Cédric PHILIBERT Renewable Energy Division International ... · ©OECD/IEA 2013 Renewables:...

43

© OECD/IEA 2013 Renewables: challenges and opportunities for the power grid Cédric PHILIBERT Renewable Energy Division International Energy Agency Atoms for the Future, Paris, 22 October 2013

Transcript of Cédric PHILIBERT Renewable Energy Division International ... · ©OECD/IEA 2013 Renewables:...

© OECD/IEA 2013

Renewables: challenges and

opportunities for the power grid

Cédric PHILIBERT

Renewable Energy Division

International Energy Agency

Atoms for the Future, Paris, 22 October 2013

© OECD/IEA 2013

� Renewable electricity projected to scale up by 40% from 2012 to 2018

� Broadly on track with 2020 IEA 2°C scenario targets

Positive mid-term outlook for renewable

electricity

0%

5%

10%

15%

20%

25%

30%

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2006 2008 2010 2012 2014 2016 2018 2020

TWh

Hydropower Bioenergy Onshore windOffshore wind Solar PV CSPGeothermal Ocean % Total generation

IEA 2° C Scenario

Global renewable electricity production, by technol ogy

Gas-fired generation 2016

Nuclear generation 2016

Source: Medium-Term Renewables Market Report 2013

© OECD/IEA 2013

The whole RE power mix accelerating its growth

� Hydro remains the largest increasing single renewable technology

� But for the first time additional generation from all non-hydro sources

exceeds that from hydro

Recent cumulative additions (TWh) Forecast cumulative additions (TWh)

© OECD/IEA 2013

But other technologies lagging behind

� Potential of offshore power remains high, but technical, financial

and grid connection issues pose challenges

� Storage adds value to CSP, but deployment hampered by

relatively high costs

0

10

20

30

40

50

60

70

80

90

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

TWh

OECD Americas OECD Asia Oceania OECD Europe Africa Asia ChinaNon-OECD Europe Non-OECD Americas Middle East MTRMR 2012

Wind offshore Concentrated Solar Power

0

5

10

15

20

25

30

35

40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

TWh

OECD Americas OECD Asia Oceania OECD Europe Africa Asia ChinaNon-OECD Europe Non-OECD Americas Middle East MTRMR 2012

