Challenger Diversified Property Group (ASX: CDI) · PDF fileChallenger Diversified Property...

45

1 Challenger Diversified Property Group (ASX: CDI) Results presentation for half-year ended 31 Dec 2011

Transcript of Challenger Diversified Property Group (ASX: CDI) · PDF fileChallenger Diversified Property...

1

Challenger Diversified Property Group (ASX: CDI)

Results presentation

for half-year ended 31 Dec

2011

2 2

Important notice

Information contained in this publication is current as at 7 February 2012 unless otherwise specified and is provided by Challenger Listed

Investments Limited (ABN 94 055 293 644) (AFSL 236887) (“Challenger”), as Responsible Entity of the Challenger Diversified Property

Trust 1 (ARSN 121 484 606) and the Challenger Diversified Property Trust 2 (ARSN 121 484 713) which together comprise the

Challenger Diversified Property Group (“Group”). This document has been prepared for general information purposes only and not with

regard to any particular recipient’s financial situation, objectives or needs nor to solicit offers or invitations for the Group's securities.

Nothing contained in this document constitutes investment, legal, tax or other advice. Accordingly, recipients should, before acting on

any information in this document, consider its appropriateness, having regard to their objectives, financial situation and needs, and seek

the assistance of their financial or other licensed professional adviser before making any investment decision.

Challenger makes no representation, gives no warranty and does not accept any responsibility for the accuracy or completeness of any

recommendation, information or advice contained herein. To the maximum extent permitted by law, the recipient releases Challenger,

each member of the Challenger Group, their directors, officers, employees, representatives and advisors from any liability (including,

without limitation, in respect of direct, indirect or consequential loss or damage or loss or damage arising by negligence) arising in

relation to any recipient relying on anything contained in or omitted from this document.

Past performance is no guarantee or assurance as to the future performance, profitability or capital value of the Group or its securities.

Any forward looking statements included in this document are by nature subject to significant uncertainties, risks and contingencies,

many of which are outside the control of, and are unknown to, Challenger, so that actual results or events may vary from those forward

looking statements, and the assumptions on which they are based.

Challenger, or persons associated with it, may have an interest in the securities or financial products mentioned in this document and

may earn fees including as a result of transactions in any such securities or financial products.

3 3

Results overview

Operating results • Profit from operating activities: $23.91 million; net property income: $33.8 million

• Statutory net profit after tax: $18.8 million, impacted by fair value movements

• 1H12 normalised EPU: 2.67 cents; DPU: 2.05 cents

• Net tangible assets (NTA): 68 cpu

• Pro forma balance sheet gearing at 28.9%2

Upgraded guidance • Upgraded FY12 guidance: normalised EPU3 5.0 cents, DPU 4.2 cents

• Due to earnings upside from extended timetable of French sales and the

strong operating profit from The Domain car park

Property metrics • Occupancy: 92.9%4; WALE: 5.04 years

• Property valuations up $9.3 million on 30 June 2011

• Challenging leasing market continues

Developments progressing well • The Junction Industrial Park - Bunzl

• The Jam Factory

• The Domain car park

1 For a detailed reconciliation between statutory net profit after tax & profit from operating activities refer to slide 41 2 Pro forma balance sheet gearing post payment of 1H12 distribution in February 2012 3 EPU calculated using profit from operating activities and weighted average units on issue 4 Includes The Junction, Stage 2 “As if Complete”

4

Challenger Diversified Property Group

High yielding quality earnings underpinned by sound property

fundamentals

Domestic focus

Diversified properties with focus on office income

Positioned well for macro volatility

KEY DATA – CDI 31 December 2011

Unit price 6 February 2012 - 10 day VWAP 49 cents

Market capitalisation $434 million

Total assets 31 December 2011 $879 million

Net tangible assets 31 December 2011 68 cents

Discount to NTA Based on 6 February 2012 - 10 day

VWAP

27.9%

Distribution guidance FY12 (per unit) 4.20 cents

DPU yield Based on 6 February 2012 - 10 day

VWAP and FY12 DPU guidance

8.6%

5 5

Strategy…

Talavera Rd North Ryde, NSW

Fund Objective: to provide investors with exposure to a diversified

portfolio of properties generating stable income

returns and potential for capital growth

6

CDI strategic objectives

Portfolio enhancement

Improve leasing metrics

Active capital management

Grow earnings

Close price to NTA gap

Portfolio enhancement

7

• French marketing campaign initiated Q4 2011

• French properties remain on market for orderly sale Domestic focus

• Increase focus on multi tenanted properties

• Reduce exposure to purpose built properties

• Concentrate on properties in deeper leasing markets with strong long term rental growth

