Chapter 10 Section 1

22

Chapter 10 Section 1 Interest

-

Upload

libby-chambers -

Category

Documents

-

view

17 -

download

2

description

Chapter 10 Section 1. Interest. Terms. Interest : Fee that is paid for the use of money Principal : Amount of initial deposit or initial/current balance Compound Amount : Amount to which the principal grows (after the addition on interest). Alternate term: Balance Compounded : Computed. - PowerPoint PPT Presentation

Transcript of Chapter 10 Section 1

Chapter 10 Section 1

Interest

Terms

• Interest : Fee that is paid for the use of money

• Principal : Amount of initial deposit or initial/current balance

• Compound Amount : Amount to which the principal grows (after the addition on interest). Alternate term: Balance

• Compounded : Computed

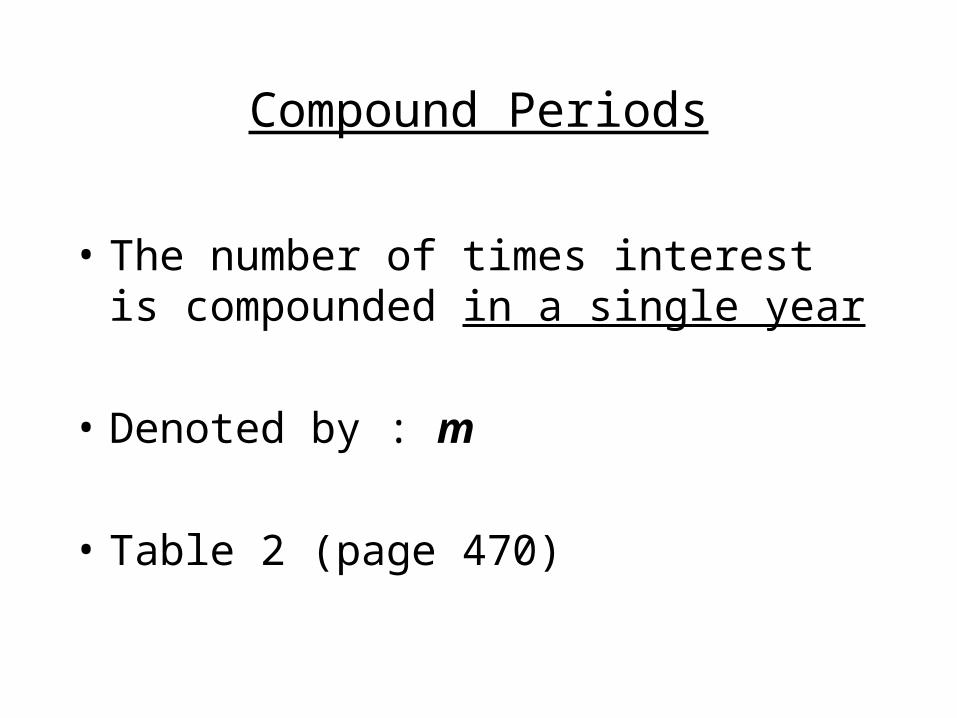

Compound Periods

• The number of times interest is compounded in a single year

• Denoted by : m

• Table 2 (page 470)

Compound Periods Table

Interest Compounded …

Number of Interest Periods Per Year

Annually m = 1

Semiannually m = 2

Quarterly m = 4

Monthly m = 12

Weekly m = 52

Daily m = 365

Annual Interest Rate

• Denoted by : r

• Also known as Nominal Rate or Stated Rate.

• Number which is stated / advertised and used to calculate the interest rate per period.

• Use decimal form when calculating by hand.

Interest Rate Per Compound Period

• Denoted by : i

• Number which is used to calculate interest for each compounding period.

• Use decimal form when calculating.

• Formula on next slide (page 470 – Blue-gray box).

