A Review of the Pharmaceutical Industry 2010/11€¦ · · 2012-03-08OneTouch Verio Blood Glucose...

43

A Review of the Pharmaceutical Industry 2010/11

Transcript of A Review of the Pharmaceutical Industry 2010/11€¦ · · 2012-03-08OneTouch Verio Blood Glucose...

A Review of the Pharmaceutical Industry

2010/11

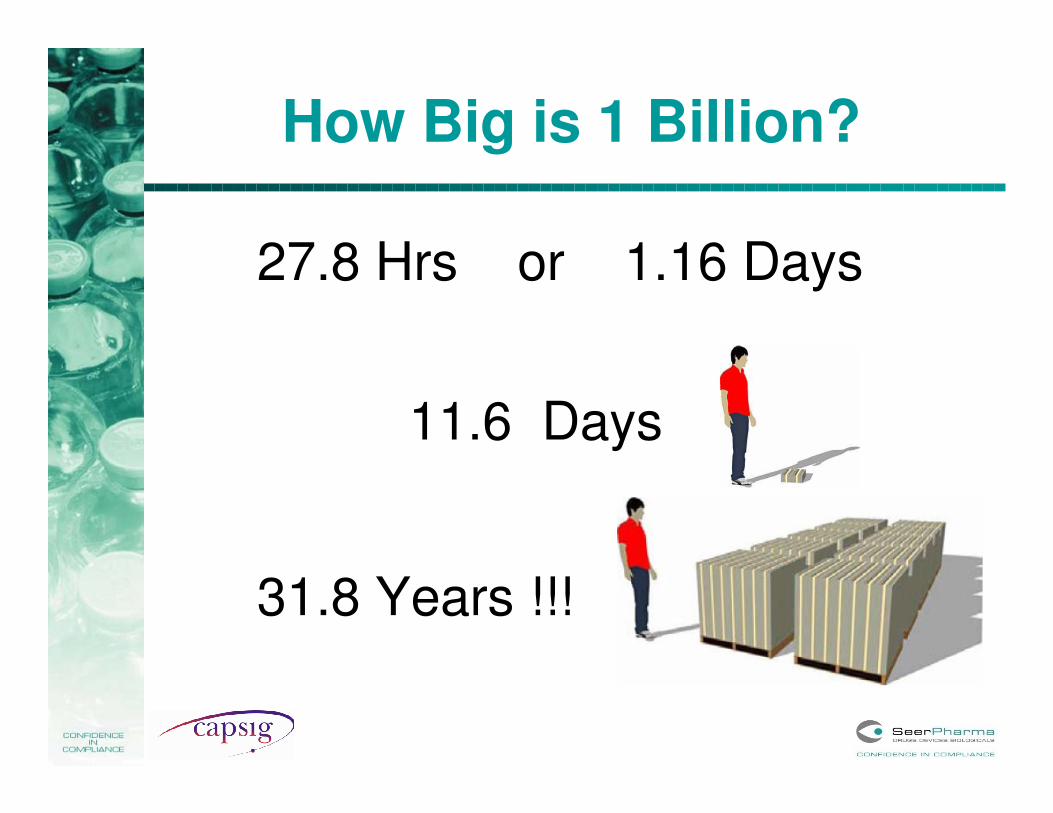

How Big is 1 Billion?

27.8 Hrs or 1.16 Days

11.6 Days

31.8 Years !!!

1 Trillion

International Market

393492 499

560605

651720

788 819 856 895

1067

0

200

400

600

800

1000

1200

Total World Market($US billions)

