Bank of Cyprus Groupbankofcyprus.com/globalassets/investor-relations/...19.7 19.0 18.8 Dec 2013 Jun...

45

Bank of Cyprus Group Investor presentation January 2017

Transcript of Bank of Cyprus Groupbankofcyprus.com/globalassets/investor-relations/...19.7 19.0 18.8 Dec 2013 Jun...

Bank of Cyprus Group

Investor presentation

January 2017

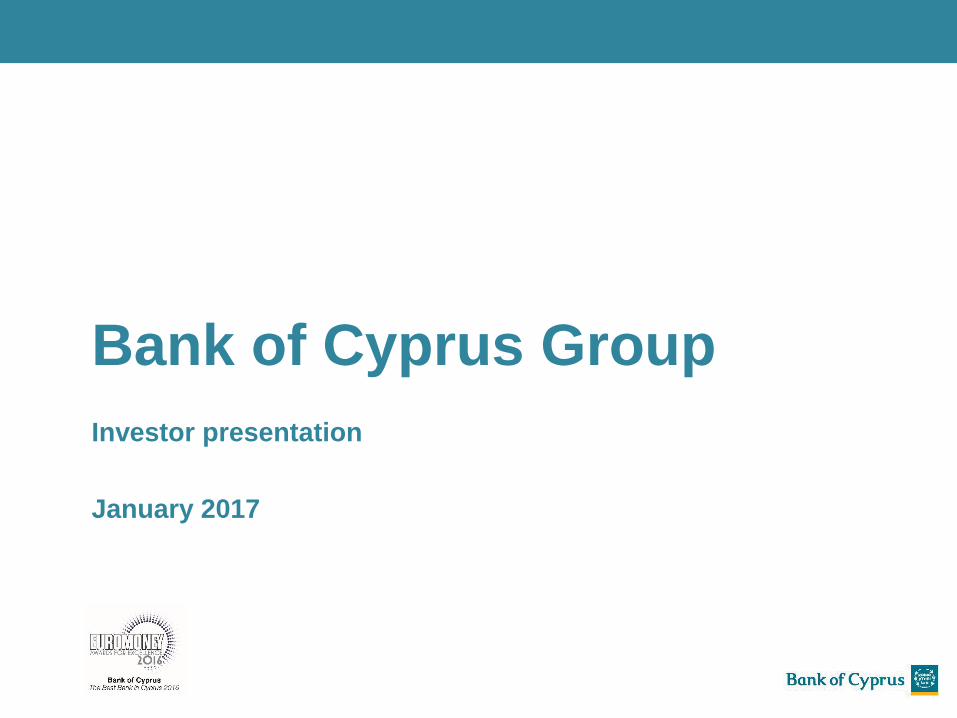

Key messages

• BOC is the largest bank in Cyprus

• Dominant position in a recovering Cypriot economy

• Significant reduction in 90+DPD3 and NPEs

• Strategic focus on core Cypriot business and

expansion of UK operations

• World class Board of Directors

• Experienced management team

• Full repayment of €11,4 bn of ELA

• Funding structure normalised

• Strong capital position

Significant

progress achieved

in normalising the

Bank

Strong market

position with a

clear strategy

going forward

• Strong local market insight

• Turnaround experience

• Proven track record of delivering results

11.40.0

Apr 2013 Jan 2017

ELA (€ bn)

GDP growth in Cyprus

CET1 ratio

Asset quality (€ bn)

12.7 14.8

8.8 11.9

90+DPD NPE

14.6% 13.5%

BOC Peer avg²

1.7% 2.8% 2.2%

2015 2016E 2017E

Market share in Cyprus1

41.1% 30.1%

Loans Deposits

Peak

Strong leadership

Source: IMF, MOF

(1) As of October 2016

(2) Based on EBA Risk Dashboard Report, data as at 30 June 2016

(3) 90+DPD: defined as loans past-due for more than 90 days and those that are impaired (impaired loans are those which are not considered fully collectable and for which a provision for

impairment has been recognised on an individual basis or for which incurred losses exist at their initial recognition or customers in Debt Recovery)

Jun 2015

Sep 2016

13.8% 13.0%

BOC Peer avg²

Transitional Fully loaded

2

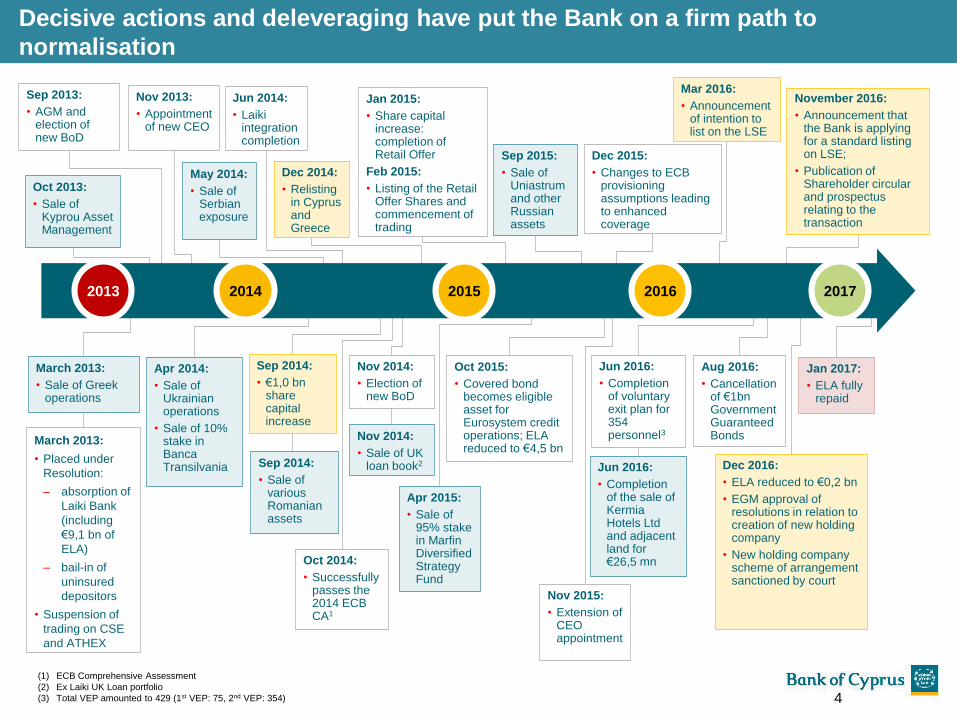

Introduction: The journey so far…

Decisive actions and deleveraging have put the Bank on a firm path to

normalisation

March 2013:

• Sale of Greek operations

Sep 2013:

• AGM and election of new BoD

Nov 2013:

• Appointment of new CEO

Nov 2015:

• Extension of CEO appointment

Dec 2014:

• Relisting in Cyprus and Greece

Sep 2014:

• €1,0 bnshare capital increase

Nov 2014:

• Election of new BoD

Mar 2016:

• Announcement of intention to list on the LSE

Dec 2015:

• Changes to ECB provisioning assumptions leading to enhanced coverage

Sep 2015:

• Sale of Uniastrumand other Russian assets

Jun 2014:

• Laikiintegration completion

Sep 2014:

• Sale of various Romanian assets

May 2014:

• Sale of Serbian exposure

Apr 2015:

• Sale of 95% stake in MarfinDiversified Strategy Fund

Apr 2014:

• Sale of Ukrainian operations

• Sale of 10% stake in BancaTransilvania

Oct 2013:

• Sale of Kyprou Asset Management

2013 2014 2015 2016

Jan 2015:

• Share capital increase: completion of Retail Offer

Feb 2015:

• Listing of the Retail Offer Shares and commencement of trading

Oct 2015:

• Covered bond becomes eligible asset for Eurosystem credit operations; ELA reduced to €4,5 bn

Oct 2014:

• Successfully passes the 2014 ECB CA1

(1) ECB Comprehensive Assessment

(2) Ex Laiki UK Loan portfolio

(3) Total VEP amounted to 429 (1st VEP: 75, 2nd VEP: 354)

Jun 2016:

• Completion of voluntary exit plan for 354 personnel3

Aug 2016:

• Cancellation of €1bn Government Guaranteed Bonds

Jun 2016:

• Completion of the sale of KermiaHotels Ltd and adjacent land for €26,5 mn

March 2013:

• Placed under

Resolution:

– absorption of

Laiki Bank

(including

€9,1 bn of

ELA)

– bail-in of

uninsured

depositors

• Suspension of

trading on CSE

and ATHEX

Nov 2014:

• Sale of UK loan book2

November 2016:

• Announcement that the Bank is applying for a standard listing on LSE;

• Publication of Shareholder circular and prospectus relating to the transaction

Jan 2017:

• ELA fully repaid

Dec 2016:

• ELA reduced to €0,2 bn

• EGM approval of resolutions in relation to creation of new holding company

• New holding company scheme of arrangement sanctioned by court

2017

4

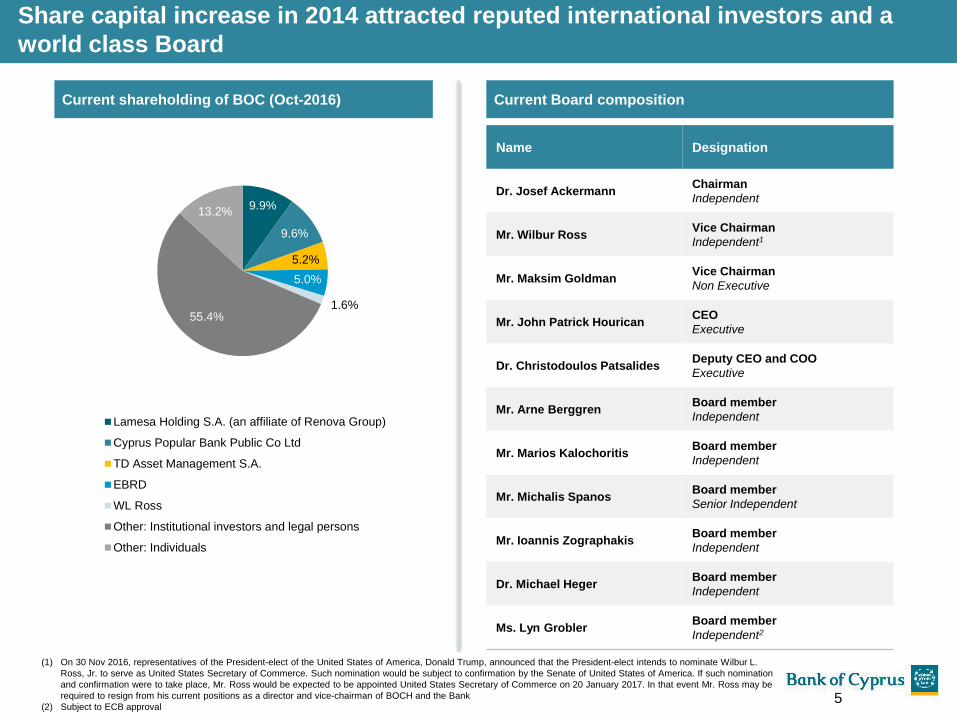

Current shareholding of BOC (Oct-2016) Current Board composition

9.9%

9.6%

5.2%

5.0%

1.6%55.4%

13.2%

Lamesa Holding S.A. (an affiliate of Renova Group)

Cyprus Popular Bank Public Co Ltd

TD Asset Management S.A.

EBRD

WL Ross

Other: Institutional investors and legal persons

Other: Individuals

Name Designation

Dr. Josef AckermannChairman

Independent

Mr. Wilbur RossVice Chairman

Independent1

Mr. Maksim GoldmanVice Chairman

Non Executive

Mr. John Patrick HouricanCEO

Executive

Dr. Christodoulos PatsalidesDeputy CEO and COO

Executive

Mr. Arne BerggrenBoard member

Independent

Mr. Marios KalochoritisBoard member

Independent

Mr. Michalis SpanosBoard member

Senior Independent

Mr. Ioannis ZographakisBoard member

Independent

Dr. Michael HegerBoard member

Independent

Ms. Lyn GroblerBoard member

Independent2

Share capital increase in 2014 attracted reputed international investors and a

world class Board

(1) On 30 Nov 2016, representatives of the President-elect of the United States of America, Donald Trump, announced that the President-elect intends to nominate Wilbur L.

Ross, Jr. to serve as United States Secretary of Commerce. Such nomination would be subject to confirmation by the Senate of United States of America. If such nomination

and confirmation were to take place, Mr. Ross would be expected to be appointed United States Secretary of Commerce on 20 January 2017. In that event Mr. Ross may be

required to resign from his current positions as a director and vice-chairman of BOCH and the Bank

(2) Subject to ECB approval5

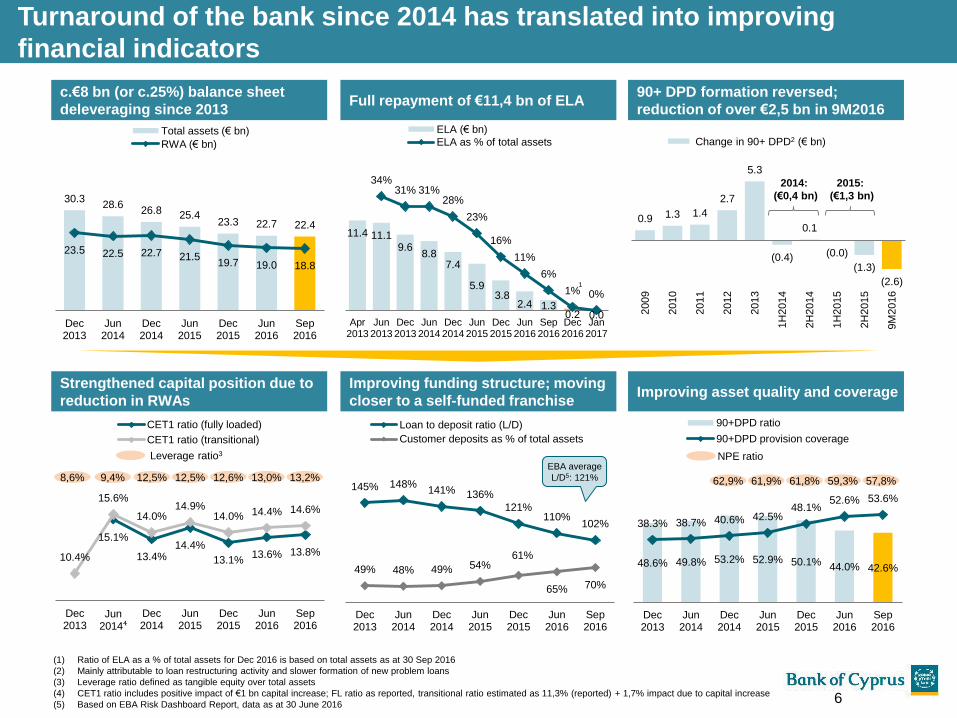

Strengthened capital position due to

reduction in RWAs

c.€8 bn (or c.25%) balance sheet

deleveraging since 2013

Improving funding structure; moving

closer to a self-funded franchise

Turnaround of the bank since 2014 has translated into improving

financial indicators

(1) Ratio of ELA as a % of total assets for Dec 2016 is based on total assets as at 30 Sep 2016

(2) Mainly attributable to loan restructuring activity and slower formation of new problem loans

(3) Leverage ratio defined as tangible equity over total assets

(4) CET1 ratio includes positive impact of €1 bn capital increase; FL ratio as reported, transitional ratio estimated as 11,3% (reported) + 1,7% impact due to capital increase

(5) Based on EBA Risk Dashboard Report, data as at 30 June 2016

30.328.6

26.8 25.423.3 22.7 22.4

23.5 22.5 22.7 21.519.7 19.0 18.8

Dec2013

Jun2014

Dec2014

Jun2015

Dec2015

Jun2016

Sep2016

Total assets (€ bn)

RWA (€ bn)

145% 148%141% 136%

121%110%

102%

49% 48% 49% 54%61%

65% 70%

Dec2013

Jun2014

Dec2014

Jun2015

Dec2015

Jun2016

Sep2016

Loan to deposit ratio (L/D)

Customer deposits as % of total assets

Full repayment of €11,4 bn of ELA90+ DPD formation reversed;

reduction of over €2,5 bn in 9M2016

Improving asset quality and coverage

0.9 1.3 1.4

2.7

5.3

(0.4)

0.1

(0.0)

(1.3)

(2.6)

2009

2010

2011

2012

2013

1H

2014

2H

2014

1H

2015

2H

2015

9M

2016

48.6% 49.8% 53.2% 52.9% 50.1% 44.0% 42.6%

38.3% 38.7% 40.6% 42.5%48.1%

52.6% 53.6%

Dec2013

Jun2014

Dec2014

Jun2015

Dec2015

Jun2016

Sep2016

90+DPD ratio

90+DPD provision coverage

15.1%

13.4%14.4%

13.1%13.6% 13.8%

10.4%

15.6%

14.0%14.9%

14.0% 14.4% 14.6%

Dec2013

Jun2014⁴

Dec2014

Jun2015

Dec2015

Jun2016

Sep2016

CET1 ratio (fully loaded)

CET1 ratio (transitional)

Change in 90+ DPD2 (€ bn)

EBA average

L/D5: 121%

2014:

(€0,4 bn)

2015:

(€1,3 bn)

62,9% 61,9% 61,8% 59,3% 57,8%

NPE ratio

11.4 11.19.6

8.87.4

5.93.8

2.4 1.30.2 0.0

34%31% 31%

28%

23%

16%

11%

6%

1% 0%

Apr2013

Jun2013

Dec2013

Jun2014

Dec2014

Jun2015

Dec2015

Jun2016

Sep2016

Dec2016

Jan2017

ELA (€ bn)

ELA as % of total assets

1

12,5% 12,5% 12,6% 13,0% 13,2%

Leverage ratio3

9,4%8,6%

6

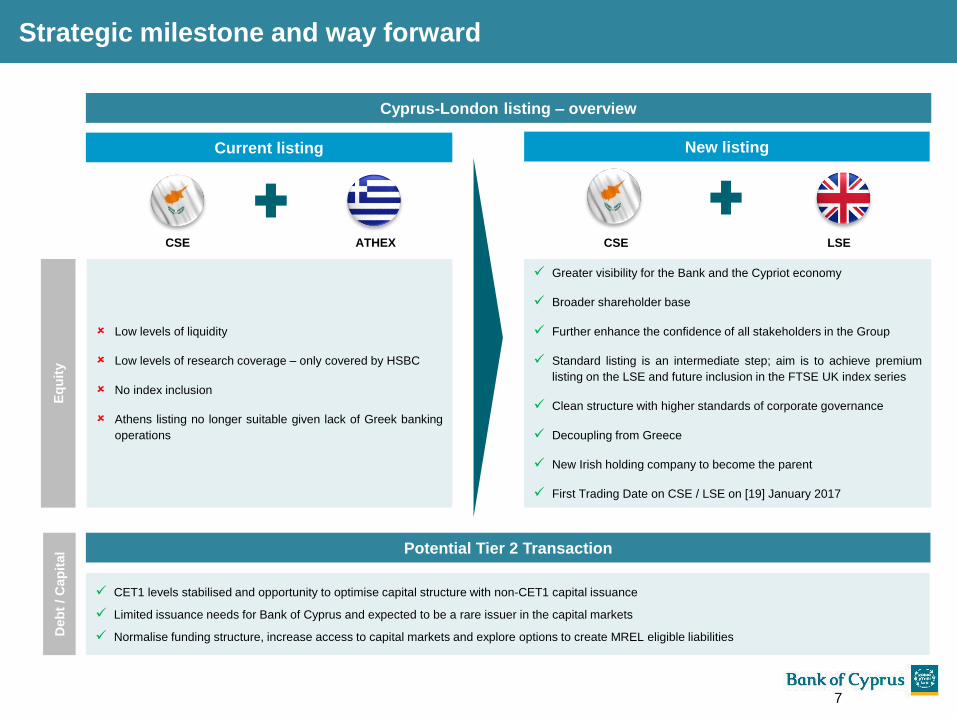

Strategic milestone and way forward

Low levels of liquidity

Low levels of research coverage – only covered by HSBC

No index inclusion

Athens listing no longer suitable given lack of Greek banking

operations

Greater visibility for the Bank and the Cypriot economy

Broader shareholder base

Further enhance the confidence of all stakeholders in the Group

Standard listing is an intermediate step; aim is to achieve premium

listing on the LSE and future inclusion in the FTSE UK index series

Clean structure with higher standards of corporate governance

Decoupling from Greece

New Irish holding company to become the parent

First Trading Date on CSE / LSE on [19] January 2017

Current listing New listing

CSE ATHEX CSE LSE

Potential Tier 2 Transaction

CET1 levels stabilised and opportunity to optimise capital structure with non-CET1 capital issuance

