Challenger Diversified Property Group Annual Report … Diversified Property Group Annual Report...

96

Challenger Diversified Property Group Annual Report 2012 Challenger Diversified Property Group comprising: Challenger Diversified Property Trust 1 (ARSN 121 484 606) Challenger Diversified Property Trust 2 (ARSN 121 484 713) Responsible Entity Challenger Listed Investments Limited (ABN 94 055 293 644) (AFSL 236887)

Transcript of Challenger Diversified Property Group Annual Report … Diversified Property Group Annual Report...

Challenger Diversified Property GroupAnnual Report 2012

Challeng

er Diversifi

ed Prop

erty Gro

up A

nnual Rep

ort 2012

Challenger Diversified Property Groupcomprising:

Challenger Diversified Property Trust 1(ARSN 121 484 606)

Challenger Diversified Property Trust 2(ARSN 121 484 713)

Responsible EntityChallenger Listed Investments Limited (ABN 94 055 293 644) (AFSL 236887)

Level 15 255 Pitt Street Sydney NSW 2000 telephone 02 9994 7000 facsimile 02 9994 7777

www.challenger.com.au

1378

4/C

G92

7/0

812

Contents

Key highlights 1

Chair’s letter 2

Fund Manager’s report 3

Case study 6

Portfolio summary 8

Property summaries 11

About Challenger 21

Corporate governance statement 22

Directors’ report 29

Financial report 40

Unitholder information 86

Additional information 88

Directory 90

Challenger Listed Investments Limited (ABN 94 055 293 644) (AFSL 236887) (CLIL) is the Responsible Entity of Challenger Diversified Property Trust 1 (ARSN 121 484 606) and Challenger Diversified Property Trust 2 (ARSN 121 484 713) which together form the Challenger Diversified Property Group (CDI).

CLIL, as the Responsible Entity of CDI, has prepared this Annual Report (Report) based on information available to it. The information in this Report should be regarded as general information only. Nothing contained in this Report constitutes investment, legal, tax or other advice. It has been prepared without taking account of any person’s objectives, financial situation or needs. Recipients should, before acting on any such information, consider its appropriateness, having regard to their objectives, financial situation and needs, and seek the assistance of their financial or other licensed professional adviser before making any investment decision.

Any investment in CDI is subject to investment risk and other risks, including possible loss of income and principal invested. None of CLIL, Challenger Management Services Limited (ABN 29 092 382 842) (AFSL 234678) (CMSL), Challenger Limited (ABN 85 106 842 371) (Challenger) or any other member of the Challenger Group gives any guarantee or assurance as to the performance of CDI or the repayment of capital.

Nothing in this Report should be considered a solicitation, offer or invitation to buy, subscribe or sell any, or a recommendation of, financial products.

All reasonable care has been taken to ensure that the facts stated and opinions given in this Report are fair and accurate. To the maximum extent permitted by law, the recipient releases CLIL, each member of the Challenger Group, their directors, officers, employees, representatives and advisers from any liability (including, without limitation, in respect of direct, indirect or consequential loss or damage or loss or damage arising by negligence) arising in relation to any recipient relying on anything contained in or omitted from this Report.

Any forward looking statements included in this Report involve subjective judgment and analysis and are subject to significant uncertainties, risks and contingencies, many of which are outside the control of, and are unknown to, CLIL. In particular, they speak only as of the date of these materials, they assume the success of CDI’s business strategies, and they are subject to significant regulatory, business, competitive and economic uncertainties and risks. Actual future events may vary materially from forward looking statements and assumptions on which those statements are based. Given these uncertainties, recipients are cautioned not to place undue reliance on such forward looking statements.

Any past performance information provided in this Report is not a reliable indication of future performance.

CLIL does not receive any specific remuneration for any general advice which may be provided to you in this Report. However, CLIL and CMSL receive trustee and management fees as issuer and manager of CDI, respectively. For more details on fees, please refer to the Financial Report contained in this Report along with the Constitution and Management Agreement on CDI’s website www.challenger.com.au/cdi (under the Corporate Governance tab). Financial advisers may receive fees or commissions if they provide advice to you or arrange for you to invest in a Challenger product (including CDI). CLIL and its associates may have an interest in the financial products referred to in this Report and may earn fees or other benefits as a result of transactions in any such financial products.

Members of the Challenger Group and their officers and directors may hold securities in CDI from time to time.

Important notice

500 Chapel Street South Yarra Victoria

Challenger Diversified Property Group Annual Report 2012

1

Key highlights

Strategy delivering results. Profit from operating activities: $44.8 million, equivalent to 5.06 cents per unit, up from 4.86 cents per unit in FY11.

Exceeded earnings guidance of 5.00 cents per unit and delivered distribution of 4.2 cents per unit.

1 2 3

4 5 6

7 8 9

Property metrics improving; Occupancy: 94.1% up from 93.7% in FY11, and WALE maintained at 5.0 years across the periods.

Investment property valuations up $17.1 million on 30 June 2011, a 2.2% increase in valuation over the 12 month period.

Balance sheet gearing of 29.8% post payment of 2H12 distribution, in line with target.

Strategic objectives remain to grow earnings via portfolio enhancement, improve lease metrics and active capital management in order to close the gap between price and NTA.

Portfolio enhancement progress; practical completion of both the development of Stage 2 at the Junction Industrial Park and the upgrade of the Domain Car Park. Talavera Road sold, down weighting exposure to hi-tech industrial sector.

Improving leasing metrics progress; numerous key leasing deals have been completed during the year, significantly de-risking the portfolio by reducing the lease expiries for the 2013 financial year from 12% to 4%.

10 11 12

Active capital management progress, buyback, purchased 6.2% of issued capital. To date ~57 million units purchased at 23% average discount to NTA – equivalent to purchasing a property on a 10.6% yield.

FY13 guidance announced; earnings of 5.25 cents per unit (EPU) and distributions 4.35 cents per unit (CPU), growth of 4% respectively in each.

1 for 4 unit consolidation undertaken.

2

The 2012 financial year has been both pleasing and challenging for AREITs, on one hand leasing conditions remain challenging and business confidence remains low, while on the other, the falling interest rate and low growth environment have caused investors to search for quality, defensive, high yielding stocks. As a result the AREIT sector has outperformed general equities.

Through the last two financial years CDI’s strategy remained unchanged. Its three strategic objectives of portfolio enhancement, improve leasing metrics and active capital management are all focused on closing the unit price discount relative to Net Tangible Assets (NTA) per unit.

I am pleased to report this financial year CDI has exceeded the earnings guidance of 5.00 cents per unit and met distribution guidance of 4.20 cents per unit. Importantly, if you look back to our expectations for both earnings and distributions this time last year, these numbers both represent significant growth.

We have announced guidance for the coming financial year for earnings of 5.25 cents per unit and distribution of 4.35 cents per unit. Using the closing price on Friday 10 August of 58.5 cents, this distribution guidance represents a solid 7.3% yield to unitholders.

CDI’s portfolio consists of 28 office, industrial and retail properties with 94.5% in Australia and 5.5% in France. CDI is working towards a medium-term goal to be a 100% Australian focused REIT with the proposed orderly sale of the French properties scheduled once the banking and economic situation in Europe improves and debt becomes more readily available.

CDI is in a strong financial postion with conservative balance sheet gearing of approximately 30%. The buyback continued with 6.2% of issued capital purchased at a 23% discount to NTA. Potential sales of CDI’s high tech assets as well as the French assets will fund both the buyback and future portfolio enhancement pipeline opportunities, depending on the most efficient use of capital.

I encourage all unitholders to read the Fund Manager’s report that follows and review the portfolio summary also contained in this document for further information on all CDI’s properties.

The management team and staff have worked diligently during the past year to further strengthen CDI. I congratulate the team and thank them for their hard work that ensures the Trust is positioned for further growth.

Finally, I thank you for your continued support of CDI, and I look forward to another productive year in which Challenger Diversified Property Group closes the discount to NTA and creates additional value for unitholders.

Michael Cole Chair

Chair’s letter

3

Challenger Diversified Property Group Annual Report 2012

Fund Manager’s report

Dear unitholder

The 2012 financial year has been a busy one for CDI, and I am pleased to report that the Fund has delivered on or exceeded all guided market expectations. CDI is well positioned going into the 2013 financial year having built a strong stable portfolio and a de-risked model. At CDI we are focused on three strategic objectives; portfolio enhancement, improve leasing metrics and active capital management as the vehicles to grow earnings and close the unit price to NTA gap.

CDI has strengthened the balance sheet and is positioned for further growth. CDI has made some good progress on its strategic objectives over the period with practical completion achieved for both the upgrade of the Domain Car Park and the development of Stage 2, The Junction, as well as continued progress in the repositioning of the Jam Factory, as key portfolio enhancement initiatives. Leasing has been very pleasing with a large number of expiries renewed, reducing our FY13 expiries materially. Lastly, for our active capital management initiatives the on market buyback, our primary capital management initiative, has now purchased 6.2% of issued capital, creating accretion for unitholders.

