August 2012 Issue 513-514 www ... · equitable Life actuary Following an investigation the ... its...

24

August 2012 Issue 513-514 www.InternationalAccountingBulletin.com Balance of power Global regulatory pressures threaten global shift in firm fortunes ● Competition Commission: different views emerge ● A big GAAP in IFRS: further delays to US adoption ● India survey: Regulatory deadlock ● The Netherlands survey: Are the Dutch jumping the gun on regulatory reform?

Transcript of August 2012 Issue 513-514 www ... · equitable Life actuary Following an investigation the ... its...

August 2012 Issue 513-514 www.InternationalAccountingBulletin.com

Balance of power

Global regulatory pressures threaten global shift in firm

fortunes

● Competition Commission: different views emerge● A big GAAP in IFRS: further delays to US adoption

● India survey: Regulatory deadlock ● The Netherlands survey: Are the Dutch jumping the gun on regulatory reform?

Give your students a business perspective of the world of accounting. Give your students access to content they can trust. Give your students the edge. Subscribe to The Accountant

www.vrl-financial-news.com

Give your students a business

Give your students access to

A subscription to The Accountant is the ideal accompaniment to an accountancy course of study. Including exclusive features and interviews with major figures in the accountancy sector, The Accountant will help your students to understand the real-world implications of the theory they are learning, and help improve their employability in a competitive jobs market. A weekly newswire gives you regular updates of all the big stories, while IP access means students can view our content anywhere with access to the student portal.

Subscribe to The Accountant for: • IPaccesstoourcontent.Soyourstudentscanaccessour

content campus-wide with one login

• Contentyoucantrust.Wehave125yearsofexperiencedelivering accountancy news.

• Trulyglobalanalysis.Wecoverarangeofstoriesfromaroundthe world, so your students get a wide perspective of the sector.

SIGN UP FOR THE FREE NEWSWIREGet free weekly updates and free content. Sign up here:

http://www.vrl-financial-news.com/system-pages/headernav/free-news.aspx

DON’T mISS OUT. Subscribe to The Accountant today. Contact our subscriptions team on +44(0)20 7563 5688 or email us at [email protected] to find out more.

eDItOr’S LetterInternational Accounting Bulletin

Give your students a business perspective of the world of accounting. Give your students access to content they can trust. Give your students the edge. Subscribe to The Accountant

www.vrl-financial-news.com

A subscription to The Accountant is the ideal accompaniment to an accountancy course of study. Including exclusive features and interviews with major figures in the accountancy sector, The Accountant will help your students to understand the real-world implications of the theory they are learning, and help improve their employability in a competitive jobs market. A weekly newswire gives you regular updates of all the big stories, while IP access means students can view our content anywhere with access to the student portal.

Subscribe to The Accountant for: • IPaccesstoourcontent.Soyourstudentscanaccessour

content campus-wide with one login

• Contentyoucantrust.Wehave125yearsofexperiencedelivering accountancy news.

• Trulyglobalanalysis.Wecoverarangeofstoriesfromaroundthe world, so your students get a wide perspective of the sector.

SIGN UP FOR THE FREE NEWSWIREGet free weekly updates and free content. Sign up here:

http://www.vrl-financial-news.com/system-pages/headernav/free-news.aspx

DON’T mISS OUT. Subscribe to The Accountant today. Contact our subscriptions team on +44(0)20 7563 5688 or email us at [email protected] to find out more.

August 2012 y 1www.InternationalAccountingBulletin.com

editorial advisory boardfrank arford, Crowe Horwath International CEOKevin arnold, Nexia International executive directorGeoff barnes, Baker Tilly International president and CEOGraeme Gordon, Praxity executive directorStephen Jacobs, INPACT International presidentJon Lisby, Kreston International executive director James Mendelssohn, MSI Global Alliance CEOChristian Mouillon, Ernst & Young global vice-chair, assurance ed nusbaum, Grant Thornton International CEOMichael reiss von filski, Geneva Group Inter-national CEOLiza robbins, Morison International CEOMartin van roekel, BDO International CEOJean Stephens, RSM International CEOrobert tautges, HLB International CEOPauline Wallace, PwC head of public policy and regulatory affairs

COntentS02-04neWS & anaLySIS

n BDO UK considers PKF acquisition?

n Deloitte defends its SCB work

n AADB to investigate PwC over RSM Tenon work

Earlier this month, I predicted August – as it often turns out to be – would be rather slow for news. This, I hoped, would give me plenty of

time to ease into my new editorial role, which I’ve partially taken over from my dear friend and mentor Arvind Hickman, since his recent move to pastures new. In my three years at International Account-ing Bulletin, August has always been quiet, with very little activity in the professional services market.

Soon enough, however, it became appar-ent this was no typical August as, in the past few weeks, several important news stories broke. Just to name a few: Deloitte’s alleged involvement in assisting in the concealment of Standard Chartered Bank’s transactions with Iranian clients, KPMG UK announc-ing a 3% cut in its workforce, rumours of a BDO UK takeover of PKF, PwC UK facing an accounting watchdog investigation into its work at RSM Tenon, and evidence emerging from the Competition Commission revealing serious friction between the mid-tier and the Big Four. Not an easy first month for a new editor.

Additionally, on 31 August we will see the release of the long-awaited draft report on the audit policy proposals by the European Parliament’s Legal Affairs Committee, com-monly referred to as Juri.

The profession appears, potentially, to have reached a once-in-a-generation tipping point, and several changes could take place in the coming months.

regulationSince I first started reporting on the indus-

try, the amount of regulation or proposed regulation discussed has risen dramatically. Firm leaders around the world used to tell me their major concern was the growth of their businesses, but this has recently been usurped by the potential effects of upcoming regulation.

Whether a Big Four member or a small market player, regulation is likely to change everyone’s way of doing business. Regulators are also challenging the role of the auditor, as they try to address the expectation gap.

Whether regulation is the best solution for the industry is still unclear and perhaps the leap from being a mostly self-regulated industry to one that encourages criticisms and reforms has been somewhat sudde.

The message, however, coming from many governments and watchdogs has been that retaining the status quo is not an option.It’s not only the profession in Europe that’s under scrutiny and awaiting regulation.

Firms in India could also be subject to reforms such as mandatory firm rotation and restrictions on auditors offering non-audit services (turn to page 10-14).

In China, the government has enforced strict localisation rules on the Big Four and our reporter spoke to several stakeholders about the effects of the government’s orders to place the control of large firms into the hands of Chinese CPAs (turn to page 8-9).

Globally, the profession is being chal-lenged, and while some are taking a ‘wait and see’ approach, others appear more proactive.

The Dutch government, for instance, is thinking of legislating for mandatory audit firm rotation and restricting the offer-ing of non-audit services before the out-comes of European Union audit reform are announced. Could the Dutch be jumping the gun on this? (see page 15-20).

With autumn approaching and politicians and firm leaders returning from holiday, more news will be filling my inbox and, if I’m allowed another prediction, I think this might be a time that the profession will remember for some years to come.

Surprising August foreshadows a time to remember

05-09featureS

05: COMPetItIOn COMMISSIOn

Difference in opinion between the Big Four and mid-tier comes to light

06-07: a bIG GaaP In IfrS

IAB examines the US delay in IFRS adoption decision

09-09: CHIneSe POWer PLay

Paul Golden looks at new Chinese Big Four restructuring rules

10-20COuntry SurveyS

10-14: InDIa

Plenty of opportunities in the mar-ket, but what’s hurting the profes-sion is the uncertainty around key regulations that is also vitiating the environment for Indian business.

15-20: tHe netHerLanDS

A slow economy, relentless fee pressure and a struggle to gain new clients have become perennial prob-lems for the Dutch accountancy pro-fession as new regulation looms.

2 y August 2012 www.InternationalAccountingBulletin.com

neWS DIGeSt International Accounting Bulletin

MOverS & SHaKerS

neWS rOunD-uP

LinkedIn Group World Accounting Intelligence

twitterWAI_News

facebook pageWorld Accounting Intelligence

Scan our Qr code for quick smartphone access to Iab

Join our online community

IAB OnLIne - auGuSt

top 5 articles

Deloitte in spotlight over Standard Chartered

Former Deloitte US partner pleads guilty to insider trading

Mid-tier hit back at PwC in competition probe

Deloitte US CEO defends SCB work

Australia’s Big Four jostle for top spot

Most re-tweeted article

PKF UK discusses barriers to entry: Competition Commission

read in 151 countries

United Kingdom (27%)

United States (15%)

Australia (5%)

Hong Kong (3%)

India (3%)

Other (47%)

reSuLtS

Deloitte uK revenues up 11%Deloitte UK has reported an 11% increase in annual revenues to £2.3bn in the year to 31 May 2012, attributing to growth to strategic investments made. The firm’s audit practice revenues were £663m, up 13%. This is a significant improvement from last years 4% audit service fees increase.Double digit growth, 14%, was also reported in the firm’s consulting arm, which made £402m. Tax revenues grew to £529m, up 7%, while corporate finance revenues increased by 6%.Deloitte UK revenues also include fee income from the network’s Swiss practice; ehich was up 21% to £211m.

LeGaL

aaDb closes e&y case over equitable Life actuaryFollowing an investigation the UK Accountancy and Actuarial Discipline Board (AADB) has decided not to take any further action and close the case against Ernst & Young UK (E&Y) over its audits of the Equitable Life Assurance Society (ELAS).“Following the conclusion of this investigation, it has been decided that there is no realistic prospect that a tribunal would make an adverse finding against the actuary concerned. Consequently, no further action will be taken and the case will be closed,” the AADB said.ELAS became insolvent in 2000 after it was decided that the insurer was to pay £1.5bn of annuities following a House of Lords inquery.

