Chapter 9 Work Sheet and Adjustments for a Merchandising ... · PDF fileChapter 9 Work Sheet...

32

Chapter 9 Work Sheet and Adjustments for a Merchandising Business 1 Adjustments for the Merchandise Inventory account Complete a work sheet for a merchandising business Merchandise Inventory adjustment and Worksheet Using Perpetual Inventory system

-

Upload

truongthuy -

Category

Documents

-

view

231 -

download

1

Transcript of Chapter 9 Work Sheet and Adjustments for a Merchandising ... · PDF fileChapter 9 Work Sheet...

Chapter 9 Work Sheet and Adjustments for a Merchandising Business

1

Adjustments for the Merchandise Inventory account

Complete a work sheet for a merchandising business

Merchandise Inventory adjustment and Worksheet Using Perpetual Inventory system

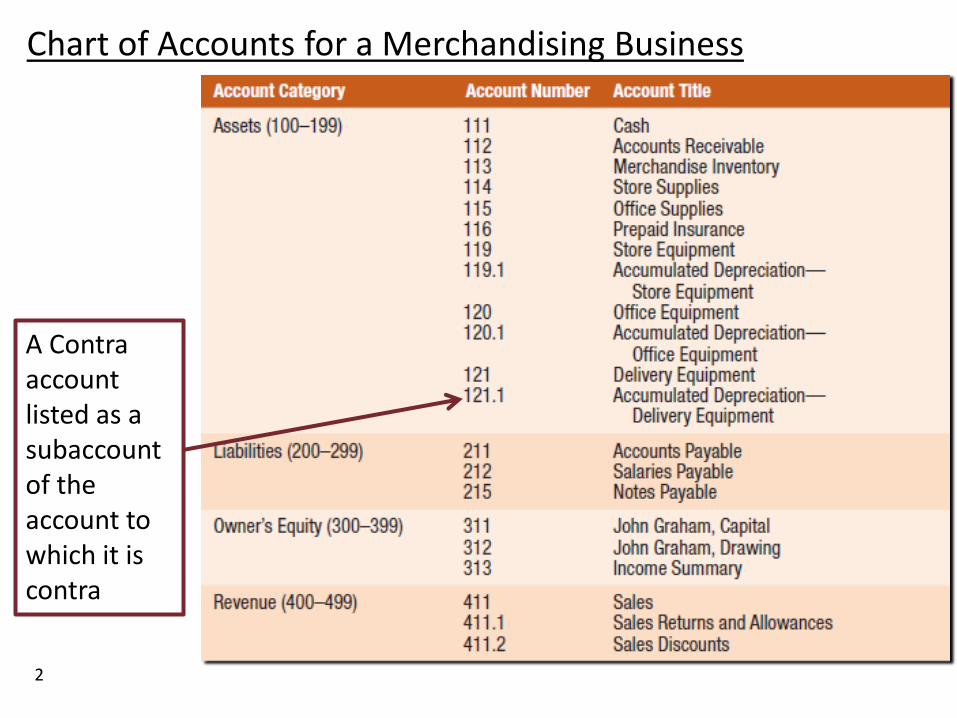

Chart of Accounts for a Merchandising Business

2

A Contra account listed as a subaccount of the account to which it is contra

Chart of Accounts for a Merchandising Business (continued)