Financial performance

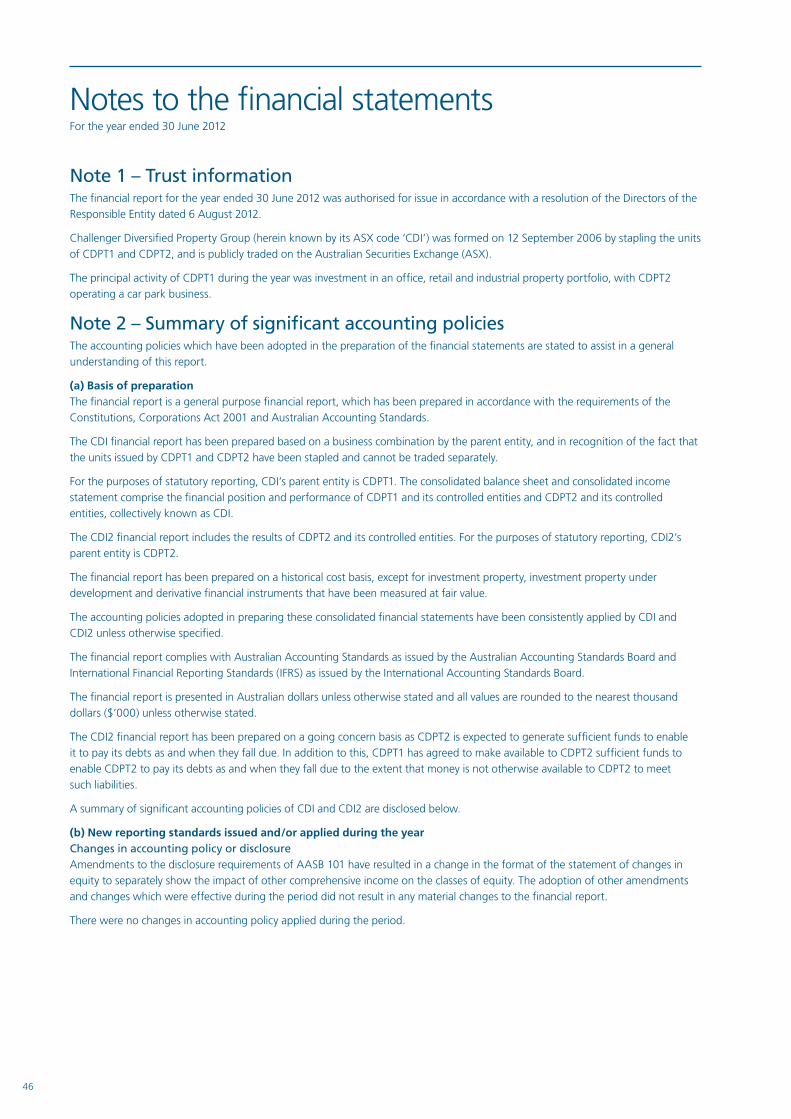

For the financial year to 30 June 2012 (FY12), CDI delivered solid profit from operating activities for the year of $44.8 million or

5.06 cents per unit, up from 4.86 at FY11 and representing 4% growth. This was primarily due to portfolio rental growth and the benefits of the accretion from the unit buyback. Distribution of 4.20 cents per unit was in line with guidance and up from 4.00 cents, again growing by 4% over the previous year, proving the quality and underlying resilience of the portfolio. Statutory net profit after tax of $36.2 million was primarily impacted by the unrealised adverse movement in interest rate swaps.

Total assets at 30 June 2011 were $880 million, with net tangible assets (NTA) of $586.7 million. On a per unit basis NTA was up 1 cent per unit to 68 cents from June 2011 due to the accretion from the buyback.

Distribution

Our policy is to distribute accounting profit earned from operating activities adjusted for non-cash expenses, such as straight-lining of rental income, and then deduct expected and incurred leasing costs, debt establishment fees and maintenance capex. After these adjustments, CDI distributed 4.2 cents per unit, which represents an operating profit payout ratio of 82%, and an available funds from operations (AFFO) payout ratio of 99.5%.

Portfolio

The CDI portfolio comprises interests in 28 office, industrial and retail properties located in Australia and France. CDI also holds a cumulative 25 year leasehold interest in respect to Sydney’s Domain Car Park.

All properties in CDI’s portfolio were revalued as at 30 June 2012, 66% by value were independently revalued and the remainder were internally valued. The investment property revaluation resulted in

a $17.1 million uplift or 2.2% on 30 June 2011 valuations. The carrying value of the total portfolio as at 30 June 2012 was $852 million.

CDI has progressed and completed a number of portfolio enhancement projects during the year. Practical completion was achieved on both the upgrade of the Domain Car Park and the development of Stage 2, The Junction. These projects were completed on time and to budget. The Jam Factory repositioning is progressing well and expected to complete in December 2012. All projects aim to realise latent value within the portfolio.

Stage 2 of The Junction development commenced after securing a 10 year lease pre-commitment for a 20,200 sqm distribution facility. The site is located in the inner west, the geographical heart of Sydney, and the facility’s attributes ensure a prime industrial grading that will meet the requirements of a broad group of distribution and warehouse users in the future. The lease commenced 3 July 2012 and will add to net property income in the coming period.

The Domain Car Park upgrade is now complete. The key aim of the upgrade was to improve the customer experience. The works included upgrading the façade and travelator, installing new lifts and service improvements. The car park is expected to provide an increased contribution to earnings now that the upgrade is complete and it can operate to its full potential.

The aim of the Jam Factory repositioning is to make the centre more contemporary, accessible and sought after by a broader demographic. The tenancy remix is nearing completion; focusing

4

on popular food, fashion and entertainment brands like TOPSHOP, Urban by Target, Salsa’s, Groove Train, Lindt Chocolates and Nando’s to complement the existing Village Cinemas. The food court commenced trading in June, while the upgrade of the 970 bay car park has commenced and is due to complete in September 2012.

The Jam Factory repositioning is the latest of CDI’s committed value add initiatives. There is a pipeline of future initiatives to take advantage of latent opportunities within the portfolio. The portfolio enhancement strategy also targets the continued value add to existing

portfolio through the recycling of capital.

Market cap rates remain relatively constant across the portfolio at 8.23%, the domestic portfolio tightening marginally across the period and the French portfolio remaining flat at 7.81%. CDI is currently trading on an implied cap rate of 9.6%, which looking across the market at relative peers looks compelling.

Leasing

Occupancy (94.1%) has increased on the prior period while the WALE (5.0 years) has been maintained across the periods. This is particularly pleasing given the backdrop of a challenging leasing market. Leasing activity throughout the market has been subdued, with tenants preferring to remain in their premises rather than relocate. However, CDI’s leasing progress during the year has been significant, with 38 lease deals negotiated representing a total of 70,767 sqm or $13.1 million in gross rent (14.2% of total; gross income). Our retention rate of existing tenants has been over 70%.

CDI has significantly reduced the expiry risk for the financial year 2013, down from 12% as at June 2011 to 4%, demonstrating the significant inroads made into the retention of these tenants.

There have been some key lease deals signed in this year with the highlights including the TOPSHOP lease for 10 years and approximately 1700 sqm as well as the recently signed 12 year Village office lease for 6,700 sqm. In 31 Queen Street and Makerston House there has been a total of 12 individual leases signed throughout these properties. 6 Foray Street has been a great result, signing IFC up for over 17,000 sqm of industrial warehousing space. Two French leases at Exel and ATAC have been renewed for 6 and 9 years respectively.

The leasing up of our current vacancies, sitting at 5.9%, represents upside in future earnings and therefore subsequently distribution. CDI has been actively marketing these premises and engaging in negotiations with prospective tenants; however, lead times have lengthened.

Capital management

In April 2011, CDI announced an on-market unit buyback, with the intention to buy back up to 10% of issued capital. The buyback is both NTA per unit and earnings accretive. Management believes the current discount to NTA does not represent the intrinsic value of CDI and a buyback will work to close the gap between NTA per unit and the unit price for the benefit of all unitholders.

Fund Manager’s report (continued)

Challenger Diversified Property Group Annual Report 2012 Challenger Diversified Property Group Annual Report 2012

5

CDI has bought back 6.2% of issued capital in the on-market unit buyback since commencement. CDI has purchased ~57 million units at an average of 23% discount to NTA per unit, generating $9 million in value. This is equivalent to purchasing a property on a 10.6% yield. CDI has approached the buyback tactically. Accordingly, purchases have been made on an opportunistic basis. This is reflected by CDI’s average purchase price of 52.50 cents being 1.6% lower than the market VWAP of 53.40 cents and CDI only purchasing on average 27% of available market volume.

The increase in the buyback during the six months to 30 June 2012 has been funded through the capital recycling strategy, specifically the sale of 75 Talavera Road. Further progress of the buyback will continue in line with future asset sales, subject to the most efficient use of capital.

On 7 August, CDI announced that it was undertaking a 1 for 4 unit consolidation. Management believes that the unit consolidation for a negligible cost will have the following benefits: reduced unit price volatility; improved market perception; and alignment with other A-REITs.

CDI has no maturities until July 2013. The undrawn capacity of approximately $35 million will be used to complete the current committed developments and provide CDI with financial flexibility and a liquidity buffer.

Environmental sustainability

CDI is committed to improving the environmental sustainability of its properties. The portfolio summary pages in this annual report provide

details of the energy rating of each rateable building. The rating system we utilise is the NABERS energy rating scale, a performance-based rating system for existing buildings. NABERS rates a building on the basis of its measured operational impacts on the environment, and provides a simple indication of how well environmental impacts are managed compared with peers and neighbours.

The NABERS energy ratings scale across our office buildings is currently at a weighted average 4.0 stars today. The NABERS rating has increased from 3.6 stars as at June 2011 to 4.0 stars. This increase is the result of three sustainability capex projects being completed across. The Forum Verizon, Makerston House and Discovery House Stage 1. CDI remains committed to lifting its NABERS rating. Over the next 12 months we have a pipeline of further projects which we expect will lift the NABERS rating across the office portfolio closer to our medium- term target of 4.5 stars.