Source: IMS Health

International Market

0123456789

10% Growth Over Previous Year

Source: IMS Health

International Market

Source: IMS Health

Market Dynamics

• Robust Patient demand

• Growth of Pharmerging Markets – 14-17%

• Growth of Major Developed Markets – 3-6%

• Broad availability of Low Cost generics

• Growth of New Drugs for Oncology, Diabetes, MS, HIV

• Cuts in Public Health Spending

• Impact of Patent Expiries

• Closer Scrutiny of New Products

International Market

US

36%

EU5

17%

Rest of Europe

7%

Rest of World

8%

Pharmerging

18%

Canada

3%

Japan

11%

2010 Market Share $US

Source: IMS Health, The Global Use of Medicines: Outlook Through 2015, May 2011

International Market

Source: IMS Health, The Global Use of Medicines: Outlook Through 2015, May 2011

Source: The Lull Between Two Storms - www.pharmexec.com: May, 2011

International MarketTop 10 Pharmaceutical Companies 2010/11

International Market

Source: The Lull Between Two Storms - www.pharmexec.com: May, 2011

International Market

Source: The Lull Between Two Storms - www.pharmexec.com: May, 2011

International Market

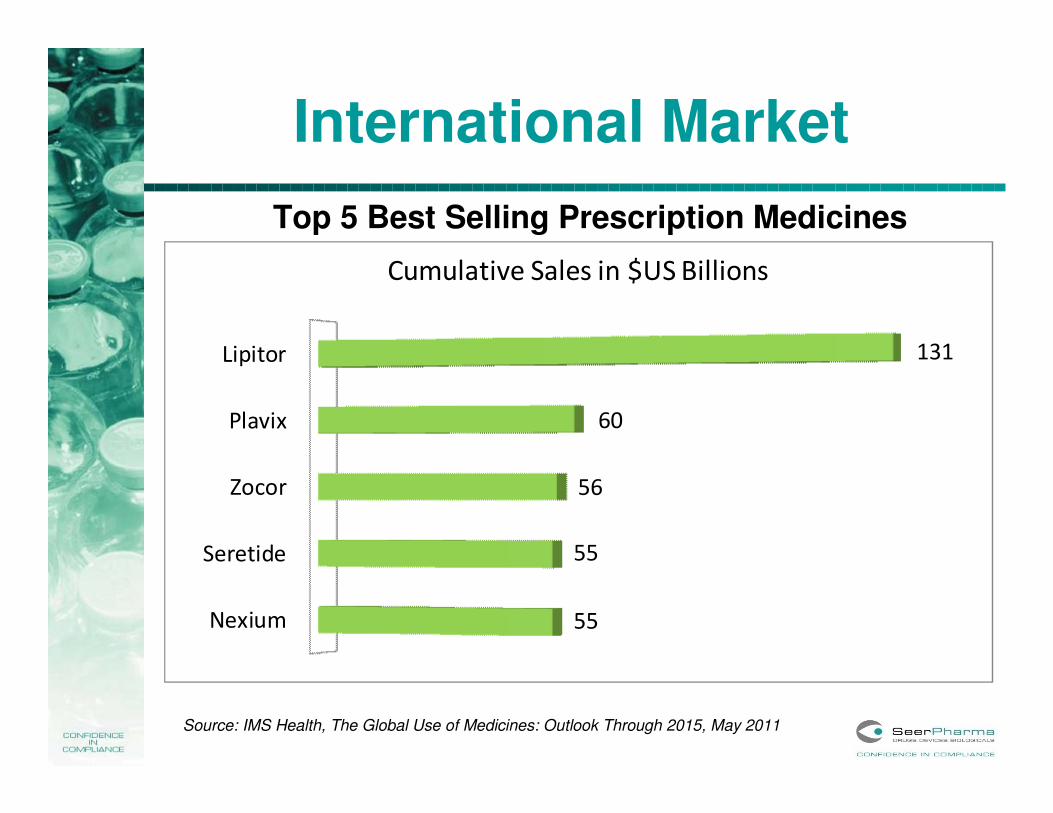

Nexium

Seretide

Zocor

Plavix

Lipitor

55

55

56

60

131

Cumulative Sales in $US Billions

Source: IMS Health, The Global Use of Medicines: Outlook Through 2015, May 2011

Top 5 Best Selling Prescription Medicines

International MarketOTC Pharmaceuticals

Source: The Rising Tide of OTC in Europe - www.imshealth.com

Total Pharma = $US856bnTotal OTC = $US100bn

International MarketOTC Pharmaceuticals

Source: The Rising Tide of OTC in Europe - www.imshealth.com

International MarketOTC Pharmaceuticals

Source: The Rising Tide of OTC in Europe - www.imshealth.com

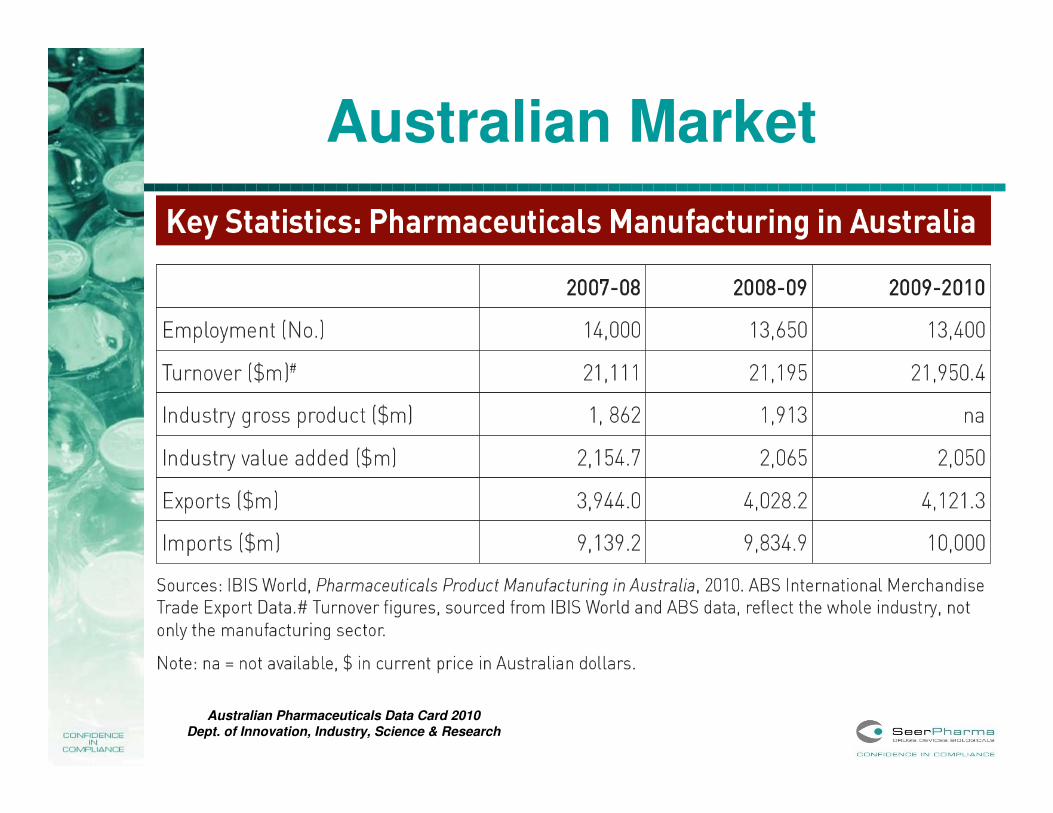

Australian Market

• Ranked 15th Largest in World

• 1% of Global Market Value

• Largest Exporter of manufactured goods -> $4.1 bn• Generics Account for approx 12% of Market• Export to 60+ markets

• Employs 1% of manufacturing workforce but produce almost 10% of manufacturing exports

• Highest manufacturing industry investor in R&D

• Employs >40,000 people, approx.13,400 in manufacturing

• Over last 4 yrs investment growth @ 6.2%/annum Australian manufacturing sector 19%

