Back to the Basics Best Practices in Risk Management ... material in this presentation is the...

58

The material in this presentation is the property of Fair Isaac Corporation, is provided for the recipient only, and shall not be used, reproduced, or disclosed without Fair Isaac Corporation's express consent. © 2009 Fair Isaac Corporation. 1 Back to the Basics Best Practices in Risk Management Series – Session 6 Basel II & Credit Card Act FICO - Transforming the way businesses make decisions Sharon O’Connor-Clarke Alissa McCarthy Principal Consultant Senior Consultant February 10, 2010

Transcript of Back to the Basics Best Practices in Risk Management ... material in this presentation is the...

The material in this presentation is the property of Fair Isaac Corporation, is provided for the recipient only, and shall not be used, reproduced, or disclosed without Fair Isaac Corporation's express consent.

© 2009 Fair Isaac Corporation. 1

Back to the Basics

Best Practices in Risk Management

Series – Session 6

Basel II & Credit Card Act

FICO - Transforming the way businesses make decisions

Sharon O’Connor-Clarke Alissa McCarthyPrincipal Consultant Senior ConsultantFebruary 10, 2010

The material in this presentation is the property of Fair Isaac Corporation, is provided for the recipient only, and shall not be used, reproduced, or disclosed without Fair Isaac Corporation's express consent.

© 2009 Fair Isaac Corporation. 2

Best Practice Webinar Series Dates

Overview & Originations September 9

Account Management October 14

Collections November 11

Fraud December 9

Portfolio Management January 13

Basel II & Credit Card Act Today

DDA March 10

Small Business April 14

© 2009 Fair Isaac Corporation. 3

Join Us at FICO World, April 13-16 in Miami

Keynote Speaker Michael PorterAuthor, On Competition, Competitive StrategyBishop William Lawrence University Professor, Harvard Business School

90+ Panel Discussions, Case Studies and Presentations, Including:

• Banking in the Reset Economy — Panel chaired by Michael Lafferty

• Regulation Redefined – Panel

• Scoring Today Workshop

• Can Credit Cards Still Be Profitable? — Panel chaired by Ted Iacobuzio

• Making Real-Time Decisions with Transaction Analytics

• Debit is the New Credit

• Managing Credit Risk Across the Lifecycle

• Risk Management Fundamentals — Customer Management

• Optimizing Credit Lines Under New Regulatory Requirements

• Increasing Personal Loan Portfolio Profitability

• Connecting Customer Management and Collections to Increase

• 360 Degree View of Credit Risk

Register now and save $200!

www.fico.com/ficoworld

© 2009 Fair Isaac Corporation. 4 © 2009 Fair Isaac Corporation. Confidential.4

Agenda

» Best Practices Overview

» Basel II

» Analytics Solutions for Basel II

» Stress Testing

» Credit Card Act

» Analytic Solutions for CCA

© 2009 Fair Isaac Corporation. 5

Best Practices in Risk Management -Themes and Conclusions

» Customer behaviors and the economic environment constantly change, strategies, scores, and policies must evolve with the latest data

» Risk Management is a culture and crucial skill set requiring:

» Disciplined use of data

» Understanding the impact of management actions on segment level behavior; scores, policies, processes, treatments, products

» Analytical insights identify actions necessary to enhance the understanding of segment and customer level behavior

» statistically controlled testing and reporting to observe changes in customer behavior

» Risk Management works with Risk Operations to insure

» Disciplined execution of risk and marketing policies

» Centralized control of strategies to create the flexibility pro-active decisioning environment necessary for sustained growth

© 2009 Fair Isaac Corporation. 6

Fundamentals of Risk Management Across The Customer Lifecycle

» Strategies must be aligned with business objectives, across the customer lifecycle to manage risk and grow revenue

» Appetite for risk or degree of risk aversion drives attitude toward credit granting

» Management of key risk metrics (i.e., delinquency rate, loss rate,% net bad debt) requires focus on risk and revenue

» For example: originations screening can be used to eliminate up to 80% of risk or you can balance an aggressive originations strategy with an equally aggressive portfolio monitoring strategy

» Scores of different types and performance outcomes can be used to prioritize treatments and allocate resources

» Acquisitions, collections, recovery, and fraud operations combine risk management and operations execution discipline to meet business goals

© 2009 Fair Isaac Corporation. 7

© 2009 Fair Isaac Corporation. Confidential.7

Agenda

» Best Practices Overview

» Basel II

» Analytics Solutions for Basel II

» Stress Testing

» Credit Card Act

» Analytic Solutions for CCA

© 2009 Fair Isaac Corporation. 8

What is Basel II?

» International set of standards regulating how lenders need to set their minimum capital reserves

Short Term

Ensure banks set aside

enough money to

weather tough times

Long Term

Bring best practice risk

management to banks

Ensure stability in the

financial markets

© 2009 Fair Isaac Corporation. 9

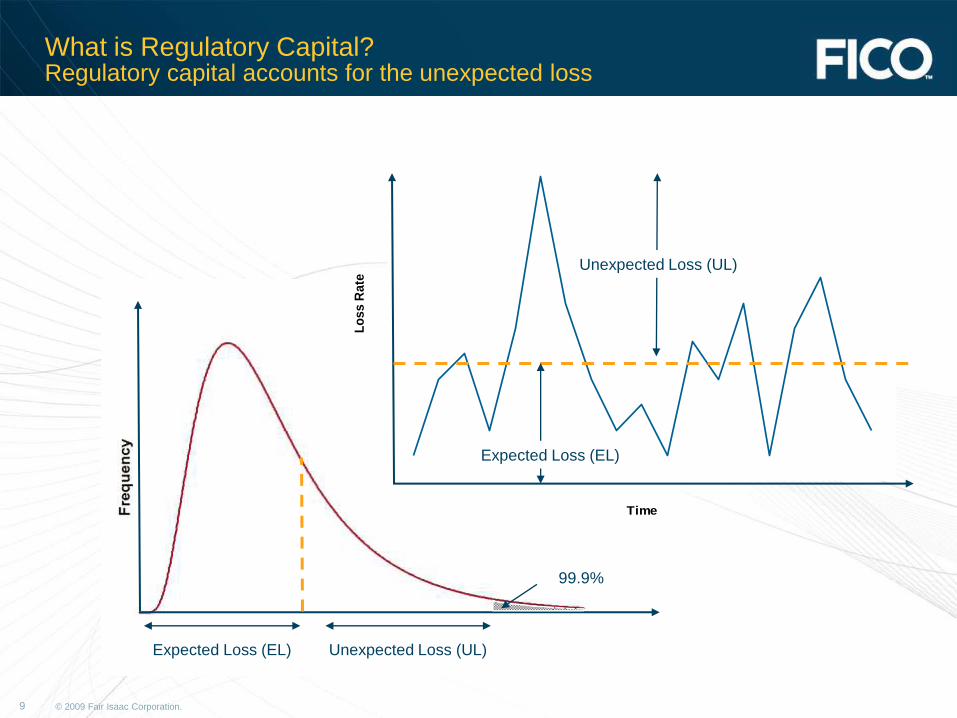

What is Regulatory Capital?Regulatory capital accounts for the unexpected loss

Expected Loss (EL) Unexpected Loss (UL)

99.9%

0

2

4

6

8

10

12

14

0 2 4 6 8 10 12 14 16 18 20

Time

Lo

ss

Ra

te

Expected Loss (EL)

Unexpected Loss (UL)

© 2009 Fair Isaac Corporation. 10

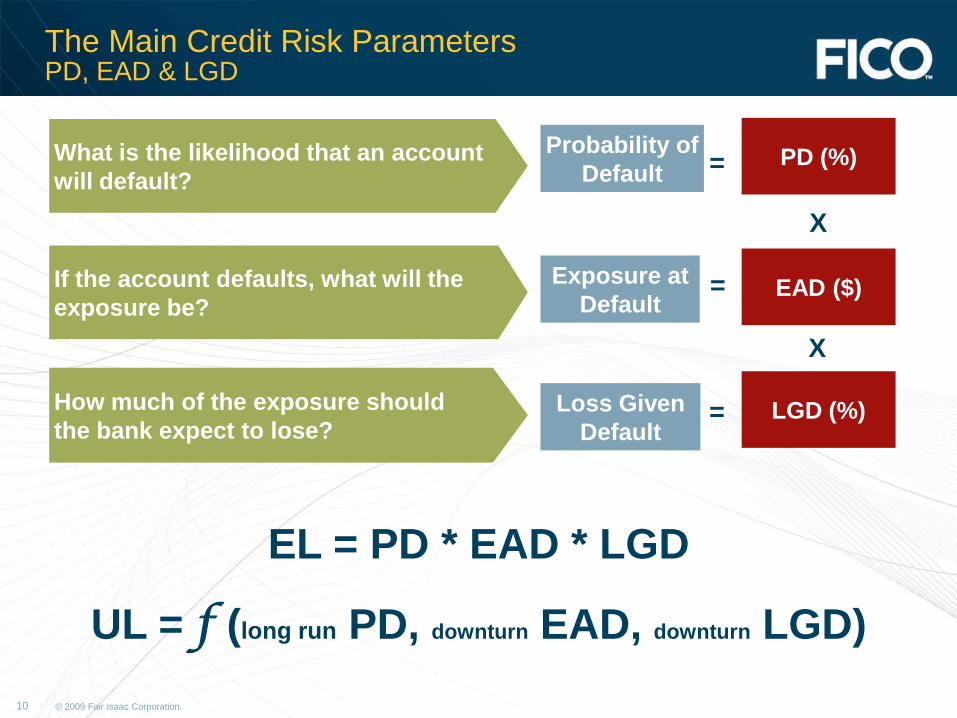

The Main Credit Risk ParametersPD, EAD & LGD

What is the likelihood that an account

will default?

If the account defaults, what will the

exposure be?

How much of the exposure should

the bank expect to lose?