Outlook

The management of CDI has a clearly defined strategy which has delivered results over the year. The Fund’s primary goal is to close the unit price to NTA per unit gap through growing earnings. The growth in earnings will be achieved through the three strategic initiatives; portfolio enhancement, improving leasing metrics and active capital management.

We have provided both earnings and distribution guidance for the coming financial year, 5.25 cents per unit and 4.35 cents per unit respectively. Within this guidance we have incorporated realistic assumptions around reletting and leasing costs. The 4.35 cent distribution guidance represents an 83% payout ratio and an implied yield of 7.4% (based on a 14 August close price of 58.5 cents).

With a clearly defined strategy and significant progress in leasing, capital management and portfolio enhancement, CDI is positioned well towards achieving its goals of growing earnings and closing the price to NTA per unit gap.

On behalf of management and our team at CDI, thank you for your ongoing support. I look forward to updating you on CDI’s progress and achievements during the coming year.

Trevor Hardie Fund Manager

Case study

6

Case Study – Stage 2 The Junction Industrial Park, Enfield

CDI acquired an 8.56 ha site at 34-48 Cosgrove Road Enfield in 2007 for the purpose of developing a prime industrial facility. The site is strategically located in Inner Western Sydney within the established industrial precinct of Enfield. The site is easily accessed via the M4 Motorway to the north and the M5 Motorway to the south and is located adjacent to the Enfield Intermodal Logistics Centre.

Stage 1, comprising 13,437sqm of warehouse facilities, was developed on a speculative basis and was completed in December 2008. A seven year lease to KW Doggett was secured on completion of the facility.

Stage 2 was developed after securing a 10 year lease pre-commitment to Bunzl Australasia Limited (Bunzl) for a 20,200sqm distribution facility in August 2011. Bunzl PLC, the parent company of Bunzl, is a leading global supply chain management and specialist distribution company operating in 23 countries and is listed on the London Stock Exchange.

Bunzl’s NSW Distribution Centre at The Junction Industrial Park will accommodate circa 170 personnel, with three businesses consolidating operations into the facility. Bunzl will move their businesses in on a staged basis occurring through the rest of 2012 and into early 2013.

Stage 2 also comprises a 150sqm café facility servicing the estate. Practical completion was achieved on 2 July 2012. The project has been delivered on time, within budget and to valuation. This has been achieved through effective builder selection, detailed up front commercial assessment and strong risk and project management throughout the process.

CDI entered into a Development and Construction Contract with FDC for the delivery of the base building and Bunzl also entered into contracts with FDC for the delivery of an integrated fitout. The construction period of ten months included both the construction of the base building as well as the integrated office and warehouse fitout. This ensured Bunzl were able to operate from the facility immediately upon practical completion.

The development of the Bunzl facility is in accordance with CDI’s strategies of portfolio enhancement, through the reduced exposure to purpose built facilities and improving leasing metrics. Stage 2 of The Junction Industrial Park is a prime industrial facility that will meet the requirements of a broad group of distribution and warehouse users in the future.

Stage 3 can accommodate a further 12,660sqm of warehouse and distribution facilities and is currently being marketed with a delivery time of 8 months from signing of AFL.

On completion The Junction Industrial Park will house 46,447sqm of facilities with a completion value of circa $75m.

Development Metrics

On Completion Valuation $34.0m

Total Development Cost $32.4m

Unrealised Value add $1.6m

Investment Metrics

Cap Rate 7.75%

Initial Income Yield on Cost 8.15%

5 year Investment IRR 11.5%

Impact on Industrial Portfolio Metrics

Pre Development

Post Development

WALE 3.9 years 5.5 years

Occupancy 93% 95%

Weighted average cap rate 8.81% 8.48%

7

8

Portfolio summary

Property Location

Net lettable

area (sqm)

Occupancy at 30 June

2012 (by income)

(%)

Weighted average lease

expiry (WALE) (by income)

(years)Date

acquired

Prior period

valuation ($m)

Prior market

cap rate (%)

Currentvaluation

($m)

Current market

cap rate (%)

Valuation change

($m)

Discount rate (%) Valuer

Book value

30 June 2012 ($m)

Average gross

passing rent

($/sqm)

Average gross

market rent

($/sqm)

Asset values

($/sqm)Office portfolioABS House Belconnen, ACT 31,050 100.0 4.7 Oct-2006 88.8 7.75 87.6 8.25 (1.2) 9.25 m3 87.6 457 420 4,702

31 Queen Street Melbourne, VIC 19,339 97.4 3.7 Mar-2011 89.0 8.00 91.0 8.00 2.0 9.50 m3 91.0 456 471 4,705

DIAC Building Belconnen, ACT 29,530 100.0 7.3 Oct-2006 68.4 7.75 69.0 8.00 0.6 9.25 m3 69.0 347 375 3,894

The Forum, Cisco St Leonards, NSW 16,584 99.1 2.4 Oct-2006 62.4 8.25 63.1 8.25 0.7 9.50 Internal 63.1 576 548 6,338

Discovery House Woden, ACT 22,239 100.0 10.2 Oct-2006 60.6 7.75 61.4 7.75 0.8 9.00 Internal 61.4 415 415 4,605

Makerston House Brisbane, QLD 14,652 100.0 2.8 Oct-2006 44.4 8.50 45.1 8.50 0.7 9.75 Internal 45.1 509 520 5,132

The Forum, Verizon St Leonards, NSW 11,711 69.0 3.2 Oct-2006 41.0 8.50 41.8 8.50 0.8 9.75 Internal 41.8 534 526 5,952

Elder House Adelaide, SA 14,086 100.0 3.8 Oct-2006 28.3 8.75 27.9 9.00 (0.4) 9.75 m3 27.9 434 368 3,301

Executive Building Hobart, TAS 9,887 100.0 3.0 Oct-2006 20.6 8.75 20.4 8.75 (0.2) 9.50 Savills 20.4 379 389 3,439

Office portfolio total/average 169,078 96.8 4.7 503.4 8.08 507.3 8.21 3.9 9.42 507.3 443 436 4,647

Retail portfolioJam Factory South Yarra, VIC 20,1271 98.7 8.0 Oct-2006 70.2 8.25 71.1 7.75 0.8 9.00 JLL 71.1 517 517 5,884Century City Walk Glen Waverley, VIC 8,289 100.0 5.2 Jun-2008 30.0 8.50 30.0 8.50 – 9.50 Savills 30.0 443 443 3,619Innaloo Cinema Centre Woodlands, WA 11,549 100.0 6.1 Oct-2006 25.0 8.00 25.5 8.00 0.5 9.25 JLL 25.5 388 388 3,680Kings Langley Shopping Centre Kings Langley, NSW 4,157 100.0 7.4 Oct-2006 9.7 8.75 9.4 8.75 (0.3) 9.75 Savills 9.4 420 420 3,753Retail portfolio total/average 44,122 99.3 7.0 134.9 8.30 135.9 8.03 1.0 9.21 135.9 445 445 4,563

Industrial portfolioDistribution centresThe Junction, Stage 2 Enfield, NSW 20,360 99.3 9.9 Jul-2012 34.0 7.75 34.0 7.75 – 9.50 Colliers 34.0 146 146 1,682The Junction, Stage 1 Enfield, NSW 13,437 100.0 3.5 Dec-2008 20.4 8.25 20.4 8.50 – 9.50 Internal 20.4 152 146 1,5186 Foray Street Fairfield, NSW 22,960 71.6 2.1 Oct-2006 16.3 10.00 15.3 10.00 (1.0) 10.00 Colliers 15.3 90 88 664Spotlight Laverton North, VIC 20,723 100.0 9.0 Oct-2006 16.8 8.25 17.3 8.25 0.4 9.75 Internal 17.3 77 77 83512-30 Toll Drive Altona North, VIC 13,885 100.0 3.6 Oct-2006 13.5 8.75 14.0 8.75 0.5 11.00 Colliers 14.0 114 107 1,0082-10 Toll Drive Altona North, VIC 6,244 100.0 0.6 Oct-2006 6.4 8.75 6.4 8.75 0.1 9.75 Internal 6.4 125 110 1,0251-9 Toll Drive Altona North, VIC 3,239 100.0 3.6 Oct-2006 3.5 8.50 3.9 8.50 0.4 10.50 Colliers 3.9 134 133 1,204Distribution portfolio total/average 100,848 94.5 5.5 110.8 8.45 111.3 8.48 0.5 9.85 111.3 115 112 1,103

High techTaylors House Waterloo, NSW 11,084 99.2 4.7 Oct-2006 26.9 8.25 26.9 8.25 – 9.25 Internal 26.9 465 377 4,042187 Todd Road Port Melbourne, VIC 9,308 24.9 1.0 Oct-2006 13.6 9.50 13.6 9.50 – 10.00 Internal 13.6 303 296 2,428Giffnock Avenue North Ryde, NSW 5,973 – 0.0 Jun-2008 12.0 8.75 9.9 9.50 (2.1) 9.75 Colliers 9.9 – 240 1,657High tech portfolio total/average 26,365 55.6 2.6 52.4 8.69 50.3 8.83 (2.1) 9.55 50.3 247 310 2,765Industrial portfolio total/average 127,213 80.1 4.4 163.2 8.53 161.6 8.59 (1.6) 9.75 161.6 132 137 1,357

