Binomial Market Model

60

7: The CRR Market Model Marek Rutkowski School of Mathematics and Statistics University of Sydney MATH3075/3975 Financial Mathematics Semester 2, 2016 7: The CRR Market Model

Transcript of Binomial Market Model

7: The CRR Market Model

Marek RutkowskiSchool of Mathematics and Statistics

University of Sydney

MATH3075/3975 Financial MathematicsSemester 2, 2016

7: The CRR Market Model

Outline

We will examine the following issues:

1 The Cox-Ross-Rubinstein Market Model

2 The CRR Call Option Pricing Formula

3 Call and Put Options of American Style

4 Dynamic Programming Approach to American Claims

5 Examples: American Call and Put Options

7: The CRR Market Model

PART 1

THE COX-ROSS-RUBINSTEIN MARKET MODEL

7: The CRR Market Model

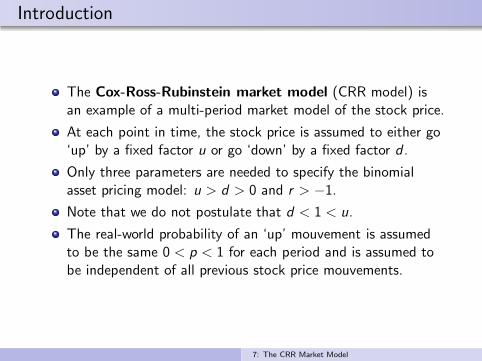

Introduction

The Cox-Ross-Rubinstein market model (CRR model) isan example of a multi-period market model of the stock price.

At each point in time, the stock price is assumed to either go‘up’ by a fixed factor u or go ‘down’ by a fixed factor d .

Only three parameters are needed to specify the binomialasset pricing model: u > d > 0 and r > −1.

Note that we do not postulate that d < 1 < u.

The real-world probability of an ‘up’ mouvement is assumedto be the same 0 < p < 1 for each period and is assumed tobe independent of all previous stock price mouvements.

7: The CRR Market Model

Bernoulli Processes

Definition (Bernoulli Process)

A process X = (Xt)1≤t≤T on a probability space (Ω,F ,P) is calledthe Bernoulli process with parameter 0 < p < 1 if the randomvariables X1,X2, . . . ,XT are independent and have the followingcommon probability distribution

P(Xt = 1) = 1− P(Xt = 0) = p.

Definition (Bernoulli Counting Process)

The Bernoulli counting process N = (Nt)0≤t≤T is defined bysetting N0 = 0 and, for every t = 1, . . . ,T and ω ∈ Ω,

Nt(ω) := X1(ω) + X2(ω) + · · · + Xt(ω).

The process N is a special case of an additive random walk.

7: The CRR Market Model

Stock Price

Definition (Stock Price)

The stock price process in the CRR model is defined via an initialvalue S0 > 0 and, for 1 ≤ t ≤ T and all ω ∈ Ω,

St(ω) := S0uNt(ω)d t−Nt(ω).

The underlying Bernoulli process X governs the ‘up’ and‘down’ mouvements of the stock. The stock price moves upat time t if Xt(ω) = 1 and moves down if Xt(ω) = 0.

The dynamics of the stock price can be seen as an example ofa multiplicative random walk.

The Bernoulli counting process N counts the up mouvements.Before and including time t, the stock price moves up Nt

times and down t − Nt times.

7: The CRR Market Model

Distribution of the Stock Price

For each t = 1, 2, . . . ,T , the random variable Nt has thebinomial distribution with parameters p and t.

Specifically, for every t = 1, . . . ,T and k = 0, . . . , t we havethat

P(Nt = k) =

(t

k

)pk(1− p)t−k .

Hence the probability distribution of the stock price St at timet is given by

P(St = S0ukd t−k) =

(t

k

)pk(1− p)t−k

for k = 0, 1, . . . , t.

7: The CRR Market Model

Stock Price Lattice

−1

−0.8

−0.6

−0.4

−0.2

0

0.2

0.4

0.6

0.8

S0

S0u

S0d

S0u2

S0ud

S0d2

S0u3

S0u2d

S0d3

S0u4

S0u3d

S0u2d2

S0d4

S0ud2

S0ud3

...

...

...

