Babyboom All

56

FEATURES: Global Household Product Sales Employee Empowerment Cracking the Retail C.O.D.E. Tune Into Teens: Test Your Teen Aptitude Fall/Winter 2006 CONSUMER Ins ights tod ay for tomorrow’s d ecisions B aby B oom er Segmentation: E ig h t Is E noug h

Transcript of Babyboom All

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 1/56

FEATURES:Global Household Product Sales

Employee Empowerment

Cracking the Retail C.O.D.E.

Tune Into Teens:Test Your TeenAptitude

Fall/Winter 2006

CONSUMER

I n s i g h t s t o d a y f o r t o m o r r o w ’ s d e c i s i o n s

Baby BoomerSegmentation:

Eight Is Enough

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 2/56

Seeing Tomorrow…Today

ConsumerInsight:

In every issue…Volume 8, No. 3

TrendwatchWalk-In Retail Clinics: A Healthy Savings Idea

Publisher ACNielsen

EditorsLaurel Kennedy

Kathy Mancini

Design & LayoutBlue Lemon Design

Editorial BoardJoe BuchererCarolyn CalzavaraMark Chesney Tiffany Graves Todd HaleLaurel KennedyDan LymanKathy Mancini Troy NobleDanell O’Neill

Tom PirovanoLori Tanking

Contributing WritersDoug AndersonResearch & Development ACNielsen Homescan & Spectra

Joe BuchererSegmentation Analytics ACNielsen Homescan & Spectra

Jon BusmanMarketing ACNielsen Homescan & Spectra

Mark ChesneyCommunications

ACNielsen Global ServicesRussell EvansBusiness Technology Solutions ACNielsen

Todd Hale Thought Leadership ACNielsen Homescan & Spectra

Laurel KennedyMarketing Strategy Age Lessons

Jane PerrinCommunications ACNielsen Global Services

Tom Pirovano

Retailing Insights ACNielsen

Bill RouseWal-Mart Analytics ACNielsen Homescan & Spectra

Copyright © 2006 ACNielsen. Printed in USA. All rights reserved. ACNielsen, ACNielsen with

globe design, ACNielsen Answers, Homescan, LabelTrends and Scantrack are trademarks or

registered trademarks of ACNielsen (US), Inc. Spectra and Consumer Trade Areas are trade-

marks or registered trademarks of Spectra Marketing Systems, Inc. Other brand, product or

service names are trademarks or registered trademarks of their respective companies.

For More Information

ACNielsen U.S.

150 North Martingale Road

Schaumburg, IL 60173

800.988.4ACN

www.acnielsen.com/ci

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 3/56

contents

4

On the Cover:Baby Boomer

Segmentation

28

20

12

4 Baby Boomer Segmentation: Eight is Enough

Given its relative size and influence on U.S. consumer markets,

surprisingly little formal, quantitative segmentation work has been

conducted on Baby Boomers. The question remains: how to right-size

the huge Boomer cohort? How many segments would capture the

important often subtle nuances that can spell the difference between a

successful new product launch or marketing campaign and a complete

misfire? Turns out, eight segments is enough.

12 Global Household Product Sales:

Innovative Items Clean Up

Analyzing household products on a global scale involves a pretty big

bucket of categories and countries. What’s Hot Around the Globe—

Insights on Growth in Household Products, one in a series of ACNielsen

reports on the fastest-growing products and category drivers, encom-

passes 66 markets and 29 household product areas.

20 Tune Into Teens: Test Your Teen Aptitude

Teens are a moving target. They were born and raised during a digitized

age where change happens rapidly. Born into the MTV generation wherethe rally cry was “I want my MTV”, they have learned that what they want,

they get. In their world, everything is immediate. From instant messaging

to microwave meals, instant gratification is their mantra.

28 Employee Empowerment:

The Key to Capturing Productivity

Ask any successful salesperson, and they’ll tell you that timely, accurate

information represents the best armor they’ve got in the profit wars.

The bulletproof concept resonates with every salesperson who has

ever had to sell-in a new product, argue a price increase or stave off a

competitive threat. To be effective in today’s hyper-charged, customized,

store-level–focused retail environment, salespeople need a virtual arsenal

of presentations capable of being refreshed with current data at the

touch of a button.

34 Gas Price Hikes Put Brakes on Spending

Crude oil prices ignited again this summer, surpassing the $70 a barrel

threshold and pushing prices at the pump to an inflammatory $3+ per

gallon. Factors like market speculation, refinery capacity shortages and

a pronounced decline in spare global oil production converged, leaving

cash-strapped consumers scrambling to adjust budgets and spending

accordingly.

42 Cracking the Retail C.O.D.E.

Winning at retail is enabled by applying a simple, systematic four-step

process that we call “Cracking the Retail C.O.D.E.” The methodology

employs a series of critical steps to optimize brand or product success

in the marketplace. This consumer-centric approach links actions in thestore—where they matter the most—back to the consumers most likely

to purchase your brand.

50 Trendwatch—Walk-In Retail Clinics:

A Healthy Savings Idea

“Would you like some chicken soup with that prescription?” While grocery

stores have always stocked this form of “liquid penicillin”, today they’re

home to the real deal—walk-in clinics staffed by nurse practitioners

licensed to diagnose and treat common conditions such as allergies,

bladder infections, bronchitis, ear infections, the flu, heartburn, muscle

pain, pink eye, minor burns and rashes.

Global

Household

Product Sales:

Innovative Items

Clean Up

Tune Into Teens: TestYour Teen Aptitude

Gas Price HikesPut Brakes onSpending

EmployeeEmpowerment:The Key toCapturingProductivity

34

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 4/562 Fall/Winter 2006

OverviewACNielsen recently completed the 15th edition of its annual

Trade Promotion Practices Study which has traced industry

promotion budget and allocation trends on the manufacturer

side for 15 years, and corresponding retailer practices for nine

years. The longitudinal view of spending habits and preferences

affords unique insights into the ebb and flow of promotional

methods through time, and an enlightened look at the similari-

ties and differences between these trade partners.

Conducted via the Internet, the online survey polled senior sales

and marketing executives from 61 manufacturers and 38 retail-

er organizations. The electronic field work was supplemented

with in-depth telephone interviews to more fully develop areas

of special interest. The Trade Promotion Practices Study has

been distributed to ACNielsen clients and is available for pur-

chase on our website at http://www.acnielsen.com/store.

Benchmarking performance

Perennial favorite topics up for debate include the efficacy of frequent shopper programs and an assessment of which ele-

ments in the category management tool kit (assortment plan-

ning, promotional planning, shelf management, category busi-

ness planning, everyday low pricing, frequent shopper/loyalty

programs, micro-merchandising and micro-marketing) have

gained or lost favor in the calendar year.

A matter of opinionWhile retailers and manufacturers disagreed on any number of

issues ranging from the sufficiency of trade promotion dollars

to the effectiveness of shelf management, there were five areas

of accord. The following topics were identified by both groups

as critical success factors important to their business:

1. understanding consumers

2. new product introductions/implementation

3. category management

4. promotion efficiency/effectiveness

5. variety and assortment

Additionally, each faction identified important subjects specific

to their operations. In the case of retailers, those subjects

included private label activities and customer loyalty/retention

programs. In the case of manufacturers, those subjects included

trade partners, vendor relationships and category management.

Tailoring content

With study input available to guide editorial selections, theFall/Winter issue of Consum er Insight magazine serves up a

number of articles that directly address the top-ranked concerns

of retailers and manufacturers. When it comes to understand-

ing consumers (factor 1), the publication places the two largest

age cohorts in the U.S. squarely in the crosshairs—Baby

Boomers and Millennials.

The article titled “Baby Boomer Segmentation: Eight is

Enough” introduces a robust segmentation model from

ACNielsen Homescan & Spectra, based on the single

most influential determinant of consumer purchase behavior—

household composition, and in particular, presence of

children in the home.

The mantra “it’s all good” describes the teen scene in the article

titled “Tune into Teens” for marketers who take the time to

understand the zeitgeist of Millennials and their propensity for

electronic multi-tasking. While teens may not have the bank

accounts to purchase big ticket items, their influence over

household spending decisions is undeniable.

