annual financial results for the 12 months ended 31 August ...€¦ · Octodec Investments Limited...

44

>1 Octodec Investments Limited | Annual Financial Results Presentation annual financial results for the 12 months ended 31 August 2016

Transcript of annual financial results for the 12 months ended 31 August ...€¦ · Octodec Investments Limited...

>1

Octodec Investments Limited | Annual Financial Results Presentation

annual financial results

for the 12 months ended

31 August 2016

>2

Octodec Investments Limited | Annual Financial Results Presentation

About us 03

Overview for 04

the year

Our property 07

portfolio

Our results 25

Outlook 36

Questions and 39

answers

Contact details 40

Appendices 41

agenda

>3

Octodec Investments Limited | Annual Financial Results Presentation

about us

• Listed on the JSE in 1990: REIT status on 1 September 2013

• Provided shareholders with an annual compounded return

over 10 years of 14%

• 324 properties (including joint ventures) in portfolio

• Properties managed by City Property Administration (Pty) Ltd

› Seven-year management contract in place (effective

1 July 2011)

› New contract in process of negotiation, separate

subcommittee formed comprising of non-executive

directors

› Over 40 years’ property management experience

› Solid track record of managing residential, retail, office

and industrial property

• The strategy remains the same

› Focus on Tshwane and Johannesburg CBD’s

› Continually improving the quality of our portfolio

› Focus on growing our residential portfolio

About us

>4

Octodec Investments Limited | Annual Financial Results Presentation

overview for the year

• Distribution growth per share of 6.5%, in line with guidance of approximately 6%

• Total property assets value at R12.3 billion, up by R692 million

• NAV up by 5.2% to R29.13 per share

• 4 major developments in progress

Overview

Highlights

› Strategic greenfield developments underway to uplift key Tshwane CBD node

› Entrance to new market outside the CBD through joint venture

› Profitable recycling of non-core assets

› Operating cost efficiencies

› Prudent capital management

Context

› Tough economic, political and operating environment

› Property fundamentals sound

› Residential increasingly competitive

› Rising costs (construction and operating costs)

› Council service delivery issues

>5

Octodec Investments Limited | Annual Financial Results Presentation

overview of Tshwane CBD

Sharon’s

Place

1 on

Mutual

Sustaining city life:

TWO decades of

building a city bears fruit

Overview

Octodec properties – current developments

Van Riebeeck Medical Building

• Concentration of investments

• Increased urbanisation

• New developments improving

node

• New Tshwane House

› GLA of 37 000 m2

› Housing in excess of

1 500 staff

Tshwane

Midtown

Octodec properties – developments under consideration

>6

Octodec Investments Limited | Annual Financial Results Presentation

overview of Johannesburg CBD

Frank’s

Place

Sustaining city life:

TWO decades of building

a city bears fruit

Overview

Octodec properties

• Urban renewal gaining

momentum

• Increasing private sector

investment

• Higher demand for property

• New residential development –

Frank’s Place fully let

>7

Octodec Investments Limited | Annual Financial Results Presentation

>7

Rental income by sector (%)

our property

portfolio

Retail:shops

28.7%

Offices

18.9%

Residential

30.6%

Retail:shoppingcentres

10.0%

Industrial

7.7%

Parking

4.1%

• Inclusive of 4 Joint Ventures

>8

Octodec Investments Limited | Annual Financial Results Presentation

12.8%

3.7%

4.4%

5.3%

7.1%

12.0%

22.5%

32.2.0%

0 10 20 30 40

Tshwane Other

Waverley, Gezina, Moot

Silverton andsurrounding areas

Tshwane Arcadia

Hatfield

Johannesburg andsurrounding areas

Johannesburg CBD

Tshwane CBD

a geographical analysis of our rental income & GLA for the year - 31 August 2016

Our property portfolio

%

157 301

64 974

70 274

78 422

99 228

126 752

141 423

426 330

504 417

0 200 000 400 000 600 000

Tshwane Other

Waverley, Gezina, Moot

Hatfield

Tshwane Arcadia

Tshwane West

Silverton and surroundingareas

Johannesburg and surroundingareas

Johannesburg CBD

Tshwane CBD

m2

Rental

income

(%)

GLA

(m2)

>9

Octodec Investments Limited | Annual Financial Results Presentation

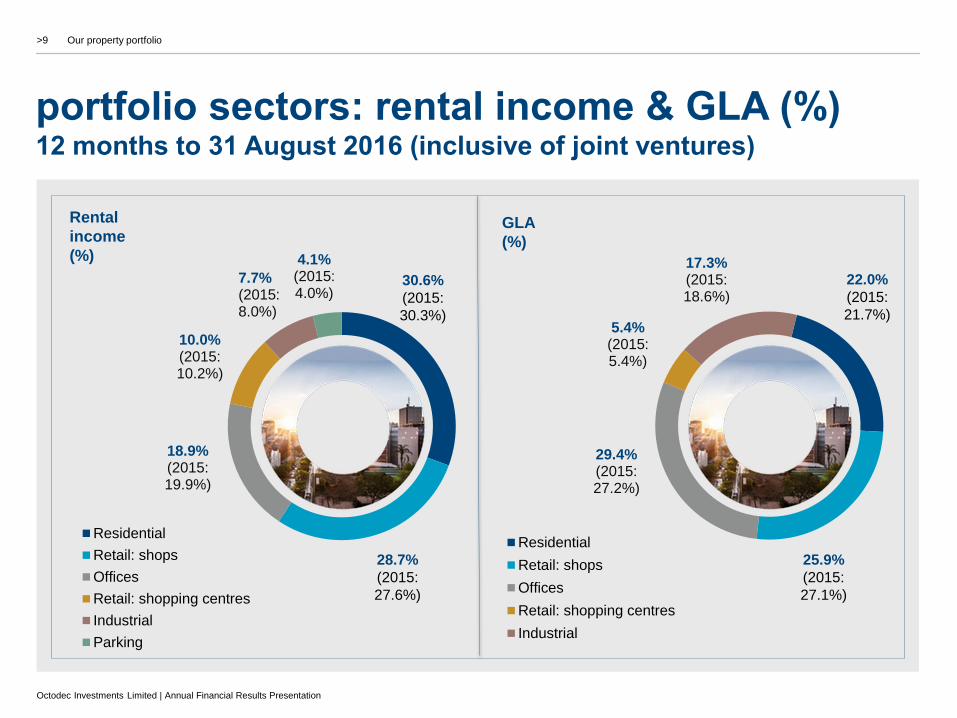

18.9%(2015: 19.9%)