3

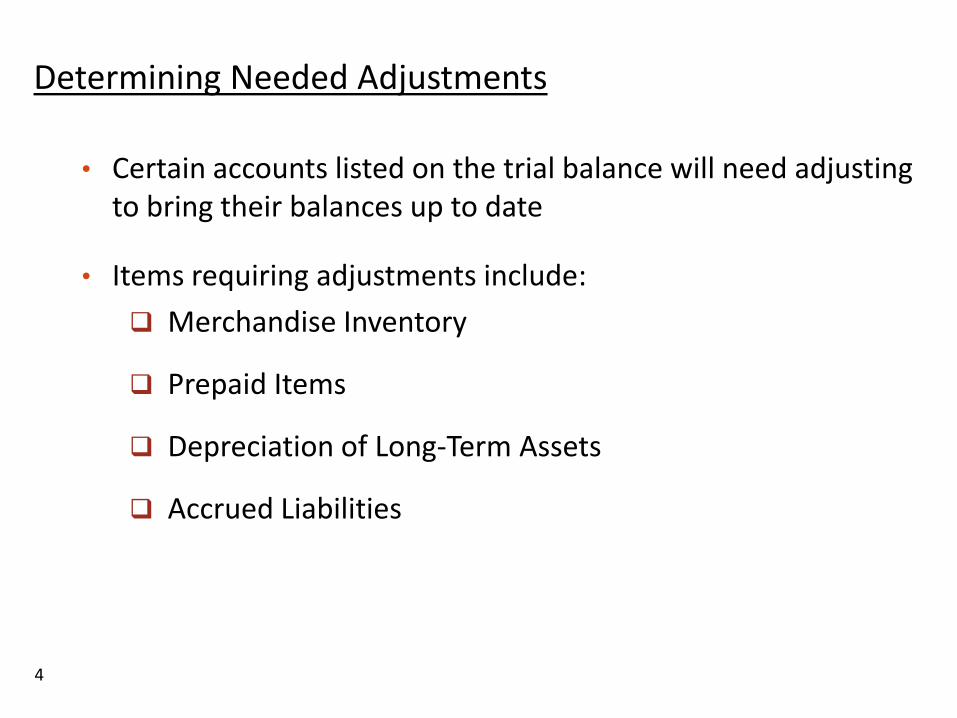

Determining Needed Adjustments

• Certain accounts listed on the trial balance will need adjusting to bring their balances up to date

• Items requiring adjustments include:

Merchandise Inventory

Prepaid Items

Depreciation of Long-Term Assets

Accrued Liabilities

4

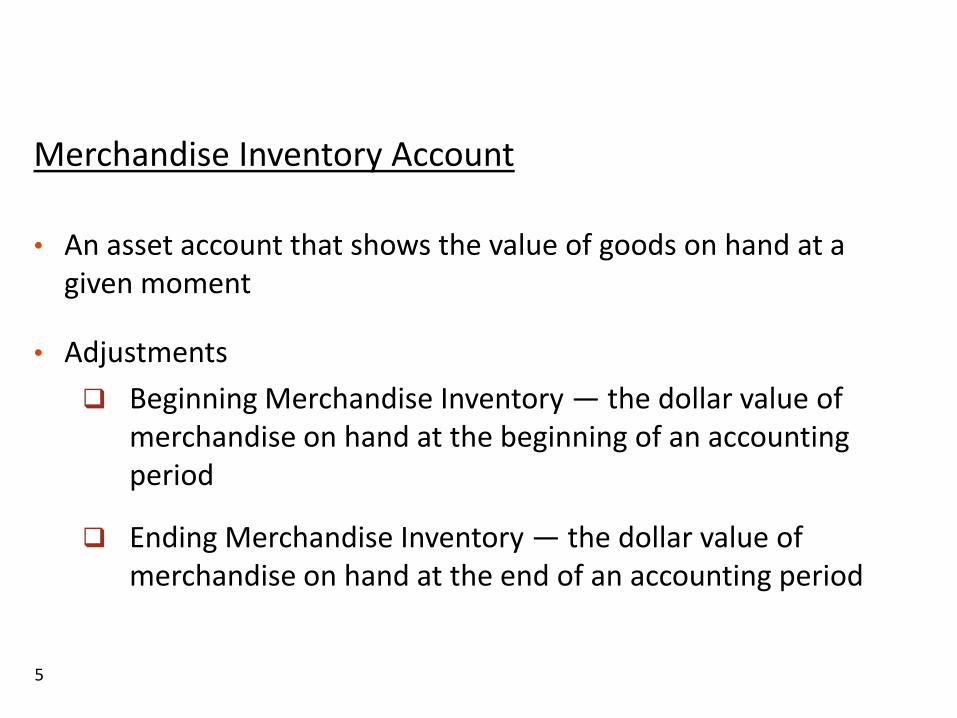

Merchandise Inventory Account

• An asset account that shows the value of goods on hand at a given moment

• Adjustments

Beginning Merchandise Inventory — the dollar value of merchandise on hand at the beginning of an accounting period

Ending Merchandise Inventory — the dollar value of merchandise on hand at the end of an accounting period

