Agri-taxation review and Budget 2015 The Busin€ss of Dairy Farming Post 2015 Rowena Dwyer, IFA...

11

Agri-taxation review and Budget 2015 The Busin€ss of Dairy Farming Post 2015 Rowena Dwyer , IFA Chief Economist 21 st October 2014

-

Upload

harriet-butler -

Category

Documents

-

view

214 -

download

0

Transcript of Agri-taxation review and Budget 2015 The Busin€ss of Dairy Farming Post 2015 Rowena Dwyer, IFA...

Agri-taxation review and Budget 2015

The Busin€ss of Dairy Farming Post 2015

Rowena Dwyer , IFA Chief Economist21st October 2014

2

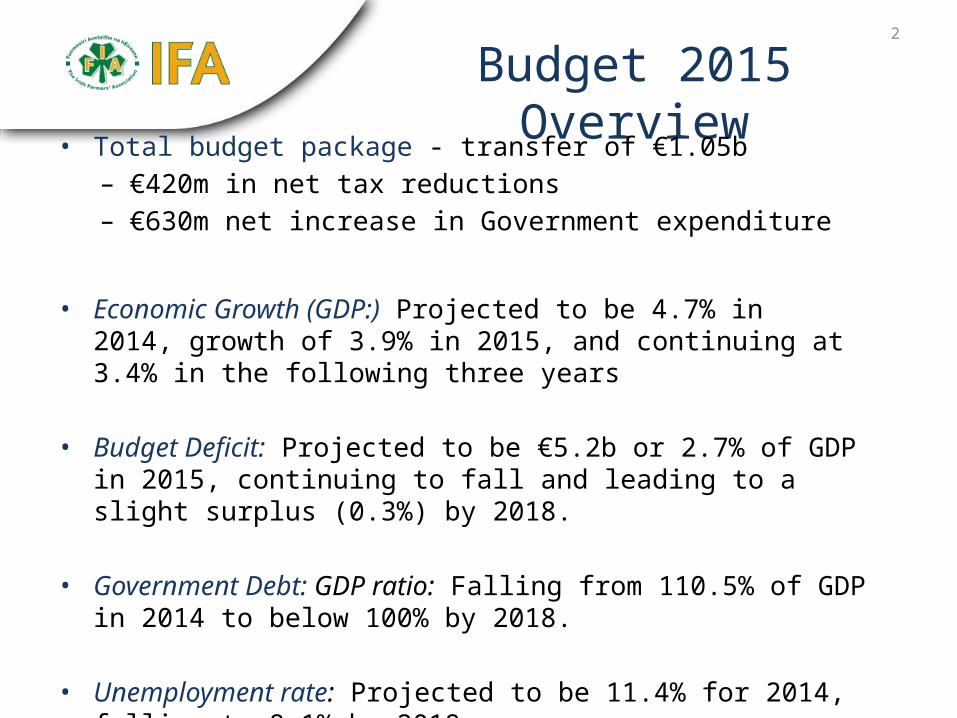

Budget 2015 Overview

• Total budget package - transfer of €1.05b– €420m in net tax reductions – €630m net increase in Government expenditure

• Economic Growth (GDP:) Projected to be 4.7% in 2014, growth of 3.9% in 2015, and continuing at 3.4% in the following three years

• Budget Deficit: Projected to be €5.2b or 2.7% of GDP in 2015, continuing to fall and leading to a slight surplus (0.3%) by 2018.

• Government Debt: GDP ratio: Falling from 110.5% of GDP in 2014 to below

100% by 2018. • Unemployment rate: Projected to be 11.4% for 2014, falling to 8.1% by

2018.

