Budgetary review and recommendations reportpmg-assets.s3-website-eu-west-1.amazonaws.com/1/... ·...

40

Budgetary review and recommendations report Water and Sanitation portfolio 04 October 2017

Transcript of Budgetary review and recommendations reportpmg-assets.s3-website-eu-west-1.amazonaws.com/1/... ·...

Budgetary review and recommendations report Water and Sanitation portfolio

04 October 2017

2

Reputation promise

The Auditor-General of South Africa (AGSA) has a constitutional mandate and, as the supreme audit institution (SAI) of South Africa, exists to strengthen our country’s democracy by enabling oversight, accountability and governance in the public sector through auditing, thereby building public confidence.

3

Role of the AGSA in the reporting process

Our role as the AGSA is to reflect on the audit work performed to assist the portfolio committee in its oversight role of assessing the performance of the entities taking into consideration the objective of the committee to produce a Budgetary review and recommendations report (BRRR).

4

ANNUAL PERFORMANCE PLAN (APP)

TARGETS PER APP

5

“Plan-Do-Check-Act Cycle”, also the Deming cycle , courtesy of the International Organization for Standardization

AGSA theme for the current year to improve outcomes

6

DO

PLAN

CHECK ACT

AGSA theme for the current year to improve outcomes

7

1 The AGSA’s annual audits

7

8

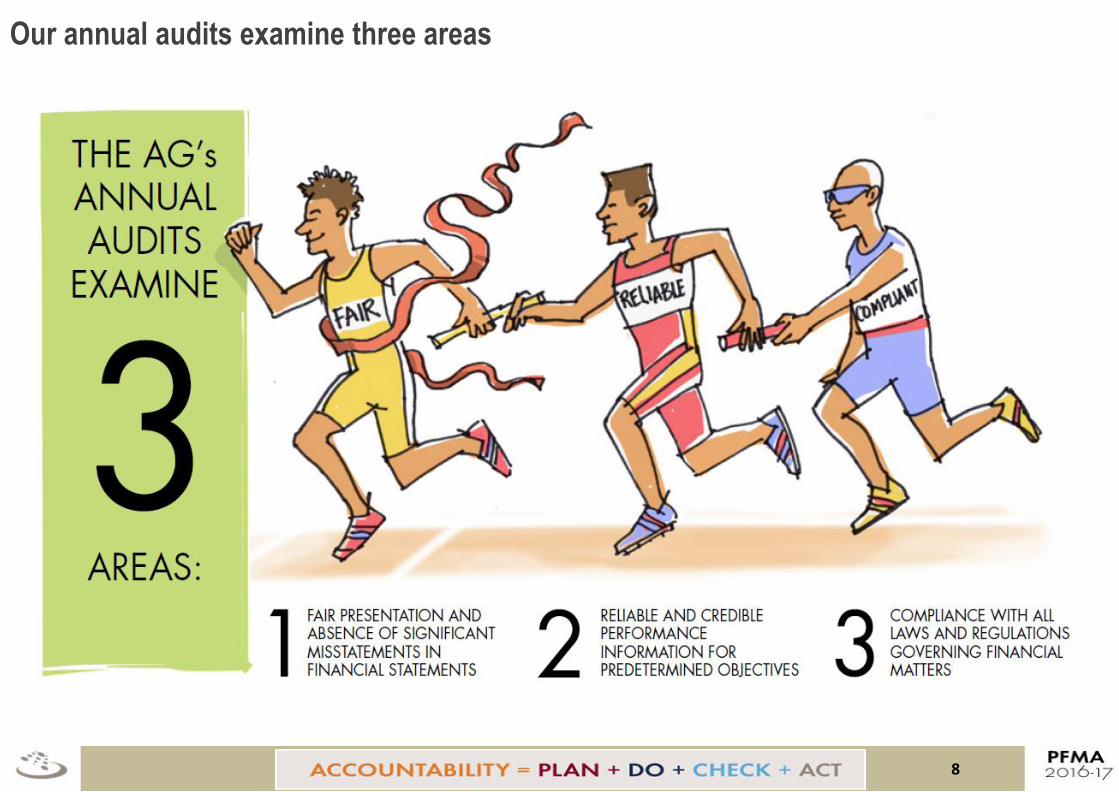

Our annual audits examine three areas

The AGSA expresses the following different audit opinions:

Unqualified

opinion with no

findings

(clean audit)

Financially

unqualified opinion

with findings

Auditee:

• Credible and reliable

financial statements

that are free of material

misstatements

• Useful and reliable

performance as

measured against

predetermined

objectives

• complied with key

legislation

Auditee produced financial

statements without material

misstatements or could correct the

material misstatements, but

struggled in one or more area to:

• align their performance reports to

the predetermined objectives

they committed to in their APPs

• set clear performance indicators

and targets to measure their

performance against their

predetermined objectives

• report reliably on whether they

achieved their performance target

• determine the legislation that they

should comply with and

implement the required policies,

procedures and controls to

ensure compliance

Qualified

opinion

Auditee:

• had material

misstatements on

specific areas in their

financial statements,

which could not be

corrected before the

financial statements

were published.

Adverse

opinion

Auditee:

• had the same challenges

as those with qualified

opinions but, in addition,

they had so many material

misstatements in their

financial statements that

we disagreed with almost

all the amounts and

disclosures in the financial

statements

Auditee:

• had the same

challenges as those with

qualified opinions but, in

addition, they could not

provide us with evidence

for most of the amounts

and disclosures reported

in the financial

statements, and we

were unable to conclude

or express an opinion on

the credibility of their

financial statements

Disclaimed

opinion

9

2

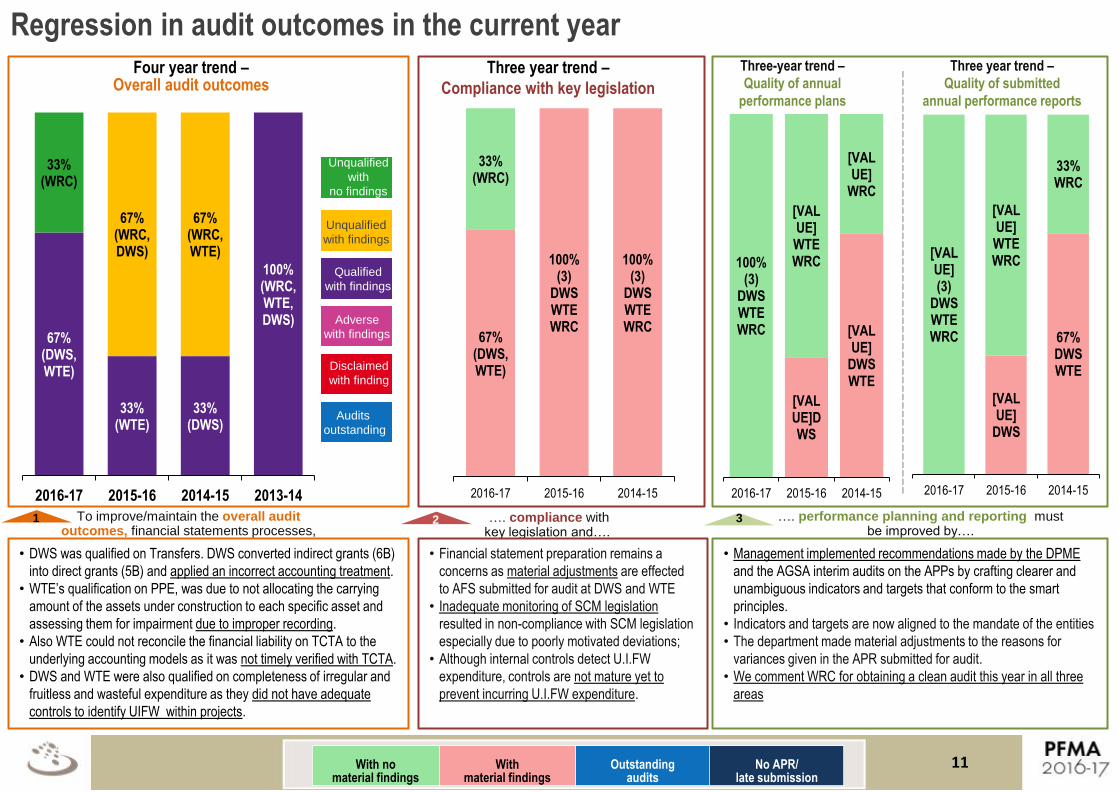

The 2016-17 audit outcomes and key messages

10

…. compliance with key legislation and….

To improve/maintain the overall audit outcomes, financial statements processes,

1 3 2

Four year trend – Overall audit outcomes

…. performance planning and reporting must be improved by….

Regression in audit outcomes in the current year

2016-1

PFMA

• DWS was qualified on Transfers. DWS converted indirect grants (6B)

into direct grants (5B) and applied an incorrect accounting treatment.

• WTE’s qualification on PPE, was due to not allocating the carrying

amount of the assets under construction to each specific asset and

assessing them for impairment due to improper recording.

• Also WTE could not reconcile the financial liability on TCTA to the

underlying accounting models as it was not timely verified with TCTA.

• DWS and WTE were also qualified on completeness of irregular and

fruitless and wasteful expenditure as they did not have adequate

controls to identify UIFW within projects.

• Financial statement preparation remains a

concerns as material adjustments are effected

to AFS submitted for audit at DWS and WTE

• Inadequate monitoring of SCM legislation

resulted in non-compliance with SCM legislation

especially due to poorly motivated deviations;

• Although internal controls detect U.I.FW

expenditure, controls are not mature yet to

prevent incurring U.I.FW expenditure.

• Management implemented recommendations made by the DPME

and the AGSA interim audits on the APPs by crafting clearer and

unambiguous indicators and targets that conform to the smart

principles.

• Indicators and targets are now aligned to the mandate of the entities

• The department made material adjustments to the reasons for

variances given in the APR submitted for audit.