Australian portfolio total/average 340,413 93.7 5.0 801.5 8.21 804.8 8.26 3.3 9.45 804.8 296 295 3,119

French portfolio m m m ($/sqm) ($/sqm) ($/sqm)Sully Sully sur Loire 15,500 100.0 5.5 Jun–2007 9.2 9.00 8.9 9.20 (0.3) – Knight Frank 8.9 104 83 713Aulnay Aulnay sous Bois, Paris 5,105 100.0 3.3 Jun–2007 8.9 6.50 9.3 6.25 0.4 – Knight Frank 9.3 217 193 2,243Béziers Rue Charles Nicolle 8,944 100.0 3.2 Jun–2007 8.1 8.25 8.2 8.25 0.2 – Knight Frank 8.2 113 103 1,141Gennevilliers Gennevilliers, Paris 7,409 100.0 8.7 Jun–2007 7.0 7.21 7.2 7.10 0.3 – Knight Frank 7.2 134 134 1,210Tours Parcay-Meslay, Tours 5,610 100.0 6.2 Jun–2007 4.2 8.25 4.4 8.65 0.2 – Knight Frank 4.4 116 105 971

French portfolio total/average 42,568 100.0 5.3 37.4 7.82 38.1 7.81 0.8 – 38.1 114 101 1,107Investment portfolio total/average

382,981 94.1 5.0 847.9 8.19 852.0 8.23 4.1 9.45 852.0 269 266 2,834

Development portfolio $m $m $mThe Junction, Stage 3 Enfield, NSW N/A – – Mar–2007 6.8 – 6.8 – – – Colliers 6.8 – – –Australian development portfolio total/average

– – – 6.8 – 6.8 – – – 6.8 – – –

1 Excludes development (strategic) vacancies.

9

Challenger Diversified Property Group Annual Report 2012

Property Location

Net lettable

area (sqm)

Occupancy at 30 June

2012 (by income)

(%)

Weighted average lease

expiry (WALE) (by income)

(years)Date

acquired

Prior period

valuation ($m)

Prior market

cap rate (%)

Currentvaluation

($m)

Current market

cap rate (%)

Valuation change

($m)

Discount rate (%) Valuer

Book value

30 June 2012 ($m)

Average gross

passing rent

($/sqm)

Average gross

market rent

($/sqm)

Asset values

($/sqm)Office portfolioABS House Belconnen, ACT 31,050 100.0 4.7 Oct-2006 88.8 7.75 87.6 8.25 (1.2) 9.25 m3 87.6 457 420 4,702

31 Queen Street Melbourne, VIC 19,339 97.4 3.7 Mar-2011 89.0 8.00 91.0 8.00 2.0 9.50 m3 91.0 456 471 4,705

DIAC Building Belconnen, ACT 29,530 100.0 7.3 Oct-2006 68.4 7.75 69.0 8.00 0.6 9.25 m3 69.0 347 375 3,894

The Forum, Cisco St Leonards, NSW 16,584 99.1 2.4 Oct-2006 62.4 8.25 63.1 8.25 0.7 9.50 Internal 63.1 576 548 6,338

Discovery House Woden, ACT 22,239 100.0 10.2 Oct-2006 60.6 7.75 61.4 7.75 0.8 9.00 Internal 61.4 415 415 4,605

Makerston House Brisbane, QLD 14,652 100.0 2.8 Oct-2006 44.4 8.50 45.1 8.50 0.7 9.75 Internal 45.1 509 520 5,132

The Forum, Verizon St Leonards, NSW 11,711 69.0 3.2 Oct-2006 41.0 8.50 41.8 8.50 0.8 9.75 Internal 41.8 534 526 5,952

Elder House Adelaide, SA 14,086 100.0 3.8 Oct-2006 28.3 8.75 27.9 9.00 (0.4) 9.75 m3 27.9 434 368 3,301

Executive Building Hobart, TAS 9,887 100.0 3.0 Oct-2006 20.6 8.75 20.4 8.75 (0.2) 9.50 Savills 20.4 379 389 3,439

Office portfolio total/average 169,078 96.8 4.7 503.4 8.08 507.3 8.21 3.9 9.42 507.3 443 436 4,647

Retail portfolioJam Factory South Yarra, VIC 20,1271 98.7 8.0 Oct-2006 70.2 8.25 71.1 7.75 0.8 9.00 JLL 71.1 517 517 5,884Century City Walk Glen Waverley, VIC 8,289 100.0 5.2 Jun-2008 30.0 8.50 30.0 8.50 – 9.50 Savills 30.0 443 443 3,619Innaloo Cinema Centre Woodlands, WA 11,549 100.0 6.1 Oct-2006 25.0 8.00 25.5 8.00 0.5 9.25 JLL 25.5 388 388 3,680Kings Langley Shopping Centre Kings Langley, NSW 4,157 100.0 7.4 Oct-2006 9.7 8.75 9.4 8.75 (0.3) 9.75 Savills 9.4 420 420 3,753Retail portfolio total/average 44,122 99.3 7.0 134.9 8.30 135.9 8.03 1.0 9.21 135.9 445 445 4,563

Industrial portfolioDistribution centresThe Junction, Stage 2 Enfield, NSW 20,360 99.3 9.9 Jul-2012 34.0 7.75 34.0 7.75 – 9.50 Colliers 34.0 146 146 1,682The Junction, Stage 1 Enfield, NSW 13,437 100.0 3.5 Dec-2008 20.4 8.25 20.4 8.50 – 9.50 Internal 20.4 152 146 1,5186 Foray Street Fairfield, NSW 22,960 71.6 2.1 Oct-2006 16.3 10.00 15.3 10.00 (1.0) 10.00 Colliers 15.3 90 88 664Spotlight Laverton North, VIC 20,723 100.0 9.0 Oct-2006 16.8 8.25 17.3 8.25 0.4 9.75 Internal 17.3 77 77 83512-30 Toll Drive Altona North, VIC 13,885 100.0 3.6 Oct-2006 13.5 8.75 14.0 8.75 0.5 11.00 Colliers 14.0 114 107 1,0082-10 Toll Drive Altona North, VIC 6,244 100.0 0.6 Oct-2006 6.4 8.75 6.4 8.75 0.1 9.75 Internal 6.4 125 110 1,0251-9 Toll Drive Altona North, VIC 3,239 100.0 3.6 Oct-2006 3.5 8.50 3.9 8.50 0.4 10.50 Colliers 3.9 134 133 1,204Distribution portfolio total/average 100,848 94.5 5.5 110.8 8.45 111.3 8.48 0.5 9.85 111.3 115 112 1,103

High techTaylors House Waterloo, NSW 11,084 99.2 4.7 Oct-2006 26.9 8.25 26.9 8.25 – 9.25 Internal 26.9 465 377 4,042187 Todd Road Port Melbourne, VIC 9,308 24.9 1.0 Oct-2006 13.6 9.50 13.6 9.50 – 10.00 Internal 13.6 303 296 2,428Giffnock Avenue North Ryde, NSW 5,973 – 0.0 Jun-2008 12.0 8.75 9.9 9.50 (2.1) 9.75 Colliers 9.9 – 240 1,657High tech portfolio total/average 26,365 55.6 2.6 52.4 8.69 50.3 8.83 (2.1) 9.55 50.3 247 310 2,765Industrial portfolio total/average 127,213 80.1 4.4 163.2 8.53 161.6 8.59 (1.6) 9.75 161.6 132 137 1,357

Australian portfolio total/average 340,413 93.7 5.0 801.5 8.21 804.8 8.26 3.3 9.45 804.8 296 295 3,119

French portfolio m m m ($/sqm) ($/sqm) ($/sqm)Sully Sully sur Loire 15,500 100.0 5.5 Jun–2007 9.2 9.00 8.9 9.20 (0.3) – Knight Frank 8.9 104 83 713Aulnay Aulnay sous Bois, Paris 5,105 100.0 3.3 Jun–2007 8.9 6.50 9.3 6.25 0.4 – Knight Frank 9.3 217 193 2,243Béziers Rue Charles Nicolle 8,944 100.0 3.2 Jun–2007 8.1 8.25 8.2 8.25 0.2 – Knight Frank 8.2 113 103 1,141Gennevilliers Gennevilliers, Paris 7,409 100.0 8.7 Jun–2007 7.0 7.21 7.2 7.10 0.3 – Knight Frank 7.2 134 134 1,210Tours Parcay-Meslay, Tours 5,610 100.0 6.2 Jun–2007 4.2 8.25 4.4 8.65 0.2 – Knight Frank 4.4 116 105 971

French portfolio total/average 42,568 100.0 5.3 37.4 7.82 38.1 7.81 0.8 – 38.1 114 101 1,107Investment portfolio total/average

382,981 94.1 5.0 847.9 8.19 852.0 8.23 4.1 9.45 852.0 269 266 2,834

Development portfolio $m $m $mThe Junction, Stage 3 Enfield, NSW N/A – – Mar–2007 6.8 – 6.8 – – – Colliers 6.8 – – –Australian development portfolio total/average

– – – 6.8 – 6.8 – – – 6.8 – – –

1 Excludes development (strategic) vacancies.

Our properties…

10

11

Challenger Diversified Property Group Annual Report 2012

Property summaries

1 % of gross income.2 Office only.

