An Overview on Islamic Modes of Financing (A Case Study of Islamic Banks in Afghanistan)

53

MONOGRAPH ON An Overview on Islamic Modes of Financing (A Case Study of Afghanistan) ίή طήر کلی بϭή میلϮϤ تسامیلی ا ما( ϥفغانستاردی اϮ مطالعۀ م) BY Ahmad Frogh “Zhakfar” 09-RC100-81 In partial fulfillment of the requirements for the award of the degree of BACHELOR OF BUSINESS ADMINISTRATION BBA IN FINANCE TO RANAUNIVERSITY Baraki Square, Kabul – Afghanistan ϥفغانستامی اساری اϮϬϤ جت عالی تحصیا وزارتوصیسات خص ریاست موست عالی تحصیا رنــــاــتــــــــــــون پـــوهـن تصدیقتصادست پوهنحی ا ریاجارت تϩت ادارϨϤ دیپارتیتή آمIslamic Republic of Afghanistan Ministry of Higher Education Directorate of Private Higher Education RANA UNIVERSITY Directorate of Industrial Economic Faculty BBA Department

-

Upload

ahmad-frogh-zhakfar -

Category

Documents

-

view

557 -

download

2

Transcript of An Overview on Islamic Modes of Financing (A Case Study of Islamic Banks in Afghanistan)

MONOGRAPH

ON

An Overview on Islamic Modes of Financing

(A Case Study of Afghanistan)

ر کلی ب ط یلم مالی اسامی ت

ردی افغانستا) (مطالعۀ م

BY

Ahmad Frogh “Zhakfar” 09-RC100-81

In partial fulfillment of the requirements for the award of the degree of

BACHELOR OF BUSINESS ADMINISTRATION

BBA IN FINANCE

TO

RANAUNIVERSITY

Baraki Square, Kabul – Afghanistan

ری اسامی افغانستا ج وزارت تحصیات عالی

ریاست موسسات خصوصی تحصیات عالی

پـــوهـنــتــــــــــــون رنــــا ریاست پوهنحی اقتصاد تصدیت ادار تجارت یت دیپارت آم

Islamic Republic of

Afghanistan

Ministry of Higher

Education

Directorate of Private Higher

Education

RANA UNIVERSITY

Directorate of Industrial

Economic Faculty

BBA Department

I

MONOGRAPH ON

An Overview on Islamic Modes of Financing

(A Case Study of Afghanistan)

ر کلی ب ط ت یلم مالی اسامی م

ردی افغانستا) (مطالعۀ م

In partial fulfillment of the requirements for the award of the degree of

BACHELOR OF BUSINESS ADMINISTRATION

BBA TO

RANA UNIVERSITY PREPARED BY:

Name: Ahmad Frogh “Zhakfar”

Father’s Name: Muhammad Hassan

Registration No:09-RC100-81

Period: Jan/2010 to Dec/2013

Serial No.:BBA/FIN/030/2015

Signature:______________________

Date:

SUPERVISED BY:

Name: Sayed Kifayatullah

Designation: Lecturer

Qualification: MSC (Hons) Economics & Finance

ID No.:

Phone No:

Email Add: [email protected]

Signature:______________________

Date:

ری اسامی افغانستا ج تحصیات عالیوزارت

ریاست موسسات خصوصی تحصیات عالی

پــوهـنــتــــــــــون رنـــا ریاست پوهنحی اقتصاد تصدیت ادار تجارت یت دیپارت آم

Islamic Republic of

Afghanistan

Ministry of Higher

Education

Directorate of Private Higher

Education

RANA UNIVERSITY

Directorate of Industrial

Economic Faculty

BBA Department

II

PROJECT APPROVAL SHEET

The undersigned certify that they have read the following Project Report and are satisfied with the

overall exam performance, and recommend the project to the Department of Business Administration

for acceptance.

Title: An Overview on Islamic Modes of Financing (A Case Study of Islamic Banks in Afghanistan)

Prepared by: Ahmad Frogh “Zhakfar”

09-RC100-81

Recommended by:

Designation in RANA

Signature and Date

Project Coordinator: _________________________________

Head of Department: _________________________________

Vice Chancellor “Academic: _________________________________

VC for Academic Affairs

RIHS Management Verification & Stamp: _________________________________

Date:

III

PROJECT EVALUATION SHEET (Decision of the Monograph Evaluation Committee)

STUDENT PARTICULARS

Name: Ahmad Frogh “Zhakfar” Registration

No.: 09-RC100-81

Father’s Name: Muhammad Hassan Project Title: An Overview of Islamic Modes of

Financing (A Case Study of Afghanistan)

Assessment Criteria Member 1

Problem Definition: Relevant Yes☐No☐Clearly phrased Yes☐ No☐ Testable Yes☐ No☐

Research Design: Theoretical Background Yes☐ No☐ Appropriate Research Method Yes☐ No☐

Research Result: Description ☐ Analysis☐

Analysis, Interpretation and Conclusion: Clear Yes☐ No☐

Further Comments (Allocate Marks out of 25%)

Name of the Committee Member: ______________________________ Sign:___________________

Date:

Member 2

Problem Definition: Relevant Yes☐No☐Clearly phrased Yes☐ No☐ Testable Yes☐ No☐

Research Design: Theoretical Background Yes☐ No☐ Appropriate Research Method Yes☐ No☐

Research Result: Description ☐ Analysis☐

Analysis, Interpretation and Conclusion: Clear Yes☐ No☐

Further Comments (Allocate Marks out of 25%)

Name of the Committee Member: _____________________________ Sign:____________________

Date:

IV

Member 3

Problem Definition: Relevant Yes☐No☐Clearly phrased Yes☐ No☐ Testable Yes☐ No☐

Research Design: Theoretical Background Yes☐ No☐ Appropriate Research Method Yes☐ No☐

Research Result: Description ☐ Analysis☐

Analysis, Interpretation and Conclusion: Clear Yes☐ No☐

Further Comments (Allocate Marks out of 25%)

Name of the Committee Member: _______________________________Sign:__________________

Date:

Member 4

Problem Definition: Relevant Yes☐No☐Clearly phrased Yes☐ No☐ Testable Yes☐ No☐

Research Design: Theoretical Background Yes☐ No☐ Appropriate Research Method Yes☐ No☐

Research Result: Description ☐ Analysis☐

Analysis, Interpretation and Conclusion: Clear Yes☐ No☐

Further Comments (Allocate Marks out of 25%)

Name of the Committee Member: _______________________________Sign:__________________

Date:

V

ANALYSIS OF MARKS ALLOCATED BY COMMITTEE MEMBERS:

Member 1 Member 2 Member 3 Member 4 Total

Initial Initial Initial Initial VC Stamp

VI

Ahmad Frogh “Zhakfar: 09.RC100.81

RANA UNIVERSITY BARAKI SQUARE, KABUL – AFGHANISTAN

DECLARATION

I hereby, declare that the Monograph [An Overview on Islamic Modes of Financing (A Case Study of

Islamic Banks in Afghanistan)] of the requirements for the Degree of Bachelor of Business

Administration (BBA) to RANA University is my original work and not submitted for any other

degree, diploma, fellowship or similar title or prize.

Ahmad Frogh “Zhakfar”

Signature:__________________

Date:

VII

FACULTY CERTIFICATE

Date:

Batch: Jan/2010 up to Dec 2013

Register Number: 09-RC100-81

Serial Number: BBA/FIN/030/2015

This is to certify that the Project / Monograph titled

An Overview on Islamic Modes of Financing (A Case Study of Islamic Banks in Afghanistan)

Submitted in partial fulfillment of the requirements for the degree of "bachelor of business

administration to RANA UNIVERSITY, Baraki Square, Kabul – Afghanistan is carried out

By

MR Ahmad Frogh “Zhakfar” Under my direct supervision and guidance and that no part of this report has been submitted

for the award of any other degree, diploma, fellowship or other similar titles or prize and that

the work has not been published in any scientific or popular journals or magazines.

FACULTY PARTICULARS

Name: Mr. Jehanzeb Khan

Qualification: MS (Management Sciences)

Designation: Lecturer

ID No.:

Signature:______________________

Date:

DEPARTMENT IN-CHARGE

Name: Sayed Kifayatullah

Qualification: MSC (Hons) Economics & Finance

Designation: Head of Department

ID No.:

Signature:______________________

Date:

Department Stamp

VIII

ACKNOWLEDGEMENT

All praises and thanks to Almighty Allah, the source of knowledge and wisdom to

mankind, who conferred me with power of mind and capability to take this material

contribution to already existing knowledge. All respect and love to him who is an everlasting

model of guidance for humanity as a whole.