Probability of

Default

Exposure at

Default

Loss Given

Default

PD (%)

EAD ($)

LGD (%)

=

=

=

X

X

EL = PD * EAD * LGD

UL = f (long run PD, downturn EAD, downturn LGD)

© 2009 Fair Isaac Corporation. 11

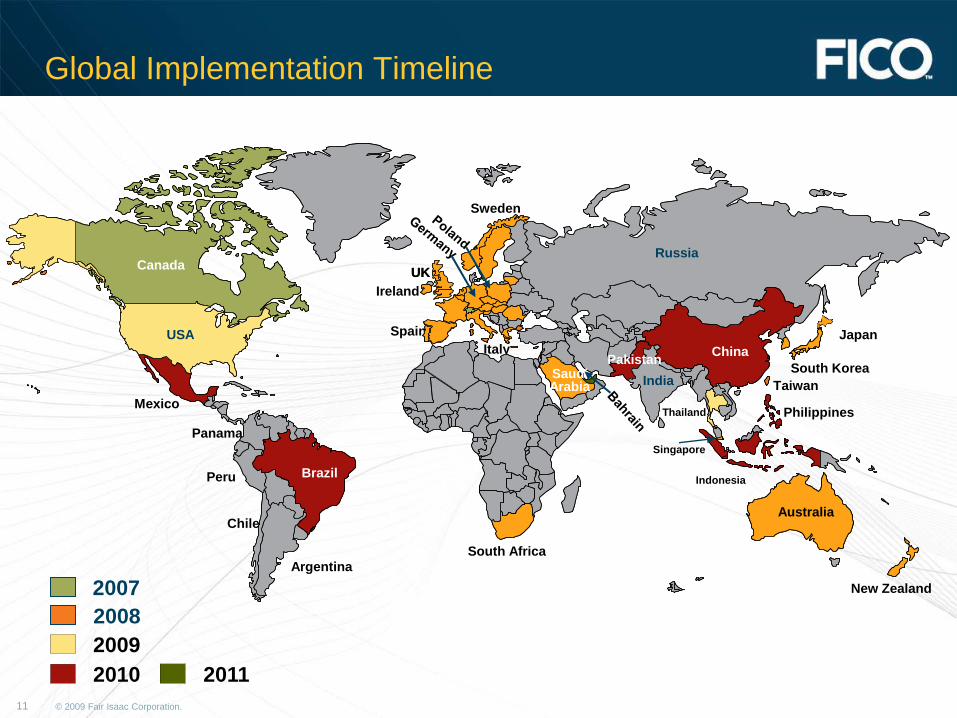

Global Implementation Timeline

SaudiArabia

UK

Sweden

Canada

US

Mexico

Brazil

TurkeyItaly

Spain

Taiwan

China

Australia

Thailand

South Korea

Japan

Philippines

Singapore

India

South Africa

Panama

Ireland

Chile

Argentina

SaudiArabia

UK

Brazil

China

Australia

2008

2009

Peru

Russia

India

Canada

USA

2010

2007

Indonesia

Pakistan

New Zealand

2011

© 2009 Fair Isaac Corporation. 12

Industry Trends

» Basel II regulations are still very much evolving, and are expected to converge among US and international standards

» Most European countries have received conditional approval, with list of to-dos

» Regulators have cited known weaknesses

» Stress Testing

» Forward looking capital estimates

» Lenders focus up to this point has been on meeting compliance

» A few banks have moved use of Basel II beyond capital adequacy to other areas of risk management

© 2009 Fair Isaac Corporation. 13

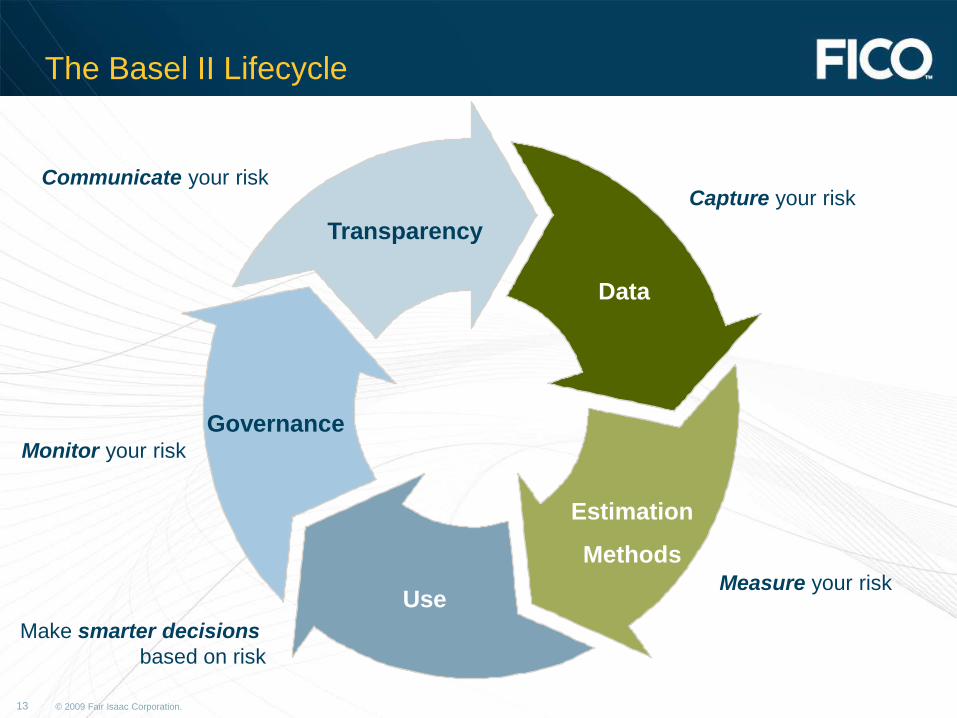

The Basel II Lifecycle

Data

Estimation

Methods

Use

Governance

Transparency

Capture your risk

Measure your risk

Communicate your risk

Monitor your risk

Make smarter decisions

based on risk

© 2009 Fair Isaac Corporation. 14

89% of senior bank executives believe banks

with a robust risk infrastructure will have a

competitive advantage over others….It is likely

that competitive advantage will be gained by

those institutions that best leverage data, the

analytics, and the processes – established in

part for Basel II purposes – to improve

business decisions.

Ernst & Young

Global Basel II 2006 Survey

―

‖

Beyond the Regulatory Requirements to Adopt Basel, Banks are Looking to Stay Competitive

© 2009 Fair Isaac Corporation. 15

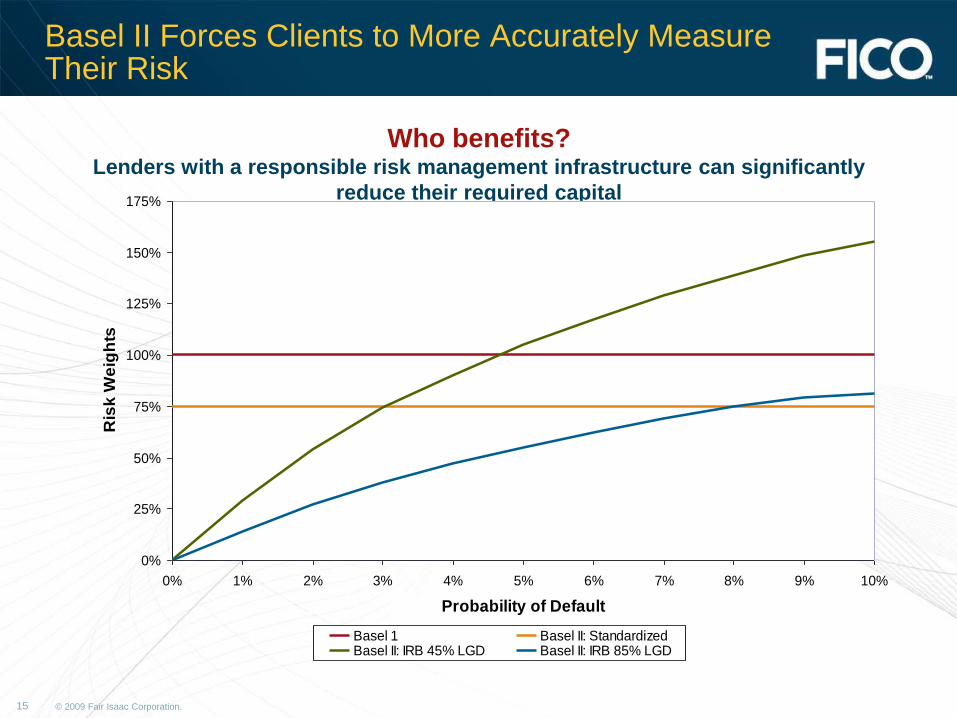

Basel II Forces Clients to More Accurately Measure Their Risk

Who benefits?Lenders with a responsible risk management infrastructure can significantly

reduce their required capital

0%

25%

50%

75%

100%

125%

150%

175%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

Probability of Default

Ris

k W

eig

hts

Basel 1 Basel II: StandardizedBasel II: IRB 45% LGD Basel II: IRB 85% LGD

© 2009 Fair Isaac Corporation. 16

Lenders Face Dire Consequences if They Fail to Meet Basel Requirements

» Higher capital reserves

» Loss of investor confidence

» Increased regulator scrutiny

» Decreased competitiveness

© 2009 Fair Isaac Corporation. 17

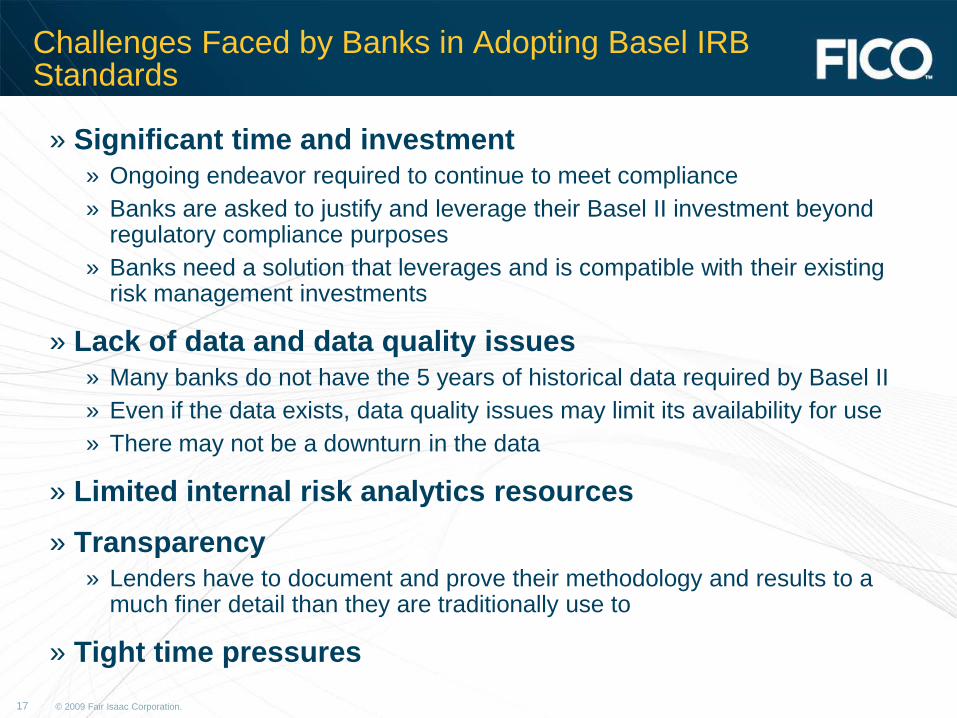

Challenges Faced by Banks in Adopting Basel IRB Standards

» Significant time and investment

» Ongoing endeavor required to continue to meet compliance

» Banks are asked to justify and leverage their Basel II investment beyond regulatory compliance purposes

» Banks need a solution that leverages and is compatible with their existing risk management investments

» Lack of data and data quality issues

» Many banks do not have the 5 years of historical data required by Basel II

» Even if the data exists, data quality issues may limit its availability for use

» There may not be a downturn in the data

» Limited internal risk analytics resources

» Transparency

» Lenders have to document and prove their methodology and results to a much finer detail than they are traditionally use to

