Bryan dow inside3 dp conference ny - mooreland presentation apr 2015

34

CONFIDENTIAL 3D Print Me an Investment Banker M&A and Financing Trends in 3D Printing Bryan Dow Executive Director, Investment Banking April 16, 2015

-

Upload

mecklermedia -

Category

Documents

-

view

59 -

download

0

Transcript of Bryan dow inside3 dp conference ny - mooreland presentation apr 2015

CONFIDENTIAL

3D Print Me an Investment Banker M&A and Financing Trends in 3D Printing

Bryan Dow Executive Director, Investment Banking April 16, 2015

CONFIDENTIAL

Senior member of Mooreland Partners Industrial Technology Group spearheading 3D Printing efforts

Advise companies in mergers, acquisitions, sales and raising growth capital

Based in Silicon Valley

Over 10 years of investment banking experience

– Previously Head of the Clean Energy and Industrial Technology Investment Banking Group at ThinkEquity

– Prior to ThinkEquity, member of the Technology Investment Banking Group at Needham & Company

– Completed over 50 transactions BS from the Leavey School of Business at Santa Clara

University

Bryan Dow Executive Director Investment Banking

2

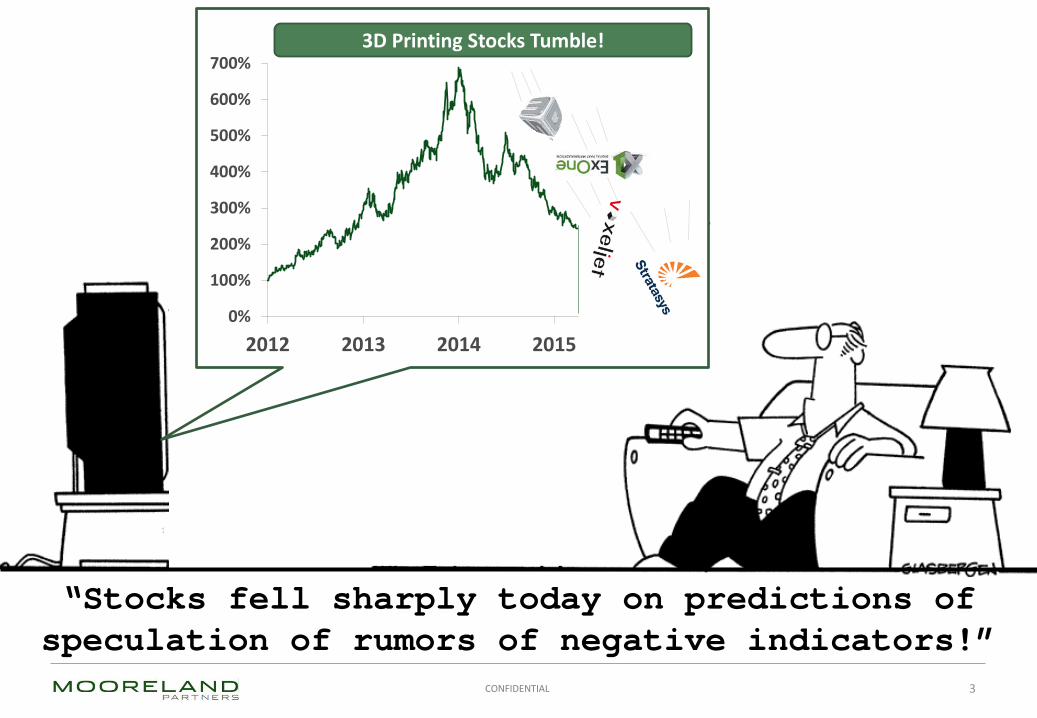

CONFIDENTIAL 3

0%

100%

200%

300%

400%

500%

600%

700%

2012 2013 2014 2015

3D Printing Stocks Tumble!

“Stocks fell sharply today on predictions of speculation of rumors of negative indicators!”

CONFIDENTIAL

3D Printing Market Overview

M&A Trends

Financing Trends

Public Markets and Valuations

Conclusion

Agenda

4

3D Printing Market Overview

CONFIDENTIAL

Mooreland 3D Printing Universe: Systems and Service Bureaus

Production (End-Use)

Serv

ice

Bure

aus

Prin

ter M

anuf

actu

rers

Co

mbo

*

Production/ Professional

Professional (Prototypes/Models)

Professional/ Personal

Personal (Hobbyist Products)

Production

Source: Mooreland Partners. *Combo companies act as both service bureaus and 3D printer manufacturers.

