Brazil, Russia, India, China Future Automotive Giants (Brazil, Russia, India, China) Future...

26

BRICs (Brazil, Russia, India, China) Future Automotive Giants Tim Armstrong Associate Director, Eastern Europe & Middle East and Africa

Transcript of Brazil, Russia, India, China Future Automotive Giants (Brazil, Russia, India, China) Future...

BRICs(Brazil, Russia, India, China)Future Automotive Giants

Tim ArmstrongAssociate Director, Eastern Europe & Middle East and Africa

Copyright © 2006 Global Insight, Inc. 22006 GLOBAL AUTOMOTIVE CONFERENCE

• Sources of growth in the world– Where do BRICs fit ?

• BRICs market facts and growth potential

• Positioning to access the BRICs markets– bodystyle, segment, and pricing

• World car projects

• Aspects of production

• Summary

Presentation Outline

Copyright © 2006 Global Insight, Inc. 32006 GLOBAL AUTOMOTIVE CONFERENCE

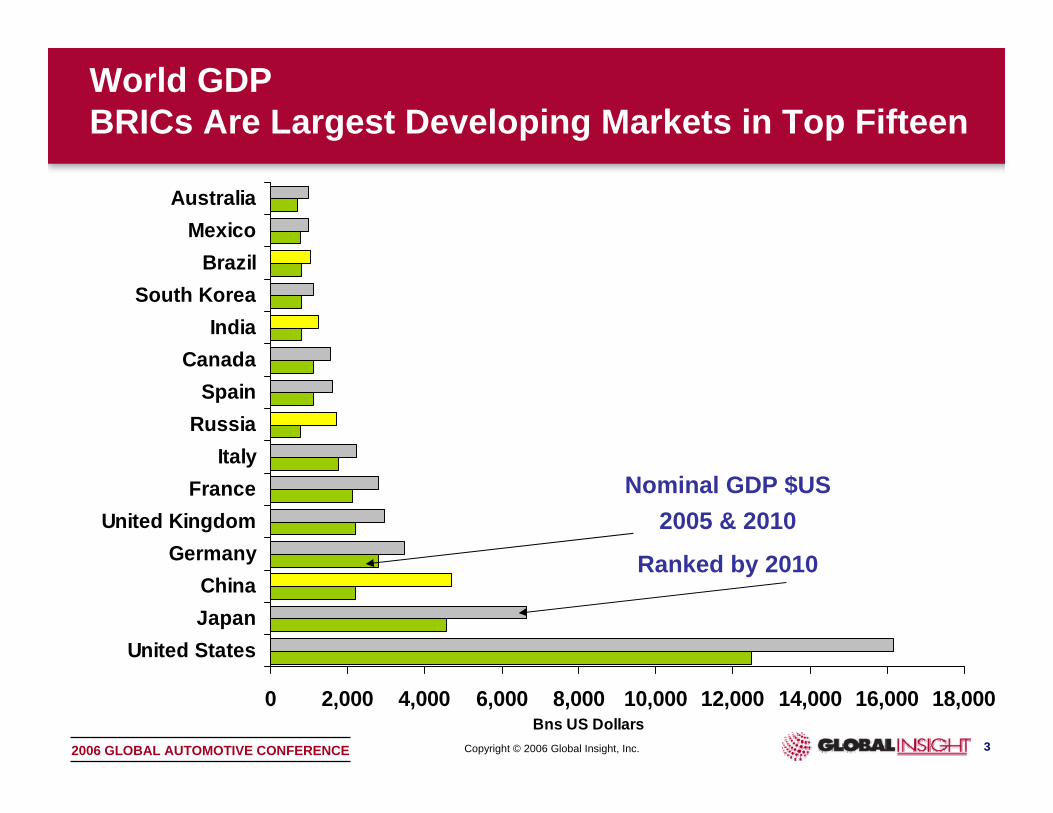

World GDP BRICs Are Largest Developing Markets in Top Fifteen

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000

United StatesJapanChina

GermanyUnited Kingdom

FranceItaly

RussiaSpain

CanadaIndia

South KoreaBrazil

MexicoAustralia

Bns US Dollars

Nominal GDP $US2005 & 2010

Ranked by 2010

Copyright © 2006 Global Insight, Inc. 42006 GLOBAL AUTOMOTIVE CONFERENCE

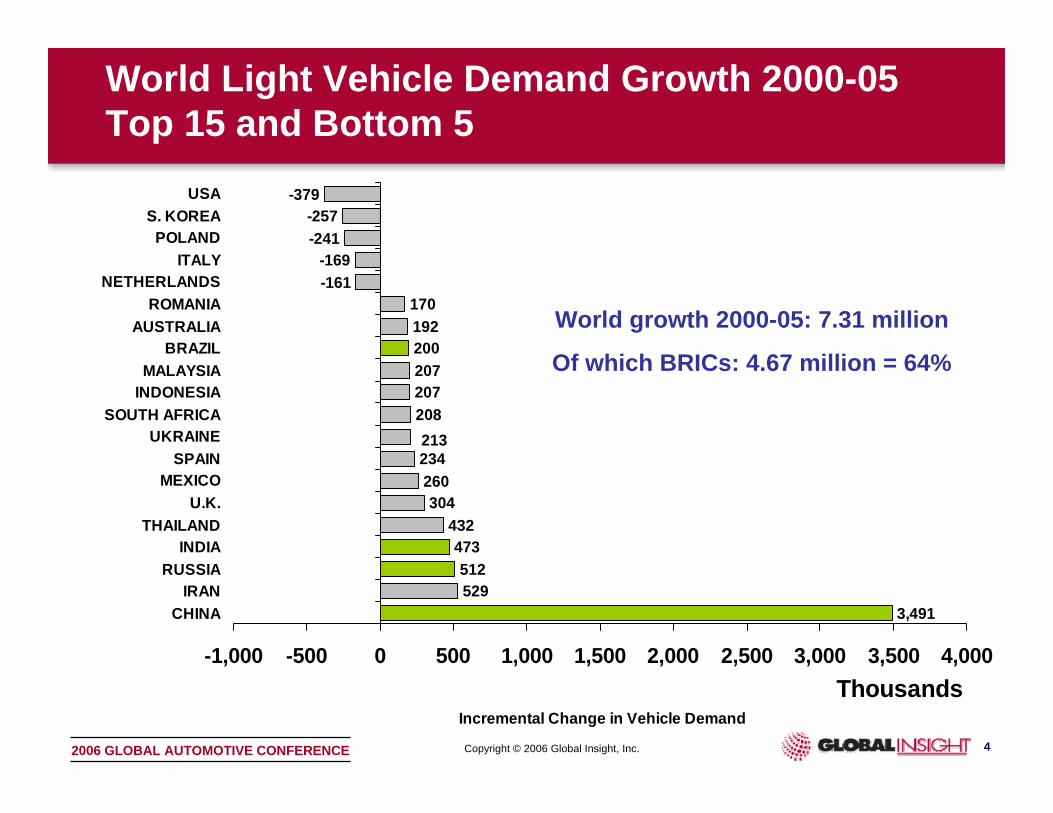

World Light Vehicle Demand Growth 2000-05 Top 15 and Bottom 5

529512

473432

304260234

208207207

192170

-161-169

-241-257

-379

213

3,491

200

-1,000 -500 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

CHINAIRAN

RUSSIAINDIA

THAILANDU.K.

