Attracting and Maintaining Institutional Investment: Solar PV

70

-

Upload

eversheds -

Category

Technology

-

view

1.072 -

download

2

Transcript of Attracting and Maintaining Institutional Investment: Solar PV

Presentation Outline

• Introduction to SgurrEnergy

• Resource & energy yield

• Technology

• Completion risk

• EPC and O&M contracts

• Financial modelling

• Key messages

SgurrEnergy

• Leading renewable energy consultancy

• Formed in 2002

• Joined Wood Group in 2010

• Global network of offices

• 100+ experienced consultants

• People and technology focused

• Company wide triple BSI accreditation & UKAS ISO/IEC accreditation for wind farm power curve analysis

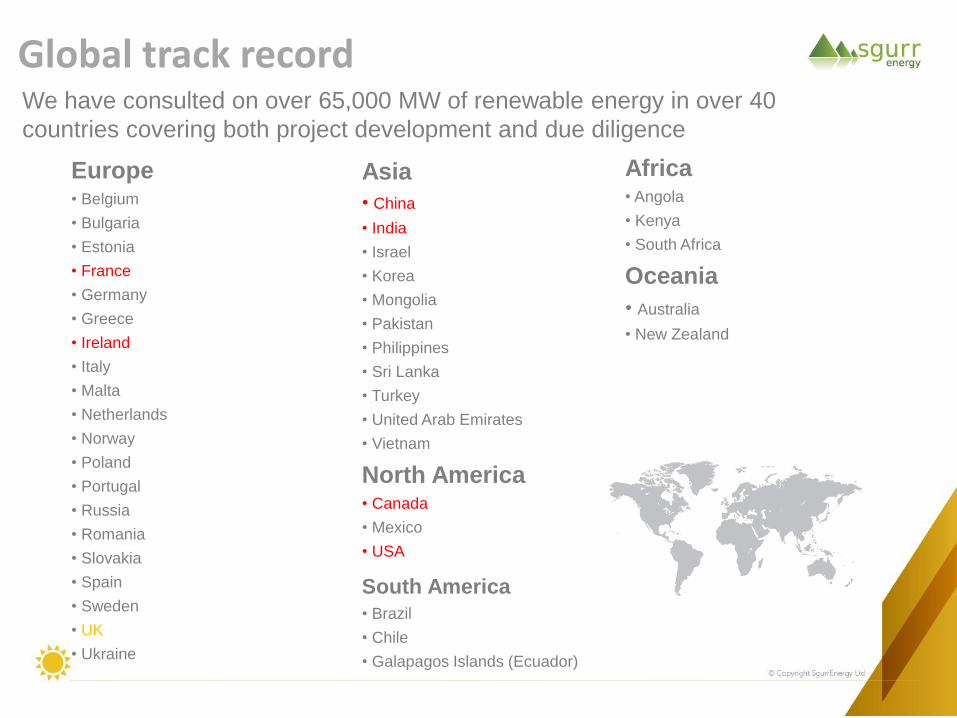

Global track record

Europe • Belgium

• Bulgaria

• Estonia

• France

• Germany

• Greece

• Ireland

• Italy

• Malta

• Netherlands

• Norway

• Poland

• Portugal

• Russia

• Romania

• Slovakia

• Spain

• Sweden

• UK

• Ukraine

Africa • Angola

• Kenya

• South Africa

Oceania

• Australia

• New Zealand

We have consulted on over 65,000 MW of renewable energy in over 40

countries covering both project development and due diligence

Asia

• China

• India

• Israel

• Korea

• Mongolia

• Pakistan

• Philippines

• Sri Lanka

• Turkey

• United Arab Emirates

• Vietnam

North America • Canada

• Mexico

• USA

South America

• Brazil

• Chile

• Galapagos Islands (Ecuador)

Experience

Due Diligence – Owner, Lender & Acquisition • Acquisition due diligence for solar PV plant, Italy, 25 MW, 2012, confidential client

• Lenders due diligence of Charanka solar PV plant, India, 15 MW, 2012, Standard Chartered

• Technical due diligence of Lorraine solar PV plant, France, 36 MW, 2012, Marguerite Advisor

• Acquisition due diligence for European solar PV portfolio, 120+ MW, 2011, confidential client

• Technical due diligence for solar PV project, France, 36 MW, 2011, confidential client

• Provisional Acceptance and witnessing commissioning, UK, 4.4 MW, 2011, Low Carbon Solar

• Owner’s Engineer/ Solar Resource Assessment for proposed PV Plant, Pakistan, 2011, Sapphire

• Owners Engineer/ Design verification and handover acceptance support, Belgium, 6.5 MW, 2011

• Acquisition due diligence of Rete Rinnovabile Solar PV Portfolio, Italy, 150 MW, 2010, Terra Firma Capital Partners

• Acquisition due diligence for solar PV project, Spain, 6.7 MW, 2011, confidential client

• Lender’s Engineer/ Construction monitoring on three PV plants, UK, 15 MW, 2011, Low Carbon

• Solar Rooftop PV Portfolio Technical Due Diligence, France, 2.4 MW, 2010, confidential client

• Solar Rooftop and Ground mounted PV Portfolio technical due diligence, France, 170 MW+, 2010, confidential client

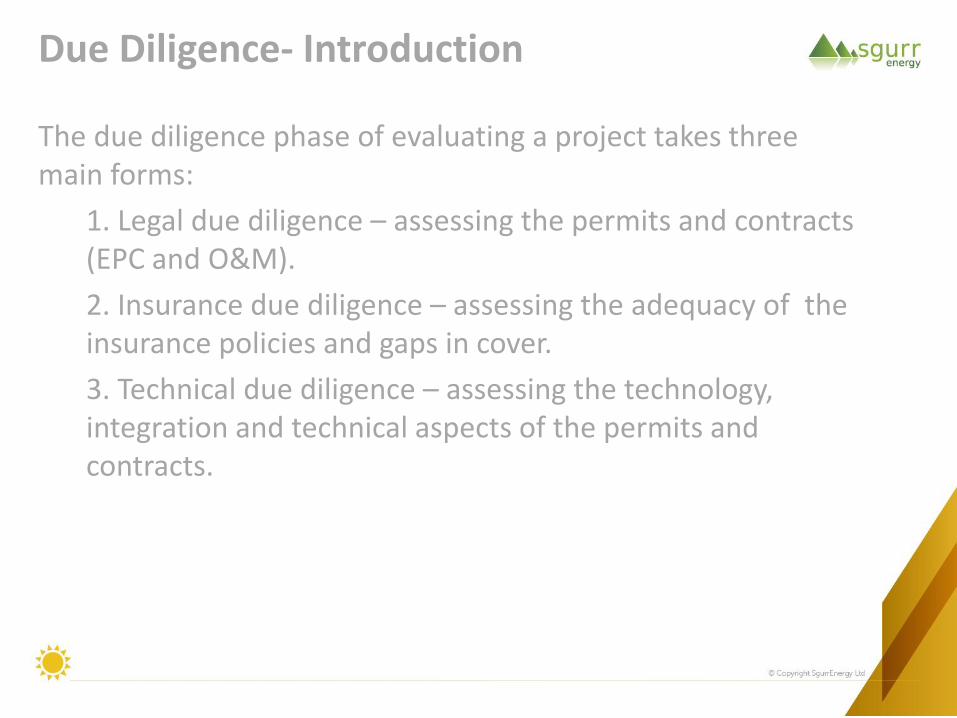

Due Diligence- Introduction

The due diligence phase of evaluating a project takes three main forms:

1. Legal due diligence – assessing the permits and contracts (EPC and O&M).

2. Insurance due diligence – assessing the adequacy of the insurance policies and gaps in cover.

3. Technical due diligence – assessing the technology, integration and technical aspects of the permits and contracts.

• Feasibility – Solar Resource & Energy Yield

• Planning & Permitting

• Technical development – Grid connection

– Design and Technology

• Contracts – EPC

– O&M

– Power Purchase Agreement (PPA)

• Financial Close

• Construction – Provisional Acceptance Test

• Operation - Revenue – Final Acceptance Test

Project Stages

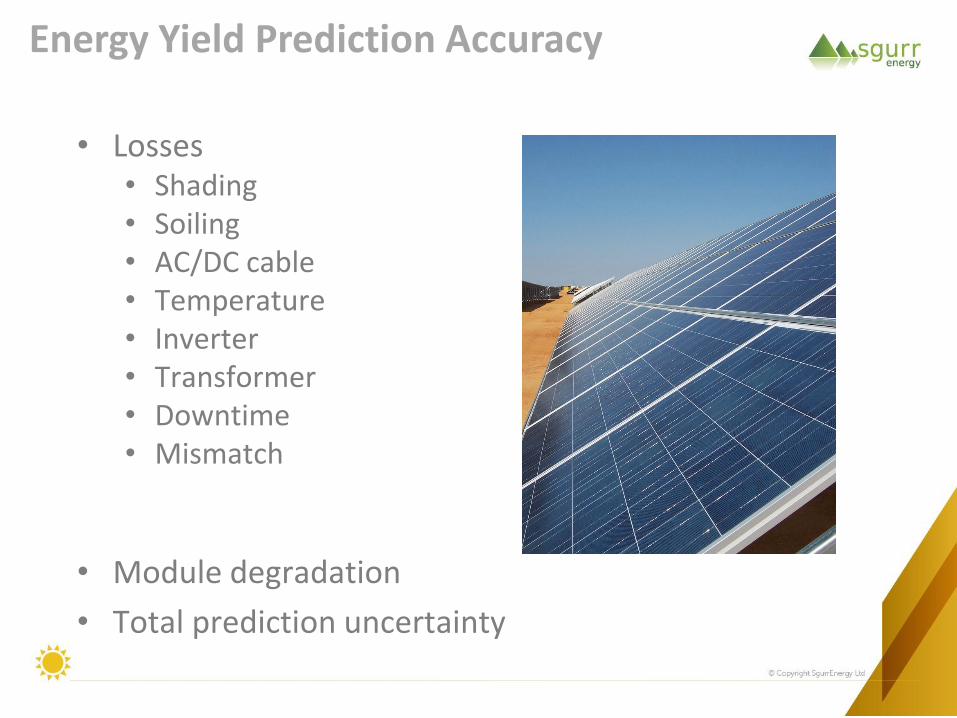

• Losses • Shading • Soiling • AC/DC cable • Temperature • Inverter • Transformer • Downtime • Mismatch

• Module degradation

• Total prediction uncertainty

Energy Yield Prediction Accuracy

• Power is approximately proportional to the plane of array irradiance

• Uncertainty in the yield prediction is dominated by uncertainty in the solar irradiation

Effect of Solar Resource on Energy Yield

Solar Resource Assessment

• Require historical data close to site and over a long period of time

• Data sources typically provide global horizontal irradiation (GHI) in hourly intervals

