Beurs stappenplan sessie 1

107

EFFICIËNT VERMOGENSBEHEER INLEIDEND KADER Enkele Principes en Concrete Toepassingen 07/02/2022 1 [email protected] 32 474 977 464

-

Upload

ekonomikabeursstappenplan -

Category

Education

-

view

390 -

download

3

description

Beurs Stappenplan: Sessie 1 (Stefaan Duchateau)

Transcript of Beurs stappenplan sessie 1

1

EFFICIËNT VERMOGENSBEHEER

INLEIDEND KADER

Enkele Principes en Concrete Toepassingen

10/04/2023

[email protected]+32 474 977 464

2

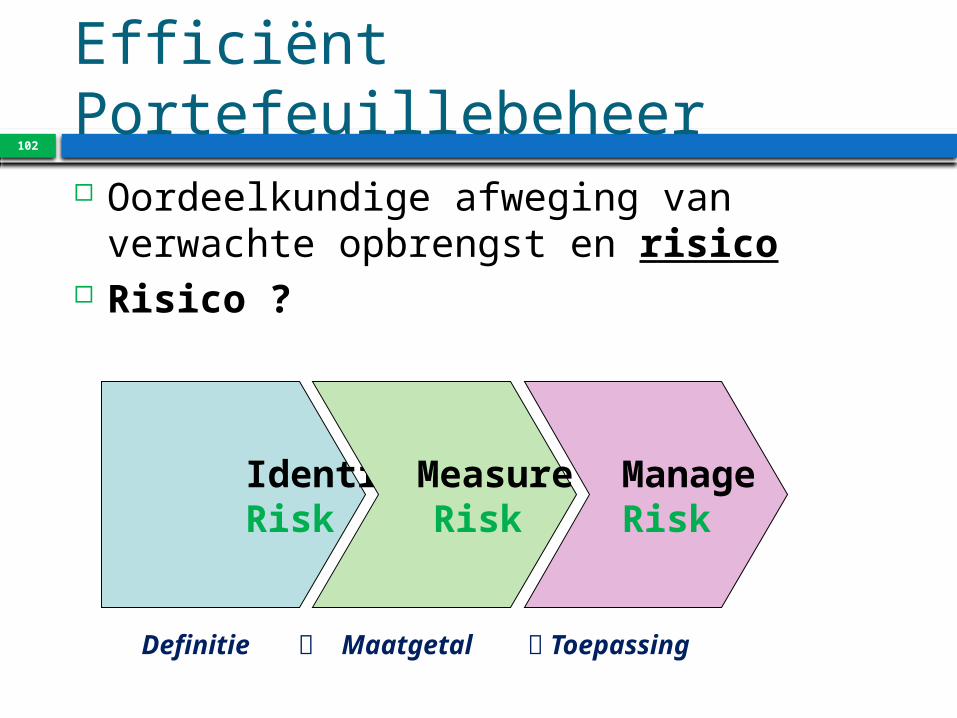

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico …“In a hole in the ground there lived a hobbit”

“Not a nasty, dirty, wet hole, filled with the ends of worms and an oozy smell, nor yet a dry, bare, sandy hole with nothing in it to sit down on or to eat: it was a hobbit-hole, and that means comfort …”

10/04/2023

3

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

Oordeelkundig Principes voor coherente keuze van asset

klassen, individuele waarden, … ?

Afweging Welk keuzecriterium ?

10/04/2023

4

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

Verwachte opbrengst ?Beknopte historische schets

Statistische interpretatieDynamische interpretatie

Model ?Actief portefeuillebeheer

5

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

Risico ?

Identify Risk

Measure Risk

Manage Risk

Definitie Maatgetal Toepassing

10/04/2023

6

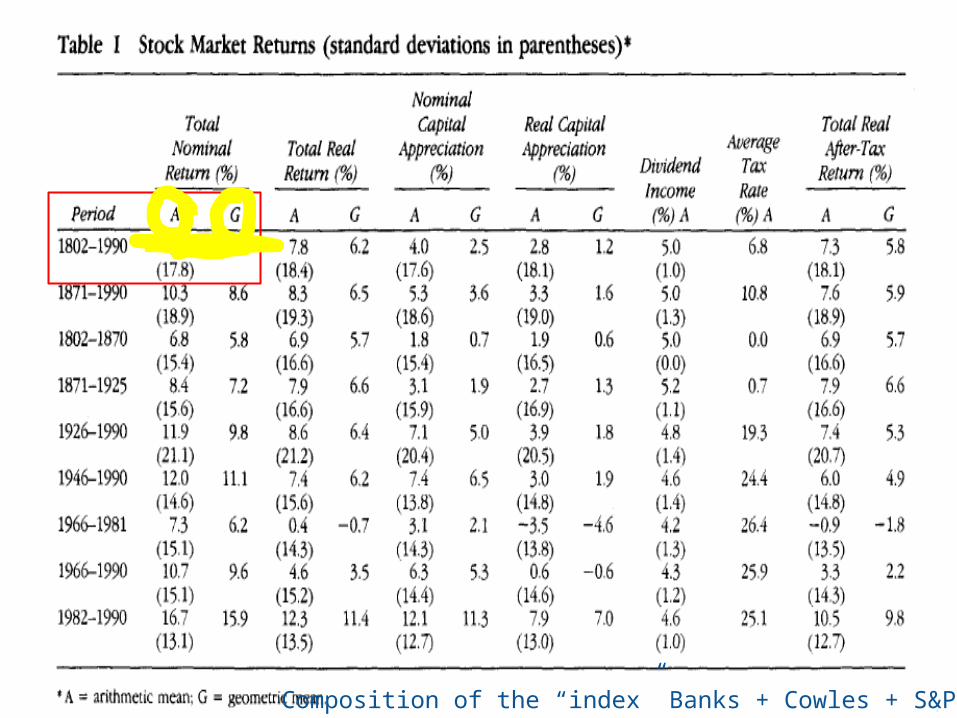

Verwachte Opbrengst

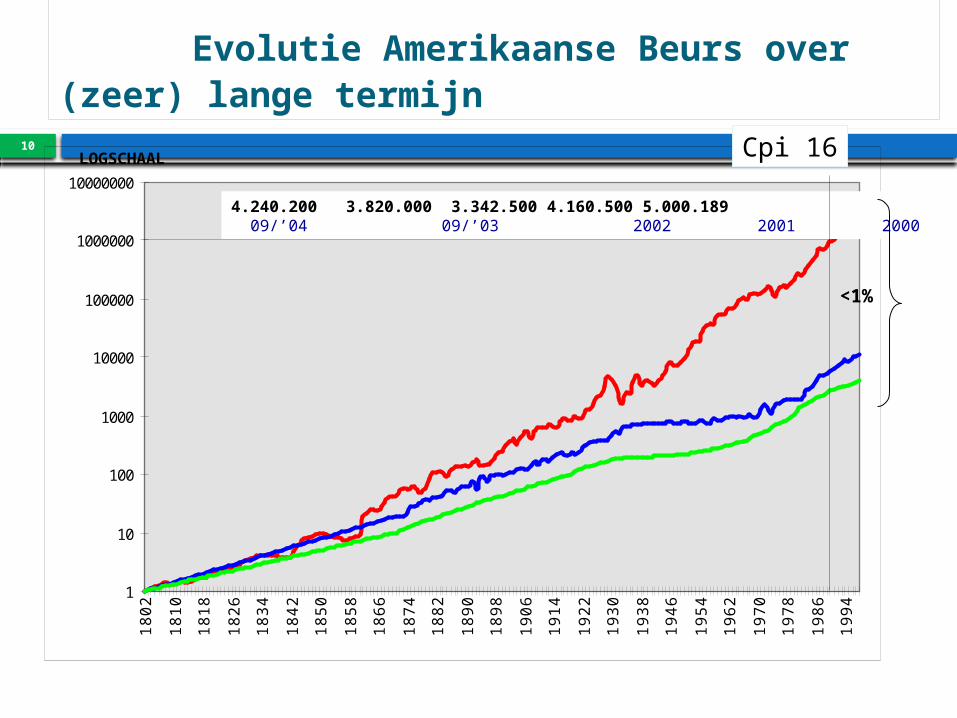

J. Siegel 1802-1990 Repliek op Equity Premium Paradox Gemiddelde GR = 7,6% SDN ~18%

So what ? Survivorship bias ? Merkwaardige outperformance van aandelen over andere

asset klasses (EPP) 2.7% A over B Merkwaardige stabiliteit van reële returns van aandelen over

deelperiodes Outperformance niet eenduidig in verband te brengen met

onderliggende economische reeksen $1 ~ $1.000.000 …

Evolutie 1990 – 2013 Gemiddelde GR = …

$1.000.000 …

Advanced Portfolio Management7

Nadien bestseller :Stocks for the long run

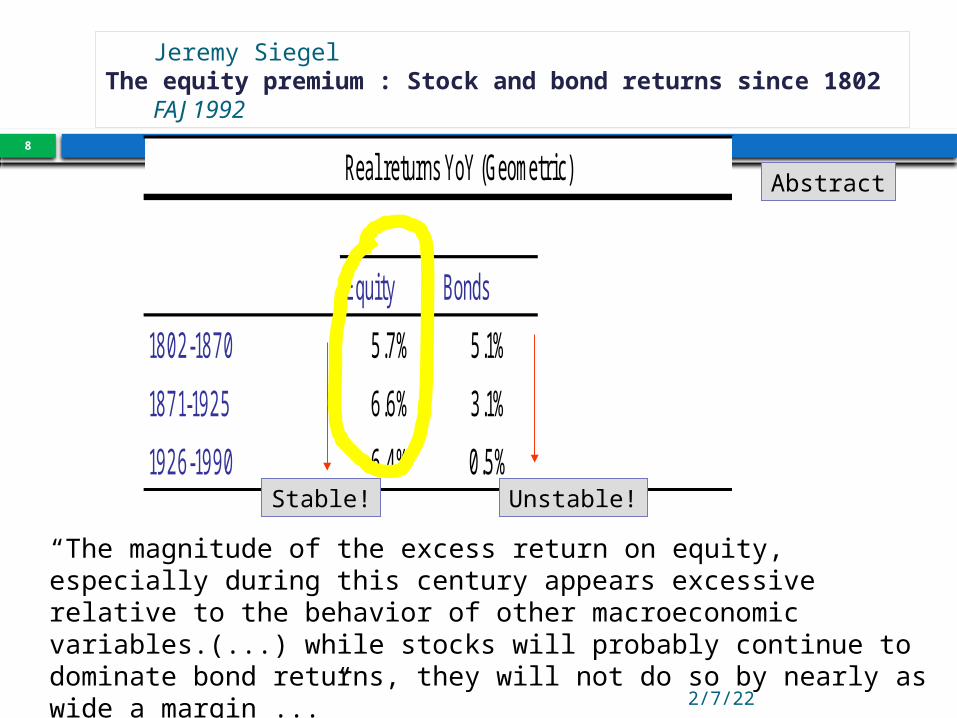

Jeremy SiegelThe equity premium : Stock and bond returns since 1802

FAJ 1992

Apr 10, 2023

8

Real returns YoY (Geometric)

Equity Bonds

1802-1870 5.7% 5.1%

1871-1925 6.6% 3.1%

1926-1990 6.4% 0.5%

“The magnitude of the excess return on equity, especially during this century appears excessive relative to the behavior of other macroeconomic variables.(...) while stocks will probably continue to dominate bond returns, they will not do so by nearly as wide a margin ...”

Abstract

Stable! Unstable!

Apr 10, 20239

Jeremy SiegelThe equity premium :Stock and bond returns since 1802FAJ 1992

1802

Evolutie Amerikaanse Beurs over (zeer) lange termijn

10

1

10

100

1000

10000

100000

1000000

10000000

1802

1810

1818

1826

1834

1842

1850

1858

1866

1874

1882

1890

1898

1906

1914

1922

1930

1938

1946

1954

1962

1970

1978

1986

1994

4.240.200 3.820.000 3.342.500 4.160.500 5.000.189 09/’04 09/’03 2002 2001 2000

LOGSCHAAL

<1%

Cpi 16

21

Total Return index S&P Comp

Apr 10, 2023

11

Advanced Portfolio Management

17/10/13919293949596979899000102030405060708091011120100200300400500600700800900S&P 500 COMPOSITE - TOT RETURN INDSource: Thomson Datastream

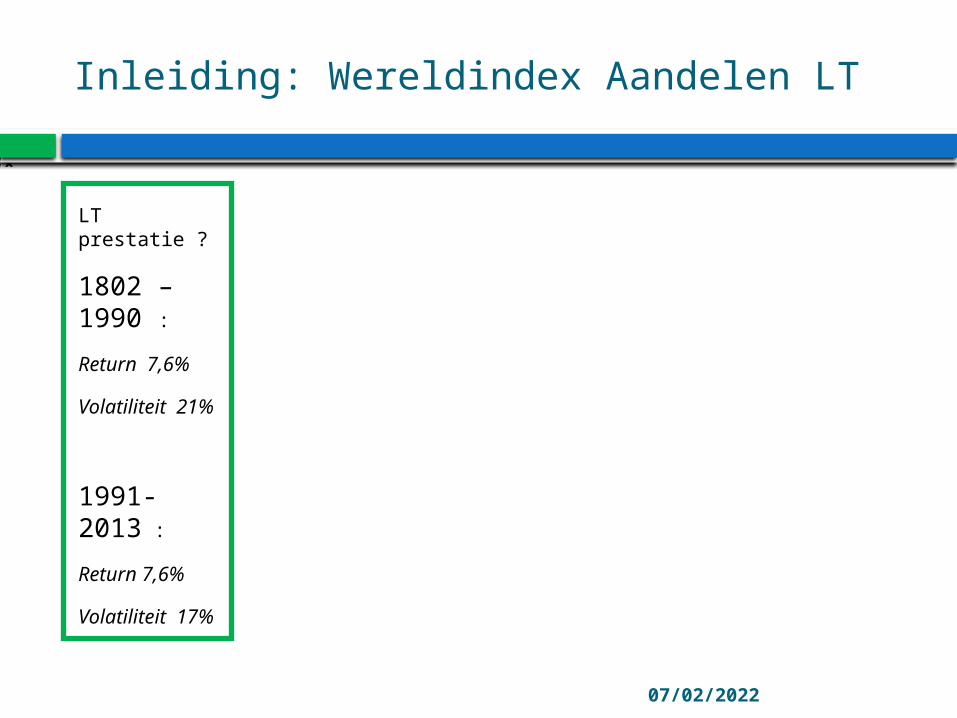

Inleiding: Wereldindex Aandelen LT

10/04/2023

LT prestatie ?