StrateGy

rSM admits vietnamese firmRSM has bolstered its Asian presence by admitting RSM DTL Auditing Company in Vietnam. Established in 2001, DTL Auditing Company has almost 200 employees in offices in Hanoi and Ho Chi Minh City, specialising

in audit and assurance, tax consulting, accounting, information and communication technologies consulting, and transaction services. Its clients cover various industries and include large Vietnamese groups and multinational corporations such as Orange FT, Fuji Xerox and IATA. StrateGy

nexia secures JH Cohn and reznick Group membershipRecently merged US top 20 firms JH Cohn and Reznick Group have confirmed its international affiliation with Nexia International instead of PrimeGlobal, formerly known as IGAF Polaris.Prior to the merger JH Cohn was part of Nexia International; while Reznick Group’s affiliation was with PrimeGlobal.The firm said that the merged firms will rebrand to CohnReznick from 30 September.

LeGaLformer Deloitte uS partner pleads guilty to insider tradingFormer Deloitte vice chairman and partner for clients and markets, Thomas Flanagan, has pleaded guilty to one count of securities fraud, which carries a maximum sentence of 20 years in prison and a $5m fine.Flanagan admitted to the criminal charge brought against him by saying he conducted inside trading based on non-public information from the firm’s clients, taking advantage of his capacity as advisory partner.The former Deloitte partner acknowledged illegal profits of $420,000. After a plea-bargaining with the US prosecutor, Flanagan could receive a sentence of 37 months in prison.

PeOPLe

KPMG uK to shed 3% of its workforce KPMG UK has announced it is to reduce its workforce by 3% - an estimated 350 employees according to IAB data - in the coming weeks, in an attempt to adapt to market conditions and ensure business efficiency.The UK’s third biggest firm said the decision was a necessary measure in a programme of changes designed to “actively manage its cost base”.“As a result, a number of business units within KPMG are now carrying out reviews of their structures and headcount numbers. It is likely that we will need to make a number of roles redundant over the coming weeks,” KPMG said.The firm said the redundancy situation was “regrettable” <

Association MSI Global Alliance has appointed Donal Watkin (pictured), formerly deputy executive director of Nexia International, as chief executive designate.MSI said the appointment is the first phase of a planned management transition, which will also see current chairman Peter Abels step down at the end of the

year. Current chief executive James Mendelssohn will succeed Abels

as chairman, while Watkin will become chief executive responsible for the day-to-day management of the association..

bDO uS has appointed Lee Klumpp as project

manager of the financial accounting Standards board Industry fellowship Program.

In this role Klumpp, who is also bDO’s assurance director, will be required to make technical recommendations to the faSb, as well as drafting Statements, Interpretations and faSb Staff Positions.

PwC Australia has appointed economist Jeremy Thorpe as Canberra Office managing partner, following Andrew Turnbull’s retirement from the firm.<

NO116_MagTheAccountant152x210_V2PR.indd 1 31/03/11 4:48 PM

neWS anaLySISInternational Accounting Bulletin

BDO UK considers PKF acquisition? StrateGy

BDO UK is considering acquiring the UK arm of PKF in order to grow its market share and bridge the gap between it and the Big Four, according to UK newspaper the Tel-egraph.

According to reports, the broad terms for the acquisition have already been agreed, however PKF’s UK managing partner is yet to put the deal forward to the firm’s 70 part-ners.

Both BDO UK and PKF UK said they do not wish to comment on the rumours at this time.

In fiscal 2011, PKF UK reported revenue of £140m and is the smaller of the two mid-tier firms. But if the acquisition is successful the combined revenue for the new firm would be around £430m ($674m) seeing it overtake Grant Thornton as the largest mid-tier firm in the UK market.

However, despite this huge jump in rev-enues, the combined mid-tier firm would

still be more than £1bn behind the smallest of the Big Four firms-Ernst & Young-which reported revenues of £1.5bn in 2011.

M&A has become increasingly common in the accounting market, with firms using it as a way to grow market share. The merg-ing of mid-tier firms was one of the solutions suggested at the recent UK House of Lords inquiry into audit market concentration with the Lords saying it would be an effective way to introduce more competition into the mar-ket.

The Competition Commission, which is currently investigating the UK statutory audit market, was told by PKF UK in a testi-mony that there are several barriers to entry for mid-tier firms, with PKF emphasising the predominance of Big Four alumni among company directors, followed by heavy price discounting.

The mid-tier firm also told the watchdog that it was against market intervention such

as the splitting up the Big Four and manda-tory audit firm rotation.

PKF also told the CC it has the ablility to audit quite a large number of FTSE350 com-panies and some FTSE100 companies.

If the deal is to go ahead, it will reflect the events unfolding in the Australian mid-tier market, recently where Grant Thornton Aus-tralia merged with BDO offices in Melbourne and Sydney, creating the largest national firm outside of the Big Four.

The merger added an estimated A$85m ($87m) to Grant Thornton’s annual revenue, which increased to A$245m. This is expected to catapult the firm above BDO into sixth position, behind WHK Group and above Baker Tilly Pitcher Partners.

Once BDO Australia revenues are announced later in the year they are expected to drop from A$214m to A$130m, making it the ninth largest firm in the country.<

Ana Gyorkos

August 2012 y 3www.InternationalAccountingBulletin.com

NO116_MagTheAccountant152x210_V2PR.indd 1 31/03/11 4:48 PM

www.InternationalAccountingBulletin.com4 y August 2012

neWS anaLySIS International Accounting Bulletin

Deloitte has claimed its financial advi-sory arm, which is separate from its audit business, properly performed its role as independent consultant to

Standard Chartered Bank (SCB) in full com-pliance with the highest professional stand-ards.

Deloitte’s defence came following allega-tions by the New York State Department of Financial Services that Deloitte US’s con-sultants helped SCB hide transactions with Iranian clients, worth around $250bn, from regulators when it was tasked with writing a report on SCB’s activities.

In its allegation the regulator said SCB “carefully planned its deception and was apparently aided by its consultant Deloitte & Touche, which intentionally omitted criti-cal information in its ‘independent report’ to regulators”. This ongoing misconduct was especially egregious…during a key period between 2004 and 2007,” the New York watchdog alleged.

It claims Deloitte submitted a “watered down” report and then deleted any reference to certain types of payments.

In a statement to International Accounting Bulletin, Deloitte said it had no knowledge of any alleged misconduct by any SCB employ-ees, and categorically denies that it aided in any violation of law by the bank.

The firm said it “absolutely did not delete any reference to certain types of payments from its final written report”.

“Deloitte did not include in its final written report a particular recommendation which was included in an earlier draft. It did so in favour of in-person discussions with regula-tors regarding this issue, and it included the facts relating to this issue in the final written report,” Deloitte said.

Joe Echevarria, chief executive of Deloitte in the US, has also contested the allegations.

Echevarria told news agency Reuters that the accusations, brought against the firm by the New York State Department of Finan-cial Services, represented “distortions of the facts”.

“Presumably the facts will bear out that we certainly held up all the standards required and behaved in an ethical and responsible way,” Echevarria added.

NYSDFS’ report, published at the start of August, alleged Deloitte aided SCB in hiding transactions from regulators between 2004 and 2007.

In a further charge against Deloitte, the watchdog said the firm gave SCB two reports containing highly confidential client infirma-tion.

Responding, Echevarria argued: “We have pretty robust processes in place for behav-

iour that violates law, rules or firm policies,” he said.

“Appropriate actions are taken when individuals are found to have done that,” he concluded.

Since the allegations, the London based bank has settled the case with the New York watchdog for $340m, however the bank might be facing further fines as several other US regulators are looking into its activities.<

Ana Gyorkos

Deloitte defends SCB workLeGaL

AADB to investigate PwC over RSM Tenon auditLeGaL

The UK Accountancy and Actuarial Dis-cipline Board (AADB) is to launch an investigation into the conduct of mid-tier accounting firm RSM Tenon and

its auditor PwC UK, in connection with the firms recent financial reports.

According to AADB, the aim of the inves-tigation is to focus on “the preparation, approval and audit of the financial state-ments of RSM Tenon Group and its subsidi-ary companies for the years ended 30 June 2010 and 2011”.

RSM Tenon, the only UK accounting firm listed on the London Stock Exchange (LSE), reported a 9.3% year-on-year drop in rev-enue to £107.8m for the six months leading to 31 December 2011, a poor performance largely ascribed to ongoing inefficiency in the integration of RSM Bentley Jennison, acquired in December 2009.

The firm has had to cut staff and service

lines, as well as change its executive team, in reaction to the downturn in performance.

Meanwhile, doubts have been raised over the audit and approval of RSM Tenon’s financial statements in this troubled period of trading, leading to the current AADB investigation.

AADB commented that it would be seek-ing to clarify “the preparation, approval and review of financial information in connection with the admission of RSM Tenon Group to the main market of the LSE and the acquisi-tion of RSM Bentley Jennison.”

Following AADB’s announcement, RSM Tenon auditor PwC UK committed to defending its actions in connection to the audits.

“We will be cooperating fully with the AADB investigation. We will be vigorously defending our audits and other work carried out for the RSM Tenon Group,” PwC UK

said.Earlier this year the AADB fined PwC

UK £1.4m over the firm’s handling of the JP Morgan securities audit.

RSM Tenon switched its LSE share catego-ry from premium listing to standard listing, cut its specialised tax service and appointed a new chairman and several other members of the executive team.

The firm also had to cut 10% of its work-force and was forced to restate its accounts for the previous year as a result of “signifi-cant errors and change in accounting policy”.RSM Tenon also owes £88m to Lloyds Bank-ing Group and has had to arrange new terms for committed facilities deferring some of the payments until 31 October 2012.