New product introsOpening a window onto the global new product scene

(factor 2), the article titled “Global Household Product Sales:

Innovative Items Clean Up” analyzes the packaging, ingredient

and social trends that contribute to successful new productuptake. Cleaning products with oxidizing properties swept

the worldwide sales ratings, along with so-called system

approaches to cleaning like the innovative Swiffer line.

C.O.D.E. breakersFor a comprehensive view of consumer-driven micro-

marketing, readers will want to spend time with the ar ticle

titled “Cracking the Retail C.O.D.E.”, which touches on

each of the critical success factors from the Trade Prom otion

Practices Study. Expanded, the acronym C.O.D.E. stands for

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 5/563

1. Consumer Profiling—accurately captures the

demographic profile of the brand’s consumer.

2. Opportunity Gapping—quantifies store-level

opportunities based on consumer demand potential

and diagnoses the prospect.

3. Dynamic Clustering—groups similar stores usingmultiple store a ttributes, including shopper demo-

graphics, the competitive set, and upside opportunity.

4. Executing for the Consumer—takes findings from steps

1–3 and develops store-level tactical plans, giving

the field force the right information to optimize

in-store presence.

Forward-looking insightsWith winter and the annual Consumer and Market Trends

Report release approaching, more than the ambient

temperature is dropping. The VNU Retailer Sentiment

Index (RSI) saw a continuation of the downtrend which

started in January 2005.

Comprising monthly polls of roughly 500 retailers about

current and future economic conditions, the VNU Retailer

Sentiment Index also takes into account indicators such as

store openings, hiring, earnings and general economic trends,

synthesizing the input into a comprehensive view of current

and future conditions.

Traditionally, retailers cited the competitive environment as

their top concern since the inception of the RSI. By mid-

year 2006, for the first time, the overall economy knocked

competition out of the top spot.

Social responsibilityThis year’s Consumer and Market Trends Report exhibits a

decidedly altruistic bent, delivered by two articles. One article

outlines the rise in organic products and the downstream

influence of Wal-Mart’s green commitment on the environment.

The second article discusses how corporate sustainability and

consumer pressure for environmental responsibility is sweeping

through board rooms.

True blueSegueing from the green theme, the Consumer and Market

Trends Report will also cover the subject of true blue customersin a detailed article on the subject of loyalty marketing. The

article walks through a framework for integrating a broad

range of data from loyalty programs and POS numbers, to

demographic profiles, attitudinal studies, share of wallet and

promotional responsiveness to convert regular shoppers into

loyal, high value customers.

Classic updatesNow in its tenth year, the Consumer and Market Trends

Report will include updates on classic measures of industry

performance including channel blurring and category sum-

maries. The channel blurring article investigates the impact

of consolidation on channel dominance and the behavior of

valuable multi-channel shoppers, while the category review

article examines results from the convenience channel.

Pricing it right

Price compression and assortment expansion are two opposingforces that define the fast-moving consumer goods climate of

today. From our custom analytical group comes a detailed

discussion of a repertoire modeling approach for simulating the

impact of a price change on volume, share, revenue and profit.

It’s all about youBy lifting the curtain on this and future Consum er Insight

articles, we hope to have piqued your interest in the publica-

tion, while demonstrating that we practice what we preach.

You are our readers. You are our customers. And our goal is

to provide customer-centric editorial content that addresses

the fundamental needs of your business.

To make sure that we stay on point, you can e-mail our

editor at [email protected] or contact

your client service representative any time to make a

suggestion that will improve our core product set or

thought leadership publications. We’re listening. C i

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 6/564 Fall/Winter 2006

Baby Boomer

Segmentation:Eight Is Enough

“The most important thing to remember about Boomers is

that they are rule breakers. Individuality over conformity is

a consistent Boomer pattern. They always have done it

differently than the way it was done before, and as they

get older, they will continue to demand products that fittheir individuality.”

– From Rocking The Ages:

The Yankelovich Report on Generational Marketing

by J. Walker Smith & Ann Clurman

Given its relative size and influence on U.S. consumer mar-

kets, surpr isingly little formal, quan titative segmentat ion

work has been conducted on Baby Boomers. The question

remains: how to right-size the huge Boomer cohort? How

many segments would capture the important, often subtle,

nuances that can spell the difference between a successful

new product launch or marketing campaign and a complete

misfire? Turns out, eight segments is enough.

Often, when shaping products or programs for Boomers,

marketers have viewed this generation as a single, monolithic

entity with lockstep needs and purchasing patterns. Akin to

a “big gulp” theory, this framework poured every Boomer

into one purchasing pool of interchangeable consumers.That theory just doesn’t hold water.

At best, marketers acknowledged the sweeping 19-year age

span of 1946–1964, and using a little rough justice, split the

segment in half or thirds, addressing campaigns to older or

younger Boomers. In this generational approach, age serves

as an overly simplistic proxy for the correct measure—

household composition.

Under the generations method, rather than directly measuring

the elements of household composition, observed differencesin purchasing behavior are wrongly attributed to some

underlying, shared social/political/cultural touchpo ints.

That theory is out of touch with marketplace realities.

■ See chart 1.

by: Doug Anderson

Research & DevelopmentACNielsen Homescan & Spectra

Laurel KennedyMarketing Strategy

Age Lessons

Chart 1: Finding the years of the Baby Boom is pretty easy…

A n n u a l B i r t h R a t e o f t h e U n i t e d S t a t e s

35

30

25

20

15

10

1 9 0 0

1 9 1 4

1 9 2 0

1 9 2 6

1 9 3 2

1 9 3 8

1 9 4 4

1 9 5 0

1 9 5 6

1 9 6 2

1 9 6 8

1 9 7 4

1 9 8 0

1 9 8 6

1 9 9 2

1 9 9 8

Small cohort of youngpost war adults

+

Higher incomes and aprosperous economy

Higher consumption—especially housing, autos,

homes and appliances

&Lots of children

=

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 7/56

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 8/566 Fall/Winter 2006

Simply put, there is no shared cultural milieu that resonates

with all Baby Boomers. Many age cohort members were nei-

ther born in the United States, nor grew up here, leaving the

shared culture concept significantly d iluted.

Size mattersWhen people hear the term Baby Boom generation, the first

thing that comes to mind is its massive size. The second

thing is its unabated appetite for conspicuous consumption.

Boomers have been tagged with superlatives since birth,

re-shaping American culture and institutions to reflect their

unique zeitgeist. Today, this age cohort is defined as follows:

• The biggest age band in history, numbering some 77

million persons

• The highest earners, with a median household income of

$54,170; 55% greater than post-Boomers and 61% more

than pre-Boomers

• The best educated of any group before it, with 28.5%

holding a bachelor’s degree or higher and 45 million

boasting some college

• The most influential investing group, with 40% of the

U.S. population age 50+ controlling 75% of financial assets

• The deepest pockets, responsible for more than half of all

consumer spending

• The preferred safe harbor for returning college grads (2/3

support an adu lt child) and their aging parents (25% live

with a parent)

• The largest homeowner group; 80% of Boomers vs. 69%

of the general population own a home; 25% own a t least

one property in addition to their primary residence

according to the National Association of Realtors.

More alike than differentWhile neither the one- nor the two-tier segmentation

approach is accurate, it’s easy to understand how this

convention emerged. As a group, Baby Boomer households

exhibit the least behaviorally differentiated purchasing

patterns of any generation. Th is apparent behavioral

flatness is due to the fact that there is often more behavioral

variation between different groups of Boomers than between

Boomers overall and the pre- and post-Boom populations

which bracket them.

Any segmentation structure assumes that there are behav-

ioral or other key differences within the group to be seg-

mented. As behaviorists, we believe that segments generated

should show differences in real, measurable consumer

behavior. In the case of Boomers, much of the intra-genera-

tional variation observed has more to do with household

composition, and less to do with membership in simplistic,

age-based cohorts.

Slicing the pieThe overriding factor dictating Boomer consumer segments

proved to be the presence of children in the home. In 2000,

65% of elementary and high school students had Baby

Boomer parents, and high school enrollments reached their

highest level since 1979. Nearly one in five school-age

children had at least one foreign-born parent, and their

ethnicity reflects the diversity of the Boomer band: 63%

non-Hispanic White, 16% African-American, 15%

Hispanic and 4% Asian.

A detailed ACN ielsen Homescan & Spectra analysis of Baby

Boomer households revealed eight discrete segments that

clustered into two broad groups: the four Boomer segments

with children under 18 represented 39.7% of the cohort,

while the four without children accounted for 60 .3% of

Boomer households. ■ See chart 2.