1802 –1990 :

Return 7,6%

Volatiliteit 21%

1991-2013 :

Return 7,6%

Volatiliteit 17%

17/10/13919293949596979899000102030405060708091011120100200300400500600700MSCI WORLD U$ - TOT RETURN IND (~E )Source: Thomson Datastream

Apr 10, 2023Advanced Portfolio Management13Composition of the “index” Banks + Cowles + S&P

14

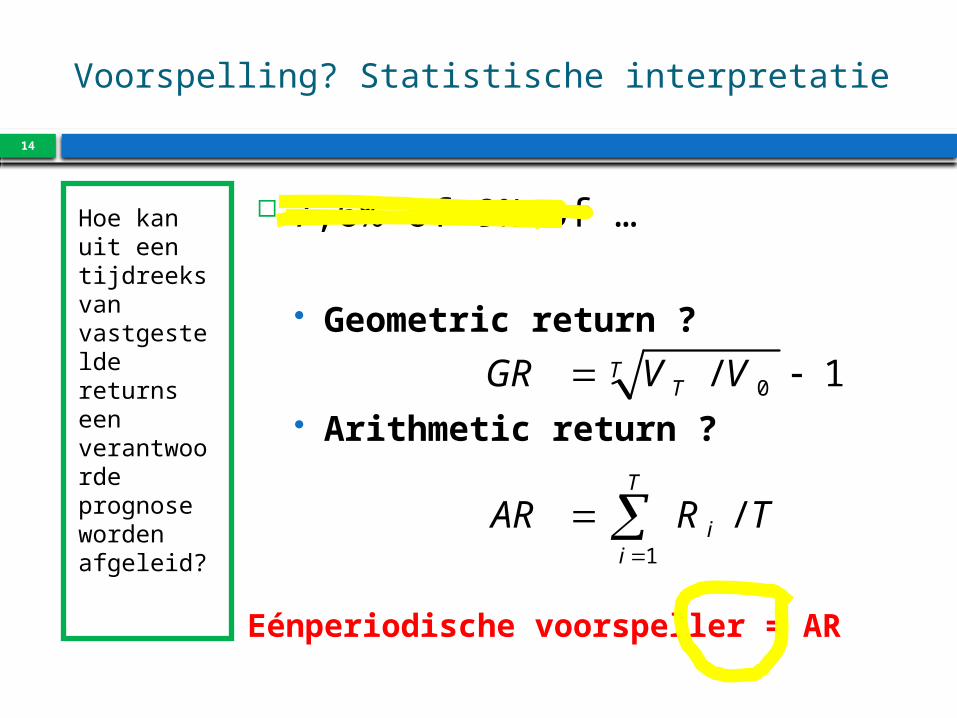

Voorspelling? Statistische interpretatie

Hoe kan uit een tijdreeks van vastgestelde returns een verantwoorde prognose worden afgeleid?

7,6% of 9% of …

Geometric return ?

Arithmetic return ?

TRAR

VVGR

T

ii

TT

/

1/

1

0

Eénperiodische voorspeller = AR

10/04/2023

15

10/04/2023

16

10/04/2023

17

18

Verklaring? Dynamische interpretatie (1)

Lagere verwachte risicopremie leidt tot hogere gerealiseerde risicopremie …

Uit het Dividend Discount Model kunnen nuttige suggesties worden afgeleid over de dynamiek op financiële markten

¾ wordt verklaard door gedrag van de verwachte risicopremie

FM

NEW0NEW

M

2NEWM

10

FMNEW

FNEWM

stijgen Θ rdegerealisee de zal dan

daalt verwachte de indien paribus, ceteris

FM

M

3

M

2

M

10

RR

P..²ER(1

DIVER1DIV

P

)E(RER )(ERER

)E(RER

...)³ER(1

DIV)²ER(1

DIVER1

DIVP

1/PP 0NEW0

, Θ

.)

04:58 AM

19

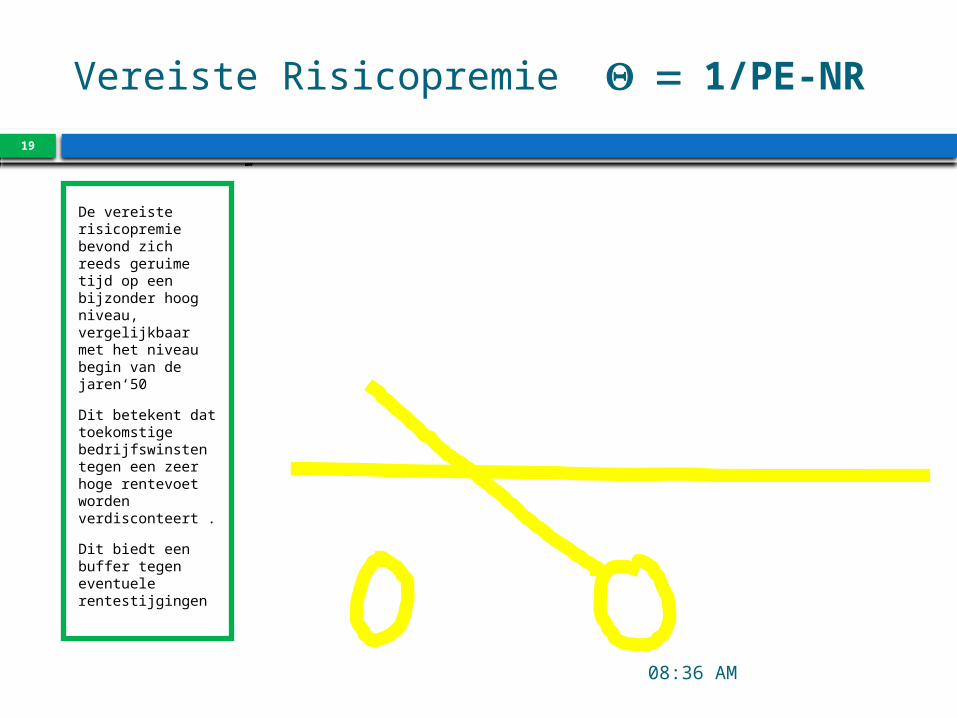

Vereiste Risicopremie = Q 1/PE-NR

De vereiste risicopremie bevond zich reeds geruime tijd op een bijzonder hoog niveau, vergelijkbaar met het niveau begin van de jaren‘50

Dit betekent dat toekomstige bedrijfswinsten tegen een zeer hoge rentevoet worden verdisconteert .

Dit biedt een buffer tegen eventuele rentestijgingen

100/@:USSP500(AF1PE)-0.6*AUSGVG1(RY)17/10/13838587899193959799010305070911-10123456789100/@:USSP500(AF1PE)-0.6*AUSGVG1(RY)Source: Thomson Datastream

10/04/2023

20

Verklaring? Dynamische interpretatie (1)

Uit DDM kan worden afgeleid:

dP/P ~= - D*( dRF + dQ - dG)

D* ~1/DY1

FRMR

M

10 ER

DIVP

g

Financiële Mechanica

Apr 10, 2023

21

Rente Groei beursoblig cash

1

2

3

4

Z

H

W

L

Hypothese : stabiele verwachte risicopremie !

dP/P ~= - D*( dR + dQ - dG)

22

Financiële Mechanica

10/04/2023

Asset Allocatie en Individuele Selectie

Belang van Asset Allocatie ? 90/10

Verklaring van de Variantie over tijd van een beheerder

Bij nader onderzoek : 50/50

Individuele selectie en asset allocatie verklaren ongeveer evenveel van de variantie tussen beheerders.

Model voor coherente keuze van Asset Allocatie en voor individuele keuzes ?

23

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

?

24

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

Oordeelkundig Principes voor coherente keuze van asset

klassen, individuele waarden, … ? EXPECTED UTILITY

Afweging Welk keuzecriterium ?

Apr 10, 202325

w+x1w+x1 w+x2w+x2

Expected Utility Paradigm

U(w+x2)

U(w+x1)

w+m

U(w+m)

Eu(w+x)

p

w+m-pw+m-p

Apr 10, 2023

26

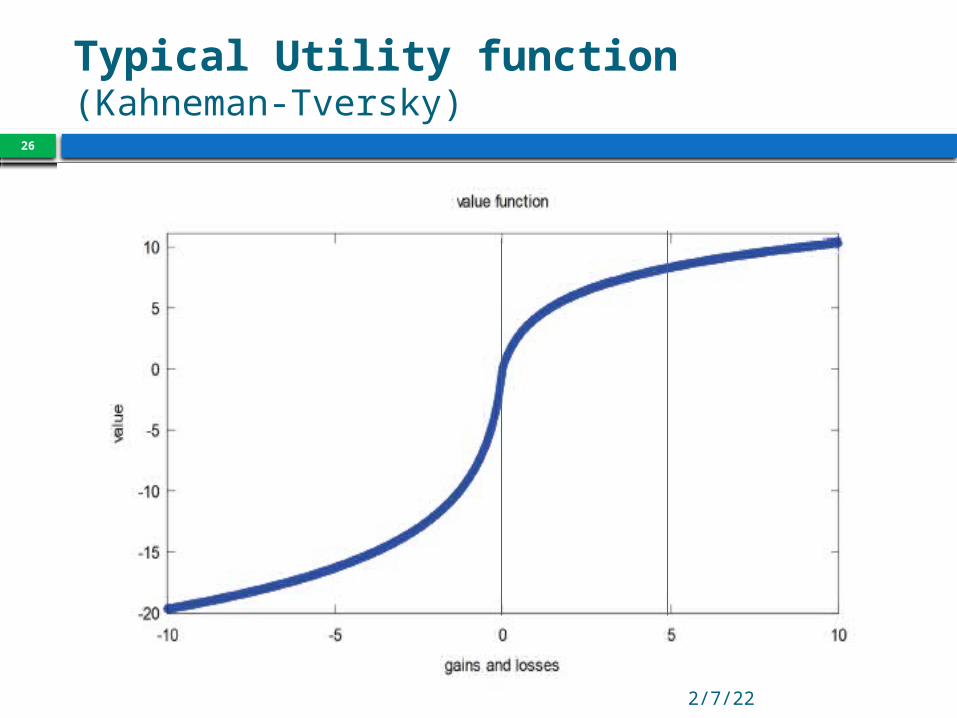

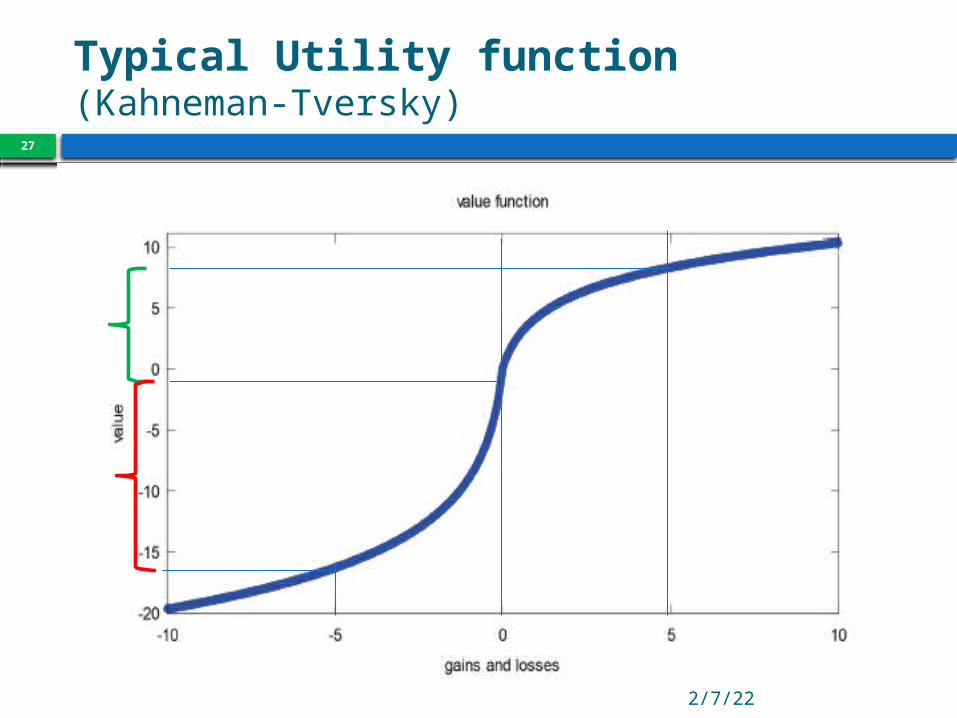

Typical Utility function (Kahneman-Tversky)

Apr 10, 2023

27

Typical Utility function (Kahneman-Tversky)

