Agritourism in Colorado: The Visitors, the Economics and the Opportunities Dawn Thilmany & Martha...

26

Agritourism in Colorado: The Visitors, the Economics and the Opportunities Dawn Thilmany & Martha Sullins Colorado State University Extension Department of Ag & Resource Economics March 2007 Photo: Pat Martin Photo: Tammy Mattics Photo: Randy Mills Photo: Joel Boymel

-

Upload

robyn-mcdaniel -

Category

Documents

-

view

215 -

download

1

Transcript of Agritourism in Colorado: The Visitors, the Economics and the Opportunities Dawn Thilmany & Martha...

Agritourism in Colorado: The Visitors, the Economics and

the Opportunities

Dawn Thilmany & Martha SullinsColorado State University Extension

Department of Ag & Resource EconomicsMarch 2007

Photo: Pat MartinPhoto: Tammy Mattics Photo: Randy Mills

Photo: Joel Boymel

Growing Agritourism in Colorado

1. Understanding the landscape

Producer inventory, 2005 – Colorado Dept of Agriculture

Agritourism directory on-line, 2007 – Colorado Dept of Agriculture

Producer inventory, 2007 – Colorado Dept of Agriculture & CSU

Photo: Nat Coalson

Growing Agritourism in Colorado

2. Understanding Colorado’s agritourists” Consumer survey, 2007

– Colorado Dept of Agriculture & CSU

Photo: Karen Seim

3. Supporting businesses & communities 3 producer workshops (Steamboat, Akron) 2 scheduled workshops (La Junta, Cortez, Delta) Numerous community outreach presentations 4 fact sheets and more to come for tech. asst.

Growing Agritourism in Colorado

Photo: Mary Erlenborn

In Colorado, agritourism includes: Outdoor recreation (fishing, hunting, wildlife

photography, horseback riding).

Educational experiences (farm and cannery tours, cooking classes, wine tasting, cattle drives, farm work).

Entertainment (harvest festivals, corn mazes).

Hospitality services (farm and ranch stays, guided tours, outfitter services).

On-farm direct sales (u-pick operations, roadside stands).

Off-the-farm direct sales (farmers’ markets, county and state fairs, special events).

Photo: Carol Lauer

Photo: Tina Beedy

Photo: Susan Hickel

Photo: Jim Deeds

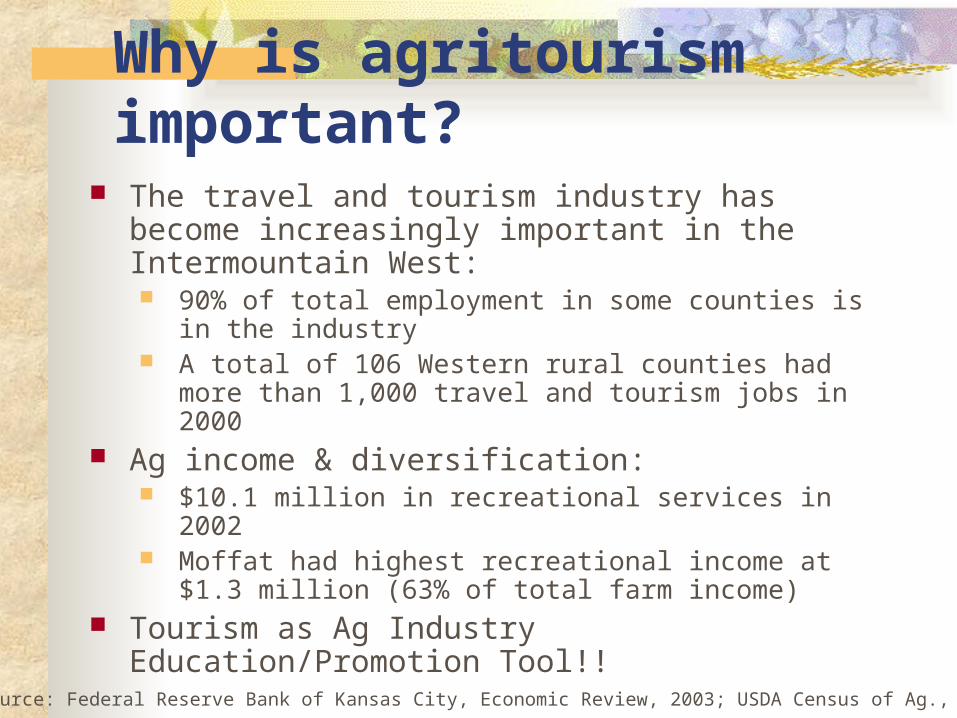

Why is agritourism important?

The travel and tourism industry has become increasingly important in the Intermountain West: 90% of total employment in some counties is in the

industry A total of 106 Western rural counties had more than

1,000 travel and tourism jobs in 2000 Ag income & diversification:

$10.1 million in recreational services in 2002 Moffat had highest recreational income at $1.3

million (63% of total farm income) Tourism as Ag Industry Education/Promotion

Tool!!Source: Federal Reserve Bank of Kansas City, Economic Review, 2003; USDA Census of Ag., 2002.