» Tight time pressures

© 2009 Fair Isaac Corporation. 18

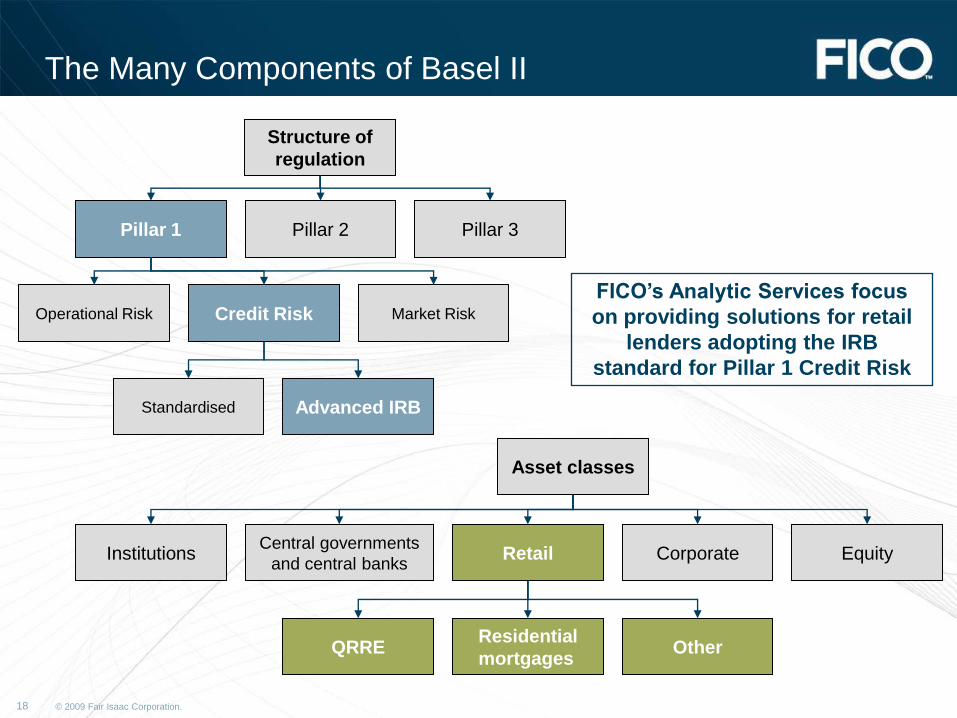

The Many Components of Basel II

Pillar 1 Pillar 3Pillar 2

Structure of

regulation

Credit Risk Operational Risk Market Risk

Advanced IRBStandardised

Asset classes

Central governments

and central banksRetail Corporate Institutions Equity

OtherResidential

mortgagesQRRE

FICO’s Analytic Services focus

on providing solutions for retail

lenders adopting the IRB

standard for Pillar 1 Credit Risk

© 2009 Fair Isaac Corporation. 19

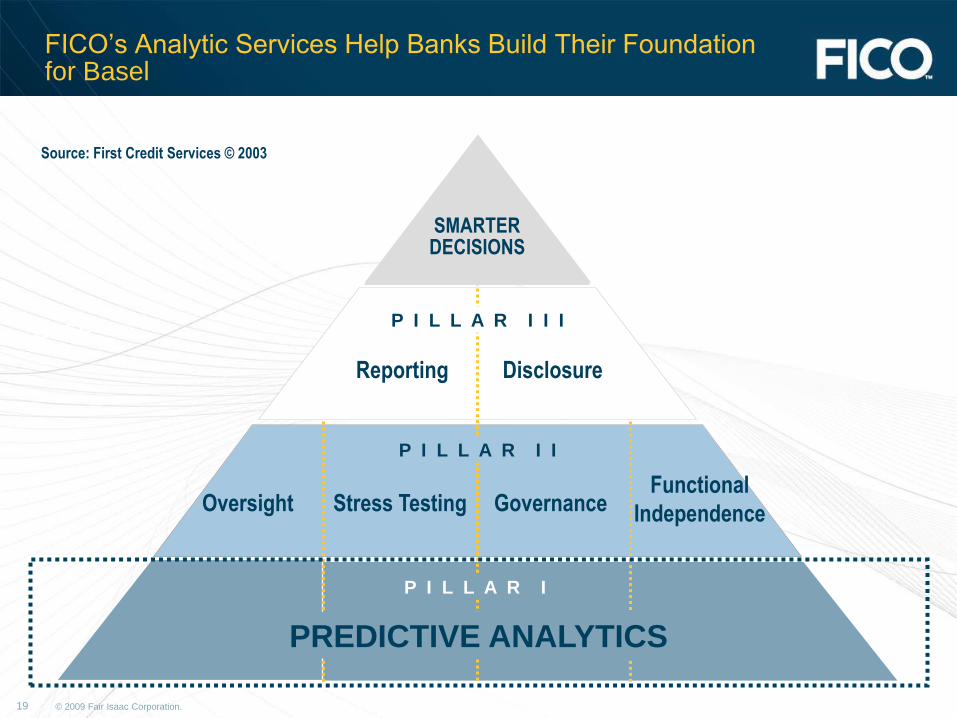

FICO’s Analytic Services Help Banks Build Their Foundation for Basel

Source: First Credit Services © 2003

DemonstratedCompliance

Use Test

Data Models Validation Documentation

Oversight Stress Testing GovernanceFunctional

Independence

Reporting Disclosure

P I L L A R I

P I L L A R I I

P I L L A R I I I

PREDICTIVE ANALYTICS

OPER

SMARTERDECISIONS

© 2009 Fair Isaac Corporation. 20 © 2009 Fair Isaac Corporation. Confidential.20

Agenda

» Best Practices Overview

» Basel II

» Analytics Solutions for Basel II

» Stress Testing

» Credit Card Act

» Analytic Solutions for CCA

© 2009 Fair Isaac Corporation. 21

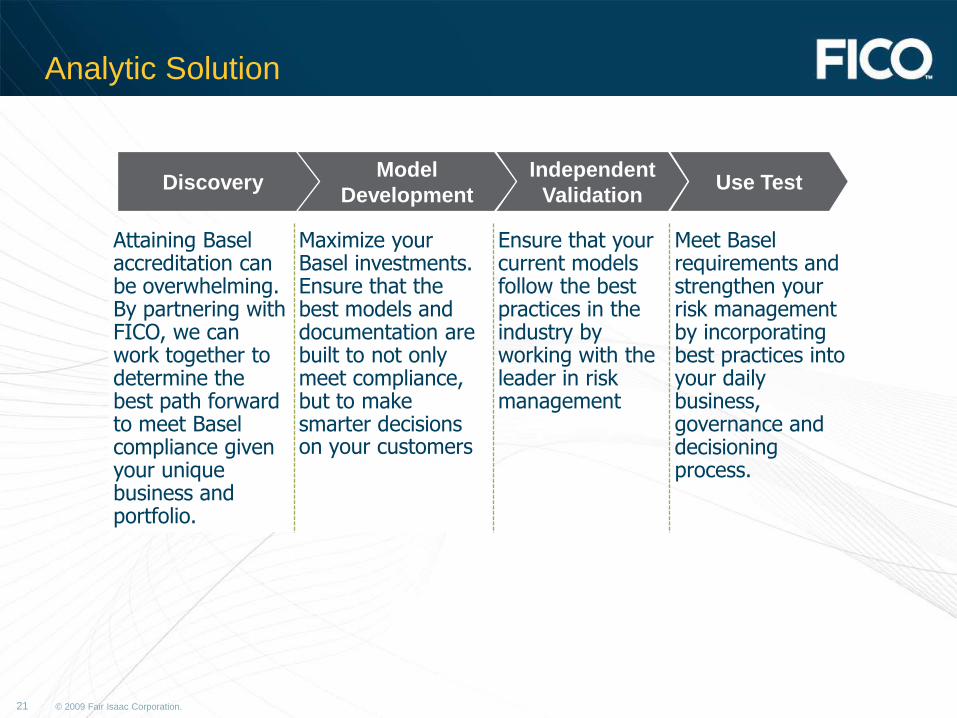

Analytic Solution

DiscoveryModel

Development

Independent

ValidationUse Test

Attaining Basel accreditation can be overwhelming. By partnering with FICO, we can work together to determine the best path forward to meet Basel compliance given your unique business and portfolio.

Maximize your Basel investments. Ensure that the best models and documentation are built to not only meet compliance, but to make smarter decisions on your customers

Ensure that your current models follow the best practices in the industry by working with the leader in risk management

Meet Basel requirements and strengthen your risk management by incorporating best practices into your daily business, governance and decisioning process.

© 2009 Fair Isaac Corporation. 22

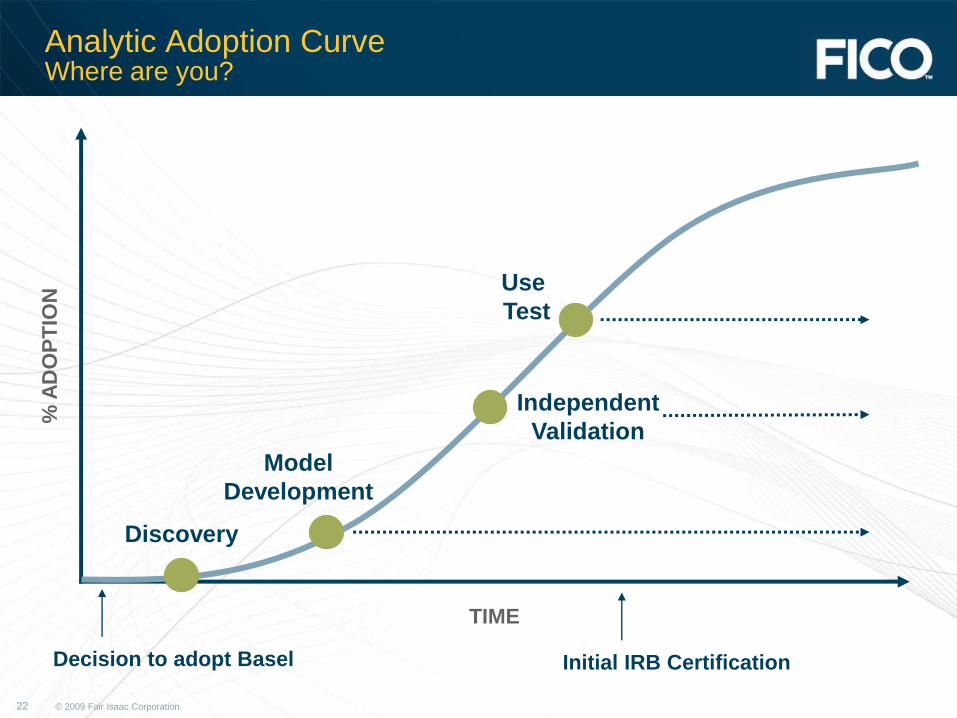

Analytic Adoption CurveWhere are you?

Discovery

Model

Development

Decision to adopt Basel Initial IRB Certification

Independent

Validation

Use

Test

TIME

% A

DO

PT

ION

© 2009 Fair Isaac Corporation. 23 © 2009 Fair Isaac Corporation. Confidential.23

Agenda

» Best Practices Overview

» Basel II

» Analytics Solutions for Basel II

» Stress Testing

» Credit Card Act

» Analytic Solutions for CCA

© 2009 Fair Isaac Corporation. 24

Why Stress Test? Because Stress Happens

» Reduce your own Stress as a risk manager - Sound Portfolio Risk Management includes proactively recognizing and mitigating the risk in your portfolio

Source: Federal Reserve

9/11 Credit Crunch

© 2009 Fair Isaac Corporation. 25

Why Stress Test?Create Regulatory Compliance – Capital Adequacy

» Basel II requires lenders adopting the Internal Ratings Based (IRB) Approach to establish use of stress testing as part of their overall risk assessment for deriving capital adequacy

» Regulators require assurances that portfolios can withstand economic downturns and that Banks have considered these in their calculations

» Banks with accurate assessments will have appropriate capital levels

» Bank with sound risk mitigation capabilities may see capital reductions

An IRB bank must have in place sound stress testing processes for use

in the assessment of capital adequacy. Stress testing must involve

identifying possible events of future changes in economic conditions that

could have unfavorable effects on a bank’s credit exposures and

assessment of the bank’s ability to withstand such changes...