Figure: Stock Price Lattice in the CRR Model

7: The CRR Market Model

Risk-Neutral Probability Measure

Proposition (7.1)

Assume that d < 1 + r < u. Then a probability measure P on

(Ω,FT ) is a risk-neutral probability measure for the CRR model

M = (B ,S) with parameters p, u, d , r and time horizon T if and

only if:

1 X1,X2,X3, . . . ,XT are independent under the probability

measure P,

2 0 < p := P (Xt = 1) < 1 for all t = 1, . . . ,T,

3 pu + (1− p)d = (1 + r),

where X is the Bernoulli process governing the stock price S.

7: The CRR Market Model

Risk-Neutral Probability Measure

Proposition (7.2)

If d < 1 + r < u then the CRR market model M = (B ,S) isarbitrage-free and complete.

Since the CRR model is complete, the unique arbitrage priceof any European contingent claim can be computed using therisk-neutral valuation formula

πt(X ) = Bt EP

(X

BT

∣∣∣Ft

)

We will apply this formula to the call option on the stock.

7: The CRR Market Model

PART 2

THE CRR CALL OPTION PRICING FORMULA

7: The CRR Market Model

CRR Call Option Pricing Formula

Proposition (7.3)

The arbitrage price at time t = 0 of the European call optionCT = (ST − K )+ in the binomial market model M = (B ,S) isgiven by the CRR call pricing formula

C0 = S0

T∑

k=k

(T

k

)pk(1− p)T−k − K

(1 + r)T

T∑

k=k

(T

k

)pk (1− p)T−k

where

p =1 + r − d

u − d, p =

pu

1 + r

and k is the smallest integer k such that

k log(ud

)> log

(K

S0dT

).

7: The CRR Market Model

Proof of Proposition 7.3

Proof of Proposition 7.3.

The price at time t = 0 of the claim X = CT = (ST − K )+ can be

computed using the risk-neutral valuation under P

C0 =1

(1 + r)TEP(CT ) .

In view of Proposition 7.1, we obtain

C0 =1

(1 + r)T

T∑

k=0

(T

k

)pk(1− p)T−k max

(0, S0u

kdT−k − K).

We note that

S0ukdT−k − K > 0 ⇔

(ud

)k

>K

S0dT

⇔ k log(ud

)> log

(K

S0dT

)

7: The CRR Market Model

Proof of Proposition 7.3

Proof of Proposition 7.3 (Continued).

We define k = k(S0,T ) as the smallest integer k such that the lastinequality is satisfied. If there are less than k upward mouvementsthere is no chance that the option will expire worthless.

Therefore, we obtain

C0 =1

(1 + r)T

T∑

k=k

(T

k

)pk(1− p)T−k

(S0u

kdT−k − K)

=S0

(1 + r)T

T∑

k=k

(T

k

)pk(1− p)T−kukdT−k

− K

(1 + r)T

T∑

k=k

(T

k

)pk(1 − p)T−k

7: The CRR Market Model

Proof of Proposition 7.3

Proof of Proposition 7.3 (Continued).

Consequently,

C0 = S0

T∑

k=k

(T

k

)(pu

1 + r

)k ((1 − p)d

1 + r

)T−k

− K

(1 + r)T

T∑

k=k

(T

k

)pk(1 − p)T−k

and thus

C0 = S0

T∑

k=k

(T

k

)pk(1− p)T−k − K

(1 + r)T

T∑

k=k

(T

k

)pk (1− p)T−k

where we denote p = pu1+r

.

7: The CRR Market Model

Martingale Approach (MATH3975)

Check that 0 < p = pu1+r

< 1 whenever 0 < p = 1+r−du−d

< 1.

Let P be the probability measure obtained by setting p = p inProposition 7.1. Then the process B

Sis a martingale under P.

For t = 0, the price of the call satisfies

C0 = S0 P(D)− KB(0,T ) P(D)

where D = ω ∈ Ω : ST (ω) > K.Recall that

Ct = Bt EP

(B−1T (ST − K )+ | Ft

)

Using the abstract Bayes formula, one can show that

Ct = St P(D | Ft)− KB(t,T ) P(D | Ft).

7: The CRR Market Model

Put-Call Parity

It is possible to derive explicit pricing formula for the calloption at any date t = 0, 1, . . . ,T .

Since CT − PT = ST − K , we see that the following put-callparity holds at any date t = 0, 1, . . . ,T

Ct − Pt = St − K (1 + r)−(T−t) = St − KB(t,T )

whereB(t,T ) = (1 + r)−(T−t)

is the price at time t of zero-coupon bond maturing at T .

