A Contracting Approach to Conservatism and Earnings...

36

A Contracting Approach to Conservatism and Earnings Management Pingyang Gao The University of Chicago Booth School of Business [email protected] August, 2011 I have beneted from many discussions on this topic with Anil Arya, Ray Ball, Jeremy Bertomeu, Judson Caskey, Qi Chen, Douglas Diamond, Richard Frankel, Matthew Gentzkow, Jonathan Glover, Zhiguo He, Jack Hughes, Pierre Liang, Christian Leuz, Xiumin Martin, Brian Mittendorf, Valeri Nikolaev, Mort Pincus, Haresh Sapra, Doug Skinner, Shyam Sunder, and Regina Wittenberg Moerman. This paper is a spin-o/ of another paper of mine titled "An Incomplete Contract Approach to Accounting Rule Design." The spin- o/ was inspired by the helpful and constructive comments I have received when I presented the latter at Carnegie Mellon University, Chicago Booth Applied Theory Workshop and Accounting Workshop, Ohio State University, Peking University, Tilburg University, UCLA, UC Irvine, and Washington University in St. Louis. All errors are my own. I also acknowledge the generous nancial support from Chicago Booth.

Transcript of A Contracting Approach to Conservatism and Earnings...

A Contracting Approach

to Conservatism and Earnings Management ∗

Pingyang Gao

The University of Chicago Booth School of Business

August, 2011

∗I have benefited from many discussions on this topic with Anil Arya, Ray Ball, Jeremy Bertomeu, Judson

Caskey, Qi Chen, Douglas Diamond, Richard Frankel, Matthew Gentzkow, Jonathan Glover, Zhiguo He,

Jack Hughes, Pierre Liang, Christian Leuz, Xiumin Martin, Brian Mittendorf, Valeri Nikolaev, Mort Pincus,

Haresh Sapra, Doug Skinner, Shyam Sunder, and Regina Wittenberg Moerman. This paper is a spin-off

of another paper of mine titled "An Incomplete Contract Approach to Accounting Rule Design." The spin-

off was inspired by the helpful and constructive comments I have received when I presented the latter at

Carnegie Mellon University, Chicago Booth Applied Theory Workshop and Accounting Workshop, Ohio State

University, Peking University, Tilburg University, UCLA, UC Irvine, and Washington University in St. Louis.

All errors are my own. I also acknowledge the generous financial support from Chicago Booth.

Abstract

This paper provides one analytical formalization of the debt contracting explanation of

conservatism articulated in the literature (e.g., Watts and Zimmerman (1990)). As a sys-

tematic measurement of a firm’s ex post economic states, accounting measures are used to

implement state-contingent debt contracts. When the manager benefits from better account-

ing measures, he has incentives to bias upward accounting measures ex post. Such earnings

management is ex post rational but ex ante ineffi cient. The asymmetric verification require-

ment under conservatism arises as an ex ante response to counteract the manager’s one-sided

incentives for ex post earnings management. By opening the black box of accounting mea-

surement, the model distinguishes the contracting explanation from the information view and

helps address some criticisms on conservatism analytically.

KeyWords: Conservatism, Accounting Measurement, Earnings Management, Accounting-

motivated Transaction, Debt Contracting

1 Introduction

When facing uncertainty, conservatism in accounting requires stronger support of evidence

to recognize good news than to recognize bad news. Despite its long and pervasive influence

on accounting around the world, conservatism has been subject to substantial controversy,

culminating at it being eliminated from the FASB and IASB’s joint conceptual framework

(FASB (2010)), which guides the making of future accounting standards. Some concerns

about conservatism seem to arise from the premise that characterizes accounting measures

as an informational input to decisions. Under this view, the asymmetric treatment of good

versus bad news generates accounting measures whose informativeness depends on their signs.

Because a priori there does not seem to be a fundamental difference in the way good versus

bad news affects decisions, the effi ciency of conservatism from this view hardly matches its

practical prevalence and profound influence in accounting. For example, Leuz (2001) points

out that under-investment could be as severe a problem as over-investment and that an

unduly tight covenant could be as detrimental to effi ciency as an unduly loose one, a theme

echoed also by Guay and Verrecchia (2006) and Lambert (2010). Gigler, Kanodia, Sapra,

and Venugopalan (2009) further observes that the fact that a project is financed ex ante

means that a priori the cost of excessive liquidation exceeds that of excessive continuation,

deepening the skepticism about conservatism. Similarly, FASB’s offi cial reason for the above

decision is that "Understating assets or overstating liabilities in one period frequently leads

to overstating financial performance in later periods" (FASB 2010 BC3.28), implying that

whatever value conservatism has in one period is inevitably reversed in others.

On the other hand, conservatism has long been advocated as part of a firm’s effi cient

contracting technology. Watts and Zimmerman (1990) summarizes the argument concisely:

"Reacting to the incentive of managers to exercise accounting discretion opportunistically,

the accepted set includes "conservative" (e.g., lower of cost or market) and "objective" (e.g.,

verifiable) accounting procedures."1 As long as the manager, who is able to ex post bias up-

ward accounting measures used in contracts, benefits from the inflated accounting measures,

1See more detailed discussions in, among others, Watts and Zimmerman (1986), Ball (1989), Watts andZimmerman (1990), Basu (1997), Ball (2001), Holthausen and Watts (2001), Watts (2003a), Watts (2003b),and Kothari, Ramanna, and Skinner (2010).

1

opportunistic earnings management occurs ex post and the asymmetric verification require-

ment arises as an ex ante response to the ex post one-sided bias. The underlying premise of

this view is that accounting measures are used to settle contracts, as opposed to influencing

decision makers’beliefs.

In this paper I attempt to provide one analytical formalization of the contracting expla-

nation for conservatism articulated in the literature such as in Watts and Zimmerman (1990).

The analytical formalization makes the explanation more transparent and generalizable. In

particular, it distinguishes the contracting explanation from the information view. The key

difference of the use of accounting measures for contracting versus for informing decision mak-

ers is that the former has to be pre-committed and thus is more vulnerable to ex post manipu-

lation. The extra vulnerability requires special safeguards in the design of measurement rules.

That is, accounting measures for contracting have to be not only informative (relevant) but

also robust to ex post opportunism (reliable). Further, accounting-based contracts are often

designed in such a way that the manager benefits from better ex post accounting measures,

because otherwise the contracts would create perverse incentives. Therefore, the manager’s

ex post opportunism is one-sided and the special safeguard against it is asymmetric as well.

By distinguishing the contracting explanation from the information view, the formaliza-

tion provides a coherent setting to evaluate the different views on conservatism transparently.

I show that conservatism could be effi cient even when the under-investment problem prevails

ex ante or when the cost of an unduly tight covenant exceeds that of an unduly loose one.

In other words, the symmetric value of information for decisions does not conflict with the

asymmetric incentives for ex post opportunism. Further, the model implies that account-

ing measures used to settle a contract are not necessarily the most informative source of

information at the time of the contractual settlement, which is consistent with the empirical

findings in Ball and Shivakumar (2008) and Beyer, Cohen, Lys, and Walther (2010). I use

this observation to show that FASB’s offi cial reason for eliminating conservatism from the

joint conceptual framework is flawed from the contracting perspective.

The model starts from the precise definition of the contracting function of accounting

and, more importantly, its subtle difference from the information view. Consider a typi-

2

cal accounting-based debt covenant that transfers the control right to the lender when the

accounting measure is bad but allows the manager to retain the control right when the ac-

counting measure is good. The accounting measure plays the contracting function when it

is chosen to settle the covenant. Meanwhile, the accounting measure could also play the

information function if it incrementally affects the contracting parties’beliefs (about the un-

derlying state) that determine their decisions such as pricing, renegotiation, and continuation.

Both functions exploit the correlation between the accounting measure and the underlying

state it measures; both could exist in a contractual setting.

However, the two functions do differ in one aspect: their vulnerability to ex post manipu-

lation. The difference is illustrated by the following example. Suppose the lender and the firm

choose the firm’s future debt level as the trigger of the covenant and specify measurement

rules that will be used to measure the firm’s indebtedness in the future. After the contract

has been signed, a new financial technology occurs that enables the firm to restructure its

borrowing in such a way that the transaction is not recognized as debt under the pre-specified

measurement rules. Assume that the transaction is observed by the lender. In this exam-

ple, the transfer of the control right is affected by the transaction because the contracting

parties have pre-committed to the measurement rules of the firm’s debt level that settles

the covenant. In contrast, there is no such pre-commitment for the information function.

The lender’s inference about the firm’s indebtedness, which guides her decisions, if any, is

not or less affected by the accounting-motivated transaction. The pre-commitment nature of

measurement rules for contracting makes them more vulnerable to ex post opportunism and

calls for special ex ante safeguards in the design of the measurement rules.