Diversify portfolio

• The Junction Industrial Park – Bunzl

• The Jam Factory

• Domain car park Value add

Update on sale of French properties

Marketing campaign initiated Q4

2011

Challenging market conditions in

France and Europe as a whole,

investors remain cautious, with

uncertain economic conditions and

limited credit availability

Properties remain on market for

orderly sale

8

Properties 100% occupied

Portfolio WALE enhanced with

French leasing activity in 2011

Strong net income continues to be

delivered

Improve leasing metrics

9

Office • Lease deals - 7 • Area 6,318 sqm

• Rent $2.3m

Retail • Lease deals - 8 • Area 1,335 sqm

• Rent $561k

Industrial - High Tech Lease deals - 1 Area - 553 sqm

Rent $128k

Total deals completed

Lease deals - 20

Area 44,247 sqm

Gross rent $6.4m

(6.8% of CDI portfolio gross income)

Industrial – Distribution Lease deals - 4 Area 36,041 sqm

Rent $3.4m

Ongoing success with renewals

WALE: 5.0 years

Occupancy: 92.9%

Expiries and vacancies remain

our priority

Note: Area’s based on 100% NLA

Active capital management

Actively managing balance sheet

gearing levels to a 25% – 35%

range

Active management of debt

limits and available liquidity, to

maintain financial flexibility

Judicious use of buyback to date

Buyback cautiously slowed given

current status of asset sales

Efficient management of retained

earnings to fund future

maintenance capex projects and

leasing costs

10

11 11

Results highlights

31 Queen St Melbourne, VIC

12 12

Operating results

Statutory NPAT: $18.8m compared to $30.1m 1H11

Profit from operating activities, $23.9m or 2.67 cpu

Distribution of 2.05 cpu

NTA per unit 68 cents

Distribution payout ratio for 1H12: 75.9%2

1 EPU calculated using profit from operating activities and weighted average units on issue 2 Calculated as distribution to unitholders / profit from operating activities 3 AFFO: available funds from operations

1H12

$ million

1H11

$ million

Net property income 33.8 30.9

Financing costs 6.9 3.7

Profit from operating activities 23.9 24.0

Normalised earnings1 per unit 2.7 2.6

Net profit/(loss) after tax (including unrealised impacts) 18.8 30.1

Cash flow from operating activities 21.4 22.2

Distribution to unitholders 18.1 18.3

Distribution per unit (cents) 2.05 2.00

Operating profit distribution payout ratio2 76% 76%

AFFO3 distribution payout ratio 103% 87%

Undistributed income 15.3 11.6

FY12 earnings guidance – Upgraded

13

Upgraded EPU guidance now

5.0 cents

Significant underlying

assumptions: • No asset sales

• No leasing of major current vacancies

• No performance fee paid

Upgraded DPU guidance of

4.2 cents

Operating profit distribution

payout ratio: 84%

4.7

0.13

0.13

(0.20)

0.11

0.13

5.0

4.5

4.6

4.7

4.8

4.9

5

5.1

Original FY12guidance

Extended sale ofFrench portfolio

Domainoutperformance

Increased downtime Net propertyoutperformance

Finance & opexsavings

FY12 forecast

14 14

Capital management

Inside The Jam Factory Melbourne, VIC

On market buyback

Buyback funded through combination of debt and asset sales

Buyback 30% complete • Total of 29.6m units ($15.2m) acquired (3.2% of issued capital)

Buyback slowed given status of asset sales

Buyback metrics • Average vwap of 51.47 cents compared to market VWAP of 52.75 cents

• Purchased at an average 24% discount to NTA, equivalent to an implied cap rate of 9.7%