Using Proposition 7.3 and the put-call parity, one can derivean explicit pricing formula for the European put option withthe payoff PT = (K − ST )

+. This is left as an exercise.

7: The CRR Market Model

PART 3

CALL AND PUT OPTIONS OF AMERICAN STYLE

7: The CRR Market Model

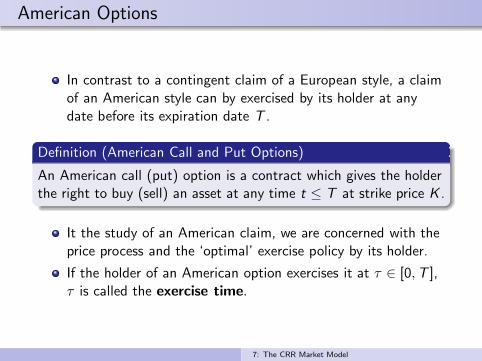

American Options

In contrast to a contingent claim of a European style, a claimof an American style can by exercised by its holder at anydate before its expiration date T .

Definition (American Call and Put Options)

An American call (put) option is a contract which gives the holderthe right to buy (sell) an asset at any time t ≤ T at strike price K .

It the study of an American claim, we are concerned with theprice process and the ‘optimal’ exercise policy by its holder.

If the holder of an American option exercises it at τ ∈ [0,T ],τ is called the exercise time.

7: The CRR Market Model

Stopping Times

An admissible exercise time should belong to the class ofstopping times.

Definition (Stopping Time)

A stopping time with respect to a given filtration F is a mapτ : Ω → 0, 1, . . . ,T such that for any t = 0, 1, . . . ,T the eventω ∈ Ω | τ(ω) = t belongs to the σ-field Ft .

Intuitively, this property means that the decision whetherto stop a given process at time t (for instance, whether toexercise an option at time t or not) depends on the stockprice fluctuations up to time t only.

Definition

Let T [t,T ] be the subclass of stopping times τ with respect to F

satisfying the inequalities t ≤ τ ≤ T .

7: The CRR Market Model

American Call Option

Definition

By an arbitrage price of the American call we mean a priceprocess C a

t , t ≤ T , such that the extended financial market model– that is, a market with trading in riskless bonds, stocks and anAmerican call option – remains arbitrage-free.

Proposition (7.4)

The price of an American call option in the CRR arbitrage-free

market model with r ≥ 0 coincides with the arbitrage price of a

European call option with the same expiry date and strike price.

Proof.

It is sufficient to show that the American call option shouldnever be exercised before maturity, since otherwise the issuerof the option would be able to make riskless profit.

7: The CRR Market Model

Proof of Proposition 7.4

Proof of Proposition 7.4 – Step 1.

The argument hinges on the inequality, for t = 0, 1, . . . ,T ,

Ct ≥ (St − K )+. (1)

An intuitive way of deriving (1) is based on no-arbitragearguments.

Notice that since the price Ct is always non-negative, itsuffices to consider the case when the current stock price isgreater than the exercise price: St − K > 0.

Suppose, on the contrary, that Ct < St − K for some t.

Then it would be possible, with zero net initial investment, tobuy at time t a call option, short a stock, and invest the sumSt − Ct > K in the savings account.

7: The CRR Market Model

Proof of Proposition 7.4

Proof of Proposition 7.4 – Step 1.

By holding this portfolio unchanged up to the maturity dateT , we would be able to lock in a riskless profit.

Indeed, the value of our portfolio at time T would satisfy(recall that r ≥ 0)

CT − ST + (1 + r)T−t(St − Ct)

> (ST − K )+ − ST + (1 + r)T−tK ≥ 0.

We conclude that inequality (1) is necessary for the absenceof arbitrage opportunities.

In the next step, we assume that (1) holds.

7: The CRR Market Model

Proof of Proposition 7.4

Proof of Proposition 7.4 – Step 2.

Taking (1) for granted, we may now deduce the propertyC at = Ct using simple no-arbitrage arguments.

Suppose, on the contrary, that the issuer of an American callis able to sell the option at time 0 at the price C a

0 > C0.

In order to profit from this transaction, the option writerestablishes a dynamic portfolio φ that replicates the valueprocess of the European call and invests the remaining fundsin the savings account.