10.0%(2015: 10.2%)

7.7%(2015: 8.0%)

4.1%(2015: 4.0%)

Residential

Retail: shops

Offices

Retail: shopping centres

Industrial

Parking

Rental

income

(%)

portfolio sectors: rental income & GLA (%)12 months to 31 August 2016 (inclusive of joint ventures)

Our property portfolio

28.7%

(2015:

27.6%)

30.6%

(2015:

30.3%)

29.4%(2015: 27.2%)

5.4%(2015: 5.4%)

17.3%(2015: 18.6%)

Residential

Retail: shops

Offices

Retail: shopping centres

Industrial

25.9%

(2015:

27.1%)

GLA

(%)

22.0%

(2015:

21.7%)

>10

Octodec Investments Limited | Annual Financial Results Presentation

residential• 8 840 high quality residential units (Johannesburg 38%,

Tshwane 62%)

• Average monthly rentals

› Bachelor unit – R3 692 per unit (average size 30 m2)

› One bedroom – R4 302 per unit (average size 44 m2)

› Two bedroom – R5 633 per unit (average size 63 m2)

• Strong demand for residential accommodation

• Total vacancies 4.0 % of sector GLA

• Core vacancies 3.6% of sector GLA

• Vacancies higher due to units under refurbishment

• Bad debts at below 1% reflect strong collection

• Increased competition in Johannesburg CBD and Hatfield,

no major impact at this stage

• Tenant profile analysis, ongoing

Portfolio sectors:

Rental income (%)

5.6%Growth in

rental income

30.6%Rental income

Our property portfolio

› Employed by government –

26% of occupants

› Students – 27% of

occupants

› churn reduced to 45% per

annum

› Average gross salary per

application of R30 000

(6 month increase of 5.0%)

› Gross salary above R35 000

– 16% of occupants

>11

Octodec Investments Limited | Annual Financial Results Presentation

retail: shops• Average monthly rentals of R84/m² (31 August 2015: R80/m²)

• Strong demand from national retailers for well-located CBD retail space

(e.g. Shoprite, Pick n Pay, Clicks, Foschini, Truworths)

• Retailers are demanding larger tenant installation contributions

• CBD retail offers more growth opportunities than traditional shopping centres

• Lower cost structures (common area costs, security, cleaning)

• Total and core vacancies – 9.1% of sector GLA

• These vacancies are situated outside of the strong CBD retail nodes

• Major national tenants:

Our property portfolio

Portfolio sectors:

Rental income (%)

5.4%Growth in

rental income

28.7%Rental income

Top 10 retailers by rentable area

Lessee m2

Shoprite Checkers 55 586

Pepkor 15 100

Edcon 13 852

Standard Bank 9 599

McCarthy Limited 6 891

Mr Price Group 6 342

Foschini Retail Group 6 098

Autozone 5 501

Nedbank 5 453

Cambridge Food 4 489

Top 10 retailers by total annual rental FY2016

Lessee Rental (R’000)

Shoprite Checkers R22 802

Pepkor R21 186

Edcon R13 643

Nedbank R10 838

Foschini Retail Group R10 774

Mr Price Group R8 429

Standard Bank R8 005

McCarthy Limited R7 886

KFC R7 683

Chrysler South Africa R6 606

>12

Octodec Investments Limited | Annual Financial Results Presentation

retail: shopping centres

• Average rentals – R129/m² (31 August 2015: R115/m²)

• Increase in vacancies during period at Elardus Park Shopping

Centre, which is in need of an upgrade. Strong interest in vacant

space

• Woodmead Value Mart – 100% let and strong rental growth

(new tenant Nike)

• Killarney Mall:

› Increase in trading density by 14%

› Upgrade of air-conditioning system, security, ceilings,

generator and other improvements at a total cost of

R46 million (FY 2016 & 2017)

• Total and core vacancies – 5.4% of sector GLA

Our property portfolio

Portfolio sectors:

Rental income (%)

4.7%Growth in

rental income

10.0%Rental income

>13

Octodec Investments Limited | Annual Financial Results Presentation

offices• Average rentals – R72/m² (31 August 2015: R70/m²)

• Offices comprise of

› Government office space

› Corporates

› Smaller units occupied by SME’s, where occupancy levels stable

• Government tenants

› 12.8% of total rental income

› Lease renewals 2 – 3 years with net additional take up of space

› 9 365m² let to government tenant effective from 1 March 2016 –

R870 800 per month

› Managed risk

› Renewals with positive reversions

• Total vacancies – 34.7% of sector GLA

• Core vacancies – 15.3% of sector GLA

• Increase in core vacancies mainly relates to Inner Court in Jhb CBD

• Mothballed office space – 19.4% of sector GLA (95 000 m2)

› Opportunity to sell, redevelop or enter into partnerships

• Upgrading of offices

› Inner Court – R19.6m

› Wits Technikon – R18.9m (let effective from 1 January 2017)

Our property portfolio

Portfolio sectors:

Rental income (%)

