Ch01 ppt godwin

34

-

Upload

karan-shah -

Category

Business

-

view

193 -

download

0

Transcript of Ch01 ppt godwin

Learning Objectives

1.Describe the four assumptions made when communicating accounting information.

2.Describe the purpose and structure of an income statement and the terms and principles used to create it.

3.Describe the purpose and structure of a balance sheet and the terms and principles used to create it.

Learning Objectives

4. Describe the purpose and structure of a statement of retained earnings and how it links the income statement and the balance sheet.

5. Describe the purpose and structure of a statement of cash flows and the terms and principles used to create it.

Learning Objectives

6. Describe the qualitative characteristics that make accounting information useful.

7. Describe the conceptual framework of accounting.

Beginning AssumptionsLOI

Accounting is the process of identifying, measuring, and communicating economic

information to permit informed judgments and decisions. Put more simply, accounting is the “language

of business.”

To accomplish the process of accounting, accountants use four assumptions:

Reporting Profitability:The Income Statement

LO2

?One of the first questions any business wants to know is whether they are making money or are profitable.

These answers can be found in the Income Statement.

The Income Statement and TermsAn income statement reports a

company’s revenues and expenses.

Revenue – An increase in resources

resulting from the sale of goods

or services

Terms

Revenue Recognition Principle – A revenue should be recorded when a resource has been earned

Expense – A decrease in resources

resulting from the sale of goods

or services

Matching Principle – Expenses should be recorded in the period resources are used to generate revenues

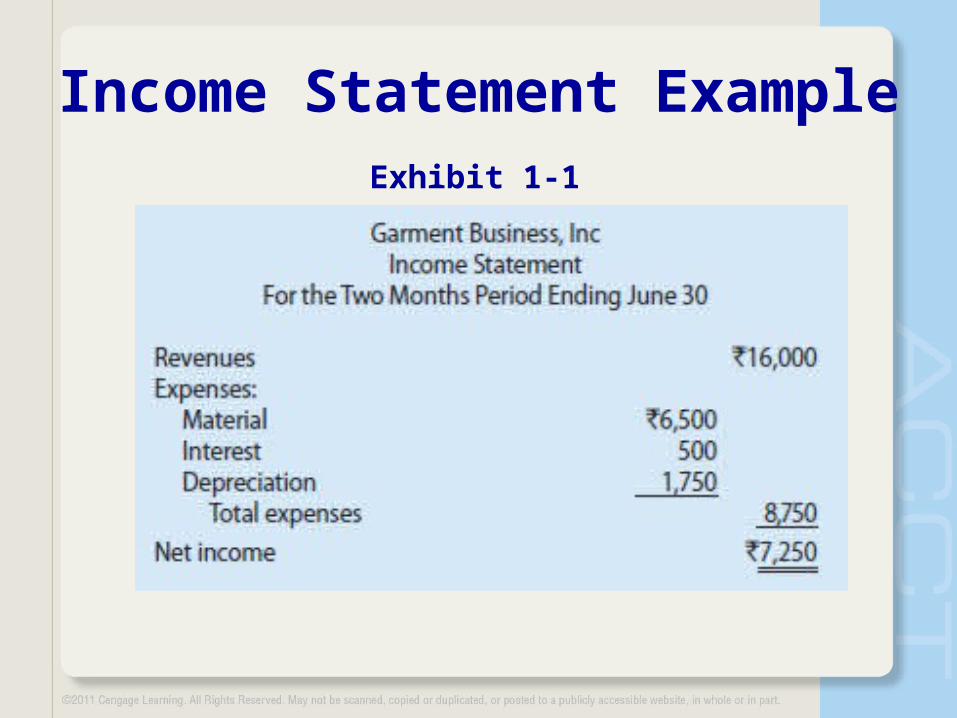

Income Statement ExampleExhibit 1-1

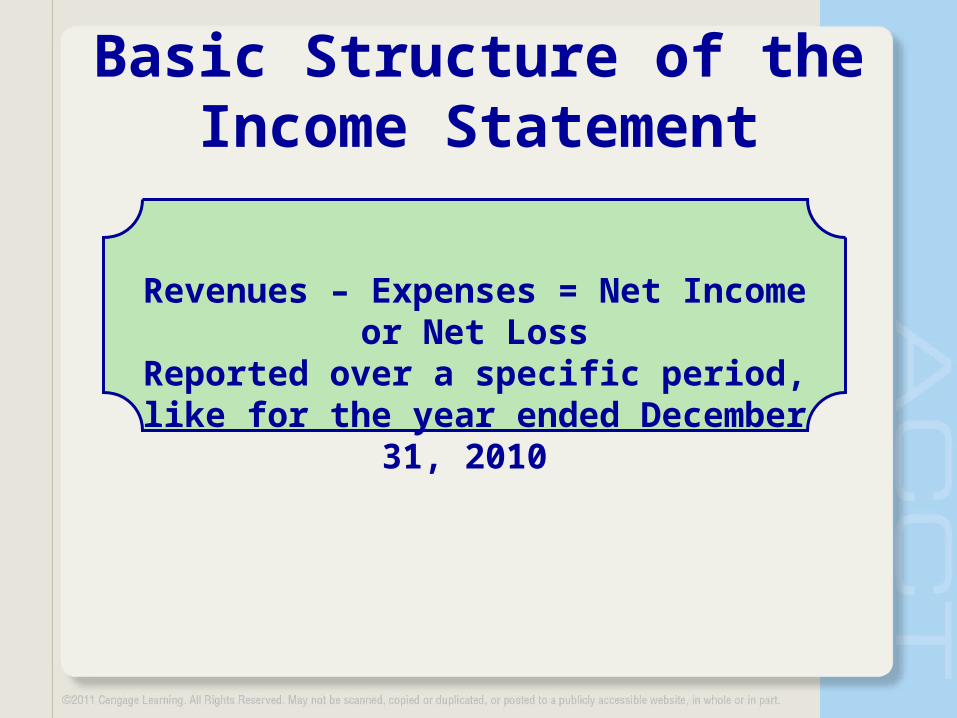

Basic Structure of the Income Statement

Revenues – Expenses = Net Income or Net LossReported over a specific period, like for the

