A Cluster Strategy Study of Printing and Publishing in...

58

A Cluster Strategy Study of Printing, Publishing and Advertising in Minnesota December 2010 Kane Bechstein Sasha Bergman Peter Jannett Lindsey Wollschlager

Transcript of A Cluster Strategy Study of Printing and Publishing in...

A Cluster Strategy Study of Printing, Publishing and Advertising in Minnesota

December 2010

Kane Bechstein Sasha Bergman Peter Jannett Lindsey Wollschlager

2

Table of Contents Economic Analysis of Minnesota’s Regional Economy ................................................................................. 4

Early Beginnings ........................................................................................................................................ 4

Roots of Minnesota’s Modern Economy .................................................................................................. 4

Challenges on the Horizon: Impact of the Great Recession .................................................................... 6

Character of Minnesota’s Export Markets ................................................................................................ 7

Investments in Education and Workforce Development.......................................................................... 8

Cluster Analysis ........................................................................................................................................... 10

Overview of the Printing, Publishing and Advertising Cluster in Minnesota .......................................... 11

Analysis of Economic Indicators for Statewide Cluster........................................................................... 12

Analysis of Printing .................................................................................................................................. 16

Analysis of Publishing .............................................................................................................................. 18

Analysis of Advertising ............................................................................................................................ 20

Underlying Economic Activity within the Cluster ................................................................................... 22

Analysis of Diamond of Advantage ............................................................................................................. 25

Firm Strategy, Structure and Rivalry ....................................................................................................... 26

Factor (Input) Conditions ........................................................................................................................ 27

Demand Conditions ................................................................................................................................ 27

Related and Supporting Industries ......................................................................................................... 28

SWOT Analysis............................................................................................................................................. 29

Strengths: ................................................................................................................................................ 29

Weaknesses: ........................................................................................................................................... 30

Opportunities: ......................................................................................................................................... 31

Threats: ................................................................................................................................................... 31

Emerging Trends in Printing, Publishing and Advertising ........................................................................... 32

Conclusion ................................................................................................................................................... 34

Recommendations to Increase Competitiveness: .................................................................................. 34

Organizing as a Cluster: ....................................................................................................................... 34

Collaborations with Related Industries or Institutions: ...................................................................... 35

Education and Workforce Development: ........................................................................................... 36

Special Thanks and Acknowledgements: .................................................................................................... 38

3

Works Cited ................................................................................................................................................. 39

Appendix A: State Location Quotients for Industry Sub-Fields .................................................................. 42

Appendix B: 2008 Advertising Employment by County ............................................................................. 44

Appendix C: 2008 Publishing Employment by County ............................................................................... 47

Appendix D: 2008 Printing Employment by County .................................................................................. 50

Printing Overall, Digital Printing and Book Printing ................................................................................ 50

Lithographic, Flexographic, Screen and Blank Book Printing .................................................................. 53

Manifold and Other Commercial Printing, Pre Press Services ................................................................ 56

4

Economic Analysis of Minnesota’s Regional Economy

Early Beginnings On May 11th, 1858, Minnesota officially became the 32nd state of the United States. The state

encompasses 86,943 square miles in north central United States. The physical composition includes

more than 11,000 lakes and a rich natural environment. Forests blanket the northern reaches of

Minnesota, while fertile prairie land extends across central and southern Minnesota. Despite being the

12th largest state geographically, Minnesota’s relatively low population places it at it 21st in the United

States with60% of Minnesotans living in the Twin Cities metro area. Rural counties are sparsely

populated except for areas near regional centers like Rochester, Duluth or Mankato.

Minnesota’s early economy was supported by natural endowments including lumber, large iron ore

deposits, and cultivatable land for agriculture. With easy access to waterways like the Mississippi River

and the Great Lakes, early millers such as the Northwestern Milling Company and Pillsbury benefitted

from the convenient shipping within the Twin Cities’ and Duluth harbors. Additionally, the University of

Minnesota began as a land-grant university in the 1850’s and provided early research support for

agriculture and other local industries.

In the early 1900’s, industrial development began to pull resources into urban areas to feed a growing

manufacturing industry. Companies like 3M and the Blandin Paper Company were founded at the turn

of the century and helped transform Minnesota’s economy through the introduction of advanced

production technologies. Following World War II, Minnesota’s economy quickly evolved with

innovations in farming practices and expansion into the food processing and biomedical technology

industries. Minnesota has continued to grow into a strong and diverse regional economy in the United

States.

The roots of the printing, publishing and advertising cluster are tied to some of these early industries.

As Minnesota developed a strong paper manufacturing sector, printing and publishing companies

appeared on the scene as well. Blandin Paper Company, for example, was established independently as

the Itasca Paper Company, but was soon bought by Charles Blandin, then owner of the St. Paul Pioneer

Press and Dispatch Printing Company (Blandin). Blandin Paper eventually transitioned away from

making newsprint paper to making magazine paper, and the company (now known as UPM) is one of

the largest producers of coated magazine paper in the world (UPM). Not coincidentally, Minnesota now

has a strong magazine publishing sector.

Roots of Minnesota’s Modern Economy Minnesota put this new prosperity to good use. Between 1929 and 1959, per capita income in

Minnesota was just average, ranking 25th in the United States (Grunewald 2010). Above average

investments in education during the 1940’s and 1950’s set the stage for “The Minnesota Miracle,” which

5

was enacted in 1971 and restructured education funding mechanisms to make it more equitable for all

school districts throughout the state (MHS). By the 1990’s, per capita income in Minnesota ranked 10th

nationally, and the state had built a strong reputation as “The State That Works” according to a Time

Magazine article written in 1973, highlighting Minnesota’s strong quality of life, low crime rate, and a

highly educated workforce (Time Magazine).

Today’s economy continues to outpace national averages. The mean personal income statewide has

remained approximately $2,500 above the U.S. average for the last decade, which indicates stable and

high productivity. Additionally, Minnesota outpaces the national average in labor force participation

and unemployment rates and is currently trending to further the gap. Ranking 10th nationally in patents

in 2008, it should come as no surprise that this innovative region is ahead of the curve.