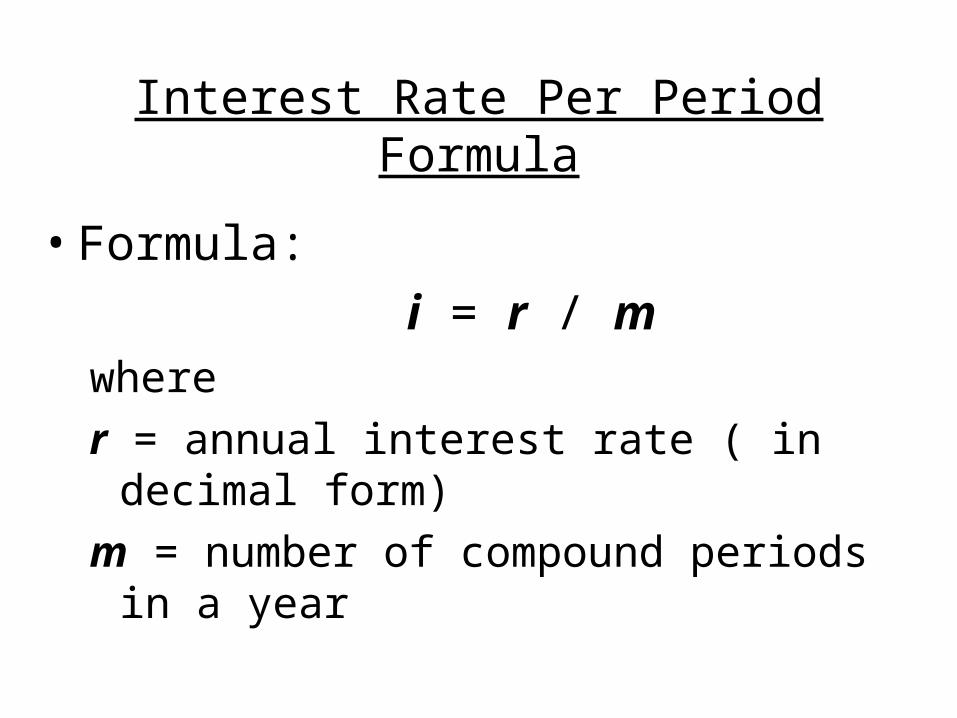

Interest Rate Per Period Formula

• Formula:

i = r / m where

r = annual interest rate ( in decimal form)

m = number of compound periods in a year

Example of Interest Rate Per Period

• Find the interest rate per period of an account that earns 6.25% interest compounded weekly.

• Solution:Given: r = 0.0625 and m = 52

i = r / m

= 0.0625 / 52 ~ 0.00120

Interest rate per period is approximately 0.12 %

Compound Interest Problems

• Basic idea for compound interest accounts1. Deposit an initial amount of money into an

account.

2. Step back and watch it grow.

3. You do not deposit or withdraw any additional money while interest is accumulating.

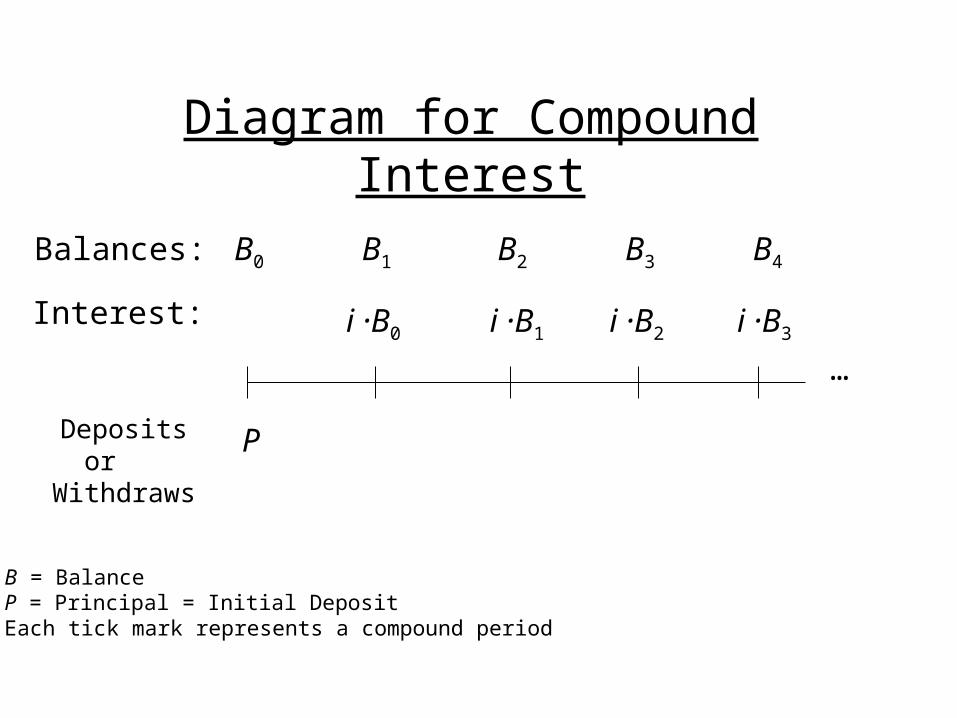

Diagram for Compound Interest

…

P

B1 B2 B3 B4B0

B = Balance P = Principal = Initial DepositEach tick mark represents a compound period

