As process development and manufacturing (cmc) for biologics development-an overview 26 nov09

28

November 26 2009 Academia Sinica NanKang, Taiwan, R.O. China

-

Upload

steven-lee -

Category

Health & Medicine

-

view

16.638 -

download

6

description

This is a high level overview presentation which was made for Academia Sinica audience as a special invitation by the President

Transcript of As process development and manufacturing (cmc) for biologics development-an overview 26 nov09

November 26 2009 Academia Sinica

NanKang, Taiwan, R.O. China

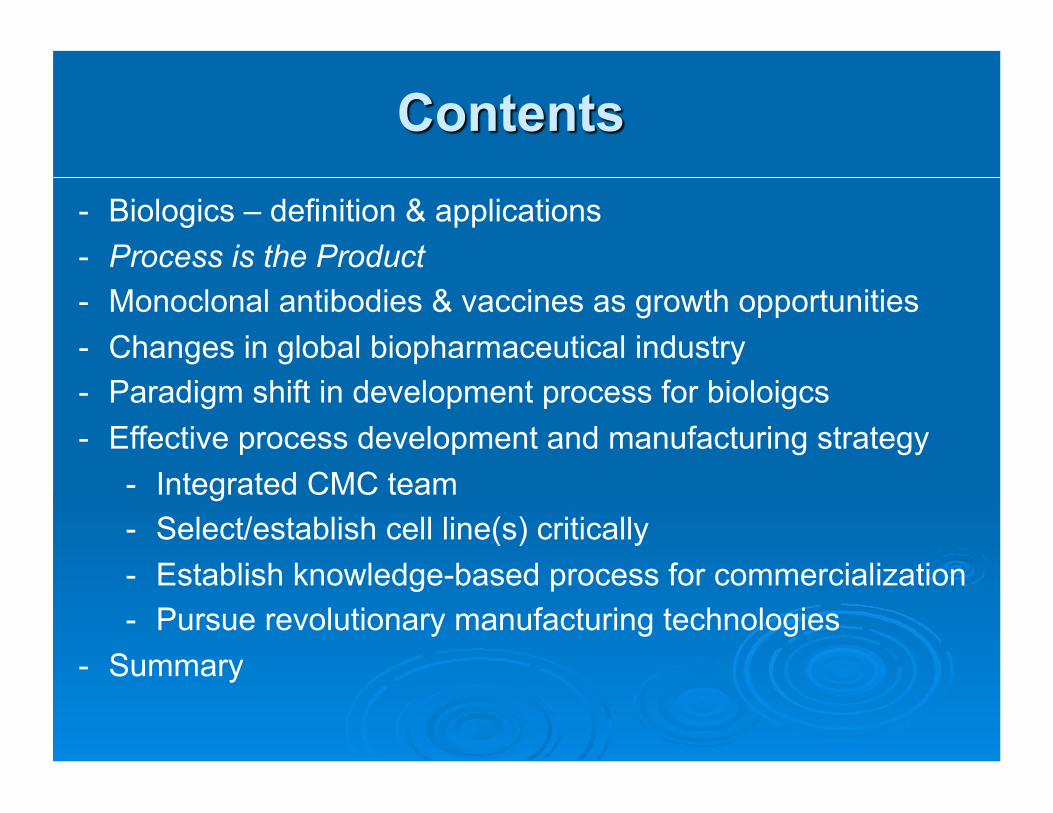

- Biologics – definition & applications - Process is the Product - Monoclonal antibodies & vaccines as growth opportunities - Changes in global biopharmaceutical industry - Paradigm shift in development process for bioloigcs - Effective process development and manufacturing strategy

- Integrated CMC team - Select/establish cell line(s) critically - Establish knowledge-based process for commercialization - Pursue revolutionary manufacturing technologies