/ /

6

Production

/

/

/

Production

/

/

/ / /

Production

/

CONFIDENTIAL

Mooreland 3D Printing Universe: Applications and Enablement

Source: Mooreland Partners.

/ /

7

/

Other

Software

CAD Tools & Services

Freeform Modeling Tools /

Sculpting Tools

Applications 3D Scanners Components / Materials

/

/

/

CONFIDENTIAL

From 2011 to today, 3D Printing companies have raised close to $4Bn in public offerings vs. ~$300M raised in the 23 years from 1987 to 2010

In 2013 the level of venture capital investments into 3D printing tripled from 2012

Annual industrial printer purchases has increased nearly 19x since 19951

# of companies exploding in recent years…

History of 3D Printing

# 3D Printing Companies Over Time (that we know of)

Systems Sold in 19951

Systems Sold in 20141

1) Source: Wohler’s 2014

~9,832 systems sold ($1.1Bn)

525 systems ($124K)

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

Maker- Jet 3D!

3

41

93

200-600

1985 1995 2005 2014

8

CONFIDENTIAL

Selected Recent Market Developments

9

HP Multi Jet FusionTM (Oct. 2014)

Ricoh RapidFab (Sep. 2014)

Arburg FreeFormer (Oct. 2014)

Alcoa Acquires RTI (Mar. 2015)

Out of Segment Leaders Building Additive Capabilities

CONFIDENTIAL

Selected Recent Market Developments (cont’d)

10

CLIP Technology (Mar. 2015)

3D Printed Electronics

Highly-Discussed Technology Advances

CONFIDENTIAL

Selected Recent Market Developments (cont’d)

11

Ongoing Advanced Around Human Body Applications

Key M&A Trends

CONFIDENTIAL

32

18

12

7

11

6

3

2015YTD201420132012201120102009

Selected Recent Noteworthy Transactions

2011 2012 2013 2014 2015

Deal volume accelerating – 2015 deal activity on pace to be

the most active – Yet, some 3D Printing companies

curtailing acquisition binge, so need for new players to backfill

Deal size increasing in recent years

– Handful of landmark transactions in last 2 years

– All 6 deals with value at or above $100M taken place after Nov. 2011

Stratasys and 3D Systems continue to be the most active acquirers in the space by far…

– … However, as more 3D Printing companies accessing public financing and larger companies enter the sector, new acquirers are emerging

3D Printing Deal Volume Since 2009 3D Printing M&A by Type Since 2009

Source: CapitalIQ and Mooreland Partners. 1) Annualized as of April 2015

13

1

Systems Manufacturer

Service Bureau

Software

Other

2015 Annualized Deal Count

CONFIDENTIAL

Who’s Buying??

`` # Deals (88 total) 62 14 4 3 2 2 1

# Deals YTD 2 2 1 - - - -

Cash on B/S $285 $443 $74 $37 $36 $60 $74

Types of Deals

Professional Equipment

Hobbyist Equipment

Service Bureaus

Software, etc.

Applications

Potential Out-of-Industry Buyers

Cash # Deals since 2012 M&A $’s Spent in 2014

Aggregate Values $194,763 573 $42,783

Leading 3D Printing Industry Participants

Source: Capital IQ as of April 2015.

$ values in millions

$ values in millions

14

Presenter

Presentation Notes

$2.6 Billion in disclosed M&A from 3DP companies

CONFIDENTIAL

11.0x

5.9x 5.7x 5.5x

4.5x 4.5x 4.2x 3.9x 3.3x 3.1x 2.9x

2.4x 1.6x

0.9x

1 2 3 4 5 6 7 8 9 10 11 12 13 14

3D Printing M&A Valuations and Common Deal Structures

Source: Capital IQ, 451 Group, company reporting and Mooreland estimates.

Transaction structure is a key variable in 3D Printing M&A negations While many deals have published very high revenue multiples, transactions are often financed by richly valued stock vs. cash,

which may involve a significant lock up period and market risk of the shares Many deals also include a variety of contingency payments

– Earn-outs based on future performance – Incentive payments to retain key executives – Future payments contingent upon achieving certain integration goals

Select 3D Printing M&A Valuations: EV / LTM Revenue

(AP&C Division)

Median: 3.9x LTM Rev

Cash Stock Contingencies

15

CONFIDENTIAL

Key Themes Observed in 3D Printing M&A

/

Aggressive service bureau acquisition, largely by equipment makers, as well as other service bureaus

Particularly active since Jan 2014 – 11 acquired

/ / / /

Notes Noteworthy Consolidations

Acquisition of specific capabilities such as mobile accessories, prosthetics, jewelry etc.