year ended December 31, 2010

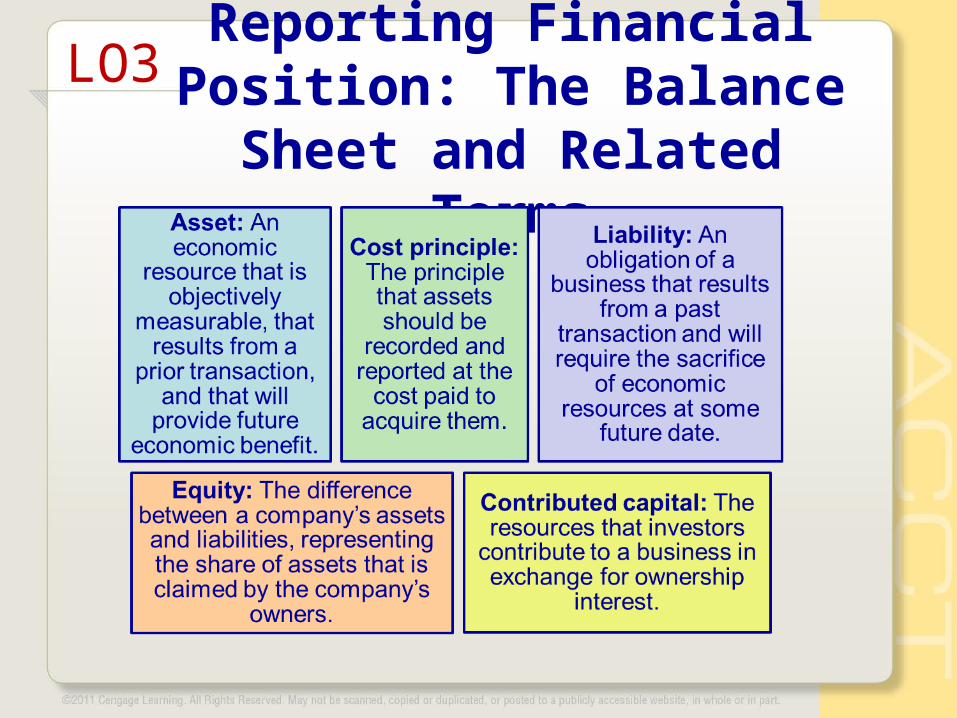

Reporting Financial Position: The Balance Sheet and Related

Terms

LO3

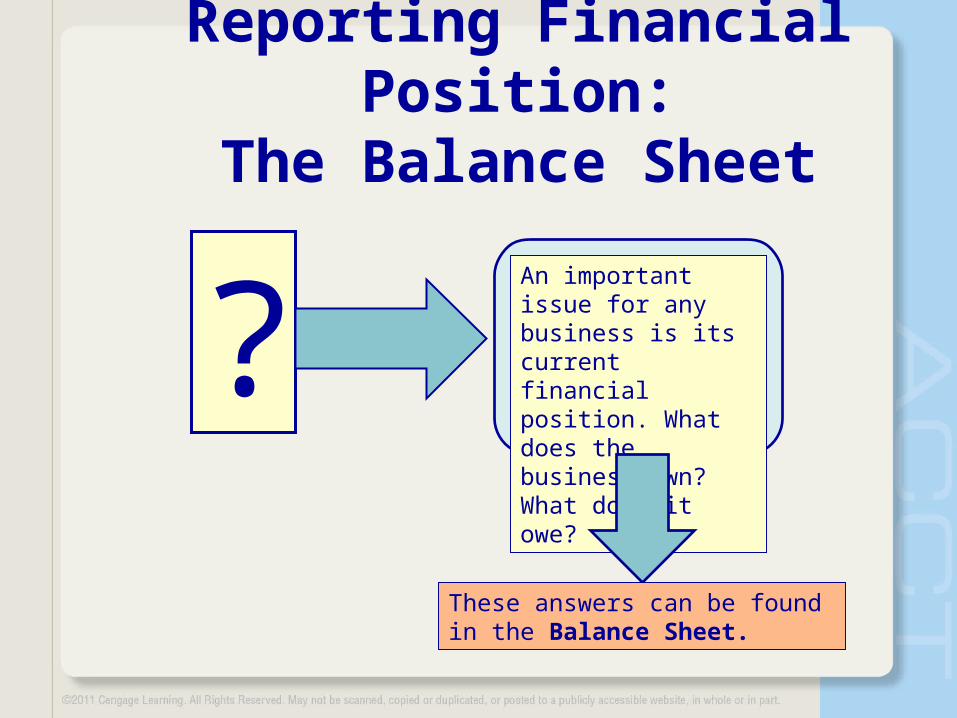

Reporting Financial Position:The Balance Sheet

?An important issue for any business is its current financial position. What does the business own? What does it owe?

These answers can be found in the Balance Sheet.