In 2011 RSM Tenon was ranked the sixth largest firm in the UK, according to Interna-tional Accounting Bulletin data. <

n One of SCB’s offi ces

www.InternationalAccountingBulletin.com August 2012 y 5

Big Four and mid-tier clash in CC probeDifference of opinion between the Big Four and the mid-tier is apparent from the evidence released by the UK competition authority investigating statutory audit market concentration. ana Gyorkos reports

In July PwC UK issued a response to the Competition Commission (CC) criti-cising comments made to it by certain stakeholders and mid-tier audit firms on

the back of its investigation into audit mar-ket concentration.

In the document PwC UK criticised mid-tier comments stating that large audit firms have a “superior market reputation for qual-ity and trust in conducting large company audits”. PwC UK also opposed the mid-tier suggestions that those responsible for acquir-ing audit services and other stakeholders are operating under a systemic misconcep-tion and that this superior reputation is not deserved.

PwC said mid-tier arguments suggesting large audit firm reputation is ‘undeserved and/or is relied on inappropriately by large companies when selecting an audit firm’ did not stand up when scrutinised.

Grant Thornton and BDO UK hit back at PwC’s criticism in documents submitted to the CC. The mid-tier firms said PwC UK “misrepresented” some of the arguments made by the mid-tier and third parties such as investor groups in its submission to the CC.

“PwC has itself inaccurately mischarac-terised the evidence of Grant Thornton and sought to attack propositions that have not, in fact, been made by Grant Thornton,” the firm wrote in its response to the CC.

Grant Thornton said PwC’s suggestion that “The mid-tier firms themselves recognise that they have lesser attributes and resources than the largest firms” has a “disingenuous” comment.

BDO said the firm’s response did not imply that “higher and sustained quality would be achieved if the structure of the market were different” as claimed by the Big Four firm.

“What we have said is that an improved market structure would give more choice and would reduce the systematic dependence on the four largest firms, and could lead to more innovation in the market,” BDO explained.

Another clear instance of ‘difference of opinion’ is with audit quality and the find-ings of the UK oversight body - the Audit Inspection Unit (AIU).

Grant Thornton said PwC asserts that, contrary to what is suggested by it and oth-ers, AIU reports do not provide a compre-hensive basis for assessing the comparative merits of individual audit firms.

PwC bases its findings on audit quality and it being ranked highly among the Big Four accounting firms in a report by Copenhagen Economics, which assessed the impact of the European Commissions audit reform pro-posals. The assessment was commissioned by the Big Four.

The Copenhagen Economics report states that more than 90% of the AIU-inspected Big Four audits were in the category “good with limited improvements required” or “accept-able but with improvements required”, while less than 60% of inspected audits from smaller audit firms were categorised in the same to top categories.

Grant Thornton argues that the Copen-hagen Economics report “leans heavily on selective information taken out of context based upon a single year’s AIU reports to sug-gest that audit quality is highest at the four largest firms and that scale leads to higher quality”.The latest document released by the CC represented only a fractioned and redacted version of the information that is being gathered, as proceedings are taking place behind closed doors.

The CC is required to report on its findings by 20 October 2013<

A UK Competition Commission (CC) statutory audit survey has found 83% of FTSE 350 companies that recently switched auditors opted to

choose another Big Four firm while 97% of all switches have been among the Big Four. This highlights a high level of concentration in the UK’s audit sector, in which four firms carry out an overwhelming majority of listed company work.

The survey included a sample of 607 inter-views with FTSE 350 and non-FTSE 350 finan-cial directors, chief financial officers and audit committee chairs.

Similar to FTSE 350 companies, 90% of non-FTSE 350 companies also stuck to the Big Four when switching auditor.

Half of FTSE 350 companies that switched auditor said it led to a decrease in audit fees and 64% said it led to improved audit quality.

Half of the companies surveyed last tendered six or more years ago or have never tendered. The most common reasons for not changing auditor were high quality service, good value for money and the fact that a companies were happy as things are.

Interestingly, companies that used a non-Big Four firm (26%) were more likely to have never tendered than those who used a Big Four firm (11%). When respondents were asked which firms were most commonly invited to tender, the Big Four dominated with KPMG and Ernst & Young mentioned most.The survey found Big Four-only tenders were linked to size: Sev-

enty percent of companies with 10,000 or more employees only invited the Big Four to tender compared to 59% of companies with fewer than 10,000 employees.

When asked who they would consider if their current auditor ceased trading, FTSE 350 com-panies indicated they were much more likely to consider the Big Four. In terms of audit fees, 26% of FTSE 350 companies spent between £1m-£5m on audit annually while 45% spend anything up to £500,000.

Most FTSE 350 financial directors and chief financial officers said that a disagreement over non-audit services would not be a trigger to con-sider switching auditors, indicating that compa-nies do not view the provision of non-audit ser-vices as a conflict of interest with audit.<

CC survey highlights concentrationSurvey

featureInternational Accounting Bulletin auDIt MarKet COnCentratIOn

feature International Accounting BulletinIfrS

A Big GAAP in IFRS The ‘big bang’ approach to introducing IFRS in the US has been reduced to a whimper by the Securities and Exchange Commission, as its latest report on international standards effectively leaves the project in no man’s land. IAB reports

6 y August 2012 www.InternationalAccountingBulletin.com

The decision by the US Securities & Exchange Commission (SEC) to put the transition to International Finan-cial Reporting Standards (IFRS) on ice

for the foreseeable future means that firms will continue to advise US-based businesses to keep a closer eye on the work of the Finan-cial Accounting Standards Board (FASB), the country’s national standard setter.

It’s another blow for the International Accounting Standards Board (IASB), which sets global accounting standards, in its pro-tracted efforts to convince the world’s larg-est economy to move away from Generally Accepted Accounting Principles (GAAP) and fully endorse IFRS.

Ken Marshall, leader of Ernst & Young US’ financial accountancy services practice, says: “The real top companies in the US have looked at their in-house IFRS steering com-mittees and what they have done is to move them to anticipating and understanding the US GAAP projects that are currently under-way.

“If, as a business, you are going to use valuable internal resources at the moment, it should be in watching the deliberations between the FASB and IASB, with a particu-lar view towards where the FASB will end up with these standards.”

The stance taken by the SEC, outlined in its recently published staff report, came as little surprise as concerns over IFRS, notably around the four key areas of revenue rec-ognition, financial instruments, leasing and insurance, have been played out loudly in prolonged discussions between the FASB and IASB. Major questions were also asked about the lack of consistency of international stand-ards as they have been interpreted differently from country to country, causing concerns about the comparability of financial state-ments and the ease with which accounts can be audited on a like for like basis.

tread carefully Big Four and mid-tier firms in the US have broadly welcomed the SEC’s report, seeing it as a prudent step given the complexity of the undertaking to try and manoeuvre US GAAP over to IFRS.

Jim Castellano, chairman of Baker Tilly International, tells IAB: “There are very important points raised in this paper and how we get there in the US. The work-plan rightly points out that there are very few jurisdictions that are adopting IFRS outright without having mechanisms of their own. How should the US take this?”

Overall, Castellano believes the latest developments are positive. “I don’t really think it is a delay,” he continues. “Rather, it’s all part of a very good and deliberate pro-cess in the US to carefully and methodically get to a position where we can have IFRS as the basis for public company reporting in the US.” Nate Van der Hamm, national IFRS prac-

tice leader for Grant Thornton, agrees that this report shouldn’t be viewed in a negative light.

“This was a necessary step by the SEC in completing its due diligence on IFRS. The impacts of adoption of IFRS would be very significant in the US and as such the SEC has performed a very detailed and thorough analysis.

“What does appear to be a delay is that the report didn’t provide a recommendation as to whether or not a move to IFRS should be made. The report does however spend a sig-nificant amount of time discussing the chal-lenges of doing an immediate conversion, also referred to as the ‘big bang’ approach.”

The cost burden of a switch to interna-tional standards remains a hot topic, espe-cially for smaller companies. Keith Wallace, international assurance practice leader for RSM McGladrey, comments: “Our clients tend to be the middle market companies. Any decision to change to a new standard would result in a sizeable commitment of resources both in terms of dollars and time, which is critical for these businesses.

“That is a keen focus for us. Some of the larger companies have the technical staff to assist with projects, whereas smaller compa-nies tend to run much leaner. Taking on these types of changes will be a fairly sizeable pro-ject for them and they would have to divert significant resources from their main focus.”

To put it mildly, the timing of the switch is hardly favourable given the global financial crisis and the introduction of new legislation such as the controversial Dodd-Frank Act, not to mention the forthcoming presidential election. Marshall says we are in a very bad economy.

“There is quite a bit of pressure on the SEC to deal with substantial issues – part of this is whether it is the right time in the economy to do this.

“For those in the profession, it’s seen as a new accounting language, but for others it would be regarded as regulation. The SEC is dealing with monumental issues still and therefore accounting standards are not front of mind for them.”

Paul Rohan, director of financial reporting and quality control at UHY, concedes that “the timing was such that maybe it would have been reckless” to convert to IFRS, but he argues that an opportunity has been missed which is neither in the long-term interests of smaller businesses or, for that matter, the US capital markets in general.He explains: “There is never an ideal time to make a change. All of Europe went through that several years ago. I am sure there were folks in the individual countries in Europe and indeed around the world that thought their standards were, in certain instances, better than the international standards.”

Kristine Brands, a CMA and CPA who sits on the global board of the Institute of

“the aim is to develop one set of high quality global standard and my disappointment stems from the SeC working on it for two and consistantly postponing the deadline leaving our uS filers in the air.”