5

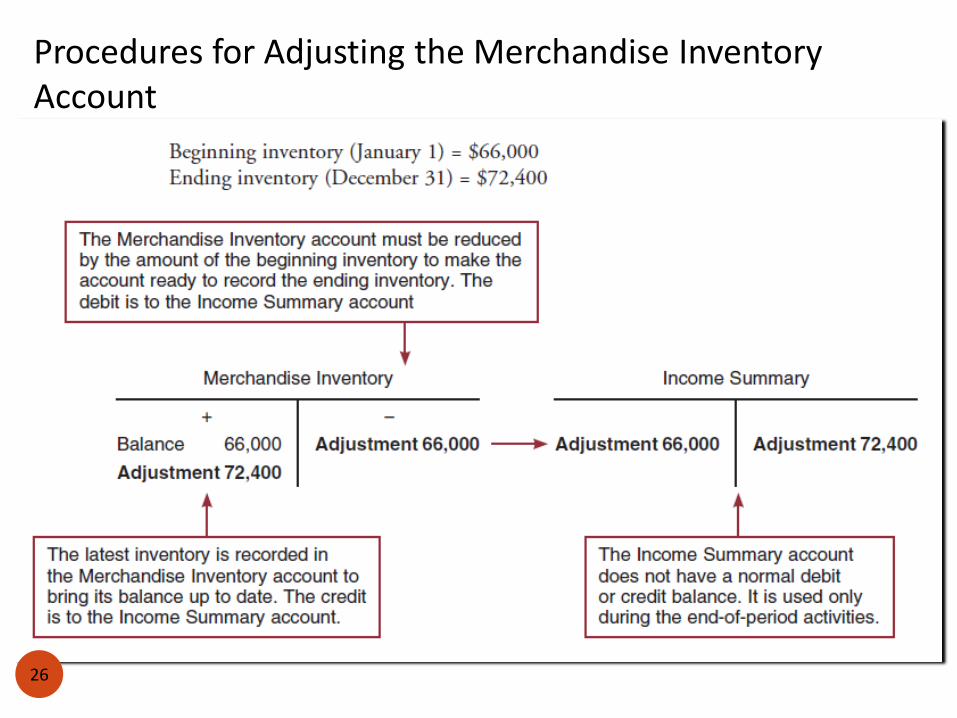

Adjustment for Merchandise Inventory

Step 1. Transfer the Beginning Inventory figure from the Merchandise Inventory account to the Income Summary account. (Assume the beginning inventory was $66,000)

6

The Income Summary account does not have a normal debit or credit balance.

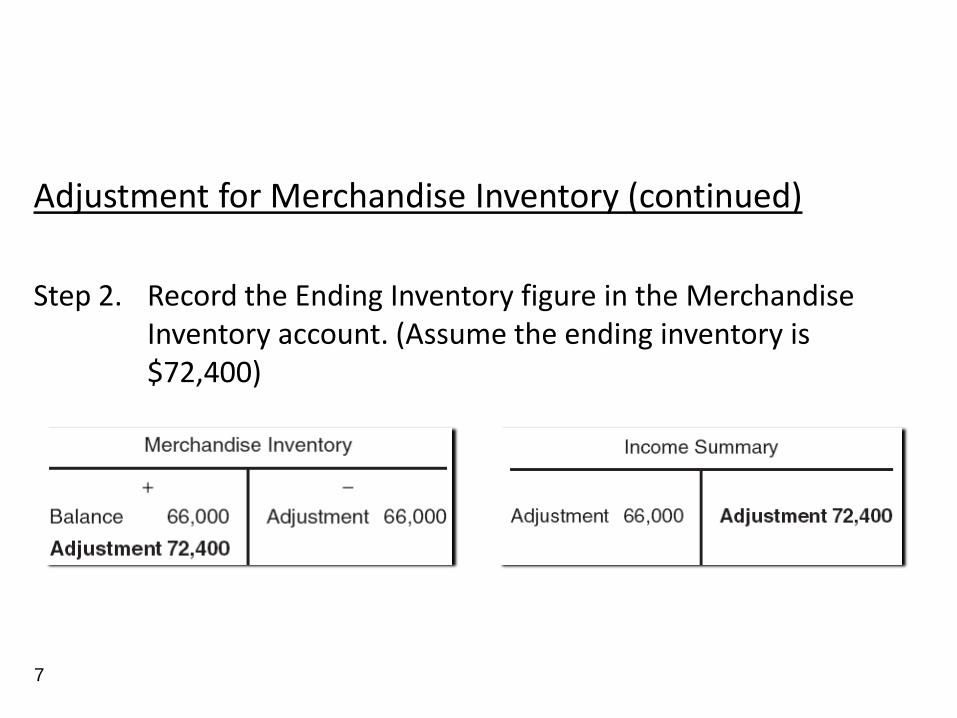

Adjustment for Merchandise Inventory (continued)

Step 2. Record the Ending Inventory figure in the Merchandise Inventory account. (Assume the ending inventory is $72,400)

7

Remember!

