BaoshanIron & Steel Co.,Ltd. 2012Full Year Results …BaoshanIron & Steel Co.,Ltd. 2012Full Year...

32

Baoshan Iron & Steel Co.,Ltd. 2012 Full Year Results April 2013

Transcript of BaoshanIron & Steel Co.,Ltd. 2012Full Year Results …BaoshanIron & Steel Co.,Ltd. 2012Full Year...

Baoshan Iron & Steel Co.,Ltd.

2012 Full Year Results

April 2013

Disclaimer

The following presentation distributed herewith includes forward-looking statements. All statements, other than statements of historical facts, that address activities, events

or developments that Baoshan Iron & Steel Co.,Ltd.(Baosteel) expects or anticipates will or may occur in the future are forward-looking statements.

Baosteel’s actual results or developments may differ materially from those indicated by these forward-looking statements as a result of various factors and uncertainties, including but not limited to price fluctuations, actual demand, exchange rate fluctuations, competition and other risks and factors beyond our control.

I. Operation Results

II. Industry Dynamics

III.Company Outlook

� Production and Sales

unit::::million tons 2010 2011 2012 YoY

Crude steel output 26.45 26.64 23.00 -13.7%

Sales of finished products 25.26 25.80 23.57 -8.6%

including::::domestic 22.93 23.06 21.23 -7.9%

export 2.33 2.74 2.34 -14.6%

Note:Stainless and special steel assets were sold to Baosteel Group corporation on 1 April, 2012;

Only Q1 results of stainless and special steel were included.

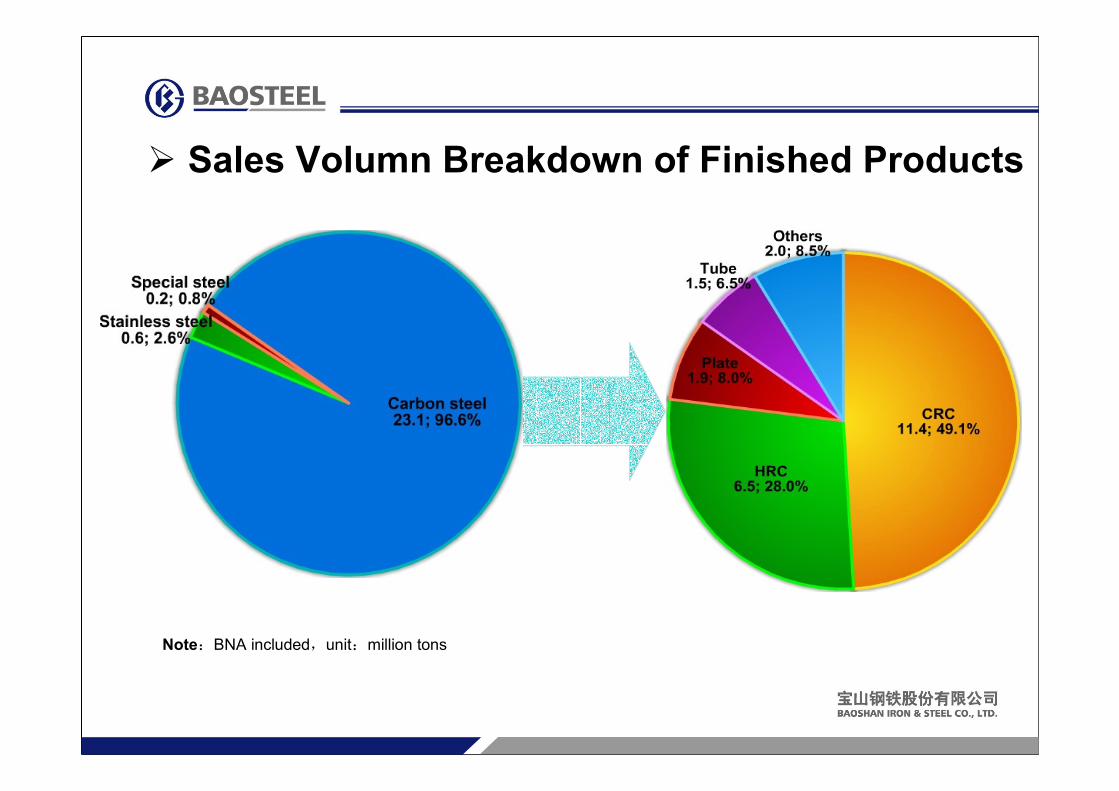

� Sales Volumn Breakdown of Finished Products

Note:BNA included,unit:million tons

unit::::million tons

billion YuanSales Revenue YoY Cost YoY

Gross

marginYoY

CRC 9.4 52.0 -11.8% 46.2 -10.6% 11.2% ↓↓↓↓1.2 ppts

HRC 8.0 32.0 -17.7% 29.1 -15.8% 8.8% ↓↓↓↓2.1 ppts

Plate 1.9 8.5 -27.7% 9.5 -25.8% -11.7% ↓↓↓↓2.8 ppts

Tube 1.5 10.3 -5.3% 9.4 -4.8% 9.0% ↓↓↓↓0.5 ppts

Stainless steel 0.6 7.5 -58.6% 7.5 -57.6% -1.1% ↓↓↓↓2.4 ppts

Special steel 0.2 2.2 -80.1% 2.4 -79.0% -6.3% ↓↓↓↓5.4 ppts

Others 2.0 8.2 -6.1% 8.5 -2.4% -3.9% ↓↓↓↓3.9 ppts

Total 23.6 120.6 -23.8% 112.6 -23.3% 6.6% ↓↓↓↓0.7 ppts

� Gross Profit--By Product

� Income Statement Summary

unit::::billion Yuan 2010 2011 2012 YoY

Revenue 202.41 222.86 191.51 -14.1%

Cost 186.59 214.64 189.12 -11.9%

Gross profit 24.33 19.61 14.37

Gross margin%%%% 12.02 8.80 7.50 ↓↓↓↓1.30 ppts

Operating profit 16.67 8.84 3.60

Operating margin%%%% 8.24 3.97 1.88 ↓↓↓↓2.09ppts

Net profit 12.89 7.36 10.39

Net profit margin%%%% 6.37 3.30 5.42 ↑↑↑↑2.12 ppts

Note:Decline in 2012 operating profit was due to 2.65 billion Yuan impairment loss of Luojing remaining assets.

