Factoring Accounts Receivables By: Veronica Wallace Vice President Vice President.

TheLooming

Crisis

Who Will Pay ForYour Retirement?

A Statement by the Research and Policy Committeeof the Committee for Economic Development

Who Will Pay ForYour Retirement?

TheLooming

Crisis

Library of Congress Cataloging-in-Publication Data

Committee for Economic Development. Research and Policy Committee.Who will pay for your retirement? : the looming crisis : a statement /by the Research and Policy Committee of the Committee for Economic Development.p. cm.Includes bibliographical references.ISBN 0-87186-119-4 : $20.001. Old age pensions — United States. 2. Retirement income — United States.

3. Social security — United States. 4. Civil service — Pensions — United States.5. Individual retirement accounts — United States. I. Committee for EconomicDevelopment. II. Title.HD7105.35.U6C65 1995331.25'2'0973 — dc20 95-3345

CIP

First printing in bound-book form: 1995Paperback: $20.00Printed in the United States of AmericaDesign: Rowe & Ballantine

COMMITTEE FOR ECONOMIC DEVELOPMENT477 Madison Avenue, New York, N.Y. 10022(212) 688-2063

2000 L Street, N.W., Suite 700, Washington, D.C. 20036(202) 296-5860

84 iii

CONTENTS

RESPONSIBILITY FOR CED STATEMENTS ON NATIONAL POLICY vi

PURPOSE OF THIS STATEMENT ix

CHAPTER 1: EXECUTIVE SUMMARY AND POLICY RECOMMENDATIONS ....................................... 1The Challenge Posed by an Aging Population ...................................................................................................... 2The Untimely Decline in Retirement Saving .......................................................................................................... 5

Pension Contributions and Funding ................................................................................................................. 5Economic Effects of Declining Retirement Saving........................................................................................... 6

Policy Options to Tackle the Retirement Finance Problem .................................................................................. 7Regulatory Reform for Private Retirement Plans ............................................................................................ 7Retirement Information and Individual Responsibility ................................................................................. 8Reforming Government Employee Pensions and the Social Security Program.......................................... 8

Summary of Policy Recommendations ................................................................................................................... 9

CHAPTER 2: RETIREMENT SAVING AND ECONOMIC SECURITY ...................................................... 15The Economic Security of Future Retirees ............................................................................................................ 15The Economy and Retirement Saving ................................................................................................................... 16Private- and Public-Sector Responsibilities for Pensions ................................................................................... 21Actions Required to Meet These Responsibilities ................................................................................................ 22

CHAPTER 3: THE BASIC FACTS ON OUR AGING POPULATION AND RETIREMENT SAVING .................................................................................................................................. 24An Aging Population ............................................................................................................................................... 24Private Sector Preparation for Retirement of the Baby Boomers....................................................................... 27

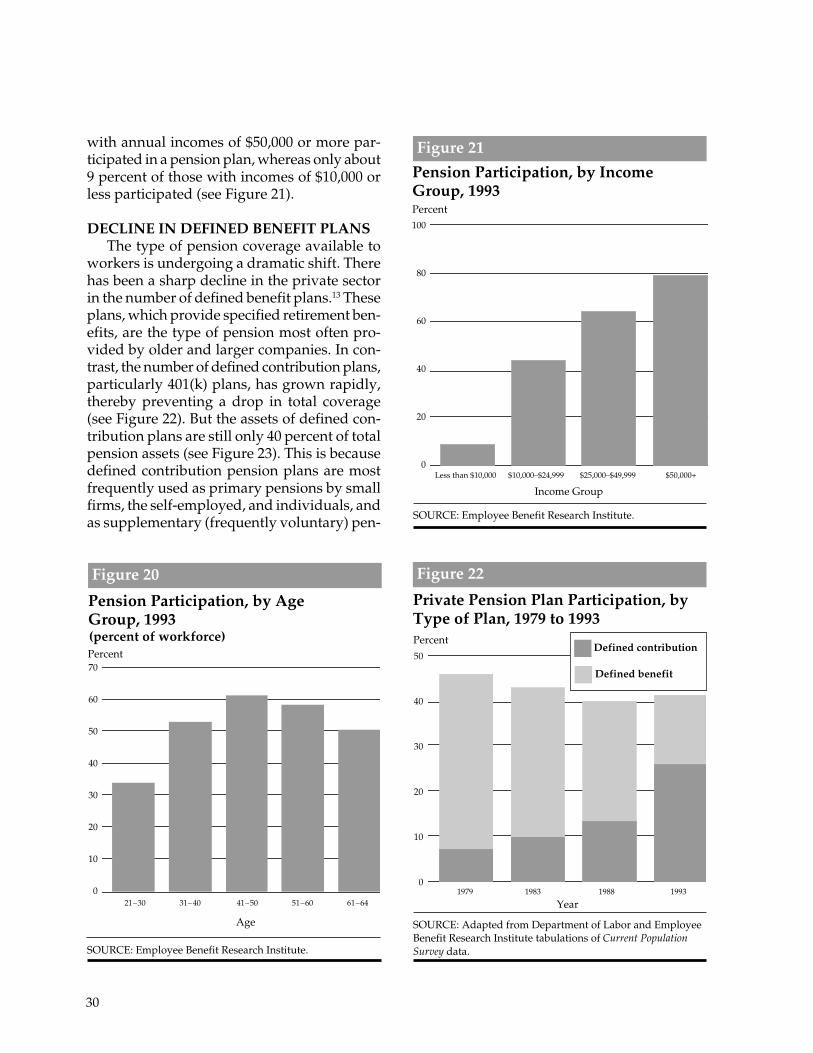

Private Pension Contributions .......................................................................................................................... 28Private Pension Coverage.................................................................................................................................. 29Decline in Defined Benefit Plans ...................................................................................................................... 30Preretirement Withdrawals of Pension Funds ............................................................................................... 31

The Status of Pension Funds ................................................................................................................................... 32Private Pension Funds ....................................................................................................................................... 32Public Sector Funding of Pensions ................................................................................................................... 33

Expectations of the Baby Boomers for Retirement Income ................................................................................ 37How Much Should Workers Save for Retirement? ............................................................................................. 38

Undersaving by Baby Boomers ........................................................................................................................ 39

CHAPTER 4: DESIGNING TAX INCENTIVES TO RAISE SAVING .......................................................... 42The Tax Base Controversy ....................................................................................................................................... 42Tax Incentives and Saving ....................................................................................................................................... 43

Design of Tax-Preferred Saving Incentives..................................................................................................... 44Proposals for Compulsory Saving Programs ................................................................................................. 45

The Budget Deficit .................................................................................................................................................... 46

85iv

CHAPTER 5: THE REGULATORY TANGLE: PROPOSALS FOR SIMPLIFICATION ........................... 48Favorable Tax Treatment ......................................................................................................................................... 48Federal Regulation ................................................................................................................................................... 48ERISA and Subsequent Legislation........................................................................................................................ 49Regulations Limiting Private Pension Contributions and Benefits .................................................................. 50

Funding Limit for Defined Benefit Plans ........................................................................................................ 51Reductions in Contribution and Benefit Limits ............................................................................................. 53

Regulations to Prevent Discrimination in Pension Plans ................................................................................... 59Top-heavy Rules ................................................................................................................................................. 60Social Security Integration ................................................................................................................................. 60Coverage and Vesting Rules ............................................................................................................................. 60

Preserving Pension Funds for Retirement ............................................................................................................ 61Preretirement Lump-Sum Withdrawals and Borrowing from Pensions ................................................... 61Portability of Pensions ....................................................................................................................................... 61

Pension Benefit Guaranty Corporation ................................................................................................................. 61The Premium Structure ..................................................................................................................................... 62Moral Hazard ...................................................................................................................................................... 63

Rising Regulatory Costs Discourage Pension Saving ......................................................................................... 64Sources of Cost Increases ................................................................................................................................... 65Impact of Cost Increases on Plan Terminations and Formations ................................................................ 65

APPENDIX: A BRIEF HISTORY OF GOVERNMENT REGULATION OF PRIVATE PENSIONS ............................................................................................................... 66

NOTES 72

MEMORANDUM OF COMMENT, RESERVATION, OR DISSENT 82

OBJECTIVES OF THE COMMITTEE 83

The Committee for Economic Developmentis an independent research and policy organi-zation of some 250 business leaders and edu-cators. CED is nonprofit, nonpartisan, and non-political. Its purpose is to propose policies thatbring about steady economic growth at highemployment and reasonably stable prices, in-creased productivity and living standards,greater and more equal opportunity for everycitizen, and improved quality of life for all.

All CED policy recommendations musthave the approval of trustees on the Researchand Policy Committee. This Committee isdirected under the bylaws which emphasizethat “all research is to be thoroughly objectivein character, and the approach in each instanceis to be from the standpoint of the generalwelfare and not from that of any special politi-cal or economic group.” The Committee isaided by a Research Advisory Board of lead-ing social scientists and by a small permanentprofessional staff.

The Research and Policy Committee doesnot attempt to pass judgment on any pending

specific legislative proposals; its purpose is tourge careful consideration of the objectives setforth in this statement and of the best means ofaccomplishing those objectives.