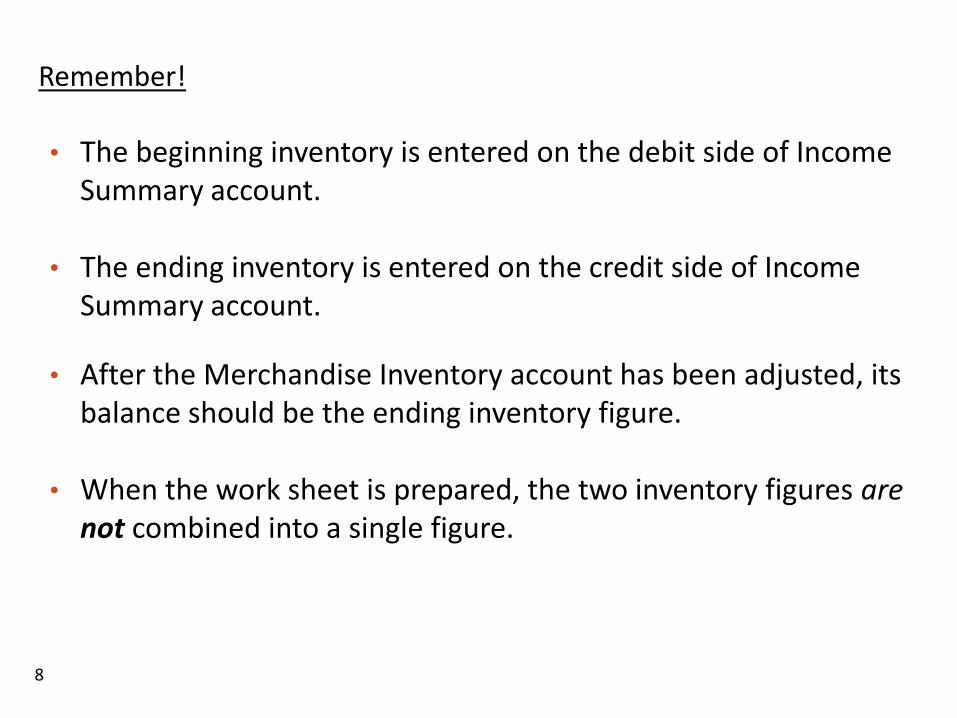

• The beginning inventory is entered on the debit side of Income Summary account.

• The ending inventory is entered on the credit side of Income Summary account.

• After the Merchandise Inventory account has been adjusted, its balance should be the ending inventory figure.

• When the work sheet is prepared, the two inventory figures are not combined into a single figure.

8

Adjustment for Store Supplies Used

Assume the Store Supplies account has a balance before adjustment of $2,015.

An inventory account on December 31 shows $500 of supplies still on hand.

Therefore $1,515 of supplies has been used during the accounting period.

9

Store Supplies Expense

+ -

Adjustment 1,515

Store Supplies

+ -

Balance 2,015 Adjustment 1,515

Adjustment for Office Supplies Used

Assume the Office Supplies account has a balance before adjustment of $667.

An inventory account on December 31 shows $250 of supplies still on hand.

Therefore $417 of supplies have been used during the accounting period.

10

Office Supplies Expense

+ -

Adjustment 417

Office Supplies

+ -

Balance 667 Adjustment 417

Adjustment for Insurance Expired

Assume the Prepaid Insurance account has a balance before adjustment of $720, representing a two-year insurance policy, purchased on Oct. 1.

The amount of insurance will be $720 24 months or $30 per month.

The depreciation for October 1 through December 31 will be for $90 ($30 3 months).

11

Depreciation of Office Equipment and Office Furniture

• Depreciation — describes the expense that results from the loss in usefulness of an asset due to age, wear and tear, and obsolescence

• The purpose of depreciation accounting — to spread the cost of an asset over its useful life rather than treating the asset’s cost as an expense in the year it was purchased

12

Depreciation Calculations

The straight-line method is one of the most popular depreciation methods that yield the same amount of depreciation for each full period an asset is used.