Apr 10, 2023

28

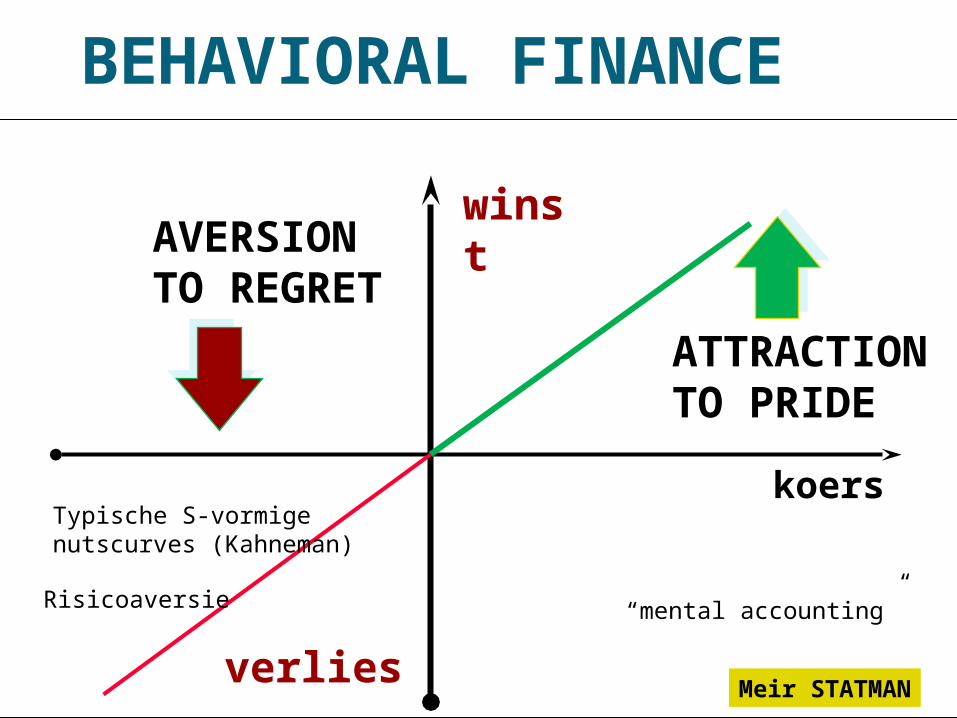

BEHAVIORAL FINANCE

koers

winst

verlies

AVERSIONTO REGRET

ATTRACTIONTO PRIDE

Meir STATMAN

Typische S-vormigenutscurves (Kahneman)

Risicoaversie “mental accounting”

10/04/2023

29

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

Oordeelkundig Principes voor coherente keuze van asset

klassen, individuele waarden, … ? EXPECTED UTILITY

Afweging Welk keuzecriterium ?

Apr 10, 202330

(.)'''6

³(.)''

2

²(.)~)~(

0)~(

(.)...'''6

)³~((.)''

2

)²~((.)')~((.)~)~(

(.))(

~

)...('''6

)³()(''

2

)²()(')()()(

uuuxwEu

xxE

uxxE

uxxE

uxxEuxwEu

uxwu

xwxwat

afat

afat

afataftf

Expected UtilityExpected Utility

Skewness is 0 if the underlying probability-distribution is normal

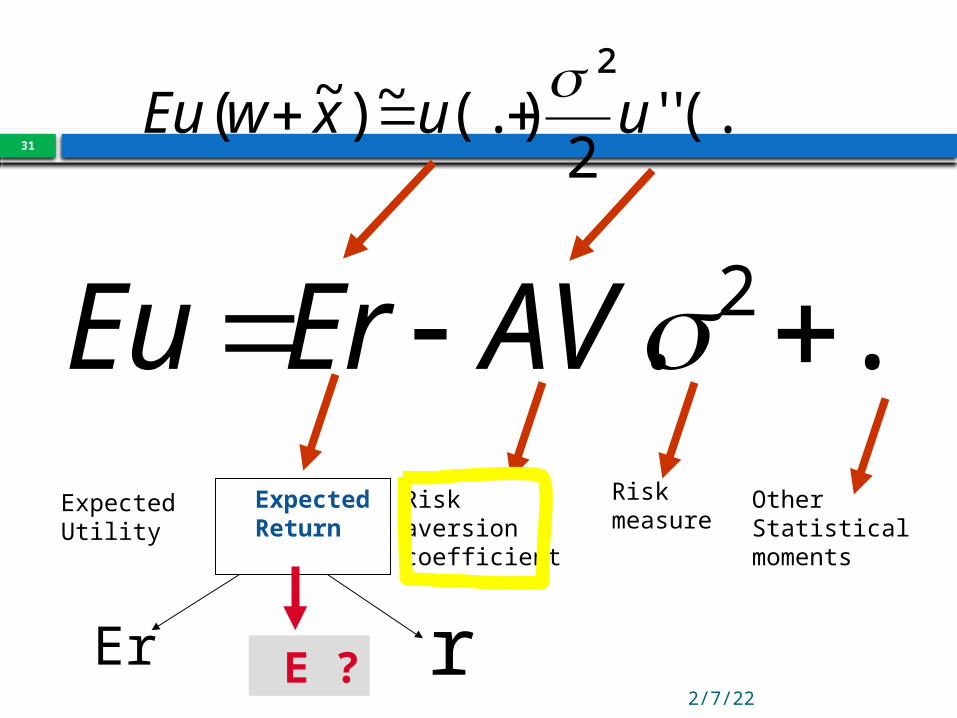

.... 2 AVErEu

Apr 10, 2023

31

.... 2 AVErEuExpectedUtility

ExpectedReturn

Risk aversion coefficient

Riskmeasure

OtherStatisticalmoments

rEr E ?

(.)''2

²(.)~)~( uuxwEu

Apr 10, 2023

32

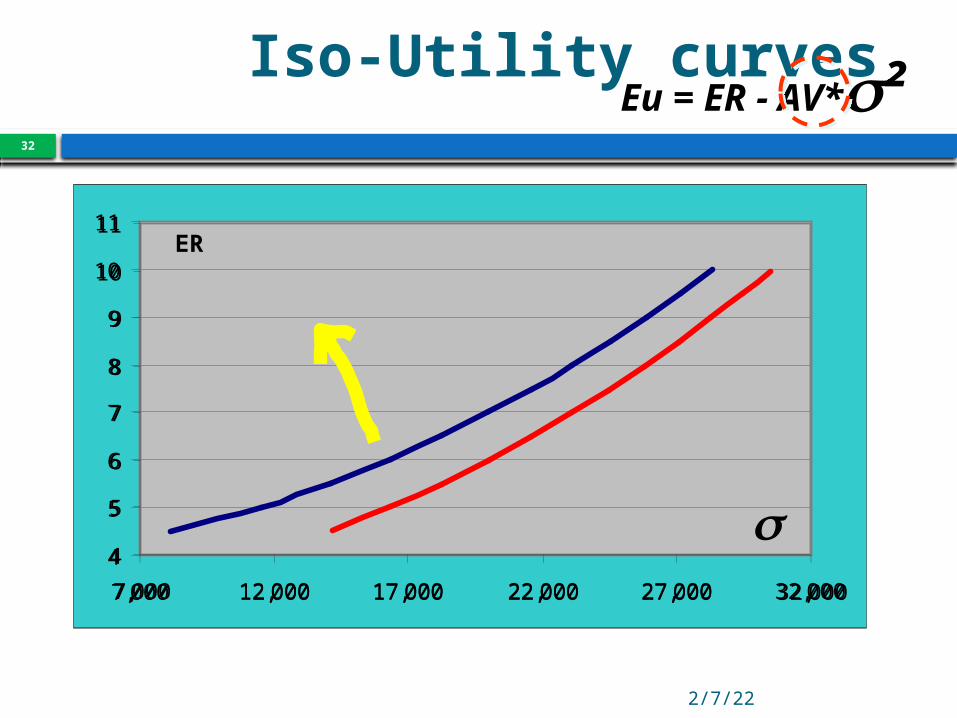

Iso-Utility curves

4

5

6

7

8

9

10

11

7,000 12,000 17,000 22,000 27,000 32,000

4

5

6

7

8

9

10

11

7,000 12,000 17,000 22,000 27,000 32,000

Eu = ER - AV*s²

ER

s

Apr 10, 202333

Impact correlatie r = 1.00

0.04

0.05

0.06

0.07

0.08

0.09

0.1

0 0.05 0.1 0.15 0.2 0.25

Return

Risk

Apr 10, 202334

Impact correlatie r = 0.20

0.04

0.05

0.06

0.07

0.08

0.09

0.1

0 0.05 0.1 0.15 0.2 0.25

Return

Risk

Apr 10, 2023

35

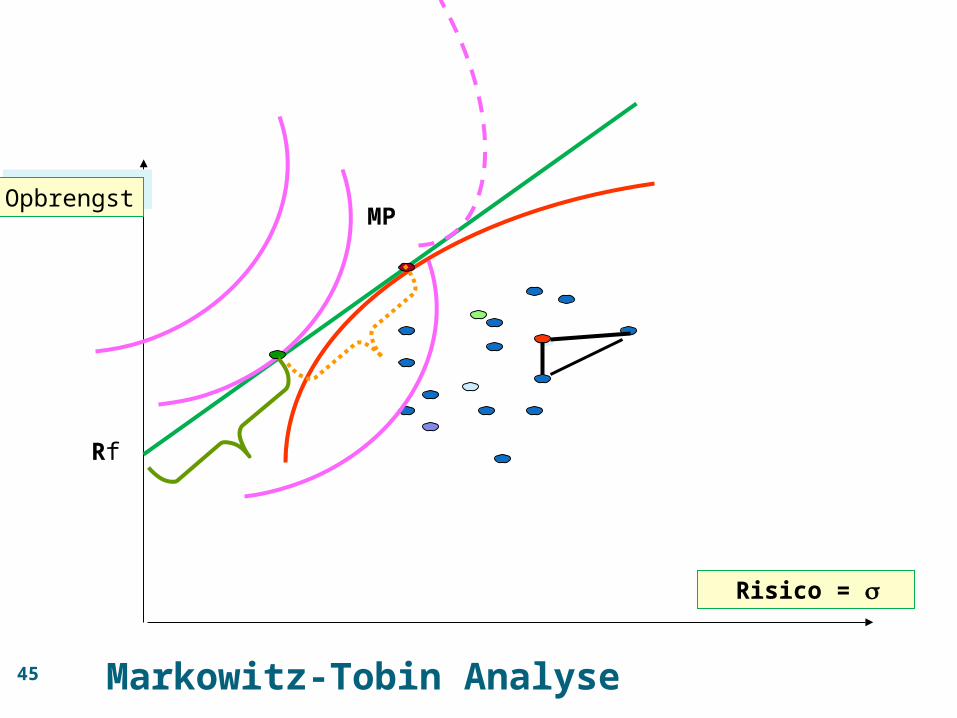

Efficient Frontier

36

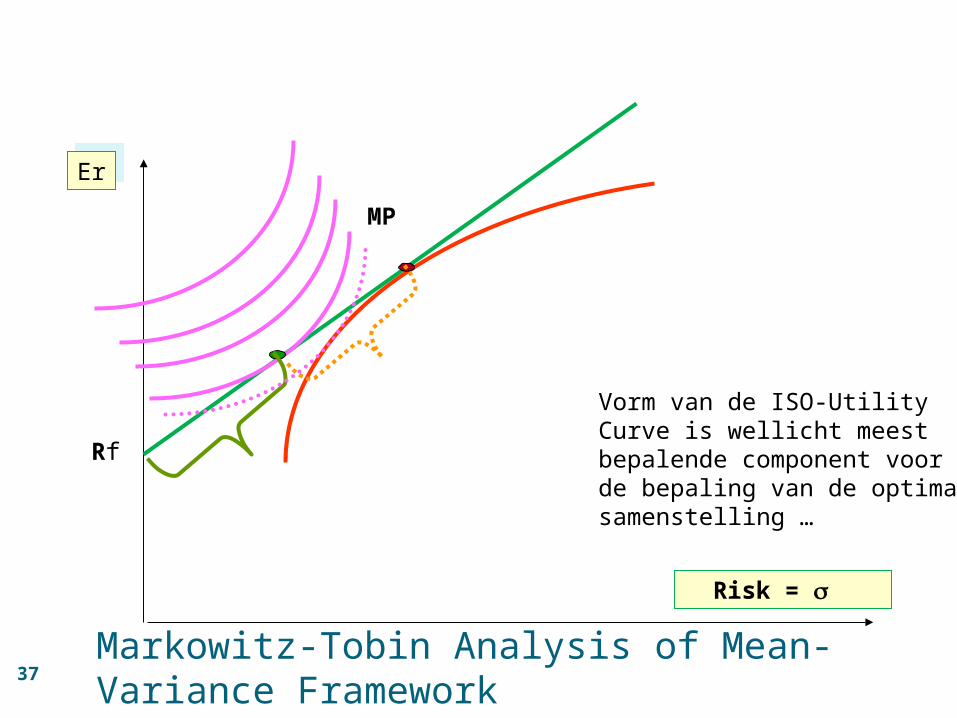

Markowitz-Tobin Analysis of Mean-Variance

Framework

Risk = s

return MP

Rf

ErEr

37Markowitz-Tobin Analysis of Mean-Variance Framework

Risk = s

return MP

Rf

ErEr

Vorm van de ISO-UtilityCurve is wellicht meestbepalende component voorde bepaling van de optimale samenstelling …