• Purchased on average 25% of total market volume

Management continue to believe units are currently undervalued

15

16 16

Debt metrics

Pro forma 31 December 20112

AUD denominated

borrowings

Euro

denominated

borrowings

Total

Borrowings A$206m A$48m1 A$254m

Gearing (debt to total assets) (%) 24.8 100.1 28.9

Covenant gearing (total liabilities to total tangible assets) (%) 27.5 102.7 31.7

Proportion hedged3 (%) 85.1 26.2 73.9

Weighted average hedged term (yrs) 3.0 0.7 2.8

Average cost of drawn debt (including margin) (%) 7.0 3.9 6.4

Weighted average undrawn commitment fee (%) 1.0

1 A$ / € spot rate of 0.7897 as at 31 December 2011; net of deferred borrowing costs 2 Post payment of the 1H12 distribution in February 2012 3 The adverse fair value movement of interest rate swaps during the period was $6.2m

Average cost of Australian drawn debt post refinance – 7.0% • includes average margin of 183 bps on drawn debt

Weighted average undrawn commitment fee: 100 bps

Incremental cost of drawing additional Australian debt - 5.3%

17

Facility expiry profile

Facility limit increased to $300m with no expiries until FY14

Undrawn $42m to fund committed developments and provide financial

flexibility

17

• 31 December 2011 pro forma expiry profile1

1. Pro-forma debt post payment of 1H12 distribution in February 2012 and includes bank guarantees issued by CDI

$25

-

90 100

68

20 -

22

-

50

100

150

200

Jul-12 Jul-13 Jul-14 Jul-15

$m

Expiry

Drawn Undrawn

18 18

Development progress

The Junction Industrial Park – Stage 2 Enfield, NSW

The Junction Industrial Park

Stage 2

GLA 20,200sqm

Lease term 10 yrs

Total project cost - excluding land

$21m

Total project cost - including land

$32m

Initial income yield

on cost (including

land)

8.15%

Target completion June 2012

Expected value on

completion

$34m

Bunzl

19

The project is forecast to complete

within budget

Key activities undertaken to date

include: • Earthwork compaction and piering complete

• Structural steel 79% complete

• Precast concrete 51% complete

• Formwork 70% complete

• Hydraulic services 63% complete

• Cost to complete $14m

Stage 3

Seeking 12,660 sqm pre-

commitment for Stage 3 (final

stage)

Forecast incremental cost for

Stage 3 - $13m

The Jam Factory

Operations World record opening for a Topshop franchise store

– 540 stores in 34 countries

Centre traffic increased by 27% in December 2011

(compared to December 2010)

Tenant refurbishments; Boost (Dec 11) and TGI

Friday’s (May 12)

Wilson Parking appointed to manage car park from

mid March 2012

20

Tenancy remix strategy underway targeting

fashion, food and entertainment

New major brands Topshop, Urban by Target

and Nando’s now open

Food court to open in April 2012.

Car park renovation works to start in March

2012

Cost to complete $6m (60%, CDI share)

Repositioning Works

Project cost $16m (100%)

Target completion July 2012

Value on

commencement

$104m

Expected value on

completion

$123m

Repositioning to make the centre more contemporary, accessible and

sought after by a broader demographic

The Domain car park

Refurbishment Targeting completion May 2012, ahead of contract

completion date 18 July 2012

Key activities undertaken to date include:

• Lift installation 45% complete

• Services upgrades and painting car park pods

complete

• Façade upgrade 95% complete

• Travelator upgrade complete

Forecast to be completed within budget

Cost to complete $2.9m

Operations Occupancy levels above expectations during

refurbishment, delivering above budget financial results

Marketing leveraged key events in locale – Picasso

exhibition, Open Air Cinema, Sydney Festival, Domain

events through summer

21

22 22

Portfolio performance

The Forum St Leonards, NSW

23 23

State of play

Office

• Demand for office space in most markets is likely to be subdued (excluding Perth and Brisbane)

• Incentive levels are forecast to remain high through 2012

• Prime stock with long WALE’s will remain attractive to investors. Cap rates to remain flat until more certainty

exists in the broader global market

Industrial

• Fewer pre-lease deals are expected to be completed in 2012 with many larger requirements satisfied in 2011

• Rents are expected to remain at current levels

• Investment yields are expected to remain static. Limited sales activity expected