Balances:

Interest:

Depositsor

Withdraws

i ·B0 i ·B1 i ·B2 i ·B3

Balance for Compound Interest

New balance based on the old balance

Bnew = Bprevious + i·Bprevious

which simplifies to

Bnew = (1+ i)Bprevious (Note that this is in the form

of a difference equation)

Note that i·Bprevious represents the amount of interest that one earns for

the compound period

Balance after n interest/compounding periods

F = ( 1 + i )n ·P

Where: F = compounded amount after n compounding periods.

P = Principal (in the form of an initial deposit or current balance).

Notational Differences

Book Calculator Term

n N Number of compounding periods

F FV Future Value

P PV Principal Value

m P/Y

&

C/Y

Number of compounding periods in a year

R PMT Rent / Payment per period

Accessing the TVM Solver

1. Hit APPS key

2. Select 1:Finance function (Hit ENTER key)

3. Select 1:TVM Solver …function (Hit ENTER key)

TVM Solver Variables • N = Number of compound periods• I% = Annual Interest Rate (in percent form ( r% ))• PV = Principal Value (or) “Previous/Current” Balance• PMT = Rent / Payment Per Compound Period• FV = Future Value• P/Y = Payments Per Year = m• C/Y = Compounding Periods Per Year = m• PMT:END = Payments(/Interest) made(/calculated)

at the end of the compounding period

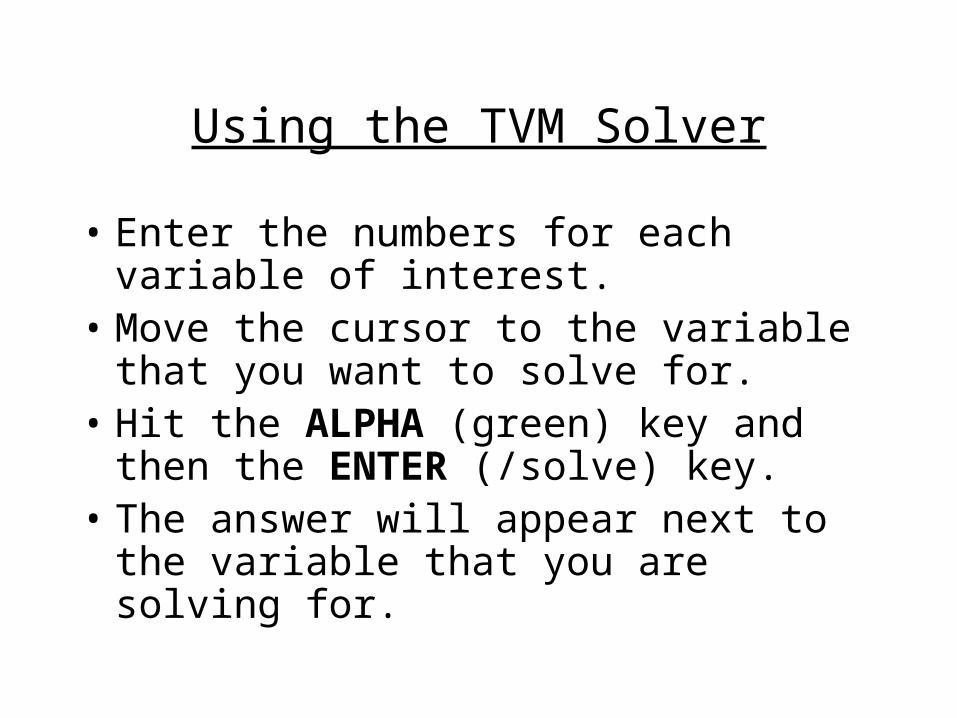

Using the TVM Solver

• Enter the numbers for each variable of interest.