• Use transposition algorithms to convert from the horizontal plane to the tilted plane

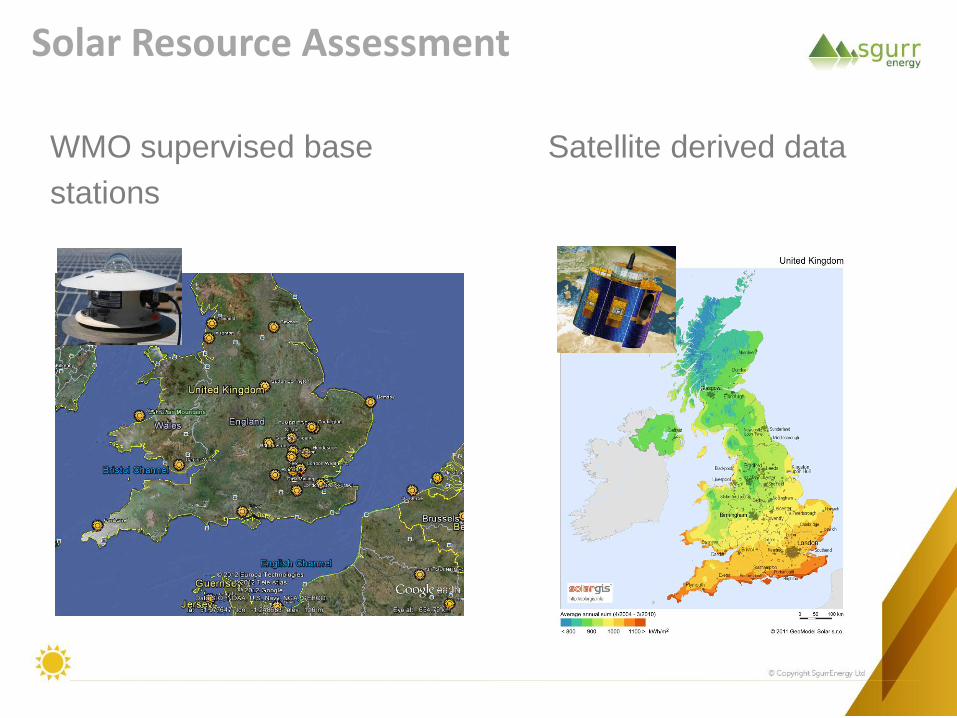

Solar Resource Assessment

WMO supervised base

stations

Satellite derived data

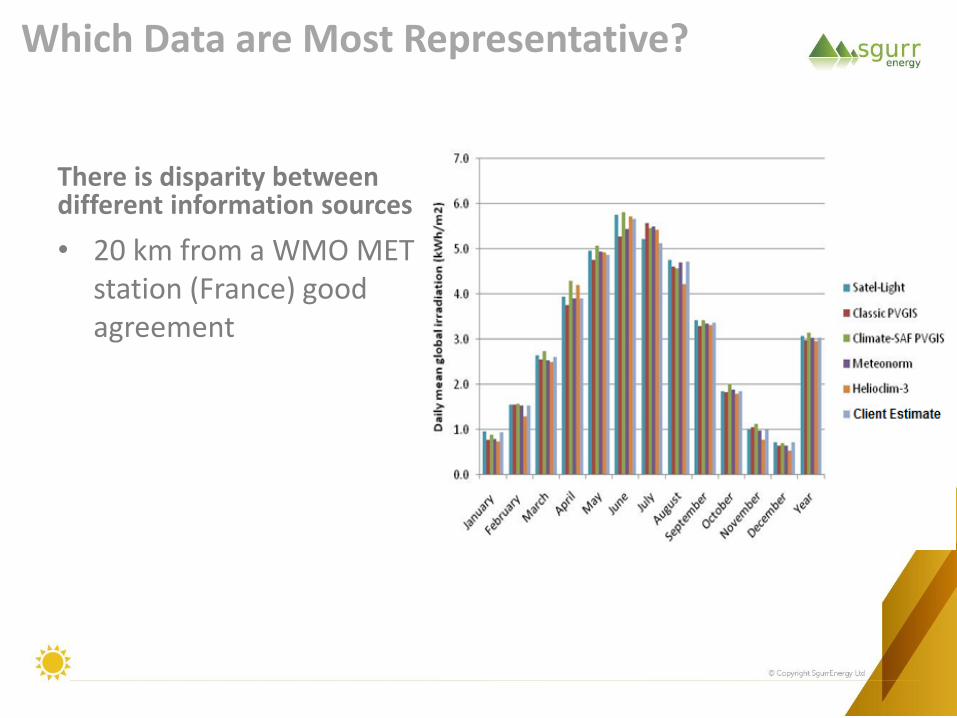

Which Data are Most Representative?

There is disparity between different information sources

• 20 km from a WMO MET station (France) good agreement

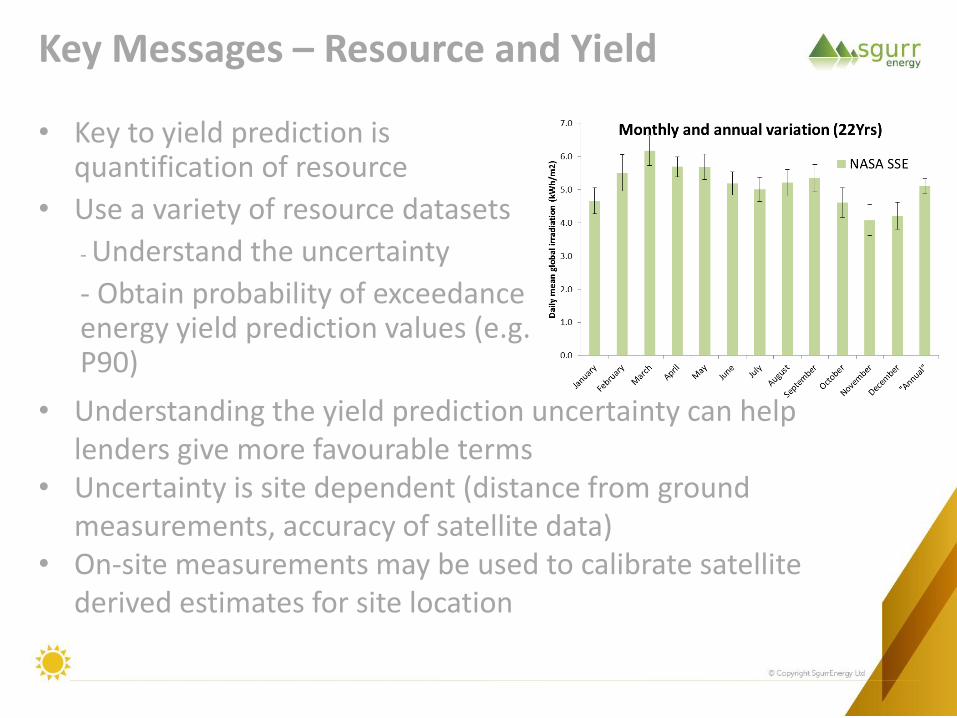

Key Messages – Resource and Yield

• Key to yield prediction is quantification of resource

• Use a variety of resource datasets

- Understand the uncertainty

- Obtain probability of exceedance energy yield prediction values (e.g. P90)

• Understanding the yield prediction uncertainty can help lenders give more favourable terms

• Uncertainty is site dependent (distance from ground measurements, accuracy of satellite data)

• On-site measurements may be used to calibrate satellite derived estimates for site location

Resource and Yield– Common Mistakes

• Only using one resource dataset

• No assessment of inter-annual variability in resource

• No assessment of the yield uncertainty (P90)

• No assessment of inter-row shading or horizon shading losses

• Ignoring shading from nearby obstructions including poles, control rooms and switch yard equipment

• AC losses and plant self consumption ignored

• Plant downtime and grid unavailability ignored

• Degradation of the modules and plant components over the lifetime of the plant ignored

Technology

Module Type: • Crystalline Silicon (mono or

multi) • Thin film (CdTe, a-si)

Inverter Type: • Central Inverter • String inverter System Design: • Row spacing • Electrical design • Orientation and tilt • Shading

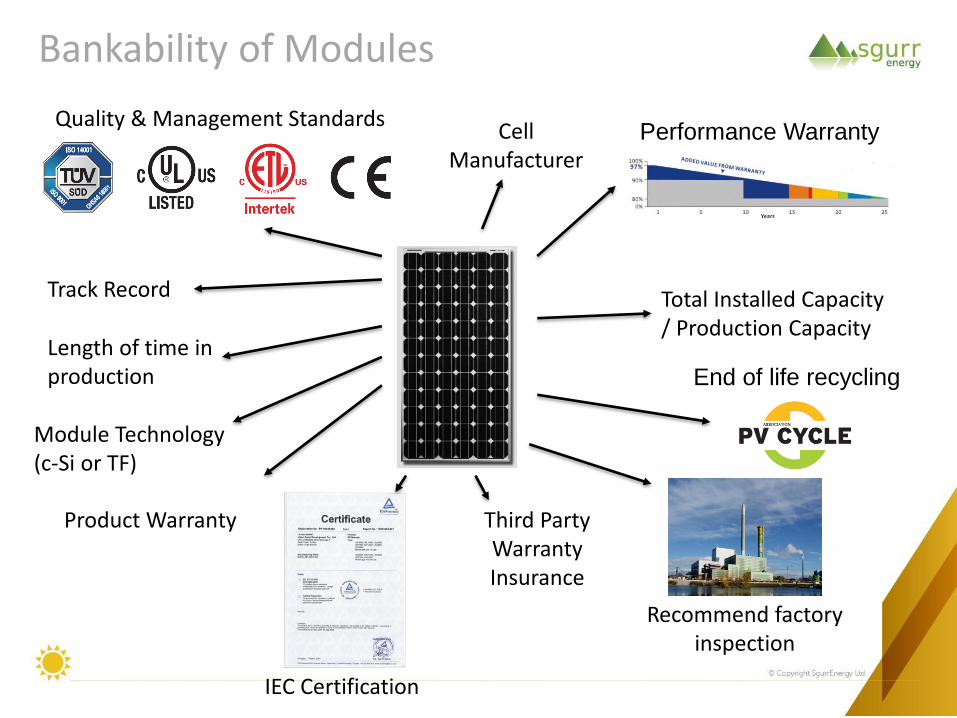

Bankability of Modules

Performance Warranty Quality & Management Standards

End of life recycling

Product Warranty Third Party Warranty Insurance

Track Record Total Installed Capacity / Production Capacity

Length of time in production

Recommend factory inspection

Cell Manufacturer

IEC Certification

Module Technology (c-Si or TF)

