Applied Materials is accelerating Solar - pole-derbi.com Romain Beau de Lomenie ERBI... · Applied...

17

External Use Applied Materials is accelerating Solar Romain Beau de Lomenie Thin Film Module Group Head Solar Business Group Applied Materials, Inc. DERBI Conference, Perpignan, France June 6 th 2008

Transcript of Applied Materials is accelerating Solar - pole-derbi.com Romain Beau de Lomenie ERBI... · Applied...

External Use

Applied Materials is accelerating SolarRomain Beau de LomenieThin Film Module Group HeadSolar Business GroupApplied Materials, Inc.

DERBI Conference, Perpignan, FranceJune 6th 2008

External Use2

Safe Harbor StatementThis presentation contains forward-looking statements, including those relating to Applied Materials’ growth opportunities, product capabilities. acquired businesses, cost-per-watt-reduction strategy, efficiency roadmap, solar contracts, and financial goals. These statements are subject to known and unknown risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements, including but not limited to: demand for solar products, which is subject to many factors, including global economic and market conditions, government policies and incentives relating to renewable energy, technological innovations, the cost of competing sources of energy, and evolving industry standards; the performance of acquired businesses; Applied’s ability to (i) successfully develop, deliver and support its broad range of products and expand its markets and develop new markets, (ii) effectively manage its resources and production capability, (iv) accurately predict the characteristics of, and capitalize on opportunities in, emerging markets, and (v) attract and retain key employees; and other risks described in Applied’s SEC filings. All forward-looking statements are based on management’s estimates, projections and assumptions as of February 20, 2008, and Applied undertakes no obligation to update any such statements.

External Use3

– Oct 1967 in Mountain View, California� Founded

– > 19,000 Silicon IC systems– > 600 Flat Panel Display systems– > 500 Glass and Web Coating Systems

� Installed Base

– ~ 3,500 field engineers� Service

– $5.1 Billion� RD&E Investment (FY’03 – FY’07)

– 18 countries, over 100 locations– Owned manufacturing in Germany,

Israel, Switzerland, Taiwan, US– Development in North America, Asia,

Europe and Israel

� Worldwide Locations

– ~ 14,000� Worldwide Employees

– $9.73 Billion� Revenue (Fiscal 2007)