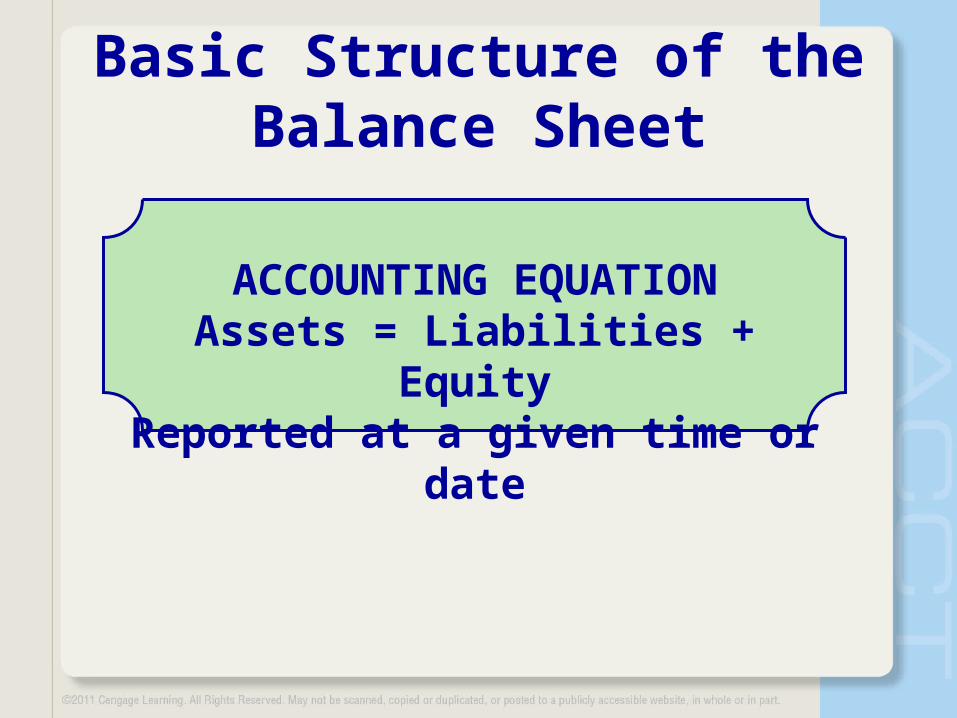

Basic Structure of the Balance Sheet

ACCOUNTING EQUATIONAssets = Liabilities + Equity

Reported at a given time or date

Balance Sheet ExampleExhibit 1-2

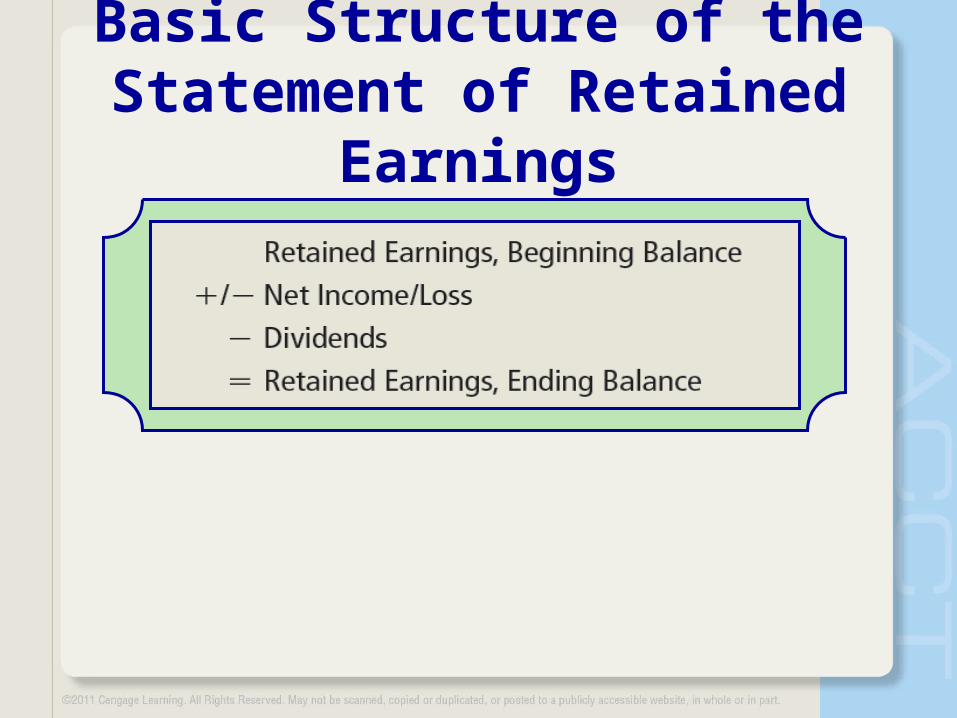

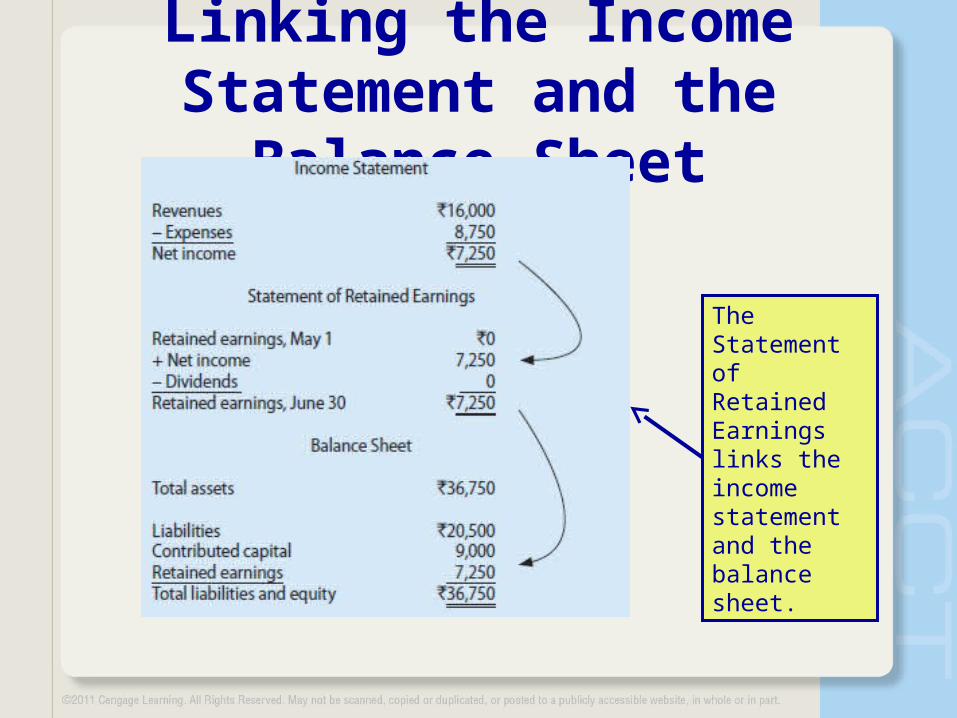

Reporting Equity: The Statement of Retained Earnings

LO4

A statement of retained earnings shows the change in a company’s retained

earnings over a specific period of time.

Basic Structure of the Statement of Retained Earnings

Statement of Retained Earnings Example

Exhibit 1-3

Linking the Income Statement and the Balance Sheet