Our properties…

ABS House

45 Benjamin Way, Belconnen, ACT

Property details

Ownership interest 60%

Net lettable area 31,050 sqm

Car spaces 400

Occupancy 100%

WALE 4.7 years

Tenancy Multi-tenant

Review type/s Fixed annual reviews

Average gross passing rent $457 psm

Average gross market rent $420 psm

Date acquired October 2006

Book value $87.6 million

Valuation $87.6 million

Valuation date June 2012

Capitalisation rate 8.25%

NABERS energy rating 4.5 star

Property description

The property is located in Belconnen, approximately 10 kilometres north-west of the Canberra CBD. The ‘A’ grade building was completed in 2002 as the national headquarters for the Australian Bureau of Statistics (ABS), and comprises two seven-level office wings joined by a glazed roof atrium. The property provides basement parking for 60 vehicles and on-grade for 340 vehicles.

Major tenants

% Lease leased 1 expiry

Government 99 FY 2017

31 Queen Street

31 Queen Street, Melbourne, VIC

Property details

Ownership interest 100%

Net lettable area 19,339 sqm

Car spaces 172

Occupancy 97.4%

WALE 3.7 years

Tenancy Multi-tenant

Review type/s Mix of CPI-linked and fixed reviews

Average gross passing rent 2 $456 psm

Average gross market rent 2 $471 psm

Date acquired March 2011

Book value $91.0 million

Valuation $91.0 million

Valuation date June 2012

Capitalisation rate 8.00%

NABERS energy rating 2.5 star

Property description

A 27-level office building comprising ground floor retail, 21 upper levels of office accommodation and five levels of basement parking for 172 vehicles. The building has recently undergone a progressive refurbishment program including upgrade of the ground floor foyer and facade, lifts, numerous upper level lift lobbies, and major items of plant and equipment.

Major tenants

% Lease leased 1 expiry

OZ Minerals 14.0 FY 2013/ FY 2016

Defence Bank 8.3 FY 2021Hyder Consulting 10.3 FY 2016

DIAC Building

6 Chan Street, Belconnen, ACT

Property details

Ownership interest 60%

Net lettable area 29,530 sqm

Car spaces 525

Occupancy 100%

WALE 7.3 years

Tenancy Multi-tenant

Review type/s Fixed annual reviews

Average gross passing rent 2 $347 psm

Average gross market rent 2 $375 psm

Date acquired October 2006

Book value $69.0 million

Valuation $69.0 million

Valuation date June 2012

Capitalisation rate 8.00%

NABERS energy rating 4.5 star

Property description

The property is located in Belconnen, approximately 10 kilometres north-west of the Canberra CBD. The ‘A’ grade building was completed in November 2004 as the national headquarters for the Department of Immigration and Citizenship (DIAC), and comprises two six-level office wings, basement parking for 100 vehicles and on-grade for approximately 425 vehicles. The site also includes vacant land available for development.

Major tenants

% Lease leased 1 expiry

Government 97.8 FY 2020

1 % of gross income.2 Office only.

The Forum, Cisco

201 Pacific Highway, St Leonards, NSW

Property details

Ownership interest 60%

Net lettable area 16,584 sqm

Car spaces 262

Occupancy 99.1%

WALE 2.4 years

Tenancy Multi-tenant

Review type/s Mix of turnover-linked, CPI-linked and fixed reviews

Average gross passing rent 2 $576 psm

Average gross market rent 2 $548 psm

Date acquired October 2006

Book value $63.1 million

Valuation $63.1 million

Valuation date June 2012

Capitalisation rate 8.25%

NABERS energy rating 3 star

Property description

The property is a landmark development located directly above the St Leonards railway station on Sydney’s lower north shore, approximately six kilometres north of the Sydney CBD. The ‘A’ grade building was completed in 2000 and comprises 20 retail tenancies, 10 floors of office accommodation and basement parking for 262 vehicles.

Major tenants

% Lease leased 1 expiry

Cisco Systems 36.6 FY 2014

Flexi Rent 23.6 FY 2015

HCN 7.2 FY 2017

NAB 6.5 FY 2018

12

Discovery House

47 Bowes Street, Woden, ACT

Property details

Ownership interest 60%

Net lettable area 22,239 sqm

Car spaces 238

Occupancy 100%

WALE 10.2 years

Tenancy Single-tenant

Review type/s Fixed annual reviews

Average gross passing rent 2 $415 psm

Average gross market rent 2 $415 psm

Date acquired October 2006

Book value $61.4 million

Valuation $61.4 million

Valuation date June 2012

Capitalisation rate 7.75%

NABERS energy rating Stage 1 – 4.5 star Stage 2 – 5 star

Property description

The property is located in Woden, approximately 10 kilometres south of the Canberra CBD. The property comprises two stages, the first completed in 1997 and the second in 2007, when the building was extended and IP Australia renewed its lease for 15 years.

The whole building now comprises a well integrated design and construction between the new and old sections, with contemporary accommodation and finishes. The total accommodation comprises 20,642 sqm of office, 1,441 sqm of storage, 156 sqm of retail (café), 180 basement and 58 on-grade car spaces.

Major tenants

% Lease leased 1 expiry

Government 100 FY 2023

Makerston House

30 Makerston Street, Brisbane, QLD

Property details

Ownership interest 60%

Net lettable area 14,652 sqm

Car spaces 180

Occupancy 100%

WALE 2.8 years

Tenancy Multi-tenant

Review type/s Fixed annual reviews

Average gross passing rent 2 $509 psm

Average gross market rent 2 $520 psm

Date acquired October 2006

Book value $45.1 million

Valuation $45.1 million

Valuation date June 2012

Capitalisation rate 8.50%

NABERS energy rating 4.5 star

Property description

The property is located on the western fringe of the legal precinct of the Brisbane CBD, approximately 65 metres south-west of the Brisbane Transit Centre. The building comprises a ground floor, 11 upper levels of office and five levels of basement parking and storage.

Major tenants

% Lease leased 1 expiry

QLD Police 34.8 FY 2015

Tourism Queensland 26.3 FY 2013/ FY2019

Shine Lawyers 13.8 FY2016

Property summaries (continued)

13

Challenger Diversified Property Group Annual Report 2012 Challenger Diversified Property Group Annual Report 2012

1 % of gross income.2 Office only.

The Forum, Verizon

203 Pacific Highway, St Leonards, NSW

Property details

Ownership interest 60%

Net lettable area 11,711 sqm

Car spaces 151

Occupancy 69.0%

WALE 3.2 years

Tenancy Multi-tenant

Review type/s Mixture of fixed, market and CPI-linked reviews

Average gross passing rent 2 $534 psm

Average gross market rent 2 $526 psm

Date acquired October 2006

Book value $41.8 million

Valuation $41.8 million

Valuation date June 2012

Capitalisation rate 8.50%

NABERS energy rating 3 star

Property description

The property is a landmark development located directly above the St Leonards railway station on Sydney’s lower north shore, approximately six kilometres north of the Sydney CBD. The ‘A’ grade building was completed in 2000 and comprises seven retail tenancies, 10 floors of office accommodation and basement parking for 151 vehicles.

Major tenants

% Lease leased 1 expiry

Verizon 27.3 FY 2015

Cardno 28.1 FY 2019

Elder House

27-39 Currie Street, Adelaide, SA

Property details

Ownership interest 60%

Net lettable area 14,086 sqm

Car spaces 0

Occupancy 100%

WALE 3.8 years

Tenancy Single-tenant

Review type/s Fixed annual reviews

Average gross passing rent2 $434 psm

Average gross market rent2 $368 psm

Date acquired October 2006

Book value $27.9 million

Valuation $27.9 million

Valuation date June 2012

Capitalisation rate 9.00%

NABERS energy rating 3.5 star

Property description

The property is located in the core of the Adelaide CBD, and incorporates the heritage section of the former Elder House, constructed in 1940. The ‘A’ grade building comprises a ground level, six upper levels of office accommodation and a basement area, all of which were substantially refurbished and extended in 2001.

Major tenants

% Lease leased 1 expiry

Elders Limited 100 FY 2016

Executive Building

15 Murray Street, Hobart, TAS

Property details

Ownership interest 60%

Net lettable area 9,887 sqm

Car spaces 125

Occupancy 100%

WALE 3.0 years

Tenancy Single-tenant

Review type/s Market reviews

Average gross passing rent $379 psm

Average gross market rent 2 $389 psm

Date acquired October 2006

Book value $20.4 million

Valuation $20.4 million

Valuation date June 2012

Capitalisation rate 8.75%

NABERS energy rating 3.5 star

Property description

The property is located in the core of the Hobart CBD. The ‘A’ grade building was completed in March 1987 and comprises nine levels of modern office accommodation and two levels of parking for 125 vehicles.

Major tenants

% Lease leased 1 expiry

The Crown in Right of 100 FY 2015 the State of Tasmania

Innaloo Cinema Centre

57 Liege Street, Woodlands, Perth, WA

Property details

Ownership interest 60%

Net lettable area 11,549 sqm

Car spaces 1,046

Occupancy 100%

WALE 6.1 years

Tenancy Multi-tenant

Review type/s Mix of CPI-linked, fixed and market reviews

Average gross passing rent $388 psm

Average gross market rent $388 psm

Date acquired October 2006

Book value $25.5 million

Valuation $25.5 million

Valuation date June 2012

Capitalisation rate 8.00%

Property description

The property is located in Woodlands, approximately 11 kilometres north-west of the Perth CBD. Originally a small cinema and drive-in complex, the property has undergone a staged redevelopment and today comprises a modern 16-screen cinema complex with on-site parking for in excess of 1,046 vehicles.