Chart 2: Percent of Baby Boomer households

by the behavioral consumer segments

SingleBoomers

Kids <18

New FamilyFrontiers

Ready toLaunch

No Kids

Late BloomingBoomers

Trailing EdgeFamilies

Leading EdgeFamilies

Leading EdgeCouples

Trailing EdgeCouples

11.35.1

15.5

9.8

9.322.1

15.5

11.5

Source: ACNielsen Homescan & Spectra

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 9/567

Kid stuffMarketing to the Boomer segments with children is anything

but child’s play. It requires an understanding of the nuances

between the four groups. For example, highly educated Late

Blooming Boomers may have made the choice to start fami-

lies later in life or are the by-product of divorce. As a result,

Late Blooming Boomers have smaller, younger families com-

prising one to two children under the age of 12. A single

parent heads fully one-third of Late Blooming households,

which also index above average for African-American and

Asian ethnicities, but below average for Hispanics.

Late Blooming heads of household span the entire Baby

Boomer age group. Since education correlates strongly with

income, any attempt to divide Boomers on the basis of age

alone would clearly miss the mark here, and leave out a

significant number of a ffluent Lat e Blooming households.

■ See chart 3.

Trailing Edge Families comprise larger, stable households

of 4+ persons who have lived at the same address for more

than five years. Unlike Late Blooming Boomers, Trailing

Edge heads of household fall into a narrow age parameter,

sharing a birth date between the years 1958 and 1964.

Averaging 2.5 children per household, they have far fewer

(less than half as many) adult children than Leading Edge

families, which appears to be a direct function of

parental age.

The least educated of any Boomer group, Trailing Edgers

are even less educated than the post-Baby Boom cohort.

Another note of internal segment consistency demarcating

Trailing Edgers is the above average concentration of

Hispanics populating the group, the most of any Boomer

sub-segment.

Older, not necessarily wiser, kidsLeading Edge Families feature older parents born between

1946 and 1957, large households averaging 2.4 children,

with approximately one “adult child” for every four chil-dren under age 18. As one might expect from the doting

parents who pioneered those ubiquitous baby-on-board

signs, the apron strings are proving hard to cut—or perhaps

just more elastic—as young adult children bounce back to

the security of home.

The purse strings to Junior are even harder to untie. As a

consequence, Boomer offspring are returning to the nest

after college in record numbers, or remaining at home while

getting their start in the working world. According to 2000

U.S. Census figures, 56% of men and 43% of women in the

18–24 age bracket reside with a parent, and 65% of recent

college grads enjoy the largesse of Mom & Dad’s hospitality.

While better educated than pre-and post-Boomers, Leading

Edge Families fall into the lower tier of academic accom-

plishment compared with other Boomer segments. After

Trailing Edge Families, Leading Edge Families are the most

Hispanic-dominant of any Boomer group and far and away

the “most married.” Seven in ten Leading Edge Family

households are headed by married couples.

Chart 3: Segmenting Baby Boomer households with

children less than 18

YoungerChildren

< 12 Only

OlderChildren

12 +

Trailing EdgeHOH

Age 42–48

Leading EdgeHOH

Age 49–60

Smaller FamiliesSize 2–3

Larger FamiliesSize 4+

Total BabyBoomer HHswith Children

Late BloomingBoomers

Ready toLaunch

Trailing EdgeFamilies

Leading EdgeFamilies

Source: ACNielsen Homescan & Spectra

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 10/568 Fall/Winter 2006

Working

RetirementsWork long and prosper. That’s the new mantra of the Boomer

generation as it edges toward Social Security eligibility and

retirement age. So hold on to those gold watches, because the

Boomers plan on retiring the traditional concept of retirement

with a characteristically bold move that will surprise detractors

and benefit—rather than hijack—the economic future of the

generations that follow.

The idea is simplicity itself: keep on working, earning and

contributing to the economy for as long as one is able and

enabled. Driven by a host of motivations ranging from self-

actualization to financial need, many Boomers reject the idea of

a leisurely retirement and plan to work well into their 70s and

beyond. In a 2006 Merrill Lynch study, 71% of adults envision

working in retirement, and half of those said they intended to

work as long as they were physically and intellectually able.

Companies need the workersWhile the statistics vary dramatically (estimates of a labor short-

age as early as 2010 range from 800,000 workers to almost

10 million), the inescapable fact remains that the “baby bust”

generation numbers 11 million fewer bodies than the Boomers.

Even with productivity gains, process changes, outsourcing

options and immigration inflows, there simply may not be

enough workers to fill available jobs. The obvious solution:

retain the ones you’ve got.

Progressive employers are experimenting with any number of

riffs on the traditional consulting contracts or part-time posi-

tions available to retired employees. Among the more innova-

tive working retirement ideas:

• capability-specific personnel banks of skilled temporaryworkers;

• roadblocking schedules, where retirees rotate between timeon/off the job for a pre-determined time increment (e.g.,three months on/off);

• job sharing, reviving what Boomer women elevated to an artform; two individuals sharing a job, salary and performanceexpectations;

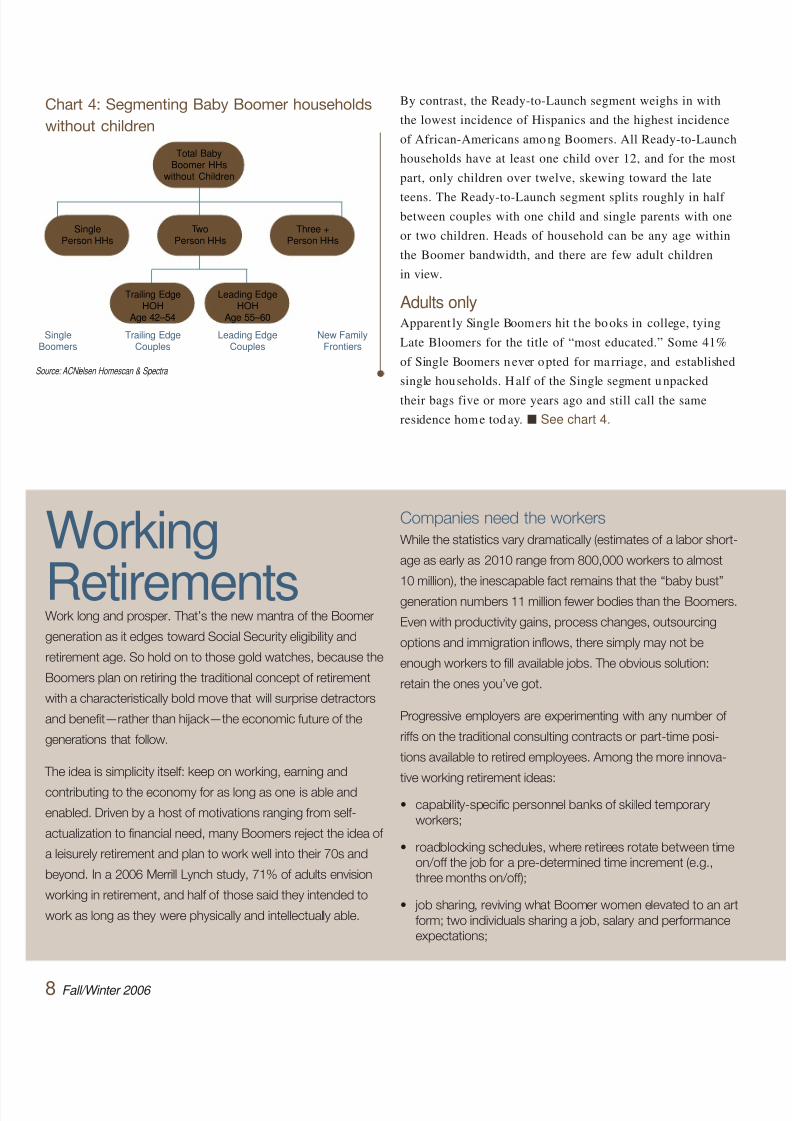

By contrast, the Ready-to-Launch segment weighs in with

the lowest incidence of Hispanics and the highest incidence

of African-Americans among Boomers. All Ready-to-Launch

households have at least one child over 12, and for the most

part, only children over twelve, skewing toward the late

teens. The Ready-to-Launch segment splits roughly in half between couples with one child and single parents with one

or two children. Heads of household can be any age within

the Boomer bandwidth, and there are few adult children

in view.