- Summary

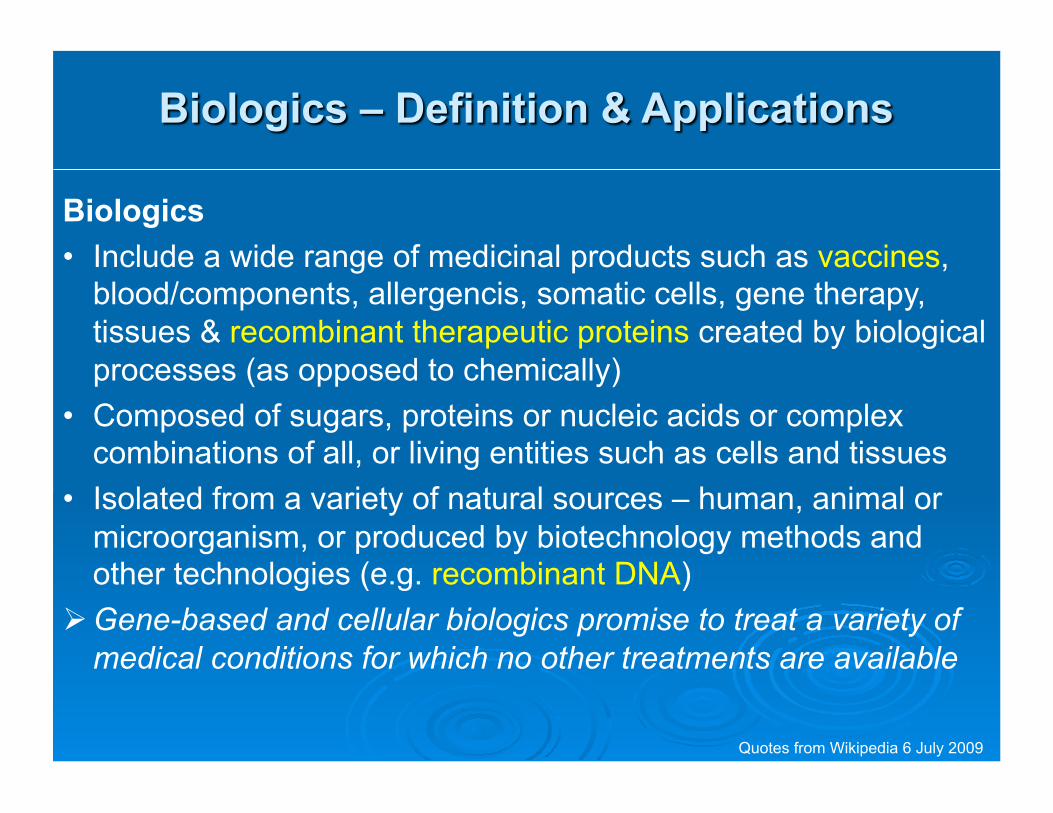

Biologics • Include a wide range of medicinal products such as vaccines,

blood/components, allergencis, somatic cells, gene therapy, tissues & recombinant therapeutic proteins created by biological processes (as opposed to chemically)

• Composed of sugars, proteins or nucleic acids or complex combinations of all, or living entities such as cells and tissues

• Isolated from a variety of natural sources – human, animal or microorganism, or produced by biotechnology methods and other technologies (e.g. recombinant DNA)

Gene-based and cellular biologics promise to treat a variety of medical conditions for which no other treatments are available

Quotes from Wikipedia 6 July 2009

Chemical Biologics Size (M.W.) < 500* 20,000 - 200,000+* Complexity Low High Process Conditions (T/P) High Ambient

In-Process Concentration Concentrate (~100g/L) Dilute (.5 -5g/L) Reactor Volume < 8,000 L ~20,000+L Reaction Steps Multiple chemical Complex product

reactions/isolations made by living cells Production Solvents Organic Aqueous Isolation/Purification Crystallization Chromatography Product Definition Few simple assays Many complex assays Process Changes Equivalency Comparability

maybe clinical trials Patent/IP Molecules Process Knowhow IP Expiration Threat Generics dominant Biosimilars evolving