Major tenants

% Lease leased 1 expiry

Greater Union 75.1 FY 2019

Sizzlers 8.8 FY 2020

14

Jam Factory

500 Chapel Street, South Yarra, VIC

Property details

Ownership interest 60%

Net lettable area 3 20,127 sqm

Car spaces 970

Occupancy 98.7%

WALE 8.0 years

Tenancy Multi-tenant

Review type/s Mix of CPI-linked and fixed reviews

Average gross passing rent $517 psm

Average gross market rent $517 psm

Date acquired October 2006

Book value $71.1 million

Valuation $71.1 million

Valuation date June 2012

Capitalisation rate 7.75%

Property description

The property is located on Chapel Street, South Yarra, approximately six kilometres south-east of the Melbourne CBD. Originally a manufacturing plant for jams and preserves, the property has been converted into a popular cinema and retail complex. The building comprises a 15-screen cinema complex, a retail precinct, level two office precinct and a five-level car park for 970 vehicles.

Major tenants

% Lease leased 1 expiry

Village Cinemas 31.6 FY 2018

Village Office 20.6 FY 2025

Topshop 7.2 FY 2022

Property summaries (continued)

1 % of gross income.2 Initial 60% purchased October 2006, balance purchased 30 June 2008.3 Ex Strategy’s/Development vacancy.

Century City Walk

285-287 Springvale Road, Glen Waverley, VIC

Property details

Ownership interest 100%

Net lettable area 8,289 sqm

Car spaces N/A

Occupancy 100%

WALE 5.2 years

Tenancy Multi-tenant

Review type/s Mix of CPI-linked and fixed reviews

Average gross passing rent $443 psm

Average gross market rent $443 psm

Date acquired 2 June 2008

Book value $30.0 million

Valuation $30.0 million

Valuation date June 2012

Capitalisation rate 8.50%

Property description

The property is located adjacent to the Novotel Hotel on Springvale Road, Glen Waverley, approximately 26 kilometres south-east of the Melbourne CBD. The building was originally completed in 1998 and refurbished in 2010. It comprises a 10-screen cinema centre, Strike bowling alley, seven restaurant and café tenancies and a bar plus gaming area situated around a ground level pedestrian mall.

Major tenants

% Lease leased 1 expiry

Village Cinemas 46.0 FY 2020

Century City 20.1 FY 2015 Entertainment

15

Challenger Diversified Property Group Annual Report 2012 Challenger Diversified Property Group Annual Report 2012

1 % of gross income.2 Development completion date.

Kings Langley Shopping Centre

13 Ravenhill Street, Kings Langley, NSW

Property details

Ownership interest 60%

Net lettable area 4,157 sqm

Car spaces 140

Occupancy 100%

WALE 7.4 years

Tenancy Multi-tenant

Review type/s Mix of turnover-linked, CPI-linked and fixed reviews

Average gross passing rent $420 psm

Average gross market rent $420 psm

Date acquired October 2006

Book value $9.4 million

Valuation $9.4 million

Valuation date June 2012

Capitalisation rate 8.75%

Property description

The property is located in Kings Langley, approximately 40 kilometres north-west of the Sydney CBD. The property is a neighbourhood shopping centre which comprises a Woolworths supermarket, a mezzanine area, nine specialty retail shops and on-site parking for 140 vehicles.

Major tenants

% Lease leased 1 expiry

Woolworths 66.0 FY 2022

Network Video 5.0 FY 2016

Commonwealth Bank 7.0 FY 2018 of Australia

The Junction Industrial Park (Stage 2)

34-48 Cosgrove Road Enfield, NSW

Property details

Ownership interest 100%

Net lettable area 20,360 sqm

Car spaces 155

Occupancy 99%

WALE 9.9 years

Tenancy Multi-tenant

Review type/s Mix CPI/Fixed with market

Average gross passing rent $146 psm

Average gross market rent $146 psm

Date acquired 2 July 2012

Book value $34 million

Valuation $34 million

Valuation date June 2012

Capitalisation rate 7.75%

Property description

CDI has secured a 10-year lease pre-commitment with Bunzl Australasia Limited for construction of a new 20,200 sqm distribution facility on Stage 2, with the Stage 2 development also including 150 sqm of café facilities. Construction commenced in September 2011 and practical completion was achieved 2 July 2012, with rent commencement 3 July 2012.

Major tenants

% Lease leased 1 expiry

Bunzl Australasia 99.3 FY 2022 Limited

The Junction Industrial Park (Stage 1)

34-48 Cosgrove Road, Enfield, NSW

Property details

Ownership interest 100%

Net lettable area 13,437 sqm

Car spaces 73

Occupancy 100%

WALE 3.5 years

Tenancy Single-tenant

Review type/s Fixed annual reviews

Average gross passing rent $152 psm

Average gross market rent $146 psm

Date acquired 2 December 2008

Book value $20.4 million

Valuation $20.4 million

Valuation date June 2012

Capitalisation rate 8.50%

Property description

The property comprises a recently constructed industrial facility extending to a lettable area of 13,437 sqm.

The property is located on the fringe of the established central Sydney suburb of Enfield.

Major tenants

% Lease leased 1 expiry

K.W. Doggetts 100 FY 2016

1 % of gross income.16

Property summaries (continued)

12-30 Toll Drive

12-30 Toll Drive, Altona North, VIC

Property details

Ownership interest 100%

Net lettable area 13,885 sqm

Car spaces 215

Occupancy 100%

WALE 3.6 years

Tenancy Single-tenant

Review type/s Fixed annual reviews

Average gross passing rent $114 psm

Average gross market rent $107 psm

Date acquired October 2006

Book value $14.0 million

Valuation $14.0 million

Valuation date June 2012

Capitalisation rate 8.75%

Property description

The property is located in Altona North, approximately 12 kilometres south-west of the Melbourne CBD. The site includes a warehouse facility, office accommodation, hardstand space, a security gatehouse, canopied areas, a weigh bridge, landscaping and parking for 215 vehicles.

Major tenants

% Lease leased 1 expiry

Toll Transport Pty Ltd 100 FY 2016

Spotlight

217-225 Boundary Road, Laverton North, VIC

Property details

Ownership interest 100%

Net lettable area 20,723 sqm

Car spaces N/A

Occupancy 100%

WALE 9.0 years

Tenancy Single-tenant

Review type/s Fixed annual reviews

Average gross passing rent $77 psm

Average gross market rent $77 psm

Date acquired October 2006

Book value $17.3 million

Valuation $17.3 million

Valuation date June 2012

Capitalisation rate 8.25%

Property description

The property is located on Boundary Road, Laverton North, approximately 15 kilometres west of the Melbourne CBD. This is an established industrial area that is well serviced by major roads including Princes Freeway, which provides excellent access to the Western Ring Road, Westgate Freeway and Melbourne CityLink. The building was completed in November 1999 and comprises warehouse and office facilities which were purpose built for Spotlight Stores Pty Ltd.

Major tenants

% Lease leased 1 expiry

Spotlight Stores Pty Ltd 100 FY 2021

6 Foray Street

6 Foray Street, Fairfield, NSW

Property details

Ownership interest 100%

Net lettable area 22,960 sqm

Car spaces N/A

Occupancy 71.6%

WALE 2.1 years

Tenancy Multi-tenant

Review type/s Fixed annual reviews

Average gross passing rent $90 psm

Average gross market rent $88 psm

Date acquired October 2006

Book value $15.3 million

Valuation $15.3 million

Valuation date June 2012

Capitalisation rate 10.00%

Property description

The property is located at Fairfield, approximately 29 kilometres west of the Sydney CBD, within close proximity of several major arterial roads including the Cumberland Highway, the M4 Motorway, Horsley Drive and Woodville Road. The property has been developed in various stages over the past 30 years, and today comprises two main manufacturing and warehouse buildings, commercial office facilities and a large parking area.

Major tenants

% Lease leased 1 expiry

IFC Warehousing 71.6 FY 2015 and Distribution

1 % of gross income. 17

Challenger Diversified Property Group Annual Report 2012 Challenger Diversified Property Group Annual Report 2012

1 % of gross income.2 Office only.

2-10 Toll Drive

2-10 Toll Drive, Altona North, VIC

Property details

Ownership interest 100%

Net lettable area 6,244 sqm

Car spaces N/A

Occupancy 100%

WALE 0.6 years

Tenancy Single-tenant

Review type/s Fixed annual reviews

Average gross passing rent $125 psm

Average gross market rent $110 psm

Date acquired October 2006

Book value $6.4 million

Valuation $6.4 million

Valuation date June 2012

Capitalisation rate 8.57%

Property description

The property is located in Altona North, approximately 12 kilometres south-west of the Melbourne CBD. The site includes a warehouse facility, office accommodation, hardstand space and canopied areas.

Major tenants

% Lease leased 1 expiry

Toll Transport Pty Ltd 100 FY 2013

1-9 Toll Drive

1-9 Toll Drive, Altona North, VIC

Property details

Ownership interest 100%

Net lettable area 3,239 sqm

Car spaces 42

Occupancy 100%

WALE 3.6 years

Tenancy Single-tenant

Review type/s Fixed annual reviews

Average gross passing rent $134 psm

Average gross market rent $133 psm

Date acquired October 2006

Book value $3.9 million

Valuation $3.9 million

Valuation date June 2012

Capitalisation rate 8.50%

Property description

The property is located in Altona North, approximately 12 kilometres south-west of the Melbourne CBD. The site is currently utilised as a truck depot and comprises a single-level office, amenities and sleeping quarters building, a high clearance mechanic workshop and truck wash facility and a large four-bay undercover fuelling station. It also includes hardstand space and truck manoeuvring areas, landscaping and parking for 42 vehicles.

