Accounting & Tax Issues in Developing the Malaysian ABS Market - A Regulator’s Perspective Wong...

25

Accounting & Tax Issues in Accounting & Tax Issues in Developing the Malaysian ABS Market Developing the Malaysian ABS Market - A Regulator’s Perspective - A Regulator’s Perspective Wong Sau Ngan SECURITIES COMMISSION, MALAYSIA Shanghai 8 November 2005 Workshop on the Rise of Securitization in East Asia 7 – 9 November 2005

-

date post

21-Dec-2015 -

Category

Documents

-

view

222 -

download

0

Transcript of Accounting & Tax Issues in Developing the Malaysian ABS Market - A Regulator’s Perspective Wong...

Accounting & Tax Issues in Developing the Accounting & Tax Issues in Developing the Malaysian ABS MarketMalaysian ABS Market

- A Regulator’s Perspective - A Regulator’s Perspective

Wong Sau NganSECURITIES COMMISSION, MALAYSIA

Shanghai 8 November 2005

Workshop on the Rise of Securitization in East Asia

7 – 9 November 2005

AgendaAgenda

• Overview of ABS market in MalaysiaOverview of ABS market in Malaysia

• Accounting mattersAccounting matters Impediments & IssuesImpediments & Issues Initiatives takenInitiatives taken

• Tax mattersTax matters Impediments & IssuesImpediments & Issues Initiatives takenInitiatives taken

• Moving forwardMoving forward

2

3

95 12308955 8068

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

2001 2002 2003 2004Year

Amou

nt (R

M Mi

llion)

MGS PDS ABS

Efforts to develop ABS market in Malaysia accelerated after 1997 financial crisis

• Prior to 2001, ABS market was non-existent due to a wide range of legal, regulatory, tax & accounting impediments

• As at end-September 2005, 21 ABS have been issued, amounting to RM 17.76 billion (USD 4.75 billion equivalent)

• However, size of ABS market is relatively small compared to MGS and PDS markets

• More developmental initiatives required to further boost the ABS market

Size of ABS market vs MGS and PDSSize of ABS market vs MGS and PDS

4

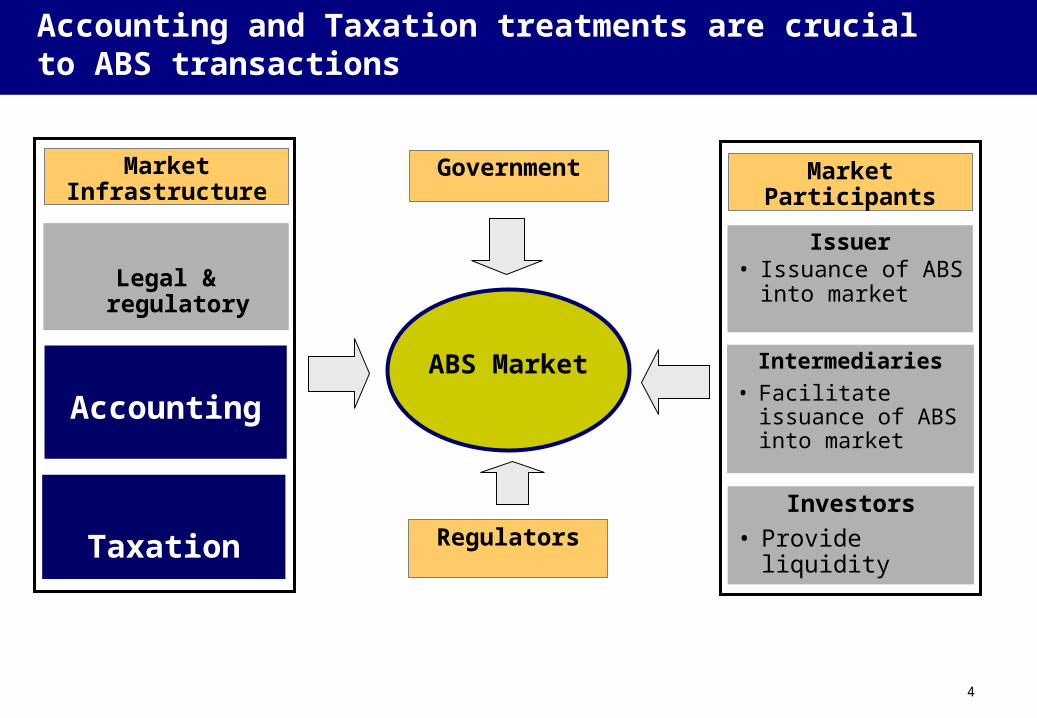

Accounting and Taxation treatments are crucial to ABS transactions

Issuer• Issuance of ABS

into market

Intermediaries

• Facilitate issuance of ABS into market

Investors

• Provide liquidity

ABS Market

Regulators

Government Market ParticipantsMarket Infrastructure

Legal & regulatory

Accounting

Taxation

5

Significance of accounting treatment for ABS transactions

Why is it important to the originator?Why is it important to the originator?