Suppose that the holder of the option decides to exercise it atinstant t before the expiry date T .

7: The CRR Market Model

Proof of Proposition 7.4

Proof of Proposition 7.4 – Step 2.

Then the issuer of the option locks in a riskless profit, sincethe value of his portfolio at time t satisfies

Ct − (St − K )+ + (1 + r)t(C a0 − C0) > 0.

The above reasoning implies that the European and Americancall options are equivalent from the point of view of arbitragepricing theory.

Both options have the same price and an American call shouldnever be exercised by its holder before expiry.

Note that the assumption r ≥ 0 was necessary to obtain (1).

7: The CRR Market Model

American Put Option

Recall that the American put is an option to sell a specifiednumber of shares, which may be exercised at any time beforeor at the expiry date T .

For the American put on stock with strike K and expiry dateT , we have the following valuation result.

Proposition (7.5)

The arbitrage price Pat of an American put option equals

Pat = max

τ∈T [t,T ]

EP

((1 + r)−(τ−t)(K − Sτ )

+ | Ft

), ∀ t ≤ T .

For any t ≤ T, the stopping time τ∗t which realizes the maximum

is given by the expression

τ∗t = min u ≥ t |Pau = (K − Su)

+ .

7: The CRR Market Model

PART 4

DYNAMIC PROGRAMMING APPROACH

TO AMERICAN CLAIMS

7: The CRR Market Model

Dynamic Programming Recursion

The stopping time τ∗t is called the rational exercise timeof an American put option that is assumed to be still aliveat time t.

By an application of the classic Bellman principle (1952),one reduces the optimal stopping problem in Proposition 7.5to an explicit recursive procedure for the value process.

The following corollary to Proposition 7.5 gives the dynamicprogramming recursion for the value of an American putoption.

Note that this is an extension of the backward inductionapproach to the valuation of European contingent claims.

7: The CRR Market Model

Dynamic Programming Recursion

Corollary (Bellman Principle)

Let the non-negative adapted process U be defined recursively by

setting UT = (K − ST )+ and for t ≤ T − 1

Ut = max(K − St)

+, (1 + r)−1EP(Ut+1 | Ft)

.

Then the arbitrage price Pat of the American put option at time t

equals Ut and the rational exercise time after time t admits the

following representation

τ∗t = min u ≥ t |Uu = (K − Su)+ .

Therefore, τ∗T = T and for every t = 0, 1, . . . ,T − 1

τ∗t = t1Ut=(K−St)+ + τ∗t+11Ut>(K−St)+.

7: The CRR Market Model

Dynamic Programming Recursion

It is also possible to show directly that the price Pat satisfies

the recursive relationship, for t ≤ T − 1,

Pat = max

(K − St)

+, (1 + r)−1EP

(Pat+1 | Ft

)

subject to the terminal condition PaT = (K − ST )

+.

In the case of the CRR model, this formula reduces thevaluation problem to the simple single-period case.

To show this we shall argue by contradiction. Assume firstthat (2) fails to hold for t = T − 1. If this is the case, onemay easily construct at time T − 1 a portfolio which producesriskless profit at time T . Hence, we conclude that necessarily

PaT−1 = max

(K − ST−1)

+, (1+ r)−1EP

((K − ST )

+ | FT

).

This procedure may be repeated as many times as needed.

7: The CRR Market Model

American Put Option: Summary

To summarise:

In the CRR model, the arbitrage pricing of the American putoption reduces to the following recursive recipe, for t ≤ T − 1,

Pat = max

(K − St)

+, (1 + r)−1(pPau

t+1 + (1− p)Padt+1

)

with the terminal condition

PaT = (K − ST )

+.

The quantities Paut+1 and Pad

t+1 represent the values of theAmerican put in the next step corresponding to the upwardand downward mouvements of the stock price starting from agiven node on the CRR lattice.

7: The CRR Market Model

General American Claim

Definition

An American contingent claim X a = (X ,T [0,T ]) expiring at Tconsists of a sequence of payoffs (Xt)0≤t≤T where the randomvariable Xt is Ft -measurable for t = 0, 1, . . . ,T and the set T [0,T ]

of admissible exercise policies.

We interpret Xt as the payoff received by the holder of theclaim X a upon exercising it at time t.