38

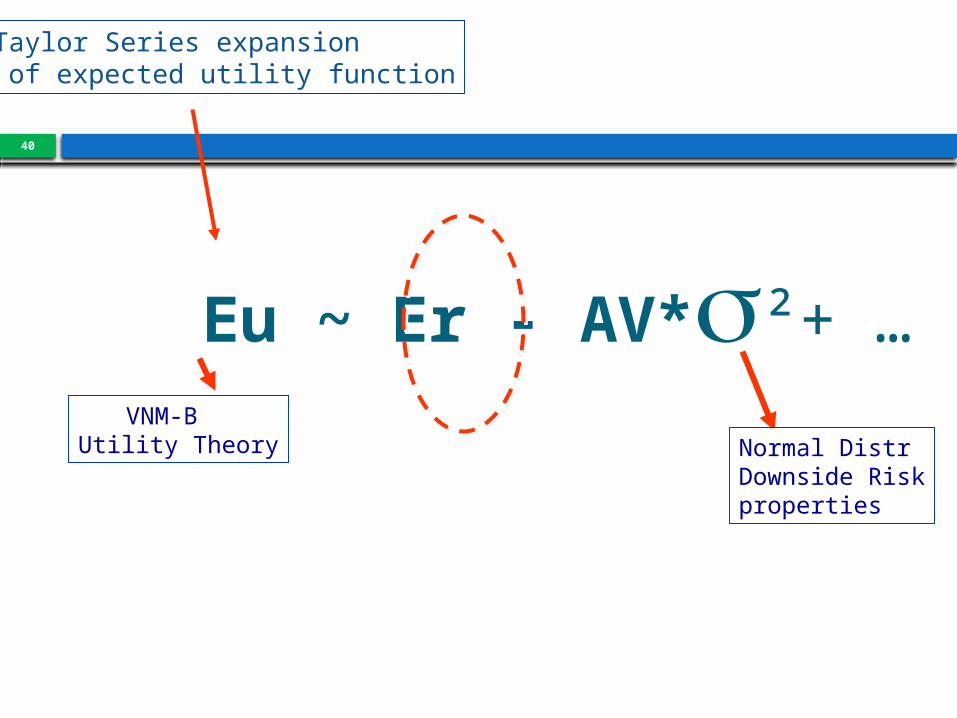

Eu ~ Er - AV*s²+ …VNM-BUtility Theory Normal Distr

Downside Riskproperties

Taylor Series expansion of expected utility function

Vermogen, inkomen, opleiding en leeftijd

genetische factor , sociale factor

39

Risico-Aversie en Leeftijd

10/04/2023

40

Eu ~ Er - AV*s²+ …VNM-B

Utility Theory Normal DistrDownside Riskproperties

Taylor Series expansion of expected utility function

41

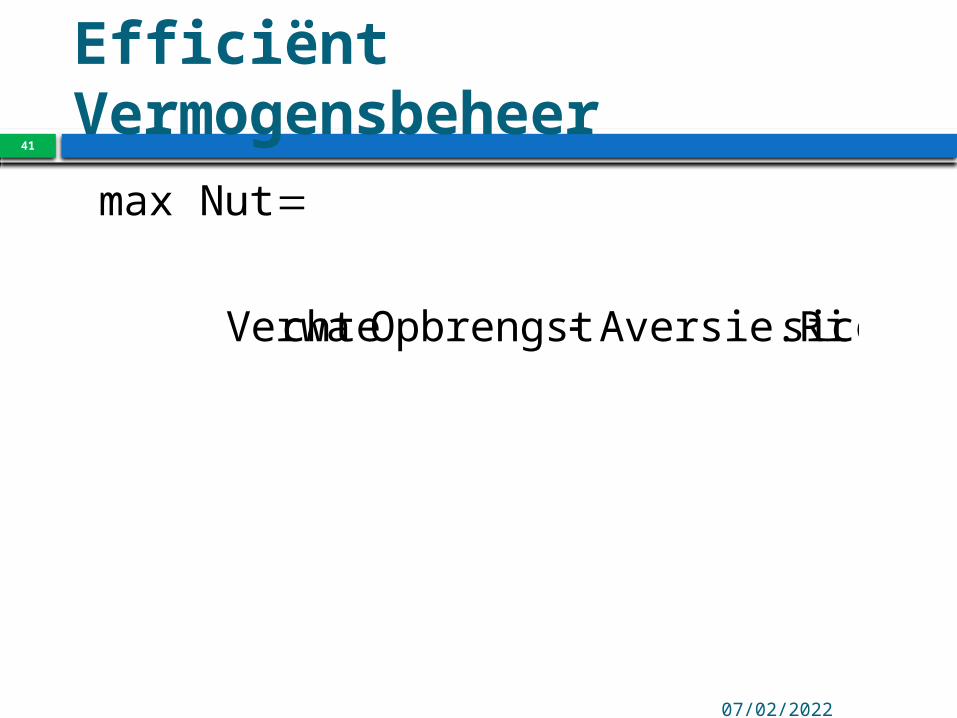

Efficiënt Vermogensbeheer

10/04/2023

sicoAversie.RiOpbrengst chte Verwa

Nutmax

42

Efficiënt Vermogensbeheer

10/04/2023

sicoAversie.RiOpbrengst chte Verwa

Nutmax

Asset Allocatie macro economische inschatting van relevante

parameters verwacht scenario

Individuele keuzes

43

Efficiënt Vermogensbeheer

10/04/2023

sicoAversie.RiOpbrengst chte Verwa

Nutmax

-Risicometing

-Risicobeheersing ? Neerwaartse Component

44

10/04/2023

sicoAversie.RiOpbrengst chte Verwa

Nutmax

Risicoweging Beleggersprofiel

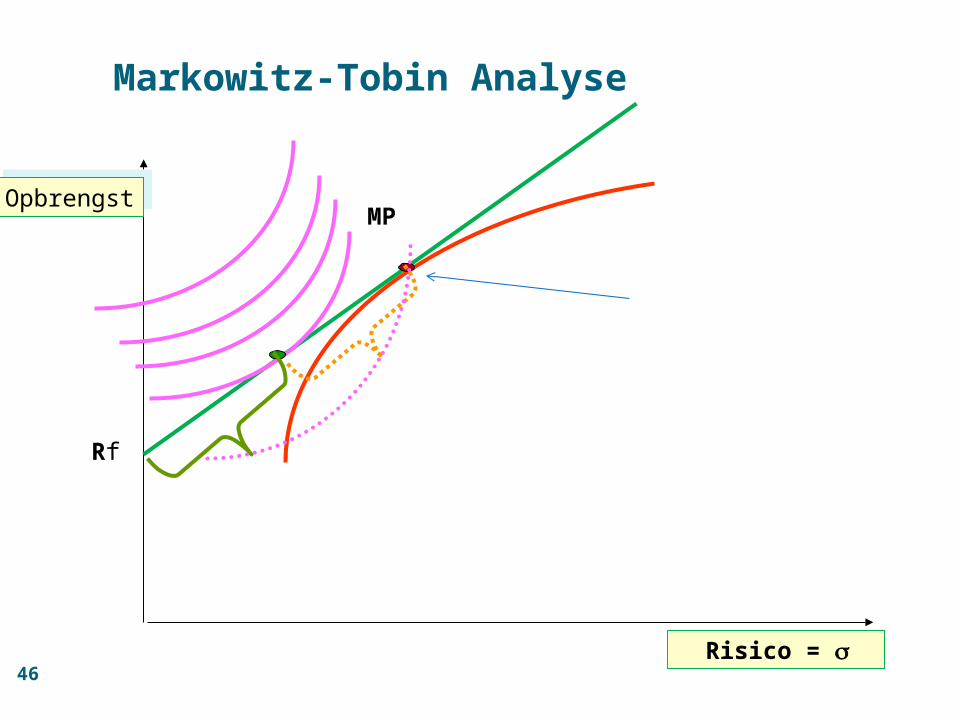

45 Markowitz-Tobin Analyse

Risico = s

return MP

Rf

OpbrengstOpbrengst

46

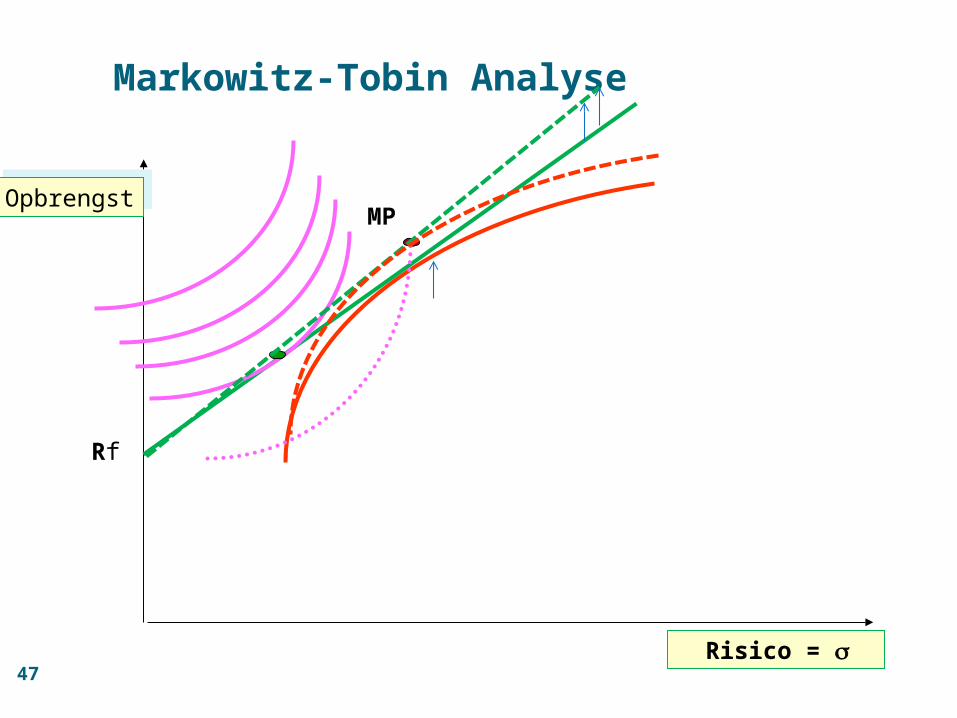

Markowitz-Tobin Analyse

Risico = s

return MP

Rf

OpbrengstOpbrengst

47

Markowitz-Tobin Analyse

Risico = s

return MP

Rf

OpbrengstOpbrengst

10/04/2023

48

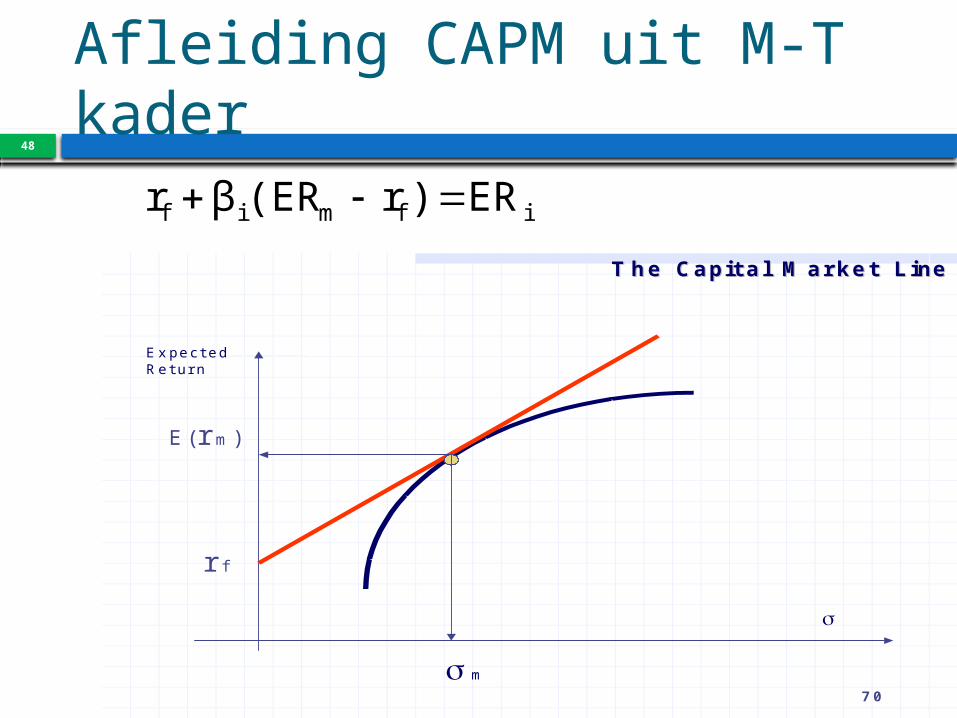

Afleiding CAPM uit M-T kader

70

r f

E(rm)

ExpectedReturn

The Capital Market LineThe Capital Market Line

m

ifmif ER)r(ERβr

49

Diversificatie

²σ²² σβ)²E(R²σ

Rβα)εRβE(αER

εRβαR

εmjjj

mjjjmjjj

jmjjj

?