© OECD/IEA 2013

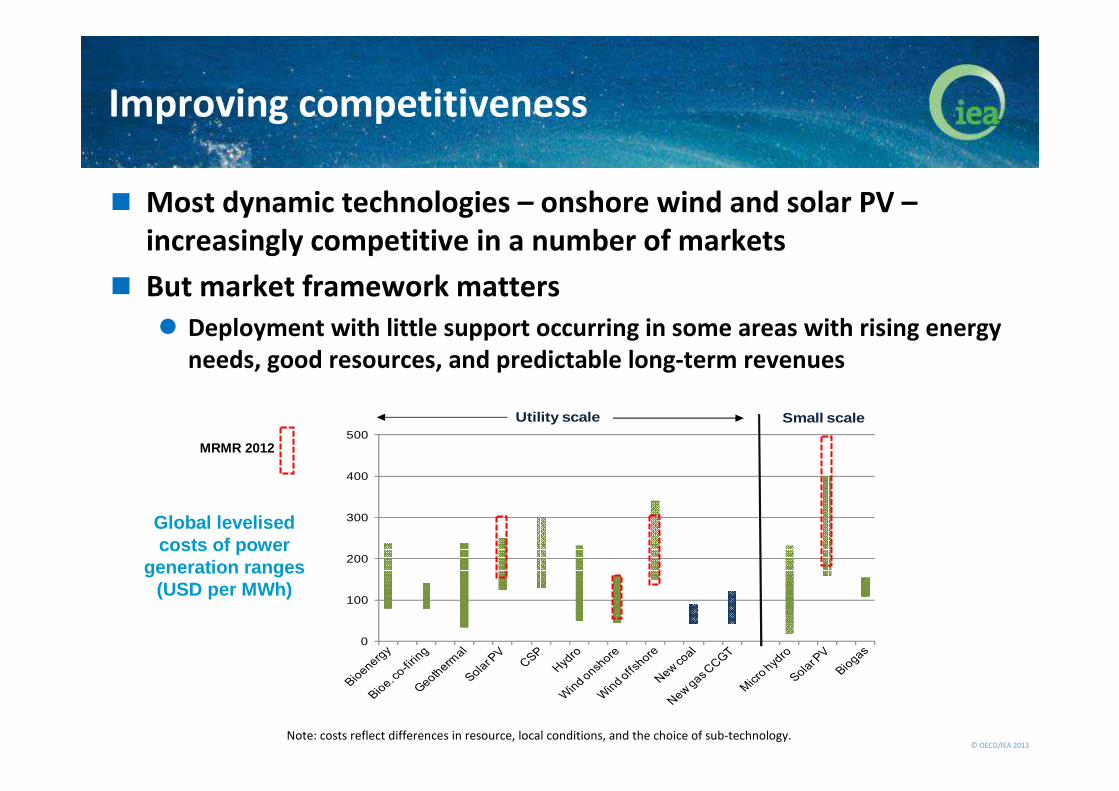

Improving competitiveness

� Most dynamic technologies – onshore wind and solar PV –

increasingly competitive in a number of markets

� But market framework matters

� Deployment with little support occurring in some areas with rising energy

needs, good resources, and predictable long-term revenues

Global levelised costs of power

generation ranges (USD per MWh)

Note: costs reflect differences in resource, local conditions, and the choice of sub-technology.

MRMR 2012

0

100

200

300

400

500

Small scaleUtility scale

© OECD/IEA 2013

Renewable power spreading out everywhere

� Emerging markets more than compensate for slowing growth and volatility

in markets such as Europe and the US

Total Renewable Annual Capacity Additions, by regio n (GW)

This map is without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any

territory, city or area.

Source: Medium-Term Renewables Market Report 2013

© OECD/IEA 2013

Non-OECD accounts for two-thirds of growth

� In 2018, non-OECD comprises 58% of total renewable generation, up

from 54% in 2012 and 51% in 2006

� China leads with deployment of a broad portfolio of renewables

� Other key markets: Brazil (wind, bioenergy), India (wind, solar, bioenergy), South

Africa and Morocco (wind, solar), Thailand (bioenergy), Middle East (solar)

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

TWh

OECD Americas OECD Asia Oceania OECD Europe Africa Asia ChinaNon-OECD Europe Non-OECD Americas Middle East MRMR 2012

Global renewable electricity production, by region

© OECD/IEA 2013

RE largest contributor to total

electricity increase in OECD

� Renewables expected to grow almost like fossils in America,

and more than total demand in Europe

- 100

100

300

500

700

900

1 100

Total OECD OECD Americas OECD Asia Oceania OECD Europe

TWh

Renewables Nuclear Fossil fuels Others

Changes in power generation by source and region, O ECD, 2012-18

© OECD/IEA 2013

Over the longer term, the power

generation mix is set to change

Global electricity generation by source, 2010-2035

Renewables electricity generation overtakes natural gas by 2016 & almost coal by

2035; growth in coal generation in emerging economies outweighs a fall in the OECD

2 000

4 000

6 000

8 000

10 000

12 000

14 000

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

TWh

Coal

Renewables

Gas

Nuclear

Oil

Source: IEA World Energy Outlook 2012 New Policies Scenario

© OECD/IEA 2013

Global climate-friendly electricity

mix by 2050

Renewables to provide 57 to 71% of World’s electricity by 2050

in 2 degree scenarios - VRE 22 to 32%

Renewables57%

Variables32%

22%

71%

© OECD/IEA 2013

The IEA Technology Roadmaps:

Hydropower

� IEA roadmaps look at

technologies required to limit

climate change at 2°C

� HP roadmpa co-authored with

Brazil’s Ministry of Mines and

Energy

� Reviewers from agencies,

academia, governments,

industry, NGOs

� Support from CEPEL, ADEME,

Iberdrola

© OECD/IEA 2012

© OECD/IEA 2013

Vision for Hydropower IEA

Roadmap

Hydropower generation will double by 2050 and

reach 2 000 GW and 7 000 TWh, mostly from

large plants in emerging/developing economies© OECD/IEA 2012

China

India

AseanOther Asia Pacific

Africa M. East

OECD Europe

RussiaTransition eco.