The set of admissible exercise policies is restricted to the classT [0,T ] of all stopping times with values in 0, 1, . . . ,T.Let g : R× 0, 1, . . . ,T → R be an arbitrary function. Wesay that X a is a path-independent American claim with thepayoff function g if the equality Xt = g(St , t) holds for everyt = 0, 1, . . . ,T .

7: The CRR Market Model

General American Claim (MATH3975)

Proposition (7.6)

For every t ≤ T, the arbitrage price π(X a) of an American claim

X a in the CRR model equals

πt(Xa) = max

τ∈T [t,T ]

EP

((1 + r)−(τ−t)Xτ | Ft

).

The price process π(X a) satisfies the following recurrence relation,

for t ≤ T − 1,

πt(Xa) = max

Xt , EP

((1 + r)−1πt+1(X

a) | Ft

)

with πT (Xa) = XT and the rational exercise time τ∗t equals

τ∗t = minu ≥ t |Xu ≥ E

P

((1 + r)−1πu+1(X

a) | Fu

).

7: The CRR Market Model

Path-Independent American Claim: Valuation

For a generic value of the stock price St at time t, we denoteby πu

t+1(Xa) and πd

t+1(Xa) the values of the price πt+1(X

a)at the nodes corresponding to the upward and downwardmouvements of the stock price during the period [t, t + 1],that is, for the values uSt and dSt of the stock price at timet + 1, respectively.

Proposition (7.7)

For a path-independent American claim X a with the payoff process

Xt = g(St , t) we obtain, for every t ≤ T − 1,

πt(Xa) = max

g(St , t), (1+r)−1

(p πu

t+1(Xa)+(1−p)πd

t+1(Xa))

.

7: The CRR Market Model

Path-Independent American Claim: Summary

Consider a path-independent American claim X a with the payofffunction g(St , t). Then:

Let X at = πt(X

a) be the arbitrage price at time t of X a.

Then the pricing formula becomes

X at = max

g(St , t), (1 + r)−1

(p X au

t+1 + (1− p)X adt+1

)

with the terminal condition X aT = g(ST ,T ). Moreover

τ∗t = minu ≥ t | g(Su , u) ≥ X a

u

.

The risk-neutral valuation formula given above is valid foran arbitrary path-independent American claim with a payofffunction g in the CRR binomial model.

7: The CRR Market Model

Example: American Call Option

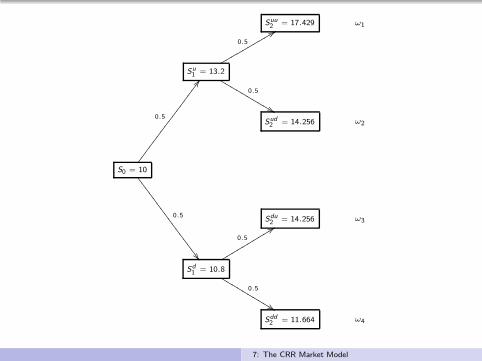

Example (7.1)

We consider here the CRR binomial model with the horizondate T = 2 and the risk-free rate r = 0.2.

The stock price S for t = 0 and t = 1 equals

S0 = 10, Su1 = 13.2, Sd

1 = 10.8.

Let X a be the American call option with maturity date T = 2and the following payoff process

g(St , t) = (St − Kt)+.

The strike Kt is variable and satisfies

K0 = 9, K1 = 9.9, K2 = 12.

7: The CRR Market Model

Example: American Call Option

Example (7.1 Continued)

We will first compute the arbitrage price πt(Xa) of this option

at times t = 0, 1, 2 and the rational exercise time τ∗0 .

Subsequently, we will compute the replicating strategy for X a

up to the rational exercise time τ∗0 .

We start by noting that the unique risk-neutral probabilitymeasure P satisfies

p =1 + r − d

u − d=

(1 + r)S0 − Sd1

Su1 − Sd

1

=12− 10.8

13.2 − 10.8= 0.5

The dynamics of the stock price under P are given by the firstexhibit (note that Sud

2 = Sdu2 ).

The second exhibit represents the price of the call option.

