Building the next Georgian copper-gold producer · July 2017 3 AIM listed exploration and...

24

July 2017 Building the next Georgian copper-gold producer

Transcript of Building the next Georgian copper-gold producer · July 2017 3 AIM listed exploration and...

July2017

BuildingthenextGeorgiancopper-goldproducer

July2017

Disclaimer

This presentation has been prepared by Georgian Mining Corporation(“GMC” or the “Company”) and does not constitute an offer or invitation for the sale or purchase of any securities, nordoes it purport to, set out, or refer to all or any of the information an investor might require or expect in making a decision as to whether or not to deal in shares in the Company.

This presentation does not constitute and is not a prospectus or listing particulars (under either the Prospectus Regulations 2005 (as amended), the Financial Services and Markets Act 2000(“FSMA”) or the Prospectus Rules of the Financial Services Authority) nor does it comprise an AIM admission document for the Rules of AIM, a market operated by the London Stock Exchangeplc and should not be construed as such. No representation or warranty or other assurance, express or implied, is made by or on behalf of the Company or any of its respective directors,officers, employees, advisers or any other persons as to the fairness, accuracy or completeness of the information or estimates or opinions or other statements about the future prospects ofthe Company or any of its respective businesses contained in or referred to in the presentation given in connection therewith and no responsibility, liability or duty of care whatsoever isaccepted by any such person in relation to any such information, projection, forecast, opinion, estimate or statement.

The Company’s Nomad S.P. Angel Corporate Finance LLP (“S.P. Angel”) has not approved the presentation as a financial promotion for the purposes of section 21 of FSMA or otherwise.

This presentation may not be (i) taken or transmitted into the United States of America, (ii) distributed, directly or indirectly, in the United States of America or to any US person (within themeaning of regulations made under the Securities Act 1933, as amended), (iii) taken or transmitted into or distributed in Canada, Australia, the Republic of Ireland or the Republic of SouthAfrica or to any resident thereof, or (iv) taken or transmitted into or distributed in Japan or to any resident thereof. Any failure to comply with these restrictions may constitute a violation ofthe securities laws or the laws of any such jurisdiction. The distribution of this document in other jurisdictions may be restricted by law and the persons into whose possession this documentcomes should inform themselves about, and observe, any such restrictions.

This presentation must not be copied, reproduced, published, distributed, disclosed or passed to any other person at any time without the prior written consent the Company.

By accepting a copy of the presentation you agree to be bound by the foregoing provisions.

Forward-looking Statements

This presentation may contain forward-looking statements. These statements relate to the future prospects, developments and business strategies of the Company and its subsidiaries (the“Group”). Forward-looking statements are identified by the use of such terms as “believe”, “could”, “envisage”, “estimate”, “potential”, “intend”, “may”, “plan”, “will” or the negative of those,variations or comparable expressions, including references to assumptions. The forward-looking statements contained in the presentation are based on current expectations and are subject torisks and uncertainties that could cause actual results to differ materially from those expressed or implied by those statements. If one or more of these risks or uncertainties materialises, or ifunderlying assumptions prove incorrect, the Group’s actual results may vary materially from those expected, estimated or projected. Given these risks and uncertainties, potential investorsshould not place any reliance on forward-looking statements. These forward-looking statements speak only as at the date of the presentation.

Competent Person

The Competent Person responsible for the technical information contained in this presentation is Mr James Royall, a Member of Australian Institute of Geoscientists and a Competent Personas defined in the 2004 Edition of the 'Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves'.

2

GeorgianMiningCorporation

July2017

3

AIM listed exploration and development company focused on thedevelopment of copper and gold projects in Georgia

GeorgianMiningCorporation

PROLIFICREGIONLicencelocatedontheTethyan Belt,hosttomultiplehighgradecopper-golddepositsandproducingminesinTurkey,Armenia,

SerbiaandGeorgia

HUGEEXPLORATIONUPSIDEKvemoBolnisirepresentsapotentialnew

epithermaldiscoverywitha50Mtexplorationtarget.KBisjustoneof14targetareas

identifiedwithinthe860sq kmlicencearea

FIRSTMOVERADVANTAGEINPROMININGJURISDICTION

Georgiahighlysupportiveofforeigndirectinvestmentandmineral

development- 30yearmininglicencegrantedundertheGeorgianMiningCode

PHASEDEXPLORATIONPLANThreestageplanfocussedonrapidlydelineatingasignificantresourceacrosslicenceareaanddelivering