Likely area for future out-of-industry buyers (e.g. GE /Morris)

/

/ / Majority of 3DP deals (DDD & SSYS land grab)

While DDD has executed 5x the number of deals, SSYS has led a number of market defining transactions (e.g. MakerBot, Solid Concepts)

/ /

/ / /

Most commonly equipment manufacturers adding software to extend capabilities around managing scanned images

/

/

/

/

/

Expanding Service Bureau Platforms

Market Consolidation

Ancillary Capabilities

Application Specific

Acquisitions

/ / /

16

/

/ / /

/

Financing Trends

CONFIDENTIAL

Tech Generalist VCs Formulated Strategy

Recently Active (1+) in

the Space

Recently Invested in the

Space

Private Investors in 3D Printing

Selected Current 3D Printing Investors

Explicit Strategy Around 3D Printing

Source: Mooreland Partners.

18

Strategic Investors in 3D Printing

CONFIDENTIAL

Selected Venture Capital Investors and Portfolio Companies

Investor Targets Global 3D printing market grew 68% in 2014, generating $3.3B in revenue and interest from major tech investors

Source: Mooreland Partners and Venture Beat

19

CONFIDENTIAL

Crowdfunding Successes

Name Campaign End Amount Raised

TIKO 3D Mar 15 $1.7M+

BoXZY Mar 15 $862K+

M3D LLC May 14 $2.9m+

Full Spectrum Laser Feb 14/ Sep 12 $1M+

3Doodler Jan 14 $2.3M+

Pirate 3DP Jun 13 $1.4M

While traditional VCs continue to invest in the 3D Printing space, start-ups have also found great success from crowdfunding platforms, such as Kickstarter and Indiegogo

Source: Manufacturing Disruption, Kickstarter, Indiegogo and Mooreland Partners (As of April 2015).

20

Year # Campaigns

2012 18

2013 61

2014 68

2015YTD 25

Total Since 2012 157

Avg. $ Raised $178K

3DP Crowdfunding Deals since 2012 Selected 3DP Campaigns

CONFIDENTIAL

Who Has Raised Outside Capital?

Funded Crowd Funded Selected Bootstrapped Vast majority (>90%) of 3D Printing companies are still self-funded

Source: Mooreland Partners.

21

CONFIDENTIAL

Investment Themes: VC’s Recently Interested in Applications and Enablement More Than Systems and Services Application-focused companies starting to attract Venture Capital investment above systems manufacturers and service bureaus

22

Applications

Combining basic scanning technologies with 3D printing to offer custom fit products

Great expectations surrounding penetration of additive into orthopedic and custom molded medical equipment

Software, Scanners and Design Enablement

Some investors view equipment as potentially moving towards commodity, focused on lean business models that enable pro-sumer 3D printing

Investment interest in enabling technologies that accelerate adoption of 3D printing in a scalable software or e-commerce business model

Public Markets & Valuations

CONFIDENTIAL

~1.3x

8.3x

2.1x

~1.2x

14.3x 14.9x 14.8x

5.7x

$20M

$2M

$99M

$17M $29M

$14M

$30M

$99M

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$0

$2

$4

$6

$8

$10

$12

$14

$16

1 2 3 4 5 6 7 8

EV / Rev

LTM Rev

LTM Revenue and Valuation Multiples of IPOs

1987 1994 2012 2013 2014 1) 3D Systems multiple based on earliest available financials in September 2001; assumes Net Debt = 0 2) Arcam values from Nasdaq OMX relisting in 2012; previously traded on Nordic Growth Market

24

CONFIDENTIAL

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

DDD SSYS XONE PRLB VJET SLM ARCM MATLS ARCW

Total Public Fundraisings

Source: Capital IQ. Excludes commercial debt and working capital lines.