I feel pride in expressing my deepest sense of gratitude to Mr. Kifayatullah who is the

source of origination of this project. His scholastic, consistent advice, encouraging behavior,

valuable suggestion, personal interest and dynamic supervision enabled me to complete the

present Project. This research work was hard to be accomplished without his cooperation.

I am extremely thankful to my colleagues and classmates whose help and good wishes made

this project a success.

Last of all no acknowledgement could never express my obligations to my loving parents,

brothers, and the whole family of mine, because my success is really the fruit of their devoted

prayers. I can never compensate their unlimited love and kindness. My words are extremely

dedicated to my Mother, without her continuous support and encouragement I never would

have been able to achieve my goals. All I am I owe to my mother. I attribute all my success

in life to the moral, intellectual and physical education I received from her.

Sincerely Yours,

Ahmad Frogh “Zhakfar”

09-RC100-81

BBA

Finance

IX

TABLE OF CONTENTS

PROJECT APPROVAL SHEET ......................................................................................................................... II

PROJECT EVALUATION SHEET ................................................................................................................... III

DECLARATION .................................................................................................................................................. VI

FACULTY CERTIFICATE ............................................................................................................................... VII

ACKNOWLEDGEMENT ................................................................................................................................. VIII

ABSTRACT .......................................................................................................................................................... XI

CHAPTER 1:INTRODUCTION

1.1 INTRODUCTION ................................................................................................................................ 1 1.2 DEFINITION OF ISLAMIC BANKING ............................................................................................. 3 1.3 HISTORY OF ISLAMIC BANKING ............................................................................................................. 4

1.4 ORIGIN OF ISLAMIC BANKING ................................................................................................. 4

1.5 MAJOR SIMILARITIES & DIFFERENCES BETWEEN ISLAMIC & CONVENTIONAL FINANCIAL SYSTEMS…....6

1.6 IMPACT OF ISLAMIC BANKING ON ECONOMIC GROWTH......................................................................12

1.6.1 DEFINITION AND IMPACT OF MURABAHA.............................................................................................13

1.6.2 DEFINITION AND IMPACT OF MUSHARAKAH........................................................................................13

1.6.3 DEFINITION AND IMPACT OF MUDARABAH.........................................................................................14

1.6.4 DEFINITION AND IMPACT OF IJARAH (LEASING)...................................................................................14

1.6.5 DEFINITION AND IMPACT OF ISTISNA...................................................................................................15

1.6.6 DEFINITION AND IMPACT OF SALAM....................................................................................................15

1.7 RESEARCH QUESTIONS...........................................................................................................................17

1.8 RESEARCH OBJECTIVES..........................................................................................................................17

1.9 SIGNIFICANCE TO STUDY.......................................................................................................................17

1.9 SCHEME OF THE STUDy.............................................................................................................18

CHAPTER 2:LITERATURE REVIEW……………………………………………………………………………………………………….…….19

2.1 BACKGROUND……..……….………………………………...………………………………….….19

2.2 PREVIOUS LITERATURES….………………………………………………………..………………………………………19

CHAPTER 3:RESEARCH METHODOLOGY ............................................................................................... 26

3.1 TYPE OF RESEARCH .................................................................................................................. 26

3.2 RESEARCH APPROACH ............................................................................................................. 26

3.3 RESEARCH METHODOLOGY ................................................................................................... 26

3.4 SOURCE OF DATA .......................................................................................................................... 26

3.5 POPULATION .................................................................................................................................... 26

3.6 SAMPLE ............................................................................................................................................. 26

3.7 SAMPLING METHOD ...................................................................................................................... 26

3.8 SAMPLING TECHNIQUE ................................................................................................................. 26

3.9 LIMITATIONS.........................................................................................................................26

CHAPTER 4:DATA ANALYSIS AND INTERPRETATION ........................................................................ 27

4.1 BACKGROUND ........................................................................................................................................ 27