‘proofofconcept’productionin2017

Overview

[email protected]%Cuand

0.1g/tAubeingexpandedbyongoingdrilling

July2017

KeyData

4

GeorgianMiningCorporation

KeyData

Market AIM

EPIC GEO

SharePrice(1) 19.625 pence

SharesinIssue 114,574,491

MarketCap £22.5m

NOMAD/Broker SP Angel

JointBroker Shard Capital

SignificantShareholders

Name Holding %

TBAmatiUK 6,712,491 5.86

Fahad Al-Tamimi 6,149,075 5.37

MrLeoN.S.Berezan 6,148,100 5.37

Edale Capital 4,000,000 4.97

Board&Management(2) 5,584,967 6.94

(1) Share price as at closing 30 June2017

Options &WarrantsOutstandingNumber ExercisePrice Expiry date5,000,000 14p 20July2021

1,900,000 12p 3April2022

3,300,000 18.25p 21July2022

July2017

TheTeamtoDeliver

5

GeorgianMiningCorporation

JamesRoyallChiefGeologist

MarkOwenSeniorAdvisor

• Over 20 years’ professional experience as a geologist in Europe, Africa and South America.• Previously at Rio Tinto, Berkeley Resources, White Star Resources, Medgold Resources. Based in Georgia

• Over 35 years’ experience in mining industry, expert in both underground and open pit mining• Specialised in conversion of Soviet mineral resources (GKZ) to internationally recognised codes

GregKuenzelManagingDirector• CharteredaccountantandadvisortominingandexplorationcompaniesprimarilylistedonAIM• Over20years’experienceinthecorporateandresourcesectors

MartynChurchouseExplorationDirector• Over33years'experienceinEuropeandAfricainexploration,minedevelopmentandminemanager• SeniorAdvisortoLundinMining.PreviouslyatAngloAmericanandGoldFields

Dr.NeilO’BrienNon-executiveDirector

• SeniorVPExplorationofLundinMiningCorp.withover30yearsofindustryexperience• PhDEconomicGeology,expertiseinTethyan Beltgeologywithatrackrecordofvalue-creativediscoveries

LaurieMutchNon-executiveDirector• Internationalmanagementconsultantwithover40years’experienceintheresourcesandenergysectors• FormerlyExecutiveDirectorofShellInternationalGas&Power

B O A R D

K E Y M A N A G E M E N T

PeterDamouniNon-executiveDirector

• Over16yearsofexperienceininvestmentbankingandcapitalmarkets,withexpertiseinminingandoilandgas.• DirectorofKerrMinesInc,aTSXlistedgolddevelopment&miningcompany

July2017

Tethyan BeltRegionalandGeologicalComparatives

6

The Tethyan Belt, which hosts numerous multi million oz deposits, extendsinto Georgia; GEO has extensive licences with identified resources