Basel II: 434

© 2009 Fair Isaac Corporation. 26

What can I do about it?Portfolio Stress Testing

» Credit defaults are a function of many factors:

» Observable account-level factors (CB files, etc.)

» Unobservable account-level factors (health & job status, etc.)

» Market factors (GDP, housing prices, competitive dynamics)

» Traditional credit scoring accounts for only what’s observed about individual borrowers

» This works well in stable economies and normal risk management practices

» Stress testing adds the market dimension to allow for portfolio-level ―what ifs‖

» Allows for multiple predictions of defaults across a range of potential economic conditions

» Simulates the impact of origination changes stemming from credit policy changes and competitive factors

© 2009 Fair Isaac Corporation. 27

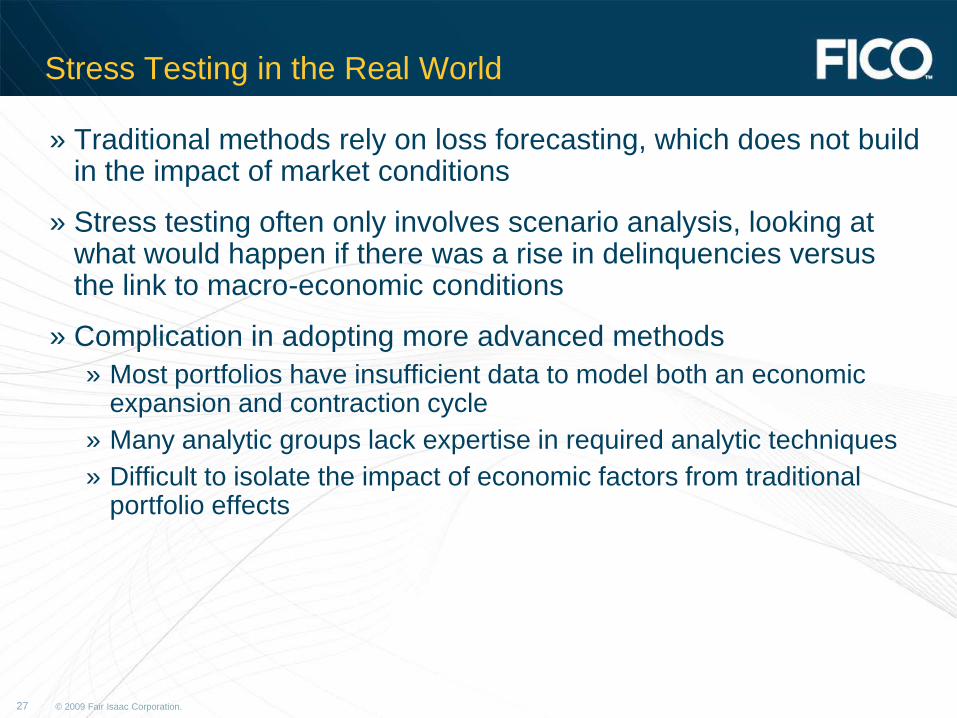

Stress Testing in the Real World

» Traditional methods rely on loss forecasting, which does not build in the impact of market conditions

» Stress testing often only involves scenario analysis, looking at what would happen if there was a rise in delinquencies versus the link to macro-economic conditions

» Complication in adopting more advanced methods

» Most portfolios have insufficient data to model both an economic expansion and contraction cycle

» Many analytic groups lack expertise in required analytic techniques

» Difficult to isolate the impact of economic factors from traditional portfolio effects

© 2009 Fair Isaac Corporation. 28

Basel II Lifecycle Forms the Foundation for Account and Portfolio Level Decisions…

» How much capital do I need to hold for this account?

» Should I accept or decline this account?

» What existing mortgage customers should I cross-sell my auto loan products to?

» How much line should I allocate this account?

» How much capital do I need to reserve for my portfolio?

» If I want to grow my portfolio by 3%, what is the best way from a Return on Capital perspective?

» In an economic downturn, how should I modify my strategic direction to achieve desired results?

Transaction Portfolio

smallest details big picture

Account

© 2009 Fair Isaac Corporation. 29 © 2009 Fair Isaac Corporation. Confidential.29

Agenda

» Best Practices Overview

» Basel II

» Analytics Solutions for Basel II

» Stress Testing

» Credit Card Act

» Analytic Solutions for CCA

© 2009 Fair Isaac Corporation. 30

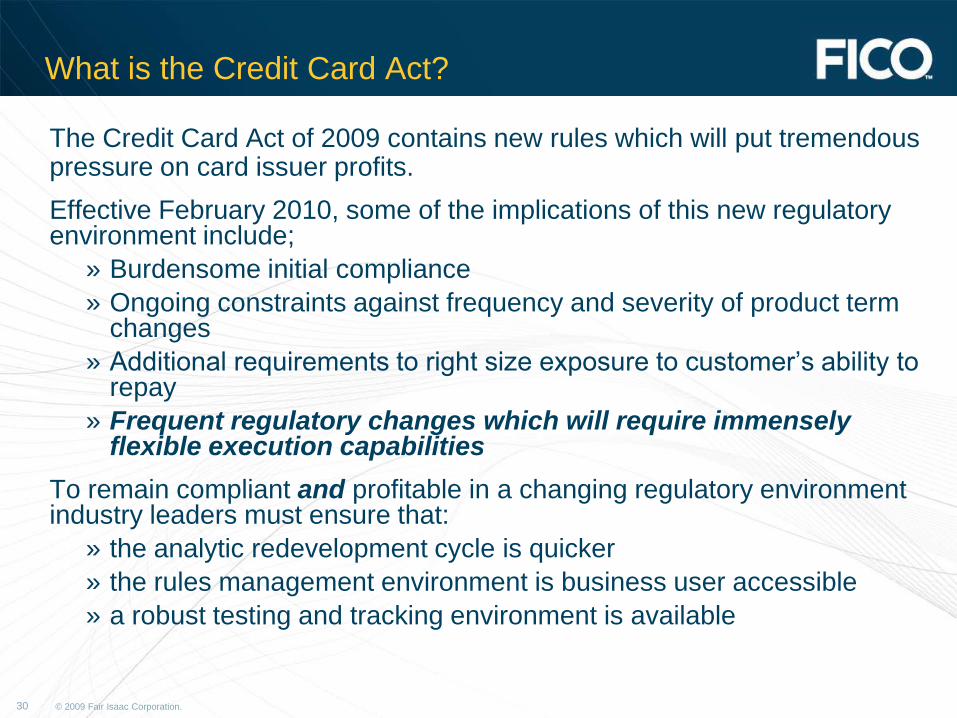

What is the Credit Card Act?

The Credit Card Act of 2009 contains new rules which will put tremendous pressure on card issuer profits.

Effective February 2010, some of the implications of this new regulatory environment include;

» Burdensome initial compliance

» Ongoing constraints against frequency and severity of product term changes

» Additional requirements to right size exposure to customer’s ability to repay

» Frequent regulatory changes which will require immensely flexible execution capabilities

To remain compliant and profitable in a changing regulatory environment industry leaders must ensure that:

» the analytic redevelopment cycle is quicker

» the rules management environment is business user accessible

» a robust testing and tracking environment is available

© 2009 Fair Isaac Corporation. 31 © 2009 Fair Isaac Corporation.31

―The most comprehensive and sweeping

reforms ever adopted by the Board for credit

card accounts.‖

Fed Chairman Ben Bernanke

© 2009 Fair Isaac Corporation. 32

Identify Imperatives & Impacts of Regulatory Change

» The rules introduced by this legislation represent an increased compliance challenge affecting all areas of the customer lifecycle from marketing and originations through account management and collections.

» The key questions every issuer must ask themselves are:

» What are the revenue and loss impacts of the new law?

» What are the various strategy changes that will be necessary to accommodate the new law?

» What systems changes must be made for compliance? What will these changes cost?

» What strategies might be implemented to preserve and strengthen overall profits within this new legal environment?

The answers to these questions must focus on an approach that balances regulatory compliance with income protection, portfolio quality, and loss prevention.

© 2009 Fair Isaac Corporation. 33

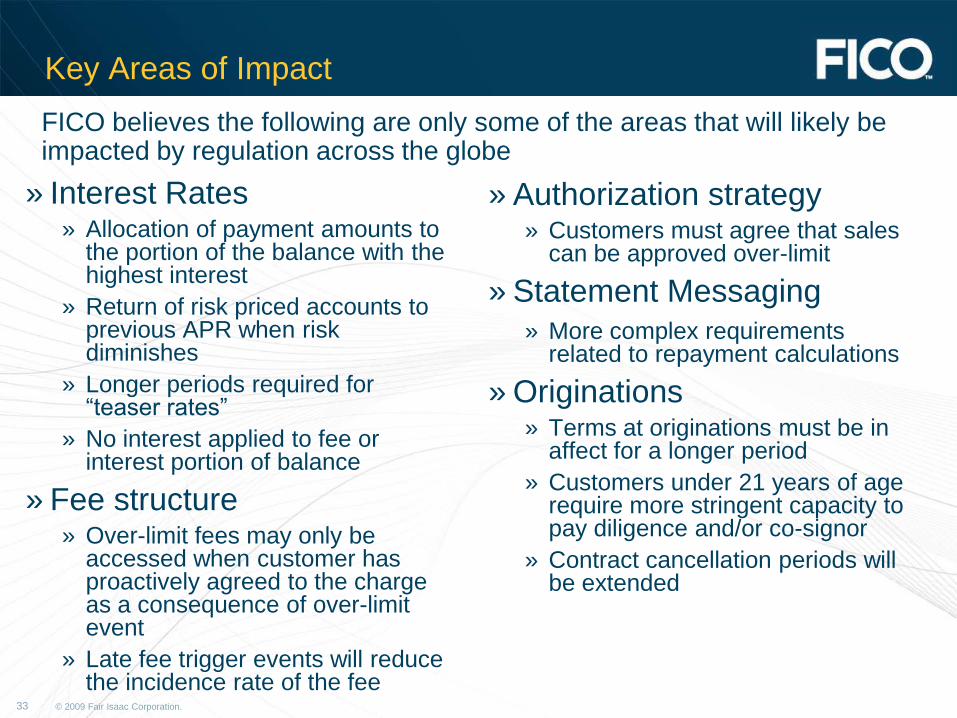

Key Areas of Impact

» Interest Rates» Allocation of payment amounts to

the portion of the balance with the highest interest

» Return of risk priced accounts to previous APR when risk diminishes

» Longer periods required for ―teaser rates‖

» No interest applied to fee or interest portion of balance

» Fee structure» Over-limit fees may only be

accessed when customer has proactively agreed to the charge as a consequence of over-limit event

» Late fee trigger events will reduce the incidence rate of the fee

» Authorization strategy» Customers must agree that sales

can be approved over-limit

» Statement Messaging» More complex requirements

related to repayment calculations

» Originations» Terms at originations must be in

affect for a longer period

» Customers under 21 years of age require more stringent capacity to pay diligence and/or co-signor

