BUSINESS - bslaboratory.net vol. 3 issue 1-2014.pdf · Mauro Sciarelli. Full Professor of Business...

97

Transcript of BUSINESS - bslaboratory.net vol. 3 issue 1-2014.pdf · Mauro Sciarelli. Full Professor of Business...

BUSINESS SYSTEMS REVIEW ISSN 2280-3866

www.business-systems-review.org

Volume 3, Issue 1 January - June, 2014

JOURNAL SCOPE Business Systems Review (BSR- ISSN 2280-3866) is a peer reviewed, half-yearly journal,

published by the non-profit association Business Systems Laboratory. BSR publishes high level

and innovative theoretic, qualitative, quantitative and empirical contributions of researchers and

practitioners in the business systems field.

The journal aims to endow a multi-field approach with a special emphasis on the systemic

approach for business.

PUBLICATION FREQUENCY Six-monthly, published in June and December plus special issues.

COVERAGE The main topics covered in the journal may include, but not are limited to, the following topic

areas:

The main topics include, but not are limited to, the following topic areas:

• Systemic Approach in Business • Complex Systems Theory • Management Cybernetics •

Economic and Social Systems • Business Communication Systems • Systems Dynamics • Viable

Systems Approach • Innovation Systems • Financial Systems • Service Science • Sustainability •

Corporate Social Responsibility • Knowledge Management • Supply Chain Management •

Strategic Management • Environmental Business • Environmental Management • Marketing •

Consumer Behavior • Customer Satisfaction • Corporate Finance • Banking • Finance for SME •

e-Business • e-Learning • Business Process Management • Fuzzy Logic • Heterodox Economics •

Ethnography.

KEY JOURNAL AUDIENCES Academics, researchers, business consultants, business engineers, computer scientists,

management systemists, online libraries supplying students, academics and researchers.

KEY BENEFITS BSR is an important forum for the exchange of knowledge, addressing major areas of concern

and debate whilst highlighting future developments. The challenging and comprehensive nature

of systems science in business is reflected in the published articles which involve not only

theoretical and methodological-oriented studies but also in-depth discussions of their related

appliances and implementations.

PEER REVIEW The journal adopts a double-blind system for peer-review; both reviewers and authors’ identities

remain anonymous. The paper will be peer-reviewed by three experts: two reviewers from

outside and one associate editor from the journal. Our commitment is to complete the entire

review process within a maximum of three months since the submission. The acceptance rate in

2013 has been of about 25%.

BUSINESS SYSTEMS REVIEW ISSN 2280-3866

www.business-systems-review.org

Volume 3, Issue 1 January - June, 2014

INDEXING AND ABSTRACTING

value 2012: 0.497

value 2012: 5.54

ETHICAL CODE

The Business Systems Review (BSR) aims to choose and publish, through a double blind peer

review process, the highest quality research in business systems. In order to achieve this goal, the

whole peer review and publication process must be scrupulous and fair.

Journal standing depends greatly on the trust of all people involved in the process coming from

their acknowledgment of the fairness of the double blind peer review and publication process.

This trust can be enhanced by the implementation of a formal ethical code, with clear guidelines

for fair behavior. For these reasons, the BSR Ethical Code is intended to be a complete policy for

peer review and publication ethics in the Business Systems Review.

The Code depicts BSR's policies to guarantee the ethical conduct of all participants in the peer

review and publication process. BSR Authors, Editors and Reviewers are encouraged to read

these guidelines and address any questions or concerns to one of the BSR co-Editor in Chief.

For further details about BSR ethical code:

http://www.business-systems-review.org/BSR_ethical_code.htm

BUSINESS SYSTEMS REVIEW ISSN 2280-3866

www.business-systems-review.org

Volume 3, Issue 1 January - June, 2014

AUTHORS’ GUIDELINES

Submission of an article implies that the work described has not been published previously

(except in the form of an abstract or a conference proceeding), that it is not under consideration

for publication elsewhere, that its publication is approved by all authors and that, if accepted, will

not be published elsewhere in the same form, in English or in any other language, without the

consent of the Publisher.

The Editors reserve the right to edit or otherwise alter all contributions, but authors will receive

proofs for approval before publication.

Authors must check their manuscripts for possible violations of copyright law and obtain the

required permissions before submission.

Authors should be punctual with their manuscript revisions. If an Author cannot meet the

deadline given, he should contact the Editor to determine whether a longer time period or

withdrawal from the review process should be chosen.

Authors authorize the publisher to archive the article into databases and indexes, and permit the

publisher to apply DOI to the article.

All manuscripts should be prepared in MS-Word format, and submitted by e-mail to the editor in

chief. For further details please go to:

http://www.business-systems-review.org/BSR_authors_guidelines.htm

BUSINESS SYSTEMS REVIEW ISSN 2280-3866

www.business-systems-review.org

Volume 3, Issue 1 January - June, 2014

EDITOR IN CHIEF

GANDOLFO DOMINICI

e-mail: [email protected]

EDITORIAL ASSISTANT

FEDERICA PALUMBO

e-mail: [email protected]

ASSOCIATE EDITORS

Dimitris Antoniadis. Lecturer in Project Management, University of West London (UK)

Gianpaolo Basile. Senior Lecturer of Marketing, University of Salerno (IT)

Michelle Bonera. Asst. Professor of Marketing, University of Brescia (IT)

Ockie Bosch. Prof. of Systems Design & Complexity Management, University of Adelaide (AU)

Fernando Buendia. Asst. Prof. of Business Administration. EGADE Business School (MX)

Nikhilesh Dholakia. Full Professor of Marketing, University of Rhode Island (US)

Primiano Di Nauta. Asst. Professor of Business Management, Univ. of Foggia (IT)

Nezihe Figen Ersoy. Associate Professor of Marketing, Anadolu University (TR)

Lucio Fuentelsaz. Full Professor of Strategy & Management, University of Zaragoza (ES)

Marco Galvagno. Asst. Professor of Marketing, University of Catania (IT)

Giuseppe Giordano. Associate Professor of Statistics, University of Salerno (IT)

Nastaran Haji Heydari. Asst. Prof. of e-Business, University of Tehran (IR)

José Rodolfo Hernandez Carrìon. Professor of Applied Economics, Univ. of Valencia (ES)

Giulio Maggiore. Asst. Professor of Business Management, Univ. Unitelma Sapienza (IT)

Ignacio Martinez de Lejarza. Professor of Applied Economics, University of Valencia (ES)

Piero Mella. Full Prof. of Business Administration, University of Pavia (IT)

Pierre McDonagh. Full Prof. of Marketing, School of Management, University of Bath (UK)

Mahito Okura. Associate Professor of Risk Manag. & Insurance, Nagasaki University (JP)

Nacima Ourahmoune. Associate Professor of Marketing, Reims Manag. School (FR)

Luca Pazzi. Ass. Professor of Information Systems, Univ. Modena & Reggio Emilia (IT)

Igor Perko. Asst. Prof. of Business Informatics, University of Maribor (SI)

Vincenzo Pisano. Asst. Professor of Business Management, University of Catania (IT)

Enzo Scannella. Asst. Prof. of Banking and Finance, University of Palermo (IT)

John Schouten. Full Professor of Marketing, Aalto University School of Economics (FI)

Mauro Sciarelli. Full Professor of Business Management, University “Federico II” Naples (IT)

Giancarlo Scozzese. Asst. Prof. of Business Management, “Univ. Stranieri”, Perugia (IT)

Josip Stepanić. Ass. Professor of Social Thermodynamics, University of Zagreb (HR)

BUSINESS SYSTEMS REVIEW ISSN 2280-3866

www.business-systems-review.org

Volume 3, Issue 1 January - June, 2014

Eleuterio Vallelado. Professor of Finance, University of Valladolid (ES)

Ivona Vrdoljak Raguž. Associate Professor of Management, University of Dubrovnik (HR)

Maurice Yolles. Emeritus Professor of Organisational Science, Liverpool John Moores

University (UK)

TABLE OF CONTENTS

pp.1-17

José Rodolfo Hernández-Carrión, David B. Ruiz Hall

A NEED FOR A PARADIGM SHIFT IN THE SPANISH BANKING SECTOR? THE

EVOLUTION FROM REGIONAL TO MULTINATIONAL BANKS IN SPAIN.

pp. 18-31

Giancarlo Scozzese, Roberto Bruni.