Australian Market

Australian Pharmaceuticals Data Card 2010

Dept. of Innovation, Industry, Science & Research

Australian Market

Australian Pharmaceuticals Data Card 2010

Dept. of Innovation, Industry, Science & Research

Australian Market

Australian Pharmaceuticals Data Card 2010

Dept. of Innovation, Industry, Science & Research

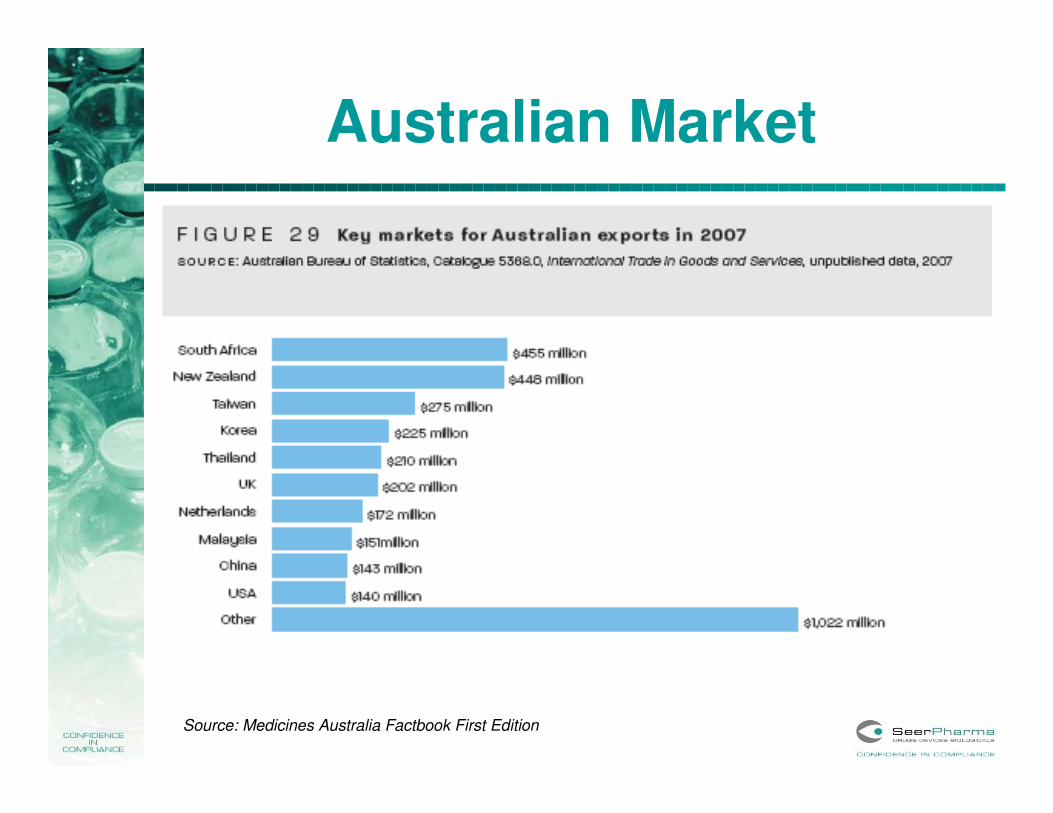

Australian Market

Source: Medicines Australia Factbook First Edition

Australian Market

Source: Medicines Australia Factbook First Edition

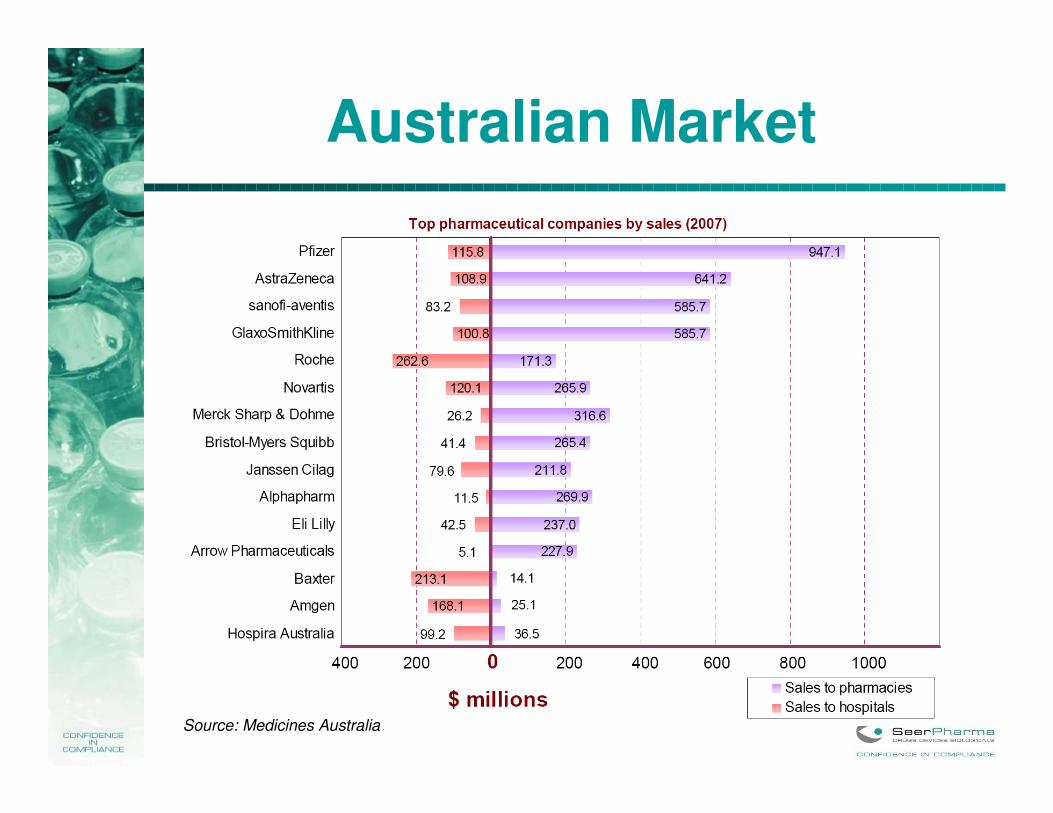

Australian Market

Source: Medicines Australia

Australian Manufacturing Market

Key Statistics Snapshot

Revenue Annual Growth06-11

Annual Growth11-16

$9.4bn 2.3% 2.6%

Profit Exports Businesses

$562.5m $4.1bn 151

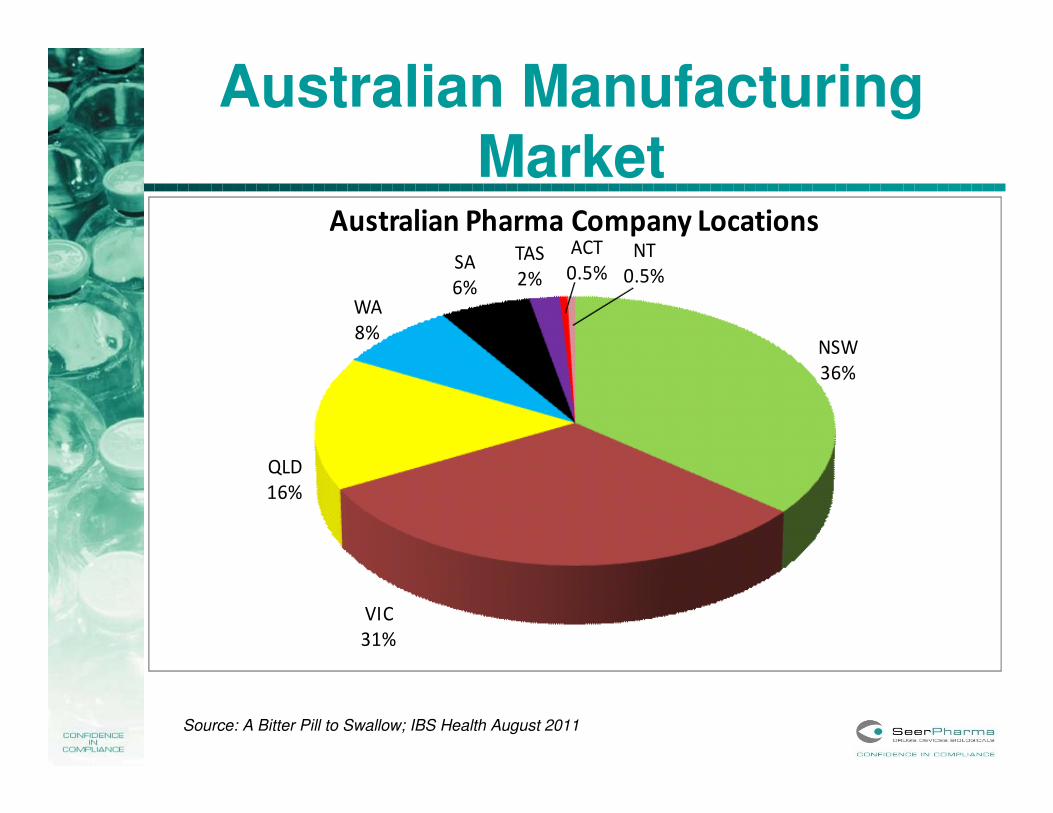

Australian Manufacturing Market

NSW

36%

VIC

31%

QLD

16%

WA

8%

SA

6%

TAS

2%

ACT

0.5%NT

0.5%

Australian Pharma Company Locations

Source: A Bitter Pill to Swallow; IBS Health August 2011

Australian MarketBiotech at a Glance

2006 2007 2008 2009 2010 2011

Number of ASX listed biotechs72 75 75 65* 64 62

Market Cap of listed biotechs (including CSL) (A$bn)

16.7 24.9 22.4 23.4 25.1 20.4

Market Cap of listed biotechs (excluding CSL) A$bn)3

4.8 4.9 2.1 4.2 4.0 4.7

Employment for publicly listed biotech companies (number) 9,180 8,350 8,820 9,770 10,480 N/A

Major Exports Intellectual Property, through licensing deals with large international pharmaceutical and biotechnology

companies.

*During 2009, 10 former BBI listed companies were either delisted following aquisition or left biotech for other industry sectors

Source: Medicines Australia Factbook First Edition

Biotech Business Indicators – Dept. of Innovation, Industry, Science & Research

Australian MarketBiotech at a Glance

Source: Medicines Australia Factbook First Edition

Biotech Business Indicators – Dept. of Innovation, Industry, Science & Research

Australian MarketBiotech at a Glance

Source: Medicines Australia Factbook First Edition

Biotech Business Indicators – Dept. of Innovation, Industry, Science & Research

Australian MarketGenerics

Employment in Generics Manufacturing 1,700 (2008)

Overall Employment in Generics Medicines Industry 5,000 (2008)

Value of Export Products $470 Mill (2009)

Key Export destinations Asia Europe, Canada, USA & NZ

Source: Medicines Australia Factbook First Edition & GMiA (www.gmia.com.au)

