% who don’t hold discussions regarding

annual budget provisions) believe that it is very difficult task to

understand such provisions and so that they have entrusted this

work to their tax consultant.

5.B.I.iv Filing of Return of Income

As per the Income-Tax Act, 1961, an individual if his total

income or total income of any other person in respect of which he

is assessable under the Income-Tax Act, during the previous year

exceeds the maximum amount not liable to income-tax, have to

furnish a return of his income or the income of such other person. It

is mandatory. The details in this regard are as under:

1. First Return of Income:

Though the Income-Tax Act provisions compile the person

whose income is taxable to file his return of income, it is observed

that the first return of income is generally filed by assessees to

claim refund of Tax Deducted at Source (TDS), to carry forward

loss, to provide copy of return of income to the financial

institutions or banks etc. Very few individuals file return of income

118

voluntarily on their own accrual. Table no.5.31 shows the position

in this regard:

Table No. 5.32

First Return of Income

Particulars No. of Individuals Percentage (%)

Regular provision 275 91.67

Refund claim 22 7.33

Voluntary 3 1.00

Source: Primary Data

The table no. 5.32 shows that, 275 (91.67%) individual

assessees filed their first return of income for fulfillment of regular

provisions of Income-Tax Act, 1961. It means their income

exceeds the maximum limit of income which is not liable to tax or

they have losses to carry forward or they have to provide copy of

return of income to the financial institutions or banks etc. 22

(7.33%) individual assessees have filed their first return of income

for refund purpose. It means their amounts are deducted at sources

for tax but they are not liable to pay tax. So to get back these

amounts they have filed returns. 3 (1%) individual assessees have

filed returns voluntarily without any reason.

2. Preparation for Filing of Returns of Income

In case of individual assessees, the return of income must be

filed in a prescribed form or by specified computer readable media

and verified in the prescribed manner, on or before 31st July of the

assessment year. Each and every assessee starts preparation as to

119

completing of accounts, getting necessary certificates, collection of

documents to be attached to the returns etc. The preparation period

varies according to the assessee. Early preparation avoids many

difficulties and inconvenience at the point of filing up of returns.

The assessees studied shows following position in this regard.

Table No. 5.33

Preparation for Filing of Returns of Income

Particulars No. of Individuals Percentage (%)

1 month before due date 241 80.33

1 week before due date 40 13.33

2-3 days before due date 14 4.67

After due date 5 1.67

Total 300 100

Source: Primary Data

The table no. 5.33 table indicates that 241 (80.33%) individual

assessees are punctual in filing of returns of their income. They

start preparation 1 month before due date. They fulfill all tax

obligations, collect required documents and approach to their tax

consultants for further process. As they get sufficient time for

compliance the percentage of mistakes in returns of income filed

by them is lesser.

40 individuals do prepare for filing the return within 1 week just

before due date i.e. 31st July of the assessment year. This time

period is still sufficient for salaried individuals or individual

assessees requiring less documents to attach with return of income.

120

14 (i.e. 4.67%) individual assessees start preparatory work just

2-3 days before 31st July of the assessment year. As the period for

preparation is very short and the chances of mistakes in their

returns of income are more.

5 individual assessees wake up after 31st July. They are

penalized. However, as per sec.271F, the Assessing Officer may

waive the penalty on proving reasonable grounds for delay in filing

the return of income. Interest u/s 234A/B/C is however, mandatory

and can not be waived.