Limited issuance needs for Bank of Cyprus and expected to be a rare issuer in the capital markets

Normalise funding structure, increase access to capital markets and explore options to create MREL eligible liabilities

Cyprus-London listing – overview

Eq

uit

yD

eb

t / C

ap

ital

7

Key Investment Highlights

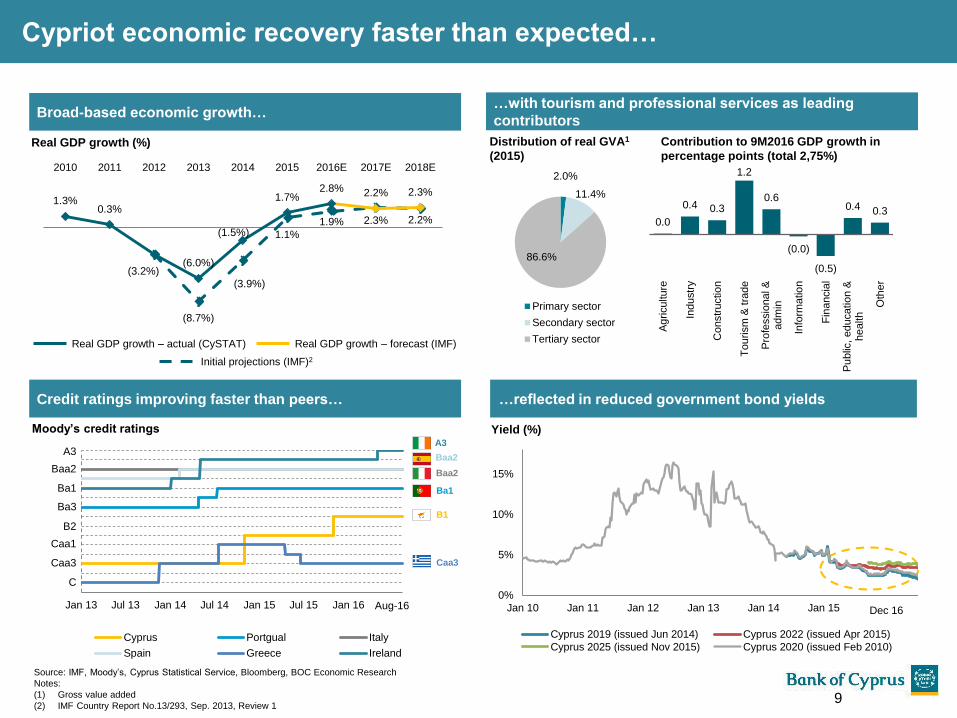

Cypriot economic recovery faster than expected…

Real GDP growth (%) Contribution to 9M2016 GDP growth in

percentage points (total 2,75%)

Source: IMF, Moody’s, Cyprus Statistical Service, Bloomberg, BOC Economic Research

Notes:

(1) Gross value added

(2) IMF Country Report No.13/293, Sep. 2013, Review 1

Broad-based economic growth……with tourism and professional services as leading

contributors

…reflected in reduced government bond yields

(8.7%)

(3.9%)

1.1%

1.9% 2.3% 2.2%

1.3%0.3%

(3.2%)(6.0%)

(1.5%)

1.7%2.8% 2.2% 2.3%

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Yield (%)

Jan 13 Jul 13 Jan 14 Jul 14 Jan 15 Jul 15 Jan 16 Jul 16

Cyprus Portgual Italy

Spain Greece Ireland

Baa2

Ba1

Ba3

B2

Caa1

C

A3

B1

Baa2

Ba1

Baa2

Caa3

Moody’s credit ratings

Caa3

Credit ratings improving faster than peers…

A3

Aug-16

0.0

0.4 0.3

1.2

0.6

(0.0)

(0.5)

0.4 0.3

Ag

riculture

Industr

y

Constr

uctio

n

To

urism

& tra

de

Pro

fessio

nal &

adm

in

Info

rma

tio

n

Fin

ancia

l

Pu

blic

, educatio

n &

health

Oth

er

0%

5%

10%

15%

Jan 10 Jan 11 Jan 12 Jan 13 Jan 14 Jan 15 Jan 16

Cyprus 2019 (issued Jun 2014) Cyprus 2022 (issued Apr 2015)

Cyprus 2025 (issued Nov 2015) Cyprus 2020 (issued Feb 2010)

Dec 16

2.0%

11.4%

86.6%

Primary sector

Secondary sector

Tertiary sector

Distribution of real GVA1

(2015)

Initial projections (IMF)2

Real GDP growth – actual (CySTAT) Real GDP growth – forecast (IMF)

9

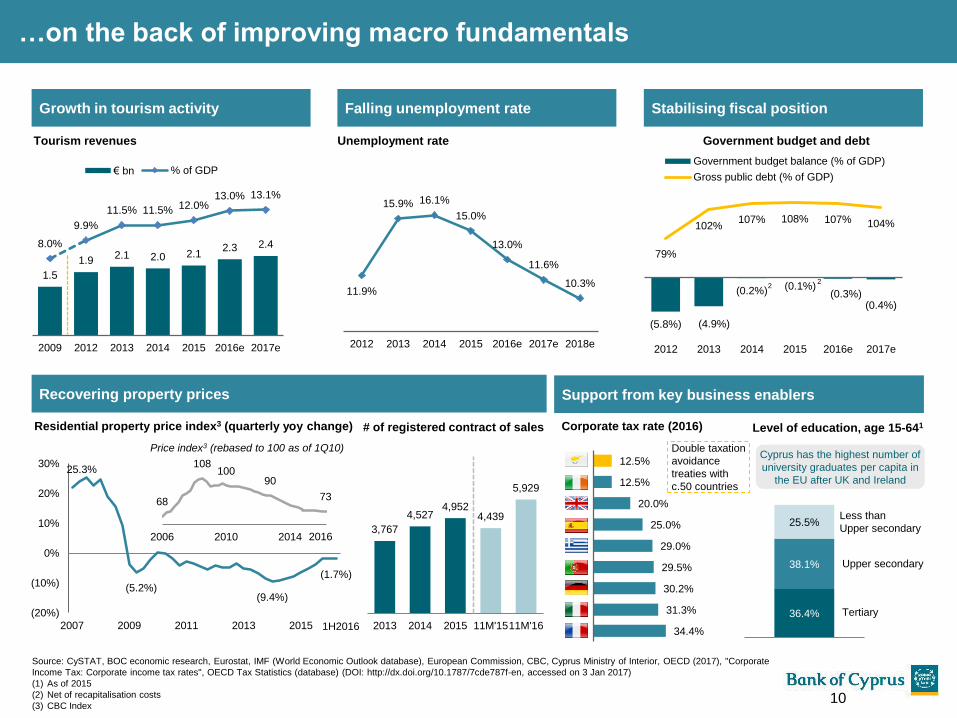

…on the back of improving macro fundamentals

Falling unemployment rateGrowth in tourism activity

Tourism revenues

1.5

1.9 2.1 2.0 2.1

2.3 2.4 8.0%

9.9%

11.5% 11.5% 12.0%13.0% 13.1%

2009 2012 2013 2014 2015 2016e 2017e

€ bn % of GDP

(5.8%) (4.9%)

(0.2%) (0.1%)(0.3%)

(0.4%)

79%

102%107% 108% 107% 104%

2012 2013 2014 2015 2016e 2017e

Government budget balance (% of GDP)

Gross public debt (% of GDP)

Government budget and debt

Stabilising fiscal position

Support from key business enablers

Unemployment rate

11.9%

15.9% 16.1%

15.0%

13.0%

11.6%

10.3%

2012 2013 2014 2015 2016e 2017e 2018e

Recovering property prices

Residential property price index3 (quarterly yoy change)

1H2016

3,767

4,527 4,952

4,439

5,929

2013 2014 2015 11M'1511M'16

# of registered contract of sales

68

108 100

90

73

2006 2010 2014

Price index3 (rebased to 100 as of 1Q10)

2016

34.4%

31.3%

30.2%

29.5%

29.0%

25.0%

20.0%

12.5%

12.5%

Corporate tax rate (2016)

Double taxation

avoidance

treaties with

c.50 countries

Source: CySTAT, BOC economic research, Eurostat, IMF (World Economic Outlook database), European Commission, CBC, Cyprus Ministry of Interior, OECD (2017), "Corporate

Income Tax: Corporate income tax rates", OECD Tax Statistics (database) (DOI: http://dx.doi.org/10.1787/7cde787f-en, accessed on 3 Jan 2017)

(1) As of 2015

(2) Net of recapitalisation costs

(3) CBC Index

22

25.3%

(5.2%)(9.4%)

(1.7%)

(20%)

(10%)

0%

10%

20%

30%

2007 2009 2011 2013 201536.4%

38.1%

25.5%

Upper secondary

Less than

Upper secondary

Tertiary

Level of education, age 15-641

Cyprus has the highest number of

university graduates per capita in

the EU after UK and Ireland

10

45 46

Non-life

18.8

12.3

5.3 4.21.5

61 55

Gross loans

€ bn

Branch

network

# branches

Deposits

€ bn

29,5%3

Insurance

premiums1

€ mn

Source: CBC, company disclosure as of 9M2016

(1) 9M2016 (provisional results)

(2) 49,9% owned by the Bank

(3) Market shares for insurance premiums as at 30 September 2016 (on provisional results)

(4) As of October 2016

Life

13,5%3

2 2

14.2 12.5

1.96.0

3.7

123

246

2255

8

41,1%4

30,1%4

xx% Market shares

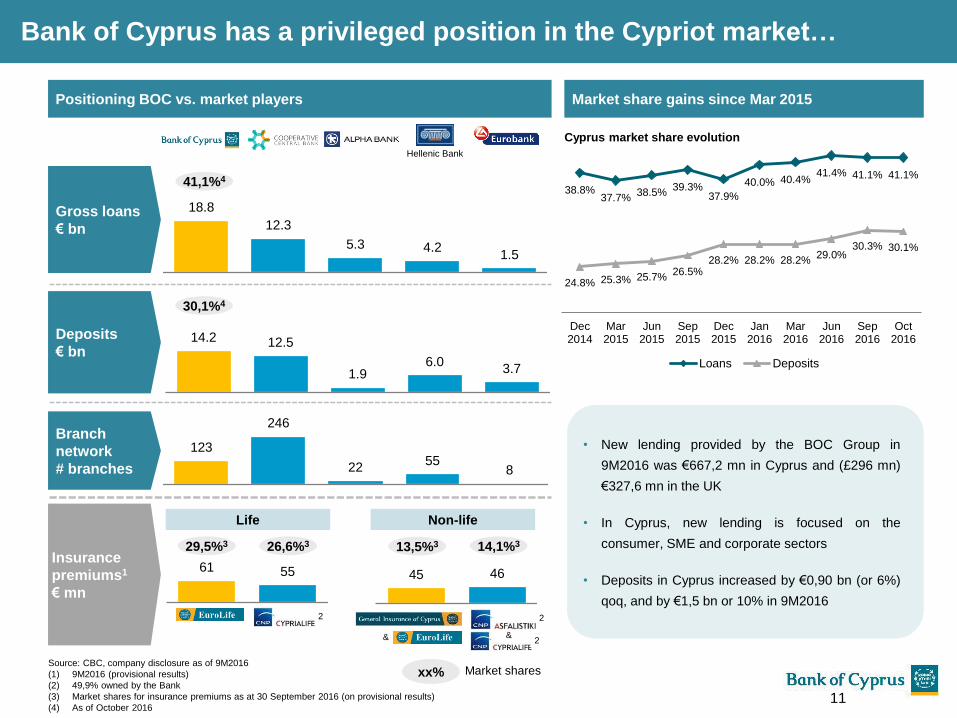

Bank of Cyprus has a privileged position in the Cypriot market…

Hellenic Bank

& &2

38.8%37.7%

38.5%39.3%

37.9%

40.0% 40.4%41.4% 41.1% 41.1%

24.8% 25.3% 25.7%26.5%

28.2% 28.2% 28.2%29.0%

30.3% 30.1%

Dec2014

Mar2015

Jun2015

Sep2015

Dec2015

Jan2016

Mar2016

Jun2016

Sep2016

Oct2016

Loans Deposits

Cyprus market share evolution

Positioning BOC vs. market players Market share gains since Mar 2015

• New lending provided by the BOC Group in

9M2016 was €667,2 mn in Cyprus and (£296 mn)

€327,6 mn in the UK

• In Cyprus, new lending is focused on the

consumer, SME and corporate sectors

• Deposits in Cyprus increased by €0,90 bn (or 6%)

qoq, and by €1,5 bn or 10% in 9M2016

26,6%3 14,1%3

11

44%

22%

23%

11%

Corporate SME Retail housing Retail other

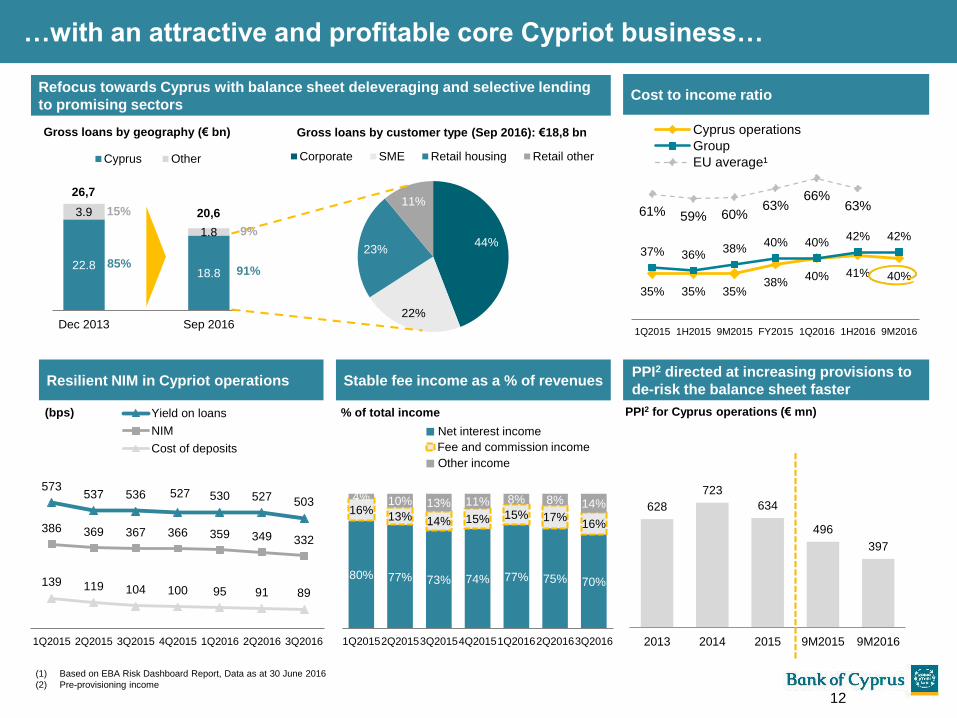

Resilient NIM in Cypriot operations

573537 536 527 530 527 503

386 369 367 366 359 349 332

139 119 104 100 95 91 89

1Q2015 2Q2015 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016

Yield on loans

NIM

Cost of deposits

Refocus towards Cyprus with balance sheet deleveraging and selective lending

to promising sectors

80% 77% 73% 74% 77% 75% 70%

16%13% 14% 15% 15% 17%

16%

4% 10% 13% 11% 8% 8% 14%

1Q20152Q20153Q20154Q20151Q20162Q20163Q2016

Stable fee income as a % of revenues

(bps)

12

…with an attractive and profitable core Cypriot business…

PPI2 directed at increasing provisions to

de-risk the balance sheet faster

Gross loans by geography (€ bn) Gross loans by customer type (Sep 2016): €18,8 bn

Cost to income ratio

22.818.8

3.9

1.8

Dec 2013 Sep 2016

Cyprus Other

15%

85%91%

9%

26,7

20,6

Net interest income

Fee and commission income

Other income

% of total income

628

723

634

496

397

2013 2014 2015 9M2015 9M2016

PPI2 for Cyprus operations (€ mn)

35% 35% 35%38%

40% 41% 40%

37% 36%38%

40% 40%42% 42%

61% 59% 60%63%

66%63%

1Q2015 1H2015 9M2015 FY2015 1Q2016 1H2016 9M2016

Cyprus operations

Group

EU average¹

(1) Based on EBA Risk Dashboard Report, Data as at 30 June 2016

(2) Pre-provisioning income

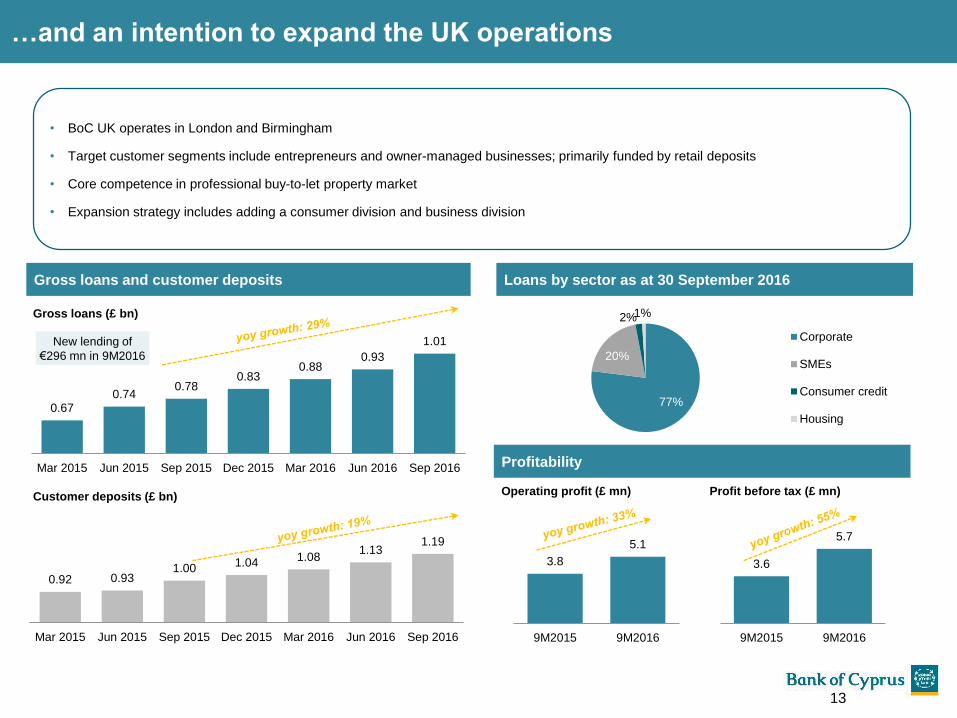

…and an intention to expand the UK operations

• BoC UK operates in London and Birmingham

• Target customer segments include entrepreneurs and owner-managed businesses; primarily funded by retail deposits

• Core competence in professional buy-to-let property market

• Expansion strategy includes adding a consumer division and business division

Gross loans and customer deposits Loans by sector as at 30 September 2016

0.67 0.74

0.78 0.83

0.88 0.93

1.01

Mar 2015 Jun 2015 Sep 2015 Dec 2015 Mar 2016 Jun 2016 Sep 2016

77%

20%

2%1%

Corporate

SMEs

Consumer credit

Housing

0.92 0.93 1.00 1.04 1.08

1.13 1.19

Mar 2015 Jun 2015 Sep 2015 Dec 2015 Mar 2016 Jun 2016 Sep 2016

Gross loans (£ bn)

Customer deposits (£ bn)

