ASSESSING FACTORS AFFECTING THE REPAYMENT RATE OF ...

27

247 Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions Gadjah Mada International Journal of Business May-August 2006, Vol. 8, No. 2, pp. 247–273 ASSESSING FACTORS AFFECTING THE REPAYMENT RATE OF MICROFINANCE INSTITUTIONS A Case Study of Village Credit Institutions of Gianyar, Bali Lincolin Arsyad This paper attempts to assess the influence of several factors on the repayment rate of the Village Credit Institutions (Lembaga Perkreditan Desa or simply LPDs) in Gianyar district in Bali. Using a quantitative approach (logistic model) the findings of this study indicate that the Balinese social custom, including social values, norms, and sanctions (informal institutions) have an influence on sustaining the high repayment rate of the LPDs. This finding con- forms to the some previous studies using institutional approach that reveal the high repayment rate of the LPDs in Gianyar district is influenced by their institutional arrangement that based on custom regulation which includes social norms, sanctions, and involvement of custom village leader in screening process and contractual en- forcement of loan (informal institutions), by regulations set up by the Central Bank (formal institutions), and by the mechanism of collect- ing loan repayments applied by the LPDs management. Keywords: informal institutions; microfinance institutions; repayment rate

Transcript of ASSESSING FACTORS AFFECTING THE REPAYMENT RATE OF ...

247

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

Gadjah Mada International Journal of BusinessMay-August 2006, Vol. 8, No. 2, pp. 247–273

ASSESSING FACTORS AFFECTING THE REPAYMENT RATE OF

MICROFINANCE INSTITUTIONSA Case Study of Village Credit Institutions

of Gianyar, Bali

Lincolin Arsyad

This paper attempts to assess the influence of several factors onthe repayment rate of the Village Credit Institutions (LembagaPerkreditan Desa or simply LPDs) in Gianyar district in Bali. Usinga quantitative approach (logistic model) the findings of this studyindicate that the Balinese social custom, including social values,norms, and sanctions (informal institutions) have an influence onsustaining the high repayment rate of the LPDs. This finding con-forms to the some previous studies using institutional approach thatreveal the high repayment rate of the LPDs in Gianyar district isinfluenced by their institutional arrangement that based on customregulation which includes social norms, sanctions, and involvementof custom village leader in screening process and contractual en-forcement of loan (informal institutions), by regulations set up by theCentral Bank (formal institutions), and by the mechanism of collect-ing loan repayments applied by the LPDs management.

Keywords: informal institutions; microfinance institutions; repayment rate

248

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

Introduction

The term microfinance refers tothe provision of financial services (gen-erally savings and credit) to low-in-come clients (ADB 2000; Ledgerwood1999; Robinson 2001). The clients areoften identified as traders, street ven-dors, small farmers, service providers(hairdressers, rickshaw drivers), andartisans and small producers, such asblacksmiths and seamstresses. In prac-tice, however, in addition to financialintermediation, some microfinanceinstitutions provide social intermedia-tion services such as group formation,development of self-confidence, andtraining in financial literacy and man-agement capabilities among membersof a group intended to benefit low-income women and men (Bennett 1998;Ledgerwood 1999). Part of the rea-sons is because low-income peopleface strong barriers (such as illiteracy,gender discrimination, and remote-ness) in trying to gain access to ordi-nary financial service institutions(Ledgerwood 1999: 63). This meansthat the skills and confidence of low-income people have to be developed inaddition to credit provision. There-fore, the microfinance approach is nota minimalist approach offering onlyfinancial intermediation but an inte-grated approach offering both finan-cial intermediation and other servicesmentioned above (Ledgerwood 1999:65). It can also then be expected toreduce poverty and to develop andstrengthen the institutional capacity oflocal financial systems through find-

ing ways to cost-effectively lend moneyto poor households (Ledgerwood 1999;Morduch 1999; Morduch 2000; Otero1999; Snow 1999).

Microfinance institutions are gen-erally characterized by a collage ofdynamic, innovative, and flexible ar-rangements tailored to the local eco-nomic and social environment (Adamsand Fitchett 1992: 3). They argue thatthese arrangements are resilient andthat many of them have grown over along period. This flexibility is accordedby the limited regulation, along withsmall size, with most microfinanceinstitutions operating in a circum-scribed area, or in a specific niche ofthe market where personal knowledgeof borrowers is possible (Ghate 1988).The type of transaction is small andshort-term, which is based on personalrelationships or the institution’s inti-mate knowledge of its clientele (Wai1992), and which usually occur closeto where clients live, shop, or work. Tofacilitate the clients’ entry, microfi-nance institutions also apply a simpleapplication procedures, and loans aredisbursed quickly (ADB 2000). Theinterest rates charged by microfinanceinstitutions are market-oriented andintended to cover both their opera-tional and financial costs, based on theassumption that the poor are willing topay for access and convenience. Tosum up, Wai argues that these arrange-ments are flexible, adapt to economicchange, innovative, involve low trans-action costs for both lender and bor-rower, and result in high loan recoveryrates (Wai 1992: 340).

249

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

As a lending institution, micro-finance is a risky business becauserepayment of loans can seldom be fullyguaranteed. The failure of a large num-ber of microfinance institutions inmany developing countries was due,among other things, to their inabilityto ensure good repayment rates amongtheir borrowers (Adams 1984;Woolcock 1999; Yaron 1994). Ac-cording to some authors (Christen1998; Sharma and Zeller 1997;Woolcock 1999; Yaron 1994; Zeller1998), the repayment rate is the mostimportant performance indicators ofmicrofinance institution. Woolcock(1999), for instance, points out that themost common measure of a micro-finance program’s performance is itsloan repayment rate, since this has alarge bearing on whether a program islikely to be financially sustainable.Yaron (1994) also emphasizes that ahigh profit earned by micro-financeinstitutions cannot be used as the onlyindicator of self-sustainability of theinstitutions, since a high profit couldbe attained only in the short period.Attaining a high rate of loan collection(repayment rate) is a necessary condi-tion for a micro-finance institution tobecome self-sustainable in the longrun. Loan losses often have been thelargest cost borne by the institutionsand the principal cause of insolvencyand illiquidity. The importance of theportfolio quality indicator includingthe repayment rate is also reflected inthe health criteria of banking institu-

tion in Indonesia set up by the CentralBank –the so-called CAMEL criteria –that gives a high weight of thirty per-cent for this indicator (Bank Indonesia1997).

This paper attempts to assess theinfluence of several factors on the re-payment rate of the Village CreditInstitutions [Lembaga PerkreditanDesa (LPD)] in Gianyar district inBali. The rationale in selecting LPDsin Gianyar as the case of this study isan explorative reason. An exploratorycase1 may be selected for the examina-tion of a subject area on which there islittle prior theory or evidence avail-able (Scapens 1990: 272-273). Basedon this perspective, the LPD case is anexploratory one since even though theLPD is considered to be a fully sustain-able microfinance institution in Indo-nesia by some scholars (Chaves andGonzales-Vega 1996; Christen et al.1995), the LPD represents a micro-finance institution little understoodfrom the point of view of its sociocul-tural context, its management, andother factors influencing its perfor-mance.

The paper is structured as fol-lows. Section 2 briefly discusses thedevelopment of the LPDs in Gianyardistrict in Bali and followed by a shortdescription of their sociocultural envi-ronment. Section 4 presents the meth-odology and the results of analysis.Conclusions are presented in the lastsection.

1 Yin uses the terms ‘representative’ or ‘typical’ case (see Yin 2003: 42)

250

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

The Development of LPD ofGianyar

The LPDs are community-basedfinancial institutions (microfinanceinstitutions) that are owned, managedand used by the members of the cus-tom village (desa adat) in Bali (Gov-ernment of Bali 1988). The first LPDwas established in 1984 and manymore followed in the following years.The objectives of establishing an LPDin each custom village are to supportrural economic development throughenhancing savings behavior of rural

people and providing credit for small-scale enterprise, to eliminate exploit-ative forms of credit relations, to cre-ate an equal opportunity for businessactivities at the village level, and toincrease the degree of monetization inrural areas (Government of Bali 2002).These objectives reflect the develop-ment mission of the LPDs to providefinancial service for rural people inBali.

