annual report 2006 - · PDF fileannual report 2006 DISCOVERY ANNUAL ... 100% Science-based...

189

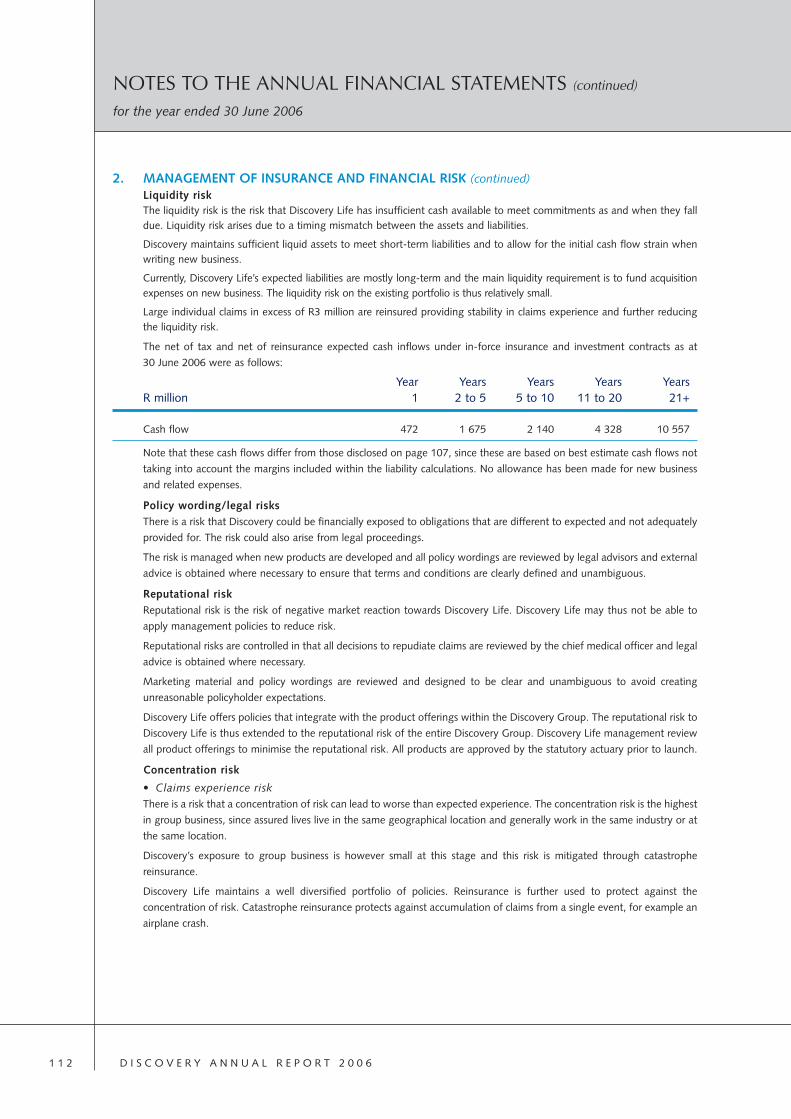

annual report 2006

Transcript of annual report 2006 - · PDF fileannual report 2006 DISCOVERY ANNUAL ... 100% Science-based...

www.discovery.co.za

annual report 2006

DISC

OV

ERY

AN

NU

AL R

EPO

RT

20

06

Discovery covers 9/11/06 0:36 Page 1

CONTENTS

Group operating structure 2

Group financial highlights 3

Group at a glance 6

Chief executive’s report 8

Discovery Health report 18

Discovery Life report 26

Discovery Vitality report 32

Destiny Health report 38

PruHealth report 44

Value added statement 50

Group consolidated embedded value statement 51

Directorate, secretary and corporate governance committees 64

Corporate governance 67

Annual financial statements 72

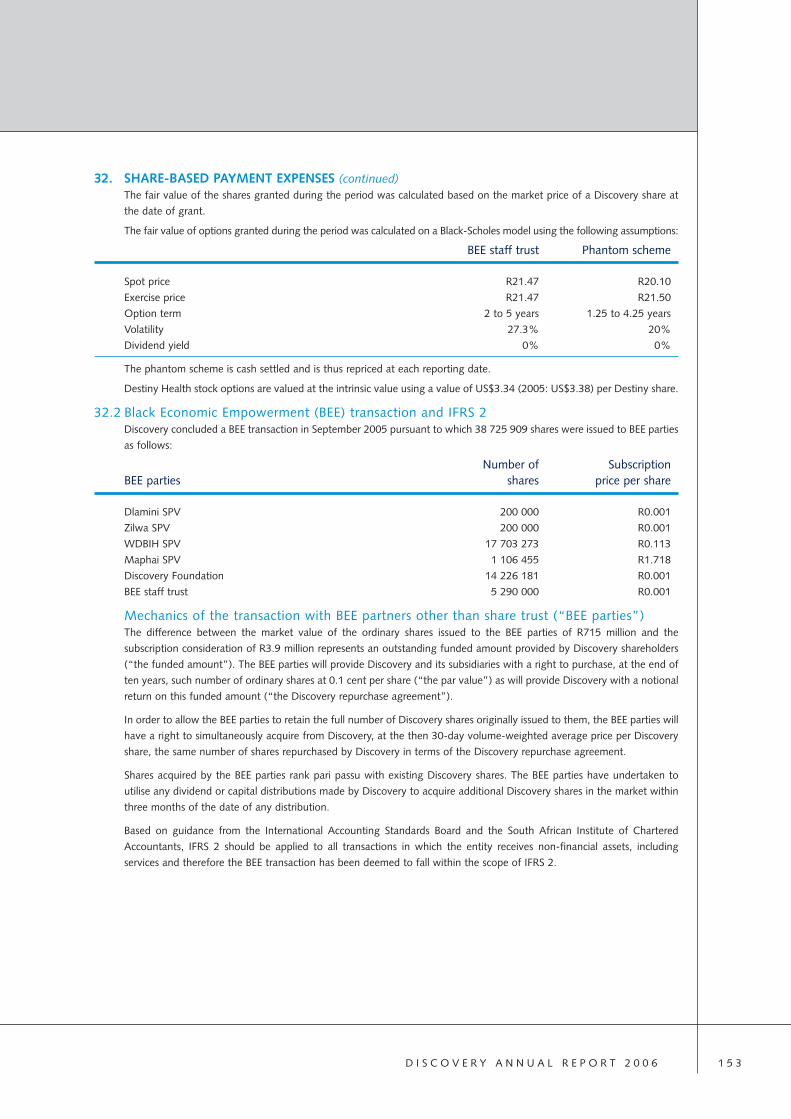

Shareholders’ information 177

›DISCOVERY’S CORE PURPOSE:

TO MAKE PEOPLEH E A LT H I E R A N D E N H A N C EAND PROTECT THEIR L IVES

OUR BUSINESS IS BUILT ON AN ETHOS OF MEETING

CLIENTS’ NEEDS F IRST AND FOREMOST

Discovery covers 9/11/06 0:36 Page 2

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 1

MEETING CLIENTS’ NEEDS THROUGH INNOVATIVE SOLUTIONS

AND CAREFUL RISK MANAGEMENT CREATES A SUSTAINED

DEMAND FOR OUR PRODUCTS, WHICH IN TURN LEADS TO

SUPERIOR PROFITABIL ITY AND STRONG GROWTH

DISCOVERY IS AT ONCE CONSERVATIVE IN ITS APPROACH TO

FINANCIAL RISK-TAKING, INNOVATIVE IN ITS PRODUCT DESIGN

AND RESPONSIVE TO CONSUMER NEEDS

A SOLUTION-CENTRIC BUSINESSBUILT ON ORGANIC GROWTH

It was a successful year for Discovery with

important developments in each of its

businesses, strong earnings growth and the

declaration of a maiden dividend.

All of Discovery’s businesses focused

intensely on innovations designed

to meet specific client needs –

resulting in strong organic growth.

A SUCCESSFUL YEAR

7558-discovery front 7-11 9/11/06 2:02 Page 1

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 62

100% South Africa’s leading private health care funder

Established in 1992

Covers 2 million livesDISCOVERY HEALTH

100% South Africa’s fastest growing major life assurer

Established in 2000

Covers 200 000 livesDISCOVERY LIFE

100% Science-based wellness programme and unique value creator

Established in 1997

Covers 1,2 million livesDISCOVERY VITALITY

98% US-based health insurance company innovative in consumer-directed care

Established in 2000

Covers 60 000 livesDESTINY HEALTH

50% UK-based joint venture leading change in the private medical insurance market

