Carbon Removal Potential: An Overview

13

Confidential. © 2021 IHS Markit ® . All rights reserved. 2 August 2021 Paola Perez-Peña, Principal Research Analyst, [email protected] Edurne Zoco, Executive Director, [email protected] Global Clean Energy Technology Carbon Removal Potential: An overview Workshop

Transcript of Carbon Removal Potential: An Overview

Confidential. © 2021 IHS Markit®. All rights reserved.

2 August 2021

Paola Perez-Peña, Principal Research Analyst, [email protected]

Edurne Zoco, Executive Director, [email protected]

Global Clean Energy Technology

Carbon Removal Potential: An overview

Workshop

Confidential. © 2021 IHS Markit®. All rights reserved.

Carbon sequestration solutions are classified in two main groups: nature-

based solutions and technology-based solutions

Engineered Carbon Removal Workshop | August 2021

2

Carbon sequestration solutions

Technology-based solutions Nature-based solutions

Afforestation and reforestation

Soil carbon sequestration

Biochar

Enhanced weathering and ocean

alkalinization

Ocean fertilization

Direct air capture (DAC)

Bioenergy with carbon

capture and storage (BECCS)

Carbon capture, utilization and

storage (CCUS)

• Carbon capture and storage

(CCS)

• Carbon capture and utilization

(CCU)

© 2021 IHS Markit.

Source: IHS Markit

Carbon removal: Is a group of nature-base

and technology-base solutions that remove

and sequester carbon dioxide (CO2) from the

atmosphere.

Confidential. © 2021 IHS Markit®. All rights reserved.

Engineered Carbon Removal Workshop | August 2021

3

• CCUS focuses on reducing CO2 emission from new

and existing fossil fuel-based power and industrial

plants.

• CCUS could address up to 54% of global

emissions if deployed in sectors such as power

generation/heat, industrial processes, and

transformation sectors (refining). However, owing

to competition with other technologies, CCUS is

expected to address between 4% and 20% of

emissions.

While CCUS removes CO2 emissions from fossil fuel–based power and

industrial plants, carbon removal solutions balance emissions in atmosphere

Confidential. © 2021 IHS Markit®. All rights reserved.

Overview of the current market

Engineered Carbon Removal Workshop | August 2021

4

Confidential. © 2021 IHS Markit®. All rights reserved.

Technology-based solutions have been driven by CCU projects, which

account for 79% of current CO2 capture capacity

16%

79%

5%

0%

CCS CCU BECCS DAC

Current CO2 capture capacity by

solution

© 2021 IHS Markit

Note: This chart does not include “storage

only” projects.

Source: IHS Markit

0

20

40

60

0

1

2

3

4

5

6

7

8

9

CCU CCS BECCS DAC Total CO2 cumlative capacity

Evolution of CO2 capture capacity—All technology-based solutions

Note: This chart does not include “storage only” projects.

Source: IHS Markit © 2021 IHS Markit

Ye

arl

y c

ap

ac

ity a

dd

itio

ns

by

tec

hn

olo

gy (

MM

t/y)

Cu

mu

lati

ve

CO

2c

ap

ture

ca

pa

cit

y (

MM

t/y)

Total CO2 cumulative capacity

Engineered Carbon Removal Workshop | August 2021

5

Confidential. © 2021 IHS Markit®. All rights reserved.

Most of the current CCUS* capacity is in the Americas, with the US accounting

for more than 50% of the capacity, mainly from natural gas processing

Engineered Carbon Removal Workshop | August 2021

6

* CCUS includes CCS and CCU projects.

Note: AE = United Arab Emirates; AU = Australia; BR = Brazil; CA = Canada; CN = mainland China; NO = Norway; US = United States.

Confidential. © 2021 IHS Markit®. All rights reserved.