Demographically, challenges are on the horizon for Minnesota. Population growth in the state is slightly

lower than national trends. Our workforce is aging faster than some other regions as well. Although

Minnesota is known for its highly productive workforce, a challenging transition may be ahead as Baby

Boomers retire and Minnesota employers turn to younger workers to fill in the gaps. This will be

particularly true for the printing industry, where the average age of employees is 57 and the average

length of employment within the industry is nearly 20 years (K. Davis). Interview sources suggest a

similar trend is playing out within publishing as well, though data is not available to confirm this

observation. As a result, future workforce training is a dominant concern among firms in publishing,

printing and advertising.

Table 1: Economic and Demographic Characteristics of Minnesota Compared to the U.S.

Source: U.S. Census and MN DEED

Basic Demographics & Performance

Minnesota U.S.

2008 Population 5,220,000 304,060,000

2007-08 Growth Rate 0.73% 0.92%

2008 Personal Income/Capita $43,037 $40,208

2008-09 Growth 3.05% 1.97%

2009 Labor Force Participation 71.90% 64.90%

2008-09 Growth Rate 0.56% -1.52%

2010 Unemployment Rate 6.90% 9.50%

2009-10 Change -0.90 pts -0.10 pts

Persons Below Poverty 9.60% 13.20%

6

As in other states, most jobs in Minnesota exist to serve local needs. According to Joe Cortright, an

economist and president of the Oregon consulting firm Impresa, most of the jobs in a given geographic

area serve the local economy. Cortright finds that about two-thirds of economic activity is the same

everywhere and is primarily local in nature. The other one-third to one-fourth of an area’s economic

activity is “unique” from other economies and primarily export-driven (Cortright).

In 2007, about a quarter of jobs in Minnesota were in “traded clusters,” or in other words, economic

sectors that produce goods and services primarily for export (Bryden). The Minneapolis-St. Paul

metropolitan region has a slightly larger share of jobs involved with export activity. In 1998, however,

the share of jobs in the traded sector was nearly 30%, suggesting that the traded sector has contracted

(Bryden). Both these measurements are snap-shots in time, so caution should be taken when trying to

infer a precise trendline for export activity. It would appear, however, that attention should be paid to

the potential weakening of our traded sectors. Michael Porter, of the Harvard Business School, suggests

that export activity is a good way to track the health of a regional economy since exports reflect an

ability to draw new money into a region to stimulate new growth.

Challenges on the Horizon: Impact of the Great Recession The “Great Recession” hit Minnesota hard. From 2008 to 2009 the state lost over 103,000 jobs

(-2.9%) (BEA). The big losses came from a 36,000 job decline in the manufacturing industry as well as a

19,500 job decline in construction. As seen in Table 2, 13 of the top 20 industries in Minnesota saw

declines in employment from 2008 to 2009. Only farming, utilities, and health care saw employment

increase above two percent during this period. Recent statistics from the Department of Employment

and Economic Development (DEED) note that Minnesota’s jobless rate is holding steady at 7% (DePass).

Overall, Minnesota performed better than the nation did in 12 of the 20 categories and by 0.3

percentage points overall.

One challenge in identifying trends within the printing, publishing and advertising cluster is that each

has subsector industries that are tracked within separate categories by governmental economic

agencies. Printing is included within manufacturing, as are the related industries of paper, inks, and

printing equipment such as engraved printing plates. Publishing is included within the information

sector, and advertising is included within the designation of “professional, scientific and technology”

services. Advertising is further split into categories that track the actual design work of advertising, as

well as marketing consulting and the sales and distribution of advertising materials.

Manufacturing employment in MN declined 10% in 2009, compared to 3-4% for the information and

professional services industries. Although the information below in Table 1 is a high level summary of

industry sectors in Minnesota, the relative declines in manufacturing versus information and

professional services reflects trends within the smaller printing, publishing and advertising cluster. Job

losses during the recession occurred across the cluster, but printing was impacted most severely. While

publishers and advertisers expect their work to pick up after the recession, uncertainty exists within the

7

printing sector. However, printing will remain an important industry for Minnesota. As technology

continues to change the face of printing it will likely increase its ties to advertising while distancing even

further from publishing. Direct mail advertising and packaging will increasingly become important

regional specializations for printers, as well as for advertisers.