PROCESS is the product

Rituxan® 145,000

Glucophage® 166

Taxol® 854

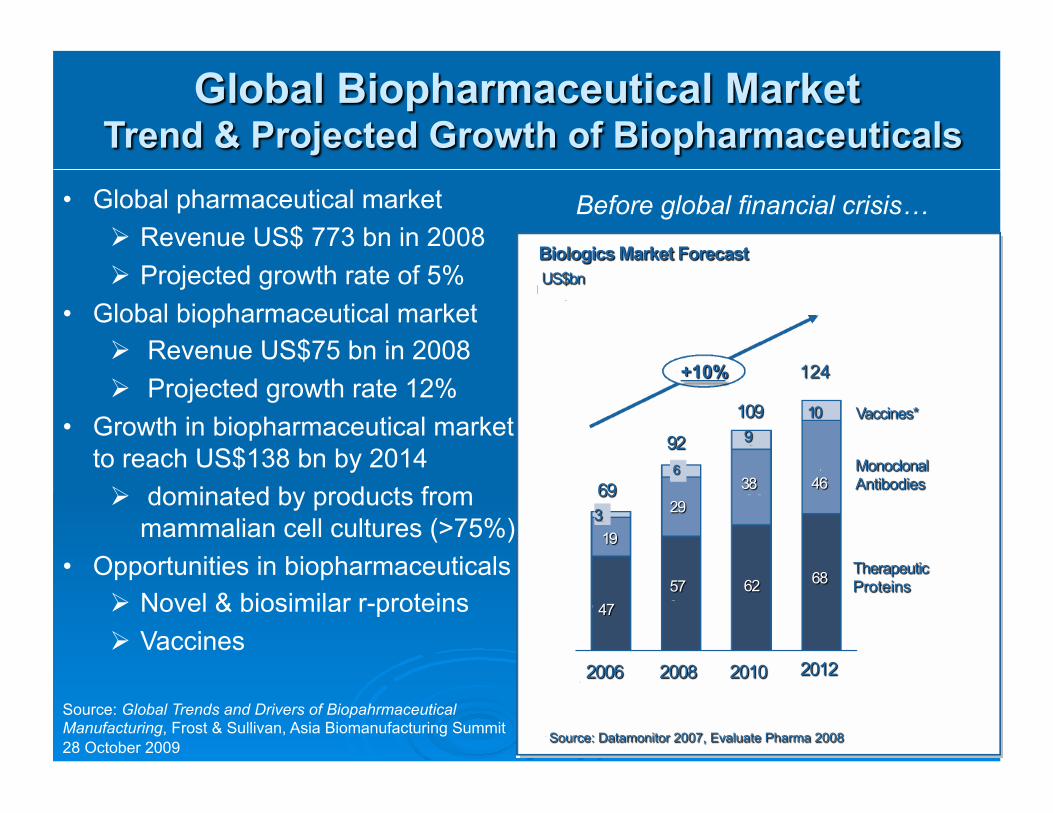

• Global pharmaceutical market Revenue US$ 773 bn in 2008 Projected growth rate of 5%

• Global biopharmaceutical market Revenue US$75 bn in 2008 Projected growth rate 12%

• Growth in biopharmaceutical market to reach US$138 bn by 2014 dominated by products from

mammalian cell cultures (>75%) • Opportunities in biopharmaceuticals

Novel & biosimilar r-proteins Vaccines

Source: Global Trends and Drivers of Biopahrmaceutical Manufacturing, Frost & Sullivan, Asia Biomanufacturing Summit 28 October 2009

Before global financial crisis…

Therapeutic Proteins = Biopharmaceuticals • 75 FDA approved therapeutic proteins • > 500 additional proteins under development • Broad applications:

Cancers & autoimmune diseases (treated by monoclonal antibodies and interferons)

Heart attacks, strokes, cystic fibrosis and Gaucher's disease (treated by Enzymes and blood factors)

Metabolic diseases: diabetes (treated by insulin) Blood diseases: anemeia (treated by erythropoietins), hemophilia

(treated by blood clotting factors). • Worldwide sales approximately $57 billion in 2006 with projected growth of

13% , or >$90 bn by 2010. • Monoclonal antibodies (Mabs) ~32bn in 2008, growing rapidly to 30% global

biologics market Piribo, “Global Protein Therapeutics Market Analysis", ProLOG Feb 13, 2008

Best Selling Monoclonal Antibodies 2006-2008 ($33 billion)