Established in 2004

Covers 75 000 livesPRUHEALTH

GROUP OPERATING STRUCTURE

2006

7558-discovery front 7-11 9/11/06 2:02 Page 2

4

VALUE CREATORS

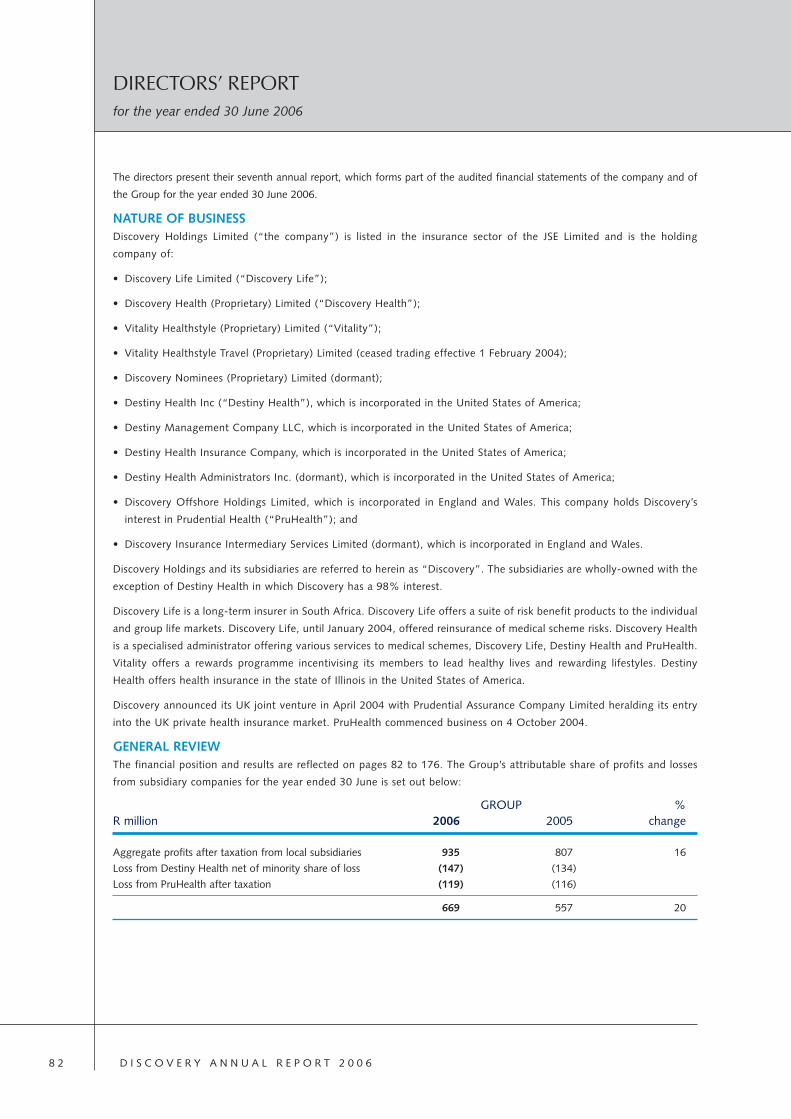

R million 2006 2005 2004 2003 2002 2001 2000

Gross inflows under management 20 427 17 295 14 345 10 946 7 739 5 494 3 559

Gross inflows under management measures the total funds managed

and received by Discovery and is an accurate measure of the continual

growth of Discovery.

25 000

20 000

15 000

10 000

5 000

000 01 02 03 04 05 06

(R million)

5 000

4 000

3 000

2 000

1 000

0

(R million)

00 01 02 03 04 05 06

R million 2006 2005 2004 2003 2002 2001 2000

New business annualised premium income

Discovery Health and Discovery Vitality 2 612 2 869 2 184 2 346 1 869 2 071 1 322Discovery Life 789 629 535 423 264 94 0Destiny Health 796 809 494 379 206 12 0PruHealth 282 35 0 0 0 0 0

4 479 4 342 3 213 3 148 2 339 2 177 1 322

New business annualised premium income measures the annualised

premiums generated by clients who have purchased Discovery

products over the last financial year. All business written by

Discovery is recurring in nature.

THE RESULTS

R million 2006 2005 2004 2003 2002 2001 2000

Embedded value 10 587 9 173 6 832 4 928 3 321 3 212 2 114

Embedded value is an actuarial calculation of the current value of

Discovery as it exists today. An embedded value calculation assumes

no growth in the current business. The continual growth of the embedded

value shows continuous shareholders’ value created by Discovery.

12 000

10 000

8 000

6 000

4 000

2 000

0

(R million)

00 01 02 03 04 05 06

GROUP FINANCIAL HIGHLIGHTS (CONTINUED)

7558-discovery front 7-11 9/11/06 2:02 Page 4

5

Cents 2006 2005 2004 2003 2002 2001 2000

Diluted headline earnings per share before abnormal items 97,0 94,2 77,4 65,7 48,1 33,6 14,3

Diluted headline earnings per share before abnormal items measures

the sustainable earnings attributable to ordinary shareholders.

2 500

2 000

1 500

1 000

500

0

(Thousand clients)

00 01 02 03 04 05 06

2006 2005 2004 2003 2002 2001 2000

Discovery Health clients 1 939 339 1 788 566 1 593 975 1 446 371 1 180 121 960 494 701 395

This is the number of lives administered by Discovery Health at

30 June. This large and diverse membership base reduces the reliance

on any one member or employer who purchases Discovery products.

2006 2005 2004 2003 2002 2001

Life individual policyholders 204 891 170 642 123 977 67 998 31 918 9 331

This is the number of principal lives on risk at 30 June. As premiums

collected from individual policyholders are recurring, each policyholder

adds to Discovery Life’s value.

250 000

200 000

150 000

100 000

50 000

0

(Clients)

01 02 03 04 05 06

70 000

60 000

50 000

40 000

30 000

20 000

10 000

0

(Clients)

01 02 03 04 05 06

2006 2005 2004 2003 2002 2001

Destiny Health clients 62 041 60 470 36 234 21 643 9 544 497

This is the number of lives administered by Destiny Health, including

its joint ventures with Guardian Life Insurance and Tufts Health Plan.

Each life adds to Destiny Health’s value.

120

100

80

60

40

20

0

(Cents)

00 01 02 03 04 05 06

7558-discovery front 7-11 9/11/06 2:02 Page 5

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 3

• OPERATING PROFIT (BEFORE BEE EXPENSES) +37% TO R1,3 BILLION

• NET PROFIT AFTER TAX (BEFORE BEE EXPENSES) +51% TO R827 MILLION

• DILUTED HEPS (BEFORE BEE EXPENSES) +34% TO 126,4 CENTS PER SHARE

• NEW BUSINESS ANNUALISED PREMIUM INCOME +3% TO R4,5 BILLION

• MAIDEN DIVIDEND OF 27 CENTS PER SHAREDECLARED

GROUP FINANCIAL HIGHLIGHTSfor the year ended 30 June 2006

7558-discovery front 7-11 9/11/06 2:02 Page 3

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 66

GROUP AT A GLANCE

DISCOVERY

It has been a successful year for

Discovery. The Group’s core purpose

of “making people healthier and

enhancing and protecting their lives”

imposes an ethos wherein always

meeting clients’ needs first and

foremost leads to superior growth

and profitability. The year under

review has illustrated the continued

efficacy of this approach.

ADRIAN GORE (42)

BSc (Hons), FFA, ASA, MAAA, FASSA

Chief Executive Officer

Discovery

NEVILLE KOOPOWITZ (42)

BCom, CFP

Chief Executive Officer

Discovery Health

HERSCHEL MAYERS (46)

BSc (Hons), FIA, FASSA

Chief Executive Officer

Discovery Life

DISCOVERY HEALTH

Discovery Health’s strong growth and

solid financial performance has again

positioned it as a major contributor to

the Discovery Group’s success. Its

scale, size and financial solidity have

further strengthened our ability to

ensure that our members receive

health care on a sustainable basis

backed by exceptional service, price

and quality.

DISCOVERY LIFE

Discovery Life’s performance every

year is characterised by a cycle of

consumer-centric innovation, followed

by rapid organic growth and

consequently, solid financial results.

In the past year, we have seen a 25%

increase in new business and a 31%

increase in operating profit. This has

bolstered Discovery Life’s contribution

to the overall performance of the

Discovery Group.

7558-discovery front 7-11 9/11/06 2:02 Page 6

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 7

ALAN POLLARD (38)

BSc (Hons), FIA, FASSA

Chief Executive Officer

Discovery Vitality

BARRY SWARTZBERG (41)

BSc, FFA, ASA, FASSA, CFP

Executive Director

Discovery

ARTHUR CARLOS (40)

BSc, FSA, ERISA (EA)

Chief Executive Officer

Destiny Health

SHAUN MATISONN (34)

BSc, FFA, FASSA, ASA, MAAA

Chief Executive Officer

PruHealth

DISCOVERY VITALITY

Discovery Vitality posted a pleasing

performance in every respect:

profitability, growth and, most

importantly, value generated for

Discovery clients. We added 47 000

lives to Vitality during the year.

Vitality’s greatest contribution to

Discovery’s overall success is the

unique integration capabilities and

product differentiation that it creates

for our other businesses.

DESTINY HEALTH

Destiny Health’s performance was

disappointing. Particularly in the first

half of the year, we saw relatively flat

growth in membership, reduced new

business and worse than expected

losses driven by elevated loss ratios.

However, we have already implemented

a number of bold steps to address the

situation and have committed to

pinning losses down to a more

sustainable level.

PRUHEALTH

PruHealth has posted an exceptional

performance. The company’s rapid

growth in new business and

membership along with better than

expected rates of renewal, indicate

that UK consumers are embracing its

unique and innovative consumer-

directed approach. If new business

growth continues at projected rates,

we expect the company to achieve

the 100 000 lives milestone by

January 2007.

7558-discovery front 7-11 9/11/06 2:02 Page 7

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 68

Adrian Gore

Chief Executive Officer, Discovery

We strive to meet clients’ needs through

innovation, operational excellence and

sound financial management, leading to

strong organic growth.