The Statement of Retained Earnings links the incomestatement and the balance sheet.

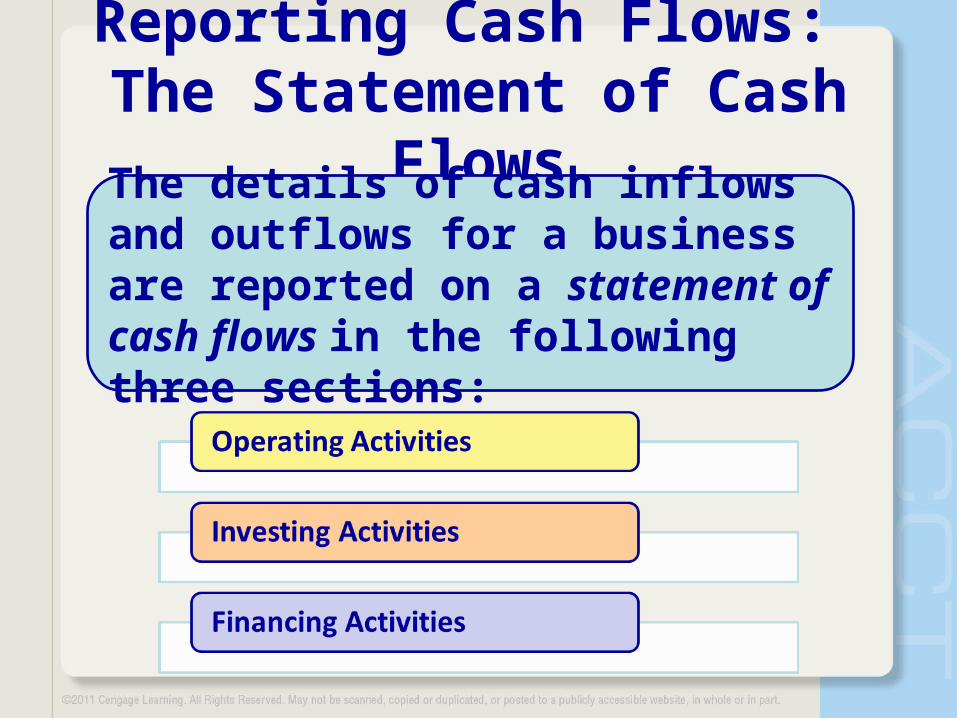

Reporting Cash Flows: The Statement of Cash Flows

?A business needs to answer questions about the management of cash:

• Where does a company get its cash?• Where does its cashgo? • Will there be enough cash to pay bills?

These answers can be found in the Statement of Cash Flows.

LO5

Reporting Cash Flows: The Statement of Cash Flows

The details of cash inflows and outflows for a business are reported on a statement of cash flows in the following three sections:

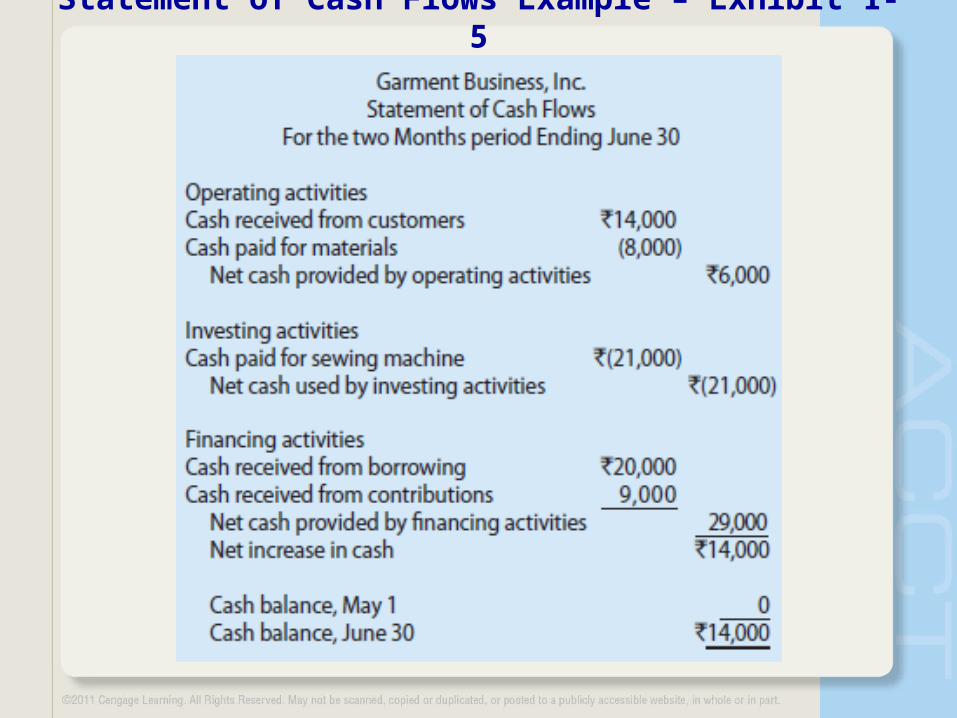

Statement of Cash Flows Example – Exhibit 1-5

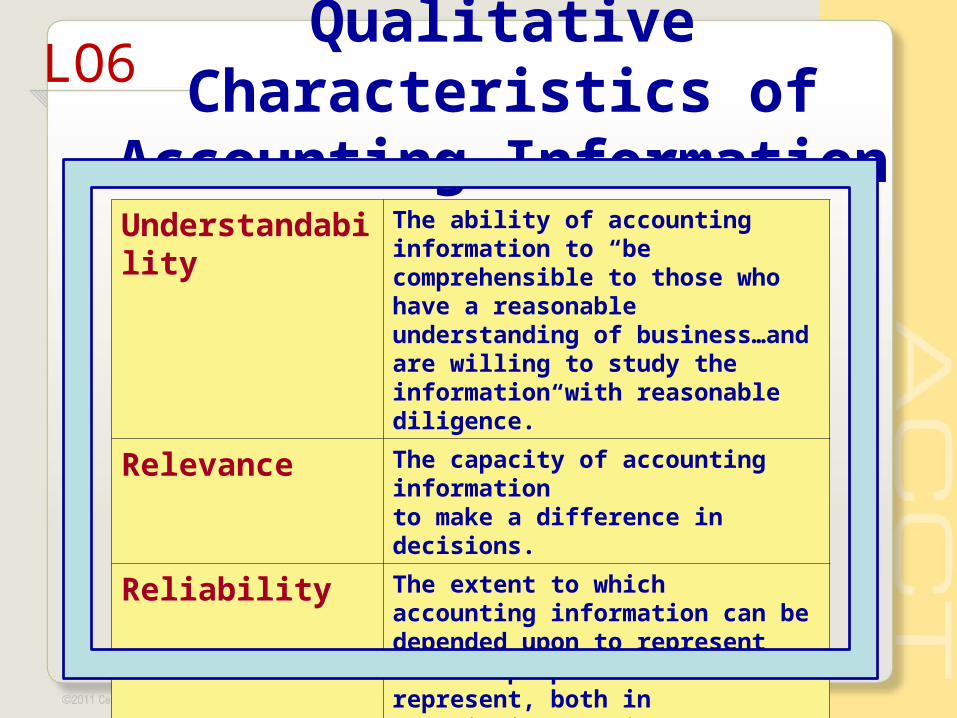

Qualitative Characteristics of Accounting Information

Understandability The ability of accounting information to “be comprehensible to those who have a reasonable understanding of business…and are willing to study the information with reasonable diligence.”

Relevance The capacity of accounting informationto make a difference in decisions.

Reliability The extent to which accounting information can be depended upon to represent what it purports to represent, both in description and in number.

Comparability The ability to use accounting information to compare or contrast the financial activities of different companies.

LO6

Qualitative Characteristics (Continued)

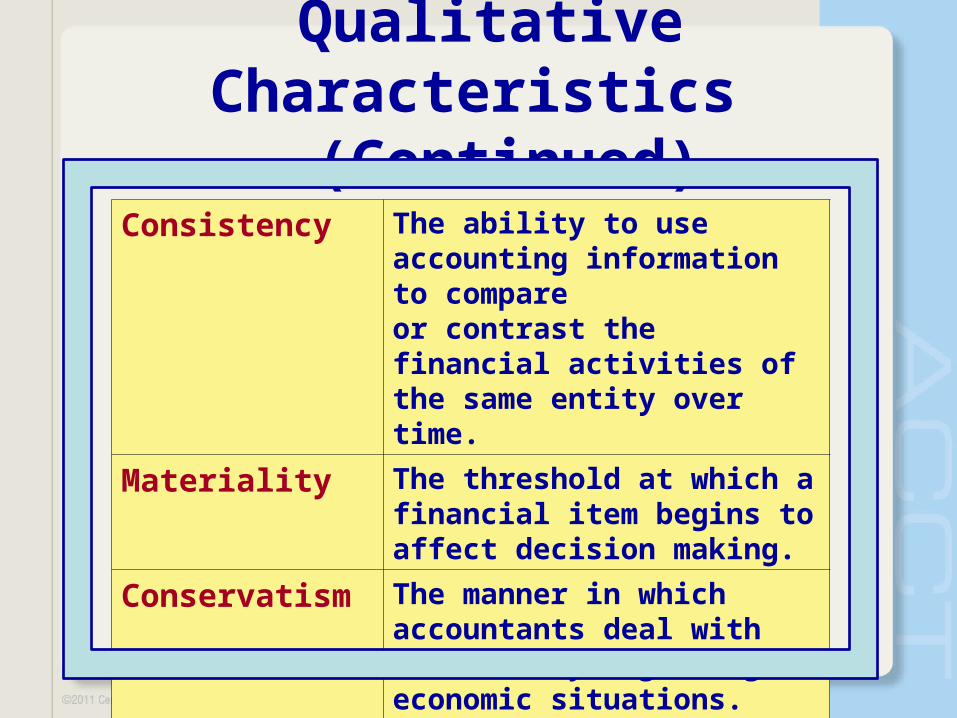

Consistency The ability to use accounting information to compareor contrast the financial activities of the same entity over time.