To formalize the measurement rule design problem, I open the black box of accounting

measurement and model the ex post implementation of a measurement rule as a two-step

process. First, the underlying state of the firm manifests itself in informative characteristics

of the firm’s transactions. Second, these characteristics are converted into an accounting

measure by a pre-specified measurement rule.2 Consequently, a measurement rule is opera-

2Take revenue recognition rule as an example. The state is whether the firm has earned revenue from atransaction. Before this uncertainty is completely resolved, the characteristics of the transaction are informa-tive about the state. These characteristics include, for example, whether the product has been delivered, whatthe transaction arrangement stipulates about returns and warranty, whether the customer has paid for the

3

tionalized as a vector of weights assigned to each transaction characteristic. A measurement

rule is conservative if it assigns a smaller weight to a positive transaction characteristic in

support of the recognition of the good state than to a negative (but equally informative)

transaction characteristic in support of the recognition of the bad state. Moreover, the man-

ager’s manipulation of the measurement process, or earnings management, is modeled as his

influence on the first step to generate positive transaction characteristics, which increases the

chance that the manager receives a better accounting measure for any given measurement

rule.

Conservatism then arises as an ex ante safeguard against the ex post earnings manage-

ment. In the benchmark setting without earnings management, the relative weight assigned

to each characteristic in the optimal measurement rule is equal to its relative informativeness

and thus independent of its sign. As a result, a conservative rule only increases the chance

that the good state is not recognized as good, resulting in lower effi ciency.

The optimal measurement rule is conservative only when the manager can engage in ex

post earnings management. Ex post, the manager can keep out the lender’s intervention and

pursue his own interest at the lender’s expense, as long as the state is measured (recognized)

as good by the measurement rule pre-specified in the contract. While it is ex post rational for

the manager to retain the control right through earnings management, earnings management

is ex ante ineffi cient. The lender anticipates the ex post exploitation by the manager and

demands a higher interest rate ex ante. Such ex ante price protection, however, does not

eliminate the manager’s ex post distortionary earnings management. By placing a smaller

weight on positive characteristics, which the manager has incentives to produce, conservatism

reduces the manager’s incentives to engage in earnings management and thus improves the

effi ciency. Therefore, it is the manager’s one-sided incentives for ex post earnings management

that justifies the ex ante asymmetric recognition requirement of conservatism.

In addition to making a step towards the reconciliation of the contracting and informa-

tion perspectives on conservatism, the paper also contributes to the earnings management

project, and so on. The first step of the measurement process corresponds to the mapping from the true earn-ings process to the observable transaction characteristics. The second step implements a revenue recognitionrule that effectively assigns a weight to each characteristic in support of the recognition of revenue.

4

literature. Earnings management is often seen "as sneaky managers pulling the wool over

the eyes of gullible owners" (Arya, Glover, and Sunder (1998)). Accordingly, the vast liter-

ature on earnings management has focused on its interaction with the rational expectations

(e.g., Stein (1989), Dye (2002)). In contrast, from the contracting perspective, sneakiness

(non-observability) is not necessary for the equilibrium existence of earnings management.

This is useful, partly because many empirical works on earnings management rely on the

measurability (and thus observability) of earnings management. Many accounting-motivated

transactions, which have been a chronic and central concern in accounting standard setting,

resemble the transparent earnings management in the model. It also implies that trans-

parency of the measurement process, for example, requiring the manager to disclose inputs

used to estimate fair value, does not eliminate opportunistic earnings management from the

contracting perspective.

This paper also has implications for the incomplete contracts literature. This literature

has focused almost exclusively on mechanism design to circumvent the exogenous constraint

of the lack of contractible information. Scant attention has been paid to the institutions that

create contractible information in practice, of which accounting is a major one. My model

shows that the incompleteness in contracts (or in measurement rules) can arise endogenously

from the existence of ex post earnings management. The long history of accounting standard

setters fighting against accounting-motivated transactions may shed some fresh lights on the

understanding of the source of incompleteness in contracts.

Finally, the two-step process of accounting measurement in the model isolates the con-

tracting function from the information function and makes it possible to model transparent

earnings management. It could also be useful for studying other issues, such as the distinction

between disclosure and recognition or the enforcement of accounting standards.

There have been a number of models on conservatism. My model might be differentiated

by its focus on the interaction between conservatism and ex post earnings management. The

ex post manipulation of accounting measurement is absent in Antle and Gjesdal (2001),

Venugopalan (2001), Guay and Verrecchia (2007), Gigler, Kanodia, Sapra, and Venugopalan

(2009), Caskey and Hughes (2010), Li (2010), Nan and Wen (2011), and Jiang (2011). In

5

Gox and Wagenhofer (2009a) and Gox and Wagenhofer (2009b) the main results are obtained

without earnings management. Chen, Hemmer, and Zhang (2007) also studies the role of

conservatism in dampening the insiders’ incentive to manipulate earnings. While the two

models differ in many other aspects, the main difference is that in their model accounting

information plays mainly the information function: it affects the outsiders’inference about the

underlying state based on which their pricing decisions are made. As a result, the interaction

between conservatism and earnings management is different in two models. For example,

earnings management has to be non-observable in their model.

There are also models on conservatism in a principal-agent setting. Antle and Lambert

(1988) motivates conservatism from the auditor’s asymmetric loss function and Antle and

Nalebuff (1991) further endogenizes the auditor’s preference from the strategic interaction

between the auditor and the privately informed manager. In Kwon, Newman, and Suh

(2001), conservatism loosens the limited liability of the agent and thus improves effi ciency.

Gigler and Hemmer (2001) models the link between the bias in accounting measurement and

the incentives for the managers to issue voluntary disclosure. They argue that the concave

earnings-return relation does not necessarily result from the conservatism in accounting.

Bagnoli and Watts (2005) and Chen and Deng (2010) model conservatism as a signaling

device to convey the manager’s private information.

The rest of the paper proceeds as follows. In Section 2, I describe the model in which

the demand for an accounting-based covenant arises endogenously. I introduce the two-step

measurement process that decouples the contracting and information functions. In Section

3, I demonstrate that the optimal measurement rule is conservative as long as the manager

has one-sided incentive to increase accounting measures. I also study the determinants of the

optimal level of conservatism. In Section 4 I extend the model to show that FASB’s reason for

eliminating conservatism from the conceptual framework is consistent with the information

view but flawed from the contracting perspective. I also consider the case with renegotiation.

Section 5 concludes.

6

2 The model

In Subsection 2.1, I adapt Aghion and Bolton (1992) to present a setting that demands a

debt covenant endogenously. Given the demand for covenant, Subsection 2.2 describes the

problem of designing the measurement rule for the covenant.

2.1 A model of demand for a debt covenant

An owner-managed firm (henceforth the manager or the firm) has a project that requires

an initial investment of I at date 0. The manager finances his project with a standard debt

contract at date 0. The lender provides I at date 0 and in return receives a prioritized

payment up to the face value D at date 2. The implied interest rate equals DI − 1. Because

I is a constant, I call D face value or interest rate interchangeably. Both the manager and

the lender are risk neutral and the risk free rate is 0. The lending market is competitive at

date 0 and thus the lender breaks even. As a result, the lender’s Individual Rationality (IR)

condition binds in equilibrium and the surplus to the manager also measures the effi ciency

of the contract. In addition, the face value must at least exceed the initial investment (for

the lender to break even), i.e., D ≥ I. Ex ante refers to the time before signing the debt

contract, and ex post refers to the time after.

At date 1, the project could be liquidated for cashflow L < I. Alternatively, the project

could be continued to date 2 with its payoffs determined by the state ω at date 1. ω could be

Bad (B), Good (G), or Superb (S), i.e., ω ∈ {B,G, S}. Each state occurs with probability

qω with qB + qG + qS = 1. ω is observable at date 1 but not directly contractible at date 0,

as will be explained in more details in the next subsection. If the state at date 1 is ω, the

project at date 2 will yield a cashflow Fω ≥ 0 and a private benefit for the manager Xω > 0,

ω ∈ {B,G, S}.

The difference between the cashflow and the private benefit is that the private benefit

cannot be paid out to the lender. That is, Xω is non-pledgeable. Since the manager has spent

time in initiating, developing, and implementing the project, he cares not only about the

cashflow of the project but also about other non-monetary aspects such as social objectives,

7

employee relationship, reputation, etc. Further, the manager may also accumulate skills and

human capitals from implementing the project in his own way that could improve his value

in the labor market in the future. Most of these benefits are non-pledgeable.3

The Superb state derives its name from the assumption that the cashflow in this state

(FS) is so large that the project can always be financed at date 0, regardless of the design

of the contract. Without this simplification, we would have to track both the surplus of the

project conditional on it being financed and whether the project is financed, whenever we

vary the design of contracts. This is the role played by the Superb state in the model.