Adults onlyApparent ly Single Boomers hit the books in college, tying

Late Bloomers for the title of “most educated.” Some 41%

of Single Boomers never opted for marriage, and established

single households. Half of the Single segment unpacked

their bags five or more years ago and still call the same

residence home today. ■ See chart 4.

Chart 4: Segmenting Baby Boomer households

without children

Trailing EdgeHOH

Age 42–54

Leading EdgeHOH

Age 55–60

SinglePerson HHs

TwoPerson HHs

Three +Person HHs

Total BabyBoomer HHs

without Children

SingleBoomers

Trailing EdgeCouples

Leading EdgeCouples

New FamilyFrontiers

Source: ACNielsen Homescan & Spectra

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 11/569

• seasonal positions that follow employees who split timebetween two geographical locations (e.g., New York andFlorida);

• sampling arrangements that enable a worker to move

across departments for a new challenge.

Boomers need the moneyIt’s a good thing that Boomers say they want to work, because

it’s clear that many will have to work for financial reasons. One

factor that impacted even diligent savers was the stock market

decline of 2001–2003 that eradicated roughly $7–8 trillion in

shareholder wealth, much of it held by Boomers.

In the process, the dot-com crash ate away some $279 billion

in 401(k) assets and huge chunks of other retirement savings.Boomers dialed-in to the nuances of finance recognize that

401(k) and IRA/retirement money statements can create a false

sense of wealth, since these amounts will be federally taxed on

withdrawal (with the exception of Roth IRAs).

Everybody winsWorking Boomer retirees will have more discretionary income

to continue fueling the economic engine, less need to draw

down savings and liquidate investments, and can readily fill the

emerging labor gap by staying employed. Meaningful employ-

ment enables critical knowledge transfer from highly skilled

Boomers to other workers, and keeps older employees men-

tally and physically engaged.

At the same time, employers access a labor pool of proven

workers with the flexibility to calibrate hours to match demand.

In a Center for Retirement Research survey, older workers

earned consistently higher marks than younger counterparts

from employers for their “knowledge of procedures and other

job aspects” and “ability to interact with customers”. Overall,

older workers were seen as more productive based on their

accumulated institutional knowledge and efficient work habits.

Retailers like CVS Pharmacy, Home Depot and Borders have

already tapped the retiree talent vein with outstanding results.

When it comes to the workplace, some things apparently do

get better with age.

Trailing Edge Couples carved their own path on the matri-

monial front, and report the highest rate of unmarried

partners living together. Trailing Edge Couples typically

are headed by a person born in the 1952–1964 period,

who have occupied the same house for the past five years,

find themselves situated in the bottom Boomer tier on theeducation dimension, and have fewer than expected

Hispanic and African-American members.

The social vanguardLeading Edge Couples, with a head of household born

between 1946 and 1951, represent the first group of the

Boomer generation to serve as social change agents. One

of the top three best-educated Boomer segments, Leading

Edge Couples exhibit just half the unmarried rate of Trailing

Edge Couples and two-thirds have shared a residence for

five or more years. Less ethnically diverse than o ther

Boomer strata, Leading Edge Couples report a low incidence

of Hispanics and the lowest African-American incidence of

all Boomer groups.

One of the most interesting segments to emerge from the

Boomer study was the New Family Frontiers faction, char-

acterized by three or more adults sharing a household. The

typical New Family Frontiers household encompasses 1.1

children between the ages of 18 and 24, with 40% claiming

another resident relative such as a parent (1/3 of such family

units) or adult siblings.

From an economic perspective, it is worthwhile to note that

54% of New Family Front iers households have three or

more employed workers in the home. Among the highest

earning households, New Family Frontiers do a pretty

good job of hanging on t o wha t they make, second onlyto Leading Edge Couples on the savings front.

■ See chart 5 on page 10.

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 12/56

Gray mattersThe shift towards adult-only households will continue as

Boomers age. By 2007, fewer than 30% of Boomer house-

holds will have children under 18 at home. By 2010, that

number will have declined again to just 20% . By 2014,

fewer than 10% of all Boomer households will include

children under 18 . Americans are getting older, living

longer and having fewer children.

An 85+ population growing eight times faster than the

country as a whole will throw a new wrinkle into long-

standing assumptions which form the underpinnings of

social services programs. In 1995, Federal spending per

child under 18 years of age was $1,693 per child. For the

same period, per capita spending on each 65+ adult was

$15,636. The combined effect of population t rends and

federal spending patterns results in a double whammy—fewer wage earners paying into a system serving an

exploding population base.

Golden, global concernsNot only is the U.S. population aging, the very old compo-

nent is growing at an even faster rate. In 2000, there were

approximately 72,000 centenarians in the U.S. By 2050,

using mid-range Census Bureau estimates, that number will

increase fourt een-fold, exceeding 834,000. To get a relative

sense of size, it would take a city as large as Detroit to

house all the people older than 100 at the mid-century point.

Concerns about aging are not confined within the bo rders

of the United States. Worldwide, the current ratio between

the young (under 20) and the old (over 65) is roughly 3:1.By 2050, that ratio will recalibrate to equilibrium at 1:1.

At that point, older people will outnumber younger ones

for the first time in recorded history.

Spending shiftsConsumption and spending patterns mirror changes in the

Boomer demographic. Food away from home eats up a

larger share of Boomer budgets when the need to stage a

nightly family dinner with the kids goes away. Beer and

wine top off the shopping list for those Boomers furthest

from child-rearing responsibilities. Alcoholic beverage mar-

keters can expect to tap into this bottled-up demand in the

future as consumption levels are expected to maintain even

as Boomers age.

When it comes to home improvements, Boomers gravitate

toward household textiles and furniture, outspending other

segments. Staying connected to friends and families is a

10 Fall/Winter 2006

Chart 5: New family configurations have new numbers of workers

P e r c e n t o f H

H s

100

80

60

40

20

0

No Workers One Worker Two Workers Three or More Workers

P o s t B

a b y B

o o m

L a t e B

l o o m i n

g B o o

m e r s

T r a i l i n

g E d g

e F a m

i l i e s

L e a d i n

g E d g

e F a m i l i e

s

R e a d y t o

L a u n c h

S i n g l e

B o o m

e r s

T r a i l i n

g E d g

e C o u

p l e s

L e a d i n g

E d g e

C o u p l e s

N e w F a

m i l y F

r o n t i e

r s

P r e B a b y

B o o m

Source: ACNielsen Homescan & Spectra

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 13/5611

Boomer imperat ive, accounting for their 50% higher spend-

ing rate on cellular phones and pagers. Plugged in to elec-

tronic entertainment media, Boomer spending rates outpacethe average for audio equipment, televisions and radios.

The Boomer obsession with health and wellness extends to

their extended family—including the four-footed, finned and

winged members. Boomers willingly open their wa llets for

veterinary care and other pet services such as grooming and

doggie day care.

Family financesThe Boomer relationship with money is complicated and

convoluted. Shaped by parental stories of the Depressionand WWII deprivation, Boomers learned to respect money,

save money, value work over leisure and savings over debt.

They look askance at credit issuers who mail out unsolicited

cards to college students, in the hopes they’ll be used. All

in all, one could say Boomers are a fiscally conservative

bunch—except when it comes to their kids.

It is not uncommon to find a Boomer parent liquidating

retirement savings or mortgaging their home to subsidize

their child’s college tuition. Despite years of denying them-

selves luxuries, they will indulge an offspring’s demands for

a car, expensive vacation or the latest and greatest in con-

sumer electronics.

A perfect stormThe graying of America presents a number of questions such

as the prospective impact of impending retirements on:

1. financial markets, as Boomers prepare to liquidate equity

holdings and supplement retirement savings;

2. real estate markets, as Boomers prepare to trade down

from large homes—a flurry of sales may add momentum

to the imploding housing market;

3. employment issues, as Boomers exit the workplace and

the baby bust generation comes up 11 million people

short of available openings;

4. consumer spending, as Boomers retire or are forced into

second careers, part-time or lower paying positions;

5. healthcare system, as Boomers begin to experience the

inevitable decline of physical vigor and the onset of

chronic illnesses like high blood pressure and diabetes.