• Reliability Issues – Quick connector reliability

– Corrosion

– Improper insulation

– Delamination

– Discolouration

– Moisture ingress

– Bypass diode failure

Technology risk- modules

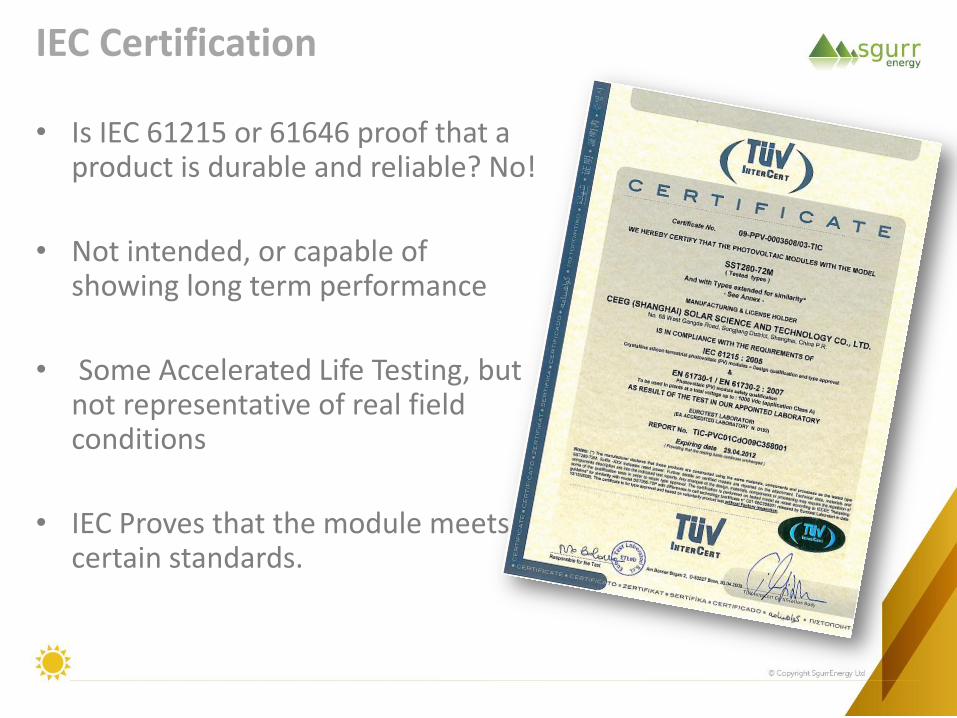

• Is IEC 61215 or 61646 proof that a product is durable and reliable? No!

• Not intended, or capable of showing long term performance

• Some Accelerated Life Testing, but not representative of real field conditions

• IEC Proves that the module meets certain standards.

IEC Certification

Third Party Insurance

Not Backed by third party insurance Backed by third party insurance

Suntech

First Solar

Yingli

Trina

Sharp

Sunpower

Hanwha Solar One

Kyocera

Jinko

Chint (Astronergy)

LDK

Canadian Solar

Solar Frontier

Solairedirect SA

NexPower Technology Corp

Signet Solar Inc

SolFocus Inc.

China Sunergy

• Module manufacturing industry currently in period of consolidation. • Ther is uncertain whether suppliers will be around for lifetime of warranty. • Third-party warranty insurance provides security even if company becomes

insolvent. • Several mainly tier 2 manufacturers now offer this, although not industry

standard. • Expect more manufacturers to offer in the next year due to highly

competitive nature of the market.

Insurance Providers: PowerGuard, Zurich, SPIB, Chartis, Solarif

• Temperature factors – Derating

– Shutdown

• Enclosure ratings – Indoor / outdoor

• Cooling – Forced or natural

• Fans – dusty environments

• Matched to the modules and strings

• Efficiency (Eu η%)

• Lifetime – Mid term replacements

Inverters

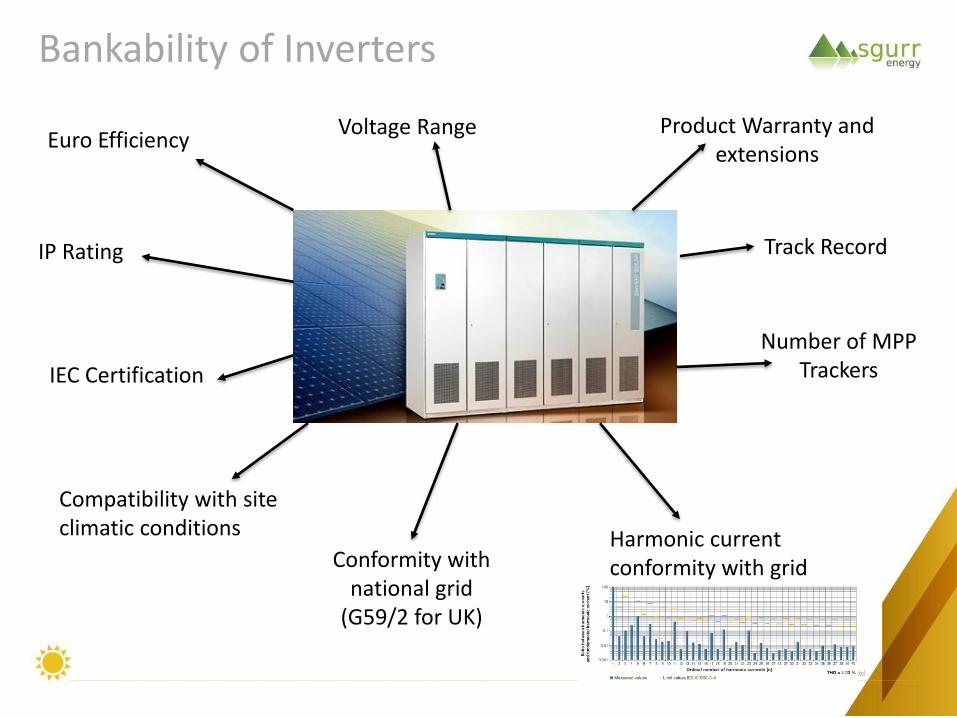

Bankability of Inverters

Product Warranty and extensions

Track Record

Compatibility with site climatic conditions

Euro Efficiency

IP Rating

Number of MPP Trackers

Voltage Range

Harmonic current conformity with grid Conformity with

national grid (G59/2 for UK)

IEC Certification

Technology (2)

Module Risks

• IEC certification

• Power tolerance

• Track record

• Financial standing

• De-rate with temperature

• Degradation rate

• Guarantees for power

Inverter Risks • Temperature factors

– De-rating – Shutdown

• Enclosure IP ratings – Indoor / outdoor

• Cooling – Forced or natural – Fans – dusty environments

• Matched to the modules and strings

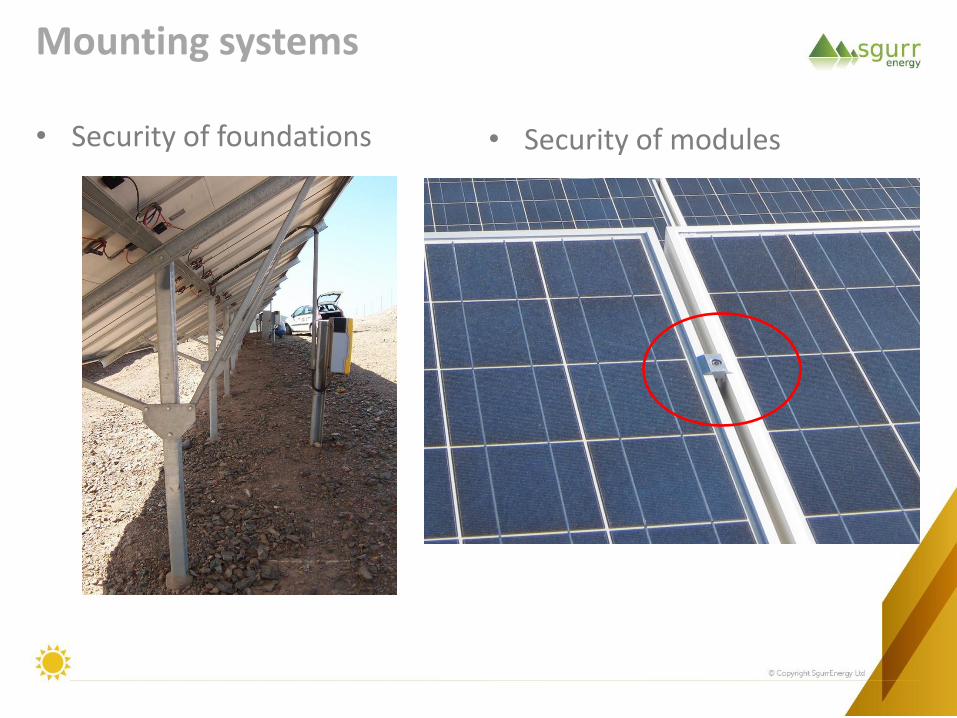

• Security of foundations

Mounting systems

• Security of modules

• Contract strategy (EPC or Multi-contract)

– Both have benefits & drawbacks

• Interfaces

• Design

• Construction

• Who handles them?

• Programme

• Realistic

• Lead times

• Critical path

• Weather delays

• Adequate liquidated damages

• Supply contracts

• EPC contract

Team Capability – Completion Risk

• Trial Operation (10 days - 4 weeks)

– Reliability of:

• Inverters

• Tracking

• Whole System

– Performance Ratio Tests

• Acceptance

– Provisional Acceptance

– Final Acceptance (12-24 months later?)

Completion

Typical Acceptance Procedure

Mechanical Completion

Commissioning/start-up

Test Operation Period

(couple of days)

Performance Testing for Provisional Acceptance

(around 10 days)

Performance Testing for Final Acceptance

(over 1 or 2 years)

Provisional Acceptance

• Provisional Acceptance Testing starts after a short test operation.

• Successful completion of the tests marks the Provisional Acceptance of the plant.

• Failure of Provisional Acceptance Testing may require remedial measures and repeat testing.

• If the Plant again fails the test then liquidated damages will be payable.

Provisional Acceptance Tests (1)

Performance Ratio Test:

• Checks if the power plant is performing at or above the PR agreed or warranted within the EPC contract.

• Standard testing period would be continuous testing for around 10 consecutive days.

• If there are significant differences between the contracted and actual PR, the EPC contractor should identify and rectify the problem before repeating the PR test.

• The quality of a PV power plant may be described by its Performance Ratio (PR). The PR, usually expressed as a percentage, can be used to compare PV systems independent of size and solar resource. It quantifies loss associated with electrical elements of the plant.

• PR is a measure of actual generation versus the maximum based on DC capacity and irradiation received over a given time period.

• Installed DC capacity is defined at: – 1,000W/m2 irradiance

– 25 degrees C

– A defined solar spectrum

Performance Ratio

Final Acceptance

• Final Acceptance takes place after a successful repeated PR test.