7: The CRR Market Model

Suu2 = 17.429 ω1

Su1 = 13.2

0.5

88rrrrrrrrrr

0.5

&&LLL

LLLL

LLL

Sud2 = 14.256 ω2

S0 = 10

0.5

CC

0.5

777

7777

7777

7777

7

Sdu2 = 14.256 ω3

Sd1 = 10.8

0.5

99rrrrrrrrrr

0.5

%%LLL

LLLL

LLL

Sdd2 = 11.664 ω4

7: The CRR Market Model

(17.429 − 12)+ = 5.429

max (3.3, 3.202) = 3.3

55kkkkkkkkkkkkkk

))SSSSS

SSSSSS

SSS

(14.256 − 12)+ = 2.256

max (1, 1.7667) = 1.7667

;;wwwwwwwwwwwwwwwwwwwww

##GGG

GGGG

GGGG

GGGG

GGGG

GG

(14.256 − 12)+ = 2.256

max (0.9, 0.94) = 0.94

55kkkkkkkkkkkkkk

))SSSSS

SSSSSS

SSS

(11.664 − 12)+ = 0

7: The CRR Market Model

Example: Replicating Strategy

Example (7.1 Continued)

Holder. The rational holder should exercise the Americanoption at time t = 1 if the stock price rises during the firstperiod. Otherwise, the option should be held till time 2.Hence τ∗0 : Ω → 0, 1, 2 equals

τ∗0 (ω) = 1 for ω ∈ ω1, ω2τ∗0 (ω) = 2 for ω ∈ ω3, ω4

Issuer. We now take the position of the issuer of the option.At t = 0, we need to solve

1.2φ00 + 13.2φ1

0 = 3.3

1.2φ00 + 10.8φ1

0 = 0.94

Hence (φ00, φ

10) = (−8.067, 0.983) for all ω.

7: The CRR Market Model

Example: Replicating Strategy

Example (7.1 Continued)

If the stock price rises during the first period, the option isexercised and thus we do not need to compute the strategy attime 1 for ω ∈ ω1, ω2.If the stock price falls during the first period, we solve

1.2 φ01 + 14.256φ1

1 = 2.256

1.2 φ01 + 11.664φ1

1 = 0

Hence (φ01, φ

11) = (−8.46, 0.8704) for ω ∈ ω3, ω4.

Note that φ01 = −8.46 is the amount of cash borrowed at time

1, rather than the number of units of the savings account B .

The replicating strategy φ = (φ0, φ1) is defined at time 0 forall ω and it is defined at time 1 on the event ω3, ω4 only.

7: The CRR Market Model

− − −

V u1 (φ) = 3.3

55llllllllllllll

))RRRRR

RRRRRR

RRR

− − −

(φ00, φ

10) = (−8.067, 0.983)

::ttttttttttttttttttttt

$$HHH

HHHH

HHHH

HHHH

HHHH

HHH

V du2 (φ) = 2.256

(φ01, φ

11) = (−8.46, 0.8704)

66lllllllllllll

((RRRRR

RRRRRR

RR

V dd2 (φ) = 0

7: The CRR Market Model

PART 5

IMPLEMENTATION OF THE CRR MODEL

7: The CRR Market Model

Derivation of u and d from r and σ

We fix maturity T and we assume that the continuouslycompounded interest rate r is such that B(0,T ) = e−rT .

From the market data for stock prices, one can estimate thestock price volatility σ per one time unit (typically, one year).

Note that until now we assumed that t = 0, 1, 2, . . . ,T , whichmeans that ∆t = 1. In general, the length of each period canbe any positive number smaller than 1. We set n = T/∆t.

Two widely used conventions for obtaining u and d from σand r are:

The Cox-Ross-Rubinstein (CRR) parametrisation:

u = eσ√

∆t and d =1

u.

The Jarrow-Rudd (JR) parameterisation:

u = e

(r− σ

2

2

)∆t +σ

√

∆tand d = e

(r− σ

2

2

)∆t − σ

√

∆t.

7: The CRR Market Model

The CRR parameterisation

Proposition (7.8)

Assume that Bk∆t = (1 + r∆t)k for every k = 0, 1, . . . , n and

u = 1d= eσ

√∆t in the CRR model. Then the risk-neutral

probability measure P satisfies

P (St+∆t = Stu |St ) =1

2+

r − σ2

2

2σ

√∆t + o(

√∆t)

provided that ∆t is sufficiently small.

Proof of Proposition 7.8.

The risk-neutral probability measure for the CRR model is given by

p = P (St+∆t = Stu |St ) =1 + r∆t − d

u − d

7: The CRR Market Model

The CRR parameterisation

Proof of Proposition 7.8.