An uncertain outcomeSome pundits ponder these issues and see the makings of

a perfect storm capable of capsizing the U.S. economy.

Others see the opportunity to extend the consumer use-life

by extending the Boomer work-life from an arbitrary retire-

ment at age 65, to an open-ended employment contract that

keeps people working, and earning, for as long as they are

physically able. ■ See sidebar on “Working Retirements”

on pages 8 and 9.

Society has never been asked t o solve a socioeconomic equa-

tion with so many unknown variables before. There simply

have never been so many old people, living so long and

staying so healthy.

From a marketing perspective, one thing is certain. Older

Boomers represent both a viable market and one too large

to ignore. C i

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 14/5612 Fall/Winter 2006

by: Jane PerrinCommunications

ACNielsen Global Services

Mark Chesney

CommunicationsACNielsen Global Services

Global Household

Product Sales:Innovative Items Clean Up

Analyzing household products on a global scale involves a

pretty big bucket of categories and countries. W hat’s Hot

Around the Globe: Insights on G rowth in Household

Products, one in a series of ACNielsen reports on the

fastest-growing products and category drivers, encompasses66 markets and 29 household product areas.

Findings surfaced by the study identified four major trends

responsible for growth: new product innovation, health and

wellness concerns, convenient delivery systems and develop-

ing country contributions. Aggregated 2005 sales growth

remained consistent with other reports in the series covering

food and beverages and personal care products, showing

4% growth.

Regional resultsOn an upbeat note, there were several regional pockets of

double-digit growth. Emerging markets posted a 13%

increase and Lat in America an 11% jump in household

product sales, leading Asia Pacific, North America andEurope results. Romania and Russia, both classified as

emerging markets, reported impressive category expansion

rates of 25%. ■ See chart 1.

The complexity of dissecting regional and country contribu-

tions is illustrated by Asia Pacific, a sector comprising both

emerging and developed markets, where the modest 4%

gain in Japan blended with the momentum of a 14% jump

in China. Turning from percentages to the absolute dollar

metric, Asia Pacific achieved the largest dollar value growth

overall at just under $U.S. 1 billion in 2005.

Chart 1: Global findings

Global (66)

Europe (19)

North America (2)

Asia Pacific (15)

Latin America (12)

Emerging Markets (18)

4%

0%

3%

6%

11%

13%

Global (66)

Europe (19)

North America (2)

Asia Pacific (15)

Latin America (12)

Emerging Markets (18)

15%10%5%0%

Value Sales (U.S.$M) inHousehold Products*

Global Growth inHousehold Products* (2004–2005)

0 $50,000 $100,000

*Based on number of countries measured (Number of countries in parentheses)

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 15/56

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 16/5614 Fall/Winter 2006

Leading categoriesAmong the 29 categories studied, only nine grew faster than

the global average, five paced the 4% rate; and t he rest

lagged behind. In prior studies, the fastest-growing categories

were also among the smallest in dollar sales. That was not

the case in 2005. Five categories in the fastest-growing top

nine—garbage bags, household cleaners, air fresheners,

insect control and fabric softener—also registered among

the top 10 categories in value sales. ■ See chart 2.

The remaining top performers included abrasive cleaning

pads, which shared top b illing with disinfectants at 13% ,

laundr y stain removers/boosters at 6% and plastic storage

bags at 5% .

Performance enhancersOn closer examination, specific sub-segments accounted for

the strong overall showing in some categories. For example,

battery-operated freshening systems powered up a 191%

sales increase, and air sanitizing sprays vaporized the

category with their supercharged growth in sales of 36% .

Similarly, the power cleaning sub-segment o f household

cleaners (75% ) and those products with oxidizing ingredi-

ents for stain removal (11% ) wiped up the rest of the category.

The cleaning system concept debuted by Swiffer, comprising

a re-useable element such as a handle with disposable

cloths, sponges or brushes, has been syndicated to other cat-

egories including bathroom cleaners, toilet bowl cleaners,

dusters, air care and insect control. The jury is still out on

whether or no t the consumer uptake on systems and one-

step, multi-use products will successfully cross category

boundaries.

Worthy of considerationConsumer health concerns gave a shot in the arm to house-

hold cleaner and disinfectant category results. Both recorded

higher than average growth rates, which may indicate a shift

in the type of products used to clean around the world.

While the discussion to date has surrounded growth rates, it

is worthwhile to note that even though laundry detergent

only expanded at the average pace, it represents the largest

category overall and contributed more than any other cate-

gory to global growth.

EuropeTotal Household Care (0%)

Brooms, Brushes, Mops (10%)

Disinfectants (3%)

Household Cleaners (3%)

Laundry Stain Remover (3%)

Garbage Bags (3%)

Auto Dish Detergent (2%)

Auto Dish Additives (2%)

Plastic Storage Bags (2%)

Batteries (2%)

Waste Pipe Openers (2%)

North AmericaTotal Household Care (3%)

Disinfectants (23%)

Laundry Stain Remover (12%)

Garbage Bags (12%)

Abrasive Cleaning Pads (7%)

Toilet Care (7%)

Kitchen Paper/Towel (7%)

Air Fresheners (5%)

Plastic Storage Bags (5%)

Household Cleaners (5%)

Aluminum Foil (4%)

Asia PacificTotal Household Care (6%)

Auto Dish Detergent (17%)

Auto Dish Additives (16%)

Abrasive Cleaning Pads (14 %)

Fabric Fresheners (10%)

Air Fresheners (10%)

Plastic Storage Bags (9%)

Fabric Softener (9%)

Batteries (8%)

Garbage Bags (8%)

Brooms, Brushes, Mops (8%)

Latin AmericaTotal Household Care (11%)

Abrasive Cleaning Pads (74%)

Laundry Stain Remover (36%)

Air Fresheners (16%)

Bleach/Ammonia (15%)

Plastic Storage Bags (14%)

Fabric Softener (14%)

Insect Control (13%)

Aluminum Foil (13%)

Toilet Care (12%)

Household Cleaners (11%)

Emerging MarketsTotal Household Care (13%)

Fabric Fresheners (277%)

Carpet/Rug Cleaner (37%)

Waste Pipe Openers (37%)

Air Fresheners (23%)

Laundry Water Softeners (21%)

Auto Dish Detergent (20%)

Cleaning Cloths/Sponges (19%)

Household Cleaners (17%)

Fabric Softener (16%)

Laundry Stain Remover (16%)

Chart 2: Only nine categories grew

faster than 4%Top No. of Markets Category CategoryGrowing Growing/ Growth Rate Growth Value

Categories Measured 04–05 $000

1. Abrasive Cleaning Pads 13 of 23 13% 129,2 15

2. Disinfectants 18 of 26 13% 81,1 483. Garbage Bags* 15 of 19 8% 209 ,806

4. Laundry Stain Remover/Booster 30 of 37 6% 82,87 6

5. Household Cleaners* 55 of 65 6% 338 ,553

6. Air Fresheners* 50 of 61 5% 244 ,081

7. Insect Control* 28 of 47 5% 168 ,489

8. Plastic Storage Bags 28 of 34 5% 78,04 0

9. Fabric Softener* 44 of 58 5% 255 ,008

*Also among the largest 10 categories in value sales

Chart 3: Top 10 categories and growth rate by region

continued on page 16

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 17/56

Stepping Outside Your

Own Borders?

Use the right marketing information tomake your expansion decisions.

Contact ACNielsen Global Services at 847-605-5904.

Global Services

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 18/5616 Fall/Winter 2006

Different strokesThe t op ten categories within each region d iffer significantly,

and none of the overall fastest-growing products shows up

in every regional ranking. In Europe, only the leading cate-

gory— brooms, brushes and mops—charted 2005 results

that bettered the global average. ■ See chart 3, page 14.

In North America, disinfectants killed off any competition

in the top ten with a 23% annual growth rate. Only the

laundry stain remover and garbage bag categories also posted

double digit regional growth at 12% .

Automatic dish detergents and automatic dish additives

floated to the top of the Asia Pacific top ten list. In Latin

America, every top ten contender boasted double-digit

growth, but abrasive cleaning pad results scoured all comers

with a whopping 74% . Laundry stain removers were a

distant second in the line-up at 36% .

The Emerging M arkets’ winning entr y, fabric fresheners,

was in a class by itself with a 277% annual growth rate.