• We comment WRC for obtaining a clean audit this year in all three

areas

Three year trend –

Compliance with key legislation

67% (DWS, WTE)

100% (3)

DWS WTE WRC

100% (3)

DWS WTE WRC

33% (WRC)

2016-17 2015-16 2014-15

Three-year trend –

Quality of annual

performance plans

Three year trend –

Quality of submitted

annual performance reports

[VALUE]DWS

[VALUE]

DWS WTE

100% (3)

DWS WTE WRC

[VALUE] WTE WRC

[VALUE]

WRC

2016-17 2015-16 2014-15

[VALUE]

DWS

67% DWS WTE

[VALUE] (3)

DWS WTE WRC

[VALUE] WTE WRC

33% WRC

2016-17 2015-16 2014-15

Unqualified

with

no findings

Unqualified

with findings

Qualified

with findings

Adverse

with findings

Disclaimed

with finding

Audits

outstanding

--------------------------------------------------

67% (DWS, WTE)

33% (WTE)

33% (DWS)

100% (WRC, WTE, DWS)

67% (WRC, DWS)

67% (WRC, WTE)

33% (WRC)

2016-17 2015-16 2014-15 2013-14

11 With no

material findings With

material findings Outstanding

audits No APR/

late submission 11

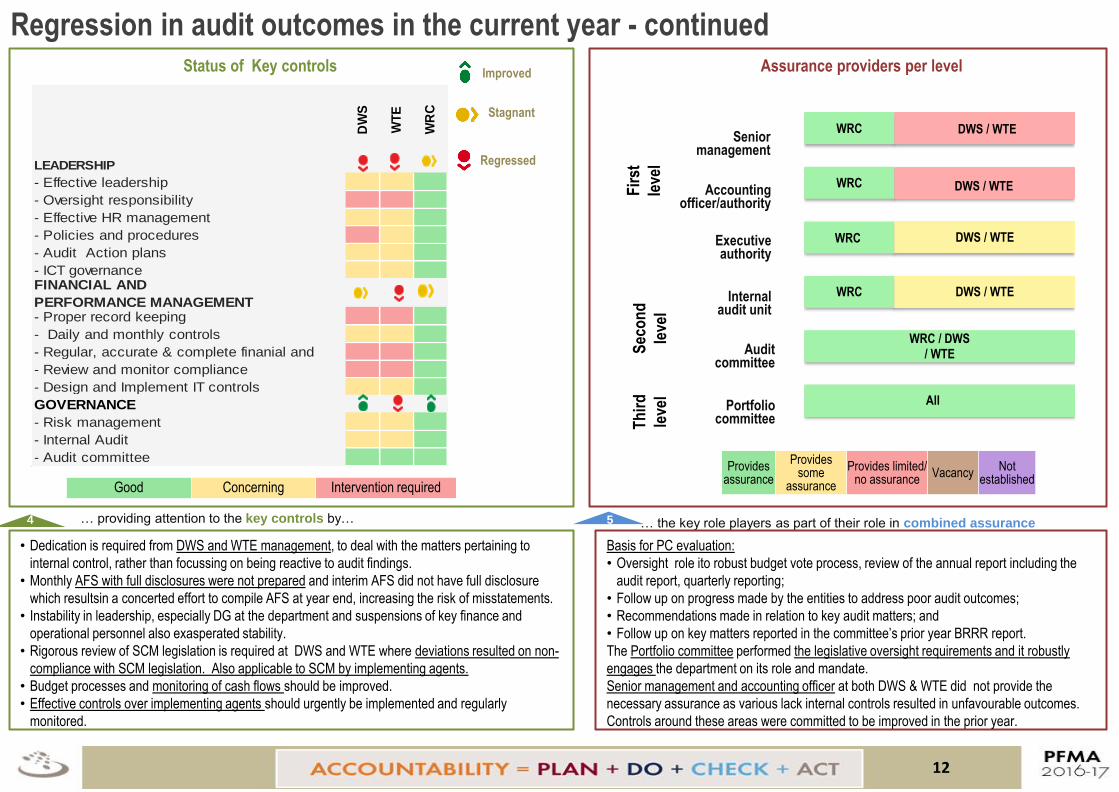

DW

S

WT

E

WR

C

- Audit committee

- Proper record keeping

- Daily and monthly controls

- Regular, accurate & complete finanial and

- Review and monitor compliance

- Design and Implement IT controls

GOVERNANCE

- Audit Action plans

- ICT governance

- Risk management

- Internal Audit

FINANCIAL AND

PERFORMANCE MANAGEMENT

- Oversight responsibility

- Effective HR management

- Policies and procedures

LEADERSHIP

- Effective leadership

Status of Key controls

Good Concerning Intervention required

4 … providing attention to the key controls by…

Regression in audit outcomes in the current year - continued

• Dedication is required from DWS and WTE management, to deal with the matters pertaining to

internal control, rather than focussing on being reactive to audit findings.

• Monthly AFS with full disclosures were not prepared and interim AFS did not have full disclosure

which resultsin a concerted effort to compile AFS at year end, increasing the risk of misstatements.

• Instability in leadership, especially DG at the department and suspensions of key finance and

operational personnel also exasperated stability.

• Rigorous review of SCM legislation is required at DWS and WTE where deviations resulted on non-

compliance with SCM legislation. Also applicable to SCM by implementing agents.

• Budget processes and monitoring of cash flows should be improved.

• Effective controls over implementing agents should urgently be implemented and regularly

monitored.

Fir

st

leve

l

… the key role players as part of their role in combined assurance

Assurance providers per level

WRC / DWS / WTE

WRC

WRC

WRC

DWS / WTE

DWS / WTE WRC

DWS / WTE

DWS / WTE

Senior management

Accounting officer/authority

Executive authority

Internal audit unit

Audit committee

Portfolio committee T

hir

d

leve

l

Sec

on

d

leve

l

Basis for PC evaluation:

• Oversight role ito robust budget vote process, review of the annual report including the

audit report, quarterly reporting;

• Follow up on progress made by the entities to address poor audit outcomes;

• Recommendations made in relation to key audit matters; and

• Follow up on key matters reported in the committee’s prior year BRRR report.

The Portfolio committee performed the legislative oversight requirements and it robustly

engages the department on its role and mandate.

Senior management and accounting officer at both DWS & WTE did not provide the

necessary assurance as various lack internal controls resulted in unfavourable outcomes.

Controls around these areas were committed to be improved in the prior year.

Provides assurance

Provides some

assurance

Provides limited/ no assurance

Vacancy Not

established

5

Improved

Stagnant

Regressed

12

All

3

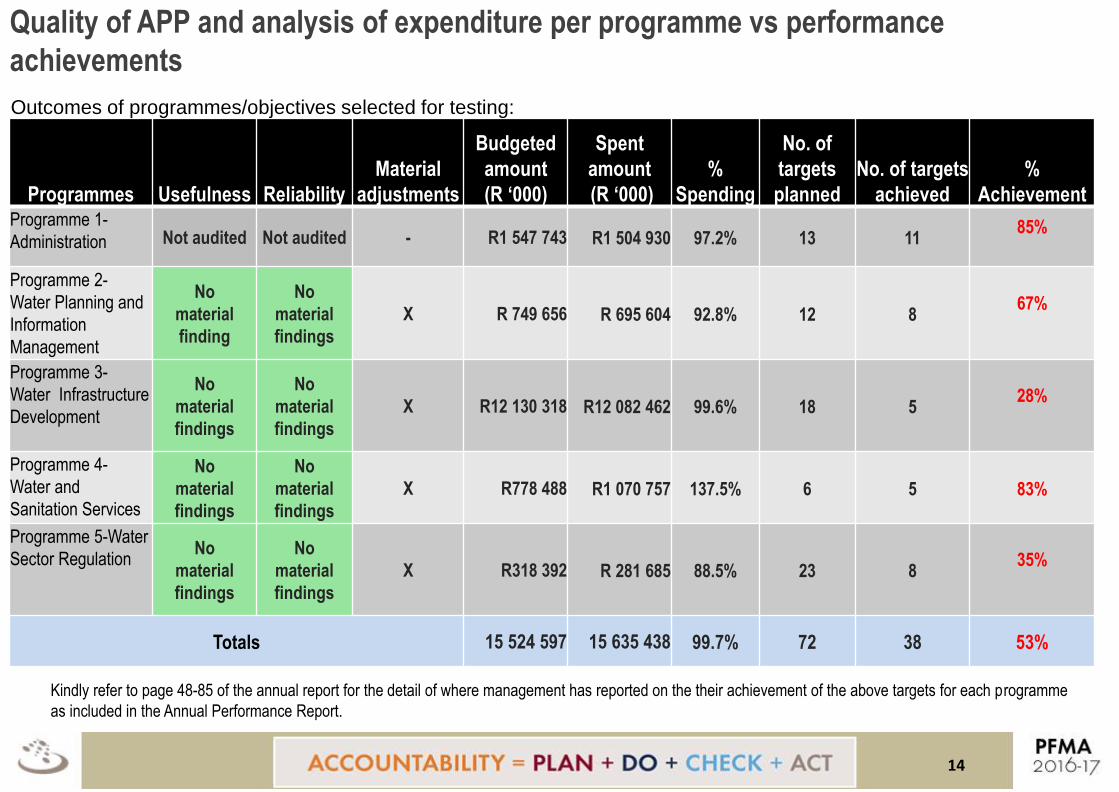

Performance management linked to programmes/ objectives tested & key projects audited

13

Programmes Usefulness Reliability

Material

adjustments

Budgeted

amount

(R ‘000)

Spent

amount

(R ‘000)

%

Spending

No. of

targets

planned

No. of targets

achieved

%

Achievement Programme 1-

Administration Not audited Not audited - R1 547 743 R1 504 930 97.2% 13 11 85%

Programme 2-

Water Planning and

Information

Management

No

material

finding

No

material

findings

X R 749 656 R 695 604 92.8% 12 8 67%

Programme 3-

Water Infrastructure

Development

No

material

findings

No

material

findings

X R12 130 318 R12 082 462 99.6% 18 5 28%

Programme 4-

Water and

Sanitation Services

No

material

findings

No

material

findings

X R778 488 R1 070 757 137.5% 6 5 83%

Programme 5-Water

Sector Regulation No

material

findings

No

material

findings

X R318 392 R 281 685 88.5% 23 8 35%

Totals 15 524 597 15 635 438 99.7% 72 38 53%

Quality of APP and analysis of expenditure per programme vs performance

achievements

14

Kindly refer to page 48-85 of the annual report for the detail of where management has reported on the their achievement of the above targets for each programme

as included in the Annual Performance Report.

Outcomes of programmes/objectives selected for testing:

15

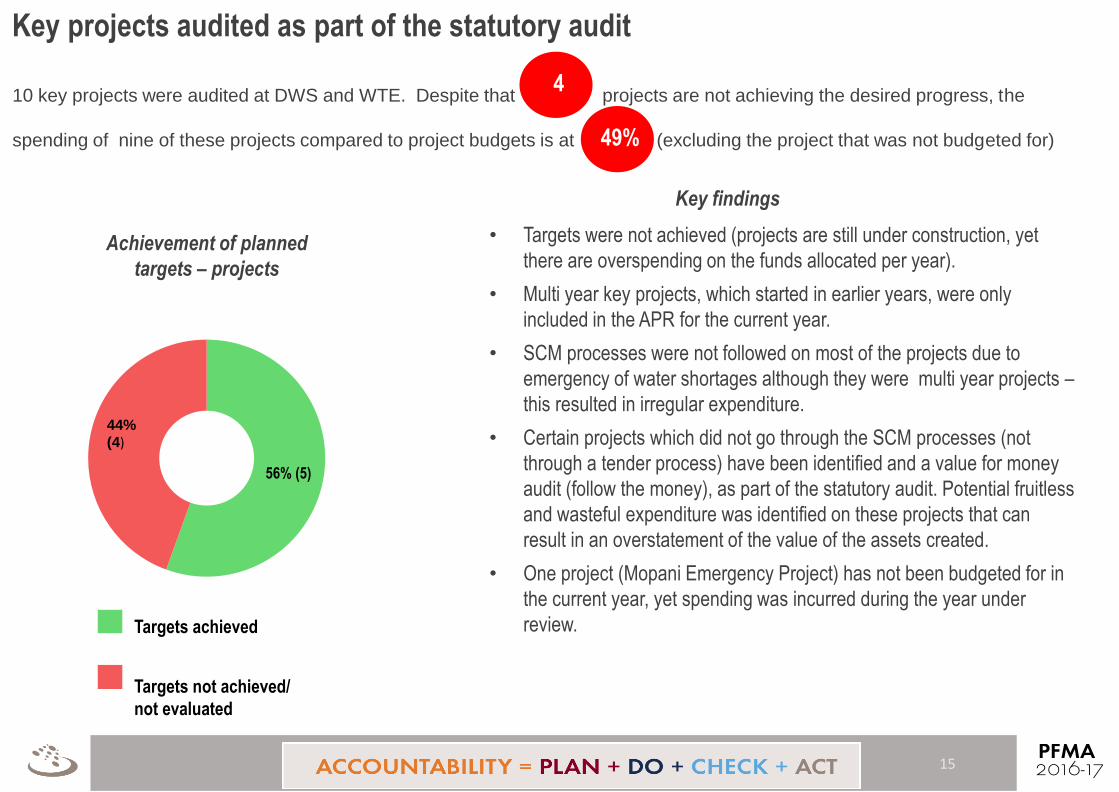

Key projects audited as part of the statutory audit

10 key projects were audited at DWS and WTE. Despite that projects are not achieving the desired progress, the

spending of nine of these projects compared to project budgets is at (excluding the project that was not budgeted for)

4

• Targets were not achieved (projects are still under construction, yet

there are overspending on the funds allocated per year).