• Move the cursor to the variable that you want to solve for.

• Hit the ALPHA (green) key and then the ENTER (/solve) key.

• The answer will appear next to the variable that you are solving for.

When using the TVM Solver on the calculator

• Think:

1. Outflow = NEGATIVE cash flow

(i.e. You DO NOT have the instantaneous use of your money )

2. Inflow = POSITIVE cash flow

(i.e. You do have the instantaneous use of your money )

Exercise 5 (page 477) Formula Solution

• Calculate the compound amount of $1,000 after 2 years if deposited at 6% interest compounded monthly.

• Solution:n = 2 ·12 = 24

i = r/m = 0.06/12 = 0.005

F = ( 1 + i )n ·P

F = ( 1 + 0.005 )24 ·1000

F = ( 1.12715977…) ·1000

F = 1127.15977Answer :$1,127.16

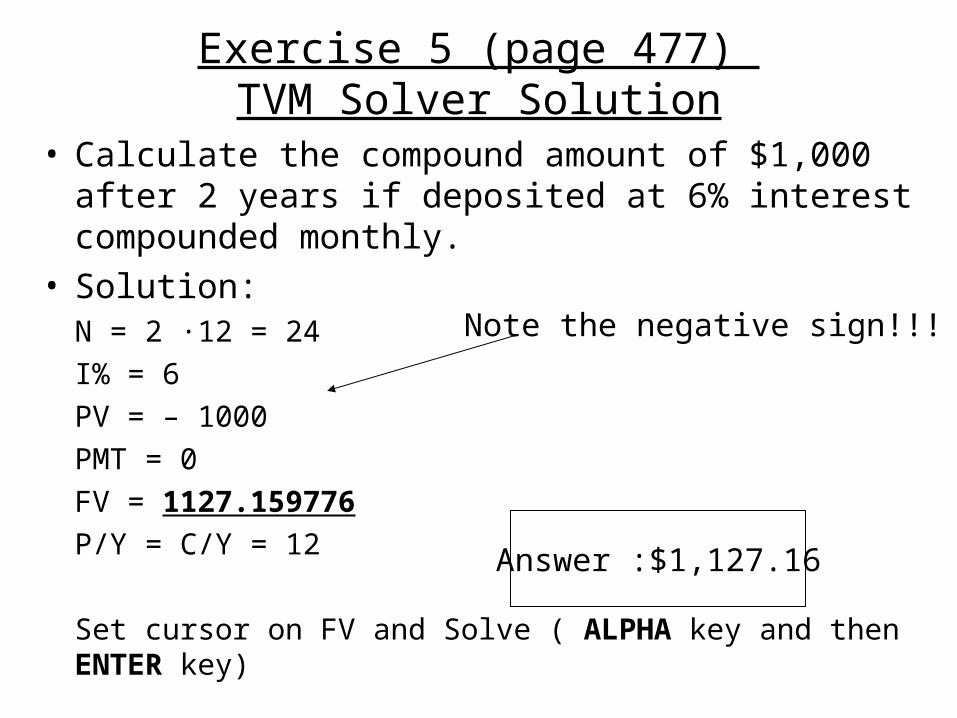

Exercise 5 (page 477) TVM Solver Solution

• Calculate the compound amount of $1,000 after 2 years if deposited at 6% interest compounded monthly.

• Solution:N = 2 ·12 = 24

I% = 6

PV = – 1000

PMT = 0

FV = 1127.159776

P/Y = C/Y = 12

Set cursor on FV and Solve ( ALPHA key and then ENTER key)

Answer :$1,127.16

Note the negative sign!!!

Effective Rate of Interest

• Page 474

• Used to1. Compares two annual interest rates that have

two different yearly compounding periods.

2. When money from the interest is reinvested in the account, will tell you the ‘true’ interest rate that you are earning.

Effective Rate of Interest Formula

Formula:

reff = ( 1 + i )m – 1

where:

reff = Effective Rate of Interest

i = Interest Rate Per Period = r / m

m = Number of compounding periods in a

single year

Effective Rate of Interest on the Calculator

• Access– Hit APPS key– Select 1:Finance function– Use down (or up) arrow key to select C: Eff(

function

• SyntaxEff( r% , m )

( r% = Annual Interest Rate in % form)