The labels, "Good" and "Bad," originate from the assumption that continuing the project

is a positive NPV (Net Present Value) decision in the Good state but a negative one in the

Bad state, when the total payoff, including both cashflow and private benefit, is considered.

That is, FG +XG > L > FB +XB. Thus, the socially optimal continuation decision at date

1 is to liquidate the project in and only in the Bad state.

Finally, I assume L > FG. It means that in the Good state the liquidation value is higher

than the cashflow of the project (even though it is lower than the total payoff of the project).4

With these assumptions, the lender and the manager have diverging preferences for the

continuation decision at date 1, neither of which coincides with the socially optimal ones.

More importantly, the conflict cannot be fully resolved by the interest rate of the debt con-

tract, as shown in the following Lemma.

Lemma 1 For any face value D in a feasible debt contract that does not use a covenant, the

socially optimal actions are not implemented in all states. In particular,

1. In the Bad state when the socially optimal action is to liquidate the project, the lender

prefers to liquidate but the manager prefers to continue.

3Models using private benefit for similar purposes include, among others, Diamond (1991), Aghion andBolton (1992), Dewatripont and Tirole (1994), and Zingales (1995). There has also been a large empiricalliterature confirming the existence and importance of private benefit, including Barclay and Holderness (1989),Doidge (2004), and Dyck and Zingales (2004), and Doidge, Karolyi, Lins, Miller, and Stulz (2009).

4 If the opposite L < FG is true, the socially optimal actions at date 1 can be implemented by a short termdebt contract through which the manager refinances the debt at date 1. The lender will refuse to roll overthe short-term debt and demand liquidation in and only in the Bad state, which coincides with the sociallyoptimal actions. Therefore, there will be no demand for either a long-term debt contract or a covenant.

8

2. In the Good state when the socially optimal action is to continue the project, the man-

ager prefers to continue but the lender prefers to liquidate.

3. In the Superb state when the socially optimal action is to continue the project, both the

lender and the manager prefer to continue.

Lemma 1 is proved by comparing in each state the payoff to each party across two actions.

Because D ≥ I and I > L, D > L. That is, the face value exceeds the liquidation value. As a

result, when the project is liquidated, the lender receives all the proceeds from liquidation and

the manager receives nothing.5 In contrast, if the project is continued in state ω, the total

payoff is Fω +Xω, which is divided as min{D,Fω} to the lender and Fω +Xω −min{D,Fω}

to the manager. Because FS ≥ D > L > FG and L > FB, the lender receives min{D,FB} =

FB,min{D,FG} = FG, and min{D,Fs} = D, in three states, respectively. Because FB < L,

FG < L, and D > L, the lender prefers continuation only in the Superb state. Similarly, the

manager receives XB, XG, and FS +XG −D, in three states, respectively. Because XB > 0,

XG > 0 and FS + XG − D > 0, the manager prefers continuation in all states. The payoff

structure is summarized in Table 1.

Table 1: Payoffs of project, lender, and managerState Bad Good Superb

Probability qB qG qS

Cashflow FB FG FS

Private benefit XB XG XS

Continuation Total payoff FB +XB FG +XG FS +XS

Lender’s payoff FB FG D

Manager’s payoff XB XG FS +XS −D

Cashflow (total payoff) L L L

Liquidation Lender’s payoff L L L

Manager’s payoff 0 0 0

5See the discussion of this feature of the model in Footnote 9.

9

Note that the conflicting preferences exist for any face value of the debt contract. No

interest rate at date 0 can induce the manager or the lender to take the socially optimal actions

in all states. In other words, the implementation of the socially optimal actions requires that

the lender intervene selectively: intervene in the Bad state but not in the Good state. Interest

rate at date 0 alone cannot induce such state contingencies, resulting in the possibility of both

under-investment and over-investment. For convenience, I denote ∆Over ≡ L− (XB +FB) as

the ex post effi ciency loss from the ineffi cient continuation of the project in the Bad state, or

the ex post cost of over-investment. Similarly, ∆Under ≡ (XG+FG)−L is the ex post effi ciency

loss from the excessive liquidation in the Good state, or the ex post cost of under-investment.

qB∆Over and qG∆Under are the ex ante cost of over-investment and under-investment.

We thus face the classic "diffi culty of selective intervention," a term coined by Williamson

(1985). What promotes the effi ciency of the contracting relation in this situation is to provide

the right protection to both the lender and the manager, that is, to allocate the control right

to the lender in the Bad state and to the manager in the Good state. This is exactly what a

state-contingent covenant attempts to do. The implementation of a state-contingent covenant

requires the measurement of the state at date 1, of which accounting is one major source.

How to design the measurement rule at date 0 for this contracting purpose is the central

question of the paper and will be specified in the next subsection.

It is worthwhile to highlight the role of private benefit in creating the demand for a

covenant in the debt contract. The non-pledgeability of private benefit creates the discrepancy

between the total payoff and the total pledgeable payoff of the project. This discrepancy is

responsible for the diffi culty of selective intervention in Lemma 1. This parsimonious device

makes the model tractable enough to study the design of the measurement rule for the

covenant. An alternative modeling device is to invoke moral hazard explicitly.6

I make one further simplification before turning to the design of the measurement rule

6Assume that the payoff of the project at date 2 requires a non-contractible effort from the manager betweendate 1 and date 2. This moral hazard problem requires that some payoff at date 2 be given to the manageras incentive to exert the effort. As a result, not all the payoff of the project at date 2 can be paid out tothe lender. Therefore, the role of the (non-pledgeable) incentive pay to the manager is similar to that of theprivate benefit used here (see more examples and discussions in Tirole (2006)). The benefit of using privatebenefit is that it avoids the extra complexity of modeling the moral hazard problem, which is not the focus ofthe paper.

10

for the covenant. Because there is no conflict of interest in the Superb state, I assume that

the payoffs of the project in the Superb state are realized at date 1. As a result, there is no

measurement issue with the Superb state and I can focus only on the measurement of the

Good and Bad states.

2.2 The covenant and its measurement rule

Denote by r the accounting measurement of state ω at date 1 according to whatever mea-

surement rules specified in the covenant, r ∈ {g, b}. Without loss of generality, I assume that

the covenant stipulates that the manager retains the control right if the state is recognized

as good, i.e., r = g, and the lender receives the control right if the state is recognized as bad,

i.e., r = b.

The central question of the paper is the design of the measurement rule at date 0 that

will be used to generate accounting measure r at date 1. The key diffi culty of the design

problem arises from the fact that the measurement rule has to be specified at date 0 but will

be implemented at date 1. This pre-commitment nature of the measurement rule makes it

vulnerable to ex post manipulation, as we will see soon.

While the design of the measurement rule and its implementation involve various parties

and numerous institutional details, I abstract away from the details to focus on the interaction

between the ex ante rule design and the ex post implementation in a stylized model. I start

with the implementation of any measurement rule at date 1 and decompose it to two steps.

First, the firm’s underlying state ω manifests itself in various characteristics of the trans-

actions the firm has engaged in. Without loss of generality, I assume that the transaction

characteristic is either positive or negative. Further, I assume that the transaction charac-

teristics are perfectly correlated with their respective states in the absence of the manager’s

manipulation. That is, if the underlying state is Good, the transaction characteristic is

positive with probability 1; if the underlying state is Bad, the transaction characteristic is

negative with probability 1. I discuss this assumption at the end of this subsection.