3. Time Lag for Filing of Returns after Documentation

Tax consultants demand required documents to file the return of

income of the assessee. When assessee provides such required

documents the tax consultants start preparing his return, for the

purpose some time lag is required to him. The minimum time lag in

filling the return is the sign of efficient service. The time lag taken

by the tax consultants after receiving documents in filling up

returns in the cases under study are:

Table No. 5.34

Time Lag for Filing of Returns after Documentation

Particulars No. of Individuals Percentage (%)

Within 1 day 17 5.67

Within a week 208 69.33

Within a month 71 23.67

More than a month 4 1.33

Total 300 100

Source: Primary Data

121

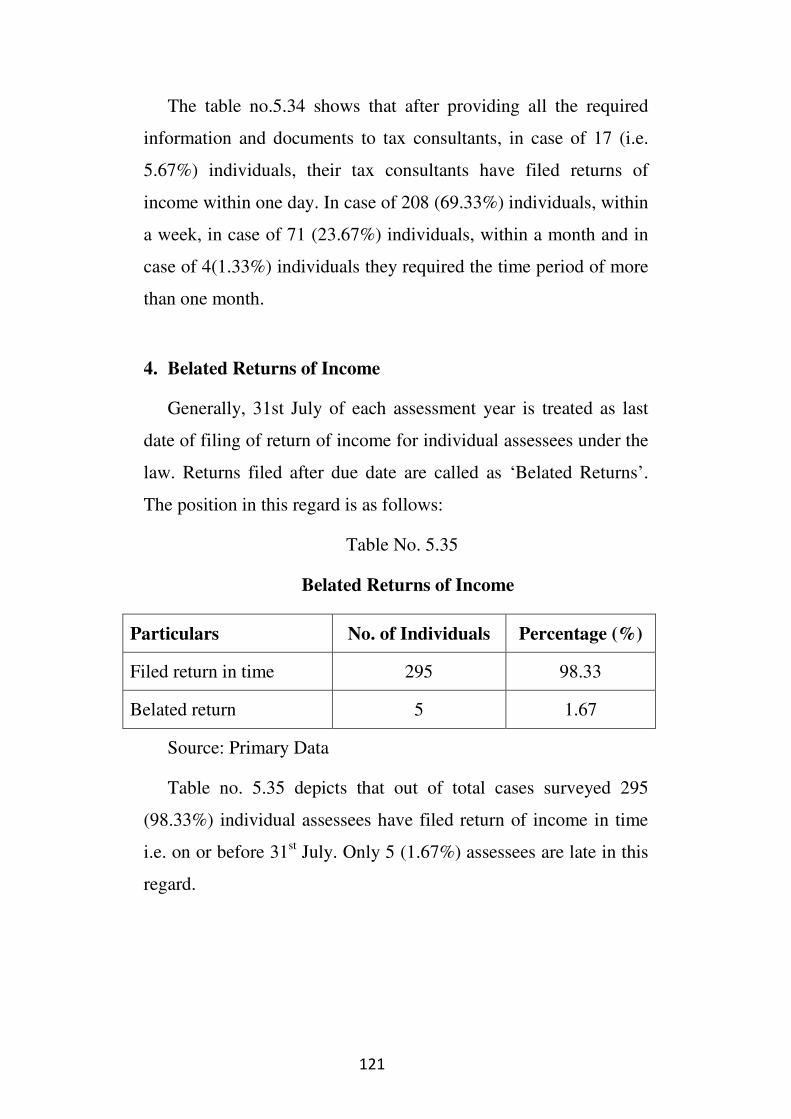

The table no.5.34 shows that after providing all the required

information and documents to tax consultants, in case of 17 (i.e.

5.67%) individuals, their tax consultants have filed returns of

income within one day. In case of 208 (69.33%) individuals, within

a week, in case of 71 (23.67%) individuals, within a month and in

case of 4(1.33%) individuals they required the time period of more

than one month.

4. Belated Returns of Income

Generally, 31st July of each assessment year is treated as last

date of filing of return of income for individual assessees under the

law. Returns filed after due date are called as ‘Belated Returns’.

The position in this regard is as follows:

Table No. 5.35

Belated Returns of Income

Particulars No. of Individuals Percentage (%)

Filed return in time 295 98.33

Belated return 5 1.67

Source: Primary Data

Table no. 5.35 depicts that out of total cases surveyed 295

(98.33%) individual assessees have filed return of income in time

i.e. on or before 31st July. Only 5 (1.67%) assessees are late in this

regard.