Australian MarketGenerics

Source: Medicines Australia Factbook First Edition

Leading Generics Medicines Companies’ Sales - 2008

Australian MarketNewsworthy Events

• Apsen Pharmacare’s acquisition of Sigma Pharmaceutical Division became effective

• TGA finally settled legal action arising form Pan Pharmaceuticals. Total cost to tax payer - $127.5M

• Sanofi acquired Genzyme

• Phebra announced plans for a $16M manufacturing facility in Sydney’s North West

• Federal Government announced deferral of PBS submissions

• Ascent Pharmaceuticals acquired by Indian pharmco, Strides Arcolab

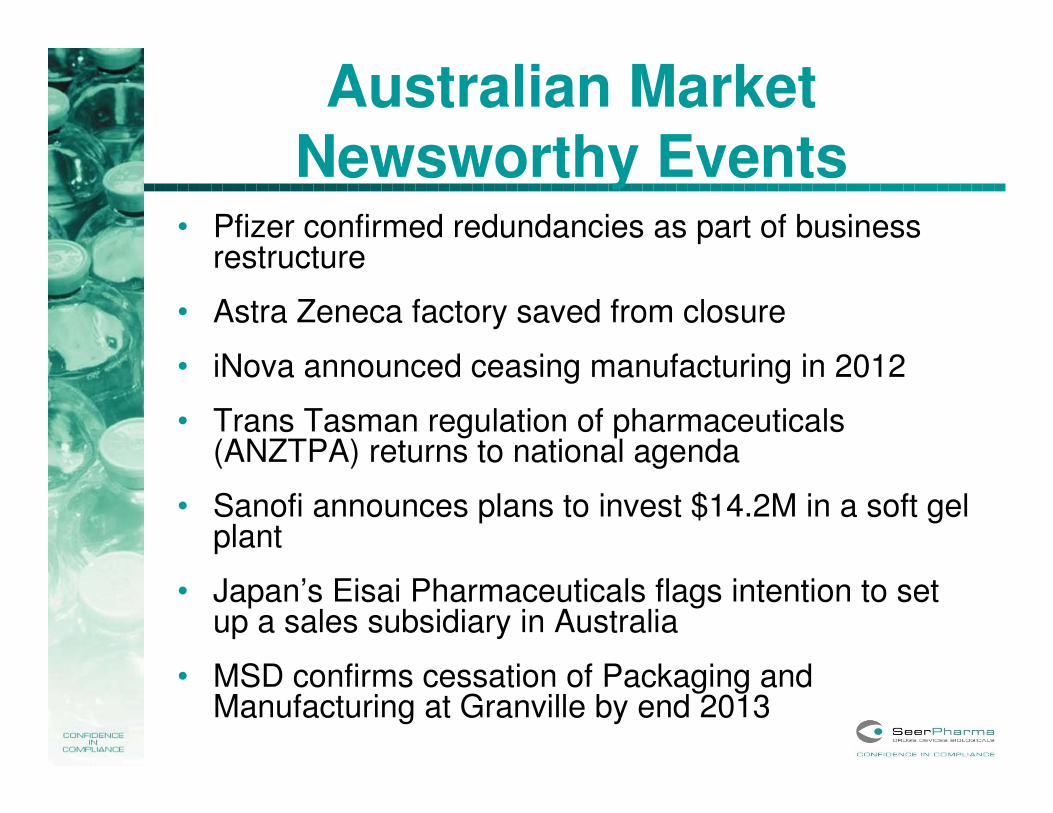

Australian MarketNewsworthy Events

• Pfizer confirmed redundancies as part of business restructure

• Astra Zeneca factory saved from closure

• iNova announced ceasing manufacturing in 2012

• Trans Tasman regulation of pharmaceuticals (ANZTPA) returns to national agenda

• Sanofi announces plans to invest $14.2M in a soft gel plant

• Japan’s Eisai Pharmaceuticals flags intention to set up a sales subsidiary in Australia

• MSD confirms cessation of Packaging and Manufacturing at Granville by end 2013

Product Recalls - 2011

Product Class Level Reason

Savacol Antispetic Mouth & Throat Rinse II Consumer Microbial Contamination

Product Class Level Reason

Trident Catheter Valve II Consumer Concerns over product sterility

Avaira Sphere Contact Lenses II Consumer Unintentional residue left on lenses

Oto-Ease® Ear Lubricant II Consumer Potential bacterial contamination

OneTouch Verio Blood Glucose Meter System kits

II Consumer Error messages due to contamination of component during manufacture

Cochlear nucleus CI500 implant II Consumer High incidence of component failure

Avaira Toric Contact Lenses II Consumer Unintentional residue left on lenses

TRIAD Sterile Lubricating Jelly II Consumer Concerns over product sterility

Safety 1st Complete Healthcare Kits II Consumer Thermometer reading in degrees Fahrenheit