Each statement is preceded by extensivediscussions, meetings, and exchange of memo-randa. The research is undertaken by a sub-committee, assisted by advisors chosen for theircompetence in the field under study.

The full Research and Policy Committeeparticipates in the drafting of recommenda-tions. Likewise, the trustees on the draftingsubcommittee vote to approve or disapprovea policy statement, and they share with theResearch and Policy Committee the privilegeof submitting individual comments for publi-cation.

Except for the members of the Research andPolicy Committee and the responsible subcommit-tee, the recommendations presented herein are notnecessarily endorsed by other trustees or by theadvisors, contributors, staff members, or othersassociated with CED.

RESPONSIBILITY FOR CED STATEMENTS ON NATIONAL POLICY

vi

CED RESEARCH AND POLICY COMMITTEE

REX D. ADAMSVice President–AdministrationMobil Corporation

IAN ARNOFPresident and Chief Executive OfficerFirst Commerce Corporation

ALAN BELZERRetired President and Chief

Operating OfficerAlliedSignal Inc.

PETER A. BENOLIELChairman of the BoardQuaker Chemical Corporation

ROY J. BOSTOCKChairman and Chief Executive OfficerD’Arcy, Masius, Benton & Bowles, Inc.

THEODORE A. BURTISRetired Chairman of the BoardSun Company, Inc.

OWEN B. BUTLERRetired Chairman of the BoardThe Procter & Gamble Company

FLETCHER L. BYROMChairmanAdience, Inc.

PHILIP J. CARROLLPresident and Chief Executive OfficerShell Oil Company

JOHN B. CAVEPrincipalAvenir Group, Inc.

ROBERT CIZIKChairman and Chief Executive OfficerCooper Industries Inc.

A. W. CLAUSENRetired Chairman and Chief

Executive OfficerBankAmerica Corporation

JOHN L. CLENDENINChairman and Chief Executive OfficerBellSouth Corporation

RONALD R. DAVENPORTChairman of the BoardSheridan Broadcasting Corp.

ChairmanJOSH S. WESTONChairman and Chief Executive OfficerAutomatic Data Processing, Inc.

Vice ChairmenFRANK P. DOYLEExecutive Vice PresidentGEW.D. EBERLEChairmanManchester Associates, Ltd.WILLIAM S. EDGERLYChairmanFoundation for PartnershipsCHARLES J. ZWICKCoral Gables, Florida

LINNET F. DEILYChairman, President and

Chief Executive OfficerFirst Interstate Bank of Texas

GEORGE C. EADSVice President, Worldwide

Economic & Market AnalysisGeneral Motors Corporation

WALTER Y. ELISHAChairman and Chief Executive OfficerSprings Industries, Inc.

EDMUND B. FITZGERALDManaging DirectorWoodmont Associates

HARRY L. FREEMANPresidentThe Freeman Company

RAYMOND V. GILMARTINPresident and Chief Executive OfficerMerck & Company, Inc.BOYD E. GIVANSenior Vice President and Chief Financial

OfficerThe Boeing Company

BARBARA B. GROGANPresidentWestern Industrial Contractors

RICHARD W. HANSELMANRetired ChairmanGenesco Inc.

EDWIN J. HESSSenior Vice PresidentExxon Corporation

RODERICK M. HILLSPartnerMudge Rose Guthrie Alexander &

Ferdon

LEON C. HOLT, JR.Retired Vice ChairmanAir Products and Chemicals, Inc.

MATINA S. HORNERExecutive Vice PresidentTIAA-CREF

CORDELL W. HULLExecutive Vice President and DirectorBechtel Group, Inc.

SOL HURWITZPresidentCommittee for Economic Development

HARRY P. KAMENChairman and Chief Executive OfficerMetropolitan Life Insurance Company

HELENE L. KAPLAN, Esq.Of CounselSkadden Arps Slate Meagher & Flom

JOSEPH E. KASPUTYSChairman, President and Chief

Executive OfficerPrimark Corporation

ALLEN J. KROWEVice Chairman and Chief Financial

OfficerTexaco Inc.

RICHARD J. KRUIZENGASenior FellowISEM

CHARLES R. LEEChairman and Chief Executive OfficerGTE Corporation

FRANKLIN A. LINDSAYRetired ChairmanItek Corporation

WILLIAM F. MAYChairman and Chief Executive OfficerStatue of Liberty - Ellis Island

Foundation, Inc.

ALONZO L. MCDONALDChairman and Chief Executive OfficerAvenir Group, Inc.

HENRY A. MCKINNELLExecutive Vice President and Chief

Financial OfficerPfizer Inc.

JOSEPH NEUBAUERChairman and Chief Executive OfficerARAMARK Corp.

JOHN D. ONGChairman of the Board, President and

Chief Executive OfficerThe BFGoodrich Company

VICTOR A. PELSONExecutive Vice President, Chairman-

Global Operations TeamAT&T Corp.

PETER G. PETERSONChairmanThe Blackstone Group

DEAN P. PHYPERSNew Canaan, Connecticut

JAMES J. RENIERRenier & Associates

JAMES Q. RIORDANStuart, Florida

HENRY B. SCHACHTChairman of the Executive CommitteeCummins Engine Company, Inc.

ROCCO C. SICILIANOBeverly Hills, California

ELMER B. STAATSFormer Comptroller General of

the United States

ARNOLD R. WEBERChancellorNorthwestern University

LAWRENCE A. WEINBACHManaging Partner – Chief ExecutiveArthur Andersen & Co, SC

WILLIAM S. WOODSIDEVice ChairmanLSG Sky Chefs

MARTIN B. ZIMMERMANExecutive Director, Governmental Relations and Corporate EconomicsFord Motor Company

*

vii

*Voted to approve the policy statement but submitted memorandum of comment, reservation, or dissent. See page 82.

viii

ChairmanLAWRENCE A. WEINBACHManaging Partner-Chief ExecutiveArthur Andersen & Co, SC

REX D. ADAMSVice President-AdministrationMobil CorporationIAN ARNOFPresident & Chief Executive OfficerFirst Commerce CorporationELI BROADChairman, President &

Chief Executive OfficerSunAmerica Inc.STEPHEN L. BROWNChairman & Chief Executive

OfficerJohn Hancock Mutual Life

Insurance CompanyJ. GARY BURKHEADPresidentFidelity Management and Research

CompanyPHILIP CALDWELLSenior Managing DirectorLehman Brothers, Inc.KATHLEEN COOPERChief EconomistExxon CorporationGARY L. COUNTRYMANChairman & Chief Executive OfficerLiberty Mutual Insurance CompanyW. D. EBERLEChairmanManchester Associates, Ltd.JAMES D. ERICSONPresident & Chief Executive OfficerNorthwestern Mutual Life

Insurance CompanyKATHLEEN FELDSTEINPresidentEconomics Studies, Inc.RICHARD W. HANSELMANRetired ChairmanGenesco Inc.RODERICK M. HILLSPartnerMudge Rose Guthrie Alexander

& Ferdon

Ex-Officio TrusteesJOHN L. CLENDENINChairman & Chief Executive OfficerBellSouth CorporationFRANK P. DOYLEExecutive Vice PresidentGESOL HURWITZPresidentCommittee for Economic DevelopmentJOSH S. WESTONChairman & Chief Executive OfficerAutomatic Data Processing, Inc.

Non-Trustee MembersW. GORDON BINNS, JR.Former Vice PresidentGeneral Motors CorporationMARSHALL N. CARTERChairman & Chief Executive OfficerState Street Bank and Trust CompanyMARVIN GREENEManaging Director, Retirement ServicesTowers Perrin

GuestsWILLIAM CHENEYEconomistJohn Hancock Financial ServicesCATHERINE L. HERONVice President & Senior Counsel,

Tax, Pension, and InternationalInvestment Company InstituteSANFORD KOEPPELVice President, Issues ManagementPrudential Asset Management CompanyEDWARD V. REGANPresidentThe Jerome Levy Economics InstituteCAROL REUTERPresidentNew York Life FoundationDAVID M. WALKERCompensation and Benefits ConsultingArthur Andersen & Co, SC

HARRY G. HOHNChairman & Chief Executive OfficerNew York Life Insurance CompanyROBERT C. HOLLANDSenior Economic ConsultantCommittee for Economic DevelopmentMATINA S. HORNERExecutive Vice PresidentTIAA-CREFTHOMAS W. JONESPresident & Chief Operating OfficerTIAA-CREFHARRY P. KAMENChairman & Chief Executive OfficerMetropolitan Life Insurance CompanyROBERT W. LUNDEENRetired ChairmanThe Dow Chemical CompanyLEIF H. OLSENPresidentLeif H. Olsen Investments, Inc.JAMES F. ORR IIIChairman & Chief Executive OfficerUNUM CorporationDEAN P. PHYPERSNew Canaan, ConnecticutS. LAWRENCE PRENDERGASTVice President & TreasurerAT&T Corp.JAMES Q. RIORDANStuart, FloridaIAN M. ROLLANDChairman & Chief Executive OfficerLincoln National CorporationGEORGE F. RUSSELL, JR.ChairmanFrank Russell CompanyJOHN L. STEFFENSExecutive Vice PresidentMerrill Lynch & Co., Inc.RICHARD F. SYRONChairman & Chief Executive OfficerAmerican Stock Exchange

PROJECT DIRECTORWILLIAM J. BEEMANVice President and Director of

Economic StudiesCommittee for Economic Development

ADVISORSB. DOUGLAS BERNHEIMProfessor, Department of EconomicsStanford UniversityBERNARD SAFFRANFranklin & Betty Barr Professor of

EconomicsSwarthmore CollegeJOHN B. SHOVENCharles R. Schwab Professor of

EconomicsDean, School of Humanities and SciencesStanford University

*

*Voted to approve the policy statement but submitted memorandum of comment, reservation, or dissent. See page 82.