122

5. Penalization for Delay

According to sec.271F of Income Tax Act, if a person who is

required to furnish a return of his income, as required u/s 139(1)

or by the provisions to that sub-section, fails to furnish such

return of income before the end of the relevant assessment year,

the Assessing Officer may direct such person shall pay, by way

of penalty. 5 individuals have failed to file returns before due

date. Details of penalty levied to them are as under:

Table No. 5.36

Penalization for Delay

Particulars No. of Individuals Percentage (%)

Fined for late submission 5 100

Not fined for late --- ---

Source: Primary Data

Above table no. 5.36 indicates that 5 individuals who failed to

file return on or before due date are penalized. It means all the

individuals who are late in filing return of income are penalized.

6. Responsibility for Delay

For delay of filing return either assessees or tax consultants

remain responsible. On the part of assessee such delay arises due to

non-submission of documents in time, non- payment of advance

tax etc. while reasons arise on the part of tax consultants are work

pressure, omission etc. Some other reasons of offices remaining

closed on due date or other uncontrollable reasons arise.

123

Table No. 5.37

Responsibility for Delay

Particulars No. of Individuals Percentage (%)

Assessee himself 2 40

Income-Tax consultant 2 40

Other reasons 1 20

Total 5 100

Source: Primary Data

Figure No. 5.13

Responsibility for Delay

Out of 5 individual assessees who have filed belated returns of

income, 2 individuals considered themselves responsible for such

delay. 2 individuals (40%) hold tax consultants responsible for

such delay. Only 1(20%) individual assessee considered some

technical matters responsible for late filing of return of income.