Targeting traveler segments

“Cluster” visitors by like characteristics Planning Mode of travel Activities chosen Expenditures, etc.

Easier to develop cohesive marketing strategies than for “average” traveler

We can define them…

….target those with greatest potential

…..and create recommendations

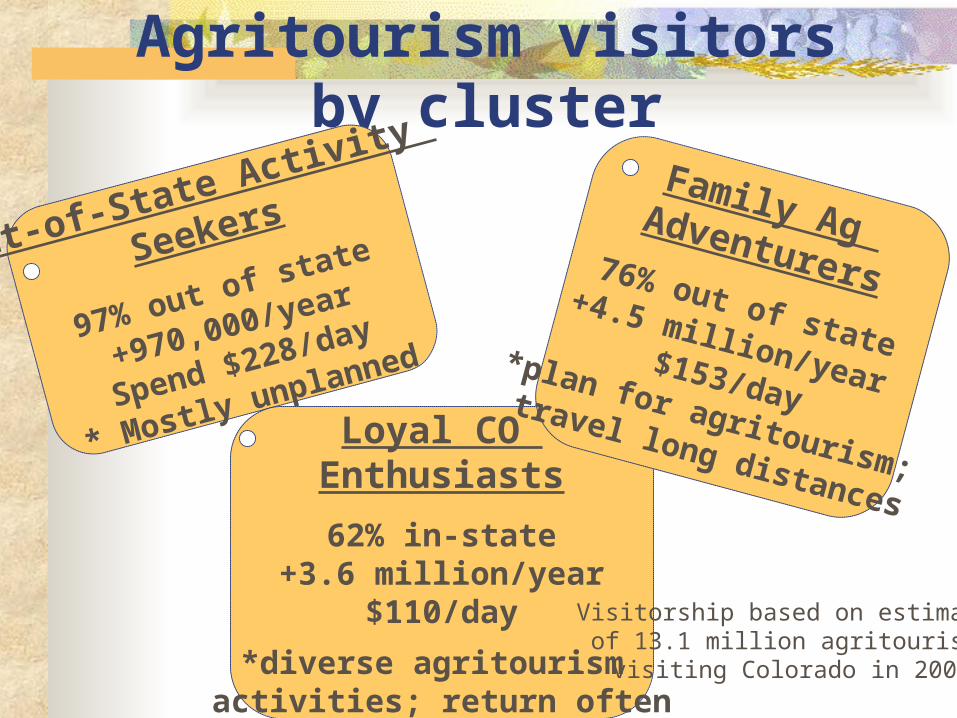

Agritourism visitors by cluster

Out-of-State Activity

Seekers

97% out of state

+970,000/year

Spend $228/day

* Mostly unplanned

Loyal CO Enthusiasts

62% in-state+3.6 million/year

$110/day

*diverse agritourism activities; return often

Family Ag Adventurers76% out of state+4.5 million/year $153/day*plan for agritourism;

travel long distances

Visitorship based on estimates of 13.1 million agritourists visiting Colorado in 2006.