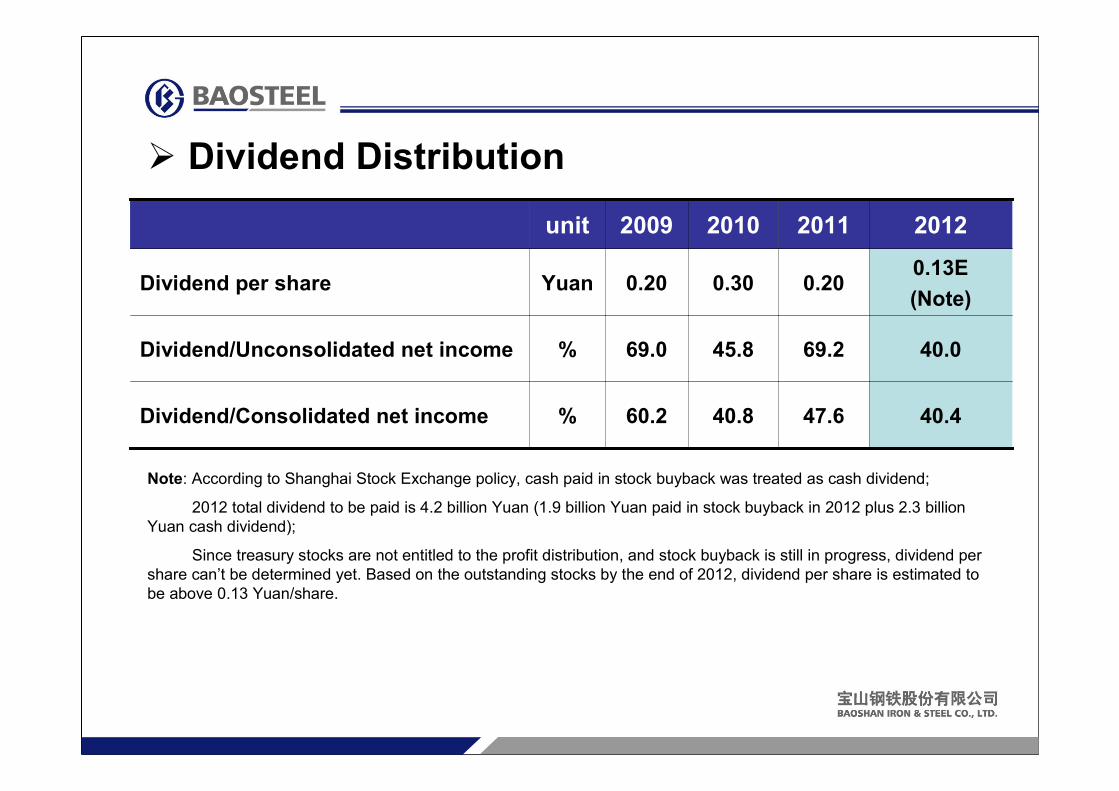

� Dividend Distribution

unit 2009 2010 2011 2012

Dividend per share Yuan 0.20 0.30 0.200.13E

(Note)

Dividend/Unconsolidated net income % 69.0 45.8 69.2 40.0

Dividend/Consolidated net income % 60.2 40.8 47.6 40.4

Note: According to Shanghai Stock Exchange policy, cash paid in stock buyback was treated as cash dividend;

2012 total dividend to be paid is 4.2 billion Yuan (1.9 billion Yuan paid in stock buyback in 2012 plus 2.3 billion

Yuan cash dividend);

Since treasury stocks are not entitled to the profit distribution, and stock buyback is still in progress, dividend per

share can’t be determined yet. Based on the outstanding stocks by the end of 2012, dividend per share is estimated to

be above 0.13 Yuan/share.

unit::::Yuan 2010 2011 2012 YoY

EPS 0.74 0.42 0.60 42.9%

BVPS 5.98 6.08 6.51 7.1%

Net CFO per share 1.08 0.69 1.30 88.4%

Gross margin% 13.25 8.75 7.46 ↓↓↓↓1.29 ppts

ROE (weighted)% 12.95 7.02 9.52 ↑↑↑↑2.50 ppts

� Financial Highlights

Financial index unit 2011-12-31 2012-12-31 Change

Solvency

Total debts/

total assets%%%% 50.89 45.26 ↓↓↓↓ 5.63 ppts

Current ratio 0.80 0.84 ↑↑↑↑ 0.04

Quick ratio 0.42 0.49 ↑↑↑↑ 0.07

Financial index unit 2011 2012 Change

Liquidity

Days of receivables day 8.4 19.0 126.2%

Days of inventories day 74.9 70.8 -5.5%

Cash conversion

cycleday 51.1 51.6 1.0%

� Solvency and Liquidity

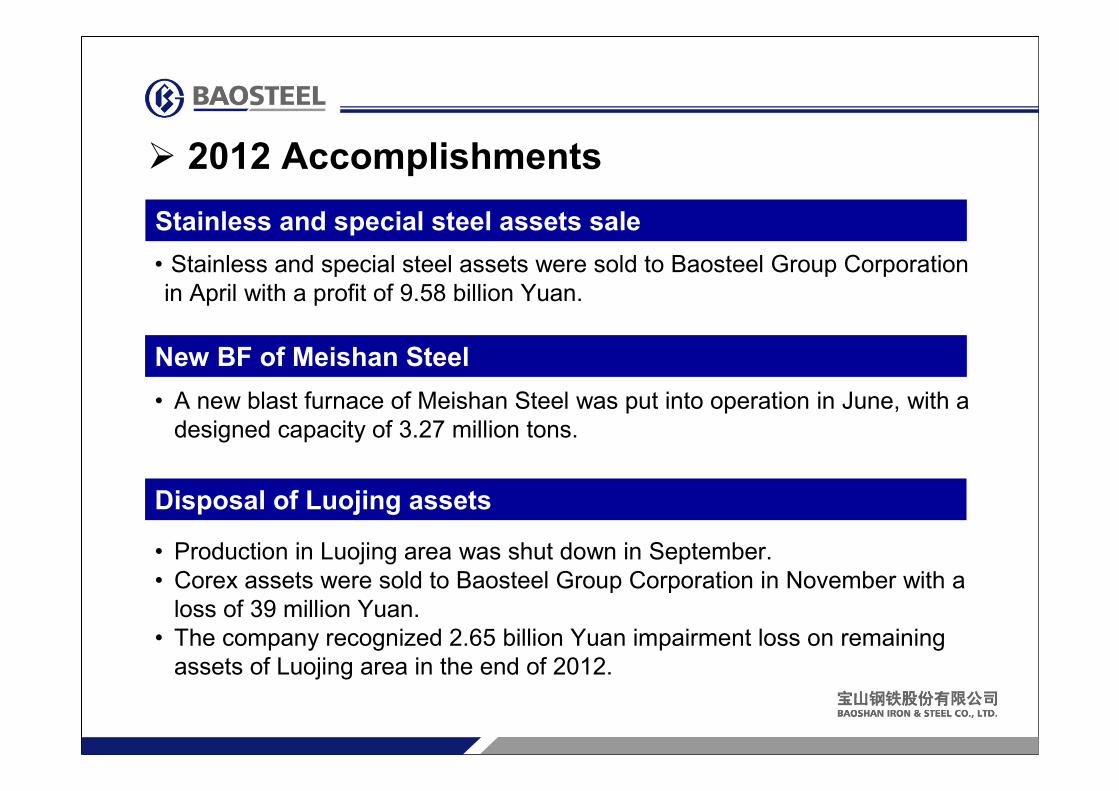

� 2012 Accomplishments

Stainless and special steel assets sale

• Stainless and special steel assets were sold to Baosteel Group Corporation

in April with a profit of 9.58 billion Yuan.