Second, the measurement rule specified at date 0 is implemented as a mapping from

transaction characteristics to accounting recognition r at date 1. I assume that when the

11

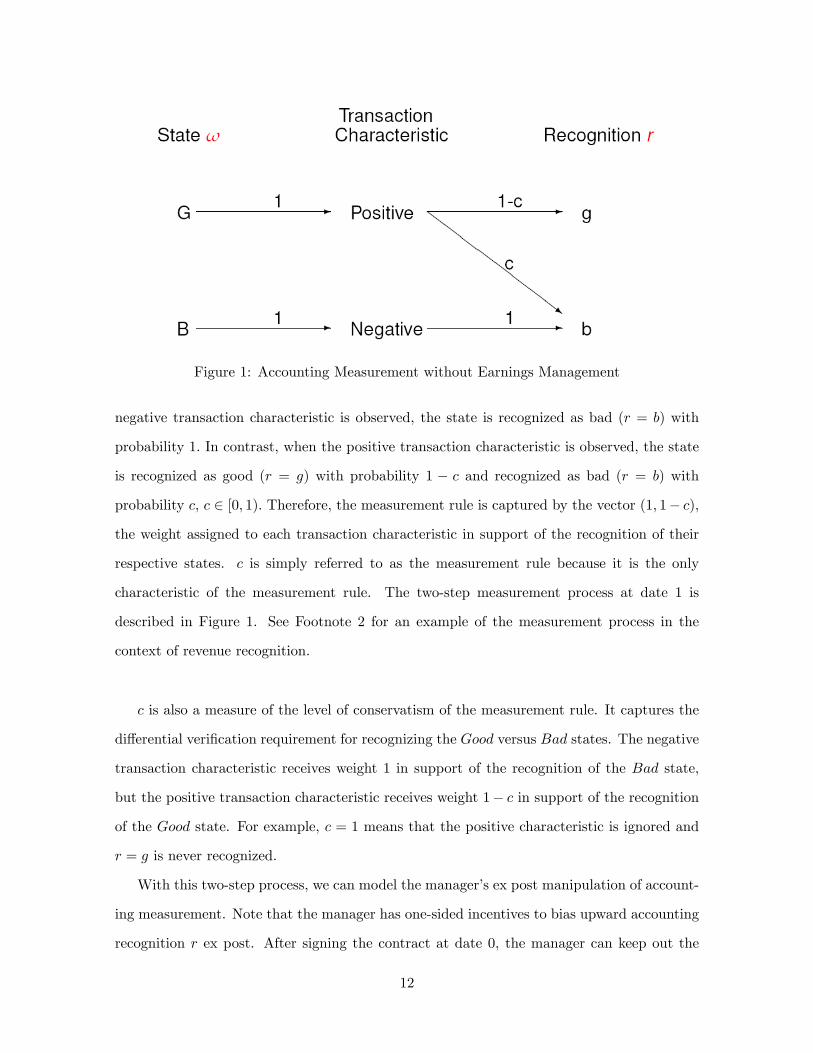

Figure 1: Accounting Measurement without Earnings Management

negative transaction characteristic is observed, the state is recognized as bad (r = b) with

probability 1. In contrast, when the positive transaction characteristic is observed, the state

is recognized as good (r = g) with probability 1 − c and recognized as bad (r = b) with

probability c, c ∈ [0, 1). Therefore, the measurement rule is captured by the vector (1, 1− c),

the weight assigned to each transaction characteristic in support of the recognition of their

respective states. c is simply referred to as the measurement rule because it is the only

characteristic of the measurement rule. The two-step measurement process at date 1 is

described in Figure 1. See Footnote 2 for an example of the measurement process in the

context of revenue recognition.

c is also a measure of the level of conservatism of the measurement rule. It captures the

differential verification requirement for recognizing the Good versus Bad states. The negative

transaction characteristic receives weight 1 in support of the recognition of the Bad state,

but the positive transaction characteristic receives weight 1− c in support of the recognition

of the Good state. For example, c = 1 means that the positive characteristic is ignored and

r = g is never recognized.

With this two-step process, we can model the manager’s ex post manipulation of account-

ing measurement. Note that the manager has one-sided incentives to bias upward accounting

recognition r ex post. After signing the contract at date 0, the manager can keep out the

12

Figure 2: Accounting Measurement with Earnings Management

intervention by the lender as long as the state is recognized as good (r = g) at date 1 by the

measurement rule c specified at date 0. Thus, the manager could engage in costly activities to

manipulate the transaction characteristics and I refer to these activities as earnings manage-

ment. In particular, I assume that between date 0 and date 1 the manager can increase the

probability that its transactions generate the positive characteristic by β ∈ [0, 1] at a cost.

This increases (weakly) the chance that the manager receives r = g for any given measure-

ment rule and for any future state. The earnings management converts Figure 1 to Figure 2,

with the only change that the transaction characteristic could be positive with probability β

even if the true state is Bad.

I assume that the manipulation of transaction characteristics induces the firm to take

some suboptimal actions that reduce the cashflow of the transaction in the Superb state by

hK(β).7 h > 0 measures the vulnerability of a transaction characteristic to the manager’s

manipulation. A higher h means that it is more costly for the manager to manipulate the

characteristic. Thus, h could be interpreted as reliability, or verifiability, or hardness of a

transaction characteristic. K(β) has the following properties:

7The main results are qualitatively the same if the cost of manipulation is assumed to affect the cashflowin other states or to be born by the manager directly. FS − hK(β) is assumed to satisfy all the assumptionsimposed on FS before. In particular, FS − hK(β) ≥ D.

13

• Assumption 1: K′ ≥ 0, K

′′> 0, K

′(0) = 0, and K

′(1) is suffi ciently large;

• Assumption 2: ∂∂β [K

′

K′′ ] = (K′′

)2−K′K′′′

(K′′ )2 > 0.

Assumption 1 is standard. Earnings management is useful for obtaining preferred account-

ing treatment (K′ ≥ 0); the marginal cost of earnings management is increasing (K

′′> 0).

Further, K′(0) > 0 and K

′(1) being suffi ciently large guarantee that the earnings manage-

ment choice is interior. Assumption 2 sets a bound on the speed at which K′′increases.

K′′could be increasing, constant, or decreasing, as long as it does not increase too fast.8

Assumption 2 is needed solely for the generality of K. For example, the standard quadratic

cost function K(β) = β2

2 satisfies Assumption 2.

One example of this type of earnings management is accounting-motivated transactions.

The Securities and Exchange Committee (SEC) defines accounting-motivated structured

transactions as "those transactions that are structured in an attempt to achieve reporting

results that are not consistent with the economics of the transaction" (SEC (2005)). The

report identifies a long list of areas where firms engage in accounting-motivated transactions.

The accounting literature has well established the prevalence of accounting-motivated trans-

actions. For example, Imhoff and Thomas (1988) shows that around the adoption of SFAS

13 firms restructure lease contracts to enhance the chance being recognized as operating

leases (as opposed to capital lease) that present favorable accounting leverage ratio. Lys and

Vincent (1995) presents a striking case in which AT&T paid between $50 and $500 millions

to satisfy the requirements for using pooling accounting, which increases its EPS by 17%

(relative to the alternative accounting treatment) without changing the cash flow. Lehman

Brothers’infamous Repo-105 is another example. Lehman paid a higher haircut to counter-

parties and shopped a legal opinion from UK in order to convince its auditor to accept its

aggressive accounting treatment (see Valukas et al. (2010)).

In sum, the time line of the events is as follows:

1. At date 0, the manager chooses face value D and measurement rule c of the debt

8As Shleifer and Wolfenzon (2002) explains, this assumption on the cost function eliminates the "boil themin oil" results, in which earnings management is prevented entirely with suffi ciently large punishment for evensmall amount of earnings management.

14

contract; the lender decides whether to take the contract;

2. At date 12 (between 0 and 1), the manager chooses the level of earnings management β;

3. At date 1, the state is observed, transaction characteristics occur, accounting measure r

is generated according to the pre-specified measurement rule c, the covenant is settled,

and the decision to continue or liquidate is made.

4. At date 2, cashflow realizes and payment is made.

Note that the allocation of the control right is settled by accounting measure r. This is the

contracting function of accounting. It is isolated from the information function because both

the lender and the manager’s continuation decisions are not affected by their beliefs about the

underlying state. As long as they receive the control right, the lender liquidates the project

and the manager continues the project in both the Good and Bad states, as inferred from

Lemma 1. As a result, accounting measure r does not play the information function of influ-

encing contracting parties’continuation decision. This irrelevance of the contracting parties’

beliefs for the continuation decision means that the model is robust to the observability of

the state at date 1. To make the contracting explanation as transparent as possible, I have

assumed that the transaction characteristics at date 1 are perfectly informative about the

underlying state and that both the transaction characteristics and the earnings management

are observable. In other words, the state ω at date 1 is observable. If the state were assumed

to be non-observable, the results regarding conservatism would be the same, but the subtle

distinction of the contracting and information functions cannot be made.

3 The Main Results

In this section I solve the model using backward induction and explain how conservatism

arises an ex ante optimal response to the ex post earnings management.

15

3.1 The formulation of the problem

At date 1, given the manager’s earnings management β, the contracting parties’(expected)

payoffs depend on both state ω and its accounting recognition r. Since these payoffs are

repeatedly used later, I summarize them in Table 2.

Table 2: Payoffs in Various Scenarios at date 1

State ω Recognition r Probability Lender’s Payoff Manager’s Payoff

B b qB(1− β(1− c)) L 0

B g qBβ(1− c) FB XB

G b qGc L 0

G g qG(1− c) FG XG

S N/A qS D FS +XS −D − hK(β)

The table is self-explanatory. For example, the first row describes the payoffs when

the Bad state occurs and is recognized as bad. This combination occurs with probability

qB(1−β(1− c)).When it occurs, the lender receives the control right, liquidates the project,

and gets all the liquidation value L. The manager receives 0. Other rows can be explained

similarly.