Retail

• Pressure on discretionary retail to continue with occupancy costs expected to rise

• Food and restaurant performance complementary to cinema attendance has produced solid results for 2011

and is expected to continue throughout 2012

• Solid Australian cinema box office results for 2011: $1.09bn marginally down from 2010’s record year of

$1.13bn

24

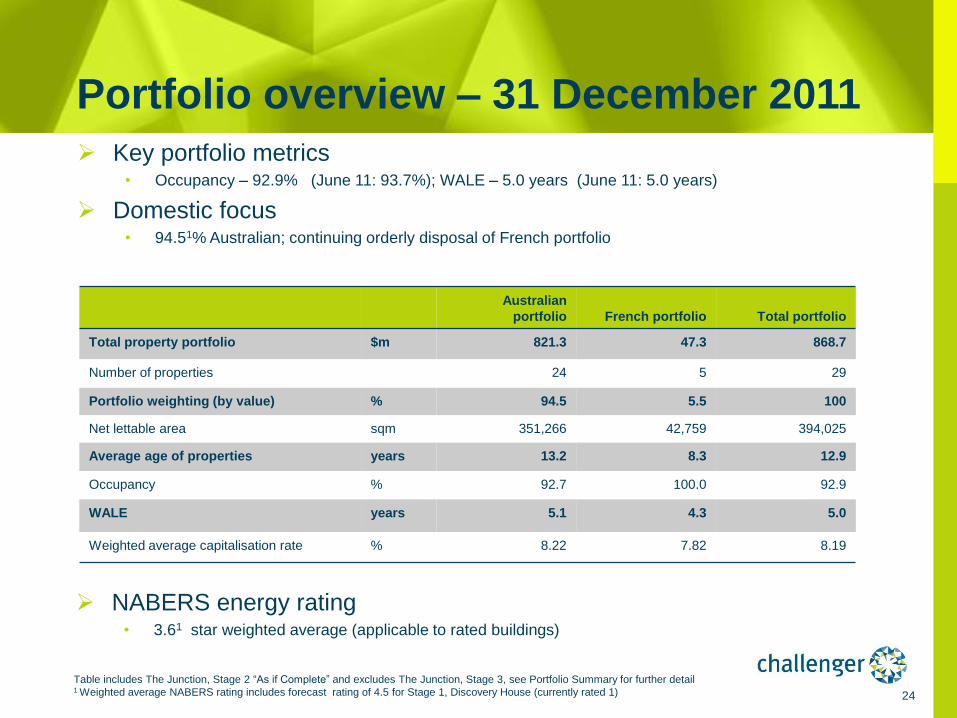

Portfolio overview – 31 December 2011

Australian

portfolio French portfolio Total portfolio

Total property portfolio $m 821.3 47.3 868.7

Number of properties 24 5 29

Portfolio weighting (by value) % 94.5 5.5 100

Net lettable area sqm 351,266 42,759 394,025

Average age of properties years 13.2 8.3 12.9

Occupancy % 92.7 100.0 92.9

WALE years 5.1 4.3 5.0

Weighted average capitalisation rate % 8.22 7.82 8.19

Key portfolio metrics • Occupancy – 92.9% (June 11: 93.7%); WALE – 5.0 years (June 11: 5.0 years)

Domestic focus • 94.51% Australian; continuing orderly disposal of French portfolio

NABERS energy rating • 3.61 star weighted average (applicable to rated buildings)

Table includes The Junction, Stage 2 “As if Complete” and excludes The Junction, Stage 3, see Portfolio Summary for further detail 1 Weighted average NABERS rating includes forecast rating of 4.5 for Stage 1, Discovery House (currently rated 1)

25

Portfolio revaluations at

31 December 2011

Carrying value

($m)

As at 31 Dec 11

Market cap rate

As at 31 Dec 11

Market cap rate

As at 30 Jun 11

Domestic office portfolio 503.4 8.08% 8.07%

Domestic retail portfolio 130.2 8.30% 8.30%

Domestic industrial (distribution centres) 110.8 8.45% 8.56%

Domestic industrial (high tech) 76.9 8.63% 8.64%

TOTAL DOMESTIC PORTFOLIO 821.3 8.22% 8.22%

French portfolio1 47.4 7.82% 7.66%

TOTAL 868.7 8.19% 8.19%

All properties revalued: 46% (by value) independently revalued

Total Portfolio up $9.3m, up 1.1% from FY11 • A-IFRS fair valuation movements down $1.1m