New BF of Meishan Steel

• A new blast furnace of Meishan Steel was put into operation in June, with a

designed capacity of 3.27 million tons.

Disposal of Luojing assets

• Production in Luojing area was shut down in September.

• Corex assets were sold to Baosteel Group Corporation in November with a

loss of 39 million Yuan.

• The company recognized 2.65 billion Yuan impairment loss on remaining

assets of Luojing area in the end of 2012.

� 2012 Accomplishments

Zhanjiang Project

• Investment in Zhanjiang Project was approved by the general shareholders’

meeting in September. Static investment is expected to be 40 billion Yuan.

• The company purchased 71.8% equity of Zhanjiang Steel with 4.98 billion

Yuan in October.

• The company increased the capital of Zhanjiang Steel from 7.093 billion

Yuan to 8 billion Yuan in January 2013.

Stock Buyback

• Stock buyback was approved by the general shareholders’ meeting in

September. The company decided to use no more than 5 billion Yuan at price

no more than 5 Yuan/share.

• The company has paid 2.96 billion Yuan to repurchase 0.625 billion stocks by

the end of March 2013.

I. Operation Results

II. Industry Dynamics

III.Company Outlook

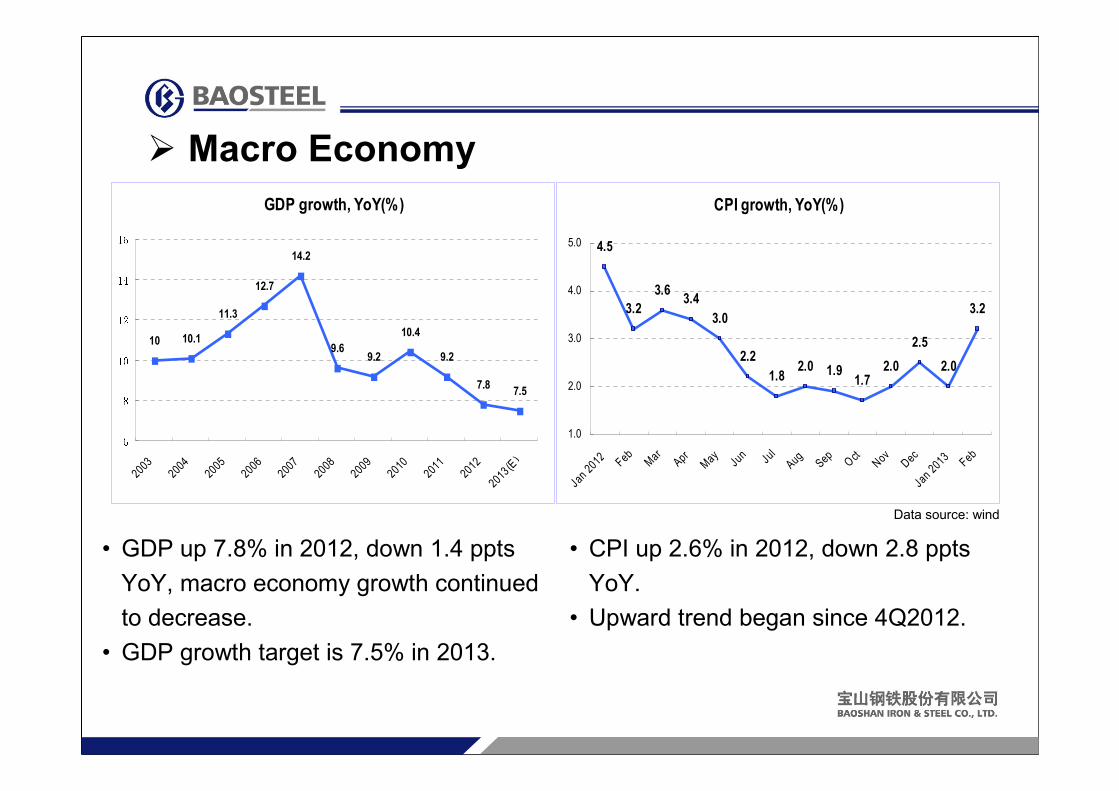

� Macro Economy

• GDP up 7.8% in 2012, down 1.4 ppts

YoY, macro economy growth continued

to decrease.

• GDP growth target is 7.5% in 2013.

Data source: wind

• CPI up 2.6% in 2012, down 2.8 ppts

YoY.

• Upward trend began since 4Q2012.

GDP growth, YoY(%)

10 10.1

11.3

12.7

14.2

9.69.2

10.4

9.2

7.87.56810

121416

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

(E)

CPI growth, YoY(%)

4.5

3.2

3.63.4

3.0

2.2

1.82.0 1.9

1.72.0

2.5

2.0

3.2

1.0

2.0

3.0

4.0

5.0

Jan 20

12 Feb

Mar

Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

Jan 20

13 Feb

� Demand and Supply Analysis--Supply(Crude Steel)

• Crude steel output still grew in 2012, while the growth rate slowed down.

• Crude steel output was 589 million tons from member steelmakers in CISA, down 0.6% YoY, and 127 million tons from others, up 24.8% YoY.

• FAI in steel industry was 658 billion Yuan, up 3% YoY. The growth rate was down 12.5 ppts YoY.

• Output growth rate was expected a further decrease in 2013.