Genetic Name Brand FDA

approval Companies

Sales ($ billion) 2006 2007 2008

1 Infliximab c Remicade 1998 J&J 4.2 5.04 6.5

2 Rituximab c Rituxan 1997 Roche 4.7 5.01 5.6

3 Trastuzumab hz Herceptin 1998 Roche 3.14 4.4 4.8

4 Bevacizumab Avastin 2004 Roche 2.4 3.93 4.7

5 Adalimumab h Humira 2002 Abbott 2.04 3.06 4.4

6 Cetuximab c Erbitux 2004 Bristol Myers Squibb, Merck KgA 1.1 1.35 2.0

7 Ranibizumab hz Lucentis 2006 Novartis, Roche 0.38 1.2 1.5

8 Palivizumab hz Synagis 1998 Astra Zeneca 1.1 0.62 1.2

9 Omalizumab hz Xolair 2003 Roche, Novartis 0.52 0.64 0.85

10 Natalizumab, hz Tysabri 2004/2006 Biogen Idec, Elan 0.06 0.46 0.6

11 Panitumumab h Vectibix 2006 Amgen 0.04 0.21 0.3

12 Abciximab c ReoPro 1994 J&J, Lilly 0.28 0.29 0.29

13 Efalizumab hz Raptiva 2003 Genentech, Merck Serono 0.16 0.21 0.28

14 Certolizumab TNFα Cimzia 2008 UCB 0.10

15 Tocilizumab Actemra Japan 2008 Roche

16 Ustenkinumab Stelara Canada 2008 EMEA 2009 J&J

12 approved and marketed monoclonal antibodies with low sales (<$100 million) are not included

Source: Krishan Maggon, Global Monoclonal Antibodies Market Review 2008 (World Top Ten mAbs)

Source: Global Trends and Drivers of Biopahrmaceutical Manufacturing, Frost & Sullivan, Asia Biomanufacturing Summit 28 October 2009

• Global vaccines market will grow to over a USD $23.8 bn by 2012, growing at ~11% per year • Novel and improved vaccines growing at 58% p.a.

Traditional and combinations Include mostly pediatric & partially adult vaccines

Novel and therapeutic vaccines include both adult & therapeutic

Global Vaccine Market US$ bn

• Pandemic & seasonal Flu vaccines: to reach $7.1 bn in 2010 with 19.8% growth rate, driven by pandemic flu vaccine global supply shortage (H5N1, H1N1)

• Driven by bird flu (2005) and swine flu (2009), government spending worldwide on Pandemic Influenza Preparedness tripled to $7 bn in 2009 ($2.2 bn in 2004, 17% CAGR), reaching ~ $10 bn by 2015 (5% CAGR)

• Global Pandemic Influenza Preparedness Market: estimated @$52 bn in 2010-2015 (5% CAGR)

Novel cell-based process & manufacturing technology reaching the market: Baculovirus system/Insect cells (Protein Sciences, Novavax) Mammalian cells: Vero (Baxter), MDCK (Novartis) Per.C6 (Sanofi/Crucell); in serum-free media Avian cells: EB66, duck embryonic stem cell line by Vivalis DNA vaccines: VGX Pharma (IND) early development

Global Pandemic Influenza Preparedness Market Forecast 2010-2015, Publication: 04/2009 by Market Research Media.