Carpet/rug cleaners and waste pipe openers trailed with

strong 37% increases.

Coming cleanAbrasive cleaning pads, the runaway category growth winner

in Latin America, owes its phenomenal success to a single

country: Brazil. This one country accounted for more

than 95% of category sales, divided among three brands.

Aggressive media suppor t generated a 45% increase for the

leading brand, with the number two and three brands each

expanding by more than 200% .

Global brand dominance was more diffused than in Latin

America, with the top th ree brands comprising 65% of

category sales and private label brands absorbing an addi-

tional 16% .

Hygienic habitsGerm-aphobic Americans kicked their cleaning standards

up a notch, striving for a sanitized—versus merely clean—

household. This microbe-free goal resulted in a 23% regional

category sales increase. As always, convenience played into

consumer decision-making, explaining why 80% of the

absolute dollar growth in U.S. sales (excluding Wal-Mart)

derived from a 60% increase in wipes.

Disinfectant wipes, measured in only five markets, mopped

up consumer dollars on a global basis for a 35% growth in

sales. Their counterpart, disinfectant sprays, expanded at

an average 10% rate in 12 of 19 markets measured. Brand

sales are so heavily concentrated in this category that three

brands accounted for 71% of dollar sales on a globa l basis.

It’s worthy of note that a lthough only 8% of sales can be

ascribed to private label brands, their sales expanded by

26% in 2005.

Tying up salesGarbage bag sales expanded at an 8% annual rate, twice the

global tempo, with North America the sole region to wrap the

year with double digit growth (12% ). For such a seemingly

mundane category, garbage bags represent an endless sourceof innovative benefits from anti-odor attributes to a host of

tying options to stretch-and-flex fabrics that won’t rip.

New features, coupled with raw material cost increases for

the oil-based resins used in manufacturing, combined to

justify the higher reta il prices that raised dollar value sales.

Private label products captured a significant share of

Global Household Product Trends continued from page 14

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 19/5617

garbage bag sales (40% ), almost enveloping the 49% sales

component contributed by the top three brands. Both private

label and branded offerings increased by 8% .

Spotless outcomesBoth t he pre-wash and in-wash products that compose the

laundry stain remover category captured double-digit sales

in three of five regions, with four of five regions ranking

the category among the top ten. Tepid Asia Pacific results

of 1% growth dampened the overall category average.

“Oxi” products cleaned up in the category, spreading in

seven of the 10 markets measured at an 11% overall rate.

No-wash stain removers, including pen delivery systems,

achieved explosive sales of 200% over the pr ior year. Key

manufacturers virtually own the category, with the top three

brands accounting for 72% of sales.

Shipshape resultsConvenient, effective household cleaners were swept off

shelves by tidy consumers, with Emerging Market and

Latin America households setting the pace. The two

attributes dominating product selection were convenience

and effectiveness.

Major multinationals entered the power cleaning competi-

tive fray, where sales velocity reached 75% last year. Spray-

ons earned high marks on the convenience criteria, and at11% represented one of the fastest-growing segments.

Product proliferation served to modulate the trend toward

brand dominance observed in other categories, with the top

three branded household cleaners garnering 43% , pr ivate

label 9% and other products 48% of sales.

Something in the airAir freshener sales caught a favorable updraft in Emerging

Markets, Latin America and Asia Pacific, where 2005 con-

sumption increased by 23% , 16% and 10% , respectively.Recent new product entries have kept sales aloft and in the

top-ten tiers for four of five regions studied.

Battery a ir fresheners, unveiled just last year, saw 2005 sales

rocket into the stratosphere at a 150% rate. Air sanitizers

eliminated odors and obstacles to consumer trial, hitting a

respectable 36% growth number. Air freshener candle sales,

reinvigorated by the introduction of scented oils, achieved

an 8% growth rate, doub le that of the global average.

Abuzz with potentialInsect control, the eighth fastest-growing category, ow ed

its 5% expansion to Latin America, a region where bugs

are more than a nuisance; they carry potentially harmful

diseases such as dengue fever and malaria. Product refine-

ments, such as electrically-powered items, command a price

premium reflected in sales results.

The North American no-growth scenario masks a 7% spike

from Canada, possibly reflecting that country’s concern with

the mosquito-borne West Nile virus. Private Label products

barely show up on the radar screen in the insect control

Chart 4: Private Label growth by categoryPrivate Label Private Label Manufacturer

Product Area Share Growth Growth

1 Aluminum Foil 43% 0% 3%

2 Plastic Storage Bags* 41 % 8% 3%

3 Garbage Bags* 40% 8% 8%

4 Kitchen Paper/Towel 28 % 5% 3%

5 Cleaning Cloths/Sponges 26 % 7% 1%

6 Auto Dish Additives 22% 1% 4%

7 Plastic Wrap 19% 4% -3 %

8 Auto Dish Detergent 18% 4% 4%

9 Bleach/Ammonia 17% 4% 5%

10 Abrasive Cleaning Pads* 16 % 4% 15 %

11 Laundry Water Softeners 16% -18% 6%12 Toilet Care 12% 4% 2%

13 Brooms, Brushes, Mops 11% 18% 1%

14 Fabric Softener* 11% 4% 5%

15 Batteries 10% 3% 2%

16 Hand Dish Detergent 10% 5% 4%

17 Household Cleaners* 9% 5% 6%

18 Disinfectant* 8% 26 % 12%

19 Oven Cleaners 7% 5% -1 %

20 Laundry Starch 7% -16% 0%

21 Carpet/Rug Cleaner 6% 6% -4 %

22 Laundry Detergent 6% 1% 4%

23 Air Fresheners* 6% 1% 6%24 Laundry Stain Remover* 5% 16 % 6%

25 Fabric Fresheners 5% -5% -8 %

26 Furniture Polish 5% 6% -4 %

27 Waste Pipe Openers 4% 13 % 2%

28 Floor Polish/Wax 2% -12% -2 %

29 Insect Control* 2% -4% 5%

*Fastest Growing Categories

Manufacturer brands growing faster than Private Label

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 20/5618 Fall/Winter 2006

About the Study This survey of Household Products included 66 markets around the world and 29 categories. These 66 markets account for

more than 90% of the world’s GDP and over 75% of the world’s population. The markets have been grouped regionally into

five areas: Asia Pacific, Emerging Markets, Europe, Latin America and North America. For the purposes of this study, Mexico

has been included in Latin America.

ACNielsen analyzed data across 29 Household Products categories, comparing year-ending data from December 2005 with

December 2004. Within these 29 categories, ACNielsen reviewed subcategories of products, which for the purposes of this studyare called “segments.” This study looks at some of these key segments to understand the changes impacting the categories.

New to the study this year is the inclusion and analysis of private label products within each category. ACNielsen Global

Services intends to include private label information in future reports on product areas, to show the impact of both manufac-

turer and retailer products as drivers of consumer purchasing behavior.

As with Global Services’ other studies, this report is based on purchasing information from retailers in grocery, drug and mass

merchandise outlets and generally excludes kiosks or vending machines. In a few markets, sales from convenience stores

may be included. Within the United States, data from the ACNielsen Homescan consumer panel service has been included

to provide a total market read that includes Wal-Mart information.

category with a miniscule 2% of sales; the top three brands

and all others split the rest of the category sales evenly at

49% apiece.

In the bagPlastic storage bag sales did slightly better at 5% than the

global all-product average, with pockets of strength in Latin

America (14% ) and Asia Pacific (9% ). Interestingly, pr ivate

label sales for this category (8% ) bested manufacturer brand

performance of 3% . The pr ivate label preference was clearly

strongest in Europe, North America and Emerging Markets,

but picking up in Asia Pacific.

A soft touchNew product formulations, improved distribution, increased

advertising penetration and price reductions contributed to

the fabric softener category sales increases in EmergingMarkets (16% ) and Latin America (14% ). Of note, in

Mexico, products such as Downy Libre Enjuague (Rinse-

Free) reduced the hassle factor for consumers who hand

wash by eliminating the rinse step.

The top th ree brands occupy the number 1, 2 and 3 posi-

tions across the majority of markets studied and together

claim 68% of category sales.