Table 2: Changes in Minnesota Employment by Industry, 2008 to 2009

Minnesota Industry Employment

2008 2009 Change Change %

Farm employment 81,796 87,074 5,278 6.45%

Mining 9,002 9,076 74 0.82%

Utilities 13,253 13,550 297 2.24%

Construction 179,790 160,319 -19,471 -10.83%

Manufacturing 348,577 312,726 -35,851 -10.28%

Wholesale trade 144,258 137,240 -7,018 -4.86%

Retail trade 364,052 345,599 -18,453 -5.07%

Transportation and warehousing 108,316 102,406 -5,910 -5.46%

Information 67,188 64,545 -2,643 -3.93%

Finance and insurance 199,219 207,173 7,954 3.99%

Real estate and rental and leasing 134,773 132,025 -2,748 -2.04%

Professional, scientific, and technology 209,577 202,744 -6,833 -3.26%

Management of companies 72,697 71,492 -1,205 -1.66%

Administrative and waste services 167,999 154,722 -13,277 -7.90%

Educational services 78,712 79,507 795 1.01%

Health care and social assistance 430,576 440,818 10,242 2.38%

Arts, entertainment, and recreation 78,844 79,656 812 1.03%

Accommodation and food services 220,146 213,394 -6,752 -3.07%

Other services 182,899 177,288 -5,611 -3.07%

Government 419,931 416,473 -3,458 -0.82%

Source: U.S. Bureau of Economic Analysis

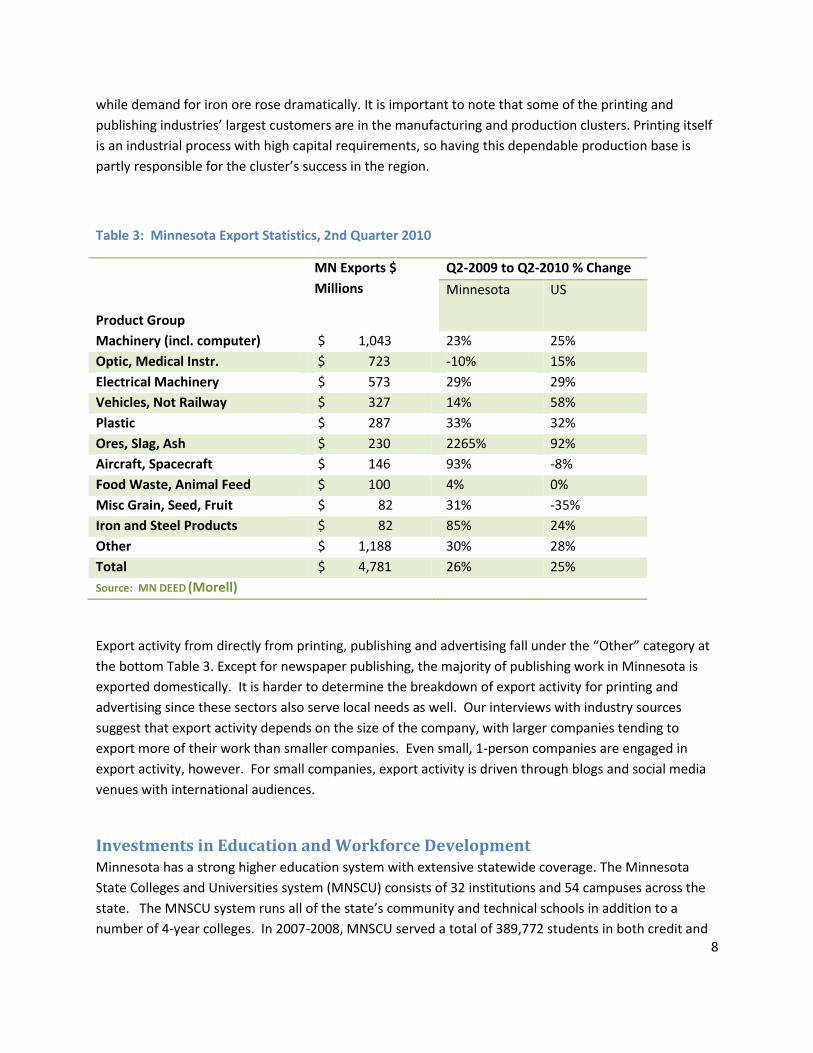

Character of Minnesota’s Export Markets Most recently there has been a strong upward trend in exports at both the state and national levels.

Exports for the US and Minnesota have increased 25% and 19% respectively in the past year. At almost

$5 billion in the second quarter alone, exports are a crucial piece of Minnesota’s economy and

competitive position. As demonstrated in Table 3 below, machinery was the largest export product in

2009, amounting to more than 20% of total export dollars. Minnesota’s biomedical industries

accounted for 15%of exports over this time and Ores, Slag, and Ash had tremendous gains as overseas

8

while demand for iron ore rose dramatically. It is important to note that some of the printing and

publishing industries’ largest customers are in the manufacturing and production clusters. Printing itself

is an industrial process with high capital requirements, so having this dependable production base is

partly responsible for the cluster’s success in the region.

Table 3: Minnesota Export Statistics, 2nd Quarter 2010

Product Group

MN Exports $

Millions

Q2-2009 to Q2-2010 % Change

Minnesota US

Machinery (incl. computer) $ 1,043 23% 25%

Optic, Medical Instr. $ 723 -10% 15%

Electrical Machinery $ 573 29% 29%

Vehicles, Not Railway $ 327 14% 58%

Plastic $ 287 33% 32%

Ores, Slag, Ash $ 230 2265% 92%

Aircraft, Spacecraft $ 146 93% -8%

Food Waste, Animal Feed $ 100 4% 0%

Misc Grain, Seed, Fruit $ 82 31% -35%

Iron and Steel Products $ 82 85% 24%

Other $ 1,188 30% 28%

Total $ 4,781 26% 25%

Source: MN DEED (Morell)

Export activity from directly from printing, publishing and advertising fall under the “Other” category at

the bottom Table 3. Except for newspaper publishing, the majority of publishing work in Minnesota is

exported domestically. It is harder to determine the breakdown of export activity for printing and

advertising since these sectors also serve local needs as well. Our interviews with industry sources

suggest that export activity depends on the size of the company, with larger companies tending to

export more of their work than smaller companies. Even small, 1-person companies are engaged in

export activity, however. For small companies, export activity is driven through blogs and social media

venues with international audiences.

Investments in Education and Workforce Development Minnesota has a strong higher education system with extensive statewide coverage. The Minnesota

State Colleges and Universities system (MNSCU) consists of 32 institutions and 54 campuses across the

state. The MNSCU system runs all of the state’s community and technical schools in addition to a

number of 4-year colleges. In 2007-2008, MNSCU served a total of 389,772 students in both credit and

9

non-credit courses, and the system graduated 33,722 students in 2008. Additionally, the University of

Minnesota system operates 5 campuses, 16 regional extension offices, and 16 research and outreach

centers statewide, with an enrolled student population of over 65,000.

Due in part to the educational achievements of its residents, 67% of jobs in Minnesota currently require

a post-secondary education. A report sponsored by the Georgetown University Center on Education and

the Workforce projects that the number of jobs requiring a college education will continue to rise,

possibly as high as 70% by 2018 (Carnevale). This positions Minnesota to continue growing its

knowledge-based economy, as well as to continue attracting well-educated workers to the state.

Minnesota’s continued demand for college-educated workers brings good tidings for our local publishing

and advertising sectors as they rely on highly literate and creative employees. However, Minnesota’s

shift towards a “knowledge economy” stands in contrast to the workforce needs of the manufacturing

sector. The 2010 State of Manufacturing report produced by Enterprise Minnesota finds that only 50%

of manufacturing jobs in Minnesota require training beyond high school, and the vast majority do not

require a full 4-year degree (Enterprise Minnesota). Further, in our interviews we learned that two-year

technical degrees are in demand by printing employers, since printing is a high-skill occupation requiring

specialized knowledge.