The firm’s debt contract design problem at date 0 can be formulated as the following

maximization problem, labeled as Problem 1:

max(D,c)

V (D, c) = qBβ∗(1− c)XB + qG(1− c)XG + qS(FS +XS −D − hK(β∗)) (1)

subject to

I ≤ qB((1− β̂(1− c))L+ β̂(1− c)FB) + qG(cL+ (1− c)FG) + qSD (IR )

β∗ = arg maxβqBβ(1− c)XB − qGhK(β) (IC)

β∗ = β̂ ( Rational Expectations)

The manager chooses interest rate D and measurement rule c at date 0 to maximize

his expected surplus, subject to the lender’ break-even condition, the anticipated ex post

16

earnings management, and the rational expectations requirement. The objective function V

is the manager’s expected payoff at date 0 and calculated as the inner product of the third

and fifth columns of Table 2 with β being replaced by β∗. The right hand side of the lender’s

IR condition is the lender’s expected payoff from the debt contract. It is based on the lender’s

conjecture about the manager’s ex post earnings management β̂ and calculated as the inner

product of the third and fourth columns of Table 2 with β being replaced by β̂. The manager’s

IC (incentive compatible) condition describes the manager’s decision at date 12 . β benefits

the manager only if the Bad state occurs and r = g is recognized at date 1, which occurs

with probability qBβ(1 − c). In this case, the manager receives XB instead of 0. Therefore,

the expected benefit of earnings management β at date 12 is qBβ(1 − c)XB. qGhK(β) is the

expected cost in the form of reducing the cashflow in the Superb state. The existence of the

IC condition means that the manager cannot commit to the choice of earnings management

at date 0. Finally, the rational expectations require that the lender’s conjecture about the

manager’s ex post earnings management be consistent with the manager’s actual choice.

3.2 Benchmark: no earnings management

To highlight the role of earnings management, we first look at the benchmark in which the

manager cannot engage in earnings management. That is, β = 0 is imposed. Then the IC

condition is dropped from Problem 1 and β̂ = β∗ = 0. The binding IR condition determines

the face value: DBM = I−(qBL+qG(cL+(1−c)FG)qS

. Substituting DBM for D in the objective

function and rearranging the terms, we get

V BM (c) = V FB − cqG∆Under. (2)

V FB is defined as the manager’s expected surplus when the socially optimal actions are

implemented, that is, the project is liquidated in and only in the Bad state. It is calculated

as follows:

V FB ≡ qBL+ qG(FG +XG) + qS(FS +XS)− I.

Proposition 1 In absence of earnings management, conservatism reduces the ex ante debt

17

contracting effi ciency by distorting the measurement of the Good state.

Proposition 1 is straightforward from inspecting equation 2. Recall that qG∆Under ≡

qG(FG+XG−L) is the ex ante cost of under-investment resulting from allocating the control

right wrongly to the lender in the Good state. In absence of earnings management, conser-

vatism increases the chance that the good state is recognized as bad (r = b) with probability

c. When r = b is recognized, the lender seizes the control right. Even though the project has

positive NPV, its cashflow is not suffi cient to get the lender to continue the project, resulting

in under-investment. This cost is minimized at c = 0.

The ex post earnings management is thus necessary for the effi ciency of conservatism.

3.3 Ex post earnings management

The manager’s earnings management decision at date 12 is described in the IC condition in

Problem 1. The optimal earnings management β∗ satisfies the following first-order condition:

qB(1− c)XB = qGhK′(β∗). (3)

The second order condition for a maximum is satisfied with Assumption 1. From the man-

ager’s perspective, the left hand side of the first-order equation (equation 3) is the marginal

benefit of earnings management and the right hand side is the marginal cost.

Proposition 2 Suppose Assumption 1 holds. The optimal earnings management, β∗, satis-

fies these properties:

1. β∗ > 0;

2. β∗ decreases in conservatism c.

Part 1 is proved by Assumption 1 that K′(0) = 0 and K

′′> 0. It suggests that earnings

management is ex post rational for the manager. After signing the contract (ex post), the

manager could keep out the external intervention and receive the private benefit as long as

the state is recognized as good by the pre-specified measurement rule. Any activity that

18

is not contractually prohibited is pursued by the manager. Notably, what is necessary for

earnings management to arise in equilibrium is the non-contractibility, rather than the non-

observability, of earnings management.

Part 2 is obtained by differentiating the first-order equation with respect to c. It implies

that ex ante conservatism makes ex post earnings management less attractive. By putting a

smaller weight on the positive characteristic, conservatism diminishes the benefit of generating

the positive transaction characteristic through costly earnings management.

With Part 2 of Proposition 2, I take a detour to have a closer look at the information

content of accounting measure r. Suppose an econometrician starts out to examine the

informational properties of the accounting measure r in the model, she will find the following.

Proposition 3 As the measurement rule becomes more conservative, good news (r = g)

becomes more informative and bad news (r = b) becomes less informative of their respective

states.

It is proved by the application of the Bayes rule. Conditional on r = g, the probability

that the state is Good (ω = G) is calculated by the Bayes rule: Pr(ω = G|r = g) = qGqG+qBβ

∗ .

The information content of r = g is contaminated by earnings management β∗ because it

makes it more likely that r = g comes from ω = B. As conservatism increases, β∗ drops,

making r = g more informative. Similarly, Pr(ω = B|r = b) =qB

qG+qB(1−β∗(1−c))

qBqG+qB

(1−β∗(1−c))+ qGqG+qB

cand

is shown to decrease in c in the Appendix. The information content of r = b is affected by

conservatism c in two ways. First, by discounting the positive transaction characteristic, c

makes it more likely that r = b comes from ω = G. Second, c reduces earnings management

and thus makes it more likely that r = b comes from ω = B. It is proved in the Appendix that

the first effect dominates the second. As a result, conservatism makes r = b less informative

about the ω = B.

In sum, my definition of conservatism is consistent with that used in the literature, such as

in Venugopalan (2001) and Gigler, Kanodia, Sapra, and Venugopalan (2009). The two-step

measurement process thus can be viewed as providing a micro-foundation of their definition.

The advantage of the two-step measurement process is that it enables us to distinguish the

19

contracting and information functions.

3.4 Ex ante design of the debt contract: interest rate D

The ex ante design of the debt contract has two elements, the interest rate D and the

measurement rule c. We examine them in turn. At date 0, the lender conjectures that the

manager will choose β̂ and prices the debt accordingly. Given the conjecture β̂, the binding

IR condition in Problem 1 determines the face value D(c, β̂):

D(c, β̂) =I − qB((1− β̂(1− c))L+ β̂(1− c)FB)− qG(cL+ (1− c)FG)

qS. (4)

Proposition 4 The interest rate D(c, β̂) in equation 4 satisfies these properties:

1. it increases in the lender’s conjecture about earnings management β̂;

2. it decreases in conservatism c, given β̂.

Proposition 4 is proved by differentiating the expression of D(c, β̂) above with respect to

β̂ and c. The first part captures the notion of ex ante price protection. If the lender believes

that the manager is more likely to engage in earnings management after contracting, which

enables the manager to pursue his own interest at the expense of the lender’s, the lender

demands a higher interest rate at date 0. As a result of the price protection, the manager

bears the consequences of ex post earnings management.

However, the ex ante price protection through the adjustment of interest rate does not

eliminate the ex post opportunism. Because earnings management occurs after the interest

rate is negotiated, the manager takes the interest rate as given when he chooses the level of

earnings management. The first-order condition for the choice of earnings management, i.e.,

equation 3, suggest that earnings management β∗ does not depend on the interest rate D.9

9While β∗ is completely independent of D in equation 3, a covenant is incrementally relevant as long asβ∗ is not completely determined by D. In other words, the measurement rule for the covenant is relevantas long as the ex ante price protection does not perfectly align the contracting parties’ex post preferences.The assumptions about the special payoff structures that result in the complete independence of β∗ of D, asdiscussed in the reference to Lemma 1, do make the model more tractable by eliminating the dependence ofβ on D in equation 4.

20

Therefore, interest rate alone in the debt contract does not perfectly align the contracting

parties’preferences, leaving room for a covenant to improve effi ciency.

Part 2 implies that the interest rate and the measurement rule are (imperfect) substitutes.