MEXICOSPAIN

UKRAINESOUTH AFRICA

INDONESIAMALAYSIA

BRAZILAUSTRALIA

ROMANIANETHERLANDS

ITALYPOLAND

S. KOREAUSA

ThousandsIncremental Change in Vehicle Demand

World growth 2000-05: 7.31 million

Of which BRICs: 4.67 million = 64%

Copyright © 2006 Global Insight, Inc. 52006 GLOBAL AUTOMOTIVE CONFERENCE

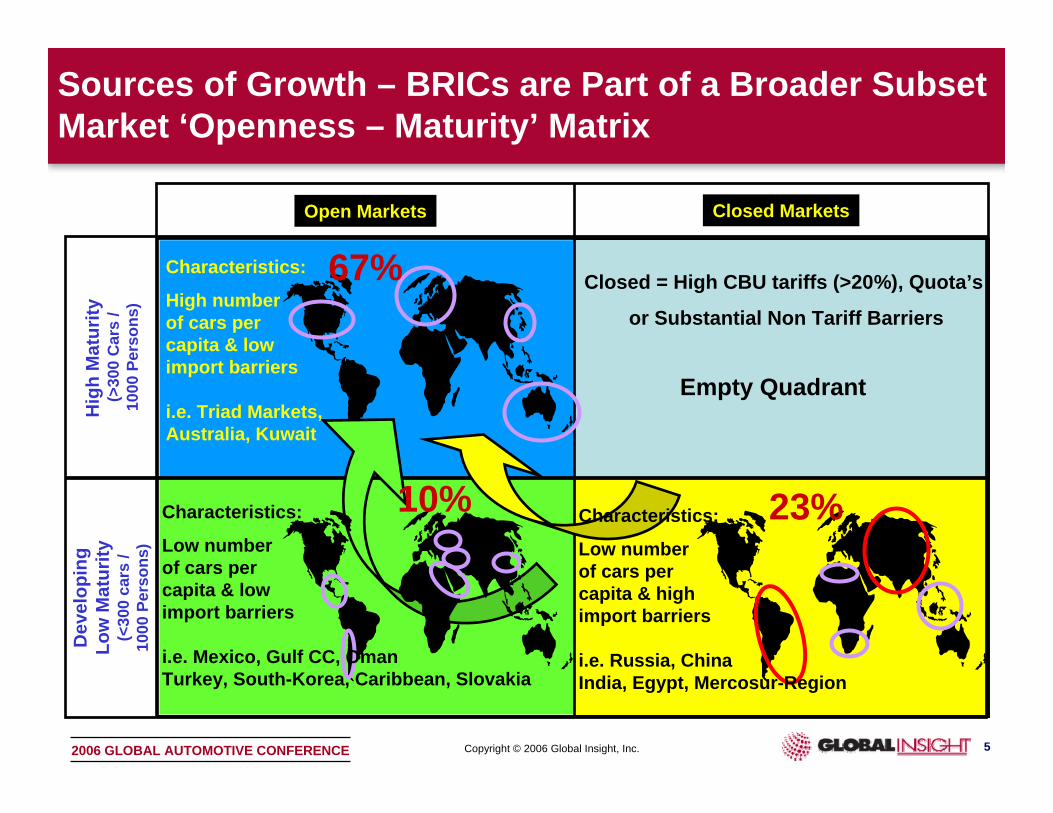

Sources of Growth – BRICs are Part of a Broader SubsetMarket ‘Openness – Maturity’ Matrix

Dev

elop

ing

Low

Mat

urity

(<30

0 ca

rs /

1000

Per

sons

)

Open Markets Closed Markets

Hig

h M

atur

ity(>

300

Car

s /

1000

Per

sons

)

Characteristics:

High numberof cars per capita & lowimport barriers

i.e. Triad Markets,Australia, Kuwait

Characteristics:

Low numberof cars per capita & lowimport barriers

i.e. Mexico, Gulf CC, OmanTurkey, South-Korea, Caribbean, Slovakia

Characteristics:

Low numberof cars per capita & highimport barriers

i.e. Russia, ChinaIndia, Egypt, Mercosur-Region

Empty Quadrant

23%10%

67% Closed = High CBU tariffs (>20%), Quota’s

or Substantial Non Tariff Barriers

Copyright © 2006 Global Insight, Inc. 62006 GLOBAL AUTOMOTIVE CONFERENCE

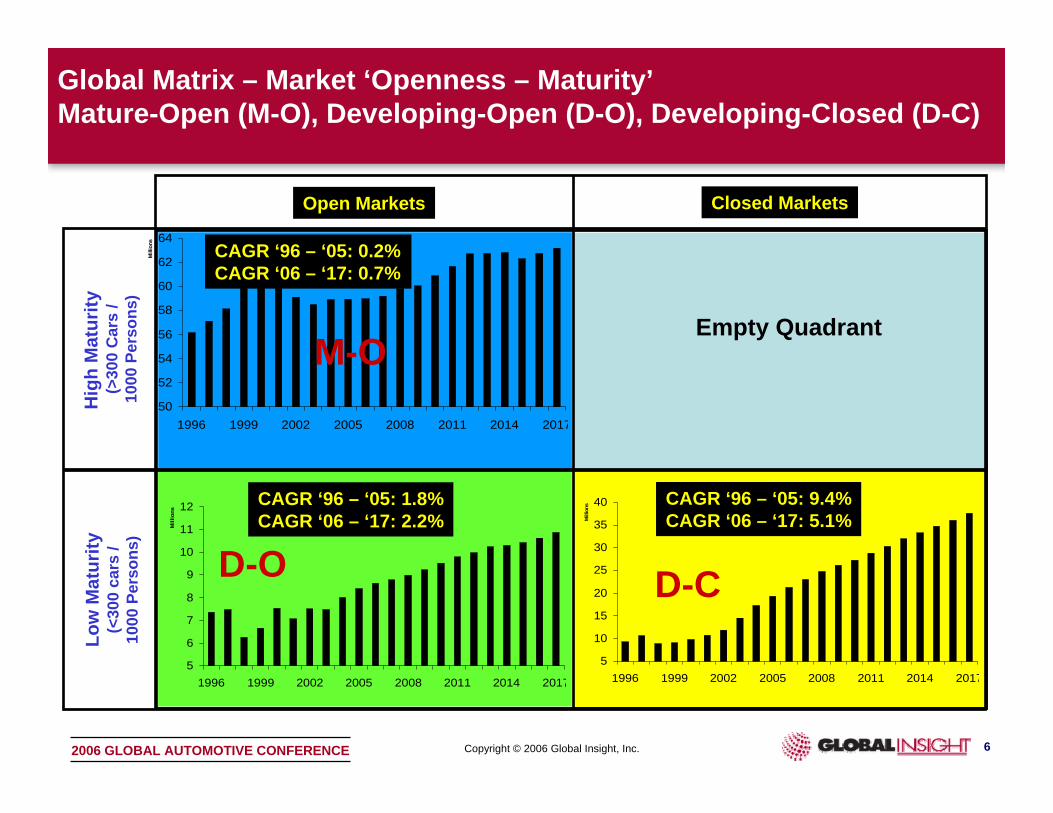

Global Matrix – Market ‘Openness – Maturity’Mature-Open (M-O), Developing-Open (D-O), Developing-Closed (D-C)

Low

Mat

urity

(<30

0 ca

rs /

1000

Per

sons

)

Open Markets Closed Markets

Hig

h M

atur

ity(>

300

Car

s /

1000

Per

sons

)