Canada

Other LAM+Mex

Brazil

USA

Asia Pacific

Africa

Europe & Eurasia

Central & South America

North America

Middle East

16%

19%

17%

Share on total electricity generationTWh

© OECD/IEA 2013

Technical improvements

� Strengthened environmental requirements may

reduce hydropower output and potential

� Technical improvements allow to increase or

maintain performance and output, and reduce

environmental impacts© OECD/IEA 2012

© OECD/IEA 2013

IEA Wind Power Roadmap 2013

� Update considers recent trends

and revised long-term targets:

� By 2050, 15% to 18% of global

electricity, vs. 12% targeted in the

former roadmap

� Technology and cost evolution

� 2050 “Vision” based on global

energy context and system

optimization

� Barriers and policy

recommendations

© OECD/IEA 2013

Wind power deployment to 2050

in the Roadmap Vision

� Wind power to provide 15% to 18% of global electricity

� China, Europe and the USA together account for two thirds

© OECD/IEA 2013

Land-based and offshore

deployment and costs

� By 2050, 25% of total global wind capacity to be located at sea,

up from 6% in 2020

� Investment costs for wind power to decrease by 25% on land

and 45% off shore by 2050

© OECD/IEA 2013

Technology Evolution

� Growth in size, height

and capacity

� Greater capacity

factors

� Easier access to sites

with lower-speed

winds

� Easing grid

integration with

more regular output

© OECD/IEA 2013

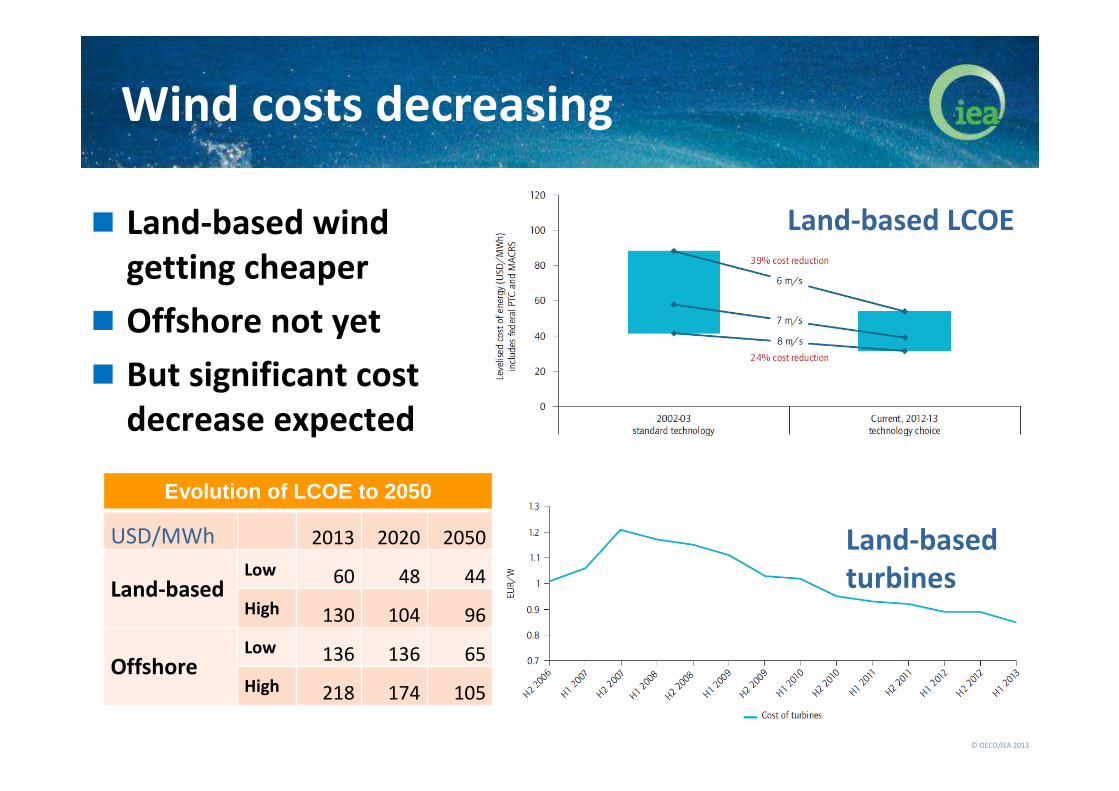

Wind costs decreasing

� Land-based wind

getting cheaper

� Offshore not yet

� But significant cost

decrease expected

Land-based LCOE

Land-based

turbines

Evolution of LCOE to 2050

USD/MWh 2013 2020 2050

Land-basedLow 60 48 44

High 130 104 96

OffshoreLow 136 136 65

High 218 174 105

© OECD/IEA 2013

PV Annual Capacity Additions (GW)