18.9%Rental income

5.2%Growth in

rental income

>14

Octodec Investments Limited | Annual Financial Results Presentation

industrial

• Average monthly rental – R36/m² (31 August 2015:

R33/m²)

• Successful redevelopment of properties – demand for

upgraded properties

› Upgrade largely tenant driven

› The Tannery Industrial Park (R10 million) – improved

occupancy and rentals expected

• Lower demand for mini units – tough trading environment

• Low cost of occupation – competitive advantage

• Total and core vacancies – 10.8 % of sector GLA

Our property portfolio

Portfolio sectors:

Rental income (%)

3.3%Growth in

rental income

7.7%Rental income

>15

Octodec Investments Limited | Annual Financial Results Presentation

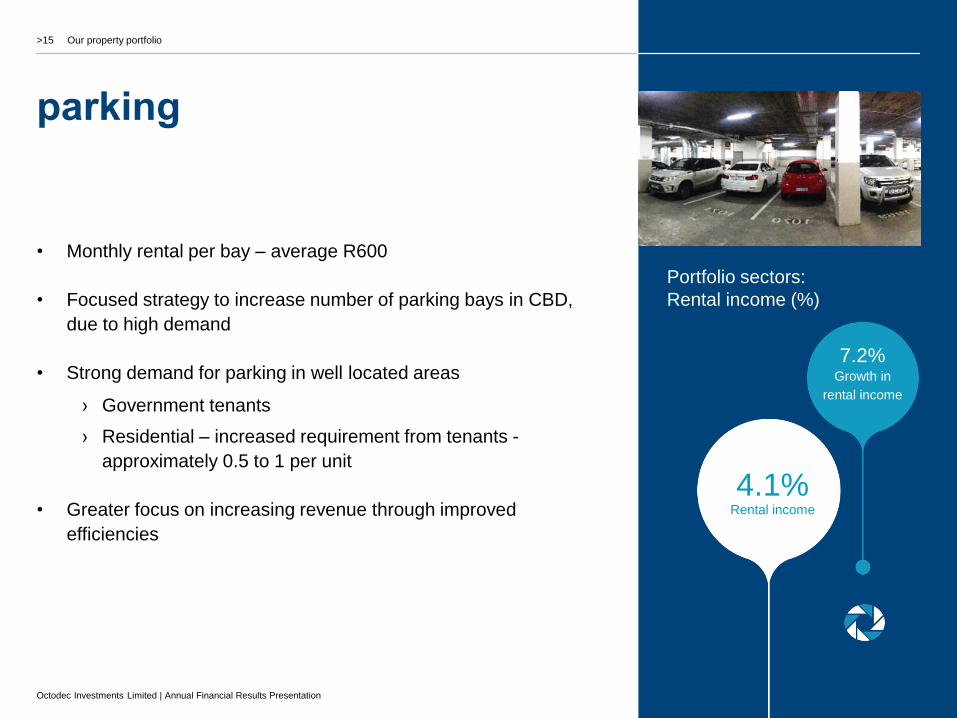

parking

• Monthly rental per bay – average R600

• Focused strategy to increase number of parking bays in CBD,

due to high demand

• Strong demand for parking in well located areas

› Government tenants

› Residential – increased requirement from tenants -

approximately 0.5 to 1 per unit

• Greater focus on increasing revenue through improved

efficiencies

Our property portfolio

Portfolio sectors:

Rental income (%)

4.1%Rental income

7.2%Growth in

rental income

>16

Octodec Investments Limited | Annual Financial Results Presentation

34.7%

9.1%

5.4%

10.8%

4.0%

15.6%15.3%

9.1%

5.4%

10.8%

3.6%

9.8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Offices Retail shops Retail: Shoppingcentres

Industrial Residential Total

Perc

en

tag

e o

f g

ross l

ett

ab

le a

rea (

by s

ecto

r)

Total vacancies

Core vacancies

vacancies by sectoras at 31 August 2016

Note: Core vacancies exclude lettable area of properties that are held for development or properties that are currently being developed

Our property portfolio

>17

Octodec Investments Limited | Annual Financial Results Presentation

vacancies• Total vacancies were at 15.6% of total GLA

(31 August 2015: 15.1%)

• Core vacancies were at 9.8% of total GLA

(31 August 2015: 9.1%)

• Core vacancies increased slightly in the residential, office, and

industrial sectors. Retail – shopping centre vacancies increased

mainly at Killarney Mall and Elardus Park Shopping Centre

• Total office vacancies increased due to the acquisition of the

Van Riebeeck Medical Building, comprising 11 497m² of

mothballed offices for residential conversion

• Residential vacancies increased slightly due to upgrades

underway. Strong demand for well-located quality

accommodation

• In recent years, certain properties were acquired where little

consideration was paid for vacant space. These vacancies

represent opportunities for future unlocking of value

(for example Frank’s Place and Centre Walk redeveloped into

residential & upgraded office space respectively)

• 95 000 m2 of office space available to unlock value

(redevelopment or disposal)

Total core

vacancies at

9.8%

Our property portfolio

>18

Octodec Investments Limited | Annual Financial Results Presentation

lease expiry profile

Gross lettable

area m² GLA (%)

Monthly

contractual rent

R

Rental

income (%)

Residential (12 months and less) 352 002 21.1% 40 044 955 34.4%

Monthly commercial 177 805 10.7% 9 378 771 8.1%

to 31 August 2017 329 973 19.8% 24 286 707 20.9%

to 31 August 2018 237 239 14.2% 17 123 906 14.7%

to 31 August 2019 112 104 6.7% 9 370 768 8.0%

to 31 August 2020 92 075 5.5% 7 496 738 6.4%

Thereafter 107 265 6.4% 8 773 790 7.5%

Vacancies 260 657 15.6% - -

Total 1 669 120 100.0% 116 475 635 100.0%

Our property portfolio

>19

Octodec Investments Limited | Annual Financial Results Presentation

lease expiry profile

• Government leases concluded for 3-year term on average

• Residential leases – short term leases (12 month contracts

providing for a month to month arrangement on expiry)

