ACCOUNTING 2 CH. 2. ADJUSTMENTS Adjustments transfer the cost of “used up” assets to expense...

33

ACCOUNTING 2 CH. 2

-

Upload

ezra-fitzgerald -

Category

Documents

-

view

218 -

download

0

Transcript of ACCOUNTING 2 CH. 2. ADJUSTMENTS Adjustments transfer the cost of “used up” assets to expense...

ACCOUNTING 2

CH. 2

ADJUSTMENTS

Adjustments transfer the cost of “used up” assets to expense accounts.

Adjustments for changes in merchandise inventory are made directly to the Income Summary account.

Glencoe Accounting

Key Terms

adjustment

beginning inventory

ending inventory

physical inventory

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

COMPLETING END-OF-PERIOD WORK

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

Managers, stockholders, and creditors need

to know net income and the value of

stockholders’ equity to make sound

business decisions.

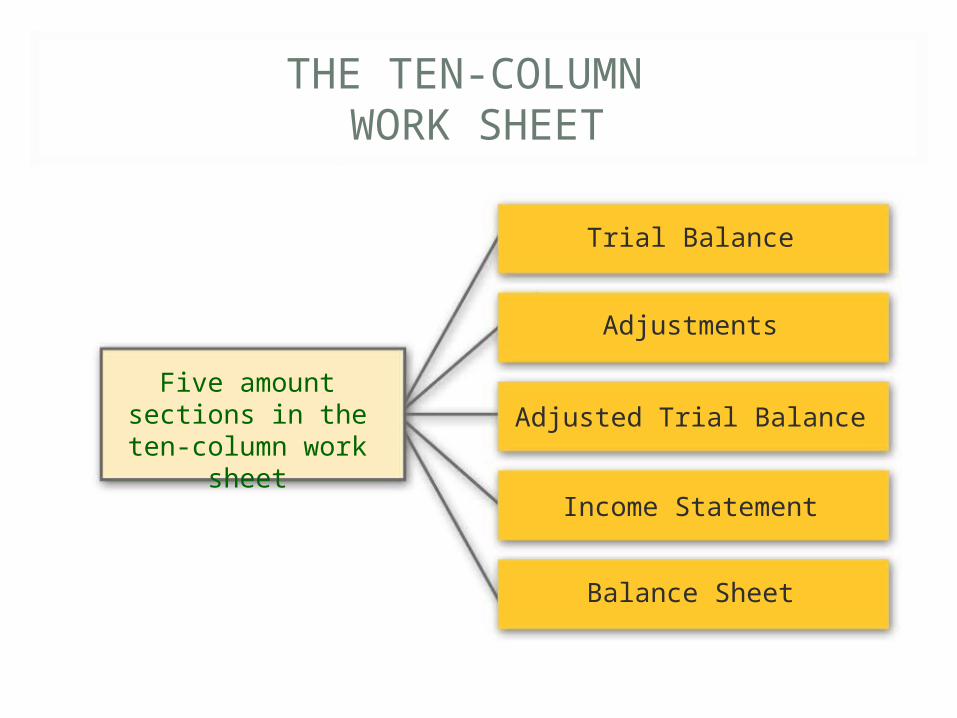

THE TEN-COLUMN WORK SHEET

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

Five amount sections in the ten-column work

sheet

Trial Balance

Adjustments

Adjusted Trial Balance

Income Statement

Balance Sheet

THE TEN-COLUMN WORK SHEET

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

adjustmentAn amount that is added to or subtracted from an account balance to bring that balance up to date.

At the end of the period, adjustments are made to transfer the costs of assets consumed from asset accounts to the appropriate

expense accounts.

THE TEN-COLUMN WORK SHEET

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

If a balance is not up to date as of the last day of the fiscal period, it must be adjusted.

THE TEN-COLUMN WORK SHEET

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

Section 18.1

Three Types of Inventory

BeginningInventory

EndingInventory

PhysicalInventory

beginning inventoryThe merchandise a business has on hand at the

beginning of a period.

THE TEN-COLUMN WORK SHEET

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

Three Types of Inventory

BeginningInventory

EndingInventory

PhysicalInventory

ending inventoryThe merchandise a business has on hand at the

end of a period.

THE TEN-COLUMN WORK SHEET

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

Section 18.1

Three Types of Inventory

BeginningInventory

EndingInventory

PhysicalInventory

physical inventoryAn actual count of all merchandise on hand

and available for sale.