Applied MaterialsApplied Materials ’’ OverviewOverview

External Use4

Large Area Platforms

ATON™

MULTIWEB™

PECVD 5.7

Applied Materials Capabilities

Integration

Automation

Process Technology

Service & Support

External Use5

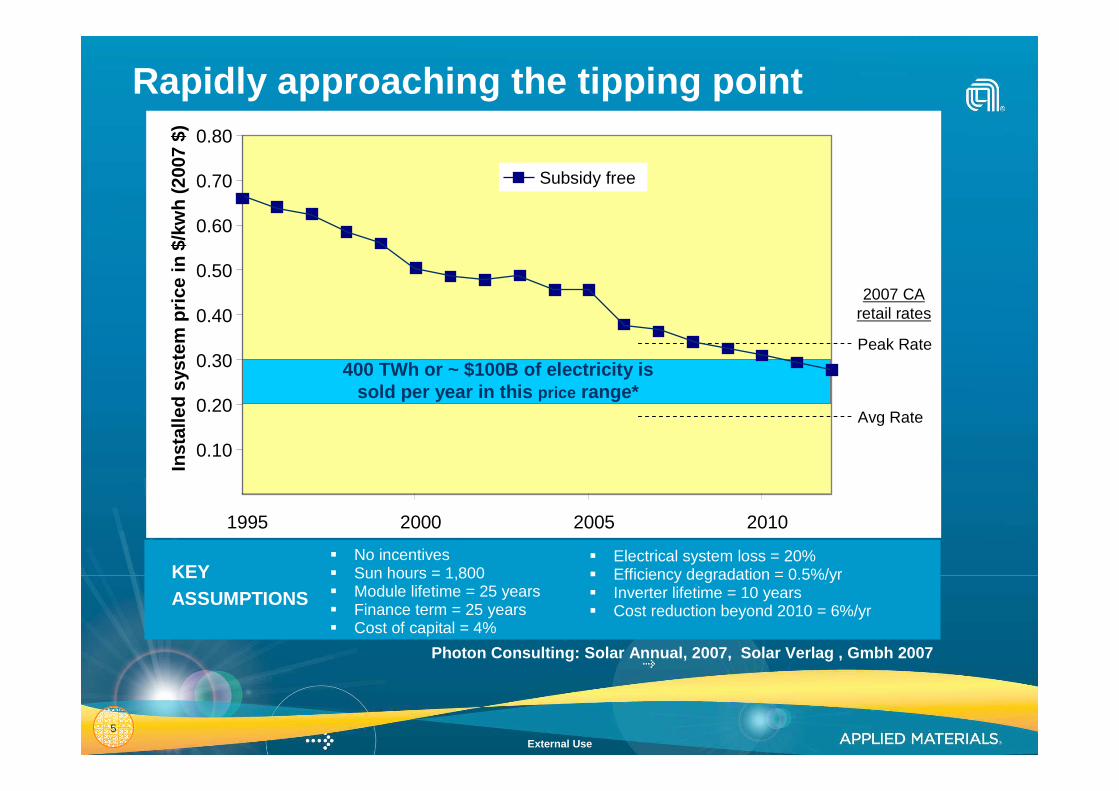

Rapidly approaching the tipping point

Peak Rate

Avg Rate

2007 CAretail rates

400 TWh or ~ $100B of electricity is sold per year in this price range*

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

1995 2000 2005 2010

Inst

alle

d sy

stem

pric

e in

$/k

wh

(200

7 $)

Subsidy free

Photon Consulting: Solar Annual, 2007, Solar Verla g , Gmbh 2007

� No incentives� Sun hours = 1,800� Module lifetime = 25 years� Finance term = 25 years� Cost of capital = 4%

� Electrical system loss = 20%� Efficiency degradation = 0.5%/yr� Inverter lifetime = 10 years� Cost reduction beyond 2010 = 6%/yr

KEYASSUMPTIONS

External Use6

Mid-Size Installations (no ITC)

Utility Scale PV electricity

Peak Rate

Avg Rate

Assumptions:PV Cost reduction past 2010 = 6% per yearUtility rate increase = 3% per year

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

2006 2008 2010 2012 2014 2016 2018 2020

Price below which PV goes mainstream ($2.50 - $3.00 $/Wp)

Inst

alle

d sy

stem

pric

e $/

kWh

(200

7 $)