Strong growth seen in China, Africa, Middle East, and Latin America

0

1

2

2012 2015 2018

0

5

10

15

20

2012 2015 2018

0

1

2

3

2012 2015 2018

0

1

2

3

4

5

2012 2015 2018

Solar PV growing out of Europe

© OECD/IEA 2013

Medium Term RE Market Report 2013

PV generation to 2018 by regions

© OECD/IEA 2013

PV Module Prices

� Technology improvements and economies of scale

drive sharp cost reduction

� Overcapacity leads to price setting below costs

© OECD/IEA 2013

Rapid system cost cuts

0

1

2

3

4

5

6

7

8

20

08

20

09

20

10

20

11

20

12

20

08

20

09

20

10

20

11

20

12

20

08

20

09

20

10

20

11

20

12

20

08

20

09

20

10

20

11

20

12

20

08

20

09

20

10

20

11

20

12

€/

W

PV system Price (€/W) Median

1-3 kW 3-20 kW 20-200 kW 200 – 1000 kW > 1 MW

Solar PV system costs in Italy by size, EUR/W

Source: GSE, 2013. Note: includes VAT.

© OECD/IEA 2013

PV LCOE depends on

Solar Resource and Cost of CapitalBest ‘sustainable’price ground-mounted PV systems: USD 1.7/W

� Costs soon to reach competitive levels when and

where all favourable circumstances are met

Murcia, Spain

South Germany Sicily, Italy

South France

© OECD/IEA 2013

Time GW TWh Scenario Source

2018308

(370-390)

368Medium Term RE Market Report 2013

2020 210 298 IEA Technology Roadmap (2010)

2035

602 846 NPS

World Energy Outlook 2012

966 1 371 450

2050

3 155 4 572 IEA Technology Roadmap (2010)

2 017 2 655 2DS

Energy Technology Perspectives 2012

3 289 4 822 hiRen

>2060 12 000 18 000 « Testing

limits »

Solar Energy Perspectives (2011)

Various IEA scenarios for PV

© OECD/IEA 2013

Distributed PV reaching “grid parity”

in some markets � Economics of distributed PV for self-consumption improving rapidly

� Difficult to quantify deployment – further monitoring needed

Residential solar PV LCOE vs. average retail power prices (variable tariff)

Examples correspond to Southern Germany, Southern California and Southern Italy. LCOEs use average residential system costs (include VAT and sales tax in California and Italy where they are applicable) and do not include financial incentives; ranges represent differences in financing costs and full load hours. The variable component of residential electricity prices calculated from average annual household electricity prices and estimation of fixed and variable components as reflected on a household electricity bill. In Germany and Italy, variable component is estimated at 91% while in California variable tariffs account for 99% of the bill. 2012 electricity prices are taken as proxy for 2013 in Germany and Italy where data not yet available. 2013 prices in California based on 1Q2013.

0

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013

USD/MWh

Germany Italy California

Average residential electricity price (variable tarif f )

USD/MW

Residentialsolar PV, LCOE

estimates:

© OECD/IEA 2013

Variability limits self-consumption

June - cloudy June - sunny June – partly cloudy

March – partly sunny

December –cloudy

December – very cloudy

In grey, electricity drawn from the grid. In blue, electricity injected into the grid. In green, self-

consumption. Numbers indicate the percentage of self-consumed electricity. Horizontal axes: hours.

Vertical axes: watts. Source: Génin, 2013.

� Self-consumption higher for:

� Some office and commerce buildings with high daily consumption,

and relatively small systems on multi-storey dwellings

� Self-consumption potentially increased with:

� Load management

� Decentralised electricity storage (if/when affordable)

Daily self-consumption example – a household with 5-kW PV system in Germany

© OECD/IEA 2013

Paying for grid injected excess power

Payment System

Where Observations

FIT/FIP Germany •FIT below LCOE•Reduces FIT costs

Net Metering Denmark, US States, Australia(Italy since July )

•Netting period critical•Can over-reward generation•Overall level often capped

Market based or avoided

cost

California •Likely to be more sustainable in long-term

© OECD/IEA 2013

Electricity System Implications

System Concerns

RE Surcharge

Foregone Tax

Fixed Grid Cost Recovery

•Who pays as commercial power demand reduced?