» Contract cancellation periods will be extended

FICO believes the following are only some of the areas that will likely be impacted by regulation across the globe

© 2009 Fair Isaac Corporation. 34

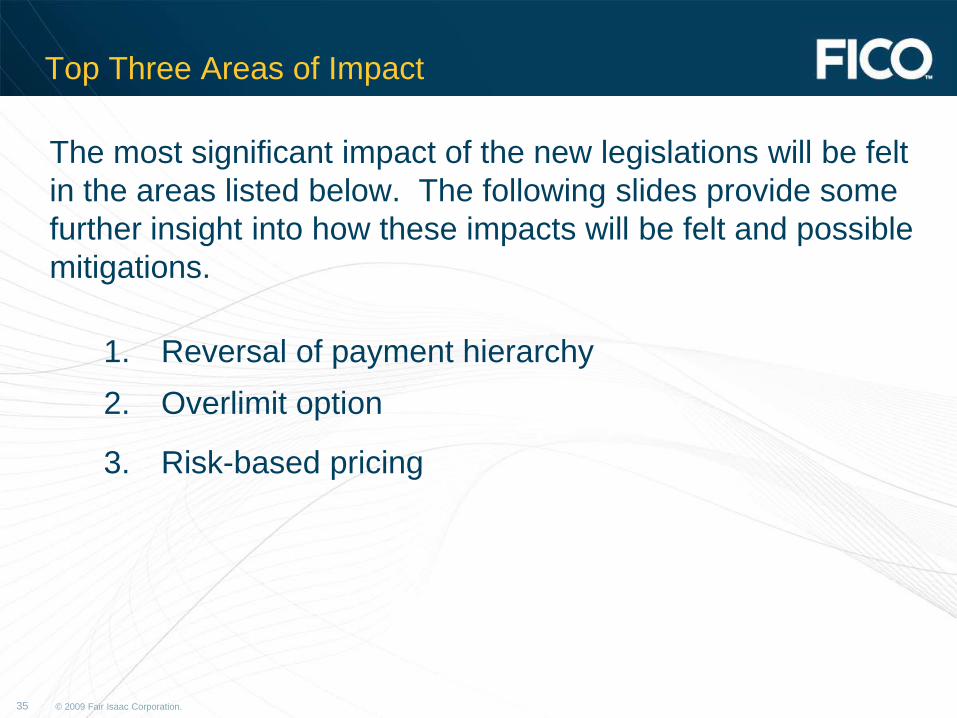

Top Three Areas of Impact

The most significant impact of the new legislations will be felt

in the areas listed below. The following slides provide some

further insight into how these impacts will be felt and possible

mitigations.

1. Reversal of payment hierarchy

2. Overlimit option

3. Risk-based pricing

© 2009 Fair Isaac Corporation. 35

Top Three Areas of Impact

The most significant impact of the new legislations will be felt

in the areas listed below. The following slides provide some

further insight into how these impacts will be felt and possible

mitigations.

1. Reversal of payment hierarchy

2. Overlimit option

3. Risk-based pricing

© 2009 Fair Isaac Corporation. 36

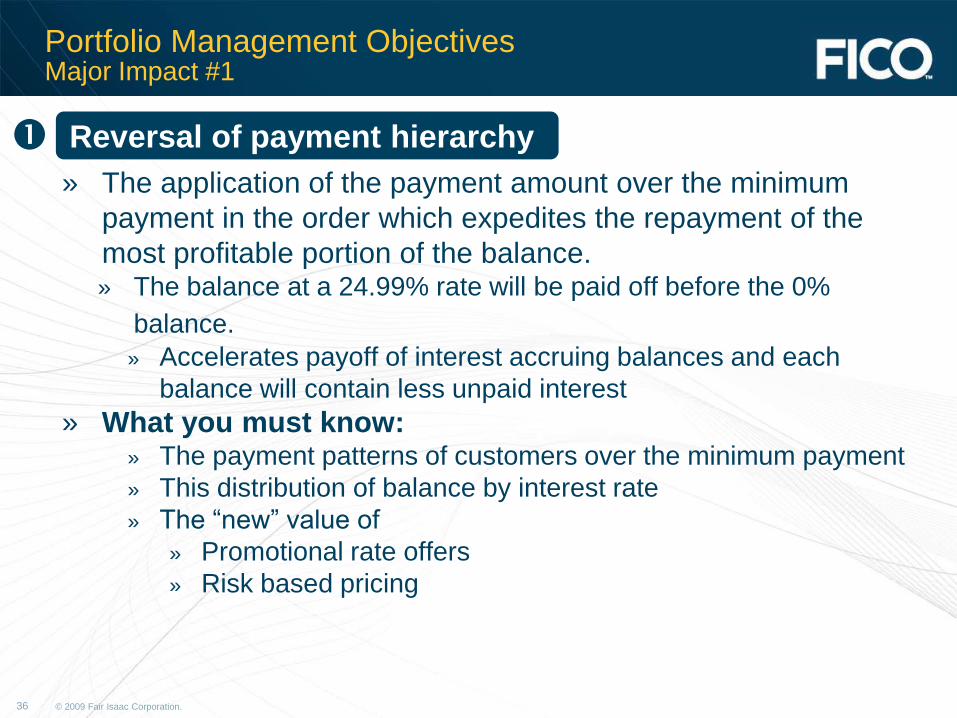

Portfolio Management ObjectivesMajor Impact #1

Reversal of payment hierarchy

» The application of the payment amount over the minimum

payment in the order which expedites the repayment of the

most profitable portion of the balance.» The balance at a 24.99% rate will be paid off before the 0%

balance.

» Accelerates payoff of interest accruing balances and each

balance will contain less unpaid interest

» What you must know:» The payment patterns of customers over the minimum payment

» This distribution of balance by interest rate

» The ―new‖ value of

» Promotional rate offers

» Risk based pricing

© 2009 Fair Isaac Corporation. 37

Portfolio Management ObjectivesMajor Impact #2

Overlimit opt-in

» Only those customers who ―opt in‖ may be charged a fee for overlimit

amounts

» What you must know

» Which/how many customers will ―opt in‖ to overlimit authorizations in

order to understand average daily balance (interest revenue) and

overlimit fee impacts

» How to process overlimit amounts under floor limits for ―opt out‖

customers

» How to manage overlimit authorization buffers

» How to possibly amend risk assessments and account management

policies that previously used overlimit event as risk indicator

© 2009 Fair Isaac Corporation. 38

Portfolio Management ObjectivesMajor Impact #3

Risk-Based Pricing

» Risk-based pricing has new timing conditions. No increase in APR, fees or finance charges during the first year the account is open.

» Pricing increase imposed due to 60-day delinquency must be reversed when the customer maintains the account as current for 6 months

» An increase in APR following the expiration of a specified period cannot be applied to transactions that occurred prior to the commencement of the period.

» What you must know» Understand the risk factors which guide risk based pricing and which

customers will ―cure‖

» What share of 30-day delinquency re-pricing events will qualify at 60 days delinquent

» What share of 60+ day delinquent priced accounts will ―cure‖ in 6 months

» What interest rate will the workout plans return to and how does this differ from today’s post-workout rate

© 2009 Fair Isaac Corporation. 39 © 2009 Fair Isaac Corporation.39

―Card issuers are going to need to rethink their entire business model.‖

Sandra Braunstein, Director»Federal Reserve Consumer & Community Affairs

© 2009 Fair Isaac Corporation. 40

Beyond Compliance: Profitability

»Many banks are scrambling to comply with the new regulations

» Differing interpretations

» Changing and evolving regulations

»Few banks have asked the question

» ―What is the impact of compliance on my business?‖

»Even fewer have asked

» ―How do I keep my card portfolio profitable and stay in business?‖

© 2009 Fair Isaac Corporation. 41 © 2009 Fair Isaac Corporation. Confidential.41

Agenda

» Best Practices Overview

» Basel II

» Analytics Solutions for Basel II

» Stress Testing

» Credit Card Act

» Analytic Solutions for CCA

© 2009 Fair Isaac Corporation. 42

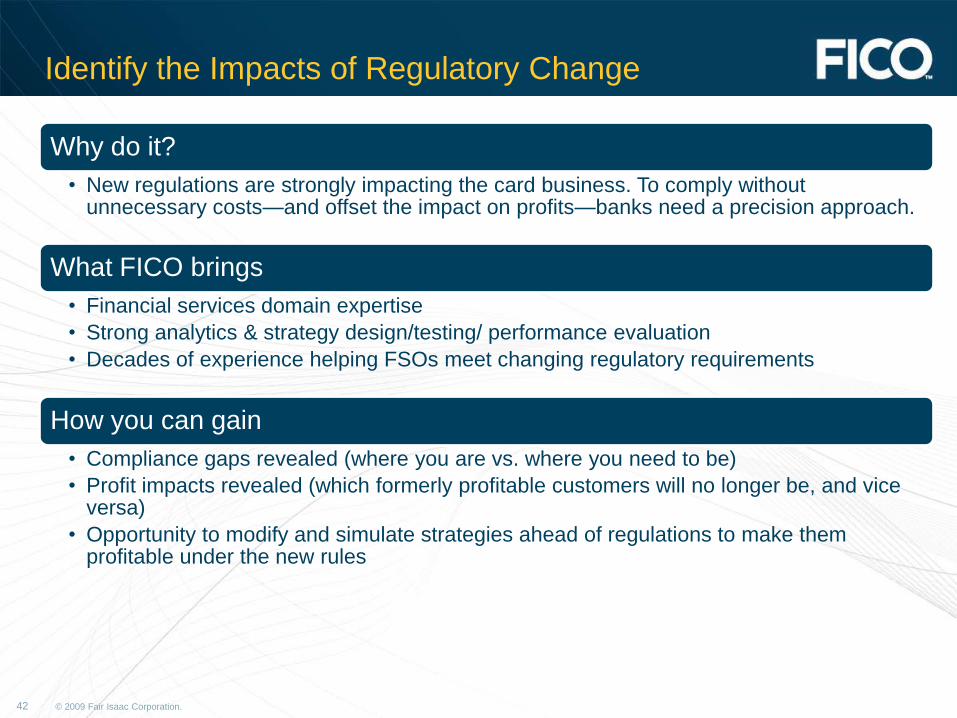

Identify the Impacts of Regulatory Change

Why do it?

• New regulations are strongly impacting the card business. To comply without unnecessary costs—and offset the impact on profits—banks need a precision approach.