124

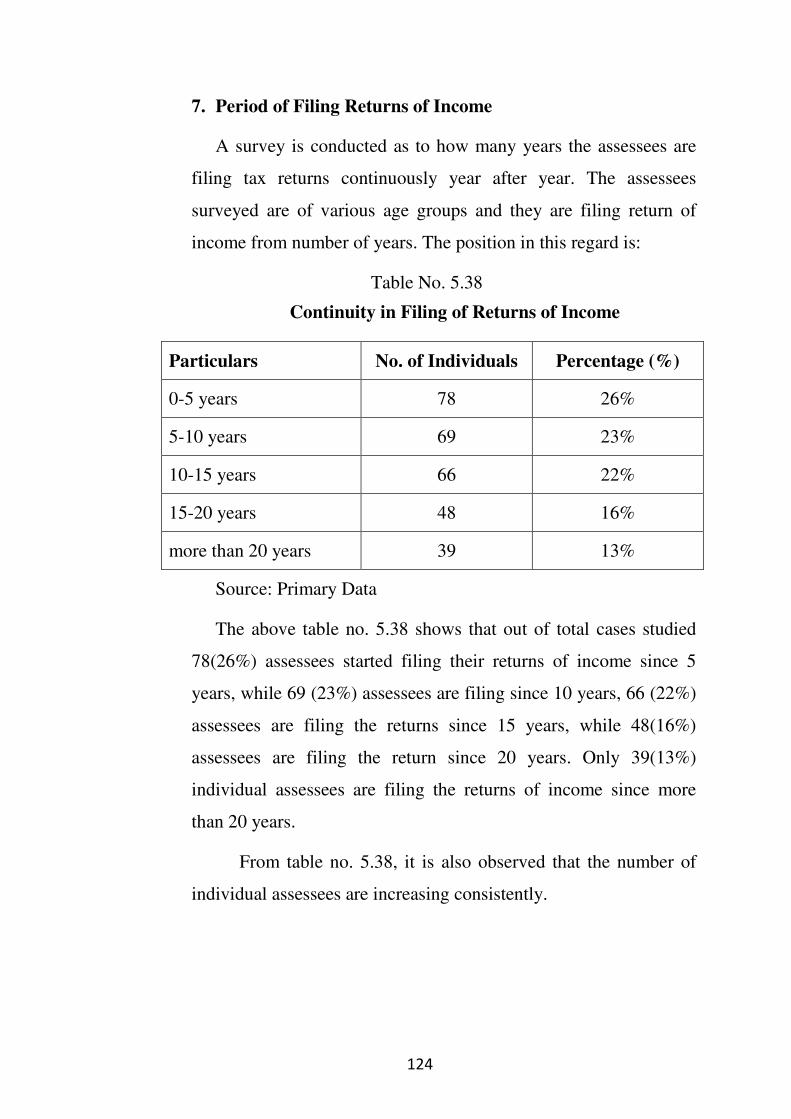

7. Period of Filing Returns of Income

A survey is conducted as to how many years the assessees are

filing tax returns continuously year after year. The assessees

surveyed are of various age groups and they are filing return of

income from number of years. The position in this regard is:

Table No. 5.38

Continuity in Filing of Returns of Income

Particulars No. of Individuals Percentage (%)

0-5 years 78 26%

5-10 years 69 23%

10-15 years 66 22%

15-20 years 48 16%

more than 20 years 39 13%

Source: Primary Data

The above table no. 5.38 shows that out of total cases studied

78(26%) assessees started filing their returns of income since 5

years, while 69 (23%) assessees are filing since 10 years, 66 (22%)

assessees are filing the returns since 15 years, while 48(16%)

assessees are filing the return since 20 years. Only 39(13%)

individual assessees are filing the returns of income since more

than 20 years.

From table no. 5.38, it is also observed that the number of

individual assessees are increasing consistently.

125

5.B.I.v. Change of Income-Tax Consultant

1. Change of Income-Tax Consultant

Generally amount of income earned by one is very personal

thing for him. So assessees try to keep their earnings confidential.

For the same they select their tax consultant very carefully and

hardly change tax consultant. But due to some reasons assessees

may change their tax consultants. Following table no. 5.39 gives

information in this regard.

Table No. 5.39

Change of Income-Tax Consultant

Particulars No of Individuals Percentage (%)

Changed tax consultant 10 3.33%

Not changed tax consultant 290 96.67%

Total 300 100%

Source: Primary Data

Above table shows that only 10 i.e. 3.33% assessees have

changed their tax consultant.