Data resource: National Bureau of Statistics, MIIT, Customs statistic and company forecast

648648648648

35353535

683683683683

2011

699699699699

38383838

737737737737

2013EUnit: million tons YoY 2012 YoY YoY

Output 8.9%8.9%8.9%8.9% 717717717717 4.9%4.9%4.9%4.9% 2.9%2.9%2.9%2.9%

Net export 29.6%29.6%29.6%29.6% 44444444 25.7%25.7%25.7%25.7% ----14.2%14.2%14.2%14.2%

Apparent

Consumption 8.2%8.2%8.2%8.2% 673673673673 3.9%3.9%3.9%3.9% 4.0%4.0%4.0%4.0%

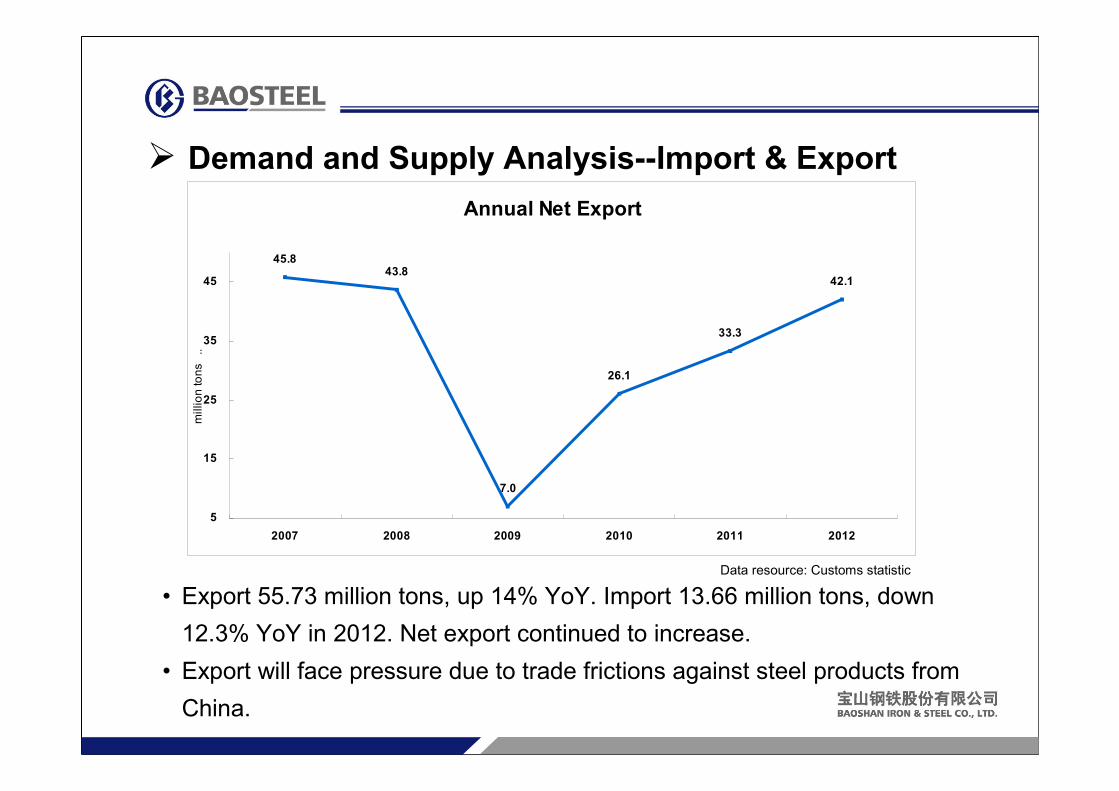

� Demand and Supply Analysis--Import & Export

• Export 55.73 million tons, up 14% YoY. Import 13.66 million tons, down

12.3% YoY in 2012. Net export continued to increase.

• Export will face pressure due to trade frictions against steel products from

China.

Data resource: Customs statistic

Annual Net Export

45.843.8

7.0

26.1

33.3

42.1

5

15

25

35

45

2007 2008 2009 2010 2011 2012

million tons ..

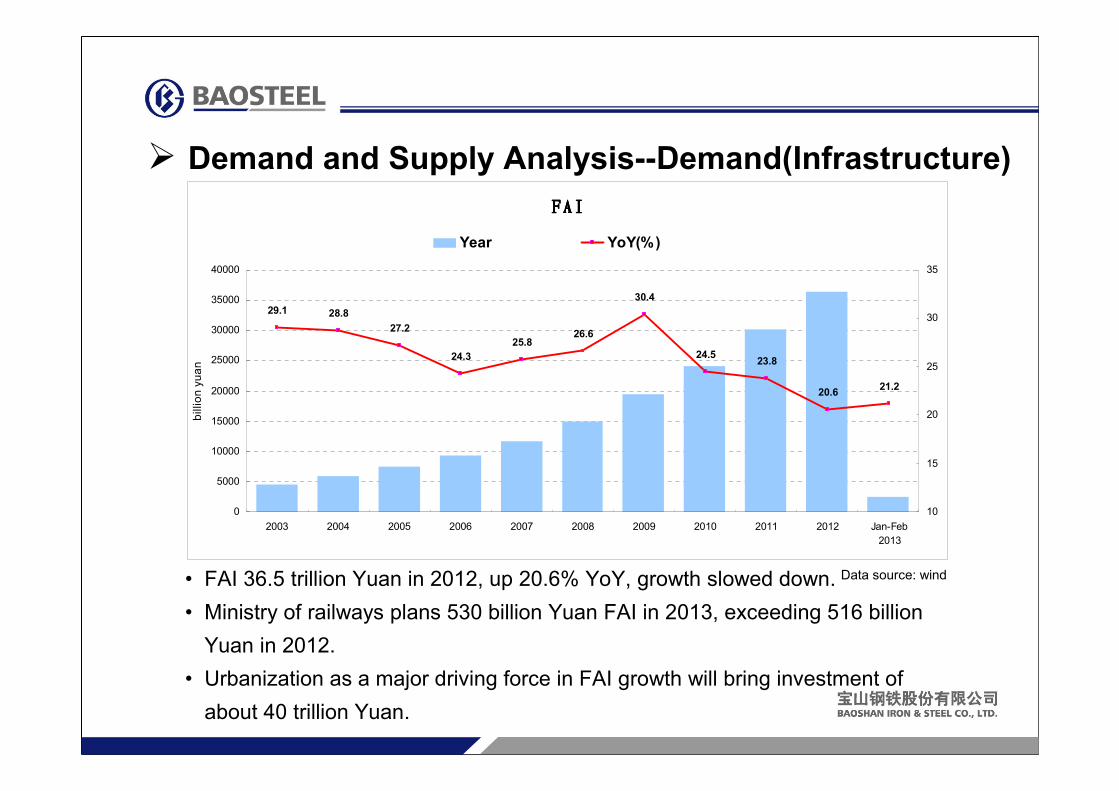

� Demand and Supply Analysis--Demand(Infrastructure)

• FAI 36.5 trillion Yuan in 2012, up 20.6% YoY, growth slowed down.

• Ministry of railways plans 530 billion Yuan FAI in 2013, exceeding 516 billion

Yuan in 2012.