THE EFFECT OF THE COUNTRY OF ORIGIN OF EUROPEAN COMPANIES IN

THE CONTEXT OF YOUNG ARGENTINIANS.

pp. 32-47

Rosa Lombardi, Simone Manfredi, Fabio Nappo.

THIRD PARTY OWNERSHIP IN THE FIELD OF PROFESSIONAL FOOTBALL: A

CRITICAL PERSPECTIVE.

pp. 48-65 Michal Pružinský, Bohuslava Mihalčová.

FINANCIAL LITERACY OF SLOVAK UNIVERSITIES’ STUDENTS.

pp. 66-89

Luca Carrubbo, Roberto Bruni, Emanuela Antonucci.

ANALYZING PLACE BOUNDARIES USING THE SERVICE SCIENCE

PARADIGM

www.business-systems-review.org

Business Systems Review

ISSN: 2280-3866 Volume 3, Issue 1

January-June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

1

A Need for a Paradigm Shift in the Spanish

Banking Sector? The Evolution from

Regional to Multinational Banks in Spain

José Rodolfo Hernández-Carrión

Associate Professor of Applied Economics. Faculty of Economics, University of Valencia, Spain.

e-mail: [email protected]. Corresponding author

David B. Ruiz Hall

Attorney-at-Law

GB Consultants, Finance, Tax & Legal, GDF Consultants, Valencia, Spain.

Submitted: May 30, 2013 / Accepted: February 20, 2014 / Published online: February 22, 2014.

DOI: 10.7350/BSR.D01.2014 – URL: http://dx.medra.org/10.7350/BSR.D01.2014

ABSTRACT

Since the approval of Spain’s 2012 National Budget on March 30, 2012, some doubts and

controversies have added up to many fears in the private sector regarding the measures and

stimuli that the Spanish government was going to undertake. At the same time, this situation was

in some measure aggravated by the financial backlog of many small and medium companies,

which are and will continue, in the following years to be completely unable to comply with their

financial requirements.

In line with Boronat Ombuena’s (2009a, 2009b, 2010, 2012) requirements in his new approach

to finance and private sector liaisons, the purpose of this paper is to analyze the recent years of

the credit sector in Spain as well as its direct and mid-term effects that its mergers and

acquisitions (M&A) have contributed up to date, and will still produce in the near future. We will

take a closer look at the evolution of the banking sector in Spain from 1995 to 2012 through a

historically-based methodology, compiling and synthesizing the existing financial and risk

market information and analyzing its evolution.

We shall observe that in a single year, the total number of savings banks in Spain decreased from

45 to only 15 entities and that the risks the financial system took over these last few years were

not equally distributed across the entities, resulting in an advanced foreclosure of the regional

savings banks and in a market-share growth for the commercial banking entities.

This process has resulted in creating larger entities and, in some cases, a vacuum of regional and

local credit entities that in the mid-long term will eventually end up in a representative loss on

credit availability. These circumstances call into question the need for a paradigm change and

most importantly, new approaches to solve the new challenges that can result in the financial

fluidity of the system and the eventual recovery of the economic structure.

Keywords: Spanish banking sector, savings banks, financial crisis, tax adjustments convergence,

mergers and acquisitions, M&A, Spain.

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

2

1. INTRODUCTION: THE CREDIT SYSTEM EVOLUTION IN SPAIN

The early years of this decade have become a challenge for the already-used economic models

and the common uses of the financial markets. We have been able to see old market strategies fail

and old banking procedures be completely inadequate for the ever-changing needs of the new

paradigm and requirements of the private business sector. However, these challenges are the

result of changes that have been taking place from late 1995.

Since the end of the last decade, Spain has slowly been changing its economic model, specifically

modifying the banking procedures and credit requirements of core capital in order to restructure

its own market, industries and budgetary assignments as a whole.

Whereas in other countries such changes had been undertaken many years in advance, we could

still see big financial players in the Spanish banking system which had other legal strategies that

seem to be unknown to other countries. We talk about significantly different legal structures and

different credit-concerning procedures.

In Spain, since the late eighteenth century, the earlier Italian model of the fifteenth century of the

impounding houses of pious character started to grow (although history would take us back to the

year 1834, to the Spanish town of Jerez de la Frontera (Cadiz, Spain), with the “Sacred and royal

impounding house of the souls of the purgatory of Madrid”). Later on, after more than a century

of existence, such structures started to evolve in the mid-nineteenth century to the actual German

Sparkasse-model-like based entities, that is, a public banking system working as banks with local

and regional interests and centred in a non-profit and regional compromised entities with large

reinvestment and public service programs.

Nevertheless, such models started to modify their original commitment, which was only to lend

small loans for specific personal purposes, not competing with larger and more professionalized

banks for the business market and commercial loans to the large private sector investment groups.

These entities were nominated Savings Banks (Savings Bank or Caja, in Spanish, or Caixa, in

Catalan language equivalent) and were specialized in accepting savings deposits and granting

loans.

These changes ended up in the opening of their own regional enclosed interests in favour of a

nationwide expansion that started mainly after 1992 with three entities ahead of the rest, the

Madrid-based Caja Madrid, the Barcelona-based Caixa Catalunya and the Leon-based Caja

Castilla-León, among many others that we shall later expose and analyse. The nation-wide

assault began with the creation of hundreds of micro-offices in every corner of large and later

medium-sized cities. This expansion model wanted to export the regional and proximity-based

model of the original entities while giving them a larger impact in the economy as a whole.

On the other side of the spectrum we could find a more-efficient and more professionalized

banking system which entities were growing or had been restructuring themselves for more than

a decade, creating large banking conglomerates that we know of today, such as the BBVA (Banco

de Bilbao Vizcaya Argentaria) (the merging result of the historical banks in Spain such as the

Bank of Bilbao, Bank of Vizcaya, and also the Argentaria Group, which itself was the nationwide

group of the industrial investment state banks such as the Bank of External Commerce -BEX-,

Bank of local Credit -BC- and many others, also we found the best known BSCH (Banco de

Santander Central Hispano), as well as the natural evolution from the following three private

entities: Bank of Santander, Central Bank, and Hispano Bank. This “Central Bank” or “Banco

Central” was a private entity with this name, a small commercial bank significantly different

from the important concept associated with the Central Bank of a country, and in the case of

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

3

Spain it is officially named Banco de España or Central Bank of Spain (BDE). In the new context

of the European Union, the role of the central bank of the Spanish economy has changed

significantly in the last years (Jaime & Hernández-Carrión, 2012).

The end result of this evolution has been that in almost fifteen years, by the beginning of the

twentieth century, the banking map in Spain had been completely overhauled. There was no real

difference in products or goals between savings and commercial banks and by then, the credit

mass had grown to a spectacular rate, nearly one hundred thousand new employees had been

hired in new offices in all Spain (adding also the new foreign banks that opened in the expansion

period), resulting in an office or ATM machine in every corner of every city or town.

2. CHRONOLOGICAL EVOLUTION FOR THE 1995-2012 PERIOD

In the early years of the twentieth century, very few mergers had taken place of any strategic

importance at the national or regional level. We could only start to see small mergers and small

acquisitions by other entities, however, except for the Cajamar conglomerate, there was no entity

big enough to modify the credit access or fluency in any region by itself. This would later change

in regions like the Valencian Community, which, as the foremost example of the national

intervention and bank nationalisation, would eventually lose the three larger credit institutions in

its soil, the Bank of Valencia, the CAM (Savings bank from Alicante and Murcia, previously

known as Caja de Ahorros de Alicante y Murcia) and Bancaja (former Savings bank from the

provinces of Valencia region, or Caja de Ahorros de Valencia, Castellón y Alicante).