4.2 TABLE 1: MURABAHA IN ISLAMIC BANKS OF AFGHANISTAN ....................................................... 28

4.3TABLE 2: IJARAH IN ISLAMIC BANKS OF AFGHANISTAN .................................................................. 28

4.4TABLE 3: MUSHARAKAH IN ISLAMIC BANKS OF AFGHANISTAN .................................................... 30

X

4.5TABLE 4&5: MUDAREBAH IN ISLAMIC BANKS OF AFGHANISTAN ............................................... 31

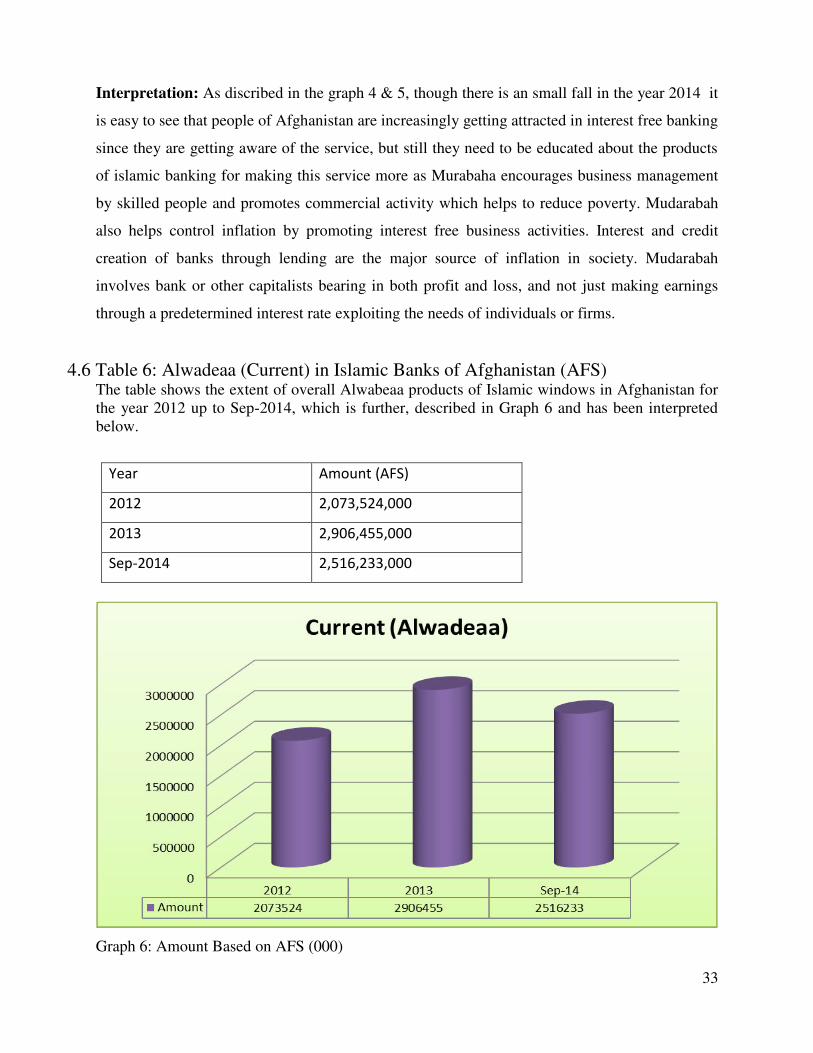

4.6TABLE 6: ALWADEAA IN ISLAMIC BANKS OF AFGHANISTAN.......................................................... 33

4.7TABLE 7: FINANCE + INVESTMENTOF ISLAMIC BANKS OF AFGHANISTAN .................................. 34

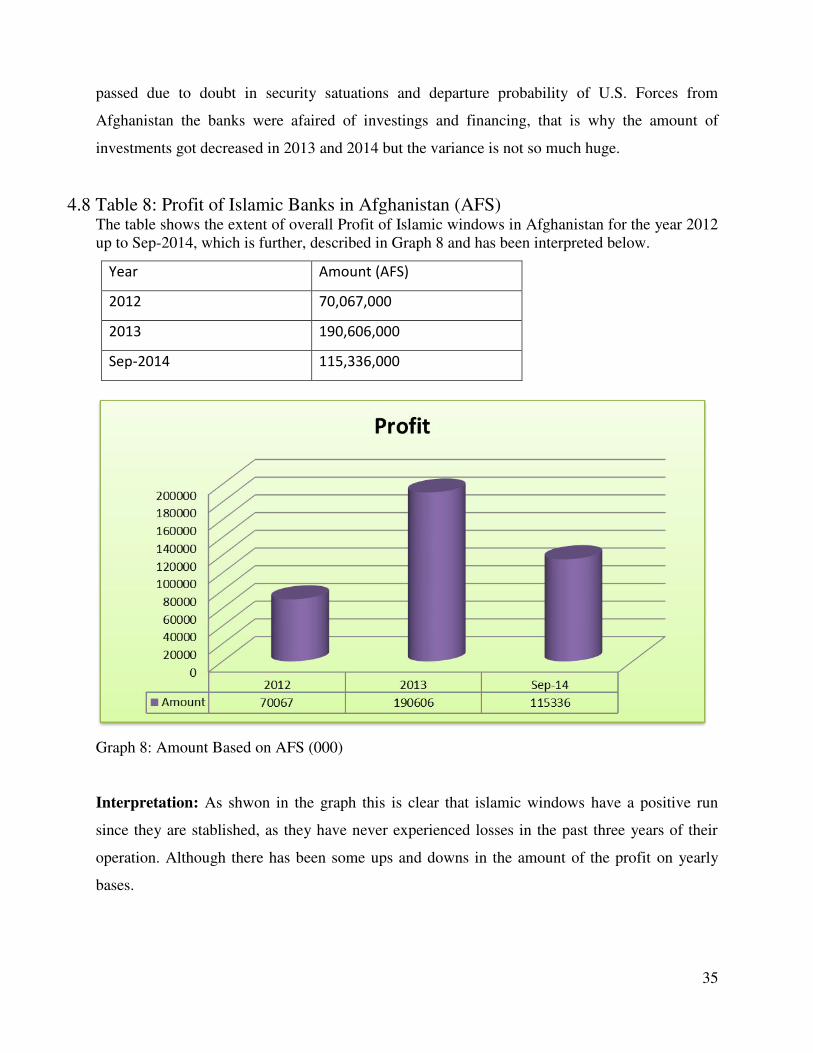

4.8TABLE 8: PROFITOF ISLAMIC BANKS OF AFGHANISTAN ................................................................. 35

4.9TABLE 9: ASSESTSOF ISLAMIC BANKS OF AFGHANISTAN ............................................................... 36

CHAPTER 5:CONCLUSION AND RECOMMENDATIONS ....................................................................... 37

5.1 CONCLUSION ................................................................................................................................... 37

5.2 RECOMMENDATIONS FOR FUTURE GROWTH .............................................................. 39

5.3 BIBLIOGRAPHY ................................................................................................................................ 39

END PAGE SIGN AND STAMP ....................................................................................................................... 40

XI

Abstract

The purpose of this study is to conduct an overview on Islamic modes of financing” while sub-

objectives are to know the main Islamic modes of financing currently applicable in Afghanistan, to

know the current statistics about Islamic modes of financing of Islamic banks in Afghanistan, How to

compare and investigate the efficiency of Islamic banking with conventional banks? It indicates that

Islamic banking system has in the terms of assets; deposit, financing and other activities have grown

gradually in our country. The study shows the measurement, technical and cost efficient that are using

by Islamic banking system. The study indicates that efficiency of Islamic banking system has been

increased, however the conventional banks are still stable, and however the efficiency of Islamic

banks is still lower than conventional bank. In Afghanistan, All banks operate as per compliance of

rule and regulation of DA Afghanistan Bank, they are allowed to offer both Islamic and conventional

scheme. This study will help the readers to find Islamicaly acceptable financial products which can

help them to be more financially sustainable, the study covers the definition of all the products

through which Islamic banks are operating, and the impact of each on the economic growth as well.

Further it discovers the previous study or literatures of deferent scholars and researchers. and after the

data analysis done in chapter four it is concluded that the modes of financing which are currently in

practice by Islamic windows of Afghanistan are: Murabaha, Ijarah, Musharakah, Mudarebah, and

Alwabeaa, further data analysis from year 2012 until 2014 shows that there is an increase of 67% in

Murabaha , a decrease of 2.50% in Ijarah, a decrease of 19.54% in Musharakah, a decrease of 1.12%

in Mudarebah, an increase of 21.35% in Alwadeaa and a decrease of 10.2% in Finance + Investments

of the Islamic Banks in Afghanistan compared to the year 2012. Further it is concluded that overall

banks have been in profit constantly during the years of 2012, 2013, 2014 and according to analysis

there has been an increase of 64.61% in profit of year 2014 compared to 2012, and that none of the

banks in Afghanistan are full pledge of Islamic Banking but Islamic Windows. Finally, it can be

concluded that Islamic finance has great potential to become a key instrument in project financing and

to play a major role in the banking industry. Furthermore It is recommended to permit the licensing of

Islamic banks rather than Islamic windows, to permit the licensing of specialized Islamic financial

institutions such as Mudaraba banks, Murabaha banks and Musharaka banks, to introduce the Islamic

insurance in Afghanistan to reduce the risk of Islamic financing, And Finally, it is recommended

that use of Islamic finance principles for public sector financing needs more attention, and ensure that

proper procedures for good corporate governance, transparency and ensuring Shariah compliance are

in place, it could be helpful in ensuring fiscal discipline and thus giving a just basis for monetary

management.

1

CHAPTER ONE

INTRODUCTION TO THE STUDY

1.1 Introduction:

Can we imagine a world without banks? In the past, banks focused on loans, deposits, debits,

and credits. Now, due to dramatic changes in the world economy, banking is a far more

complex business. On a daily basis, the industry must deal with margin pressures,

consolidation, and technological and marketing challenges, not to mention unforeseen

financial and political crises. However, with cash and capital, banks are positioning

themselves to succeed in the future, while coping with regulatory compliance, global

competition, and financial and operational risk. This provides an overview of the Islamic

banking industry. This section will be a brief introduction to the Islamic banking industry's

value chain, business model, and trends. Second, examines the business and regulatory issues

and challenges facing of the Islamic banking industry. Third this research will address the

issues that will play a significant role in the Islamic banking and how may increase their

ability to participate in economic growth of Afghanistan, Finally this will look at some of the

successful strategies that leading banking companies are applying. Target Audience

=Consulting houses, corporations, and small-to-medium-sized enterprises that sell products

or services to other sectors and industries; companies looking for knowledge and key

business information about Islamic banking industry.

Banking and finance are part of economics or the economic system. As indicated that all

economic and financial contracts in the frame work Islamic finance have to conform to the

Shariah rules with the objective of helping to achieve the wellbeing of people in the worldly

life as well as in the hereafter. Hence studying economics is important for the dual purpose

of having better sustenance and the religious imperatives. The sources of rules dealing with

economic aspects of human beings are the Holy Quran and Sunnah of his last messenger

2

Mohammad (Pbuh), in addition to the Quran and Sunnah, Ijma Qiyas and Ijitihad provide a

hierarchical framework of sources of rules governing Islamic economics and finance.

Many people may think that Islamic banking is for the Muslim only and that Islamic banking

is a gateway to the significant wealth amassed by the oil-producing countries in the Gulf. Mr.

Yahi Abdul Rahman mentioned in his book that is not true that‘s why he wrote his book by

the name Art of Islamic banking and Finance. The Islamic financial system has a centuries-

old history. As noted by Chapra and Khan (2000), from the very early stage in Islamic

history, Muslims were able to establish a financial system without interest for activating

resources to finance productive activities and consumer needs. The system worked quite

effectively during the heyday of Islamic civilization and for centuries thereafter.‘ However,

as the centre of economic gravity shifted over the centuries to the Western world, Western

financial institutions (including banks) became principal and the Islamic tradition remained

undeveloped. As being a Muslim, my personnel experience, dealing with different banks in

Afghanistan that I have studied make me interested to explore my experience, therefore

always questions raised on my mind, whether Islamic Banking is Shariah based or Shariah-

compliant? What are the major difference between conventional banking and Islamic

banking and what will be the impacts of Islamic banking on the economy of Afghanistan?

Islamic banking is all about Riba/ribit free banking or a new brand of banking and finance

services.

The purpose of this study shows that how Islamic banking works? How to compare and

investigate the efficiency of Islamic banking with conventional banks? It indicates that

Islamic banking system has in the terms of assets; deposit, financing and other activities have

grown gradually in our country. The study shows the measurement, technical and cost

efficient that are using by Islamic banking system. The study indicates that efficiency of

Islamic banking system has been increased, however the conventional banks are still stable,

and however the efficiency of Islamic banks is still lower than conventional bank. In

Afghanistan, All banks operate as per compliance of rule and regulation of DA Afghanistan

Bank, they are allowed to offer both Islamic and conventional scheme.

Now we can see that Islamic banking system has been accepted in universes. We noticed that

economists have been debate the impact of religion on economic performance for many

years. Should we mix mixed economics with religion? And it is a significant question these

days, more specifically; can Islam be helpful in economic growth? Or it is a drag on

3

economic growth? Focusing on finance is the most strategic part of any economic system.