Minnesota’s economic future depends largely on whether or not its education system can provide the

necessary number of workers to meet future demands. Among Minnesota schools, few colleges offer

courses related to the printing, publishing and advertising industry cluster. A brief survey of current

course offerings in the UofMN and MnSCU systems found 10 campuses offering classes related to the

cluster. Most of these programs emphasize teaching desktop software skills, but these are not the skills

needed to fill current and projected job openings within the cluster. Only three colleges statewide

(Hennepin Technical College, Mesabi Technical College, and South Central College) offer programs and

courses in shop-floor production techniques that are critical to the printing industry, such as binding. In

addition, there is not a single college in MN that offers a degree program in publishing (Wallek). Book

publishers, in particular, spoke of the need for employees who are trained in layout, fact-checking, and

design for digital media like e-readers and social media applications.

In recent years there have been significant drop-offs in job-placement rates for these training programs.

This perhaps explains why there are many open seats in the technical and floor operation classes

offered by MnSCU. These technical and floor operation print skills are the most in-demand from

employers, however. Because of high demand for these skills from employers in the printing industry,

the inability to achieve full enrollment is troubling. The enrollment statistics in Table 4 detail the

difficulties in filling seats in shop-floor classes.

10

Table 4: Yearly Enrollment Statistics for MNSCU Printing Courses

Year College Program Seats Available

Seats Filled

Percent Filled

2007 Mesabi Graphic and Printing Equipment 480 259 54%

2008 Mesabi Graphic and Printing Equipment 480 307 64%

2009 Mesabi Graphic and Printing Equipment 480 266 55%

2010 Mesabi Graphic and Printing Equipment 588 394 67%

2007 Hennepin Graphic and Printing Equipment 61 47 77%

2008 Hennepin Graphic and Printing Equipment 53 34 64%

2009 Hennepin Graphic and Printing Equipment 65 46 71%

2010 Hennepin Graphic and Printing Equipment 56 34 61%

2007 Hennepin Operator 394 204 52%

2008 Hennepin Operator 351 164 47%

2009 Hennepin Operator 322 140 43%

2010 Hennepin Operator 292 118 40%

Source: MNSCU Academic Director Tamara Aarnodt

Cluster Analysis Traditional cluster definitions separate advertising from printing and publishing. The reasons for this are

historical. The printing and publishing industries have long-standing ties to each other. The first printing

and publishing companies in Minnesota date back to the late 1800s, and these early companies were

often vertically integrated with paper companies. For example, Charles Blandin purchased the Itasca

Paper Company in 1916 to secure a reliable source of newsprint paper for the St. Paul Pioneer Press /

Dispatch Printing Company (Blandin). Blandin later sold the Pioneer Press / Dispatch Printing Company,

but kept the paper mill, which became world famous under the Blandin name (Blandin). Similar

arrangements existed for book and periodical publishers as well. For example, the University of MN

Press developed as a joint printing and publishing operation to produce and disseminate the work of

University professors. Historically newspaper and periodical publishers played the role of local

advertisers as well. Around the 1950s, advertising developed as a mature industry in Minnesota.

Specialized firms emerged and operated independently of existing publishers. Yet, advertisers remained

an integral partner in the success of local printers and publishers. Because these new advertising

agencies were not vertically integrated with printers and publishers, the advertising industry has been

considered a separate entity. Economic development specialists have been slow to recognize that these

three industries operate together as one cluster.

This report began as a study of printing and publishing, but our interview subjects identified advertising

as an important component. In our analysis, the inclusion of advertising came late in the progress of this

study. Because we were operating under a limited timeline, we were not able to fully explore the

degree to which the advertising industry plays a role in the publishing and printing industry cluster. In

11

many ways, advertising is a distinctly different economic activity from publishing, and the skill sets

involved tend to be very different. Yet in Minnesota, publishers and advertising agencies draw upon

many of the same freelance writers, graphic designers and illustrators. These phenomena may be due

to strong occupational spillover. Further, innovations in printing are driven by customer demands from

publishing and advertising alike. Our research shows that these three industries are intricately bound

together in an interdependent customer-supplier network. Figure 1 provides a visual description for the

way we began to view the cluster.

Figure 1: Paradigm Shift in Defining Cluster

Overview of the Printing, Publishing and Advertising Cluster in Minnesota Minnesota is a hub for several industry clusters that have a competitive edge over other regions,

including medical devices, forest products, and many others. Depending on the region of focus within

the state, the presence and performance of industry clusters varies. The printing, publishing and

advertising cluster is one of the strongest in Minnesota, though the reach of these sectors do not spread

evenly across the state. Printing and publishing firms can be found in nearly every county of the state,

but advertising is generally concentrated in regional urban centers like Duluth, St. Cloud, Rochester and

the Twin Cities. In 2009, 68,000 people were employed in these three industries, representing more

than 3% of all jobs in Minnesota (BLS). More than 18,000 jobs have been lost since 2001, however,

reflecting the impact of the “Great Recession” but also some larger structural shifts in the economy

(BLS).

The University of Minnesota published an industry cluster report in 1995 that examined the

performance of printing and publishing, among other clusters located in the Minneapolis-St. Paul

metropolitan area (Munnich). The study found that the publishing and printing cluster in Minnesota had

12

the highest cluster employment concentration in the country, reflected by the presence of several large

firms in this market (Deluxe Corporation, West Publishing, and Quebecor). In the mid-1990s, the

printing industry in Minnesota ranked 5th in the United States behind Chicago, Los Angeles, New York

City and Philadelphia. According to the organization Printing Industry of Minnesota (PIM), Minneapolis

is now ranked 4th behind New York City, Los Angeles and Chicago (D. Radzeij, K. Davis).