However, if we continue to analyse this evolution, we can clearly see that after 2009, large

conglomerates were created, ending in the actual chain of events.

We shall not endeavour in analysing the internal pros, cons or even wrongdoings in every-single

entity, however, in recent studies (Climent Serrano, 2012), there has been a reasonable consensus

that there have been many causes that have led to the actual financial crisis.Firstly, those of

internal origin:

i. Capacity excess

ii. Non-levered housing investment

iii. Excessive and disproportionate growth

iv. Large levered operations based on non-profitable operations

v. Doubtful credits ending in excessive depreciations and amortizations affecting the banking

system cash flow.

vi. Benefit depletion ending in insolvency situations.

Furthermore, there have also been external causes to all this change and late developments, such

as:

i. Negative GDP evolution of the EU countries in general and Spain in particular.

ii. Unemployment rate well above the 20% figure during the process, continuously readjusting

the demand to a lower local optimum giving the industrial offer curve little to no time to

readjust its means, prices or qualities, ending suddenly in many cases in a structural excess

in production.

iii. State value inversion demise

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

4

iv. Regulation system modification that subsequently changed most of the financial variables

in the model.

Following 2009, several mergers started to really take place and change the regional and national

financial landscape, regional savings banks started either to purchase banks due to the legal

framework then in place. It was impossible to do it the other way round, since savings banks had

no legal core or legal force and therefore were outside the mercantile legislation -due to their

particular history- whereas banks were -and still are- specialized companies that function in the

financial market.

Figure 1. Chronological Evolution of the M&A operations in the Spanish banking system (First

stage from 1995 to 2009)

2.1 Spanish banking and financial system evolution in 2009

03.29.2009 - CCM (Caja Castilla La Mancha) is shut down and intervened after the merger with

the Andalusian Unicaja savings bank.

05.26.2009 - The then Spanish President, Mr. Rodriguez Zapatero (of the Socialist Party PSOE),

starts the Fund for Orderly Bank Restructuring FROB or Fondo de Reestructuración Ordenada

Chronological Evolution

Cajasur - (Caja de Ahorros and Monte de Piedad de Córdoba)

CaixaNova - (Caja de Ahorros de Ourense, Vigo and Pontevedra)

CajaNavarra - (Caja de Ahorros de Navarra and Caja de Ahorros Municipal de Pamplona)

Nueva Caja Rural Almería y Málaga - (Cajas Rurales de Almería and Málaga )

Caja de Ahorros de Carlet integrates into Bancaja

Multicaja - (Cajas Rurales de Huesca y Zaragoza )

Cajasol - (Caja de Ahorros de Huelva y Sevilla and la C.A Provincial San Fernando de Sevilla y Jerez)

Caja Rioja - (Caja de Ahorros Inmaculada and la Caja insular de Ahorros de Canarias) - FAIL

Caja Castilla la Mancha integrates into Cajastur

Grupo Cooperativo Cajamar - (Cajamar Caja Rural, Caja Campo and Caja Rural de Casinos)

1995

1999

2000

2001

2002

2007

2009

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

5

Bancaria) which aims to manage the restructuring and resolution of credit institutions and

strengthen the resources of these in the integration processes.

These reforms invested 7,550 million Euros through the FROB, although total recapitalization of

entities was 13,389 million Euros, compared to 15,152 million Euros initially planned.

This process was done via the legal framework provided by the Royal Decree-law 9/2009 (RD

Law 9/2009 or Law Fund for Orderly Bank Restructuring), and Royal Decree Law 11/2010

(Banks Act) and Royal Decree Law 2/2011 (Act Recapitalization).

13.08.2009 - The Bank of Andalusia (Banco de Andalucía) delisted in the Spanish stock market,

after successfully culminating the merger of the subsidiary Andalusian by the Banco Popular.

03.11.2009 - The Bank of Spain (Central Bank of the country, officially nominated Banco de

España belonging to the Governing Council of the European Central Bank or ECB) approved the

integration of CCM in Cajastur.

12.11.2009 - The Bank of Spain authorized the establishment of Cajamar Cooperative Group

(Cajamar, Caja Rural, Caja Campo and Caja Rural de Casinos) as the first merger under the SIP

formula made in Spain.

2.2 Spanish banking and financial system evolution in 2010

03.25.2010 - Unnim savings bank receives aid from FROB passing to be in full control.

05.11.2010 - The Andalusian savings banks Unicaja and Caja de Jaen constitute a new entity

after the signing of the merger deed.

05.22.2010 - Cajasur is then intervened after the merger with Unicaja is rejected and asks for help

for an amount over 500 million Euros to FROB.

07.01.2010 - The two major mergers of Catalan banks, Catalunya Caixa (Caixa Catalunya,

Tarragona and Manresa) and Unnim (integrated by the savings banks from Manlleu, Sabadell and

Terrassa) started their operational activity.

The governing councils of Caixa Rural Cajamar and Balearic Caixa agree to merge.

07.16.2010 - Cajasur is awarded to the Basque savings bank BBK (Bilbao Bizkaia Kutxa).

09.18.2010 - Shareholders' meetings of Banco Sabadell and Banco Guipuzcoano agree their

integration in the first merger of any kind of Spanish banking for more than a decade. Banco

Sabadell acquires Banco Guipuzcoano.

09.21.2010 - CCM savings bank becomes a commercial Bank (participated by 75% by the

Cajastur Group and by 25% by the CCM Foundation).

01.10.2010 - Caja España Duero savings bank, as a result of Caja Duero and Caja España,

officially merge.

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

6

04.10.2010 - The National Competition Commission approved the merger of Caja Guadalajara

by Cajasol, which supposed the first interregional integration of savings banks in Spain.

12.01.2010 - Novacaixagalicia, the resulting savings bank from the merger of Caixa Galicia and

Caixanova started operating after its registration in the commercial register and became a bank

by September 14, 2011. Novacaixagalicia was operated by 93% by the FROB and is pending

auction or tender for adjudication. It has received aid worth of 2,465 million euros.

12.20.2010 - The presidents of Cajamar and Caixa de Balears formalise Rural notarized the deed

of merger of both entities.

12.22.2010 - Grupo Banco Mare Nostrum (the resulting integration of Caja Murcia, Caja

Granada, Sa Nostra, Caixa Penedès and a SIP) obtains commercial banking operations

authorisation.

2.3 Spanish banking and financial system evolution in 2011

01.01.2011 - La Caixa savings bank completes the merger of Caixa Girona.

01.01.2011 – The year 2011 marks the beginning of operations of the new group of Finance and

Savings Bank called Bankia. The SIP of Caja Madrid, Bancaja, Caixa Laietana, Caja de Avila,

Caja Insular de Canarias, Caja Segovia and Caja Rioja, whose new trademark is Bankia.

01.03.2011 - BBK Bank starts operating and trading.

01.26.2011 - Banca Civica (the SIP of Caja Navarra, Caja Canarias, Caja Burgos and Cajasol)

starts with operational capacity to handle new customers.

04.06.2011 - Banco Base savings bank (cold fusion provided between the Mediterranean-CAM

savings bank, Cajastur and other savings banks from Extremadura and Cantabria) settled their

project, while acquiring the CAM bank tab, finally intervened on 22 July of the same year.

06.29.2011 - Cajastur, CCM Bank, Caja Extremadura and Caja Cantabria assemblies approve the

transfer of financial assets to the new bank (subsequently called Liberbank), created under the

SIP formula.

07.22.2011 - Mediterranean Savings Bank (CAM) is intervened after failing integration with

Cajastur, Caja Cantabria and Caja Extremadura in the Bank Base. The Alicante-based bank was

forced to ask 2,800 million euros to the FROB. The Bank of Spain now has a credit line of EUR

3,000 million for its feasibility and was capitalized with 2,800 million euros, so that the state

controls between 80 and 85% of its capital.

09.30.2011 - CatalunyaCaixa passes to the FROB which now controls 90% of its capital in the

state after injecting 1,719 million Euros.