PROJECTASSOCIATEMICHAEL K. BAKEREconomistCommittee for Economic Development

SUBCOMMITTEE ON PENSIONS AND SAVING

ix

PURPOSE OF THIS STATEMENT

Major reforms are needed in policies thataffect both private retirement plans and SocialSecurity if the United States is to avoid a seri-ous crisis in retirement funding and livingstandards in the next century. Our goal inpreparing this report is to show as clearly aspossible the consequences of inadequateretirement saving for those retiring early inthe next century and thereafter. If policies andpractices are not changed, many twenty-first–century retirees will experience an unexpectedand substantially reduced standard of living,due in no small part to a retirement systemthat is underfunded, overregulated, and soonto be strained as never before with the retire-ment of the baby-boom cohort.

Who Will Pay for Your Retirement? issues astrong warning, but it also offers comprehen-sive, specific, and workable recommendations.These recommendations, if taken together, willnot only allow the nation to avert disaster butwill also:

• Strengthen and streamline the way we fundand regulate retirement programs.

• Educate workers and employers aboutretirement needs, and provide incentivesfor people to save adequately for theirown retirement.

• Significantly broaden the scope and cover-age of private plans.

• Preserve Social Security for generations tocome by improving funding and limitingthe growth of benefits.

We are keenly aware of the enormousimpact that retirement policies have onnational saving and the economy. Decisions

on retirement policies should place top prior-ity not only on coverage and increased ben-efits but also on national saving, capitalformation, and economic growth.

The Committee for Economic Developmenthas a long-standing interest in retirement poli-cies. In 1981, CED issued Reforming RetirementPolicies, which outlined a strategy for broad-ening the reach of private pensions, increas-ing individual saving, and strengtheningSocial Security. Although a number of therecommendations in that report have beenimplemented (e.g., a gradual rise in the retire-ment age), recent changes in federal regula-tion (many made in the name of deficit reduc-tion or antidiscrimination policy) havecurtailed new pension formation and soundfunding.

With this policy statement, we call on Con-gress to reverse government policies that arestrangling private pensions and threateningtheir financial soundness. Although this state-ment deals primarily with policy for privatepensions, we also say that Social Securitycannot be ignored and that changes are neces-sary to preserve that system well into the nextcentury. We call on all Americans to educatethemselves about their retirement needs andoptions so that they can make sound and sen-sible decisions for themselves and their fami-lies.

ACKNOWLEDGMENTSI want to thank the very able group of

CED Trustees and advisors who served onthe CED subcommittee that prepared this re-port (see page viii).

Very special thanks are due to the sub-committee’s chairman, Lawrence A.Weinbach,Managing Partner-Chief Executive of ArthurAndersen & Co, for the energy, expertise,and wisdom he brought to this project. Weare also indebted to Project DirectorWilliam J. Beeman, CED’s Vice President andDirector of Economic Studies, not only for hiscomprehensive knowledge but also for theclarity he has brought to this complex set ofissues.

Thanks are also due to CED EconomistMichael Baker for his contributions to thisproject and to Carol Alvey for her secretarialassistance.

x

We are deeply grateful to Merrill Lynchand Company, the New York Life Founda-tion, Morgan Stanley Group Inc., JohnHancock Mutual Life Insurance Company,Lincoln National Corporation, the InvestmentCompany Institute, Household International,and Towers Perrin for their generous sup-port of this most important program.

Josh S. WestonChairmanCED Research and Policy Committee

1

America’s retirement system is under-funded, overregulated, and soon to be chal-lenged by unprecedented growth in theretirement-age population. Consequently, ournation will confront a major crisis in financingthe needs of the elderly at the beginning of thetwenty-first century unless policies arereformed to make retirement saving a top pri-ority. If steps are taken promptly to imple-ment the reforms recommended by CED inthis statement, significant sacrifices will berequired, but they will be manageable. Ifaction is postponed, the nation will face thevery unpleasant choice of a substantial cut inthe economic status of the elderly or an eco-nomically damaging and unfair tax burdenon future generations of workers.

The economic well-being of future retireesand, indeed, of workers is seriously at riskbecause of the interaction of several demo-graphic, economic, and fiscal trends:

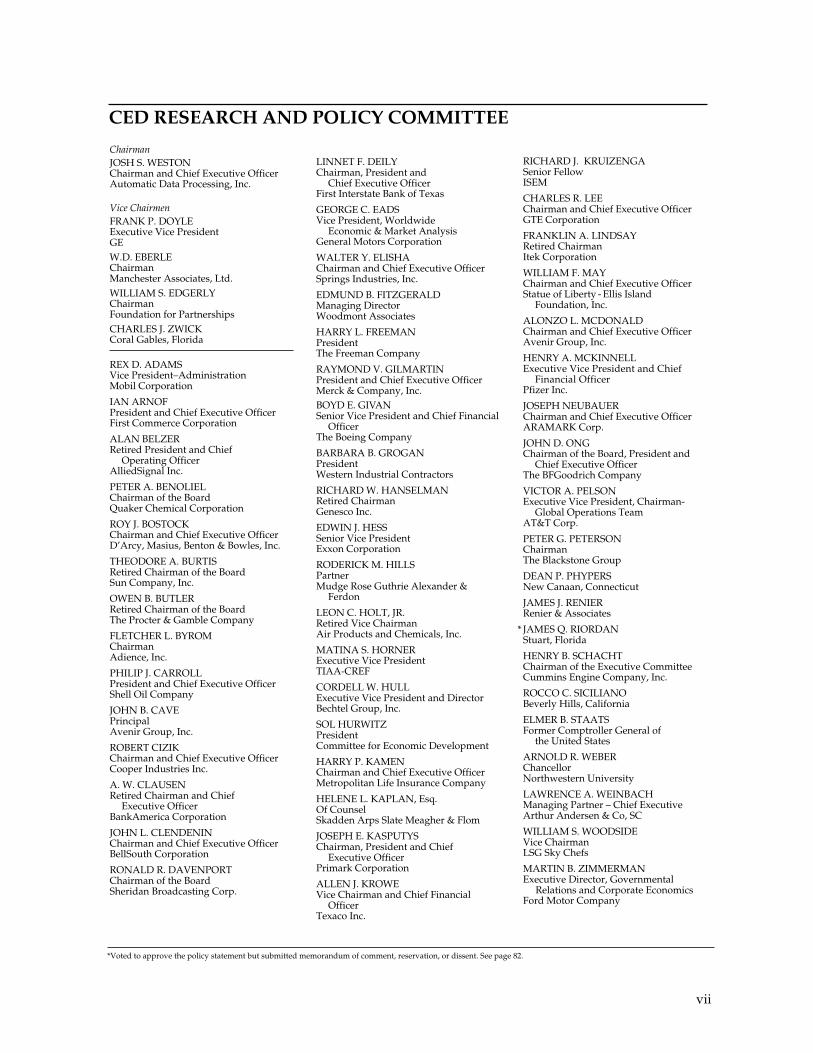

• Growth in the elderly population in theUnited States, which is already quite rapidbecause of increasing life expectancy anddeclining fertility rates, will accelerate whenthe baby-boom generation reaches retire-ment age in about a decade. A sharpdecline in the ratio of workers to retireeswill result.1

• Private saving for retirement is woefullyinadequate, and national saving hasdeclined.

• Underfunded pension promises in bothprivate and public retirement programs area growing and often understated problem.

• Rapid growth in government spending forthe elderly threatens to get so far out ofcontrol when the baby-boom generationretires that it cannot be financed by reason-able burdens on taxpayers.

Private saving is only a fraction of thatneeded to enable future retirees to fulfill theireconomic expectations in retirement. Onerecent study showed that the baby-boom gen-eration needs to triple its rate of accumulationof assets in order to maintain its preretirementliving standard during retirement. Moreover,this projection assumes that Social Securitybenefits will not be cut.2 But it is now clearthat the Social Security system has made prom-ises to future retirees that cannot be kept with-out vastly improving prefunding or imposinga harsh burden on future workers. This situa-tion has been exacerbated by ill-advisedchanges in regulatory and tax policies thathave discouraged private saving for retire-ment and by federal budget policies that havegenerated huge deficits. These deficits con-tinue to absorb the lion’s share of private sav-ing needed to ensure the economic prosperityof future citizens.