CHIEF EXECUTIVE’S REPORT

7558-discovery front 7-11 9/11/06 2:02 Page 8

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 9

THIS YEAR’S PERFORMANCEThe 2006 financial year was a successful one for the

Discovery Group, featuring important strategic developments

in each of its businesses, as well as strong earnings growth.

As in previous years, all of Discovery’s businesses focused

intensely on innovations designed to meet specific client

needs in rapidly-changing markets. The group has reached

an important stage in its evolution, where it is positioned for

continued strong growth, yet has been able to generate

excess cash within the business. Given this strong cash-flow

position, we declared our maiden dividend at the

announcement of our annual results.

OUR STRATEGYA solution-centric approach to meeting clients’ needsDiscovery’s core purpose is making people healthier and

enhancing and protecting their lives. To deliver on our

purpose necessitates a solution-centric approach that focuses

on meeting clients’ needs. Developing effective solutions for

our clients helps to create a sustained demand for our

products, which in turn leads to strong organic growth.

Importantly, because we essentially go into areas where our

clients most need us, Discovery’s products are not defined or

bound by the specific industries we operate in.

We manage somewhat contradictorycompetencies to create a unique advantageOver the past five years, Discovery has increased its gross

inflows under management from R5,5 billion to almost

R20,5 billion, while its embedded value has grown from

around R3,2 billion to R10,6 billion. It has achieved this

superior growth and profitability purely organically based on

its ability to manage the apparent tensions between financial

prudence, innovation, and a customer-centric approach.

Somewhat paradoxically, Discovery is at once conservative in

its approach to financial risk-taking, innovative in its product

design and responsive to consumer needs.

FINANCIAL HIGHLIGHTS

• Operating profit before BEE R1 263 million (+37%)

• Profit before tax and BEE expense R1 237 million (+45%)

• Taxation R410 million (+34%)

• Net profit before BEE expense R827 million (+51%)

• BEE expense R161 million

• Net profit attributable to shareholders

R669 million (+20%)

7558-discovery front 7-11 9/11/06 2:02 Page 9

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 61 0

THE ENVIRONMENT IN WHICH WE OPERATEWe only enter markets where we make a differenceDiscovery enters markets where we clearly discern the need

for structural change – and only if we believe that we will

make a profound difference. We operate in health and life

assurance markets, fundamental areas of social need. Along

with our ethos of putting people at the centre of our

business, this positions us to introduce changes that make

a real difference.

Rising consumerism remains a keyenvironmental feature in all our marketsIn health care, the worldwide move to consumer-

engagement is accelerating. Discovery has long been

established as a leader in consumer-driven health care. The

market now demands a combination of consumer

engagement and supply-side cost controls. Discovery

Health, distinctive in its size in the South African health care

context, has the scale to control costs and maximise quality

for our members. In both the UK and US markets, while

legislation and the competitive landscape are different, the

issues of cost, quality and access are just as critical. There,

Discovery is using its extensive expertise and vast

operational platform to deliver innovative consumer-

directed solutions.

In life insurance, in the 80s and 90s, the industry migrated

to investments. Recently, however, consumer demand for

transparency and better value has led to the disintermediation

of the industry. Discovery Life, when it entered the market

six years ago, recognised the need to increase the efficiency

and flexibility of life assurance products. It did so by

specialising instead in risk protection, separating out the

investment aspects completely. Our risk-based product has

since led an industry shift to a greater focus on risk and has

further evolved its value proposition to clients. The recent

consumer backlash against insurers’ investment products,

which are seen as opaque and offering poor returns, has

now created an opportunity for Discovery Life to apply its

consumer-centric approach to investment products. We see

it as an important future focus area.

In the areas of wellbeing and lifestyle benefits, Discovery

Vitality has allowed us to respond to both the growing

scientific evidence for the powerful impact of lifestyle in

disease management, and growing demand for products

that acknowledge consumers’ need for personalisation,

convenience and added value.

With the addition of the DiscoveryCard to the Vitality

offering, we can now offer an even more integrated suite

of products to meet the entire spectrum of clients’ financial

protection needs. Before its launch, the credit card market

was largely the exclusive domain of banks. Since

DiscoveryCard launched two years ago, we have seen other

non-traditional providers follow our lead – with airlines,

retailers and others entering the credit card market. As a

result of the trend, credit cards have emerged as a true

consumer commodity, with enhanced competition helping

to lower costs and improve benefits.

THIS YEAR’S KEY FOCUS AREASDiscovery continued to deliver strong earningsand good growth across the GroupDiscovery has achieved exceptional growth in earnings and

embedded value over the past few years, performing well

for our shareholders. Encouragingly, the consistently strong

earnings performance has translated into an improved cash

flow position, as the business has evolved to the point

where new ventures have become either cash flow positive

or require less capital funding from the Group. During the

year under review, this process of evolution saw Discovery

Life become cash flow positive for the first time, being a

significant contributor to the increase in the cash generated

from operations to R656 million, from a like-for-like

comparative of R585 million in the preceding year.

See figure 1

During the year under review, the strong earnings performance

continued across the Group.

• Discovery Life delivered strong growth, profitability

and a better-than-expected underwriting performance,

demonstrating the quality of the business.

• Discovery Health, despite its dominant size, grew strongly

and further established itself as a major player in the

emerging lower income market, in addition to achieving

significant operational efficiencies.

• Vitality, while in essence an underpin to our other

businesses, also grew its profitability.

CHIEF EXECUTIVE’S REPORT (CONTINUED)

7558-discovery front 7-11 9/11/06 2:02 Page 10

Figure 1: Cash generated from operations

* Note: 2005 has been adjusted to exclude the effect of the quota shareagreement.

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 1 1

• Destiny Health’s performance was in many respects a

disappointing one, but during the period we took steps

to limit the Group’s exposure to future losses and have

committed to pinning losses down at a more sustainable

level of below 5% of Group earnings.

• PruHealth, while continuing to operate at a loss in the short

term, achieved outstanding new business growth and

persistency rates, placing it firmly on track to profitability.

We based our maiden dividend on the guidingprinciples of sustainability and future growthDiscovery’s maiden dividend announcement of 27 cents per

share reflects the Group’s strong cash generative position and

future growth opportunities. Discovery Life achieved cash-flow

positive status during the year, a significant development in this

regard. The following principles underpinned our decision to

announce the dividend:

• Sustainability: We have always said Discovery would only

commence paying dividends when it could do so without

hampering the Group’s growth, on a sustainable basis,

and without placing undue stress on our business.

• Constant payout ratio: Discovery should pay dividends

based on a fixed proportion of earnings ratio.

We calculated the dividend at a conservative level with a

dividend cover of four-and-a-half times.

See figure 2

Discovery Health’s scale and size gives it thepurchasing power to create a balanceDiscovery Health has grown phenomenally in the past

fourteen years and is now a dominant player in South

African health care. It has close to two million lives on its

books, and 26% of the overall market share in an otherwise

fragmented medical schemes market. Despite its market

dominance, current market dynamics such as buy-downs

from more comprehensive cover, as well as growth in the

lower income market, have further entrenched Discovery

Health’s competitive position.

See figure 3

Discovery Health is in a unique position of leadership,

which enables it to offer members choice, increase their

700

600

500

400

300

200

100

0

Cash generated from operations(R million)

02 03 04 05 06

2 500

2 000

1 500

1 000

500

0

Free cash flow under different payout ratios(R million)

2006 2007 2008 2009

2x cover 3x cover 4x cover5x cover 6x cover No dividend

Figure 2: We still have access to sufficient cash resources to

pursue future growth opportunities

Schemes that grew or shrank during the year(Principal members – thousands)

–40 0 40 100–20 20 60

DiscoveryOxygen

FedHealthSpectramed

MedicoverHosmed

ResolutionLiberty

BestMedMunimedMediHelp

SizweMedshield

ProSanoBonitas

Momentum

80

Figure 3: Change in membership levels of top 16 medical

schemes from December 2004 to December 2005

7558-discovery front 7-11 9/11/06 2:02 Page 11

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 61 2

access to care and, through its buying power, bring down

the cost of private health care for our members.

Interestingly, when it entered the market in the Nineties,

Discovery Health helped to check rampant medical inflation

by interventions on the demand side, despite its relatively

small size. Through innovations like the Medical Savings

Account and Vitality, it was able to empower consumers

to better understand and manage their health care costs.

The massive scale it has since achieved now allows it to

combine this consumer-driven approach with initiatives

focused on cost management on the supply side. The result

is that we are able to maximise choice, access and

affordability for our members.

By way of example, during the year we:

• Rolled out the Discovery Health Primary Care Network,

which came into effect on 1 January 2006. Prior to its

launch, there were only two players in this market, which

is characterised by significant barriers to entry. Discovery

was able to leverage its significant scale and size to

overcome these barriers, bringing innovation and

renewal to the lower income market. In less than a year,

the network has grown to incorporate over 2 000 GPs

and more than 60 hospitals. With the launch of the

Discovery Health GP Network, which will roll out next

year, we aim to build on this successful innovation to the

benefit of consumers.