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

7

07.10.2011 - Banco Popular communicates to the National Securities Market Value Commission

(CNMV) its claim to control all of the Banco Pastor through a process of absorption.

20.10.2011 - General meetings of the three Basque savings banks, BBK, Vital Kutxa and approve

their integration to create Kutxabank bank, which will begin operating on January 2, 2012.

11.21.2011 Bank of SpainintervenesBanco de Valencia after the forced resignation of its

operators and injects 1.000 million Euros through FROB to ensure its viability and 2.000 million

to ensure its liquidity.

11.23.2011 - The Caja3 savings bank reports to the CNMV the segregation of business of Caja

Inmaculada (CAI), Caja Círculo de Burgos and Caja Badajoz for their organization.

12.07.2011 - The Bank of Spain informs that the Mediterranean Savings Bank (CAM) has been

bought in an open public auction by Banco Sabadell.

2.4 Spanish banking and financial system evolution in 2012

02.03.2012 - The new president in office, Mr. Mariano Rajoy, from the Conservative Party

(Partido Popular or PP), holds his first reform with the approval of the Royal Decree Law for the

reorganization of the financial system, which required financial institutions to increase by 50,000

million Euros its provisions in order to withstand the complete risk of their real estate assets and

pushing some of the already existing entities to new mergers and acquisitions.

02.29.2012 - The Ibercaja savings bank and Caja3 boards agree to initiate the process of merging

in their banking business.

07.03.2012 - The Bank of Spain decrees that Unnim (merger of Caixa Sabadell, Terrassa and

Manlleu) is won by open public auction by the BBVA (Banco de Bilbao Vizcaya Argentaria) for

one euro and helps Deposit Guarantee Fund in the amount of 953 million euros.

03.30.2012 - The boards of Unicaja and Caja España-Duero (CEISS) approve the integration

and complete absorbing process of the Andalusian entity (Unicaja) by the Castile and Leon

region savings bank.

04.18.2012 - The boards of Caixabank and Banca Civica (Caja Navarra, Caja Canarias, Caja

Burgos and Cajasol) approved their proposed merger.

05.09.2012 - The Minister of Economy and Competitiveness, Luis de Guindos (PP), announces

the nationalization of 100% of Financial and Savings Bank, the Bankia bank matrix, which will

be controlled by 45% of the latter company. Bankia, by this time, becomes the biggest former

savings bank intervention carried to date.A key figure in this development is the formerPresident

of Bankia, Rodrigo Rato. Rato was Minister of the Economy in Spain from 1996 to 2004,

Managing Director of the International Monetary Fund (IMF) from 2004 to 2007, who assumed

the presidency of the main savings bank in the Bankia merger (Caja Madrid), and resigned on

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

8

May 7, 2012. By July 4th, 2012, Rato had been charged with accounting irregularities, along

with thirty other former members of the board of directors of Bankia.

05.11.2012 - The then new Spanish government takes another step in this restructuring of banks

with a new Royal Decree Law on the reorganization and sale of real estate assets in the financial

sector, with the aim of cleaning up and protecting the balance sheets of banks to promote new

risk-taking operations.

This new reform also includes the creation of "bad banks" in order to group toxic assets and to

require higher provisions for entities to ensure their viability.

It also raises the general provision of the loan portfolio and real estate assets of the banking

unproblematic (123,000 million Euros), which will mean around 30,000 million Euros of new

banknotes that will have to be made before December 31 of that year.

These write downs join the 54,000 million Euros and made after the approval of Royal Decree

Law February financial reform, so that the total sanitation made will be placed near the 84,000

million Euros.

05.29.2012 - The Ibercaja savings bank, Caja3 savings bank and Liberbank boards, approve the

protocol integration to create the seventh largest Spanish financial group.

06.08.2012 - The Spanish government announced a third round of write downs pending to be

analysed about the sector.

07.10.2012 - The Mediterranean savings Bank-CAM is merged with Sabadell bank and

disappears after 137 years of existence. Banco Sabadell acquires Banco CAM.

11.27.2012 - Caixabank purchases Banco de Valencia from the former Bankia Group.

As shown in the timelines, the end result of all these years of changing models could not have

been more catastrophic, the fourth largest financial entity nationalized (Bankia, only behind

BSCH, BBVA and La Caixa savings bank), the foreclosure of the savings banks social system in

favour of a solely commercial banking system. In other words, the model that had taken more

than two centuries to build, took less than a decade and a half to ground it.

After the merger, Bankia was initially owned by a holding company named Banco Financiero y

de Ahorros (BFA), and the seven banks controlled BFA. The most toxic assets from the banks

were transferred to this new bank BFA, which obtained 4.5 billion euros from the Spanish

government rescue fund FROB in exchange for preference shares, so the resulting new entity is

now BFA-Bankia.

A large amount of literature has been published only acknowledging the abovementioned causes

(Caja Meri et al., 2008; Pérez 2011; Pons 2011) for example have contributed in several

fundamental analyses of the matter at hand),of this financial development, yet, as we will see in

our paper, this has not only been the sole reason, but, among many others, show the lack of

general knowledge that general public had of the financial market in Spain.

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

9

Figure 2. Chronological Evolution of the M&A operations in the Spanish banking system

(Second stage from 2010 to 2012).

3. THE RISK UNDERTAKEN IN SOME FINANCIAL AND REAL ESTATE ASSETS

AND THEIR BANKING EFFECTS IN SPAIN IN 2008-2011

Although many circumstances and factors (both internal and external), can be related to the actual

evolution of the banking system in Spain, one that is sometimes forgotten or set aside is the

amount of risk that mostly savings banks, contrary to their own financial model and contrary to

their own business procedure (in most cases as a consequence from their regional-political

control and supervision) ended up by absorbing operations that after some time resulted in total

investment failure and a severe and long-term harmful effect on their equity.

If we were to analyse the total assets of each bank (that we shall represent by the size of the

circle) and measure the TIER 1 mass on the Y axis, while at the same time, on the Xaxis we

could in contrast measure the doubtful risks ratios and rankings back in 2008, this was the

graph1 the Spanish financial sector was representing:

Chronological EvolutionCaja España de Inversiones, Salamanca y Soria - (Caja España and Caja Duero )

Banca Cívica - (Caja Navarra, Caja Canarias and Caja de Burgos)

CajaSol - (Merges with Caja Guadalajara )

Unicaja - (Marges with Caja de Jaén )

Catalunya Caixa - (Cajas Rurales de Cataluña, Manresa and Tarragona )

Caja España Duero - (Caja España and Caja Duero)

Caja3 - (Caja Inmaculada, Caja Círculo y Caja Badajoz)

NovaCaixaGalicia - (Caixanova and Caixa Galicia)

Unnim - (Cajas Rurales de Sabadell, Terrasa and Manlleu )

Fusion between Cajasur and Unicaja - (BE takes over Cajasur ) - FAIL

La Caixa absorbs Caja Girona

Bankia – (Caja Madrid, Bancaja, Caja Laietana, Caja Canaria, Caja Segovia y Caja Rioja)

Sabadell-CAM – (Banco Sabadell absorbs Caja de Ahorros del Mediterráneo CAM)

Banco Mare Nostrum – (Caja Murcia, Caja Penedés, Sa Nostra, Caja Granada)

Liberbank – (Cajastur, Caja Castilla La Mancha, Caja Cantabria, Caja Extremadura)

Kutxabank – (BBK, Cajasur, Kutxa, Banco Vital)

Bankia is nationalized

La Caixa is fused with Banca CívicaLiberbank is fused with Caja3

2010

2011

2012

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

10

Figure 3. Tier 1 Ratio of the Spanish Banking Sector in 2008.

In this case, we can clearly see that minor (small to mid-sized financial players such as CCM,

Caixa Catalunya or Caja Madrid) were taking a larger-than average risk on their daily

operations, were as by their TIER 1 ratio (established2 as the core measure of a bank's financial

strength from a regulator's point of view and composed of equity capital and published reserves

from post-tax retained earnings) they were not extremely more funded than other entities nor

were their assets larger than others with the same investment and doubtful risk operations

amount.