50

Apr 10, 2023

ifmifi )r(RRR

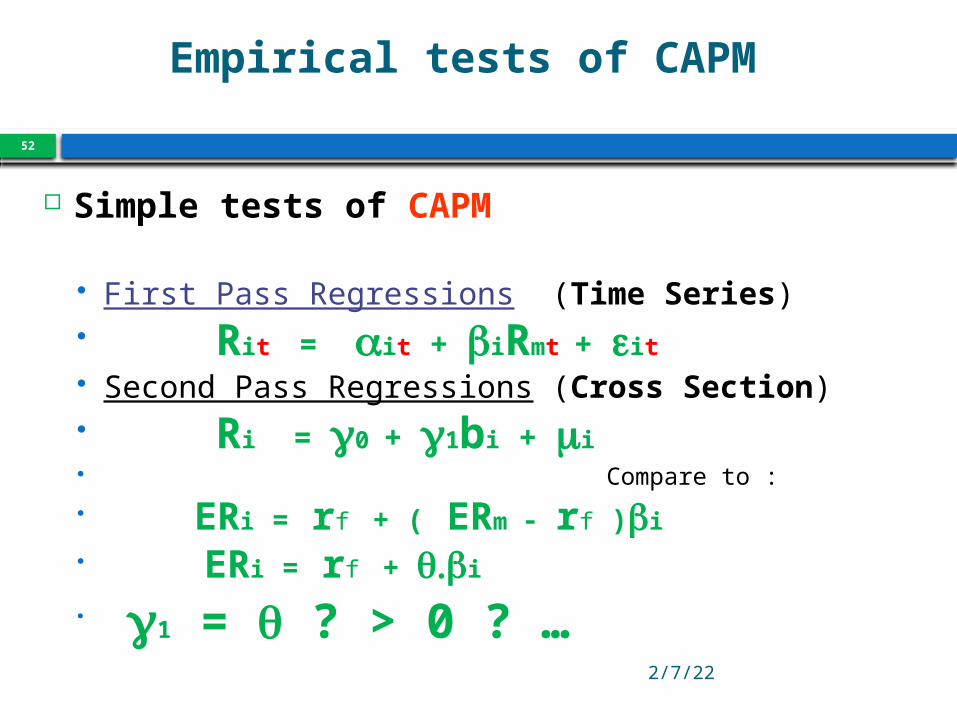

Empirical Tests of CAPM

2 purposes :

-Test whether a theory should be rejected

- Provide information that enables better financial decision making and improves the theoretical framework

51

i ifmifi )r(RRR

Empirical Tests of CAPM

00 RiskPremium

Noinfluence

Noinfluence

Linear in Beta ?

0...

52

Apr 10, 2023

Empirical tests of CAPM

Simple tests of CAPM

First Pass Regressions (Time Series) Rit = ait + biRmt + eit

Second Pass Regressions (Cross Section) Ri = g0 + g1bi + mi Compare to : ERi = rf + ( ERm - rf )bi

ERi = rf + .q bi

g1 = q ? > 0 ? …

Meaning of m and s over longer periods of time?

Neerwaarts risico

Apr 10, 2023

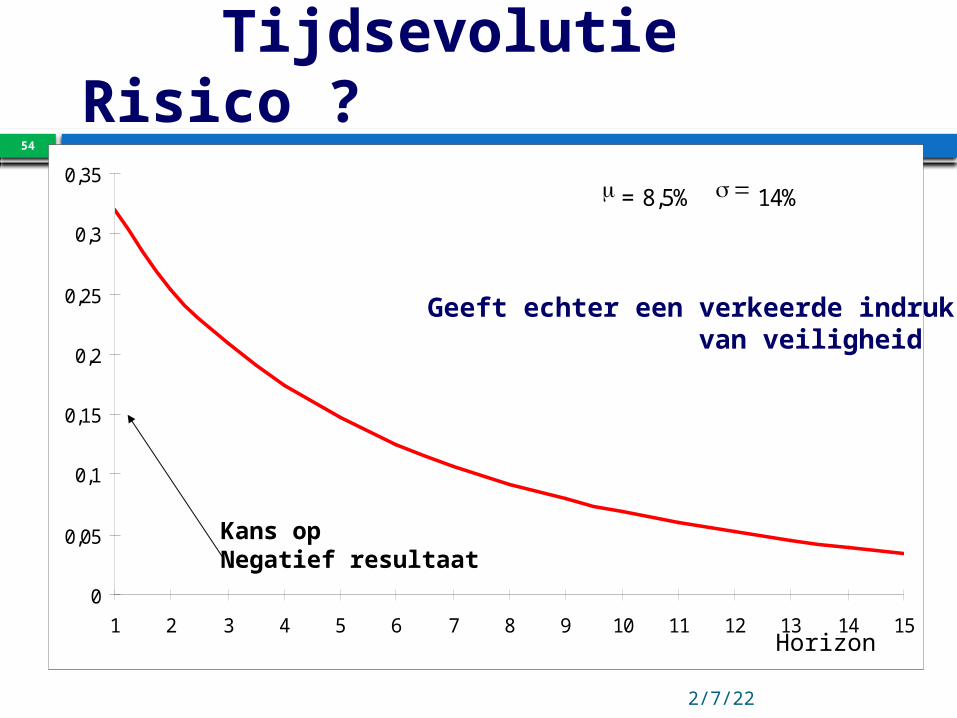

54

Tijdsevolutie Risico ?

0

0,05

0,1

0,15

0,2

0,25

0,3

0,35

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

m = 8,5% 14%

Geeft echter een verkeerde indruk van veiligheid

Kans op Negatief resultaat

Horizon

Apr 10, 2023

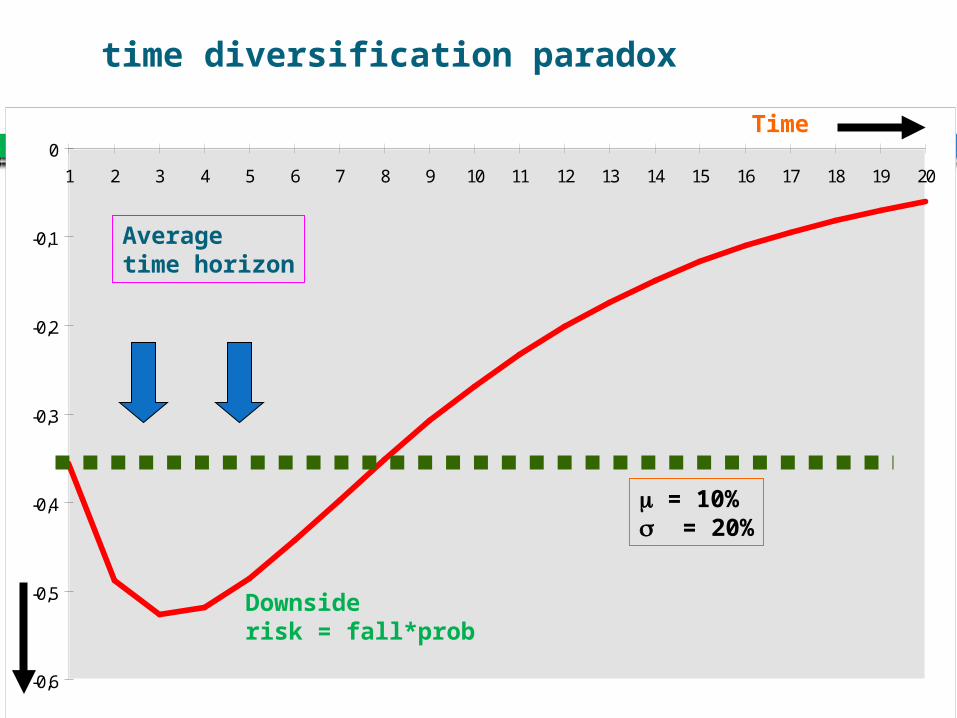

55

time diversification paradox

-0,6

-0,5

-0,4

-0,3

-0,2

-0,1

0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

m = 10%s = 20%

Averagetime horizon

Downsiderisk = fall*prob

Time

Apr 10, 2023

56

0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8 8.5 9 9.5 10

-25%

-20%

-15%

-10%

-5%

0%r 8%

s 25%

TR 0%

Tijdsevolutie neerwaarts risico

10/04/2023

57

Vermogensbeheer? Asset Allocatie

Efficiëntbeheer

Portefeuille

Constructie

Neerwaartse bescherming

Winst “Lock In”

Asset Allocation

Individuele selectie

10/04/2023

58

Asset Allocatie

Efficiëntbeheer

Portefeuille

Constructie Asset

Allocation

RenteSpread

sBedrijfswinst

RisicoPremie

verwacht scenario Groei ?

10 apr 2023S Duchateau

59

Index Aankoopdirecteuren VS

USCNFBUSQ17/10/132004200520062007200820092010201120123035404550556065US ISM PURCHASING MANAGERS INDEX (MFG SURVEY) SADJUS ISM NONMANUFACTURERS SURVEY INDEX: COMPOSITE NADJ50Source: Thomson Datastream

10/04/2023

60

Efficiëntbeheer

Portefeuille

Constructie Asset

Allocation

Rente

10/04/2023

61

Duitsland : LT Rente

De diepgang van de Duitse LT tart iedere prognose en weerspiegelt diverse economische, demografische en financiële aspecten

De meest recente terugval van de LT Duitse rente is een combinatie van een zoveelste neerwaartse bijstelling van de Europese groeivooruitzichten , eerder dan een toegenomen kans op een chaotische afwikkeling van de eurozone

BDBRYLD17/10/13200920102011201220131.001.502.002.503.003.504.004.50GERMANY BENCHMARK BOND 10 YR (DS) - RED. YIELDSource: Thomson Datastream

10/04/2023

62

Duitsland en VS: LT Rente

De geleidelijke dispersie tussen de Duitse en Amerikaanse rentevoeten reflecteert enerzijds de sterk neerwaartse druk op de LT rente in Duitsland, veroorzaakt door de eurocrisis maar anderzijds ook zwakte van de Europese conjunctuur

BDBRYLD17/10/13APRMAYJUNJULAUGSEPOCT1.001.201.401.601.802.002.202.402.602.803.00GERMANY BENCHMARK BOND 10 YR (DS) - RED. YIELDUS TREAS.BENCHMARK BOND 10 YR (DS) - RED. YIELDSource: Thomson Datastream

10 apr 2023S Duchateau

63

Reële Rente VSUSBD10Y-PCH#(USCPCOREF,1Y)17/10/13200420052006200720082009201020112012-5-4-3-2-1012345USBD10Y-PCH#(USCPCOREF,1Y)AVG#(USBD10Y-PCH#(USCPCOREF,1Y))PCH#(USGDP...D,1Y)AVG#(PCH#(USGDP...D,1Y))Source: Thomson Datastream

10/04/2023

64

Duitsland en Japan: LT Rente …

Japanse LT rente , 10 jaar vertraagd

De huidige zeer lage rente in de eurozone valt een gelijkaardig pad

Na een zware financiële schok duurt het gemiddeld 25 jaar vooraleer de LT rente zich hersteld …

BDBRYLD17/10/139092949698000204060810121416182012345678910GERMANY BENCHMARK BOND 10 YR (DS) - RED. YIELDMAV#(LAG#(JPGBOND.,10Y),3Y)Source: Thomson Datastream

10/04/2023

65

Europa : Verwachte Inflatie

De verwachte inflatie in de Eurozone (teruggerekend uit Inflation Linked Bonds op 5 jaar) geeft aan dat de ECB door de financiële markten als betrouwbaar wordt beschouwd in haar beleid tegen inflatie maar tevens dat de monetaire groei (nog) niet in staat is de Europese economie noemenswaardig aan te zwengelen

EURIS5Y17/10/132011201220131.401.601.802.002.202.402.60EUR INFLATION LINKED SWAP 5Y - MIDDLE RATE2Source: Thomson Datastream

10 apr 2023S Duchateau

66

KT Rente EurozoneBBERB3M17/10/13201120122013-0.2000.200.400.600.801.001.201.401.601.80EURO REPO BENCHMARK 3 MTH (EUR:FBE) - MIDDLE RATEEURIBOR 3 MONTH - OFFERED RATEEURO MAIN REFINANCING ECB - MIDDLE RATESource: Thomson Datastream

10/04/2023

67

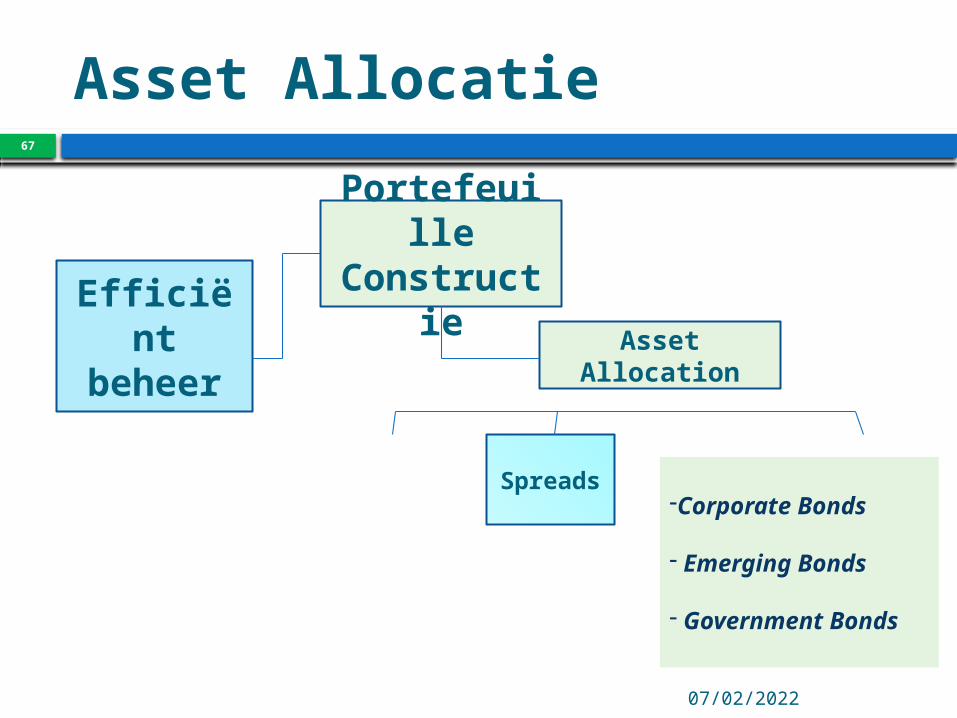

Asset Allocatie

Efficiëntbeheer

Portefeuille

Constructie Asset

Allocation

Spreads -Corporate Bonds

- Emerging Bonds

- Government Bonds

10/04/2023

68

Spreads Bedrijfsobligaties

LHAC7YE(RY)-TREUR7Y17/10/139900010203040506070809101112130123456LHAC7YE(RY)-TREUR7YLHAC3YE(RY)-TREUR3YAVG#(LHAC7YE(RY)-TREUR7Y)Source: Thomson Datastream