• Multi year key projects, which started in earlier years, were only

included in the APR for the current year.

• SCM processes were not followed on most of the projects due to

emergency of water shortages although they were multi year projects –

this resulted in irregular expenditure.

• Certain projects which did not go through the SCM processes (not

through a tender process) have been identified and a value for money

audit (follow the money), as part of the statutory audit. Potential fruitless

and wasteful expenditure was identified on these projects that can

result in an overstatement of the value of the assets created.

• One project (Mopani Emergency Project) has not been budgeted for in

the current year, yet spending was incurred during the year under

review.

Achievement of planned

targets – projects

56% (5)

44%

(4)

Targets achieved

Targets not achieved/

not evaluated

Key findings

49%

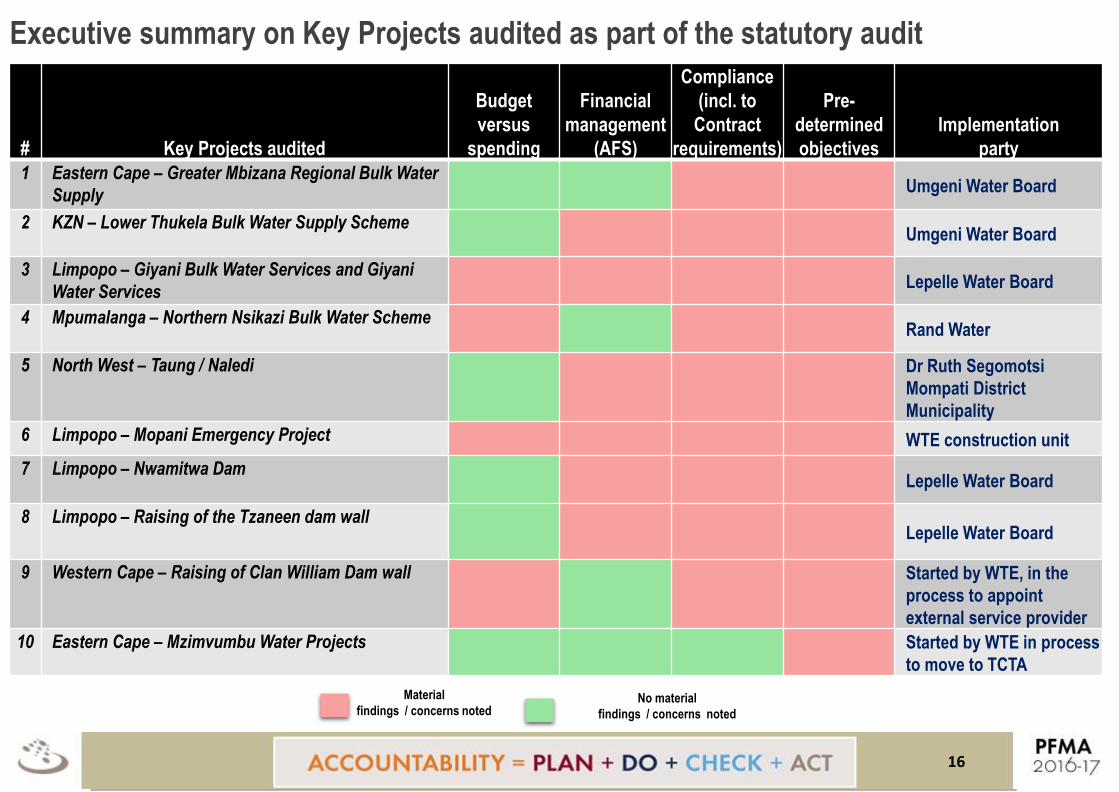

16

# Key Projects audited

Budget

versus

spending

Financial

management

(AFS)

Compliance

(incl. to

Contract

requirements)

Pre-

determined

objectives

Implementation

party

1 Eastern Cape – Greater Mbizana Regional Bulk Water

Supply Umgeni Water Board

2 KZN – Lower Thukela Bulk Water Supply Scheme Umgeni Water Board

3 Limpopo – Giyani Bulk Water Services and Giyani

Water Services Lepelle Water Board

4 Mpumalanga – Northern Nsikazi Bulk Water Scheme Rand Water

5 North West – Taung / Naledi Dr Ruth Segomotsi

Mompati District

Municipality

6 Limpopo – Mopani Emergency Project WTE construction unit

7 Limpopo – Nwamitwa Dam Lepelle Water Board

8 Limpopo – Raising of the Tzaneen dam wall Lepelle Water Board

9 Western Cape – Raising of Clan William Dam wall Started by WTE, in the

process to appoint

external service provider

10 Eastern Cape – Mzimvumbu Water Projects Started by WTE in process

to move to TCTA

Executive summary on Key Projects audited as part of the statutory audit

16

Material

findings / concerns noted No material

findings / concerns noted

4

Financial health and financial management

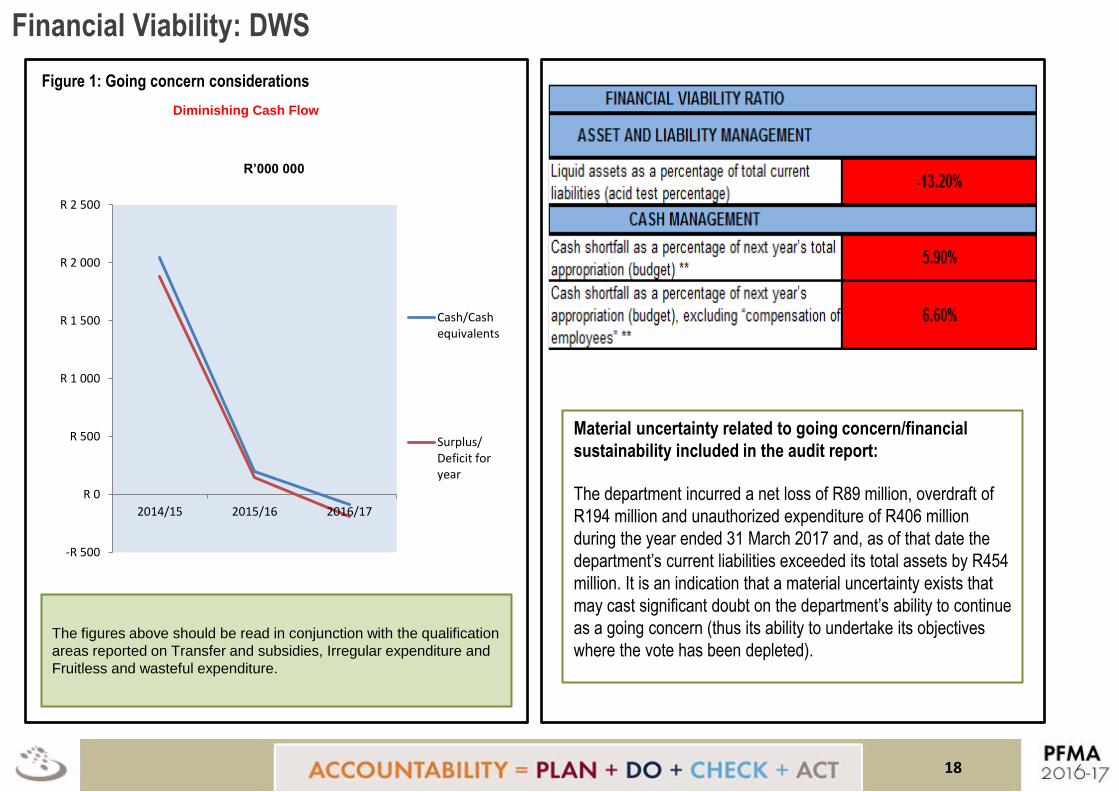

17

-R 500

R 0

R 500

R 1 000

R 1 500

R 2 000

R 2 500

2014/15 2015/16 2016/17

Cash/Cashequivalents

Surplus/Deficit foryear

R’000 000

Diminishing Cash Flow

Financial Viability: DWS

Figure 1: Going concern considerations

The figures above should be read in conjunction with the qualification

areas reported on Transfer and subsidies, Irregular expenditure and

Fruitless and wasteful expenditure.

Material uncertainty related to going concern/financial

sustainability included in the audit report:

The department incurred a net loss of R89 million, overdraft of

R194 million and unauthorized expenditure of R406 million

during the year ended 31 March 2017 and, as of that date the

department’s current liabilities exceeded its total assets by R454

million. It is an indication that a material uncertainty exists that

may cast significant doubt on the department’s ability to continue

as a going concern (thus its ability to undertake its objectives

where the vote has been depleted).

18

-R 4 000 000

-R 3 000 000

-R 2 000 000

-R 1 000 000

R 0

R 1 000 000

R 2 000 000

R 3 000 000

R 4 000 000

2014 2015 2016 2017

CashReserves

NetProfit/Loss

Financial Viability : WTE

The expenditure incurred moved closer to the revenue and in 16/17

FY exceeded revenue.

Figure 1: Going concern considerations

0

2 000 000 000

4 000 000 000

6 000 000 000

8 000 000 000

10 000 000 000

12 000 000 000

14 000 000 000

16 000 000 000

18 000 000 000

14/13 14/15 15/16 16/17

Revenue

Expenditure(InclEmployee comp)

Key financial health indicators The cash reserves are consistently diminishing over the years and

so are the profits. This is a strong indicator of going concern

challenges with a current year Overdraft of R2.186 billion (PY –R0)

19

Liquidity ratios Ratios

Current ratio 0.91

Current acid ratio 0.81

Component 2016-17 2015-16 Movement

Revenue R10 296 475 R9 494 713 8%

Total trade

Receivables R10 301 980 R8 415 301 22%

Provisions for

impairment R6 774 299 R4 717 762 44%

Payables R1 943 563 R1 168 507 66%

• A healthy current ratio is deemed at 2:1 and the entity’s ration is

less than one.