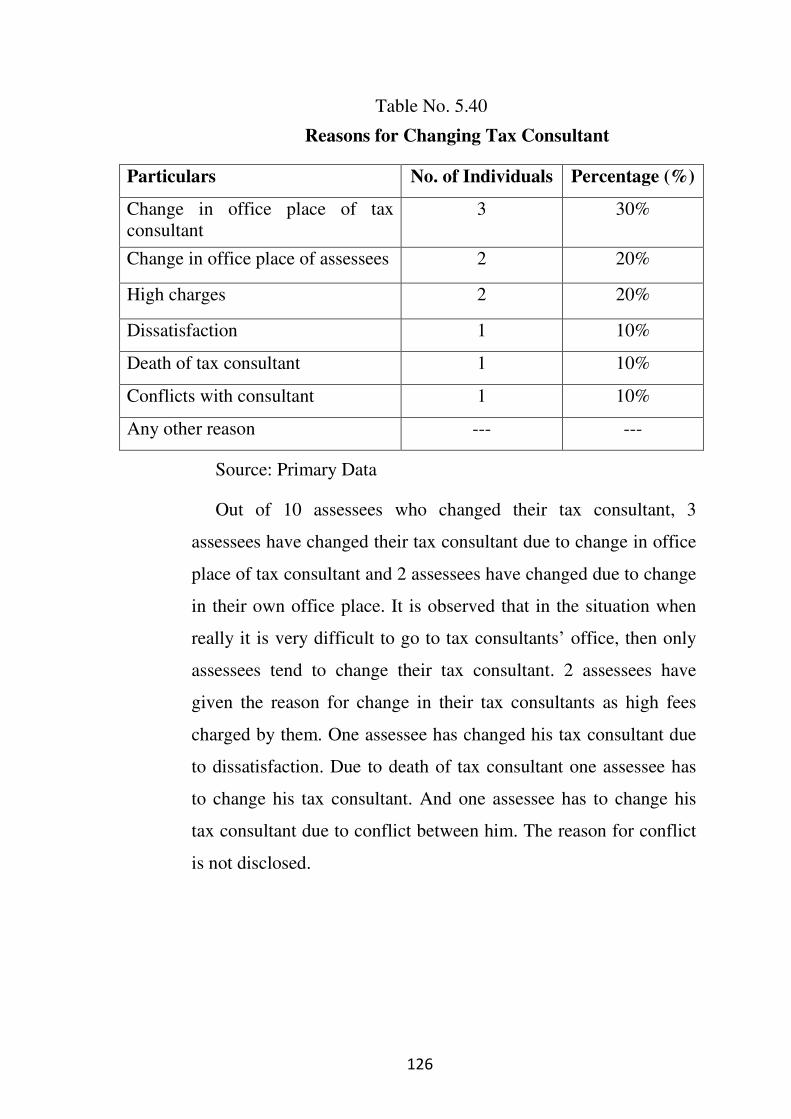

2. Reasons for Changing Tax Consultant

As discussed above, assessees are very particular about their tax

consultant. But due to some reasons it happens that they have to

change their tax consultants. These reasons and the details are

discussed as under.

126

Table No. 5.40

Reasons for Changing Tax Consultant

Particulars No. of Individuals Percentage (%)

Change in office place of tax

consultant

3 30%

Change in office place of assessees 2 20%

High charges 2 20%

Dissatisfaction 1 10%

Death of tax consultant 1 10%

Conflicts with consultant 1 10%

Any other reason --- ---

Source: Primary Data

Out of 10 assessees who changed their tax consultant, 3

assessees have changed their tax consultant due to change in office

place of tax consultant and 2 assessees have changed due to change

in their own office place. It is observed that in the situation when

really it is very difficult to go to tax consultants’ office, then only

assessees tend to change their tax consultant. 2 assessees have

given the reason for change in their tax consultants as high fees

charged by them. One assessee has changed his tax consultant due

to dissatisfaction. Due to death of tax consultant one assessee has

to change his tax consultant. And one assessee has to change his

tax consultant due to conflict between him. The reason for conflict

is not disclosed.

127

3. Period of Filing Returns of Income with Serving Tax

Consultant

A survey is conducted as to how many years the assessee is

availing the services continuously from the same tax consultant.

The data is as follows:

Table No. 5.41

Continuous Availing the Services from the Same Tax Consultant

Particulars No. of Individuals Percentage (%)

0-5 years 83 27.67%

5-10 years 71 23.67%

10-15 years 65 21.67%

15-20 years 46 15.33%

more than 20 years 35 11.66%

Source: Primary Data

Figure 5.14

Continuous Availing the Services from the Same Tax Consultant

128

Table 5.41 and figure no. 5.14 shows that 83 (27.67%)

individual assessees have filing returns of income from same tax

consultants since 5 years. 71 (23.67%) individual assessees are

filing returns of income with same tax consultants since last 10

years while 65 individuals since 15 years. 46 individuals have

filing the returns of income with the same tax consultant since 20

years and 35 individuals since more than 20 years.

5.B.I.vi. Scrutiny of Returns of Income by Income-Tax Department

If the low income than reasonable income is shown in the

return of income by assessee or to confirm the genuineness of

source of huge investments made in the business by assessee,

Income-Tax Department may call that assessee for scrutiny. With

this Department randomly selects some cases for scrutiny. The

details in this regard are as under:

Table No. 5.42

Scrutiny

Particulars No of Individuals Percentage (%)

Scrutinized --- ---

Not Scrutinized 300 100 %

Total 300 100 %

Source: Primary Data

129