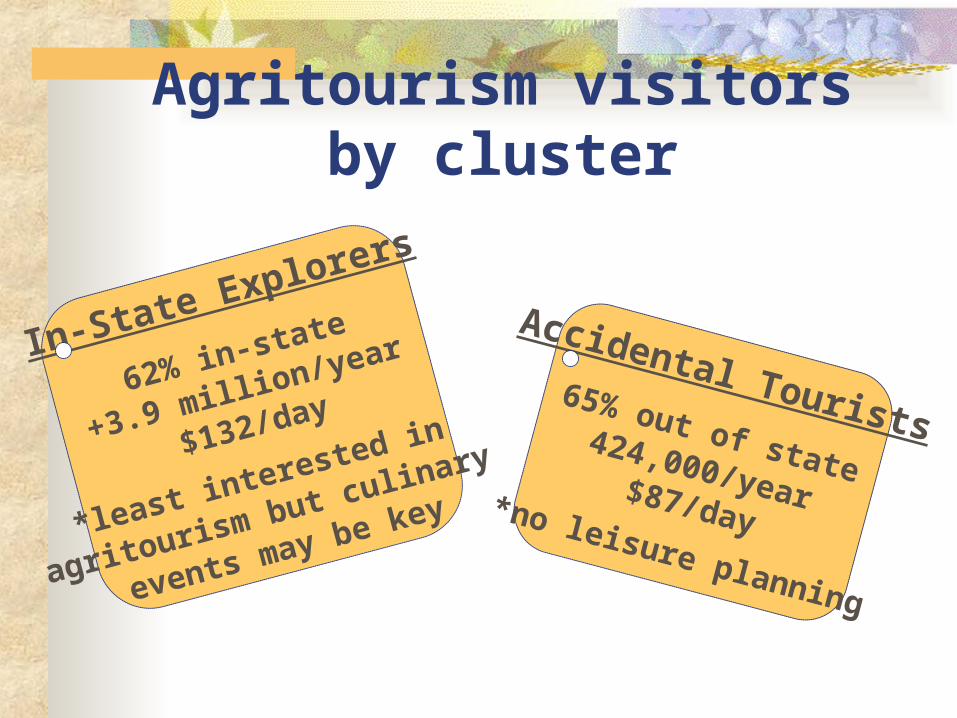

Agritourism visitors by cluster

Accidental Tourists65% out of state424,000/year$87/day*no leisure planning

In-State Explorers

62% in-state

+3.9 million/year

$132/day

*least interested in

agritourism but culinary

events may be key

Economic contribution Overall, 13.2 million visitors engaged in

some agritourism in 2006: Total contribution to economy estimated at $2.2

billion with $1.26 billion in direct activity $1.7 billion from out of state bigger impact 14% of total tourism by CTO estimates

14,665 in direct employment (7% of tourism)

Will these numbers be maintained or grow in 2007 and beyond?

Photo: Spencer George

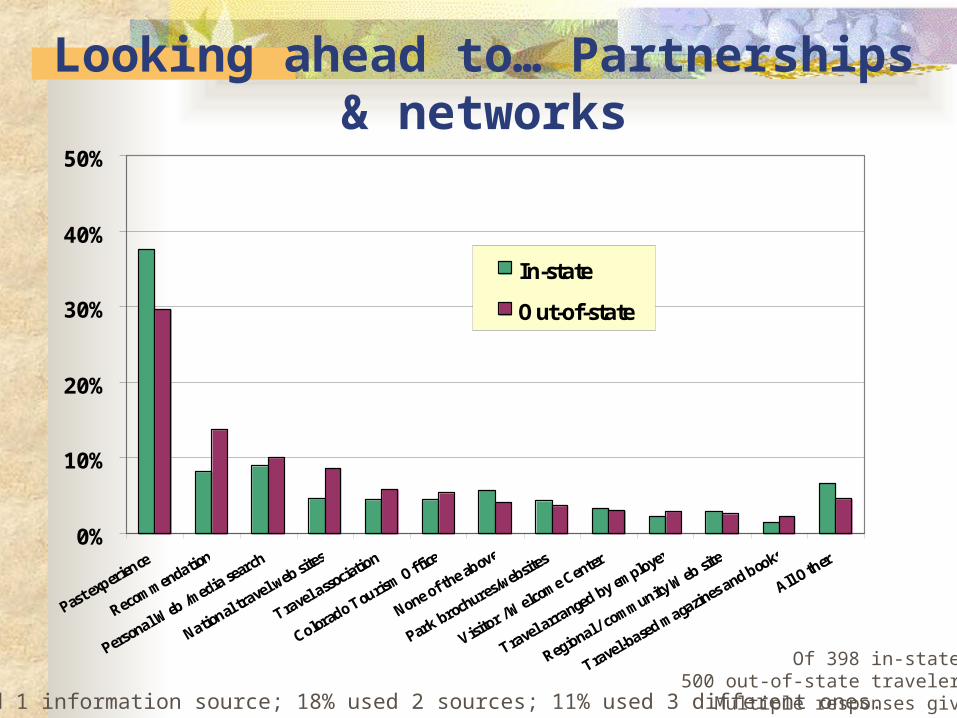

0%

10%

20%

30%

40%

50%

Past experience

Recommendation

Personal Web /m

edia search

National travel w

eb sites

Travel associatio

n

Colorado Tourism Offic

e

None of the above

Park brochures/website

s

Visitor /

Welcome Center

Travel arranged by employer

Regional / community W

eb site

Travel-based magazin

es and books

All Other

In-state

Out-of-state

Looking ahead to… Partnerships & networks

Of 398 in-state; 500 out-of-state travelers.Multiple responses given54% used 1 information source; 18% used 2 sources; 11% used 3 different ones.