Kristine Brands, CMA and CPA sitting on the global board of the IMA

featureInternational Accounting Bulletin IfrS

August 2012 y 7www.InternationalAccountingBulletin.com

Management Accountants (IMA), admits to being “extremely disappointed” by the non-committal outcome of the Staff Report.

“The aim is to develop one set of high quality global accounting standards and my disappointment stems from the SEC work-ing on this for two years and consistently postponing the deadline and leaving our US filers up in the air. This time it’s even worse as not only are they up in the air, the SEC has effectively suspended the project with no firm date of resuming,” she says.

“That is detrimental to the goal of eve-rybody reporting to one set of high quality standards.”

When it comes to the debate about small-er businesses converting to IFRS from US GAAP, Rohan suggests that in some respects it’s a question of ambition.

“If the SEC had made the decision for public companies, two to three years down the road, for complete convergence to IFRS, that would have been instrumental in getting other companies to make the switch along with those who have to do it anyway. It would have left small businesses in the US with a decision to make about whether they want to have the reporting that the big com-panies are using or not.”

If a business is serious about international expansion, or considers itself an attractive acquisition target for larger concerns, then the phasing in of IFRS should make sense. However, for Wallace, there are dangers to adopting a one-size fits all approach: “It depends on the industry of the company and the size and nature of its operation. The lion’s share of the middle market companies are seeing their global footprint growing and, with that, the establishment of a global set of standards would be beneficial for them in order to simplify their reporting require-ments as they seek to expand.”

Conversely, he notes there is a group of middle market companies that tend to oper-ate only domestically.

“We continue to support having an alter-native to global standards for those busi-nesses, which is consistent with some of the AICPA [American Institute of Certified Pub-lic Accounts] initiatives that we have in the US.”

Kristine argues that concessions for small-er enterprises could be made, as opposed to reporting to another set of standards.

“All of these actions are an extra burden in terms of time and money on the smaller companies and I think relief needs to be given for reporting standards in order to help com-panies through the transition. It’s a different project for the larger multi-national compa-nies as they have the resources, which the smaller companies lack.”

Mixed bagThere is plenty to weigh up as the primary reason for introducing IFRS was to reduce the time and cost of reconciling accounts to the different national standards. Hamm com-ments that keeping separate standards is a significant burden for companies operating in and outside the US.

“I expect to see a greater number of com-panies facing these issues as our economy continues to become more integrated with others around the world. So, for many com-panies in the US, moving to one set of stand-ards is already very important. But for oth-ers, there may not be any current benefit,” Hamm says.

The indefinite delay by the SEC allows for the convergence project between the IASB and FASB to carry on, addressing some of those key technical sticking points around the standards, which does haves its upside. Wallace says that as the standard setters con-tinue to narrow the ‘GAAP gap’, the cost of transition only improves with time, which is again something that is very important to middle market companies.

Partners speaking to IAB are unanimous that comparable cross-border reporting standards are inevitable for US companies. Marshall says: “I would have liked to have seen an adoption of IFRS full stop. I didn’t think that was going to happen for quite some time and that the idea of the endorse-ment mechanism is the most likely way to move if and when the SEC gets to the point of making a decision on it.”

Wallace says that ultimately, where many see this going is that the goal of a global set of standards will be realised.

“The only thing that is yet to be addressed is the timing and amount of effort it requires – it might happen in two years, five years or ten years. Different groups have different positions on that timeline. As you look at it, even if it is five years, that is a reasonably short period given the complexity of what needs to be done,” Wallace says.

Whichever way this is viewed, a significant portion of the US business and regulatory community clearly harbour strong doubts about IFRS, its impact on businesses, inves-tors and the volatility it could cause in the public markets. Inevitably, it cranks up pres-sure on the IASB as there will be countries that are wondering what the indefinite post-ponement by the US means for the credibility of international standards.

“Those who look to the IASB for its rules have every reason in the world to question if the US is not playing by the rules, should they have a member on the IASB, and be par-ticipating in interpreting those rules,” Rohan says.

Marshall says that we have to face it that the Japanese are rethinking the issue and they are looking at the US decision.

“From the balance of views and influence of the IASB, I think this clearly amplifies the influence the Europeans have over standard setting,” Marshall says.

Going forward, this is something that has to be addressed. Marshall continues: “I think that is why the IASB is trying to engage the Asian economies to try and balance it out. But if the US had come on board, I guess those in Europe would have said it was swayed too far to the US side of the pond, but the IASB would have regarded it as a bal-ancing affect. They need to figure this out.”

The interpretations, endorsements and carve-outs by national standard-setters have arguably warped IFRS from the initial vision of the project as outlined by the IASB back in 2001, but perhaps that was unavoidable in such a highly charged, political endeavour. “I do believe there will always be differences,” says Marshall.

“I don’t think the FASB would relinquish its duties to just rubber stamp IFRS propos-als and standards. Was this ever really going to be a one GAAP world? It can be close to one but it won’t be achieved, at least not in my lifetime.”<

8 y August 2012 www.InternationalAccountingBulletin.com

PwC, KPMG, Ernst & Young and Deloitte would appear to have more to fear in China from the rise

of mid-tier firms than from regulations designed to place control of their Chinese operations in local

hands. Paul Golden reports

featurefeature International Accounting BulletinreGuLatIOn In CHIna

Chinese power play

Two decades after the world’s largest accounting firms were first permitted to establish joint ventures by a gov-ernment conscious of the shortage of

experienced accountants available to pro-vide services and meet the increased demand for overseas listings by Chinese enterprises, KPMG became the first of the Big Four to establish a special general partnership.

The new structure created on 1 August places the firm on the same legal footing as other large and mid-size Chinese accounting firms and is an important step in the devel-opment of China’s accounting industry, says Stephen Yiu, chairman of KPMG China and senior partner of KPMG Huazhen.

“The conversion will not affect our staff, the quality of our practice or our ability to serve our clients. The requirement for part-ners to be Chinese Institute of Certified Pub-lic Accountants (CICPA) qualified – a transi-tion period of five years is granted for this process-is in line with international practice. Accounting and auditing qualifications are standardising, which has meant that increas-ing numbers of overseas staff already have become, or are in the process of becoming, CICPA qualified.”

By 2017, Big Four firms must have no more than 20% of partners, who qualified outside China. Partners have to be at least 40 years old and no older than 65.

Yiu is confident that the additional local partners required will be found. “During the transition period we will have increas-ing numbers of local staff being promoted to partner level each year. Therefore, we are on track to meet the requirements for partners under the new rules.”

Raymund Chao, PwC assurance leader for Asia Pacific says his firm has been close-ly following the development of the new regulations by China’s Ministry of Finance.

The potential time frame for transition to special general partnership status was differ-ent for PwC than for the other members of the Big Four in China since its joint venture was not due to expire until 2018, but Chao confirmed that the new structure would be in place within a year at most. “We will sup-port the conversion and move quickly – our current time frame is 2013, possibly early 2013.”

Accord ing to Chao, there have been few discuss ions with c l ients about the implications of the change. “It is a change of legal structure, which does not affect the substance of what we do, so it really has no impact on our ability to service our clients. To a large extent it will be the same people delivering the service,” he says.

He rejects the suggestion that the new reg-ulations are an attempt to limit the influence of the Big Four in China.

“The requirements for locally qualified staff are no different to those in many other countries and clients are looking for qual-ity whether you are a local or international firm,” he says.

However, Chao accepts that the timing could pose some problems saying: “The regulator decided it was time to adopt this change, which could be challenging as it takes quite a number of years to train and develop quality professional accountants.”

Regardless, PwC’s assurance leader for Asia Pacific is confident that it will have enough people to meet the special group partnership criteria.

“We have been going through a process of localisation for more than a decade, creat-ing local partners, so the 60-40 ratio of local CPAs will not be an issue for us,” he says.

Ernst & Young refused to comment beyond confirming that the Ministry of Finance had approved the conversion of

Ernst & Young Hua Ming into a limited lia-bility partnership on 31 July and stating that the move would create more development opportunities for local talent, while Deloitte failed to respond to International Account-ing Bulletin’s request for an interview.

Paul Gillis, co-director of the international MBA program at Peking University’s Guan-ghua School of Management and a regular commentator on accounting issues in China, says the Big Four have little to be worried about.

“It will be business as usual,” he says. “KPMG’s recent reorganisation indicates that the Big Four are going to comply with the new rules only in form, not in spirit. KPMG has set up its new firm with only 25 partners – 15 local and 10 expatriate – despite the fact that it has hundreds of partners. While the firms could have been required to complete-ly localise their partner base, they were able to negotiate a very favourable deal that lets them have up to 40% expatriate partners, going down to 20% in five years. Long term, the Big Four in China will eventually localise at the partner level, but it is apparent that Chinese regulators are going to let them take their own sweet time.”

rise of the mid-tierGillis points out that the larger local firms are growing rapidly.

“In 2011 the top ten domestic firms grew by 38% compared to the Big Four’s growth of 6%,” he says. “Chinese firms affiliated with BDO and RSM are rapidly closing the gap with the Big Four. BDO Lixin in 2011 reached 78% of the size of KPMG, the small-est of the Big Four in China. In the US, BDO is only 12% of the size of KPMG.”

“If present trends continue, both BDO and RSM are likely to match the Big Four in size in China.”

August 2012 y 9www.InternationalAccountingBulletin.com

featureInternational Accounting Bulletin reGuLatIOn In CHIna

“As Chinese companies globalise, this has the potential to restructure the accountancy market worldwide and the Chinese member firms are likely to be the dominant firms in the second tier.”

RSM’s global leader, quality and risk, Bob Dohrer, says changes to the ownership struc-ture of the Big Four in China will result in increased competition in some sectors of the audit market.