GeorgianMiningCorporation

CukaruPeki

July2017

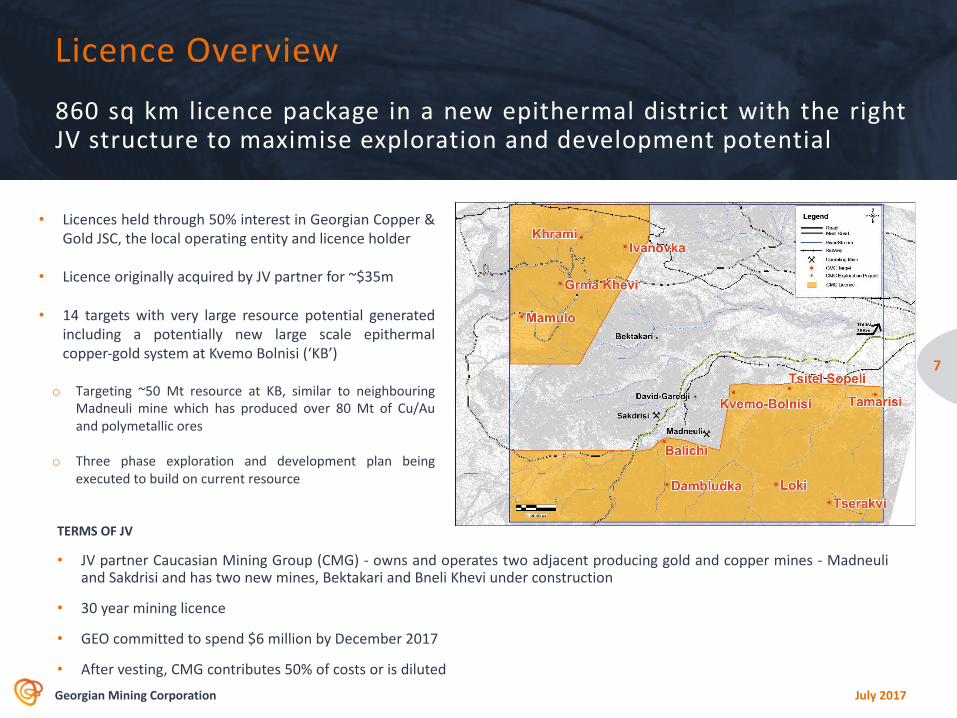

LicenceOverview

• Licences held through 50% interest in Georgian Copper &Gold JSC, the local operating entity and licence holder

• Licence originally acquired by JV partner for ~$35m

• 14 targets with very large resource potential generatedincluding a potentially new large scale epithermalcopper-gold system at Kvemo Bolnisi (‘KB’)

o Targeting ~50 Mt resource at KB, similar to neighbouringMadneuli mine which has produced over 80 Mt of Cu/Auand polymetallic ores

o Three phase exploration and development plan beingexecuted to build on current resource

7

860 sq km licence package in a new epithermal district with the rightJV structure to maximise exploration and development potential

GeorgianMiningCorporation

TERMS OF JV

• JV partner Caucasian Mining Group (CMG) - owns and operates two adjacent producing gold and copper mines - Madneuliand Sakdrisi and has two new mines, Bektakari and Bneli Khevi under construction

• 30 year mining licence

• GEO committed to spend $6 million by December 2017

• After vesting, CMG contributes 50% of costs or is diluted

July2017

Kvemo Bolnisi

8

GeorgianMiningCorporation

“Theonlygroupmakingnoises(inGeorgia),whicharebecomingconsiderablylouderoflate,isGeorgianMiningCorporation,whichisexploringatitsKvemo Bolnisicopper-goldprojectwithits