• Current acid ration should be 1:1 which is also less than one.

It thus indicates that the entity will experience significant challenges

in paying their current liabilities as and when they fall due. This

inability to pay results in increased accruals.

R’000

• The increase in receivables of 22% is not as a result of increase in

revenue/ business, but due to the inability of the entity to collect its

debt owed to it.

• The inability to collect monies due to it, resulted in a significant

impairment of receivables, as these are now deemed highly unlikely

to be recovered.

• Payables also increased drastically from the prior year with 66% as

the entity is not able to pay its short term liabilities as and when they

fall due.

• All these indicate highly unfavourable indicators of going concern .

67%

33% WRC

67%

33% WRC

DWS WTE

Figure 1: Findings on compliance with

key legislation – all auditees

2016-17 2015-16

Improvement in compliance with legislation and poor quality of financial statements

Prevention of unauthorised, irregular and/

or fruitless and wasteful expenditure

Management of procurement and/

or contracts

Consequence management

100% (3)

67% (DWS / WTE)

67% (DWS / WTE)

67% (DWS /WTE)

67% (DWS / WTE)

Material misstatements in submitted

annual financial statements

67% (DWS / WTE)

Figure 3: Auditees who avoided qualifications due to the correction of material misstatements

during the audit

Outcome if

NOT corrected

Outcome

after corrections

2016-17

With no material misstatements With material misstatements

-------------------------------------------------------------------------------------------------------------------------------------------------

Figure 2: Qualification areas over two years

Improved Stagnant Regressed

Fruitless

and

Wasteful

Irregular

expenditure Transfers

Fin

Liabilities

(TCTA) PPE

Accruals /

Commitmen

ts

Auditee

2016

-17

2015

-16

2016

-17

2015

-16

2016

-17

2015

-16

2016

-17

2015

-16

2016

-17

2015

-16

2016

-17

2015

-16

DWS X X X X

WTE X X X X X

DWS

WTE

20

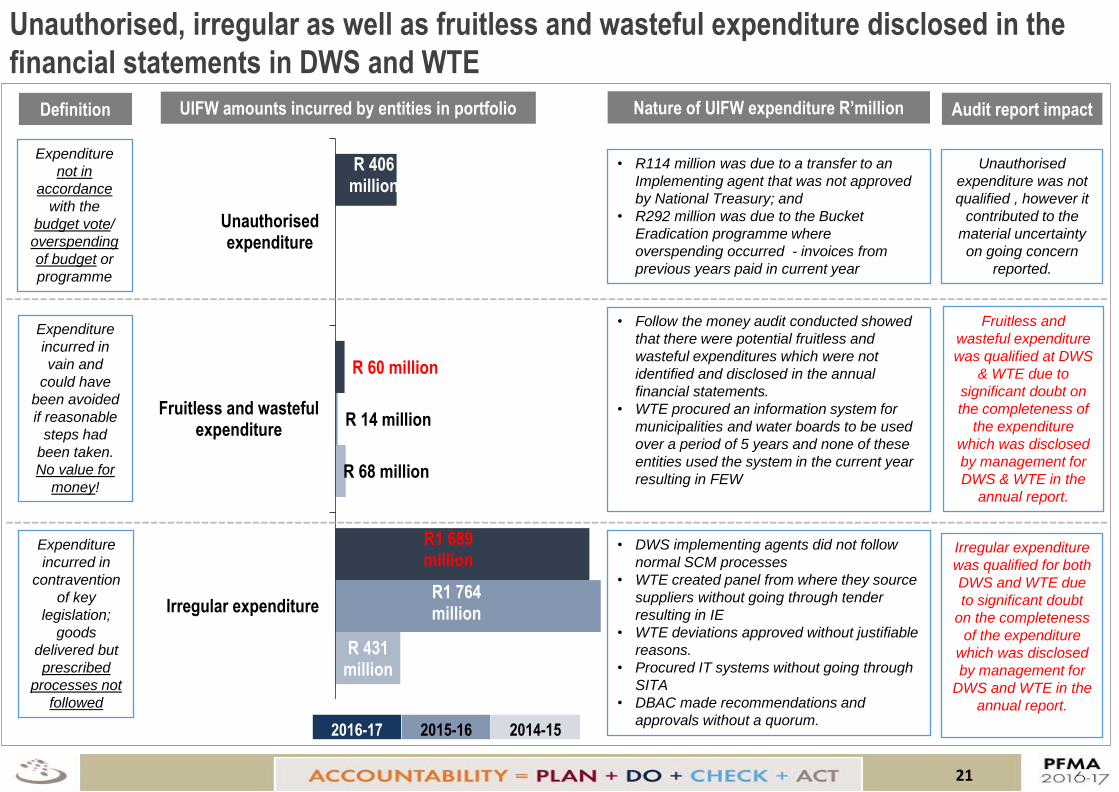

Unauthorised, irregular as well as fruitless and wasteful expenditure disclosed in the

financial statements in DWS and WTE 2016-17

PFMA

R 431 million

R 68 million

R1 764 million

R 14 million

R1 689 million

R 60 million

R 406 million

Irregular expenditure

Fruitless and wastefulexpenditure

Unauthorisedexpenditure

Expenditure

incurred in

contravention

of key

legislation;

goods

delivered but

prescribed

processes not

followed

Expenditure

not in

accordance

with the

budget vote/

overspending

of budget or

programme

Expenditure

incurred in

vain and

could have

been avoided

if reasonable

steps had

been taken.

No value for

money!

Definition UIFW amounts incurred by entities in portfolio Nature of UIFW expenditure R’million

2016-17 2015-16 2014-15

Appointment of the service provider bythe implementing Agent on an

emergency basis (IA - DWS), Possibleirregular due to overpayments of RBIG,MWIG and sanitation contracts, Other

DWS and WTE

Penalties and interest, Accomodation,transportation, standing time and

overpayment to suppliers

R114 million was due to a transfer to anImplenting agent that was not approvedby National Treasury and R292 million

was due to the Bucket Eradicationprogramme where overspending

occurred - invoices from previous yearspaid in current year

• R114 million was due to a transfer to an

Implementing agent that was not approved

by National Treasury; and

• R292 million was due to the Bucket

Eradication programme where

overspending occurred - invoices from

previous years paid in current year

• Follow the money audit conducted showed

that there were potential fruitless and

wasteful expenditures which were not

identified and disclosed in the annual

financial statements.

• WTE procured an information system for

municipalities and water boards to be used

over a period of 5 years and none of these

entities used the system in the current year

resulting in FEW

• DWS implementing agents did not follow

normal SCM processes

• WTE created panel from where they source

suppliers without going through tender

resulting in IE

• WTE deviations approved without justifiable

reasons.

• Procured IT systems without going through

SITA

• DBAC made recommendations and

approvals without a quorum.

Audit report impact

Unauthorised

expenditure was not

qualified , however it

contributed to the

material uncertainty

on going concern

reported.

Fruitless and

wasteful expenditure

was qualified at DWS

& WTE due to

significant doubt on

the completeness of

the expenditure

which was disclosed

by management for

DWS & WTE in the

annual report.

Irregular expenditure

was qualified for both

DWS and WTE due

to significant doubt

on the completeness

of the expenditure

which was disclosed

by management for

DWS and WTE in the

annual report.

21

----------------------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------------------

22

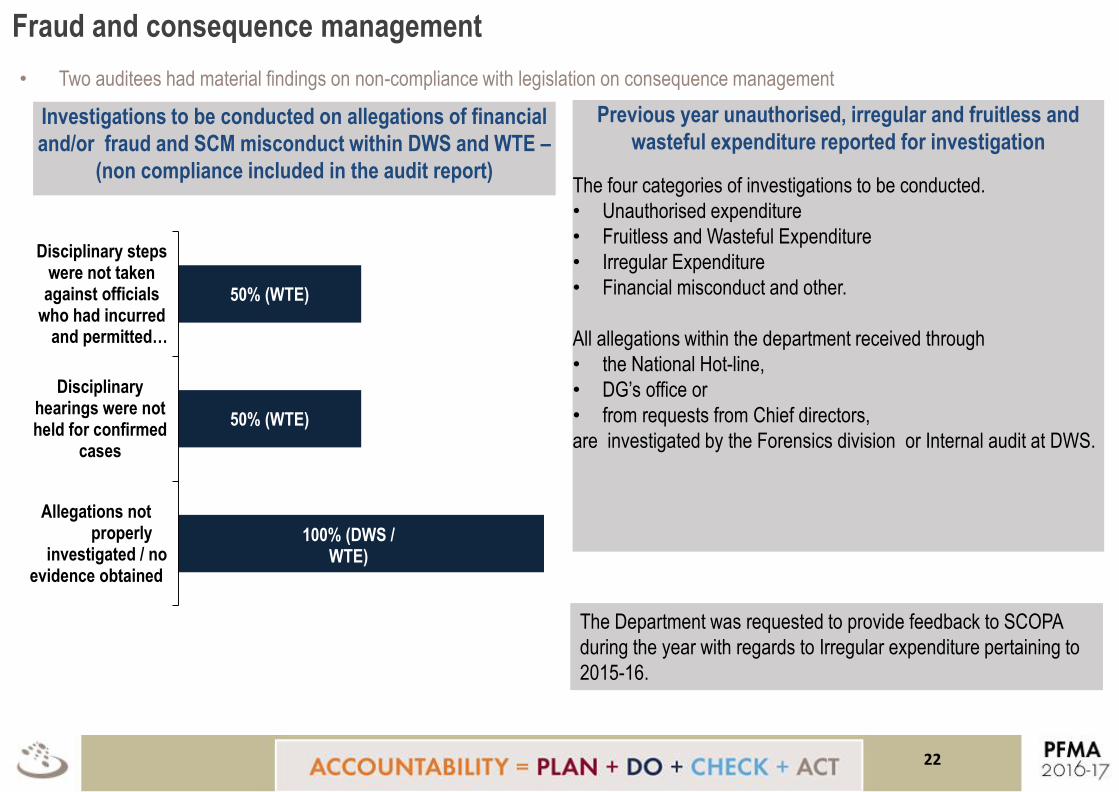

Fraud and consequence management

Investigations to be conducted on allegations of financial

and/or fraud and SCM misconduct within DWS and WTE –

(non compliance included in the audit report)

50% (WTE)

50% (WTE)

100% (DWS / WTE)

Disciplinary stepswere not takenagainst officials

who had incurredand permitted…

Disciplinaryhearings were notheld for confirmed

cases

Allegations not properly

investigated / noevidence obtained

Previous year unauthorised, irregular and fruitless and

wasteful expenditure reported for investigation

The four categories of investigations to be conducted.

• Unauthorised expenditure

• Fruitless and Wasteful Expenditure

• Irregular Expenditure

• Financial misconduct and other.