The lender demands a lower interest rate when the measurement rule in the covenant is more

conservative. The reason is because conservatism increases the chance that the control right

is transferred to the lender. The control right at date 1 is valuable and thus the lender is

willing to receive less cashflow in return for more control right. In other words, the lender

can be "protected" by either a higher interest rate or a more conservative measurement rule

in the covenant. I now turn to show that these two types of protection have distinct cost and

benefit structures. As a result, an interior combination of the two is optimal.

3.5 Ex ante design of the debt contract: measurement rule c

We turn to the design of the measurement rule and show that the optimal measurement rule

is conservative. Substituting D(c, β̂) into the objective function V , imposing the rational

expectations requirement of β̂ = β∗, and rearranging the terms, the objective function in

Problem 1 can be expressed as a function of conservatism c :

V (c) = V FB − qBβ∗(c)(1− c)∆Over − qGc∆Under − qShK(β∗(c)). (5)

Recall V FB is the first-best effi ciency of the contract when the socially optimal actions are

implemented in all states. Equation 5 shows that even though earnings management is ex post

rational for the manager, it is ex ante distortionary and ineffi cient. It lowers the effi ciency of

the contract by three terms relative to V FB. The first is the cost of over-investment when the

manager receives the control right in the Bad state as a result of earnings management. The

second term is the cost of under-investment when the lender receives the control right in the

Good state as a result of conservatism, which arises as a response to earnings management.

Finally, in the manager’s pursuit of the control right through earnings management, the

project’s cashflow is reduced.

Earnings management results in over-investment, but conservatism results in under-

21

investment. Therefore, using conservatism to counteract earnings management has a trade-

off, which is reflected in the following first-order condition that determines the optimal level

of conservatism c∗:

dV (c∗)

dc= qBβ

∗(c∗)∆Over − qB(1− c∗)∆Over ∂β∗(c∗)

∂c− qG∆Under − qShK

′ ∂β∗(c∗)

∂c= 0 (6)

The second order condition for a maximum is satisfied with Assumption 2. Given earn-

ings management β∗, conservatism diminishes the effectiveness of earnings management in

securing the preferred treatment r = g by discounting the positive transaction characteristic,

saving the cost of over-investment (the first term). Moreover, conservatism reduces earnings

management (because ∂β∗(c)∂c < 0 from Part 2 of Proposition 2), resulting in further saving of

the cost of over-investment (the second term) and in the saving of the direct cost of earnings

management (the last term). Finally, the ex ante discounting of the positive transaction

characteristic is costly because it increases the measurement error of the Good state, as we

have analyzed in the benchmark case. This explains the third term in the above first-order

condition.

Proposition 5 Suppose both Assumption 1 and 2 hold, and c∗ ∈ (0, 1). The optimal mea-

surement rule becomes more conservative, i.e., c∗ increases, if

1. it is easier for the manager to manipulate the measurement process, i.e., h is smaller;

2. the ex ante cost of over-investment is larger, i.e., qB or ∆Over is larger

3. the ex ante cost of under-investment is smaller, i.e., qG or ∆Under is smaller.

Proposition 5 is proved by differentiating the first-order condition dV (c∗)dc = 0 with re-

spect to relevant parameters. It characterizes the interaction of conservatism with earnings

management. The optimal level of conservatism of the measurement rule increases as the

ex post earnings management becomes more severe a problem, heightening the central con-

tention of the paper that conservatism arises as an ex ante response to the manager’s ex post

opportunistic manipulation of the measurement process.

22

Consider Part 1 of Proposition 5 first. As h decreases, it becomes increasingly easier for

the manager to manipulate the accounting presentation of the firm’s transactions, making

it more attractive to use the costly conservatism to counteract the manager’s incentives for

earnings management. At one extreme, as h goes infinitely large, the firm finds it too costly

to engage in any ex post earnings management. This gets us back to the benchmark case in

which conservatism only distorts the recognition of the Good state and thus the optimal level

of conservatism is 0. At the other extreme, as h goes to zero, earnings management becomes

so severe that the optimal measurement rule does not recognize any good news at all, i.e.,

c∗ approaches 0. For example, if it is extremely diffi cult to describe the characteristics of a

successful R&D activities ex ante and thus it is easy for the manager to manipulate these

characteristics ex post, the optimal measurement rule is not to recognize (capitalize) any

R&D expenditure at all.

Part 2 and 3 of Proposition 5 could be understood similarly. A higher ex ante cost of

over-investment resulting from the wrong allocation of the control right to the manager makes

conservatism more attractive, and a higher ex ante cost of under-investment resulting from

the wrong allocation of the control right to the lender makes conservatism more costly.10

Consider the example with K(β) = β2

2 . In the Appendix, we solve for c in closed-form as:

1 − c∗ = qG∆Under

(2qB∆Over+qBXB)qShXBqB

. Thus, qG∆Under and qB∆Over do not completely determine

c∗.

Note that the interaction of over-investment and under-investment with conservatism

differs from that from the information view. While it is true that the measurement error

of the accounting measure is responsible for the wrong allocation of the control right and

thus the ineffi cient investment decision, it is not the lack of information that prevents the

contracting parties from making the right investment decision. Therefore, while the cost of

under-investment is a cost of using conservatism and reduces the optimal level of conservatism

on margin, the optimal measurement rule could still be conservative even if the ex ante cost

of under-investment dominates that of over-investment.10Note that ∆Lender = FG + XG − L. The change in FG or XG affects ∆Lender but not other parameters

in first-order condition dV (c∗)dc

= 0. Thus, the statement should be viewed with respect to FG or XG, ratherthan to ∆Lender. Similarly, FB is a free parameter in ∆Firm.

23

Finally, we briefly discuss the condition under which c∗ is not at the corner, as required

in Proposition 5. With Assumption 2, the second order condition for maximum is satisfied,

that is, d2V (c)dc2

< 0. Thus, dV (c)dc is decreasing in c. Evaluating dV (c)

dc at c = 1, dV (c)dc |c=1 =

−qG∆Under < 0. By the intermediate value theorem, c∗ is interior if and only if dV (c)dc |c=0 > 0.

Because dV (c)dc |c=0 = qBβ

∗(0)∆Over−qB∆Over ∂β∗

∂c |c=0−qShK′ ∂β∗

∂c |c=0−qG∆Under, dV (c)dc |c=0 >

0 could be rewritten as qB∆Over >qG∆Under+qShK

′ ∂β∗∂c|c=0

β∗(0)− ∂β∗∂c|c=0

.11 Since neither β∗(0) nor ∂β∗

∂c |c=0

is a function of ∆Over or ∆Under (more precisely, the free parameters in ∆Over or ∆Under),

the condition becomes a comparison of qB∆Over and qG∆Under. As long as qB∆Over is suf-

ficiently larger than qG∆Under, the condition can always be satisfied. When the condition is

violated, that is, when qB∆Over is suffi ciently small relative to qG∆Under, the optimal level

of conservatism is at the corner of c∗ = 0. That is, if the manager’s opportunism is not a

serious concern, the measurement rule is not conservative in equilibrium, highlighting the

main contention of the paper that conservatism is an ex ante response to the ex post earnings

management.

4 Extensions

4.1 Does the conservative bias in current contracts have to reverse in fu-

ture contracts?

The FASB’s offi cial reason for eliminating conservatism is that the conservative bias in current

period leads to upward bias in future periods. In this extension, I show that while this

observation is valid, it does not diminish the effi ciency of conservatism if it is understood

from the contracting perspective.

To examine this issue, the model has to be extended to multiple periods. A simple way

is to repeat the same stage game every period. Suppose every period the firm discovers a

project that needs financing. All the payoffs of the projects across periods are independent

and identically distributed. The firm enters into one new contract to finance the newly

11Using the above example with K(β) = β2

2, this condition could be written as qB∆Over >

qG∆Under− qBXBqSh

qBXB

2qBXBqSh

.

24

discovered project each period. The timeline could be depicted as follows:

date t− 1 t t+ 1 t+ 2

Project t Contract t signed ωt measured ωt+1 realized

Project t+ 1 Contract t+ 1 signed ωt+1 measured ωt+1 realized

At date t, the state of project t, ωt, is measured as rt(ωt). The bias of the accounting

measure for contract t is conservative if rt(ωt) − ωt < 0. Similarly, at date t + 1, the state

of project t + 1, ωt+1, is measured as rt+1(ωt+1). In addition, ωt is realized at date t + 1.

The realization of ωt then reverses the bias in the previous measurement rt(ωt). That is, the

reversal, −(rt(ωt) − ωt), is added to the accounting measure at date t + 1. The aggregate

accounting measure at date t+ 1 is

rt+1(ωt, ωt+1) = rt+1(ωt+1) + (ωt − rt(ωt)).

rt+1(ωt, ωt+1) has an upward bias ωt − rt(ωt) > 0 because contract t has a conservative

bias, i.e., rt(ωt)−ωt < 0. Under-measuring state ωt at date t leads to the over-measurement

of state ωt+1 at date t+ 1. In this sense, FASB’s observation is correct.