• The period of operation between Provisional Acceptance and Final Acceptance is dependent on the EPC contract and the level of risk that may be accepted.

• A two year PR Warranty provided by the EPC Contractor followed by Final Acceptance provides good comfort to Investors since it covers risk degradation of the modules.

Acceptance Testing: Lessons Learned

• Use good quality calibrated measuring devices- this is often not observed

• A two year PR Warranty followed by Final Acceptance is often not observed

• PR tests should be carried out using clean pyranometers- often soiled pyranometers are used

• Availability formulas should take into account the scenario when only a proportion of the plant is operational- this is often overlooked

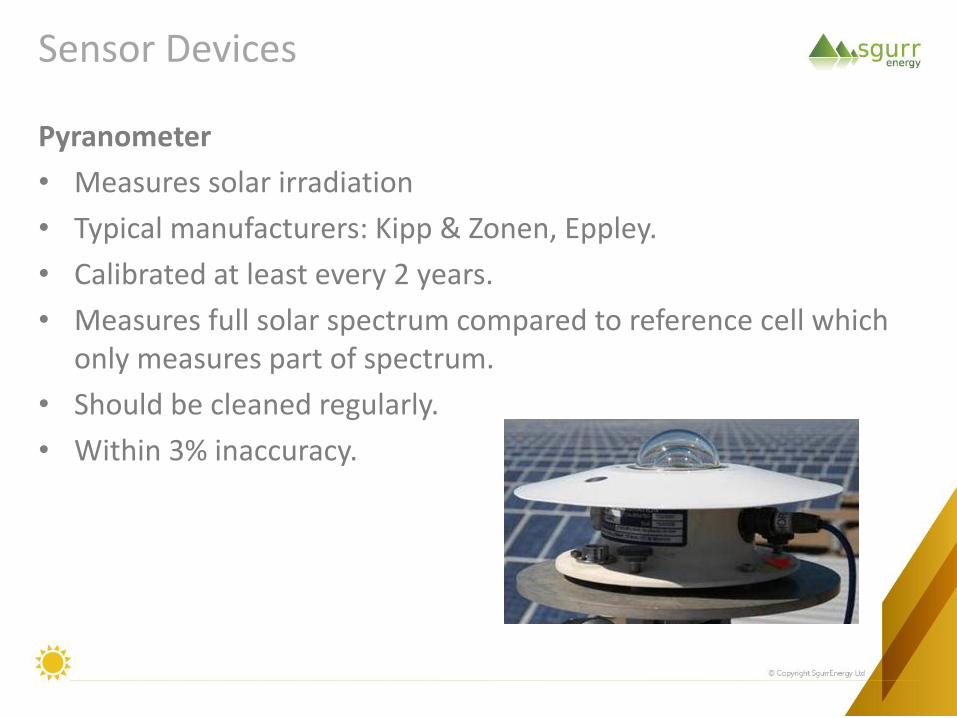

Sensor Devices

Pyranometer

• Measures solar irradiation

• Typical manufacturers: Kipp & Zonen, Eppley.

• Calibrated at least every 2 years.

• Measures full solar spectrum compared to reference cell which only measures part of spectrum.

• Should be cleaned regularly.

• Within 3% inaccuracy.

Monitoring Requirements

Measurement Description

Plane of Array Irradiance (Pyranometer) W/m2

Ambient Temperature °C

Module Temperature °C

Array DC Voltage V

Array DC Current I

Inverter AC Power VA

Exported Power VA

Imported Power VA

Wind Speed & direction if detailed modelling of system required

Horizontal Irradiance for comparisons with resource data sources

Inverter Output Current & Voltage I, V

Inverter Temperature Additional ventilation/cooling required?

Humidity Can effect lifetime of low quality modules

Monitoring: Common Mistakes

• Monitoring systems not installed in representative locations.

• Pyranometers not kept clean.

• Pyranometers not installed at module tilt.

• Only one pyranometer used. For a 5 MWp plant would expect two plane of array pyranometers (3 for >20MW) and one pyranometer on the horizontal plane.

• Reference cells should not be used in place of pyranometers as they may under-estimate the irradiation

Financial Model: What are The Risks?

• Sensitivity Analysis: – Annual module degradation 0.3% - 0.5% - 0.8%

– O&M costs ±10%

– Inverter replacement- once over project life?

– Module soiling losses: 2% , 3%, 4% (O&M dependent)

– Unavailability: 99%, 98% and 97% (dependent on grid strength)

• Reduce the likelihood or impact of the risk – Module cleaning linked to performance monitoring

– Include a maintenance reserve account

• Yield is often skewed seasonally – Include additional financial reserves to ease financial strain

Key Messages

• The process of technical due diligence can require considerable effort from the developer to satisfy the requirements of the lender.

• When well performed the lenders will fully understand the technical risks associated with the project and can decide if these are acceptable.

• A robust technical due diligence prior to designs being implemented can also pick up errors the developers have missed, and save them money.

• With experienced project partners, effective due diligence and good technical advisors, solar PV can be a low risk investment.

Any questions? www.sgurrenergy.com [email protected]

Risk Management

Lee Moscovitch, Infrastructure Principal

2

Introduction to Zouk Capital

Private equity investor focused on renewable energy

infrastructure and cleantech growth companies

Over €400m under management in 4 funds

Largest cleantech growth capital fund in Europe

3

Zouk’s dual track approach to the cleantech market

Alternative & Renewable Energy

Environmental Services & Technologies

Resource Efficiency Technologies

Solar

Biomass

Wind

Smart grid

Energy efficiency

Energy storage

Recycling Water

Waste management

Emissions solutions Advanced materials

Transport

Clean Technology

Marine

Fuel cells

Market intelligence

Deal flow

Commercial insight

Sector knowledge

Cleantech networks

Resource EfficiencyInfrastructure

Renewable EnergyGeneration

Environmental Infrastructure

Solar PV

Waste-to-Energy

Wind

Smart grid

Water treatment

Energy storage

Recycling

Waste management

Clean Infrastructure

Hydro

Transportation

Biomass Transmission

Biogas

Geothermal

Building efficiency

Focus on European expansion-stage cleantech companiesFocus on European expansion-stage cleantech companies

12 cleantech investments made over 2 funds12 cleantech investments made over 2 funds

4

Zouk’s cleantech growth capital strategy

Cleantech Europe II raised €230m and is the largest fund of its type in EUCleantech Europe II raised €230m and is the largest fund of its type in EU

Targeting high growth companies with established revenues (>€10m)Targeting high growth companies with established revenues (>€10m)

Select cleantech company investments

5

Water Solutions

Rural / Semi-urban Solar Building-integrated Solar

Solar / Recycling

Waste to Energy

Advanced thermal insulation

Electrical contractor

Energy efficiency services

Smart Grid

6

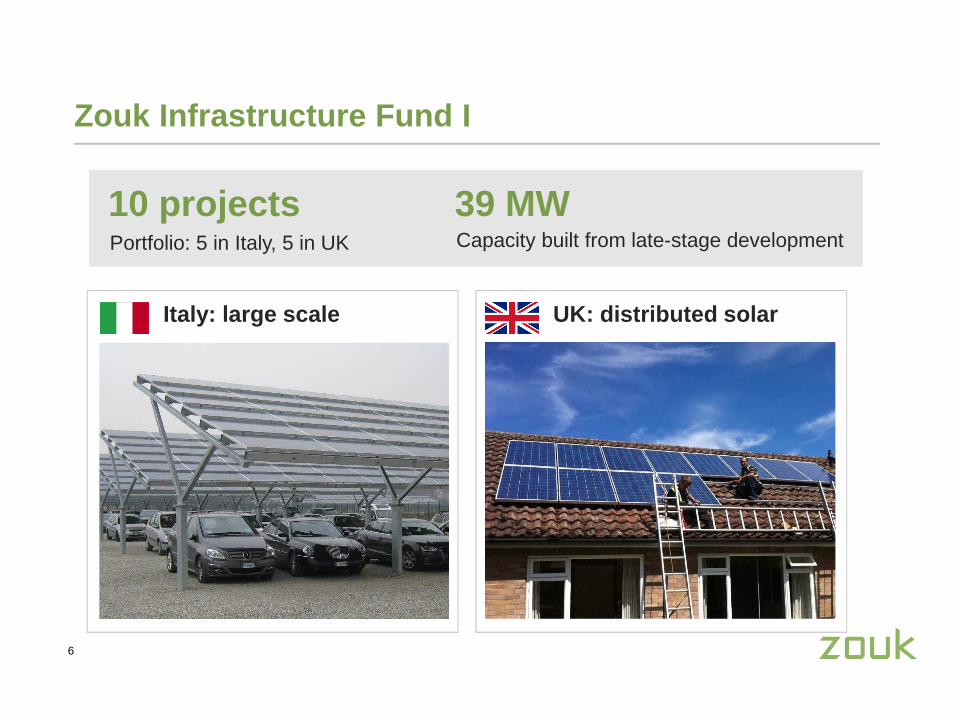

Zouk Infrastructure Fund I

39 MWCapacity built from late-stage development

10 projectsPortfolio: 5 in Italy, 5 in UK

Italy: large scale UK: distributed solar

7

Zouk Infrastructure Fund II

Financing renewable energy and environmental assets

Focusing on late-stage development and operational (distressed)

Investing primarily in Europe

Diversified range of sectors: geothermal, wind, solar, waste, hydro, biomass

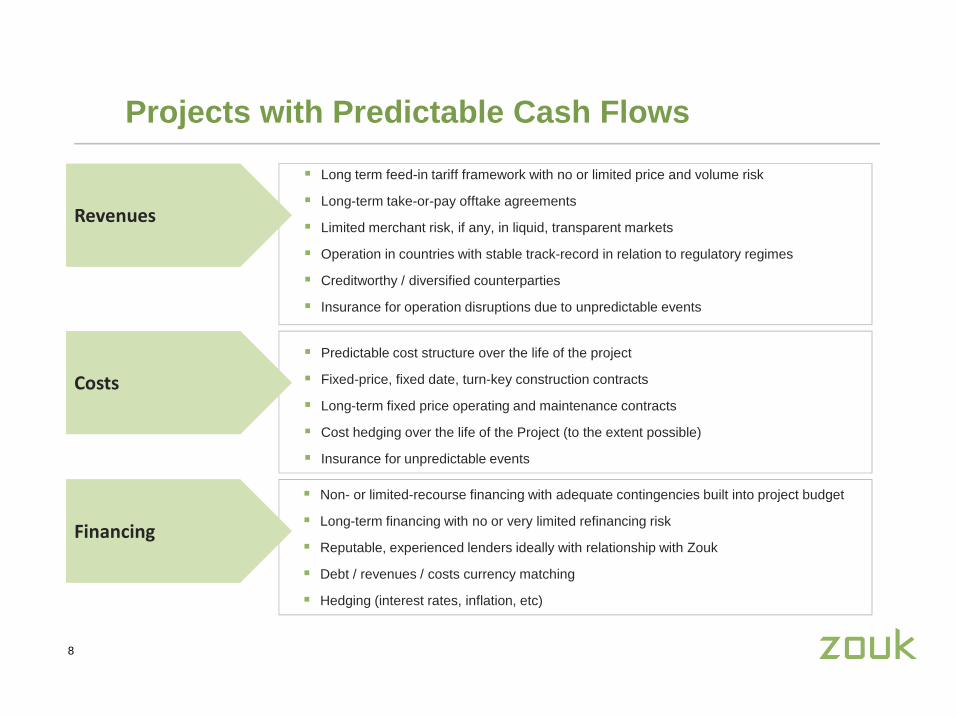

Projects with Predictable Cash Flows

8

� Long term feed-in tariff framework with no or limited price and volume risk

� Long-term take-or-pay offtake agreements

� Limited merchant risk, if any, in liquid, transparent markets

� Operation in countries with stable track-record in relation to regulatory regimes