Market capitalisation rates remain unchanged at 8.19%

French portfolio value down 7.7%

Currently trading on an implied cap rate of 10.4%

Table includes The Junction, Stage 2 “As if Complete”, see Portfolio Summary for further detail 1 Converted at 31 December 2011 spot rate (0.7897)

26

Lease expiry profile

(by gross income)

1 Includes The Junction, Stage 2 “As if Complete”

Investment portfolio 92.9%1 occupied

WALE 5.01 years

0.6% 0.4%

1.7% 0.2%

0.1% 1.7%

1.5%

0.9%

1.3%

0.9%

1.5%

1.3% 1.4%

1.1%

0.9%

0.7%

1.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Vacant FY 12 FY 13

Minor Expiry

187 Todd Rd

6 Foray Street

75 Talavera Rd

The Forum,

Verizon

Giffnock

Avenue

Minor Expiry

Retail Expiry

6 Foray Street

31 Queen Street

Minor

Expiry

Retail Expiry

Oz Minerals – 31

Queen St

Village Roadshow

Jam Factory

Tours (France)

Beziers (France)

Makerston Ave

7.1%

3.3%

6.9%

Summary

Jam Factory – Tenants Logos Melbourne, VIC

28 28

Summary

Operating results on target • 1H12 normalised earnings and distribution of 2.67 and 2.05 cpu delivered

• Net tangible assets (NTA): 68 cpu

• Pro forma balance sheet gearing at 28.9%

Property metrics • Investment property valuations up $9.3 million from 30 June 2011

• Occupancy: 92.9%; WALE 5.0 years

Execute on strategy - closing the gap by growing earnings

• Portfolio enhancement strategy

• Active capital management

• Improve leasing metrics

Upgraded FY12 guidance

• Normalised EPU: 5.0 cents; DPU: 4.2 cents

29

Contacts

Trevor Hardie Fund Manager

Tel: + 61 (0)2 9994 7546

Email: [email protected]

Website www.challenger.com.au/cdi

Tim Evans Assistant Fund Manager

Tel: + 61 (0)2 9994 7131

Email: [email protected]

Appendices

31 31

Distribution policy

CDI’s distribution policy is to distribute accounting profit earned from operating activities adjusted for non-cash

expenses, straight-line rent, incurred and expected: leasing costs, debt establishment fees and capital expenditure to

maintain the investment properties, subject to the ongoing objective to distribute an amount which results in CDI not

being subject to income tax.

Realised impacts from the sale of assets will be distributed on a discretionary basis which will be determined with

regard to capital management strategies, market conditions and tax consequences.

On average in any year, the income distributed will represent approximately 80-85% of operating profit earned before

write downs.

32

Management

Fee type Calculation

Base management fee

Performance fees

From 1 July 2010, 0.5% of gross assets of CDI per annum, payable in cash

5% of first 2% out performance against S&P/ASX200 property accumulation index,

and 15% of any out-performance thereafter, capped at 0.25% of gross assets per

annum (capped with no carry forward)

Transactional fees are payable only for offshore acquisitions/divestments as detailed in the PDS. No fees

are payable on domestic acquisitions/divestments.

For full details refer to the CDI PDS, Constitution and Management Agreement at

www.challenger.com.au/cdi

Management agreements published on website

Management expense ratio: 57.0 bps

Management fees:

Hedge profiles

33

Half year ending AUD/EUR

30 June 2012 0.7972

31 December 2012 0.7828

Income hedges

$ A denominated hedges

Notional Hedge rate Maturity date

$15m 4.83% April 2012

$40m 5.37% Feb 2014

$25m 5.11% April 2014

$20m 5.10% June 2014

$12.5m 5.55% Oct 2015

$12.5m 5.39% Oct 2015

$40m 5.07% Feb 2016

$10m 7.40% July 2018

€ Euro denominated hedges

Notional Hedge rate Maturity date

€10m 4.08% Sept 2012

Interest rate hedges

61% 16%

17% 6%

Office

Retail

Industrial - DC

Industrial - HT

33%

36%

3%

29%

Government

Listed

MultiInternationalPrivate

25%

14%

19%

36%

7%

AAA

AA+ → A-

BBB+ → BBB-

BB+ → B-

CCC+ → D

NR

28%

25%

27%

5%

3% 3%

2% 5%

NSW

ACT

VIC

QLD

SA

WA

TAS

France

Sector diversification (by value) Geographic diversification (by value)