Empty Quadrant

50

52

54

56

58

60

62

64

1996 1999 2002 2005 2008 2011 2014 2017

Mill

ions

5

10

15

20

25

30

35

40

1996 1999 2002 2005 2008 2011 2014 2017

Mill

ions

5

6

7

8

9

10

11

12

1996 1999 2002 2005 2008 2011 2014 2017

Mill

ions

CAGR ‘96 – ‘05: 0.2%CAGR ‘06 – ‘17: 0.7%

CAGR ‘96 – ‘05: 9.4%CAGR ‘06 – ‘17: 5.1%

CAGR ‘96 – ‘05: 1.8%CAGR ‘06 – ‘17: 2.2%

D-O

M-O

D-C

Copyright © 2006 Global Insight, Inc. 72006 GLOBAL AUTOMOTIVE CONFERENCE

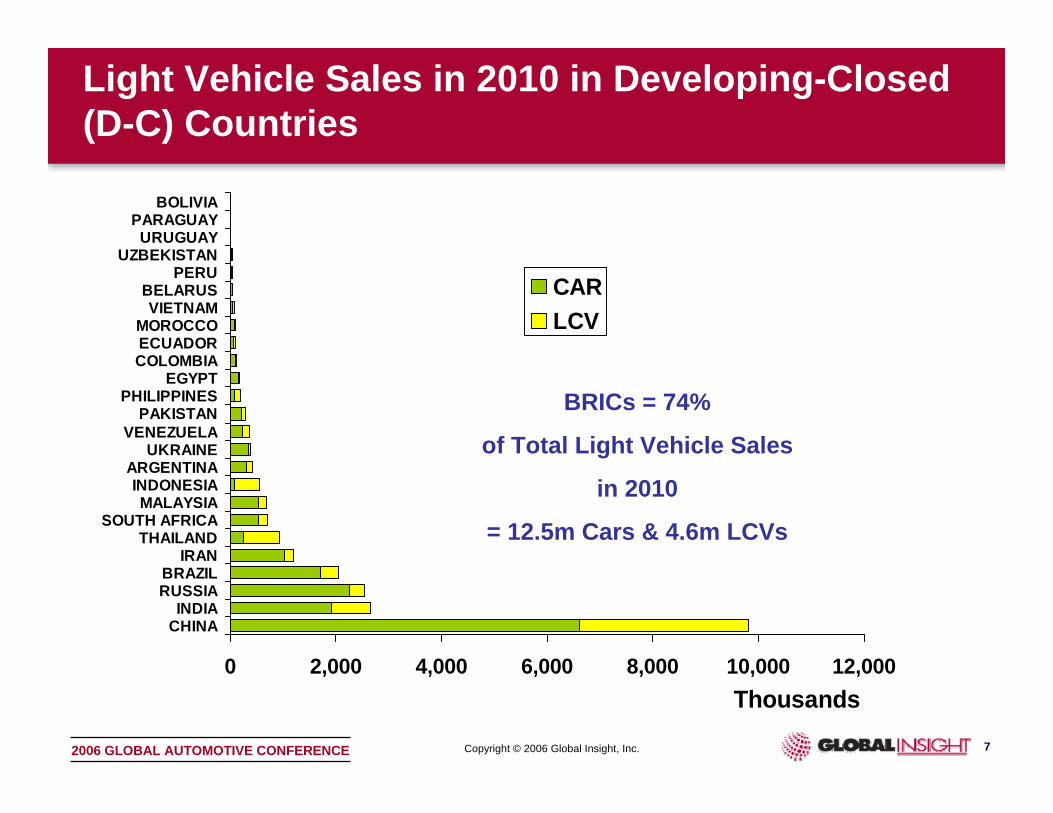

Light Vehicle Sales in 2010 in Developing-Closed (D-C) Countries

0 2,000 4,000 6,000 8,000 10,000 12,000

CHINAINDIA

RUSSIABRAZIL

IRANTHAILAND

SOUTH AFRICAMALAYSIA

INDONESIAARGENTINA

UKRAINEVENEZUELA

PAKISTANPHILIPPINES

EGYPTCOLOMBIAECUADORMOROCCO

VIETNAMBELARUS

PERUUZBEKISTAN

URUGUAYPARAGUAY

BOLIVIA

Thousands

CARLCV

BRICs = 74%

of Total Light Vehicle Sales

in 2010

= 12.5m Cars & 4.6m LCVs

Copyright © 2006 Global Insight, Inc. 82006 GLOBAL AUTOMOTIVE CONFERENCE

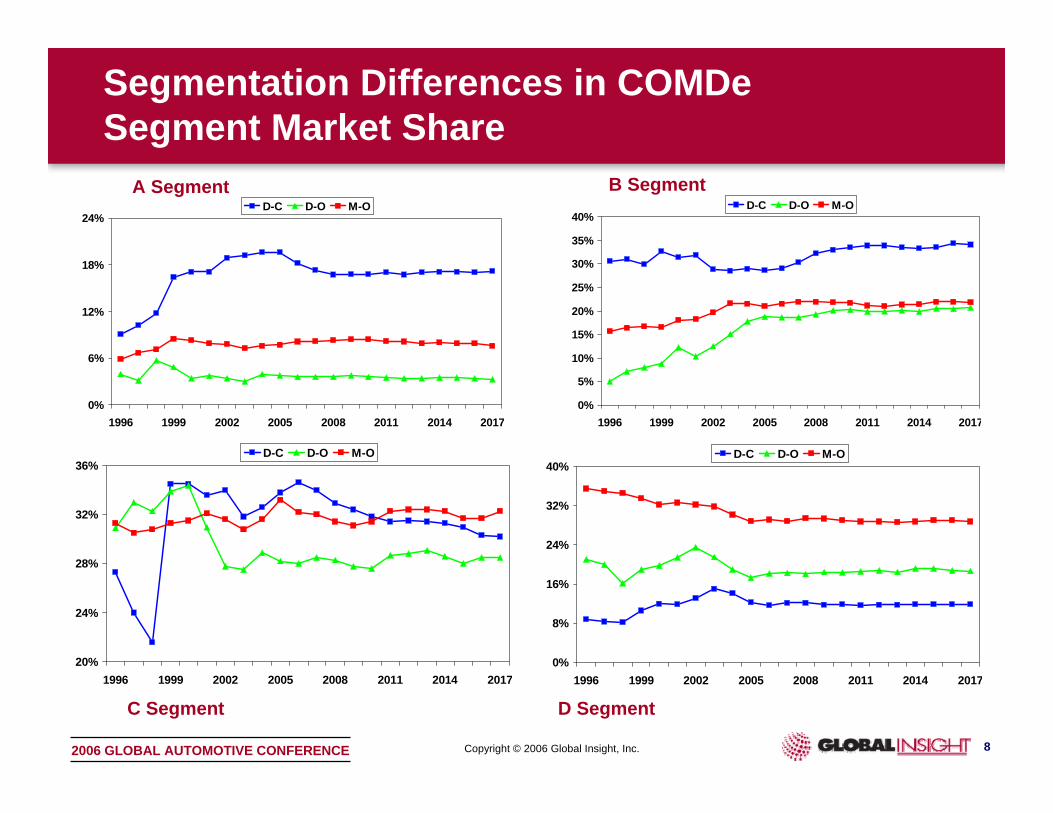

Segmentation Differences in COMDeSegment Market Share

0%

6%

12%

18%

24%

1996 1999 2002 2005 2008 2011 2014 2017

D-C D-O M-O

0%

5%

10%

15%

20%

25%

30%

35%

40%

1996 1999 2002 2005 2008 2011 2014 2017

D-C D-O M-O

20%

24%

28%

32%

36%

1996 1999 2002 2005 2008 2011 2014 2017

D-C D-O M-O

A Segment B Segment

C Segment

0%

8%

16%

24%

32%

40%

1996 1999 2002 2005 2008 2011 2014 2017

D-C D-O M-O

D Segment

Copyright © 2006 Global Insight, Inc. 92006 GLOBAL AUTOMOTIVE CONFERENCE

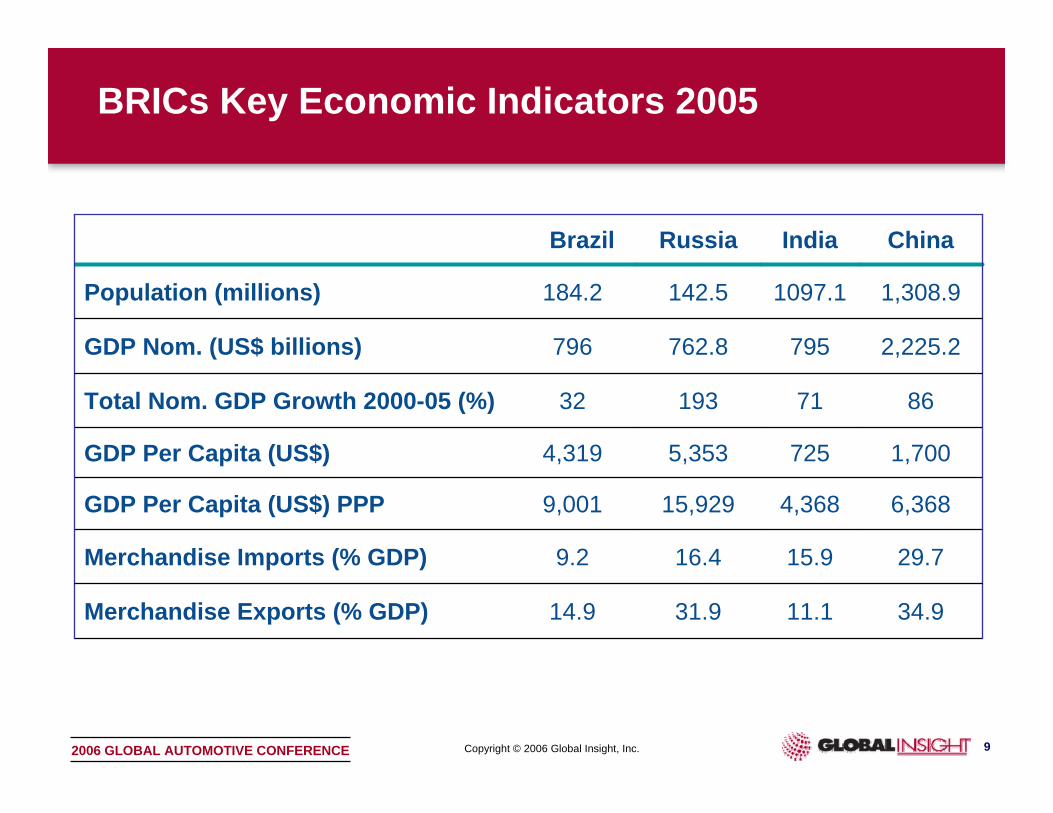

BRICs Key Economic Indicators 2005

34.911.131.914.9Merchandise Exports (% GDP)