10/04/2023

69

Emerging BondsJPMETOC(RY)17/10/13ONDJFMAMJJASO1.802.002.202.402.602.803.003.203.403.603.804.00JPM EU EMBI GLB DIVS COMPOSITE - RED. YIELDJPM EU EMBI GLB DIVS 7-10 YEAR - RED. YIELDJPM EU EMBI GLB DIVS 1-3 YEAR - RED. YIELDJPM EU EMBI GLB DIVS 3-5 YEAR - RED. YIELDSource: Thomson Datastream

10/04/2023

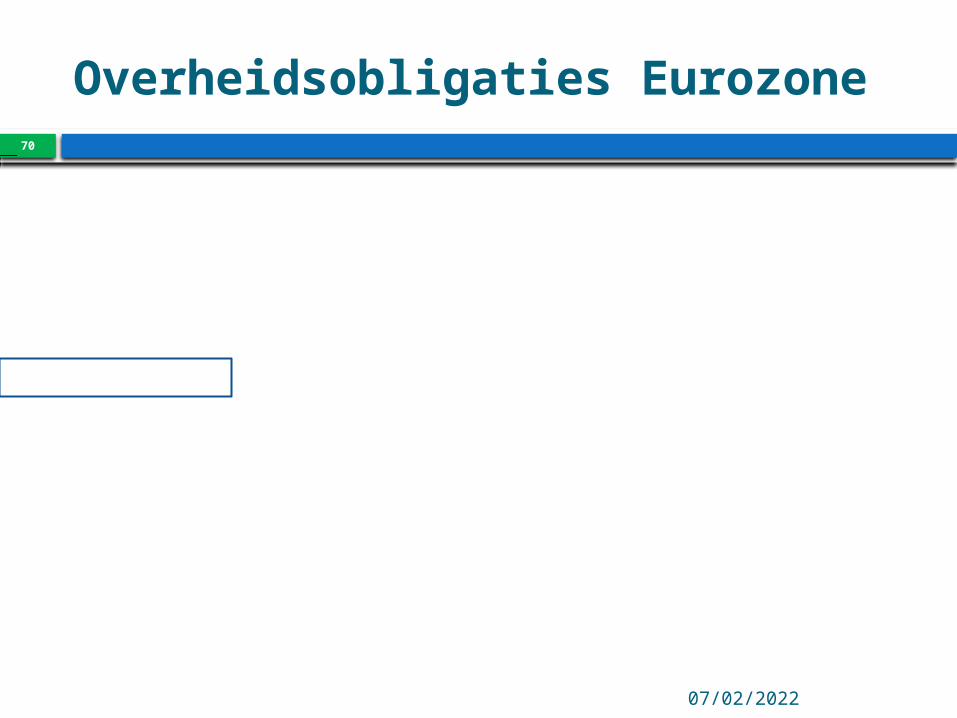

70

Overheidsobligaties EurozoneESBRYLD-BDBRYLD17/10/13ONDJFMAMJJASO12345678ESBRYLD-BDBRYLDITBRYLD-BDBRYLDPTBRYLD-BDBRYLDIRBRYLD-BDBRYLDSource: Thomson Datastream

10/04/2023

71

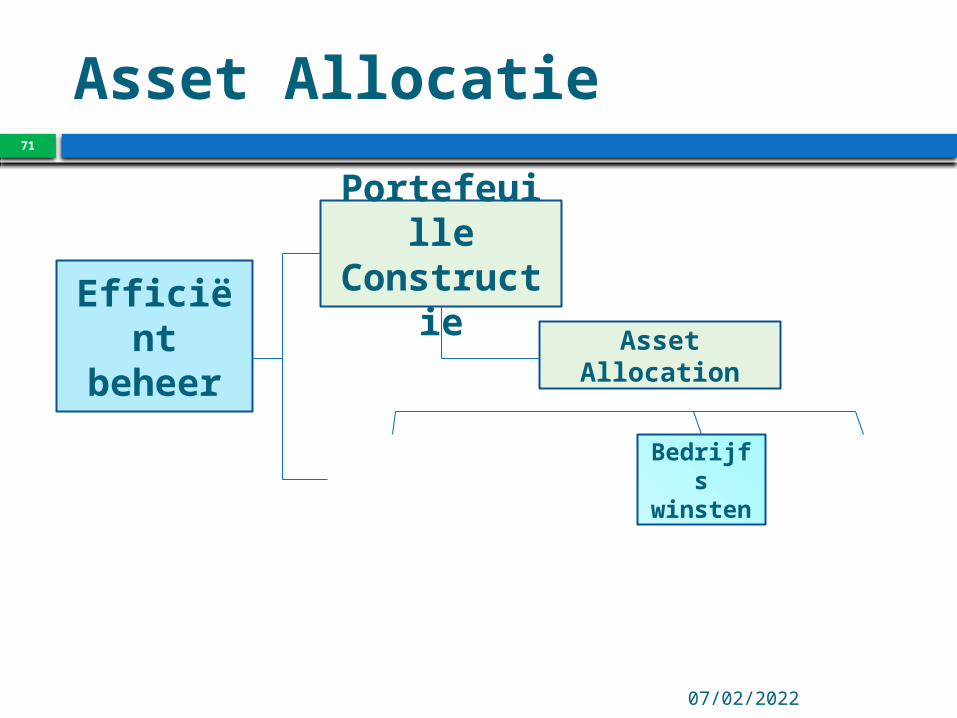

Asset Allocatie

Efficiëntbeheer

Portefeuille

Constructie Asset

Allocation

Bedrijfswinsten

10 apr 2023S Duchateau72

17/10/1320042005200620072008200920102011201250100150200250300MSCI EMG - 12MTH FWD WTD EPS (~E )MSCI EMU (UNADJUSTED) - 12MTH FWD WTD EPSMSCI U.S.A - 12MTH FWD WTD EPS (~E )MSCI GERMANY - 12MTH FWD WTD EPSMSCI JAPAN - 12MTH FWD WTD EPS (~E )Source: Thomson Datastream

10/04/202373

17/10/13200920102011201220136080100120140160180MSCI INDIA - 12MTH FWD WTD EPS (~E )MSCI BRAZIL - 12MTH FWD WTD EPS (~E )MSCI CHINA - 12MTH FWD WTD EPS (~E )MSCI EMU (UNADJUSTED) - 12MTH FWD WTD EPSSource: Thomson Datastream

10 apr 2023

74

17/10/13200720082009201020112012201330405060708090100110120MSCI GERMANY - 12MTH FWD WTD EPS (~E )MSCI EUROPE - 12MTH FWD WTD EPS (~E )MSCI EMU - 12MTH FWD WTD EPS (~E )MSCI FRANCE - 12MTH FWD WTD EPSMSCI ITALY - 12MTH FWD WTD EPSMSCI SPAIN - 12MTH FWD WTD EPSMSCI SWEDEN - 12MTH FWD WTD EPS (~E )MSCI BELGIUM - 12MTH FWD WTD EPS (~E )Source: Thomson Datastream

10/04/2023

75

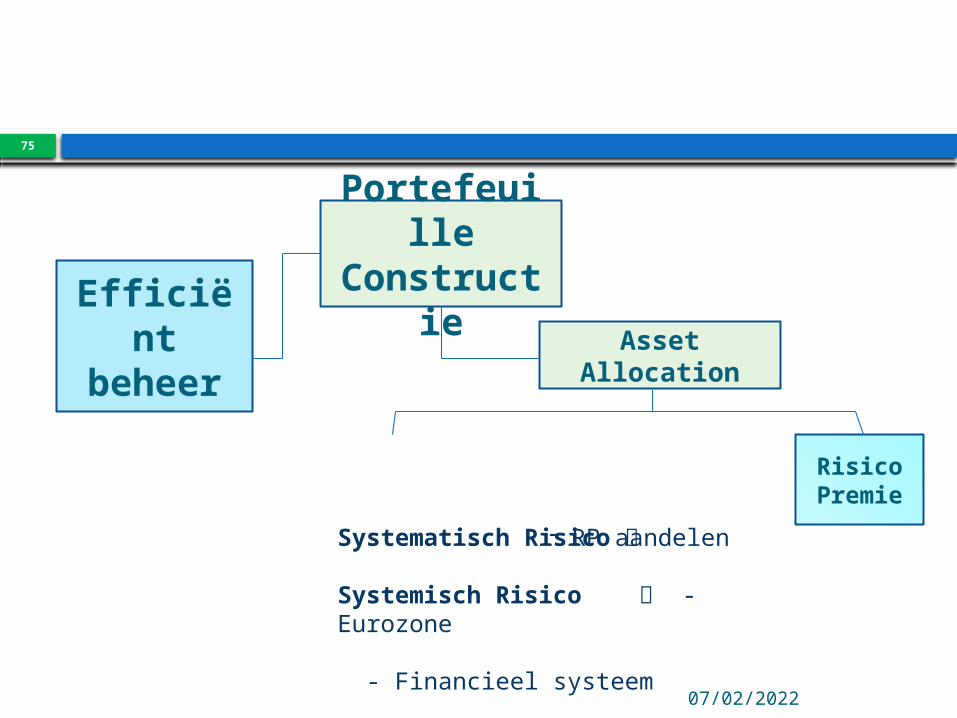

Efficiëntbeheer

Portefeuille

Constructie Asset

Allocation

RisicoPremie

Systematisch Risico

Systemisch Risico - Eurozone - Financieel systeem

- RP aandelen

10/04/2023

76

Verwachte Risicopremie100/@:USSP500(AF1PE)-0.6*AUSGVG1(RY)17/10/13838587899193959799010305070911-10123456789100/@:USSP500(AF1PE)-0.6*AUSGVG1(RY)Source: Thomson Datastream

10/04/2023

77

VolatiliteitCBOEVIX17/10/139495969798990001020304050607080910111213010203040506070CBOE SPX VOLATILITY VIX (NEW) - PRICE INDEXAVG#(CBOEVIX)Source: Thomson Datastream

10/04/2023

78

Flight-to-Quality Duitsland

TREUR2Y-GBBD02Y(RY)17/10/1320052006200720082009201020112012201300.200.400.600.801.001.201.40TREUR2Y-GBBD02Y(RY)Source: Thomson Datastream

10/04/2023

79

Lopende Rekening Eurozone landen

MAV#(ITCURBALA,1Y)17/10/13990001020304050607080910111213000'S -10-8-6-4-202468MAV#(ITCURBALA,1Y)MAV#(GRCURBALA,1Y)MAV#(IRCURBALA,1Y)MAV#(BGCURBALA,1Y)MAV#(ESCURBALA,1Y)Source: Thomson Datastream

10/04/2023

80

Reële effectieve wisselkoersen17/10/13000102030405060708091011121395100105110115120125130135BGI..RECE/BDI..RECEPTI..RECE/BDI..RECEGRI..RECE/BDI..RECEESI..RECE/BDI..RECEIRI..RECE/BDI..RECEITI..RECE/BDI..RECENLI..RECE/BDI..RECEFRI..RECE/BDI..RECESource: Thomson Datastream

10/04/2023

81

Financiële StabiliteitEIBOR3M-BBERB3M17/10/132006200720082009201020112012201300.200.400.600.801.001.201.401.601.802.00EIBOR3M-BBERB3MSource: Thomson Datastream

+

-

-

+ +

-

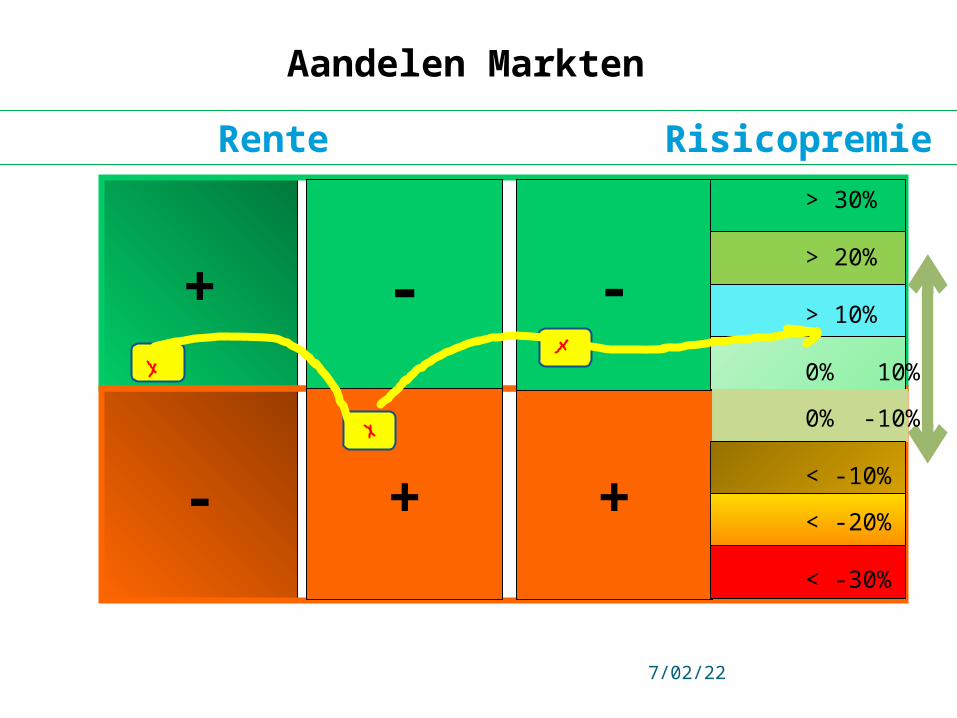

Aandelen Markten

> 30%

> 20%

> 10%

0% 10%

0% -10%

< -10%

< -20%

< -30%

Groei Rente Risicopremie Beurs

10 apr 2023

83

Efficiëntbeheer

Portefeuile

constructie

Security Selection

- process - 4-factor model a-Specifieke sectorale accenten :