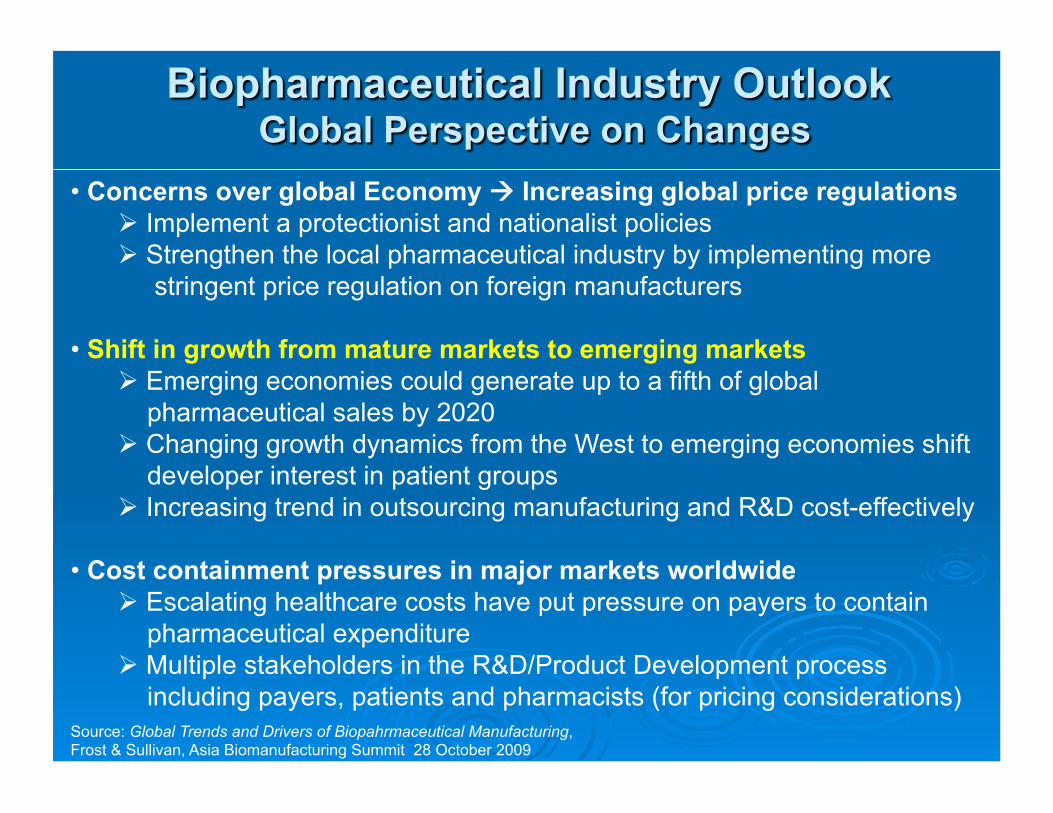

• Concerns over global Economy Increasing global price regulations Implement a protectionist and nationalist policies Strengthen the local pharmaceutical industry by implementing more stringent price regulation on foreign manufacturers

• Shift in growth from mature markets to emerging markets Emerging economies could generate up to a fifth of global pharmaceutical sales by 2020 Changing growth dynamics from the West to emerging economies shift developer interest in patient groups Increasing trend in outsourcing manufacturing and R&D cost-effectively

• Cost containment pressures in major markets worldwide Escalating healthcare costs have put pressure on payers to contain pharmaceutical expenditure Multiple stakeholders in the R&D/Product Development process including payers, patients and pharmacists (for pricing considerations)

Source: Global Trends and Drivers of Biopahrmaceutical Manufacturing, Frost & Sullivan, Asia Biomanufacturing Summit 28 October 2009

Source: Global Trends and Drivers of Biopahrmaceutical Manufacturing, Frost & Sullivan, Asia Biomanufacturing Summit 28 October 2009

Emerging, 115

Japan, 88

EU, 172

Global Pharmaceutical: 2009 Market Sizes*

US, 302

* All values are in US$, Billions

Global Pharmaceutical Sales

2008

Growth Rate 4.5-5.5%

2009

Gro

wth

Rat

e in

Sal

es (%

)