50%joint-venturepartner,CMG.”MiningJournal,11May2017

July2017

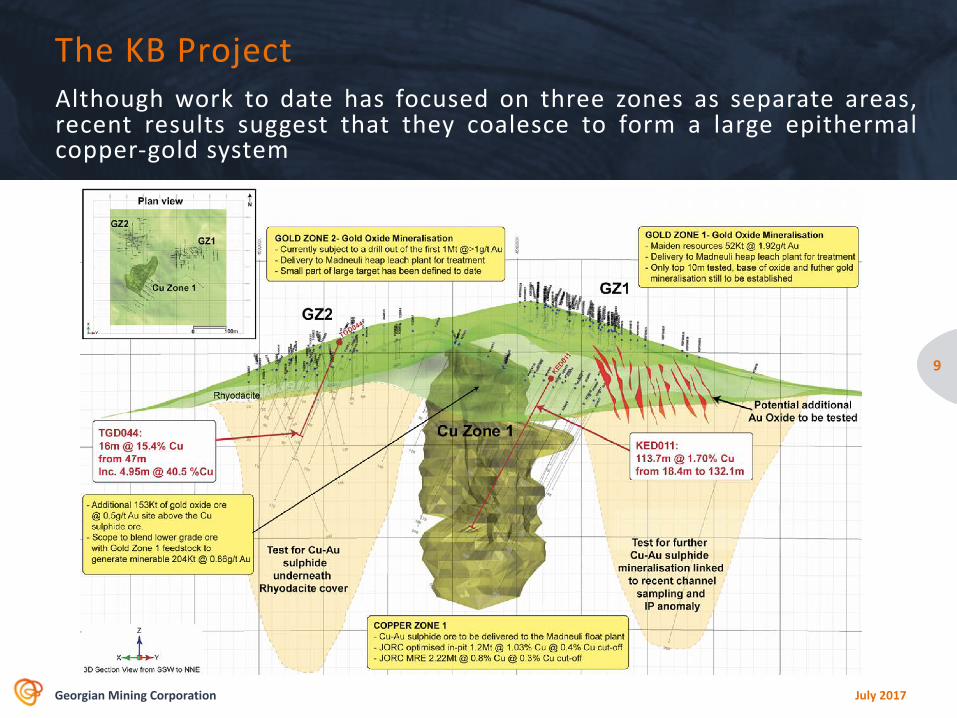

TheKBProject

9

Although work to date has focused on three zones as separate areas,recent results suggest that they coalesce to form a large epithermalcopper-gold system

GeorgianMiningCorporation

July2017

KBProjectEpithermalCuAuPotential

10

New epithermal ore geology model provides exceptional explorationopportunities that previous explorers had not considered – has thepotential to deliver both bulk tonnage and high grade zones

GeorgianMiningCorporation

July2017

• Initial JORC Mineral Resource estimate of 2.22 million tonnes @ 0.8%Cu and 0.1g/t Au at a 0.3% Cu cut-off

• JORC optimised in-pit 1.2 million tonnes @ 1.03% Cu at a 0.4% Cu cutoff

• Triggers discussions with JV partner regarding the delivery of an initial1Mt @ 1% Cu for toll treatment

• Initial drill results included significant copper-gold mineralisationintersected at shallow depths:

• KED001– [email protected]%Cuand0.12g/tAufrom89.75m• KED006– [email protected]%Cuand0.1g/tAufrom47.0m• KED 011 - 113.7m @ 1.70% Cu from 18.4 to 132.1m, including:

• 46.4m @ 2.88% from 19.6m; and• 16.2m @2.20% from 75.8m

• KED 008 – 28.6m @ 1.60% Cu and 0.80g/t Au from 47.4m

• New epithermal ore geology model provides exceptional explorationopportunities that previous explorers had not considered – has thepotential to deliver both bulk tonnage and high grade zones

KBCopperZone1

11

GeorgianMiningCorporation

July2017

GoldOxideZones• Initial Indicated and Inferred gold oxide Resource of 204,000 tonnes at

an average grade of 0.83 g/t Au – includes gold oxides at Gold Zone 1and Copper Zone 1

• Peak grades from individual drill samples confirm the presence of high-grade gold-bearing structures as part of gold mineralised zone:

• 82.1 g/t Au (0.25m sample)• 7.31 g/t Au (1.0m sample)• 7.12 g/t Au (1.5m sample)• 6.61 g/t Au (1.0m sample)

• Gold mineralisation open in all directions - Updated resource expectedwithin weeks covering Gold Zone 1 and Gold Zone 2

• 65 drill holes completed to date, depths varying from 20 metres to 120metres - additional deeper drilling now underway

• Metallurgical test work – column tests underway, excellent recoveriesachieved to date from BTR’s

• Nearby heap leach plants could accept all output of gold oxidemineralisation

12

GeorgianMiningCorporation

Selectedgold(‘Au’)drillinterceptsfromthefirst45drillholesinclude:

TGD007: [email protected]/tAufrom0.0m

TGD002: [email protected]/tAufrom5.0m

TGD003: [email protected]/tAufrom8.0m

TGD015:[email protected]/tAufrom8.0m

TGD026:[email protected]/tAufrom10.0m

TGD030:[email protected]/tAufrom0.0m

TGD034:[email protected]/tAufrom1.0m

TGD036:[email protected]/tAufrom3.0m

TGD037:[email protected]/tAufrom5.0m

TGD038:[email protected]/tAufrom0.0m

Initialdrillingtriggeredbychannelsamplingofoutcroppingrock:

July2017

ExceptionalgradesfromGoldZone2• Exceptionally high copper grades identified with continuous copper

mineralisation intercepted from the base of the gold oxide zone (~47 m) tothe end of the hole at 120 m