Tenant credit rating (by gross income) (Challenger internal ratings based on rating agency methodology)

Tenant diversification by type (by gross income)

34

Diversification enhances portfolio

quality

As at 31 December 2011

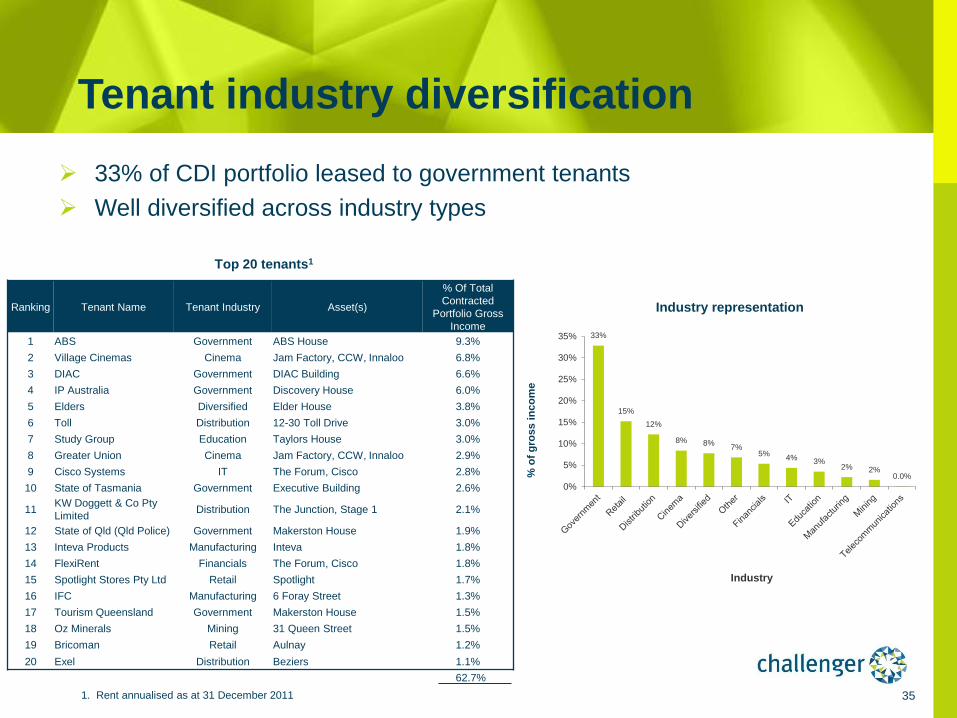

Ranking Tenant Name Tenant Industry Asset(s)

% Of Total

Contracted

Portfolio Gross

Income

1 ABS Government ABS House 9.3%

2 Village Cinemas Cinema Jam Factory, CCW, Innaloo 6.8%

3 DIAC Government DIAC Building 6.6%

4 IP Australia Government Discovery House 6.0%

5 Elders Diversified Elder House 3.8%

6 Toll Distribution 12-30 Toll Drive 3.0%

7 Study Group Education Taylors House 3.0%

8 Greater Union Cinema Jam Factory, CCW, Innaloo 2.9%

9 Cisco Systems IT The Forum, Cisco 2.8%

10 State of Tasmania Government Executive Building 2.6%

11 KW Doggett & Co Pty

Limited Distribution The Junction, Stage 1 2.1%

12 State of Qld (Qld Police) Government Makerston House 1.9%

13 Inteva Products Manufacturing Inteva 1.8%

14 FlexiRent Financials The Forum, Cisco 1.8%

15 Spotlight Stores Pty Ltd Retail Spotlight 1.7%

16 IFC Manufacturing 6 Foray Street 1.3%

17 Tourism Queensland Government Makerston House 1.5%

18 Oz Minerals Mining 31 Queen Street 1.5%

19 Bricoman Retail Aulnay 1.2%

20 Exel Distribution Beziers 1.1%

35

Tenant industry diversification

33% of CDI portfolio leased to government tenants

Well diversified across industry types

1. Rent annualised as at 31 December 2011

% o

f g

ros

s i

nc

om

e

Top 20 tenants1

Industry representation

62.7%

33%

15%

12%

8% 8% 7%

5% 4% 3%

2% 2% 0.0%

0%

5%

10%

15%

20%

25%

30%

35%

Industry

36

Lease expiry profile

(by gross income)