See figure 4

• Developed the Specialty Medication Benefit, which will

help to address the challenging issue of access to high

cost new medical technologies. Around the world, in the

past number of years, we have seen increasing debate

around the funding of expensive new medical

technologies. The new class of biological drugs, such as

the controversial breast cancer drug, Herceptin, has

served to highlight the difficulties faced by health care

funders the world over, who are all grappling with how

to provide affordable, sustainable access to these

groundbreaking new technologies. Our philosophy has

always been that we want to offer our members access

to the best quality care. While it has been a challenging

process, we are proud that we have now been able to

create a funding solution that ensures Discovery Health

Discovery 2006 Faranani 2006 Prime Cure 2006

0

Size of Provider Network relative to the market(%)

200 400 600100 300 500 700

Gauteng

KZN

Western Cape

Free State

Mpumalanga

North West

Eastern Cape

Limpopo

Northern Cape

CareCross 2006

Figure 4: Relative size of primary care provider networks

250

200

150

100

50

0

Integrator versus non-integrator experience(Integrator experience as a % of non-integrator)

Ave

rage

NB

prem

ium

Ave

rage

Ben

efit

cou

nt

Loss

Rat

io(R

isk

prem

ium

A t

o E

)

Laps

e ra

te

VNB

per

pol

icy

Figure 5: Integrated plans as a percentage of

non-integrated plans

CHIEF EXECUTIVE’S REPORT (CONTINUED)

7558-discovery front 7-11 9/11/06 2:02 Page 12

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 1 3

members may have access to biological drugs and other

new medical technologies on a sustainable basis. The

Specialty Medication Benefit will be available next year.

These, and other consumer-directed innovations, such as

the Discovery Hospital Rating Index, are discussed in greater

detail in the report by Neville Koopowitz on page 21.

Discovery Life has enhanced its valueproposition for consumers through integration Discovery Life is growing rapidly in the highly-

commoditised life insurance market. Through its consumer-

driven approach, which hinges on two clear strategies of

innovation and integration, Discovery Life is able to offer

clients a unique and compelling value proposition.

The benefits of this approach transcend the client

spectrum. Discovery Life’s analysis demonstrates that

integrated plans are on average of higher value, greater

profitability and have better risk experience when

measured against their non-integrated counterparts.

See figure 5

• An example of integration is the DiscoveryCard Integrator,

which was launched in June 2006, and uniquely links

credit card spending patterns to life insurance cover.

Discovery Life policyholders are able to use their

projected future spend to secure more financial

protection for their beneficiaries.

• Recent innovations include enhancements to the Severe

Illness Benefit. Policyholders now have the option of

O U R M O D E L O F E N G A G I N G C O N S U M E R S I N M A N A G I N G T H E I R

H E A LT H , P L A C E S D I S C O V E R Y I N A S T R O N G P O S I T I O N .

receiving a full lump-sum payout on claiming for severe

illness benefits, or choosing to receive a partial lump-sum

payout plus world-class treatment at a network of

leading US health care facilities.

As outlined in the report by Herschel Mayers on page 29,

Discovery Life’s integrated offerings now enable policyholders

to effectively control their premiums, increase their family's

future financial protection and even influence their own income

in retirement, simply by actively managing their health.

Destiny Health has recognised the need tooffer US consumers a soft landingDestiny Health’s relatively weak performance stems, we

believe, from a failure to capitalise fully on its early

leadership position in the US shift to consumer-directed

health care. This was compounded during the year under

review by a significant shift in the competitive dynamics of

the markets in which it operates.

While the concept of Consumer-Directed Healthcare

continues to grow significantly in the US health insurance

markets – presenting a substantial and unique opportunity

for Discovery given its experience and capabilities – Destiny

was poorly positioned to make positive progress.

A positive underwriting cycle and significantly deeper

discounts available to our major competitors, created an

environment in which Destiny is simply not price

competitive – particularly in Illinois, Destiny’s major market

– resulting in slow growth and worse-than-expected loss

ratios. In addition, Destiny’s pace of expansion into other

7558-discovery front 7-11 9/11/06 2:02 Page 13

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 61 4

markets was inadequate and contingent upon partner

influences. As outlined in detail in the report by Art Carlos

and Barry Swartzberg, we have taken bold steps to address

these specific operational issues and have already seen

operating losses reduce as a result.

However, at a more strategic level, Discovery has made the

decision that the business model must change. Discovery,

Destiny Health and the Guardian Life Assurance Company

of New York (Destiny Health’s exclusive distribution partner

in the US) are in the process of revisiting their partnership

arrangement.

Potential changes may include a construct wherein Destiny

will provide the intellectual capital and an operational

platform for the Guardian in return for a fixed fee per

member in some states in the US, while Destiny Health will

market its own products in other US states. However, it

must be stressed that any growth outside of this will be

opportunistic, confined to those markets where competitive

pricing can be obtained and will be pursued with great care

to limit any downside.

PruHealth is making private medical insurancecover more accessible In the context of a highly sophisticated private medical

insurance market that has seen little change in recent years,

PruHealth in itself represents an industry-leading

innovation. Pent-up consumer demand for quality,

affordable cover has resulted in it gaining rapid traction,

which has far exceeded our expectations. PruHealth

reached the 75 000 member milestone in October 2006,

just two years after its launch.

Importantly, we have been able to apply to PruHealth the

lessons we have learnt in both the South African market

through Discovery Health, and in the US market through

Destiny Health. While it is growing at a phenomenal rate,

PruHealth does not yet possess significant scale in the UK

market. However, by using innovative, consumer-directed

constructs like Vitality that allow consumers to play a more

active role in managing their risks – and the cost of their

cover – PruHealth offers superior benefits at a discount

relative to other more traditional players. Based on their

Vitality status and claims, PruHealth clients are able to

lower their renewal premium or receive cash back at the

end of the year.

Examples of Vitality engagement

Over 300 preventive health screenings each month

20 000 gym visits per month

Over 4 000 FitBug events in just two months

More than 600 000 Vitality points awarded each month

142 000 online assessments to date

PruHealth has also applied Discovery’s cycle of regular

innovation, launching new benefits annually. Most recently,

it launched Vitality Underwriting and the Personal Health

Fund in June 2006:

• PruHealth has tapped into Discovery’s expertise to create

Vitality Underwriting. This innovative approach to

underwriting recognises that people are able to reduce

their long-term risks and health care expenditure simply

by eating healthily, exercising regularly, by not smoking

and through regular health screenings. PruHealth now

has the capability to appeal to a previously untapped

market and at the same time, practise sound risk

management.

• Private medical insurance in the UK typically provides

cover for once-off, high-cost medical conditions and

events. With the introduction of the Personal Health

Fund, PruHealth has for the first time introduced cover

for primary care expenses such as GP visits and routine

health screens.

PruHealth is also able to deliver superior service through its

capacity to tap into Discovery’s technological capability and

infrastructure. We have seen the combination of affordable,

quality benefits and exceptional service delivery result in

consumer endorsement of its products – independent

research results indicate that the majority of PruHealth

clients have recommended the company to others.

Reinvigorating the Vitality value propositionVitality remains first and foremost a wellness programme.

But it is also a strategic platform for integration across all of

CHIEF EXECUTIVE’S REPORT (CONTINUED)

7558-discovery front 7-11 9/11/06 2:02 Page 14

Figure 8: Discovery’s score in relation to FSC targets

*Please note these three pillars are beyond the scope of Discovery’s operations

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 1 5

our brands, as well as a unique value creator for our clients.

We therefore constantly focus on renewing its appeal

through the addition of attractive new partners and

benefits. As outlined in the report by Alan Pollard, our

partnership with kulula.com, which came into effect in

February 2006, has proven to be particularly popular with

Vitality members.

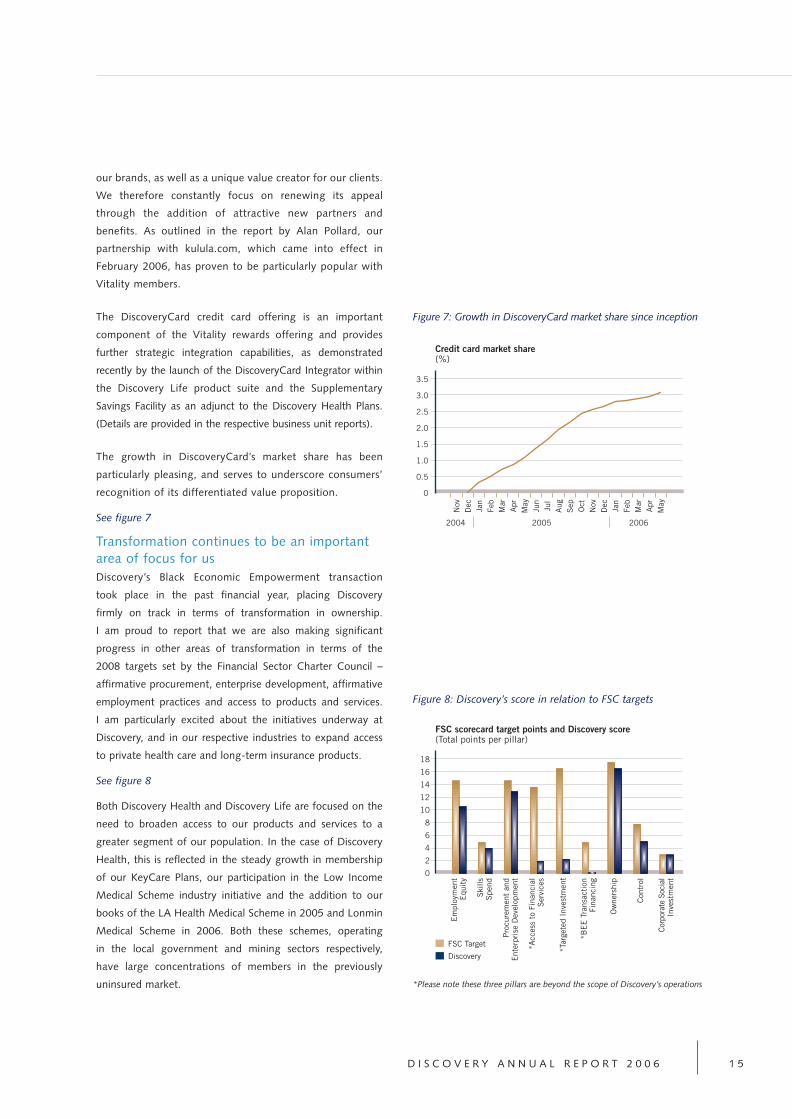

The DiscoveryCard credit card offering is an important

component of the Vitality rewards offering and provides

further strategic integration capabilities, as demonstrated

recently by the launch of the DiscoveryCard Integrator within

the Discovery Life product suite and the Supplementary

Savings Facility as an adjunct to the Discovery Health Plans.