Under the CRR parametrisation, we obtain

p =1 + r∆t − d

u − d=

1 + r∆t − e−σ√∆t

eσ√∆t − e−σ

√∆t

.

The Taylor expansions up to the second order term are

eσ√∆t = 1 + σ

√∆t +

σ2

2∆t + o(∆t)

e−σ√∆t = 1− σ

√∆t +

σ2

2∆t + o(∆t)

7: The CRR Market Model

The CRR parameterisation

Proof of Proposition 7.8.

By substituting the Taylor expansions into the risk-neutralprobability measure, we obtain

p =1 + r∆t −

(1− σ

√∆t + σ

2

2 ∆t)+ o(∆t)

(1 + σ

√∆t + σ

2

2 ∆t)−(1− σ

√∆t + σ

2

2 ∆t)+ o(∆t)

=σ√∆t +

(r − σ

2

2

)∆t + o(∆t)

2σ√∆t + o(∆t)

=1

2+

r − σ2

2

2σ

√∆t + o(

√∆t)

as was required to show.

7: The CRR Market Model

The CRR parameterisation

To summarise, for ∆t sufficiently small, we get

p =1 + r∆t − e−σ

√∆t

eσ√∆t − e−σ

√∆t

≈ 1

2+

r − σ2

2

2σ

√∆t.

Note that 1 + r∆t ≈ er∆t when ∆t is sufficiently small.

Hence the risk-neutral probability measure can also berepresented as follows

p ≈ er∆t − e−σ√∆t

eσ√∆t − e−σ

√∆t

.

More formally, if we define r such that (1 + r)n = erT for afixed T and n = T/∆t then r ≈ r∆t since ln(1 + r) = r∆t

and ln(1 + r) ≈ r when r is close to zero.

7: The CRR Market Model

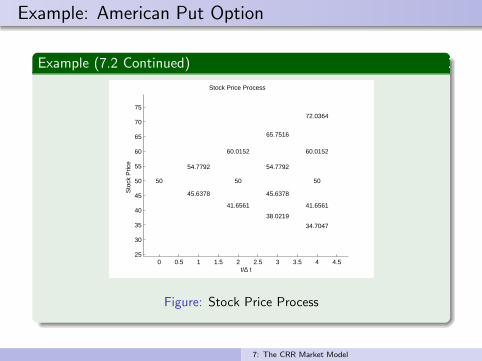

Example: American Put Option

Example (7.2 – CRR Parameterisation)

Let the annualized variance of logarithmic returns be σ2 = 0.1.

The interest rate is set to r = 0.1 per annum.

Suppose that the current stock price is S0 = 50.

We examine European and American put options with strikeprice K = 53 and maturity T = 4 months (i.e. T = 1

3).

The length of each period is ∆t = 112 , that is, one month.

Hence n = T∆t

= 4 steps.

We adopt the CRR parameterisation to derive the stock price.

Then u = 1.0956 and d = 1/u = 0.9128.

We compute 1 + r∆t = 1.00833 ≈ er∆t and p = 0.5228.

7: The CRR Market Model

Example: American Put Option

Example (7.2 Continued)

0 0.5 1 1.5 2 2.5 3 3.5 4 4.525

30

35

40

45

50

55

60

65

70

75

50

54.7792

45.6378

60.0152

50

41.6561

65.7516

54.7792

45.6378

38.0219

72.0364

60.0152

50

41.6561

34.7047

t/∆ t

Sto

ck P

rice

Stock Price Process

Figure: Stock Price Process

7: The CRR Market Model

Example: American Put Option

Example (7.2 Continued)

0 0.5 1 1.5 2 2.5 3 3.5 4 4.525

30

35

40

45

50

55

60

65

70

750

0

3

11.3439

18.2953

0

1.4198

6.9242

14.5401

0.67199

4.0132

10.4714

2.2478

7.0366

4.4957

t/∆ t

Sto

ck P

rice

Price Process of the European Put Option

Figure: European Put Option Price

7: The CRR Market Model

Example: American Put Option

Example (7.2 Continued)

0 0.5 1 1.5 2 2.5 3 3.5 4 4.525

30

35

40

45

50

55

60

65

70

750

0

3

11.3439

18.2953

0

1.4198

7.3622

14.9781

0.67199

4.2205

11.3439

2.3459

7.557

4.7928

t/∆ t

Sto

ck P

rice

Price Process of the American Put Option

Figure: American Put Option Price

7: The CRR Market Model

Example: American Put Option

Example (7.2 Continued)