Follow-on Offerings IPOs $4B+

Raised

25

$ values in thousands

CONFIDENTIAL

-100%

0%

100%

200%

300%

400%

500%

600%

2012 2013 2014 20153D Printing Index Russell 2000 NASDAQ

Aggregate Public Stock Performance Since 2012 Since 2012, 3D Printing stocks have outperformed the Nasdaq by more than 2-to-1, despite severe correction in stock prices since early 2014

26

Feb‘12 IPO

Jun‘12 IPO

Feb‘13 IPO

Oct‘13 IPO

May‘13 IPO

Jun‘13 IPO

+145% since

Jan. 12

-20% YTD

Source: Capital IQ, as of April 2, 2015.

CONFIDENTIAL 27

Public Markets Commentary: Continued Multiple Compression

Source: Capital IQ, as of April 2015

38.9x

8.9x

2.3x 1.9x

(5.0x)

-

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

40.0x

Dec-13 Feb-14 Apr-14 Jun-14 Aug-14 Oct-14 Dec-14 Feb-15 Apr-15

Month End EV / Revenue LTM Multiples

-43%

Group High Multiple

Group Low Multiple Median Multiple

CONFIDENTIAL

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

28

SSYS and DDD NTM EV/Revenue has averaged 6.4x and 7.5x respectively over the last two years; now trading at 2.6x and 3.4x, respectively

Key drivers: underperforming Street expectations, company lowering guidance

Public Markets Commentary: Fundamental Market Factors

Source: Capital IQ, as of April 2015

Earnings Miss

Earnings & Organic Growth Miss

HP MultiJet

Street Analyst Lowers Earnings Estimate

Lowers Profit Forecast

-59% since

Jan. 14

CONFIDENTIAL 29

DDD and SSYS shares have also been pressured by speculative short sellers

Rising popularity of retail investors and hedge funds selling against “bubbles”

Since Jan. 1, 2014, the percentage of DDD and SSYS shares outstanding that have been sold short has increased 120% and 427% respectively

DDD is the 19th most heavily shorted stock on the NYSE1

Public Markets Commentary: Market Factors – Trading

Source: Capital IQ, as of April 2015 1) By short interest as a percentage of float

0%

5%

10%

15%

20%

25%

30%

35%

% S

/0 S

old

Shor

t

DDD - Short Interest as % of S/OSSYS - Short Interest as % of S/O

35%

21%

Comments % of S/O Sold Short Over Time

CONFIDENTIAL

7.3x

4.7x 4.7x 4.0x

3.5x 3.1x 2.6x 2.4x 1.6x

PRLB SLM DDD ARCM XONE SSYS VJET MTLS ARCW

9.2x

7.2x 6.7x

5.7x 4.5x

3.9x 3.4x

2.7x 1.8x

PRLB ARCM SLM VJET DDD XONE SSYS MTLS ARCW

Today’s 3D Printing Public Markets Valuations

Source: Capital IQ, as of April 13, 2015.

CY2015 Revenue Multiples

CY2014 Revenue Multiples

Median: 3.5x 2015P Rev

Median: 4.5x 2014A Rev

30

Presenter

Presentation Notes

11.1x

Conclusion

CONFIDENTIAL

Valuations will continue to become more reasonable – Not necessarily by further declining stock prices, but companies growing into their valuations that

investors ascribe

Strategic and VC private investments to continue to ramp, but slowly – Strategics already developing strategies at the BU level, but this takes time to trickle down – VCs are more cautious in hardware investments in this environment; into capital light models

Limited IPO activity as certain “public ready” companies are waiting for the comp group to bounce back – Will provide more choices for public investors, which is good for the index – Increases buyer universe driving further M&A

More consolidation by existing players – Continued “land grab” for market share and defense reasons – Economies of scale and technical advancements are increasing quality and bringing costs down

Large conglomerates and 2D printer companies to enter via M&A – They have been on the sidelines for too long, starting to enter (i.e. HP, Arburg, etc.) – As the market becomes more established with customer qualifications, necessary market opportunity

will exist

What We Expect…

32

CONFIDENTIAL

Bryan G. Dow Executive Director

950 Tower Lane, Suite 1950 Foster City, CA 94404 tel: +1 (650) 330-3788 [email protected]

Mooreland Partners LLC is a member of FINRA / SIPC

33

SILICON VALLEY 950 Tower Lane, Suite 1950

Foster City, CA 94404 Tel: +1 (650) 330-3790

GREENWICH 537 Steamboat Road, Suite 200

Greenwich, CT 06830 Tel: +1 (203) 629-4400

LONDON 2-4 King Street,

London SW1Y 6QL Tel: +44 (0) 20 7484 1350

www.moorelandpartners.com