US EU Japan Emerging

10%

15%

5%

Growth in emerging country markets: Far outstrip growth in the US & EU

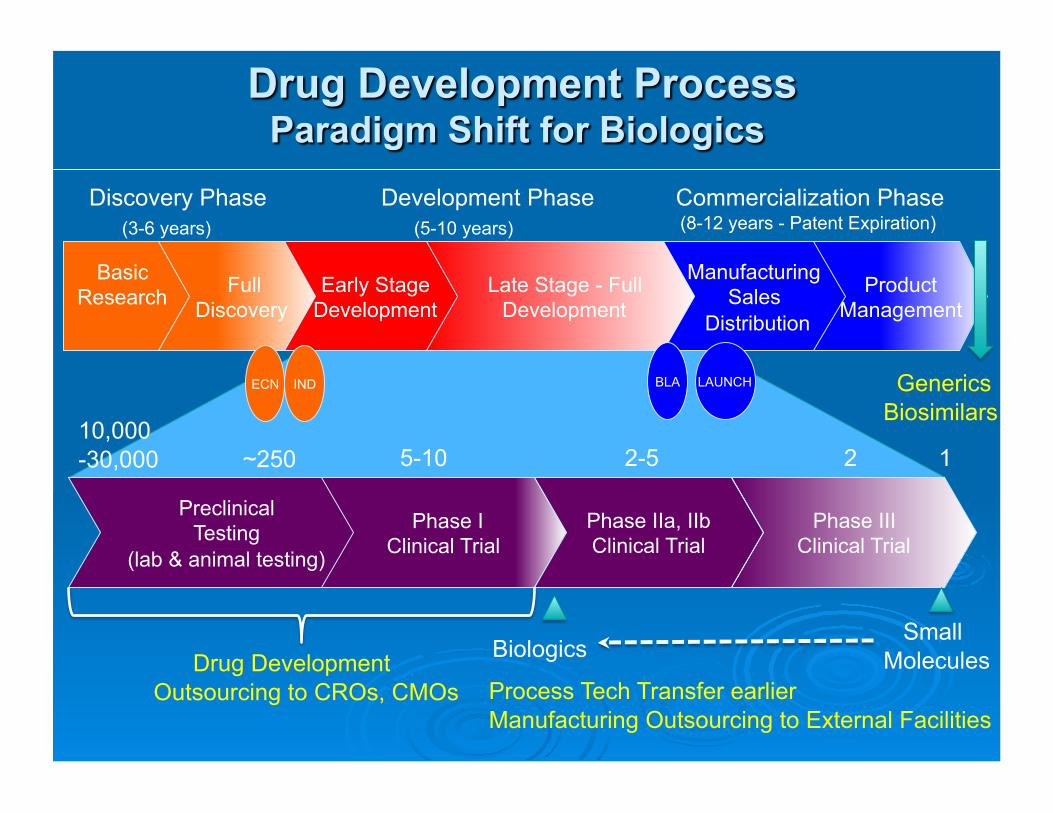

Basic Research Full

Discovery

Discovery Phase (3-6 years)

Early Stage Development

Late Stage - Full Development

Development Phase (5-10 years)

Product Management

Manufacturing Sales

Distribution

Commercialization Phase (8-12 years - Patent Expiration)

BLA LAUNCH ECN

Preclinical Testing

(lab & animal testing)

10,000 -30,000 ~250

Phase I Clinical Trial

5-10

Phase IIa, IIb Clinical Trial

2-5

Phase III Clinical Trial

2 1

Generics Biosimilars

Process Tech Transfer earlier Manufacturing Outsourcing to External Facilities

Small Molecules Biologics Drug Development

Outsourcing to CROs, CMOs

IND

Full Drug Development Capabilities and Infrastructure Required - CMC: Process development & biologics Manufacturing - Preclinical and Clinical: Toxicity, Phases 1 and III, comparability studies - Filing and regulatory challenges

High Barriers to Entry - $50M – $500M long term investment required - Competition with existing brands (low price differentials) - Complexity of products (not API) and manufacturing facilities

Highly Competitive Markets - Large pharmaceutical companies moved in: Merck, Novartis, Aztrazeneca - Major generics companies formed alliance: Teva & Lonza

Launch & Commercialization

Molecular Biology Cell Line & Process

Development

2-3 years

Preclinical & Clinical

Development

3-4 years

Filing, Regulatory Review & Approval

1-2 years

Chemistry, manufacturing and control (CMC) • Manufacturing Information “pertaining to the

composition, manufacture, stability and controls used for manufacturing the drug substance and the drug product”

• Information “ensure that the company can adequately produce and supply consistent batches of the drug”

Early development stage Evaluate current technology to produce product, begin

cell line and process development, and product characterization

Supply GLP material for preclinical toxicology study & produce GMP material for clinical trials

Begin developing process with end in mind

CELL CULTURE • Molecular Biologists • Microbiologists • Cell Biologists • Virologists

ANALYTICS • Analytical Biochemists • Biophysical Chemists • Protein Biochemists

PURIFICATION • Chromatographers • Protein Biochemists • Biochemical Engineers

Biologics Process Research

<10L

Commercial scale production 2000lL – 20,000L

Process Devt & Medium Scale

production 10L-500L

Fill & Finish

• Process development, optimisation, scale-up

• Productivity enhancement • QbD, PAT implementation • Product quality & stability

• New cell line development

• Expression engineering

• Media design • Novel product

• Process scale up • DS Manufcturing

facility operations • COGS improvement • Lean manufacturing

FORMULATION • Formulation chemists • Protein Biochemists • Engineers

• Vial filling, packing • Lyophilization, • Supply chain operations • COGS improvement • Lean manufacturing

FUNCTIONAL EXCELLENCE

New cell line? Process changes? Formulation changes?