• Majority of leases for non-national tenants concluded for

1- to 10-year term

• National tenants – leases concluded for 3- to 10-year term

• No major concern other than loss of government tenant in

Hatfield (3 448 m2 / R 518 000 per month, effective from

1 March 2017)

Octodec’s portfolio features a mix of short- to long-term

leases with the majority of short-term leases providing for

a monthly agreement at expiry, which is typical of the

residential market

Our property portfolio

>20

Octodec Investments Limited | Annual Financial Results Presentation

recent acquisitions

Property Location Details Rentable m²

Total purchase

price R’million

Initial yield

%

Date of

transfer

Van Riebeeck

Medical

Building

Corner Lilian Ngoyi and

Francis Baard Streets,

Tshwane CBD

Mothballed offices and

shops for residential

development

11 497 28.9 Development

under

consideration

February 2016

Ross

Electrical

389 Johannes

Ramakhoase Street,

Tshwane CBD

Retail – forms part of

site assembly

525 2.6 8.0 April 2016

Our property portfolio

>21

Octodec Investments Limited | Annual Financial Results Presentation

Property Location Details

Rentable

m²

Total

sales price

R’million

Exit

yield

%

Date of

transfer

Dirk du Toit

(1) & (2)

323, 325, 327 Charlotte

Maxeke Street, Tshwane West

Shops and workshop 2 909 9.5 11.0 November 2015

Herriotdale Green Street,

Herriotdale

Open parking 7 307 5.5 9.0 November 2015

Eloff Street 17 & 19 Eloff Street,

Johannesburg

Warehouse 596 2.5 10.0 April 2016

Mitchbuit 590 Charlotte Maxeke Street,

Tshwane West

Shops 1 692 4.8 11.0 June 2016

Landkirk 568 Bonita Crescent, Tshwane Warehouse 1 265 3.2 11.0 June 2016

Works@

Registry

Corner of Kerk and Troye

Streets, Johannesburg CBD

Retail offices and parking

(includes 5 565m² of mothballed

office space)

10 505 30.0 4.0 July 2016

Total 55.5 7.0

recent salesIn line with our strategy to dispose of non-core assets, the following properties

were sold and transferred during the period under review

• The profit on the disposal consideration of R55.5 million amounted to R8.5 million, a premium of 15.3% above book value at 31 August 2015

• A further 10 properties have been sold and transfer is expected to take place shortly

• The total expected proceeds from the disposals after 31 August 2016 amount to R179 million, at well above book value

Our property portfolio

>22

Octodec Investments Limited | Annual Financial Results Presentation

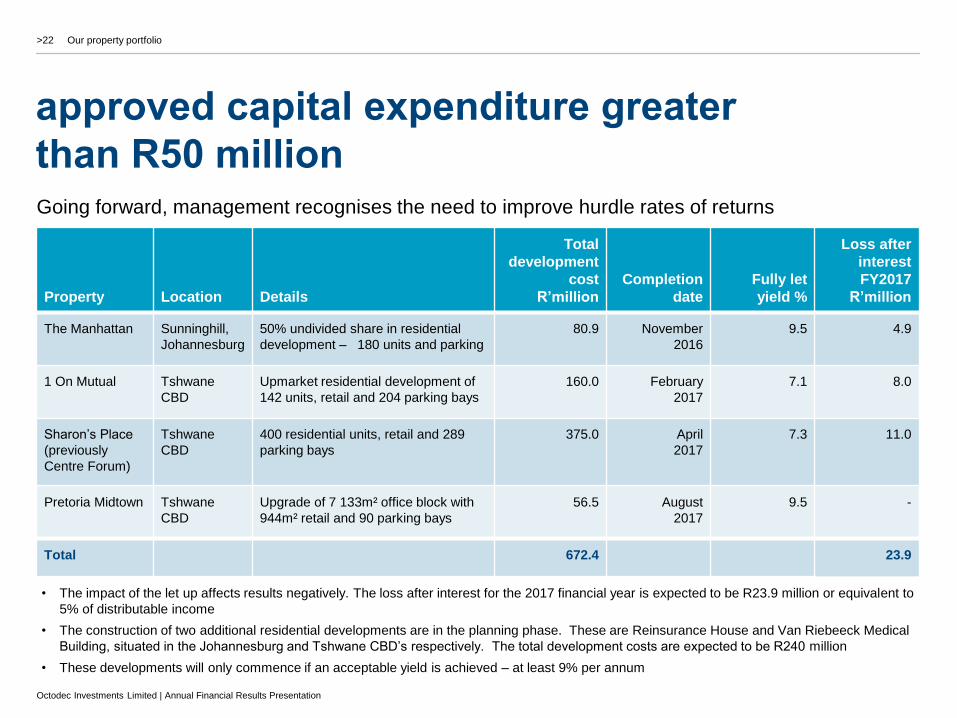

approved capital expenditure greater

than R50 millionGoing forward, management recognises the need to improve hurdle rates of returns

Property Location Details

Total

development

cost

R’million

Completion

date

Fully let

yield %

Loss after

interest

FY2017

R’million

The Manhattan Sunninghill,

Johannesburg

50% undivided share in residential

development – 180 units and parking

80.9 November

2016

9.5 4.9

1 On Mutual Tshwane

CBD

Upmarket residential development of

142 units, retail and 204 parking bays

160.0 February

2017

7.1 8.0

Sharon’s Place

(previously

Centre Forum)