13

= Annual depreciation expense Cost of asset – Trade-in value

Estimated years of usefulness

Assume delivery equipment costs $56,000 with a trade-in value of $800.

The delivery equipment has a useful life of 6 years.

The annual depreciation will therefore be

($56,000 – $800) 6 years = $9,200 per year.

The Depreciation Entry

Depreciation is always recorded by

Debiting an expense account — Depreciation Expense

Crediting an account — Accumulated Depreciation

Contra asset account

Always has a credit balance

14

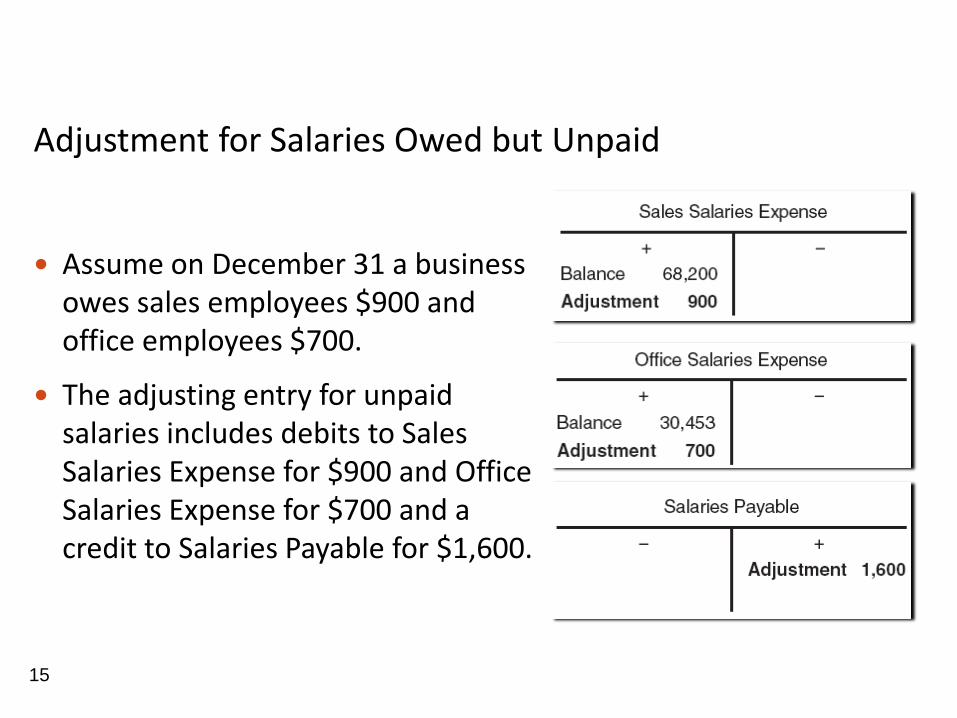

Adjustment for Salaries Owed but Unpaid

Assume on December 31 a business owes sales employees $900 and office employees $700.

The adjusting entry for unpaid salaries includes debits to Sales Salaries Expense for $900 and Office Salaries Expense for $700 and a credit to Salaries Payable for $1,600.

15

End-of-Period Work Sheet

• An informal working paper is used by the accountant to

Organize data

Make end-of-period work easier

• Not a financial statement, never be published

• An excellent tool that is widely used, particularly by large businesses that could have hundreds of adjustments

16

The Trial Balance and Adjustments Columns 17

The Trial Balance and Adjustments Columns

18

The Adjusted Trial Balance Columns

• If an account does not have an adjustment, carry over the Trial Balance figure to the appropriate Adjusted Trial Balance column.

• The ending balance for Merchandise Inventory is carried over to the debit Adjusted Trial Balance column.

• If an account has a debit balance, and the adjustment is a credit, the difference between the two amounts is entered in the Adjusted Trial Balance Debit column.

19

The Adjusted Trial Balance Columns

• If an account has a debit balance, and the adjustment is also a debit, add the two figures and move the total to the Adjusted Trial Balance Debit column.

• If an account has a credit balance, and the adjustment is also a credit, add the two figures and enter the total in the Adjusted Trial Balance Credit column.

• If an account has a credit balance, and the adjustment is a debit, the difference between the two amounts is entered in the Adjusted Trial Balance Credit column.