What FICO brings

• Financial services domain expertise

• Strong analytics & strategy design/testing/ performance evaluation

• Decades of experience helping FSOs meet changing regulatory requirements

How you can gain

• Compliance gaps revealed (where you are vs. where you need to be)

• Profit impacts revealed (which formerly profitable customers will no longer be, and vice versa)

• Opportunity to modify and simulate strategies ahead of regulations to make them profitable under the new rules

© 2009 Fair Isaac Corporation. 43

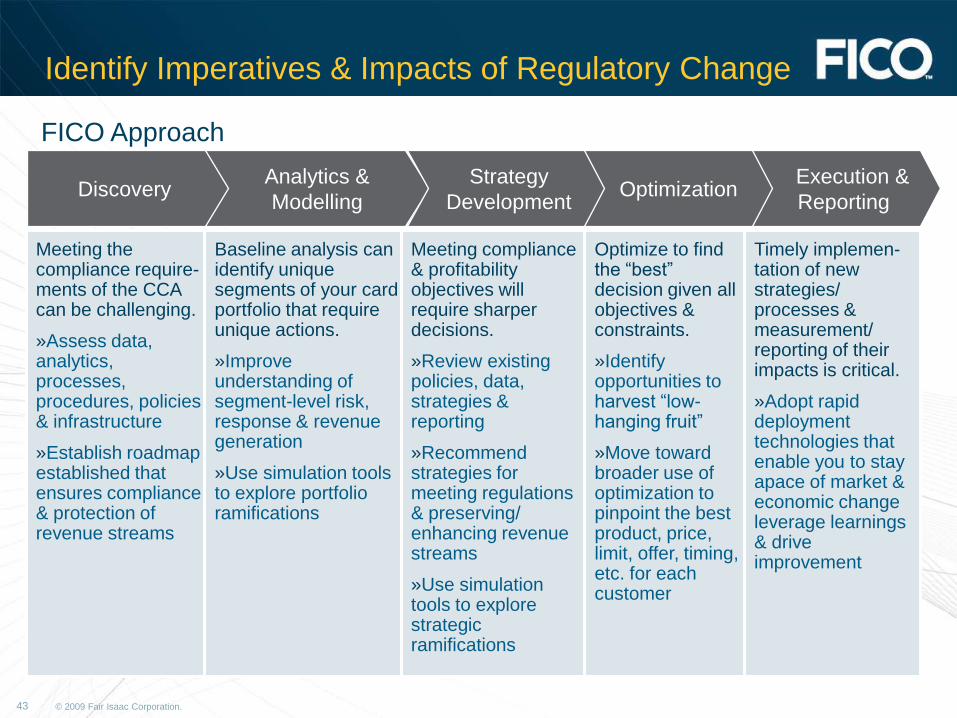

Identify Imperatives & Impacts of Regulatory Change

Meeting the compliance require-ments of the CCA can be challenging.

»Assess data, analytics, processes, procedures, policies & infrastructure

»Establish roadmap established that ensures compliance & protection of revenue streams

Baseline analysis can identify unique segments of your card portfolio that require unique actions.

»Improve understanding of segment-level risk, response & revenue generation

»Use simulation tools to explore portfolio ramifications

Meeting compliance & profitability objectives will require sharper decisions.

»Review existing policies, data, strategies & reporting

»Recommend strategies for meeting regulations & preserving/ enhancing revenue streams

»Use simulation tools to explore strategic ramifications

Optimize to find the ―best‖ decision given all objectives & constraints.

»Identify opportunities to harvest ―low-hanging fruit‖

»Move toward broader use of optimization to pinpoint the best product, price, limit, offer, timing, etc. for each customer

Timely implemen-tation of new strategies/ processes & measurement/ reporting of their impacts is critical.

»Adopt rapid deployment technologies that enable you to stay apace of market & economic change leverage learnings & drive improvement

DiscoveryAnalytics &

Modelling

Strategy

Development

Execution &

ReportingOptimization

FICO Approach

© 2009 Fair Isaac Corporation. 44

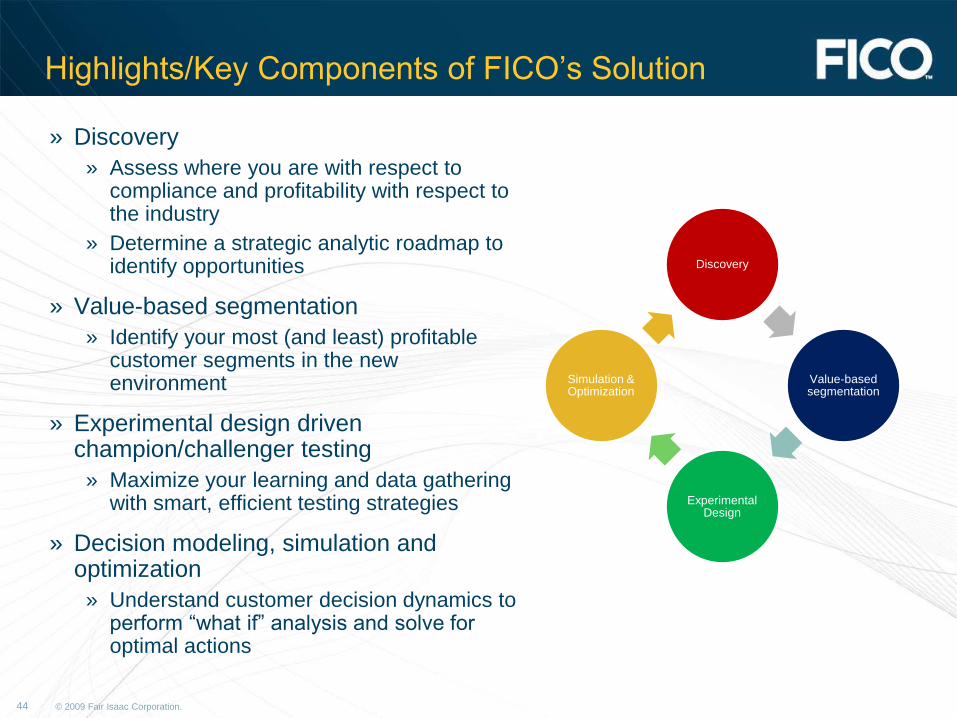

Highlights/Key Components of FICO’s Solution

» Discovery

» Assess where you are with respect to compliance and profitability with respect to the industry

» Determine a strategic analytic roadmap to identify opportunities

» Value-based segmentation

» Identify your most (and least) profitable customer segments in the new environment

» Experimental design driven champion/challenger testing

» Maximize your learning and data gathering with smart, efficient testing strategies

» Decision modeling, simulation and optimization

» Understand customer decision dynamics to perform ―what if‖ analysis and solve for optimal actions

Discovery

Value-based segmentation

Experimental Design

Simulation & Optimization

© 2009 Fair Isaac Corporation. 45

Discovery: CARD Readiness Evaluation

The foundation of the CARD Readiness Evaluation lies in a comprehensive review of the gaps between where your organization is and where it needs to go.

In order to effectively assess these gaps it is necessary to:

» Have your Legal department provide an interpretation of each section of the law

» Determine what areas are affected. This includes, but is not limited to, processes, procedures, systems, interfaces, data, and models

» Identify what actions need to be taken to achieve compliance

» Assess the immediate and ―downstream‖ impacts of these actions

» Create a timeline for implementation based on the required compliance date

» Prioritize the necessary changes based on things such as scope, complexity, and resource and system availability

© 2009 Fair Isaac Corporation. 46

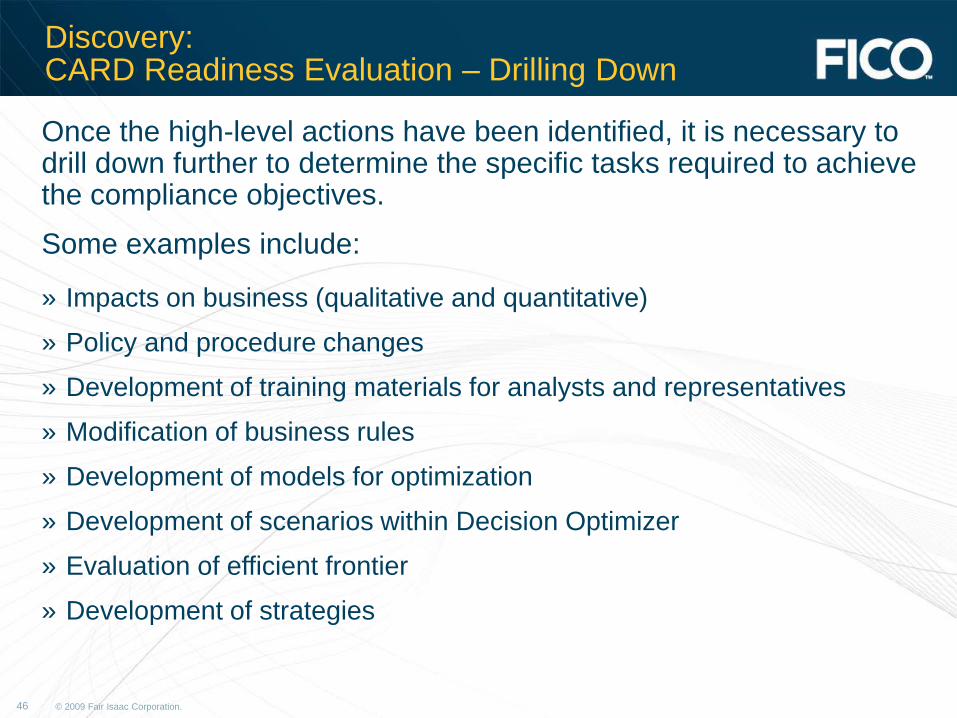

Discovery:CARD Readiness Evaluation – Drilling Down

Once the high-level actions have been identified, it is necessary to drill down further to determine the specific tasks required to achieve the compliance objectives.

Some examples include:

» Impacts on business (qualitative and quantitative)