Most of scholars have blamed the relative poverty of Muslims today on their religious

beliefs, but Marcus Noland, a well-known economist maintains that this long-standing idea is

wrong. This is not in their inherent that Muslims have to perform poorly in the societies.

Islam promotes growth and deals with the creation of wealth. The Islamic economic system

is different from the other systems only to the extent of ownership and distribution of

resources among the factors of production and various groups of society. This is a well-

defined role of the government to ensure that injustice is not done to any of the individuals ,

parties or groups in fact Islamic financing can promote a balance between the social and

economic aspect of human society .the income distribution and poverty aid issues can be

effectively address while capitalism has not been able to address. The principles laid down in

the Holy Qur‘an and the Sunnah of the prophet Mohammad (PBUH), significantly played a

strategic role in the development of Human society from the second half of the seventh to the

tenth century AD.

For the smooth and proper functioning of the banking and finance sectors, governments and

regulators should be obliged to perform an effective overseeing role to ensure that market

forces and different stakeholder do not exploit one another. For justice, fairness and the

longer term health of the system, they have to ensure that monetary growth is adequate and

not excessive or deficient.

1.2 Definition of Islamic Banking:

Islamic banking is banking based on Islamic law (Shariah). It follows the Shariah, called fiqh

muamalat (Islamic rules on transactions). The rules and practices of fiqh muamalat came

from the Quran and the Sunnah, and other secondary sources of Islamic law such as opinions

collectively agreed among Shariah scholars (ijma‘), equivalence (qiyas) and personal

reasoning (ijtihad).

Islamic banks obey to the concepts of Islamic law. This form of banking turns around several

well-established principles based on Islamic standards. Islamic finance is ruled by the

Shariah, which prohibits interest and instructs that income must be derived as profits from

shared business risk rather than guaranteed return. These banks, which neither charged nor

paid interest, invested mostly by engaging in trade and industry, directly or in partnership

4

with others, and shared the profits with their depositors. Therefore, they functioned

essentially as saving investment institutions rather than as commercial banks.

1.3 History of Islamic Banking:

During the Islamic Golden Age, early forms of capitalism markets were present in the early

Islamic kilafath, where an early market economy and an early form of mercantilism were

developed between the 9th-12th centuries. The Islamic Financial sectors, which are includes,

Islamic banks, Islamic Windows, Islamic non-banking financial institutions , Islamic

insurance , Islamic capital markets, Fund management institutions and Islamic Mortgage

companies.

The first Islamic institution in Malaysia was the Muslims Pilgrims Savings Corporation set

up in 1963.The first modern experimentation with Islamic banking was undertaken by

Ahmad El Najjar, in the Egyptian civic of Mit Ghamr in 1963. The Nasir Social Bank,

incorporated in Egypt in 197l, was acknowledged an interest-free commercial bank. The

Islamic Development Bank (IDB) was established in 1974 by the Organization of Islamic

Countries (OIC), but it operations are free of interest and are openly based on Shariah

principles. The evolution of the interest free banking concept to the 1970s when economics

of Arab countries had started experiencing huge financial benefits from price hike in the

petroleum products. In the seventies, a number of Islamic banks, came into reality in the

Gulf, e.g., the Dubai Islamic Bank (1975) the first modern commercial Islamic Bank, the

Faisal Islamic Bank of Sudan (1977), the Faisal Islamic Bank of Egypt (1977), the Bahrain

Islamic Bank (1979), and the Philippine Amanah Bank (PAB) was established in 1973,

operates two windows for deposit transactions in commercial and Islamic.

1.4 Origin of Islamic Banking (Shariah Compliant Vs Shariah Based products):

Shariah is defined as Islamic law or Law of Allah. It shows one of many ways that humanity

strives to harmonize and maintain internal and external belief systems in an holistic approach

to life. Hence Shariah covers not only religious rituals, but also many aspects of day-to-day

life, politics, economics, banking, business or contract law, and social issues.

5

The authority of Shariah is drawn from two primary sources. The first major source is the

specific guidance in the Holy Quran, and the second source is the Sunnah, literally the

―Way,‖ as in the way that Prophet Muhammad (pbuh) lived his life. Shariah law can be

broadly divided into two main sections; the acts of worship or known as al-ibadat and the

human interaction or known as al-mu‘amalat which includes financial transactions,

endowments, laws of inheritance, foods and drinks, judicial matters and others.

Shariah based products and services are the products and services that straightly derived from

the primary sources of Islamic laws such as the Qard‘al-hassan (benevolent loan).

Shariah based products and services are said to be originated during Prophet‘s period. These

products and services have undergone the process of cleansing where any prohibited

elements were removed by Prophet Muhammad (pbuh) such as al-bay‘ (trade), mudarabah

(profit sharing), musyarakah (joint venture, profit and loss sharing),murabahah (cost

plus), and Ijarah (leasing).

On the other hand, Shariah compliance products and services are the products and services

that comply or obey to the requirements to the Shariah itself. The good example would be

the Sukuk (Islamic bond) that is invented from the application of rules from Shariah based

products. Therefore, it is permissible and complies to the requirements of Shariah. Shariah

compliance products and services are also can be said as the modern day products and

services after Islamisation of it.

Shariah based also refers to the desired objectives of the Shariah (known as the maqasid

shariah) when determining a hukm (rules) aimed at the protecting human maslahah (public

interest). Thus, Shariah based products and services like mudarabah are aimed to encourage

the entrepreneurship among public and to maintain risk-reward relationships in a just

manner. The mudarabah principle also implies to recognize same and equal ability to

undertake responsibility and to have full authority to act on behalf of the other and are jointly

and severally liable for the liabilities of the partnership business.

However, the Shariah compliance products and services focusing on what it is needed to

make the products and services provided in line with the permissibility in Islam.

6

Therefore, the products and services must not have any elements of riba (usury), maisir

(gambling), gharar (excessive uncertainties), excessive speculations, haram (impermissible

elements like pork) and others.

Shariah based products and services are also the products from the full-fledged Islamic

financial institutions or banks. However, for the Islamic products and services provided by

the conventional banks through Islamic windows are known as the Shariah compliance

products and services.

1.5 Major Similarities & Differences between Islamic & Conventional Financial Systems

Islamic Financial Institutions (IFIs) are operating in the same society where conventional

banks are operating and perform all those functions which are expected from a financial

institution. IFIs are assisting business world by providing all the services required to run the

economy smoothly, however, the philosophy and operations are different. In this section I

will analyze the operations and products of IFIs in comparison with traditional conventional

banks. Any financial system is expected to assist in running the economy by providing the

following services grouped in two headings. First; Savings mobilization from savers to

entrepreneurs and Second; Provision of general utility services including transfer of funds,

facilitation in international trades, consultancy services, safekeeping of valuables, and any

other service for a fee.

There is no restriction on provision of such services by IFIs as for the service is not against

the Sharia. However there exists difference in mechanism of funds mobilization from savers

to entrepreneurs as described following. Savings mobilization consists of two phases i.e.

accepting deposits and extending financing and investments.

1.5.1 Deposits: Deposits are collected from savers under both type of institutions for reward

irrespective a bank is operating under conventional system or Islamic system. The difference

lies in agreement of reward.

Under conventional system reward is fixed and predetermined while under Islamic deposits

are accepted through Musharaka and Mudaraba where reward is variable. Under

7

conventional banking return is higher on long-term deposits and lower for short-term

deposits. Same is the practice in Islamic banking to share profit with depositors.

Higher weight for profit sharing is assigned to long-term deposits being available to bank for

investing in longer term projects making superior returns and lower weight for short-term

deposits which cannot be invested in long term projects. The only difference in conventional

and Islamic system lies in sharing of risk and reward. Under conventional system total risk is

born by the bank and total reward belongs to it after servicing the depositors at fixed rate

while under Islamic system risk and reward both are shared with depositors. Reward of

depositors is linked with outcomes of investments made by IFIs. Under Islamic financial

system only those IFIs will be able to collect deposits who can establish trust in the eyes of

masses hence leading to optimal performance by financial industry

1.5.2 Financing and Investments: The second phase in savings mobilization process is extension

of credit facility to business and industry for return. Both types of institutions (Islamic and

Conventional) are providing financing to productive channels for reward. The difference lies

in financing agreement. Conventional banks are offering loan for a fixed reward while IFIs

cannot do that because they cannot charge interest. IFIs can charge profit on investments but

not interest on loans. In conventional banking three types of loans are issued to clients

including short term loans, overdrafts and long-term loans. Islamic banks cannot issue loans

except interest free loans (Qarz e Hasna) for any requirement however they can do business

by providing the required asset to client. In following paragraphs I present the comparative

working of different products (financing scheme) of both systems.