20

The Adjusted Trial Balance Columns

• If an account does not have a balance in the Trial Balance columns, but there is an adjustment, the amount of the adjustment becomes the balance.

• Both the debit adjustment and the credit adjustment to the Income Summary account are moved over to the Adjusted Trial Balance columns. We do this because both figures will appear on the income statement, which is prepared from the completed work sheet.

21

Remember!

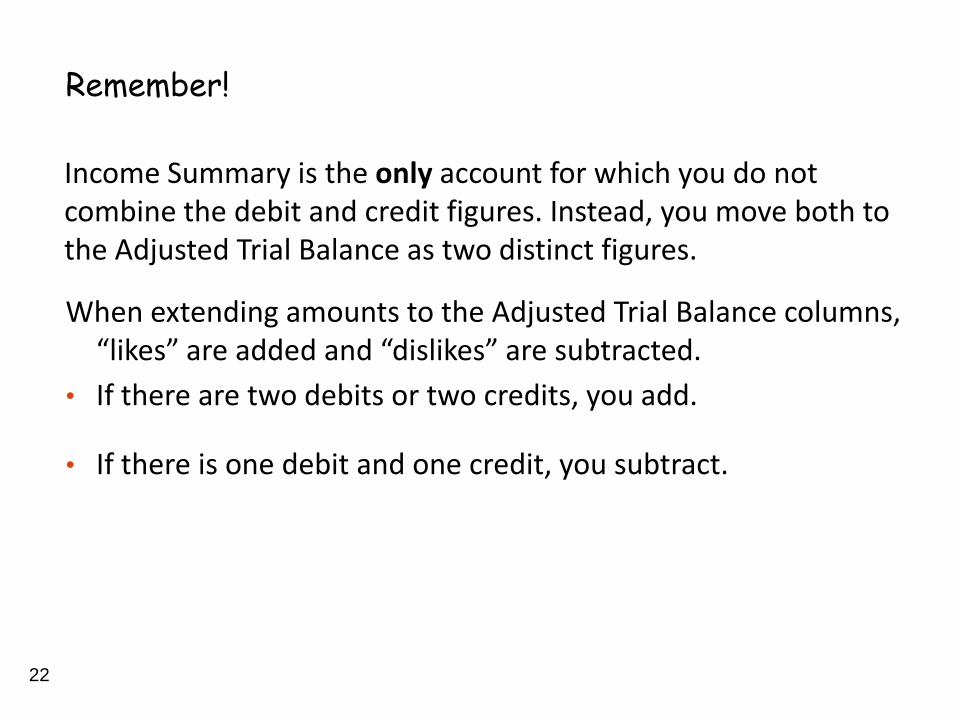

Income Summary is the only account for which you do not combine the debit and credit figures. Instead, you move both to the Adjusted Trial Balance as two distinct figures.

22

When extending amounts to the Adjusted Trial Balance columns, “likes” are added and “dislikes” are subtracted.

• If there are two debits or two credits, you add.

• If there is one debit and one credit, you subtract.

The Financial Statement Columns

From the Adjusted Trial Balance Columns:

• Assets and the owner’s drawing account are moved to the Balance Sheet Debit column.

• Accumulated depreciation, liabilities, and the owner’s capital account are moved to the Balance Sheet Credit column.

• Both amounts shown for the Income Summary account are moved to the Income Statement columns.

From the Adjusted Trial Balance Columns:

• Revenue and contra purchases accounts (Purchase Returns and Allowances and Purchases Discounts) are moved to the Income Statement Credit column.

• Expenses, Purchases, and contra sales accounts (Sales Returns and Allowances and Sales Discounts) are moved to the Income Statement Debit column.

23

Completing the Work Sheet

1. Total the Income Statement Debit and Credit columns.

2. Total the Balance Sheet Debit and Credit columns.

3. Determine the amount of net income (or net loss) by finding the difference between the Income Statement Credit column and the Income Statement Debit column.

4. Write the words net income (or net loss) in the Account Title column.

5. Enter the net income figure under the Income Statement Debit column and the Balance Sheet Credit column. If a net loss exists, the net loss figure is entered under the Income Statement Credit column and the Balance Sheet Debit column.