• Urbanization as a major driving force in FAI growth will bring investment of

about 40 trillion Yuan.

Data source: wind

FAIFAIFAIFAI

29.1 28.8

27.2

24.3

25.826.6

24.523.8

20.621.2

30.4

0

5000

10000

15000

20000

25000

30000

35000

40000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Jan-Feb

2013

billion yuan

10

15

20

25

30

35

Year YoY(%)

� Demand and Supply Analysis--Demand(Real Estate)

• Investment up 16.2% YoY, new start area down 7.3% YoY, and sales area up

1.8% YoY in 2012.

• Industry began to rebounce in the end of 2012, while the recent new control

policy brings uncertainty.

Data source: wind

0

0.5

1

1.5

2

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Jan-Feb

2013

New start area (billion square meters)

Sales area (billion square meters)

Investment (billion Yuan, left)

Growth Ytd, YoY (%, right)

0

1000

2000

3000

4000

5000

6000

7000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Jan-Feb

2013

0

5

10

15

20

25

30

35

� Demand and Supply Analysis—Demand(Automobile)

• Growth picked up from the low level of 2011.

• Japanese car sales decreased in 2012, while has improved since Dec 2012.

• Subsidy to energy-saving and new energy cars is expected in the near future.

• Growth rate is expected 8% in 2013.

Data source: wind

Output

0

5

10

15

20

2003 2005 2007 2009 2011 Jan-Feb

2013

million

0

10

20

30

40

50

output YoY%

Sales

0

5

10

15

20

2003 2005 2007 2009 2011 Jan-Feb

2013

million

0

10

20

30

40

50

sales YoY%

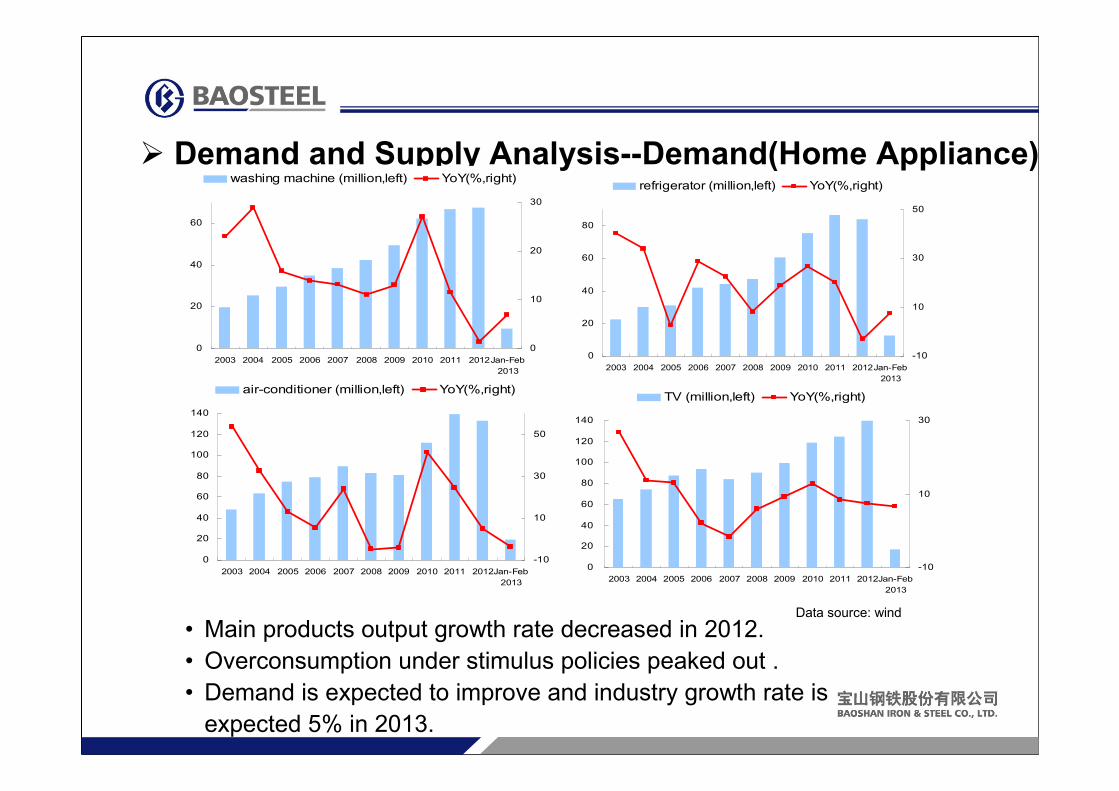

� Demand and Supply Analysis--Demand(Home Appliance)

• Main products output growth rate decreased in 2012.

• Overconsumption under stimulus policies peaked out .

• Demand is expected to improve and industry growth rate is

expected 5% in 2013.

Data source: wind

0

20

40

60

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Jan-Feb

2013

0

10

20

30

washing machine (million,left) YoY(%,right)

0

20

40

60

80

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Jan-Feb

2013

-10

10

30

50

refrigerator (million,left) YoY(%,right)

0

20

40

60

80

100

120

140

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Jan-Feb

2013

-10

10

30

50

air-conditioner (million,left) YoY(%,right)

0

20

40

60

80

100

120

140

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Jan-Feb

2013

-10

10

30

TV (million,left) YoY(%,right)

� Demand and Supply Analysis--Demand(Machinery)

• Machinery industry was still in downward trend in 2012.

• In 2013, growth will pick up driven by related industries, like infrastructure, real

estate and autos. The growth rate is expected 15%.

• In sub-industries: construction machinery is still depressed, railway equipment

and agricultural machinery may improve.

Data source: CMIF

Machinery industry growth,YoY

11.9% 11.9% 12.2%14.2%

11.6%13.3% 12.1% 11.9% 12.2% 11.9% 12.0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Jan-Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010 2011 2012

� Demand and Supply Analysis--Demand(Ship Building)

• Completion, new order and carrying order were :60, 20 and 110

million tonnages, down 21%, 44% and 29% YoY respectively in 2012.

• Industry is still depressed in 2013 and little chance of improvement in

a short run.

Data source: CANSI

Ship-building Completion

7.19

4.024.44

6.88

9.67

3.29

2.34

3.75

5.09

3.88

9.66

0

2

4

6

8

10

12

14

16

Jan-Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

million tonnage

2009 2010 2011 2012

� Steel Inventory

• Year end inventory down 7.9% YoY.

• Inventory increased slowly before Feb 2013. There was a explosive inventory growth

after the Spring Festival, with the release of steel output .

• Inventory growth slowed down after mid-March, great pressure of later destocking.