This ranking should not cause over-confidence, however. Even as our local competitive advantage

increases, other regions continue to challenge us. Pennsylvania remains a competitive region for

printing, as is Dallas, TX (Bijnagte). Highly specialized printers in Colorado and Florida are also making

their mark, according to interviews with publishing and advertising sources. Silicon Valley is becoming a

new supply chain destination for publishers seeking talent to design online applications for digital

content. Outside the United States, printers in Winnipeg, CN, draw a lot of business away from

Minnesota, as do printers located in China. Minnesota is becoming known for producing high-quality

products with “artisanal touches.” Our reputation is positive, but it poses special challenges for local

companies trying to attract orders from companies who are primarily concerned with obtaining low

prices. Minnesota companies are price-competitive, but our region is not always perceived as being so.

Analysis of Economic Indicators for Statewide Cluster For the state as a whole, each sector of this cluster demonstrates a regional comparative advantage

compared to other states. Later sections will dive into the particular details of printing, publishing and

advertising, but for now it is worth noting that within each industry, Minnesota has developed niche

specializations that are highly concentrated here in Minnesota as compared to elsewhere. In the table

below, statewide location quotients are provided for the major industries involved in this cluster.

Generally, Minnesota’s regional competitiveness in printing, publishing and advertising has grown over

time, but qualifiers must be placed on this statement. For example, advertising in general is losing

regional competitiveness, but direct mail advertising is experiencing strong growth. Book publishing, is

also increasing growing more geographically concentrated, but Minnesota is losing competitiveness in

periodical publishing. The decline in specialized design services could be a worrying trend since

designers support the creative aspects of publishing and advertising.

13

Table 5: Specialization of MN Employment Compared to National Employment per Industry, 2001 and 2009

Industry 2009 Jobs

2001 LQ^

2009 LQ^

Change in LQ

Printing and Related Support Activities 26,374 2.06 2.46 0.40

Printing 24,280 2.08 2.44 0.36

Support Activities for Printing 2,094 1.90 2.78 0.88

Paper manufacturing 10,679 1.27 1.28 0.01

Pulp, paper, and paperboard mills 3,145 1.33 1.32 -0.01

Converted paper product manufacturing 7,533 1.24 1.27 0.03

Publishing Industries 22,647 1.32 1.39 0.07

Newspaper Publishers 6,517 1.10 1.14 0.04

Periodical Publishers 1,724 1.06 0.67 -0.39

Book Publishers 7,932 4.13 5.11 0.98

Advertising, PR, and related services 10,310 1.33 1.20 -0.13

Advertising agencies 3,763 1.14 1.08 -0.06

Direct mail advertising 1,924 1.40 1.72 0.32

Specialized design services 2,004 1.03 0.79 -0.24

Other professional and technical services 12,416 0.90 1.06 0.16 Data Source: U.S. Bureau of Labor Statistics Quarterly Census of Employment and Wages (QCEW)

^ A location quotient greater than 1.00 signifies greater local specialization in the industry than the nation as a whole. Positive changes between 2001 and 2009 means the industry is becoming more geographically concentrated in Minnesota. Negative changes between 2001 and 2009 means that the industry is shifting geographically towards other regions.

*2008 data

A location quotient greater than 1 indicates that the industry has a higher concentration of employment

relative to the nation. This indicator suggests that firms in these industries are more competitive than

other firms nationally due to the higher concentration of employment. A high location quotient also

indicates that the industry may produce a significant amount of exports to other regions.

As mentioned earlier, the printing, publishing and advertising industries have experienced job losses in

recent years. The “Great Recession” played a large role, but so did changing dynamics within each

industry. New printing technologies drive efficiency gains on the printing side, leading to reduced

employment. Additionally, the internet and growth of smart phones and other devices is transforming

the way people access information, leading to reduced demand for printed materials.

14

A few major trends can be noted. Minnesota’s regional competitiveness in printing has been growing

over time, though this trend is offset by declining employment. Comparatively, other states have lost

more jobs than Minnesota has. Book publishing has an extremely strong regional advantage in

Minnesota, but our regional competitiveness in periodical publishing is declining. Within advertising,

our state is developing a dominant position in direct mail advertising. Specialized design services

include graphic design, an important input for both advertising and publishing. Other professional

services include industries like private mail houses and packaging and labeling services.

Within the larger narrative of job losses, there is a silver lining. When local job loss rates are analyzed

against national industry trends and the performance of the U.S. economy as a whole, the particular

impact of the local industry is revealed. The shift-share table below “decomposes” job losses by parsing

out the effect of national employment trends, employment trends within the industry as a whole, and

employment trends within the local industries. This type of analysis shows that local job losses in

printing and publishing are largely driven by national factors. Advertising did not see any positive effect

from local trends. Without the strong performance of local firms, regional job losses over the past

decade would have been much higher.

Table 6: Analysis of Employment Changes in MN by Industry, 2001 - 2009

Changes in total employment

due to

Industry

National Economic

Trends

Local Industry Trends

National Industry Trends

Total Job Growth/ Loss

% Change in Jobs

Printing and Related Support Activities -697 4,356 -9,577 -5,917 -18.%

Paper manufacturing -324 132 -4,140 -4,332 -29%

Publishing Industries -596 1,045 -5,414 -4,965 -18%

Advertising, PR, and related services -281 -1,159 -1,256 -2,696 -21%

Specialized design services -59 -608 -69 -736 -27%

Other professional and technical services -189 1,883 1,956 3,650 42%

Business support services -334 -3,820 1,205 -2,949 -19% Data Source: MN Department of Employment and Economic Development and U.S. Bureau of Labor Statistics Quarterly Census of Employment and Wages (QCEW)

15

Printing and publishing firms are competitive across most regions of the state, except for the

northeastern corner by Duluth. As shown in Table 7 below, Southwest Minnesota has the highest

location quotient for publishing and printing, though to some degree this is a function of the low

population density in this region of the state. Southwest MN is also home to Mankato’s Taylor

Corporation, one of the country’s largest privately held firms (Taylor). Taylor Corporation owns more

than 80 subsidiaries in the United States and internationally, and on the whole, the company employs

more than 9,000 people. The Twin Cities metropolitan region has the next highest concentration of

printing and publishing jobs in the state. The major player in this region is Thomson Reuters. Thomson

Reuters employs tens of thousands people in over 400 locations worldwide, and the company traces its

roots back to 1799 with the founding of Sweet & Maxwell legal publishing company in London (Thomson

Reuters). West Publishing, a subsidiary of Thomson Reuters, is headquartered in Eagan, MN, and

employs about 8,500 people across the United States (West).