External Use7

Cost per watt

Extending Cost Reduction Focus to SolarExtending Cost Reduction Focus to Solar

5 nano-dollars10 cents

1,400,000 trillion4 trillion

20041974

20,000,000x Cost Reduction

Source: SIA, IC Knowledge LLC$1,500/m2$30,000/m2

25 million /m20.3 million/m2

20051995

20x Cost ReductionSource: Display Search, Nikkei BP, Applied Materials

Cost per transistor

FIRSTFIRST

Cost per area

THENTHEN

NOWNOW

External Use8

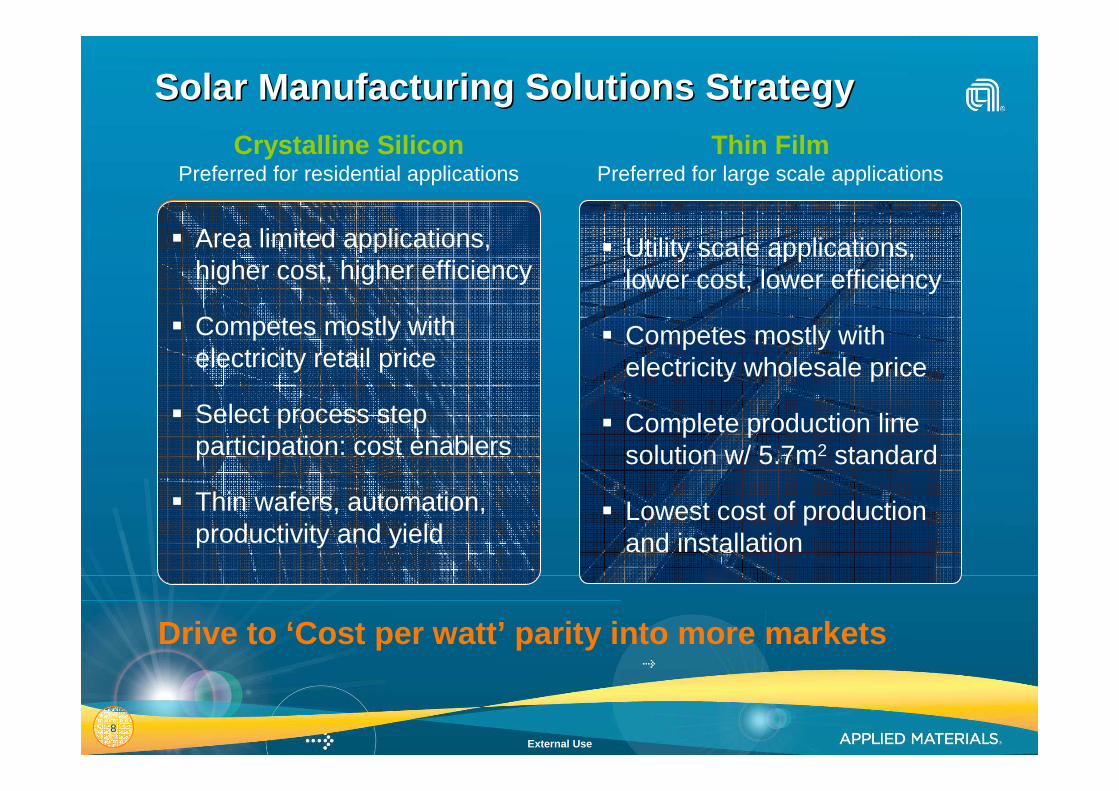

Crystalline SiliconPreferred for residential applications

Thin FilmPreferred for large scale applications

� Area limited applications, higher cost, higher efficiency

� Competes mostly with electricity retail price

� Select process step participation: cost enablers

� Thin wafers, automation, productivity and yield

� Utility scale applications, lower cost, lower efficiency

� Competes mostly with electricity wholesale price

� Complete production line solution w/ 5.7m2 standard

� Lowest cost of production and installation

Solar Manufacturing Solutions StrategySolar Manufacturing Solutions Strategy

Drive to ‘Cost per watt’ parity into more markets

External Use9

c-Si: Focus on High Value Processes

Thin Wafer Processing

� High Productivity Systems

� Cell Efficient Processes

� Low Manufacturing Cost

InstallationModuleLaminateCell Production / ManufactureWaferingIngotsPoly

SiliconStep Names Inspect / Test

Edge IsolationMetallizationPassivationEmitter

FormationSaw

Damage

Applied’s c-Si Defined TAM

Applied’s 2008 c-Si SAM ~42% of c-Si TAM

Pho

to

External Use10

Scaling up: Scaling up: SunFabSunFab ™™ Thin Film LineThin Film Line

� Complete production line of world largest 5.7m2 largest PV modules

� Thin film silicon glass-PVB-glass module design

� 50MW~75MW single line capacity w/ multi-line GW capacity design

� 2010 goals: $1.00/Wp production cost @10% efficiency

� > 20% reduction in BOS cost with large size and bonded rail design

External Use11

Going BigGoing Big

LCD industry leading world largest PECVD platform

External Use12

$1/Wp at 10% efficiency within reach

� Current initial tandem cell efficiency: 11.6%

� Current steady state module aperture efficiency: 9. 3%

� Current cell uniformity over 5.7m 2 substrate: 7% (rel.)