Commodity concernsWhile private label offerings earned a 12% share of global

household product sales, that penetration level underper-

formed the norm reported in the ACNielsen 2005 study,

The Power of Private Label. However, the private label

expansion velocity equaled that of manufacturer branded

household products (4% ), so private label neither gain nor

lost ground in relative terms.

Private label share and growth figures varied widely by cate-

gory, from a 43% share in aluminum foil with zero growth ,

to an 8% share in disinfectants with a 26% growth rate.

Regional considerations such as economic development and

lifestyles influenced product uptake and u tilization figures.

■ See chart 4, page 17.

Home basicsHousehold products weighed in with overall global growth

rates consistent with other fast moving consumer product

areas. There is no denying the influence of Emerging

Mar kets as a factor in household product category growth,

alongside a continuous stream of product innovations that

keep consumers engaged and p rices on the rise. Uniformly,

consumers across the world gravitate to products that deliv-

er against two key benefits: value and convenience. C i

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 21/56

The Beauty Care Panel will help you:

• Identify high opportunity distribution channels and quantify the

sales opportunity of gaining distribution there.

• Identify “white space” in the marketplace and quantify new prod-

uct development opportunities.

• Evaluate new product performance and quantify cannibalization.

• Target high opportunity consumers and monitor your performance

across all channels.

The Beauty Care Panel gives you:

• The most comprehensive measurement of Beauty Care purchase

behavior across all channels in 32 beauty care categories, including:

–Make-up/Color Cosmetics

–Facial Skin Care

–Hand & Body Skin Care

–Self-Tanning

–Bath & Shower

–Men’s & Women’s Fragrance

• The Spectra BehaviorScape™ Framework, which helps you

increase the effectiveness of your marketing dollars.

Identify and Target High OpportunityBeauty Care Consumer Segments

Look at the world of beauty care through the

eyes of a consumer and what do you see? A

world filled with choice. As new products and

efficacy claims proliferate and the retail land-

scape becomes increasingly fragmented, mar-

keters are challenged to find a complete meas-

ure of their brands’ performance and identify

high opportunity consumer segments and new

product opportunities.

ACNielsen’s Beauty Care Panel provides

the most complete, accurate and actionable

view of beauty care consumers across all

categories and channels. From mass-

market to high-end/prestige brands and from

supermarkets to specialty beauty stores, the

Homescan ® Beauty Care Panel provides data

at the most granular level to help you effectively

target consumers and maximize sales opportu-

nities in these channels.

To learn more about the Beauty Care Panel, please contact your ACNielsen Client Service or Retail Services representative

or visit our web site at www.acnielsen.com.

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 22/56

Tune Into Teens:Test Your Teen Aptitude

If you’ve never visited YouTube.com, listened to Gnarls

Barkley or used the acronym ROTFL while instant messag-

ing, then find yourself a teenager and get educated. Today’s

younger generation , typically called M illennials (born

between 1980 and 2000), represent a group of well-connected, over-stimulated, media-savvy consumers who

are open-minded, optimistic and well-educated. They

represent the future. Tune in to what drives this very diverse

group of consumers and you will not only score points on

the “uber-cool” chart, but will also deliver messaging that

resonates with the world they live in.

Test your teen aptitudeIf you are thinking that teens do as teens did, then think

again. While it is true that all teens go through the same

growing pains, history tells us that each generation leavesbehind its own distinctive mark (see U.S. Teens Through

the Decades on page 24). To test your knowledge of today’s

teen market, see if you can answer the following questions:

1. Who is one of the lead singers for the Black Eyed Peas?

2. Who said, “Don’t be jealous that I’ve been chatting

online with babes all day”?

3. Who hosted MTV’s 2006 Video Music Awards?

4. What is an emoticon?5. Who is known for the phrase, “That’s Hot”?

6. What is the starting price for a Tracfone?

7. Billie Joe Armstrong is the lead singer of which band?

8. What is Naruto?

9. Who is Shiloh?

10.Who are two ma in characters on “Degrassi the N ext

Generation”?

So how did you do? If you were able to answer 8 out of

the 10 questions, then you are either: a) the parent of a

teenager, b) an actual teenager, c) a teenager wannabe, or

d) a superbly in-sync teen marketer. However, if you are

like most of us and had some trouble, then it is time tobrush up your knowledge of this influential and lucrative

market segment.

A moving targetTeens are a moving target. They were born and raised during

a digitized age where change happens rapidly. Born into the

MTV generation where the rally cry was “I want my MTV”,

they have learned that what they want, they get. In their

world, everything is immediate. From instant messaging to

microwave meals, instant gratification is their mantra.

Millennials are the first generation of true multi-taskers,

easily balancing e-mail, text messaging, music downloads,

homework and a strict schedule of sporting and other

activities, simultaneously. Th is generation is more adept at

communications than any of its predecessors. The wireless

Internet is their central nervous system, and simply put, they

just don’t need much else.

If they’re that connected, then connecting with teens should

be simple, right? Not necessarily. While it may seem easy to

develop a systematic marketing plan (if teens = computers,then website advertising = success), connecting in t he right

places at the right time to the right audience is a challenge

at best.

20 Fall/Winter 2006

by: Tom PirovanoRetailing Insights

ACNielsen

A n s w e r s : 1 . W i l l . I . A m o r F e r g i e ; 2 . K i p D y n a m i t e ; 3 . J a c k B l a c k ; 4 . E m o t i o n I c o n = ) m a d e u s i n g p u n c t u a t i o n o r t y p e ; 5 . P a r i s H i l t o n ; 6 . $ 2 9 . 9 9 ; 7 . G r e e n D a y ; 8 . J a p a n e s e a n i m e s e r i e s ; 9 . D a u g h t e r o f B r a d P i t t a n d A n g e l i n a J o l i e ; 1 0 . E m m a N e l s o n , J i m m y B r o o k s .

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 23/56

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 24/56

Equally differentAll teens are not alike, and grouping them together could be

a roadmap for disaster. Take, for example, a typical eighth

grader compared with a college student. While Disney’s

“High School Musical” is all the rage for one, the other is

much more engaged by the latest drama on MTV’s “The

Real World.”

And don’t discount the hugely important gender differences.

Anybody with kids knows how different boys are from girls.

Therefore, when analyzing teens, boys and girls need to be

viewed separately. For example, girls believe that they are

more grown-up than boys, and spend their money on very

different things, such as jewelry and clothing, while boys’

interests trend toward games and electronics. However, both

spend money on music and movies, which increases as kids

shift from the 12–14 age bracket to the 15–17 one.

It is also important to realize that “what’s hot” can be

polarizing, because for each teen fad with adoring fans,

there is a subset of teens who simply hate it. Finding a teen

idol as a spokesperson for a brand could divide an audience.

For each loyal fan of Justin Timberlake, there is another

teen who simply abhors h im. Interestingly, th is love/hate

relationship seems to be more common with the “beautiful

people” than with stars like John Heder or Jack Black, who

garner more universal appeal.

Stay ahead of the curveFor the most part, young people take their cues from those

a few years older than themselves for trends. This may be

why the Harry Potter books and movies which feature teens

have their strongest appeal to younger children. Or why

movies with a PG-13 rating are more enticing to teens. Or

why Paris Hilton, who is in her mid-twenties, is a fashion

icon for m any teenage girls.

Whether the new fashion is Crocs or Lacoste, whether the

latest video craze is Nintendo DS Lite or GameTap, you

can be sure of one thing: what’s hot today is not tomorrow.

Rather than focusing on what’s hot right now, it is more

important to develop too ls and approaches to monitor and

anticipate changes.

For example, tap into the fickle world of teen trends by

checking out websites such as Billboard.com for the most

popular ringtones, which btw, as of this writing, is the

Nintendo Super Mario Brothers Theme by Koji Kondo, or

the hottest d igital songs (Fergie’s London Bridge), or num-

ber one album (the self-named Danity Kane), or top single

(Justin Timberlake’s “SexyBack” ). Another popular teen

website is MySpace.com, where teens connect with others,

blog, rank music, and much more.

Cash or creditThe fact of the matter is, teenagers represent a powerful

buying force in the U.S. market. According to the 2005

Roper Youth Report, kids are earning $29.20 per week, two

dollars more than in 2004, with 29% of their money com-

ing straight from parents. Chores (37% ) and gifts (23% )

account for other popular sources of teen income. Nearly

one-third (30% ) of 8–17-year-olds say they are involved in

making family purchase decisions, up four percentage points

from last year, as parents increasingly turn to their kids for

advice on what to buy. Teens also indicate that they influ-

ence purchase decisions on everything from cell phone serv-

ice to the right cable provider.