� Creditworthy / diversified counterparties

� Insurance for operation disruptions due to unpredictable events

� Non- or limited-recourse financing with adequate contingencies built into project budget

� Long-term financing with no or very limited refinancing risk

� Reputable, experienced lenders ideally with relationship with Zouk

� Debt / revenues / costs currency matching

� Hedging (interest rates, inflation, etc)

� Predictable cost structure over the life of the project

� Fixed-price, fixed date, turn-key construction contracts

� Long-term fixed price operating and maintenance contracts

� Cost hedging over the life of the Project (to the extent possible)

� Insurance for unpredictable events

RevenuesRevenues

FinancingFinancing

CostsCosts

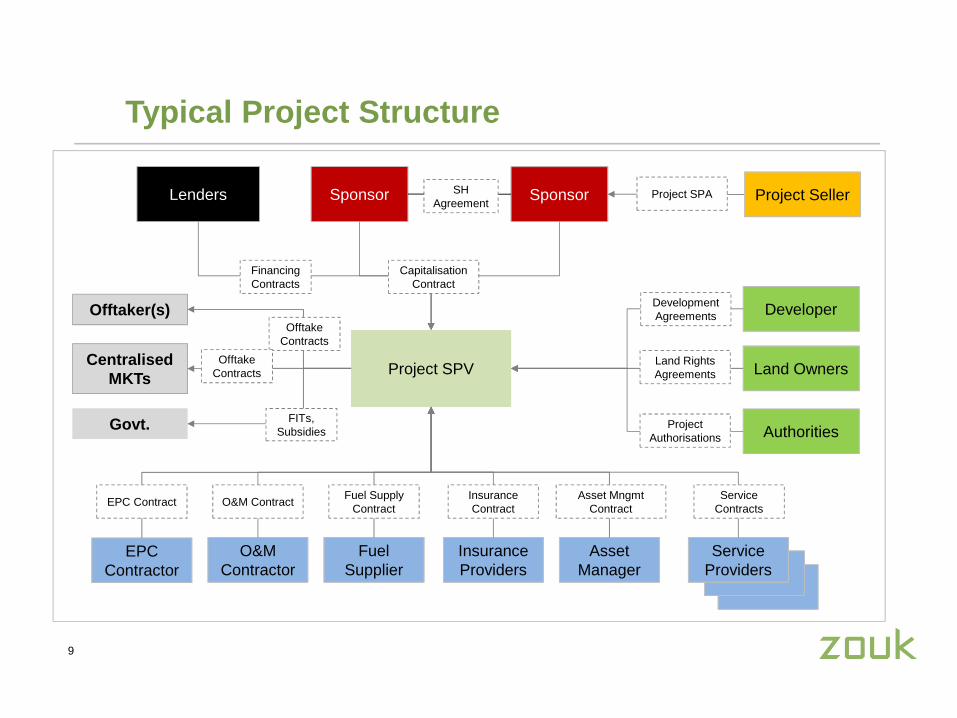

Typical Project Structure

9

Centralised MKTs

Land Owners

Sponsor

Project SPVProject SPV

Govt.Govt.

Lenders

Offtaker(s)

FITs, Subsidies

OfftakeContracts

EPC Contractor

O&MContractor

Fuel Supplier

Insurance Providers

Financing Contracts

Asset Manager

Service Providers

Authorities

Developer

ProjectAuthorisations

Land Rights Agreements

Development Agreements

Project SellerProject SPA

EPC Contract O&M ContractFuel Supply

ContractInsurance Contract

Asset MngmtContract

Service Contracts

Sponsor

Capitalisation Contract

SH Agreement

OfftakeContracts

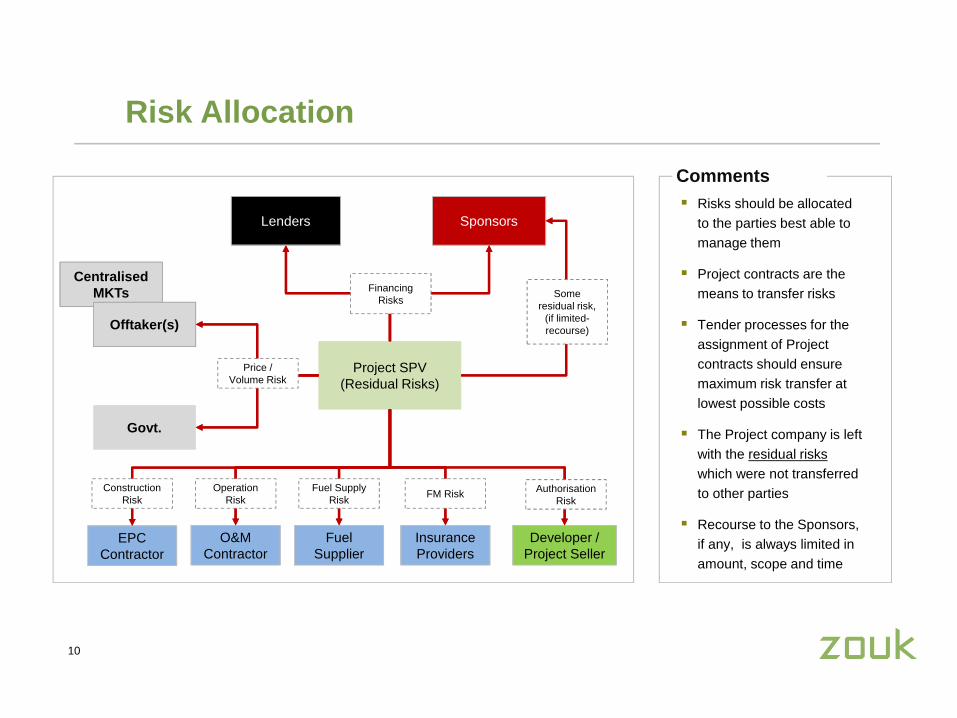

Risk Allocation

10

Centralised MKTs

Sponsors

Project SPV(Residual Risks)

Project SPV(Residual Risks)

Govt.Govt.

Lenders

Offtaker(s)

Price / Volume Risk

EPC Contractor

O&MContractor

Fuel Supplier

Insurance Providers

Developer / Project Seller

Construction Risk

Operation Risk

Fuel Supply Risk

FM Risk Authorisation Risk

Financing Risks

Comments� Risks should be allocated

to the parties best able to manage them

� Project contracts are the means to transfer risks

� Tender processes for the assignment of Project contracts should ensure maximum risk transfer at lowest possible costs

� The Project company is left with the residual risks which were not transferred to other parties

� Recourse to the Sponsors, if any, is always limited in amount, scope and time

Some residual risk,

(if limited-recourse)

Legal notices

The information contained in this document (the "Information") is issued by Zouk Capital LLP (the "Issuer") on a confidential basis to a limited number of prospective investors ("ProspectiveInvestors") and their respective legal counsel and/or other advisers ("Advisers") for the sole purpose of providing information in relation to the potential investment by Prospective Investorsin interests ("Interests") in the fund to be known as Renewable Energy and Environmental Infrastructure Fund II (the "Fund"). Neither Prospective Investors nor their Advisers shouldconstrue the Information as legal, tax, financial, investment, accounting or other advice, or as a recommendation by the Issuer, any of its affiliates, advisers, directors, employees or agents,that any Prospective Investor should acquire any Interest. Prior to making any investment, potential investors should arrive at an independent evaluation of such investment opportunity.The Information is qualified in its entirety by reference to the subscription agreements, limited partnership agreement(s) and any other legal documents constituting the Fund (the "FundDocuments"). Each investor who acquires an Interest will be bound by the terms and conditions of the Fund Documents. In the event that the descriptions in, or terms of, the Informationare inconsistent with, or contrary to, the descriptions in, or terms of, the Fund Documents, the Fund Documents shall prevail. The Information is subject to withdrawal, cancellation,modification or updating without notice, and is subject to the approval of certain legal matters by counsel and certain other conditions. This document is strictly private, proprietary andconfidential. This document may not be distributed, published, reproduced or transmitted in whole or in part, and the information contained herein (including the potential investmentopportunity) may not be disclosed by a recipient to any third party. By accepting delivery of this document, the recipient agrees to keep the information it contains strictly private andconfidential, and to return this document to the Issuer at any time upon the Issuer's request. No representation or warranty, express or implied, is or will be given by the Issuer or itsaffiliates, advisers, directors, employees or agents, and, without prejudice to any liability for, or remedy in respect of, fraudulent misrepresentation, no responsibility or liability or duty of careis or will be accepted by the Issuer or its affiliates, advisers, directors, employees or agents, as to the fairness, accuracy, completeness, currency, reliability or reasonableness of theinformation or opinions contained in the Information or any other written or oral information made available to any Prospective Investor or its Advisers in connection with any application tosubscribe for interests in the Fund (a "Proposed Subscription") or otherwise in connection with the Information. In particular, but without prejudice to the generality of the foregoing, norepresentation or warranty is given as to the achievement or reasonableness of any future projections, forecasts, targeted or illustrative returns (“Forward-Looking Information”). Actualevents and circumstances are difficult or impossible to predict and will differ from assumptions. A number of factors could cause actual results to differ materially from those in any Forward-Looking Information. There can be no assurance that the Fund’s investment strategy or objective will be achieved or that investors will receive a return of the amount invested. To the fullestextent possible by receipt of, and using, the Information, you release the Issuer and each of its affiliates, advisers, directors, employees and agents, in all circumstances (other than fraud)from any liability whatsoever and howsoever arising from your use of the Information or any information or communications provided in connection with any Proposed Subscription. Inaddition, no responsibility or liability or duty of care is or will be accepted by the Issuer or its respective affiliates, advisers, directors, employees or agents, for updating the Information (orany additional information), correcting any inaccuracies in it or providing any additional information to any Prospective Investor or its Advisers. Accordingly, none of the Issuer or its affiliates,advisers, directors, employees or agents shall be liable (save in the case of fraud) for any loss (whether direct, indirect or consequential) or damage suffered by any person as a result ofrelying on any statement in, or omission from, the Information or in, or omitted from, any other information or communications provided in connection with any Proposed Subscription.Investment in the Interests will involve significant risks. An investment in the Fund is only suitable for sophisticated investors and requires the financial ability and willingness to accept thehigh risks and lack of liquidity inherent in an investment in the Fund. The Fund's investments may be difficult to value and involve an above-average level of risk. No assurance can begiven, and no representation is made herein, that the Fund's investment strategy will be achieved or that investors will receive a return of their capital. Any offer or sale of securities (orInterests such as those described in this Information) may in certain jurisdictions be restricted by law. Any Prospective Investors who are considering making an investment in the Fund arerequired to inform themselves about, and to observe, any such restrictions. It is the responsibility of each Prospective Investor to satisfy themselves as to full compliance with the applicablelaws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. No action hasbeen taken to permit a public offering of the Interests in any jurisdiction where action for that purpose would be required. This Information does not constitute an offer to sell or a solicitationof an offer to buy Interests in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction.