Tshwane

CBD

400 residential units, retail and 289

parking bays

375.0 April

2017

7.3 11.0

Pretoria Midtown Tshwane

CBD

Upgrade of 7 133m² office block with

944m² retail and 90 parking bays

56.5 August

2017

9.5 -

Total 672.4 23.9

• The impact of the let up affects results negatively. The loss after interest for the 2017 financial year is expected to be R23.9 million or equivalent to

5% of distributable income

• The construction of two additional residential developments are in the planning phase. These are Reinsurance House and Van Riebeeck Medical

Building, situated in the Johannesburg and Tshwane CBD’s respectively. The total development costs are expected to be R240 million

• These developments will only commence if an acceptable yield is achieved – at least 9% per annum

Our property portfolio

>23

Octodec Investments Limited | Annual Financial Results Presentation

1 on mutual

Pick n Pay

and

Mugg & Bean

Tshwane CBD development

cost of: R160.0m

Residential units: 142

Retail: 1 746m2

Offices: 443m2

Parking bays: 204

Our property portfolio

>24

Octodec Investments Limited | Annual Financial Results Presentation

sharon’s place (centre forum)

Tshwane CBD development

cost of: R375m

Residential units: 400

Retail: 5 660m²

Parking bays: 289

Retail fully let

Shoprite and

Clicks as

anchors

Our property portfolio

>25

Octodec Investments Limited | Annual Financial Results Presentation

>25

our results

>26

Octodec Investments Limited | Annual Financial Results Presentation

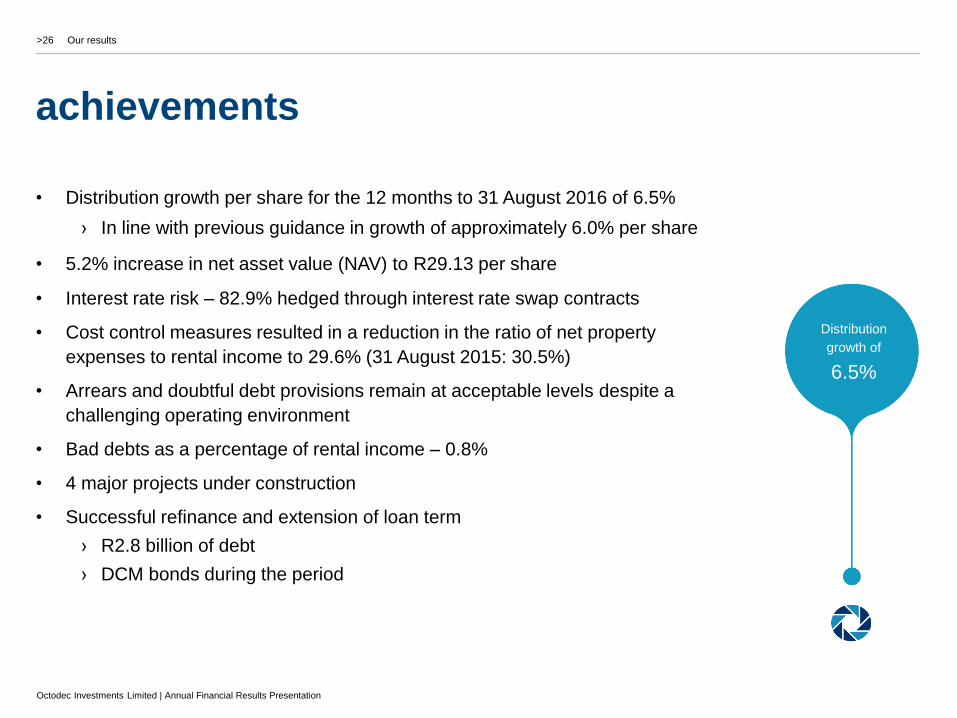

achievements

• Distribution growth per share for the 12 months to 31 August 2016 of 6.5%

› In line with previous guidance in growth of approximately 6.0% per share

• 5.2% increase in net asset value (NAV) to R29.13 per share

• Interest rate risk – 82.9% hedged through interest rate swap contracts

• Cost control measures resulted in a reduction in the ratio of net property

expenses to rental income to 29.6% (31 August 2015: 30.5%)

• Arrears and doubtful debt provisions remain at acceptable levels despite a

challenging operating environment

• Bad debts as a percentage of rental income – 0.8%

• 4 major projects under construction

• Successful refinance and extension of loan term

› R2.8 billion of debt

› DCM bonds during the period

Distribution

growth of

6.5%

Our results

>27

Octodec Investments Limited | Annual Financial Results Presentation

challenges

New development

impact

• Tough economic environment

• Like-for-like growth in rental income of 5.3%, under pressure

• Rise in costs (utilities, assessment rates)

• Core vacancies in portfolio (excludes properties held for

redevelopment) at 9.8% (31 August 2015: 9.1%)

• Higher interest rates (all-in weighted average cost of funding at 9.0%

at 31 August 2016)

• Dilutionary impact on distribution due to:

› Let up phase of new residential developments –

6 to 12 months

› major upgrades to properties

› acquisition of vacant buildings (Van Riebeeck Medical

Building R28.9 million)