Overdrafts/Credit Cards etc.: Conventional banks offer the facility of

overdrawing from account of the customer on interest. One of its form is use of credit

card whereby limit of overdrawing for customer is set by the bank. Credit card provides

dual facility to customer including financing as well as facility of plastic money whereby

customer can meet his requirement without carrying cash. As for facility of financing is

concerned that is not offered by Islamic banks except in the form of Murabaha (which

means IFI shall deliver the desired commodity and not the cash) however facility to

shop/meet requirement is provided through debit card whereby a customer can use his

card if his account carries credit balance. Under conventional banking a customer is

charged with interest once the facility availed however under Murabaha only profit is due

8

when the commodity is delivered to the customer. Furthermore in case of default

customer is charged with further interest for the extra period under conventional system

however extra charging is not allowed under Murabaha. International Journal of Business

and Social Science Vol. 2 No. 2; February 2011 170 Third under conventional system

customer can avail the opportunity of rescheduling by entering into a new agreement to

pay interest for extended period which is not the case under Murabaha. IFIs can claim

only the original receivable amount agreed in initial contract. Another practical issue

under Murabaha is how to deal with intentional defaulters. Different options are lying

with IFIs including to blacklist the defaulter for any further financing facility, to stipulate

in the contract that in case of default all installments will be due at once, to stipulate in

the contract a penalty shall be imposed but the same shall not form income of IFIs rather

it will go in charity (Usmani, 2002).

Short term loans: Short term and medium term loans are provided to customer to

meet working capital requirements of firm by conventional banks. Working capital is

required by firms to invest in inventories and accounts receivables and meet the expenses.

As for inventory investment is concerned that is provided by Islamic banks through

Murabaha. As for meeting of day to day expenses of business is concerned financing is

provided through participation term certificates where by profit of a certain period (e.g.

quarter, six month, one year) is shared by IFIs on prorate basis. However financing

through participation term certificates is not as easy as a short term loan from

conventional bank due to risk involved for IFIs in the transaction. Firm seeking short-

term facility from IFIs has to prove the survival of the project/business to the satisfaction

of investor. For meeting the working capital requirements of nonprofit organizations to

date there is no arrangement under Islamic financial system. Personal consumption loans

are also not issued by IFIs however any individual of sound financial position can acquire

anything for his personal use under Murabaha financing whereby a certain percentage of

profit is added on cost by IFIs. Murabaha financing is very useful for short to medium

term financial requirements of business/nonprofit organizations and individuals.

Murabaha financing is asset based financing and anyone can request to an IFI for

provision of an asset generally used for Halal (lawful) purposes. By default under Islamic

financial system IFIs cannot lend cash for interest (only exception is Qarz e Hasna—

Charity loan). One of the features of Murabaha is in case of delay in payment by

9

customer IFI cannot ask for extra amount as time value of money like conventional

banks. However penalty is imposed on defaulter if stipulated in original contract of

Murabaha duly signed by the customer but same cannot be included in the income of IFI.

This penalty must be spent for charitable purposes. Under Murabaha scheme of financing

facility is linked with assets which leads to economic stability and creates linkage

between real and financial sector. It is not zero sum game because utility is created

through services and products and not by mere building the blocks of wealth through

dealing in paper money. Although Murabaha is being used by IFIs successfully and have

succeeded in meeting short to medium term requirements of firms by providing a

successful replacement of conventional loans yet certain differences exist in both type of

financing. First is one cannot get cash under Murabaha. Second asset is purchased by IFI

initially then transferred to customer hence IFI participate in risk. Third refinancing

facility is not available under Murabaha. Fourth in case of default price of the commodity

cannot be enhanced however penalty may be imposed if stipulated in original contract of

Murabaha however same cannot be included in income of IFI. Fifth only those assets can

be supplied by IFIs under Murabaha whose general and/or intended use is not against the

injunctions of Sharia (e.g. supply of a machine to produce liquor)

Medium to long term loans: Medium to long-term loans are provided for

purchase or building of fixed assets by firms to expand or replace the existing assets.

Under Islamic financial system requirement of firms and individuals are fulfilled through

Murabaha, Bai Muajjal and Istasna (discussed Further). Another financing option for

long-term financing is profit sharing under Musharaka and Mudaraba. Although

financing under Murabaha, Bai Muajjal and Istasna is very much look like conventional

loans with the only difference of provision of asset and not cash to client however

differences exist in the contracts which alter the nature of risks and returns. Financing

under Musharaka and Mudaraba is challenging for IFIs and firms as well. Under Sharia

based financing schemes firms have to prove the viability/profitability of the

project/business to the satisfaction of IFIs to get the finance because risk of losing the

amount is involved.

Leasing: Leasing is relatively recent source of financing whereby usufruct of an

asset is transferred to lessee for agreed amounts of rentals. Under leasing ownership may

10

or may not be transferred. © Centre for Promoting Ideas, USA www.ijbssnet.com 171

Same facility is provided by IFIs under agreement of Ijara. Under Ijara asset is provided

to customer for use with out transfer of ownership for a specific period of time in

exchange for agreed rentals. Ownership of asset can be transferred to customer through

mutual agreement at the completion of lease term. All ownership risks are born by IFIs

during Ijara tenure. Certain differences exist in the transaction under both systems. First

is rental under Ijara are not due until asset is delivered to the lessee for use. Second

additional rent cannot be demanded in case of default except a penalty (if stipulated in

original contract of lease) which is not the income of IFI. Third during period of major

repair rent cannot be demanded by IFI. Fourth if asset is lost or destroyed IFI cannot

claim further installments hence all risks of ownership are born by IFI.

Agricultural Loans: Agricultural loans include both types of loans short-term as

well as long-term. Short-term loans are required by farmers for seeds and fertilizers and

long-term loans are required to develop additional lands and purchase of equipments.

Normally farmers return these loans after selling the finished crops. Conventional banks

are providing credit facility by charging interest. Same facility is provided by IFIs to the

farmers under Bai Slam, Bai Murabaha Musharaka and Mudaraba. Under Bai Salam cash

is provided to farmers for purchase of seeds and fertilizers however this is not loan rather

purchase of finished crops to be delivered by farmers. For purchase of equipments

Murabaha facility is used and for development of additional land Musharaka and

Mudaraba is used by IFIs. To get finance for land development farmers have to convince

the IFIs about profitability of the venture due to risk involved in the transaction.

House financing: Housing finance/Mortgages is the more secured form of

financing for both conventional banks and IFIs. Under conventional system loan is

provided for interest while under Islamic financial system facility is provided through

diminishing Musharaka. Under diminishing Musharaka house is purchased jointly by IFI

and customer. IFI rents out its share in property to customer for an agreed amount of rent.

Share of financier is divided in units of small denomination. Customer pays the

installments to IFI consist of rentals plus purchase price of a unit. Stake of customer in

property is increasing while of IFI is decreasing with payment of every installment.

Finally with the payment of last installment stake of IFI reaches to zero and property is

11

transferred in the name of customer. Diminishing Musharaka model can help out in

avoiding the real estate crisis because when market value of property decreases both IFI

and customer suffers according to their share in property and whole burden is not shifted

on customer alone

Investments: In order to maintain liquidity conventional banks have many

avenues including government securities, shorter term loans and money at call and short

notices, leasing companies‘ bonds, investment in shares etc. Interestingly mandatory

reserve maintenance by conventional banks with central banks is also rewarded in the

form of interest. Conventional banks can also create liquidity by issuing the bonds against

their receivables. Commercial banks are also protected by central bank by providing

liquidity in rainy days for interest. Interbank deposits are also rewarded in the form of

interest by commercial banks. For IFIs avenues are very limited to create required

liquidity at the same time to earn some revenue by investing in short term and liquid

securities. IFIs cannot invest in government securities, short term loans, bonds and

money at call and short notices because of interest based transactions. Mandatory reserve

with central bank is maintained by IFIs but they are not rewarded like conventional

banks. Looking towards central bank in rainy days to maintain liquidity is also not as

straightforward due to interest demand of central bank. IFIs cannot demand interest on

interbank deposits. As for investment in market able securities are concerned again IFIs

are not free to invest in any equity security due to two reasons. First Halal business of the

underlying firm is required. Second financial operations of underlying firm should be

interest free. Keeping in view the dominance of conventional banking and existing

business practices one can conclude safely that a very negligible number of firms meet

both conditions. IFIs can invest only in those securities which are declared Sharia

compliant securities through filtering of Sharia compliance criteria. International Journal

of Business and Social Science Vol. 2 No. 2; February 2011 172 Listing here the major

conditions to qualify a security as Sharia compliant is worth mentioning as follow.