» Policy and procedure changes

» Development of training materials for analysts and representatives

» Modification of business rules

» Development of models for optimization

» Development of scenarios within Decision Optimizer

» Evaluation of efficient frontier

» Development of strategies

© 2009 Fair Isaac Corporation. 47

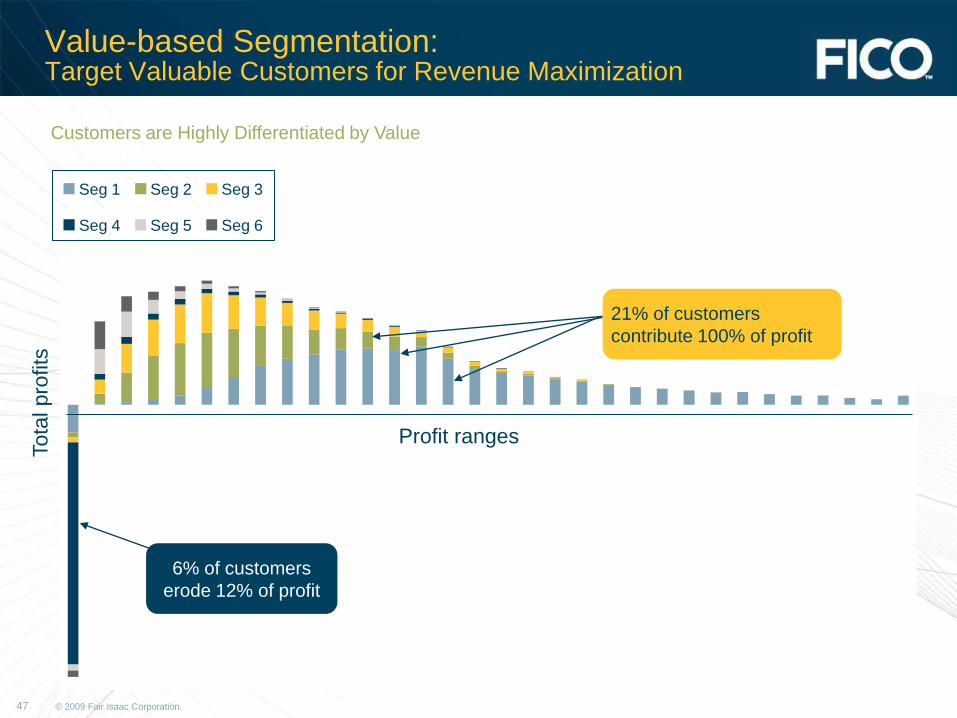

Value-based Segmentation:Target Valuable Customers for Revenue Maximization

Customers are Highly Differentiated by Value

Profit ranges

Tota

l pro

fits

6% of customers

erode 12% of profit

21% of customers

contribute 100% of profit

Seg 1 Seg 2 Seg 3

Seg 4 Seg 5 Seg 6

© 2009 Fair Isaac Corporation. 48

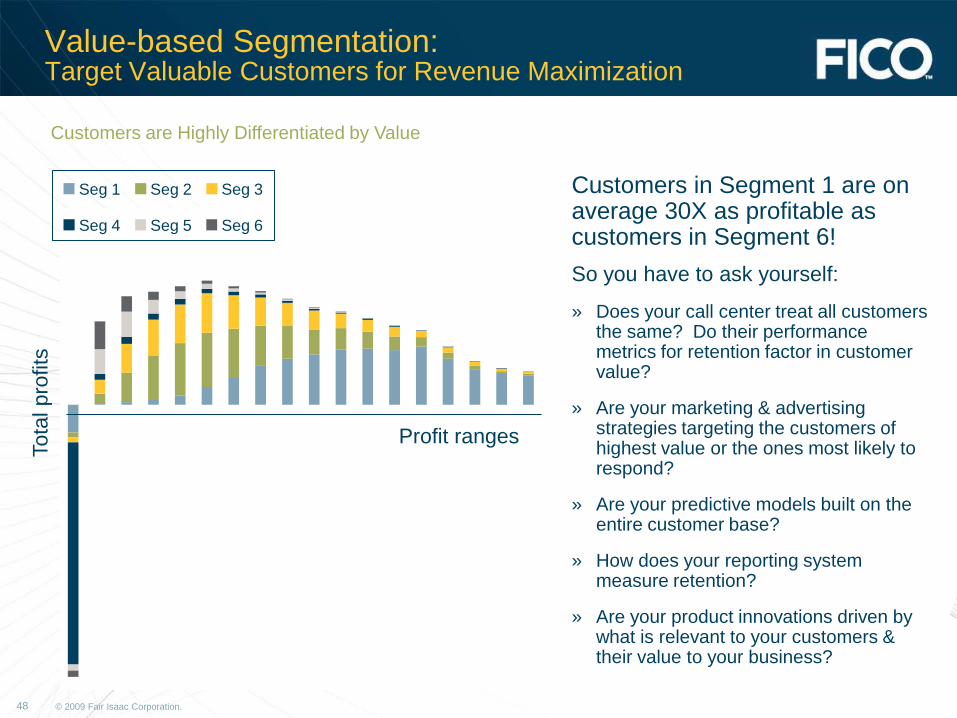

Value-based Segmentation:Target Valuable Customers for Revenue Maximization

Customers are Highly Differentiated by Value

Profit ranges

Tota

l pro

fits

Seg 1 Seg 2 Seg 3

Seg 4 Seg 5 Seg 6

Customers in Segment 1 are on average 30X as profitable as customers in Segment 6!

So you have to ask yourself:

» Does your call center treat all customers the same? Do their performance metrics for retention factor in customer value?

» Are your marketing & advertising strategies targeting the customers of highest value or the ones most likely to respond?

» Are your predictive models built on the entire customer base?

» How does your reporting system measure retention?

» Are your product innovations driven by what is relevant to your customers & their value to your business?

© 2009 Fair Isaac Corporation. 49

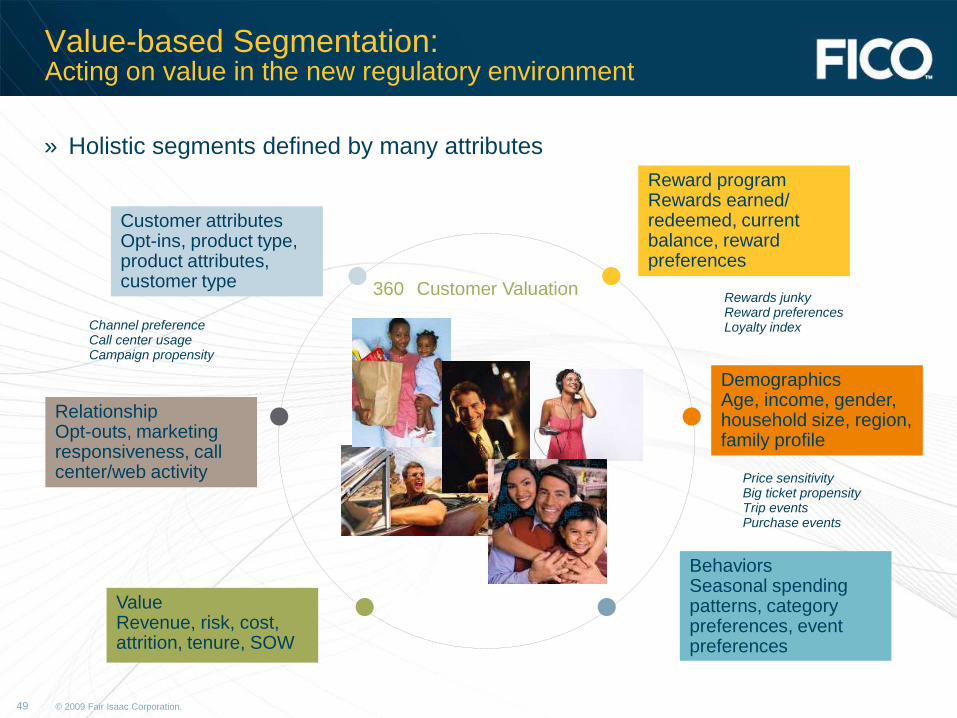

Value-based Segmentation:Acting on value in the new regulatory environment

Channel preference Call center usageCampaign propensity

Price sensitivityBig ticket propensityTrip eventsPurchase events

Rewards junkyReward preferencesLoyalty index

360 Customer Valuation

» Holistic segments defined by many attributes

Reward programRewards earned/ redeemed, current balance, reward preferences

DemographicsAge, income, gender, household size, region, family profile

BehaviorsSeasonal spending patterns, category preferences, event preferences

Customer attributesOpt-ins, product type, product attributes, customer type

RelationshipOpt-outs, marketing responsiveness, call center/web activity

ValueRevenue, risk, cost, attrition, tenure, SOW

© 2009 Fair Isaac Corporation. 50

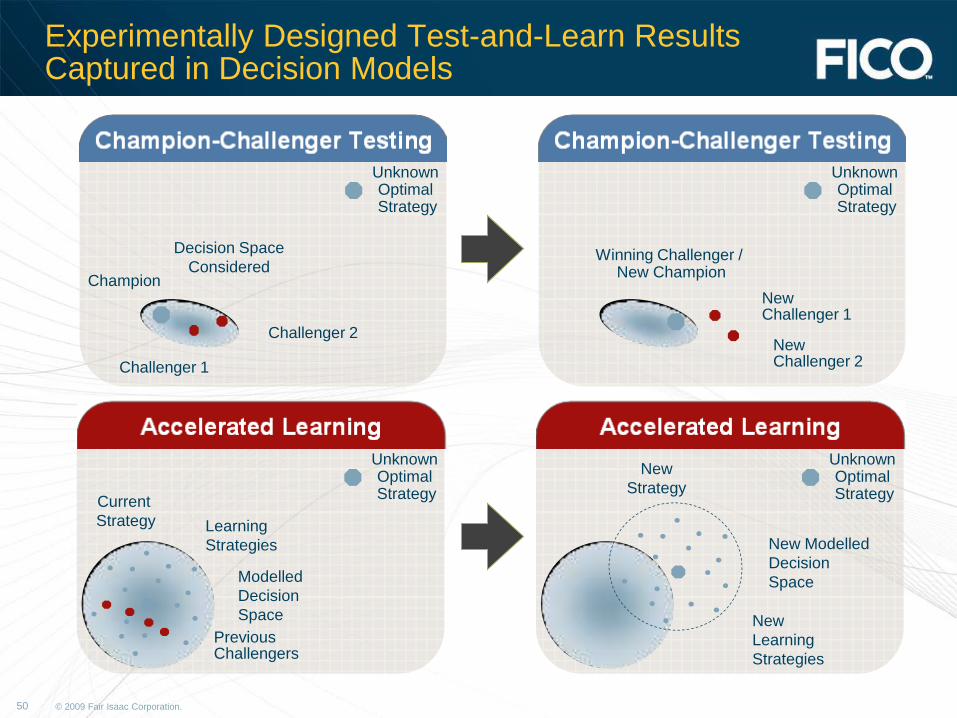

Experimentally Designed Test-and-Learn Results Captured in Decision Models

Unknown Optimal Strategy

Current

Strategy

Modelled

Decision

Space

Learning

Strategies

PreviousChallengers

Champion

Challenger 1

Challenger 2

Decision Space

Considered

Unknown Optimal Strategy

Unknown Optimal Strategy

Winning Challenger /New Champion

New Challenger 1

New Challenger 2

Unknown Optimal Strategy

New

Strategy

New Modelled

Decision

Space

New

Learning

Strategies

© 2009 Fair Isaac Corporation. 51

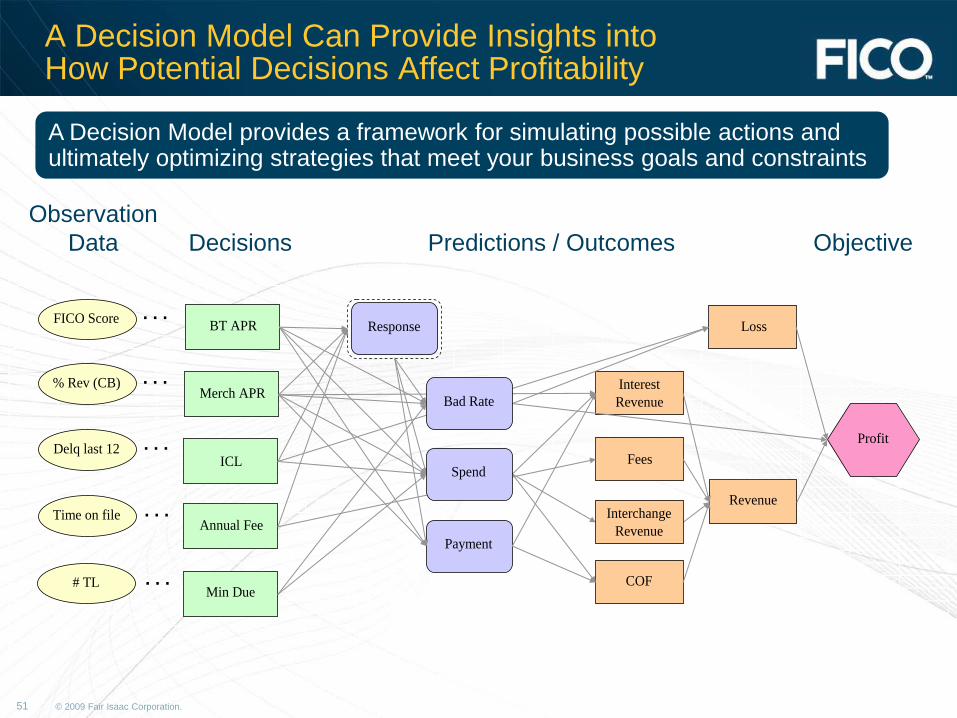

FICO Score

% Rev (CB)

Delq last 12

Time on file

Merch APR

ICL

Annual Fee

Min Due

Response

Payment

Loss

Revenue

Interest

Revenue

Fees

COF

Profit

# TL

Interchange

Revenue

BT APR

. . .