In Gianyar district of Bali, thefirst Village Credit Institution (LPD)established was LPD Manukaya, asone of LPD pilot projects, located in

Table 1. General indicators of Village Credit Institutions (LPDs) within GianyarDistrict of Bali Province, 1999-2001

General Indicators 1999 2001

Information on the Village Credit Institutions (LPD): Number of LPDs 142 174

Number of staff 723 873 Total assets (billion Rp) 58 125 Total equity (billion Rp) 10.9 25.4 Total profit (billion Rp) 4.4 10.2

Lending and savings activities: Volume of loans outstanding (billion Rp) 36 89 Number of borrowers 36,454 49,593

Average loans size per borrower (000 Rp) 954 1,603 Volume of time deposits (billion Rp) 23 47 Number of time deposits account (depositors) 6,820 7,948 Average deposit per depositor (million Rp) 3.5 5.7

Volume of savings (billion Rp) 22.5 50 Number of savings account (savers) 81,178 114,994 Average savings per saver (000 Rp) 243 415

Bank deposits in Bank BPD Bali (billion Rp) 20 29

Financial intermediation indicators: Deposits to loan ratio (DLR) in % 111 106 Savers and depositors to borrowers ratio (%) 241 248

Source: PLPDK, Financial Report of LPD Gianyar District of Bali Province 1999 and 2001(computed by the author).

251

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

the custom village of Manukaya in1984. Subsequently, the growth of LPDin Gianyar district has been very fast.On the one hand, the rapid rise of LPDsis due the increasing demand of Ba-linese for rural financial institutionssince the institutions have been able tomeet their needs for an easy access forcredit (Arsyad 2005b; Arsyad 2005).On the other hand, the provincial gov-ernment of Bali and Bank BPD Baliactively support the establishment ofnew LPDs by funds provision as aninitial capital and supervision for theestablishment of the LPDs. The pro-vincial government of Bali plans to setup one LPD in each of the 1,600 cus-tom villages.

As seen in Table 1, at the end of2001, it was recorded that 174 LPDshave been established in Gianyar dis-trict, and they were spread over all ofthe seven subdistricts. These LPDstogether employ 873 employees di-rectly. In terms of asset development,the LPDs of Gianyar have also experi-enced a remarkable growth. Table 1also shows that in only two years be-tween 1999 and 2001, total assets in-creased almost 2.5 times from Rp58billion to Rp125 billion. This growthwas mainly caused by the growth ofloans outstanding that more thandoubled from Rp36 billion in 1999 toRp89 billion in 2001. In addition, es-tablishment of new LPDs also has in-creased the total assets.

Meanwhile, its equity also morethan doubled from Rp10.9 billion in1999 to Rp25.4 billion in 2001. Equityhere refers to value to invested capital

(initial investment) plus retained earn-ings. The increasing equity resultedfrom the increase of retained earnings(total profit). As shown in Table 1,total profit of the LPDs has increasedfrom Rp4.4 billion in 1999 to Rp10.2billion in 2001. In addition to the profit,the initial investment for new estab-lishments of the LPDs also has raisedthe total equity.

The main activity of the LPDs islending-savings activity for mainlysmall-scale entrepreneurs, small trad-ers, and farmers. The volume of loansoutstanding also rapidly increases fromyear to year. The data in Table 1 showsthat in 1999 the volume of loans out-standing was Rp36 billion and in 2001this amount increased to Rp89 billion.Moreover, other than the volume ofloans outstanding, the number of bor-rowers also increased from 36,454borrowers to 49,593 borrowers in thesame period.

The development indicators ofLPDs from deposits side are savingsand time deposits. Both savings andtime deposits are very high, not only interms of the value of funds generated,but also in terms of the number ofsavers and depositors. Table 1 showsthat the total amount of funds gener-ated from the clients through savingsand time deposits exceeded the totalamount of loans outstanding in 1999and 2001. In 1999 the generated fundsfrom the clients were Rp45.5 billionwhile the total of loans outstandingwere Rp36 billion. In 2001 theseamount increase to Rp97 billion andRp89 billion respectively. Table 1 also

252

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

shows that the number of savers anddepositors also exceeded the numberof borrowers in 1999 and 2001. In2001, the number of borrowers of49,593 was much lower than the num-ber of savers and depositors accountsof 122,942. These high growth of num-ber of borrowers, outstanding loans,savings and deposits is the evidence ofstrong client demand.

The figures above will in turnaffect the deposits to loans ratio (DLR)and savers (and depositors) to borrow-ers ratio. Table 1 shows that these tworatios were higher than 100 percentand the most remarkable thing is thatthe savers and depositors to borrowersratio exceeded 200 percent in 1999and 2001. This phenomenon impliesthat the LPDs in Gianyar have suc-ceeded in achieving their role as finan-cial intermediaries and to enhance theiroutreach, which is a proxy of its posi-tive impact on rural economic devel-opment. There are five main reasonsthat could explain this phenomenon(Arsyad 2005b; Arsyad 2005). Firstly,the high savers and depositors to bor-rowers ratio might be caused by socialand cultural ties (social cohesion) be-tween the people in a custom villageand its LPDs. Secondly, the peoplehave an easy access to reaching theLPD since the LPD is located in acustom village. Therefore, transporta-tion cost is very low or even zero. Thiscould also be an attractive factor forthe clients to save their money in LPDs.Thirdly, the LPDs also apply a simpleand easy procedure –both in lendingand saving services– and use mobile

banking techniques to reach their cli-ents. Fourthly, the competition amongfinancial institutions is not tight in thevillage level. Lastly, the growth ofthose figures might also be affected bythe stable and growing economy ofGianyar district. Presently, Gianyardistrict with a population of 395,000 isone of the growth engines of Bali’sprovincial economy. According to Sta-tistics of Bali Province 2001, withGross Regional Domestic Product(GRDP) of Rp 2,307 billion, Gianyarwas the fourth biggest contributor(12.16%) to Bali province after Badungdistrict (20.86%), city of Denpasar(19.19%), and Buleleng district(12.19%). Based on GRDP per capita,Gianyar was ranked third after Badungdistrict and city of Denpasar in thesame period. During Indonesian eco-nomic crisis from 1997 until 1999, theGianyar economy still experienced apositive economic growth. Gianyareconomic growth rates were 6 and 4.5percent annually in 1997 and 2001,respectively. Its economic growth ratein 2001 was higher than Bali and na-tional average growth rate of 3.4 and3.3 percent per annum, respectively.According some studies (Chaves andGonzales-Vega 1996: Franks 2000;Robinson 2001), it is argued thatmicrofinance institutions can evolvesustainably in a stable and growingeconomy.

From another perspective, therapid growth in the number of borrow-ers, savers, depositors, loan outstand-ing, savings and deposits –as has beennoted earlier– is evidence of strong

253

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

clients demand in Gianyar district.According to some interviewees2 andOka (1999), the rapid growth is anindication that the LPDs have –as fi-nancial institutions– suited to the needsof rural people and succeeded to de-velop a trust of them.

On the contrary, the high savingsand deposits growth rates could be aburden for the LPDs to pay the interestcost. To avoid this problem the LPDsdeposit some of their unloanable funds(excess liquidity) –at market interestrate– in Bank BPD Bali in accordanceto the Bali Provincial Regulation No.8/2002, Article 7 (Government of Bali2002). Table 1 shows that the LPDs’deposit in Bank BPD Bali was quitehigh. It was Rp20 billion in 1999, orabout a half of savings plus time de-posits, and Rp29 billion in 2001, orabout one-third of savings plus timedeposit. Besides its operational income,this large number of the LPD depositsin Bank BPD Bali has also contributedthe total income of the LPDs and, inturn, increased its total profit fromRp4.4 billion to Rp10.2 billion in 1999and 2001 respectively, as shown inTable 1. On the other hand, this largenumber of the LPDs deposit to BankBPD Bali also indicates that the ab-sorption capacity of rural people forcredit is still limited. This condition,however, is mainly caused by the smalland limited operational area of eachLPD which is restricted to only onecustom village according to the regu-

lation mentioned above (Governmentof Bali).