It should be noted that this table was drawn from work done by the MN Department of Employment

and Economic Development, and it only includes information for printing and publishing. Advertising

employment is not included in these calculations because advertising is generally concentrated in the

Twin Cities region.

Table 7: Regional Location Quotients for Publishing and Printing (Advertising Not Included)

Region Location Quotient for Publishing and Printing Cluster

(2008)

Northeast Minnesota 0.8

Northwest Minnesota 1.1

Southeast Minnesota 1.1

Central Minnesota 1.4

Twin Cities Metro Area 1.99*

Southwest Minnesota 3.2 Source: MN Department of Employment and Economic

Development (DEED)

*2006 data.

Some organizations we interviewed expressed doubt about the validity of using location quotients as a

basis for measuring the regional competitiveness of industries. Since location quotients are measuring

relative concentrations of employment, a high location quotient could indicate lower relative

productivity, since other regions may have higher capital investment rates that lead to reduced

employment. This is a valid question, and our existing data cannot entirely address this concern. With

location quotients close to 1, it would be difficult to rule out the confounding factor of capital

investment rates. Location quotients much higher than 1, however, are extremely difficult to achieve

without a true concentration of employment here.

16

Analysis of Printing Printing has a broad impact on Minnesota’s statewide economy. In 2009, there were over 900

companies located in most counties of the state and employing more than 26,000 people. Printing firms

paid a collective $1.2 billion in wages and generated more than $5.5 billion in sales (BLS, PIM). Average

annual wages for a printer is about $45,000, while average annual wages for prepress services is closer

to $58,000. This industry provides well-paying jobs, reflective of the skills demanded by the work

involved. Employment has declined 18% since 2001, however (BLS).

The printing industry is in an important period of transition. Some firms are starting to identify as being

in the “graphic communications industry” rather than “printing” (Taylor). The printing industry has a

strong presence across the state stemming from its historic relationship to the newspaper publishing

industry. Printing is a highly specialized industry, however. Without getting too bogged down in the

details, it is worth noting that new printing technologies have emerged over time without necessarily

replacing previous technologies. Some printing processes are better suited for certain types of

materials, while other processes are better suited for different size capacities. Even some printing

processes that could have been left for dead a generation ago are experiencing a revival. Letterpress

technology is on the rise again, as are engraving and etching processes. Thinking about what kinds of

policies could benefit the printing industry is a challenge. Official definitions don’t capture everything

the printing industry does or is capable of doing. This is a dynamic industry that is evolving with the

times, though they are facing challenges as the economy moves away from a dependence on printed

information. Direct mail advertising and packaging represent important growth sectors for Minnesota

printers. Other firms that focus solely on printing brochures and other materials are having a more

difficult time transitioning to the new era of digital media.