• Assays have returned 16m @ 15.4% Cu from 47m, including [email protected]% Cu, 0.46g/t Au and 55.6 g/t Ag (TGD-044)

• Additionally identified continuous gold mineralisation in the oxide zone fromsurface to the base of oxides at 47 m including 24m @1.58 g/t Au from 1m

• Gold oxides, typically occurring from surface down to the base of oxidationat between 40 and 70m depth, are followed by intersections of copperminerals in a chalcocite blanket

• Drilling underway to test whether the gold oxide and copper-gold sulphidemineralisation extends to the south and may potentially link up with thecurrent copper-gold JORC Resource

• Most holes ended in mineralisation so this new copper-gold zone is open atdepth

13

GeorgianMiningCorporation

Selectedcopper(‘Cu’)drillintercepts

TGD-038:[email protected]%Cufrom56m

TGD-041:[email protected]%Cufrom34m

TGD-045:[email protected]%Cufrom24m

July2017

Phase1 Phase2 Phase3

FocusedonpositioningKBtodeliver‘proofofconceptcopperandgoldproduction’usingJVPartner’s

processinginfrastructure

TostartbuildingtheresourcetowardslongertermtargetandtostrengthenGEO’sgeologicalmodelforKBand

beyond

Toestablishaworldclassoperationwhichiscapableofhostingownplant

andoperations

Todelineateaminimumof1-2Mtinlinewiththeprocessingcapacityavailableatitspartner’sneighbouringoperations

Todelineatea3-5Mtresourceofcombinedcopper-goldsulphideandgoldoxidemineralisation

Todelineatea50Mt+resourceatKBandtodevelopadditionaldiscoveriesacrossthe860sq kmlicencebasedonnewinterpretationofgeologicalmodel

Achievedandexceeded Ontracktocompletein2017 TocommenceoncompletionofPhase2

• Tode-risktheprojectbyrefiningprocessingroute

• Toprovidecashflowtocontributetowardsfurtherexploration

• Tostrengthenpartnerrelationship

• Tobuildvaluebycreatingastrengthenedunderstandingofthelicenceareaandproveepithermalcharacteristicsoftheground

• TotransformGEOintoabluechipminerwithastrongholdinGeorgia

ResourceDevelopmentPlan

14

Phased development with long-term target of 50Mt + for KB alone,through the application of phased exploration and development

GeorgianMiningCorporation

VISION

TARG

ETSTAT

US

WHY

?

July2017

WhyProofofConceptProduction?

15

GeorgianMiningCorporation

Benefits include:

• Access to established infrastructure and plants atMadneuli and Sakdrisi mines with available underutilised capacity

• Projected low contract mining and processingcosts based on signed MoU with actual costssupplied by JV partner

• Low capital expenditure and potentially shortlead time to production

HeapLeachOperation Sampleprep&labfacilities Loadingfacilitiesatprocessingplant

FlotationCircuit

Processing plants with excess capacity at nearby mines owned byGEO’s JV Partner offer a potentially short lead time to production withmodest capital expenditure

July2017

AdditionalTargets

16

Additional targets offer the opportunity to expand the resourcebeyond the 50MT exploration target in place for KB

GeorgianMiningCorporation

Dambludka• Base and precious metal project covers a

2km by 1km area, 8km SW of theMadneuli mine

• Area subject to historical mining and aditdevelopment during later explorationprogrammes

• GCG is compiling data and will follow upwith field sampling programmes toidentify potential bulk tonnage targets

July2017

Dambludka – HistoricSamplingResults

17

GeorgianMiningCorporation

July2017

OtherExplorationTargetsWithinLicenceArea

Tsitel Sopeli• Located12kmNEofMadneuli Mineand

processingfacilityand6kmEofKB

• 1x1.5kmfootprintofoutcroppinggoldoxidewithbasemetalandbaritemineralisation

• 14holesconfirmgoldandbasemetalmineralisation;resultsinclude:• [email protected]/tAufromsurface• [email protected]/tAufromsurface• [email protected]/tAuand0.25%Cufrom18.5m• [email protected]/tAuand0.152%Cufrom18.5m

• RecentIPsurveyidentifiedaHotMaddentypetargetwhichwarrantsfollowup

18

Significant historical exploration undertaken across licence area;opportunity to apply modern exploration techniques