From 2008 and by 2009 we were observing a tendency not to reduce risk, but to stretch further on

more risky operations by compensating on the core capital values. (Y axis Tier 1; X axis,

doubtful and risk operations).

Figure 4. Tier 1 Ratio of the Spanish Banking Sector in 2009 with CCM.

0

5

10

15

20

25

0,00 2,00 4,00 6,00 8,00 10,00 12,00 14,00 16,00 18,00

Co

re T

ier

1

Doubtful Risk Ratio

CCM

Banco March

Caja MadridBBK

Caixa CatalunyaBankinter

BBVA

Santander

Banco Sabadell

Banco Popular

Caja España

Caja Penedés

Banesto

Ibercaja

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

11

Then again, in 2009, CCM statistically shows a far larger Doubtful Risk Ratio, and therefore, we

had to recreate the graph without CCM, the result is shown below:

Figure 5. Tier 1 Ratio of the Spanish Banking Sector in 2009 without CCM.

By 2010 (below) with many M&A operations already undertaken, the overall risk was slightly

reduced, although we could clearly see that two entities, Caja España-Duero and CAM were out

of the scale in risk terms.

Figure 6. Tier 1 Ratio of the Spanish Banking Sector in 2010.

Also, by this time, we could see some market trends, such as the smaller risk tendencies by some

major operators, such as BSCH or even by smaller ones (in comparison) such as BBK and Banca

March (or Banco March). By this time, we can also clearly see the next to be out of trend as

Banco de Valencia and Cajasol.

0

5

10

15

20

25

0,00 1,00 2,00 3,00 4,00 5,00 6,00 7,00

Co

re T

ier 1

Doubtful Risk Ratio

Banco March

Caja MadridBBK

Caixa CatalunyaBankinter

BBVASantander

Banco Sabadell

Banco Popular

Caja EspañaCaja Penedés

La Caixa

IbercajaBanco Valencia

Bancaja

Caixa Sabadell

Caja Murcia

0

5

10

15

20

25

30

0,00 2,00 4,00 6,00 8,00 10,00 12,00

Co

re T

ier 1

Doubtful Risk Ratio

Caja España- DueroCAM

Caja Sol

Banco Valencia

BBK Banco March

Bankinter Caja España- DueroCAM

Caja Sol

Banco Valencia

BBK Banco March

Bankinter

BBVA

SantanderCCM

Ibercaja

La Caixa

Banco Sabadell y Guipuzcoano

Banco PopularCaixa Galicia

Caixa CatalunyaCaja Madrid

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

12

In 2011, the market is completely polarised as we can see in the graph below (Y axis Tier 1, X

axis, doubtful and risk operations):

Figure 7. Tier 1 Ratio of the Spanish Banking Sector in 2011 with CAM.

However, the then CAM and Banca March inclusion in the graph distorts the analysis of the

group, in which case we opted to eliminate such entity, resulting as follows:

Figure 8. Tier 1 Ratio of the Spanish Banking Sector in 2011 without CAM.

Finally, in not more than three years, we can clearly conclude that the risk that had already been

taken by 2008 by several entities (specially the then existing savings banks), was one of the clear

and main reasons for the latter demise. Also, this explicitly means that all M&A processes taken

in the 2008-2011 period were utterly insufficient for the reduction to significant levels of all the

risk in the system and, therefore, were only prolonging the problem and were not the solution of

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

0 5 10 15 20 25

Co

re T

ier

1

Doubful Risk Ratio

Banco March

CAMUnimm

Santander

Banco Popular

BBVA

BankinterIbercaja

Bankia

Caja 3 Catalunya Caixa

Banca Cívica

Banco ValenciaNovacaixa Galicia

La Caixa

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

0 1 2 3 4 5 6 7 8 9 10

Core

Tie

r 1

Doubtful Risk Ratio

Banco March

Kutxa Bank

UnimmCatalunya Caixa

Banca CívicaBankia

Caja 3

Novacaixa GaliciaBanco Valencia

Caixa Pollença

SantanderBanesto

Banco Popular

Caixa OntinyentIbercaja

Grupo BBK Bank Cajasur

UnicajaLa Caixa

BBVA

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

13

all the financial problems that the new commercial model used by mostly old and insufficiently

regulated savings banks had approached and developed.

4. MERGERS AND ACQUISITIONS (M&A) PROCESSES AND OLIVER-

WYMAN’S REPORT ON SPANISH BANK’S ASSETS

By September 20123, Olive-Wyman’s report, on request of the EU Council to the Government of

Spain, was published.The report contained Oliver Wyman’s conclusions from the bottom-up

stress testing analysis undertaken for the Recapitalization and Re-structuring of the Banking

Sector of the Banco de España and the Ministerio de Economía y Competitividad. The objective

of this work was to assess the resilience of the Spanish banking system and its ability to

withstand a severe adverse stress of deteriorating macroeconomic and market conditions, and to

estimate the capital that each individual bank would require in the event of such an adverse

scenario.

Such report was based around the top-down stress-testing exercise conducted in June 2012, in

which the bottom-up analysis covered fourteen banking groups representing approximately 90%

of the total domestic credit of the Spanish financial system. The scope of asset coverage also

remained in the report the same as in the top down exercise and included the domestic lending

books, excluding other assets, such as foreign assets, fixed income and equity portfolios and

sovereign borrowing.

The base and adverse macroeconomic scenarios were also maintained as specified by the

Strategic Coordination Committee, with an adverse case implying a 6.5% cumulative GDP drop,

unemployment reaching 27.2% and additional drops in house and land price indices of 25% and

60% respectively, for the 3 year period from 2012 to 2014. Therefore, it presented a base

macroeconomic situation (considered likely) and another extremely adverse (considered very

unlikely), both defined for 2012-2014 period.

These capital requirements were justified by the relationship between the loss-absorbency and the

actual institutions’ total losses. These were expressed in terms of the weighty assets by degree of

risk owned by each entity.

Having said that, the additional capital requirements of the Spanish banking system, of December

31, 2011, according to the report amounted to 59,300 million Euros when the integration

processes ongoing and deferred tax assets weren’t included. If they were to be considered, this

figure drops to 53,745 million given the ongoing M&A operations tax modifications.

While the Oliver-Wyman’s report does mention the end result of the M&A operations as stated, it

didn’t analyse the background of all of them4. Since they have been part of the problem, the

solution or both, we consider it to be of the utmost importance not only to analyse all of the most

important ones, but also to synthesize the final results and effects of all of them.

5. CONCLUSIONS

The private sector credit availability and state tax demand have changed abruptly in these last few

years, and to date, signs of an internal crisis have been constantly appearing, both in Spain and in

the Valencian Community. The credit in Spain as a whole is following a trend of sharp correction

contractions due to the sum of two factors. First, due to exogenous factors, such as restricting

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

14

international liquidity resulting from the international crisis, which are affecting the uptake of

external resources. Second, by endogenous factors, resulting from the contraction of the domestic

market (such as tax increases) and strong positions of financial institutions in the construction

and domestic sectors. This turn of events of the last few years has resulted in a downturn, with

negative values which minimum reached in October 2010, with a variation of -3.8%, the credit

liquidity in the system.

If we look closely at the financial credit availability and absorption in the marketin the 2008-2011

period, credit cooperatives are the only type of entity with positive values, all being stable at

around 1%, while banks had shown negative values until the summer of 2010, with variation

which evolves positively, reaching the value of 4.86% in December 2010. Finally, due to the

heavier credit crunch, the savings banks have negative credit values through the period ranging

from -0.71% to -3.78%.

Also in the same period, we are able to appreciate the great variation in the granted credit by

savings banks, from those that had higher positive values in the first half of 2008, to become

those with a higher decline in credit in the second half of 2010 (38.545 million Euros compared

to -29.769 million Euros). With regard to banks, the values recovery has seen positive values in

2010 after the fall semester of the variation in credit suffered in 2009. Finally, the credit

cooperatives have shown its stable and positive trend in the three years, but with absolute values

much lower than the banks and savings banks.