7.1%

3.3%

6.9% 5.7%

11.0%

65.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Vacant Jun-12 Jun-13 Jun-14 Jun-15 FY 2016 Beyond

% E

xp

iry b

y g

ross i

nco

me

37

Review type FY12 rental

proportion

(%)

Rent reviews

Fixed 56% Average 3.5%

CPI 11% Last CPI 3.5%1

French CCI 7% Last CCI 6.84%2

Market 2% n/a

Total 76%

Rent review profile provides built-in

growth

Significant weighting to fixed and indexed rental reviews over next three years

76% of portfolio subject to rental reviews in FY12

Rent review profile (by income)

1. Sept 2011ABS All Cities

2. French Cost of Construction Index average for 12 months to Q3 2011 11% 12% 8%

56% 58% 60%

2% 2% 3%

7% 7% 7%

23% 20% 22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY 11/12 FY 12/13 FY 13/14

No Review in Period (incl. New Leases) & Other

FCCI

Market Review

Fixed Review

CPI Review

38

CDI investment portfolio diversification

28% 25%

27%

5% 3%

3% 2%

5%

-

$50

$100

$150

$200

$250

$300

NSW ACT VIC QLD SA WA TAS France

Valu

e (

$m

)

Geographic Sector Diversification

Office Retail Industrial-DC Industrial - High Tech

61%

16% 17%

6%

-

$100

$200

$300

$400

$500

$600

Office Retail Industrial-DC Industrial - High Tech

Va

lue

($

m)

Sector Geographic Diversification

NSW ACT VIC QLD SA WA TAS France

39

Income statement

31 December 2011 31 December 2010

$’000 $’000

Rental income 36,811 34,375

Other property income 6,439 4,890

Income from operating business activities 3,772 3,658

Interest income 301 176

Revenue 47,323 43,099

Property related expenses (9,438) (8,371)

Expenses from operating business activities (2,607) (3,014)

Property expenses (12,045) (11,385)

Finance costs (6,920) (3,657)

Responsible Entity’s and Manager’s fees (2,189) (1,984)

Operating expenses (304) (627)

Trust expenses (9,413) (6,268)

Fair value movement of derivatives held at the end of the period (6,154) 2,909

Fair value movement of investment properties sold during the period (64) (219)

Fair value movement of investment properties held at the end of the

period (1,082) 1,947

Fair value movements (7,300) 4,637

Foreign exchange gain/(loss) (161) 69

Net loss on development property - (110)

Net profit before tax 18,404 30,042

Income tax credit 443 8

Net profit after income tax 18,847 30,050

Reconciliation of profit

40

Reconciliation of net profit after tax to profit from operating activities

31 December

2011

31 December

2010

$’000 $’000

Net profit after tax attributable to unitholders of CDI 18,847 30,050

Adjusted for:

Straight-lining of rental (income)/expense (2,020) (1,476)

Fair value movement of derivatives held at the end of the period 6,154 (2,909)

Fair value movement of investment properties sold during the period 64 219

Fair value movement of investment properties held at the end of the period 1,082 (1,947)

Fair value movements 7,300 (4,637)

Foreign exchange (gain)/loss 161 (69)

Property, plant and equipment depreciation 14 12

Net (gain)/loss on development property - 110

Income tax (credit)/expense (443) (8)

Profit from operating activities 23,859 23,982

Normalised earnings per unit (cents) 2.67 2.63

41

Distribution statement

31 December 2011 31 December 2010

$’000 $’000

Profit from operating activities 23,859 23,982

Non-cash expenses

Amortisation of borrowing costs 590 118

Other transfers per distribution policy

Debt establishment costs (1,210) (575)