Sociocultural Environment ofthe LPDs

Socio-cultural characteristics ofan environment are also one of theimportant factors in the success ofmicrofinance institutions (Chaves andGonzales-Vega 1996; Franks 2000;Robinson 2001; Snow 1999). This sec-tion discusses the socio-cultural char-acteristics of the Balinese focusing onthe custom village (desa adat) andbanjar (hamlet) as corporate groups(social system) since it will be veryuseful in assessing the factors affect-ing the repayment rate of the LPDs. Aswidely known and argued, some ofthese sociocultural factors have playeda major role in the success of govern-ment programs such as family plan-ning, small-scale industry training, andloan programs in Bali (Jayasuriya andNehen 1989: 13; Warren 1991: 233).

In Bali, besides the administra-tive village (desa dinas), which is anelement of government administration,Balinese also recognize the existenceof custom villages. The administrativevillage or perbekelan was first intro-duced by the Dutch in the early part ofthe twentieth century as the basic unitof colonial government (Warren 1993:22). The existence of administrativevillage in Bali and all over Indonesia

2 The list of interviewees is presented in Appendix 1

254

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

was reinforced by the Government ofRepublic of Indonesia through the Vil-lage Government Law No. 5/1979. ThisLaw sets out to create a uniform localadministrative structure across Indo-nesia, with the stated objective of in-creasing the effectiveness of villageadministration and public participa-tion in development policy (Warren1991: 238). However, custom villagesin Bali continued to exist as customaryinstitutions and to function alongsidetheir newly created administrativecounterparts.

The custom village is an associa-tion of people rather than a geographicor administrative unit. Warren (1993:20) describes the custom village as “acorporate community sharing collec-tive descent from the original villagefounders, who are worshipped as dei-fied ancestors in the classic three vil-lage temples the so called KahyanganTiga (The Three Holy Temples).” Eachof the three temples has a special func-tion and location in the village (Geertzand Geertz 1975; Hobart et al. 1996).3

There are two fundamentals dif-ferences between custom village (desaadat) and administrative village. Thedesa dinas boundaries are determinedalong administrative lines and seldom

coincide with those of the custom vil-lage. The custom village leader, theso-called Bandesa Adat, is elected andcustom matters are decided by the com-munity (banjar) members in a demo-cratic way in the custom village meet-ing (paruman desa). In contrast, dinas(administrative) leaders, the so-calledPerbekel or Kepala Desa, are appointedby, and responsible to, higher govern-ment levels such as subdistrict anddistrict government level. Accordingto Nordholt (1991), in the Soehartoera, villages maintained the right tochoose their Perbekel or Kepala Desain Bali, but in practice there were sev-eral restrictions. Candidates werescreened and sometimes there was pres-sure from above to eliminate candi-dates considered to be too independentor anti Golkar (state party) (Nordholt1991).

The status of the custom village asa societal unit based on customary lawwas reinforced by the Bali ProvincialRegulation of 1986 on the Status, Func-tion, and Role of Custom Village inBali (Government of Bali 1986). Thecustom village, as stated in article 5 ofthe Regulation, is a unit of societalcustomary law that is social and reli-gious in nature. The village is the for-

3 The first temple is Pura Puseh (Temple of Origin). This is the temple of origin in which thevillage community worships its purified and deified ancestors. It lies in the ‘godly direction,’ thatis, towards the mountains and/or east of the village core. Various gods are worshipped in this temple,but the main ones are an anonymous host of deified predecessors of the present inhabitants of thevillage. In the centre of the village, in the intermediate area between earthly and godly activity, liesPura Desa (Temple of Village or Great Council). This second temple is primarily concerned withthe fertility of the farmland in its neighbourhood. The third temple is Pura Dalem (Temple of Death)which is usually located next to the cemetery. It lies in the direction of the sea and/or the westernpart of the village. This temple, in addition to being temple of death, is the temple of chthonic powerswhere, among other things, the deceased who are not yet fully purified are remembered.

255

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

mal repository and guardian of cus-tomary law and ritual. Meanwhile, thefunction and role of custom village, asstated in article 6 of the Law, is tosupport the implementation of the de-velopment program planned by thegovernment, especially in the religious,cultural, and social areas; and to main-tain and utilize the wealth of the cus-tom village for the welfare of the peoplewithin the village. The ratification ofthe Provincial Regulation of 1986 re-flects the Provincial Government’sconcern with reinforcing the role ofcommunity institutions, grounded incustomary law and practice. The con-sideration of the regulation states thatit recognizes custom village since theyhave have grown and developed forcenturies and contributed significantlyto the livability of people in Bali.

The custom villages are usuallysubdivided into several banjar (ham-lets) for densely populated regions(Warren 1993). However, Warrenpoints out that in a large number ofcommunities, especially those foundin the mountain areas, banjar and cus-tom village represent two associationscovering a single bounded population.The banjar is the most basic associa-tion of people in custom villages (com-munities) through which religious rites,mutual aid, cultural groups, local de-velopment projects and savings andcredit activities are organized withinclose social ties. The members of banjarcomprise adult men who can prove the

completeness of their identity througha female partner – usually the wife, butsometimes sister, mother, or daughter.The focus of religious, social, and eco-nomic life of the Balinese is the banjar,which effectively4 implements localcustom (adat) in the name of the cus-tom village, and organizes communitylife in Bali (Geertz and Geertz 1975;Hobart et al. 1996; Mabbet 1985).Arsyad (2005a and 2005b) points outthat the LPDs are rooted in the com-munity and their establishment isgrounded in the customary law andpractice of its people. The institutionsare community financial institutionsowned, managed, and used by themembers of the custom village. Thestaff and clients of the LPDs, there-fore, have to follow the customaryrules (awig-awig) of the custom vil-lage.

There have been two importantduties of the banjar (Hobart et al. 1996:86-88; Mabbet 1985: 38-40). First,among the most important duties ofthe banjar is the maintenance and res-titution of the ritual purity of the cus-tom village. Each banjar has specifictasks and ritual duties to fulfill thebenefit of the village temples. Thisindicates that the village as a religious-magical authority is ranked above thesecular autonomy of the banjar. How-ever, banjar activities can be verymundane, for example, improvingroads through community work or re-storing the meetinghouse (bale banjar).

4 The banjar is effective since its decisions involved the equal participation of all families andbecause it operates through consensus rather than confrontation (Mabbet 1985: 39).

256

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

The banjar is generally responsible forpublic institutions and even more forpublic welfare, which requires not onlymaterial support but also assistance inritual matters.

Another important task of thebanjar relates to social control andsurveillance of the actions and behav-ior of the members in relation to thecustom (Hobart et al. 1996). The banjaris legally permitted to impose sanc-tions against members who do notfollow the rules (awig-awig), and finesmay be incurred. Serious offencesagainst the rules are punished by theexclusion of the wrongdoer from thebanjar. This means that he/she loseshis/her share of banjar ownership andthe plot of land on which his/her fam-ily compound is built is withdrawn.He/she also loses the right, in accor-dance to the custom, to a funeral in thevillage cemetery and subsequent cre-mation. He/she becomes an outsiderwithout security of the banjar commu-nity and must look for new life faraway from their native village. In rela-tion to the LPDs, which are owned bythe custom village, these kind social ofsanctions can be applied to the staff orclients who violate the rules of thefinancial institution, such as by cor-ruption or failure to repay their creditsproperly (Oka 1999). In other words,the rules can be expected to have apositive effect on the repayment rateof the LPDs.