Unit:

million tons

22 Mar

2013

1 Mar

2013

1 Feb

2013

28 Dec

2012

YoY

Change %

Rebar 10.80 10.34 7.06 5.20 0.34 6.9%

Wire 3.21 3.16 1.77 1.23 0.11 9.7%

HRC 4.72 4.72 3.65 2.75 -1.28 -31.8%

CRC 1.69 1.71 1.53 1.54 0.05 3.2%

Plate 1.67 1.81 1.48 1.16 -0.23 -16.3%

Long product 14.01 13.51 8.83 6.43 0.45 7.5%

Flat product 8.07 8.24 6.66 5.45 -1.46 -21.2%

Total 22.08 21.75 15.49 11.88 -1.02 -7.9%

Data source: Mysteel

Note: range of social inventory statistics is expanded since 2013

� Iron Ore Inventory

• Downward trend in iron ore port inventory, down 23.5% YoY.

• Inventory dropped below 90 million tons in Nov 2012 and now 67.92

million tons (29 Mar, 2013).

Data source: Mysteel

Iron ore port inventory

1

6

11

16

21

26

31

36

41

Jan-11 Mar-11 Jun-11 Aug-11 Oct-11 Jan-12 Mar-12 Jun-12 Aug-12 Oct-12 Jan-13 Mar-13

million tons

Australian Brazil India

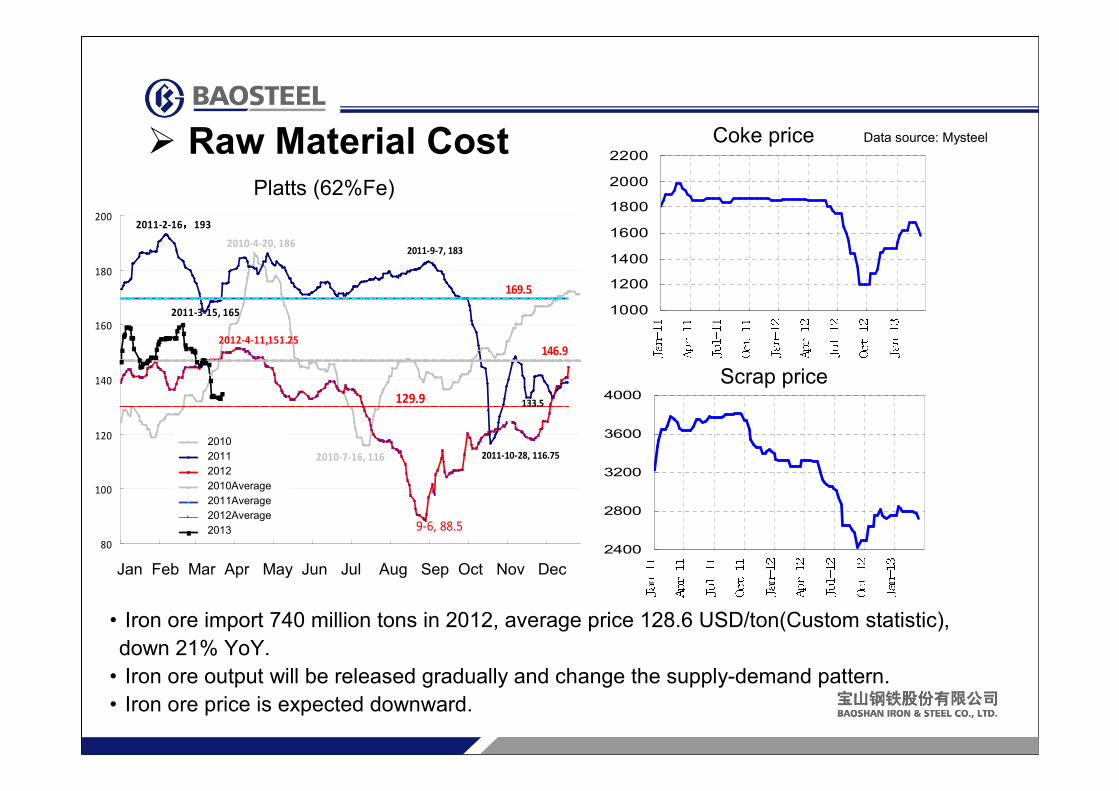

� Raw Material Cost

• Iron ore import 740 million tons in 2012, average price 128.6 USD/ton(Custom statistic),

down 21% YoY.

• Iron ore output will be released gradually and change the supply-demand pattern.

• Iron ore price is expected downward.

62%粉矿62%粉矿62%粉矿62%粉矿PlattsPlattsPlattsPlatts指数价格走势指数价格走势指数价格走势指数价格走势((((CFR,CFR,CFR,CFR,美元/干吨美元/干吨美元/干吨美元/干吨))))

2010-7-16, 116

2010-4-20, 186

2011-10-28, 116.75

2011-9-7, 183

2011-2-16,,,,193

2011-3-15, 165

133.5

2012-4-11,151.25

9-6, 88.5

146.9

169.5

129.9

80

100

120

140

160

180

200

1

月

2

月

3

月

4

月

5

月

6

月

7

月8

月9

月1

0

月1

1

月1

2

月2010年2011年2012年2010年指数年均价2011年指数年均价2012年指数年均价2013年

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010

2011

2012

2010Average

2011Average

2012Average

2013

Platts (62%Fe)

焦炭价格焦炭价格焦炭价格焦炭价格1000

1200

1400

1600

1800

2000

2200

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13Coke price

废钢价格废钢价格废钢价格废钢价格2400

2800

3200

3600

4000

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13Scrap price

Data source: Mysteel

� Steel Price

Unit:

Yuan/ton22 Mar MoM% YoY%

Average

2012YoY%

HRC 4020 -3.8 -7.2 4117 -12.7

CRC 4930 -1.8 -6.3 4888 -10.6

Plate 3990 -2.9 -10.1 4007 -16.6

Wire 3490 -5.2 -15.9 3830 -18.5

Rebar 3680 -6.4 -12.8 3954 -15.9

Data source: Mysteel

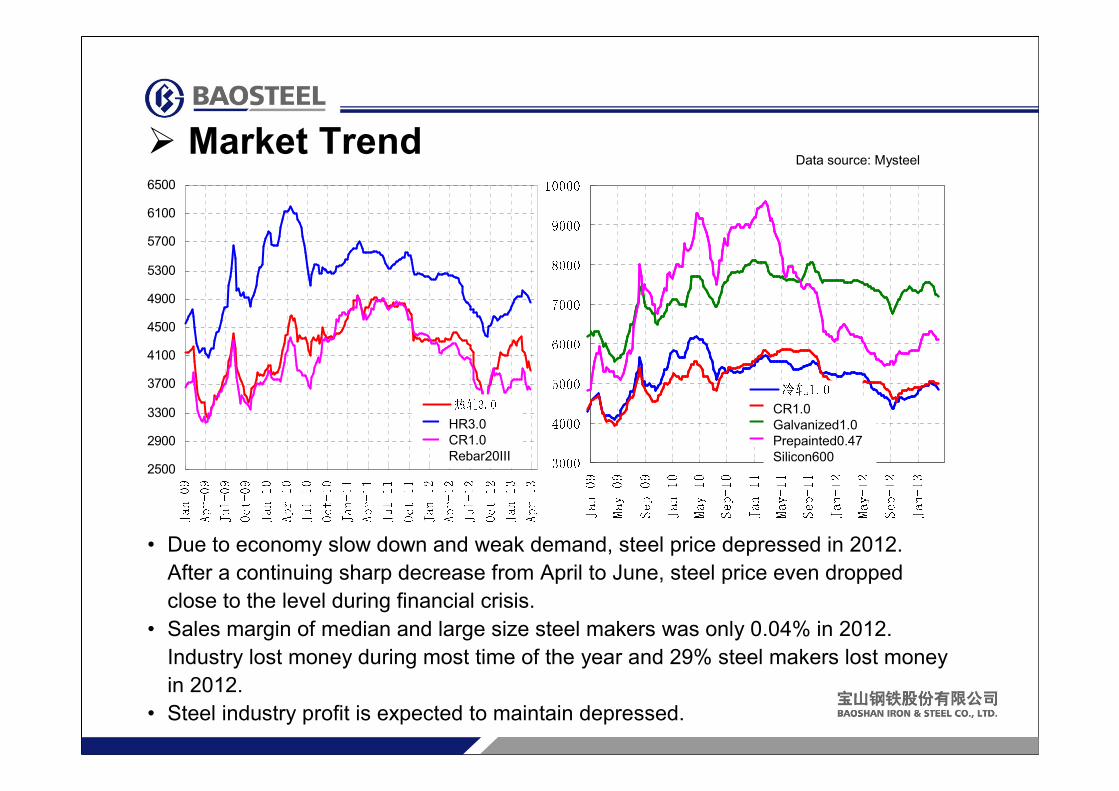

• Due to economy slow down and weak demand, steel price depressed in 2012.

After a continuing sharp decrease from April to June, steel price even dropped

close to the level during financial crisis.

• Sales margin of median and large size steel makers was only 0.04% in 2012.

Industry lost money during most time of the year and 29% steel makers lost money

in 2012.

• Steel industry profit is expected to maintain depressed.

� Market TrendData source: Mysteel

2500

2900

3300

3700

4100

4500

4900

5300

5700

6100

6500

Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13热轧3.0冷轧1.0螺纹20Ⅲ级HR3.0

CR1.0

Rebar20III 300040005000600070008000900010000

Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13冷轧1.0镀锌1.0彩涂0.476硅钢600CR1.0

Galvanized1.0

Prepainted0.47

Silicon600

I. Operation Results

II. Industry Dynamics

III.Company Outlook

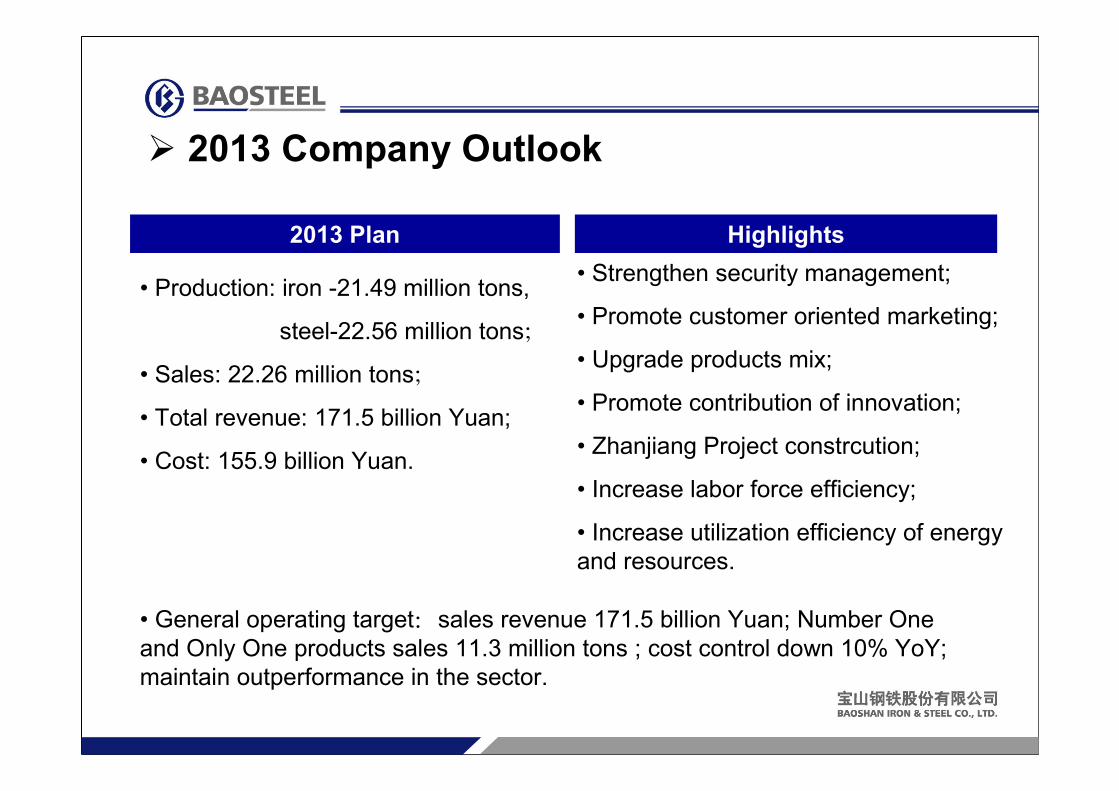

� 2013 Company Outlook

2013 Plan Highlights

• Production: iron -21.49 million tons,

steel-22.56 million tons;

• Sales: 22.26 million tons;

• Total revenue: 171.5 billion Yuan;

• Cost: 155.9 billion Yuan.

• Strengthen security management;

• Promote customer oriented marketing;

• Upgrade products mix;

• Promote contribution of innovation;

• Zhanjiang Project constrcution;

• Increase labor force efficiency;

• Increase utilization efficiency of energy

and resources.

• General operating target:sales revenue 171.5 billion Yuan; Number One

and Only One products sales 11.3 million tons ; cost control down 10% YoY;

maintain outperformance in the sector.