Does contract t+ 1 have to use rt+1(ωt, ωt+1) as it is? From the information perspective,

the answer is Yes because rt(ωt) is the best source of information at t. However, from the

contracting perspective, recall that at date t when contract t is settled, ωt is observed. In other

words, the conservative bias rt(ωt)− ωt is transparent. Therefore, contract t+ 1 could use a

modified accounting measure rt+1Modified(ω

t, ωt+1) = rt+1(ωt, ωt+1)−(ωt−rt(ωt)) = rt+1(ωt+1)

to exclude the impact of the reversal of the conservative bias from contract t. As a result, the

conservative bias used in contract t is not carried over to contract t + 1. FASB’s reason for

eliminating conservatism from the conceptual framework is thus flawed from the contracting

perspective.

Consider the example in which R&D is expensed for the current contract. At the time

the current contract is settled, there is a conservative bias in the accounting measure that

will be reversed when the actual benefit of the R&D realizes in future. The key observation

25

is that conservatism in the model affects the settlement of the current contract but does not

affect contracting parties’information about the future benefit of the R&D. It is the latter

that guides the negotiation of the new contract. As a result, the conservative bias in the

current contract does not affect the new contract.

4.2 Renegotiation

From the contracting perspective, at the time of contractual settlement there could be sources

of information that are more informative about the state than the accounting measures used

in the contract. A natural question is that whether the contracting parties could improve

effi ciency by utilizing the ex post information, say, through renegotiation? Empirically, debt

covenants are often renegotiated (e.g., Roberts and Sufi (2009)). Does the possibility of

costless renegotiation after the settlement of the debt covenant preempt the value of using

conservative accounting measure? The answer is somewhat surprising: the possibility of ex

post renegotiation intensifies earnings management and thus could make conservatism more

attractive.

The only case in which renegotiation is possible is when the state is Bad but recognized as

good.12 The manager would continue the project ineffi ciently and incur the ex post effi ciency

cost of ∆Over. Thus, the lender could "bribe" the manager to liquidate the project by paying

the manager some surplus from the saving of ∆Over. Denote the manager’s bargaining power

as µ ∈ [0, 1] and consider a Nash bargaining solution. The manager’s payoff in the Bad

state with r = g changes from XB to XB + µ∆Over. Anticipating the increased payoff in the

Bad state with r = g, the manager’s earnings management β∗∗ is determined by the new

first-order condition:

qB(1− c)(XB + µ∆Over) = qShK′(β∗∗). (7)

Comparing it with its counterpart in the baseline model (eqn. 3), it is straightforward that

β∗∗ ≥ β∗. In addition to receiving the private benefit, the manager also receives a fraction

12 If the state is good, there are two cases. In the case r = g renegotiation is not necessary because the firmcontinues the project effi ciently. In the case of r = b renegotiation is not feasible because the firm does nothave any wealth to pay the lender. If the state is bad but recognized as bad, renegotiation is not necessarybecause the lender liquidates the project effi ciently.

26

of the surplus resulting from the renegotiation. As a result, the marginal benefit of earn-

ings management increases and the manager chooses a higher level of earnings management.

Therefore, while renegotiation improves the continuation decision at date 1, it intensifies

earnings management. As a result, conservatism could be more attractive.

5 Conclusion

The paper has formalized a simple contracting explanation for conservatism that has been

widely cited in the literature. The formalization makes it clear that the mechanism relies

on two main factors. First, accounting-based contracts are designed in such a way that the

manager benefits from better accounting measures. Second, the manager is able to influence

the measurement process ex post. The combination of the two implies that the manager

has one-sided incentives to manipulate accounting measurement. Such earnings management

is ex post rational but ex ante ineffi cient. Conservatism, by putting a smaller weight on

positive transaction characteristics in the measurement rule, serves as an ex ante device for

the manager to commit to engaging in less earnings management. As such it is part of a

firm’s effi cient contracting technology.

Both factors required for conservatism to be effi cient seem fairly descriptive. Accounting

measures are proxies for the underlying states. Conditional on the use of accounting mea-

sures in a contract, rewarding the manager more for bad accounting measures than for good

accounting performance would create perverse incentives for the manager not to take actions

that increase firm value or even worse to take actions that destroy firm value. Thus, contracts

in practice almost always (weakly) reward the manager for better accounting performance.

As a result, the manager has incentives to bias upward accounting measures, in particular

when the entire life of a contract is considered. Further, the manager’s central role in con-

ducting transactions and his proximity to the measurement process make it possible that he

could influence the measurement process much more than other contracting parties. As a

result, the rationale for conservatism obtained from the model is likely to be more general.

The simplicity and generality of this mechanism seem to match the long-lasting and prevalent

27

influence conservatism has on accounting.

The main feature of the model is that it distinguishes the contracting function of ac-

counting from its information function. The two functions are related but not the same.

Both exploits the correlation between the accounting measure and the underlying state the

accounting measure intends to represent; both could occur in a contracting setting. How-

ever, the contracting function is more vulnerable to ex post manipulation because of its

pre-commitment nature. Thus, the design of measurement rules for contracting purposes

emphasizes not only on the informativeness but also on the reliability of accounting mea-

sures. As a result, accounting measures that are used to settle a contract are often not the

most informative sources of information available to decision makers at the time the contract

is settled. One implication is that from the contracting perspective, earnings management is

a threat even if it is transparent. Many accounting-motivated transactions could be viewed

as transparent earnings management and thus could be understood from the contracting

perspective.

The two-step measurement process opens the black box of accounting measurement and

makes it possible to distinguish the contracting and information functions analytically. This

tool could also be useful for understanding other accounting issues, such as the relationship

between disclosure and recognition.

In practice, accounting seems to play both the information function and the contracting

function. Accounting is an important source of information that influence the beliefs and

decisions of market participants; on the other hand, accounting is widely used in contracts

and regulation. Therefore, it might be interesting and important to model the two functions

at the same time in the future research.

6 Appendix

Most proofs are explained in the text. Here I provide more details of the proofs of Proposition2, 3, and 5. Most of them are based on standard comparative statics.

Proof. of Proposition 2: At date 12 , the manager chooses β to maximize qBβ(1 − c)XB −

28

qGhK(β). The first-order condition is

qB(1− c)XB − qShK′(β∗) = 0. (8)

The second-order condition is −qShK′′(β∗) < 0 because K

′′> 0. Because K

′(0) = 0 and

K′′> 0, β∗ > 0. Differentiating the first-order condition with respect to c, we have

∂β∗

∂c= − qBXB

qShK′′(β∗)

= − K′(β∗)

(1− c)K ′′(β∗) < 0. (9)

For the proof of Proposition 5 later, we also differentiate the first-order condition with respectto qB, qS , and h :

∂β∗

∂qB=

(1− c)XB

qShK′′(β∗)

> 0; (10)

∂β∗

∂qS= − K

′

qSK′′ < 0; (11)

∂β∗

∂h= − K

′

hK ′′< 0. (12)

We also differentiate ∂β∗

∂c with respect to c, qB, qS , and h :

∂2β∗

∂c2= −K

′′′

K ′′(∂β∗

∂c)2; (13)

∂2β∗

∂c∂qB= − 1

(1− c)(K′′)2 −K ′K ′′′

(K ′′)2

∂β∗

∂qB< 0; (14)

∂2β∗

∂c∂qS= − 1

(1− c)(K′′)2 −K ′K ′′′

(K ′′)2

∂β∗

∂qS> 0; (15)

∂2β∗

∂c∂h= − 1

(1− c)(K′′)2 −K ′K ′′′

(K ′′)2

∂β∗

∂h> 0. (16)

Proof. of Proposition 3:

Pr(ω = G|r = g) =Pr(G) Pr(g|G)

Pr(G) Pr(g|G) + Pr(B) Pr(g|B)

=

qGqG+qB

(1− c)qG

qG+qB(1− c) + qB

qG+qBβ∗(1− c)

=qG

qG + qBβ∗

29

Because ∂β∗

∂c < 0,Pr(ω = G|r = g) is increasing in c. Thus, the good news becomes moreinformative with a more conservative measurement rule.