For better or worse (probably the latter), teens are also

enamored by the magic of credit. According to the

Jump$tart Coalition for Personal Financial Literacy, an edu-

cational organization, nearly a third of high school seniors

reported having a credit card of their own or one co-signed

by a parent.

22 Fall/Winter 2006

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 25/5623

Products with appealIf you live in a household with a teen, get ready to stock

up on deodorants, grooming aids, acne remedies and

other personal care products, instant meals and school

supplies—in that order. According to information from

ACNielsen Homescan, categories such as these are greatly

overdeveloped for the teen market.

While that may not come as a complete shocker, consider

the fact that many of the brands that have risen to t he top

of this typical list are those that cater to this trend-conscious

segment by offering something new, different or cutting

edge. Take for example Unilever’s AXE deodorant for men.

Appealing to the raging hormones of boys (and young men),

the product comes complete with its own risqué website

where the “AXE effect” promises to attract the opposite sex

“when used responsibly.” AXE now generates $269 million

per year in the food, drug and mass merchandiser channels

(including Wal-Mart).

Another product high on the dollar volume index scale pur-

chased by households with teens offering a unique edge is

Hershey’s Ice Breakers gum that explodes with a burst of

mouth-freshening extra mint taste. Cutesy advertising fea-

turing Hilary and Haylie Duff appeals like a gem to their

target audience.

While these products get high marks for originality, there is

a t remendous untapped opportunity to cross-merchandise.

For example, most cereals are marketed to either young

children or adults, but not teens. Offering a free iTune

download on t he package would certainly have more appeal

to this audience than would an action figure from the latest

kid movie.

Chart 1: Boys spend more on video games than girls

LifeStyle

Affluent Struggling Modest PlainCosmopolitan Suburban Comfortable Urban Working Rural

BehaviorStage Centers Spreads Country Cores Towns Living TotalMale 12–14 253 234 202 205 215 129 202

Male 15–17 89 144 113 178 97 101 120

Female 12–14 103 45 42 129 38 51 62

Female 15–17 2 4 30 26 8 5 13

Total 114 107 97 138 92 72 100

Source: ACNielsen Homescan & Spectra, Penetration (Population)/% Penetration Index, All Channels/United States, BehaviorScape Framework.

Chart 2: Girls spend more on clothes than boys

LifeStyleAffluent Struggling Modest Plain

Cosmopolitan Suburban Comfortable Urban Working RuralBehaviorStage Centers Spreads Country Cores Towns Living Total

Male 12–14 56 47 36 86 56 36 50

Male 15–17 50 52 67 82 32 63 58

Female 12–14 186 132 127 122 187 11 4 141

Female 15–17 97 173 132 123 135 223 156

Total 97 101 90 103 101 108 100

Source: ACNielsen Homescan & Spectra, Penetration (Population)/% Penetration Index, All Channels/United States, BehaviorScape Framework.

High Consumer, 120–149 Very High Consumer, 150+

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 26/56

Aligning the cross hairsFor marketers, targeting households with teens is just a

start. For some products in which consumption is driven by

individuals, however, a more granular approach is necessary.

Using Simmons Teen N ationa l Consumer Survey (NCS)

data, Spectra has developed a Teen Targeting Solution that

helps to understand the teen consumer and identify the best

way to reach and locate teens in their neighborhoods.

The NCS Simmons Teens Survey is a comprehensive survey

of American teens aged 12–17. It provides single-source

measurement of major media, products, services and in-

depth consumer demographics and lifestyle/psychographic

characteristics. Fueled by this survey, the Teen Targeting

Solution allows marketers to more precisely market their

brand to the teenager who buys the product.

The importance of analyzing teens by both age and gender

is illustrated in the following example. Young males ages

12–14 are twice as likely as the average teen to spend their

allowance on video games. Interestingly, teens in Struggling

Urban Core neighborhoods are also 38% more likely to buy.

24 Fall/Winter 2006

U.S. Teens Through the Decades1920s 1930s 1940s

• Youth Crisis—

Kids spending toomuch on gamblingand watching movies

• U.S. Boy Scouts andCampfire Girls founded

• World War One

• “Newsies”— kidsselling newspapers

• Many teens workedvs. attending school

• The Charleston,fox-trot andshimmy (dances)

• Flappers

• Flagpole sitting

• Marathon dancing

• Jazz• Emily Post’s

manners book

• First peanut butter

& jelly sandwiches

• First Miss America

• The Depression

• Fair Labor Standards Actlimited the age of child

laborers to 16

• Roosevelt’s Civilian

Conservation Corps

• Long-playing

phonograph records• The “golden age”

of radio

• 250,000 teens living

on the railroad

• Swing music

• Board games

• Hats were mandatory

for men

• First drive-in theaters

• The word “teenager”was coined

• World War 2, rationing,victory gardens

• Many jobs available toteens during WW2

• Seventeen magazinefounded in 1944

• The jitterbug (dance)

• Term “juvenile

delinquent” coined

• Zoot suits for young men,

“slacks” for women

• Largest number of teen

marriages after WW2

• Swallowing goldfish

• “Kilroy was here.”

1950s• Birth of rock & roll

• First hula hoops

• Brylcreem(hair tonic)

• Jack Kerouac, beatnik

• Marilyn Monroe, Elvis

Presley, James Dean

• Telephone booth stuffi

• 3D movies

• Poodle skirts, saddle

shoes, letter sweaters

• Car hops (before

drive-throughs)

• Sideburns

1910s

8/6/2019 Babyboom All

http://slidepdf.com/reader/full/babyboom-all 27/5625

By contrast, female teens are much more interested in the

fashion scene, spending far more than average on clothing.

Thus, marketing programs designed only for the household

or for the adult consumer will not offer the most effective

way to reach heavy teen consumers. ■ See charts 1 and 2,

page 23.

Zooming inOnce the teen consumer has been identified, direct market-

ing can begin. Using the Spectra system, a t argeted profile of

the Brand A teen consumer is devised to reveal what maga-

zines they read, what TV shows they watch, what websites

they surf, how they spend their free time and where they shop.

In addition, subtle neighborhood differences are also

exposed. For example, in the upscale urban areas character-

ized by Cosmopolitan Centers, teens are more likely to beachievers. They have good access to home computers, are

savvy with money, and are less likely to watch TV. Teens in

more downscale areas, Struggling Urban Cores, are more

likely to access the Internet at school, and are very music

oriented. They know what songs are in the Top 10, wear

clothes that reflects their musical tastes and are likely to

characterize themselves as rebels.

Understanding the unique demographic nuances of teen con-

sumers allows the execution of a precise marketing strategy

among all the consumer segments that purchase the brand.

In addition, not only do teens represent a large share of

some product’s volume, they also are the next generation of

consumers who will fuel growth for all brands in the CPGindustry. A successful marketing campaign to teens will pro-

vide the foundation for brand loyalty and growth among

this generation well into the future.

The next big thingKeeping abreast of the next big thing on the horizon is criti-

cal. Think back to when the iPod Nano was introduced in

September 2005 and the Video iPod in October 2005. At

that time, Apple discontinued their older models, but several

mainstream retailers continued to advertise these models

while selling the incompatible accessories. Only a very few

nimble retailers were quick to align themselves with the new

iPod models by including photos and information on the

front page of their websites.

1960s 1970s1980s

1990s• 40% of the U.S.

population was under20 years old in 1965

• Woodstock

• Protests, civil rights,

Vietnam

• British invasion, Beatles

• Bell bottoms, miniskirts, turtlenecks

• The twist (dance)

• Love beads

• Surfing

• Tie-dyed shirts

• Bouffant hairdos,hair ironing, Afros

• Go-go boots

• Hippies, counter-culture

or “ alternative” culture

• Recreational drugs

• Voting aged dropped

to 18

• The draft ended

• 8-track tapes

• Streaking

• Feminism

• Punk rock

• Mopeds• Platform shoes,

earth shoes

• Disco

• First video games

• Rocky Horror Picture Show

• Ecology

• MTV goes on the air

• Latchkey kids

• Jelly shoes

• Video arcades

• Rubik’s Cube

• Boom boxes