LifeScan OneTouch Verio Blood Glucose Monitoring System

II Consumer Error messages due to contamination of component during manufacture

Minicrosser-Cyclone DX 3 & 4 Wheel Mobility Scooters

II Consumer Some units in Europe have spontaneously ignited

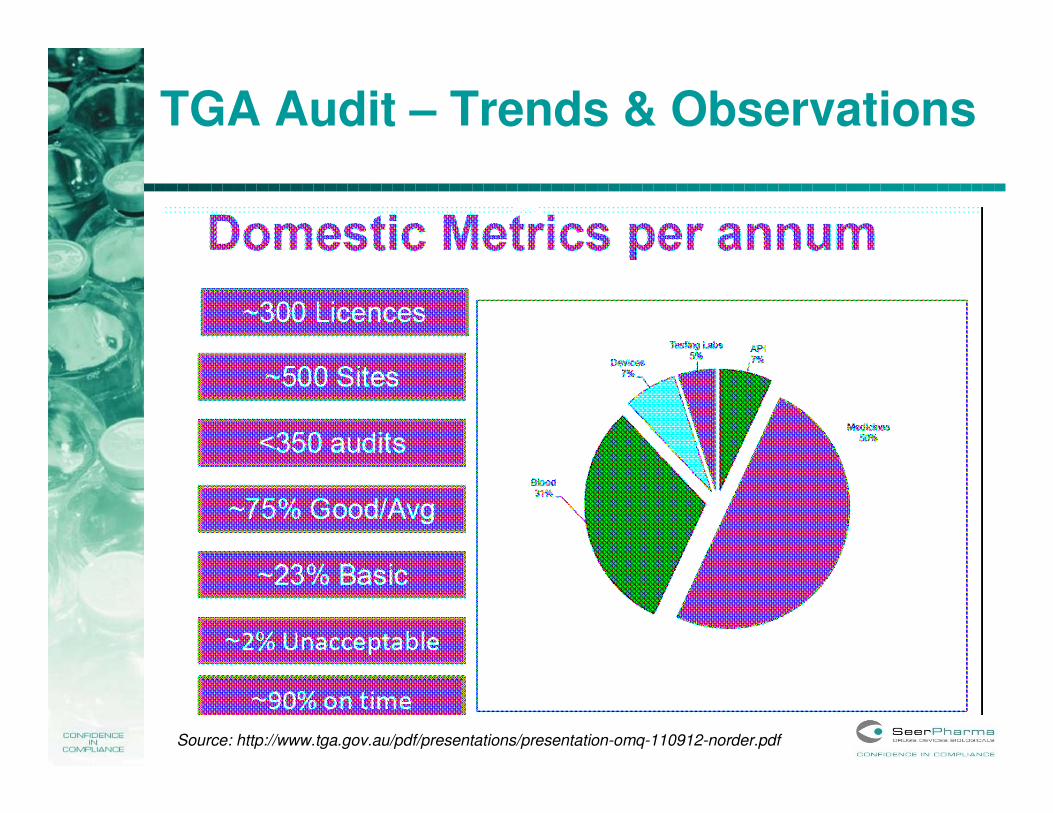

TGA Audit – Trends & Observations

Source: http://www.tga.gov.au/pdf/presentations/presentation-omq-110912-norder.pdf

TGA Audit – Trends & Observations

Source: http://www.tga.gov.au/pdf/presentations/presentation-omq-110912-norder.pdf

TGA Audit – Trends & Observations

Source: http://www.tga.gov.au/pdf/presentations/presentation-omq-110912-norder.pdf