(Details are provided in the respective business unit reports).

The growth in DiscoveryCard’s market share has been

particularly pleasing, and serves to underscore consumers’

recognition of its differentiated value proposition.

See figure 7

Transformation continues to be an importantarea of focus for usDiscovery’s Black Economic Empowerment transaction

took place in the past financial year, placing Discovery

firmly on track in terms of transformation in ownership.

I am proud to report that we are also making significant

progress in other areas of transformation in terms of the

2008 targets set by the Financial Sector Charter Council –

affirmative procurement, enterprise development, affirmative

employment practices and access to products and services.

I am particularly excited about the initiatives underway at

Discovery, and in our respective industries to expand access

to private health care and long-term insurance products.

See figure 8

Both Discovery Health and Discovery Life are focused on the

need to broaden access to our products and services to a

greater segment of our population. In the case of Discovery

Health, this is reflected in the steady growth in membership

of our KeyCare Plans, our participation in the Low Income

Medical Scheme industry initiative and the addition to our

books of the LA Health Medical Scheme in 2005 and Lonmin

Medical Scheme in 2006. Both these schemes, operating

in the local government and mining sectors respectively,

have large concentrations of members in the previously

uninsured market.

18

16

14

12

10

8

6

4

2

0

FSC scorecard target points and Discovery score(Total points per pillar)

FSC Target

Discovery

Em

ploy

men

tE

quit

y

Ski

llsS

pend

Pro

cure

men

t an

dE

nter

pris

e D

evel

opm

ent

*Acc

ess

to F

inan

cial

Ser

vice

s

*Tar

gete

d In

vest

men

t

*BE

E T

rans

acti

onFi

nanc

ing

Ow

ners

hip

Con

trol

Corp

orat

e So

cial

Inve

stm

ent

Credit card market share(%)

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0

2004 20062005

Nov

Dec Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep Oct

Nov

Dec Jan

Feb

Mar

Apr

May

Figure 7: Growth in DiscoveryCard market share since inception

7558-discovery front 7-11 9/11/06 2:02 Page 15

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 61 6

In the case of Discovery Life, we have to date provided

access to funeral cover underwritten by Discovery Life to

members of KeyClub, the loyalty programme for KeyCare

members. Discovery Life is currently working on an exciting

initiative that will provide cover for the lower income

market, which we plan to take to market towards the end

of 2006.

In our Sustainability Report, available at www.discovery.co.za,

we outline initiatives in the arena of transformation and

sustainability issues in general.

OUR PROSPECTS FOR THE COMING YEARThere is significant scope for growth in each of Discovery’s

core businesses in the year ahead, and the key growth

strategies for each are outlined in the various subsidiary

reports. However, I would like to take the opportunity to

highlight a few of Discovery’s initiatives for next year that

I find especially noteworthy.

Vitality WellPoint applies the Vitalityphilosophy to the wellbeing of corporatesWith the introduction of Vitality WellPoint, which will be

available to South African corporates from February 2007,

Discovery is entering an exciting new space. WellPoint does

for corporates what Vitality does for individuals –

leveraging Discovery’s scale, size and expertise to unlock

value they would otherwise be unable to access.

WellPoint is a suite of products and services that integrates

the clinical and health insights, technological infrastructure

and actuarial expertise of Discovery Health and Vitality to

create a unique and comprehensive corporate wellness

programme. WellPoint encourages and rewards employers

and their employees for behaviours that improve their

health status, reduce absenteeism, and so, improve

productivity within the workplace. WellPoint integrates

seamlessly with Vitality, the Discovery Health Plans and the

Discovery HIVCare programme to help employers

understand and manage health-related risk within their

business. However, employees need not belong to

Discovery Health to participate in the programme. Through

employer discounts on the Discovery Life Group Risk Plans,

and enhanced DiscoveryCard benefits for employees, both

the employer and the employee are strongly incentivised to

participate actively in the programme.

Vitality WellPoint provides an opportunity for Discovery to

tap into its existing corporate client base of over 200 000

companies, to provide added value and enhanced cross-

selling opportunities across the business.

The Discovery Foundation aims to improveaccess to health care for all South AfricansThe Discovery Foundation was established as part of

Discovery’s BEE transaction announced in September 2005.

Its aim is to invest in the education and training of medical

specialists in South Africa, with the focus on:

1. Increasing the number of specialists in rural areas;

2. Contributing to academic and medical research centres

of excellence in South Africa; and

3. Increasing the number of black and female specialists in

South Africa.

The Discovery Foundation is an autonomous shareholder of

Discovery, capitalised through its shareholding of

Discovery. Its trustees have been independently elected and

appointed to ensure sound governance and autonomy.

Its establishment flowed from our wish to ensure that our

empowerment deal would make a real difference to the

broader community, within the context of our core purpose

of making people healthier and enhancing and protecting

their lifestyles.

Over the next decade, the Discovery Foundation Awards,

launched in August 2006, will contribute in excess of

R100 million to bursaries and fellowships that reward and

encourage excellence in the South African health care

sector. The Awards are expected to contribute to the

training of 300 new medical specialists. We believe this will

not only help to build on one of our nation’s greatest

assets, our world-class health care capability, but hopefully

make a tangible difference in the accessibility of quality

care for thousands of South Africans.

Discovery’s Prosperity programme takes ourcore purpose to our greatest asset, our peopleUltimately, the quality of Discovery’s people is what sets

our organisation apart. I believe they are the reason for

every success achieved. Our people are unique in their

CHIEF EXECUTIVE’S REPORT (CONTINUED)

7558-discovery front 7-11 9/11/06 2:02 Page 16

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 1 7

diversity, their talent, their dedication and their quality.

Liberating the greatness within our people is one of our

core values at Discovery, and so we have decided to make

their wellbeing a particular area of focus in the year ahead

through our new Prosperity programme.

This unique incentive programme gears the rewards of

Vitality to encourage our people to participate in activities

that support their wellbeing, aid their development,

increase their level of engagement and improve their

productivity. These include maintaining a work-life balance,

participating in our CSI employee volunteer programmes

and in learning and development initiatives.

In developing the Prosperity programme, we have applied

what we have learnt from Vitality in terms of structuring

a compelling rewards programme that incentivises a

higher level of engagement. As with Vitality, we hope

our employees will not only benefit from the incomparable

rewards offered by the programme, but also from the

great sense of personal accomplishment associated with

participation.

MESSAGE OF THANKSAs always, I feel it is fitting to end my report by thanking

Discovery’s people. Our team is made up of over 4 000

talented and dedicated individuals who work hard every

day to pursue our core purpose and make a difference in

the lives of the people we serve. I thank them for their

commitment and for the privilege of working with them.

They truly are exceptional.

O U R P E O P L E A R E U N I Q U E I N T H E I R D I V E R S I T Y, T H E I R TA L E N T,

T H E I R D E D I C AT I O N A N D T H E I R Q U A L I T Y.

7558-discovery front 7-11 9/11/06 2:02 Page 17

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 61 8

Neville Koopowitz

Chief Executive Officer, Discovery Health

DISCOVERY HEALTH

Helping more people access quality health care on a sustainable basis

Discovery Health continued to grow strongly in

2006, and remains the dominant player in the

South African medical schemes market.