� More time-based pricing and different user profile-adjusted

tariffs

Integration Costs•Depend on match of PV output and peak demand

�Need for better assessment

© OECD/IEA 2013

Solar thermal electricity (CSP plants)

Solar Receiver

Heliostats

Absorber Tube

Pipe with thermal fluid

Curved mirror

Receiver / Engine

Reflector

Central Receiver

Parabolic Trough

Dish/Engine

Linear Fresnel

Absorber tube andreconcentrator

Curvedmirror

Solar Receiver

Heliostats

Solar Receiver

Heliostats

Absorber Tube

Pipe with thermal fluid

Curved mirror

Receiver / Engine

Reflector

Receiver / Engine

Reflector

Central Receiver

Parabolic Trough

Dish/Engine

Linear Fresnel

Absorber tube andreconcentrator

Curvedmirror

Linear Concentration

C: 100

T: ~ 500 °C

Point Concentration

C: 1000+

T: ~ 1000+ °C

© OECD/IEA 2013

� Higher costs but built-in

thermal storage

� When demand peaks after

sunset!

� If PV (plus minimum load of

back-up, if any) already

saturates demand at noon

Why STE/CSP might survive the

competition of PV

� Only competing option (for now): pump-hydro storage

� Saudi Arabia plans for 2032: PV 16 GW and 25 GW STE/CSP;

China’s plans for 2030

� STE very flexible, helps accommodating more PV (when

replacing coal)

© OECD/IEA 2013

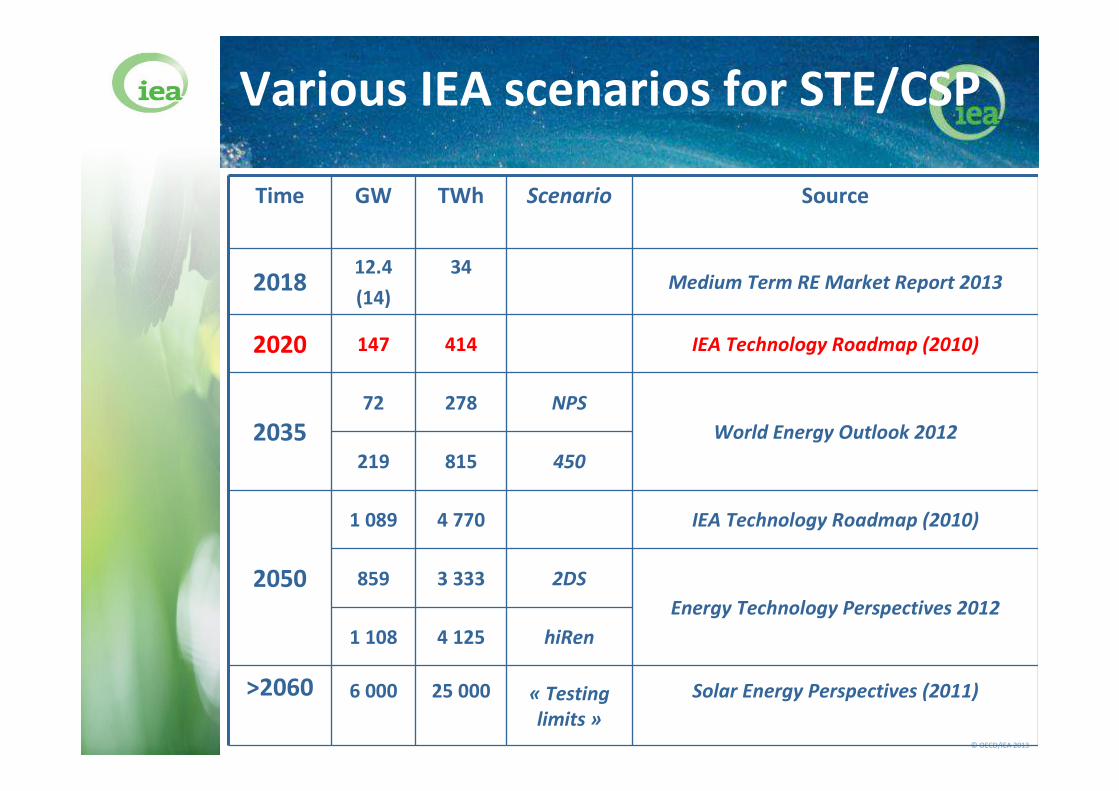

Time GW TWh Scenario Source

201812.4

(14)