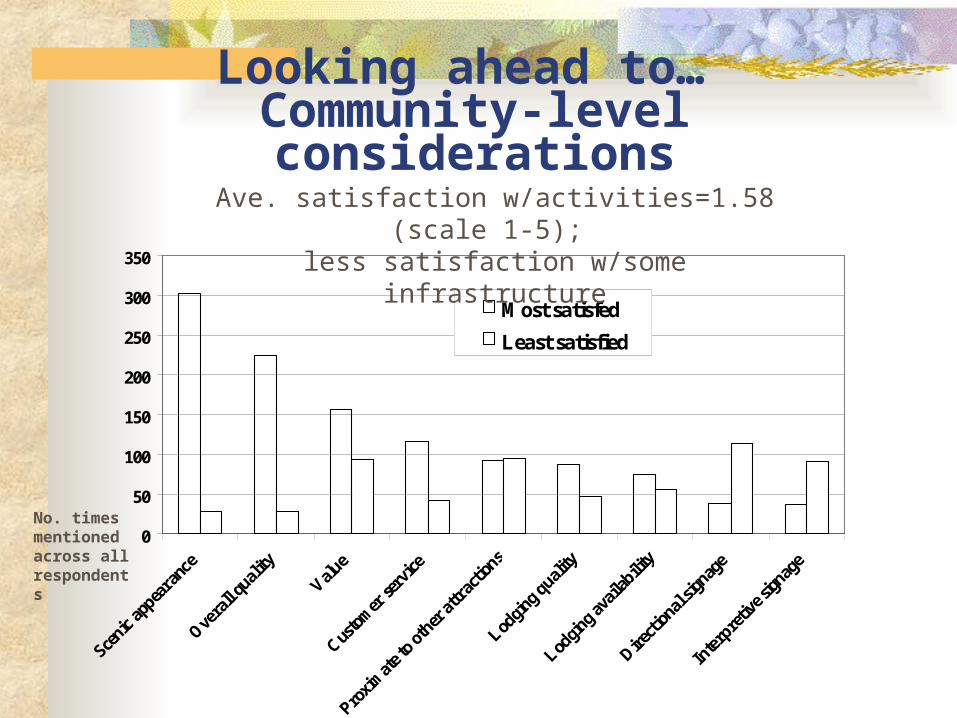

Looking ahead to… Community-level considerations

0

50

100

150

200

250

300

350

Scenic

appea

ranc

e

Overa

ll qu

ality

Value

Custo

mer

serv

ice

Proxim

ate t

o oth

er at

trac

tions

Lodgin

g quali

ty

Lodgin

g ava

ilabili

ty

Direct

ional

signag

e

Inte

rpre

tive s

ignag

e

Most satisfed

Least satisfied

No. timesmentioned across all respondents

Ave. satisfaction w/activities=1.58 (scale 1-5); less satisfaction w/some infrastructure

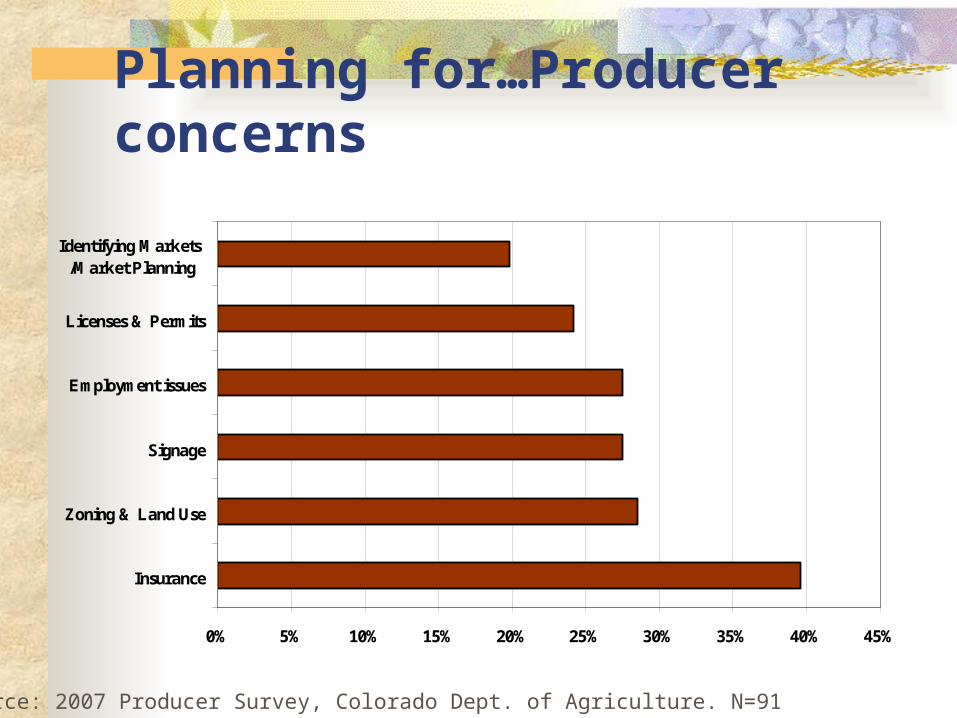

Planning for…Producer concerns

Source: 2007 Producer Survey, Colorado Dept. of Agriculture. N=91

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Insurance

Zoning & Land Use

Signage

Employment issues

Licenses & Permits

Identifying Markets /Market Planning

Challenges Shifting visitors from unplanned to planned agritourism

Increases expenditures at local level Rounding out trips: 87% of all travelers were satisfied with

their visits But 13% would have liked more agritourism and other activities to

round out their trip; would have paid for it Creating impression that Colorado is a “good value” trip for

them, especially those with large expense to travel Especially those for whom CO is a big, planned expense on leisure

Improving tourism infrastructure for agritourism Tying more on-farm & ranch activities to food-oriented events Directional signage to make travelers more aware & directed Interpretative signage for those wanting an educational experience