Maintenance capital expenditure (1,345) (1,597)

Leasing costs (2,880) (260)

Income tax expense/(credit) (14) -

Total income available for distribution 19,000 21,668

Less: Current year undistributed income carried forward (881) (3,399)

Distribution to unitholders 18,119 18,269

Distribution per unit (cents) 2.05 2.00

Available funds from operations (AFFO)

42

Available funds from operations (AFFO)

31 December

2011

31 December

2010

$’000 $’000

Profit from operating activities 23,859 23,982

Add/(deduct):

Amortisation of borrowing costs 590 118

Leasing costs (2,880) (260)

Maintenance capital expenditure (1,345) (1,597)

Debt establishment fees (1,210) (575)

Capitalised interest (1,369) (704)

Available funds from operations 17,645 20,964

Distribution to unitholders 18,119 18,269

AFFO distribution payout ratio 102.7% 87.1%

43 43

Net property income

-

Acquisition

Australian portfolio 1H12 1H11 Variance

($'000) ($'000) ($'000) %

Office

ABS House, Belconnen, ACT 3,693 3,593 100 3

31 Queen Street, Melbourne, VIC 3,181 - 3,181 Large

DIAC Building, Belconnen, ACT 2,582 2,505 77 3

The Forum, Cisco, St Leonards, NSW 2,560 2,397 163 7

Discovery House, Woden, ACT 2,342 2,283 59 3

Makerston House, Brisbane, QLD 1,924 1,827 97 5

The Forum, Verizon, St Leonards, NSW 481 765 (284) (37)

Elder House, Adelaide, SA 1,379 1,328 51 4

Executive Building, Hobart, TAS 933 964 (31) (3)

Office total 19,075 15,662 3,413 22

Retail

Jam Factory, South Yarra, VIC 2,579 2,558 21 1

Century City Walk, Glen Waverley, VIC 1,389 1,233 156 13

Innaloo Cinema Centre, Innaloo, WA 827 902 (75) (8)

Kings Langley, Kings Langley, NSW 383 432 (49) (11)

Retail total 5,178 5,125 53 1

Industrial – Distribution Centres

The Junction Stage 1, Enfield, NSW 823 818 5 1

6 Foray Street, Fairfield, NSW 352 222 130 59

Spotlight, Laverton North, VIC 625 691 (66) (10)

12-30 Toll Drive, Altona North, VIC 642 609 33 5

2-10 Toll Drive, Altona North, VIC 315 303 12 4

1-9 Toll Drive, Altona North, VIC 169 153 16 10

Industrial – Distribution Centres total 2,926 2,796 130 5

Industrial – High-Tech

Taylors House, Waterloo, NSW 1,282 1,247 35 3

75 Talavera Road, North Ryde, NSW 600 402 198 49

187 Todd Road, Port Melbourne, VIC (80) 72 (152) (211)

Giffnock Avenue, North Ryde, NSW 623 687 (64) (9)

Industrial – High-Tech total 2,425 2,408 17 1

Sold properties

Pacific Brands, Port Melbourne, VIC 112 532 (420) (79)

478 Freeman Road, Richlands, QLD - 445 (445) (100)

Sold properties total 112 977 (865) (89)

Australia total 29,716 26,968 2,748 10

44 44

Net property income - continued

Note: All amounts exclude straight-lining of rental income.

Sold

French portfolio 1H12 1H11 Variance

(€'000) (€'000) (€'000) %

Sully, Sully sur Loire 533 521 12 2

Aulnay, Aulnay sous Bois, Paris 337 289 48 17

Beziers, Villeneuve les Beziers 357 336 21 6

Gennevillers, Gennevilliers, Paris 337 333 4 1

Tours, Parcay-Meslay, Tours 223 214 9 4

1,787 1,693 94 6

Sold properties

Toulouse, Toulouse - 67 (67) (100)

Europe total 1,787 1,760 27 2

![NetworkiE] - Bombay Stock Exchangemedia conglomerates in India and also the most diversified. Under a single unified group, we cater to diversified but synergistic interests with a](https://static.fdocuments.net/doc/165x107/5eca859b9aeafb5f637065d9/networkie-bombay-stock-exchange-media-conglomerates-in-india-and-also-the-most.jpg)