Major tenants

% Lease leased 1 expiry

Toll Transport Pty Ltd 100 FY 2016

Taylors House

965 Bourke Street, Waterloo, NSW

Property details

Ownership interest 60%

Net lettable area 11,084 sqm

Car spaces 96

Occupancy 99.2%

WALE 4.7 years

Tenancy Multi-tenant

Review type/s Fixed annual reviews

Average gross passing rent 2 $465 psm

Average gross market rent 2 $377 psm

Date acquired October 2006

Book value $26.9 million

Valuation $26.9 million

Valuation date June 2012

Capitalisation rate 8.25%

NABERS energy rating Exempt

Property description

The property is located in Waterloo, approximately five kilometres south of the Sydney CBD. The building was completed in January 2001, and comprises a ground floor retail area, four levels of office and college accommodation and basement parking for 96 vehicles.

Major tenants

% Lease leased 1 expiry

Taylors College 84.0 FY 2018

Possum Furniture 7.4 FY 2013

18

Property summaries (continued)

Property details

Ownership interest 60%

Net lettable area 9,312 sqm

Car spaces 350

Occupancy 24.9%

WALE 1.0 years

Tenancy Multi-tenant

Review type/s Fixed annual reviews

Average gross passing rent $303 psm

Average gross market rent $296 psm

Date acquired October 2006

Book value $13.6 million

Valuation $13.6 million

Valuation date June 2012

Capitalisation rate 9.50%

NABERS energy rating Exempt

Property description

A modern commercial building located in a prime commercial/industrial high tech precinct on a corner allotment enjoying three street frontages in close proximity to the Melbourne CBD and major transport linkages (Westgate Freeway and CityLink Tollway). The property provides three levels of modern office accommodation, together with ancillary laboratory and warehouse/storage areas. 333 undercover car parks are provided on-site over two levels, plus 17 original parking spaces fronting Wirraway Drive.

Major tenants

% Lease leased 1 expiry

George Western 24.9 FY 2017

187 Todd Road

187 Todd Road, Port Melbourne, VIC

Property details

Ownership interest 100%

Net lettable area 15,500 sqm

Car spaces N/A

Occupancy 100%

WALE 5.5 years

Tenancy Single-tenant

Review type/s Annual reviews to INSEE Construction Cost Index

Average gross passing rent a84 psm ($104 psm)

Average gross market rent a67 psm ($83 psm)

Date acquired June 2007

Book value a8.9 million ($11.1 million)

Valuation a8.9 million ($11.1 million)

Valuation date June 2012

Capitalisation rate 9.20%

Property description

The property is a modern factory and office headquarters located approximately 50 kilometres east of Orleans and 160 kilometres south of Paris. The property is leased to Inteva, a major European car component manufacturer.

Major tenants

% Lease leased 1 expiry

Inteva 100 FY 2018

Sully

105 Route d’Orleans, Sully sur Loire, France

1 % of gross income.2 Excludes amenities.

Property details

Ownership interest 100%

Net lettable area 2 5,972 sqm

Car spaces 133

Occupancy –

WALE 0 years

Tenancy Vacant

Review type/s N/A

Average gross passing rent NIL psm

Average gross market rent $262 psm

Date acquired June 2008

Book value $9.9 million

Valuation $9.9 million

Valuation date June 2012

Capitalisation rate 9.50%

NABERS energy rating 1.5 star

Property description

This is a key strategic holding approximately 12 kilometres north-west of the Sydney CBD within close proximity to Lane Cove Road and the new Chatswood-Epping rail link. Within 200 metres of Macquarie Park station, the site offers potential for capital growth through future redevelopment. The property comprises a two-storey office building with an attached high clearance warehouse to the rear and on-grade parking for 133 vehicles.

Major tenants

% Lease leased 1 expiry

Vacant

Giffnock Avenue

2-4 Giffnock Avenue, North Ryde, NSW

1 % of gross income.

Property details

Ownership interest 100%

Net lettable area 5,105 sqm

Car spaces 285

Occupancy 100%

WALE 3.3 years

Tenancy Single-tenant

Review type/s Annual reviews to INSEE Construction Cost Index

Average gross passing rent a175 psm ($217 psm)

Average gross market rent a156 psm ($193 psm)

Date acquired June 2007

Book value a9.3 million ($11.5 million)

Valuation a9.3 million ($11.5 million)

Valuation date June 2012

Capitalisation rate 6.25%

Property description

The property is a modern retail warehouse located in a suburban centre approximately 19 kilometres to the north-east of central Paris in a high tech industrial precinct. The property is leased to Bricoman, a hardware retailer.

Major tenants

% Lease leased 1 expiry

Bricoman 100 FY 2016

19

Challenger Diversified Property Group Annual Report 2012 Challenger Diversified Property Group Annual Report 2012

Aulnay

54 Avenue de Savigny, Aulnay sous Bois, Paris, France

Property details

Ownership interest 100%

Net lettable area 8,944 sqm

Car spaces N/A

Occupancy 100%

WALE 3.2 years

Tenancy Single-tenant

Review type/s Annual reviews to INSEE Construction Cost Index

Average gross passing rent a91 psm ($113 psm)

Average gross market rent a83 psm ($103 psm)

Date acquired June 2007

Book value a8.2 million ($10.2 million)

Valuation a8.2 million ($10.2 million)

Valuation date June 2012

Capitalisation rate 8.25%

Property description

The property is a modern chillstore/logistics facility located in Béziers’ prime logistics estate adjacent to the A9 – the main east/west road link between Spain, France and Italy. The property is leased to Exel, a major French logistics and distribution operator.

Major tenants

% Lease leased 1 expiry

Exel 100 FY 20192

Béziers

Rue Charles Nicolle, Villeneuve-lès-Béziers, France

Property details

Ownership interest 100% (Leasehold until 2047)

Net lettable area 7,409 sqm

Car spaces N/A

Occupancy 100%

WALE 8.7 years

Tenancy Single-tenant

Review type/s Annual reviews to INSEE Construction Cost Index

Average gross passing rent a108 psm ($134 psm)

Average gross market rent a108 psm ($134 psm)

Date acquired June 2007

Book value a7.2 million ($9.0 million)

Valuation a7.2 million ($9.0 million)

Valuation date June 2012

Capitalisation rate 7.10%

Property description

The property is a modern industrial warehouse facility located in the established North Paris mixed commercial area of Zac de Louvresses. The property is leased to GrDF, a major French gas supplier and distributor.

Major tenants

% Lease leased 1 expiry

GrDF 100 FY 2021

Gennevilliers

ZAC des Louvresses, Gennevilliers, Paris, France

1 % of gross income.2 Tenant can break lease in FY 2016 and this is reflected in the WALE.

1 % of gross income.2 Tenant can break lease in FY 2019 and this is reflected in the WALE.20

Property summaries (continued)

Tours

ZI du Papillon, Parcay-Meslay, Tours, France

Property details

Ownership interest 100%

Net lettable area 5,610 sqm

Car spaces N/A

Occupancy 100%

WALE 6.2 years

Tenancy Single-tenant

Review type/s Annual reviews to INSEE Construction Cost Index

Average gross passing rent a94 psm ($116 psm)

Average gross market rent a85 psm ($105 psm)

Date acquired June 2007

Book value a4.4 million ($5.4 million)

Valuation a4.4 million ($5.4 million)

Valuation date June 2012

Capitalisation rate 8.65%

Property description

The property is a modern chillstore/logistics facility centrally located in a prime logistics park in Tours, the regional centre of the Indie et Loire. The property is leased to ATAC, a major French logistics and distribution operator.

Major tenants

% Lease leased 1 expiry

ATAC 100 FY 20222

The Junction Industrial Park (Stage 3)

34-48 Cosgrove Road Enfield, NSW

Property details

Ownership Interest 100%

Property description

The 8.56 ha site is located near the intersection of the Hume Highway and Roberts Road and opposite the Enfield Intermodal Logistics Centre in the established central western industrial area of Enfield.

Stage 1 and 2 comprising 33,637 sqm of warehouse facilities are fully leased and CDI is continuing to pursue a tenant pre-commitment for Stage 3.

Stage 3 comprises the remaining developable portion of the site, extending to an area of 22,828 sqm with master plan approval to construct a 12,660 sqm warehouse/distribution facility.

Property details

Ownership interest 100%

Property description

In May 2008, CDI signed two leases and a development deed with the Royal Botanic Gardens Trust (BGT) to manage and upgrade the Domain car park. CDI has two leases – four years and 21 years. The Domain car park is a three-level 1,123 bay car park located in close proximity to Sydney’s midcity CBD, the Royal Botanic Gardens and the Art Gallery of NSW. The car park is one of the largest car parks in Sydney and benefits from recent refurbishment works including lift installations, increased upgrades to building safety and security systems.

Refurbishment works reached practical completion on 18 July.

Domain

Royal Botanic Gardens, Sydney, NSW

21

Challenger Diversified Property Group Annual Report 2012 Challenger Diversified Property Group Annual Report 2012

About Challenger

Challenger Limited (Challenger) (ASX: CGF) is an ASX listed investment management firm originally established in 1985, with assets under management of A$31 billion at balance date.