Meeting of following tests is required to declare a security as Sharia compliant. First the

core business of the company should be Halal (not prohibited by Islamic Law such as

liquor, pork and pornography etc). Second illiquid assets should be equal to 20% of total

assets of the company. Shares of a company merely dealing in liquid assets are not Sharia

compliant hence IFIs cannot invest. Third ratio of all interest based debts including

12

preferred stock should be less than 40% of total assets of the company. Fourth ratio of

non-Sharia compliant investments to total assets of the company should be less than 33%.

Fifth revenue from non-compliant investments should be less than 5% of total revenue of

the company and even then IFIs are required to purify their earnings by spending this

non-compliant revenue as charity. Finally market price per share should be greater than

the net liquid assets per share. Recently IFIs have created an avenue to meet their

liquidity requirement in the form of Skuks (Islamic Bonds) whereby servicing is fixed

like conventional bonds however such types of Skuks can be issued against Ijara

receivables. Under Ijara Skuks initially asset is given on rent to the customer for an

agreed period and rentals while ownership remains with IFI. To meet liquidity

requirements IFI issues Skuks (bonds) to the investors equal to the value of asset, hence

ownership of the asset is transferred to Skukholders. While it is known the rentals of the

asset so the return on investment is predetermined and known with certainty to the

investors. Skuks of Murabaha cannot be sold except at par being sale of loans. Other

types of Skuks (Musharaka etc) are not carrying fixed return although tradable in

secondary security market. Underlying principle in issue of Skuks is that illiquid assets

should dominate in the portfolio against which Skuks are issued. Under Islamic financial

system Skuks are ownership certificates and not mere debt securities hence all risks and

rewards are shared by Skukholders.

1.6 Impact of Islamic Banking on Economic Growth:

Islam encourages the earning of profit as profit represents successful business dealing and

creation of new wealth. Interest on the other hand is a cost that is in place regardless of the

outcome of business operations. If business losses are experienced, there may not be real wealth

creation. Social justice requires that lenders and borrowers share both profit and loss in an

equitable manner and that the method of collecting and distributing wealth in the economy is

fair and represents true productivity. To achieve these goals, there are several modes of finance

used in Islamic banking which are very helpful and will have a good impact on the economic

growth of any country specially Afghanistan where people are more likely to have interest free

banking. And they are discussed below:

13

ISLAMIC MODES OF FINANCING

1.6.1 Definition and Impact of Murabaha

A kind of ―cost-plus‖ transaction in which the bank buys the asset then immediately sells it to the

customer at a pre-agreed higher price payable by installments. This facility is often used in the

way that conventional banking customers might seek a loan when buying property.

The most preferred method of financing for many Islamic banks due to the simplicity of the

model. Or An Islamic financing structure, where an intermediary buys a property with free and

clear title to it. The intermediary and prospective buyer then agree upon a sale price (including

an agreed upon profit for the intermediary) that can be made through a series of installments, or

as a lump sum payment. Murabaha has no direct effect upon poverty reduction, but indirectly it

provides a good tool for an efficient deferred sale, providing business men the asset of its choice

and providing banks profit for the effort and risk that it tool. Murabaha has little effect on the

reduction of unemployment; there is no clear study on the effect of Murabaha on inflation.

1.6.2 Definition and Impact of Musharakah

This is a partnership, normally of limited duration, formed to carry out a specific project.

Participation in a Musharakah can either be in a new project, or by providing additional funds for

an existing one. Profits are divided on a pre-determined basis, and any losses shared in

proportion to the capital contribution. In this case, the bank enters into a partnership with a

client, in which both share the equity capital- and maybe even the management -of a project or

deal, and both share in the profits or losses according to their equity shareholding.

Musharakah encourages partnerships, also created jobs for many people in society, promotes

enterprise and partnership ventures, creating jobs in the country, and promotes business

enterprise culture in society and growth of skilled people. Musharakah has a strong effect on

controlling inflation and extent of baseless credit, promoting joint ventures without potent

investigations and research ensures business successes, not speculations. And it also decreases

available credit, which also reduces spending.

14

1.6.3 Definition and Impact of Mudarabah

"Mudarabah" is a special kind of partnership where one partner gives money to another for

investing it in a commercial enterprise. The investment comes from the first partner who is called

"rabb-ul-mal", while the management and work is an exclusive responsibility of the other, who is

called "mudarib. The rabb-ul-mal may specify a particular business for the mudarib, in which

case he shall invest the money in that particular business only. This is called al-mudarabah al-

muqayyadah (restricted mudarabah). But if he has left it open for the mudarib to undertake

whatever business he wishes, the mudarib shall be authorized to invest the money in any

business he deems fit. This type of mudarabah is called 'almudarabah al-mutlaqah" (unrestricted

mudarabah). Mudarabah is a very potent tool for removing interest from the society by providing

an interest free tool for skill utilization and it can especially help in mobilizing resources of the

society by employing them as a manager, while banks will provide the finance and also bear the

chances of profit and loss, which is absent in interest based financing for venture capital.

Mudarabah has a significant effect on reducing the unemployment in both the short and long run,

as it encourages business management by skilled people and promotes commercial activity

which helps to reduce poverty. Mudarabah also helps control inflation by promoting interest free

business activities. Interest and credit creation of banks through lending are the major source of

inflation in society. Mudarabah involves bank or other capitalists bearing in both profit and loss,

and not just making earnings through a predetermined interest rate exploiting the needs of

individuals or firms.

1.6.4 Definition and Impact of Ijarah (Leasing)

A form of Shariah law-compliant leasing involving the rights over the use of an asset under

which the bank buys the asset then leases it to the customer over a fixed period in return for a

pre-agreed monthly price. Provisions can be made for the customer to buy the asset at the end of

the agreed period. Thought needs to be given to issues such as the provision of insurance, as the

asset is effectively owned by the bank during the lease period.

Or

Ijarah is an operating lease whereby the bank will buy and lease out equipment required by the

customer for an agreed rental fee. The agreement does not include a promise that the leased asset

at the end of the lease term will be transferred to the lessee.

Ijarah is defined in Fiqh as a possession of a usufruct or benefits for consideration in the Islamic

Fiqh. This term is used to denote two things:

15

To employ the services of a person on wages given to him as consideration for his hired

services.

It relates to the rights of assets and properties. Here it means To transfer the rights of a

particular property to another person and exchange for a rent claim from him

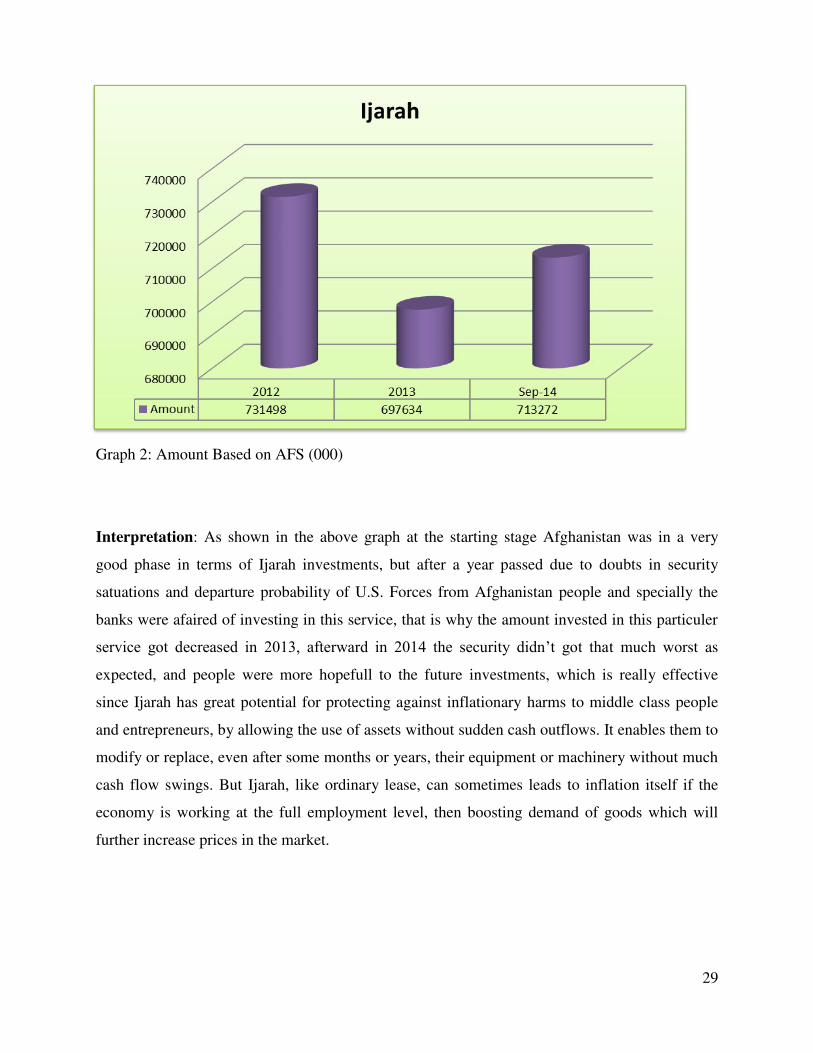

Ijarah has no direct effect upon poverty reduction and has a little effect on reducing

unemployment. However, it has great potential for protecting against inflationary harms

to middle class people and entrepreneurs, by allowing the use of assets without sudden

cash outflows. It enables them to modify or replace, even after some months or years,

their equipment or machinery without much cash flow swings. But Ijarah, like ordinary

lease, can sometimes leads to inflation itself if the economy is working at the full

employment level, then boosting demand of goods which will further increase prices in

the market.

