ACA: YEAR 2

16

ACA : YEAR 2 WHAT SHOPPERS DID... AND WHY Survey results and strategic insights for health insurance marketers Post-Enrollment Survey: April 2015

Transcript of ACA: YEAR 2

ACA: YEAR 2WHAT SHOPPERS DID... AND WHYSurvey results and strategic insights for health insurance marketers

Post-Enrollment Survey: April 2015

READ ON TO SEE THE FINDINGS.

With the second ACA Open Enrollment period in the books, some obvious trends are solidifying – AND NEW CHALLENGES ARE EMERGING.

Competiscan and health care marketing agency Media Logic teamed up again to better understand how Exchange consumers shop for, choose and use their health plans – to help health insurers improve the member experience and prepare for Open Enrollment.

Survey insights include...

How many Exchange consumers chose a new insurer for 2015 – and why

Better ways to target and talk to prospects

The importance of onboarding for “self-help” consumers

Advice to improve member retention

© 2015 Competiscan, LLC & Media Logic USA, LLC.

31

SWITCHEDTO A NEW HEALTH INSURER FOR 2015

The fact that almost 1/3 (32%) of Exchange consumers decided to switch insurers is concerning. For instance, only 13% of Medicare members change insurers each year, and less than 8% of consumers on employer-sponsored plans make a change (per HHS March 2015). Retention will clearly be an annual challenge for Exchange products.

Retention Insights (among consumers returning to the Exchange)

© 2015 Competiscan, LLC & Media Logic USA, LLC.

DIFFERENT PLAN DIFFERENT INSURANCE COMPANY14%

DIFFERENT PLAN SAME INSURANCE COMPANY21%

SIMILAR PLAN DIFFERENT INSURANCE COMPANY18%

RENEW SAME PLAN, SAME INSURANCE COMPANY48%

In the most recent Open Enrollment, did you:

I HAD CHOSEN TO AUTOMATICALLY RENEW MY PLAN WHEN I SIGNED UP LAST YEAR6%

IT WAS EASIER THAN SWITCHING TO A NEW PLAN20%

I SHOPPED FOR OTHER PLANS BUT DIDN’T SEE ANYTHING BETTER18%

I AM SATISFIED WITH MY CURRENT PLAN & INSURANCE COMPANY67%

If you renewed your health plan, why?

Here’s a closer look at the retention numbers and the reasons that consumers renewed. The top reason to stay: “I am satisfied with my current plan and insurance company.” Insurers will need to increase this satisfaction – with better plan design, onboarding and customer experience – to maximize retention.

Retention Insights (among consumers returning to the Exchange)

© 2015 Competiscan, LLC & Media Logic USA, LLC.

PROVIDER NETWORK

#4MONTHLY PLAN COST(PREMIUM)#1 #3

OOP COSTS( DEDUCTIBLES OR COPAYS)

BENEFITS THAT MEET MY HEALTH NEEDS#2

NAME AND REPUTATION OF INSURANCE COMPANY

#5CUSTOMER SERVICE

#6TOP REASONS TO CHOOSE A PLAN

While it’s not surprising to see that premium cost is the top reason, it’s interesting that “benefits” and “out-of-pocket (OOP) costs” were perceived as more important than “provider network” or “reputation of company.” After a year of ACA, consumers have learned that benefits and OOP costs can vary significantly among the different metal levels... and they are becoming better informed when it comes to choosing a plan. Insurers must develop solutions that balance cost and coverage.

Plan Preferences

© 2015 Competiscan, LLC & Media Logic USA, LLC.

THAT THEY DID NOT RECEIVE AN ORIENTATION GUIDE WITH THEIR NEW HEALTH PLAN

REPORTED26%

Among those who did, 49% found it “moderately helpful” at best

With all the dollars being invested, are your onboarding materials working hard enough? Are they easy to navigate or just a “pile of stuff?” Have you thought of ways to personalize your materials to make them more relevant for each member?

The Bumpy Process of Onboarding

© 2015 Competiscan, LLC & Media Logic USA, LLC.

And only 36% fully understand how their deductibles workFULLY UNDERSTAND THEIR PLAN BENEFITS ONLY35%

SAID THEY

Managing deductibles and out-of-pocket dollars can be complicated – are you providing the tools and support that members need to feel in control of their health care?