Methodology

Data and model specification

The fieldwork of this study wasconducted in two parts, the first beingfrom early December 2001 until theend of March 2002 and the second inMarch 2003. The dataset used as thebasis for calculation and analysis aremainly based on financial reports ofthe LPDs of the Gianyar district in1999 and 2001 because of the limita-tions of time and other resources, andto omit the influence of Indonesianeconomic crisis before 1999. Hence,this study only focuses on the condi-tion of the LPD in the period of 1999-2001 when the economic situation ofBali was stable. The economic situa-tion after 2001 –that might havechanged– is outside the scope of thisstudy. In addition, other related datasuch as the number of client data (in-cluding borrowers, savers, and deposi-tors), the data on population and GrossRegional Domestic Product (GRDP)of Gianyar district and its subdistrictsfrom the Central Board of Statistics ofGianyar district are also used in thisanalysis.

At the end of 2001, it was re-corded that 174 LPDs have been estab-lished in Gianyar district and they werespread all over seven subdistricts.There are 103 LPDs located in foursubdistricts which are the centre of

257

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

handicraft industries (handicraft-basedsubdistricts) and 71 located in threeagricultural-based subdistricts asshown in Table 2.

After conducting the normalitytest for the data using Lilliefors test5

(Coakes and Steed 1999; Keller andWarrack 2000), the results reveal thatthe performance indicators data arenot normally distributed. Since thedatasets are not normally distributedand the repayment rate is a continuousvariable, an ordinary least squaresmodel will lead to inefficient param-

eters estimates, because of hetero-scedasticity problem (Maddala 1983:16). Alternatively, followingGoldberger (1964), Maddala (1983)suggests the use of binomial or binarychoice model6 –such as probit (or thenormit model) and logit model– toovercome the problems because it usesa dummy variable (for the repaymentrate) instead of a continuous variable.The probit and logit models usuallygive similar results and it is difficult todistinguish them statistically, since thecumulative normal distribution of

Table 2. Number of LPDs in Gianyar District by Subdistricts and EconomicCharacteristic (2001)

No. Subdistrict Number of LPD Economic characteristics

1 Sukawati 26 Handicraft industry2 Gianyar 28 Handicraft industry3 Ubud 24 Handicraft industry4 Tegallalang 25 Handicraft industry

Subtotal (a) (103)

5 Blahbatuh 25 Agriculture6 Tampaksiring 23 Agriculture7 Payangan 23 Agriculture

Subtotal (b) (71)

TOTAL (a + b) 174

Source: PLPDK, Financial Report of LPD Gianyar District of Bali Province (2001)

5 The procedure of this test is presented in the appendices. This test is suited for this case sincethe population data which mean and standard deviation are unknown. A test for normality ofKolmogorov and Smirnov is not relevant to this case since it assumes that the mean and standarddeviation of population is known (Keller and Warrack 2000: 614).

6 These binary-choice models are regression models using discrete dependent variable andinvolving two or more qualitative choices. These models assume that individuals are faced with achoice between two alternatives and that their choice depends on their characteristics.

258

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

probit model and the logistic distribu-tion are very close to each other(Amemiya 1985: 09-310; Amemiya1981: 1502; Maddala 1983: 23;Tabachnick and Fidell 2001: 536).However, the assumption that under-lying distribution is normal makesprobit analysis somewhat more re-stricted than logit analysis. Hence, thelogit analysis is considered better thanprobit analysis if there are too manycases with very high or very low prob-abilities so that an underlying normaldistribution is untenable (Tabachnickand Fidell 2001: 536). The logit modelhas another advantage over the probitmodel which is the ease of numericalcalculation, as a logistic function ismuch easier to calculate that the cumu-lative normal function of the probitmodel (Amemiya 1981). In addition,the logit model can be used withoutany change even with unequal samplesizes (Maddala 1992: 330-331). Forthese reasons, this study estimates themodel by using the logistic model(logit).

The logit model is based on thecumulative logistic probability func-tion and is specified as (Pindyck andRubinfeld 1991)

where e represents the base of naturallogarithms, which is approximatelyequal to 2.718. Pi is the probability ofa certain event, given X

i. The first step

to estimate the model is both sides ofthe model is multiplied by 1 + e–z

i to

get

(1 + e–zi)Pi = 1

Dividing by Pi, and then subtracting 1

leads to

By definition, however, e–zi = 1/ezi, sothat

Now, by taking the natural logarithmof both sides,

or

Since Pi is the probability of being theone group, and (1 - P

i) is the probabil-

ity of being other group, the ratio Pi / (1

- Pi), known as odds ratio, is simply the

odds in favor of an event A. The natu-ral log of this odds ratio is called thelogit, and therefore the model is calledthe logit model. X

i is the vector of

independent variables for the ith obser-vation; is the intercept parameter;and is the vector of coefficient pa-rameters.

e–zi =P

i

1 - Pi

Zi = log

Pi

1 - Pi

log = Zi = + Xi

Pi

1 - Pi

Pi = F(Zi) = F( + X

i) =

=

1

e –zi

1

1 + e–( + Xi)

e–zi = - 1=1

Pi

1 - Pi

Pi

259

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

The procedure of estimating coef-ficients is maximum likelihood tech-niques7 (Amemiya 1981: 1493-1499;Tabachnick and Fidell 2001: 518), andthe goal is to find the best linear com-bination of predictors to maximize thelikelihood of obtaining the observedoutcome frequencies. A positive andsignificant estimated coefficient wouldimply that an increase in the value ofthe particular explanatory variable isassociated with an increased probabil-ity of the dependent variable taking thevalue one. Given the exploratory na-ture of the analysis, the reliance onimperfect proxies and the nonlinearrelationship between the dependent andindependent variables, no attempt hasbeen made to interpret the magnitudesof the coefficients of the explanatoryvariables. Rather, the analysis focuseson the signs and significance of theestimated coefficients. Collinearitydiagnostics are performed on each setof explanatory variable employed inthe model, to ensure that multi-col-linearity is not adversely affecting theestimation of the coefficients

The logit model is used to studythe repayment rate (RR) of 154 LPDsin Gianyar district, in 2001. Since therepayment rates in this study are con-tinuous variable, they are converted toa discrete variable. In this model, P

i is

probability of LPDs having repaymentrates “above” average of repaymentrate of its population, (1 - P

i ) is a

probability of LPDs having repaymentrates “below” average of repaymentrate of its population.

Hence the logit model becomes

The repayment rate is expected tobe influenced by a range of explana-tory variables that reflect program-specific and community socioeco-nomic characteristics. The expectedsigns for the parameters coefficientare shown in Table 3. The independentvariables are as follow. First, OUTSTLis a total balance of outstanding loansof each LPD (in Rupiah). The hypoth-esis is the higher total balance of out-standing loans of the LPD, the higheris its repayment rate (Sharma and Zeller1997). This is because the greater theloan size put pressure on the borrowerto reduce the delinquency rate. Sec-ond, NUMBOR is number of clients(borrowers) of each LPD. The hypoth-esis is the larger the number of clientsof a microfinance institution, the loweris its repayment rate. The larger num-ber of borrowers could raise asymmet-ric information problem and makemonitoring and enforcing costly andless effective (Sharma and Zeller 1997).

7 Maximum likelihood estimation is an iterative procedure that starts with arbitrary values ofcoefficients and determines the direction and size of change in the coefficients that will maximizethe likelihood of obtaining the observed frequencies (Tabachnick and Fidel 2001: 518).

1, if the repayment rate is “above” average

0, otherwisey

i {

log = Zi = + X

i

Prob (RR>above)

1 - Prob (RR>above)

260

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

Third, NUMSAVER is the num-ber of savers. The hypothesis is thehigher number of savers in microfi-nance institution, the higher its repay-ment rate. The number of savers (andsavings) is an essential element forimproving the repayment rate sincesavers may indicate the bankingmindedness and the financial disci-plines of clients (Zeller 1998: 614).Fourth, NUMSTAF is number of staff,which is measured by number of staffof each LPD. I hypothesize that thelarger number of staff in the LPDs, thehigher its repayment rate. It is ex-pected that a larger number of staff inthe LPDs will result in a better repay-ment rate, since they would be able tomanage the LPDs better.