7558-discovery front 7-11 9/11/06 2:03 Page 18

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 1 9

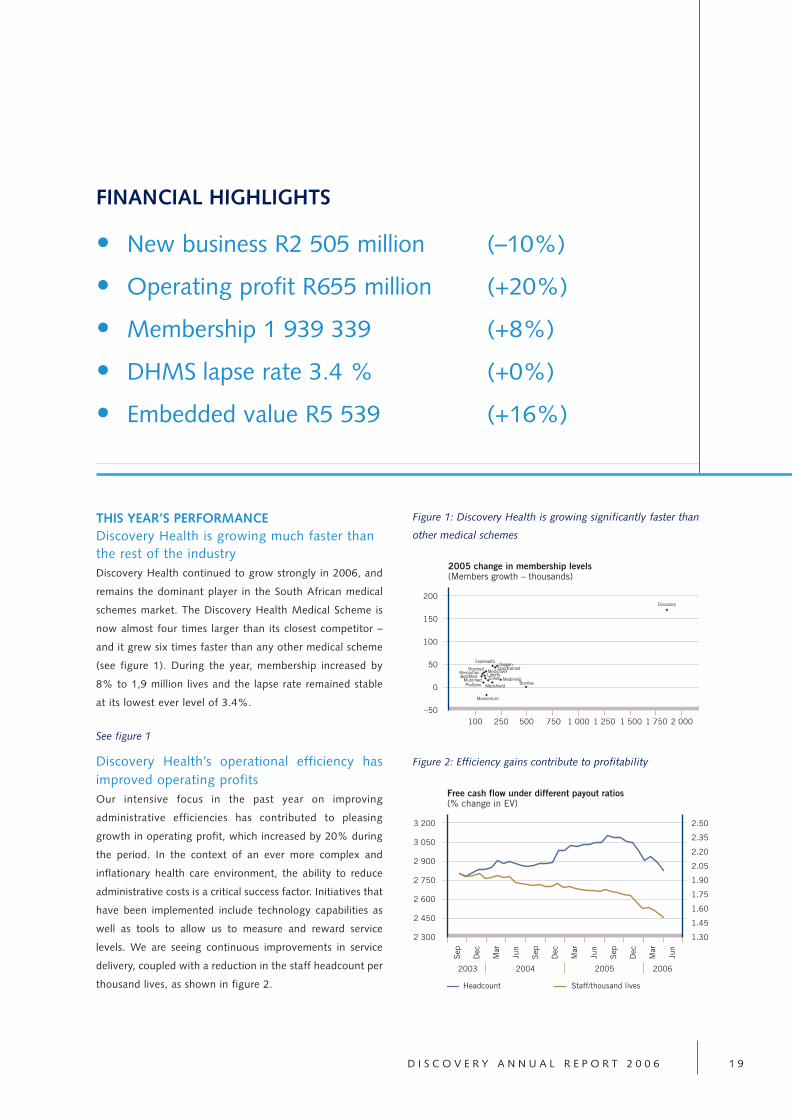

THIS YEAR’S PERFORMANCEDiscovery Health is growing much faster thanthe rest of the industryDiscovery Health continued to grow strongly in 2006, and

remains the dominant player in the South African medical

schemes market. The Discovery Health Medical Scheme is

now almost four times larger than its closest competitor –

and it grew six times faster than any other medical scheme

(see figure 1). During the year, membership increased by

8% to 1,9 million lives and the lapse rate remained stable

at its lowest ever level of 3.4%.

See figure 1

Discovery Health’s operational efficiency hasimproved operating profits Our intensive focus in the past year on improving

administrative efficiencies has contributed to pleasing

growth in operating profit, which increased by 20% during

the period. In the context of an ever more complex and

inflationary health care environment, the ability to reduce

administrative costs is a critical success factor. Initiatives that

have been implemented include technology capabilities as

well as tools to allow us to measure and reward service

levels. We are seeing continuous improvements in service

delivery, coupled with a reduction in the staff headcount per

thousand lives, as shown in figure 2.

FINANCIAL HIGHLIGHTS

• New business R2 505 million (–10%)

• Operating profit R655 million (+20%)

• Membership 1 939 339 (+8%)

• DHMS lapse rate 3.4 % (+0%)

• Embedded value R5 539 (+16%)

Figure 1: Discovery Health is growing significantly faster than

other medical schemes

200

150

100

50

0

–50

2005 change in membership levels(Members growth – thousands)

100 250 500 750 1 750 2 000

Discovery

1 5001 2501 000

OxygenSpectramed

FedHealth

MedicoverHosmedResolutionBestMed Liberty

MunimedProSano

Sizwe

MedshieldMediHelp

Momentum

Bonitas

Figure 2: Efficiency gains contribute to profitability

3 200

3 050

2 900

2 750

2 600

2 450

2 300

Free cash flow under different payout ratios(% change in EV)

Headcount Staff/thousand lives

2.50

2.35

2.20

2.05

1.90

1.75

1.60

1.45

1.30

2004 20062005

Sep

Dec

Mar

Jun

Sep

Dec

Mar

Jun

Sep

Dec

Mar

Jun

2003

7558-discovery front 7-11 9/11/06 2:03 Page 19

Our industry leadership creates value forshareholders and consumers alikeDiscovery Health’s strong growth and solid financial

performance has again positioned it as a major contributor

to the Discovery Group’s success – the company’s

embedded value has increased to over R5,5 billion. More

importantly, its scale, size and financial solidity have further

strengthened our ability to ensure that our members

receive health care on a sustainable basis backed by

exceptional service, price and quality.

OUR STRATEGYOur consumer-driven health care model aimsto improve quality and encourage lower costsThe South African health care environment has changed

significantly in the fourteen years since Discovery Health

was established. At the time of our entry, inefficient benefit

structures had created the wrong incentives, leading to

rampant medical inflation and consumer concern. We early

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 62 0

on identified the need to engage consumers more actively

in managing their health care costs, and structured our

unique products in a way that supported direct consumer

involvement. Our aim: to contain costs by empowering

consumers, giving our members affordable access to quality

care over the long term.

Since then, the number of medical scheme members in

South Africa has remained largely unchanged at around

seven million. However, the regulatory requirements, the

benefit structures, the number of industry players, the way

prices are determined and the expectations of medical

scheme members, have all shifted dramatically. The

dynamics are different, but the Discovery Health approach

to dealing with them is the same – to put consumers first

and provide them with affordable access to quality care.

We believe it is this consumer-focused, innovative

approach that has allowed Discovery Health to achieve and

maintain its leadership position in the industry, as

demonstrated by:

Figure 3: Discovery Health’s service levels compare favourably against international benchmarks

Query metrics US benchmark Discovery Health

Answer speed 80% in 21.93 seconds 35 000 calls per day

Average: 38 seconds Actual: 85% in 10 seconds

Average: 8 seconds

Abandon rate Average: 4.58% Actual 2005: +1.75%

Best 3.52%

First call resolution Average: 75.33% >90%

Best: 79.32%

Source: 2005 Purdue report on health insurance industry call centres

Claims metric US benchmark Discovery Health

Turnaround HMOs*: Mean 71 days 2 million claims per month

Medicare**: 95% of Avg < 1 day

claims in 30 days > 96% in 3 days

Accuracy US Managed Care***:

98% – 99.1% > 99% accurate

* From interstudy 2000 analysis of 600 Health Management Organisations in the US

** From US Managed Care Handbook

*** Cap Gemini, Ernst & Young US Managed Care Benchmark Study 2002.

DISCOVERY HEALTH (CONTINUED)

7558-discovery front 7-11 9/11/06 2:03 Page 20

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 2 1

O U R S C A L E A N D S I Z E E N T R U S T S U S W I T H A N E N O R M O U S

R E S P O N S I B I L I T Y, B U T A L S O C R E AT E S C O N S I D E R A B L E O P P O RT U N I T I E S

F O R U S T O W O R K T O T H E B E N E F I T O F O U R M E M B E R S .

• Our growth

While other medical schemes are losing members,

Discovery Health is gaining them.

• Our financial strength

The Discovery Health Medical Scheme has yet again

been awarded the highest credit rating in the industry

for its claims paying ability – an AA rating from Global

Credit Ratings.

• Our service levels

We constantly measure and benchmark our service

interactions to ensure continual improvement

(figure 3 shows how we perform against international

benchmarks).

THIS YEAR’S KEY FOCUS AREASInitiatives that help to ensure our members getthe best quality careAs the largest medical scheme administrator in South

Africa, and administrator of the Discovery Health Medical

Scheme (the largest open medical scheme), as well as eight

other closed schemes, Discovery Health has almost two

million people in our care. Our scale and size entrusts

us with an enormous responsibility, but also creates

considerable opportunities for us to work to the benefit

of our members. In September 2005, we introduced two

important initiatives aimed at using our scale and size to

provide additional peace of mind for our members about

their medical care:

1. Discovery 911 provides rapid medical care in an

emergency

Discovery Health has partnered with Netcare 911 to offer

our members – at no additional charge – Discovery 911, our

emergency rapid response service. We believe this unique,

value-added service is making an important difference to

the quality of care received at the most crucial stage of a

medical emergency. This is the so-called Platinum Ten

Minutes; the first ten minutes after a medical trauma event.

Discovery 911 includes a cellphone alert service, allowing

members to alert us to an emergency situation at the press

of a button, even if they are unable to speak. We dispatch

an emergency response vehicle to the scene immediately

upon receiving the alert. The trained paramedics are able to

take the appropriate action to treat or stabilise the patient’s

condition while emergency transport is underway. They are

also able to assess which transport and facilities are most

appropriate based on the patient’s injury and condition.

2. The Discovery Hospital Rating Index allows

consumers to assess quality of careThe Discovery Hospital Rating Index has been very popular

with consumers. Around 5 000 people – not just Discovery

Health members – click into our website every month to

look up the cost and quality ratings of South Africa’s private

hospitals. It is the only index of its kind in South Africa and

7558-discovery front 7-11 9/11/06 2:03 Page 21

uses data collected by Discovery Health over a period of

five years to assess the quality and cost of care. The data is

based on the actual claims experience of our almost two

million members.