29.715.916.49.2Merchandise Imports (% GDP)

2,225.2795762.8796GDP Nom. (US$ billions)

1,308.91097.1142.5184.2Population (millions)

15,929

5,353

193

Russia

9,001

4,319

32

Brazil

6,3684,368GDP Per Capita (US$) PPP

1,700725GDP Per Capita (US$)

8671Total Nom. GDP Growth 2000-05 (%)

ChinaIndia

Copyright © 2006 Global Insight, Inc. 102006 GLOBAL AUTOMOTIVE CONFERENCE

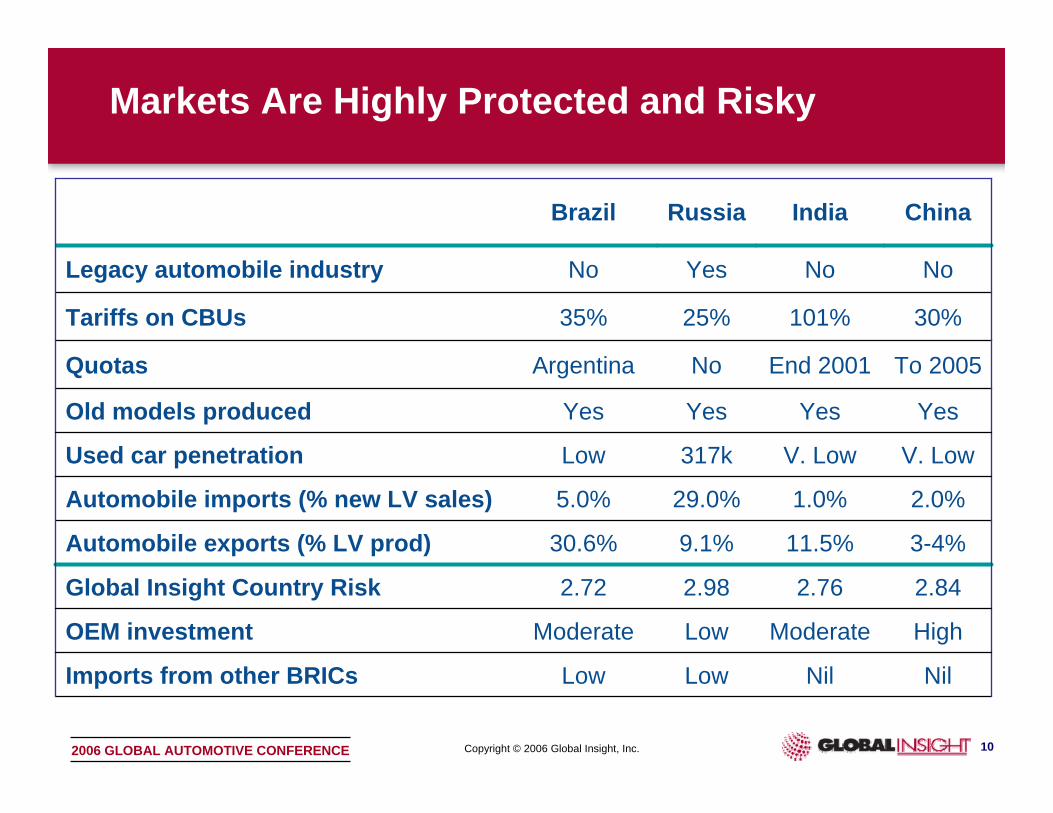

Markets Are Highly Protected and Risky

2.842.762.982.72Global Insight Country Risk

V. LowV. Low317kLow Used car penetration

HighModerateLowModerateOEM investment

YesYesYesYesOld models produced

To 2005End 2001NoArgentinaQuotas

30%101%25%35%Tariffs on CBUs

NoNoYesNoLegacy automobile industry

Low

9.1%

29.0%

Russia

Low

30.6%

5.0%

Brazil

NilNilImports from other BRICs

3-4%11.5%Automobile exports (% LV prod)

2.0%1.0%Automobile imports (% new LV sales)

ChinaIndia

Copyright © 2006 Global Insight, Inc. 112006 GLOBAL AUTOMOTIVE CONFERENCE

Automotive Demand Market Summary 2005

12.88.0125.4618.17Car parc (millions)10.17.3178.0100.0Car ownership per 000 population

5.41.21.61.6Light vehicle sales (millions)4.11.711.28.7LV sales per ‘000 population

RussiaBrazil ChinaIndia

1,413921

3,293196

305

317

1,330

284

2,067

0

1,000

2,000

3,000

4,000

5,000

6,000

BRAZIL RUSSIA INDIA CHINA

Thou

sand

s

Used ImportsLCVCAR

0

1000

2000

3000

4000

5000

6000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Thou

sand

s

China

India

RussiaBrazil

LV Sales 1995-2005 LV Sales 2005

Copyright © 2006 Global Insight, Inc. 122006 GLOBAL AUTOMOTIVE CONFERENCE

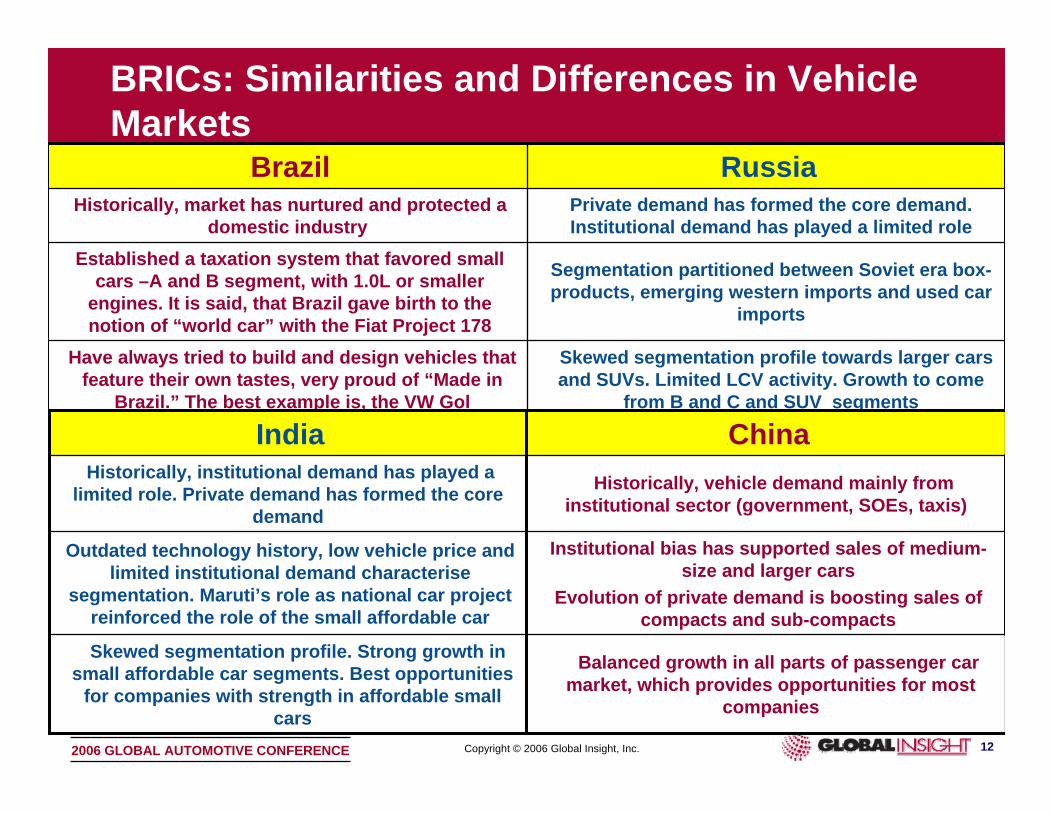

BRICs: Similarities and Differences in Vehicle Markets

RussiaCBrazil

Skewed segmentation profile towards larger cars and SUVs. Limited LCV activity. Growth to come

from B and C and SUV segments

Have always tried to build and design vehicles that feature their own tastes, very proud of “Made in