Fifth, WEALTH (dummy) is adummy variable for the wealth indexof the clients. It is hypothesized thatthe wealth of clients has a positive andsignificant relationship with the re-payment rate (Zeller 1998: 615). Thisvariable equals one if the LPDs lo-cated in subdistricts having GRDP per

capita “above” the GRDP per capita ofthe district and zero when the LPDslocated in subdistricts having GRDPper capita “below” average of the dis-trict. Sixth, DUMVIL (dummy vari-able for region) is a control variablefor the economic base of villages thatmight influence the repayment rate(Zeller 1998: 613). The hypothesis isthere will be a significant relationshipbetween the economic base of a vil-lage and the repayment rate of the LPDin that village. This variable has thevalue of one if the LPD is located insmall-scale industries based village andzero when it is located in agriculturalbased village. It is expected that therepayment rate is affected by theclient’s occupation, in particular,whether he or she is employed in theagricultural sector or in small-scaleindustry. Table 3 summarizes the in-dependent variables and expected signsfor the ordinary least square model.The specification model of the repay-ment rate is as follows:

Table 3. Independent Variables and Expected Signs of Logit Model for theRepayment Rate of the LPDs

Independent Variable Expected Sign

Outstanding loans (OUTSTL) +

Number of borrowers (NUMBOR) -

Number of savers (NUMSAVER) +

Number of staff (NUMSTAF) +

Wealth index (WEALTH) +

Dummy regions (DUMVIL) *

Note: * = no a priori expectation for sign direction

261

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

+ 1OUTSTL + 2NUMBOR +

3NUMSAVER + 4NUMSTAF +

5WEALTH + 6DUMVIL

Results and Analysis

According to Bank BPD Bali(2000), the loans portfolio of LPD isclassified into four categories: pass,doubtful, substandard, and loss. In thisstudy the repayment rate refers to theratio between the first three categoriesof outstanding loans divided by totaloutstanding loans (all four categories),and delinquent borrower ratio refers tothe number of borrowers who do notrepay their loans until past due relativeto total borrowers. Based on the data inTable 4, the LPDs within Gianyar dis-trict have a high repayment rate.

In 1999 the repayment rate was 95percent and increased to 97 percent in

2001 (Table 4). Compared to the othermicrofinance institutions in Indone-sia, these figures are quite high.8 Therepayment rate of Badan KreditKecamatan (Subdistrict CreditOrganisation) of Central Java was only80 percent. Meanwhile, the repaymentrate of the BRI Unit Desa System wasestimated 95 percent (Yaron et al.1998). In addition to a high repaymentrate, its delinquent borrowers ratiowas only 0.5 percent in 1999 and de-creased to 0.4 percent in 2001. Follow-ing Christen et al (1995: 3), these highrepayment rate and the low delinquentborrowers ratio of the LPDs are evi-dences of the willingness of the clientsto pay the interest rate even the interestrates are significantly above the rate ofinflation.

There are four interrelating rea-sons that could explain the high repay-ment rate (Arsyad 2005b; Arsyad2005). Firstly, in accordance with itsregulation, an LPD only gives loans tothe clients who have their own busi-ness, such as small-scale industry en-trepreneurs, farmers, or small traders.The credit should be used for produc-tive economic activities purposes(Government of Bali 2002) . For theLPDs management, it is relatively easyto identify the credit applicants whetheror not they have business activitiessince the operational area of each LPDis limited in a custom village in whichmost of the people know each other.

logProb (RR>above)

1 - Prob (RR>above)

8 This comparison is not intended to judge that the LPD has a better repayment rate than theothers, since it was calculated in different period and the methods of calculation might be differenteither. Nevertheless, it is still useful as a general illustration.

Table 4.Repayment Rate of LPDswithin Gianyar District ofBali Province (1999 and2001) (means)

Indicator 1999 2001

Repayment rate (%) 95 97

Source: PLPDK, Financial Report of LPDGianyar District of Bali Province (1999and 2001) (computed by the author).

262

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

As a result, this could positively influ-ence their repayment ability. The useof village agents, such as custom vil-lage leader in Bali, in screening poten-tial borrowers and collecting repay-ment would help to mitigate the infor-mation problems that hamper the per-formance of microfinance institutionswhen lending to small entrepreneurs(Arsyad 2005b; Arsyad 2005; Chavesand Gonzales-Vega 1996; Fuentes1996; Onchan 1992; Timberg andAiyar 1984; Yaron 1992). In addition,by gaining access through the agent tovillage-level enforcement mechanismssuch as social sanctions, the micro-finance institution may also mitigatesome of the problems it faces whencollecting repayment.

Secondly, most of the borrowersare from the custom village where theLPD is located. The LPDs are commu-nity financial institutions which areowned, managed, and used by themembers of the custom village. Thisembeddedness of the LPDs within itslocal institutions has caused the cli-ents’ sense of belonging of their LPDand moral obligation to help the devel-opment of their LPD. Moreover, incredit mechanism including screeningprocess and contractual enforcement,the LPDs management cooperates withthe Board of Commissioners (DewanPengawas) –led by the custom villageleader (Bendesa Adat)– who knowsthe character (reputation) of the cli-ents well. This technique has beencomparatively efficient in avoidingcostly mistakes in assessing the prob-

ability of loan repayment (Arsyad2005b; Arsyad 2005).

Thirdly, the custom (social) sanc-tions –that can be applied in accor-dance with the written custom villageregulations (awig-awig) – have forcedthe borrowers to repay their creditstimely. According to the intervieweesand Oka (1999: 17), the custom villageregulation has been effective in over-coming the problem of delinquent bor-rowers or low repayment rate. Finally,the LPDs staff members have a highmobility in respect to collecting loanrepayments. A LPD staff member vis-its the clients in their houses (mobilebanking techniques) to collect savingsdeposits and loan repayments in per-son. This system has also forced theclients to repay their loans regularlyand timely.

In summary, it could be arguedthat a high repayment rate of LPDs isaffected by practical arrangement ofLPD management using custom regu-lation which includes social norms,sanctions, and involvement of customvillage leader in screening process andcontractual enforcement of loan (in-formal institutions), regulations set upby the Central Bank (formal institu-tions), and the mechanism of collect-ing loan repayments applied by theLPDs management.

As mentioned earlier, a direct lo-gistic regression analysis was per-formed on the repayment rate and sixpredictors: outstanding loans, numberof borrowers, number of savers, num-ber of staff, wealth index, and dummy

263

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

variable for regions. Analysis was per-formed using SPSS LOGIT. After de-letion of 2 cases of missing values,data from 152 LPDs were available foranalysis: 88 LPDs with the repaymentrates (RR) above the average RR of itspopulation rate and 64 LPDs with RRbelow the average RR of its populationrate.

The first step in any regressionanalysis is to ask if the predictors, as agroup, contribute to prediction of theoutcome. In logistic regressions, thisis the comparison of the constant-onlymodel with the constant plus all pre-dictors model. The test results of thefull model with all six predictors againsta constant-only model using Hosmerand Lemeshow test are statisticallyreliable, 2(8, N =152) = 18.36, p<0.05(p-calculated = .019). This indicatesthat the predictors, as a set, reliablypredict the repayment rate of the LPDs.Moreover, this result also indicatesthat there is no multicollinearity prob-lem (Tabachnick and Fidell 2001).