11

Contact details

12

Zouk Capital LLP

100 Brompton Road

London

SW3 1ER

United Kingdom

+44 (0)20 7947 3400

www.zouk.com

Lead contacts

Lee Moscovitch [email protected] +44 (0)20 7947 3414

Ref: 1126192

The UK solar PV investment opportunity

02 July 2012

Eversheds conference

Ref: 1126192

The Ernst & Young Environmental Finance team

The solar PV investment opportunity

Navigating incentives

The funding backdrop

Summary

Agenda

Eversheds conference June 2012 2

Ref: 1126192

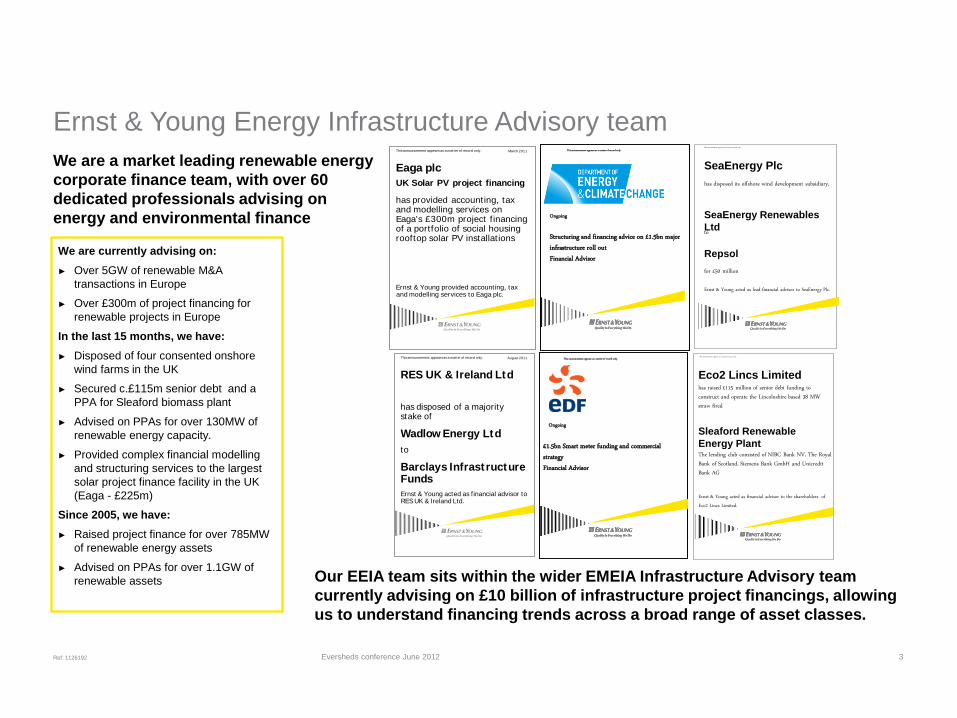

Ernst & Young Energy Infrastructure Advisory team

We are a market leading renewable energy

corporate finance team, with over 60

dedicated professionals advising on

energy and environmental finance

Ernst & Young acted as lead financial advisor to SeaEnergy Plc.

SeaEnergy Plc

This announcement appears as a matter of record only.

has disposed its offshore wind development subsidiary,

SeaEnergy Renewables

Ltd

Repsol

to

for £50 million

Ernst & Young acted as financial advisor to RES UK & Ireland Ltd.

has disposed of a majority stake of

Wadlow Energy Ltd

to

Barclays Infrastructure Funds

RES UK & Ireland Ltd

This announcement appears as a matter of record only. August 2011

3 Eversheds conference June 2012

Ernst & Young acted as financial advisor to the shareholders of Eco2 Lincs Limited.

Eco2 Lincs Limited

This announcement appears as a matter of record only.

has raised £115 million of senior debt funding to construct and operate the Lincolnshire based 38 MW straw fired

Sleaford Renewable

Energy Plant The lending club consisted of NIBC Bank NV, The Royal Bank of Scotland, Siemens Bank GmbH and Unicredit Bank AG

We are currently advising on:

► Over 5GW of renewable M&A

transactions in Europe

► Over £300m of project financing for

renewable projects in Europe

In the last 15 months, we have:

► Disposed of four consented onshore

wind farms in the UK

► Secured c.£115m senior debt and a

PPA for Sleaford biomass plant

► Advised on PPAs for over 130MW of

renewable energy capacity.

► Provided complex financial modelling

and structuring services to the largest

solar project finance facility in the UK

(Eaga - £225m)

Since 2005, we have:

► Raised project finance for over 785MW

of renewable energy assets

► Advised on PPAs for over 1.1GW of

renewable assets

Ernst & Young provided accounting, tax and modelling services to Eaga plc.

has provided accounting, tax and modelling services on Eaga's £300m project f inancing of a portfolio of social housing rooftop solar PV installations

Eaga plc

UK Solar PV project financing

This announcement appears as a matter of record only. March 2011 This announcement appears as a matter of record only.

Ongoing

Structuring and financing advice on £1.5bn major infrastructure roll out Financial Advisor

This announcement appears as a matter of record only.

Ongoing

£1.5bn Smart meter funding and commercial strategy Financial Advisor

Our EEIA team sits within the wider EMEIA Infrastructure Advisory team

currently advising on £10 billion of infrastructure project financings, allowing

us to understand financing trends across a broad range of asset classes.

Ref: 1126192

Sector thought leadership

Eversheds conference June 2012 4

Our market leading thought leadership and research addresses a broad spectrum of challenges, from industry-wide issues to specific technical, business, regulatory and compliance concerns

4

Country attractiveness indices

Our quarterly Country Attractiveness Indices have become a benchmark for all our clients. It provides scores for national renewable energy

markets, renewable energy infrastructures and their suitability for individual technologies (wind, solar and biomass).

The CAI has been reported in 107 different publications worldwide, spanning most forms of media including TV, global and national

mainstream press and trade press and is one of the leading publications in the global renewable energy market.

Utilities unbundled

Utilities Unbundled, Ernst & Young’s semi-annual global power and utilities magazine, features insight from leading industry figures,

comment on key industry issues and analysis of the latest trends. Read about what your peers around the world are thinking and doing

about common industry concerns.

Growing beyond

The EY Global Cleantech Centre produces its “Growing beyond: the cleantech growth journey” publication on an annual basis. It includes

the findings from our annual Cleantech CEO Growth Journey retreat. Developed with Bloomberg New Energy Finance, the event brings

together nearly 50 CEOs to address the industry's capital, partnership and expansion challenges.

.

Cleantech matters

The cleantech-enabled transformation to a resource-efficient and low carbon economy is characterised by many observers as the next

industrial revolution. Our quarterly “Cleantech Matters” publication includes material covering the sector’s key drivers, trends and issues.

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so that

text sizes are applied to the

standard two column layout in the

correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

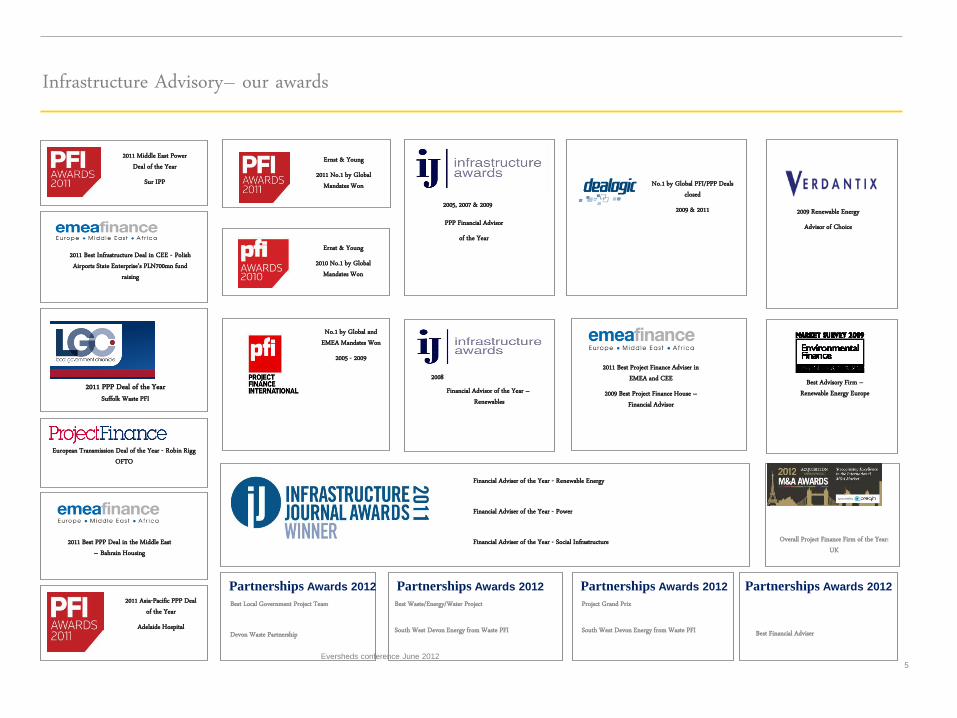

No.1 by Global and EMEA Mandates Won

2005 - 2009

No.1 by Global PFI/PPP Deals closed

2009 & 2011

Ernst & Young 2011 No.1 by Global

Mandates Won

2009 Renewable Energy Advisor of Choice

Ernst & Young 2010 No.1 by Global

Mandates Won

Financial Advisor of the Year – Renewables

2008

PPP Financial Advisor of the Year

2005, 2007 & 2009

2011 Best Project Finance Adviser in EMEA and CEE

2009 Best Project Finance House – Financial Advisor

Best Advisory Firm – Renewable Energy Europe

Financial Adviser of the Year - Renewable Energy Financial Adviser of the Year - Power Financial Adviser of the Year - Social Infrastructure