Brazil.” The best example is, the VW Gol

Segmentation partitioned between Soviet era box-products, emerging western imports and used car

imports

Established a taxation system that favored small cars –A and B segment, with 1.0L or smaller

engines. It is said, that Brazil gave birth to the notion of “world car” with the Fiat Project 178

Private demand has formed the core demand. Institutional demand has played a limited role

Historically, market has nurtured and protected a domestic industry

Skewed segmentation profile. Strong growth in small affordable car segments. Best opportunities

for companies with strength in affordable small cars

Outdated technology history, low vehicle price and limited institutional demand characterise

segmentation. Maruti’s role as national car project reinforced the role of the small affordable car

Historically, institutional demand has played a limited role. Private demand has formed the core

demand

India CChina

Balanced growth in all parts of passenger car market, which provides opportunities for most

companies

Institutional bias has supported sales of medium-size and larger cars

Evolution of private demand is boosting sales of compacts and sub-compacts

Historically, vehicle demand mainly from institutional sector (government, SOEs, taxis)

Copyright © 2006 Global Insight, Inc. 132006 GLOBAL AUTOMOTIVE CONFERENCE

Company and Market Specific SuccessFactors

Segment

Bodystyle

Powertrain

PricingStrategic objectives

Geographicalfootprint

Brandimage

Product range

Modelcycle

Marketgrowth

Copyright © 2006 Global Insight, Inc. 142006 GLOBAL AUTOMOTIVE CONFERENCE

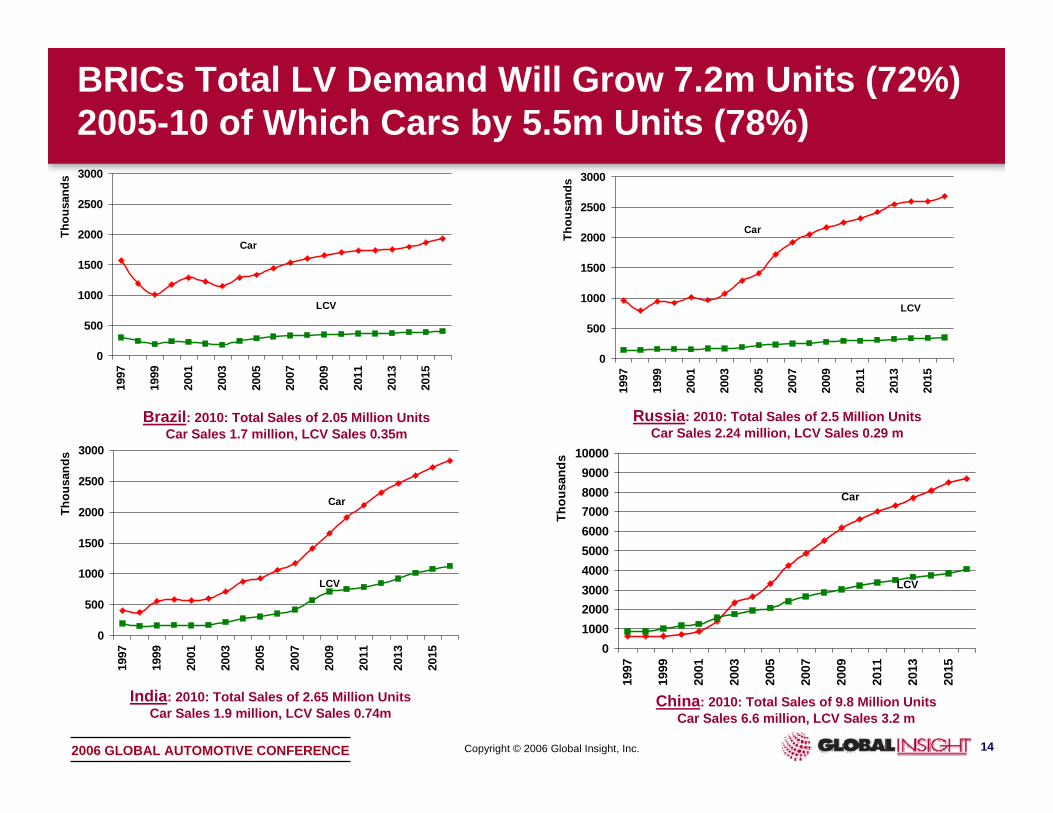

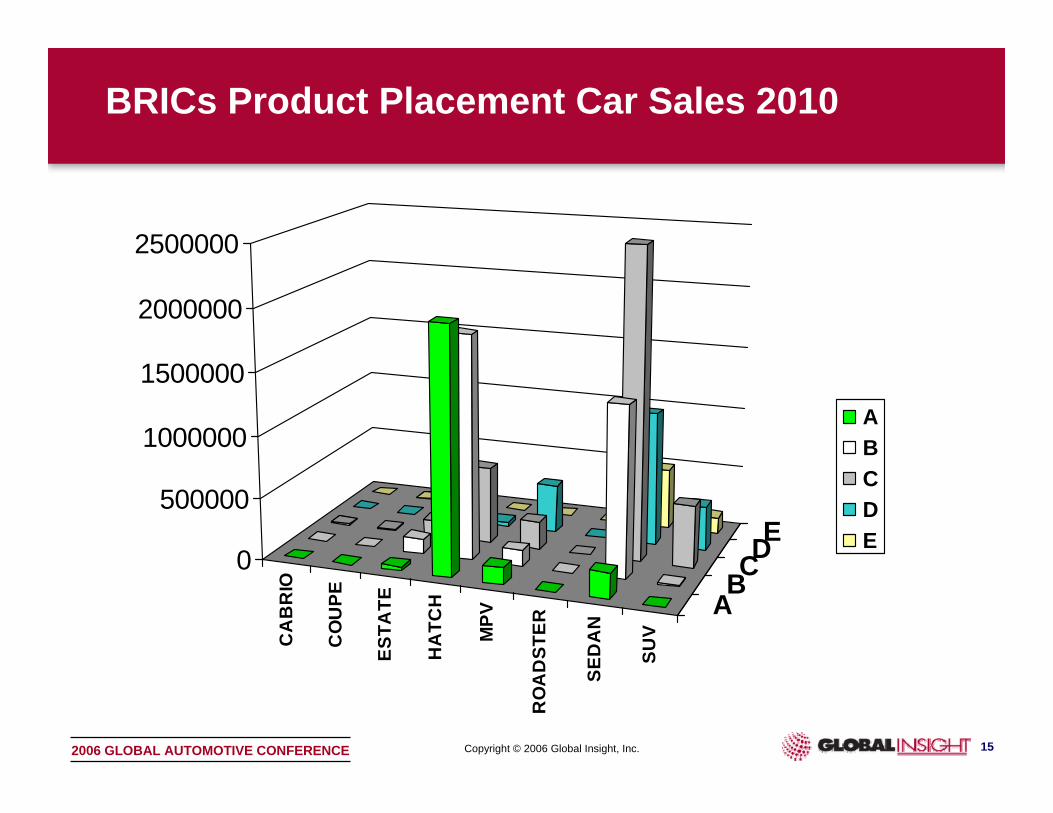

BRICs Total LV Demand Will Grow 7.2m Units (72%) 2005-10 of Which Cars by 5.5m Units (78%)

0

500

1000

1500

2000

2500

3000

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Thou

sand

s

Car

LCV

0

500

1000

1500

2000

2500

3000

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Thou

sand

s

Car

LCV

0100020003000400050006000700080009000

10000

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Thou

sand

s

Car

LCV

China: 2010: Total Sales of 9.8 Million UnitsCar Sales 6.6 million, LCV Sales 3.2 m

0

500

1000

1500

2000

2500

3000

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Thou

sand

s

Car

LCV

Russia: 2010: Total Sales of 2.5 Million UnitsCar Sales 2.24 million, LCV Sales 0.29 m