BECCS and DAC solutions are still in the demonstration phase, current

operating capacity accounts for only 5% of total CO2 capture capacity

Engineered Carbon Removal Workshop | August 2021

7

0

2

4

6

8

10

12

14

16

18

20

0

1

2

3

4

5

North America Europe Asia Total CO2 cumlative capacity

DAC projects additions by year

Note: Two projects on 2010 and 2018 from Global Thermostat are not operating. The innovation center from Carbon Engineering is not considered in

this chart.

Source: IHS Markit, IEA, company website © 2021 IHS Markit

Nu

mb

er

of

pro

jects

Cu

mu

lati

ve C

O2

cap

ture

cap

acit

y (

tho

usan

d

metr

ic t

on

s p

er

year)

Total CO2 cumulative capacity

0

1

2

3

0

1

2

3

4

North America Europe Asia Total CO2 cumlative capacity

Bioenergy with CCU/CCS operating projects by year

Note: *All project during 2019 were pilots.

Source: IHS Markit, IEA, NETL CCUS Database, MIT Carbon Capture and Storage Project Database © 2021 IHS Markit

Nu

mb

er

of

pro

jects

Cu

mu

lati

ve C

O2

Cap

ture

Cap

acit

y

(MM

t/yr)

Total CO2 cumulative capacity

Confidential. © 2021 IHS Markit®. All rights reserved.

Carbon sequestration potential

Engineered Carbon Removal Workshop | August 2021

8

Confidential. © 2021 IHS Markit®. All rights reserved.

Consensus on the need for carbon sequestration is increasing

0%

5%

10%

15%

20%

25%

0 1 2 3 4 5 6 7 8 9

CCUS BECCS and other carbon removal Current capacity

Carbon sequestration share to meet net-zero targets—Scenarios

© 2021 IHS Markit

CO

2em

issio

ns a

bate

men

t (%

)

CO2 capture capacity by 2050 (billion metric tons per year)

Note: IHS Markit Accelerated Carbon Capture and Storage numbers includes both CCUS and BECCS.

*These scenarios estimate net zero will be reached beyond 2050.

Source: IHS Markit, IRENA, IEA, IPCC, BP, Shell

Engineered Carbon Removal Workshop | August 2021

9

CCUS

Bioenergy

IRENA -1.5 S

IRENA -1.5 S

Shell’s Sky

Scenario*

Shell’s Sky

Scenario*

IEA SDS*

IPCC 1.5

(low-overshoot)

0 2 4 6 8 10

IPCC 1.5

IRENA - 1.5 S

CCUS

CCUS capacity expected by 2050 per scenario

© 2021 IHS Markit

CO2 capture capacity by 2050 (billion metric tons per year)

Source: IHS Markit, IRENA, IPCC

52xCurrent capacity

190xCurrent capacityOptimistic

scenario

Conservative

scenario

BP Net-Zero Scenario

BP Net-Zero

Scenario

IPCC 1.5

(low-overshoot)

Various energy scenarios define different paths to meet net-zero targets; however, all of them concur with the need for carbon sequestration solutions

to reduce emissions, and therefore the significant increase of CCUS projects required in the next 30 years.

Between 4% and 20% of CO2 abatement could come from carbon sequestration solutions by 2050

IHS Markit*

Accelerated Carbon

Capture and Storage

(44 MMt/y)

IEA SDS*

Confidential. © 2021 IHS Markit®. All rights reserved.

The number of CCUS operating projects is expected to more than double in

the next 10 years, mainly driven by decarbonization ambitions

North America Europe

Asia Pacific Middle East

Expected operational CCUS

projects between 2021 and 2026

© 2021 IHS Markit

Note: Only includes CCUS large-scale projects.

Source: IHS Markit

Engineered Carbon Removal Workshop | August 2021

10

0

60

120

0

4

8

12

16

Hydrogen production Natural gas procesingPower generation Chemical productionOthers* Total CO2 cumlative capacity

CCUS projects additions by year

* “Others” includes cement and iron production, and water to energy.