2011 Middle East Power Deal of the Year

Sur IPP

2011 Best Infrastructure Deal in CEE - Polish Airports State Enterprise’s PLN700mn fund

raising

2011 PPP Deal of the Year Suffolk Waste PFI

European Transmission Deal of the Year - Robin Rigg OFTO

2011 Best PPP Deal in the Middle East – Bahrain Housing

2011 Asia-Pacific PPP Deal of the Year

Adelaide Hospital

Infrastructure Advisory– our awards

5

Partnerships Awards 2012

Best Local Government Project Team Devon Waste Partnership

Partnerships Awards 2012 Partnerships Awards 2012

Best Waste/Energy/Water Project South West Devon Energy from Waste PFI

Project Grand Prix South West Devon Energy from Waste PFI

Overall Project Finance Firm of the Year: UK

Partnerships Awards 2012

Best Financial Adviser

Eversheds conference June 2012

Ref: 1126192

Section 2

The PV investment opportunity

Ref: XX00000

A snapshot of UK Solar PV

Eversheds conference June 2012 7

Greg Barker – 24 May 2012

► “We can now look with confidence to a future for solar which will see it go from a small cottage

industry, anticipated under the previous scheme, to playing a significant part in Britain's clean

energy economy”

DECC recognise solar in RE roadmap

► DECC 2020 solar power pathway central scenario delivers 22GW of solar PV

Buyers market

► Continued over supply with ever decreasing panel and EPC prices

► Falling tariff regimes across Europe

► Grid parity around the corner?

Consultation, consultation, consultation

► DECC RO Banding consultation (ongoing) 2.0 ROCs falling to1.8 ROC

► FIT consultations known for now, awaiting response on Phase 2B

Other policy Renewable Heat Incentive / Green deal

► First of its kind support for renewable heat generation including solar thermal

► Energy efficiency loan scheme, domestic market minimum EPC requirements

Ref: XX00000

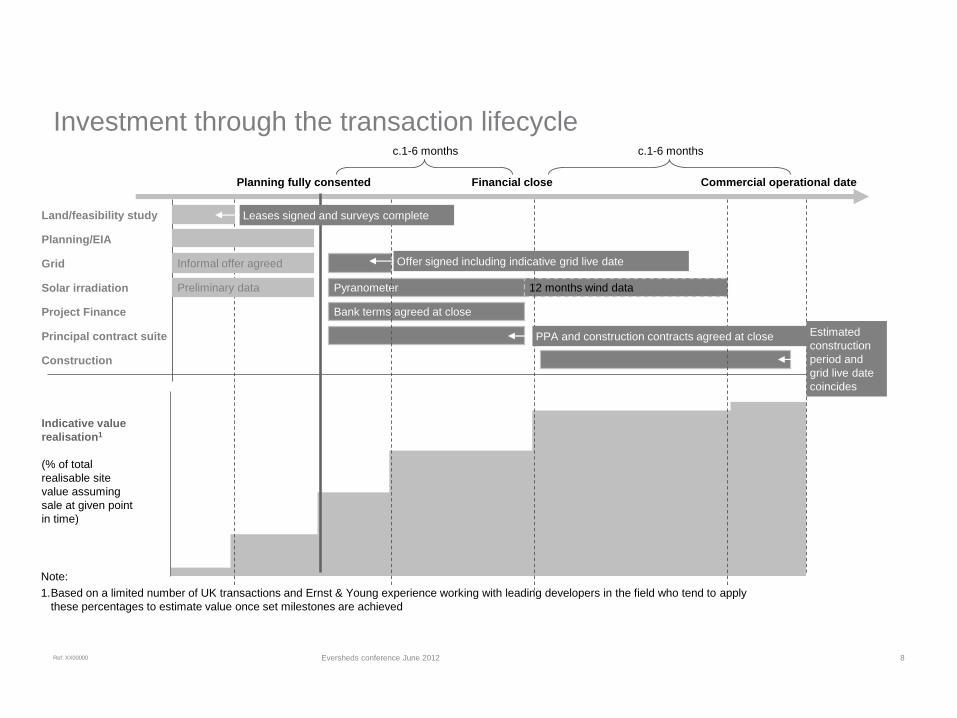

Investment through the transaction lifecycle

Eversheds conference June 2012 8

Note:

1. Based on a limited number of UK transactions and Ernst & Young experience working with leading developers in the field who tend to apply

these percentages to estimate value once set milestones are achieved

0%

20%

40%

60%

80%

100%

Land/feasibility study

Planning/EIA

Grid

Solar irradiation

Planning fully consented Financial close Commercial operational date

Bank terms agreed at close Project Finance

Pyranometer

Principal contract suite

Construction

12 months wind data

c.1-6 months c.1-6 months

Indicative value

realisation1

(% of total

realisable site

value assuming

sale at given point

in time)

Leases signed and surveys complete

Informal offer agreed

Preliminary data

Offer signed including indicative grid live date

PPA and construction contracts agreed at close Estimated

construction

period and

grid live date

coincides

Ref: XX00000

Section 3

Navigating incentives

Ref: XX00000

0

200

400

600

800

1,000

1,200

1,400

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

Dep

loym

ent (

MW

)

Domestic Commercial Industrial Community

FiTs indexed linked revenues give stability, but in unstable regime

May 2012

Confirmed cut in FiT

in August 2012

March 2012

Supreme court

rejects DECC appeal

Feb2012

DECC issue publish

response to Phase 1

consultation and

issue Phase 2

consult

January 2012

DECC looses court

of appeal decision

December 2011

DECC issue publish

response to Phase 1

consultation and

issue Phase 2

consult

December 2012

Judicial review

rejected, high court

appeal granted to be

heard

October 2011

DECC publish

comprehensive

consultation to

reduce tariffs on 10

December

April 2010

FiT launched

March 2011

DECC publish fast

track review on FiTs

June 2011

Response to fast

track review

confirming cut to PV

tariffs >50kWp

August 2011

New rates for

installations <50kW

take effect

August 2012

20yr tariff

Quarterly degression

Deployment

dependant

90% multi installation

tariff (>25 systems)

Increased export

E EPC rating or get

standalone tariff

Ref: XX00000

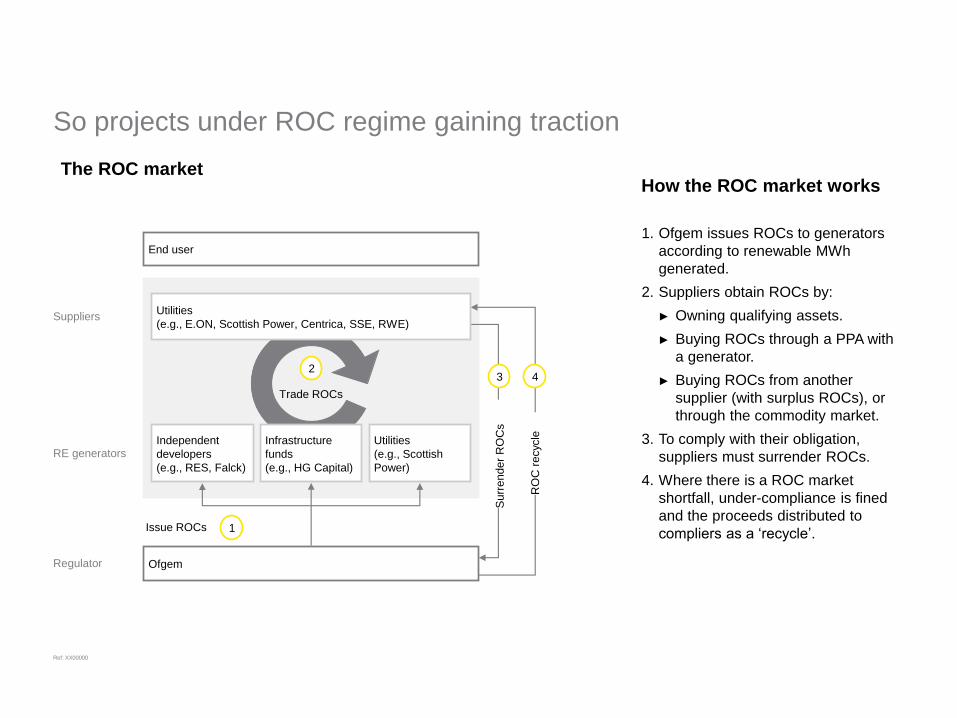

So projects under ROC regime gaining traction

Suppliers

RE generators

Trade ROCs

2

Issue ROCs 1

Regulator

End user

Ofgem

Utilities

(e.g., E.ON, Scottish Power, Centrica, SSE, RWE)

Independent

developers

(e.g., RES, Falck)

Infrastructure

funds

(e.g., HG Capital)

Utilities

(e.g., Scottish

Power)

Su

rre

nd

er

RO

Cs

3

RO

C r

ecycle

4

How the ROC market works

1. Ofgem issues ROCs to generators

according to renewable MWh

generated.

2. Suppliers obtain ROCs by:

► Owning qualifying assets.

► Buying ROCs through a PPA with

a generator.

► Buying ROCs from another

supplier (with surplus ROCs), or

through the commodity market.

3. To comply with their obligation,

suppliers must surrender ROCs.

4. Where there is a ROC market

shortfall, under-compliance is fined

and the proceeds distributed to

compliers as a ‘recycle’.