3

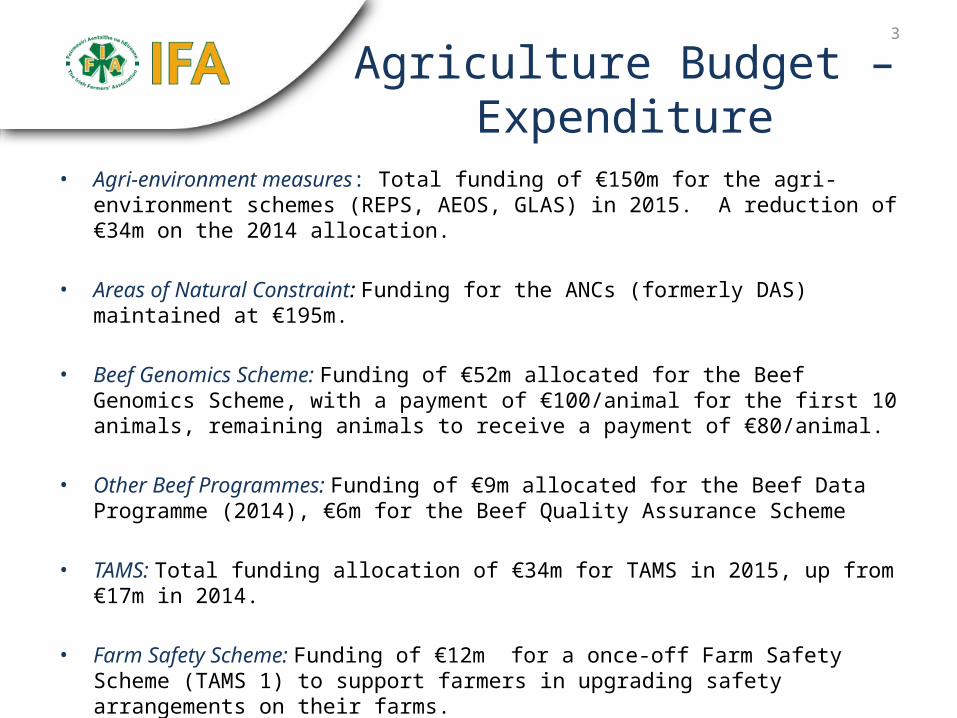

Agriculture Budget – Expenditure

• Agri-environment measures: Total funding of €150m for the agri-environment schemes (REPS, AEOS, GLAS) in 2015. A reduction of €34m on the 2014 allocation.

• Areas of Natural Constraint: Funding for the ANCs (formerly DAS) maintained at €195m.

• Beef Genomics Scheme: Funding of €52m allocated for the Beef Genomics Scheme, with a payment of €100/animal for the first 10 animals, remaining animals to receive a payment of €80/animal.

• Other Beef Programmes: Funding of €9m allocated for the Beef Data Programme (2014), €6m for the Beef Quality Assurance Scheme

• TAMS: Total funding allocation of €34m for TAMS in 2015, up from €17m in 2014.

• Farm Safety Scheme: Funding of €12m for a once-off Farm Safety Scheme (TAMS 1) to support farmers in upgrading safety arrangements on their farms.

• Forestry: Funding allocation of €110m, for a planned afforestation programme of 7,000 hectares.

4

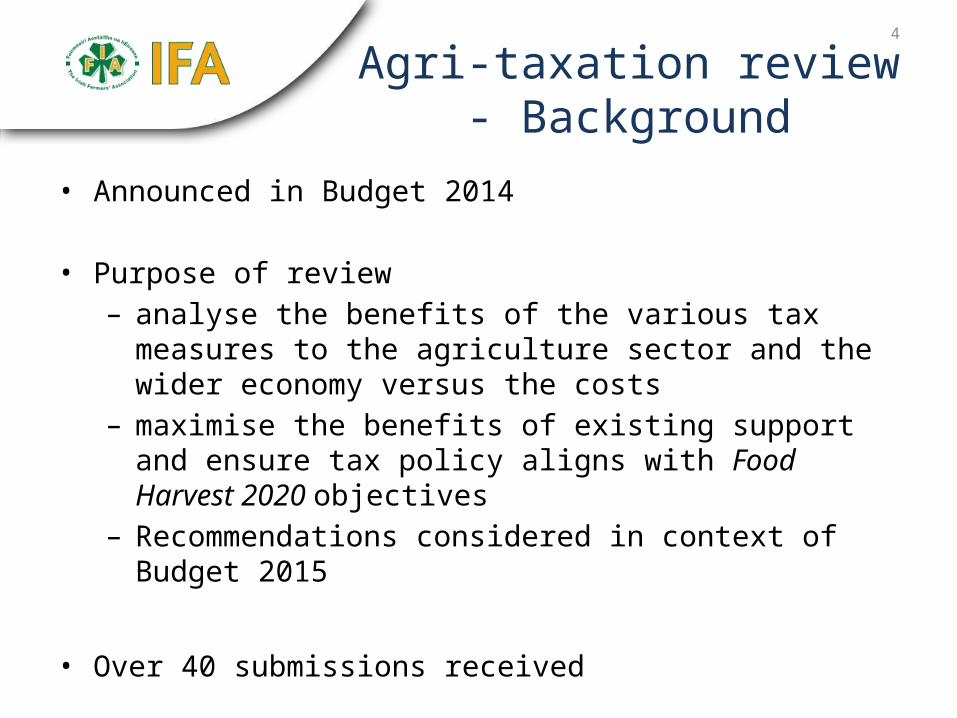

Agri-taxation review - Background

• Announced in Budget 2014

• Purpose of review – analyse the benefits of the various tax measures to the

agriculture sector and the wider economy versus the costs– maximise the benefits of existing support and ensure tax policy

aligns with Food Harvest 2020 objectives– Recommendations considered in context of Budget 2015