Therefore, we must conclude that all financial institutions have reduced their new credit

concession, they have closed all financial means to the SMEs, and have only been there for

precise refinancing procedures. However, those with only restructuring-debt operation and never

implying the most urgent requirements, were to sustain and develop the industry by lending more

financial aid, injected via the EU as financial loans to the Spanish banking sector, and through the

forced restructuring of several failed entities.

Such changes and market evolutions have collided with the persistent crisis that has hit southern

Europe and most noticeably, Spain. Also, within Spain, many regions have had severe cuts in

their public spending against all Keynesian models, yet, the Valencian Community has endured

even more changes and cuts than other regions not only in Spain but also in Europe.

These changes have been the cause of the actual financial crisis, internal and external to the

system, especially important, have been the changes made in several tax structures and in the

revenue-making-process for some industrial sectors.They have had a direct effect on the change

in paradigm (adaptation of Jánossy’s 1971 H. model), while existing for the last fifty years, has

been in extensive and intensive use for the past decade.

To this extent, during 2012, the Ibex 35 index lost almost five per cent of its value (-4.7%), a far

lower evolution than the DJ Stoxx Banks (+23.1%) or the DJ Stoxx 50 (+8.8%). While the real

economy is failing to grow, the new born Asset Management Company from the Bank

Restructuring (henceforth, SAREB), a private company established under Law 9/2012 of 14

November as part of the process of restructuring and consolidation of the Spanish financial

system, is attempting to maximize the value of assets that the restructuring of the banking

systems has left out as dubious and high-risk. This new company has its capital provided by

private entities (55%) and by the Fund for Orderly Bank Restructuring (FROB) as a minority

(45%). Its sole purpose to hold and manage directly or indirectly the administration, acquisition

and disposal of assets to be transferred to the banks, established by the Royal Decree-Law

24/2012, of 31st August, to restructure banks, that are majority owned by the FROB or deemed

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

15

by the Bank of Spain to require the opening of a restructuring or resolution of under Law 9/2012.

The decision by the Bank of Spain is taken after independent assessment of capital needs and

asset quality of the Spanish financial system, conducted under the Memorandum of

understanding signed between Spanish and European authorities on July 20, 2012. The first case

included BFA-Bankia, Catalunya Bank, Banco Gallego Novagalicia Bank and Banco de

Valencia, and the second case, consisted of BMN, Liberbank, Caja3 and CEISS.

Further exacerbating this macroeconomic and financial breakdown resulting in the present system

credit-crunch, the two main sectors that thrive in the Valencian Community, the industrial sector

and the tourist sector, specially this latter one, have been losing their main strengths. They have

increased their weaknesses due to new countries offering large competitive leisure and tourist

packages with an even more competitive currency.

On the international level, stock markets around the world prepare for one of the best quarters of

the past 40 years within the Q2 of 2013, with those of the U.S., UK and Japan in the lead,

specially, regarding equity improvement in various emerging markets and in the U.S. However,

the local capabilities of the SME’s growth factor in the Valencian Community are still limited to

credit access and availability.

Although in the future we shall be able to quantify the financial constraints that end up affecting

the Valencian Community, we are already able to see that the deep economic crisis in which we

find ourselves has resulted in a worrying situation for the increasing loss of homes for many

families who are in serious difficulties in meeting their obligations to return the debt incurred by

the purchase of their home. And yet, this is just the tip of the iceberg, as currently there are about

500,000 million Euros of mortgage bonds in Spain as well as Spanish mortgage securitization

funds distributed worldwide. Notwithstanding, many of these titles serve as collateral in the

Eurosystem lending operations to our financial institutions, which has become the key funding

instrument.

Therefore, what will happen to the regulation affecting the warranty (mortgages) of those

securities issued could result in a loss of attractiveness of these values and, consequently, a

further obstacle to the development of not only the Spanish mortgage market, and subsequently,

reducing the chances of restructuring the financial banks and their debts and liabilities.

This risk does not only revolve around the already existing situation, it also implies that any

future growth is compromised by other variables, where the mortgage risk is increasingly high

and the defaults could increase significantly in the coming months, since any change in the

mortgage laws should also consider the effects of that risk. The mortgage default in the third

quarter of 2012 was around the 3.4%, well below the general rate of the banking debtor’s rate of

11.38%, but it is expected that this percentage will rise as unemployment, according to recent

studies, will not diminish at least until 2014.

Finally, we must conclude that the risks that the financial system has taken over these last few

years were not equally distributed across the entities, resulting in an advanced foreclosure of the

regional savings banks and in a market-share growth for the commercial banking entities. This

process has resulted in creating larger entities and in some cases, exponentially, such as in the

Valencian Community. Moreover, this has created a vacuum of regional and local credit entities

that in the mid- to long-term will eventually end up in a representative loss on credit availability.

When added up with the private and domestic sectors, furthermore increased by the

unemployment rate and the regional and country government indebtedness over these last few

years, this regional situation reflects the needfor a paradigm shift and most importantly, new

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

16

approaches that can result, both nationally and regionally, in the fluidity of the financial system

and the eventual recovery of the economy.

REFERENCES

Bilbao-Vizcaya-Argentaria Bank Research (2012). Valencian Community situation. Madrid:

Studies service BBVA.

Boronat Ombuena, G. J. (2009a). The relationships between the banking system and the private

sector: A new approach I. Estrategia Financiera, 265 (October): 44–57. Madrid: Wolkers-

Kluwer.

Boronat Ombuena, G. J. (2009b). The relationships between the banking system and the private

sector: A new approach II. Estrategia Financiera, 266 (November): 29–43. Madrid: Wolkers-

Kluwer.

Boronat Ombuena, G. J. (2010). Negotiation, risk, costs and finance: The relations with the

finance sector. Estrategia Financiera, 273(June): 14–29. Madrid: Wolkers-Kluwer.

Boronat Ombuena, G. J. (2012). Thirty years of economic and financial strategy. Estrategia

Financiera, 300(December): 20–32. Madrid: Wolkers-Kluwer.

Caja Meri, P., de Miguel, E., de Miguel, B. (2008). The industrial and Valencia Community

Services. Separata RACV 83: 31–48. Valencia: RACV.

Federal Reserve of Chicago (1994). Modern Money Mechanics, 6–17. Retrieved 01/01/2012

from: http://www.rayservers.com/images/ModernMoneyMechanics.pdf

Graell Rojas, J., Bertran Codina, S. (2010). El plan de viabilidad (The viability plan). Barcelona:

Profit.

Jaime, V., Hernández-Carrión, J. R. (2012). La política monetaria de la Unión Europea. In

Colomer Viadel, A. (Ed.). Un nuevo rapto de Europa. Las encrucijadas del Tratado de

Lisboa, 205–231. Valencia: Hathi Estudio Creativo.

Jánossy, F. (1971). The End of the Economic Miracle: Appearance and Reality in Economic

Development. White Plains, N.Y.: International Arts and Sciences Press.

Pérez, F. (2011). It is unlikely that domestic demand, consumption and investment will push

forward soon. Valencia: In business terms.

Pons, L. (2011). The economics of crisis, 2009-2011. Valencia: Official College of Economists of

Valencia-COEV.

Santandreu Martinez, E. (2009). Manual for the management of customer credit. Deusto: Deusto.

Spanish Association of Accounting and Business Administration-AECA (2008). International

regulatory framework valuation, 24–43. Madrid: Ormag.

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

17

Endnotes 1 This initial study was published by the financial newspaper ”Expansión” back in 2009 with data from Central Bank

of Spain of the year before and extracting data from the Spanish Market and Values Commission (CNMV, the

Comisión Nacional del Mercado de Valores is the regulatory body of the Spanish Stock Market) following graphs

are of the same source, own elaboration.

2 International Convergence of Capital Measurement and Capital Standards, “Basel Capital Accord I”, July 1988

(http://www.federalreserve.gov/pubs/bulletin/2003/0903lead.pdf & http://www.bis.org/publ/bcbsc111.pdf).