Clearly, for the vast majority of those cur-rently in the labor force, their future economiccircumstances will depend greatly upon theirown saving and participation in retirementplans. Those who are not making sufficientpreparations for retirement appear to have amisunderstanding about the impact of under-saving on their retirement income. CED be-lieves that this situation calls for a majoreducation campaign sponsored by both gov-

Chapter 1

Executive Summary andPolicy Recommendations

2

ernment and private employers to improveworkers’ understanding about their own re-sponsibilities and options for retirement.

Although the primary focus of this policystatement is private retirement programs, werecognize that private saving is only one com-ponent of the retirement finance problem.Therefore, our discussion of retirement sav-ing would not be complete without a briefexamination of the problem of underfundedpromises with respect to Social Security andpensions for public employees. Indeed, theoutlook for Social Security makes reform ofprivate retirement policies all the moreimportant.

The major thrust of the reforms recom-mended by CED can be described as follows:

• The federal government should streamlineand simplify regulation and reverse recentchanges in regulatory and tax policies thatact as barriers to private retirement savingand discourage growth in private pensioncoverage.

• Businesses and government sponsors ofretirement programs should fully fund pen-sion promises made to their workers andavoid making promises that cannot be kept.Business and government should alsoencourage an increase in the averageretirement age in recognition of theimproved health status of the elderly andthe projected need for skilled workers, andto compensate for added retirement costsarising from increases in life expectancy.

• In order to encourage individuals to in-crease their saving and take greater respon-sibility for their future, workers must bebetter educated about the effects of retire-ment saving and the choices they makeabout retirement ages, saving rates, andinvestment strategies on their future eco-nomic circumstances.

• Government should quickly legislate thegradual introduction of benefit-trimmingchanges in Social Security in order to pre-serve the long-run financial health of the

system. Social Security retirement benefitsand other benefits for the elderly shouldnot be promised if they cannot be financedeither by advance funding that adds tonational saving or by an acceptable level oftaxes on active workers.

We believe that the nation must act quicklyto reform retirement policies and practices sothat the future economic security of retireesand all other citizens will be protected. Post-poning action would simply raise the cost dra-matically; in contrast, early action imple-mented in gradual steps would minimize theimpact on the living standards of both work-ers and retirees.

THE CHALLENGE POSED BY ANAGING POPULATION

Growth in the nation’s real income andwealth has made it possible for the UnitedStates not only to provide for the basic needsof rapidly growing numbers of elderly butalso to greatly improve their economicwell-being. However, because of the aging ofthe baby-boom generation, the retired popu-lation will begin to rise much more rapidlyand the workforce more slowly during thefirst decade of the next century. The ratio ofworkers to retirees is expected to plunge fromits current level of about 3.4 to 1 to about 2 to 1by 2030 (see Figure 1).3 Consequently, provid-ing for the needs of growing numbers of eld-erly will become a much greater challenge forthe country. The share of the nation’s totaloutput consumed by this group will increase,placing a heavy burden on workers unlessthe increased consumption by retirees isprefinanced by saving, including funded pen-sions. Unfortunately, federal regulationsenacted since the mid-1980s have been inimi-cal to funding. Moreover, legislation requir-ing the delay of a large part of funding untilthe later part of workers’ careers, combinedwith the aging of the workforce (as the baby-boomers approach retirement), will raise thecost of many retirement plans sharply, therebydiscouraging the expansion of retirement ben-

3

efits. Delay in funding was required by theOmnibus Budget Reconciliation Act of 1987(OBRA 1987). See Chapter 5 and Figure 25 fora description of the effect on funding.

The upcoming bulge in the elderly popula-tion presents a particularly serious problemfor Social Security. Some of the increase inspending for Social Security benefits can befinanced by drawing down the reserve in theSocial Security trust funds. However, this willmerely delay a tax increase, and probably notfor long. The Social Security Administration’sintermediate projection indicates that the an-nual cash flow will turn negative beginning in2013 and that the reserve fund will be ex-hausted in 2029. Because earlier projections ofthe balance in the Social Security retirementtrust funds have been revised downward per-sistently and dramatically (see Figure 2), manybelieve it is more realistic to assume that thefund will run out much sooner, perhaps by2012, as in the Social Security Administration’smore pessimistic projection. When the reserves

Ratio of Workers to Social SecurityRecipients, 1980 to 2050

Ratio

(intermediate projection)

Figure 1

SOURCE: Office of the Actuary, Social Security Administration.

Year

Trillions of Dollars

1985 1995 2005 2015 2025 2035 2045 2055 2063

Figure 2

Revised Intermediate Projections for Social Security Trust Fund Balances(current dollars)

20

15

10

5

0

1983 projection

1989 projection

1994 projection

1980 1990 2000 2010 2020 2030 2040 2050

Year

4

3

2

1

0

NOTE: “Workers” defined as persons having earningscreditable for Social Security.SOURCE: Office of the Actuary, Social SecurityAdministration.

4

are exhausted, Social Security benefits mustbe financed by taxes on current wages (or byincreased debt), placing a uniquely heavy bur-den on future workers.

The actuarial deficiency in Social Security,taking into account all prospective revenuesand expenditures for the next seventy-fiveyears, was estimated at $1.9 trillion at the endof 1993.4 A rough indication of the potentialfuture burden of Social Security on activeworkers can be seen by comparing the cost ofretirement benefits with the wages of work-ers. The Social Security Administration’s 1994intermediate projection indicates that totalexpenditures for old age and survivors insur-ance and disability and hospital insurance ben-efits, or OASDIHI,5 which are financed by thepayroll tax, will increase by an alarming12 percent of taxable payroll (from more than15 percent to nearly 28 percent) during the1994–2030 period, largely as a consequence ofdemographic change (see Figure 3).6 OASDIHIbenefits are also projected to rise sharply as ashare of the gross domestic product (GDP),from 6.4 percent in 1994 to 10.8 percent in2030. These figures do not reflect the rapidlygrowing cost of supplementary medicalinsurance (SMI, or Part B of Medicare) that isfinanced primarily out of general tax revenues,the growth in unfunded retirement benefitsfrom government jobs that will also befinanced from general revenues, and otherprograms for the elderly for which long-termprojections are not available.7 Thus, it is notsurprising that many have concluded thatgovernment-related retirement and health ben-efits for the elderly must be cut back. In CED’sview, reliance on extremely high taxes paidby future workers to finance these benefitsfor the elderly would be very inequitable andhave an extremely adverse effect on the livingstandard of those workers born after thebaby-boom generation.

The impact of demographic change onpay-as-you-go retirement financing makes itimperative that pension policy be reformed toencourage increased retirement saving and toreduce unfair shifting of the burden to future

30

25

20

15

10

Percent

Social Security Retirement and HospitalInsurance Benefits and Revenues,1980 to 2030

Figure 3

(percent of taxable payroll)

Year

NOTE: Revenues exclude interest on trust funds.SOURCE: Office of the Actuary, Social SecurityAdministration.

Revenues

Benefits

1980 1990 2000 2010 2020 2030

generations of workers. Senator Robert Kerreyand former Senator John Danforth, co-chair-men of the Bipartisan Commission on Entitle-ment and Tax Reform, have responded to theSocial Security projections by proposing fun-damental changes in Social Security and theU.S. retirement system that would bringfuture outlays and revenues to near balance.However, there is substantial political resis-tance to changes in Social Security at thepresent time, although reform is criticallyneeded and delaying action will only makethe problem worse.8 But given the unavoid-able impact of the aging population onpay-as-you-go retirement systems, the mostpromising way to protect the economic secu-rity of future retirees without overburden-ing workers is to increase private retirementsaving. Many individuals look upon contri-

5

Personal and Pension Saving,1970 to 1991

Percent

Figure 4

butions to their pension funds, which are theirown assets, as much less of a burden thanincreased payroll taxes. If policy changes suc-ceed in encouraging individuals to forgo asignificant amount of consumption beforeretiring, and if sponsors of retirement pro-grams fully fund pension promises, theincome of retirees can be maintained withoutan unacceptable sacrifice by workers.