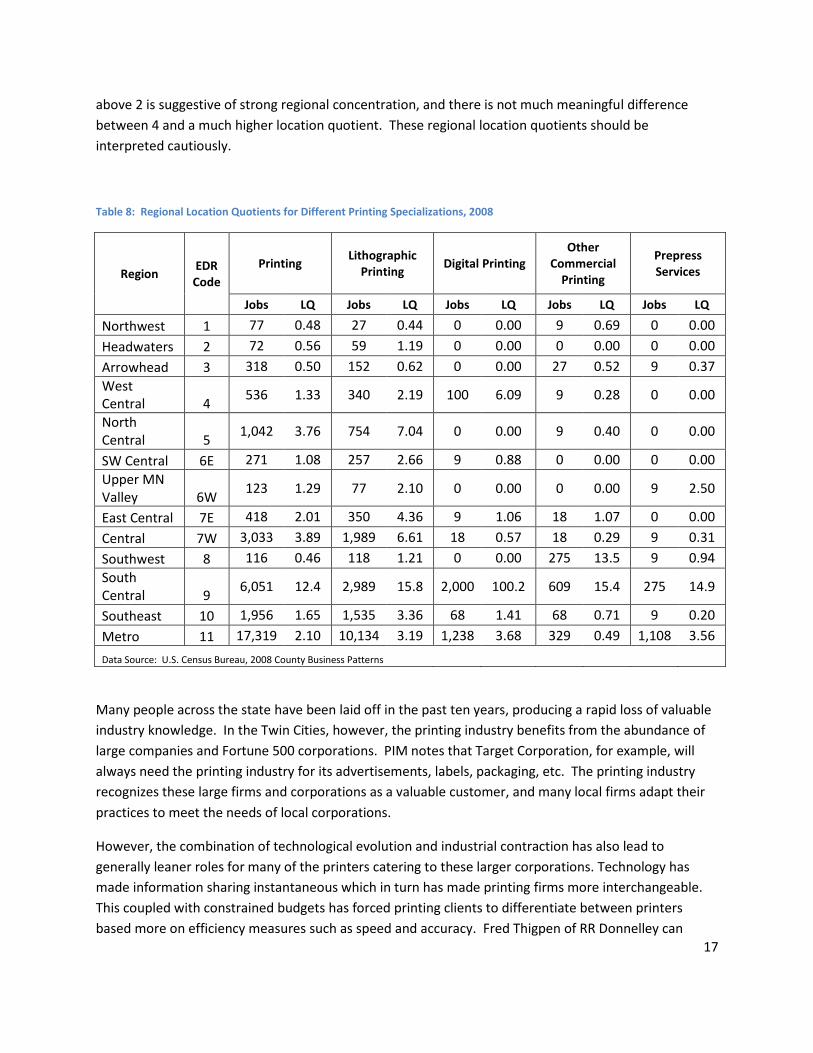

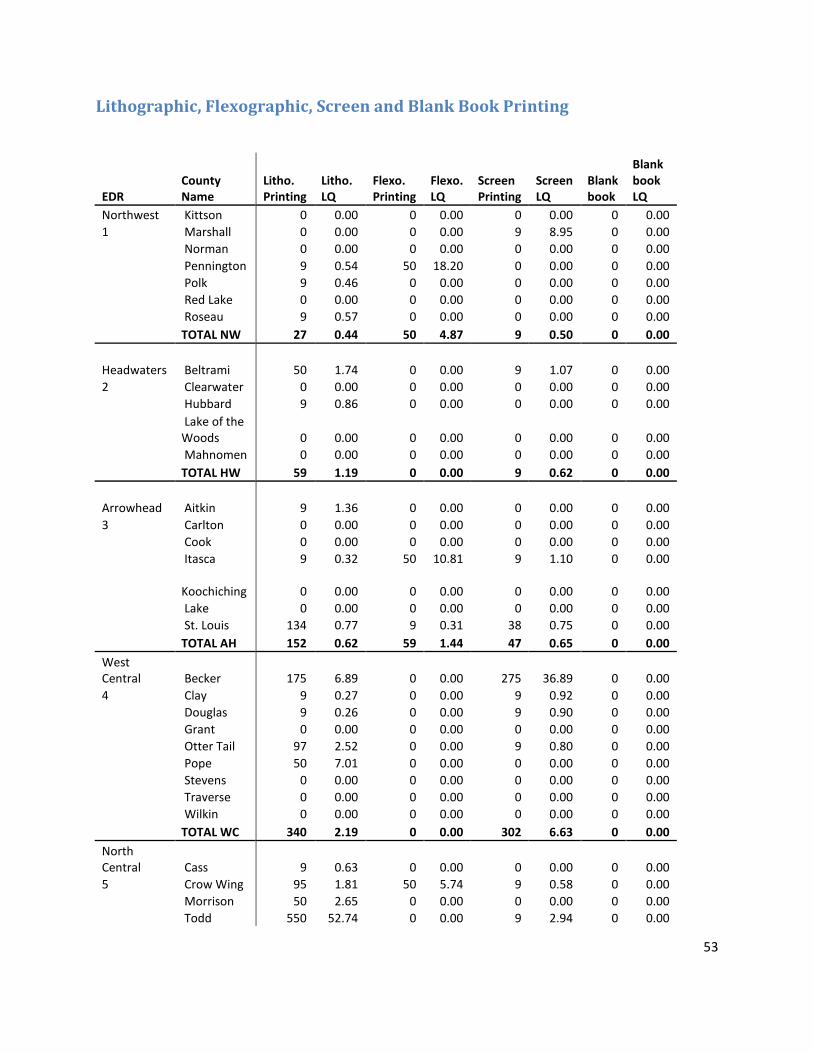

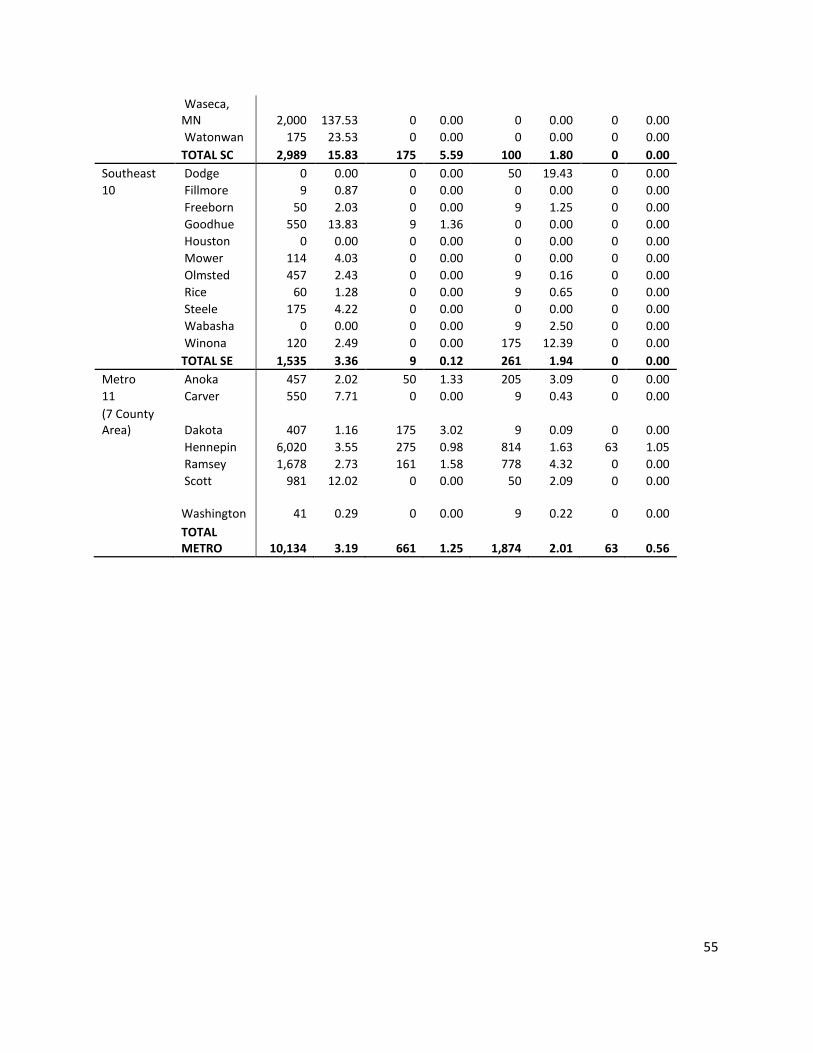

Table 8 compares the major printing specialties by economic development region. Lithographic printing

(also known as offset printing) is the most common type of printing done in Minnesota. Lithographic

printing is best suited for large print jobs, on the order of 50,000+ pieces (Westerlund). This type of

printing process is used for a wide range of products, including magazines, cardboard packaging and

some kinds of books. While large firms all have some degree of lithographic production capacity,

lithographic technology is also used by small community newspaper printers. In 2009, there were 85

newspaper printers in Minnesota, down from 219 newspaper printers in 2000 (PIA). Digital printing is

the fastest growing specialization, and these printers so far are concentrated in Mankato and the Twin

Cities (BLS). Taylor Corporation is the major player in this emerging sub-field. Prepress services are also

growing quickly, though these jobs are also largely concentrated in the Twin Cities and Mankato. Screen

printing and “other commercial printing” encompass products like clothing, labels, printing on products

like water bottles and casino chips, etc.