THE TEN-COLUMN WORK SHEET

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

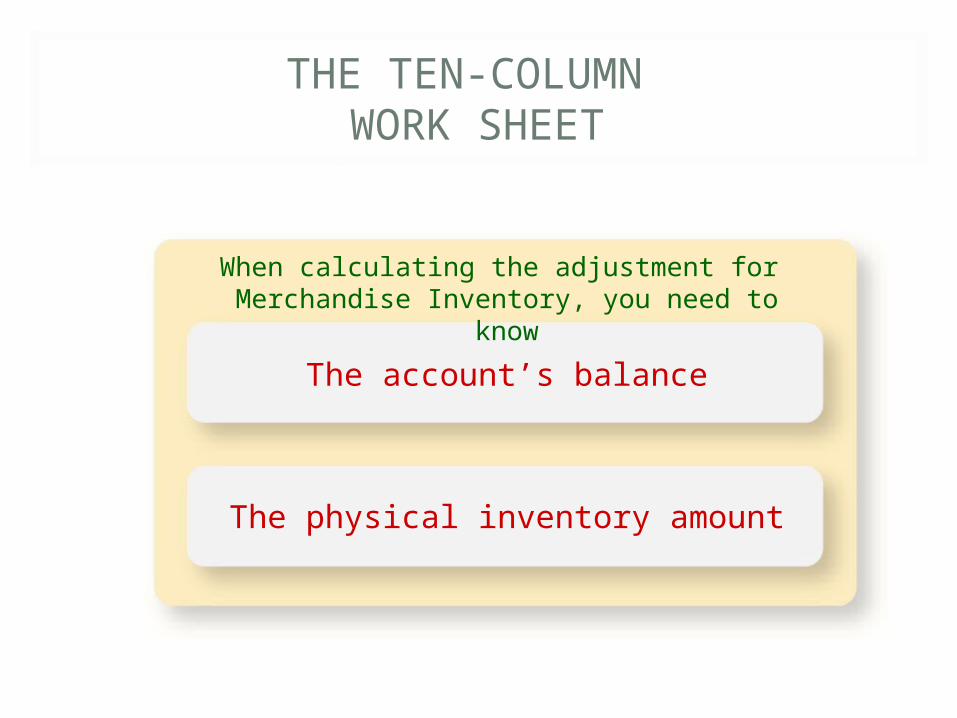

When calculating the adjustment for Merchandise Inventory, you need to know

The account’s balance

The physical inventory amount

THE TEN-COLUMN WORK SHEET

Glencoe Accounting

Identifying Accounts to be Adjusted and AdjustingMerchandise Inventory

Adjusting the Merchandise Inventory Account

Adjustment

To adjust the Merchandise Inventory account (bal. 84,921) to reflect the physical inventory amount ($81,385), the following transaction is recorded.