Some hospital groups and health care professionals have

questioned the need for such a tool, the validity of the

ratings we have assigned and the methodology we used

to rate hospitals’ performance. The Council for Medical

Schemes has endorsed the Hospital Rating Index and ruled

that it is not only a valid and sound consumer tool, but a

very necessary one. We are working with the hospital

groups that have raised concerns, to allay them. We have

already made many improvements and adjustments to the

index based on the feedback received from stakeholders,

and have seen several hospitals receive improved ratings in

terms of the cost and quality of health care outcomes.

This means that not only are consumers able to make more

informed decisions, but that we are also seeing progress in

our goal of using the tool to improve the quality and reduce

the cost of health care for consumers in the longer term.

Initiatives that help to contain the cost ofhealth careDiscovery Health has for the past two years contained its

average annual contribution increases to a single digit.

Health care is by nature costly, and funding it affordably

and sustainably is a challenge the world over. Several

factors on both the supply and demand side contribute to

the challenges – for example, the high costs involved with

developing new medical technologies and the unequal

distribution of health care resources. Certain developments

during the past year have served to highlight these

challenges, and Discovery Health has an important role to

play in finding ways to meet our members’ expectations

without compromising the long-term sustainability of their

health care benefits.

1. We are finding ways to fund high-cost new

technologies in a sustainable manner

Medical and technological advances are opening up

exciting new possibilities in health care. Research in the

field of genetics, for instance, now allows doctors to

understand how the make-up of our bodies contributes to

the likelihood of our developing a disease. It gives them the

tools to develop medicines and treatments that fight

diseases biologically, rather than chemically. However,

these advances come at a high price and health care

funders need to approach the way they fund them,

responsibly and consistently.

Guided by the principle that we want to fund the

best quality health care for our members, including

appropriate and effective new technologies, Discovery

Health carefully and constantly evaluates new treatments.

We follow a rigorous process, which includes Health

Economics Evaluations, to ensure we develop responsible

funding policies. This entails detailed clinical and economic

modelling, based on the gold-standards of evidence-based

medicine, to develop the most appropriate health care

funding decision for a particular therapy.

Many of these technologies have proven clinical benefits,

while the scientific evidence for others is less clear. Discovery

Health is continuously hard at work in evaluating these various

products. We work with the medical profession to ensure that

we keep up to date with the latest clinical evidence. On behalf

of our members, we also engage the pharmaceutical

manufacturers in evidence-based and commercial discussions

to reduce their costs. In short, we make every effort to find

sustainable solutions for our members.

Discovery Health has recently developed the Specialty

Medication Benefit, which will be available from 1 January

2007. We are the first funder in South Africa to develop a

clearly defined, consistent benefit to pay for high-cost

treatments like Herceptin®, Revellex® and Enbrel®. The

benefit is only available on the Comprehensive Plans and

covers a list of twenty clearly defined high-cost treatments.

2. We are working to meet member and providerexpectations around rates of reimbursementAnother important area where it is sometimes difficult to

strike a sound balance between health care access and cost,

is the reimbursement rates for the services of health

professionals. Health care professionals have the right to

choose how much they believe is fair to charge for their

services. Health care funders have the responsibility to

ensure that they carefully manage how much they pay for

services on behalf of the members who have entrusted

them with the management of their funds.

Ideally, all three parties – patient, doctor and funder –

should agree on the best price through a process of

negotiation. This is certainly the intent of the Competition

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 62 2

DISCOVERY HEALTH (CONTINUED)

7558-discovery front 7-11 9/11/06 2:03 Page 22

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 2 3

Commission’s banning of the price-setting practices of the

past, where health professionals collectively agreed how

much they would charge and health care funders

collectively agreed how much they would reimburse.

Since that ruling, however, there has been some

uncertainty and confusion in the industry. The National

Health Reference Price List has been treated by most health

care funders and health professional as a collective medical

aid tariff, harking back to the old system, instead of seeing

it as it was intended – merely as a reference tool in price

negotiations. The industry still has some way to go in terms

of fully understanding and embracing the new more

competitive, free market-based structures.

We are working hard to address these issues. Discovery

Health’s size provides it with the resources to work with

provider groups to create reimbursement structures that

both ensure fair remuneration for health providers and

contain costs for members. In 2006, we applied this

approach successfully in creating the proprietary KeyCare

Primary Care Network. More than 2 000 GPs joined the

network in the first year, negotiating preferential prices for

KeyCare members to ensure affordable access to primary

care for those individuals who previously didn’t enjoy

private health care. In 2007, Discovery Health will extend

these principles even further with the Discovery GP

Network. It will halve the cost of primary care for Discovery

members, who will now pay only R95 per consultation. The

Discovery Health Medical Scheme will pay the rest of the

consultation fee directly to the GP. This will enhance

members’ benefits significantly.

Similarly, Discovery Health has introduced the Discovery

Health Premier Rate for 2007 which provides certainty

around the rate of reimbursement for specialists who agree

to charge this rate, while reducing the risk of short-falls

for members.

In 2007, we will also be looking at strengthening our

relationships with various hospital groups to reduce the

high cost of hospital care and to engage in risk-sharing

initiatives for the benefit of all stakeholders.

These structures leverage Discovery Health’s strength to

protect members against co-payments, secure convenient

direct payments for health care practitioners and most

importantly, contain the cost of health care to ensure the

long-term sustainability of cover.

Initiatives that extend health care access tonew marketsWhile Discovery Health is the clear leader in the industry, it

still only holds a 26% share of the medical scheme market

in South Africa. This means it has significant scope to grow

in its existing market – the seven million people who

already belong to a medical scheme. We also see significant

opportunities to increase the size of the medical scheme

market by creating products that attract the previously

uninsured: those employed South Africans who were

historically excluded from financial services markets.

This is reflected in the steady growth in membership of our

KeyCare Plans, our participation in the Low Income Medical

Scheme industry initiative and the addition to our books of the

LA Health Medical Scheme in 2005 and Lonmin Medical

Scheme in 2006. Both these schemes, operating in the local

government and mining sectors respectively, have large

concentrations of members in the previously uninsured market.

1. KeyCare is the most successful plan in its marketDiscovery Health launched the KeyCare Plans in 2003 with

the specific aim of increasing medical scheme membership

among the previously uninsured market, particularly

employed individuals earning a household income of

between R3 500 and R6 500 per month.

Three years later, the KeyCare Plans have already attracted

140 000 lives, and we estimate that two-thirds of those

members did not belong to a medical scheme before. Its

rapid growth makes it the most successful product in the

lower income market. As demonstrated in figure 4, the

KeyCare Plans alone have more members than the majority

of medical schemes have in total.

Figure 4: the KeyCare Plans alone have more members than

most established medical schemes

Changes in total members Dec 2004 – Dec 2005(Principal members – thousands)

–40 0 40 100–20 20 60

DiscoveryOxygen

FedHealthSpectramed

MedicoverHosmed

ResolutionLiberty

BestMedMunimedMediHelp

SizweMedshield

ProSanoBonitas

Momentum

80

KeyCare

7558-discovery front 7-11 9/11/06 2:03 Page 23

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 62 4

inflationary trend we have seen in the past number of years,

where members are increasingly viewing specialists as their

first port of call when seeking medical advice.

2. Using Discovery Health’s expertise on HIV and

AIDS through Discovery HIVCare

Increasingly, quality of delivery is a key differentiator in the

health environment. We must use our scale and size, as well

as our experience, to the advantage of our members. An

important initiative that we will focus on in 2007 is

Discovery HIVCare, a comprehensive HIV and AIDS-

management programme aimed at employers, which

seamlessly integrates with Vitality WellPoint.

It provides employers with a variety of reporting tools and

interventions, including surveys, HIV and AIDS education

and awareness, voluntary counselling and testing, medical

advice and counselling and policy development. The HIV

and AIDS disease management programme also gives

access to ARVs, doctor consultations and pathology, as well

as support for employees with HIV and AIDS.

3. Managing the complex health care environment

through DiscoveryCare

Discovery Health is committed to providing our members

with access to excellent health care that is affordable in the

long-term. Through DiscoveryCare, a high-touch service to

our members who are in need of care, we manage the high

cost of health care, hospitalisation and chronic medicines

with the specialised input from experts in actuarial and

clinical risk management.

DiscoveryCare’s Hospital Utilisation Management enables

us to manage the risk of expensive and clinically complex

hospital events and allows us to make clinically appropriate

funding decisions for certain cases. Through our Disease

Management Programme, we recognise the importance of

assisting members who suffer from diseases such as HIV

and AIDS and cancer, to actively manage their lifestyles.

Interventions such as lifestyle management, managing

treatment compliance and response, and support and

counselling, all have positive effects on the prognosis of a

patient, and ultimately reduce hospital admissions.

An important focus for DiscoveryCare in 2007 will be to

engage in strong relationships with hospital groups that will

benefit all stakeholders in the health care environment.

2. New partnerships in the distribution environmentDuring the year under review, Discovery embarked on two

exciting enterprise development initiatives that are helping

to create a presence in new markets and in particular, are

helping to create greater awareness of Discovery and the

KeyCare offering. These are:

• A partnership with a black-owned intermediary house, PFM

• The opening of Discovery Consulting Services, Soweto –

our first distribution franchise in Soweto, allowing us to

better service intermediaries and clients based in the area.