Brazil: 2010: Total Sales of 2.05 Million UnitsCar Sales 1.7 million, LCV Sales 0.35m

India: 2010: Total Sales of 2.65 Million UnitsCar Sales 1.9 million, LCV Sales 0.74m

Copyright © 2006 Global Insight, Inc. 152006 GLOBAL AUTOMOTIVE CONFERENCE

CA

BR

IO

CO

UPE

ESTA

TE

HA

TCH

MPV

RO

AD

STER

SED

AN

SUV

ABCDE

0

500000

1000000

1500000

2000000

2500000

ABCDE

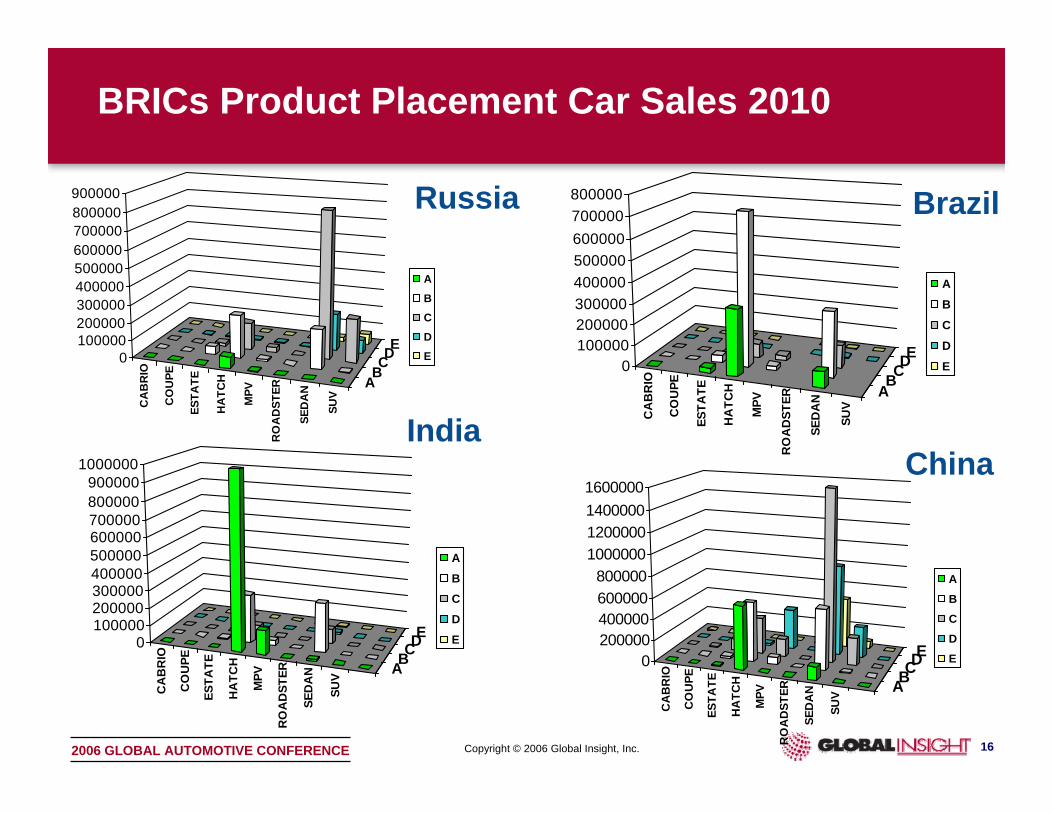

BRICs Product Placement Car Sales 2010

Copyright © 2006 Global Insight, Inc. 162006 GLOBAL AUTOMOTIVE CONFERENCE

BRICs Product Placement Car Sales 2010C

AB

RIO

CO

UPE

ESTA

TE

HA

TCH

MPV

RO

AD

STER

SED

AN

SUV

ABCDE

0100000200000300000400000500000600000700000800000900000

ABCDE

CA

BR

IO

CO

UPE

ESTA

TE

HA

TCH

MPV

RO

AD

STER

SED

AN

SUV

ABCDE

0100000200000300000400000500000600000700000800000

ABCDE

CA

BR

IO

CO

UPE

ESTA

TE

HA

TCH

MPV

RO

AD

STER

SED

AN

SUV ABCDE0

100000200000300000400000500000600000700000800000900000

1000000

ABCDE

CA

BR

IO

CO

UPE

ESTA

TE

HA

TCH

MPV

RO

AD

STER

SED

AN

SUV AB

CDE0

200000400000600000800000

1000000120000014000001600000

ABCDE

Russia Brazil

ChinaIndia

Copyright © 2006 Global Insight, Inc. 172006 GLOBAL AUTOMOTIVE CONFERENCE

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

0 200000 400000 600000 800000 1000000 1200000 1400000 1600000Cumulative Sales

Pric

e eu

ro

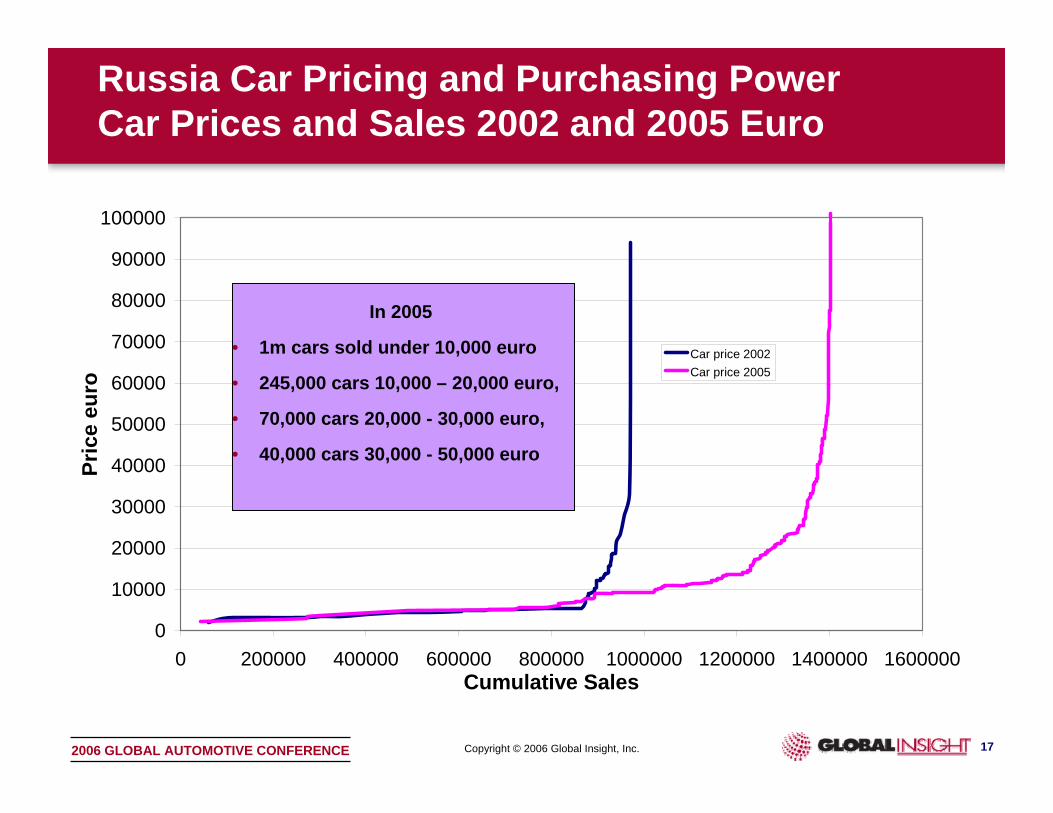

Car price 2002Car price 2005

In 2005

• 1m cars sold under 10,000 euro

• 245,000 cars 10,000 – 20,000 euro,

• 70,000 cars 20,000 - 30,000 euro,

• 40,000 cars 30,000 - 50,000 euro

Russia Car Pricing and Purchasing PowerCar Prices and Sales 2002 and 2005 Euro

Copyright © 2006 Global Insight, Inc. 182006 GLOBAL AUTOMOTIVE CONFERENCE

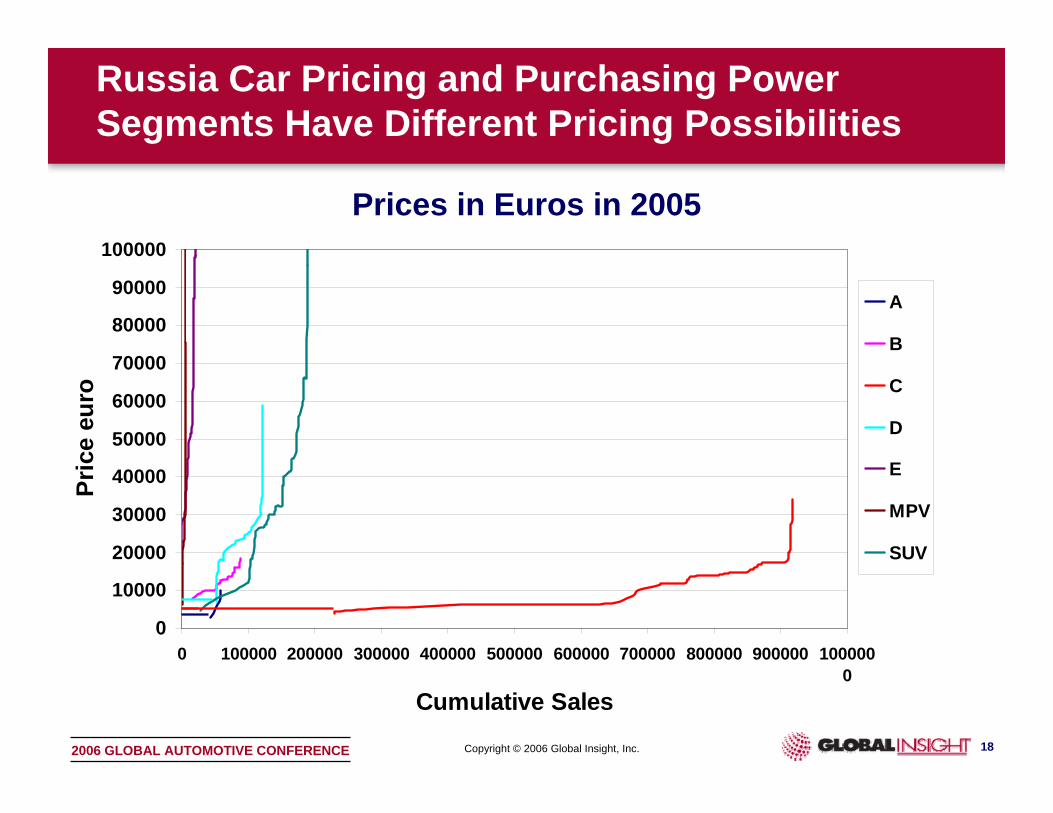

Russia Car Pricing and Purchasing PowerSegments Have Different Pricing Possibilities

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

0 100000 200000 300000 400000 500000 600000 700000 800000 900000 1000000

Cumulative Sales

Pric

e eu

ro

A

B

C

D

E

MPV

SUV

Prices in Euros in 2005

Copyright © 2006 Global Insight, Inc. 192006 GLOBAL AUTOMOTIVE CONFERENCE

0

5 0

1 00

3-D

Colu

mn 1

World Cars Competitive Space