. . .

. . .

. . .

. . .

Spend

Bad Rate

A Decision Model Can Provide Insights into How Potential Decisions Affect Profitability

Observation

Data ObjectiveDecisions Predictions / Outcomes

A Decision Model provides a framework for simulating possible actions and ultimately optimizing strategies that meet your business goals and constraints

© 2009 Fair Isaac Corporation. 52

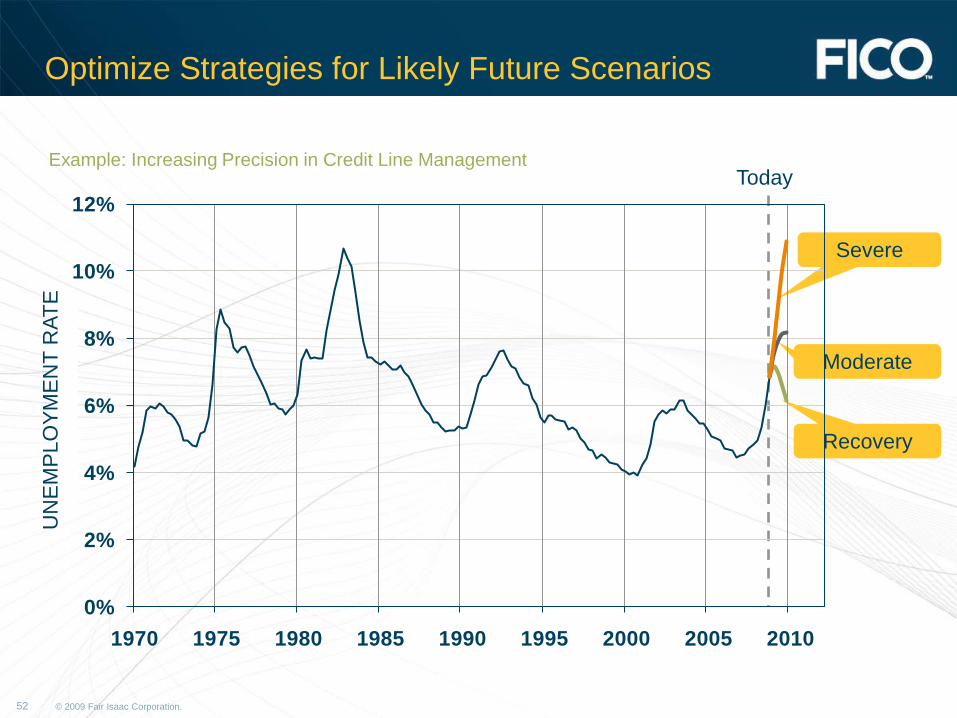

Optimize Strategies for Likely Future Scenarios

Severe

Moderate

Recovery

Today

0%

2%

4%

6%

8%

10%

12%

1970 1975 1980 1985 1990 1995 2000 2005 2010

Un

em

plo

ym

en

t R

ate

UN

EM

PLO

YM

EN

T R

AT

E

Example: Increasing Precision in Credit Line Management

© 2009 Fair Isaac Corporation. 53

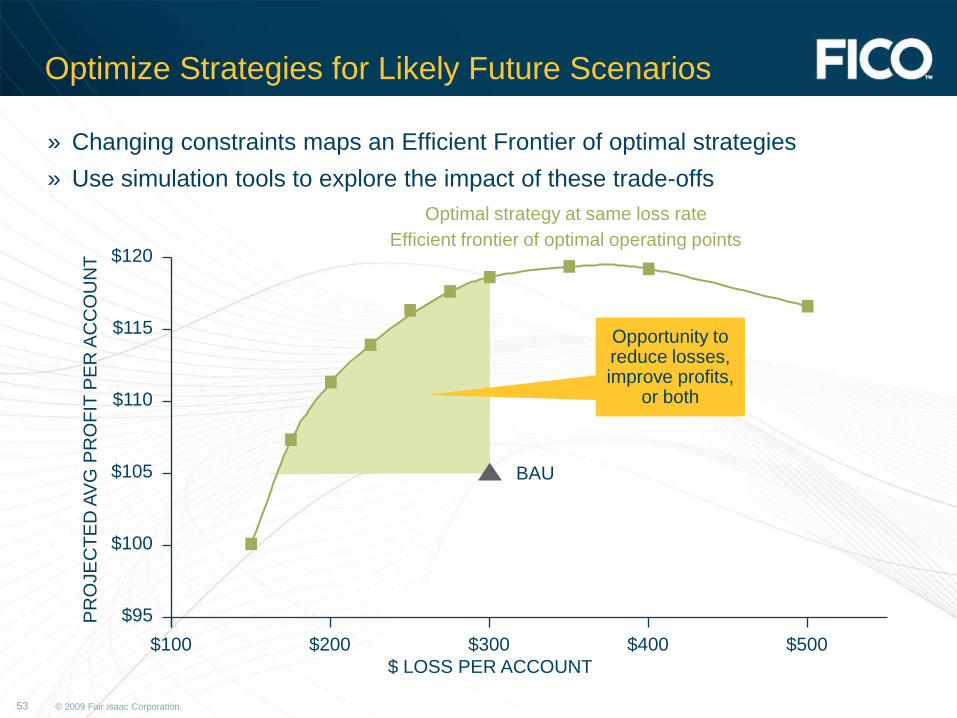

Optimize Strategies for Likely Future Scenarios

Opportunity to reduce losses, improve profits,

or both

Efficient frontier of optimal operating points

Optimal strategy at same loss rate

$95

$100

PR

OJE

CT

ED

AV

G P

RO

FIT

PE

R A

CC

OU

NT

$ LOSS PER ACCOUNT

$100

$105

$110

$115

$120

$200 $300 $400 $500

BAU

» Changing constraints maps an Efficient Frontier of optimal strategies

» Use simulation tools to explore the impact of these trade-offs

© 2009 Fair Isaac Corporation. 54

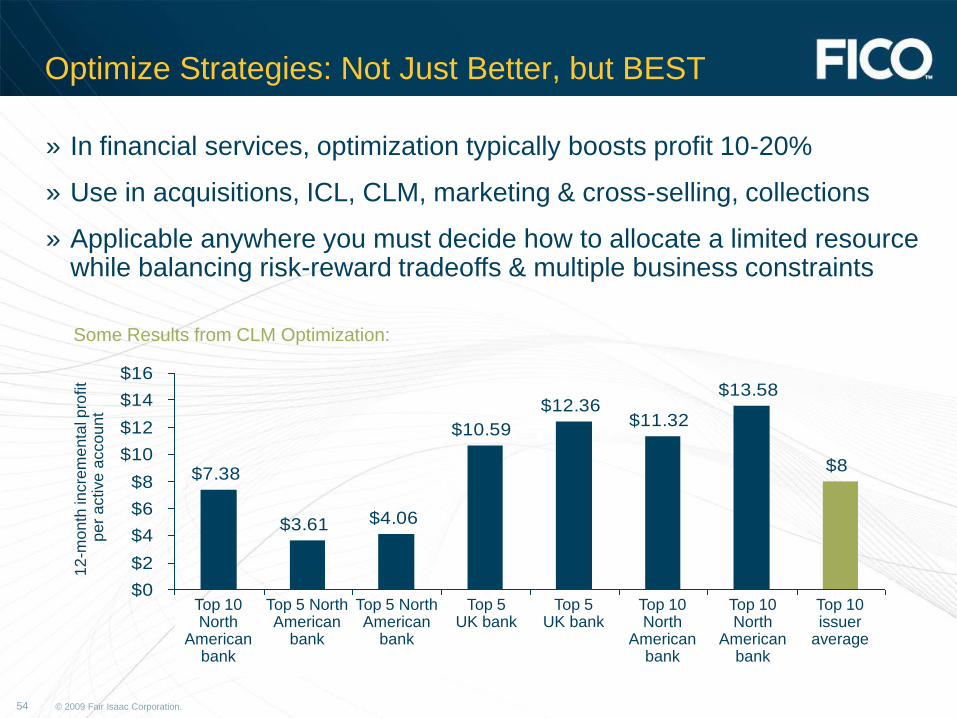

Optimize Strategies: Not Just Better, but BEST

» In financial services, optimization typically boosts profit 10-20%

» Use in acquisitions, ICL, CLM, marketing & cross-selling, collections

» Applicable anywhere you must decide how to allocate a limited resource while balancing risk-reward tradeoffs & multiple business constraints

12

-mo

nth

incre

me

nta

l pro

fit

pe

r a

ctive

acco

un

t

$7.38

$3.61 $4.06

$10.59

$12.36$11.32

$13.58

$8

$0

$2

$4

$6

$8

$10

$12

$14

$16

A Top 10

North

American

Bank

A Top 5

North

American

Bank

A Top 5

North

American

Bank

A Top 5 UK

Bank

A Top 5 UK

Bank

A Top 10

North

American

Bank

A Top 10

North

American

Bank

Top 10

Issuer

Average

Top 10 North

American bank

Top 5 North American

bank

Top 5 North American

bank

Top 5 UK bank

Top 5 UK bank

Top 10 North

American bank

Top 10 North

American bank

Top 10 issuer

average

Some Results from CLM Optimization:

Pinpoint not just better, but best

© 2009 Fair Isaac Corporation. 55

Using Basel II Parameters and CCA Competitively

» It was not about mere “compliance”, but the foundation can be used to enhance

» Credit Approval and Analysis Processes

» Portfolio Credit Quality Reporting

» Risk Management Governance

» Capital Allocation and Optimization

» Product Pricing and Development

The material in this presentation is the property of Fair Isaac Corporation, is provided for the recipient only, and shall not be used, reproduced, or disclosed without Fair Isaac Corporation's express consent.

© 2009 Fair Isaac Corporation. 56

Q & A

January, 2010

© 2009 Fair Isaac Corporation. 57

Additional Materials

Basel II

Credit Card Act

Capital Allocation

Building a Risk Management Context

Basel II Analytics

Risk Management

Ask the Right Questions About the CARD Act Impact

How Profitable Will Your Cards Be After the CARD Act?

Build Your Action Plan for the Credit CARD Act

Take These 6 Steps BEFORE New Card Pricing Rules Hit

Contact Rich Salvatto@ 415-491-5187 or [email protected] to

request any of these materials or to discuss your specific needs.

These topics will also be covered at our annual conference

Visit www.fico.com/ficoworld to register

Register now and save $200!

www.fico.com/ficoworld

The material in this presentation is the property of Fair Isaac Corporation, is provided for the recipient only, and shall not be used, reproduced, or disclosed without Fair Isaac Corporation's express consent.

© 2009 Fair Isaac Corporation. 58

THANK YOU

February, 2010