- Water ( Aqua America, American State Water, Flowserve …)

- Biotechnology (Amgen, Biogen ,Coloplast, Elekta, Gilead …)

- Schalie Gas (Cheniere, US Silica, Continental resources, …)

-Specifieke geografische accenten- VS, Duitsland, Scandinavië, Japan, China

84

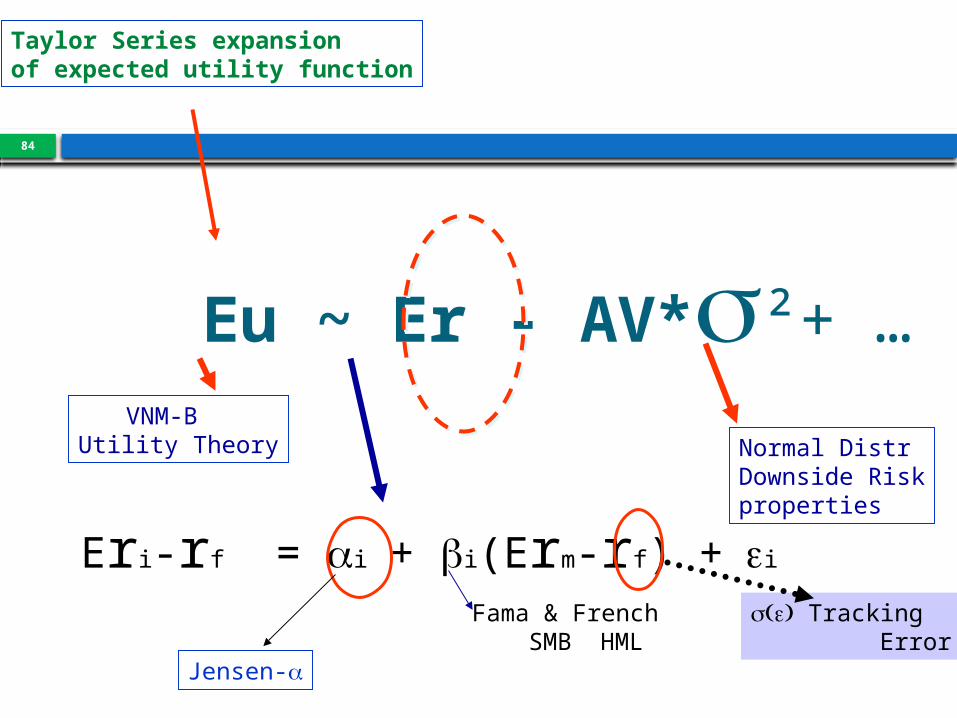

Eu ~ Er - AV*s²+ …VNM-B

Utility Theory

Eri-rf = ai + bi(Erm-rf) + ei

Normal DistrDownside Riskproperties

Taylor Series expansionof expected utility function

Jensen-a

Fama & French SMB HML

( )s e Tracking Error

85

a ?

ittitititiiit

(Carhart) lfactormode4

ittititiiit

French) & (Fama lfactormode3

ittiiit

CAPM

e.PR1YRp.HMLh.SMBs.RMβαr

e.HMLh.SMBs.RMβαr

e.RMβαr

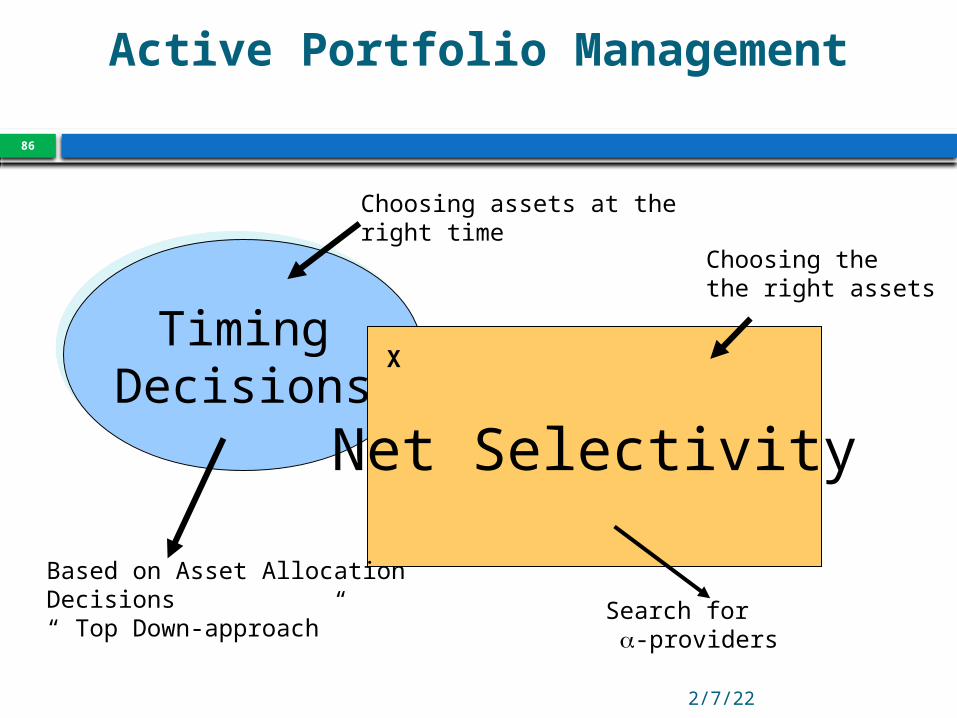

Active Portfolio Management

Apr 10, 2023

86

TimingDecisions

TimingDecisions

Net Selectivity

Based on Asset AllocationDecisions“ Top Down-approach”

Search for a-providers

Choosing assets at the right time

Choosing the the right assets

X

TESTING FOR MARKET TIMING: TREYNOR-MAZUY

c tsignifican positive, for Look

ptftmtftmtftpt errcrrbarr ~)()( 2

87

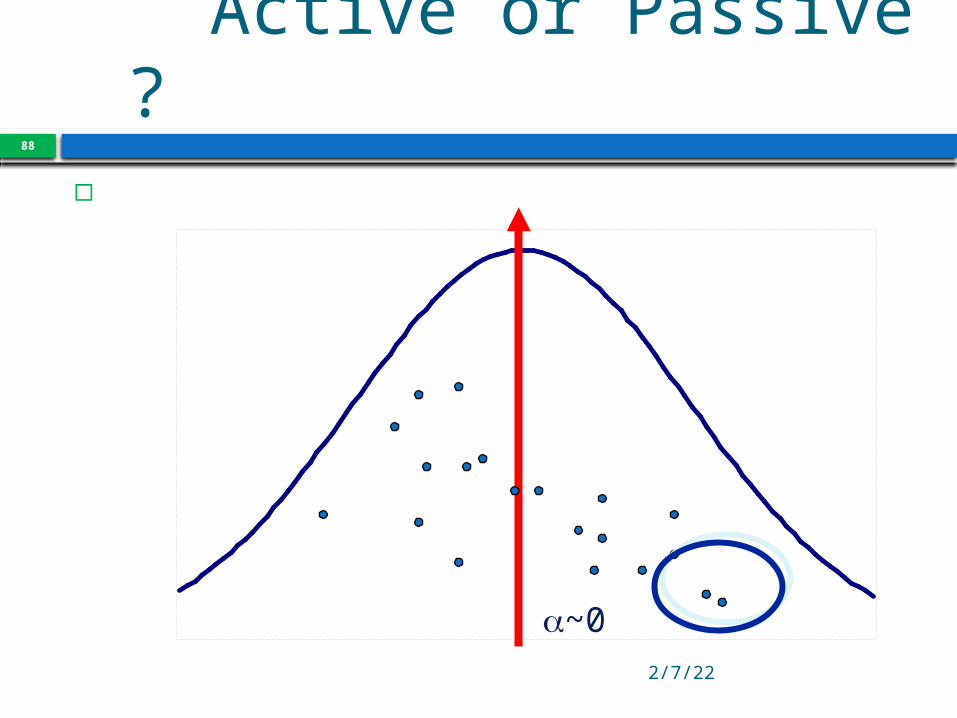

Active or Passive ?

Apr 10, 2023

88

a~0

89

11

Persistence in (out)perf ormance

•

~0

LT persistence?

Legendary outperformers(but can you pick the next one?)

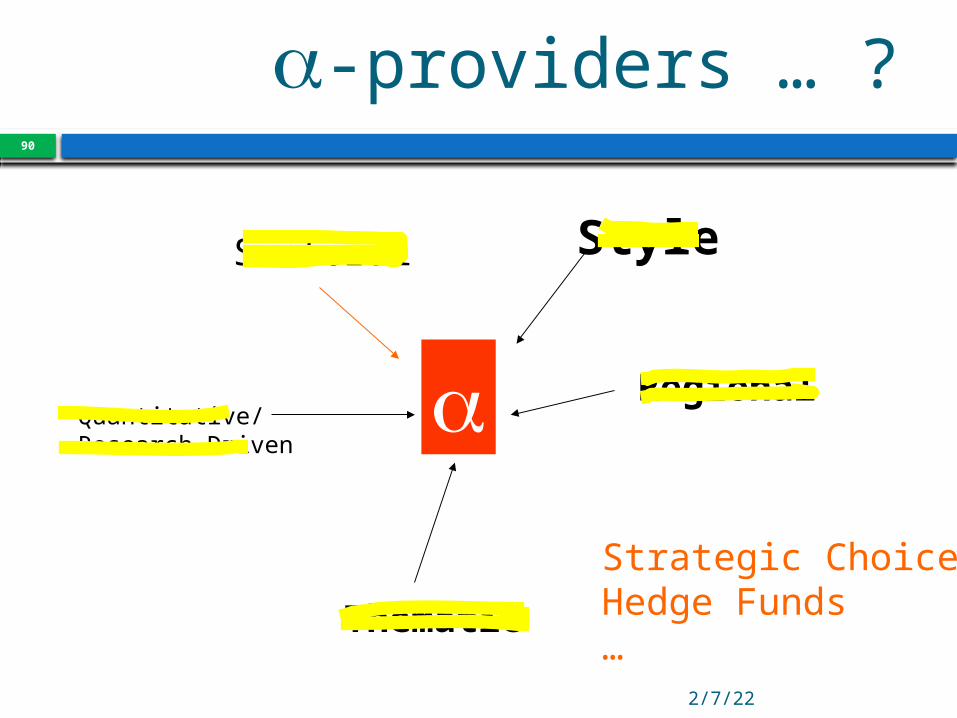

a-providers … ?

Apr 10, 2023

90

Sectoral

Regional

Thematic

Quantitative/Research Driven

a

Strategic ChoicesHedge Funds…

Style

04:5891

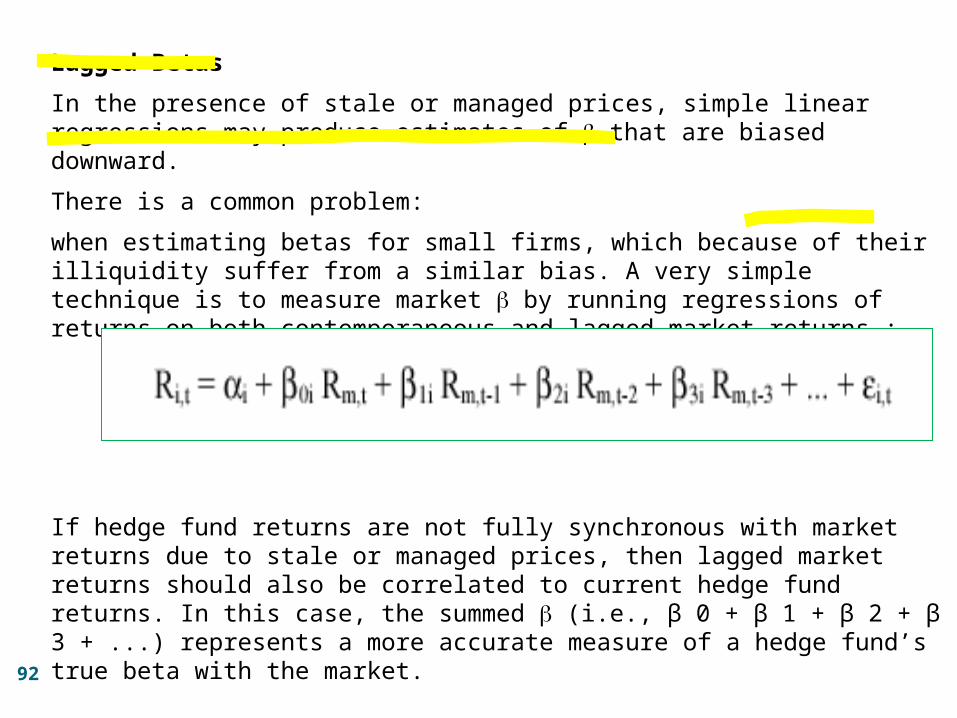

Lagged Betas

Lage b lage correlatie met de markt … ?