Materiality The threshold at which a financial item begins to affect decision making.

Conservatism The manner in which accountants deal with uncertainty regarding economic situations.

The Conceptual FrameworkLO7

The conceptual framework of accounting is the collection of concepts that guide the manner in which accounting is practiced.

The grammar or terms, explaining financial accountinglanguage in this chapter, are more formally known as

components of the conceptual framework of accounting.

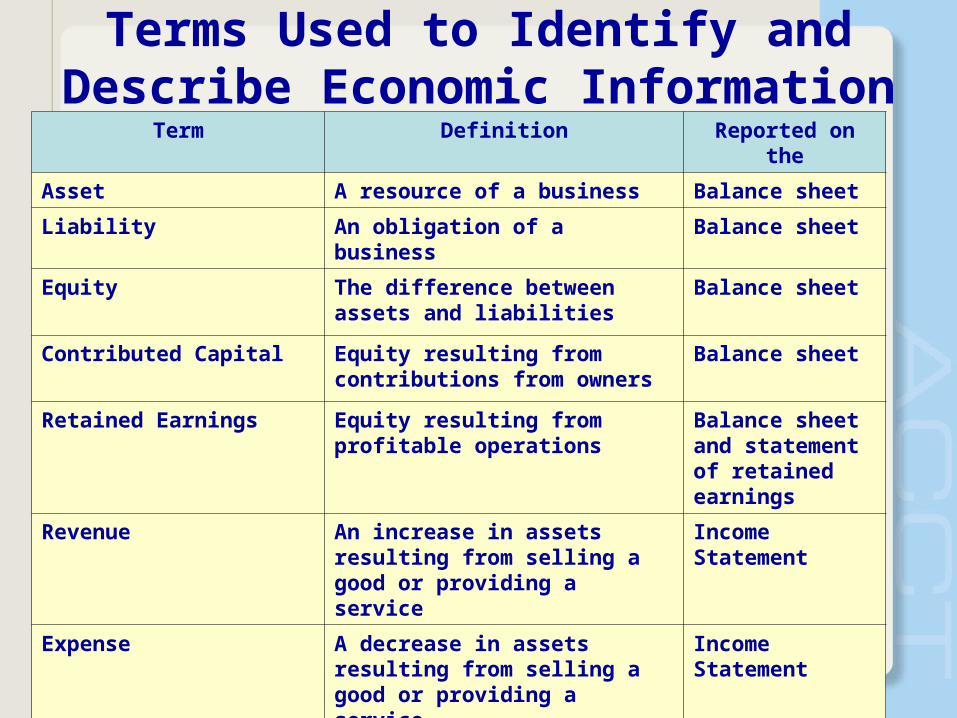

Terms Used to Identify and Describe Economic Information

Term Definition Reported on the

Asset A resource of a business Balance sheetLiability An obligation of a business Balance sheet

Equity The difference between assets and liabilities

Balance sheet

Contributed Capital Equity resulting from contributions from owners

Balance sheet

Retained Earnings Equity resulting from profitable operations

Balance sheet and statement of retained earnings

Revenue An increase in assets resulting from selling a good or providing a service

Income Statement

Expense A decrease in assets resulting from selling a good or providing a service