1.6.5 Definition and Impact of Istisna

Istisna, another form of forward sales contract, is a contract whereby a party undertakes to

produce a specific thing which is possible to be made according to certain agreed-upon

specifications at a determined price and for a fixed date of delivery. This undertaking of

production includes any process of manufacturing, construction, assembling or packaging.

Sellers can then either create the asset themselves or subcontract, with buyers also having the

option of paying the entire sum due either in advance or as installments during the manufacturing

process. Istisna is especially useful in the housing sector, boosting the construction demand,

creating employment and wealth to society without harmful effects of interest. It has also good

effects on the reduction of unemployment by boosting construction and house building activities

in society. Istisna has a little effect on inflation control.

1.6.6 Definition and Impact of Salam

A kind of forward sales contract whereby the seller undertakes to supply some specific goods to

the buyer at a future date in exchange of an advanced price fully paid at spot. The contract of

Salam creates a moral obligation on the Salam seller to deliver the goods,. The Salam contract

cannot be cancelled once signed. Salam is very useful in reducing agricultural sector poverty

16

easily, by enabling the banks and farmers to contract with each other of the crops and to get

finance at an appropriate time, instead of usurious loans, which ultimately fails through the

compounding of interest. Salam also has great potential in reducing rural sector unemployment

and reduces trend towards development, by enabling farmers and agriculturists to work. Salam

engages them at villages and towns, thus decreasing the unemployment problem. This generates

agricultural and rural sector development and eventually more income for these poor people.

Salam has a great effect on reducing inflation, where food stuff has reached its peak prices, the

main way it cuts inflation is through ensuring increased aggregate supply and reduce food

product fall by use of pesticide and fertilizers at appropriate times, boosting the yield of land and

farms to much extent.

The effect of a bank‘s activity on economic growth will therefore depend on which

modes of finance and investment the bank undertakes most, and how much each one of

these modes contributes to economic growth. At present, fixed return modes of financing

are dominating usage by most Islamic banks – modes such as Murabaha and leasing.

Even though these are clearly distinguishable from interest-based modes, as transactions

are always done through real commodities, they do not yield the full benefits in terms of

promoting growth with equity which is expected of an Islamic financial system.

17

Specialists in Islamic financial theory had counted on Islamic banks to provide a

significant amount of profit-sharing finance, which would have had economic effects

similar to direct investment and would have produced a strong economic development

impact. However, due to practical difficulties, profit-sharing finance has remained

negligible in the operations of Islamic banks (Al Hallaq, 2006)

1.7 Research Questions:

The research questions for this study are formulated as following:

What are the main Islamic modes of financing in Islamic banks?

What are the current statistics about Islamic modes of financing of Islamic banks in

Afghanistan?

1.8 Research Objectives:

The main objective of this study is ―To conduct an overview on Islamic modes of

financing‖ while sub-objectives are formulated as following.

To know the main Islamic modes of financing currently applicable in Afghanistan.

To know the current statistics about Islamic modes of financing of Islamic banks in

Afghanistan.

1.9 Significance to Study:

This study will help the readers to find Islamicaly acceptable financial products which

can help them to be more financially sustainable. And as nowadays Islamic banking is

one of the fastest growing sectors of the financial market place, largely driven by the new

wealth of Middle East and by the need for Muslims.

The readers can develop their information about the positive impacts of Islamic banking

on the countries which has launched this sector during past 20 years and what benefits

these countries has driven from this sector, so through that the readers can realize that

Islamic banking is not only for Muslims, everyone can be part of this sector and everyone

can be familiar with the financial rules of Islam and Islamic banking.

This study is also effective for my own personal experience dealing with different banks

in Afghanistan, this research will help me to improve my ability and skills and make

personal career as a good banker.

18

This study indicates that Islamic banking efficiency has grown globally over the years, as

good and big projects which might be turned down by conventional banks due to lack of

guarantee and security would be financed by Islamic banks on profit sharing basses and

this study indicates that Islamic banking can play a effective role in stimulating

economic growth.

1.10 SCHEME OF STUDY

This study addresses to Islamic Banking, Origin of Islamic Banking, Shariah Compliant

vs Sharia Based Products, the main differences between Conventional Banking and

Islamic banking, different products of Islamic Windows, the Modes of Financing of

Islamic Banks in Afghanistan (Research Question and Research Objectives), the previous

literatures review, and the data analysis of Islamic Banks‘ modes of financing all over

Afghanistan, data of which are collected from central bank of Afghanistan (Da

Afghanistan Bank).

19

Chapter Two

Literature Review

2.1 Background

The aim of this chapter is to present a vital review of the literature which adds to the Islamic

banking theory.

2.2 Previous literatures

Abdouli, A. (1991). Access to finance and collaterals: Islamic Versus Western

Banking. Journal of KAU: Islamic Economies. vol.3, pp. 55-62

Abdouli has explained that maximizing of profitability is not the only concern for Islamic

banking institutes and the principles that Islamic banks are based on are deeply integrated with

ethical and moral values. They also state that Islamic Banks do not depend on tangible collaterals

and lead to a better distribution of income, allowing access to finance for those in poorer classes

of society, and resulting in greater benefits for social justice and long term growth. In contrast

with conventional methods, Islamic financing is not centred only around creditworthiness but

rather on the worthiness and profitability of a project, and therefore recovering the principle

becomes a result of profitability and worthiness of the actual project. The nature of Islamic

banking operations are directly affected by the success or failure of client enterprises as a result

of the profit-loss-sharing process

2.2 Hassan. K, Zaher. T, (2001), A comparative Literature survey of Islamic Finance and

Banking, Institutions and Instruments 10(4): 155-199.

Hassan. Ka, Zaher explained: Shari‘a supervision by a qualified Shari‘a advisory board is an

essential component of the Islamic financial structure. The board consists of prominent scholars

who are well versed in Islamic law that relates to transactions and business dealings. The board

is supposed to be independent and screens investment strategies, implementation, monitoring and

reporting.

The second main pillar known as screening, involves the activities of including or excluding

publicly traded securities from investment portfolios or mutual funds based on the religious and

20

ethical conditions of the Islamic law. Some businesses are not in keeping with Islamic laws and

the stocks from such companies are therefore excluded.

Community based investment programs provide capital to those who are unable to access it via

conventional channels. These community-based investments allow people to improve standards

of living and assist them to develop small businesses and create jobs.

The practices and activities of Islamic banks reflect the environment in which they are based.

There are strong retail operations in Iran and Saudi Arabia. In the secular societies of northern

Africa, Islamic banks compete on the quality of products rather than on religious grounds. In

Kuwait, financing has focused on the petroleum sector and real estate investment and in the

United Arab Emirates, the emphasis is on trade and finance.

2.3 Dimitri.V and Yoon.C, Credit policies: Lessons from Japan and Korea”, World Bank

Research Observer, vol. 2, no.2, pp. 277 – 298.

According to the World Bank Research Observer (1996), commercial banks prefer to lend to

low-risk activities and are reluctant to finance high risk projects, even if such projects present

better investment opportunities. They are also less willing to finance small firms that don‘t have

satisfactory security.

In contrast, fostering serious economic development is a key objective of Islamic banks as they

seek to maximize social benefit. Islamic banks therefore work hard to overcome shortages and

difficulties to help the economy to progress to a higher stage of self-sustained development,

resulting in a favorable effect on socio economic harmony due to equal income distribution.

It has been widely claimed by development economists that policy and resource allocation is

strongly focused on large firms and that existing banking institutions prefer to grant credit

facilities to clients who are able to offer sufficient collateral security.