3.8

5.1

9M2015 9M2016

Profitability

Operating profit (£ mn) Profit before tax (£ mn)

3.6

5.7

9M2015 9M2016

New lending of

€296 mn in 9M2016

13

14

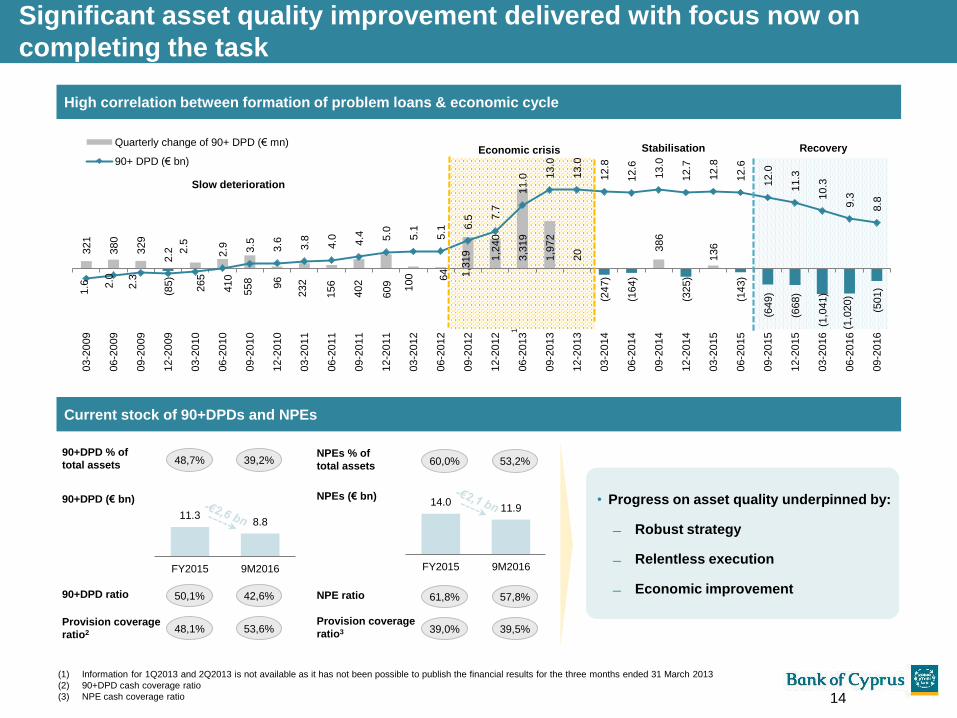

Significant asset quality improvement delivered with focus now on

completing the task

321

380

329

(85)

265

410

558 96

232

156

402

609 100 64 1,3

19 1,2

40

3,3

19

1,9

72

20

(247)

(164)

386

(325)

136

(143)

(649)

(668)

(1,0

41)

(1,0

20)

(501)1.6 2

.0

2.3

2.2 2

.5

2.9 3.5

3.6 3.8 4.0 4.4 5.0

5.1

5.1 6

.5 7.7

11.0 1

3.0

13.0

12.8

12.6

13.0

12.7

12.8

12.6

12.0

11.3

10.3

9.3

8.8

03-2

009

06-2

009

09-2

009

12-2

009

03-2

010

06-2

010

09-2

010

12-2

010

03-2

011

06-2

011

09-2

011

12-2

011

03-2

012

06-2

012

09-2

012

12-2

012

06-2

013

09-2

013

12-2

013

03-2

014

06-2

014

09-2

014

12-2

014

03-2

015

06-2

015

09-2

015

12-2

015

03-2

016

06-2

016

09-2

016

Quarterly change of 90+ DPD (€ mn)

90+ DPD (€ bn)

1

Slow deterioration

Economic crisis Stabilisation Recovery

High correlation between formation of problem loans & economic cycle

(1) Information for 1Q2013 and 2Q2013 is not available as it has not been possible to publish the financial results for the three months ended 31 March 2013

(2) 90+DPD cash coverage ratio

(3) NPE cash coverage ratio

Current stock of 90+DPDs and NPEs

• Progress on asset quality underpinned by:

Robust strategy

Relentless execution

Economic improvement

11.38.8

FY2015 9M2016

50,1% 42,6%90+DPD ratio

48,1% 53,6%Provision coverage

ratio2

90+DPD (€ bn) 14.011.9

FY2015 9M2016

61,8% 57,8%NPE ratio

39,0% 39,5%Provision coverage

ratio3

NPEs (€ bn)

48,7% 39,2%90+DPD % of

total assets 60,0% 53,2%NPEs % of

total assets

15

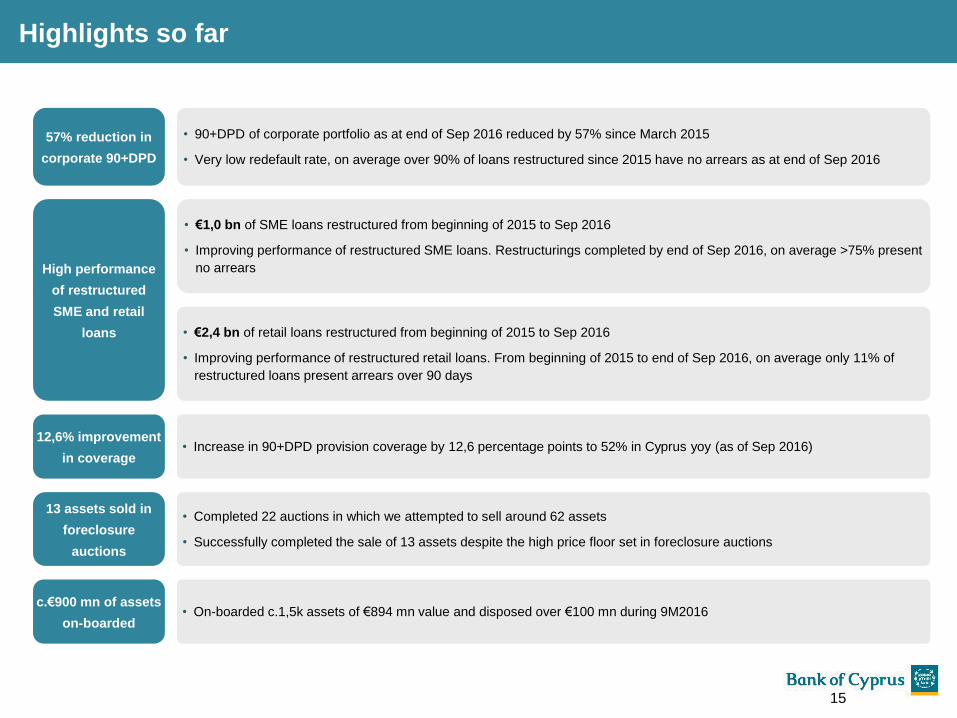

Highlights so far

• 90+DPD of corporate portfolio as at end of Sep 2016 reduced by 57% since March 2015

• Very low redefault rate, on average over 90% of loans restructured since 2015 have no arrears as at end of Sep 2016

57% reduction in

corporate 90+DPD

• €1,0 bn of SME loans restructured from beginning of 2015 to Sep 2016

• Improving performance of restructured SME loans. Restructurings completed by end of Sep 2016, on average >75% present

no arrearsHigh performance

of restructured

SME and retail

loans • €2,4 bn of retail loans restructured from beginning of 2015 to Sep 2016

• Improving performance of restructured retail loans. From beginning of 2015 to end of Sep 2016, on average only 11% of

restructured loans present arrears over 90 days

• Increase in 90+DPD provision coverage by 12,6 percentage points to 52% in Cyprus yoy (as of Sep 2016)12,6% improvement

in coverage

• Completed 22 auctions in which we attempted to sell around 62 assets

• Successfully completed the sale of 13 assets despite the high price floor set in foreclosure auctions

13 assets sold in

foreclosure

auctions

• On-boarded c.1,5k assets of €894 mn value and disposed over €100 mn during 9M2016c.€900 mn of assets

on-boarded

16

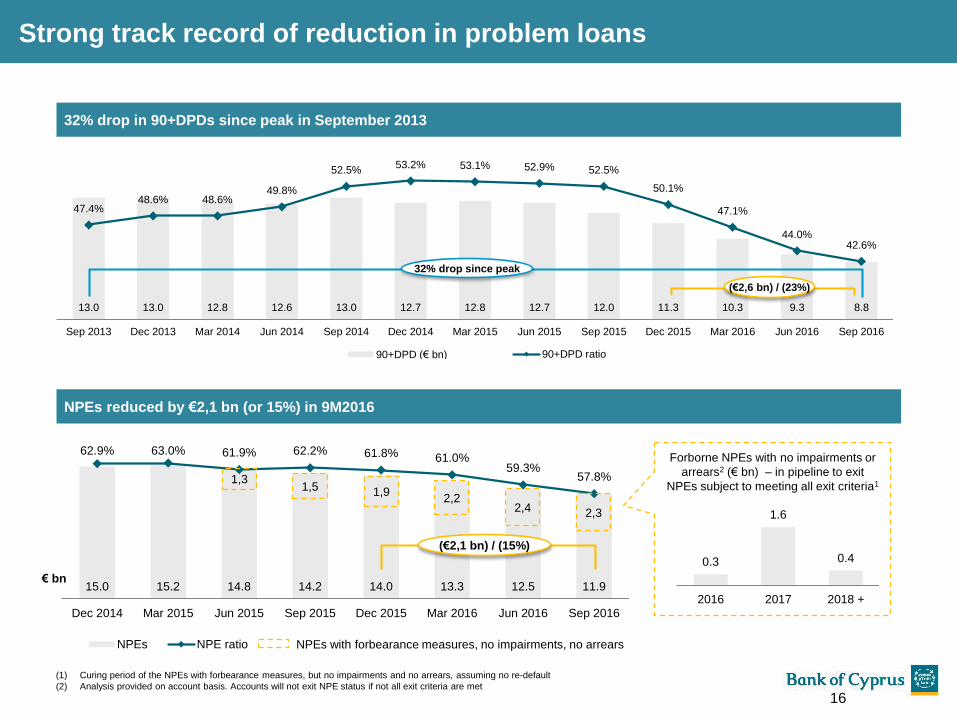

32% drop in 90+DPDs since peak in September 2013

13.0 13.0 12.8 12.6 13.0 12.7 12.8 12.7 12.0 11.3 10.3 9.3 8.8

47.4%48.6% 48.6%

49.8%

52.5%53.2% 53.1% 52.9% 52.5%

50.1%

47.1%

44.0%42.6%

Sep 2013 Dec 2013 Mar 2014 Jun 2014 Sep 2014 Dec 2014 Mar 2015 Jun 2015 Sep 2015 Dec 2015 Mar 2016 Jun 2016 Sep 2016

90+DPD (€ bn) 90+DPD ratio

(€2,6 bn) / (23%)

32% drop since peak

NPEs reduced by €2,1 bn (or 15%) in 9M2016

15.0 15.2 14.8 14.2 14.0 13.3 12.5 11.9

62.9% 63.0% 61.9% 62.2% 61.8% 61.0%59.3%

57.8%

Dec 2014 Mar 2015 Jun 2015 Sep 2015 Dec 2015 Mar 2016 Jun 2016 Sep 2016

NPEs NPE ratio

€ bn

2,4

Forborne NPEs with no impairments or

arrears2 (€ bn) – in pipeline to exit

NPEs subject to meeting all exit criteria1

0.3

1.6

0.4

2016 2017 2018 +

2,21,9

(€2,1 bn) / (15%)

2,3

(1) Curing period of the NPEs with forbearance measures, but no impairments and no arrears, assuming no re-default

(2) Analysis provided on account basis. Accounts will not exit NPE status if not all exit criteria are met

1,51,3

NPEs with forbearance measures, no impairments, no arrears

Strong track record of reduction in problem loans

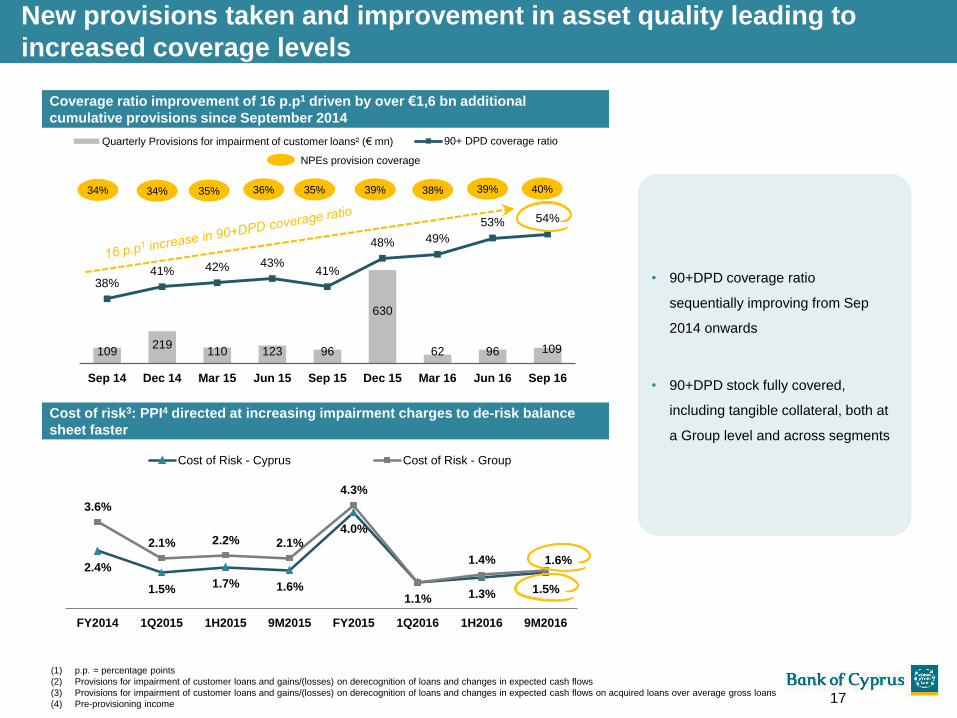

New provisions taken and improvement in asset quality leading to

increased coverage levels

Cost of risk3: PPI4 directed at increasing impairment charges to de-risk balance

sheet faster

2.4%

1.5% 1.7% 1.6%

4.0%

1.1% 1.3% 1.5%

3.6%

2.1% 2.2% 2.1%

4.3%

1.4% 1.6%

FY2014 1Q2015 1H2015 9M2015 FY2015 1Q2016 1H2016 9M2016

Cost of Risk - Cyprus Cost of Risk - Group

Coverage ratio improvement of 16 p.p1 driven by over €1,6 bn additional

cumulative provisions since September 2014

(1) p.p. = percentage points

(2) Provisions for impairment of customer loans and gains/(losses) on derecognition of loans and changes in expected cash flows

(3) Provisions for impairment of customer loans and gains/(losses) on derecognition of loans and changes in expected cash flows on acquired loans over average gross loans

(4) Pre-provisioning income

109219

110 123 96

630

62 96 109

38%41% 42% 43%

41%

48% 49%

53% 54%

Sep 14 Dec 14 Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16

Quarterly Provisions for impairment of customer loans² (€ mn) 90+ DPD coverage ratio

34% 34% 35% 36% 35% 39% 38% 39% 40%

NPEs provision coverage

• 90+DPD coverage ratio

sequentially improving from Sep

2014 onwards

• 90+DPD stock fully covered,

including tangible collateral, both at

a Group level and across segments

17

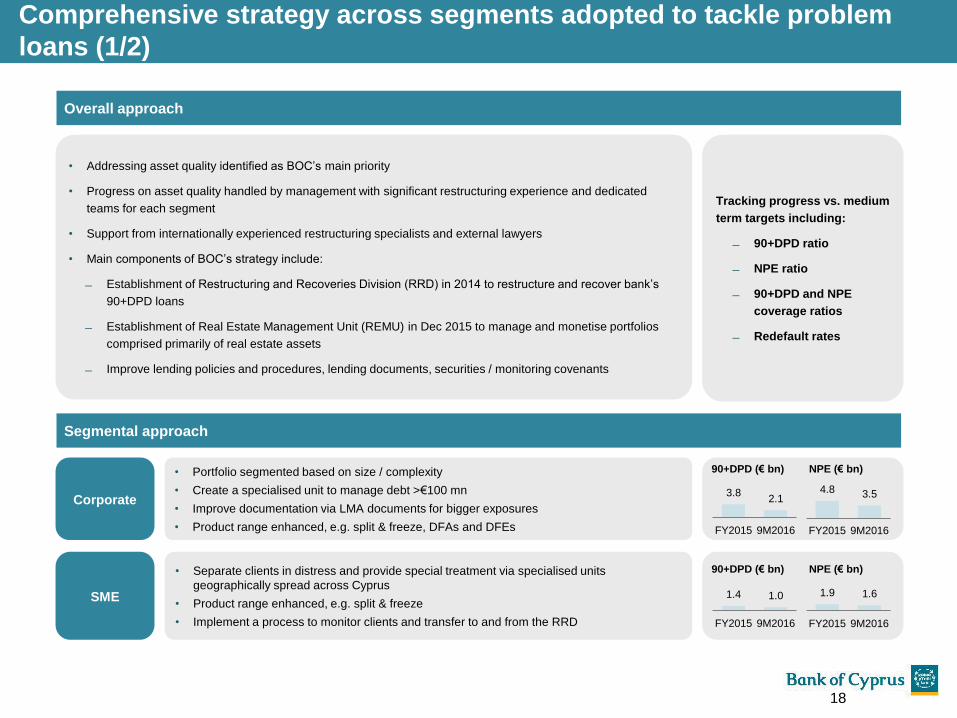

Comprehensive strategy across segments adopted to tackle problem

loans (1/2)

• Portfolio segmented based on size / complexity

• Create a specialised unit to manage debt >€100 mn

• Improve documentation via LMA documents for bigger exposures

• Product range enhanced, e.g. split & freeze, DFAs and DFEs

Corporate

• Separate clients in distress and provide special treatment via specialised units

geographically spread across Cyprus

• Product range enhanced, e.g. split & freeze

• Implement a process to monitor clients and transfer to and from the RRD

SME

3.82.1

FY2015 9M2016

90+DPD (€ bn) NPE (€ bn)

4.8 3.5

FY2015 9M2016

1.4 1.0

FY2015 9M2016

90+DPD (€ bn) NPE (€ bn)

1.9 1.6

FY2015 9M2016

Segmental approach

Overall approach

• Addressing asset quality identified as BOC’s main priority

• Progress on asset quality handled by management with significant restructuring experience and dedicated

teams for each segment

• Support from internationally experienced restructuring specialists and external lawyers

• Main components of BOC’s strategy include:

Establishment of Restructuring and Recoveries Division (RRD) in 2014 to restructure and recover bank’s

90+DPD loans

Establishment of Real Estate Management Unit (REMU) in Dec 2015 to manage and monetise portfolios

comprised primarily of real estate assets

Improve lending policies and procedures, lending documents, securities / monitoring covenants

18

Tracking progress vs. medium

term targets including:

90+DPD ratio

NPE ratio

90+DPD and NPE

coverage ratios

Redefault rates

19

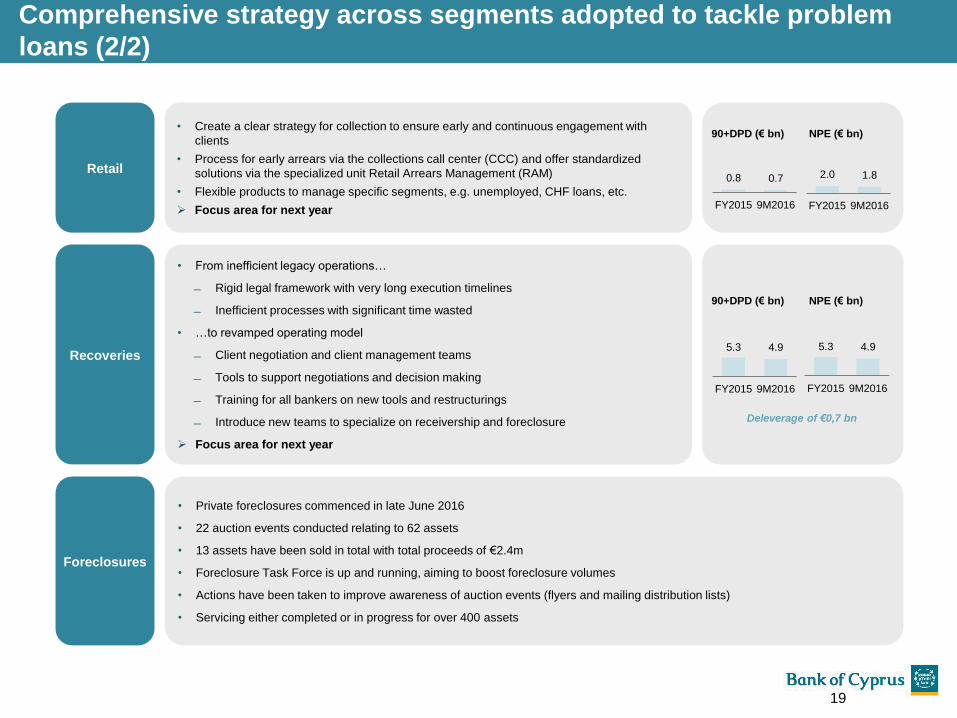

Comprehensive strategy across segments adopted to tackle problem

loans (2/2)

• From inefficient legacy operations…

Rigid legal framework with very long execution timelines

Inefficient processes with significant time wasted

• …to revamped operating model

Client negotiation and client management teams

Tools to support negotiations and decision making

Training for all bankers on new tools and restructurings

Introduce new teams to specialize on receivership and foreclosure

Focus area for next year

Recoveries

• Private foreclosures commenced in late June 2016

• 22 auction events conducted relating to 62 assets

• 13 assets have been sold in total with total proceeds of €2.4m

• Foreclosure Task Force is up and running, aiming to boost foreclosure volumes

• Actions have been taken to improve awareness of auction events (flyers and mailing distribution lists)

• Servicing either completed or in progress for over 400 assets

Foreclosures

5.3 4.9

FY2015 9M2016

90+DPD (€ bn) NPE (€ bn)

• Create a clear strategy for collection to ensure early and continuous engagement with

clients

• Process for early arrears via the collections call center (CCC) and offer standardized

solutions via the specialized unit Retail Arrears Management (RAM)

• Flexible products to manage specific segments, e.g. unemployed, CHF loans, etc.