All allegations within the department received through

• the National Hot-line,

• DG’s office or

• from requests from Chief directors,

are investigated by the Forensics division or Internal audit at DWS.

• Two auditees had material findings on non-compliance with legislation on consequence management

The Department was requested to provide feedback to SCOPA

during the year with regards to Irregular expenditure pertaining to

2015-16.

22

5

Top four root causes, follow up on commitments and proposed

recommendations

23

… the following root causes must be addressed …

Slow response by management (Accounting officer

and senior management)

Lack of consequences for poor performance and

transgressions

Instability or vacancies

in key positions

To strengthen the internal controls with reference to implementing agents.

Status of key commitments by minister

To establish a structure in the department to incorporate the

sanitation function.

To take ownership/ control over all processes within the department.

To strengthen the internal controls within the department, especially around accruals, commitments (disclosure notes)

and irregular expenditure.

Implemented In progress Not implemented New

… through honouring the following commitments made by the executive authority……

2 1

The focus risk assessment will be discussed by top management and monitored by the audit committee.

67% (2)

67% (2)

67% (2)

67% (2)

67% (2)

67% (2)

2016-17 2015-16

Instability in leadership with specific reference to the Director General position

Insufficient policies and procedures relating to implementing agents

Insufficient oversight control over decisions taken by one division that affect

another division.

Insufficient control of budget processes

Management did not ensure adequate record keeping at all times

• We met with the minister on 26 July 2016. The outcomes were

discussed with the minister and the slow progress of the

implementation of the above commitments were followed up with

the minister.

• New commitments were solicited from the minister in the prior year

and certain of the prior year’s commitments were reinforced and

are to be tracked quarterly by the minister and feedback provided

during our quarterly engagements .

2016-17 PFMA

Top four root causes, follow up on commitments and proposed recommendations … and implementation of the following

proposed recommendations to the PC.

1. PC must request management

to provide feedback on the

implementation and progress

and of the action plans to

address poor audit outcomes

during quarterly reporting.

2. PC must request management

to provide quarterly feedback on

status of key controls,

especially around project

management/ payments on key

projects implemented by

implementing agents.

3. PC must be request quarterly

feedback on the progress of

filling vacancies at DWS.

4. List of action taken against

transgressors must be provided

quarterly to PC for follow up for

all irregular and fruitless and

wasteful expenditure incurred.

5. PC must request feedback on

actions implemented to improve

the financial health, budget

management and control and

turnaround plans/ interventions.

3

24

67% (2)

Officials did not act in the best interest of the auditee

in managing the financial and performance affairs of

the entity

24

DWS WTE

DWS WTE

DWS WTE

DWS WRC

DWS WTE

DWS WTE

DWS WTE

Root Causes

6

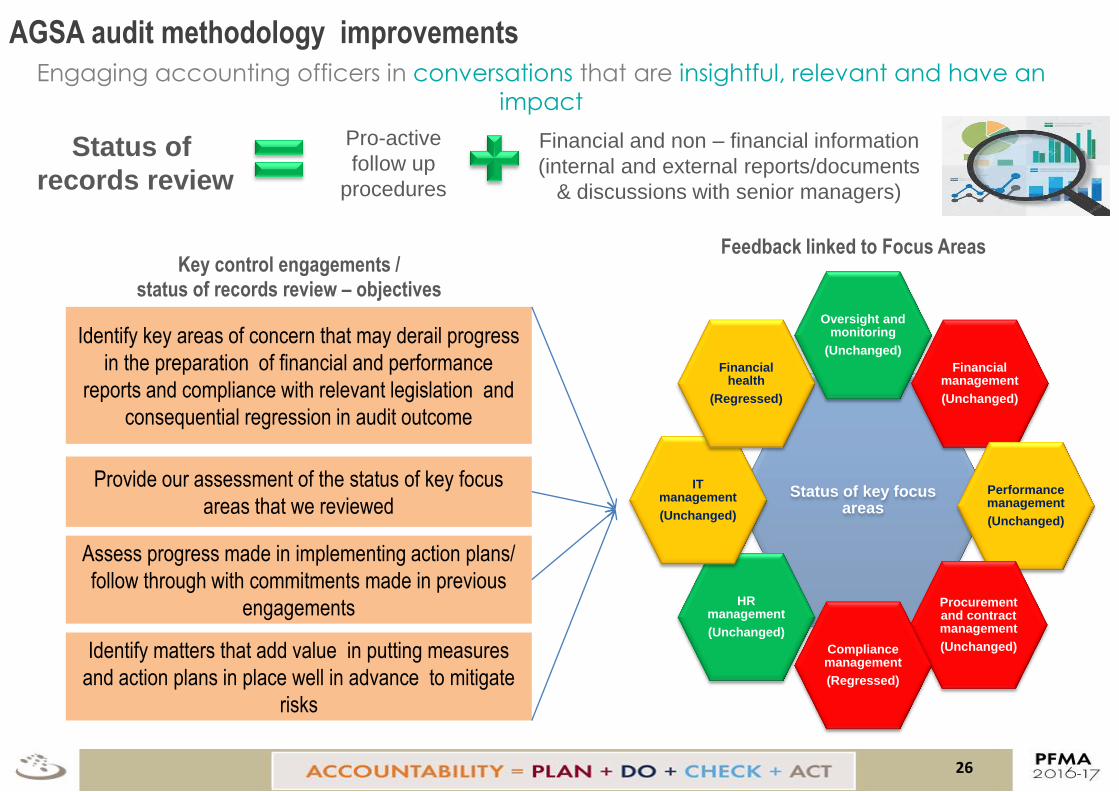

AGSA audit methodology improvements

25

Status of key focus areas

Oversight and monitoring

(Unchanged)

Financial management

(Unchanged)

Performance management

(Unchanged)

Procurement and contract management

(Unchanged) Compliance management

(Regressed)

HR management

(Unchanged)

IT management

(Unchanged)

Financial health

(Regressed)

Status of

records review

Pro-active

follow up

procedures

Financial and non – financial information

(internal and external reports/documents

& discussions with senior managers)

Feedback linked to Focus Areas

AGSA audit methodology improvements

Engaging accounting officers in conversations that are insightful, relevant and have an

impact

Identify matters that add value in putting measures

and action plans in place well in advance to mitigate

risks

Assess progress made in implementing action plans/

follow through with commitments made in previous

engagements

Provide our assessment of the status of key focus

areas that we reviewed

Identify key areas of concern that may derail progress

in the preparation of financial and performance

reports and compliance with relevant legislation and

consequential regression in audit outcome

Key control engagements / status of records review – objectives

26

26

27

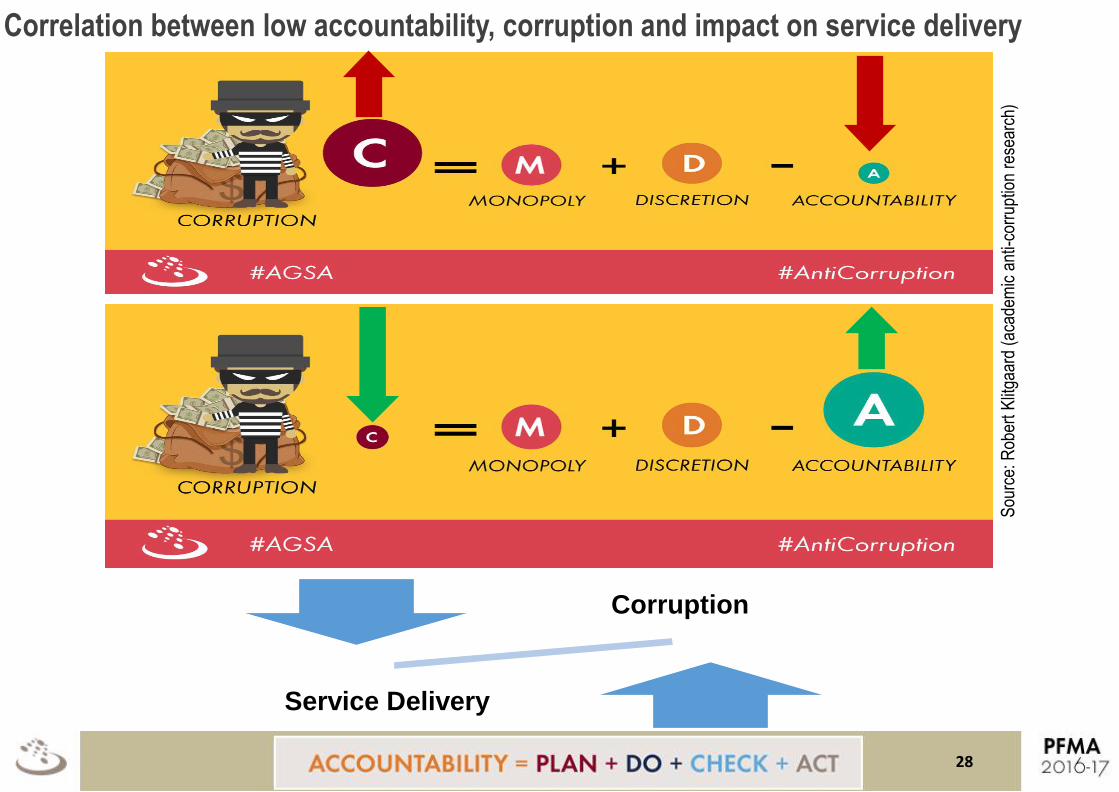

AGSA audit methodology improvements (cont.)