** 2027 and 2028 compile the projects that have been announced but do not have a defined project timeline.

Note: Only includes CCUS large-scale projects. Capacity additions between 2021 and 2026 based on company announcements.

Source: IHS Markit © 2021 IHS Markit

Nu

mb

er

of

pro

jects

Cu

mu

lati

ve C

O2

cap

ture

cap

acit

y

(MM

t/y)

North America Europe

Asia Pacific Middle East

Announced CCUS projects

© 2021 IHS Markit

Note: Only includes CCUS large-scale projects.

Source: IHS Markit

Total CO2 cumulative capacity

The CCUS industry will have to grow faster than expected in order to meet expectations from multiple net-zero scenarios.

However, this growth will be highly dependent on policy support.

2

Confidential. © 2021 IHS Markit®. All rights reserved.

BECCS and DAC solutions have a small project pipeline, therefore capacity

increase will be limited in the next five years

Engineered Carbon Removal Workshop | August 2021

11

0

1

2

3

4

5

6

7

8

9

0

1

2

3

4

North America Europe Asia Total CO2 cumlative capacity

Bioenergy with CCUS/CCS projects additions by year

*All project during 2019 were pilots. **2027 compiles the projects that have been announced but do not have a defined project timeline

Note: (1) Projects after 2020 are announced projects, timeline of these projects could change. (2) Projects in 2011 capture CO2 from two different

sources, one of them being bioenergy so only part of the carbon captured is associated to BECCS.

Source: IHS Markit, IEA, NETL CCUS Database, MIT Carbon Capture and Storage Project Database © 2021 IHS Markit

Nu

mb

er

of

pro

jects

Cu

mu

lati

ve C

O2

cap

ture

cap

acit

y (

MM

t/y)

0

2

4

6

8

10

12

14

16

18

20

0

1

2

3

4

5

North America Europe Asia Total CO2 cumlative capacity

DAC projects additions by year

Note: (1)Two projects on 2010 and 2018 from Global Thermostat are not operating. The innovation center from Carbon Engineering is not considered in

this chart. (2) 2024 project is contingent on several factors and timeline of this project could change.

Source: IHS Markit, IEA, company website © 2021 IHS Markit

Nu

mb

er

of

pro

jects

Cu

mu

lati

ve C

O2

cap

ture

cap

acit

y

(th

ou

san

d m

etr

ic t

on

s p

er

year)

Orca project—

4 Kt/y—

Climeworks

Commercial plant

1 MMt/y—Carbon

engineering

Total CO2 cumulative capacity Total CO2 cumulative capacity

Confidential. © 2021 IHS Markit®. All rights reserved.