The ROC market

Ref: XX00000

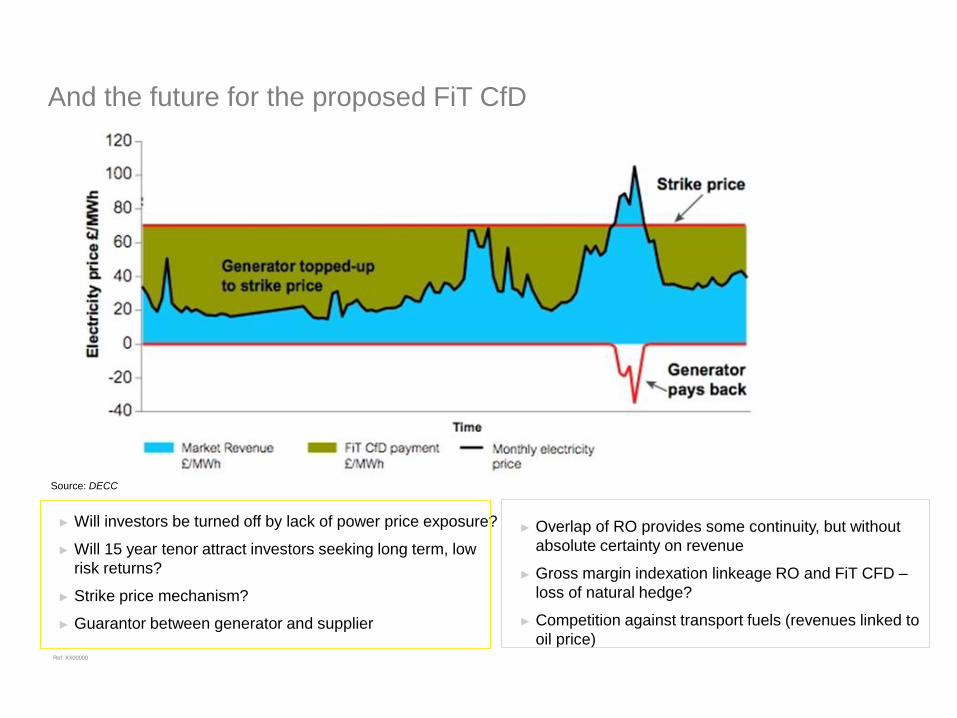

And the future for the proposed FiT CfD

► Will investors be turned off by lack of power price exposure?

► Will 15 year tenor attract investors seeking long term, low

risk returns?

► Strike price mechanism?

► Guarantor between generator and supplier

The key to achieving these objectives will be to bring forward the level of investment needed in

new low-carbon generation capacity and infrastructure at the required pace and through a

combination of measures.

Source: DECC

► Overlap of RO provides some continuity, but without

absolute certainty on revenue

► Gross margin indexation linkeage RO and FiT CFD –

loss of natural hedge?

► Competition against transport fuels (revenues linked to

oil price)

Ref: XX00000

Section 4

The funding

Ref: XX00000 03 July 2012

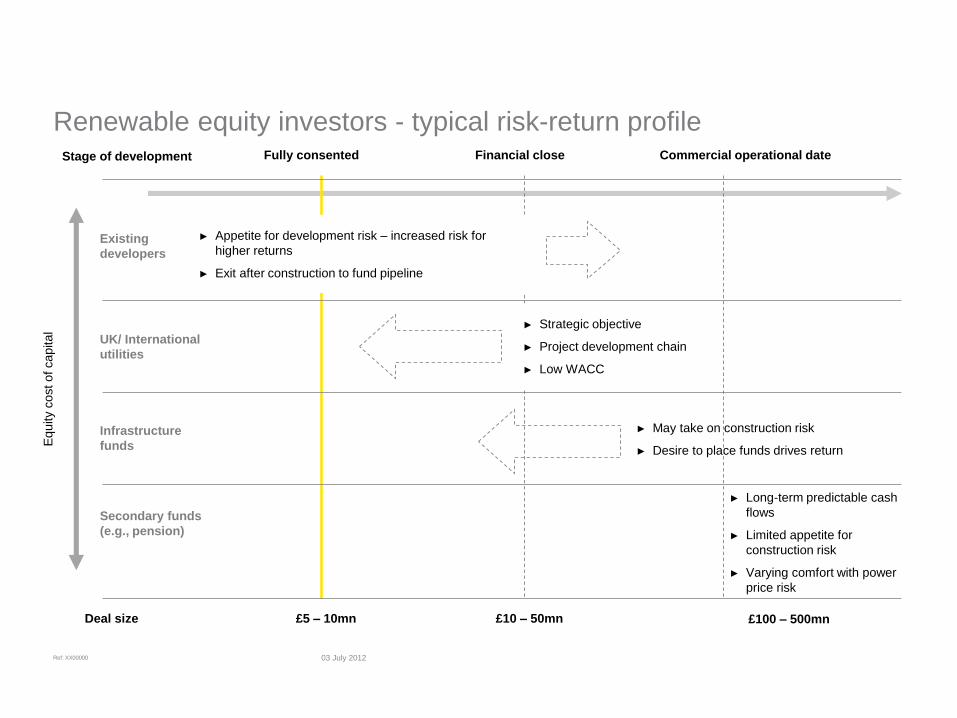

Renewable equity investors - typical risk-return profile

Existing

developers

UK/ International

utilities

Infrastructure

funds

Secondary funds

(e.g., pension)

► Appetite for development risk – increased risk for

higher returns

► Exit after construction to fund pipeline

► Strategic objective

► Project development chain

► Low WACC

► May take on construction risk

► Desire to place funds drives return

► Long-term predictable cash

flows

► Limited appetite for

construction risk

► Varying comfort with power

price risk

Eq

uity c

ost of capital

Fully consented Financial close Commercial operational date Stage of development

Deal size £5 – 10mn £10 – 50mn £100 – 500mn

Ref: XX00000

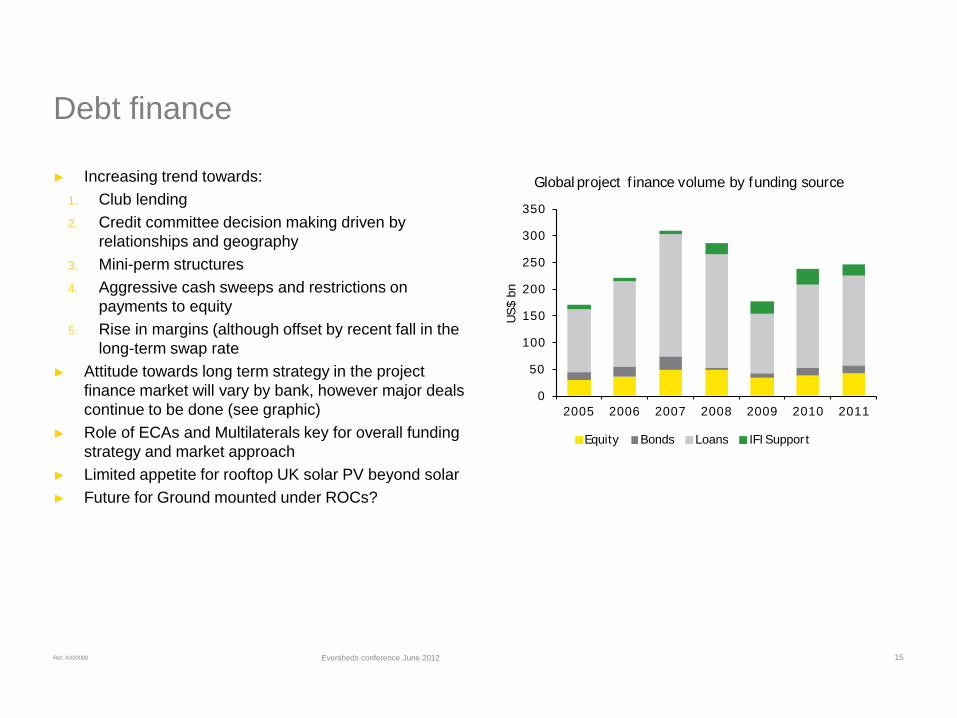

Debt finance

Eversheds conference June 2012 15

► Increasing trend towards:

1. Club lending

2. Credit committee decision making driven by

relationships and geography

3. Mini-perm structures

4. Aggressive cash sweeps and restrictions on

payments to equity

5. Rise in margins (although offset by recent fall in the

long-term swap rate

► Attitude towards long term strategy in the project

finance market will vary by bank, however major deals

continue to be done (see graphic)

► Role of ECAs and Multilaterals key for overall funding

strategy and market approach

► Limited appetite for rooftop UK solar PV beyond solar

► Future for Ground mounted under ROCs?

Source: Infrastructure Journal

0

50

100

150

200

250

300

350

2005 2006 2007 2008 2009 2010 2011

US

$ b

n

Global project f inance volume by funding source

Equity Bonds Loans IFI Suppor t

Ref: XX00000

Solar PV funding – the capital journey

Eversheds conference June 2012 16

Exit arranged whereby value of assets transferred to long-term owner

Equity capital at 15%

(business model inertia risk)

Ownership capital at 6 – 7% cost of funds

Time period (X months)

Installation

Spend Investment (X £m)

Capital increase realised through cost of funds arbitrage,

releasing capital for further installation programme

Installation spend funded unencumbered

with external capital, i.e. equity or corporate debt

Constraints:

► Pension funds/insurance funds/life funds do not have significant

capital allocations specifically for renewables investments

► Conduits do not exist that enable PV market to effectively

access this capital – these funds do not invest directly

► Inertia risk, technology performance risk, and resource risk

needs to be properly understood to access low-cost funds

► Large equity capital sources needed to build installation capex

to levels to attract such investors

Ideal world:

► Long-term ownership resides

with low cost, long-term cash

yield investors

(pension/insurance/life funds)

► Cost of funds: c 6 – 7%

► Deal size: £100mn plus

Ref: XX00000

The road to the PV financing future

Eversheds conference June 2012 17

► Aggregation and consolidation

► Flight to quality

► How do you deliver long term institutional capital?

► Right conduit

► Right portfolio

► Right structure

► Right management

► Right advisors

Ref: 1126192

Section 5

Summary

Ref: 1126192

Summary

Eversheds conference June 2012 19

Solar investment opportunity

► 22GW of deployment in UK

► Cost reductions look set to continue – 50% -70% cost reduction in few years

► Grid parity

► Low(er) risk renewable technology

Revenues – which TLA will you invest in?

► FiTs

► ROCs

► CfD

The funding backdrop

► Conventional financing solutions are not a perfect fit for highly aggregated portfolios

► Optimising finance is a major value lever of UK PV – how long will it take

► Aggregation and flight to quality likely

Ref: 1126192 Eversheds conference June 2012 20

Thank you Louise Shaw, Senior Executive,

Environmental Finance

Tel: +44 (0)20 7951 4806

Email: [email protected]

www.ey.com/renewables

Ref: 1126192

Ernst & Young LLP

Assurance | Tax | Transactions | Advisory

www.ey.com/uk

The UK firm Ernst & Young LLP is a limited liability

partnership registered in England and Wales

with registered number OC300001 and is a member firm

of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London SE1 2AF.

© Ernst & Young LLP 2012. Published in the UK.

All rights reserved.

This document has been prepared by Ernst & Young. The information and opinions contained in this document are derived from public

and private sources which we believe to be reliable and accurate but which, without further investigation, cannot be warranted as to their

accuracy, completeness or correctness. This information is supplied on the condition that Ernst & Young, and any partner or employee of

Ernst & Young, are not liable for any error or inaccuracy contained herein, whether negligently caused or otherwise, or for loss or damage

suffered by any person due to such error, omission or inaccuracy as a result of such supply. In particular any numbers, initial valuations

and schedules contained in this document are preliminary and are for discussion purposes only.