The Bumpy Process of Onboarding

© 2015 Competiscan, LLC & Media Logic USA, LLC.

FULLY UNDERSTAND THE WELLNESS AND DISEASE MANAGEMENT PROGRAMS THAT CAME WITH THEIR PLANS

ONLY25%SAID THEY

If you offer wellness/disease management programs, are you merchandising them to your members to maximize usage and perceived value?

The Bumpy Process of Onboarding

© 2015 Competiscan, LLC & Media Logic USA, LLC.

ONLINE ACCOUNT INFORMATION

#1

PHONE

SUPPORT

#2 PHYSICIAN RATINGS/REVIEWS#3

COST COMPARISON TOOLS

#4 #5EMAIL COMMUNICATIONS

THE TOP 5 MOST HELPFUL TOOLS/RESOURCES

While a dedicated phone line is vital, self-service is the new normal – and transparency is key. In a post-ACA world, consumers need (and expect) easier ways to shop for doctors and manage their health care costs.

Supporting the DIY Health Consumer

© 2015 Competiscan, LLC & Media Logic USA, LLC.

VISITED A53%HEALTH INSURER’S WEBSITE

This was the most-cited shopping method by respondents – more than double any other. Insurers need to take a fresh look at their sites and make sure they are optimized for Exchange consumers:

Is it easy to find plan info and rates?

Do you offer a subsidy calculator and tools to help consumers estimate their costs?

Is your site responsive for mobile users?

Are you capturing leads with “request info” forms and other assets?

Do you offer live chat functionality?

Are you monitoring and leveraging usage data?

How Exchange Consumers Shop

© 2015 Competiscan, LLC & Media Logic USA, LLC.

And 18% used Google or YouTube

LOOKED AT25%HEALTH INSURER REVIEWS ONLINE

Take a moment and Google your health plan.

How would you react to the results if you were a shopper? You obviously can’t control everything that’s said online, but effective content marketing and strategic SEO can make an impact on what’s seen by shoppers.

Publish positive content such as awards, ratings, community relations and membership growth. Respond to both positive and negative comments on third party sites, or follow up directly (this demonstrates that you take customer feedback seriously).

How Exchange Consumers Shop

© 2015 Competiscan, LLC & Media Logic USA, LLC.

NEW HEALTH PLAN

READ DIRECT MAIL FROM HEALTH INSURERS22%

SPOKE WITH AN INSURANCE BROKER10%

ATTENDED AN INFORMATIONAL MEETING3%ONLY

DM is still a great way to make your case.

Don’t forget about supporting the broker channel and private insurance agents.

Though results may vary by market, insurers should question if developing, promoting and staffing these events is worth the investment for Exchange consumers.

How Exchange Consumers Shop

© 2015 Competiscan, LLC & Media Logic USA, LLC.

“ Simplify! It is crazy that you have to read a novel-length write-up and are still not able to understand if your basic needs will be covered.”

SIMPLIFY LANGUAGE / CLEARER COMMUNICATIONS (33%)

#1“ Make sure all customer service reps are taught the same thing; shorter phone wait times; better call center hours.”

#2 BETTER CUSTOMER SERVICE (26%)

“ Need how-to videos instead of waiting three hours on phone; provide more thorough information; make it easier to find doctors.”

#3BETTER WEBSITE FEATURES & FUNCTIONALITY (12%)

WE ASKED “WHAT’S THE ONE THING YOUR INSURER COULD DO TO MAKE YOUR EXPERIENCE BETTER?”

OTHER THAN “REDUCE COSTS,” THE TOP 3 THEMES WERE:

We hear it, loud and clear: consumers want more help, more support and less jargon.

Improving the Customer Experience

© 2015 Competiscan, LLC & Media Logic USA, LLC.