• Over 40 submissions received

• Consultation process during 2014 – Agri-taxation working group – (Departments of Finance, Agriculture and Indecon Economic Consultants)

5

Agri-taxation review report - Overview

• Analysis showed benefits of taxation measures to the economy outweigh the overall costs (revenue foregone) of providing reliefs

• Recommended continued support for primary agriculture through taxation measures, with some additions and amendments.

• Identified the following policy objectives:– Increase the mobility and productive use of land, in particular to rebalance the letting market in

favour of long-term leasing.– Assist succession and farm transfer, improving the age profile of Irish farming.– Complement wider agriculture policies and schemes, including supporting:

• Investment to enhance competitiveness, including assisting new entrants and young trained farmers

• Environmental sustainability, including the improvement of farm efficiency• Alternative farming models such as farm partnerships, and • Responses to increasing income volatility.

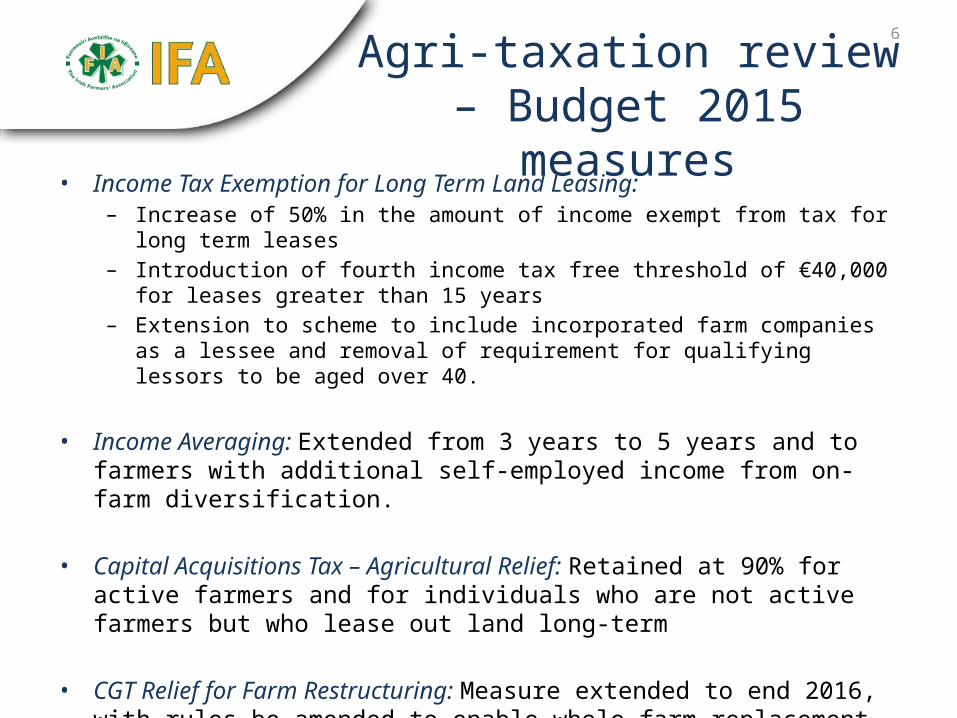

6Agri-taxation review – Budget 2015 measures

• Income Tax Exemption for Long Term Land Leasing: – Increase of 50% in the amount of income exempt from tax for long term leases – Introduction of fourth income tax free threshold of €40,000 for leases greater than 15

years– Extension to scheme to include incorporated farm companies as a lessee and removal of

requirement for qualifying lessors to be aged over 40.

• Income Averaging: Extended from 3 years to 5 years and to farmers with additional self-employed income from on-farm diversification.