See pages 524–525

Glencoe Accounting

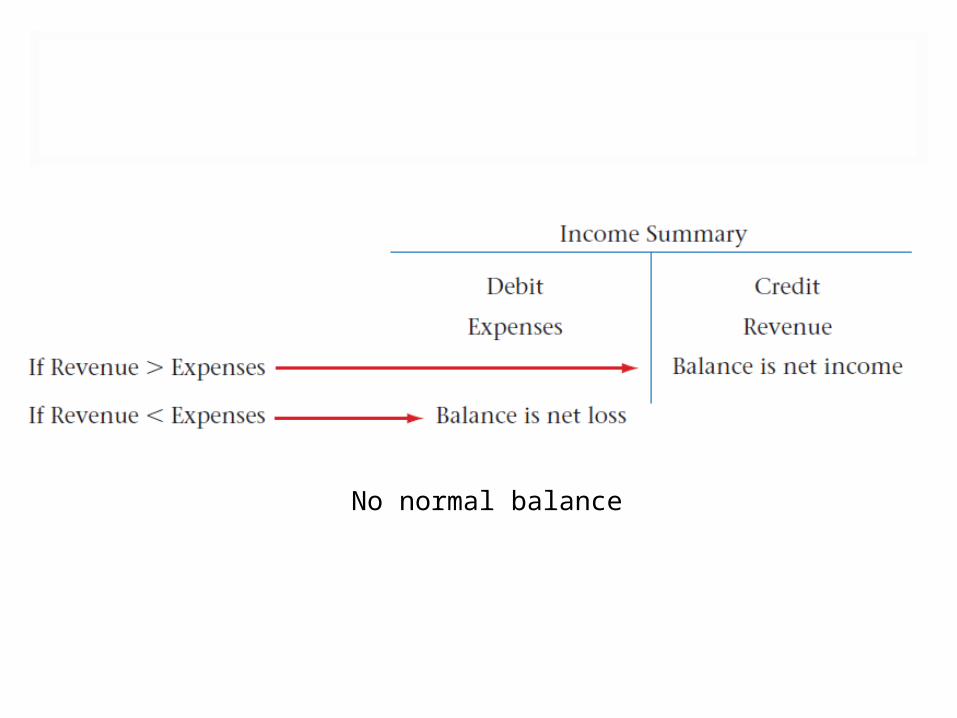

No normal balance

Glencoe Accounting

Glencoe Accounting

Key Term

prepaid expense

Adjusting Supplies, Prepaid Insurance, and Federal

Corporate Income Tax

ADJUSTING THE SUPPLIES ACCOUNT

Glencoe Accounting

Adjusting Supplies, Prepaid Insurance, and Federal

Corporate Income TaxSection 18.2

As supplies are used, they become expenses of

the business.

A physical inventory is taken at the end of the period to make an

adjustment to the Supplies account.

ADJUSTING THE SUPPLIES ACCOUNT

Glencoe Accounting

Adjusting Supplies, Prepaid Insurance, and Federal

Corporate Income Tax

Adjusting the Supplies Account

Adjustment

Record the adjustment for supplies.

Beg bal. $5,749 – on-hand $1,839 – supplies used up $3,710

ADJUSTING THE PREPAID INSURANCE ACCOUNT

Glencoe Accounting

Adjusting Supplies, Prepaid Insurance, and Federal

Corporate Income Tax

Insurance premiums are an example of a prepaid expense.

prepaid expenseAn expense paid in advance.

ADJUSTING THE PREPAID INSURANCE ACCOUNT

Glencoe Accounting

Adjusting Supplies, Prepaid Insurance, and Federal

Corporate Income Tax

Adjusting the Prepaid Insurance Account

Adjustment

Record the adjustment for the expiration of one-half month’s insurance coverage.

$1,500 for a 6 month premium = $250/month purchased Dec 15

ADJUSTING THE FEDERAL CORPORATE INCOME TAX ACCOUNTS

Glencoe Accounting

Adjusting Supplies, Prepaid Insurance, and Federal

Corporate Income Tax

When the exact

amount of federal

corporate income

tax is determined:

Additional tax may need to be paid.

The company may qualify for a refund.

Glencoe Accounting

Key Terms

adjusting entries

Completing the Work Sheetand Journalizing and Posting

the Adjusting EntriesSection 18.3

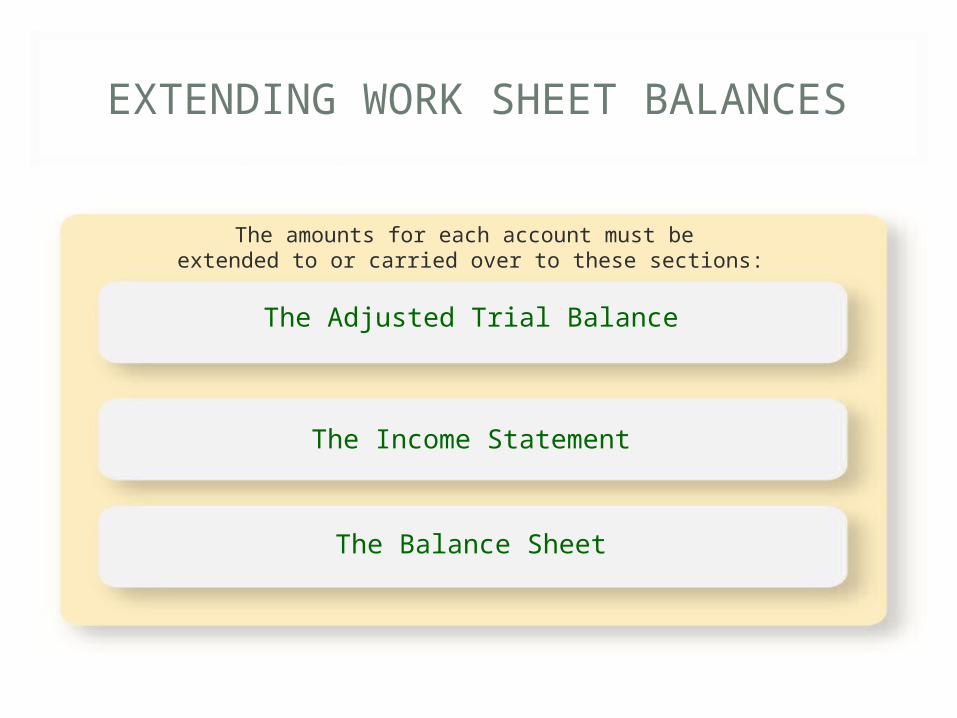

EXTENDING WORK SHEET BALANCES

Glencoe Accounting

Completing the Work Sheetand Journalizing and Posting

the Adjusting Entries

The amounts for each account must be extended to or carried over to these sections:

The Adjusted Trial Balance

The Income Statement

The Balance Sheet

EXTENDING WORK SHEET BALANCES

Glencoe Accounting

Completing the Work Sheetand Journalizing and Posting

the Adjusting Entries

Each account in

the Adjusted Trial

Balance section is

extended to one

of the following

sections:

The Income Statement section, containing temporary account

balances

The Balance Sheet section, containing permanent account

balances

JOURNALIZING AND POSTING ADJUSTING ENTRIES

Glencoe Accounting

Completing the Work Sheetand Journalizing and Posting

the Adjusting Entries

Adjusting entries come from the Adjustments section of the work sheet.

adjusting entriesJournal entries that update the general ledger

accounts at the end of a period.

JOURNALIZING AND POSTING ADJUSTING ENTRIES

Glencoe Accounting

Completing the Work Sheetand Journalizing and Posting

the Adjusting EntriesSection 18.3

Entries Recorded in the Adjustments Column

Adjusting Merchandise Inventory

Adjusting Supplies

Adjusting Insurance

Adjusting Income Tax

JOURNALIZING AND POSTING ADJUSTING ENTRIES

Glencoe Accounting

Completing the Work Sheetand Journalizing and Posting

the Adjusting EntriesSection 18.3

Adjusting entries are recorded in the general journal and

then posted to the general ledger accounts.

This will cause the general ledger account balances to

agree with the Income Statement and Balance Sheet

sections.

JOURNALIZING AND POSTING ADJUSTING ENTRIES

Glencoe Accounting

Completing the Work Sheetand Journalizing and Posting

the Adjusting EntriesSection 18.3 Posting Adjusting Entries to the General Ledger

JOURNALIZING AND POSTING ADJUSTING ENTRIES

Glencoe Accounting

Completing the Work Sheetand Journalizing and Posting

the Adjusting EntriesSection 18.3 Posting Adjusting Entries to the General Ledger

JOURNALIZING AND POSTING ADJUSTING ENTRIES

Glencoe Accounting

Completing the Work Sheetand Journalizing and Posting

the Adjusting EntriesSection 18.3 Posting Adjusting Entries to the General Ledger

Glencoe Accounting

Question 1

After taking a physical inventory, you determined that the business has $132,755 of inventory on hand. The general ledger shows the Merchandise Inventory account with a balance of $139,400. What steps are needed to record the adjusting entry?

Step 1: The accounts Merchandise Inventory and Income Summary are affected.

Step 2: Merchandise Inventory is an asset account. Income Summary is a stockholder’s equity account.

Step 3: Merchandise Inventory is decreased by $6,645 ($139,400 - $132,755). This amount is transferred to Income Summary.

Step 4: To transfer the decrease in Merchandise Inventory, debit Income Summary for $6,645

Step 5: Decreases in asset accounts are recorded as credits. Credit Merchandise Inventory for $6,645.

Glencoe Accounting

Question 2

Given the following information, determine what adjustments need to be made to the accounts. Indicate the amounts of the adjustments.

Glencoe Accounting

Question 2

The adjustments that need to be made are shown below:

Glencoe Accounting

Question 3

Explain the matching principle and why it is important to accounting.

The matching principle requires recording revenues in the period they are earned and recording expenses that were incurred to make those revenues in the same period. This may not be when expenses or revenues are paid or collected. By matching expenses and revenues, the matching principle provides an accurate measure of net income. For example, if you pay for (prepay) six months of insurance on one date, that expense is spread over the six months in which the policy is in effect. The cost of each month’s portion of the policy’s premium must be expensed in that month (1/6 of the total cost) so that records accurately reflect expenses. Having this information allows comparisons to be made for similar periods.

![· Gift]Awards/MemoriaIs Expense Legal Services Food/Beverage Expense Polling Expense Printing Expense Salaries/Wages/Contract Labor Solicitation/Fundraising Expense](https://static.fdocuments.net/doc/165x107/5c5ef74209d3f2515c8cf3a9/-giftawardsmemoriais-expense-legal-services-foodbeverage-expense-polling-expense.jpg)