Partnerships to Address Challenges Colorado Tourism Office

Expand information and promotion through these popular planning resources

Colorado Department of Agriculture Directories, MarketMaker

Other Partnerships USDA Rural Development programs,

Division of Wildlife, County Ag Boards and Economic Development agencies

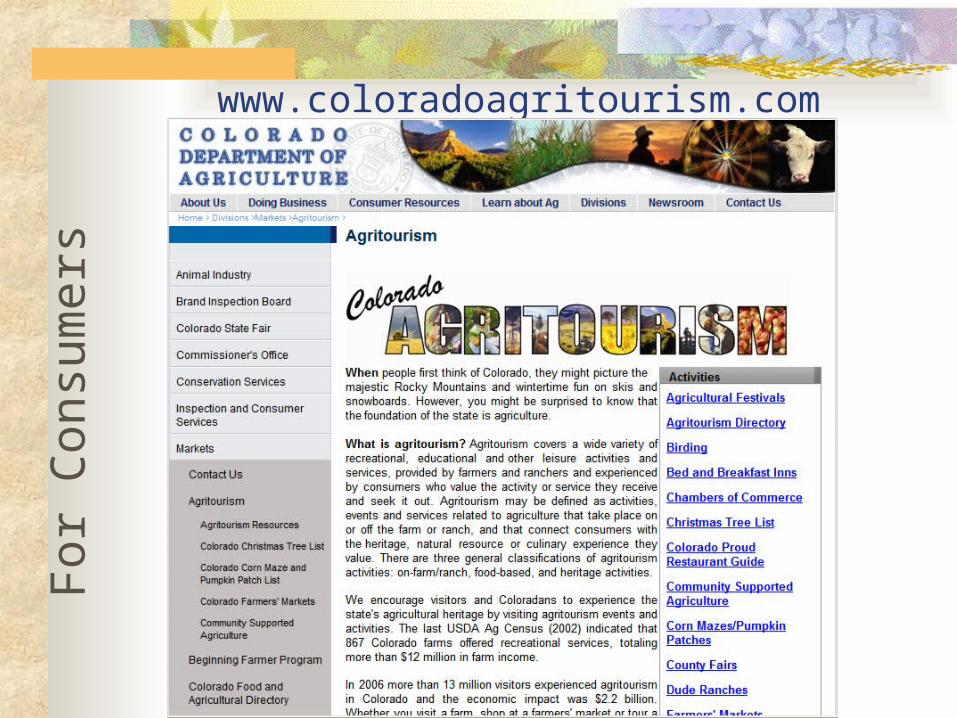

www.coloradoagritourism.comFo

r C

onsu

mers

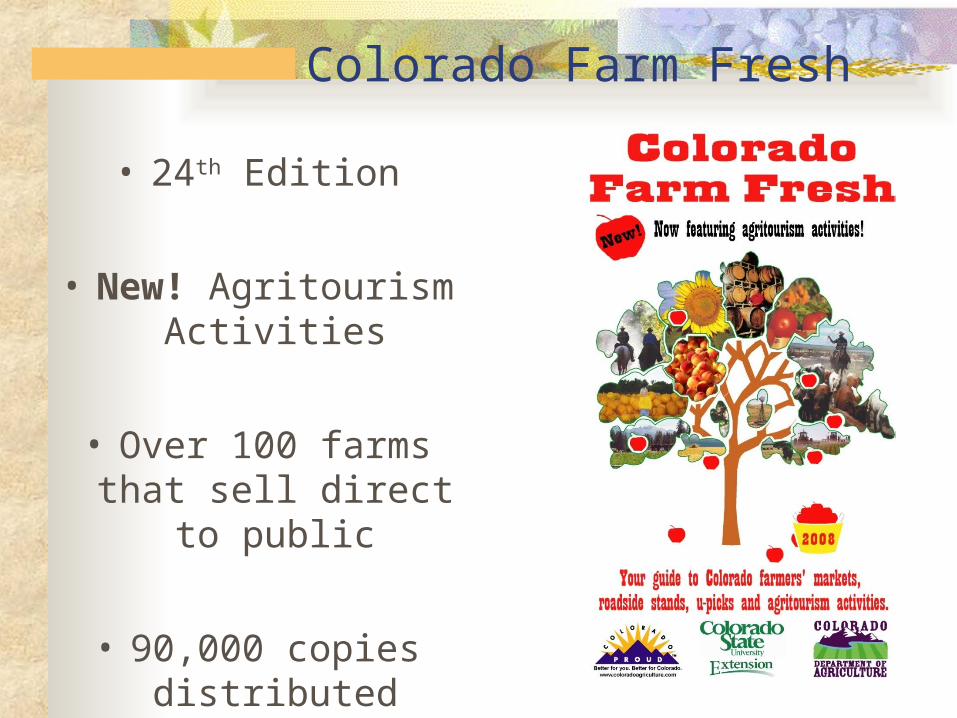

Colorado Farm Fresh

• 24th Edition

• New! Agritourism Activities

• Over 100 farms that sell direct to

public

• 90,000 copies distributed statewide

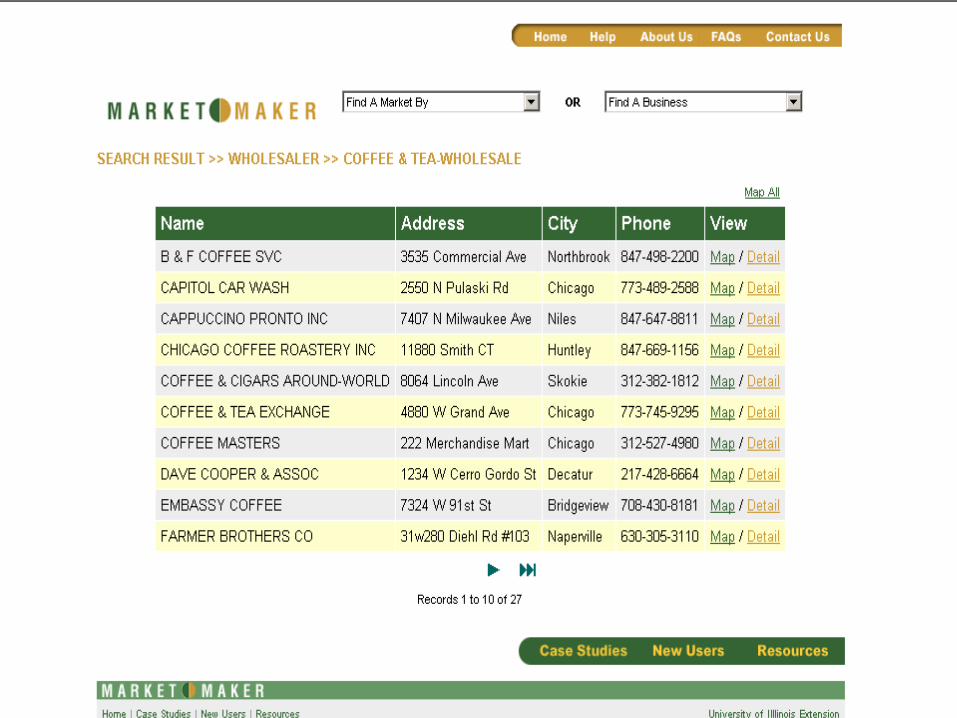

New Resource for Promotion Market Maker is a free tool to:

Help Consumers find Producers Help Producers Promote their

Operations and Products Assess the food and agriculture of

an area: Providing an inventory and great networking resource

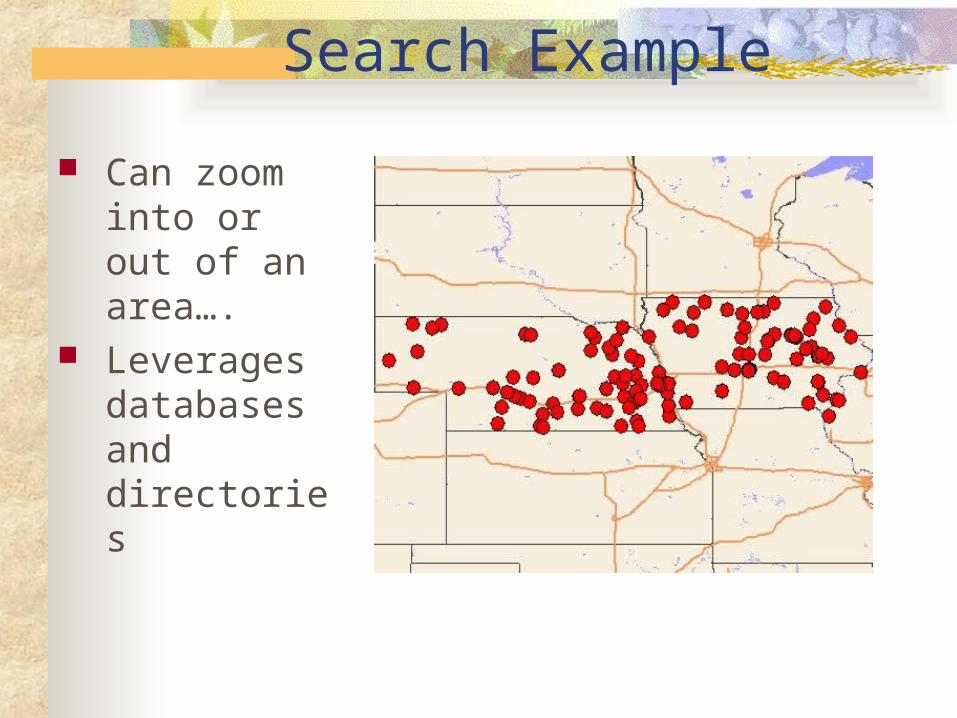

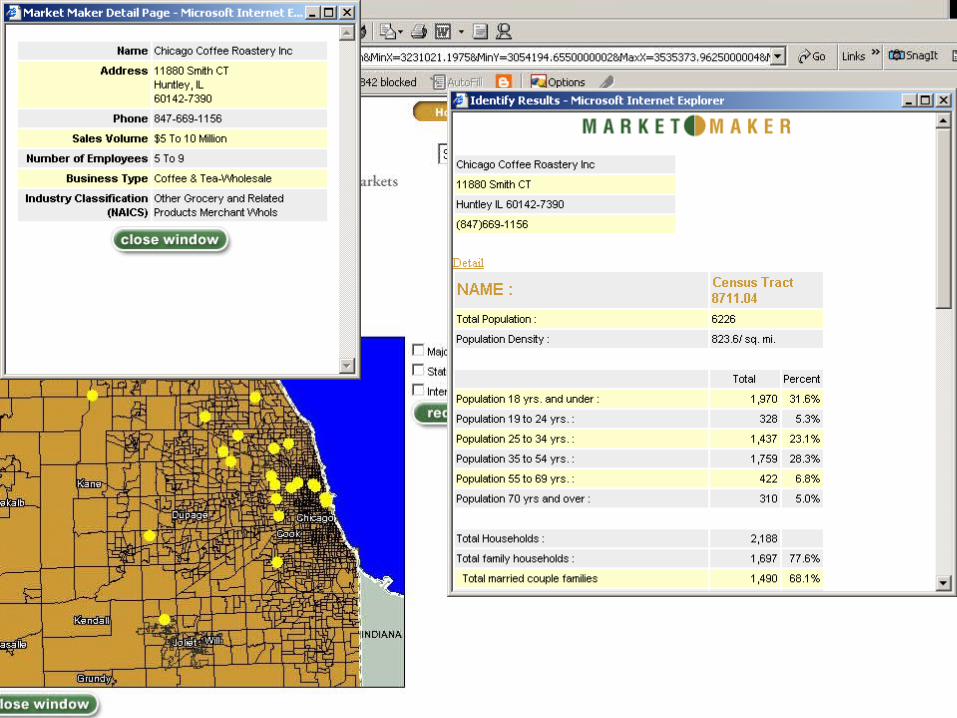

Search Example

Can zoom into or out of an area….

Leverages databases and directories

Promotion Possibilities MarketMaker is coming to Colorado!!

Collaboration of CDA and CSU Extension We will add the agritourism directory

Important to get everyone’s information Develop your Web presence now