Focus area for next year

Retail0.8 0.7

FY2015 9M2016

90+DPD (€ bn) NPE (€ bn)

2.0 1.8

FY2015 9M2016

5.3 4.9

FY2015 9M2016

Deleverage of €0,7 bn

20

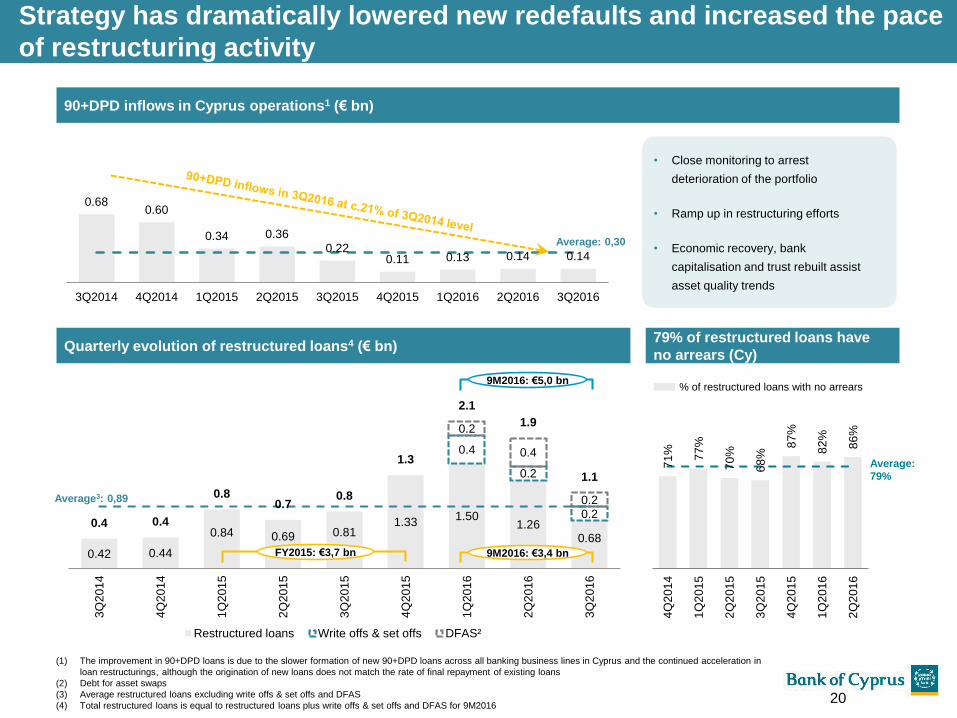

Strategy has dramatically lowered new redefaults and increased the pace

of restructuring activity

90+DPD inflows in Cyprus operations1 (€ bn)

• Close monitoring to arrest

deterioration of the portfolio

• Ramp up in restructuring efforts

• Economic recovery, bank

capitalisation and trust rebuilt assist

asset quality trends

79% of restructured loans have

no arrears (Cy)

0.680.60

0.34 0.36

0.220.11 0.13 0.14 0.14

3Q2014 4Q2014 1Q2015 2Q2015 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016

Average: 0,30

0.42 0.44

0.84 0.69 0.811.33

1.501.26

0.68

0.4

0.2

0.2

0.2

0.4

0.2

0.4 0.4

0.80.7

0.8

1.3

2.1

1.9

1.1

3Q

201

4

4Q

201

4

1Q

201

5

2Q

201

5

3Q

201

5

4Q

201

5

1Q

201

6

2Q

201

6

3Q

201

6

Restructured loans Write offs & set offs DFAS²

71

%

77

%

70

%

68

%

87

%

82

%

86

%

4Q

201

4

1Q

201

5

2Q

201

5

3Q

201

5

4Q

201

5

1Q

201

6

2Q

201

6

Average:

79%

% of restructured loans with no arrears

(1) The improvement in 90+DPD loans is due to the slower formation of new 90+DPD loans across all banking business lines in Cyprus and the continued acceleration in

loan restructurings, although the origination of new loans does not match the rate of final repayment of existing loans

(2) Debt for asset swaps

(3) Average restructured loans excluding write offs & set offs and DFAS

(4) Total restructured loans is equal to restructured loans plus write offs & set offs and DFAS for 9M2016

Quarterly evolution of restructured loans4 (€ bn)

Average3: 0,89

FY2015: €3,7 bn 9M2016: €3,4 bn

9M2016: €5,0 bn

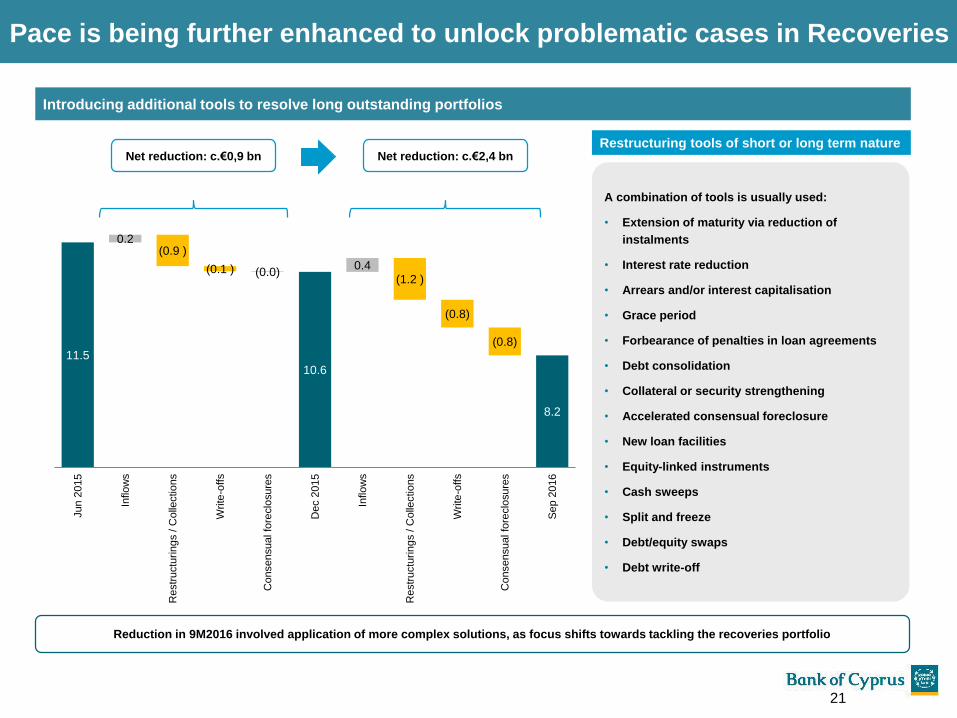

Pace is being further enhanced to unlock problematic cases in Recoveries

Introducing additional tools to resolve long outstanding portfolios

Reduction in 9M2016 involved application of more complex solutions, as focus shifts towards tackling the recoveries portfolio

A combination of tools is usually used:

• Extension of maturity via reduction of

instalments

• Interest rate reduction

• Arrears and/or interest capitalisation

• Grace period

• Forbearance of penalties in loan agreements

• Debt consolidation

• Collateral or security strengthening

• Accelerated consensual foreclosure

• New loan facilities

• Equity-linked instruments

• Cash sweeps

• Split and freeze

• Debt/equity swaps

• Debt write-off

Restructuring tools of short or long term nature

11.5

10.6 10.6

8.2

0.2 (0.9 )

(0.1 ) (0.0) 0.4

(1.2 )

(0.8)

(0.8)

Jun

2015

Inflo

ws

Restr

uctu

ring

s / C

olle

ctio

ns

Write

-offs

Consensual fo

reclo

sure

s

Dec 2

015

Inflo

ws

Restr

uctu

ring

s / C

olle

ctio

ns

Write

-offs

Consensual fo

reclo

sure

s

Se

p 2

016

Net reduction: c.€0,9 bn Net reduction: c.€2,4 bn

21

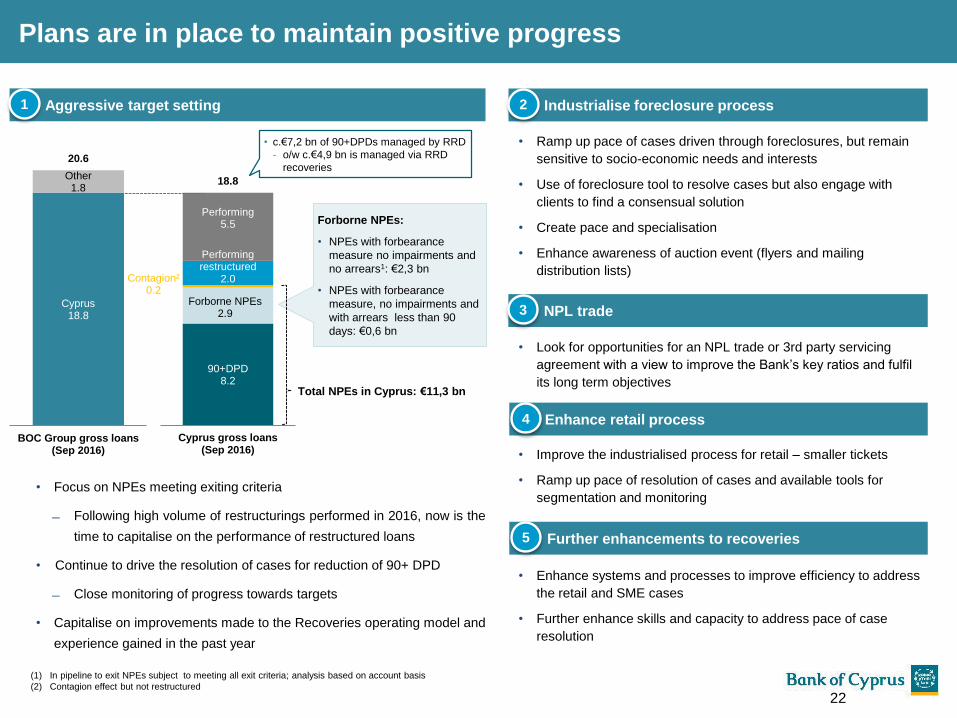

Aggressive target setting

Cyprus18.8

Other1.8

20.6

BOC Group gross loans(Sep 2016)

90+DPD8.2

Forborne NPEs2.9

Contagion²0.2

Performing restructured

2.0

Performing5.5

18.8

Cyprus gross loans(Sep 2016)

Total NPEs in Cyprus: €11,3 bn

• c.€7,2 bn of 90+DPDs managed by RRD

- o/w c.€4,9 bn is managed via RRD

recoveries

Forborne NPEs:

• NPEs with forbearance

measure no impairments and

no arrears1: €2,3 bn

• NPEs with forbearance

measure, no impairments and

with arrears less than 90

days: €0,6 bn

• Focus on NPEs meeting exiting criteria

Following high volume of restructurings performed in 2016, now is the

time to capitalise on the performance of restructured loans

• Continue to drive the resolution of cases for reduction of 90+ DPD

Close monitoring of progress towards targets

• Capitalise on improvements made to the Recoveries operating model and

experience gained in the past year

Industrialise foreclosure process

• Ramp up pace of cases driven through foreclosures, but remain

sensitive to socio-economic needs and interests

• Use of foreclosure tool to resolve cases but also engage with

clients to find a consensual solution

• Create pace and specialisation

• Enhance awareness of auction event (flyers and mailing

distribution lists)

1 2

NPL trade3

Enhance retail process4

• Look for opportunities for an NPL trade or 3rd party servicing

agreement with a view to improve the Bank’s key ratios and fulfil

its long term objectives

• Improve the industrialised process for retail – smaller tickets

• Ramp up pace of resolution of cases and available tools for

segmentation and monitoring

Plans are in place to maintain positive progress

(1) In pipeline to exit NPEs subject to meeting all exit criteria; analysis based on account basis

(2) Contagion effect but not restructured

Further enhancements to recoveries5

• Enhance systems and processes to improve efficiency to address

the retail and SME cases

• Further enhance skills and capacity to address pace of case

resolution

22

85.0%

12.3%

2.7%

Cyprus Greece Others

707250

86

66

196

Land & plots Commercial buildings³ Residential buildings Hotels Other⁴

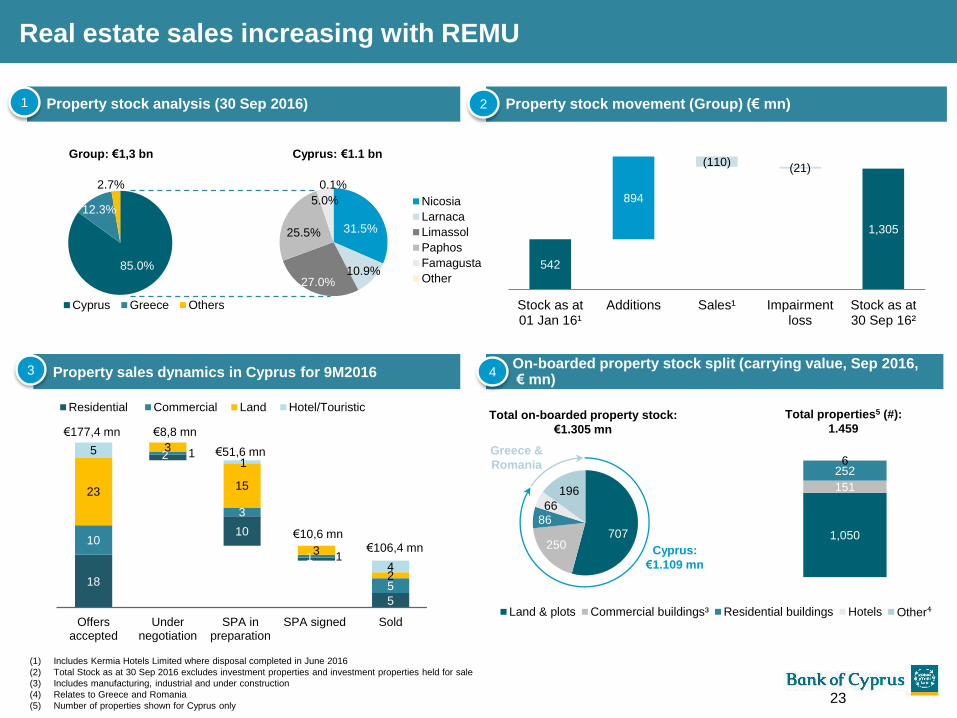

Real estate sales increasing with REMU

(1) Includes Kermia Hotels Limited where disposal completed in June 2016

(2) Total Stock as at 30 Sep 2016 excludes investment properties and investment properties held for sale

(3) Includes manufacturing, industrial and under construction

(4) Relates to Greece and Romania

(5) Number of properties shown for Cyprus only

Cyprus: €1.1 bn

Property stock analysis (30 Sep 2016)

Group: €1,3 bn

31.5%

10.9% 27.0%

25.5%

5.0%

0.1%

Nicosia

Larnaca

Limassol

Paphos

Famagusta

Other

On-boarded property stock split (carrying value, Sep 2016,€ mn)

Cyprus:

€1.109 mn

Total properties5 (#):

1.459

Greece &

Romania

Property sales dynamics in Cyprus for 9M2016

18

2

10

1

5

10

1

3

1

5

23

3

15

3

2

51

4

Offersaccepted

Undernegotiation

SPA inpreparation

SPA signed Sold

Residential Commercial Land Hotel/Touristic

€106,4 mn€10,6 mn

€8,8 mn€177,4 mn

€51,6 mn

Property stock movement (Group) (€ mn)

542

1,305

894

(110)(21)

Stock as at01 Jan 16¹

Additions Sales¹ Impairmentloss

Stock as at30 Sep 16²

1 2

43

Total on-boarded property stock:

€1.305 mn

1,050

151

252 6

23

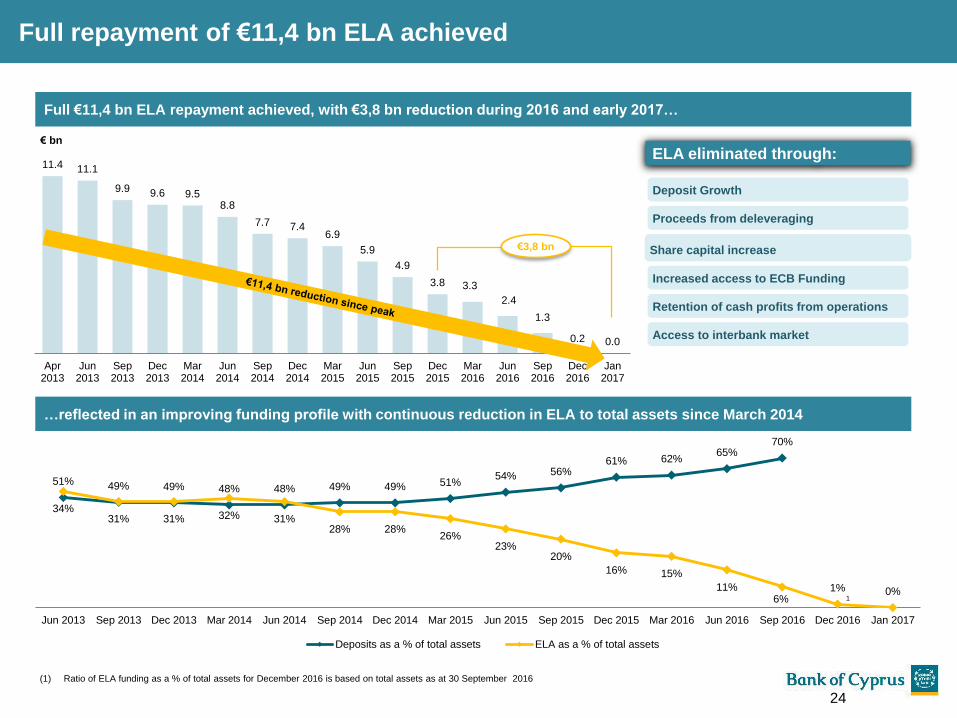

Full repayment of €11,4 bn ELA achieved

(1) Ratio of ELA funding as a % of total assets for December 2016 is based on total assets as at 30 September 2016