DaciaLogan

VW Gol

Fiat D200

Nissan projectToyota

projectTataMicrocar

Peugeot206

SkodaFabia

OpelCorsa

ToyotaAygo

Ford Ka II

Chevy Aveo

Ford B204VW

Fox

Content/Price

Vehicle Size/Segment

= engineered “World Car”

= derivative (decontented)

vehicle

Small Large

Low

High

Price/content trade off

Price/sizetrade off

Fiat Palio/Siena

HyundaiGetz

Copyright © 2006 Global Insight, Inc. 202006 GLOBAL AUTOMOTIVE CONFERENCE

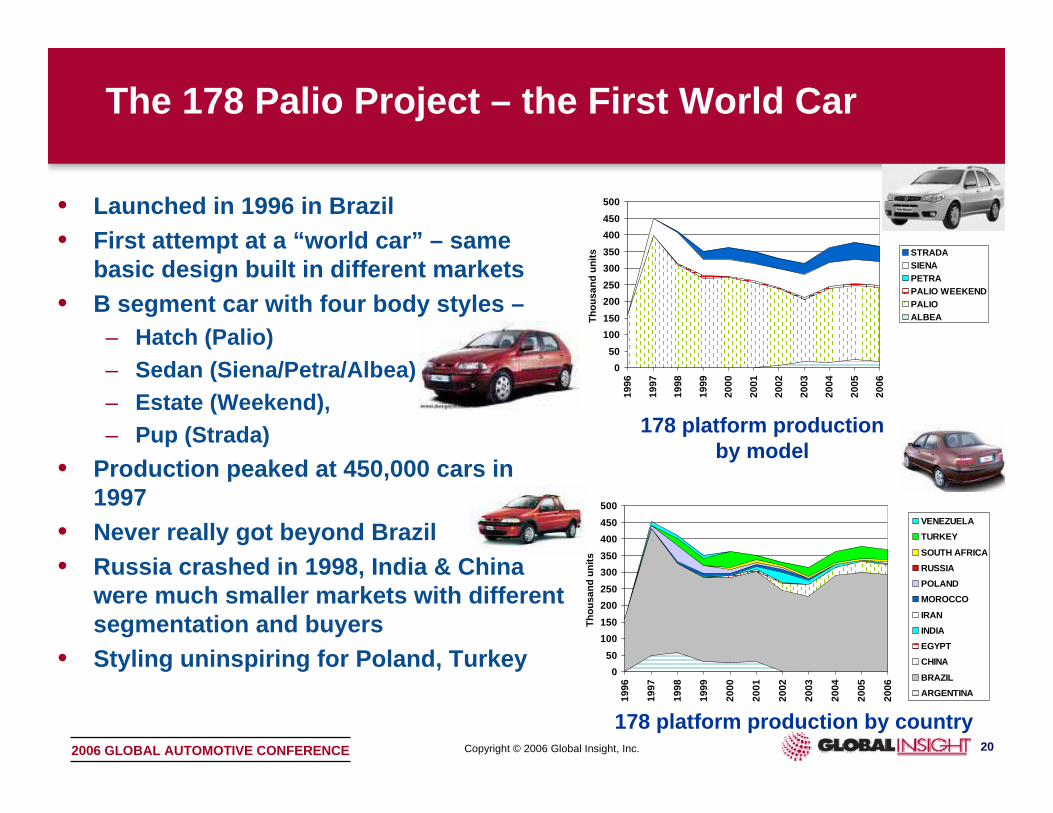

The 178 Palio Project – the First World Car

050

100150200250300350400450500

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Thou

sand

uni

ts

VENEZUELATURKEY

SOUTH AFRICARUSSIAPOLANDMOROCCO

IRANINDIAEGYPTCHINA

BRAZILARGENTINA

050

100150200250300350400450500

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Thou

sand

uni

ts STRADASIENAPETRAPALIO WEEKENDPALIOALBEA

178 platform production by country

178 platform productionby model

• Launched in 1996 in Brazil• First attempt at a “world car” – same

basic design built in different markets• B segment car with four body styles –

– Hatch (Palio) – Sedan (Siena/Petra/Albea) – Estate (Weekend), – Pup (Strada)

• Production peaked at 450,000 cars in 1997

• Never really got beyond Brazil• Russia crashed in 1998, India & China

were much smaller markets with different segmentation and buyers

• Styling uninspiring for Poland, Turkey

Copyright © 2006 Global Insight, Inc. 212006 GLOBAL AUTOMOTIVE CONFERENCE

• Initiated in 1998, Renault acquired Dacia in 1999. Model focused on 'Design to Cost‘

• C segment, based on a modified B platform, using frontal chassis modules borrowed from the X65 platform and rear chassis modules of the B platform

• Bodystyles – Sedan, Estate - October 2006, Hatchback displayed in Paris in September 2006, Pickup launched in early 2007, 4x4 under consideration for around 2008 or 2009

• Economies of scale achieved by producing 200,000 units per annum in Romania and centralising its CKD activity in the country,

• High potential for cost amortisation and/or reduction from carry-over parts, shared platform, localising production in low-cost bases and strict integration target in purchasing

• Powertrain: 1.4l, 1.6l petrol, 1.5l diesel

The Logan Project (X90)