Other Features Buyers/sellers forum More search capabilities

More Details

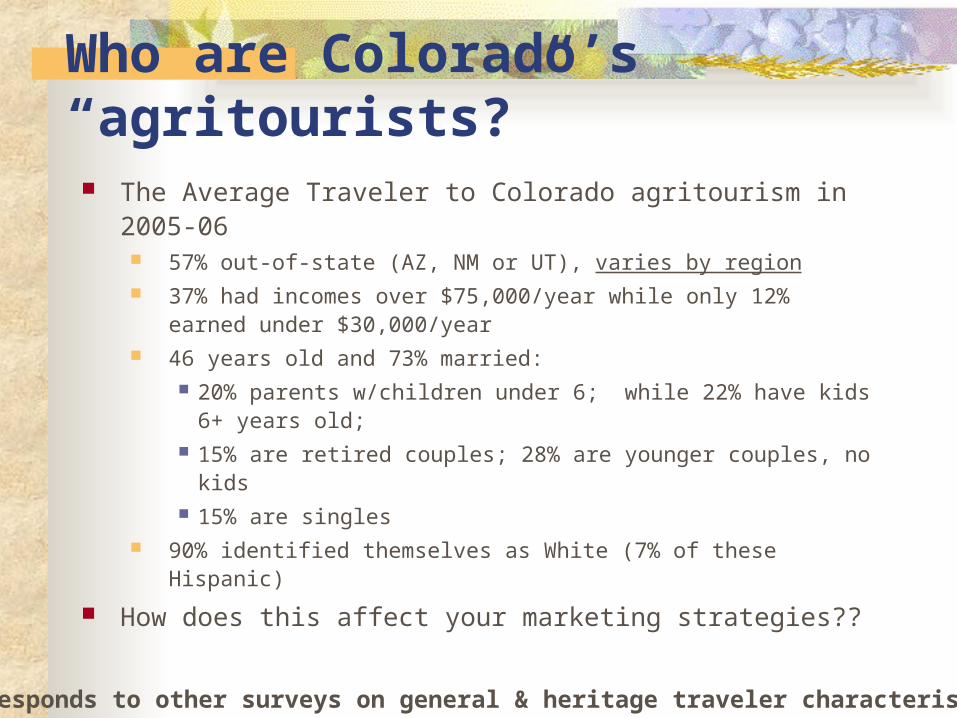

Who are Colorado’s “agritourists?” The Average Traveler to Colorado agritourism in 2005-06

57% out-of-state (AZ, NM or UT), varies by region 37% had incomes over $75,000/year while only 12% earned

under $30,000/year 46 years old and 73% married:

20% parents w/children under 6; while 22% have kids 6+ years old;

15% are retired couples; 28% are younger couples, no kids 15% are singles

90% identified themselves as White (7% of these Hispanic)

How does this affect your marketing strategies??