THE UNTIMELY DECLINE INRETIREMENT SAVING

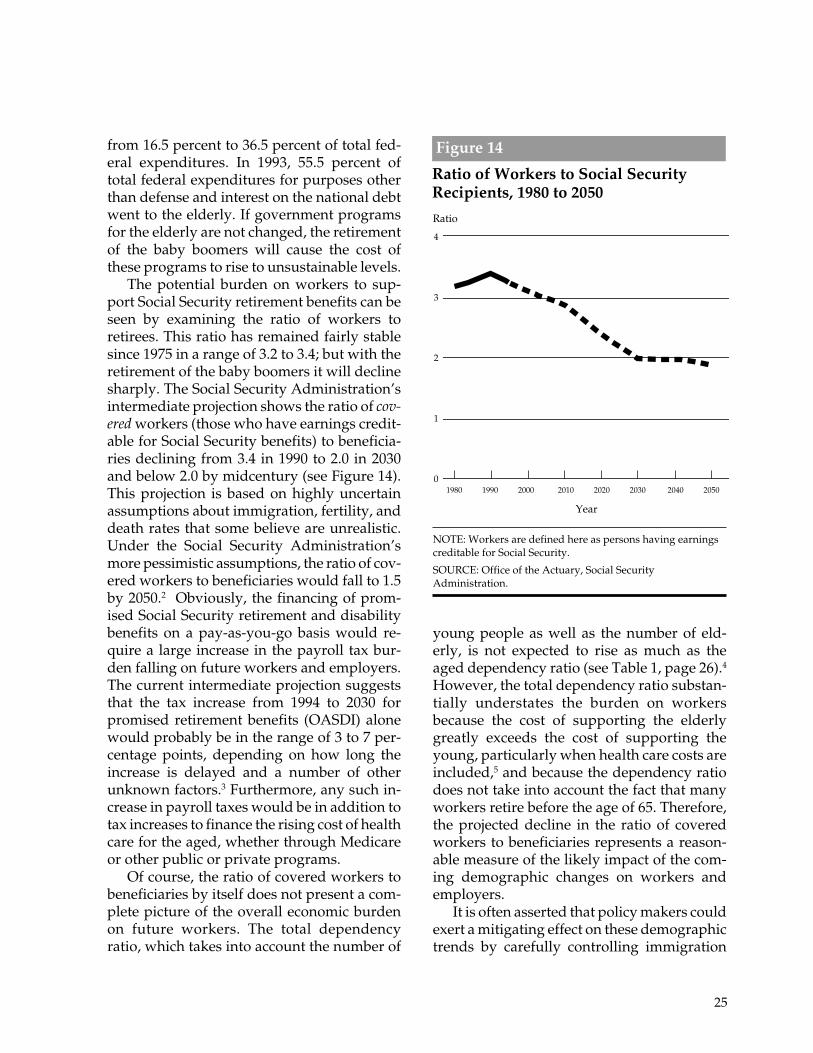

Unfortunately, saving for retirement andother purposes has declined in the UnitedStates at the very time when it should be ris-ing in anticipation of the retirement of thebaby-boom generation. Private contributionsto pensions as a percent of disposable incomehave declined in the last decade, though notas sharply as total personal saving (see Fig-ure 4).

(percent of disposable personal income)

SOURCE: Bureau of Economic Analysis; pension saving seriesprovided by staff at The Brookings Institution.

Year

10

8

6

4

2

0

Pension saving

Personal saving

Decline in Contributions to PrivatePension Plans, 1975 to 1991

Figure 5

(in 1987 dollars)

SOURCE: The Brookings Institution, Bureau of LaborStatistics, Bureau of Economic Analysis.

1975 1977 1979 1981 1983 1985 1987 1989 19911970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990

Year

Total contributions per privatesector worker

1,600

1,400

1,200

1,000

800

600

400

200

0

Employer contributions per privatesector worker

Dollars

PENSION CONTRIBUTIONSAND FUNDING

Total private pension contributionsdeclined in constant 1987 dollars from about$1,470 per worker in 1985 to about $1,140 perworker in 1991. The employer componentdeclined in real terms from about $1,039 in1980 to about $506 per worker in 1991 (seeFigure 5). Defined benefit plans, which aremore commonly sponsored by large firms, suf-fered a very sharp decrease in contributions(see Figure 6).9 Overall contributions byemployers to these plans declined largely asa consequence of three developments: (1)increased earnings on financial assets, (2) theenactment in 1987 of lower ceilings on pen-sion funding eligible for tax deductions, and(3) a sharp rise in the cost of complying withincreasingly complex regulations that discour-aged the growth of defined benefit plans, par-ticularly in small firms (see Figure 7). Total

6

Employer Contributions to DefinedBenefit Plans, 1975 to 1991

Figure 6

1975 1977 1979 1981 1983 1985 1987 1989 1991

70

60

50

40

30

20

10

0

(in 1987 dollars)

Year

SOURCE: Pension and Welfare Benefits Administration,U.S. Department of Labor.

Billions of Dollars

eral agency that insures private pensions. Itshould be noted that this insurance programalso exposes future taxpayers to a huge poten-tial liability.11

Information on underfunding of govern-ment employee pensions is incomplete, butthe magnitude of underfunding appears to begreater than for private pensions. (Of course,the government’s taxing authority makes itdifficult to compare the risks.) It has been esti-mated that the average funding ratio of allstate and local pensions is only 80 percent andthat the actuarial deficiency for federal, civil-ian, and military pensions at the end of 1992was $1.5 trillion, taking into account both pro-spective receipts and outlays.12

ECONOMIC EFFECTS OF DECLININGRETIREMENT SAVING

The decline in retirement saving not onlyjeopardizes the economic security of individual

contributions to defined contribution planscontinue to rise, however, as a consequence ofrapid growth in plan participation.

Underfunding of defined benefit pensionplans is a serious problem. Although mostprivate pensions meet legal funding require-ments, CED believes that the funding limitsenacted in the 1980s (described in detail inChapter 5) have placed many pension fundsat risk in the event of unexpected changes inthe value of financial assets and in the finan-cial strength of firms. A decline in interestrates, for example, would reduce the returnon pension assets and increase the presentvalue of future benefits, thereby causing somepensions to become underfunded. Moreover,the funding status of private pensions hasdeteriorated even by current legal fundingstandards. Underfunding of private retirementplans has been increasing rapidly, reaching$71 billion in 1993, according to the PensionBenefit Guaranty Corporation (PBGC),10 a fed-

SOURCE: Hay/Huggins Company, Inc.

15 75 500 10,000

Plan Size (number of employees)

1981

500

400

300

200

100

0

1991

Regulatory Costs Have Soared

Figure 7

(administrative costs for defined benefit plansin 1990 dollars)Dollars per Worker

7

and widespread pension coverage. Unfortu-nately, recent legislation appears to have beenmotivated by other concerns, such as the elimi-nation of every potential abuse of pensions,the impact of pension saving on the distribu-tion of income, and the budget deficit. Allthese concerns have merit but frequently can-not be addressed through pension policies with-out creating enormously complex and costlyregulation and undermining the primaryobjective of retirement policy.

CED believes that the looming crisis inretirement finance requires the prompt imple-mentation of three measures: (1) tax incen-tives and regulatory reform to encourageindividual retirement saving and to achieveincreased funding of, and coverage by, pri-vate pensions; (2) education programs thatincrease worker awareness of the need forretirement saving and encourage individualresponsibility; and (3) changes in governmentpriorities to provide full funding of publicemployee pensions, increased funding of So-cial Security, and a reduction in the growth ofspending programs and promises for the eld-erly financed from current income.

REGULATORY REFORM FOR PRIVATERETIREMENT PLANS

The objective of the 1974 Employee Retire-ment Income Security Act (ERISA), whichremains the basic pension law of the UnitedStates and deals with all facets of private pen-sions, was quite simple: to protect the pen-sions of the elderly. However, numerousamendments have since been enacted that areextremely complex, in large part because oftheir diverse objectives. These changes haveplaced many barriers in the way of increasedpension coverage and retirement saving. Forexample, complicated discrimination rules andfunding limits enacted in the 1980s havesharply increased administrative costs,reduced contributions, and placed pensionsat increased risk. From a national saving per-spective, the most serious setback wasOBRA87, which limited funding of definedbenefit plans to 150 percent of plan termination

workers but also affects the economic healthof the country, because retirement saving is avery large and growing component of nationalsaving. The U.S. national saving rate (the sumof saving for retirement and all other pur-poses by individuals, business, and govern-ment) has fallen to record low levels in recentyears. In fact, the national saving rate hasaveraged less than 2 percent of GDP so far inthe 1990s, down from 4 percent in the 1980sand about 8 percent in previous decades.Because national saving is the domestic sourceof funds for investment, its decline has anadverse effect on U.S. productivity growthand international competitiveness. Moreover,the rate of saving has been low for some time,and the cumulative effect on the nation’s capi-tal stock cannot be reversed quickly. Of course,weak growth in productivity and real wagesdoes not bode well for the living standard offuture retirees and workers.

POLICY OPTIONS TO TACKLE THERETIREMENT FINANCE PROBLEM

There are limited options for alleviatingthe burden on future workers arising from theinevitable increase in the elderly population.The most important is to make retirement sav-ing and adequate funding of pensions top pri-orities for individuals, employers, and gov-ernment. Retiree spending from retirementsaving (including benefits received fromfunded pensions) is merely the recapture ofdeferred consumption. Unlike pay-as-you-gofinancing, this recapture need not be a burdenon workers because the saving resulting fromdeferred consumption contributes to thegrowth of the economy and the growth ofworkers’ real incomes. Indeed, if the addedsaving creates sufficient income to pay for therise in benefits to retirees, active workerswould experience no increased burden as theretiree population grows.

Therefore, the basic objective of retire-ment policy should be to ensure the eco-nomic security of retirees by encouragingretirement saving, full funding of pensions,

8

liability. (Termination liability is the liability aplan would incur if it were to cease at anygiven time. 150 percent of termination liabil-ity is generally lower than 100% of projectedliability, which was the previous fundinglimit.) This change forced many firms to dis-continue further funding of pensions for sev-eral years.