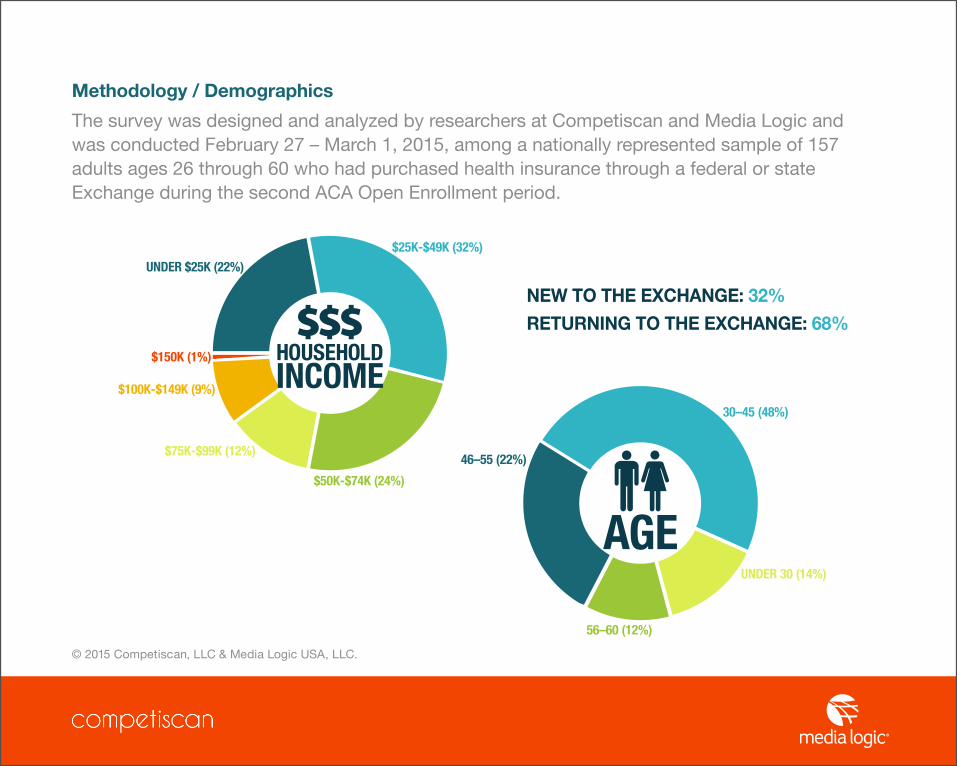

UNDER $25K (22%)

$75K-$99K (12%)

$100K-$149K (9%)

$150K (1%)

$25K-$49K (32%)

$50K-$74K (24%)

HOUSEHOLDINCOME

30–45 (48%)

56–60 (12%)

46–55 (22%)

UNDER 30 (14%)

AGE

Methodology / Demographics

The survey was designed and analyzed by researchers at Competiscan and Media Logic and was conducted February 27 – March 1, 2015, among a nationally represented sample of 157 adults ages 26 through 60 who had purchased health insurance through a federal or state Exchange during the second ACA Open Enrollment period.

NEW TO THE EXCHANGE: 32%

RETURNING TO THE EXCHANGE: 68%

© 2015 Competiscan, LLC & Media Logic USA, LLC.

About Competiscan

Founded in 2006, Competiscan provides its valued clients insights into the direct marketing strategies of competitors. Competiscan and its powerful web-based search utility monitors direct mail, email, mobile, online banners, print and social networking communications targeted at consumers, businesses, financial advisors, insurance producers and providers over time. As the market leader, Competiscan’s clients are better informed, leading to more effective communications and marketing with the ultimate goal of staying ahead of the competition. Visit www.competiscan.com for more information.

About Media Logic

Media Logic is a national leader in health care marketing – providing strategic, breakthrough solutions that drive business. Media Logic offers deep experience in branding and lead generation, and it is expert at turning research and segmentation data into actionable plans. Leveraging more than two decades of health plan marketing knowledge, Media Logic understands the nuances of group, Medicare and the individual market. From traditional ad campaigns to retention efforts to content marketing, everything Media Logic does is focused on generating results for clients… giving them an edge in a competitive, constantly changing environment. Visit www.medialogic.com for more information.

© 2015 Competiscan, LLC & Media Logic USA, LLC.

If you have any questions about this report or any of the topics covered, contact:

Richard Goldman CEO & Founder Competiscan

312.546.3489 [email protected]

Jim McDonald Director of Business Development Media Logic

866.353.3011 [email protected]

Learn more about Competiscan at competiscan.com

Learn more about Media Logic at medialogic.com and subscribe to its health care marketing newsletter at medialogic.com/signup