The strength of the relationshipbetween the dependent variable andthe independent variables –analogousto the R2 measures in multiple regres-sion– is shown by the Cox and Snell R2

and the Nagelkerke R2 with highervalues indicate greater model fit(Tabachnick and Fidell 2001: 545).Both R2 are low, the Cox and Snell R2

is only 0.063 and the Nagelkerke R2 isonly 0.08. These figures indicate thatonly around six to eight percent ofshared variance between the repay-ment rate and the set of predictors canbe found. Hence, the gain in predictionis minimal. The model prediction suc-cess confirms that the ability of themodel in predict the repayment rateare not high, even the predictors in themodel is significant. The overall suc-cess rate is 65 percent (the cut value is50 percent), with 84 percent of theLPDs with the RR above average and39 percent of the LPDs with the RRbelow average. This result also indi-cates that the predictors, as a set, reli-

Table 5. Logistic Regression Analysis of the Repayment Rate

Variables Coefficients Wald test Significance(p-value)*

1. Outstanding loans .000 .084 .772

2. Number of borrowers .000 .053 .818

3. Number of savers -.001 2.646 .104

4. Number of staff .004 .001 .972

5. Wealth index .070 .034 .853

6. Dummy regions .303 .594 .441

7. Constant .143 .066 .797

Note: * Critical p-value is 0.05 (p-value<0.05 means significant, otherwise).

264

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

ably distinguish the repayment rate ofthe LPDs with the repayment rate aboveaverage and the LPDs with repaymentrate below average.

According to the Wald criterion,there is no statistically significant pre-dictors influencing the repayment rate.Table 5 shows regression coefficientsand Wald test for each of coefficients.The signs for four regression coeffi-cients are as expected, but two othercoefficients are not. These results arediscussed below.

In methodology, outstanding loansare hypothesized to have a positiveeffect on the repayment rate. How-ever, the regression coefficient of out-standing loans (OUTSTL) is insignifi-cant (p-value>0.05). This means thatthe outstanding loans do not influencethe repayment rate. The hypothesisthat the greater the loan size, the greateris the probability of unwilling default(greater repayment rate) or the greaterloan size puts pressure on the bor-rower to reduce delinquency, is notproven. Therefore, the outstandingloans do neither improve nor worsenthe repayment rate in this case. Thefinding concurs with Sharma andZeller’s (1997) study of microfinanceinstitutions (ASA, BRAC, and RDRS)in Bangladesh (Sharma and Zeller1997).

The number of savers and the valueof savings reflect the financial disci-pline of the clients of a microfinanceinstitution, as has been mentioned ear-lier. These factors could be expectedto increase the repayment rate or tomaintain a high repayment rate. How-

ever, the regression coefficient of num-ber of savers (NUMSAVR) is insig-nificant. This means that the numberof savers does not influence their re-payment rate. The result implies thatthe influence of the savers on improv-ing the repayment rate is not signifi-cant. On the other hand, however, thisresult indicates that the financial disci-pline of the clients of LPDs is high, asshown by their high repayment ratesdiscussed earlier. Hence, regardlessthe provision of savings service, therepayment rate of the LPDs remainshigh. Referring to Arsyad’s studies(2005 and 2005b), this situation mightbe affected by the effectiveness ofsocial sanctions (written in the customvillage regulation) in enforcing con-tractual agreement between the LPDsand their clients.

The regression coefficient of num-ber of borrowers (BORROWERS) isinsignificant. This means that the num-ber of borrowers does not influencethe repayment rate. The hypothesisthat the larger number of borrowercould cause imperfect informationproblems (monitoring and enforcingproblem) that would in turn affect therepayment rate is not evident in thisstudy. The LPDs have intimate knowl-edge of their clients and rely on mecha-nisms of social control in screeningand enforcement problems based onthe shared social and religious normsof the custom village (Arsyad 2005band 2005). As a result, client informa-tion is easily available which couldeliminate the asymmetric informationand adverse selection problems as a

265

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

key problem that affects the likelihoodof default of microfi-nance institution.The study by Sharma and Zeller (1997)also reveals that the number of bor-rowers per staff does not affect therepayment rate of micro-finance insti-tutions in Bangladesh.

As is hypothesized earlier, thelarger number of staff, the higher is therepayment rate since the larger num-ber of staff, the higher is the LPDstaff’s capability of monitoring andmanaging their clients. In this study,however, the number of staff does nothave any influence on the repaymentrate which is shown by the insignifi-cant regression coefficient of numberof staff (NUMSTAF). This impliesthat the number of current staff hasbeen quite enough to manage the LPDs.With the ratio of 67 borrowers per staffin 2001, the LPDs are still able tomaintain their high repayment rates.

Two dummy variables which areWEALTH and REGION do not have asignificant effect on the repaymentrate either. The regression coefficientof dummy variable WEALTH1 andWEALTH2 –control for GRDP percapita of subdistrict– is insignificant.This means that the wealth of the cli-ents does not influence their repay-ment rate. The result shows that thewealthier clients (handicraft subdis-tricts) do not repay their debt any bet-ter than the poorer ones (agricultural

subdistricts). Hence, in other words,the wealth of group member does notimprove the repayment rate, and thecapacity to repay does not matter inactual repayment performance in thecase of LPDs. Theoretically, the re-payment rate is a function of bothcapacity and willingness to repay(Norell 2001: 128).9 Accordingly, thisimplies that willingness to repay is themost important factor affecting thehigh repayment rate of LPDs. Again,referring to Arsyad’s studies (2005and 2005b), this good willingness torepay might be a result from the effec-tiveness of social sanctions in enforc-ing contractual agreement between theLPDs and their clients.

The regression coefficient ofdummy variable REGION1 and RE-GION2 –control for socioeconomicconditions that may influence the re-payment rate– is not significant. Itmeans that the type of regions (handi-craft based subdistricts or agriculturalbased subdistricts) has no influence onthe repayment rate of the LPDs. Hence,it can be concluded that the repaymentrate of the LPDs in Gianyar district isnot influenced by the socioeconomicconditions of the regions. Then it couldbe argued that the repayment rate ofLPDs is directly affected by practicalarrangement of LPD management us-ing custom regulation including socialnorms, sanctions, and involvement of

9 In respect to capacity and willingness to repay, Norell (2001) classifies four types of clients:willing and able to repay, willing but unable to repay, unwilling but able to repay, and unwilling andunable to repay.

266

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

custom village leader in screening pro-cess and contractual enforcement ofloan (informal institutions), and indi-rectly affected regulations set up bythe Central Bank (formal institutions).

The insignificancy of all predic-tors in the model leads to a question ofwhat factors do influence the repay-ment rate. Referring to Arsyad’s stud-ies (2005 and 2005b), it could be ar-gued that this condition indicates thatthe informal institutions –such as cus-tom regulation (social norms and sanc-tions), social cohesion, and the use ofsocial mechanism in screening thecredit applicants and enforcing the re-payment through involvement of thecustom leader– have played an impor-tant role in enforcing the willingnessto repay of the clients that, in turn,results in the high repayment rate ofthe LPDs.

Some studies (Arnott and Stiglitz1990; Fuentes 1996; Stiglitz 1990) re-veal that informal institutions tend toexploit a comparative advantage inmonitoring and enforcement capacity.The primary advantage of the LPDs –as a local institution– in terms of moni-toring is that individuals who interactin a variety of non-market contextstend to know each other well. Theytherefore may have a greater ability tomonitor each other than do commer-cial banks. In this respect, the charac-ter-based lending system has been ap-plied appropriately and effectively bythe LPDs through social mechanism.

This finding also conforms toChaves and Gonzales-Vega’s (1995)argument that social pressure from lo-cal tradition is one of the importantfactors affecting compliance ofmicrofinance clients in the rural areasof Indonesia. Hence, it could be in-ferred that the high repayment rate ofthe LPDs in Gianyar district of Balihas been influenced by the informalinstitutions.

Conclusion

An analysis of the repayment rateusing quantitative approach (logisticmodel) indicates that the Balinese so-cial custom, including social values,norms, and sanctions have an impor-tant influence on sustaining the highrepayment rate of the LPDs. This find-ing conforms to the previous studiesusing institutional approach (Arsyad2005b, 2005c and 2005) revealing thatthe high repayment rate of the LPDs inGianyar district is influenced by theirinstitutional arrangement that basedon custom regulation which includessocial norms, sanctions, and involve-ment of custom village leader in screen-ing process and contractual enforce-ment of loan (informal institutions),by regulations set up by the CentralBank (formal institutions), and themechanism of collecting loan repay-ments applied by the LPDs manage-ment.