ONE CMC TEAM

Source: http://www.gene.com/gene/products/information/oncology/herceptin/moa.html

1981 - HER2 gene cloned 1985 - Axel Ullrich and Art Levinson clone HER2 gene 1990 - Creates anti-HER2 monoclonal Antibody (Herceptin) 1992 - Files Herceptin IND, Phase I trials initiated (25-50

patients) 1993 - Herceptin Phases II trials begin (250-200 patients) 1995 - Initiates Phase III, 3 trials (500-1,000 patients) 1996 - Partners with DAKO for commercial diagnostic testing

kits 1997 - Completes Phase III enrollment 1998 - Presents Phase III data demonstrating effect with

chemotherapy and increase time to disease progression 1998 - Herceptin approved by FDA

Fully integrated high performance team delivers a mAb in <10 years

• All key expertise critical for product development available in country • Government support for infrastructure and high risk investment • Early development focus

Integrate in-country project team with core elements Fill gaps in various support areas by appropriate consultants Form oversight committee to support Project Team

Discovery (internal & external)

Clinical Institutes Or CROs

Clinical hospitals

CMC Institutes or CMOs

Marketing Consultant?

Preclinical Institutes or CROs Legal/IP

Consultants

Regulatory Consultant?

Novel drug or Biosimilars Early Development

Commercial Manufacturing or CMOs

Selection of cell lines – product specific & IP sensitive Many matured cell line platforms to choose from (e.g. mAbs:

CHO, NSO, per.C6) Cell line selection and construction in early basic research stage

without considering manufacturing may result in challenges/delays in commercialization

Select cell line critically with END in mind: titer, stability, product glycosylation & manufacturability

change of cell line post phase I clinical trials undesirable process changes post phase II to be minimized

Process is Product Cell line dictates process

Selective to infection; reduces risk to adventitious agents

A-Bio notes: process information is gathered from EPAR sources and published literature; CELVAPAN information is from Baxter

Swine cell lines: EB66 duck embryonic stem cell line by Vavilis shows promises

• Product design & selection in early basic research stage without considering manufacturing may result in challenges/delays in commercialization

• Characterization of desired product driven by clinical needs impacts significantly downstream

• Product characterization requires advanced analytics • Product complexity presents challenges in consistent supply to

patients (eg. blood factors, live virus vaccines) Multiple cell hosts developed at early stage for strategic decision

including manufacturability

Process is Product Product quality challenges process (eg. glycosylation pattern)

Glycan homogenity • Large statistical population of variants • Difficult to achieve due to macro and microhetergenity • Achievable via process design and manufacturing consistency

Immunogenicity - injection site reactions/threat of anaphylaxis Change in efficacy – ADCC response (Rituxin, tumor killing) Product incomparability after scale up (Lumizyme, Genzyme)

• Myozyme (160L) = Lumizyme (2,000L) • New BLA requested submission over carbohydrate structure

changes CMC comparability issues (Erbitux, Imclone)

• pre-clinical PK issues: sBLA for non-small lung cancer withdrawn • Additional PK requested by FDA for Erbitux 1st line head & neck