“The Chinese government ultimately would like to see an audit profession where the majority of audits of Chinese companies are done by the 10 large Chinese-owned audit firms where the partners are Chinese CPAs, not foreign partners,” he says.

Competing for auditsAudits of state-owned enterprises are cur-rently awarded to firms that are owned by local CPAs. By also forcing the Big Four to become owned by Chinese CPAs, they will now be competing for audits of state-owned enterprises that were previously largely only audited by non-Big Four firms, Dohrer con-tinues.

“Our RSM International member firm in China, RSM China, is currently a dominant player in the audit market for large state-owned enterprises and will now also need to compete against the restructured Big Four firms for this portion of the market.”

The result of these changes, suggests Dohrer, is that competition will be fierce for Chinese firms and networks to end up ulti-mately as one of the top-10 accounting firms in China.

“Organic growth in Chinese firms will be challenging as restructured Big Four firms enter the market, so it is likely that solidify-ing a spot in the top 10 firms in China will involve mergers of existing Chinese firms.”

Complying with the new rules may be disruptive for the Big Four and in particular their client relationships, says Kim Hayward, chair of BDO’s Europe China desk.

“BDO sees this as an opportunity to con-tinue its impressive levels of growth in China, as it will inevitably lead to strong non-Big Four firms in China taking a larger share of the audit market in particular,” he says.

When asked whether he saw future oppor-tunities for partnerships and joint ventures in China, Hayward pointed out that joint ventures can mean different things to differ-ent people.

“There will continue to be opportunities for major accounting firms in China to work in conjunction with other niche boutiques or consultancies as they seek to offer a wider range of services to their clients,” he says.

Since the accounting industry is relatively young in China and the accounting firms are

currently enjoying a surfeit of domestic audit work, acquisition is probably not a priority at present, Hayward continues.

“However, it may prove attractive as a means to achieve even more rapid growth,” he says. “This would bring with it processes and procedures that are already tried and tested in the west, as well as a network that can support what will be a growing and increasingly global client base.

“There would be major implications across the rest of the world’s accounting pro-fessions, bodies and firms, in a world that has been dominated by British and American thinking for the last century.

“The answer to a different question is that undoubtedly over time – and maybe not that long a time frame – the Chinese member firms of the major international accounting networks will become increasingly signifi-cant,” Hayward concludes.

Coco Ke Liu, head of business channel

development at HLB International, observes that if the Big Four became more competitive in servicing local clients (large state-owned enterprises and listed companies) there might be some impact on HLB’s larger Chinese members who share some domestic clients. “It could also make retaining senior roles harder for large indigenous firms,” she says.

Ke Liu refers to an increasing trend for Chinese professional service firms acquiring or setting up overseas practices.

“Encouraged by the Ministry of Finance’s vision to create ‘bigger, stronger and more internationalised’ indigenous account-ing firms and driven by Chinese economic growth, it is very possible that one day a Chinese accounting firm or network will become a major global player, maybe in five or 10 years from now,” she says. “There are already some good examples of Chinese law firms going international.”

As the Chinese economy continues to grow, more and more businesses around the

world will seek entry points into the market. That is the view of Justin Qiu, managing partner audit services at Baker Tilly China. “Entering into a partnership or a joint ven-ture with a local business is a logical route to take, so we may see a rise in these types of structures,” he says.

International visionQiu believes the new regulation will encour-age domestic firms to speed up the cultiva-tion of talented Chinese professionals with the international vision, skills and experience that the market expects.

“The Chinese government is keen to pro-mote the growth of its domestic accounting profession and the international expansion of Chinese firms so in the next decade we might expect five of the biggest audit firms in China to be Chinese, rather than foreign-owned.”

Dickson Leung, senior partner of MSI Global Alliance network member Lehman-Brown, believes that competition for senior local talent might increase, but also feels that there may be opportunities to win business from companies who would never have pre-viously considered using a firm outside the Big Four.

BKR International member firm East Asia Sentinel partner Robert Lew reckons the domestic market for auditing private compa-nies is not attractive to smaller foreign CPA firms.

He says: “The fee scale is low and the work is not in line with international account-ing standards. Where they are conducting an audit on separate financial statements prepared under international account-ing standards, they can still do so with-out being a qualified CPA firm in China. For mid-tier auditing firms that want to establish a presence in China, they would already have engaged local Chinese CPAs to set up a purely local practice.

“As for Chinese CPA firms, if they want to expand into the field of audit-ing listed companies, they would need more local CPAs and not foreign ones. For that I cannot imagine how expanding into a foreign accounting network would help. The only reason a China-based CPA firm may need to expand into the foreign accounting field is where their Chinese clients are beginning to acquire overseas subsidiar-ies and expand into foreign markets,” Lew concludes.

As new localisation rules take effect, one thing is clear. China is taking a different approach to regulating the accounting mar-ket with a clear vision to grow its talent and to try to challenge the western monopoly in the global professional services market.<

“the Chinese government ultimately would like to see an audit profession where the majority of audits of Chinese companies are done by the 10 large Chinese-owned audit firms where the partners are Chinese CPas.”

Bob Dohrer, RSM

today, India is producing more accountants and the market is offering them more opportunities. but uncertainty around key regulations is hurting the profession-and also compromising the environment for Indian business. Swati Prasad reports

revenue

n InDIa

at a glance

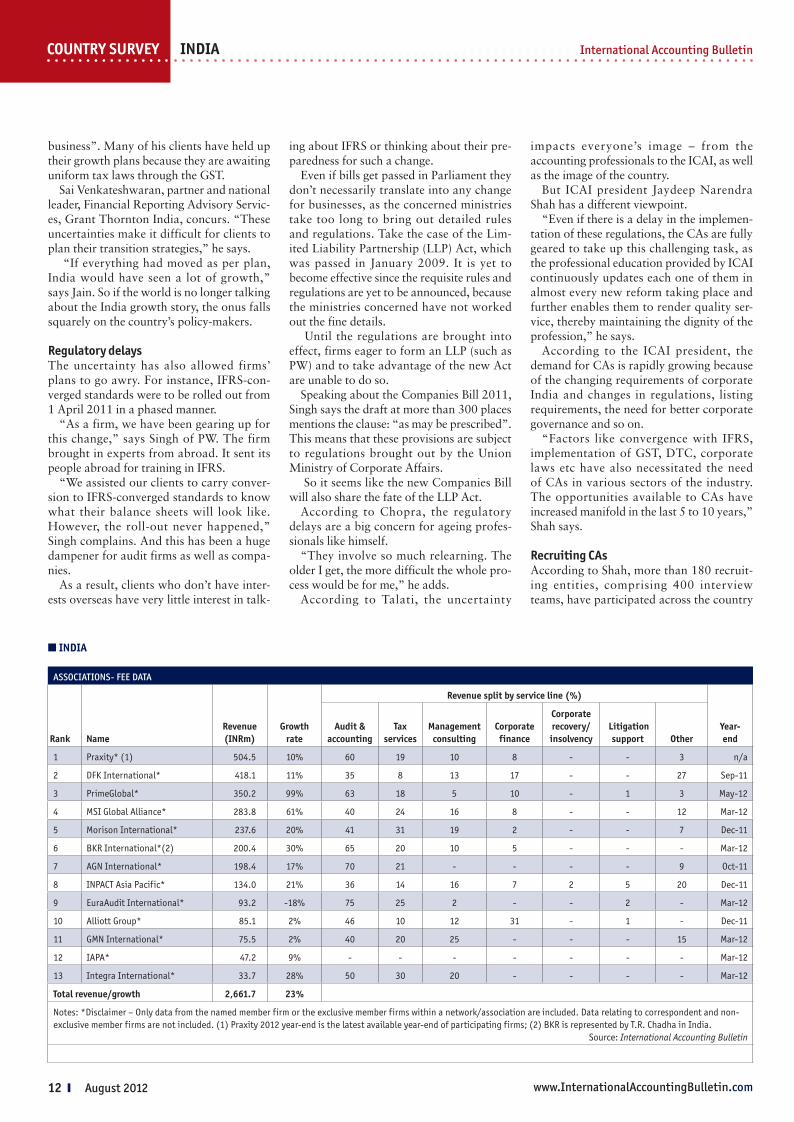

Most revenue: Grant Thornton India, INR1.87bnLeast revenue: ECOVIS International, INR26mHighest growth: PrimeGlobal, 99%Lowest growth: IAPA, -34%

Largest workforce: DFK International 1,169Smallest workforce: ECOVIS International, 33Most partners: PrimeGlobal, 88Most offices: PrimeGlobal, 33

GDP: $1.7trn GDP per head: $1,467Inflation (CPI): 8.6%Current account balance: -4.4% of GDPGovernment budget: -6.2% of GDPunemployment rate: 9.8%Population: 1.2bnNotes: Totals apply to IAB-surveyed data only, this includes firms that belong to global networks and associations.

Source: International Accounting Bulletin, Timetric, IMF

eCOnOMIC InDICatOrS

Staff

Surrounded by obstacles

www.InternationalAccountingBulletin.com August 2012 y 11

Iab COuntry SurveyInternational Accounting Bulletin InDIa

T he fiscal year 2011/12 was frustrat-ing for Indian business and that has had a direct bearing on the account-ing profession. India was to roll-out

IFRS-converged standards in April 2011, but that didn’t happen. And, similarly, a lot of other pending regulations – such as the Direct Tax Code (DTC), Goods and Service Tax (GST), the Companies Bill 2011 – didn’t see the light of the day. This policy paralysis meant that companies had to put some of their expansion plans on hold.