3 On September 28th 2012 the Central bank of Spain (BDE) released a note about the report, however, the full report

was disclosed a couple of days later.

4 Sources: Central bank of Spain (BDE), Spanish Market and Values Commission (CNMV), Oliver-Wyman’s report.

Own elaboration.

www.business-systems-review.org

Business Systems Review

ISSN: 2280-3866 Volume 3, Issue 1

January-June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

18

The Effect of the Country of Origin of

European Companies in the Context of

Young Argentinians

Giancarlo Scozzese Ph.D., Università per Stranieri di Perugia, Dept. Comparate Cultures, Perugia (Italy)

e-mail: [email protected]. Corresponding author

Roberto Bruni

Ph.D., University of Cassino and Southern Lazio, Dept. Economics and Law, Cassino (Italy)

e-mail: [email protected]

Submitted: January 10, 2014 / Accepted: March 07, 2014 / Published online: March 09, 2014.

DOI: 10.7350/BSR.D01.2014 – URL: http://dx.medra.org/10.7350/BSR.D02.2014

ABSTRACT

In this paper, we present the results of a field analysis and a literature review of the country-of-

origin effect. The field analysis involved over 300 questionnaires completed by Argentinian

youths, aged 18–30, living in the city of Buenos Aires. The aim of the study was to analyze and

verify the hypothesis that, following the major Argentinian economic crisis, European companies

can find business opportunities in the market of young Argentinians (ages 18–30) with medium-

high levels of income, because the concept of “place of origin” can contribute to the purchase of

European products, mainly through two particular intangible elements: the strong desire of

people to escape from the crisis condition, and the traditional affections between people in

Argentina and Europe.

The study reveals positive correlations between the place-of-origin effect, the connections of a

particular cluster of consumers with Europe, and the opportunities of European companies to

gain business in Argentina following the economic crisis.

Keywords: country of origin effect, place of origin effect, economic crisis, affection, business

opportunities.

1. INTRODUCTION

This work focuses on a particular aspect of the country-of-origin (COO) effect called the “place-

of-origin effect”; the main hypothesis to be verified concerns the relationship between young

Argentinian consumers (ages18–30) with good feelings about European countries and the desire

of such consumers to free themselves from the economic difficulties caused by the crisis of the

late 2000s and to buy European products; as a matter of fact, this hypothesis has suggested a

multicue approach, as it is not only the country of origin of the firm that represents a stimulus (or

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

19

deterrent) to the purchase act, but also the series of consumer features that, integrating each other,

support the product choice. In this sense, Peter & Jolibert (1995) state that, within single-cue

studies, the place-of-origin effect influences 30% of the evaluation of the product quality, while

in multicue studies, this influence is reduced to 16%; if we refer to purchase intent, the effect

decreases from 19% to 3%.

This work represents an in-depth analysis of research that has been carried out in Argentina

(Chionne & Scozzese, 2012), and which has shown the strong positive connections that

Argentinians still have with Europe, and has (among other things) highlighted the economic

conditions of development that justify further investment into Argentina on the part of European

firms.

2. POSITIONING

The COO theme and the several evolutionary paths of specific studies on place of origin (POO)

can be located among the research and reference literature that concerns international marketing.

In fact, they represent search items useful for the knowledge of countries, of consumers, and

particularly of specific relational connections between countries, products, and markets.

Firms that develop international relations of any kind must consider economic environment

conditions and the socio cultural layouts of the target countries; in many cases, they must also

compare their country of origin with the target. This is the case because the image of the country

system—especially upon its first presentation to the target nation—is the outcome of several

consumer experiences, elements of prejudice, emotions, and stereotypes, all of which may limit

or encourage the potential success of firms in foreign countries (Bartlett & Ghoshal, 1989;

Alonand McKee, 1999; Valdani, Guerini & Bertoli, 2000).

Several authors have dealt with the COO theme on the international level; in 1963, Dichter

mentioned an effect similar to the COO concerning the American inclination to purchase

Germans cars, which were perceived as quality products. With Schooler (1965), the concept of

COO was properly analyzed and, in particular, the inclination was observed of the consumer to

attribute a distinction to certain “made in” labels, even when referring to two otherwise identical

products. Nagashima (1970) was one of the earliest authors to develop a model, still used with

the appropriate variables, for surveys and the research into the COO theme; between the 1960s

and the 1970s, this author, together with Schooler, also examined the differences in perception

between more and less developed countries (Nagashima 1970, Schooler 1971). The contribution

of Obermuller (1983), in the form of a literature review, stressed that the significant differences

and the variety of analyzed countries, along with the subjects and the referred products, represent

some of the weak spots of the research into the COO. One of the earliest works in the literature

review is from 1982, in which Bolkes and Nes divide the then-extant studies into multicue and

single-cue research. The single-cue approaches are research based on single “hints” (cues) used

for the subject in studying the phenomenon.

In 1987, Shimp and Sharma produced an important contribution in identifying 17 items that are

useful for knowledge of the ethnocentric1 nature of human beings, and the associated effects on

consumer behavior during the purchase selection path.

Usunier (2006) offers a summary regarding the state-of-the-art of COO literature and, covering

the period from Schooler to Shim and Sharma (2005), splits the research into different phases.

From this review emerge the lines of research on which the present paper is focused: in

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

20

particular, this work relates the COO to the intentions of consumption; among the main authors

referred to are Peterson & Jolibert (1995) and Verlegh & Stenkamp (1999).

3. METHODOLOGY

The aim of this research is to verify the effect of the mix of features existing among the analyzed

subjects concerning the intention to purchase products from firms with “European” place of

origin, independent of the brand of the represented company and the product type. We chose to

understand that, when a European product is purchased by an Argentinian youth, it is (regardless

of brand) preferred to an Argentinian product; we also consider whether this choice may emerge

from the mix of factors we highlighted previously. The features under analysis are the desire to

escape from the economic crisis condition, the purchasers’ affection for Europe, and the

European firms’ reputations.

In order to verify the hypothesis, some other hypotheses have been formulated and verified

through the literature contributions and the data already available from ad hoc research: for the

collection of primary data that can be referred to the specific search terms of this work, a

questionnaire addressed to Argentinian young people between the ages of 18 and 30 living in

Buenos Aires has been used; this age interval has been chosen, as it represents a cluster of young

people that have personally experienced the crisis of 2001, and which have culturally and socially

developed within a national mood that has had to organize the path to economic recovery in

Argentina.

Buenos Aires Province has a population of 15, 594, 428, while the autonomous city of Buenos

Aires has 2,891,082 inhabitants2. The total number of young people between the ages of 18 and

30 in Argentina is 8,525,865; in Buenos Aires Province, there are 3,272,177 people in this age

group, while in the autonomous city of Buenos Aires, there are 818,044—about the 25% of the

total amount. A random sample of 200 people was selected from these.

The 2001 economic crisis has left a difficult situation and, after more than ten years, the

economic situation has been complicated by the effects of the 2007 global economic crisis, which

has directly involved the generation that is considered in this work—even though the country is

presently entering a phase of consumption revolution; in many cases, the younger generations are

more and more attached to new technology, to digital hyper connectivity, and to spread of trends

and information (also on a commercial level); they thus communicate quickly in space and time.

Modernity and the incentive to innovation have spread throughout the population, encouraging

the progression to a new economic and social system.

Simultaneously, although Argentina is an independent country with its own national culture,

European references and the direct connections between Europe and the older generations

endure; the feeling of belonging and the affectionate relationships with the nations of origin of

many families persevere, as do the traditions and images of certain European countries.