27

28

Sou

rce:

Rob

ert K

litga

ard

(aca

dem

ic a

nti-c

orru

ptio

n re

sear

ch)

Correlation between low accountability, corruption and impact on service delivery

Corruption

Service Delivery

28

29

Stay in touch with the AGSA

29

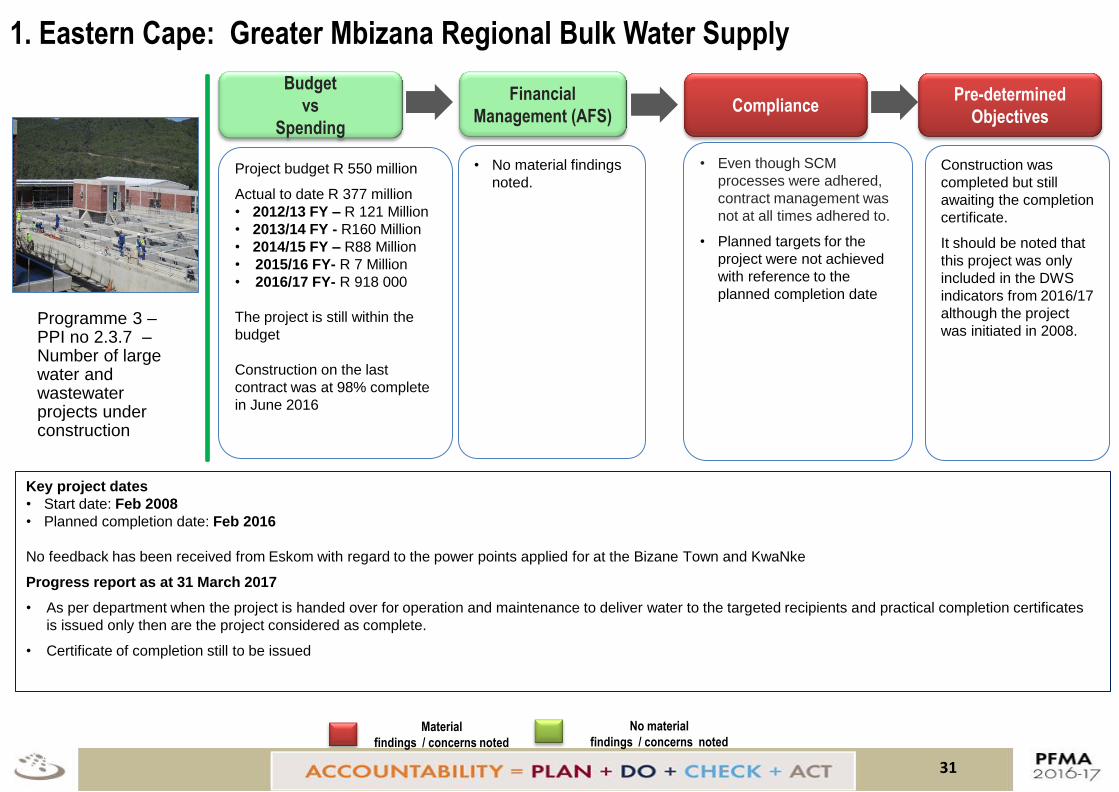

7 Annexure – Detail of key projects

30

1. Eastern Cape: Greater Mbizana Regional Bulk Water Supply

2016-17 PFMA No material

findings reported

Project budget R 550 million

Actual to date R 377 million

• 2012/13 FY – R 121 Million

• 2013/14 FY - R160 Million

• 2014/15 FY – R88 Million

• 2015/16 FY- R 7 Million

• 2016/17 FY- R 918 000

The project is still within the

budget

Construction on the last

contract was at 98% complete

in June 2016

• No material findings

noted.

• Even though SCM

processes were adhered,

contract management was

not at all times adhered to.

• Planned targets for the

project were not achieved

with reference to the

planned completion date

Construction was

completed but still

awaiting the completion

certificate.

It should be noted that

this project was only

included in the DWS

indicators from 2016/17

although the project

was initiated in 2008.

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: Feb 2008

• Planned completion date: Feb 2016

No feedback has been received from Eskom with regard to the power points applied for at the Bizane Town and KwaNke

Progress report as at 31 March 2017

• As per department when the project is handed over for operation and maintenance to deliver water to the targeted recipients and practical completion certificates

is issued only then are the project considered as complete.

• Certificate of completion still to be issued

Programme 3 – PPI no 2.3.7 – Number of large water and wastewater projects under construction

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

31

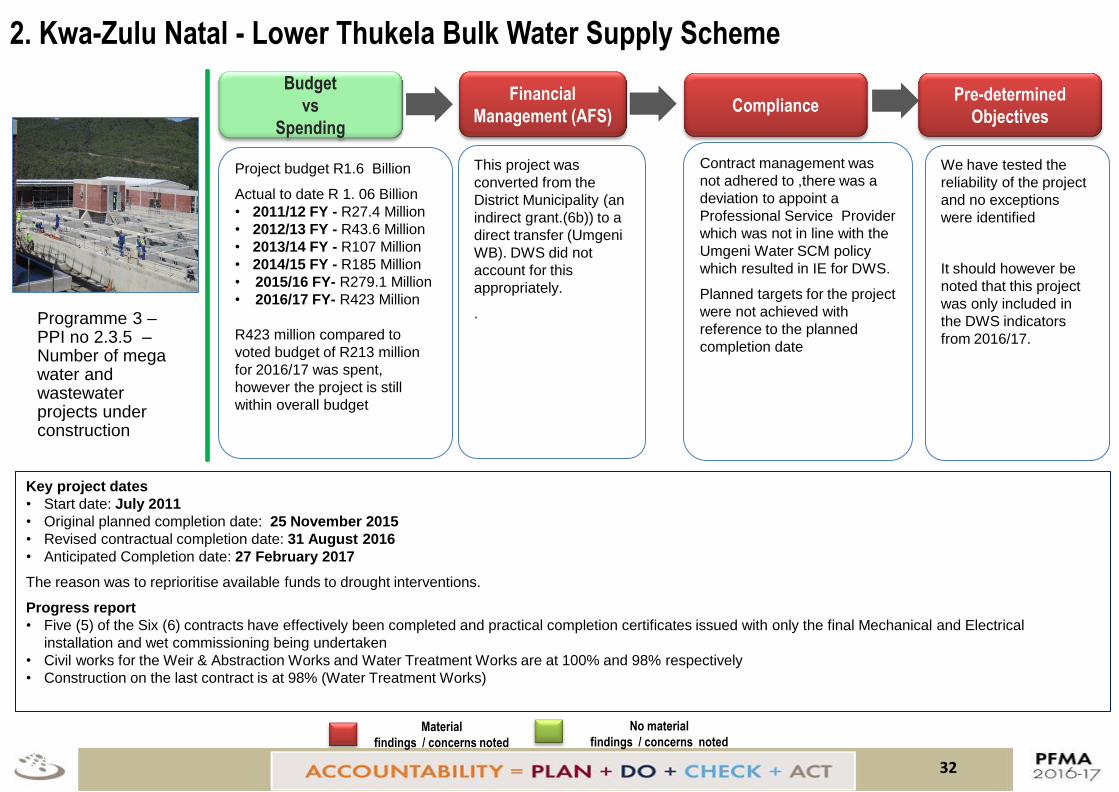

2. Kwa-Zulu Natal - Lower Thukela Bulk Water Supply Scheme

2016-17 PFMA No material

findings reported

Project budget R1.6 Billion

Actual to date R 1. 06 Billion

• 2011/12 FY - R27.4 Million

• 2012/13 FY - R43.6 Million

• 2013/14 FY - R107 Million

• 2014/15 FY - R185 Million

• 2015/16 FY- R279.1 Million

• 2016/17 FY- R423 Million

R423 million compared to

voted budget of R213 million

for 2016/17 was spent,

however the project is still

within overall budget

This project was

converted from the

District Municipality (an

indirect grant.(6b)) to a

direct transfer (Umgeni

WB). DWS did not

account for this

appropriately.

.

Contract management was

not adhered to ,there was a

deviation to appoint a

Professional Service Provider

which was not in line with the

Umgeni Water SCM policy

which resulted in IE for DWS.

Planned targets for the project

were not achieved with

reference to the planned

completion date

We have tested the

reliability of the project

and no exceptions

were identified

It should however be

noted that this project

was only included in

the DWS indicators

from 2016/17.

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: July 2011

• Original planned completion date: 25 November 2015

• Revised contractual completion date: 31 August 2016

• Anticipated Completion date: 27 February 2017

The reason was to reprioritise available funds to drought interventions.

Progress report

• Five (5) of the Six (6) contracts have effectively been completed and practical completion certificates issued with only the final Mechanical and Electrical

installation and wet commissioning being undertaken

• Civil works for the Weir & Abstraction Works and Water Treatment Works are at 100% and 98% respectively

• Construction on the last contract is at 98% (Water Treatment Works)

Programme 3 – PPI no 2.3.5 – Number of mega water and wastewater projects under construction

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

32

3. Limpopo - Giyani Bulk Water Services and Giyani Water Services

2016-17 PFMA No material

findings reported

• Project budget was revised

from 2.5 Billion to 2.8 Billion

as per IA

• Actual expenditure to date

R 2.5 billion

• 2016/17 Actual expenditure

R915 million compared to

voted budget of R750

million

• The new business plan

refers to project totalling in

excess of R10 billion

Fruitless and Wasteful

expenditure will result in

the value of the asset

being overstated

Possible receivable to

refund overcharging of

management fees

In previous year identified as

irregular expenditure due to

the basis of an emergency

Lack of contract management

on these projects,

irregularities were identified.

Scope of work changed

significantly from inception of

the project. No industry

recognised from of contract

between IA and contractor.

CIDB guidelines not followed

No signed contracts between

DWS and the implementing

agent

The reliability of the

project was tested and

there were no

exceptions identified

It should be noted that

this project was only

included in the DWS

indicators from

2016/17.

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: 28 August 2014 as an emergency intervention to restore water supply in Giyani – this was completed

• Initial completion date: September 2014

• Project expected completion date: during 2018/19 financial year as per new business plan

Progress report

• The initial emergency – restoring of the water supply was achieved. The subsequent objectives to serve the entire

Mopani District has not yet been achieved.

Value for money audit

As part of the audit an assessment of the value for money received on this project was conducted. There is estimated amounts for Fruitless and Wasteful expenditure

identified during the audit that can potentially result in the value of the asset being overstated. The following areas have been identified where the department may

have overpaid on this project.

• Project management fees & double invoices paid (double counting of professional hours)

• Excessive professional fees (rates) & excessive construction rates

The recommendation to the department is to stop the project and conduct a full investigation to determine the actual fruitless and wasteful expenditure on this project

Programme 3 – PPI no 2.3.5 – Number of mega water and wastewater projects under construction

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

33

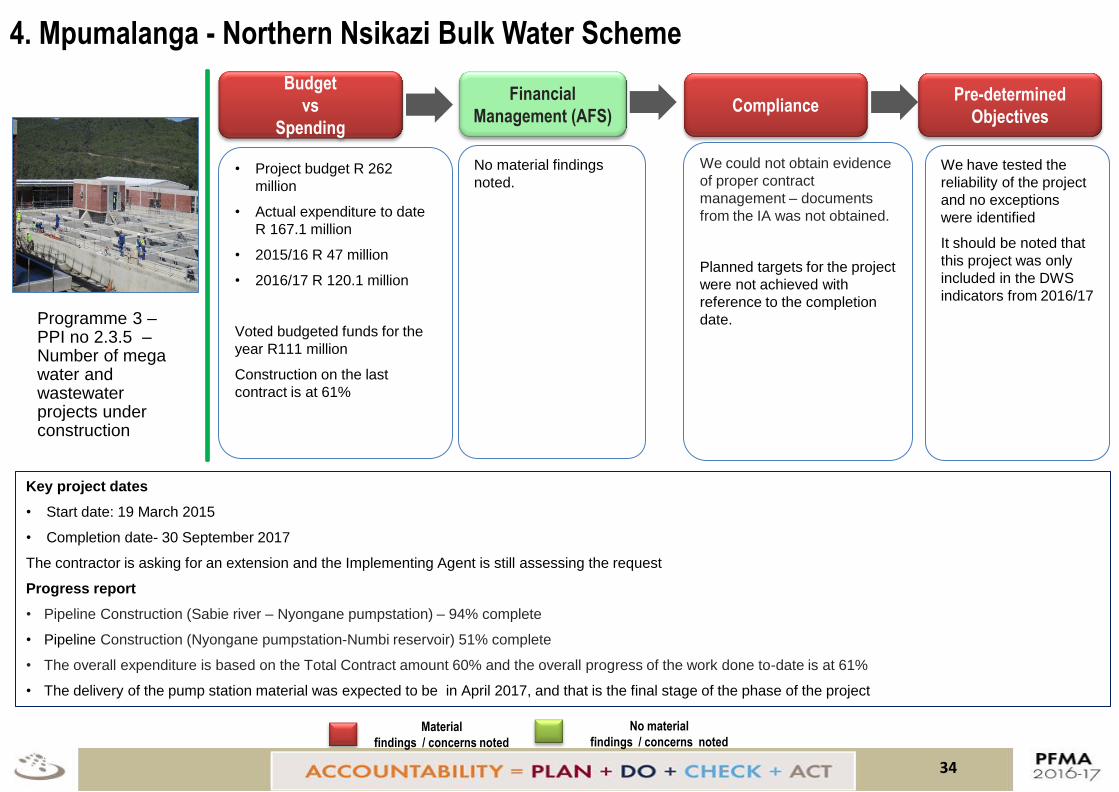

4. Mpumalanga - Northern Nsikazi Bulk Water Scheme

2016-17 PFMA No material

findings reported

• Project budget R 262

million

• Actual expenditure to date

R 167.1 million

• 2015/16 R 47 million

• 2016/17 R 120.1 million

Voted budgeted funds for the

year R111 million

Construction on the last

contract is at 61%

No material findings

noted.