Full €11,4 bn ELA repayment achieved, with €3,8 bn reduction during 2016 and early 2017…

11.4 11.1

9.9 9.6 9.58.8

7.7 7.46.9

5.9

4.9

3.8 3.3

2.4

1.3

0.2 0.0

Apr2013

Jun2013

Sep2013

Dec2013

Mar2014

Jun2014

Sep2014

Dec2014

Mar2015

Jun2015

Sep2015

Dec2015

Mar2016

Jun2016

Sep2016

Dec2016

Jan2017

€ bn

1

…reflected in an improving funding profile with continuous reduction in ELA to total assets since March 2014

€3,8 bn

51% 49% 49% 48% 48% 49% 49% 51%54% 56%

61% 62%65%

70%

34%31% 31% 32% 31%

28% 28%26%

23%20%

16% 15%

11%6%

1% 0%

Jun 2013 Sep 2013 Dec 2013 Mar 2014 Jun 2014 Sep 2014 Dec 2014 Mar 2015 Jun 2015 Sep 2015 Dec 2015 Mar 2016 Jun 2016 Sep 2016 Dec 2016 Jan 2017

Deposits as a % of total assets ELA as a % of total assets

Deposit Growth

Proceeds from deleveraging

Share capital increase

Increased access to ECB Funding

Retention of cash profits from operations

Access to interbank market

ELA eliminated through:

24

148% 141% 138% 136% 132%

121% 119% 110%

102%

124% 125% 125% 123%

121% 122%

121%

Sep 14 Dec 14 Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16

Loans to deposits EU average Loans to deposits ratio

Improved by 19 p.p2 since Dec 15

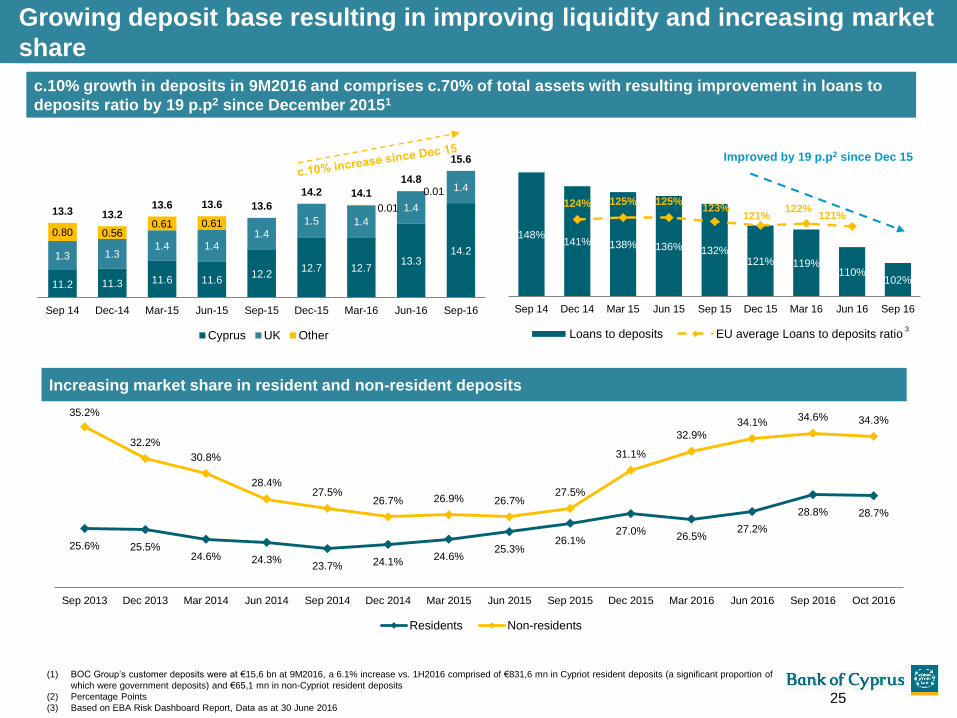

Growing deposit base resulting in improving liquidity and increasing market

share

Increasing market share in resident and non-resident deposits

(1) BOC Group’s customer deposits were at €15,6 bn at 9M2016, a 6.1% increase vs. 1H2016 comprised of €831,6 mn in Cypriot resident deposits (a significant proportion of

which were government deposits) and €65,1 mn in non-Cypriot resident deposits

(2) Percentage Points

(3) Based on EBA Risk Dashboard Report, Data as at 30 June 2016

c.10% growth in deposits in 9M2016 and comprises c.70% of total assets with resulting improvement in loans to

deposits ratio by 19 p.p2 since December 20151

11.2 11.3 11.6 11.612.2

12.7 12.713.3

14.21.3 1.31.4 1.4

1.4

1.5 1.4

1.4

1.4

0.80 0.560.61 0.61

0.01

0.01

13.3 13.213.6 13.6 13.6

14.2 14.1

14.8

15.6

Sep 14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Cyprus UK Other

25.6% 25.5% 24.6% 24.3%

23.7% 24.1% 24.6%

25.3% 26.1%

27.0% 26.5%

27.2%

28.8% 28.7%

35.2%

32.2%

30.8%

28.4% 27.5%

26.7% 26.9% 26.7% 27.5%

31.1%

32.9%

34.1% 34.6% 34.3%

Sep 2013 Dec 2013 Mar 2014 Jun 2014 Sep 2014 Dec 2014 Mar 2015 Jun 2015 Sep 2015 Dec 2015 Mar 2016 Jun 2016 Sep 2016 Oct 2016

Residents Non-residents

3

25

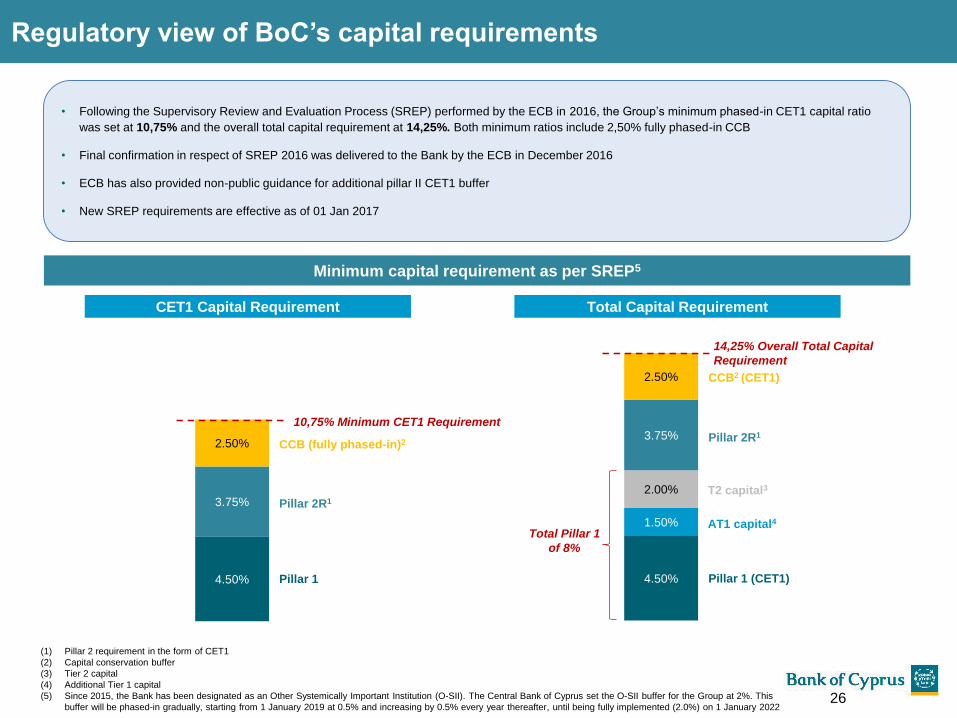

4.50%

1.50%

2.00%

3.75%

2.50%

14,25% Overall Total Capital

Requirement

CCB2 (CET1)

4.50%

3.75%

2.50%

26

Regulatory view of BoC’s capital requirements

Minimum capital requirement as per SREP5

CET1 Capital Requirement Total Capital Requirement

Pillar 1

Pillar 2R1

CCB (fully phased-in)2

(1) Pillar 2 requirement in the form of CET1

(2) Capital conservation buffer

(3) Tier 2 capital

(4) Additional Tier 1 capital

(5) Since 2015, the Bank has been designated as an Other Systemically Important Institution (O-SII). The Central Bank of Cyprus set the O-SII buffer for the Group at 2%. This

buffer will be phased-in gradually, starting from 1 January 2019 at 0.5% and increasing by 0.5% every year thereafter, until being fully implemented (2.0%) on 1 January 2022

10,75% Minimum CET1 Requirement

Pillar 2R1

Pillar 1 (CET1)

AT1 capital4

T2 capital3

Total Pillar 1

of 8%

• Following the Supervisory Review and Evaluation Process (SREP) performed by the ECB in 2016, the Group’s minimum phased-in CET1 capital ratio

was set at 10,75% and the overall total capital requirement at 14,25%. Both minimum ratios include 2,50% fully phased-in CCB

• Final confirmation in respect of SREP 2016 was delivered to the Bank by the ECB in December 2016

• ECB has also provided non-public guidance for additional pillar II CET1 buffer

• New SREP requirements are effective as of 01 Jan 2017

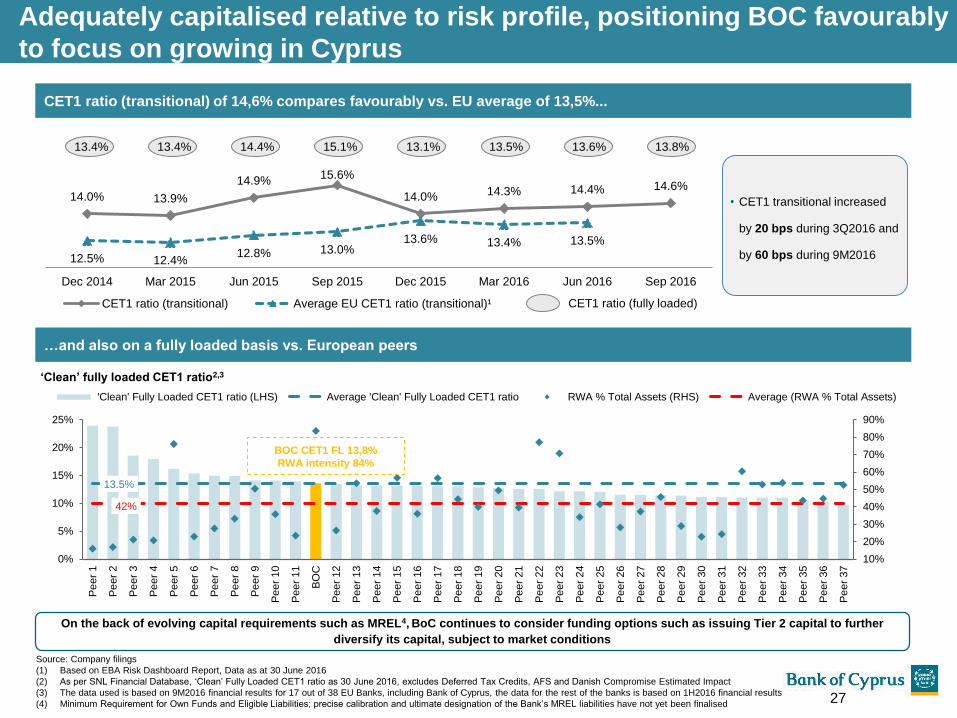

13.4% 13.4% 14.4% 15.1% 13.1% 13.5% 13.6% 13.8%

Adequately capitalised relative to risk profile, positioning BOC favourably

to focus on growing in Cyprus

Source: Company filings

(1) Based on EBA Risk Dashboard Report, Data as at 30 June 2016

(2) As per SNL Financial Database, ‘Clean’ Fully Loaded CET1 ratio as 30 June 2016, excludes Deferred Tax Credits, AFS and Danish Compromise Estimated Impact

(3) The data used is based on 9M2016 financial results for 17 out of 38 EU Banks, including Bank of Cyprus, the data for the rest of the banks is based on 1H2016 financial results

(4) Minimum Requirement for Own Funds and Eligible Liabilities; precise calibration and ultimate designation of the Bank’s MREL liabilities have not yet been finalised

14.0% 13.9%

14.9% 15.6%

14.0% 14.3% 14.4% 14.6%

12.5% 12.4% 12.8% 13.0%

13.6% 13.4% 13.5%

Dec 2014 Mar 2015 Jun 2015 Sep 2015 Dec 2015 Mar 2016 Jun 2016 Sep 2016

CET1 ratio (transitional) Average EU CET1 ratio (transitional)¹

CET1 ratio (transitional) of 14,6% compares favourably vs. EU average of 13,5%...

CET1 ratio (fully loaded)

…and also on a fully loaded basis vs. European peers

‘Clean’ fully loaded CET1 ratio2,3

On the back of evolving capital requirements such as MREL4, BoC continues to consider funding options such as issuing Tier 2 capital to further

diversify its capital, subject to market conditions

• CET1 transitional increased

by 20 bps during 3Q2016 and

by 60 bps during 9M2016

13.5%

42%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0%

5%

10%

15%

20%

25%

Pe

er

1

Pe

er

2

Pe

er

3

Pe

er

4

Pe

er

5

Pe

er

6

Pe

er

7

Pe

er

8

Pe

er

9

Pe

er

10

Pe

er

11

BO

C

Pe

er

12

Pe

er

13

Pe

er

14

Pe

er

15

Pe

er

16

Pe

er

17

Pe

er

18

Pe

er

19

Pe

er

20

Pe

er

21

Pe

er

22

Pe

er

23

Pe

er

24

Pe

er

25

Pe

er

26

Pe

er

27

Pe

er

28

Pe

er

29

Pe

er

30

Pe

er

31

Pe

er

32

Pe

er

33

Pe

er

34

Pe

er

35

Pe

er

36

Pe

er

37

'Clean' Fully Loaded CET1 ratio (LHS) Average 'Clean' Fully Loaded CET1 ratio RWA % Total Assets (RHS) Average (RWA % Total Assets)

BOC CET1 FL 13,8%

RWA intensity 84%

27

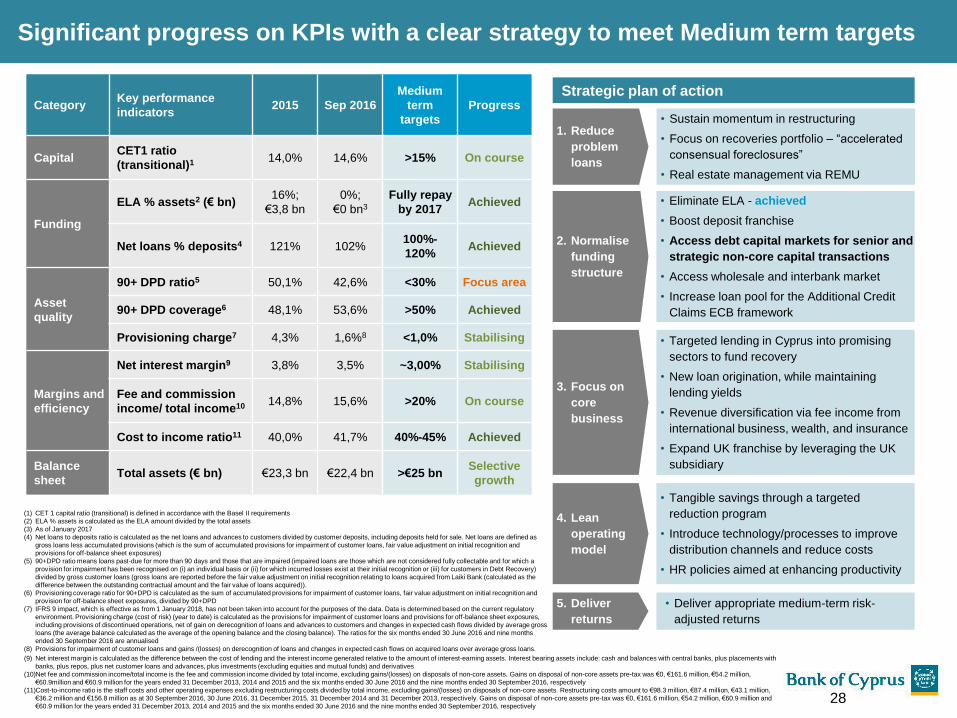

Significant progress on KPIs with a clear strategy to meet Medium term targets

(1) CET 1 capital ratio (transitional) is defined in accordance with the Basel II requirements

(2) ELA % assets is calculated as the ELA amount divided by the total assets

(3) As of January 2017

(4) Net loans to deposits ratio is calculated as the net loans and advances to customers divided by customer deposits, including deposits held for sale. Net loans are defined as

gross loans less accumulated provisions (which is the sum of accumulated provisions for impairment of customer loans, fair value adjustment on initial recognition and

provisions for off-balance sheet exposures)

(5) 90+DPD ratio means loans past-due for more than 90 days and those that are impaired (impaired loans are those which are not considered fully collectable and for which a

provision for impairment has been recognised on (i) an individual basis or (ii) for which incurred losses exist at their initial recognition or (iii) for customers in Debt Recovery)

divided by gross customer loans (gross loans are reported before the fair value adjustment on initial recognition relating to loans acquired from Laiki Bank (calculated as the

difference between the outstanding contractual amount and the fair value of loans acquired)).

(6) Provisioning coverage ratio for 90+DPD is calculated as the sum of accumulated provisions for impairment of customer loans, fair value adjustment on initial recognition and

provision for off-balance sheet exposures, divided by 90+DPD

(7) IFRS 9 impact, which is effective as from 1 January 2018, has not been taken into account for the purposes of the data. Data is determined based on the current regulatory

environment. Provisioning charge (cost of risk) (year to date) is calculated as the provisions for impairment of customer loans and provisions for off-balance sheet exposures,

including provisions of discontinued operations, net of gain on derecognition of loans and advances to customers and changes in expected cash flows divided by average gross

loans (the average balance calculated as the average of the opening balance and the closing balance). The ratios for the six months ended 30 June 2016 and nine months

ended 30 September 2016 are annualised

(8) Provisions for impairment of customer loans and gains /(losses) on derecognition of loans and changes in expected cash flows on acquired loans over average gross loans.