“When our clients do well, we do well,” says Vinod Kumar Jain, proprietor of Vinod Kumar Jain & Co, a small audit firm based in Mumbai.

During the past fiscal year, his firm grew by 15% to 20% as opposed to 30% in the previous year. “When our clients embark on a new project, they need our services for tax planning, consultancy and for arranging funds,” he says. “And when their revenues fall, audit firms are not able to revise their fee.”

Most firms had another year of strong growth, with an average increase of 20% in fee income among firms surveyed by IAB. The survey does not feature the Big Four revenues as their results are kept hidden.

This is due to fears that combining audit figures with those in other services will be viewed as being in breach of India’s inde-pendence rules.

“It was a really good year for us,” says Sunil Talati, senior partner at Talati & Tala-

n InDIa

networks - fee dAtA

rank namerevenue (Inrm)

Growth rate

revenue split by service line (%)

year-end

audit & accounting

tax services

Management consulting

Corporate finance

Corporate recovery/

insolvency Litigation

support Other

1 Grant Thornton India* 1,878.2 19% 38 20 23 19 - - - Mar-12

2 Nexia International* 871.1 4% 50 20 30 - - - - Jun-12

3 RSM International* 814.3 34% 37 16 17 1 - - 29 Jun-12

4 BDO India* 798.5 28% 34 18 27 12 - - 9 Mar-12

5 HLB India* 493.8 27% 66 8 13 - - - 13 Mar-12

6 Mazars* 486.0 11% 60 20 10 7 - - 3 Aug-12

7 PKF International* 291.2 10% 56 8 24 2 - - 10 Mar-12

8 Moore Stephens International*

280.4 16% 63 16 12 4 - - 5 Dec-11

9 Kreston International* 132.5 30% 48 36 8 3 - - 5 Oct-11

10 ECOVIS International* 26.0 13% - 8 58 23 - 4 7 Mar-12

total revenue/growth 6,072 19%

Notes: *Disclaimer – Only data from the named member firm or the exclusive member firms within a network/association is included. Data relating to correspondent and non-exclusive member firms is not included.

Source: International Accounting Bulletin

ti Chartered Accountants. Last year, Talati received a large number of applications from CAs seeking both temporary and permanent employment.

According to Amarjit Chopra, a for-mer president of the Institute of Chartered Accountants of India (ICAI), the slowdown did not affect medium-sized firms.

“It affected the bigger firms more. The mid-size firms did not add new clientele. But there was no loss of fee or business,” Chopra says.

Then again, even for a big firm like Grant Thornton India, last year was a good one. It grew by 19%, according to data submitted by the firm. Grant Thornton India national managing partner Vishesh Chandiok hopes to maintain this rate of growth until 2015.

For Price Waterhouse, it was a “normal” year. “We carried out business as usual,” says Price Waterhouse partner Harinderjit Singh, without giving further details.

One common grudge audit firms of all sizes hold against the government is that the growth rates could have been a lot better had the pending reforms been kick-started.

Failure to do this led to a lot of uncertainty in the business environment and, as a result, audit firms are unsure about what to advise their clients on key issues such as IFRS, the Companies Bill 2011 and impending tax regulations such as DTC and GST.

Furthermore, the business environment has been getting tougher by the day with vol-atility in the rupee and increased inflation.

According to Jain, regulatory uncertainty is just one of four key challenges faced by Indian business – the other three being high interest rates, exchange rate fluctuations and inflation.

“We have several importers and build-ers as our clients,” he says. “The importers faced heavy losses due to the devaluation in the rupee. And the builders didn’t get gov-ernment approvals for new projects. The entire construction industry in Mumbai has been stagnant for the last two years.”

Policy paralysisThe regulatory environment in the country is undoubtedly challenging since there is a spate of new regulation that has been on the table for a number of years, with no indica-tion of when they might see the light of day.

“From a business perspective that’s a very unstable place to be, both for clients and for practitioners, as one can’t run businesses without reasonable predictability of the reg-ulations that apply to our clients or to us,” says Chandiok.

Instead of discussing the content of the legislation and how it pushes the progress and development agenda, practitioners are left to struggle with timing.

“For instance, whether mandatory firm rotation is appropriate or not is no longer the key concern in my mind, it’s the timing,” says Chandiok.

According to Jain, “indecision has been the biggest cruelty inflicted upon Indian

12 y August 2012 www.InternationalAccountingBulletin.com

COuntry Survey International Accounting BulletinInDIa

business”. Many of his clients have held up their growth plans because they are awaiting uniform tax laws through the GST.

Sai Venkateshwaran, partner and national leader, Financial Reporting Advisory Servic-es, Grant Thornton India, concurs. “These uncertainties make it difficult for clients to plan their transition strategies,” he says.

“If everything had moved as per plan, India would have seen a lot of growth,” says Jain. So if the world is no longer talking about the India growth story, the onus falls squarely on the country’s policy-makers.

regulatory delaysThe uncertainty has also allowed firms’ plans to go awry. For instance, IFRS-con-verged standards were to be rolled out from 1 April 2011 in a phased manner.

“As a firm, we have been gearing up for this change,” says Singh of PW. The firm brought in experts from abroad. It sent its people abroad for training in IFRS.

“We assisted our clients to carry conver-sion to IFRS-converged standards to know what their balance sheets will look like. However, the roll-out never happened,” Singh complains. And this has been a huge dampener for audit firms as well as compa-nies.

As a result, clients who don’t have inter-ests overseas have very little interest in talk-

n InDIa

AssoCIAtIons- fee dAtA

rank namerevenue (Inrm)

Growth rate

revenue split by service line (%)

year-end

audit & accounting

tax services

Management consulting

Corporate finance

Corporate recovery/

insolvency Litigation

support Other

1 Praxity* (1) 504.5 10% 60 19 10 8 - - 3 n/a

2 DFK International* 418.1 11% 35 8 13 17 - - 27 Sep-11

3 PrimeGlobal* 350.2 99% 63 18 5 10 - 1 3 May-12

4 MSI Global Alliance* 283.8 61% 40 24 16 8 - - 12 Mar-12

5 Morison International* 237.6 20% 41 31 19 2 - - 7 Dec-11

6 BKR International*(2) 200.4 30% 65 20 10 5 - - - Mar-12

7 AGN International* 198.4 17% 70 21 - - - - 9 Oct-11

8 INPACT Asia Pacific* 134.0 21% 36 14 16 7 2 5 20 Dec-11

9 EuraAudit International* 93.2 -18% 75 25 2 - - 2 - Mar-12

10 Alliott Group* 85.1 2% 46 10 12 31 - 1 - Dec-11

11 GMN International* 75.5 2% 40 20 25 - - - 15 Mar-12

12 IAPA* 47.2 9% - - - - - - - Mar-12

13 Integra International* 33.7 28% 50 30 20 - - - - Mar-12

total revenue/growth 2,661.7 23%

Notes: *Disclaimer – Only data from the named member firm or the exclusive member firms within a network/association are included. Data relating to correspondent and non-exclusive member firms are not included. (1) Praxity 2012 year-end is the latest available year-end of participating firms; (2) BKR is represented by T.R. Chadha in India.

Source: International Accounting Bulletin

ing about IFRS or thinking about their pre-paredness for such a change.

Even if bills get passed in Parliament they don’t necessarily translate into any change for businesses, as the concerned ministries take too long to bring out detailed rules and regulations. Take the case of the Lim-ited Liability Partnership (LLP) Act, which was passed in January 2009. It is yet to become effective since the requisite rules and regulations are yet to be announced, because the ministries concerned have not worked out the fine details.

Until the regulations are brought into effect, firms eager to form an LLP (such as PW) and to take advantage of the new Act are unable to do so.

Speaking about the Companies Bill 2011, Singh says the draft at more than 300 places mentions the clause: “as may be prescribed”. This means that these provisions are subject to regulations brought out by the Union Ministry of Corporate Affairs.

So it seems like the new Companies Bill will also share the fate of the LLP Act.

According to Chopra, the regulatory delays are a big concern for ageing profes-sionals like himself.

“They involve so much relearning. The older I get, the more difficult the whole pro-cess would be for me,” he adds.

According to Talati, the uncertainty

impacts everyone’s image – from the accounting professionals to the ICAI, as well as the image of the country.

But ICAI president Jaydeep Narendra Shah has a different viewpoint.

“Even if there is a delay in the implemen-tation of these regulations, the CAs are fully geared to take up this challenging task, as the professional education provided by ICAI continuously updates each one of them in almost every new reform taking place and further enables them to render quality ser-vice, thereby maintaining the dignity of the profession,” he says.

According to the ICAI president, the demand for CAs is rapidly growing because of the changing requirements of corporate India and changes in regulations, listing requirements, the need for better corporate governance and so on.

“Factors like convergence with IFRS, implementation of GST, DTC, corporate laws etc have also necessitated the need of CAs in various sectors of the industry. The opportunities available to CAs have increased manifold in the last 5 to 10 years,” Shah says.

recruiting CasAccording to Shah, more than 180 recruit-ing entities, comprising 400 interview teams, have participated across the country

www.InternationalAccountingBulletin.com August 2012 y 13

Iab COuntry SurveyInternational Accounting Bulletin InDIa

4

to recruit more than 3,100 newly qualified CAs. The average starting salary offered to newly qualified CAs was around Rs500,000 per annum ($9,011). An annual package of Rs1.4m ($25,230) was offered for domestic postings and Rs2.5m ($ 45,053) for interna-tional positions.