2005 2006 2007 2008CKD Output 30,000 103,000 408,000 589,000Dacia Sales in Romania 113,276 108,000 95,000 105,000Dacia Sales on export markets 57,994 91,450 140,090 181,950

Dacia Expansion Plans

Source: Dacia

Total Annual Capacity Share of CKD UsedRomania 235,000 N.ARussia 60,000 70%Colombia 15,000 70%Morocco 30,000 70%Iran 300,000 40%India 50,000 50%Brazil N/K 3%

Logan Programme

Source: Dacia

Copyright © 2006 Global Insight, Inc. 222006 GLOBAL AUTOMOTIVE CONFERENCE

• High tariff barriers makes local production a key element in selling into BRICs

• Trade barriers prevent inter-BRIC trade, cannot easily produce in one BRIC and sell into another

• Low export potential means multiple production projects across several BRICs

• OEMs will specialise production to targeted segments within BRICs markets and should look beyond BRICs too

• Production likely to remain low and fragmented for some time -scale economies are harder to achieve

• BRICs type cars will still be among the most successful models produced here, but no super-model emerges to dominate all markets

Production Characteristics in BRICs

Copyright © 2006 Global Insight, Inc. 232006 GLOBAL AUTOMOTIVE CONFERENCE

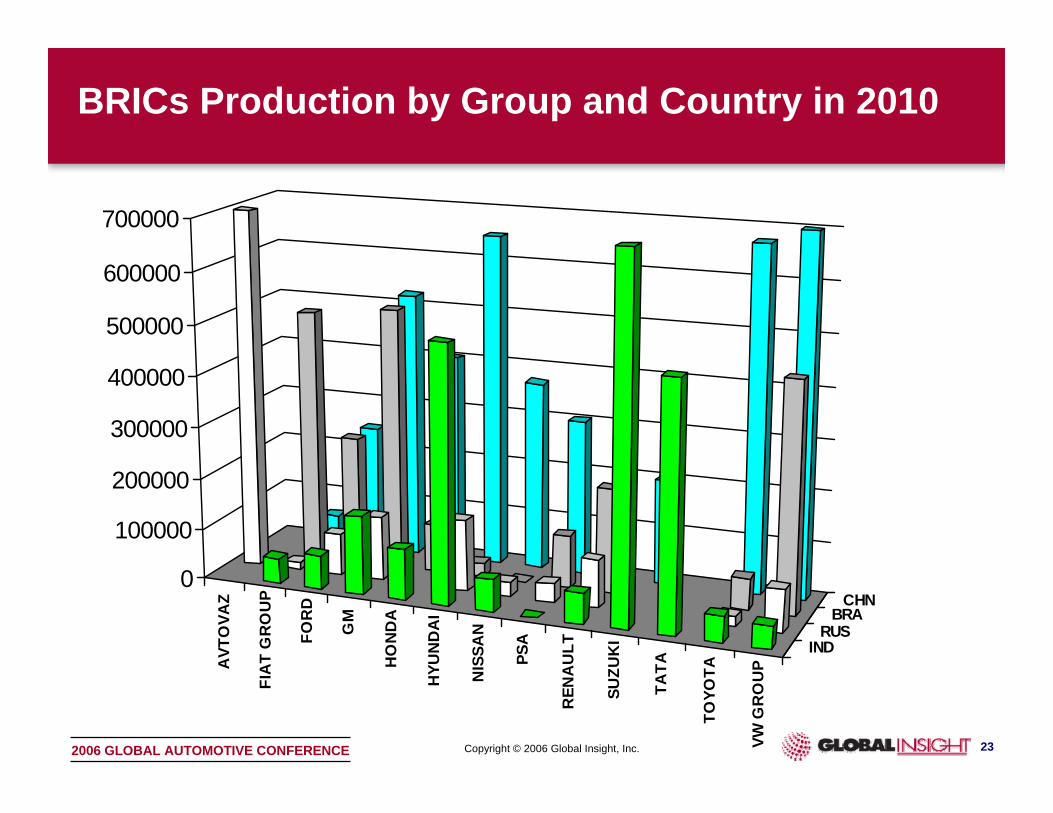

BRICs Production by Group and Country in 2010

AVT

OVA

Z

FIA

T G

RO

UP

FOR

D

GM

HO

ND

A

HYU

ND

AI

NIS

SAN

PSA

REN

AU

LT

SUZU

KI

TATA

TOYO

TA

VW G

RO

UP

INDRUS

BRACHN

0

100000

200000

300000

400000

500000

600000

700000

Copyright © 2006 Global Insight, Inc. 242006 GLOBAL AUTOMOTIVE CONFERENCE

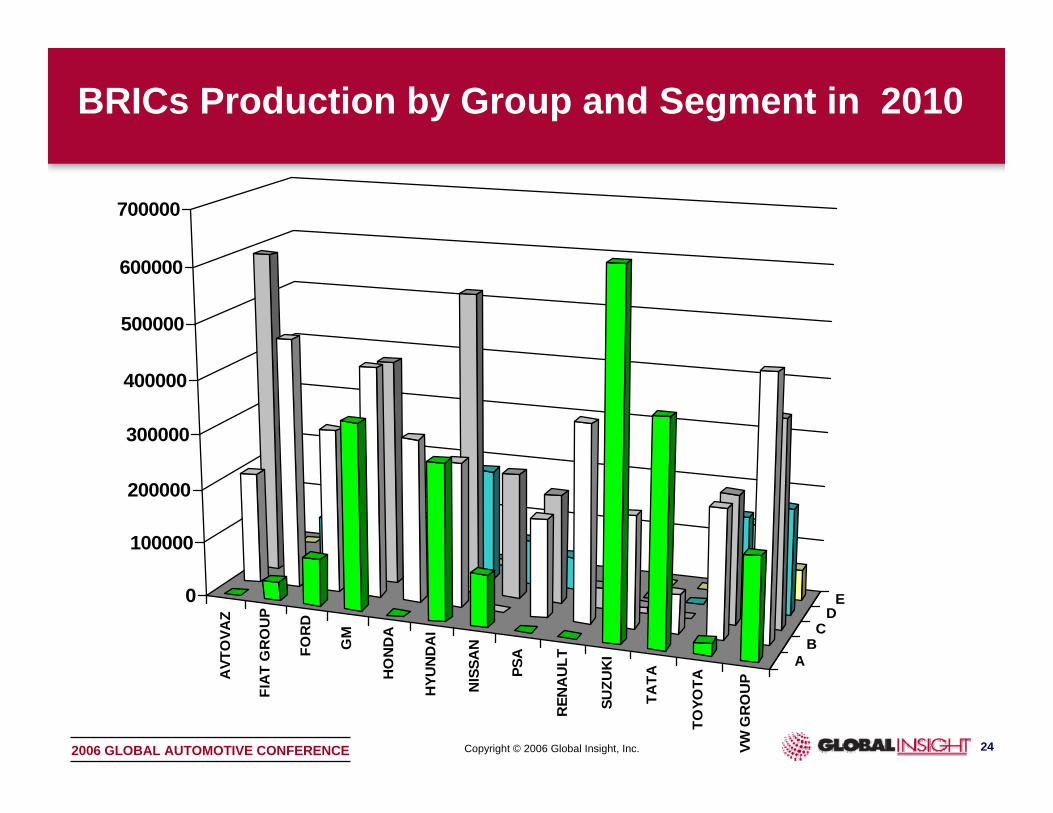

BRICs Production by Group and Segment in 2010

AVT

OVA

Z

FIA

T G

RO

UP

FOR

D

GM

HO

ND

A

HYU

ND

AI

NIS

SAN

PSA

REN

AU

LT

SUZU

KI

TATA

TOYO

TA

VW G

RO

UP

AB

CD

E0

100000

200000

300000

400000

500000

600000

700000

Copyright © 2006 Global Insight, Inc. 252006 GLOBAL AUTOMOTIVE CONFERENCE

• BRICs are the largest countries among D-C markets – but not the only ones

• Total demand growth is impressive but weighted to China

• Closed markets yield:– Ongoing and strong demand differences

• Segmentation, bodystyle, pricing and powertrain differences willremain

– Fragmented and low volume production across several markets

• A multitude of “world cars” will evolve reflecting company differences and objectives

• These cars will still be among the most successful models

Summary

Thank You

Tim ArmstrongAssociate Director, Eastern Europe & Middle East and Africa

E-mail: [email protected]