CategoryKey performance

indicators2015 Sep 2016

Medium

term

targets

Progress

CapitalCET1 ratio

(transitional)1 14,0% 14,6% >15% On course

Funding

ELA % assets2 (€ bn)16%;

€3,8 bn

0%;

€0 bn3

Fully repay

by 2017Achieved

Net loans % deposits4 121% 102%100%-

120%Achieved

Asset

quality

90+ DPD ratio5 50,1% 42,6% <30% Focus area

90+ DPD coverage6 48,1% 53,6% >50% Achieved

Provisioning charge7 4,3% 1,6%8 <1,0% Stabilising

Margins and

efficiency

Net interest margin9 3,8% 3,5% ~3,00% Stabilising

Fee and commission

income/ total income10 14,8% 15,6% >20% On course

Cost to income ratio11 40,0% 41,7% 40%-45% Achieved

Balance

sheetTotal assets (€ bn) €23,3 bn €22,4 bn >€25 bn

Selective

growth

Strategic plan of action

• Sustain momentum in restructuring

• Focus on recoveries portfolio – “accelerated

consensual foreclosures”

• Real estate management via REMU

1. Reduce

problem

loans

• Eliminate ELA - achieved

• Boost deposit franchise

• Access debt capital markets for senior and

strategic non-core capital transactions

• Access wholesale and interbank market

• Increase loan pool for the Additional Credit

Claims ECB framework

2. Normalise

funding

structure

• Targeted lending in Cyprus into promising

sectors to fund recovery

• New loan origination, while maintaining

lending yields

• Revenue diversification via fee income from

international business, wealth, and insurance

• Expand UK franchise by leveraging the UK

subsidiary

3. Focus on

core

business

• Tangible savings through a targeted

reduction program

• Introduce technology/processes to improve

distribution channels and reduce costs

• HR policies aimed at enhancing productivity

4. Lean

operating

model

• Deliver appropriate medium-term risk-

adjusted returns

5. Deliver

returns

(9) Net interest margin is calculated as the difference between the cost of lending and the interest income generated relative to the amount of interest-earning assets. Interest bearing assets include: cash and balances with central banks, plus placements with

banks, plus repos, plus net customer loans and advances, plus investments (excluding equities and mutual funds) and derivatives

(10)Net fee and commission income/total income is the fee and commission income divided by total income, excluding gains/(losses) on disposals of non-core assets. Gains on disposal of non-core assets pre-tax was €0, €161.6 million, €54.2 million,

€60.9million and €60.9 million for the years ended 31 December 2013, 2014 and 2015 and the six months ended 30 June 2016 and the nine months ended 30 September 2016, respectively

(11)Cost-to-income ratio is the staff costs and other operating expenses excluding restructuring costs divided by total income, excluding gains/(losses) on disposals of non-core assets. Restructuring costs amount to €98.3 million, €87.4 million, €43.1 million,

€36.2 million and €156.8 million as at 30 September 2016, 30 June 2016, 31 December 2015, 31 December 2014 and 31 December 2013, respectively. Gains on disposal of non-core assets pre-tax was €0, €161.6 million, €54.2 million, €60.9 million and

€60.9 million for the years ended 31 December 2013, 2014 and 2015 and the six months ended 30 June 2016 and the nine months ended 30 September 2016, respectively28

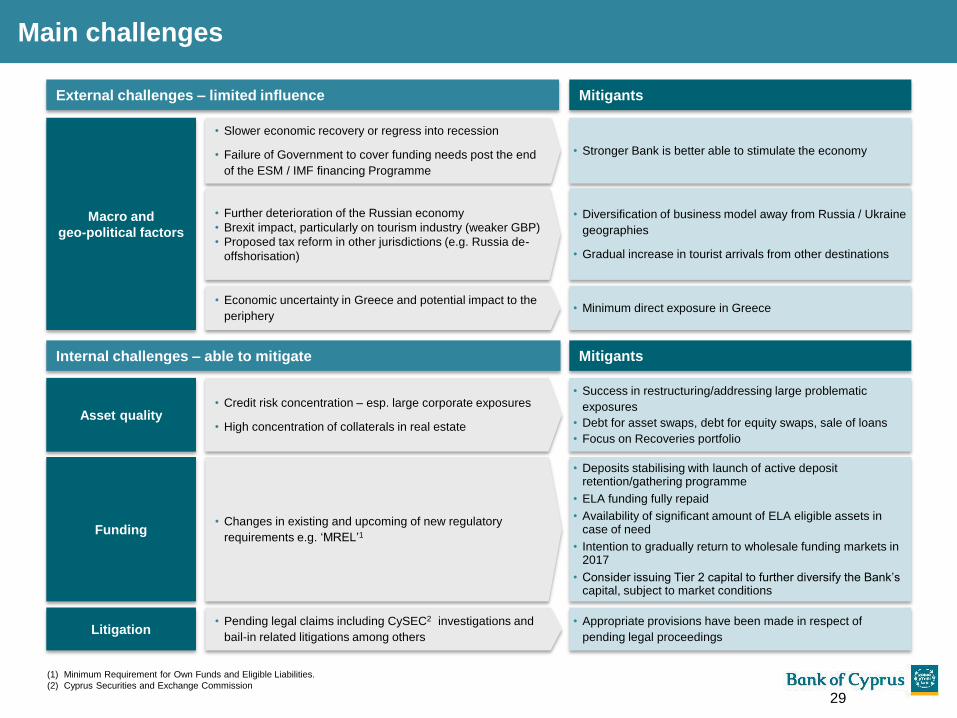

Macro and

geo-political factors

• Slower economic recovery or regress into recession

• Failure of Government to cover funding needs post the end

of the ESM / IMF financing Programme

Asset quality• Credit risk concentration – esp. large corporate exposures

• High concentration of collaterals in real estate

• Success in restructuring/addressing large problematic

exposures

• Debt for asset swaps, debt for equity swaps, sale of loans

• Focus on Recoveries portfolio

Funding

External challenges – limited influence

• Further deterioration of the Russian economy

• Brexit impact, particularly on tourism industry (weaker GBP)

• Proposed tax reform in other jurisdictions (e.g. Russia de-

offshorisation)

Internal challenges – able to mitigate Mitigants

• Changes in existing and upcoming of new regulatory

requirements e.g. ‘MREL’1

• Deposits stabilising with launch of active deposit retention/gathering programme

• ELA funding fully repaid

• Availability of significant amount of ELA eligible assets in case of need

• Intention to gradually return to wholesale funding markets in 2017

• Consider issuing Tier 2 capital to further diversify the Bank’s capital, subject to market conditions

Litigation• Pending legal claims including CySEC2 investigations and

bail-in related litigations among others

• Appropriate provisions have been made in respect of

pending legal proceedings

• Diversification of business model away from Russia / Ukraine

geographies

• Gradual increase in tourist arrivals from other destinations

Mitigants

• Stronger Bank is better able to stimulate the economy

• Economic uncertainty in Greece and potential impact to the

periphery • Minimum direct exposure in Greece

Main challenges

(1) Minimum Requirement for Own Funds and Eligible Liabilities.

(2) Cyprus Securities and Exchange Commission

29

Appendices

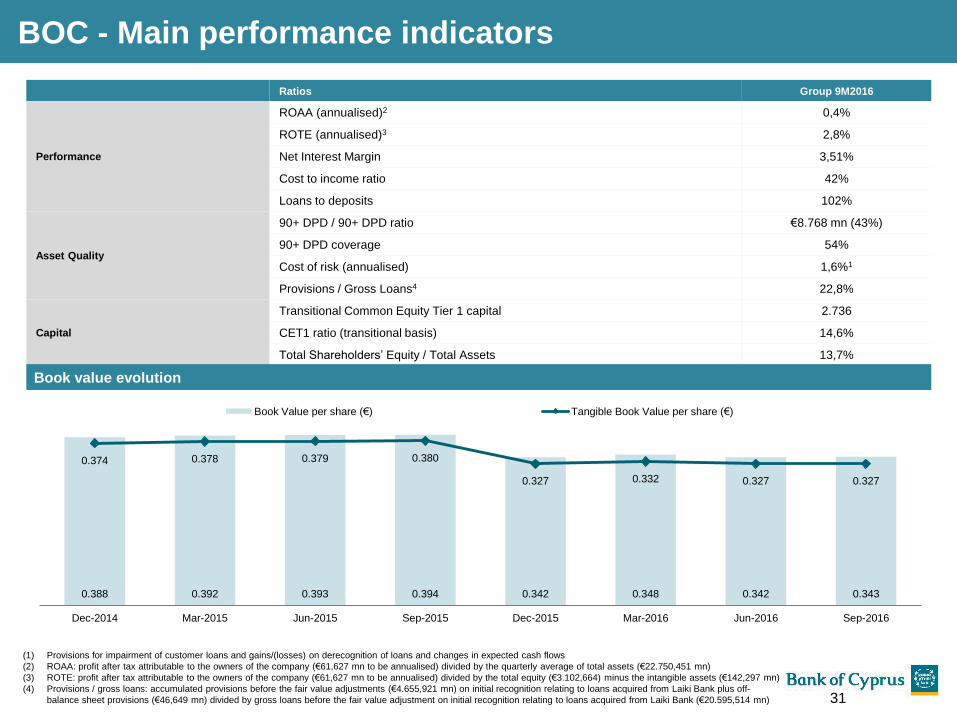

BOC - Main performance indicators

Ratios Group 9M2016

Performance

ROAA (annualised)2 0,4%

ROTE (annualised)3 2,8%

Net Interest Margin 3,51%

Cost to income ratio 42%

Loans to deposits 102%

Asset Quality

90+ DPD / 90+ DPD ratio €8.768 mn (43%)

90+ DPD coverage 54%

Cost of risk (annualised) 1,6%1

Provisions / Gross Loans4 22,8%

Capital

Transitional Common Equity Tier 1 capital 2.736

CET1 ratio (transitional basis) 14,6%

Total Shareholders’ Equity / Total Assets 13,7%

(1) Provisions for impairment of customer loans and gains/(losses) on derecognition of loans and changes in expected cash flows

(2) ROAA: profit after tax attributable to the owners of the company (€61,627 mn to be annualised) divided by the quarterly average of total assets (€22.750,451 mn)

(3) ROTE: profit after tax attributable to the owners of the company (€61,627 mn to be annualised) divided by the total equity (€3.102,664) minus the intangible assets (€142,297 mn)

(4) Provisions / gross loans: accumulated provisions before the fair value adjustments (€4.655,921 mn) on initial recognition relating to loans acquired from Laiki Bank plus off-

balance sheet provisions (€46,649 mn) divided by gross loans before the fair value adjustment on initial recognition relating to loans acquired from Laiki Bank (€20.595,514 mn)

0.388 0.392 0.393 0.394 0.342 0.348 0.342 0.343

0.374 0.378 0.379 0.380

0.327 0.332 0.327 0.327

Dec-2014 Mar-2015 Jun-2015 Sep-2015 Dec-2015 Mar-2016 Jun-2016 Sep-2016

Book Value per share (€) Tangible Book Value per share (€)

Book value evolution

31

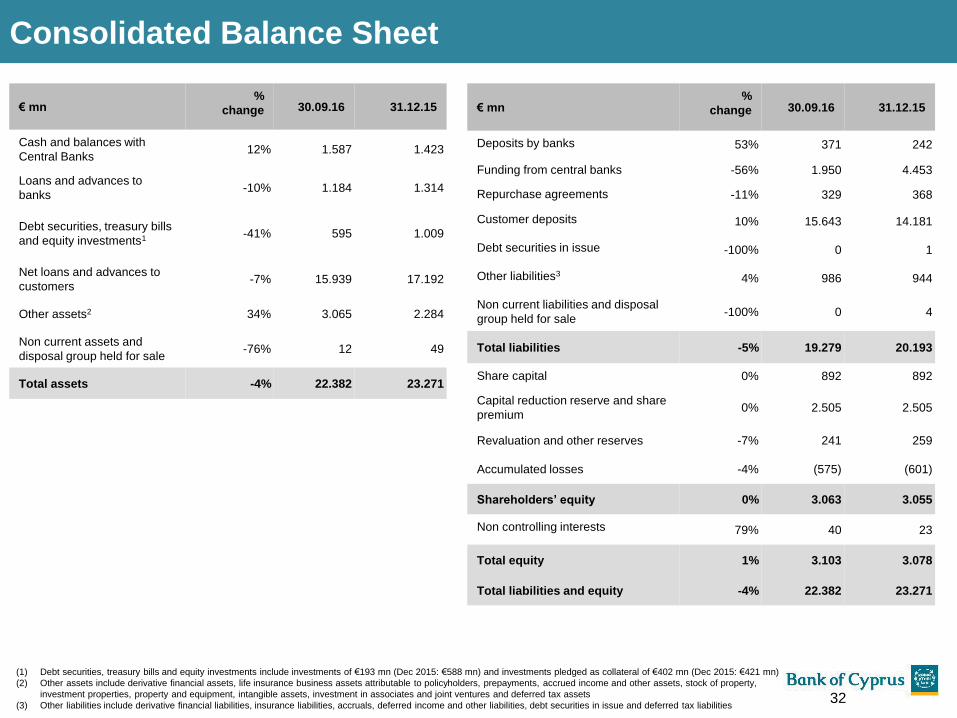

€ mn%

change 30.09.16 31.12.15

Cash and balances with

Central Banks12% 1.587 1.423

Loans and advances to

banks-10% 1.184 1.314

Debt securities, treasury bills

and equity investments1 -41% 595 1.009

Net loans and advances to

customers-7% 15.939 17.192

Other assets2 34% 3.065 2.284

Non current assets and

disposal group held for sale-76% 12 49

Total assets -4% 22.382 23.271

€ mn%

change 30.09.16 31.12.15

Deposits by banks 53% 371 242

Funding from central banks -56% 1.950 4.453

Repurchase agreements -11% 329 368

Customer deposits 10% 15.643 14.181

Debt securities in issue -100% 0 1

Other liabilities34% 986 944

Non current liabilities and disposal

group held for sale-100% 0 4

Total liabilities -5% 19.279 20.193

Share capital 0% 892 892

Capital reduction reserve and share

premium 0% 2.505 2.505

Revaluation and other reserves -7% 241 259

Accumulated losses -4% (575) (601)

Shareholders’ equity 0% 3.063 3.055

Non controlling interests 79% 40 23

Total equity 1% 3.103 3.078

Total liabilities and equity -4% 22.382 23.271

Consolidated Balance Sheet

(1) Debt securities, treasury bills and equity investments include investments of €193 mn (Dec 2015: €588 mn) and investments pledged as collateral of €402 mn (Dec 2015: €421 mn)

(2) Other assets include derivative financial assets, life insurance business assets attributable to policyholders, prepayments, accrued income and other assets, stock of property,

investment properties, property and equipment, intangible assets, investment in associates and joint ventures and deferred tax assets

(3) Other liabilities include derivative financial liabilities, insurance liabilities, accruals, deferred income and other liabilities, debt securities in issue and deferred tax liabilities32

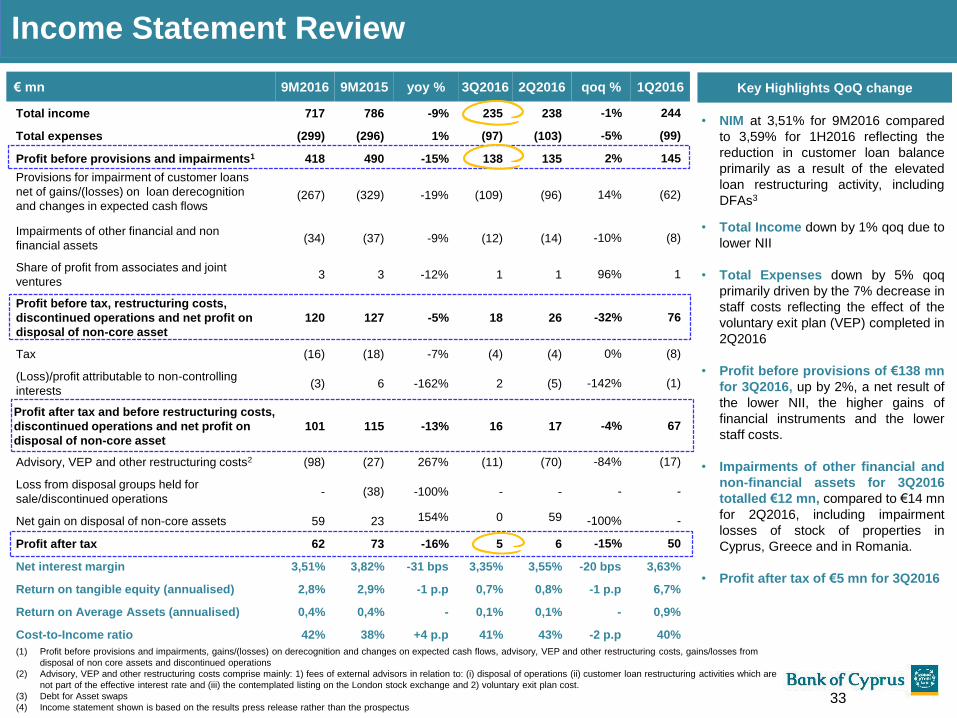

€ mn 9M2016 9M2015 yoy % 3Q2016 2Q2016 qoq % 1Q2016

Total income 717 786 -9% 235 238 -1% 244

Total expenses (299) (296) 1% (97) (103) -5% (99)

Profit before provisions and impairments1 418 490 -15% 138 135 2% 145

Provisions for impairment of customer loans

net of gains/(losses) on loan derecognition

and changes in expected cash flows(267) (329) -19% (109) (96) 14% (62)

Impairments of other financial and non

financial assets(34) (37) -9% (12) (14) -10% (8)

Share of profit from associates and joint

ventures3 3 -12% 1 1 96% 1

Profit before tax, restructuring costs,

discontinued operations and net profit on

disposal of non-core asset

120 127 -5% 18 26 -32% 76

Tax (16) (18) -7% (4) (4) 0% (8)

(Loss)/profit attributable to non-controlling

interests(3) 6 -162% 2 (5) -142% (1)

Profit after tax and before restructuring costs,

discontinued operations and net profit on

disposal of non-core asset

101 115 -13% 16 17 -4% 67

Advisory, VEP and other restructuring costs2 (98) (27) 267% (11) (70) -84% (17)

Loss from disposal groups held for

sale/discontinued operations- (38) -100% - - - -

Net gain on disposal of non-core assets 59 23 154% 0 59 -100% -

Profit after tax 62 73 -16% 5 6 -15% 50

Net interest margin 3,51% 3,82% -31 bps 3,35% 3,55% -20 bps 3,63%

Return on tangible equity (annualised) 2,8% 2,9% -1 p.p 0,7% 0,8% -1 p.p 6,7%

Return on Average Assets (annualised) 0,4% 0,4% - 0,1% 0,1% - 0,9%

Cost-to-Income ratio 42% 38% +4 p.p 41% 43% -2 p.p 40%

Income Statement Review

(1) Profit before provisions and impairments, gains/(losses) on derecognition and changes on expected cash flows, advisory, VEP and other restructuring costs, gains/losses from

disposal of non core assets and discontinued operations

(2) Advisory, VEP and other restructuring costs comprise mainly: 1) fees of external advisors in relation to: (i) disposal of operations (ii) customer loan restructuring activities which are

not part of the effective interest rate and (iii) the contemplated listing on the London stock exchange and 2) voluntary exit plan cost.

(3) Debt for Asset swaps

(4) Income statement shown is based on the results press release rather than the prospectus

Key Highlights QoQ change

• NIM at 3,51% for 9M2016 compared

to 3,59% for 1H2016 reflecting the

reduction in customer loan balance

primarily as a result of the elevated

loan restructuring activity, including

DFAs3

• Total Income down by 1% qoq due to

lower NII

• Total Expenses down by 5% qoq

primarily driven by the 7% decrease in

staff costs reflecting the effect of the

voluntary exit plan (VEP) completed in

2Q2016

• Profit before provisions of €138 mn

for 3Q2016, up by 2%, a net result of

the lower NII, the higher gains of

financial instruments and the lower

staff costs.

• Impairments of other financial and

non-financial assets for 3Q2016

totalled €12 mn, compared to €14 mn

for 2Q2016, including impairment

losses of stock of properties in

Cyprus, Greece and in Romania.