2.4 Chapra, M. (1992). The Role of Islamic Banks in Non-Muslim Countries. The Journal of

Muslim Minority Affairs. vol.13, no.2, pp.1-49.

Chapra, M. Explained: Profit sharing is more stable than the interest based system resulting in

prevention of fluctuations in rates of return. It has been pointed out that interest based debt

financing is a major factor in causing economic instability in capitalist economies.

The large number of economic ills, including poverty, social and economic injustice, inequalities

of income and wealth, economic instability and inflation of monetary assets are all in conflict

21

with the value system of Islam. It is the responsibility of the money and banking system to

contribute to the achievement of socio-economic development and hence eliminate such

economic ills. The principle goals and functions of the Islamic banking system include economic

well-being with full employment and maximum rate of economic growth, equal distributions of

income and wealth and as a result socio-economic justice, and the generation of sufficient

savings and their productive mobilization and stability in the value of money. Profit sharing is

more stable than the interest based system resulting in prevention of fluctuations in rates of

return. It has been pointed out that interest based debt financing is a major factor in causing

economic instability in capitalist economies.

2.5 Nedal El-Ghattis, (2009). Islamic Banking's Role in Economic Development: Future

Outlook. Pp. 2-7, and 16-21. Senior Lecturer Centre of Islamic Finance, Bahrain Institute

of Banking and Finance, Bahrain

Nedal El-Ghattis‘s research addressed the issues that will play a significant role in the future

outlook of Islamic banking and how may increase their ability to participate in economic

development, and how does the application of the profit-loss sharing scheme in Islamic banking

contribute to economic development.

According to El-Ghattis, the Islamic profit sharing concept helps to foster economic

development by encouraging equal income distribution and which results in greater benefits for

social justice and long term growth. And profit-loss sharing scheme improves capital allocation

efficiency as a return on capital depends on productivity and the allocation of funds is based on

the success of the project.

This profit-loss sharing scheme improves capital allocation efficiency as a return on capital

depends on productivity and the allocation of funds is based on the success of the project. And

believes that Islamic financial system is more stable than the conventional banking system due to

the elimination of debt financing. It also reduces inflation in the economy as the supply of

money is not permitted to go above the supply of goods. Islamic banks are less risky than

conventional banks as both investors and entrepreneurs share any risks that are involved in the

business.

22

2.6 Katherine Johnson, (2013). The Role of Islamic Banking in Economic Growth, Claremont

Colleges Scholarship, CMC Senior Theses. pp. 5-35

Katherine Johnson‘s researched to add to the literature by realistically analyzing the economic

growth determinative power of Islamic banks. Confirming pas research, Muslim popularity in a

population is found to be the most significant factor of the circulation of Islamic banks.

According to Katherine Johnson, Certain components of Islamic banking such as risk-sharing,

stability, and innovation are proven energizers of growth while others, including limited

liquidity, may be harmful to the economy. Therefore, elements of Islamic banking likely impact

economic growth; he has attempted to add to the literature on Islamic banks by realistically

investigating the factors of the circulation of Islamic banking, the effect of that circulation on

economic growth, and its impact on financial deepening. Furthermore, the effect of the

circulation of Islamic banking on the explanatory power of legal origin as a factor of growth and

financial deepening was tested. His finding is supported by previous evidence that Islamic

banking appears to be a complement to, rather than a substitute for, conventional banks

The research unveils two topics for further investigation and analysis. First, Islamic banking may

operate as a channel for the convergence process. Second, the degree to which Islamic banks

purify institutional environment, defined by legal origin, inconsequential is questionable in

aggregate data. This finding suggests the necessity for better measures of when Shariah laws are

strictly enforced and actually establish an alternate legal system. The results also show that the

effect of Islamic banking on financial deepening is dependent on the legal origin of the countries

in which it operates. Islamic banks are negatively correlated with financial system development

in countries of British legal origin and positively correlated in countries with French legal origin.

This outcome indicates that Islamic banks may be more beneficial to development of the

financial sector in French legal origin countries.

2.7 Dr. G. Shahul Hameed and Fayaz Ahmad (2010). Development of Islamic banking with

reference to UAE, pp.1-17

Dr. G.Shahul Hameed and Fayaz Ahmad‘s study analyzed the Islamic banking operations

currently practiced in Global banking system. This paper explains the important legal principles

of Islamic Banking, which includes a brief review of the current state of Islamic banking

development and provides the analysis of Islamic Banks with their acquired results. The paper

23

suggests a Global organization that would allow Islamic banks to develop in compliance with its

Islamic laws [shariah] principles.

According to Dr. G.Shahul Hameed and Faraz Ahmad, A key element of Islamic Finance is

division of reasonable rewards to the various factors of production. Islamic financial system

seeks system of fairness and flow of money into economy is guaranteed. Islamic Banking is a

system of business transactions that not only provides allowable (Halal) modes of transactions by

avoiding that which is revolting and objectionable, but also fosters moral, fair-haired and just

practices. They have focused on concept of Islamic banking, identifying need of Islamic banking,

basic principles of Islamic banking, importance and development likelihood of Islamic banking

in key markets, and surveying the growing literature on Islamic banking.

And they believe that Islamic banking has proved vital potential as a competitive and better

substitute against conventional banking system in many countries of the world.

While elimination of "Riba" or interest in all its forms is an important feature of the Islamic

financial system, Islamic banking is much more. Currently, two different approaches are

experienced towards the development of Islamic banking. First way experienced is to implement

Islamic banking on a country wide and on a broad basis. Second, way is to setup individual

Islamic banks in equivalent to the conventional interest based banks. It required support and

continue efforts to eliminate the interest (Riba) from the economy. Islamic Banking may be

viewed as a form of moral investing, or moral lending, except that no loans are achievable unless

they are interest-free. Its practitioners and clients need not be Muslims, but they must accept the

ethical precincts underscored by Islamic values.

2.8 Johansen (2011). Flow of Islamic Finance and Economic Growth-- an Empirical Evidence

of United Arab Emirates (UAE), JEL classification: O16, C32, pp. 1-12

Johnsen has analyzed empirically the relationship between the development of Islamic finance

system and growth of the economy in the United Arab Emirates (UAE). To document the

relationship between development of Islamic finance and economic growth, time series data

from 1990 to 2010 were used. He used Islamic banks‘ financing credited to private sector

through modes of financing as a proxy for the development of Islamic finance system and Gross

Domestic Product (GDP), Gross Fixed Capital Formation (GFCF), as indirect means for real

24

economic growth. The observed results show that there is a strong positive link between Islamic

banks‘ financing and economic growth in the UAE, which strengthens the idea that a well-

functioning banking system promotes economic growth. In this case, the development in the

Islamic financial sector acts as supply, leading to transfer of resources from the traditional, low-

growth sectors to the modern high-growth sectors, and to promote and motivate an innovative

response in these modern sectors. Furthermore, the results show that Islamic Banks‘ financing

has contributed to the increase of investment in UAE in the long term and in a positive way.

According to Johansen, The financial sector plays a growth promoting role, if it is able to direct

financial resources towards the sectors that demand those the most. When the financial sector is

more developed, more financial resources can be assigned into productive use, and more

physical capital gets formed, which will lead to economic growth. He believes that Islamic

finance theory promotes economic development through its direct link to the real economy and

physical transactions, its prohibitions against harmful products and activities, and its promotion

of economic growth and social justice. That means Islamic banks‘ financing and economic

growth move together in the long-run. It is proved that the UAE has benefited from strong

banking system.

He also found that the causality relation exist in the Islamic banks‘ financing to economic growth

in a unique direction from the development of financial system to economic growth, but not in

the opposite direction. The results also indicate that improvement of the Islamic financial

institutions in the UAE will benefit economic development, and it is critical in the long run for

the economic welfare, and also for poverty reduction. The results of study are quite significant as

it is one of the innovative studies of Islamic finance.

2.9 Hafas Furqani and Ratna Mulyany (2009). Islamic Banking and Economic Growth:

Empirical Evidence from Malaysia, pp. 1-16

Hafas Furqani and Ratna Mulyany have explained that Islamic financial system in Malaysia has

evolved as a sustainable and competitive component on the overall financial system as a driver

of economic growth and development. Central Bank of Malaysia (BNM) launched the financial

sector master plan which incorporated the 10 years master plan for Islamic banking that is aimed

at creating an efficient, progressive and comprehensive Islamic financial center for Islamic

banking and finance. And in term of economic growth, Malaysia has a remarkable record of

consistently high growth in the past three decades. The growth of GDP in real terms accelerated

25

to 5.3 percent in 2005. As a country slightly shifted toward industrial country, industrial sectors

and services contributed 80 percent to total of GDP of Malaysia. With total population 26.7