Pr(ω = B|r = b) =Pr(B) Pr(b|B)

Pr(B) Pr(b|B) + Pr(G) Pr(b|G)

=

qBqG+qB

(1− β∗(1− c))qB

qG+qB(1− β∗(1− c)) + qG

qG+qBc

=1

1 + qGqB

c1−β∗(1−c)

Consider the effect of c on c1−β∗(1−c) . The numerator increases in c because a conservative

rule makes it likely that r = b comes from ω = G. The denominator increases in c because aconservative rule reduces earnings management and thus makes it more likely that r = b isassociated with ω = B. It turns out the first effect dominates the second effect:

∂

∂c

c

1− β∗(1− c) =1− β∗(1− c) + c(∂β

∗

∂c (1− c)− β∗)(1− β∗(1− c))2

=1− β∗ + c(1− c)∂β

∗

∂c

(1− β∗(1− c))2

Denote N(c) ≡ 1− β∗ + c(1− c)∂β∗

∂c , the numerator.

∂N(c)

∂c= −2c

∂β∗

∂c+ c(1− c)∂

2β∗

∂c2

= −c∂β∗

∂c(2 + (1− c)K

′′′

K ′′∂β∗

∂c)

= −c∂β∗

∂c(2− K

′′′

K ′′K′

K ′′)

> 0

Because ∂N(c)∂c > 0 and Limit

c→0N(c) = 1 − β∗(0) > 0, N(c) > 0 for any c. Therefore,

∂∂c

c1−β∗(1−c) > 0 and Pr(ω = B|r = b) decreases in c.

Proof. of Proposition 5: Following the steps in the text, we simplify Problem 1 to a problemof choosing c to maximize V (c) in equation 5, which is reproduced here:

V (c) = V FB − qBβ∗(c)(1− c)∆Over − qGc∆Under − qShK(β∗(c)).

Differentiating V (c) with respect to c,

dV (c)

dc= −qB

∂β∗

∂c(1− c)∆Over + qBβ

∗∆Over − qG∆Under − qShK′ ∂β∗

∂c

= qB∆Overβ∗ − qG∆Under − qB(∆Over +XB)(1− c)∂β∗

∂c.

30

The second equality uses equation 8. The second-order condition for a maximum is satisfiedbecause

d2V (c)

dc2= qB∆Over ∂β

∗

∂c+ qB(∆Over +XB)

∂β∗

∂c− qB(∆Over +XB)(1− c)∂

2β∗

∂c2

= qB∆Over ∂β∗

∂c+ qB(∆Over +XB)

∂β∗

∂c+ qB(∆Over +XB)(1− c)K

′′′

K ′′(∂β∗

∂c)2

= (∆Over + (∆Over +XB)(1 + (1− c)K′′′

K ′′∂β∗

∂c))qB

∂β∗

∂c

= (∆Over + (∆Over +XB)(1− (1− c)K′′′

K ′′K′

(1− c)K ′′ ))qB∂β∗

∂c

= (∆Over + (∆Over +XB)(1− K′K′′′

(K ′′)2))qB

∂β∗

∂c

< 0.

The second equality uses equation 13 and the last inequality results from Assumption 2

and ∂β∗

∂c < 0. As analyzed in the text, when qB∆Over >qG∆Under+qShK

′ ∂β∗∂c|c=0

β∗(0)− ∂β∗∂c|c=0

, there exists

c∗ ∈ (0, 1) such that

dV (c∗)

dc= qBβ

∗(c∗)∆Over − qB(1− c∗)∆Over ∂β∗(c∗)

∂c− qG∆Under − qShK

′ ∂β∗(c∗)

∂c= 0. (17)

Differentiating it with respect to h, qB, qG, and the free parameters in ∆Over (FB) and in∆Under (FG and XG), we have

dc∗

dh= − 1

d2V (c)dc2

(qB∆Over ∂β∗

∂h− qB(∆Over +XB)(1− c) ∂

2β∗

∂c∂h) < 0;

dc∗

dqB= − 1

d2V (c)dc2

(∆Over(β∗ + qB∂β∗

∂qB)− (∆Over +XB)(1− c)∂β

∗

∂c− qB(∆Over +XB)(1− c) ∂

2β∗

∂c∂qB) > 0;

dc∗

dqG=

1d2V (c)dc2

∆Under < 0;

dc∗

dFB=

1d2V (c)dc2

(qBβ∗ − qB(1− c)∂β

∗

∂c) < 0;

dc∗

dFG=

1d2V (c)dc2

qG < 0;

dc∗

dXG=

1d2V (c)dc2

qG < 0.

31

References

Aghion, P., and P. Bolton, 1992, An incomplete contracts approach to financial contracting,The review of economic Studies 59, 473.

Antle, R., and F. Gjesdal, 2001, Dividend covenants and income measurement, Review ofaccounting studies 6, 53—76.

Antle, R., and R.A. Lambert, 1988, Accountantsï£ ¡ loss functions and induced preferencesfor conservatism, Economic Analysis of Information and Contracts: Essays in Honor ofJohn E. Butterworth pp. 373—408.

Antle, R., and B. Nalebuff, 1991, Conservatism and auditor-client negotiations, Journal ofAccounting Research 29, 31—54.

Arya, A., J. Glover, and S. Sunder, 1998, Earnings Management and the Revelation Principle,Review of Accounting Studies 3, 7—34.

Bagnoli, M., and S.G. Watts, 2005, Conservative accounting choices, Management sciencepp. 786—801.

Ball, Ray, 1989, The firm as a specialist contracting intermediary: Application to accountingand auditing, unpublished manuscript.

, 2001, Infrastructure Requirements for an Economically Effi cient System of Pub-lic Financial Reporting and Disclosure, Brookings-Wharton Papers on Financial Services2001, 127—169.

, and L. Shivakumar, 2008, How much new information is there in earnings?, Journalof Accounting Research 46, 975—1016.

Barclay, M.J., and C.G. Holderness, 1989, Private benefits from control of public corporations,Journal of financial Economics 25, 371—395.

Basu, S., 1997, The conservatism principle and the asymmetric timeliness of earnings, Journalof Accounting and Economics 24, 3—37.

Beyer, A., D.A. Cohen, T.Z. Lys, and B.R. Walther, 2010, The financial reporting environ-ment: Review of the recent literature, Journal of Accounting and Economics.

Caskey, J., and J. Hughes, 2010, Assessing the impact of alternative fair value measures onthe effi ciency of project selection and continuation, University of California, Los Angelesworking paper.

Chen, Q., T. Hemmer, and Y. Zhang, 2007, On the relation between conservatism in account-ing standards and incentives for earnings management, Journal of Accounting Research 45,541—565.

Chen, Y.J., and M. Deng, 2010, The signaling role of accounting conservatism in debt con-tracting, working paper.

Dewatripont, M., and J. Tirole, 1994, A theory of debt and equity: Diversity of securitiesand manager-shareholder congruence, The Quarterly Journal of Economics 109, 1027.

Diamond, D.W., 1991, Debt maturity structure and liquidity risk, The Quarterly Journal ofEconomics 106, 709—737.

Doidge, C., 2004, Us cross-listings and the private benefits of control: evidence from dual-classfirms, Journal of Financial Economics 72, 519—553.

, G.A. Karolyi, K.V. Lins, D.P. Miller, and R.M. Stulz, 2009, Private benefits ofcontrol, ownership, and the cross-listing decision, The Journal of Finance 64, 425—466.

32

Dyck, A., and L. Zingales, 2004, Private benefits of control: An international comparison,THE Journal of Finance 59.

Dye, R.A., 2002, Classifications manipulation and nash accounting standards, Journal ofAccounting Research 40, 1125—1162.

FASB, 2010, Statement of financial accounting concepts no. 8, Financial Accounting Stan-dards Board of the Financial Accounting Foundation.

Gigler, F., and T. Hemmer, 2001, Conservatism, optimal disclosure policy, and the timelinessof financial reports, The Accounting Review 76, 471—493.

Gigler, F., C. Kanodia, H. Sapra, and R. Venugopalan, 2009, Accounting conservatism andthe effi ciency of debt contracts, Journal of Accounting Research 47, 767—797.

Gox, R.F., and A. Wagenhofer, 2009a, Optimal impairment rules, Journal of Accounting andEconomics 48, 2—16.

, 2009b, Optimal precision of accounting information in debt contracting, EuropeanAccounting Review 19, 579—602.

Guay, W., and R.E. Verrecchia, 2006, Discussion of an economic framework for conservativeaccounting and bushman and piotroski (2006), Journal of Accounting and Economics 42,149—165.

, 2007, Conservative disclosure, Working paper, Social Science Research Network.

Holthausen, R.W., and R.L. Watts, 2001, The relevance of the value-relevance literature forfinancial accounting standard setting, Journal of Accounting and Economics 31, 3—75.

Imhoff, E., and J.K. Thomas, 1988, Economic consequences of accounting standards: Thelease disclosure rule change, Journal of Accounting and Economics 10, 277—310.