• Profit after tax of €5 mn for 3Q2016

33

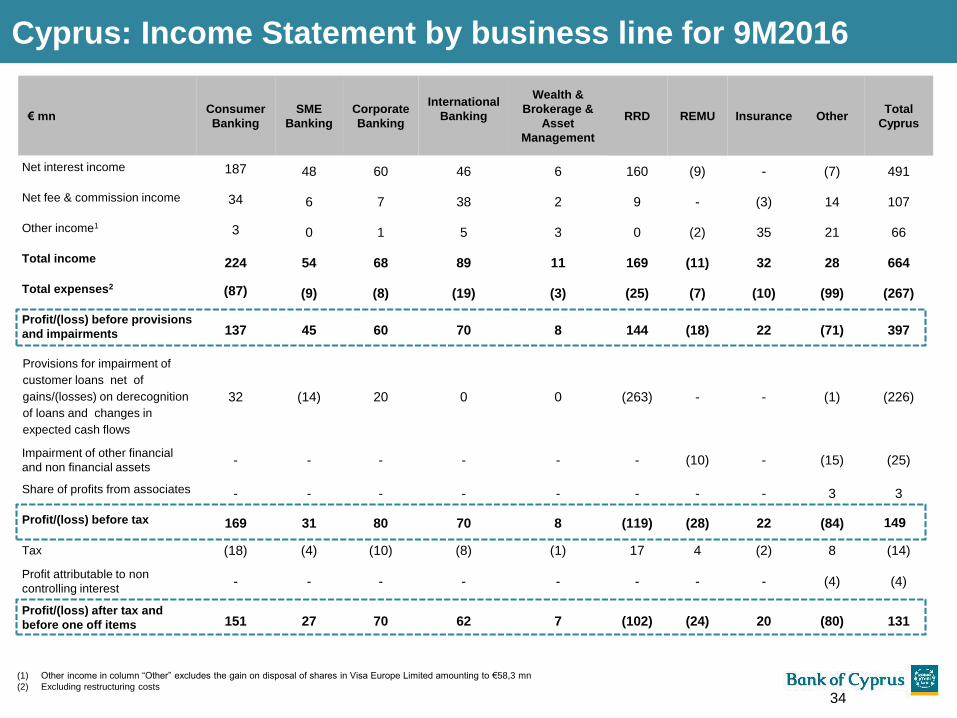

€ mnConsumer

Banking

SME

Banking

Corporate

Banking

International

Banking

Wealth &

Brokerage &

Asset

Management

RRD REMU Insurance OtherTotal

Cyprus

Net interest income 187 48 60 46 6 160 (9) - (7) 491

Net fee & commission income 34 6 7 38 2 9 - (3) 14 107

Other income1 3 0 1 5 3 0 (2) 35 21 66

Total income 224 54 68 89 11 169 (11) 32 28 664

Total expenses2 (87) (9) (8) (19) (3) (25) (7) (10) (99) (267)

Profit/(loss) before provisions

and impairments 137 45 60 70 8 144 (18) 22 (71) 397

Provisions for impairment of

customer loans net of

gains/(losses) on derecognition

of loans and changes in

expected cash flows

32 (14) 20 0 0 (263) - - (1) (226)

Impairment of other financial

and non financial assets- - - - - - (10) - (15) (25)

Share of profits from associates - - - - - - - - 3 3

Profit/(loss) before tax 169 31 80 70 8 (119) (28) 22 (84) 149

Tax (18) (4) (10) (8) (1) 17 4 (2) 8 (14)

Profit attributable to non

controlling interest- - - - - - - - (4) (4)

Profit/(loss) after tax and

before one off items 151 27 70 62 7 (102) (24) 20 (80) 131

Cyprus: Income Statement by business line for 9M2016

(1) Other income in column “Other” excludes the gain on disposal of shares in Visa Europe Limited amounting to €58,3 mn

(2) Excluding restructuring costs

34

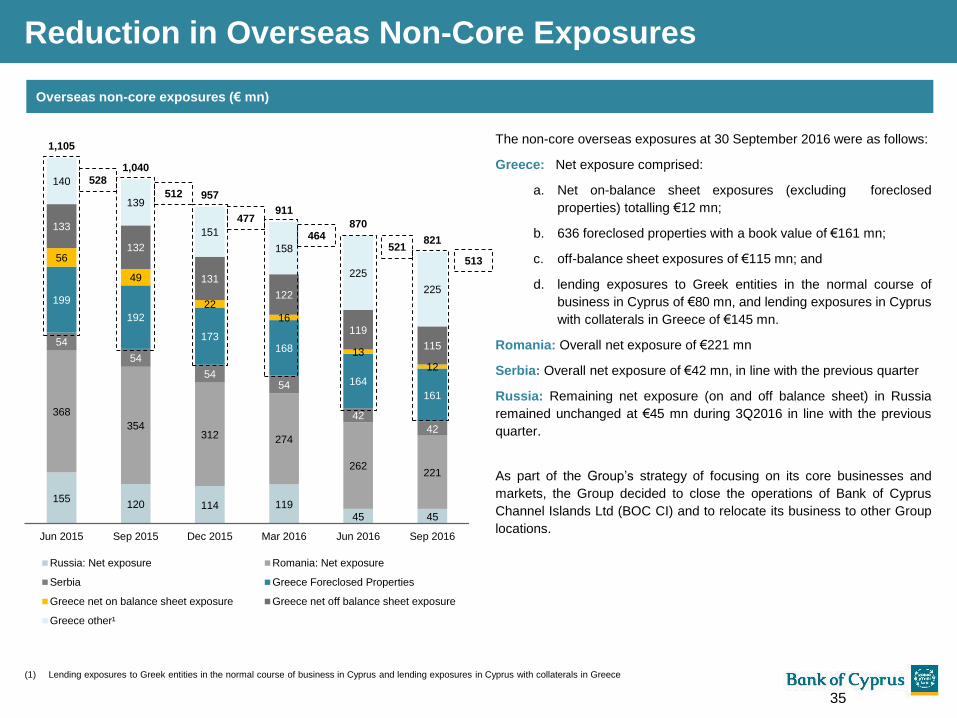

Reduction in Overseas Non-Core Exposures

Overseas non-core exposures (€ mn)

The non-core overseas exposures at 30 September 2016 were as follows:

Greece: Net exposure comprised:

a. Net on-balance sheet exposures (excluding foreclosed

properties) totalling €12 mn;

b. 636 foreclosed properties with a book value of €161 mn;

c. off-balance sheet exposures of €115 mn; and

d. lending exposures to Greek entities in the normal course of

business in Cyprus of €80 mn, and lending exposures in Cyprus

with collaterals in Greece of €145 mn.

Romania: Overall net exposure of €221 mn

Serbia: Overall net exposure of €42 mn, in line with the previous quarter

Russia: Remaining net exposure (on and off balance sheet) in Russia

remained unchanged at €45 mn during 3Q2016 in line with the previous

quarter.

As part of the Group’s strategy of focusing on its core businesses and

markets, the Group decided to close the operations of Bank of Cyprus

Channel Islands Ltd (BOC CI) and to relocate its business to other Group

locations.

(1) Lending exposures to Greek entities in the normal course of business in Cyprus and lending exposures in Cyprus with collaterals in Greece

155120 114 119

45 45

368

354312 274

262221

54

54

5454

42

42

199

192

173168

164

161

56

49

22

16

13

12

133

132

131

122

119

115

140

139

151

158

225

225

1,105

1,040

957

911

870

821

Jun 2015 Sep 2015 Dec 2015 Mar 2016 Jun 2016 Sep 2016

Russia: Net exposure Romania: Net exposure

Serbia Greece Foreclosed Properties

Greece net on balance sheet exposure Greece net off balance sheet exposure

Greece other¹

528

512

477

464521

513

35

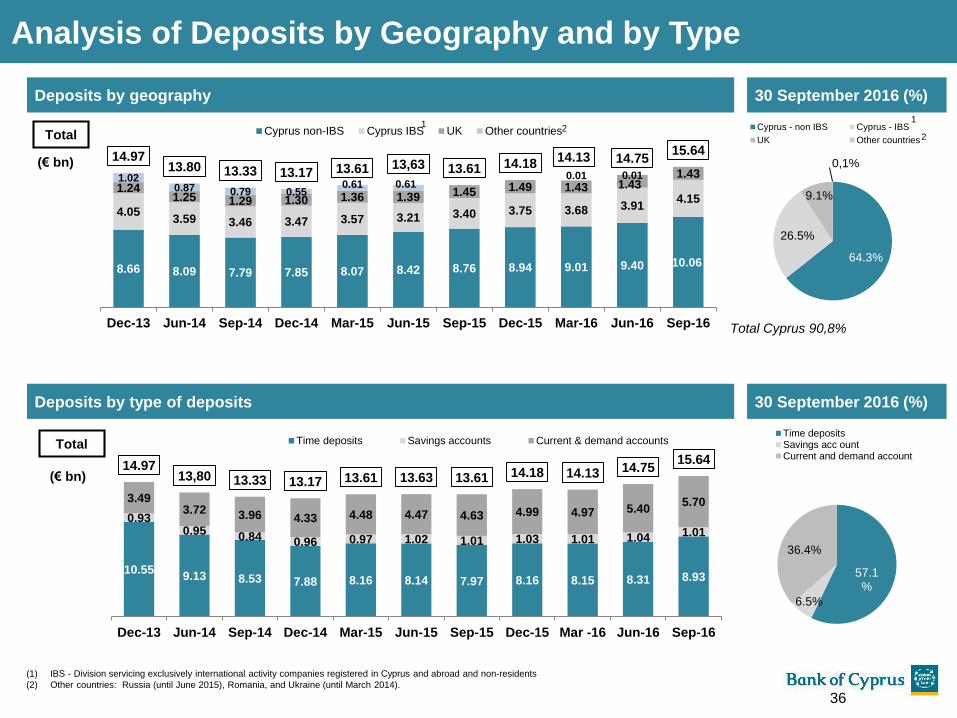

8.66 8.09 7.79 7.85 8.07 8.42 8.76 8.94 9.01 9.40 10.06

4.053.59 3.46 3.47 3.57 3.21 3.40 3.75 3.68 3.91

4.151.24

1.25 1.29 1.30 1.36 1.39 1.45 1.49 1.43 1.431.431.02

0.87 0.79 0.550.61 0.61

0.01 0.01

14.9713.80 13.33 13.17 13.61 13,63 13.61 14.18

14.13 14.7515.64

Dec-13 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Cyprus non-IBS Cyprus IBS UK Other countriesTotal

(€ bn)

(1) IBS - Division servicing exclusively international activity companies registered in Cyprus and abroad and non-residents

(2) Other countries: Russia (until June 2015), Romania, and Ukraine (until March 2014).

Deposits by geography

Analysis of Deposits by Geography and by Type

30 September 2016 (%)

64.3%

26.5%

9.1%

0,1%

Cyprus - non IBS Cyprus - IBS

UK Other countries

Total Cyprus 90,8%

1

2

10.559.13 8.53 7.88 8.16 8.14 7.97 8.16 8.15 8.31 8.93

0.930.95

0.84 0.96 0.97 1.02 1.01 1.03 1.01 1.04 1.01

3.493.72 3.96 4.33 4.48 4.47 4.63 4.99 4.97 5.40

5.70

14.9713,80 13.33 13.17 13.61 13.63 13.61 14.18 14.13 14.75

15.64

Dec-13 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar -16 Jun-16 Sep-16

Time deposits Savings accounts Current & demand accountsTotal

(€ bn)

Deposits by type of deposits 30 September 2016 (%)

57.1%

6.5%

36.4%

Time depositsSavings acc ountCurrent and demand account

12

36

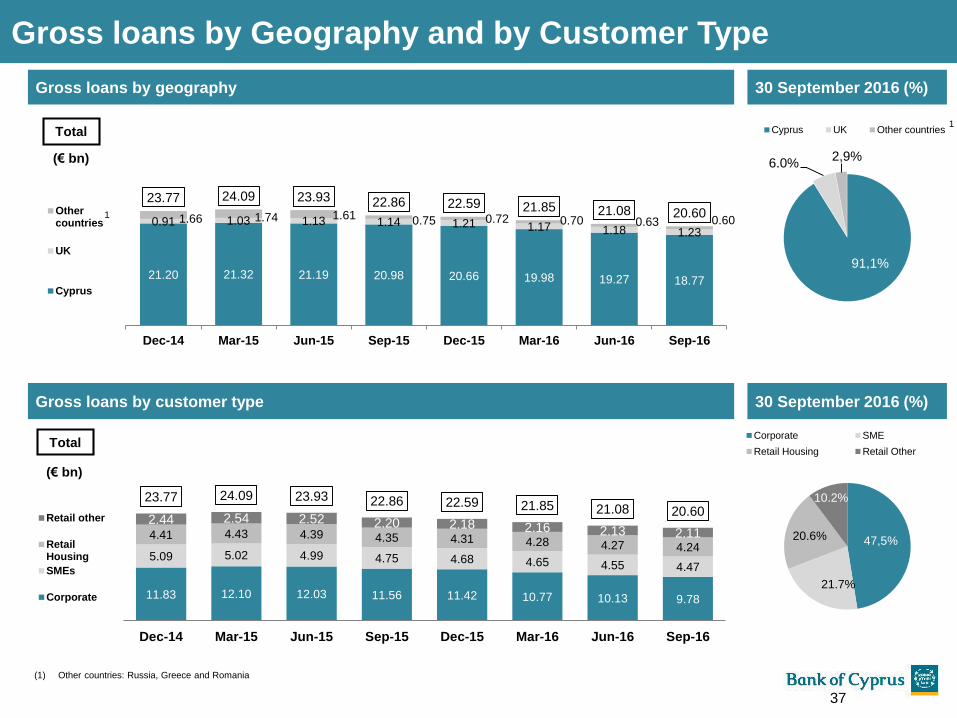

21.20 21.32 21.19 20.98 20.66 19.98 19.27 18.77

0.91 1.03 1.13 1.14 1.21 1.17 1.18 1.231.66 1.74 1.61 0.75 0.72 0.70 0.63 0.60

23.77 24.09 23.93 22.86 22.59 21.85 21.08 20.60

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Othercountries

UK

Cyprus

1

Total

(€ bn)

(1) Other countries: Russia, Greece and Romania

Gross loans by geography

Gross loans by Geography and by Customer Type

91,1%

6.0%2,9%

Cyprus UK Other countries1

11.83 12.10 12.03 11.56 11.42 10.77 10.13 9.78

5.09 5.02 4.99 4.75 4.68 4.65 4.55 4.47

4.41 4.43 4.39 4.35 4.31 4.28 4.27 4.24

2.44 2.54 2.52 2.20 2.18 2.16 2.13 2.11

23.77 24.09 23.93 22.86 22.59 21.85 21.08 20.60

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Retail other

RetailHousing

SMEs

Corporate

(€ bn)

Total

47,5%

21.7%

20.6%

10.2%

Corporate SME

Retail Housing Retail Other

30 September 2016 (%)

30 September 2016 (%)Gross loans by customer type

37

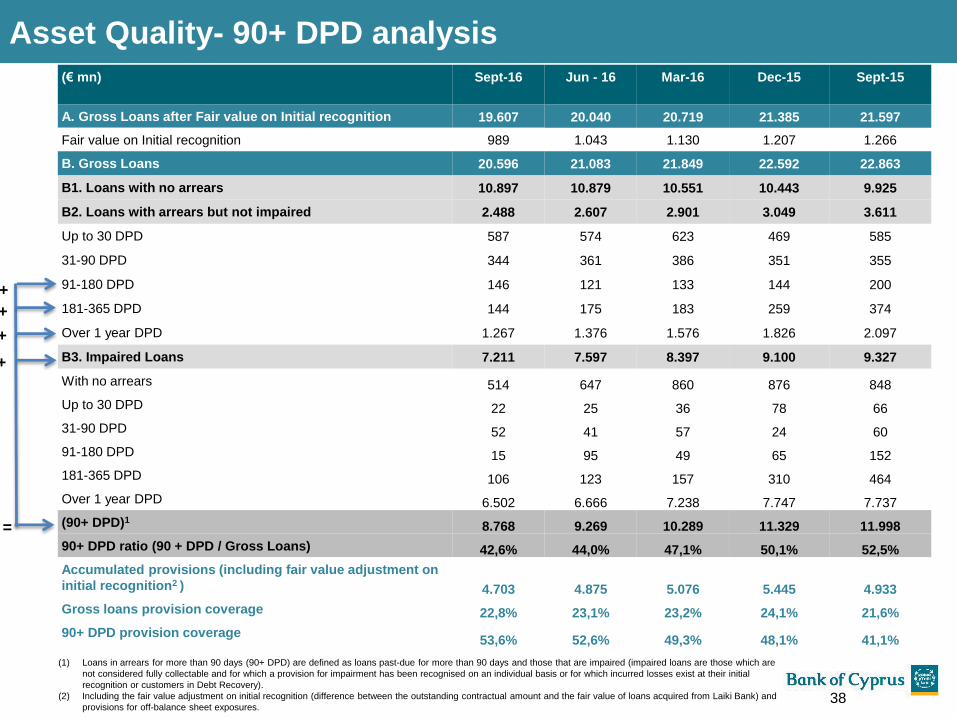

Asset Quality- 90+ DPD analysis

(€ mn) Sept-16 Jun - 16 Mar-16 Dec-15 Sept-15

A. Gross Loans after Fair value on Initial recognition 19.607 20.040 20.719 21.385 21.597

Fair value on Initial recognition 989 1.043 1.130 1.207 1.266

B. Gross Loans 20.596 21.083 21.849 22.592 22.863

B1. Loans with no arrears 10.897 10.879 10.551 10.443 9.925

B2. Loans with arrears but not impaired 2.488 2.607 2.901 3.049 3.611

Up to 30 DPD 587 574 623 469 585

31-90 DPD 344 361 386 351 355

91-180 DPD 146 121 133 144 200

181-365 DPD 144 175 183 259 374

Over 1 year DPD 1.267 1.376 1.576 1.826 2.097

B3. Impaired Loans 7.211 7.597 8.397 9.100 9.327

With no arrears 514 647 860 876 848

Up to 30 DPD 22 25 36 78 66

31-90 DPD 52 41 57 24 60

91-180 DPD 15 95 49 65 152

181-365 DPD 106 123 157 310 464

Over 1 year DPD 6.502 6.666 7.238 7.747 7.737

(90+ DPD)18.768 9.269 10.289 11.329 11.998

90+ DPD ratio (90 + DPD / Gross Loans) 42,6% 44,0% 47,1% 50,1% 52,5%

Accumulated provisions (including fair value adjustment on

initial recognition2 ) 4.703 4.875 5.076 5.445 4.933

Gross loans provision coverage 22,8% 23,1% 23,2% 24,1% 21,6%

90+ DPD provision coverage53,6% 52,6% 49,3% 48,1% 41,1%

(1) Loans in arrears for more than 90 days (90+ DPD) are defined as loans past-due for more than 90 days and those that are impaired (impaired loans are those which are

not considered fully collectable and for which a provision for impairment has been recognised on an individual basis or for which incurred losses exist at their initial

recognition or customers in Debt Recovery).

(2) Including the fair value adjustment on initial recognition (difference between the outstanding contractual amount and the fair value of loans acquired from Laiki Bank) and

provisions for off-balance sheet exposures.

+

+

+

+

=

38

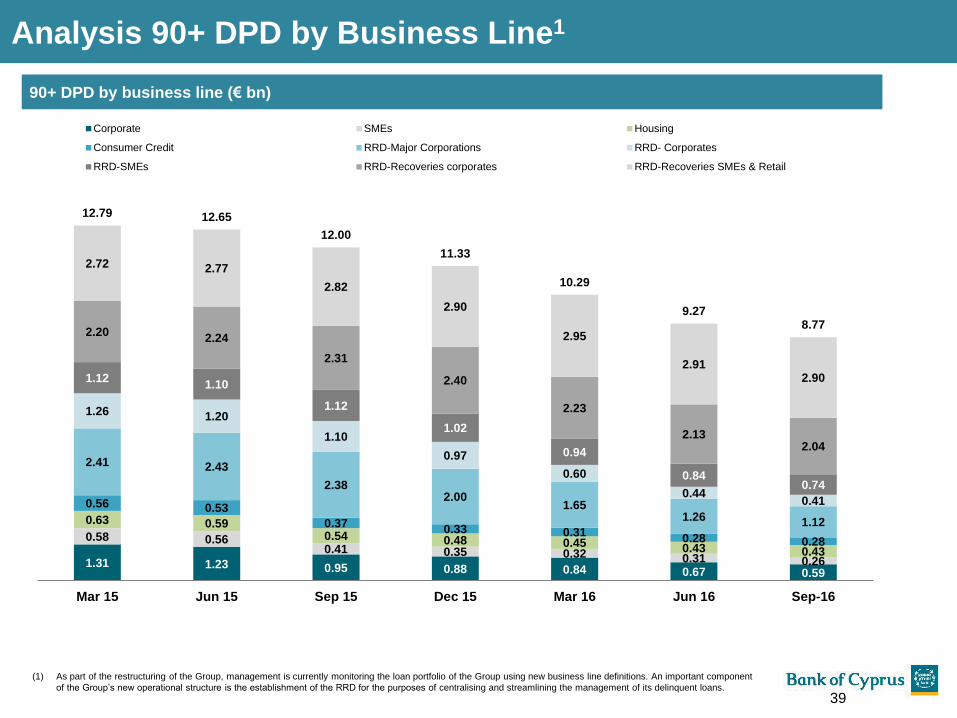

90+ DPD by business line (€ bn)

1.31 1.23 0.95 0.88 0.84 0.67 0.59

0.58 0.560.41 0.35 0.32 0.31 0.26

0.63 0.590.54 0.48 0.45 0.43 0.43

0.56 0.53

0.370.33 0.31

0.28 0.28

2.41 2.43

2.382.00

1.651.26 1.12

1.26 1.20

1.10

0.97

0.60

0.440.41

1.121.10

1.12

1.02

0.94

0.840.74

2.202.24

2.31

2.40

2.23

2.132.04

2.72 2.77

2.82

2.90

2.95

2.912.90

12.79 12.65

12.00

11.33

10.29

9.278.77

Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep-16

Corporate SMEs Housing

Consumer Credit RRD-Major Corporations RRD- Corporates

RRD-SMEs RRD-Recoveries corporates RRD-Recoveries SMEs & Retail

(1) As part of the restructuring of the Group, management is currently monitoring the loan portfolio of the Group using new business line definitions. An important component

of the Group’s new operational structure is the establishment of the RRD for the purposes of centralising and streamlining the management of its delinquent loans.