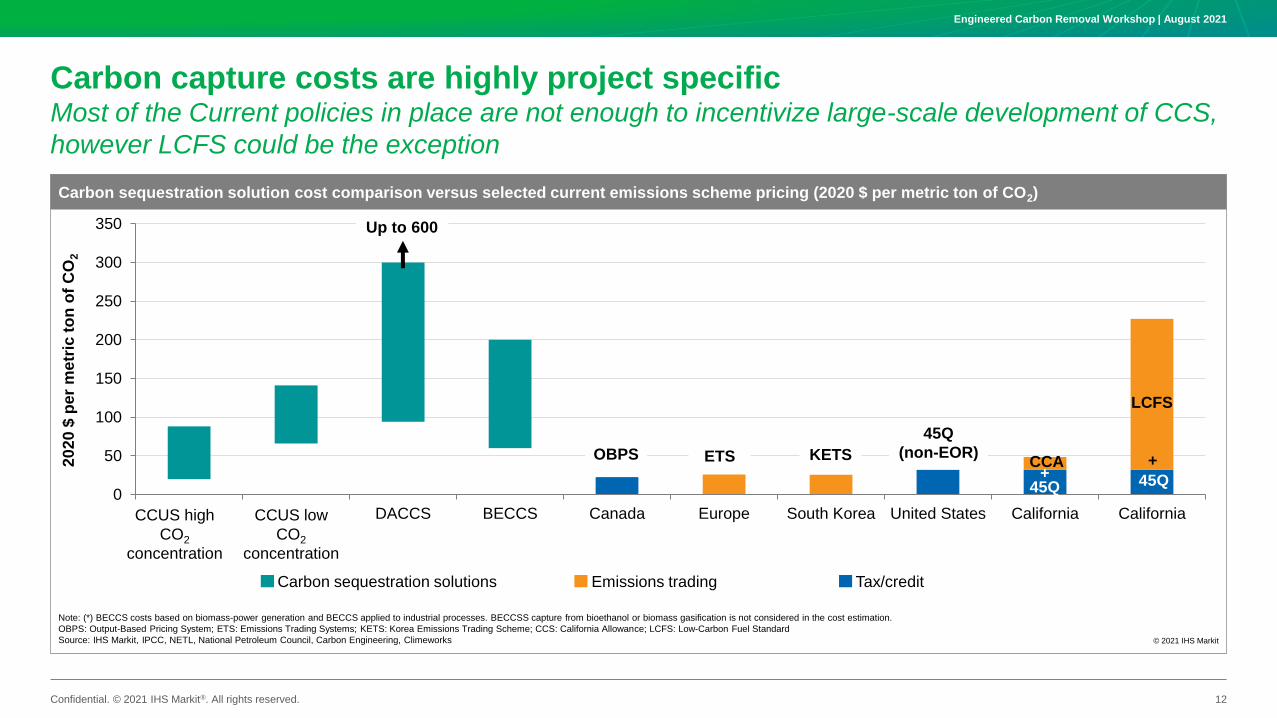

Carbon capture costs are highly project specificMost of the Current policies in place are not enough to incentivize large-scale development of CCS,

however LCFS could be the exception

Engineered Carbon Removal Workshop | August 2021

12

0

50

100

150

200

250

300

350

CCUS highCO2

concentration

CCUS lowCO2

concentration

DACCS BECCS Canada Europe South Korea United States California California

Carbon sequestration solution cost comparison versus selected current emissions scheme pricing (2020 $ per metric ton of CO2)

Note: (*) BECCS costs based on biomass-power generation and BECCS applied to industrial processes. BECCSS capture from bioethanol or biomass gasification is not considered in the cost estimation.

OBPS: Output-Based Pricing System; ETS: Emissions Trading Systems; KETS: Korea Emissions Trading Scheme; CCS: California Allowance; LCFS: Low-Carbon Fuel Standard

Source: IHS Markit, IPCC, NETL, National Petroleum Council, Carbon Engineering, Climeworks © 2021 IHS Markit

20

20

$ p

er

me

tric

to

n o

f C

O2

CCUS high

CO2

concentration

CCUS low

CO2

concentration

Carbon sequestration solutions Emissions trading Tax/credit

OBPS ETS KETS

45Q

(non-EOR)

LCFS

45QCCA

45Q

Up to 600

++

IHS Markit Customer Care

Asia and the Pacific Rim

Japan: +81 3 6262 1887

Asia Pacific: +604 291 3600

Europe, Middle East, and Africa: +44 1344 328 300

Americas: +1 800 447 2273

Disclaimer

The information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any means, without the prior written permission of IHS Markit or any of its affiliates ("IHS Markit") is strictly

prohibited. IHS Markit owns all IHS Markit logos and trade names contained in this presentation that are subject to license. Opinions, statements, estimates, and projections in this presentation (including other media) are solely those of the individual author(s) at the time of

writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or subsequently

becomes inaccurate. IHS Markit makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any inaccuracies or omissions. Without limiting the

foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with any

information provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by IHS Markit should not be understood to be an endorsement of that website or the site's

owners (or their products/services). IHS Markit is not responsible for either the content or output of external websites. Copyright © 2021, IHS Markit®. All rights reserved and all intellectual property rights are retained by IHS Markit.