cancer Biopharm Bulletin. March 13, 2009

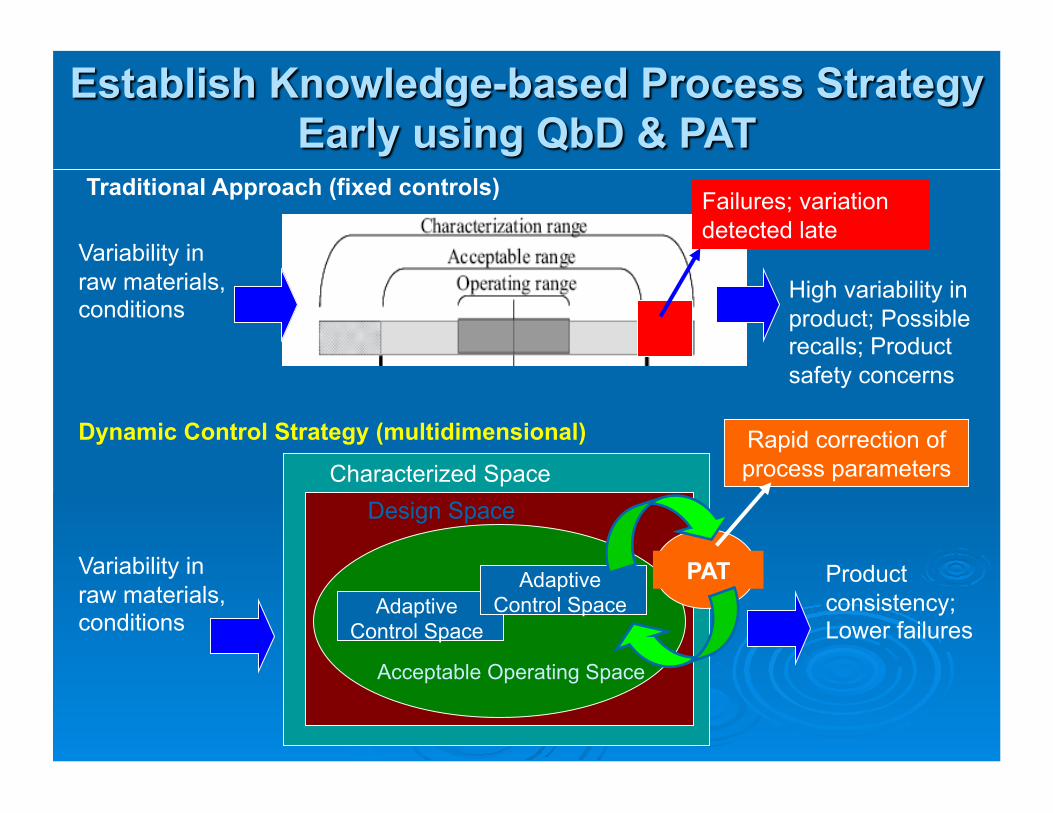

Traditional Approach (fixed controls) Failures; variation detected late

Variability in raw materials, conditions

High variability in product; Possible recalls; Product safety concerns

Dynamic Control Strategy (multidimensional)

Variability in raw materials, conditions

Characterized Space Design Space

Acceptable Operating Space

Adaptive Control Space

Adaptive Control Space

PAT Product consistency; Lower failures

Rapid correction of process parameters

Genentech has built a deep knowledge base for Quality by Design (QbD) approaches: • 5 licensed & 26 mAbs in active development • 6 licensed sites for mAb DS production & 9 successful DS site transfers • 7 successful major version changes • 13 major Drug Substance Comparability Protocols approved

40 planned comparability efforts through 2010 based on QbD Expanded Comparability Protocols: to bundle ‘like’ changes

within a single submission Successful transfer to Singapore: Lucentis DS plant (microbial

1,000L) late 2006-2010 FDA license Avastin DS plant (Cell culture, 80,000L) Early 2007 -2010 FDA license (~37 mths) “The Progress of Biotechnology manufacturing and Process Sciences” Patrick Yang, Genentech, Inc., Nov. 5, 2007, APBioCheDSC, Taiwan.

High Cell Productivity

Facility Efficiencies

Using disposable systems reduces SIP and CIP

requirements

Reduction of Process Equipment Size

Moving of process equipment into gray space reduces cleanroom space.

Process and facility modularization reduces

construction time

Process Simplification

Chromatography Alternatives Crystallization, Ppt, Q filters

Equipment with Integrated instrumentation for real time

control and release

Automated sampling and monitoring with new sensors

Current mAb platform improvement: Higher

capacity resins, One column process, No Protein A

Chemical Process like - Continuous Processing

TREND:

Higher cell productivity and process optimization result in smaller and less complex

manufacturing facilities (20,000L vs. 2,000L)

“The Progress of Biotechnology manufacturing and Process Sciences” Patrick Yang, Genentech, Inc., Nov. 5, 2007, APBioCheDSC, Taiwan.

Upstream Process

Downstream Process

Disposable Technology: Eliminates CIP, SIP, utilities Controlled Environment Modules: Gowning , operator mobility , protects product & people Advantages: 60%++ reduction in capital investment, 40% less space needed, 85% reduction in water and waste, 32% reduction in COGS Faster deployment: 12-18 months vs. 4+ years

For biologics, Process is the Product – effective process development for manufacturing critical for product quality and consistency, hence commercialization.

Monoclonal anitbodies and vaccines present significant opportunities among future biologics being developed – advanced manufacturing platform available to improve productivity and reduce COGS.

Emerging market will enjoy significant growth in biopharmaceuticals driven by global changes

Drug development process paradigm shift towards earlier tech transfer around phase I for biologics – integrated cross functional CMC team, formed early to guide process development with END manufacturing ability in mind essential for successful commercialization.