6. Retotal the Income Statement columns and the Balance Sheet columns as an arithmetic check.

7. Double rule the column totals. 24

Summary of Steps to Complete the Financial Statement Columns of a Work Sheet

25

Procedures for Adjusting the Merchandise Inventory Account

26 26

Appendix D Merchandise Inventory Adjustment and Work Sheet Using the Perpetual Inventory System

27 27

Make adjusting entries to record inventory shortages or overages

Prepare a work sheet for a company using the perpetual inventory system

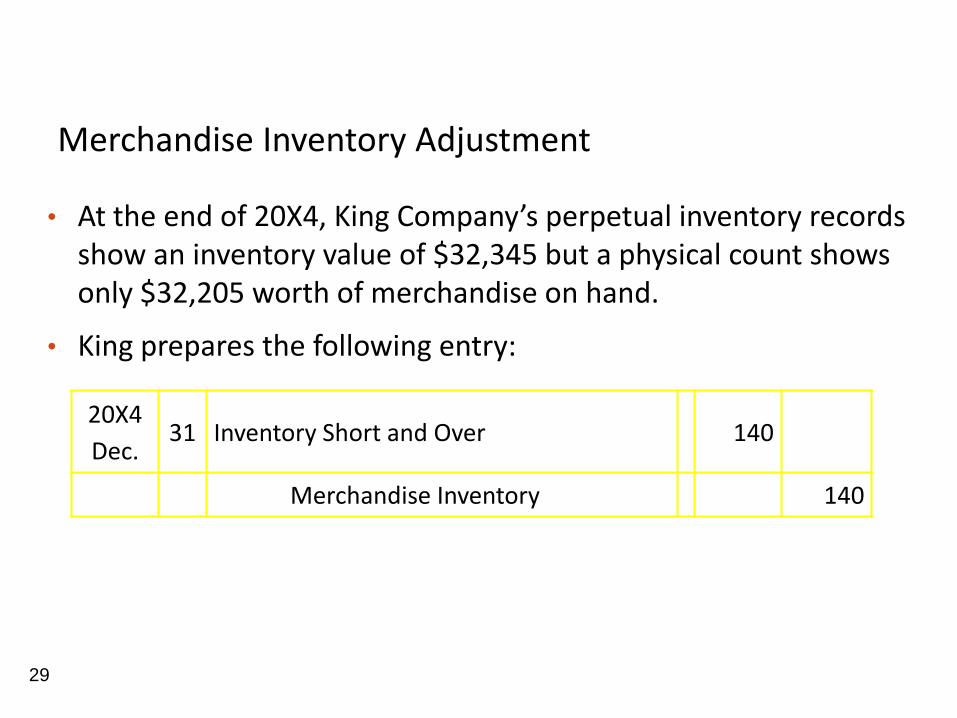

Merchandise Inventory Adjustment

• A physical inventory is needed under a perpetual inventory system so the actual quantity on hand can be compared to the merchandise inventory account.

• If there is a difference between the physical count and the perpetual records, it is necessary to make an adjusting entry to correct the records.

• The Inventory Short and Over account is used to reconcile the perpetual records to the actual inventory count.

28

Merchandise Inventory Adjustment

• At the end of 20X4, King Company’s perpetual inventory records show an inventory value of $32,345 but a physical count shows only $32,205 worth of merchandise on hand.

• King prepares the following entry:

29

20X4

Dec. 31 Inventory Short and Over 140

Merchandise Inventory 140

More on Merchandise Inventory Adjustment

• Now let’s assume at the end of 20X4, King Company’s perpetual inventory records show an inventory value of $32,345 but a physical count shows $32,400 worth of merchandise on hand.

• King prepares the following entry:

30

20X4

Dec. 31 Merchandise Inventory 55

Inventory Short and Over 55

Work Sheet for a Company Using the Perpetual Inventory System

In a periodic inventory system, we adjusted the Merchandise Inventory account with two entries.

Beginning Inventory

Debit Income Summary

Credit Merchandise Inventory

Ending Inventory

Debit Merchandise Inventory

Credit Income Summary

31

Work Sheet of a Company Using the Perpetual Inventory System

• Under the perpetual system, these adjusting entries are not needed because the inventory is updated each time goods are bought and sold.

• With the exception of the adjustments for Merchandise Inventory, the work sheet for a company using the perpetual inventory system is identical to one using the periodic inventory system.

• A work sheet for a company using the perpetual inventory system can be found in your textbook App. D.

32