• Capital Acquisitions Tax – Agricultural Relief: Retained at 90% for active farmers

and for individuals who are not active farmers but who lease out land long-term

• CGT Relief for Farm Restructuring: Measure extended to end 2016, with rules be amended to enable whole farm replacement to be eligible for the relief

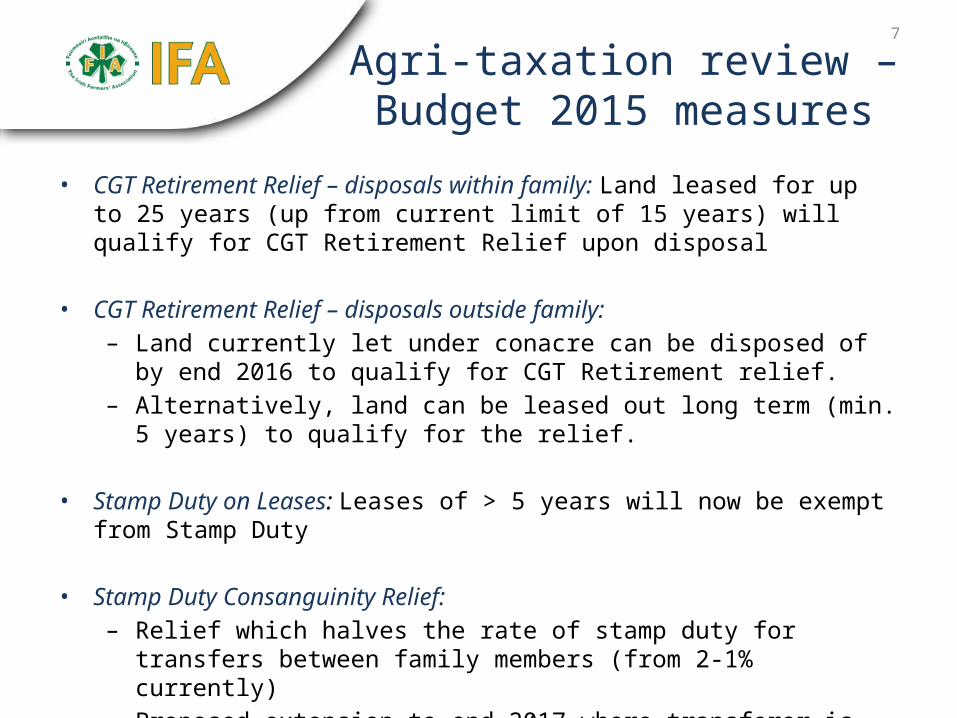

7

Agri-taxation review – Budget 2015 measures

• CGT Retirement Relief – disposals within family: Land leased for up to 25 years (up from current limit of 15 years) will qualify for CGT Retirement Relief upon disposal

• CGT Retirement Relief – disposals outside family: – Land currently let under conacre can be disposed of by end 2016 to qualify for

CGT Retirement relief. – Alternatively, land can be leased out long term (min. 5 years) to qualify for the

relief.

• Stamp Duty on Leases: Leases of > 5 years will now be exempt from Stamp Duty

• Stamp Duty Consanguinity Relief: – Relief which halves the rate of stamp duty for transfers between family

members (from 2-1% currently)– Proposed extension to end 2017 where transferor is <65 years of age and

tranferee is active farmer

8

Agri-taxation review – other recommendations

• Recommended retention of following measures

– Agricultural Relief for Capital Acquisitions Tax

– Retirement Relief from Capital Gains Tax

– Stamp duty exemptions on transfers of land (e.g. Young Trained Farmer)