34Medium Term RE Market Report 2013

2020 147 414 IEA Technology Roadmap (2010)

2035

72 278 NPS

World Energy Outlook 2012

219 815 450

2050

1 089 4 770 IEA Technology Roadmap (2010)

859 3 333 2DS

Energy Technology Perspectives 2012

1 108 4 125 hiRen

>2060 6 000 25 000 « Testing

limits »

Solar Energy Perspectives (2011)

Various IEA scenarios for STE/CSP

© OECD/IEA 2013

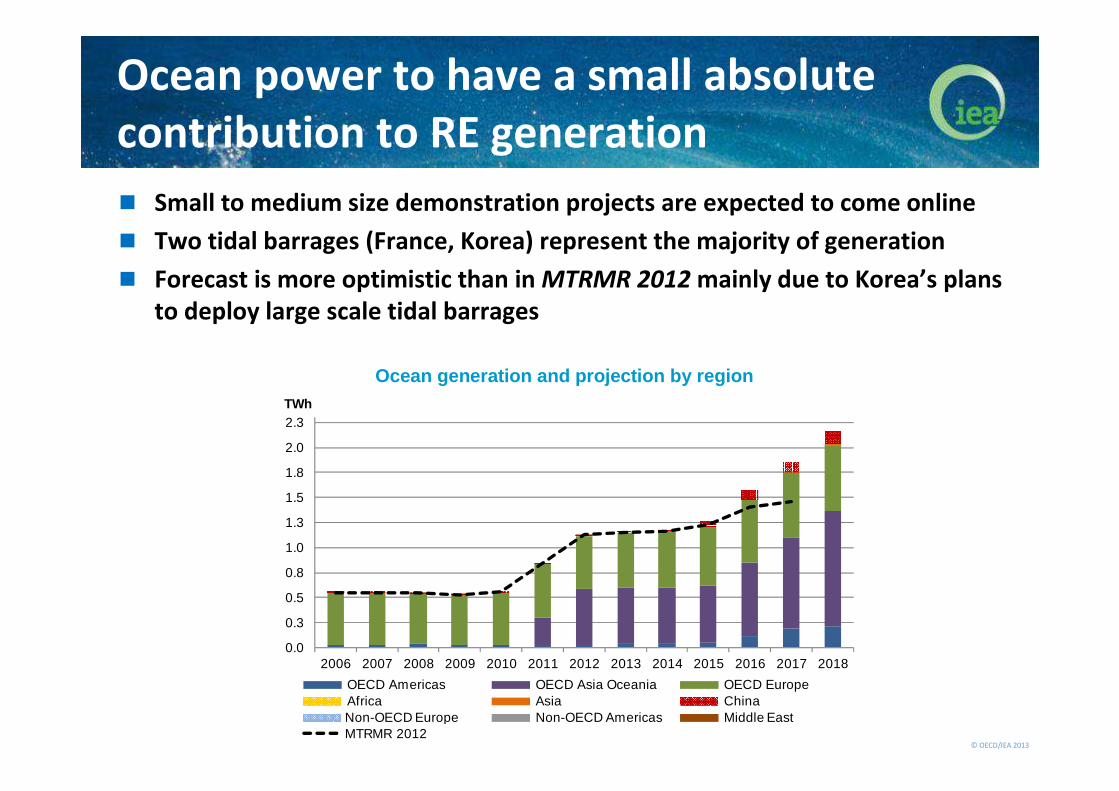

Ocean power to have a small absolute

contribution to RE generation

0.0

0.3

0.5

0.8

1.0

1.3

1.5

1.8

2.0

2.3

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

TWh

OECD Americas OECD Asia Oceania OECD Europe Africa Asia ChinaNon-OECD Europe Non-OECD Americas Middle East MTRMR 2012