Improve performance ratio Reduce gearing Fulfill capital adequacy requirements

Benefit to originator in ABS transaction is possible off-Benefit to originator in ABS transaction is possible off-balance sheet treatment for its asset transfersbalance sheet treatment for its asset transfers

6

Significance of tax treatment for ABS transactions

Why is it important to the originator and SPV?Why is it important to the originator and SPV?

• Important for originator to determine tax impact of entering into ABS transactions

• Crucial for SPV to budget its cash flows to meet its obligations which could otherwise be severely impacted by any unexpected tax charges

Tax treatment impacts the viability of ABS transactionsTax treatment impacts the viability of ABS transactions

AgendaAgenda

• Overview of ABS market in MalaysiaOverview of ABS market in Malaysia

• Accounting mattersAccounting matters Impediments & IssuesImpediments & Issues Initiatives takenInitiatives taken

• Tax mattersTax matters Impediments & IssuesImpediments & Issues Initiatives takenInitiatives taken

• Moving forwardMoving forward

7

8

Lack of clarity on accounting treatment of ABS transactions

• Currently, most ABS transactions in Malaysia are “off-balance sheet”

• IAS 39 – Financial Instruments: Recognition & Measurement took effect internationally from 1 January 2001

Crux of the matter is whether the transfer of asset in an ABS transaction is a true sale, hence be taken off-balance sheet

• Based on IAS 39, the sale will constitute a “true sale” if originator has surrendered its control over the asset and the transferee has obtained benefits of the transferred assets Principle of “substance over form” approach

1.1. Criteria for “true sale” – the “off-balance sheet” issue Criteria for “true sale” – the “off-balance sheet” issue relating to the transfer of assets from originator to SPVrelating to the transfer of assets from originator to SPV

9

SPV – to consolidate or not to consolidate?SPV – to consolidate or not to consolidate?

Originators may have to consolidate SPV that they, in substance, “control”

There is a concern that the SPV would need to be consolidated with the originator, thereby defeating the purpose of derecognising the assets in the first place

Lack of clarity on accounting treatment of ABS transactions (con’t)

2.2. Uncertainty on treatment of SPV by the originatorUncertainty on treatment of SPV by the originator

10

Accounting issues have major implications on developing ABS market

• Derecognition and consolidation rulesDerecognition and consolidation rules Introduce more stringent rules on the removal of assets from balance sheet of originator

Intended objective of transfer of assets from originator to SPV may not be achieved

Even if assets are taken off-balance sheet (derecognised), there is a possibility of consolidating the SPV at originator’s level, hence, bringing the assets back to the books of the originator

• Fair value measurement for investments in ABSFair value measurement for investments in ABS Absence of consistent transacted prices and quotes Difficulty is compounded by illiquid bond market Reliability of valuation models

• Significant implication to the ABS industrySignificant implication to the ABS industry• Adverse impact on the development and growth of ABS marketAdverse impact on the development and growth of ABS market

11

• SC is represented on Malaysian Accounting Standards Board (MASB) and Working Group on IAS 39

• Ensure that interpretation of IAS 39 is in line with international practice to provide clarity and certainty to market practitioners

• Promote discussion and debate with the view to enhance awareness of ABS structures that are allowed under SC’s ABS Guidelines from the structures seen in the financial debacles

• Active engagement with accounting practitioners, particularly, top 4 accounting firms in providing SC’s development perspectives on ABS transactions

• Strike balance between extent to which risks, rewards & control over securitised assets have been transferred resulting in a transaction being deemed as off-balance-sheet vs. on-balance-sheet

SC’s role in ABS accounting issues

12

• The adoption follows the approval recently by MASB of IAS 39, known as FRS 139 in Malaysia

• Adopted after five years of lengthy deliberation involving major constituents such as bankers, auditors, investment analysts, professional bodies, the unit trust industry and insurance industry & consultation process with the public

• Takes into account various changes to IAS 39 by IASB over the years, as well as the ongoing changes

• FRS 139 is part of MASB’s plans to issue 21 financial reporting standards in Malaysia in the current year to serve the investing community better through greater transparency in financial reporting

• In view of the far reaching implications on companies, companies are encouraged to get ready for FRS 139’s implementation on 1 January 2006

Malaysia has adopted IAS 39

AgendaAgenda

• Overview of ABS market in MalaysiaOverview of ABS market in Malaysia

• Accounting mattersAccounting matters Impediments & IssuesImpediments & Issues Initiatives takenInitiatives taken

• Tax mattersTax matters Impediments & IssuesImpediments & Issues Initiatives takenInitiatives taken

• Moving forwardMoving forward

13

14

Lack of certainty on tax treatment of ABS transactions

IssuesIssues

• How would originator be taxed on sale of asset?