We could not obtain evidence

of proper contract

management – documents

from the IA was not obtained.

Planned targets for the project

were not achieved with

reference to the completion

date.

We have tested the

reliability of the project

and no exceptions

were identified

It should be noted that

this project was only

included in the DWS

indicators from 2016/17

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: 19 March 2015

• Completion date- 30 September 2017

The contractor is asking for an extension and the Implementing Agent is still assessing the request

Progress report

• Pipeline Construction (Sabie river – Nyongane pumpstation) – 94% complete

• Pipeline Construction (Nyongane pumpstation-Numbi reservoir) 51% complete

• The overall expenditure is based on the Total Contract amount 60% and the overall progress of the work done to-date is at 61%

• The delivery of the pump station material was expected to be in April 2017, and that is the final stage of the phase of the project

Programme 3 – PPI no 2.3.5 – Number of mega water and wastewater projects under construction

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

34

5. North West - Taung / Naledi

2016-17 PFMA No material

findings reported

• Project budget R 390

million

• Actual to date R 358.1

Million

• 2013/14 R 97.6 million vs

R 95.4 million

• 2014/15 R 112 million vs

R112 million

• 2015/16 R 63.7 million vs R

63.7 million

• 2016/17 R 77 million vs 64

million

Various phases of the project

are still under construction

This project was

converted from an

indirect grant.(6b) to a

direct transfer. Due to

the fact that the project

was initiated by the

department, the risks

and responsibilities are

still at DWS and not the

municipality which

resulted in the

qualification on the

audit report

As this was a conversion from

6B to 5B, contract

management was not fully

adhere to due to this

conversion

Planned targets for the project

were not achieved with

reference to the anticipated

completion date – reasons

detailed below

Reliability on the

project was performed

and no exception was

identified

It should be noted that

this project was only

included in the DWS

indicators from 2016/17

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: for phases 1 to 2D: 2009-

• Original planned completion date: 2016

• Anticipated Completion date: Unknown and for phase 2(D) – August 2017

Due to unrest protest and changes of scope the original planned completion date was not achieved. In additional the Traditional Authority is in negotiations with the

department due to bordering his land and claiming compensation – this also affected the completion date

Progress report

• Phase 1 to Phase 2B completed

• Phase 2C - Progress of the Works is at 99% complete with only the Roof Slab to construct and Hydrolic Pipes to install at the Abstraction Point.

• Phase 2D- Under construction

• Project phase 2(E)(1) – Pre- procurement stage (currently)

• Phase 2F- Future

Programme 3 – PPI no 2.3.7 – Number of large water and wastewater projects under construction

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

35

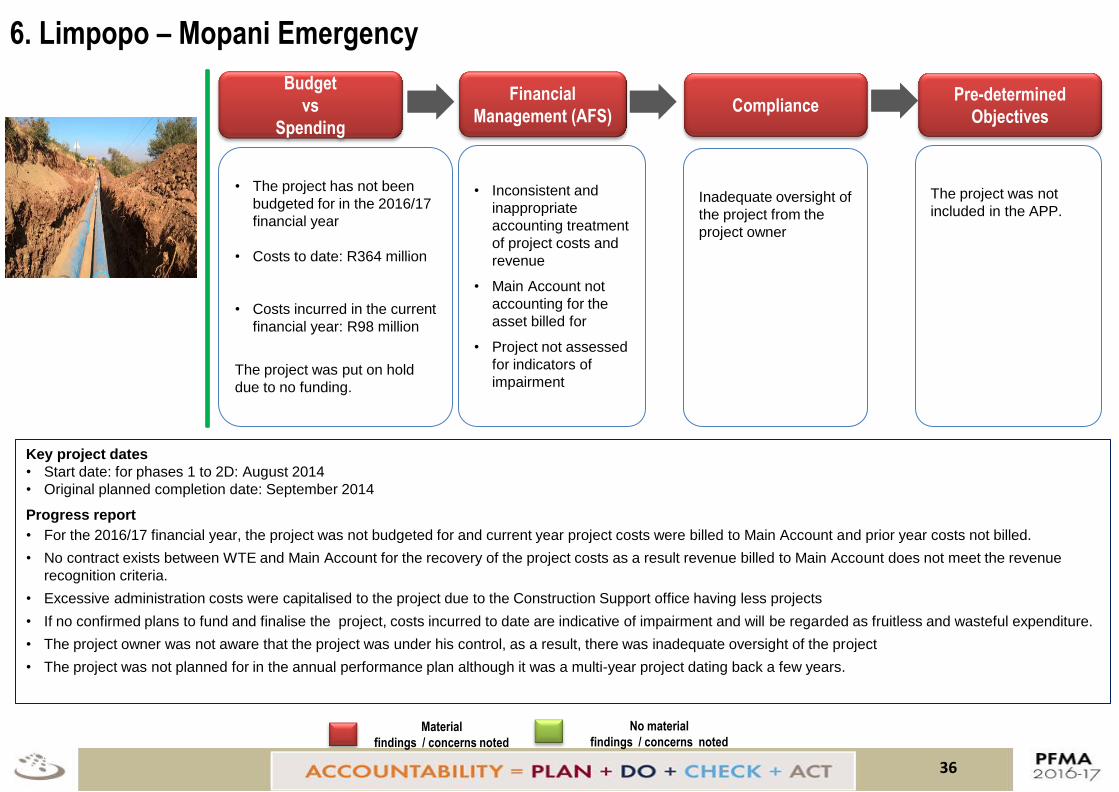

6. Limpopo – Mopani Emergency

2016-17 PFMA No material

findings reported

• The project has not been

budgeted for in the 2016/17

financial year

• Costs to date: R364 million

• Costs incurred in the current

financial year: R98 million

The project was put on hold

due to no funding.

• Inconsistent and

inappropriate

accounting treatment

of project costs and

revenue

• Main Account not

accounting for the

asset billed for

• Project not assessed

for indicators of

impairment

Inadequate oversight of

the project from the

project owner

The project was not

included in the APP.

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: for phases 1 to 2D: August 2014

• Original planned completion date: September 2014

Progress report

• For the 2016/17 financial year, the project was not budgeted for and current year project costs were billed to Main Account and prior year costs not billed.

• No contract exists between WTE and Main Account for the recovery of the project costs as a result revenue billed to Main Account does not meet the revenue

recognition criteria.

• Excessive administration costs were capitalised to the project due to the Construction Support office having less projects

• If no confirmed plans to fund and finalise the project, costs incurred to date are indicative of impairment and will be regarded as fruitless and wasteful expenditure.

• The project owner was not aware that the project was under his control, as a result, there was inadequate oversight of the project

• The project was not planned for in the annual performance plan although it was a multi-year project dating back a few years.

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

36

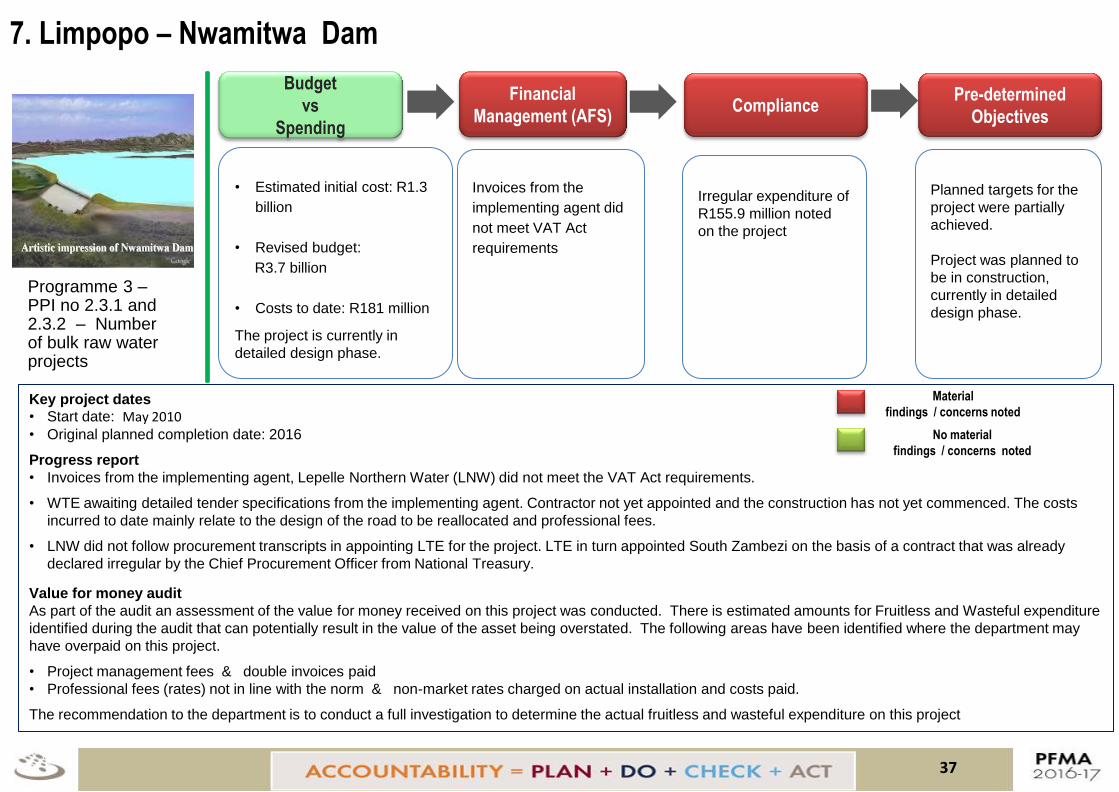

7. Limpopo – Nwamitwa Dam

2016-17 PFMA No material

findings reported

• Estimated initial cost: R1.3

billion

• Revised budget:

R3.7 billion

• Costs to date: R181 million

The project is currently in

detailed design phase.