Corresponds to other surveys on general & heritage traveler characteristics

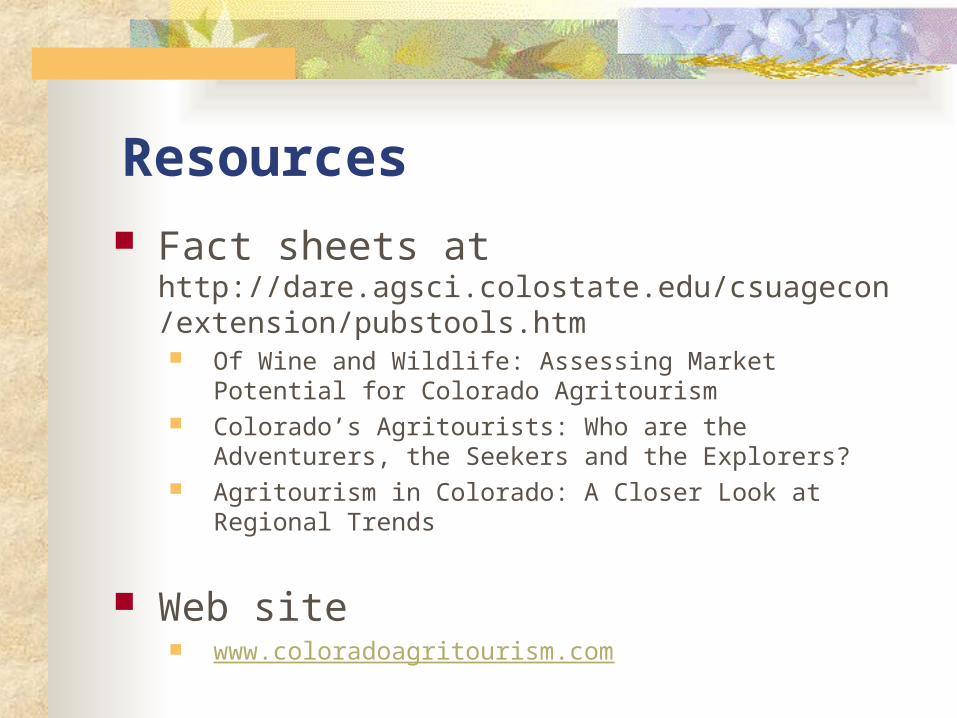

Resources

Fact sheets at http://dare.agsci.colostate.edu/csuagecon/extension/pubstools.htm Of Wine and Wildlife: Assessing Market Potential for Colorado

Agritourism Colorado’s Agritourists: Who are the Adventurers, the Seekers

and the Explorers? Agritourism in Colorado: A Closer Look at Regional Trends

Web site www.coloradoagritourism.com

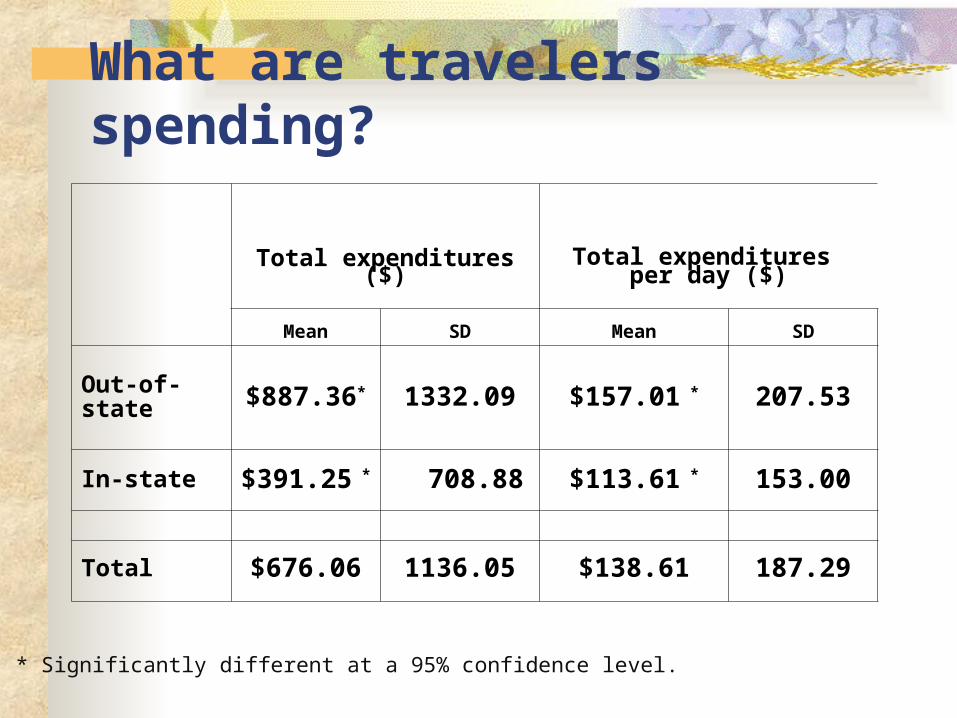

What are travelers spending?

Total expenditures ($)Total expenditures

per day ($)

Mean SD Mean SD

Out-of-state $887.36* 1332.09 $157.01 * 207.53

In-state $391.25 * 708.88 $113.61 * 153.00

Total $676.06 1136.05 $138.61 187.29

* Significantly different at a 95% confidence level.