• How would SPV be taxed?

• Implications of transaction taxes (e.g RPGT, Stamp Duty & Service tax)?

• Tax implication for investors?

OriginatorOriginator SPVSPVIssues Issues ABSABS

Sale of Sale of assetasset

InvestorsInvestors

Lack of specific tax legislation that deals with securitisationLack of specific tax legislation that deals with securitisation

Case-by-case approach according to specific facts and circumstances by reference to existing general tax legislation and practices give rise to tax uncertainties

15

Tax issues for originator

• How would proceeds of originator from sale of assets be taxed? Tax upfront; or Taxable over tenure of ABS

• Could the disposal price of asset transferred be challenged? Uncertainty as to how the disposal price should be determined and what should

be the consequential gain or loss on the sale of assets by the originator

• Are costs associated with the asset transfer deductible? If answer is affirmative, there is a need to determine the timing of deduction

• Will the transfer be subject to transaction taxes (e.g stamp duty and RPGT)?

• Would service fee received by the originator from SPV be subject to service tax?

• Need for tax certainty and clarity for ABS transactionsNeed for tax certainty and clarity for ABS transactions• Need to reduce tax cost of ABS transactionsNeed to reduce tax cost of ABS transactions• Consider exemptions from transaction taxesConsider exemptions from transaction taxes

16

Tax issues for SPV

• Basis of taxationBasis of taxation Uncertainty on the tax status of the SPV in terms of whether it is

considered carrying on a business or an investment holding company

Carrying on a business enjoys maximum tax deduction

Investment holding company subject to restrictions on deductibility of expenses

• Given the bankruptcy remote status of the SPV, the tax burden of an Given the bankruptcy remote status of the SPV, the tax burden of an SPV arising from ABS transactions should be kept to a minimumSPV arising from ABS transactions should be kept to a minimum

• This objective would not be accomplished if the SPV is considered This objective would not be accomplished if the SPV is considered to be an investment holding company as it attracts a significant tax to be an investment holding company as it attracts a significant tax burden for the SPVburden for the SPV

17

Tax issues for investors

• Tax treatment of interest received on ABS issued by the SPV

• Witholding tax implication of interest paid to non-residents

Tax incentives required to encourage investment in ABSTax incentives required to encourage investment in ABS

18

The Government has proposed in Budget 2004 that ABS be given equal tax treatment as other conventional securities to promote issuance of ABS as a means of cost-efficient fund-raising

• Established a set of specific tax treatment based on the principle of tax neutrality between ABS and other private debt securities to ensure tax neutrality and tax certainty for ABS transactions

E.g Proceeds and capital charge arising from transfer of receivables and assets respectively between the originator and the SPV would be spread out over the securitisation period, rather than charged upfront

• Tax deduction is granted to expenses incurred in the issuance of ABS for a period of 5 years

• Payment received by the servicers of the assets is deemed exempted from service tax under the Service Tax Act 1975

Tax Neutral Framework for Originators & SPV

• Originator and SPV not to be over-burdened by additional taxOriginator and SPV not to be over-burdened by additional tax• Clarification on treatment on income and expenses by originator and SPVClarification on treatment on income and expenses by originator and SPV• Specific tax treatment based on the principle of tax neutralitySpecific tax treatment based on the principle of tax neutrality

19

• Stamp Duty (Exemption) (No.12) Order 2001Stamp Duty (Exemption) (No.12) Order 2001• Stamp Duty (Exemption) (No. 4) Order 2005Stamp Duty (Exemption) (No. 4) Order 2005

Generally, all instruments (Conventional and Islamic) executed for the purpose of securitisation will be exempted from stamp duty

• Real Property Gains Tax (Exemption) Order 2001Real Property Gains Tax (Exemption) Order 2001