In both cases, we have created partnerships that allow us

better penetration into emerging markets. In turn, we

provide the resources and expertise to help individuals from

previously disadvantaged communities develop viable

business enterprises.

3. We are involved in LIMS, an industry initiativeWe have been closely involved with the private health care

industry’s investigation into extending access to medical

scheme benefits for the low income market. We expect to

see the activity around this new class of medical schemes –

the Low Income Medical Scheme – to intensify during the

year ahead and expect implementation in January 2008.

Discovery Health will continue its active role in this process,

in line with our commitment to making quality health care

accessible to a greater proportion of South Africans.

OUR PROSPECTS FOR THE COMING YEARWe are excited about Discovery Health’s future prospects –

not only in terms of growth and profitability, but also our

ability to use our leadership role to contribute to a better

health care system in South Africa. In the year ahead, we

will focus on important strategic opportunities that will

allow us to reduce the cost of health care while our

infrastructure capabilities enable us to deliver personalised

and convenient service to our members:

1. Continued focus on the quality and cost ofhealth careGoing into 2007, Discovery Health has announced its third

consecutive single digit increase. We are also excited about

the impact that the Discovery Health GP Network and our

Premier Rate agreement with specialists will have in

reducing the cost of care for our members. Importantly, the

reduced cost of GP consultations will hopefully encourage

members to make more use of primary care, only consulting

specialists when it is appropriate. This will address the

DISCOVERY HEALTH (CONTINUED)

7558-discovery front 7-11 9/11/06 2:03 Page 24

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 2 5

Our aim is to work together toward reduced hospital costs

through risk-sharing initiatives.

4. Delivering high quality health care and

personalised transactions and service

While the high cost of health care remains a challenge for

all medical schemes in South Africa, we are confident that

our actuarial and clinical expertise, resources and external

relationships with health care groups, will enable us to keep

private health care in South Africa, affordable over the long

term. The Discovery Health Medical Scheme risk pool is

in a stable position, which provides our members with the

certainty that we can pay their claims well into the future.

Our infrastructure and technology capabilities allow us

to focus on better service delivery and value for our

members. Our aim for 2007 is to personalise and refine our

service offering even more, with initiatives such as

Discovery Mobile. Our members will enjoy easy and

convenient access to their basic plan, claims, Vitality and

DiscoveryCard information, via their cellphones.

5. Keeping abreast of key regulatory developments

The Council for Medical Schemes published a number of

proposals for changes to the design of medical scheme

benefits across the industry and for expanding the

Prescribed Minimum Benefits. Discovery Health is an active

participant in the industry debates around the proposed

changes, which we expect to be implemented in 2008. We

are also assessing their potential impact on Discovery

Health and the Discovery Health Medical Scheme. Overall,

we expect them to be positive.

We have initiated a project within Discovery Health to ensure

we are ready to implement the requirements of the Risk

Equalisation Fund once the legislation is passed and

implemented. We expect implementation on 1 January 2008,

but the timelines have not yet been confirmed. In the

meantime, Discovery Health will remain involved with the

industry discussions around this initiative. (For a more

comprehensive update on regulatory issues pertinent to

Discovery Health, please view the regulatory section of the

Discovery sustainability report at www.discovery.co.za).

6. We expect steady growth to continue

The Discovery Health Medical Scheme enjoys scale, size

and stability in the South African health care environment,

and with our continued focus on providing access to quality

health care and personalised service, we expect the scheme

to steadily grow in the year ahead. Discovery Health also

has a clear leadership role in the market and as the

environment changes; we will continue to debate and

engage in industry issues.

For 2007, we have refined our lower-income offering

through enhanced benefits to the KeyCare range. We believe

that KeyCare remains the best offering in the lower-income

market and that it will continue to grow in the year ahead.

The third key-area for continued growth is the closed

scheme market. We currently administer eight closed

schemes and have signed up the Umed Medical Scheme as

a new closed scheme. We believe that this is an area for

strong future growth and our aim is to grow our current

market share of 9% considerably.

O U R I N F R A S T R U C T U R E A N D T E C H N O L O G Y C A PA B I L I T I E S A L L O W

U S T O F O C U S O N B E T T E R S E R V I C E D E L I V E R Y A N D VA L U E F O R

O U R M E M B E R S .

7558-discovery front 7-11 9/11/06 2:03 Page 25

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 62 6

Every year of Discovery Life’s short

history has been characterised by

a cycle of consumer-centric innovation,

followed by rapid organic growth

and consequently, a solid financial

performance.

South Africa’s fastest growing major life assurer

DISCOVERY LIFE

Herschel Mayers

Chief Executive Officer, Discovery Life

7558-discovery front 7-11 9/11/06 2:03 Page 26

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 2 7

THIS YEAR’S PERFORMANCEDiscovery Life drives growth and profitability,without needing further capital investmentIn less than six years, Discovery Life has grown rapidly to

become South Africa’s fastest-growing major life assurance

company. I would argue it is also the industry leader in

innovation. Every year of the company’s short history

has been characterised by a cycle of consumer-centric

innovation, followed by rapid organic growth and

consequently, a solid financial performance.

The year under review has been no exception. In the past

year, we have seen a 25% increase in new business and a

31% increase in operating profit. This has bolstered

Discovery Life’s contribution to the overall performance of

the Discovery Group. In fact, Discovery Life is now a

major contributor to the Discovery Group’s growth and

profitability, as outlined in the Discovery Holdings report by

Adrian Gore. A particularly encouraging development has

been the improvement in the operational cash flow position

of Discovery Life (see figure 1).

100

50

0

–50

–100

–150

–200

–250

–300

Operational cash flow(R million)

2003 2004 2005 2006

FINANCIAL HIGHLIGHTS

• New business R789 million (+25%)

• Gross inflows R1 768 million (+38%)

• Operating profit R546 million (+31%)

• Value of in-force (FSV Basis) R2 297 (+25%)

Figure 1: Discovery Life has turned cash-flow positive in 2006

7558-discovery front 7-11 9/11/06 2:03 Page 27

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 62 8

Our good risk experience has increasedDiscovery Life’s profitabilityAn important aspect of Discovery Life’s performance is our

good risk experience, which resulted in a risk profit of more

than R500 million in the period under review (as

demonstrated in figure 2). Put simply, policyholders are

claiming less than we projected. The positive risk experience

can be attributed to our ability to encourage healthier lives,

as well as healthier lifestyles, through the Vitality

programme. This exceptional mortality and morbidity

experience points to the actuarial soundness of Discovery

Life’s product design and underwriting practices. It also

speaks to an important, almost paradoxical feature of the

Discovery business model: our ability to be both innovative

and conservative at the same time. While we have

developed groundbreaking product structures to the benefit

of the consumer, we have done so in a way that is both

financially prudent and profitable. What’s good for our

clients is also good for our business.

Discovery Life creates real value for its parentcompany and shareholdersSix years ago, we set out to build a major life assurance

business that would compete successfully against more

established players and deliver value to the Discovery

Group and its shareholders. We are seeing this vision

manifest in the strong embedded value of Discovery Life’s

new business, which has grown to R529 million in 2006, as

shown in figure 3.

OUR STRATEGYWe want to lead our industry throughconsumer-centric product innovationDiscovery Life’s success in the risk assurance market has

hinged on a clear strategy. When we entered the market

six years ago, we set out to take a fresh look at life, as our

launch advertising campaign’s tagline put it. The ambiguous

use of the word life was intentional, and spoke to two facets

of our vision:

1. Redefining the life assurance industry through product

innovation;

2. Making a tangible difference in the lives of South

African life assurance consumers.

600

500

400

300

200

100

0

New business EV(R million)

2002 2003 2004 2005 2006

100908070605040302010

0

Actual risk experience as a % of expectation(%)

Adjusted for comparison to reflect5% improvement in expectation

EV assumption

2002 2003 2004 2005 2006

Figure 2: Discovery Life policyholders are claiming less

than expected

Figure 3: Discovery Life’s new business shows strong

embedded value

DISCOVERY LIFE (CONTINUED)

7558-discovery front 7-11 9/11/06 2:03 Page 28

D I S C O V E R Y A N N U A L R E P O R T 2 0 0 6 2 9

It also pointed to the fact that our products centred on

risk cover, rather than investment aspects. This latter aspect

of our strategy has since evolved to include investment

products, but our focus on innovation and consumer-

centricity will never shift.

THIS YEAR’S KEY FOCUS AREASThe Discovery retirement Optimiser performedwell in its first yearPerhaps the most important strategic development of the

past year has been Discovery Life’s entry into investment

markets with the Discovery retirement Optimiser. Recent

negative publicity around unfair penalty fees and poor

surrender values has painted a picture of a somewhat

beleaguered – and therefore not a very commercially

attractive industry. However, optimism is a hallmark of the

Discovery approach and we are excited about the

possibilities for positive change created by the increasing

trend to consumerism in financial services markets. In fact,

we had identified the potential for more consumer-friendly

retirement products early on. The launch of the Discovery

retirement Optimiser last year was the result of nearly two

years of product development.

I am pleased to report that it has gone well. We now hold

16% of the independent broker retirement annuity market.

New industry developments indicate a shift in the life

assurance industry’s approach to retirement funding.