Challenger is the leading issuer in Australia and provider of alternative retirement income solutions. Through Fidante Partners, our boutique stable, and the aligned investments business, Challenger is also the leading provider of investment products in Australia.

Challenger Life Company is a leading provider of annuities and alternative retirement income solutions in Australia. Via an Australian Prudential Regulation Authority (‘APRA’) regulated life company, we offer attractive returns and capital protection for our customers, making our annuities well suited to retirement income planning. Annuity premia, along with shareholder and other capital, are invested in a diversified portfolio of assets to deliver predictable, long-term cash flows to meet commitments to our annuitants while providing attractive returns for shareholders.

Challenger’s Funds Management is one of Australia’s long established and fastest growing funds management businesses. Challenger offers a wide range of fiduciary investment choices across a variety of asset classes and investment styles. Through Aligned Investment teams, we manage assets for Challenger Life and third party investors. Through our Boutique Partnership platform, we partner with a diverse array of independent fund managers in which we own equity stakes and provide distribution and administration support.

22

The Responsible Entity’s approach to corporate governance

The Board of the Responsible Entity (the Responsible Entity) recognises its duties and obligations to stakeholders to implement and maintain a robust system of corporate governance. The Responsible Entity believes that the adoption of good corporate governance adds real value to stakeholders and enhances investor confidence.

The Responsible Entity determines the most appropriate corporate governance arrangements for Challenger Diversified Property Group (CDI), taking into consideration Australian and international standards. This statement reflects the Responsible Entity’s corporate governance system as at August 2012.

This statement reports against the ASX Corporate Governance Council’s ‘Corporate Governance Principles and Recommendations’ as amended in 2010. As required by the ASX Listing Rules, this statement sets out the extent to which CDI has followed the principles or, where appropriate, indicates a departure from them with an explanation.

Principle 1 Lay solid foundations for management and oversightThe role of the Responsible Entity and delegations

The role of the Responsible Entity is to manage CDI in the unitholders’ best interests in accordance with CDI’s constitution and the Corporations Act 2001 (Cth) (Corporations Act). The Responsible Entity is accountable to unitholders for the activities and performance of CDI by overseeing the development of sustainable fund value within an appropriate framework of risk, and regard for all stakeholder

interests. The Responsible Entity has identified the key functions which it has reserved for itself. These duties are outlined below and set out in the Board Charter, a copy of which is available on CDI’s website www.challenger.com.au/cdi:

• approvalofthestrategyandannual budgets of the Funds;

• approvalofaccountingpoliciesand financial reports of the Funds;

• approvalofthefinancialandoperating policies;

• approvalofcorporategovernancestructure and monitoring of the performance and effectiveness of the corporate governance policies and procedures;

• oversightoftheestablishmentand maintenance of effective risk management policies and processes;

• evaluationandapprovalofacquisitions and investments and other corporate actions of the Fund;

• thepowertoissueunitsinaScheme;

• theissuanceofaProductDisclosure Statement;

• monitoringtheperformanceofthe Manager; and

• theevaluationoftheperformanceof the Board, Board Committees and individual Directors.

The Board has established a Committee to assist in carrying out its responsibilities and to consider certain issues and functions in detail. The Board Committee is discussed in Principle 2 below.

Non-executive Directors are issued with formal letters of appointment governing their role and responsibilities. The responsibilities of the Chair and the Directors are also set out in the Board Charter.

Management responsibility

The Corporations Act empowers the Responsible Entity to engage agents on its behalf; however, it remains fully responsible for the actions of those agents. The Responsible Entity has appointed Challenger Management Services Limited to manage CDI. Challenger Management Services Limited and the Responsible Entity are wholly owned subsidiaries of Challenger Limited (Challenger).

The Board has delegated to CDI’s Fund Manager the authority and powers necessary to implement the strategies approved by the Board for CDI and to manage the business affairs of CDI within the policies and specific delegation limits specified by the Board from time to time.

CDI’s constitution governs, among other things, how CDI will operate, how the Responsible Entity remuneration will be calculated and the rights of unitholders. The Responsible Entity must also prepare and lodge a compliance plan with the Australian Securities and Investments Commission (ASIC). The compliance plan sets out the mechanism the Responsible Entity has in place to ensure compliance with CDI’s constitution and the Corporations Act.

Relationship with Challenger Group

The corporate governance structure adopted by the Responsible Entity reflects its role as the Responsible Entity of CDI. In several ways, this will be different to the corporate governance structure of a listed company.

Challenger has expertise in developing and managing specialist investment funds in the areas of property and infrastructure.

Corporate governance statement

Challenger Diversified Property Group Annual Report 2012

23

The Responsible Entity makes extensive use of the resources available within Challenger in managing CDI.

The resources provided to assist the Responsible Entity to fulfil its role include the services of senior executives and responsible officers. Challenger appoints the executive Directors to the Responsible Entity Board and the Responsible Entity appoints appropriately skilled independent Directors to ensure that there is a majority of independent Directors and that CDI continues to be managed to maximise return to unitholders within CDI’s stated strategy and mandate.

Executive performance assessment

The performance of the Chief Executive, Funds Management and senior executives is reviewed at least annually against appropriately agreed and documented performance objectives and measures, consistent with the Performance Management Framework that applies to all Challenger employees. All Challenger Group employees are also assessed against the Challenger Corporate Principles (refer to Principle 3 below).

Performance evaluations for the Chief Executive, Funds Management and senior executives have taken place in respect of the 2012 reporting period in accordance with the above process.

Principle 2 Structure the Board to add valueMembership of the Board

The Board comprises Directors who possess an appropriate range of skills, experience and expertise to:

• haveaproperunderstandingof,and competence to deal with, the current and emerging issues of the business;

• exerciseindependentjudgement;

• encourageenhancedperformanceof the Fund; and

• effectivelyreviewandchallengethe performance of management.

The Responsible Entity’s constitution provides for a minimum of three Directors and a maximum of 12 Directors. The table below summarises the current composition of the Board. Background details of each Director are set out in the Directors’ report.

Nominations and appointment of new Directors

The Board of the Responsible Entity appoints the independent Directors, having regard to maintaining a majority of independent Directors and to ensuring an appropriate balance of skills, experience and competence on the Board. All new Directors are provided with an appropriate induction into the Responsible Entity’s business.

The Board has not appointed a formal nominations committee. This represents a departure from the ASX principles.

Review of Board performance

The Board Charter sets out the requirement for a formal review of the Board and individual Directors’ performance annually. A review of the Board and Directors’ performance was conducted in June 2012. The review involves consideration of the effectiveness of the Directors individually, and the effectiveness of the Board and the Audit and Compliance Committee, having regard to the knowledge, skills and experience of the Directors. The outcomes of the review were provided for discussion by the Board. The review indicated that the Board is performing soundly.

Independent Directors

The Responsible Entity has adopted an Independence Policy that states that an independent Director should be independent of management and free from any business or other relationship that could materially interfere with, or could reasonably be perceived to materially interfere with, the independent exercise of their judgement.

The Board regularly considers and assesses the independence of each Director in light of the interests and information which Directors disclose. In accordance with the Corporations Act, Directors are required to advise the Responsible Entity of any material personal interests they have in a matter.

Name Position Independent First appointed

Michael Cole Non-executive Chair Yes 2008

Ian Martens Non-executive Director Yes 2003

Ian Moore Non-executive Director Yes 2005

Geoff McWilliam Non-executive Director Yes 2006

Brendan O’Connor Executive Director No 2008

Rob Woods Executive Director No 2004

The roles of Chair and Chief Executive are not exercised by the same person.

24

In assessing independence, the Board will have regard to whether the Director has any of the following relationships with the Responsible Entity:

1. is a substantial shareholder (as defined by section 9 of the Corporations Act) of the Responsible Entity, or is a director or officer of, or otherwise associated directly with, a substantial shareholder of the Responsible Entity;

2. is employed, or has previously been employed in an executive capacity by a Challenger Group company, and there has not been a period of at least three years between ceasing such employment and serving on the Board;

3. has within the last three years been a principal of a material professional adviser or a material consultant to the Responsible Entity or another Challenger Group company, or an employee materially associated with the service provided;

4. is a material supplier or customer of the Responsible Entity or other Challenger Group company, or an officer of or otherwise associated directly or indirectly with a material supplier or customer; or

5. has a material contractual relationship with the Responsible Entity or another Challenger Group company other than as a Director.

The Responsible Entity will state its reasons if it considers a Director to be independent notwithstanding the existence of a relationship of the kind referred to in paragraphs 1–5 above.

In accordance with the ASX Corporate Governance Guidance for Independence, there is a majority of independent Directors on the Board.

Conflicts of interest

In accordance with the Board Charter and the Corporations Act, any Director with a material personal interest in a matter being considered by the Board must declare such an interest and may only be present when the matter is being considered at the Board’s discretion. Directors with a material interest may not vote on any matter in which they have declared a personal interest.

Meetings of the Board

During the year, the Board generally meets approximately every six weeks. In addition, the Board may meet whenever necessary to deal with specific matters needing attention between scheduled meetings. The Chief Executive, in consultation with the Chair, establishes the meeting agendas to ensure adequate coverage of strategic, financial and material risk areas throughout the year. The Fund Manager and senior management are invited to attend Board meetings and are available for contact by Non-executive Directors between meetings. The Non-executive Directors hold a private session without any executive involvement at least annually.

Director Board Audit and Compliance Committee

Eligible to attend

Attended Eligible to attend

Attended

M Cole 20 20 7 7

I Martens 20 19 7 7