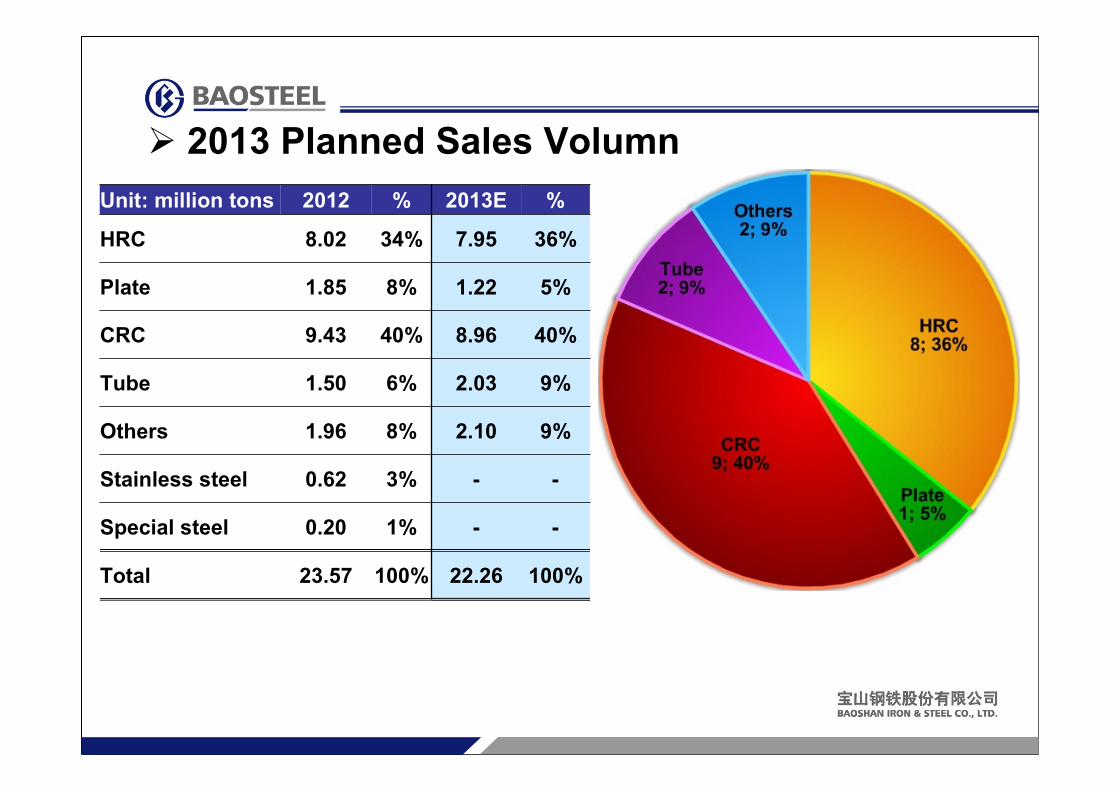

Unit: million tons 2012 % 2013E %

HRC 8.02 34% 7.95 36%

Plate 1.85 8% 1.22 5%

CRC 9.43 40% 8.96 40%

Tube 1.50 6% 2.03 9%

Others 1.96 8% 2.10 9%

Stainless steel 0.62 3% - -

Special steel 0.20 1% - -

Total 23.57 100% 22.26 100%

� 2013 Planned Sales Volumn

� CAPEX

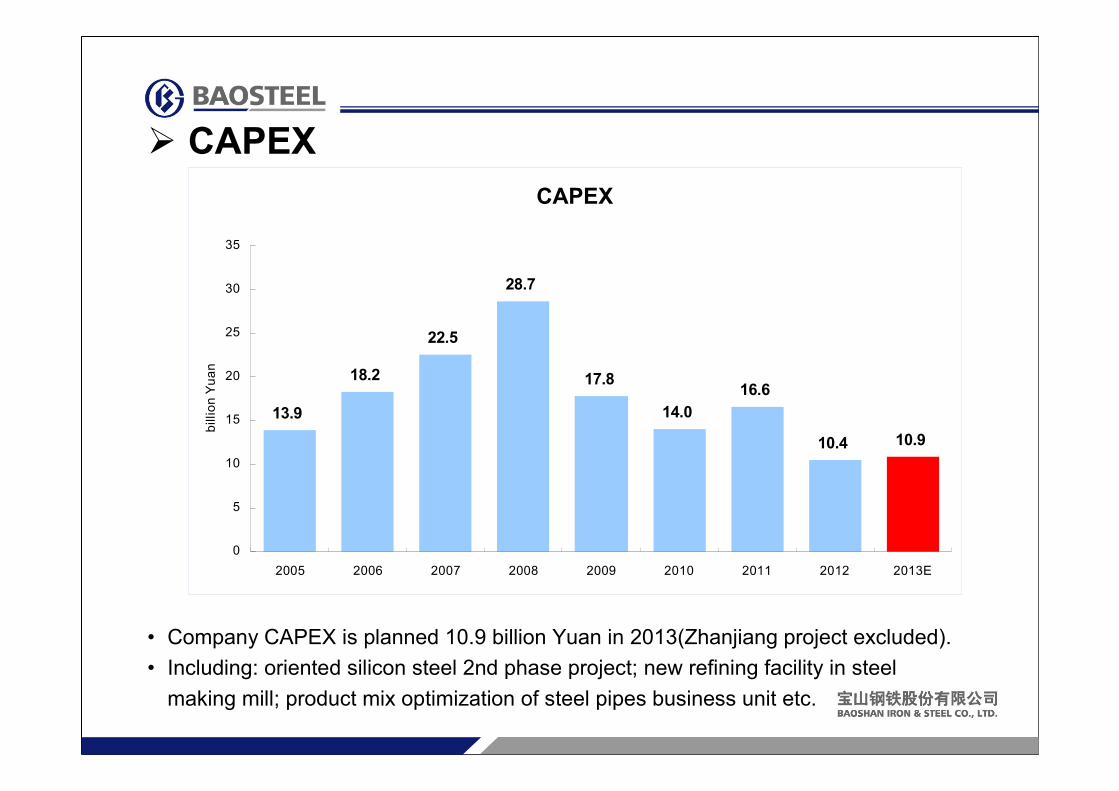

• Company CAPEX is planned 10.9 billion Yuan in 2013(Zhanjiang project excluded).

• Including: oriented silicon steel 2nd phase project; new refining facility in steel

making mill; product mix optimization of steel pipes business unit etc.

CAPEX

13.9

18.2

22.5

28.7

17.8

14.0

16.6

10.4 10.9

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012 2013E

billion Yuan