Our results

>28

Octodec Investments Limited | Annual Financial Results Presentation

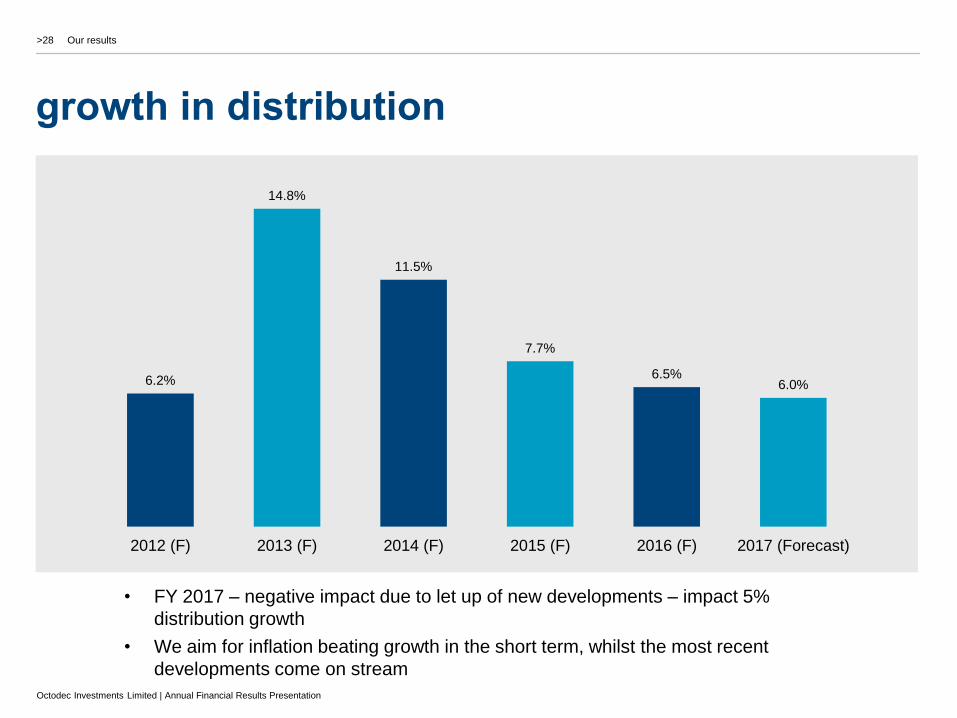

growth in distribution

6.2%

14.8%

11.5%

7.7%

6.5%6.0%

2012 (F) 2013 (F) 2014 (F) 2015 (F) 2016 (F) 2017 (Forecast)

Our results

• FY 2017 – negative impact due to let up of new developments – impact 5%

distribution growth

• We aim for inflation beating growth in the short term, whilst the most recent

developments come on stream

>29

Octodec Investments Limited | Annual Financial Results Presentation

R’000

%

Change

Reviewed

year to

31 August

2016

Audited

Year to

31 August

2015

Revenue – earned on contractual basis 6.7% 1 742 871 1 634 159 Core growth of 5.3%

Operating costs 1.1% (790 529) (742 212) Tight cost control

Net rental income from properties 6.8% 952 342 891 947

Administrative costs (71 005) (72 915) Reduction in asset management fee

Operating profit 7.6% 881 337 819 032

Interest received 10 138 5 953

Share of income from Joint Ventures 14 026 13 493 4 JV’s – each 50% held

Distributable profit before finance costs 8.0% 905 501 838 478

Finance costs 4.9% (394 751) (376 491) Increased loans to fund developments

Distributable income before taxation 10.6% 510 750 461 987

Taxation charge ̶ 15

Shareholder distributable earnings 10.6% 510 750 462 002

Number of shares in issue (000) 254 551 252 322

Dividend per share (cents) 201.5 189.2

First six months 98.4 96.8

Second six months 103.1 92.4

% growth in distribution 6.5%

distributable earnings

Note: Shareholders will be entitled to elect to reinvest the cash dividend in return for shares

Our results

>30

Octodec Investments Limited | Annual Financial Results Presentation

condensed consolidatedstatement of financial position

Reviewed Audited

31 August 31 August

R'000 2016 2015

ASSETS

Non-current assets 12 219 234 11 644 922

Investment property 11 956 631 11 449 157 320 properties

Other financial assets 51 849 -

Derivative financial instruments 38 172 34 451

Investment in joint ventures 172 582 161 314 4 JV’s – equity accounting

Current assets 200 661 158 091

Trade and other receivables 131 552 102 822

Bank and Cash 69 109 55 269

Non-current assets held for sale 173 000 - 30 properties available for sale

12 592 895 11 803 013

EQUITY AND LIABILITIES

Equity 7 413 800 6 987 679

Stated capital 3 958 207 3 907 819

Non-distributable reserves 3 112 885 2 799 231

Distributable reserves 342 708 280 629

Non-current liabilities 4 106 208 3 012 937

Interest-bearing borrowings 4 023 911 2 917 174

Derivative financial instruments 9 308 22 778

Deferred taxation 72 989 72 985

Current liabilities 1 072 887 1 802 397

Interest-bearing borrowings 755 116 1 463 699 loan terms extended

Non-interest-bearing borrowings 315 698 335 216

Dividends payable 2 073 3 482

12 592 895 11 803 013

Shares in issue ('000) 254 551 252 322

Net asset value (NAV) per share (cents) 2 913 2 769

Loan to investment value (LTV) ratio (%) 38.3% 37.3%

Our results

>31

Octodec Investments Limited | Annual Financial Results Presentation

capital management

• Domestic medium term note (DMTN) programme at

R3bn – issuance at R755.1 million at 31 August 2016

• Interest rates hedged – 82.9% of borrowings

(31 August 2015: 94.2%)

• All-in cost of debt at 9.0% (31 August 2015: 8.9%)

• Loan to value 38.3% (31 August 2015: 37.3%)