Income Statement

Dividend A distribution of profits to owners

Statement of retained earnings

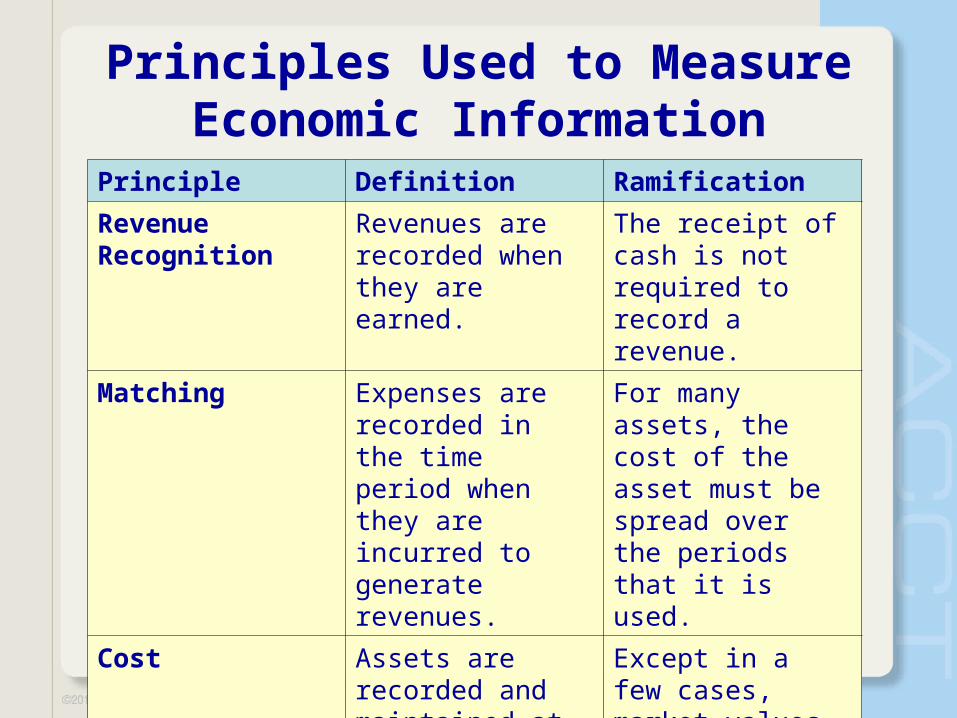

Principles Used to Measure Economic Information

Principle Definition RamificationRevenue Recognition

Revenues are recorded when they are earned.

The receipt of cash is not required to record a revenue.

Matching Expenses are recorded in the time period when they are incurred to generate revenues.

For many assets, the cost of the asset must be spread over the periods that it is used.

Cost Assets are recorded and maintained at their historical costs.

Except in a few cases, market values are not used for reporting asset values.

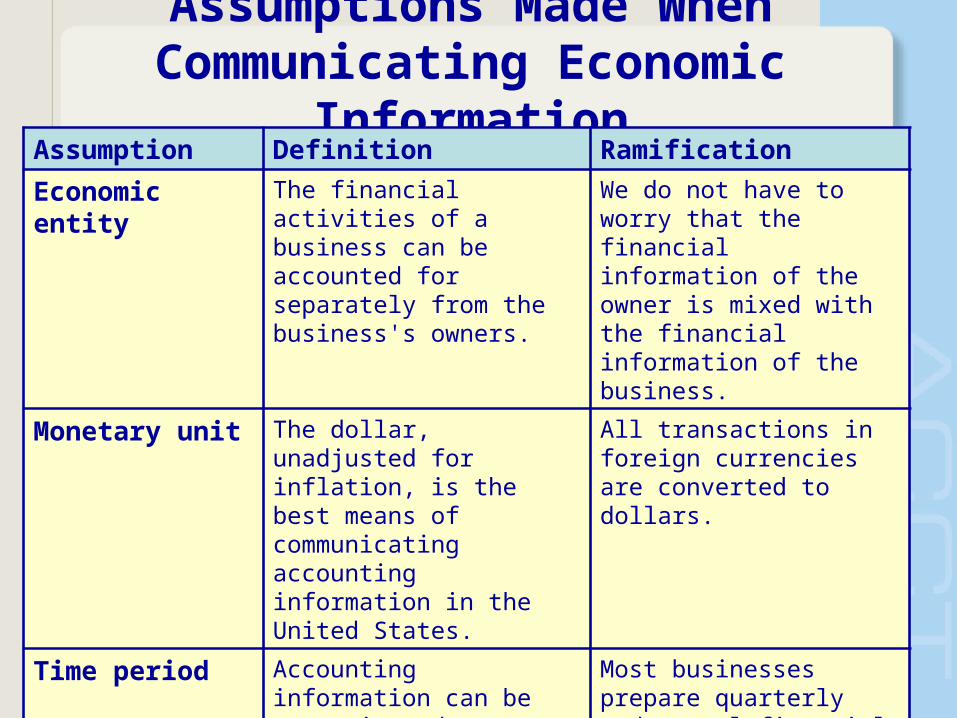

Assumptions Made When Communicating Economic Information

Assumption Definition RamificationEconomic entity The financial activities of a

business can be accounted for separately from the business's owners.

We do not have to worry that the financial information of the owner is mixed with the financial information of the business.

Monetary unit The dollar, unadjusted for inflation, is the best means of communicating accounting information in the United States.

All transactions in foreign currencies are converted to dollars.

Time period Accounting information can be communicated effectively over short periods of time.

Most businesses prepare quarterly and annual financial statements.

Going concern The company for which we are accounting will continue its operations indefinitely.

If an entity is not selling its assets, then the cost principle is appropriate.