267

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

References

Adams, D. W. 1984. Are the arguments for cheap agricultural credit sound? In Adams,Dale W. and J. D. Von Pischke (editors) Undermining Rural Development withCheap Credit. Boulder, Colorado: Westview Press.

Adams, D. W., and D. A. Fitchett (editors). 1992. Informal Finance in Low-IncomeCountries. Boulder, C.O.: Westview Press.

ADB. 2000. Finance for the Poor: Microfinance Development Strategy. Manila: AsianDevelopment Bank.

Amemiya, T. 1985. Advanced Econometrics. Oxford, UK: Basil Blackwell.

Amemiya, T. 1981. Qualitative response models: A survey. Journal of Economic Litera-ture 19 (December): 1483-536.

Arnott, R., and J. E. Stiglitz. 1990. Moral hazard and nonmarket institutions: Dysfunc-tional crowding out or peer monitoring. American Economic Review 81 (1): 179-90.

Arsyad, L.. 2005b. An assessment of microfinance institution performance: The impor-tance of institutional environment. Gadjah Mada International Journal of Business 7(3): 391-427.

Arsyad, L.. 2005c. An assessment of performance and sustainability of microfinanceinstitutions: A case study of village credit institutions of Gianyar, Bali, Indonesia.Unpublished Ph.D. Thesis. Adelaide, Australia: School of Business Economics,Flinders University.

Arsyad, L. 2005. Institutions do really matter: Important lessons from village creditinstitutions of Bali. Journal of Indonesian Economy and Business 20 (2): 105-19.

Bank Indonesia. 1997. Circular Letter of Bank Indonesia No.30/3/UPPB. Jakarta, Indo-nesia: Bank Indonesia.

Bennett, L. 1998. Combining social and financial intermediation to reach the poor: Thenecessity and dangers. In Kimenyi, M. S., R. C. Wieland, and J. D. Von Pischke(editors) Strategic Issues in Microfinance. Aldershot, England: Ashgate.

Chaves, R. A., and C. Gonzales-Vega. 1996. The design of successful rural financialintermediaries: Evidence from Indonesia. World Development 24 (1): 65-78.

Christen, R. B., E. Rhyne, and R. Vogel. 1995. Maximizing the outreach of microenterprisefinance: the emerging lessons of successful programs. Focus Note 2. Washington,D.C.: CGAP.

Christen, R. P. 1998. Keys to financial sustainability.In Kimenyi, M. S., R. C. Wieland, andJ. D. Von Pischke (editors) Strategic Issues in Microfinance. Aldershot, England:Ashgate.

Coakes, S. J., and L. G. Steed. 1999. SPSS: Analysis without Anguish. Brisbane: JohnWiley and Sons.

Franks, J. R. 2000. Macroeconomic stabilization and the microenterpreneur. Journal ofMicrofinance 2 (1): 69-89.

Fuentes, G. A. 1996. The use of village agents in rural credit delivery. The Journal ofDevelopment Studies 33 (2): 188-209.

268

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

Geertz, H., and C. Geertz. 1975. Kinship in Bali. Chicago: The University of ChicagoPress.

Ghate, P. 1988. Informal credit markets in Asian developing countries. Asian Develop-ment Review 6 (1): 64-85.

Government of Bali (Provincial). 1988. The Bali Provincial Regulation No. 2/1988 onVillage Credit Institutions.

Government of Bali (Provincial). 1986. The Bali Provincial Regulation No. 6/1986 on theStatus, Function, and Role of Custom Village.

Government of Bali (Provincial).. 2002. The Bali Provincial Regulation No. 8/2002 onVillage Credit Institutions.

Hobart, A., U. Ramseyer, and A. Leemann. 1996. The Peoples of Bali. Oxford: BlackwellPublishers.

Jayasuriya, S., and I. K. Nehen. 1989. Bali: economic growth and tourism. In Hal Hill(editor) Unity and Diversity: Regional Economic Development in Indonesia since1970. New York: Oxford University Press, Inc.

Keller, G. and B. Warrack. 2000. Statistics for Management and Economics (5th ed.).Albany: Duxbury.

Ledgerwood, J. 1999. Microfinance Handbook: An Institutional and Financial Perspec-tive. Washington, D.C.: The World Bank.

Mabbet, H. 1985. The Balinese. Wellington, New Zealand: January Books.

Maddala, G. S. 1983. Limited-Dependent and Qualitative Variables in Econometrics.Cambridge: Cambridge University Press.

Morduch, J. 1999. The microfinance promise. Journal of Economic Literature 37 (Decem-ber): 1569-614.

Morduch, J. 2000. The Microfinance schism. World Development 28 (4): 617-29.

Nordholt, H. Schulte. 1991. State, Village, and Ritual in Bali: A historical perspective.Amsterdam: VU University Press.

Norell, D. 2001. How to reduce arrears in microfinance institutions. Journal of Microfinance3 (1): 115-30.

Oka, I. G. N. 1999. Peranan awig-awig desa adat dalam operasional Lembaga PerkreditanDesa (LPD) (The role of awig-awig – custom village regulation– in operational ofLPD. Mimeo. Majelis Pembina Lembaga Adat (Forum for the Development ofCustom Institutions) Propinsi Daerah Tingkat I Bali.

Onchan, T. 1992. Informal rural finance in Thailand. In Adams, Dale W., and D. A. Fitchett(editors) Informal Finance in Low-Income Countries. Boulder, Colorado: WestviewPress.

Otero, M. 1999. Bringing development back, into microfinance. Journal of Microfinance1 (1): 8-19.

Pindyck, R. S., and D. L. Rubinfeld. 1991. Econometric Models and Economic Forecasts(3rd ed.). New York: McGraw-Hill, Inc.

269

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

Robinson, M. S. 2001. The Microfinance Revolution: Sustainable Finance for the Poor.Washington, D.C.: The World Bank.

Scapens, R. W. 1990. Researching management accounting practice: The role of case studymethods. British Accounting Review 22: 259-81.

Sharma, M., and M. Zeller. 1997. Repayment performance in grouped-based creditprograms in Bangladesh: An empirical analysis. World Development 25 (10): 1731-42.

Snow, D. 1999. Microcredit: An institutional development opportunity. InternationalJournal of Economic Development 1 (1): 65-79.

Stiglitz, J. E. 1990. Peer monitoring and credit markets. The World Bank EconomicReview 4 (3): 351-66.

Tabachnick, B. G., and L. S. Fidell. 2001. Using Multivariate Statistics (4th ed). Boston:Allyn and Bacon.

Timberg, T. A., and C. V. Aiyar. 1984. Informal credit markets in India. EconomicDevelopment and Cultural Change 33 (6): 43-59.

Wai, U. T. 1992. What have we learned about informal finance in three decades? In Adams,D. W., and D. A. Fitchett (editors) Informal Finance in Low-Income Countries.Boulder, Colorado: Westview Press.

Warren, C. 1993. Adat and Dinas: Balinese Communities in the Indonesian State. Oxford:Oxford University Press.

Warren, C. 1991. Adat and dinas: Village and state in contemporary Bali. In Geertz, H.(editor) State and Society in Bali. Leiden: KITLV Press.

Woolcock, M. J. V. 1999. Learning from Failures in Microfinance: What unsuccessfulcases tell us about how group-based programs work. The American Journal ofEconomics and Sociology 58 (1): 17-22.

Yaron, Y. 1992. Successful rural finance institutions. World Bank Discussion Papers.Washington, D.C.: The World Bank.

Yaron, Y. 1994. What makes rural finance institutions successful? The World BankResearch Observer 9 (1): 49-70.

Yaron, Y., Mc. D. Benjamin, and S. Charitonenko. 1998. Promoting efficient ruralfinancial intermediation. The World Bank Research Observer 13 (2): 147-70.