3.1 Questionnaire analysis

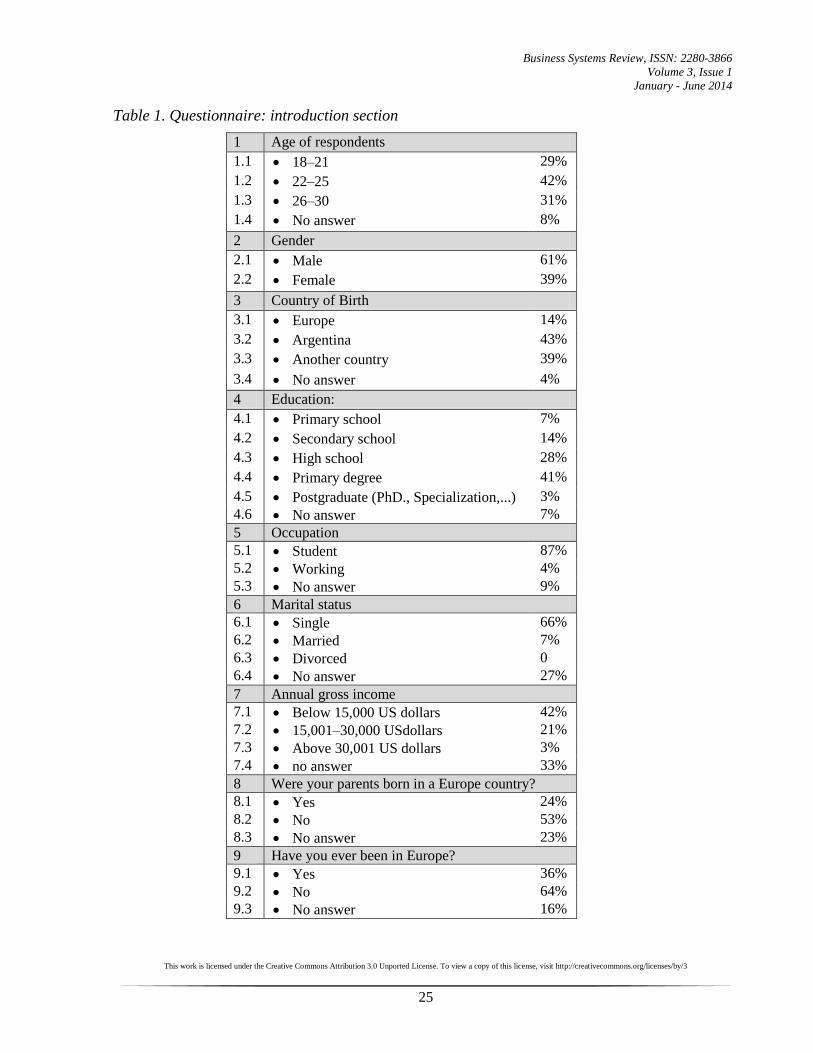

The questionnaire, in addition to covering basic information on the subjects (age, gender, place of

birth, education, and occupation), requests data on income levels and any personal links that may

exist with Europe (e.g., if the subject or the subject’s parents were born in Europe).Such elements

help to determine the connections of the subject with Europe; additionally, so as to record

indirect and affective connections with the European continent, some questions have been added

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

21

concerning whether the respondent has visited Europe. Such visits may contribute to creating an

incentive towards European products (or enhancing their appeal) in the subjects.

Some of the multiple-choice questions explore the perception of European countries on the part

of the subjects, together with their perceptions of European products, their technological

reliability, and the value attributed to them. We focused in particular on determining whether

subjects were willing to pay more for European products; this last contributes to our knowledge

of the subject’s ability to escape from the crisis condition, and provides some reflection points on

the perception of European firms and the value of their products.

In attempting to verify the knowledge and reputation of European Countries on the part of the

questionnaire respondents, some questions have been formulated with reference to a certain

group of countries and their Europemembership, the perception of their quality of life, and the

technological reliability of their products. In attempting to determine the intent of purchasing

European products—despite their higher price than local products—we asked some questions

concerning the ability of the respondents, in percentage terms, to spend more on such products,

and on their level of affection for European products.

4. SEARCH QUERY, INITIAL HYPOTHESIS, AND LITERATURE REFERENCE

The research query asks what effects result from the mix of different features observed in the

Argentinian youth population. In the past, each feature has been analyzed in the COO literature,

and we report here three hypotheses and the literature they derive from.

Specifically, Hp1 and Hp2 refer to the COO literature, while Hp3 concerns consumer behavior:

the three hypotheses, together with the questionnaire data, define elements useful in answering

the research query.

Hp1: The images of the countries and the geographical areas influence the purchase of products

from these territories;

Hp2: There are affective elements that influence the choice of products from certain countries;

Hp3: The desire to escape from the economically negative condition incentivizes the purchase of

products that have a higher price and level of quality.

The first hypothesis (Hp1) is a standard search query for COO; as a matter of fact, it is also

extended to all the other interpretations of studies on the impact of the reputation, the image, and,

in general, the value transferred from countries to the products or services and their firms.

The literature stresses that, when we are dealing with COO, we are mainly referring to a country;

some authors have also begun to study territories or origin, or even the industrial district of

origin (Guerini & Uslenghi 2006). Independent of geographical boundaries, some authors have

analyzed the relevance of regional areas to consumer influence (Ittersum, Candel & Meulenberg,

2003), or of certain very prominent cities (Lentz, Holzmuller & Schirmann, 2006). Other authors,

such as Andehn and Berg (2011), state that the “country of origin concept will be replaced by the

place of origin (POO)”, which can develop in the consumer’s mind a series of emotions and

images that, in turn, may reduce the impact (both positive and negative) of each country’s

positioning and can multiply the valorization process of the whole territorial area: the place-of-

origin effect also attributes, from a theoretical point of view, the consequences of the country-of-

Business Systems Review, ISSN: 2280-3866

Volume 3, Issue 1

January - June 2014

This work is licensed under the Creative Commons Attribution 3.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by/3

22

origin effect to broad areas, such continents or aggregations of countries—whether recognized or

not, from the administrative point view3 — on an international level.

The emotional impact of the product’s origin or, in some cases, of the origin of the producing (or

supplying) firm, falls off with the duration of the firm’s presence within the analyzed market,

since, in some cases, the presence of a firm in a foreign territory can become permanent. This

results in the involvement of several generations of customers, who at some point being to be

familiar with the firm’s products, and interiorize them within the distribution offer of their

country.

During the evaluation phase of the firms entering new countries, which takes the form of the

initial contact between the companies and the destination country, consumer choice is

progressively less and less determined by the product’s origin. According to the study of Verlegh

and Steenkamp (1999), the importance of the COO effect on consumer behavior changes

depending on the moment of the purchase decision process of the consumer. The importance of

the COO effect decreases as soon as we have the transition from the qualitative perception of the

product to the real purchase intention; as a matter of fact, the purchase intention is influenced by

several variables (price, warranty, available income, product placement, etc.), and these variables

can lessen the COO effect on the consumer at the moment of purchase choice at a certain selling

point, in the case of consumer goods or shopping. This can be less influential on the choice of

“problematic” goods or, in some cases, on the selection of the banner, selling point, or brand

when the subject is making a choice on the basis of personal sensations deriving from the COO.

Hp1 is verified from several contributions of the literature.

Hp2: There are affective elements that influence the choice of products from certain countries.

Inevitability, the study of COO, in all its variation, takes under consideration the analysis of the

existing relations that may develop over time in respect to the affective components, and that

which also evolve between the individual subjects and the countries; the subjects may be directly

involved in a positive relation with a country for various reasons which can add together and,

sometimes, overcome some difficulties existing firms, products, and consumers. The consumer

who is involved in a positive feeling toward a country may even be led by the strong

encouragement of this positive feeling to find “justifications” when the product or service does

not work.

In general, the country-of-origin effect depends on the purchaser’s characteristics, and seems to

be higher for end consumers than for industrial purchasers (Liefeld, 1993; Peterson & Jolibert,

1995; Verlegh & Steenkamp, 1999); in particular, Verlegh & Steenkamp (1999) focus on the

importance acquired by the affective and normative components: in their work, they assert that

the country of origin must not be seen as a cognitive variable purely linked to product quality, but

should be evaluated together with other factors, such as emotions, identity, social status, pride,