� TCO* tool qualification – Q3’08

* Transparent Conductive Oxide

$/W

p

On track for 10% + and <$1/W goals

µc-Si

a-Si

TCOGlass

Back Contact

External Use13

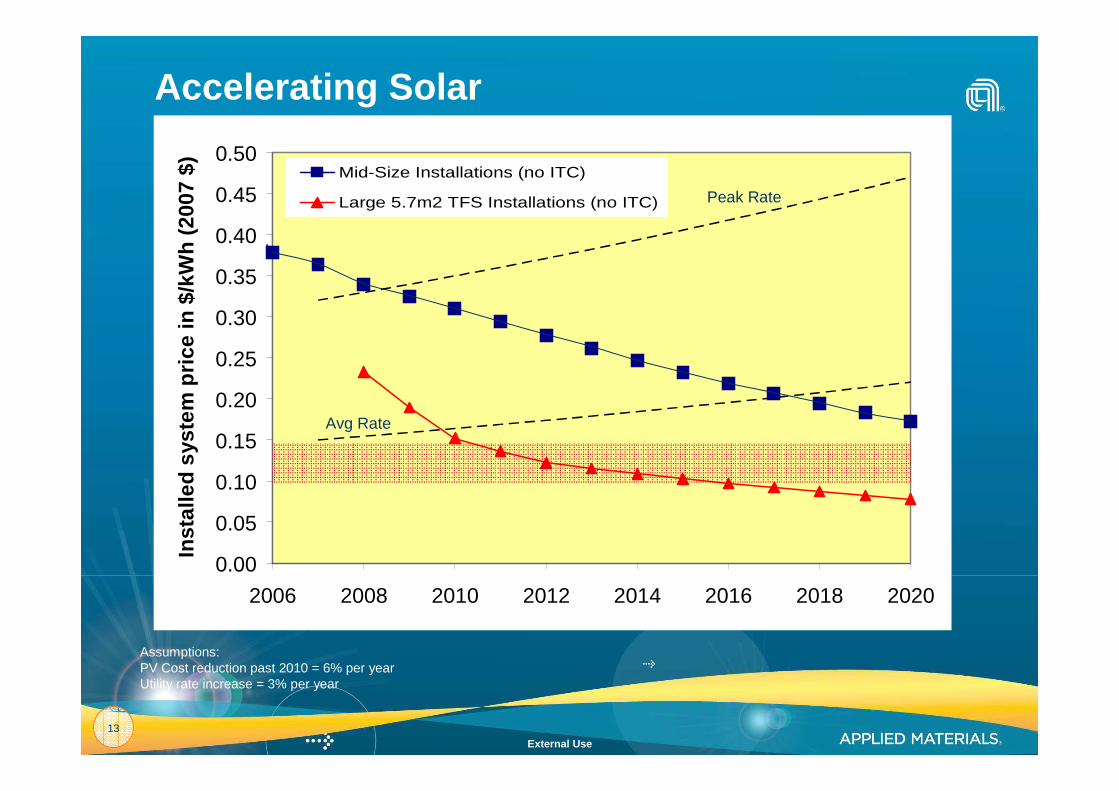

Mid-Size Installations (no ITC)

Large 5.7m2 TFS Installations (no ITC)

Accelerating Solar

Peak Rate

Avg Rate

Assumptions:PV Cost reduction past 2010 = 6% per yearUtility rate increase = 3% per year

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

2006 2008 2010 2012 2014 2016 2018 2020

Inst

alle

d sy

stem

pric

e in

$/k

Wh

(200

7 $)

External Use14

Summary

� Applied Materials is extending its cost reduction focus to Solar

� cSi: residential market, strong portfolio in cost enabling steps, focus on thin wafers and automation

� Thin film: utility scale market, Sunfab enables PV to go mainstream by 2010

� Sunfab sets the 5.7m2 standard, allowing rapid adoption and scaling globally with > 2GW of announced capacity sold

Applied Materials is accelerating Solar!

External Use15

External Use16

Applied Materials Reporting Segments

AdjacentAdjacentTechnologiesTechnologies

Design, manufacture, sale and service of equipment used to fabricate solar cells, flexible electronics and energy-efficient glass

Manufacture and sale of equipment to fabricate semiconductor chipsSiliconSilicon

Broad range of products1 to maintain, service and optimize customers’ semiconductor fabs

FabFabSolutionsSolutions

Design, manufacture, sale, and services of equipment used to make flat panel displaysDisplayDisplay

External Use17

1

10

100

1,000

10,000

100,000

2000 2010F 2020F 2030F 2040F

TW

h1 /

Yea

r

Solar Electricity Production (TWh)

1 TWh = Terrawatt-hour = 1 Billion Kilowatt-hours2 GWp = Gigawatt-peak, assuming average hours or sunshine Source: Solar Generation and IEA-PVPS

Total Electricity Production

10% Total

1% Total

World Electricity Production ForecastWorld Electricity Production Forecast(2000 (2000 –– 2040)2040)

US

= Consumption in labeled country/state

China

India

California 1 Million Roofs

Est. CAGR% ’00 - ’40Total Electricity Production 2.5%

(increase of 25,400TWh)Solar Energy Production 21%

(increase of 6,000TWh) ~5

~50

~500

~5,000

Equivalent Solar GWp 2

Current solar capacity

Potential of Existing US Rooftops (GWp)