TGA Reformshttp://www.tga.gov.au/pdf/media-2011-tga-reforms-111208.pdf

TGA Reforms

TGA Undertaken Reviews of and Considering Reforms to –

•Communications and Stakeholder Engagement

•Advertising of Therapeutic Products

•Complimentary Medicines

•Medical Devices

•Promotion of Therapeutic Goods

http://www.tga.gov.au/pdf/media-2011-tga-reforms-111208.pdf

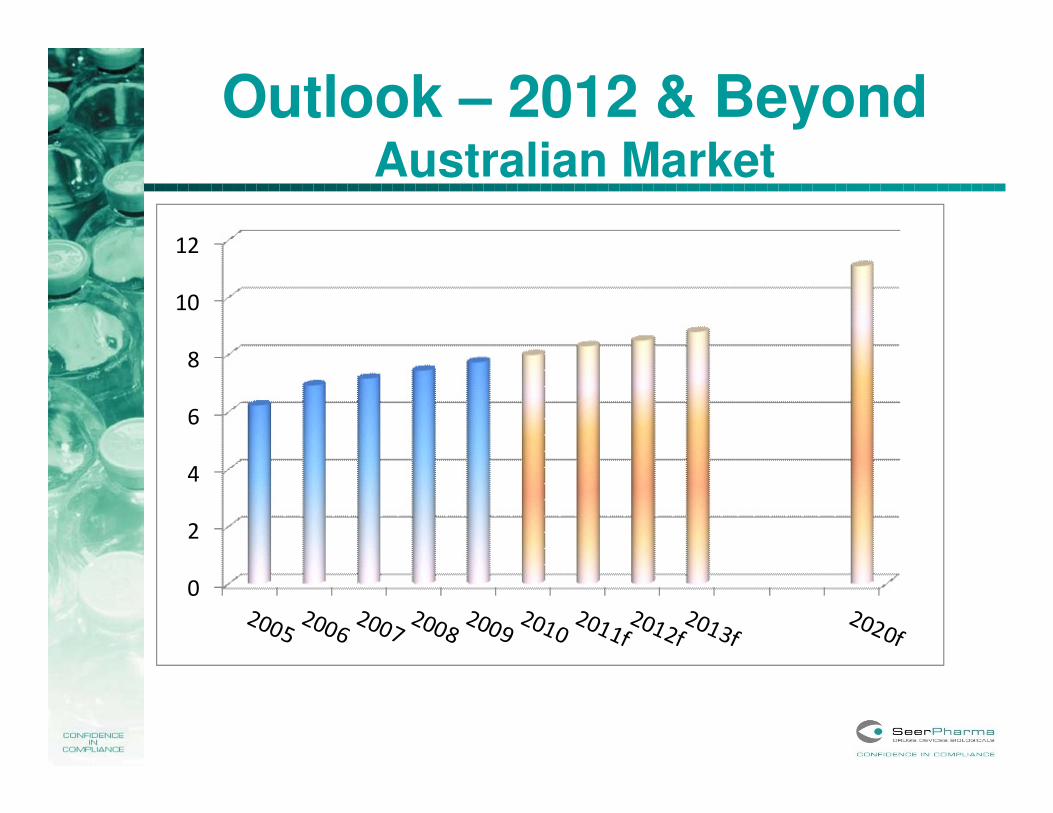

Outlook – 2012 & BeyondAustralian Market

0

2

4

6

8

10

12

Outlook – 2012 & BeyondAustralian Market

• CAGR forecasted to be 2.6% over next 10 Years

• Growth in volume, slow down in value

• Remain dynamic to ensure survival

• Growth path expected to differ to previous years

• Ongoing changes to PBS will restrain growth and squeeze margins

• Cuts in local production capacity

• Employment levels to decrease

• 2015/6 expected to be down 7% on 2005/6 levels

• Maybe offset by increases in R&D

Outlook – 2012 & BeyondAustralian Market

• Further acquisitions expected

• Manufacturers look to specialised facilities (Biotech/generics)

• Move to local contract manufacturing

• Government will continue to influence growth

• PBS will continue to dominate scene

• Patent amendment Bill 2010

Outlook – 2012 & BeyondAustralian Market

Opportunities

• Moderate economic conditions

• Ageing populations

• Changing community attitudes to healthcare

• Ongoing innovation & development of new specialist driven therapies

• Continued switch from prescription to OTC

• Increase in complimentary medicines

Threats

• Falling profits

• Patent expiration

• Thin product lines

• Lack of new blockbusters

• Public sector cost containment

• Continued concerns over drug safety

Information compiled from –

Pharma In Focus – www.pharmainfocus.com.au

Fierce Pharma – www.fiercepharma.com

Fierce Biotech – www.fiercebiotech.com

TGA Web Site – www.tga.gov.au

FDA Web Site – www.fda.gov

Drug Daily Bulletin – www.fdanews.com

IMS Health

Pharmaceutical Technology Magazine

Medicines Australia – www.medicinesaustralia.com.au

Australian Government Dept of Innovation, Industry, Science & Research –www.innovation.gov.au

Generic Medicines industry Association (GMiA) – www.gmia.com.au

The Changing Dynamics of pharma outsourcing in Asia – Price Waterhouse Coopers

Thankyou