With more students passing the exam,

n InDIa

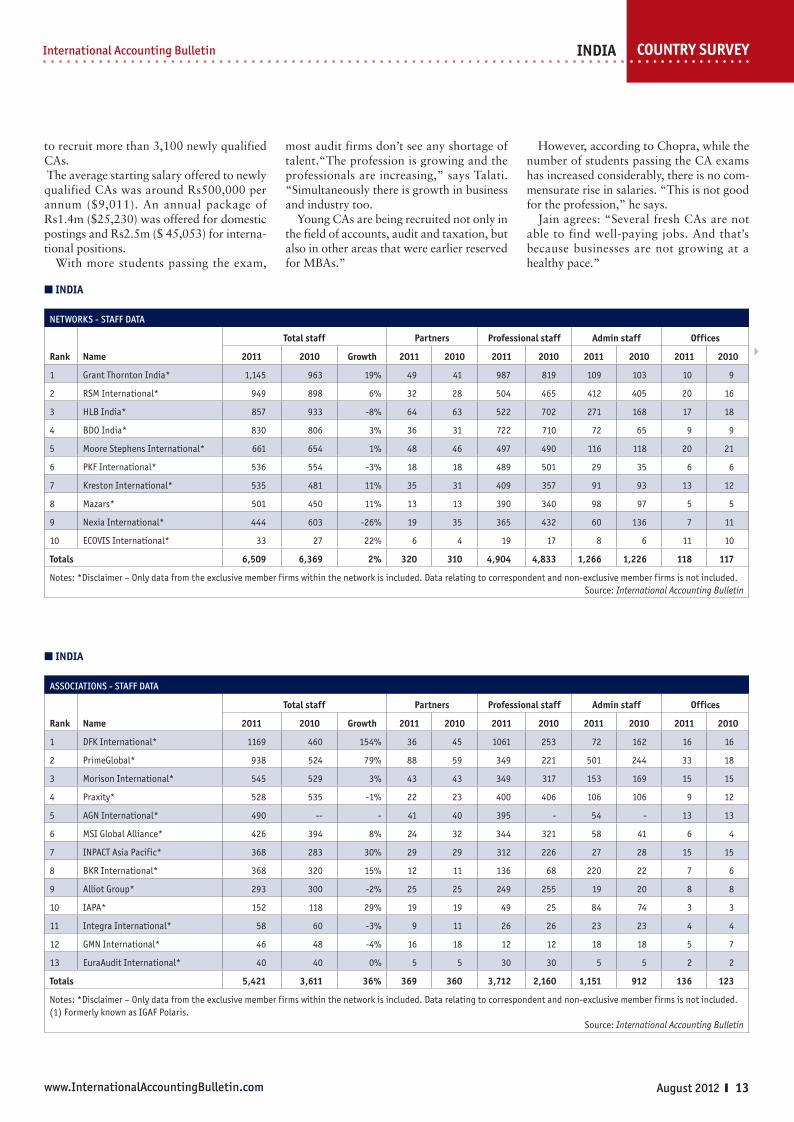

networks - stAff dAtA

rank name

total staff Partners Professional staff admin staff Offices

2011 2010 Growth 2011 2010 2011 2010 2011 2010 2011 2010

1 Grant Thornton India* 1,145 963 19% 49 41 987 819 109 103 10 9

2 RSM International* 949 898 6% 32 28 504 465 412 405 20 16

3 HLB India* 857 933 -8% 64 63 522 702 271 168 17 18

4 BDO India* 830 806 3% 36 31 722 710 72 65 9 9

5 Moore Stephens International* 661 654 1% 48 46 497 490 116 118 20 21

6 PKF International* 536 554 -3% 18 18 489 501 29 35 6 6

7 Kreston International* 535 481 11% 35 31 409 357 91 93 13 12

8 Mazars* 501 450 11% 13 13 390 340 98 97 5 5

9 Nexia International* 444 603 -26% 19 35 365 432 60 136 7 11

10 ECOVIS International* 33 27 22% 6 4 19 17 8 6 11 10

totals 6,509 6,369 2% 320 310 4,904 4,833 1,266 1,226 118 117

Notes: *Disclaimer – Only data from the exclusive member firms within the network is included. Data relating to correspondent and non-exclusive member firms is not included. Source: International Accounting Bulletin

n InDIa

AssoCIAtIons - stAff dAtA

rank name

total staff Partners Professional staff admin staff Offices

2011 2010 Growth 2011 2010 2011 2010 2011 2010 2011 2010

1 DFK International* 1169 460 154% 36 45 1061 253 72 162 16 16

2 PrimeGlobal* 938 524 79% 88 59 349 221 501 244 33 18

3 Morison International* 545 529 3% 43 43 349 317 153 169 15 15

4 Praxity* 528 535 -1% 22 23 400 406 106 106 9 12

5 AGN International* 490 -- - 41 40 395 - 54 - 13 13

6 MSI Global Alliance* 426 394 8% 24 32 344 321 58 41 6 4

7 INPACT Asia Pacific* 368 283 30% 29 29 312 226 27 28 15 15

8 BKR International* 368 320 15% 12 11 136 68 220 22 7 6

9 Alliot Group* 293 300 -2% 25 25 249 255 19 20 8 8

10 IAPA* 152 118 29% 19 19 49 25 84 74 3 3

11 Integra International* 58 60 -3% 9 11 26 26 23 23 4 4

12 GMN International* 46 48 -4% 16 18 12 12 18 18 5 7

13 EuraAudit International* 40 40 0% 5 5 30 30 5 5 2 2

totals 5,421 3,611 36% 369 360 3,712 2,160 1,151 912 136 123

Notes: *Disclaimer – Only data from the exclusive member firms within the network is included. Data relating to correspondent and non-exclusive member firms is not included. (1) Formerly known as IGAF Polaris.

Source: International Accounting Bulletin

most audit firms don’t see any shortage of talent.“The profession is growing and the professionals are increasing,” says Talati. “Simultaneously there is growth in business and industry too.

Young CAs are being recruited not only in the field of accounts, audit and taxation, but also in other areas that were earlier reserved for MBAs.”

However, according to Chopra, while the number of students passing the CA exams has increased considerably, there is no com-mensurate rise in salaries. “This is not good for the profession,” he says.

Jain agrees: “Several fresh CAs are not able to find well-paying jobs. And that’s because businesses are not growing at a healthy pace.”

www.InternationalAccountingBulletin.com14 y August 2012

COuntry Survey International Accounting BulletinInDIa

However, for PW, talent continues to be a challenge. “Our firm has its own criteria for recruitments. We look for CAs with the right communication and presentation skills. And that’s not something we find very eas-ily,” says Singh.

Shying away from auditThe Satyam fraud has made statutory audit the non-preferred practice for CAs.

“Today, CAs do not want to get into statutory audit. They want to do taxation, M&As, transfer pricing… but not audit,” says Chopra.

And that’s because audit will always be more onerous and more obligatory. “The fee is more in other practices. The remuneration for auditors is not commensurate with the kind of work they do,” Chopra adds.

Even smaller firms find non-audit services far more lucrative.

“Tax practice in the field of transfer pric-ing and international taxation is more lucra-tive, but is monopolised by the big few,” says Talati.

He feels it is high-time a mid-size firm like his took a plunge into these service lines. He is of the view that smaller firms can render equivalent services at almost half the price the bigger firms are charging.

“When we hold exit interviews, we find that a lot of people do not want to do statu-tory audits,” says Singh.

PW has been trying to make the job more interesting for auditors by varying the type of industry they are working for. “Audit can also involve very long hours of work. The quality of life gets impacted,” says Singh.

But more than that, it’s the fact that in the event of a fraud, everyone tends to point fin-gers at the auditors.

“The media does not cover practices like consultancy and taxation. For instance, no one blamed the consultants when Vodafone got into a tax dispute with the Indian government. People only point fingers at the auditors,” says Chopra.

“Post Satyam, there have been a lot of misunderstandings and expectation gaps

insofar as understanding the role of auditors is concerned,” says PW’s Singh.

Having been the auditors for Satyam, the firm has been in constant communication with its staff, its clients and with the govern-ment on this matter.

And this constant dialogue has helped, because Singh feels that the level of aware-ness about the role of auditors has increased.

“After the second report of the Parliamen-tary standing committee on the Companies Bill 2011, we have seen that some of the harsh provisions (pertaining to the role and penalties for auditors) have been reconsid-ered,” he says.

Looking into the futureOn the one hand, the delay in passing regula-tions is undoubtedly a concern. On the other, it seems that the contents of some these regu-lations are a bigger concern, especially, in the case of the Companies Bill 2011.

According to Chandiok, the coming year has the potential to shake up the Indian pro-fession rapidly, if mandatory firm rotation and restrictions in the scope of services were to be enacted as part of the revised Compa-nies Bill.

When passed, the new Act would do three things, he says. One, it could wipe out the old Indian accounting firms which have delivered excellent service to their clients, but unfortunately have not been great at marketing their services. Two, it would lead to significant additional focus on going to market as opposed to enhancing and improving quality (of service) among the large firms.

Three, auditors would not be able to pro-vide all the value-added services that their clients actually care about, thereby both reducing the ability to add value to clients while, at the same time, potentially leading to significant enhancement of audit fees, as was the case in the US post the Sarbanes Oxley Act.

As part of the Companies Bill, the Indian government is planning an overhaul of the audit and financial services sector to guard

against corporate frauds and irregularities. A major proposal made in the bill includes

the separation of audit and non-audit func-tions when offered by the same firm.

Once cleared, audit firms will no longer be able to offer non-audit services like invest-ment advisory and management services to companies, as the new law would seek to prohibit activities that may lead to any con-flict of interest, leading to a potential fraud. Several large audit firms are opposed to this proposal as it would hit their operation.

“Audit rotation can also impact audit quality,” says Venkateshwaran.

Firms would not have the incentive to invest additional time in their clients since their involvement would be temporary, along with the fact that they would not be able to render other services to the client.