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

30

40

50

60

70

80

1

1

1

1

1

1

0

1

1

0

0

1

0

0

0

t/∆ t

Sto

ck P

rice

1: Exercise the American Put; 0: Hold the American Option

Figure: Rational Exercise Policy

7: The CRR Market Model

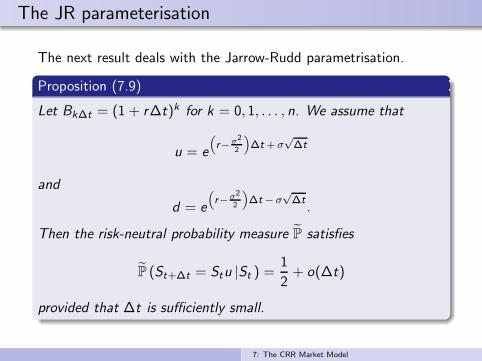

The JR parameterisation

The next result deals with the Jarrow-Rudd parametrisation.

Proposition (7.9)

Let Bk∆t = (1 + r∆t)k for k = 0, 1, . . . , n. We assume that

u = e

(r−σ2

2

)∆t + σ

√∆t

and

d = e

(r−σ2

2

)∆t − σ

√∆t

.

Then the risk-neutral probability measure P satisfies

P (St+∆t = Stu |St ) =1

2+ o(∆t)

provided that ∆t is sufficiently small.

7: The CRR Market Model

The JR parameterisation

Proof of Proposition 7.9.

Under the JR parametrisation, we have

p =1 + r∆t − d

u − d=

1 + r∆t − e

(r−σ2

2

)∆t−σ

√∆t

e

(r−σ2

2

)∆t+σ

√∆t − e

(r−σ2

2

)∆t−σ

√∆t

.

The Taylor expansions up to the second order term are

e

(r−σ2

2

)∆t+σ

√∆t

= 1 + r∆t + σ√∆t + o(∆t)

e

(r−σ2

2

)∆t−σ

√∆t

= 1 + r∆t − σ√∆t + o(∆t)

and thus

p =1

2+ o(∆t).

7: The CRR Market Model

Example: American Put Option

Example (7.3 – JR Parameterisation)

We consider the same problem as in Example 7.2, but withparameters u and d computed using the JR parameterisation.We obtain u = 1.1002 and d = 0.9166.

As before, 1 + r∆t = 1.00833 ≈ er∆t , but p = 0.5.

We compute the price processes for the stock, the Europeanput option, the American put option and we find the rationalexercise time.

When we compare with Example 7.2, we see that the resultsare slightly different than before, although it appears that therational exercise policy is the same.

The CRR and JR parameterisations are both set to approachthe Black-Scholes model.

For ∆t sufficiently small, the prices computed under the twoparametrisations will be very close to one another.

7: The CRR Market Model

Example: American Put Option

Example (7.3 Continued)

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

30

40

50

60

70

80

50

55.0079

45.8283

60.5174

50.4184

42.0047

66.5787

55.4682

46.2118

38.5001

73.2471

61.0238

50.8403

42.3562

35.2879

t/∆ t

Sto

ck P

rice

Stock Price Process

Figure: Stock Price Process

7: The CRR Market Model

Example: American Put Option

Example (7.3 Continued)

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

30

40

50

60

70

80

0

0

2.1597

10.6438

17.7121

0

1.0709

6.3488

14.0607

0.53103

3.6792

10.1204

2.0877

6.8428

4.4284

t/∆ t

Sto

ck P

rice

Price Process of the European Put Option

Figure: European Put Option Price

7: The CRR Market Model

Example: American Put Option

Example (7.3 Continued)

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

30

40

50

60

70

80

0

0

2.1597

10.6438

17.7121

0

1.0709

6.7882

14.4999

0.53103

3.8971

10.9953

2.1958

7.3846

4.7506

t/∆ t

Sto

ck P

rice

Price Process of the American Put Option

Figure: American Put Option Price

7: The CRR Market Model

Example: American Put Option

Example (7.3 Continued)

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

30

40

50

60

70

80

1

1

1

1

1

1

0

1

1

0

0

1

0

0

0

t/∆ t

Sto

ck P

rice

1: Exercise the American Put; 0: Hold the American Option

Figure: Rational Exercise Policy

7: The CRR Market Model