Invoices from the

implementing agent did

not meet VAT Act

requirements

Irregular expenditure of

R155.9 million noted

on the project

Planned targets for the

project were partially

achieved.

Project was planned to

be in construction,

currently in detailed

design phase.

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: May 2010

• Original planned completion date: 2016

Progress report

• Invoices from the implementing agent, Lepelle Northern Water (LNW) did not meet the VAT Act requirements.

• WTE awaiting detailed tender specifications from the implementing agent. Contractor not yet appointed and the construction has not yet commenced. The costs

incurred to date mainly relate to the design of the road to be reallocated and professional fees.

• LNW did not follow procurement transcripts in appointing LTE for the project. LTE in turn appointed South Zambezi on the basis of a contract that was already

declared irregular by the Chief Procurement Officer from National Treasury.

Value for money audit

As part of the audit an assessment of the value for money received on this project was conducted. There is estimated amounts for Fruitless and Wasteful expenditure

identified during the audit that can potentially result in the value of the asset being overstated. The following areas have been identified where the department may

have overpaid on this project.

• Project management fees & double invoices paid

• Professional fees (rates) not in line with the norm & non-market rates charged on actual installation and costs paid.

The recommendation to the department is to conduct a full investigation to determine the actual fruitless and wasteful expenditure on this project

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

37

Programme 3 – PPI no 2.3.1 and 2.3.2 – Number of bulk raw water projects

8. Limpopo – Raising of the Tzaneen dam wall

2016-17 PFMA No material

findings reported

Irregular expenditure

of R43.6 million noted

on the project

Planned targets for the

project were partially

achieved.

Project was planned to

have appointed

contractor, currently in

tender documentation

phase.

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: 2010

• Original planned completion date: 2016

Progress report

• Invoices from the implementing agent Lepelle Northern Water (LNW) did not meet the VAT Act requirements.

• The costs incurred to date relate to detailed dam designs and earthworks stock piling

• Appointment of Blackhead Consulting was approved as a deviation from normal tender process. The reason for deviation was not justifiable as the project was not

an emergency, thus resulting in irregular expenditure.

Value for money audit

As part of the audit an assessment of the value for money received on this project was conducted. There is estimated amounts for Fruitless and Wasteful expenditure

identified during the audit that can potentially result in the value of the asset being overstated. The following areas have been identified where the department may

have overpaid on this project.

• Project management fees & double invoices paid

• Professional fees (rates) not in line with the norm & non-market rates charged on actual installation and costs paid.

The recommendation to the department is to conduct a full investigation to determine the actual fruitless and wasteful expenditure on this project

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

38

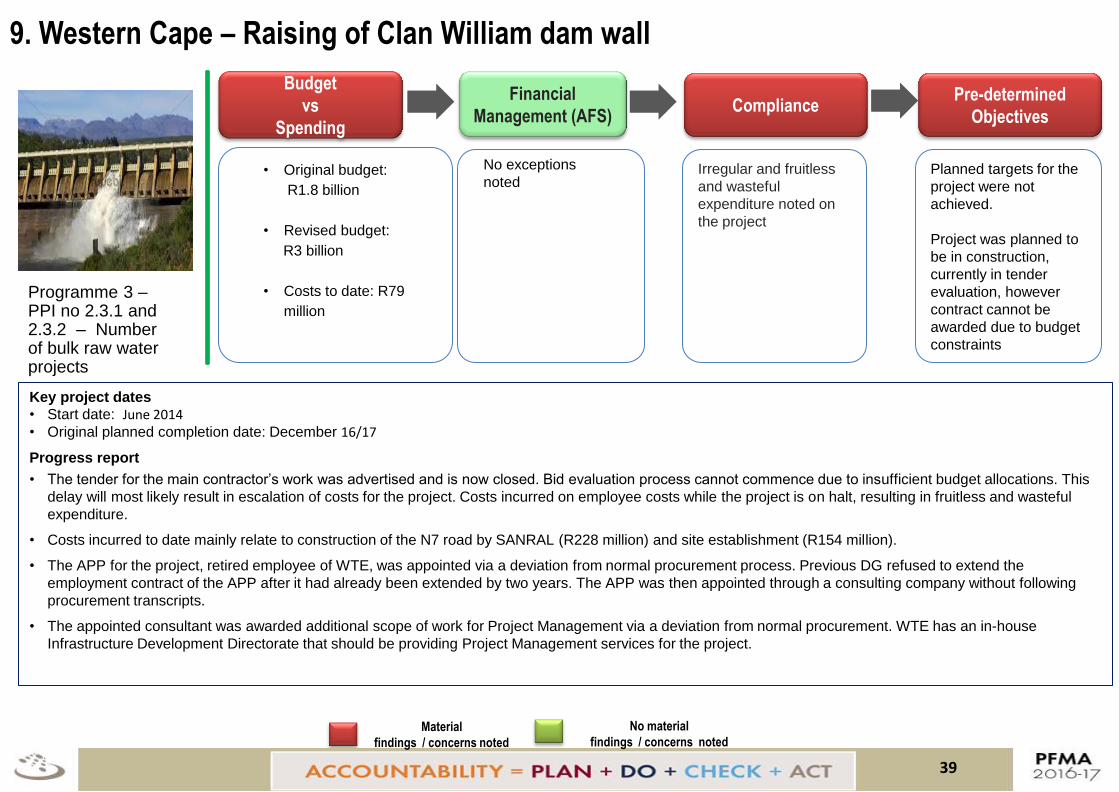

Programme 3 – PPI no 2.3.1 – Number of bulk raw water projects

• Original budget:

R88 million

• Revised budget:

R173 million

• Costs to date: R63

million

Invoices from the

implementing agent

did not meet VAT

Act requirements.

9. Western Cape – Raising of Clan William dam wall

2016-17 PFMA No material

findings reported

Irregular and fruitless

and wasteful

expenditure noted on

the project

Planned targets for the

project were not

achieved.

Project was planned to

be in construction,

currently in tender

evaluation, however

contract cannot be

awarded due to budget

constraints

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date: June 2014

• Original planned completion date: December 16/17

Progress report

• The tender for the main contractor’s work was advertised and is now closed. Bid evaluation process cannot commence due to insufficient budget allocations. This

delay will most likely result in escalation of costs for the project. Costs incurred on employee costs while the project is on halt, resulting in fruitless and wasteful

expenditure.

• Costs incurred to date mainly relate to construction of the N7 road by SANRAL (R228 million) and site establishment (R154 million).

• The APP for the project, retired employee of WTE, was appointed via a deviation from normal procurement process. Previous DG refused to extend the

employment contract of the APP after it had already been extended by two years. The APP was then appointed through a consulting company without following

procurement transcripts.

• The appointed consultant was awarded additional scope of work for Project Management via a deviation from normal procurement. WTE has an in-house

Infrastructure Development Directorate that should be providing Project Management services for the project.

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

39

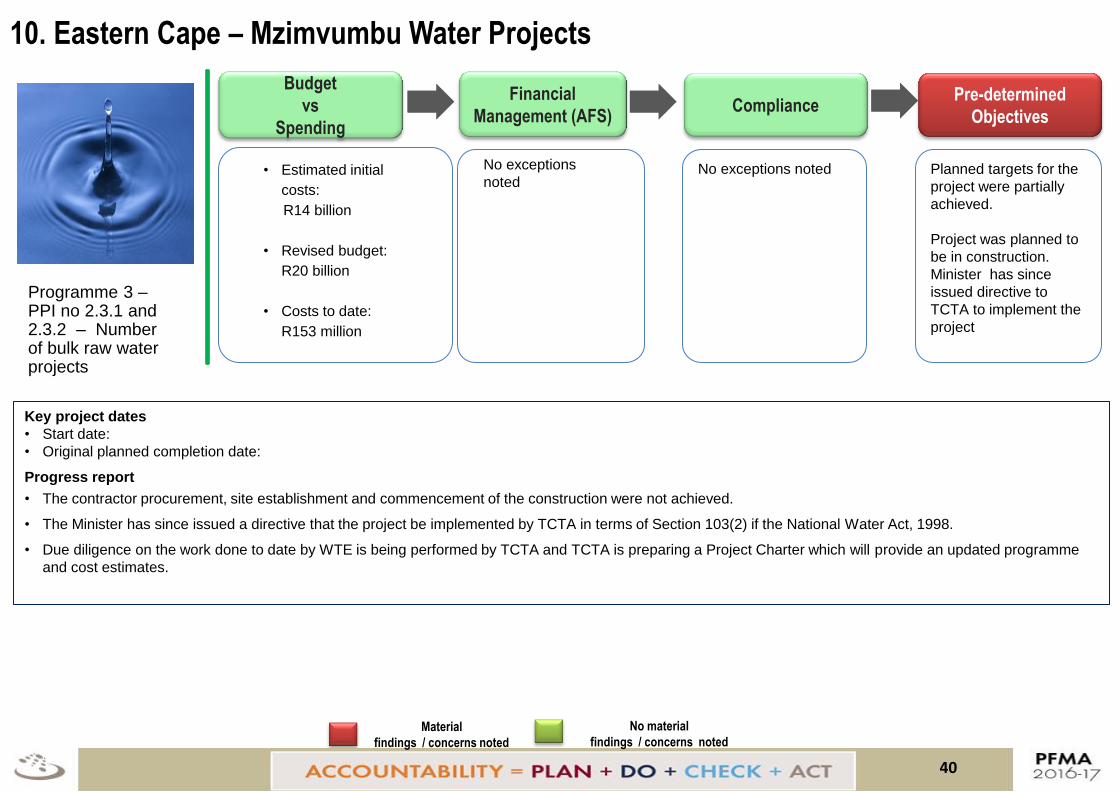

Programme 3 – PPI no 2.3.1 and 2.3.2 – Number of bulk raw water projects

• Original budget:

R1.8 billion

• Revised budget:

R3 billion

• Costs to date: R79

million

No exceptions

noted

10. Eastern Cape – Mzimvumbu Water Projects

2016-17 PFMA No material

findings reported

No exceptions noted

Planned targets for the

project were partially

achieved.

Project was planned to

be in construction.

Minister has since

issued directive to

TCTA to implement the

project

Budget

vs

Spending

Financial

Management (AFS)

Key project dates

• Start date:

• Original planned completion date:

Progress report

• The contractor procurement, site establishment and commencement of the construction were not achieved.

• The Minister has since issued a directive that the project be implemented by TCTA in terms of Section 103(2) if the National Water Act, 1998.

• Due diligence on the work done to date by WTE is being performed by TCTA and TCTA is preparing a Project Charter which will provide an updated programme

and cost estimates.

Compliance Pre-determined

Objectives

Material

findings reported

Material

findings / concerns noted

No material

findings / concerns noted

40

Programme 3 – PPI no 2.3.1 and 2.3.2 – Number of bulk raw water projects

• Estimated initial

costs:

R14 billion

• Revised budget:

R20 billion

• Costs to date:

R153 million

No exceptions

noted