Moreover, the penalties being proposed in the draft bill can make the audit profes-sion very unattractive, says Venkateshwaran. “All this could result in a situation where the profession is unable to attract and retain the best talent, which would severely impact audit quality over time,” he adds.

The biggest issue for the profession, according to Chandiok, remains the lack of vision.

“China has defined a vision of where it would like the domestic profession to be by 2020 and is taking active steps to help build scale in local accountancy firms so that they can meet the needs of growing and global Chinese companies,” says Chandiok.

In contrast “we seem to think of a new rule every few months, and hope it will be a quick fix to unfortunate events like Satyam,” he adds.

Create a stable atmosphereThe uncertain regulatory environment has undoubtedly had an impact on India’s growth and the government needs to create a more stable atmosphere in order to recreate the faith the world had in the India growth story. “People are not seeing India as a reli-able country. People talk more about China, than India now,” says Chopra.

However, Chopra feels that 2012-13 will be a lot better, with the general election due in 2014. “I am a born optimist. India should be clocking an economic growth rate of 6% to 7% this financial year.

And the government will do something about the pending regulations,” he says.

According to Shah, although global mar-kets are in a stabilising phase, the Indian market is more or less resilient to the effect of the downturn and will flourish in the years to come. For now, one can only take solace in Chopra and Shah’s optimism.<

n InDIa

netWOrK or aSSOCIatIOn fIrM aDDItIOnS, MerGerS and aCQuISItIOnS

DFK International Added: Cross Domain Solutions, Bangalore

MSI Global Alliance Added: Divakar Vijayasarathy and Associates; Chennai and Balakrishna Consulting LLP, Bangalore

RSM International Added: a firm in Gujarat; and joint venture with US member firm of RSM International RSM McGladrey

Source: International Accounting Bulletin

www.InternationalAccountingBulletin.com August 2012 y 15

Iab COuntry SurveyInternational Accounting Bulletin tHe netHerLanDS

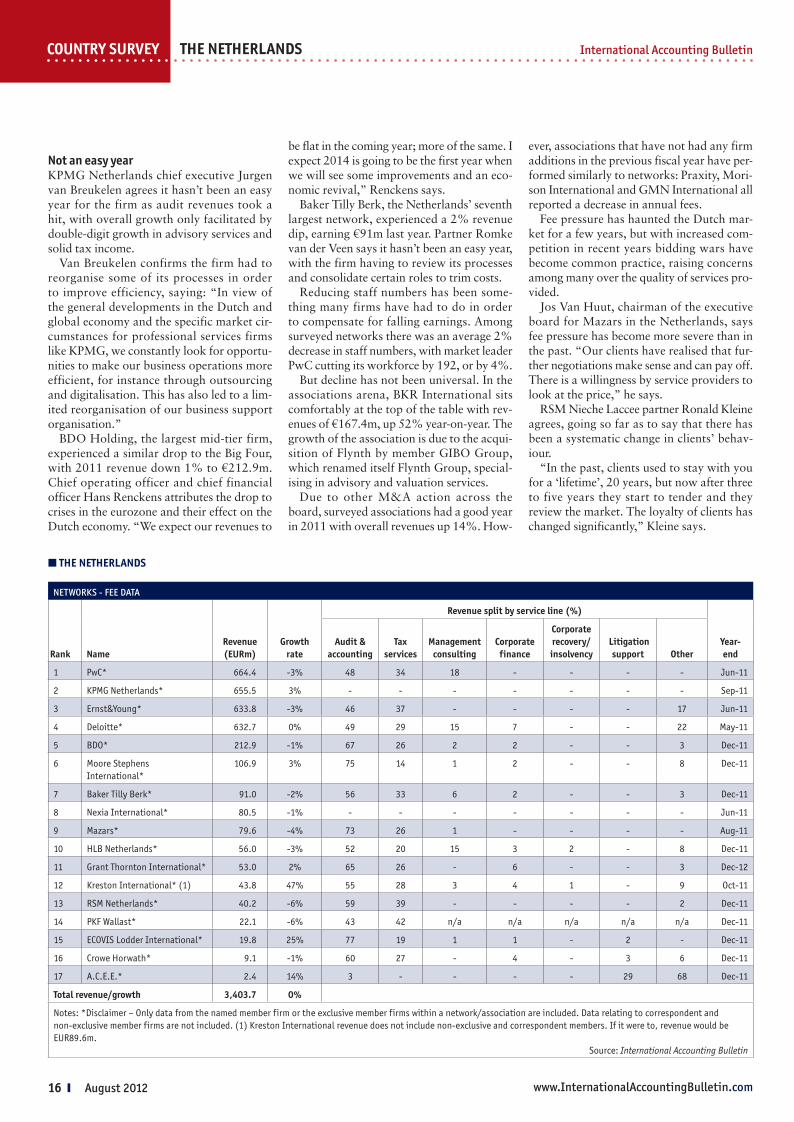

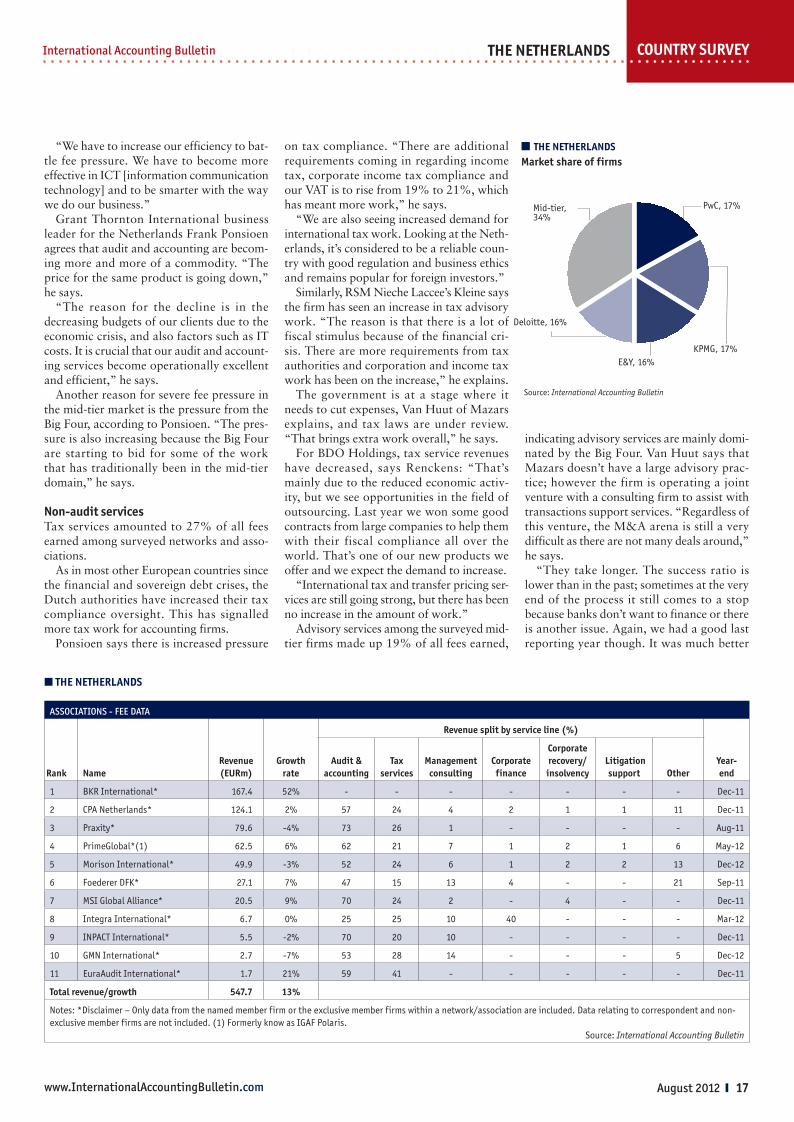

a slow economy, relentless fee pressure and a struggle to gain new clients have become perennial problems for the Dutch accountancy profession. nevertheless, fi rm leaders are convinced that times could become a lot more interesting, at least for the mid-tier, if new national audit regulation is introduced, reports ana Gyorkos

n tHe netHerLanDS

at a glance

Most revenue: PwC, EUR664.4mLeast revenue: EuraAudit, EUR1.7mHighest growth: Kreston Intr, 47%Lowest growth: GMN International, -7%

Largest workforce: Deloitte, 4,472Smallest workforce: Eura Audit, 14Most partners: PwC, 253Most offices: BKR International, 70

GDP: EUR557.8bnGDP growth: 1%GDP per capita (PPP): 33,426 unitsInflation (CPI): 2.4%Current account balance: 7.4% of GDPunemployment rate: 4.5%Population: 16.6m

revenue per employee: EUR135,349revenue per partner: EUR2.3mPartner density: 1 partner per 21 staff

Notes: Totals apply to IAB surveyed data only, this includes firms that belong to global networks and associations.

Source: International Accounting Bulletin, IMF

Iab Survey InDICatOrS

eCOnOMIC InDICatOrS

Staff

revenue

While accounting firms across Europe wait with great interest for the out-come of the European Parliament’s discussions on audit reform follow-

ing a European Commission proposal, those in the Netherlands have the added complica-tion that their government has already laid foundations for additional regulatory inter-vention.

The Dutch government has looked at introducing measures such as mandatory firm rotation and restrictions on offering non-audit services to audit clients, independ-ent of comparable proposals currently being debated on a European level.

Whether those measures will be enforced remains to be seen, since the Dutch lower house of parliament has yet to debate the matter. What’s more, the country – currently without a government – is holding a general election on 12 September, after which the new administration may have more immediate

concerns than audit reform. While most firm leaders predict a decision