By discouraging retirement saving, theseregulatory changes have clearly exacerbatedthe burden on future workers arising fromdemographic change. At the same time, regu-lators have failed to take adequate action topreserve existing retirement funds. Reformsare needed to reduce preretirement with-drawal of retirement funds for consumptionpurposes and to encourage improvements inthe portability of pension funds.

CED believes that pension regulatory andtax policies must be streamlined and simpli-fied and subjected to cost-benefit evaluation.We propose a number of changes in the regu-lation of private pensions that would greatlysimplify discrimination rules, restore thefull-funding limit to its pre-1987 level of 100percent of projected plan liability, preservepension funds for retirement, permit pensiontax preferences to be based on lifetime income(as opposed to current-year income only),encourage accelerated vesting and greaterportability of pension assets, increase theauthority of the PBGC to make sure that spon-sors of private pensions meet their fundingresponsibilities, and increase the limit on pen-sion benefits and contributions (see “Summaryof Policy Recommendations”). All our recom-mendations are designed to encourage savingand greater support for private retirement pro-grams.

RETIREMENT INFORMATION ANDINDIVIDUAL RESPONSIBILITY

Although reform of pension regulation iscritical, CED believes that it is incumbentupon individuals to take greater responsi-bility for financing their retirement. Individu-als ultimately pay for their own retirement bysaving, participating in retirement plans, and

paying taxes. We recognize, however, thatworkers are not well informed about retire-ment needs and benefits.13 Indeed, financialliteracy is low in the United States, and manyworkers do not have adequate informationabout retirement income and retirementoptions to plan intelligently for their old age.The fact that private retirement saving perworker may be only about one-third of whatwill be needed to maintain accustomed livingstandards during retirement does not appearto be widely understood by workers. There-fore, CED recommends that government andbusiness regularly provide all workers withinformation on accrued and prospectiveretirement benefits. The Social SecurityAdministration is planning to begin the distri-bution of such information soon. This isa positive development. It is criticallyimportant, however, that the information onSocial Security be as realistic as possible,including the possibility that benefits may becut in order to preserve the system. In thisway, individuals can make informed plans fortheir retirement.

REFORMING GOVERNMENTEMPLOYEE PENSIONS AND THESOCIAL SECURITY PROGRAM

It is also important to reform the fundingof government employee pensions. Indeed,CED strongly endorses the view that pen-sion promises made by both private and pub-lic employers should be fully funded andthat no promises should be made that cannotbe funded.

The specific character of required reformsin Social Security retirement programs is acomplex issue beyond the scope of this state-ment. It is clear, however, that merely passingthe burden to future generations is both ineq-uitable and bad economics. The increase intotal benefit payments that will occurbecause of the baby-boom bulge should beprefinanced, and/or benefits should be cutto limit the burden on future workers. Wealso believe that the rise in life expectancywarrants a further increase in the normal

9

of preparations for retirement and the poten-tial burden on workers, reduced benefits anddelayed retirement are not likely to be mattersof choice. However, the burden on futureretirees can be minimized by giving themadequate warning. CED believes that neces-sary reductions in future Social Security ben-efits should be enacted well before they takeeffect in order to give workers an opportu-nity to make compensating adjustments intheir saving behavior.

Such reforms would permit a largerbuildup in Social Security trust fund reservesand reduce the potential burden on futureworkers by making it possible to hold downpayroll tax rates when the baby-boom genera-tion retires. However, the effect on the payrolltax may be a misleading indicator of thefuture burden if the increased reserves do notadd to national saving. No additional resourcesare created to pay for the rise in benefitsunless the reserves add to national saving,productive capital, and economic growth.Unfortunately, it appears that the recent posi-tive cash flow in the Social Security programhas been used to pay for current governmentservices rather than to add to saving. CEDbelieves it is imperative that the positive cashflow in the Social Security program be used,not to support government consumption, butto add to national saving.

retirement age beyond the increase alreadylegislated and that the earnings limit forrecipients of Social Security should be raisedsubstantially in order to reduce the disincen-tive for the elderly to continue working. Ofcourse, a politically realistic resolution of theSocial Security financing problem is likely toinvolve both cuts in benefits, especially forhigher-income individuals, and some addi-tional taxes to increase prefunding of theretirement of the baby boomers. CED has pre-viously endorsed a proposal for full taxingof Social Security benefits in excess of thebeneficiary’s contributions. (Because low-income retirees do not pay federal incometaxes, the taxation of all benefits would havean effect somewhat similar to means testing ofbenefits.) Other reforms, such as a gradualphase-in of a lower ratio of initial benefits toincome and/or limits on the indexing of ben-efits (above the minimum subsistence level),should be considered.

The economic status of retirees hasimproved sharply in recent decades, a devel-opment that has probably raised workers’expectations relating to retirement income. Tothe degree that workers regard promisedSocial Security benefits as a right, similar to aproperty right, that should not be repealed,there may be strong resistance to theseoptions. Nevertheless, given the present state

The economic well-being of future retireesand their dependents is in jeopardy becauseof the continuing failure of our society to makeadequate preparation for an inevitable sharprise in the retirement-age population. This situ-ation is reflected in the low priority manyindividuals give to retirement saving, changesin regulations that have discouraged or lim-ited contributions to retirement plans,underfunded pensions sponsored by both pub-lic and private employers, and a looming cri-sis in the Social Security retirement system,which has promised future benefits that can-

not be provided without imposing a harshburden on future generations of workers.Unfortunately, the regulation of private pen-sions has become incredibly complex andaimed at various social objectives that oftenconflict with the goal of encouraging retire-ment saving. CED believes that policy mak-ers should focus much greater attention onthe basic goal of retirement policy, which isto ensure the economic security of the eld-erly by encouraging saving for retirement.

The adverse effects of government policieson retirement saving and work effort have led

SUMMARY OF POLICY RECOMMENDATIONS

10

us to the conclusion that current pension laws,regulations, and practices must be streamlined,simplified and designed to achieve six basicobjectives:

• Provide retirement plans for the largestpossible number of workers.

• Ensure that pension plans meet appropri-ate fiduciary standards and are funded tofulfill pension promises.

• Encourage individual saving by makingretirement saving opportunities availableto all workers through deferred taxes oncontributions and earnings and by pro-viding all workers with realistic informa-tion on their retirement saving needs,resources, and options.

• Place simple and reasonable limits on taxpreferences received by any individual(i.e., a single overall limit on eligible con-tributions indexed to inflation and a limiton benefits received from a qualifieddefined benefit plan).

• Preserve retirement saving and pensionrights by discouraging preretirementwithdrawals and by improving the port-ability of pension assets.

• Compensate for the rise in life expect-ancy by encouraging retirement at a laterage and by reducing work disincentivesfor the elderly who receive retirement ben-efits.

Both business and government shouldencourage later retirement in order to com-pensate for the rise in life expectancy, andgovernment should raise the earnings limitsapplicable to retirees receiving Social Secu-rity benefits. Although government tax andregulatory policies should encourage privatepension saving, we believe that tax incen-tives should be carefully designed to ensurethat they raise national saving as well. Pen-sion saving for retirement represent a largeand increasingly important component ofnational saving. Other legitimate fiscal policy

concerns, such as the budget deficit, shouldnot be addressed in a manner that serves toexacerbate our private saving deficiency. Inaddition, other important retirement policyissues should not be addressed in a way thatdefeats the basic saving objective of pensionpolicy.

The inadequacy of present-day retirementsaving may be due in part to confusion aboutwho is responsible for meeting the incomegoals of retirees. Apparently, some individu-als mistakenly believe that their income inretirement is entirely or principally theresponsibility of government and business. Infact, the responsibility for the income ofretirees is divided among government,employers, and individuals. However, eachindividual must bear the ultimate responsi-bility for his or her living standard in retire-ment. Social Security, which is only looselylinked to income, should continue to providea minimum level of retirement income for allworking members of society and their depen-dents. Businesses and other employers should beencouraged to voluntarily facilitate and assistsaving for retirement to the degree affordable.Company-sponsored pensions are often use-ful as a means of attracting and retaining acompetent workforce. Employer plans, com-bined with Social Security, are generallyintended to provide retirees with a reasonableminimum standard of living, though with lessincome than received by active workers.Finally, saving by individual workers should beencouraged so that they can achieve theirdesired living standard in retirement. Formany workers, their savings are a criticalsource of retirement income.

CED continues to favor strong action toreduce the federal deficit as the most certainway to increase national saving needed toimprove the growth and competitiveness ofthe U.S. economy. Some of the recommenda-tions presented in this statement wouldreduce the federal deficit; others would raiseit. We believe that any net increase in thefederal deficit resulting from reform of retire-

11

ment policies should be offset by reductionsin real spending. However, the purpose ofreducing the deficit is to increase national sav-ing; therefore, attempts to lower the deficit bytaxing private saving are counterproductiveand should be avoided.

With these goals and responsibilities inmind, CED makes the following recommen-dations:

1. Retirement plan nondiscrimination rulesgoverning coverage and contributions shouldbe streamlined and simplified in a mannerthat reduces administrative costs and in-creases saving for retirement and coverage.