RPGT exemption for the following disposals in a securitisation transaction approved by SC: Disposals to purchase by SPV; and Repurchase of the chargeable assets, to or in favour of the person

from whom those assets were acquired

Tax incentives for Originator and SPV

20

Tax incentives for investors

Non-residentNon-resident

• Blanket exemption from withholding tax granted by the Government with effect from 11 September 2004

• Interest income derived by non-residents from investments in RM-denominated Malaysian Government Securities (MGS) and corporate bonds is exempted from withholding tax

ResidentResident

• Exemption of interest income received by individuals, close end funds and unit trust funds

AgendaAgenda

• Overview of ABS market in MalaysiaOverview of ABS market in Malaysia

• Accounting mattersAccounting matters Impediments & IssuesImpediments & Issues Initiatives takenInitiatives taken

• Tax mattersTax matters Impediments & IssuesImpediments & Issues Initiatives takenInitiatives taken

• Moving forwardMoving forward

21

22

Accounting and tax issues and uncertainties impede securitisation transactions and hinder the development of

the ABS market

Malaysia’s experience in relation to accounting & tax issues on ABS transactions

Consultations with industry bodies, accounting and tax practitioners, Malaysian Accounting Standards Board and

Inland Revenue Board

Formulate an efficient, facilitative and transparent accounting and tax framework for the ABS market

23

• Educating tax authorities on ABS transactions and structures• Constantly engaging with industry participants, tax consultants and

tax authorities to clarify uncertainties and ambiguity

Next steps

• SC is constantly engaging with industry bodies & MASB to provide greater certainty on the interpretation & application of IAS39 (e.g clarification on de-recognition of asset)

AccountingAccounting

TaxationTaxation

24

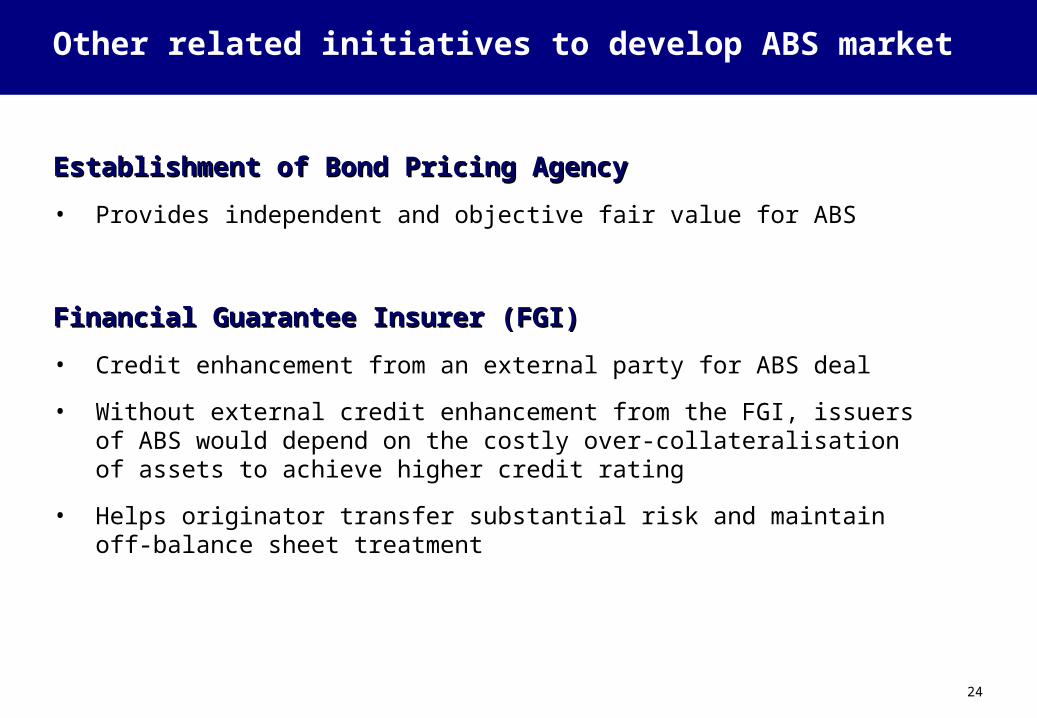

Establishment of Bond Pricing AgencyEstablishment of Bond Pricing Agency

• Provides independent and objective fair value for ABS

Financial Guarantee Insurer (FGI)Financial Guarantee Insurer (FGI)

• Credit enhancement from an external party for ABS deal

• Without external credit enhancement from the FGI, issuers of ABS would depend on the costly over-collateralisation of assets to achieve higher credit rating

• Helps originator transfer substantial risk and maintain off-balance sheet treatment

Other related initiatives to develop ABS market

25

Thank you