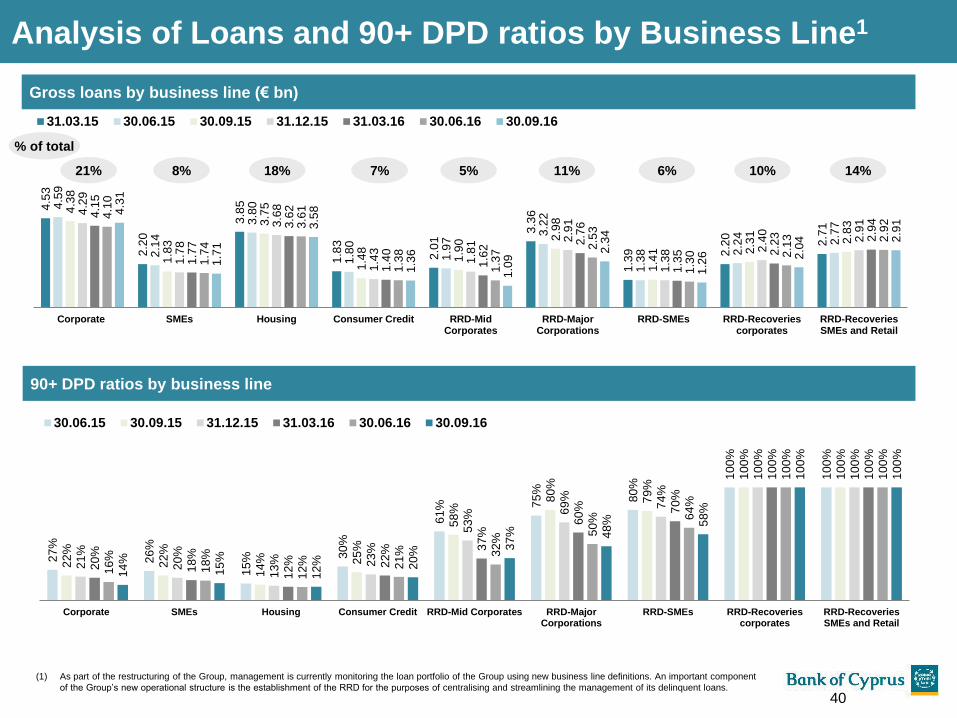

Analysis 90+ DPD by Business Line1

39

90+ DPD ratios by business line

Gross loans by business line (€ bn)

27

%

26

%

15

% 30

%

61

% 75

%

80

%

10

0%

10

0%

22

%

22

%

14

% 25

%

58

%

80

%

79

%

10

0%

10

0%

21

%

20

%

13

% 23

%

53

% 69

%

74

%

10

0%

10

0%

20

%

18

%

12

% 22

% 37

%

60

% 70

%

10

0%

10

0%

16

%

18

%

12

% 21

% 32

%

50

% 64

%

10

0%

10

0%

14

%

15

%

12

% 20

%

37

% 48

% 58

%

10

0%

10

0%

Corporate SMEs Housing Consumer Credit RRD-Mid Corporates RRD-MajorCorporations

RRD-SMEs RRD-Recoveriescorporates

RRD-RecoveriesSMEs and Retail

30.06.15 30.09.15 31.12.15 31.03.16 30.06.16 30.09.16

4.5

3

2.2

0

3.8

5

1.8

3

2.0

1

3.3

6

1.3

9 2.2

0

2.7

1

4.5

9

2.1

4

3.8

0

1.8

0

1.9

7

3.2

2

1.3

8 2.2

4

2.7

7

4.3

8

1.8

3

3.7

5

1.4

8

1.9

0 2.9

8

1.4

1 2.3

1

2.8

3

4.2

9

1.7

8

3.6

8

1.4

3

1.8

1 2.9

1

1.3

8 2.4

0

2.9

1

4.1

5

1.7

7

3.6

2

1.4

0

1.6

2

2.7

6

1.3

5 2.2

3 2.9

4

4.1

0

1.7

4

3.6

1

1.3

8

1.3

7

2.5

3

1.3

0 2.1

3 2.9

2

4.3

1

1.7

1

3.5

8

1.3

6

1.0

9

2.3

4

1.2

6 2.0

4 2.9

1

Corporate SMEs Housing Consumer Credit RRD-MidCorporates

RRD-MajorCorporations

RRD-SMEs RRD-Recoveriescorporates

RRD-RecoveriesSMEs and Retail

31.03.15 30.06.15 30.09.15 31.12.15 31.03.16 30.06.16 30.09.16

% of total

(1) As part of the restructuring of the Group, management is currently monitoring the loan portfolio of the Group using new business line definitions. An important component

of the Group’s new operational structure is the establishment of the RRD for the purposes of centralising and streamlining the management of its delinquent loans.

21% 8% 18% 5% 10%6%

Analysis of Loans and 90+ DPD ratios by Business Line1

7% 11% 14%

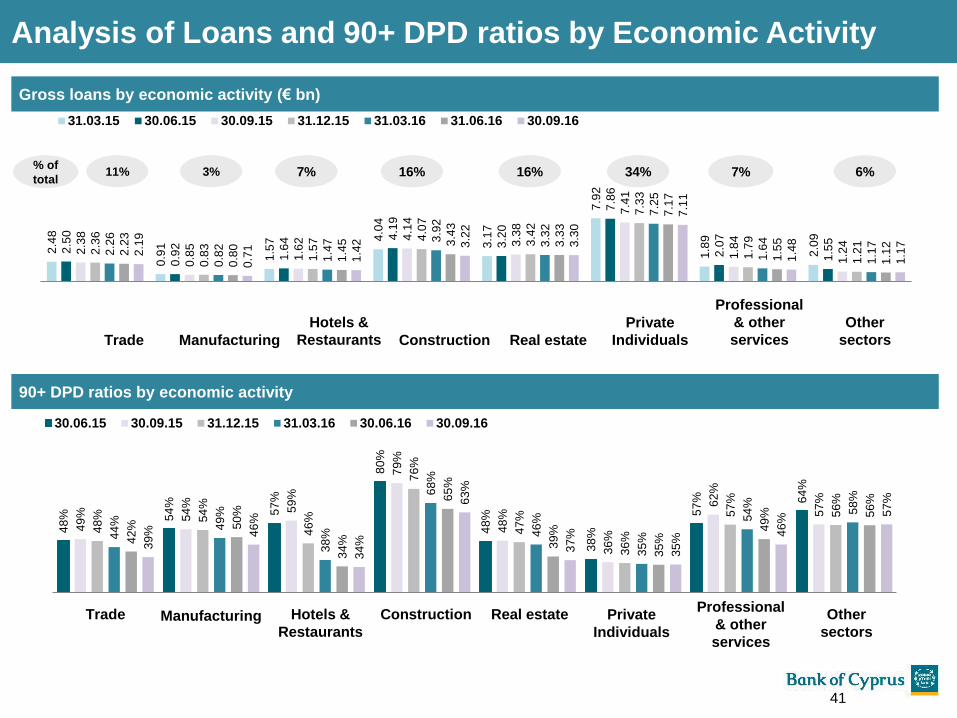

40

90+ DPD ratios by economic activity

48

% 54

%

57

%

80

%

48

%

38

%

57

% 64

%

49

% 54

% 59

%

79

%

48

%

36

%

62

%

57

%

48

% 54

%

46

%

76

%

47

%

36

%

57

%

56

%

44

% 49

%

38

%

68

%

46

%

35

%

54

%

58

%

42

% 50

%

34

%

65

%

39

%

35

%

49

% 56

%

39

% 46

%

34

%

63

%

37

%

35

%

46

%

57

%

30.06.15 30.09.15 31.12.15 31.03.16 30.06.16 30.09.16

Gross loans by economic activity (€ bn)

Trade Manufacturing Hotels &

Restaurants

Construction Real estate Private

Individuals

Professional

& other

services

Other

sectors

Analysis of Loans and 90+ DPD ratios by Economic Activity 2

.48

0.9

1

1.5

7 4.0

4

3.1

7

7.9

2

1.8

9

2.0

9

2.5

0

0.9

2

1.6

4 4.1

9

3.2

0

7.8

6

2.0

7

1.5

5

2.3

8

0.8

5

1.6

2 4.1

4

3.3

8

7.4

1

1.8

4

1.2

4

2.3

6

0.8

3

1.5

7 4.0

7

3.4

2

7.3

3

1.7

9

1.2

1

2.2

6

0.8

2

1.4

7 3.9

2

3.3

2

7.2

5

1.6

4

1.1

7

2.2

3

0.8

0

1.4

5 3.4

3

3.3

3

7.1

7

1.5

5

1.1

2

2.1

9

0.7

1

1.4

2 3.2

2

3.3

0

7.1

1

1.4

8

1.1

7

31.03.15 30.06.15 30.09.15 31.12.15 31.03.16 31.06.16 30.09.16

Trade Manufacturing

Hotels &

Restaurants Construction Real estate

Private

Individuals

Professional

& other

services

Other

sectors

16%11% 34% 7% 6%% of

total16%7%3%

41

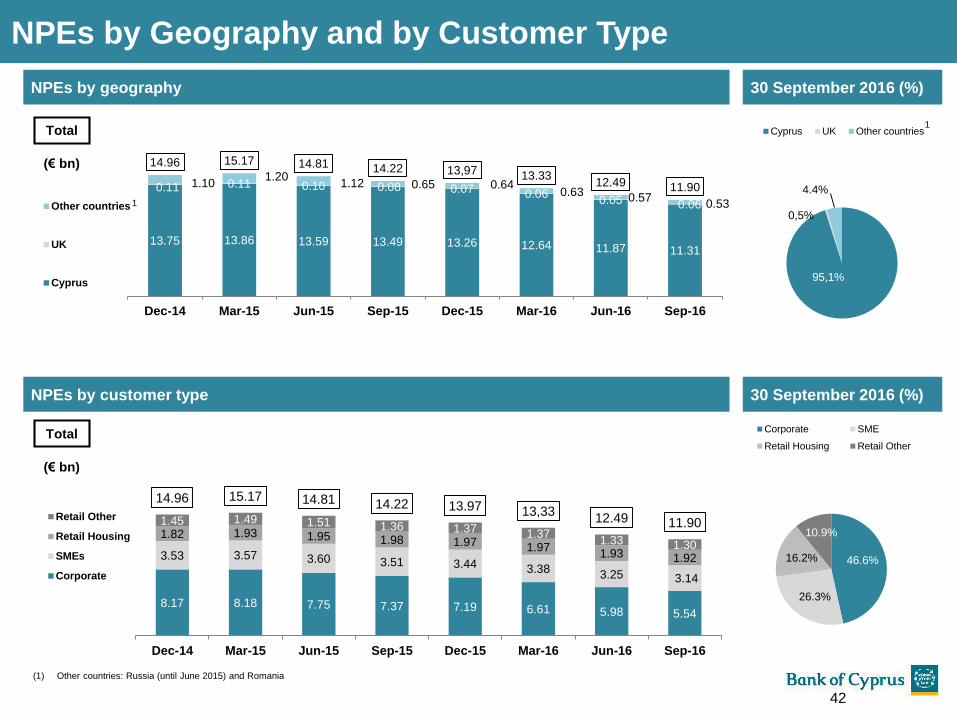

13.75 13.86 13.59 13.49 13.26 12.64 11.87 11.31

0.11 0.11 0.10 0.08 0.07 0.060.05 0.06

1.101.20

1.12 0.65 0.640.63 0.57

0.53

14.96 15.17 14.81 14.22 13,97 13.3312.49 11.90

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Other countries

UK

Cyprus

1

Total

(€ bn)

(1) Other countries: Russia (until June 2015) and Romania

NPEs by geography

NPEs by Geography and by Customer Type

95,1%

0,5%

4.4%

Cyprus UK Other countries1

46.6%

26.3%

16.2%

10.9%

Corporate SME

Retail Housing Retail Other

30 September 2016 (%)

30 September 2016 (%)NPEs by customer type

8.17 8.18 7.75 7.37 7.19 6.61 5.98 5.54

3.53 3.57 3.60 3.51 3.44 3.383.25 3.14

1.82 1.93 1.95 1.98 1.97 1.971.93 1.92

1.45 1.49 1.51 1.36 1.37 1.371.33 1.30

14.96 15.17 14.81 14.22 13.97 13,3312.49 11.90

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Retail Other

Retail Housing

SMEs

Corporate

Total

(€ bn)

42

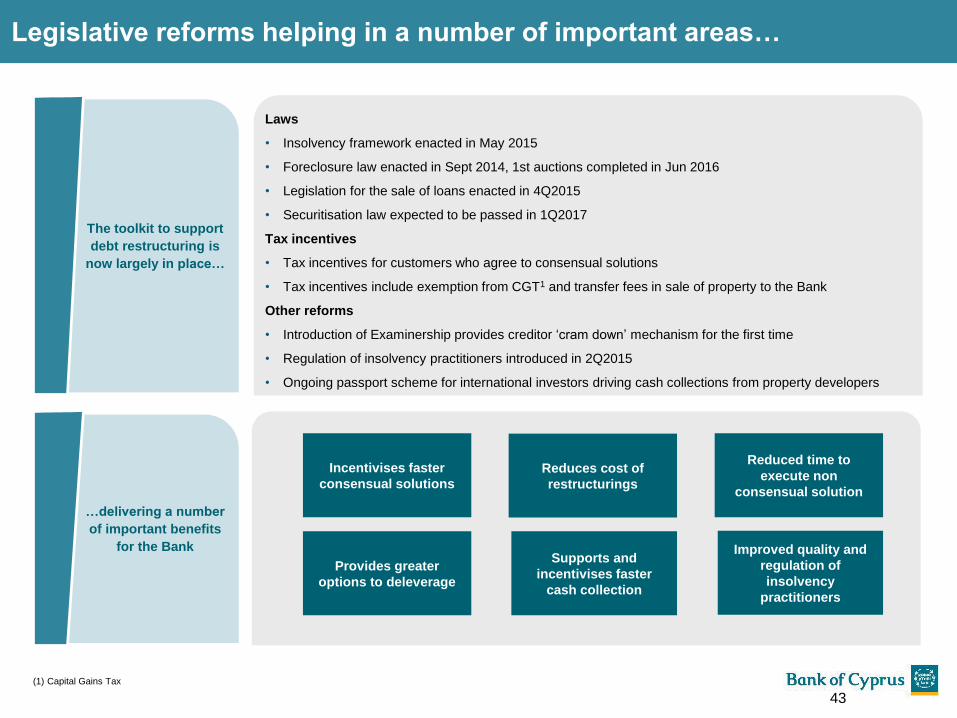

Legislative reforms helping in a number of important areas…

Laws

• Insolvency framework enacted in May 2015

• Foreclosure law enacted in Sept 2014, 1st auctions completed in Jun 2016

• Legislation for the sale of loans enacted in 4Q2015

• Securitisation law expected to be passed in 1Q2017

Tax incentives

• Tax incentives for customers who agree to consensual solutions

• Tax incentives include exemption from CGT1 and transfer fees in sale of property to the Bank

Other reforms

• Introduction of Examinership provides creditor ‘cram down’ mechanism for the first time

• Regulation of insolvency practitioners introduced in 2Q2015

• Ongoing passport scheme for international investors driving cash collections from property developers

The toolkit to support

debt restructuring is

now largely in place…

…delivering a number

of important benefits

for the Bank

Incentivises faster

consensual solutions

Reduced time to

execute non

consensual solution

Reduces cost of

restructurings

Provides greater

options to deleverage

Supports and

incentivises faster

cash collection

Improved quality and

regulation of

insolvency

practitioners

(1) Capital Gains Tax

43

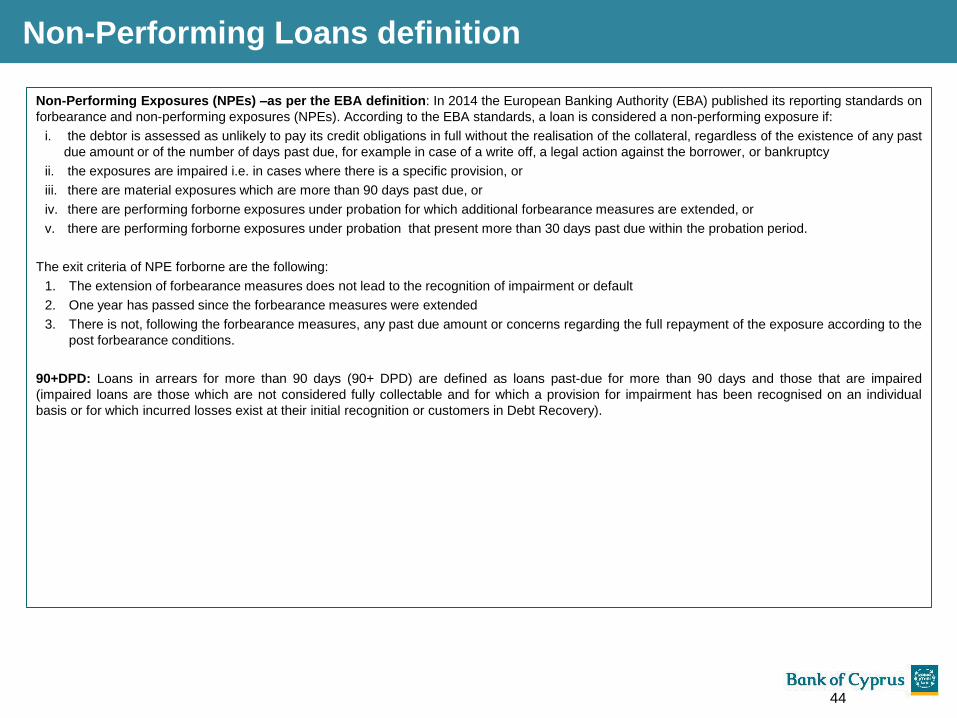

Non-Performing Loans definition

Non-Performing Exposures (NPEs) –as per the EBA definition: In 2014 the European Banking Authority (EBA) published its reporting standards on

forbearance and non-performing exposures (NPEs). According to the EBA standards, a loan is considered a non-performing exposure if:

i. the debtor is assessed as unlikely to pay its credit obligations in full without the realisation of the collateral, regardless of the existence of any past

due amount or of the number of days past due, for example in case of a write off, a legal action against the borrower, or bankruptcy

ii. the exposures are impaired i.e. in cases where there is a specific provision, or

iii. there are material exposures which are more than 90 days past due, or

iv. there are performing forborne exposures under probation for which additional forbearance measures are extended, or

v. there are performing forborne exposures under probation that present more than 30 days past due within the probation period.

The exit criteria of NPE forborne are the following:

1. The extension of forbearance measures does not lead to the recognition of impairment or default

2. One year has passed since the forbearance measures were extended

3. There is not, following the forbearance measures, any past due amount or concerns regarding the full repayment of the exposure according to the

post forbearance conditions.