• Dividend reinvestment programme

› R2.2 million shares issued

› R50 million proceeds

9.0%All-in cost

Of debt

Our results

>32

Octodec Investments Limited | Annual Financial Results Presentation

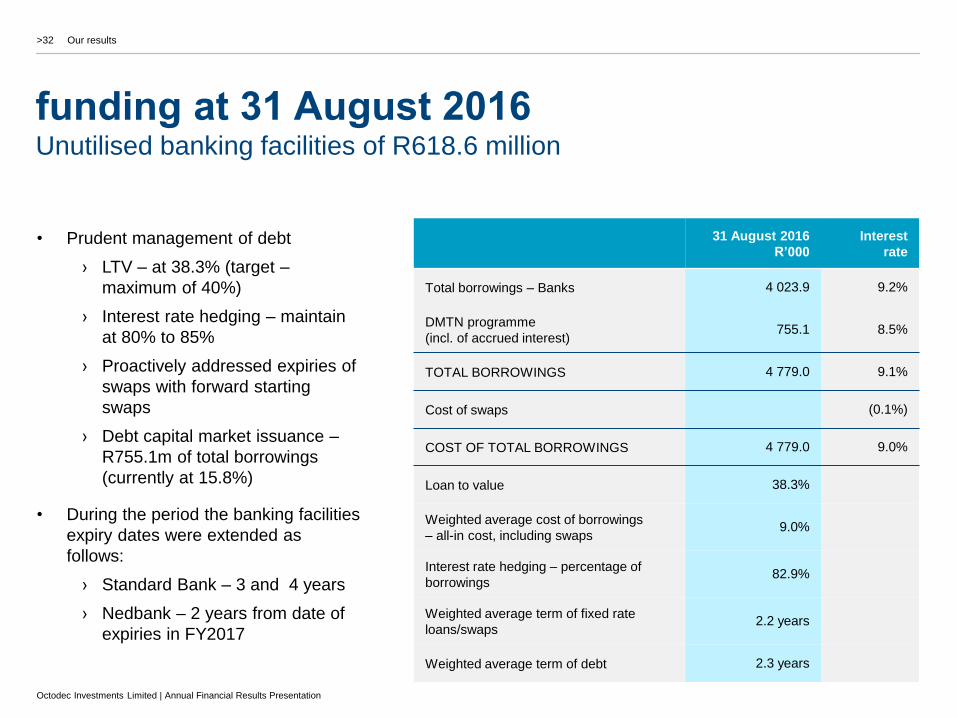

funding at 31 August 2016Unutilised banking facilities of R618.6 million

31 August 2016

R’000

Interest

rate

Total borrowings – Banks 4 023.9 9.2%

DMTN programme

(incl. of accrued interest)755.1 8.5%

TOTAL BORROWINGS 4 779.0 9.1%

Cost of swaps (0.1%)

COST OF TOTAL BORROWINGS 4 779.0 9.0%

Loan to value 38.3%

Weighted average cost of borrowings

– all-in cost, including swaps9.0%

Interest rate hedging – percentage of

borrowings82.9%

Weighted average term of fixed rate

loans/swaps2.2 years

Weighted average term of debt 2.3 years

Our results

• Prudent management of debt

› LTV – at 38.3% (target –

maximum of 40%)

› Interest rate hedging – maintain

at 80% to 85%

› Proactively addressed expiries of

swaps with forward starting

swaps

› Debt capital market issuance –

R755.1m of total borrowings

(currently at 15.8%)

• During the period the banking facilities

expiry dates were extended as

follows:

› Standard Bank – 3 and 4 years

› Nedbank – 2 years from date of

expiries in FY2017

>33

Octodec Investments Limited | Annual Financial Results Presentation

Nedbank –R2 745m

Standard Bank –R955m

DCM Commercial-

paper –R681m

31 August 2015

Nedbank Standard Bank DCM-commercial paper

funding as at

Nedbank –R2 999m

Standard Bank –

R1 025m

DCM Commercial-

paper –R755m

31 August 2016

Nedbank Standard Bank DCM-commercial paper

Our results

>34

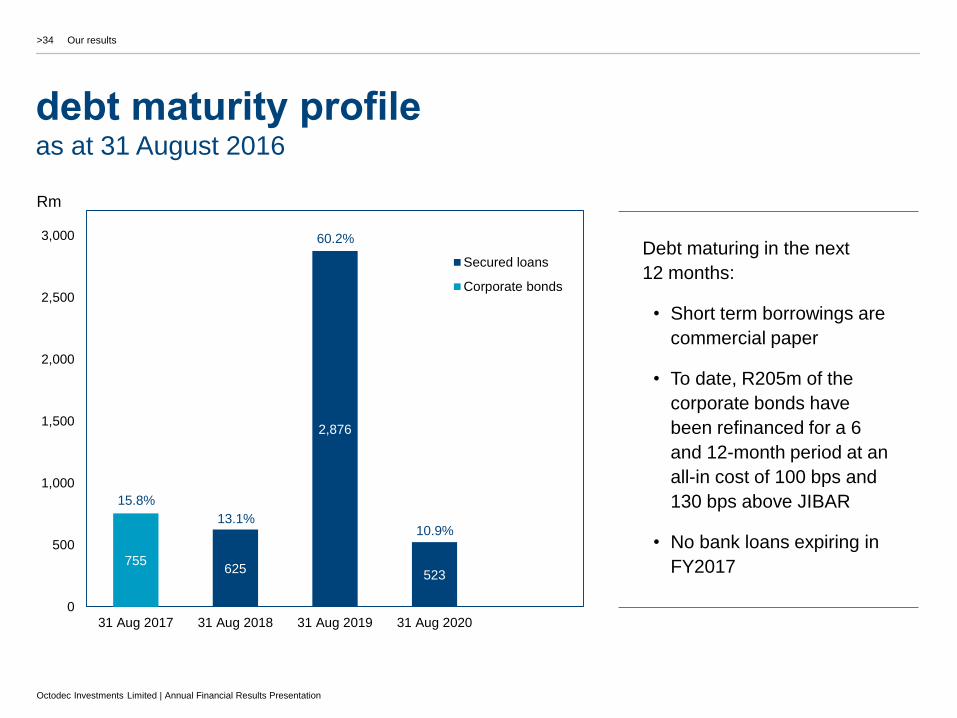

Octodec Investments Limited | Annual Financial Results Presentation

625

2,876

523755

0

500

1,000

1,500

2,000

2,500

3,000

31 Aug 2017 31 Aug 2018 31 Aug 2019 31 Aug 2020

Secured loans

Corporate bonds

debt maturity profile as at 31 August 2016

Our results

Debt maturing in the next

12 months:

• Short term borrowings are

commercial paper

• To date, R205m of the

corporate bonds have

been refinanced for a 6

and 12-month period at an

all-in cost of 100 bps and

130 bps above JIBAR

• No bank loans expiring in

FY2017

Rm

15.8%

13.1%

60.2%

10.9%

>35

Octodec Investments Limited | Annual Financial Results Presentation

1,2501,351 1,361

500

750

0

500

1,000

1,500

2,000

2017 2018 2019 2020 2021

interest rate hedges expiry profile

Our results

Fixed rate loans – R412 million

Swaps – total of R4.8 billion

Average weighted expiry – 2.2 years

• At 31 August 2016, interest rates in

respect of 82.9% of borrowings

hedged

• Subsequent to 31 August 2017

R1.250 billion of swaps entered into

› Weighted term 3.6 years

› All-in weighted cost of 8.11%

› Commencing 3 January 2017

› Forecast hedge position –

31 August 2017 – 79 %

Rm

24.0%

25.9% 26.1%

9.6%

14.4%

>36

Octodec Investments Limited | Annual Financial Results Presentation

>36

outlook

>37

Octodec Investments Limited | Annual Financial Results Presentation

outlook

• Continued weakness in the domestic economy

• Country downgrade and political uncertainty

• Increasing competition – CBD Johannesburg and Hatfield (residential)

• Well-positioned to continue to take advantage of opportunities in the CBDs

› CBD retail continues to generate strong demand from National tenants

› Strong demand for affordable and secure, quality residential accommodation – forecast of 6% core rental income growth

• Residential developments to significantly uplift the Tshwane CBD node where we have a strategic concentration of assets

› 1 on Mutual and Sharon’s Place will be ready for occupation in the 2017 financial year

• Continue to unlock value – exciting future development opportunities under discussion

• Project returns will be improved, hurdle yield required of above 9%

Forecast

• Impact on distributions during let up phase amounting to R23.9m or 5% of distribution growth

• Current forecast growth in distributable income per share of approximately 6%

6%forecast

growth

Outlook

>38

Octodec Investments Limited | Annual Financial Results Presentation

investment case

Well-positioned to continue to unlock value and

navigate the challenging economic environment

Steady and

sustainable

value

creation

Outlook

• Strategy to remain the same

• Sustainable model – urban renewal and middle-class

growth

• Well-balanced portfolio with significant synergies across

sectors in the CBDs

• Strong development pipeline – unlock value of current

portfolio (new and redevelopments)

• Proven track record – hands-on approach delivering

above average returns

• Negotiation of City Property contract well underway

>39

Octodec Investments Limited | Annual Financial Results Presentation

>39

questions

and answers

>40

Octodec Investments Limited | Annual Financial Results Presentation

>40

www.octodec.co.za

contact us

Jeffrey WapnickManaging Director

Tel: +27 12 319 8708

e-mail: [email protected]

Anthony SteinFinancial Director

Tel: +27 12 319 8780

e-mail: [email protected]

>41

Octodec Investments Limited | Annual Financial Results Presentation

5.9%Government

Employees

Pension Fund

5.8%Stanlib

4.9%Old Mutual

Group

2.5%Eskom Pension &

Provident Fund

2.2%Nedbank

Group

corporate structure

38%Institutional investors

24%Other

38%Wapnick family & directors

Top 5Beneficial institutional

shareholders

Appendix I

>42

Octodec Investments Limited | Annual Financial Results Presentation

our strategy

• Offer innovative property investment opportunities that

create and deliver long-term sustainable returns by:

› Building a diversified portfolio in the Tshwane and

Johannesburg CBDs and surrounding areas with

an exposure to residential, office, retail and

industrial sectors

› Actively promoting urban renewal in the Tshwane

and Johannesburg CBDs

• Increase the profitability of our existing portfolio by:

› Continually improving the quality of our portfolio

› Enhancing our tenant profile

› Developing well-located properties

Appendix II

>43

Octodec Investments Limited | Annual Financial Results Presentation

our strategy

• Increase the profitability of our existing portfolio by

(continued):

› Concentration of properties in Tshwane and

Johannesburg CBDs, which makes it easier to

manage and extract value from our portfolio

› Pursuing acquisitions that offer strategic value

and sustainable yield-enhancing opportunities

› Focusing on growing our residential portfolio in

the medium term

› Recycling capital from low growth, poor quality

assets to high growth, high quality assets

› Enhancing returns through effective mix of debt

and equity to optimise capital structure

› Management of interest and liquidity risk

Appendix II (continued)

>44

Octodec Investments Limited | Annual Financial Results Presentation

top 10 propertiesAccount for 26.0% of the Octodec investment property portfolio by value

Property Location Sector

Value

R’million

%

of portfolio

The Fields Hatfield, Tshwane Hotel, shops, offices, 765 flats and parking 766.9 6.3

Killarney Mall Killarney, Johannesburg Shopping centre, offices and parking 618.9 5.0

Kempton Place Kempton Park Shops, offices and 469 flats 296.2 2.4

Centre Walk Tshwane CBD Shops, offices and parking 289.0 2.4

Woodmead Value Mart Woodmead, Johannesburg Shopping centre 265.6 2.2

Louis Pasteur Medical Tshwane CBD Shops, offices, hospital and parking 208.3 1.7

Nedbank Plaza Arcadia, Tshwane Shops, offices, 144 flats and parking 205.7 1.7

Steyn’s Place Tshwane CBD Shops, 381 flats and parking 178.7 1.5

Jeff’s Place Tshwane CBD 384 flats and parking 176.0 1.5

Elardus Park Shopping Centre Tshwane East Shopping centre 168.1 1.4

Appendix III