– Capital Allowances

– Stock Reliefs

– Tax exemption for profits or gains from the commercial occupation of woodlands

– Taxation measures for farm partnerships-all registered farm partnerships

9

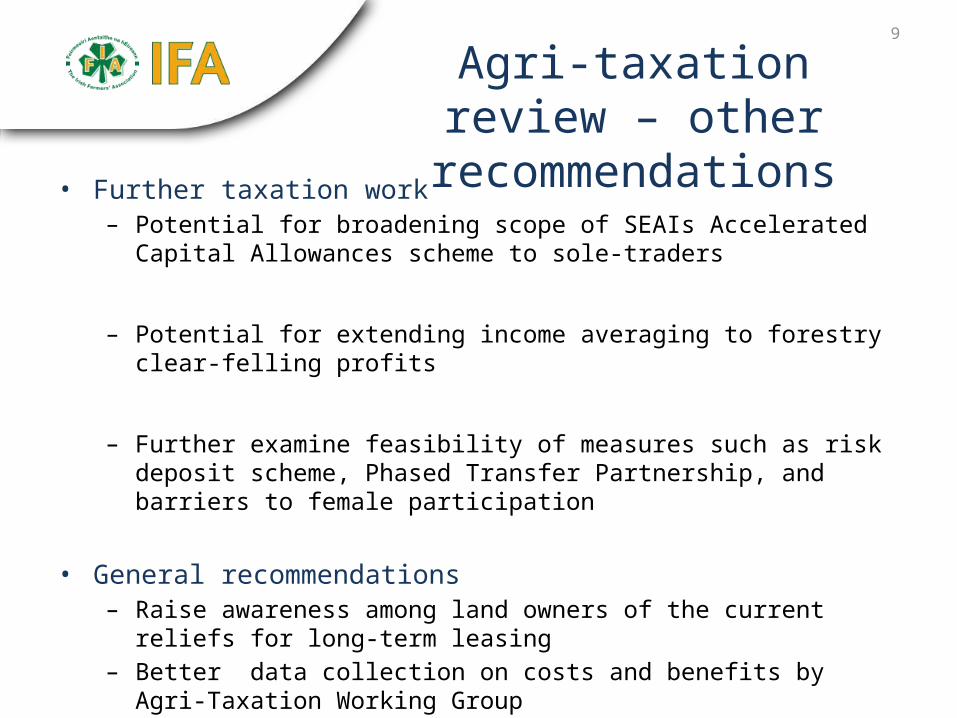

Agri-taxation review – other recommendations

• Further taxation work – Potential for broadening scope of SEAIs Accelerated Capital Allowances

scheme to sole-traders

– Potential for extending income averaging to forestry clear-felling profits

– Further examine feasibility of measures such as risk deposit scheme, Phased Transfer Partnership, and barriers to female participation

• General recommendations– Raise awareness among land owners of the current reliefs for long-term

leasing– Better data collection on costs and benefits by Agri-Taxation Working Group

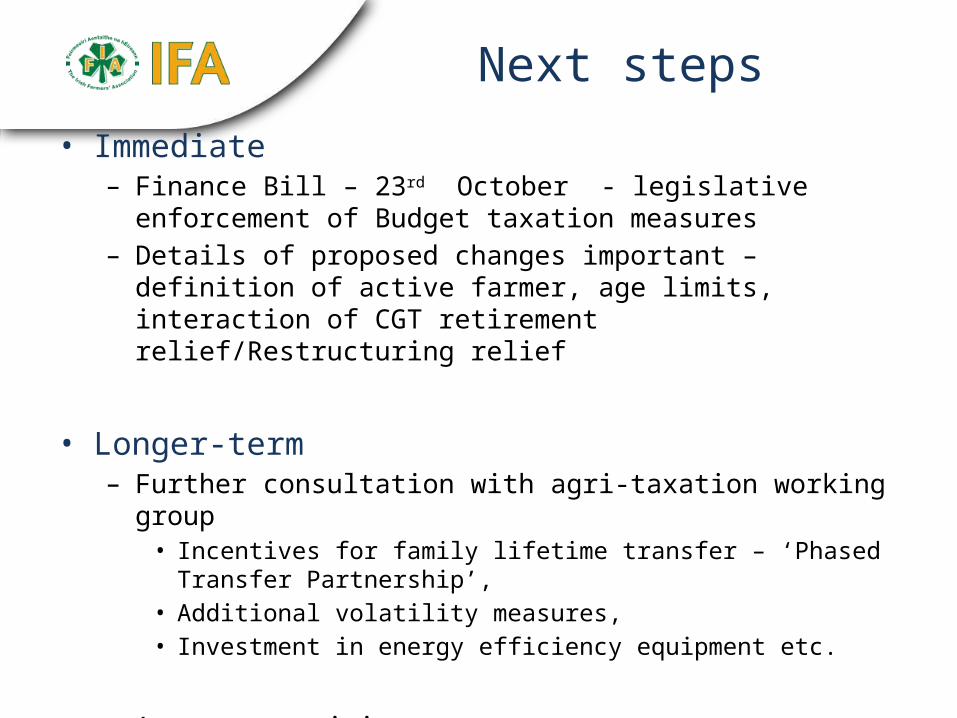

Next steps

• Immediate – Finance Bill – 23rd October - legislative enforcement of Budget

taxation measures– Details of proposed changes important – definition of active farmer,

age limits, interaction of CGT retirement relief/Restructuring relief

• Longer-term– Further consultation with agri-taxation working group

• Incentives for family lifetime transfer – ‘Phased Transfer Partnership’, • Additional volatility measures, • Investment in energy efficiency equipment etc.

– Awareness raising

– Budget 2016!

11

Thank you for listening

Any Questions?