GeorgianMiningCorporation

NewLowSulfidation EpithermalDistrict

• Historicexplorationgearedtosearchforsmalldiscretehigh-gradeVMStargetsatdepth

• Newinterpretationsuggestsenormousscopeforbulktonnagecopper-goldsulphideandgoldoxideepithermalresources.-

• NewdepositsbeingfoundinSovietbrownfieldsites

July2017

InvestmentCase

19

GeorgianMiningCorporation

LARGE,SCALABLE,HIGHGRADERESOURCEPOTENTIAL

Explorationofcopperandgoldzonesbuildinggeologicalmodeltargetinginexcessof50mtand

1millionoz

PROOFOFCONCEPTPRODUCTIONNearbyprocessingoperationswithavailablecapacity,ownedbyJV

partner– providingshorttermcashflowtofundexploration

NEWDISCOVERIESANDOPPORTUNITIES

GEO’slicencesarehighlyprospectivehavingyieldedexcellentexploration

results– LocatedintheprolificTethyan Belt

DELIVERYCAPABILITYBoardandmanagementincludeprovenminedevelopersandtechnicalstaffwithGeorgian

operationalexperience

EXCELLENTJURISDICTIONGeorgiahasanestablishedminingcodeandisopentodirectforeign

investment

July2017

Contacts

ManagingDirector:GregKuenzelE:[email protected]

ExplorationDirector:MartynChurchouse

A:47CharlesStreet,London,W1J5ELT:+44(0)2079079327

20

GeorgianMiningCorporation

July2017

Appendix

21

GeorgianMiningCorporation

July2017

Georgia– AMiningFriendlyJurisdiction

22

GeorgianMiningCorporation

InternationalBusinessDestination• BP has been operating successfully since 1996

• Intercontinental, Starwood, Hilton, have recently built new hotelsin Tbilisi, while Sheraton, Radisson and Marriot are alreadyestablished

• Multiple major accounting and law firms have offices

• Strategic location as an entry gate to the Caucasus and CentralAsia

European&WorldPartnerships

• Hosted the 2015 EBRD Annual Meeting;€2.3 billion has been invested by the EBRDto date

• EU Association - the Agreement commitsGeorgia to a reform agenda in key areassuch as security policy, trade, economicrecovery and growth and governance

• Priority country within the EuropeanNeighborhood Policy and the EasternPartnership

• NATO-Georgia Commission

• Georgia is a member of the World TradeOrganisation

• Transit country connecting severalimportant economic regions. The CaucasusTransit Corridor (CTC) is a key transit routebetween Western Europe and Central Asiaand carries over 60% of total foreign trade

• The World Bank has financed five roadimprovement projects (with totalcommitments of US$507 million)

• IFC member and shareholder in 1995. As ofDecember 31, 2016, IFC has providedaround $1.64 billion in long-term financing

July2017

Georgia– EconomicStability

23

Represents a democratic mining friendly jurisdiction with establishedinfrastructure

GeorgianMiningCorporation

Population: 4.5million

Literacyrate: 99.7%

Unemploymentrate: 12.4%

GDP: $27.6bn

GDPpercapita: US$6,145

Growth: 3.2%

Growth(5year): 3.7%

Inflation: 0.5%

EconomicFreedominEuropeWorldRank RegionalRank Country OverallScore Changefrom2016

4 1 Switzerland 81.5 0.56 2 Estonia 79.1 1.99 3 Ireland 76.7 -0.612 4 UK 76.4 0.013 5 Georgia 76.0 3.414 6 Luxembourg 75.9 2.015 7 Netherlands 75.8 1.216 8 Lithuania 75.8 0.618 9 Denmark 75.1 -0.219 10 Sweden 74.9 2.920 11 Latvia 74.8 4.422 12 Iceland 74.4 1.124 13 Finland 74.0 1.425 14 Norway 74.0 3.226 15 Germany 73.8 -0.6

Source:TransparencyInternationalGlobalCorruptionBarometer2013(latestreport)

Source:WorldBank,2017(rankoutof190countries

GeorgianMiningCorporation 24

July2017

BuildingthenextGeorgiancopper-goldproducer