Nondiscrimination rules in general, includ-ing coverage rules and nondiscrimination testsrelating to contributions under Sections 401(k)and 401(m) of the Internal Revenue Code,are complex and extremely costly to adminis-ter. These tests reduce pension saving bymiddle-income earners as well as more highlycompensated employees. With appropriategrandfathering of rules where necessary, thesetests should be replaced by a vastly moresimple and administratively inexpensive safe-guard against discrimination:

• All employees who meet nondiscrimina-tory age and service eligibility require-ments should (a) be covered and (b)receive the same ratio of employer contri-butions to wages. (In the case of definedbenefit plans, the same benefit formulashould be applied.)

If such a radical reform cannot be adoptedin its entirety, simplification should proceedalong the following lines:

• Employers who voluntarily comply withthe two nondiscrimination standardsspecified in the preceding bullet wouldbe given safe harbor from all further non-discrimination tests, such as those underSections 401(k) and 401(m) of the InternalRevenue Code.

• Employers who do not comply with boththe coverage and the uniform contribu-

tion standards mentioned above should,at a minimum, adopt the coverage rule.

• Top-heavy rules, which are already largelyredundant in view of the nondiscrimina-tion rules in place for all pension plans,should be eliminated.

• Restrictions on the employer’s ability tointegrate private pension benefits withSocial Security should be eliminated incases where the employer contribution forall employees equals or exceeds anappropriate threshold.

2. Federal regulation should encourage fullfunding of private pensions.

One of the most important causes ofdeclining business contributions to pensionsis OBRA87, which capped funding for definedbenefit plans at 150 percent of terminationliability. As a consequence of this legislationand rising asset values, many firms wereunable to make eligible contributions for sev-eral years. Firms can only ensure the viabilityof their defined benefit plans if they are per-mitted reasonable flexibility to spread the costsof funding plans over time in a manner thatrealistically reflects both expected plan liabili-ties and the firms’ ability to make contribu-tions. The full-funding limit based on termi-nation liability denies such flexibility andplaces a disproportionate burden on the firmin the later years of workers’ careers.

• The full-funding limit should be restoredto its pre-1987 level of 100 percent of pro-jected plan liability. Projected plan liabil-ity in the case of flat-dollar defined ben-efit plans should be calculated to includeanticipated increases in the dollar benefitlevel that are negotiated over time.

3. Business and government should provideworkers with adequate and realisticinformation about their pensions and SocialSecurity benefits.

Many individuals reportedly undersavebecause they are not adequately informed

12

about accumulated benefits, retirement needs,and the rate of saving required to meet thoseneeds. Individuals can prepare intelligentlyfor their retirement only if they have sufficientinformation about their retirement needs andresources as well as their saving and invest-ment options. Some employers are reportedto be reluctant to provide information on pro-spective growth of funds because they fearthat they could be liable for the outcome.

• Workers should be given realistic infor-mation about retirement needs, accumu-lated and projected benefits, the effect ofdifferent investment choices on theirretirement income (if they have controlover such choices), and the funded statusof their plan (if it is a defined benefitplan).

• The Department of Labor should provideguidance designed to encourage employ-ers to provide information on retirementsaving and investment to their employ-ees and to protect plan sponsors againstunreasonable lawsuits. For example,information provided by employers aboutpast market performance should not makeemployers legally liable if future perfor-mance is inconsistent with experience.

4. Regulation should encourage both the pres-ervation of retirement funds until the workerretires and the portability of pension assets.

Preretirement withdrawals from pensionfunds are placing the economic security offuture retirees in jeopardy. Although some ofthese withdrawals are used for investmentpurposes such as education and housing, alarge proportion is simply used for currentconsumption. CED recommends:

• In-service preretirement withdrawal andborrowing of employer contributions topension plans should be prohibited.Access to voluntary employee contribu-tions should not be prohibited, but exist-ing penalties should be retained.

• Regulators should investigate options foraccelerating vesting and for improving theportability of vested benefits from definedbenefit plans. Individuals who changeemployers should be strongly encouragedto roll over preretirement lump-sumdistributions into alternative retirementsaving instruments such as individualretirement accounts (IRAs) and definedcontribution plans maintained by theirnew employers.

5. In order to increase saving for retirementand to encourage small-business owners andmanagers to provide pension plans for allemployees, Congress should raise theannual limit on allowable plan contributionsand benefits to more reasonable levels.

Regulations limiting both contributions andbenefits are often redundant and tend toreduce pension contributions and saving, lead-ing to the abandonment of some plans anddiscouraging the formation of new ones. Lim-its on benefits also discourage higher-risk in-vestments. The following reforms should bemade:

• Retirement saving tax preferences shouldbe based on accumulated lifetime incomerather than current-year income only. Thiswould be a stimulus to saving and farmore equitable, particularly for those whomust postpone contributing because ofunusual expenses (such as medical expen-ditures) or because of a temporaryabsence from the workforce (such asparents caring for children).

• With respect to the redundancy of restric-tions on benefits and contributions, lim-its on tax preferences for contributionsare generally preferable to restrictions onbenefits. Therefore, the excise tax onannuitized pension distributions above astated threshold (now $148,500 for a singleemployee) should be eliminated, and thelimit on benefits from a qualified definedbenefit plan (now $118,800) should beraised.

13

• Given the proposed elimination of excisetaxes on distributions, a limit on total con-tributions and on considered compensa-tion should be retained. However, the con-sidered compensation limit (now $150,000)should be raised at least to its pre-OBRA93level14 (and indexed); to prevent contribu-tions for lower-income workers fromdeclining, the limit on considered com-pensation should apply only to thosewhose incomes actually equal or exceedthat limit, not to those whose projectedincomes equal or exceed it. The dollarlimit on total contributions should alsobe increased.

• Congress should discontinue the recentpractice of reducing considered compen-sation for more highly compensatedemployees as a means of raising federalrevenue. This is necessary because of itsadverse effect on pension saving, throughits impact on contributions for lower-income employees and on the willing-ness and ability of sponsors to create andmaintain qualified plans.

• Individual contributions to 401(k) plansthat are primary pension plans should besubject to the same limit that applies toother defined contribution plans, such thatthe combined employee and employercontributions do not exceed that limit.This will give workers in smaller firmsan opportunity to expand their retirementsavings and provide a greater incentivefor managers of small firms to offer theseplans to their workers.

6. The Pension Benefit Guaranty Corpora-tion reforms should improve both the sol-vency of the PBGC itself and the fundedstatus of the pension plans it insures. Thus,the PBGC premium structure and benefitguarantee should be aligned more closelywith the actual risk posed by a pension planand the PBGC should have stronger compli-ance authority to insure adequate funding

levels. Amortization periods for unfundedliabilities should be simplified and short-ened.

The PBGC’s poor financial position hasthree underlying causes: (a) Premiums for riskyplans are set too low. (b) Premiums are struc-tured in a way that creates an adverse-selectionproblem in the insurance pool. (c) The PBGC’scompliance authority is weak and there isinsufficient incentive for companies withunderfunded pension plans to increase theirfunding. Minimum-funding rules also allowamortization of some kinds of unfunded pen-sion liabilities over an excessively long period.

• The PBGC insurance premium should berestructured so that it more closelyresembles what would be offered in theprivate market. Such a redesign shouldinclude a stronger link between the pre-mium level and the actual risk that a pen-sion plan poses to the PBGC. For example,the premium calculation could take intoaccount the financial strength of the plansponsor, the marketability of plan assets,and the proportion of assets tied up in thefirm’s own equities.

• The PBGC should be given more power toinfluence the behavior of sponsors ofunderfunded plans, including the author-ity to prevent plans operating below a par-ticular funded ratio from granting benefitincreases to employees.

• The amortization schedules for unfundedliabilities should be simplified by reduc-ing the number of categories, and theamortization periods should be shortenedto accelerate the funding of liabilities.

• The PBGC’s benefit guarantee structureshould be revised to correlate more closelywith the minimum-funding requirementsattributable to specific benefits, such asshutdown benefits (see Chapter 5).

• The status of the PBGC’s claims in bank-ruptcy should be reviewed and enhanced,as appropriate.

14

7. Changes are required to place theSocial Security program on a sound finan-cial footing and avoid an unfair burden onfuture generations of workers.

Based on already-legislated benefits, pro-jected demographic changes, and other fac-tors, the Social Security Administration’slong-run projections indicate that the pro-gram’s assets will be depleted rapidly whenthe baby-boom generation retires unless ben-efits are cut and/or payroll taxes are increasedsharply. This policy statement focuses on theregulation of private pensions and does notset out a detailed program for Social Securityreform. However, the fiscal principlesespoused by CED lead us to call for the fol-lowing changes:

• All Social Security benefits that exceedpast contributions should be subject toincome tax. We also believe that the agerequirements for receiving normalretirement benefits should be raisedbeyond the increase already legislated andthat the limits on earnings of retireesreceiving benefits should be raised sub-stantially. Congress should consider otherlimitations on Social Security benefits,such as reduced cost-of-living adjustmentsfor benefits above a basic floor, and/or agradual phase-in of a lower ratio of initialbenefits to income.

• Steps should be taken to make sure thatthe building Social Security reserve fundsdo not serve to mask the non-Social Secu-

rity federal budget deficit and that theyresult in an increase in real national sav-ings.