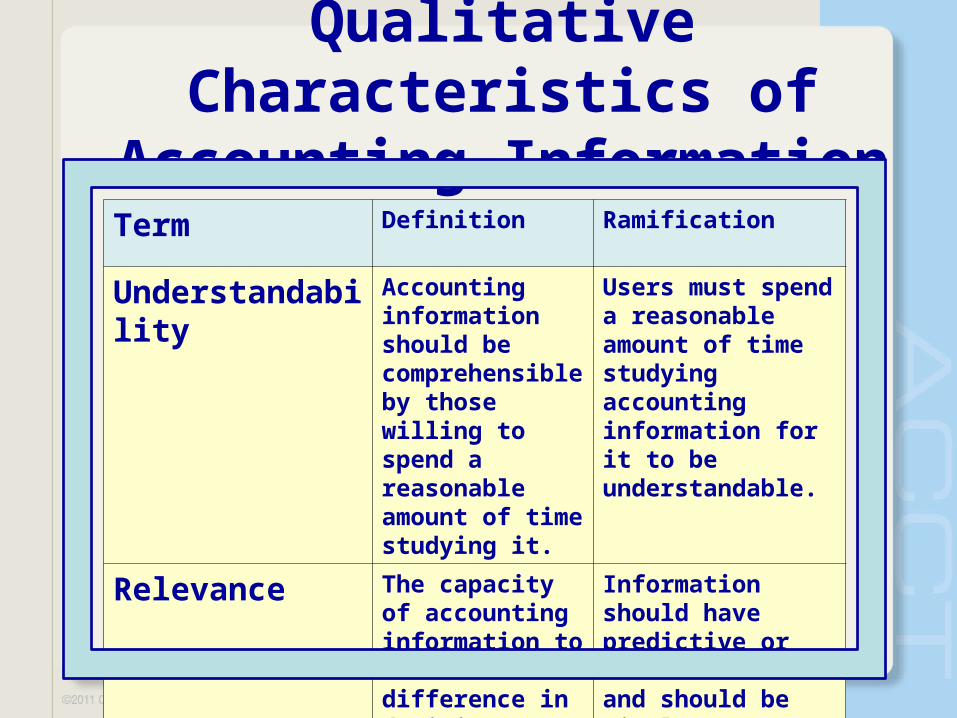

Qualitative Characteristics of Accounting Information

Term Definition Ramification

Understandability Accounting information should be comprehensible by those willing to spend a reasonable amount of time studying it.

Users must spend a reasonable amount of time studying accounting information for it to beunderstandable.

Relevance The capacity of accounting information to make a difference in decisions.

Information should have predictive or feedback value and should be timely.

Qualitative Characteristics of Accounting Information (continued)

Term Definition Ramification

Reliability The extent to which accounting information can be depended upon to represent what it purports to represent, both in description and in number.

Information should be free from error, a faithful representation, and neutral.

Comparability The ability to use accounting information to compare or contrast the financial activities of different companies.

Entities must disclose the accounting methods that they use so that comparisons across companies can be made.

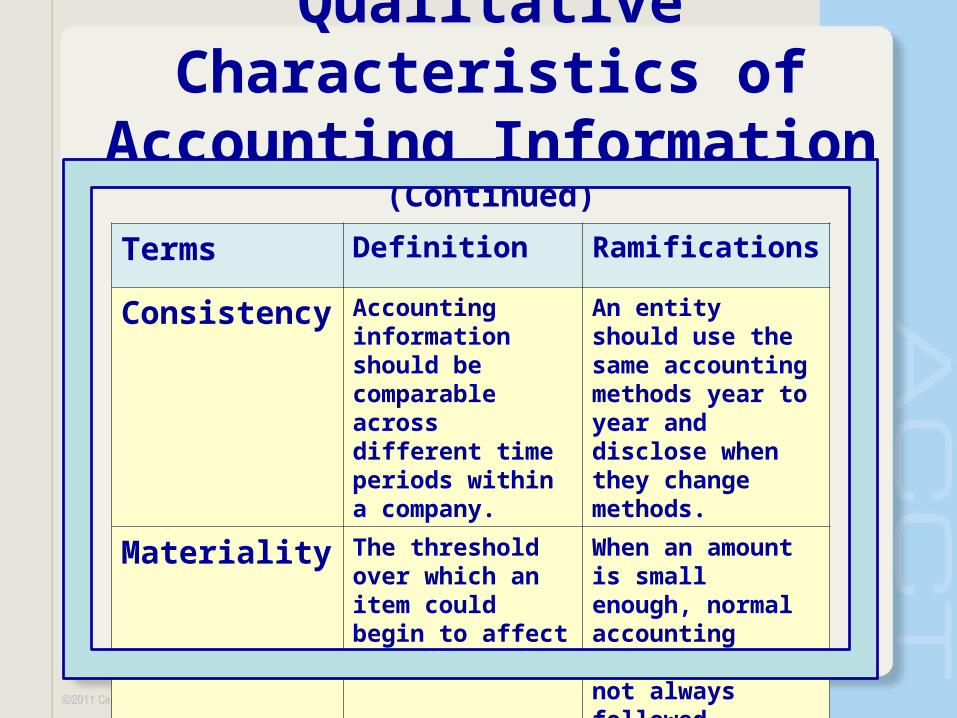

Qualitative Characteristics of Accounting Information (Continued)

Terms Definition Ramifications

Consistency Accounting information should be comparableacross different time periods within a company.

An entity should use the same accountingmethods year to year and disclose when they change methods.

Materiality The threshold over which an item could begin to affect decisions.

When an amount is small enough, normalaccounting procedures are not always followed.

Qualitative Characteristics of Accounting Information (Continued)

Terms Definition Ramifications

Conservatism When uncertainty exists, accounting informationshould present the least optimistic alternative.

An entity should choose accounting techniquesthat guard against overstating revenues or assets.

Financial Statements Used to Communicate Economic Information

Statement Purpose Structure Links to Other Statements

Balance sheet Shows a company’s assets, liabilities, and equity at a specific point in time.

Assets = Liabilities + Equity

The balance in retained earnings comes from the statement of retained earnings.The balance in cash should agree with the ending cash balance on the statement of cash flows.

Income statement

Shows a company’s revenues and expenses over a specific period of time.

Revenue - Expenses = Net Income/Loss

Net income/loss goes to the statement of retained earnings to compute retained earnings.

Financial Statements Used to Communicate Economic Information

(continued)

Statement Purpose Structure Links to Other Statements

Statement of retained earnings

Shows the changes in a company’sretained earnings over a specificperiod of time.

Beginning Retained Earnings +/- NetIncome/Loss - Dividends = EndingRetained Earnings

Ending retained earnings goes to the balance sheet.

Statement of cash flows

Shows a company’s inflows and outflows of cash over a specificperiod of time.

Operating Cash Flows +/- InvestingCash Flows +/- Financing Cash Flows = Net change in cash

The ending cash balance on thestatement of cash flows should agreewith the balance in cash on the balance sheet.

End of Chapter 1