04:5892

Lagged Betas

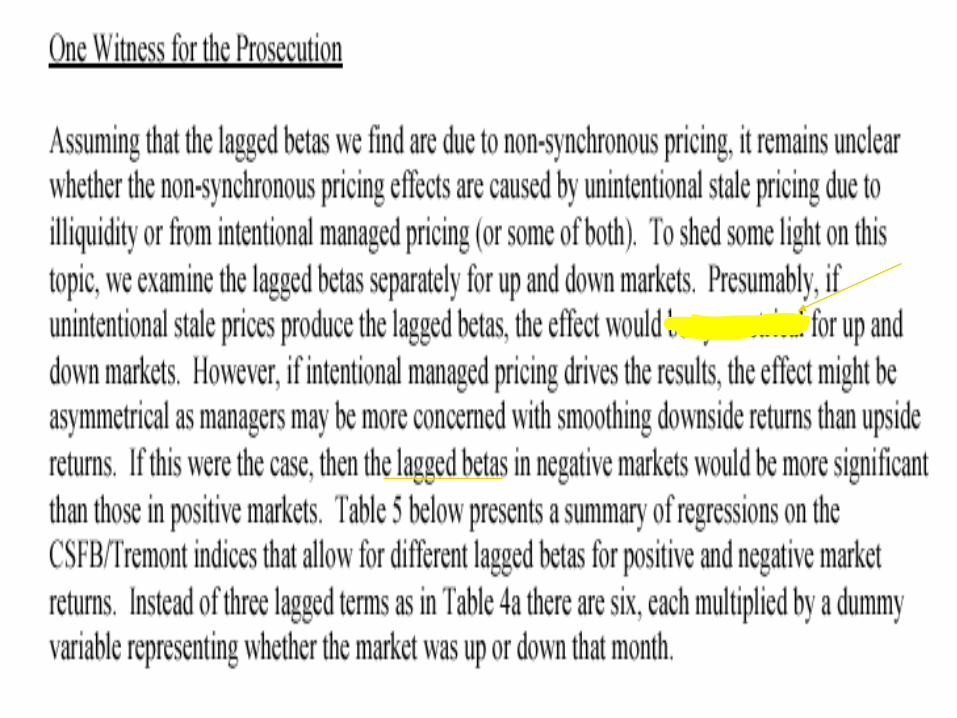

In the presence of stale or managed prices, simple linear regressions may produce estimates of b that are biased downward.

There is a common problem:

when estimating betas for small firms, which because of their illiquidity suffer from a similar bias. A very simple technique is to measure market b by running regressions of returns on both contemporaneous and lagged market returns :

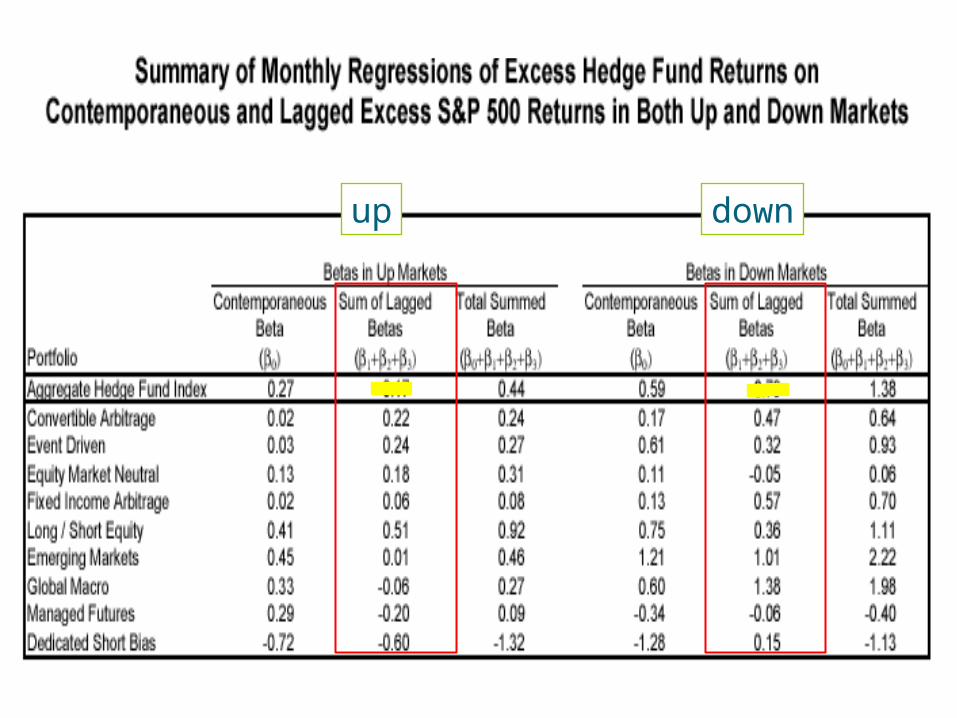

If hedge fund returns are not fully synchronous with market returns due to stale or managed prices, then lagged market returns should also be correlated to current hedge fund returns. In this case, the summed b (i.e., β 0 + β 1 + β 2 + β 3 + ...) represents a more accurate measure of a hedge fund’s true beta with the market.

04:5893

04:5894

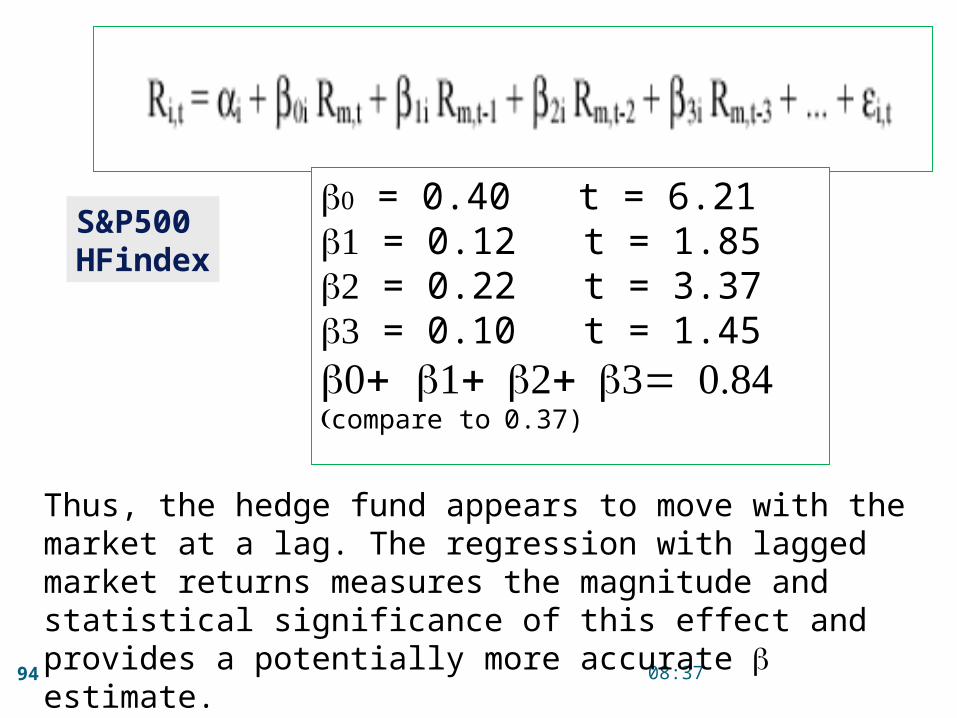

Thus, the hedge fund appears to move with the market at a lag. The regression with lagged market returns measures the magnitude and statistical significance of this effect and provides a potentially more accurate b estimate.

b0 = 0.40 t = 6.211b = 0.12 t = 1.852b = 0.22 t = 3.373b = 0.10 t = 1.45 0+b 1+ 2+ 3= 0.84b b b

(compare to 0.37)

S&P500HFindex

04:5895

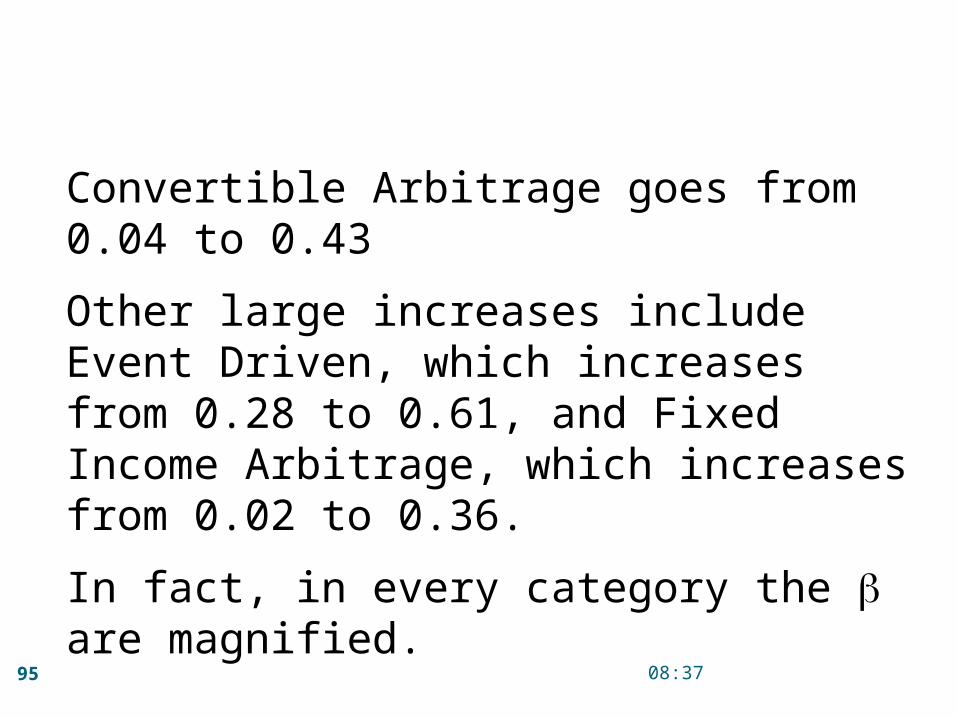

Convertible Arbitrage goes from 0.04 to 0.43

Other large increases include Event Driven, which increases from 0.28 to 0.61, and Fixed Income Arbitrage, which increases from 0.02 to 0.36.

In fact, in every category the b are magnified.

04:5896

04:5897

up down

10/04/2023

98

Efficiëntbeheer

Portefeuille

Constructie

Neerwaarts potentieel

Winst “lock in”

10/04/2023

99

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico …

10/04/2023

100

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

Oordeelkundig Principes voor coherente keuze van asset

klassen, individuele waarden, … ?

Afweging Welk keuzecriterium ?

10/04/2023

101

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

Verwachte opbrengst ?Beknopte historische schets

Statistische interpretatieDynamische interpretatie

Model ?Actief portefeuillebeheer

102

Efficiënt Portefeuillebeheer

Oordeelkundige afweging van verwachte opbrengst en risico

Risico ?

Identify Risk

Measure Risk

Manage Risk

Definitie Maatgetal Toepassing

10/04/2023

103

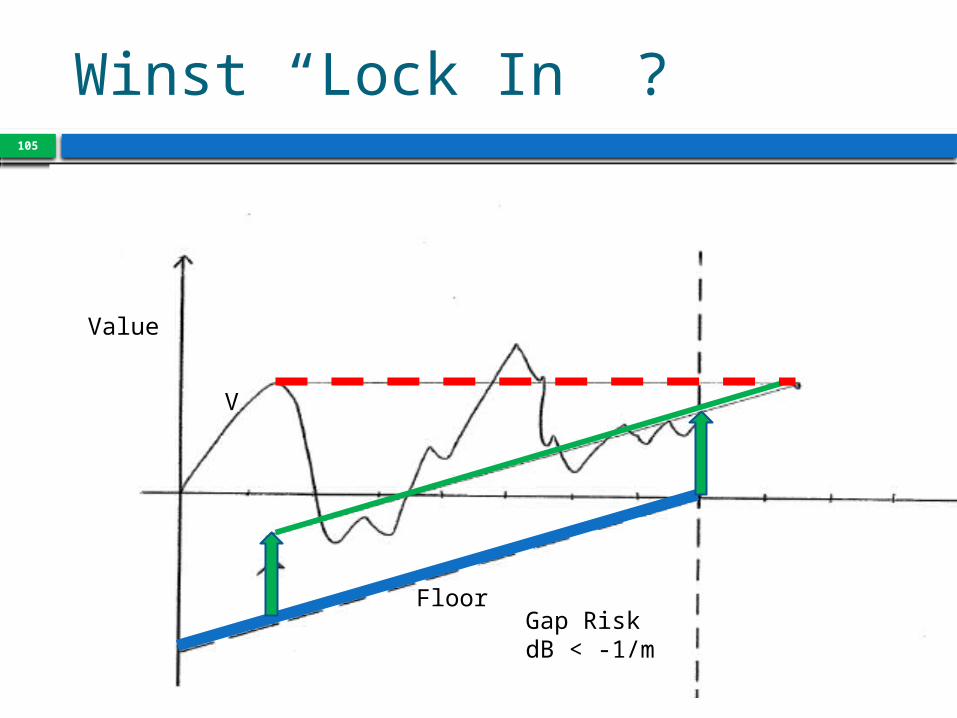

Bescherming ?

1 Kapitaalbeschermend objectief “Verstandige “horizon 6 à 8 jaar

2 “Lock In” winst

10/04/2023

104

Neerwaartse bescherming ?

V

Floor

Time

Value

E = m*C

C = Vp- Floor

105

Winst “Lock In” ?

V

Floor

Value

Gap RiskdB < -1/m

10/04/2023

106

Neerwaartse bescherming & Lock in

ValueSmoothed evolution

Professor of : HUB

Advanced Portfolio Management Financial Engineering Financial Risk Management

U Hasselt Financial derivatives

KU Leuven Investment Management Security Pricing & Portfolio Selection

1

Prof Dr Stefan Duchateau 0474 977464

![SESSIE 2l Spijbelen: een preventieve aanpak...× Stappenplan of afsprakenkader De procedure weet ik [als leerkracht] niet exact, nee. Maar ik weet dat dat tot huisbezoek gaat. Dus](https://static.fdocuments.net/doc/165x107/5f28177c7a63bc6e2e6659c9/sessie-2l-spijbelen-een-preventieve-aanpak-stappenplan-of-afsprakenkader.jpg)