Yin, R. K. 2003. Case Study Research: Design and Methods. Sage: Nebury Park.

Zeller, M. 1998. Determinants of repayment performance in credit groups: The role ofprogram design, intragroup risk pooling, and social cohesion. Economic Develop-ment and Cultural Change 46 (3): 599-620.

270

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

Appendices1. List of Interviewees*

No. Name Position Date of Interview

1 Bagus Sara Provincial Government Officer 6 February 2002

2 Gusti Arya Provincial Government Officer 6 February 200220February 2003

3 Bagus Sana Bank BPD Bali Officer 7 February 200221February 2003

4 Wayan Weka Bank BPD Bali Officer 7 February 200221 February 2003

5 Nyoman Awan Chairman of LPD Talepud 7 & 8 February 2002

6 Made Dana Chairman of LPD Mas 21-23 February 2003

7 Ketut Awan Chairman of LPD Kerta 25 & 26 February 2003

8 Wayan Jana Member of Commissioner Board of LPD Mas 23 February 2003

9 Gde Dana Chief of Commissioner Board of LPD Kerta 25 & 26 February 2003

10 Ktut Empu LPD client 22 February 2002

11 Wayan Elin LPD client 23 February 2002

12 Wayan Arsha LPD client 22 February 2002

*Name of interviewees are disguised

2. Procedure of conducting Lillifors Test

The procedure of this test is taken from Keller & Warrack (2000, p.614-617) and Coakes& Steed (2001, p.35). The procedure as follows:

Suppose a cumulative distribution function is defined as

F(x) = P (X x)

The tables of cumulative binomial and Poisson distributions provide values for

for several values of k.

The sample cumulative distribution function, S(x), is defined as the proportion of samplevalues that are less than or equal to x. The mean (x) and s are calculated from the data. Thenwe define the test statistic D as the largest absolute difference between S(x) and F(x). Thatis,

D = max F(x) – S(x)

P (X x) = P(x)

P

X=0

271

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

Then we test the hypotheses

H0: The data are normally distributed

H1: The data are not normally distributed

Suppose = 0.05 (level of significance for testing these hypotheses) or based on the levelof significance a and the sample size we can find the critical value of D from the Lilliforstable. When the significance level is greater than 0.05 or D-calculated is greater than D-critical value, then normality is assumed.

3. Computer Results of Logistic Analysis

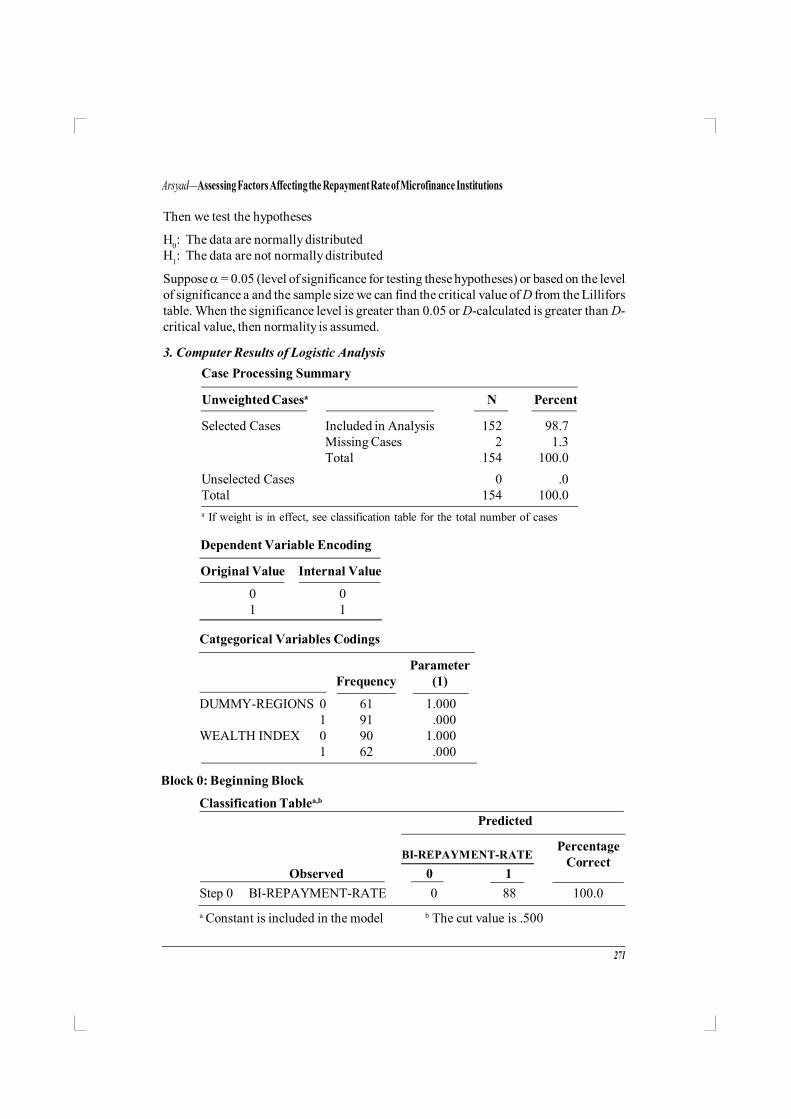

Block 0: Beginning Block

Case Processing Summary

Unweighted Casesa N Percent

Selected Cases Included in Analysis 152 98.7Missing Cases 2 1.3Total 154 100.0

Unselected Cases 0 .0Total 154 100.0

a If weight is in effect, see classification table for the total number of cases

Catgegorical Variables Codings

ParameterFrequency (1)

DUMMY-REGIONS 0 61 1.0001 91 .000

WEALTH INDEX 0 90 1.0001 62 .000

Dependent Variable Encoding

Original Value Internal Value

0 01 1

Classification Tablea,b

Predicted

BI-REPAYMENT-RATE

Observed 0 1

Step 0 BI-REPAYMENT-RATE 0 88 100.0

a Constant is included in the model b The cut value is .500

PercentageCorrect

272

Gadjah Mada International Journal of Business, May-August 2006, Vol. 8, No. 2

Variables in the Equation

B S.E. Wald df Sig. Exp (B)

Step 0 Constant -.318 .164 3.758 1 .053 .727

Variables not in the Equationa

Score df Sig.

Step 0 Variables OUTS2001 4.045 1 .044

BORROWER 4.131 1 .042

SAVERS 6.849 1 .009

NSTAFF 3.945 1 .047

WEALTH(1) .001 1 .972

DUMMY(1) .053 1 .819

a Residual Chi-Squares are not computed because of redundancies

Block 1: Method= Enter

Omnibus Tests of Model Coefficients

Chi-Square df Sig.

Step 1 Step 9.842 6 .131

Block 9.842 6 .131

Model 9.842 6 .131

.131

Model Summary

-2 Log Cox and Snell NagelkerkeStep likelihood R Square R Square

1 197.070 .063 .084

Hosmer and Lemeshow

Step Chi-Square df Sig.

1 18.357 8 0.19

273

Arsyad—Assessing Factors Affecting the Repayment Rate of Microfinance Institutions

Contigency Table for Hosmer and Lemeshow Test

BI-PAYMENT-RATE BI-PAYMENT-RATE= 0 = 1

Step Observed Expected Observed Expected Total

1 1 10 12.500 5 2.500 152 13 10.388 2 4.612 153 11 9.566 4 5.434 154 10 9.069 5 5.931 155 11 8.690 4 6.310 156 4 8.210 11 6.790 157 8 7.858 7 7.142 158 10 7.491 5 7.509 159 3 7.017 12 7.983 1510 8 7.211 9 9.789 17

Classification Tablea

BI-REPAYMENT-RATE

Observed 0 1

Step 1 BI-PAYMENT-RATE 0 74 14 84.11 39 25 39.1

Overall Percentage 65.1

a The cut value is .500

PercentageCorrect