8. Defined benefit plans sponsored by fed-eral, state, and local governments should besubject to minimum disclosure and fundingstandards. Plans should be fully funded, andpension promises that cannot be fundedshould be avoided.

The magnitude of underfunding of publicemployee pensions appears to exceed under-funding of private pensions. A substantialnumber of state and local governmentemployee pension plans are underfunded.Federal pensions are also greatly under-funded. To maintain the solvency of under-funded plans, it will be necessary toincrease taxes on future workers and/or cutbenefits.

9. Pension funds should not be required tomake investments to achieve social objec-tives other than the objective of protectingthe economic security of the elderly.

Many state and local pension funds andeven private funds are under pressure toinvest in infrastructure and to make variousother social investments. CED does notoppose arrangements that permit individualsto choose such investments, but we stronglyoppose any mandated use of pension invest-ment funds. Unless the individual chooses oth-erwise, pension investments should be basedon sound economics (e.g., risk and return),not on social considerations.*

*See memorandum by JAMES Q. RIORDAN, (page 82).

15

Chapter 2

Retirement Saving andEconomic SecurityIn coming years, America will face the

major challenge of providing for the economicsecurity of its elderly population without plac-ing unreasonable tax burdens on future gen-erations. Retirement systems are already bur-dened by the rising life expectancy and a trendtoward earlier retirement. More importantly,the United States, like many advanced indus-trial countries, will experience a very sharprise in its retired population and the retiree-worker ratio when the baby-boom generationbegins to retire.1 Unlike citizens in many othercountries, however, Americans are not settingaside resources adequate for their retirementneeds. Indeed, overall saving rates in theUnited States have fallen to record low levelswell below those of other industrial nations.Not only has the private saving rate declinedprecisely at a time when greater efforts shouldbe made to prepare for the aging of the popu-lation, but the federal budget deficit is alsoabsorbing the lion’s share of those savings,thereby further reducing the amount avail-able for investment needed to spur economicgrowth.

Saving for retirement must become a higherpriority of individuals and government policymakers if future American retirees and tax-payers are to avoid unexpected hardships. Butbuilding adequate savings, like turning a largeship, is a slow process; it will take many yearsof higher saving to boost investment to thelevels necessary to generate sufficient incometo meet the expectations of future retirees.Thus, it is urgent that saving and retirementincome policies be changed promptly. In thisstatement, CED argues that the reform of gov-

ernment tax and regulatory policies affectingprivate pension saving must play a criticalrole in this change.

THE ECONOMIC SECURITY OFFUTURE RETIREES

The retired elderly in the United Statesreceive income from a variety of sources, (see“Sources of Funds for Retirement,” page 17).The three primary components of the U.S.retirement system are: (1) the huge SocialSecurity retirement program, which providesmost retirees with benefits at least sufficientto meet their basic needs for subsistence; (2)the large and diverse private retirement sys-tem that grew rapidly with the encourage-ment of government tax incentives during thepost–World War II period and now coversabout 49 million workers;2 and (3) the retire-ment programs sponsored by federal, state,and local governments for their own employ-ees, which have grown in importance largelybecause of increasing employment in the stateand local sectors.3

These three components, together withgains in personal wealth (especially invest-ment in homes), have dramatically improvedthe well-being of present-day retirees relativeto past generations of retirees. Some studiessuggest that the overall economic welfare oftoday’s younger retirees is comparable to thatof present-day full-time workers. However,there are now serious concerns about whetherthe economic well-being of future retirees canbe maintained at the level enjoyed by currentretirees, let alone be improved, as many have

16

come to expect. The reasons for these con-cerns (discussed in detail in Chapter 3) can besummarized as follows:

• Individuals are living longer and retiringearlier. Greatly compounding this trend isthe fact that the ratio of workers to retireeswill decline sharply in the next severaldecades because of the retirement of thebaby-boom generation. Consequently, thecost to each future active worker of sup-porting retiree benefits will rise sharply.Benefits financed on a pay-as-you-go basismay have to be cut back significantly inorder to prevent taxes paid by future work-ers from becoming too burdensome.

• At present, saving for retirement is not suf-ficient in the United States to meet theincome requirements of future retirees. Thiscan be seen in the overall decline in contri-butions to retirement plans, the under-funding of many private and public plans,and record-low saving rates.

• There has been a gradual shift in coverage,especially among small employers, fromemployer-funded retirement plans to morediscretionary saving vehicles such as 401(k)plans. The impact of this trend on the eco-nomic security of future retirees is not yetknown with certainty.

Prompt changes in retirement policies canimprove the prospects of future retirees. Tocompensate for the rise in life expectancy,both business and government shouldencourage workers to take retirement at alater age. Policies should also be institutedthat encourage saving and full funding ofpension promises. Recent changes in federaltax and regulatory policies governing privatepensions have often moved policy in the wrongdirection. (For a detailed discussion, see Chap-ter 5.) Changes in pension regulation havediscouraged retirement saving and contrib-uted to the underfunding of many pensions.

The American taxpayer has more than onereason to be concerned about the impact of

insufficient saving for retirement. Futureretirees who have inadequate incomes maydemand increased retirement benefits fromSocial Security (or at least resist any cutbackin benefits). Those with inadequate savingsare more likely to become a burden on thegovernment in other areas, such as long-termhealth care. Inadequate saving for retirementalso affects the economic health of the nationmore broadly.

THE ECONOMY AND RETIREMENTSAVING

Although this statement focuses primarilyon the economic security of future retirees, wecannot overlook the adverse effect of pensionpolicy on the economy and, in turn, the im-pact of a weakened economy on the well-beingof future retirees. The decline in saving forretirement and other purposes has serious ad-verse implications for the future economicprosperity of the nation; a weak economy withlittle or no growth in productivity and realwages will, in turn, struggle to provide ad-equate support for rising numbers of retireesand to address other social problems. The So-cial Security Administration’s underfundedliability for baby-boomer retirement benefitsis a case of too many claims on too little out-put. One way to think about the impact of theburden of rising benefits for baby boomers isto ask: How much output will be left for work-ers? The implication of the Social SecurityAdministration’s intermediate projection isthat nearly a quarter of the assumed 1.2 per-cent annual gain in labor productivity (realGDP per worker) between 2010 and 2030 willbe absorbed by rising benefits paid by SocialSecurity retirement, disability and hospitalinsurance benefits alone. However, the SocialSecurity Administration’s history of overopti-mistic projections and the record-low nationalsaving rates experienced in recent years raisethe question of whether Social Security’s pro-ductivity assumption is again too optimistic.If so, these programs will absorb an even

17

SOURCES OF FUNDS FOR RETIREMENT

There are six primary sources of retirementincome, the funding of which will determinewhether retirees’ incomes meet expectations.To the degree that funding falls short, eitherretirees’ entitlements and aspirations will haveto be curtailed (by delay of retirement or byreduced living standards during retirementyears), or the intergenerational transfer of pur-chasing power from the working generation tothe retired generation must be increased, prima-rily through higher payroll taxes.

1. Social Security. About 90 percent of all work-ers participate in the Social Security system,whose role is to guarantee at least a minimumlevel of retirement income for every eligibleretiree. This government program has greatlyreduced poverty in America, although 12 per-cent of older people are still below the povertylevel. In 1994, the median benefit for an indi-vidual was about $9,972. The maximum annualbenefit for a couple is now $20,646.

2. Defined Benefit Plans. The largest accumula-tion of retirement funds is in defined benefitplans, which promise specific benefits and aretypically sponsored by large employers.Approximately 15 percent of workers areenrolled in such plans, though there has beena tendency for small employers to discontinuethe plans because of excessive regulatory bur-dens and costs. These plans, in combinationwith Social Security, generally replace about 60percent of preretirement earnings for those whohave worked at least thirty years. But workerswho change jobs frequently or work part-timeoften fail to qualify or accumulate adequatevested benefits from these plans. (Those who dobecome vested may receive benefits from morethan one plan.) Government workers are gener-ally covered by defined benefit plans, many ofwhich are underfunded and frequently havemade overly generous promises.

3. Defined Contribution Plans. These planspromise no specific retirement benefit; instead,employers make specific contributions (often

according to a formula related to income orprofits) to an employee’s retirement account.Such plans are often favored by smaller firmsbecause they are less regulated and have loweradministrative costs and more certain contribu-tion requirements. An important advantage ofdefined contribution plans is that there is nopublic liability for inadequate funding. How-ever, these plans often produce a lesser finalbenefit than a defined benefit plan. There arefive times as many defined contribution plansin the United States as defined benefit plans, butmany are small, and only about 26 percent ofU.S. workers are currently active participants ina defined contribution plan that is their primaryretirement plan.

4. Personal Savings. For retirees, the mediancash income from assets was $2,356 in 1990. Butpersonal saving has declined sharply in recentyears, perhaps reflecting misinformation aboutthe adequacy of provisions for retirement. TheSocial Security Administration will soon launcha program to provide workers with more infor-mation; this information, together with betterinformation from employers, is necessary ifworkers are to understand the need for in-creased saving.