Ocean generation and projection by region

� Small to medium size demonstration projects are expected to come online

� Two tidal barrages (France, Korea) represent the majority of generation

� Forecast is more optimistic than in MTRMR 2012 mainly due to Korea’s plans

to deploy large scale tidal barrages

© OECD/IEA 2013

Geothermal advances but with slower

growth rates

0

10

20

30

40

50

60

70

80

90

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

TWh

OECD Americas OECD Asia Oceania OECD Europe Africa Asia ChinaNon-OECD Europe Non-OECD Americas Middle East MTRMR 2012

Geothermal generation and projection by region

� Investment risks associated with drilling and exploration remains as a major

challenge to deployment

� 60% of growth to come from OECD countries and the rest from Southeast

Asia , Africa and Latin America

© OECD/IEA 2013

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 2016 2017 2018

TWh

OECD Americas OECD Asia Oceania OECD Europe Africa Asia ChinaNon-OECD Europe Non-OECD Americas Middle East MTRMR 2012

Bioenergy scales up with increased use of

agricultural, municipal waste and co-firing

� China is largest grower, with ambitious targets and increasing renewable

waste-to-energy plants

� Other non-OECD countries – Brazil, India and Thailand – also expected to

add significant new generation

� OECD growth dominated by Europe, driven by 2020 targets

Bioenergy generation and projection by region

© OECD/IEA 2013

Variable RE will need more Flexibility

Grid

infrastructure

Dispatchable

generation StorageDemand side

integration

� Value of flexibility has to be reflected in the market

� Need for a suite of different flexibility options

� GIVAR III study to be published in January 2014

© OECD/IEA 2013

PSP: 99% of current on-grid storage

� Pumped-hydro plants the reference solution

� 140 GW in service, 50 GW in development

� PSP developed from existing hydro plants

� “off-stream” or “pumped-back” schemes

� Small energy volumes but large power capacities

� Daily/weekly storage does not require large areas

© OECD/IEA, 2011

Source: Inage 2009. © OECD/IEA 2012

© OECD/IEA 2013

Vision for PSP deployment by 2050

China USA Europe Japan RoW Total

Low

vRE/totalenergy

21% 24% 43% 18%

Hydro/totalenergy

14% 6% 13% 12%

PSP/total capacity

4% 4% 6% 11% 2%

GW 119 58 91 35 109 412

High

vRE/totalenergy

34% 37% 48% 33%

Hydro/totalenergy

15% 6% 11% 13%

PSP/total capacity

5% 8% 10% 12% 3%

GW 179 139 188 39 164 700

© OECD/IEA 2010

The way forward: testing the limits� Under severe climate constraints…

� What if other low-carbon energy options are

not easily available?

� Where are the technical limits to solar energy?

� Assuming efficiency improvements and further

electrification of buildings, industry and transport

� Not always least cost, but affordable options

� Footprint, variability and convenience issues

� Three broad categories of situations:

� Sunny and dry climates, where CSP dominates

� Sunny and wet climates, with PV backed by hydro

� Temperate climates, with wind power and PV

backed by hydro, pumped-hydro and H2-NG plants

© OECD/IEA 2010

Testing limits: key role of electricity� Electricity share keeps growing as efficient end-

use technologies continue to penetrate marketsS

ou

rce: H

eid

e e

t al. 2

01

1S

ou

rce: H

eid

e e

t al. 2

01

1

©O

EC

D/IE

A, 2

01

1

� Solar energy dominated by power (STE and PV)

� Space heating needs reduced and satisfied with

ambient heat through heat pumps

� Many options converging towards USD 100/MWh

� Solar PV (and wind) electricity storage where STE is

not feasible: pumped-hydro plants

cp1

Diapositive 39

cp1 Paolo: add illustrations in these four slidesieauser; 26/08/2011

© OECD/IEA 2010

Testing the limits: Electricity by 2060

© OECD/IEA, 2012

------ 3000

© OECD/IEA 2010

� Footprint and variability solvable issues

� Solar energy, wind power, hydro power and

biomass provide most of the world’s final

energy demand

� Other renewables important in places

� Some uses of fossil fuels still required, but CO2

emissions reduced to 3 Gt or less if CCS is available

Testing limits:

key results

� If energy efficiency is greatly improved

� Solar energy

could provide a

third of final

energy after 2060

© OECD/IEA 2013

A reminder