It should be noted that Table 8 below uses 2008 data, which is the most recently available data for

breakouts by individual counties. Job numbers have changed since 2008, but the relative geographic

distribution of these companies has not changed substantially. It must also be noted that location

quotients for small areas, like counties, have wide variance and are extremely sensitive to small changes

in quantity. We conducted sensitivity testing on this data and determined that a location quotient

17

above 2 is suggestive of strong regional concentration, and there is not much meaningful difference

between 4 and a much higher location quotient. These regional location quotients should be

interpreted cautiously.

Table 8: Regional Location Quotients for Different Printing Specializations, 2008

Region EDR Code

Printing Lithographic

Printing Digital Printing

Other Commercial

Printing

Prepress Services

Jobs LQ Jobs LQ Jobs LQ Jobs LQ Jobs LQ

Northwest 1 77 0.48 27 0.44 0 0.00 9 0.69 0 0.00

Headwaters 2 72 0.56 59 1.19 0 0.00 0 0.00 0 0.00

Arrowhead 3 318 0.50 152 0.62 0 0.00 27 0.52 9 0.37

West Central 4

536 1.33 340 2.19 100 6.09 9 0.28 0 0.00

North Central 5

1,042 3.76 754 7.04 0 0.00 9 0.40 0 0.00

SW Central 6E 271 1.08 257 2.66 9 0.88 0 0.00 0 0.00

Upper MN Valley 6W

123 1.29 77 2.10 0 0.00 0 0.00 9 2.50

East Central 7E 418 2.01 350 4.36 9 1.06 18 1.07 0 0.00

Central 7W 3,033 3.89 1,989 6.61 18 0.57 18 0.29 9 0.31

Southwest 8 116 0.46 118 1.21 0 0.00 275 13.5 9 0.94

South Central 9

6,051 12.4 2,989 15.8 2,000 100.2 609 15.4 275 14.9

Southeast 10 1,956 1.65 1,535 3.36 68 1.41 68 0.71 9 0.20

Metro 11 17,319 2.10 10,134 3.19 1,238 3.68 329 0.49 1,108 3.56

Data Source: U.S. Census Bureau, 2008 County Business Patterns

Many people across the state have been laid off in the past ten years, producing a rapid loss of valuable

industry knowledge. In the Twin Cities, however, the printing industry benefits from the abundance of

large companies and Fortune 500 corporations. PIM notes that Target Corporation, for example, will

always need the printing industry for its advertisements, labels, packaging, etc. The printing industry

recognizes these large firms and corporations as a valuable customer, and many local firms adapt their

practices to meet the needs of local corporations.

However, the combination of technological evolution and industrial contraction has also lead to

generally leaner roles for many of the printers catering to these larger corporations. Technology has

made information sharing instantaneous which in turn has made printing firms more interchangeable.

This coupled with constrained budgets has forced printing clients to differentiate between printers

based more on efficiency measures such as speed and accuracy. Fred Thigpen of RR Donnelley can

18

recall when his printing job used to include meeting with publishers monthly and assisting with creative

solutions, but today this aspect of mass printing is being phased out.

In the context of relative competitiveness, it’s important to benchmark the local printing industry

against the national. According to the Printing Industry of America (PIA), printing has been in a state of

decline and consolidation for nearly two decades. Since 1993 the number of plants nationally has

declined from over 54,000 to under 34,000. With larger firms better set to weather tough times, the

lion’s share of firm closures have been from smaller firms. From 2000 to 2009, the largest total losses

came from firms with 9 or fewer employees (7,916 closures) while the largest relative decline came from

firms with 10-49 employees (35.9%) (PIA). This has in turn lead to mass consolidation industry-wide as

the average firm size based on the number of employees has leapt from 17 in 1993 to 27 in 2009 (PIA).

As a result of these consolidations, however, the industry as a whole has seen growth in productivity

from new equipment and processes. In general, PIA believes the industry will continue to contract in

the coming years, though the surviving firms will remain diverse in size with a majority family-owned.

The diversity of customers for the printing industry will maintain the high degree of niche specialization

evident within the industry (PIA).

Analysis of Publishing Publishing is commonly described as “creating and delivering a message.” This definition can blur the

lines a bit with the role advertising plays in the economy. The U.S. Department of Labor officially defines

publishing as the “distribution of information,” noting that publishers work with copyrighted material.

This distinction creates conceptual clarity, but it should be noted that there are some firms that do not

fall cleanly into either the publishing or advertising label.

Publishing has a broad impact on Minnesota’s statewide economy, though most publishing firms are

located in the Twin Cities, Duluth and Mankato. In 2009, there were 930 firms located in most counties

of the state and employing more than 23,000 people (BLS). Most of the publishers located in rural

counties are newspaper publishers employing fewer than 10 people, however. Publishing firms paid a

collective $1.5 billion in wages in 2009 (BLS). Average annual wages for a publisher varies widely

depending on the specialization, but the average salary in 2009 was about $65,000 (BLS). Other average

salaries:

Software publishers: $94,000

Book publishers: $71,000

Periodical publishers: $52,000

Newspaper publishers: $38,000

Each of these publishing specializations pays more than the average wage in Minnesota, with the

exception of newspaper publishing. Since newspaper publishing is the most broadly distributed in rural

counties, however, it is possible that newspapers pay a competitive local wage relative to the other

types of jobs available in rural counties. Like printing, publishing employment has declined 18% since

19

2001 (BLS). Most of the job losses are concentrated in newspapers (-21% with 4,400 jobs lost) and

periodicals (-53% and 1,900 jobs lost) (BLS).

Table 9 breaks down the regional specialization of publishing employment. As with the regional printing

location quotients, the regional breakouts for publishing express wide variance and high sensitivity to

small changes in quantities. Nonetheless, Table 9 gives a representative snapshot of regional

distribution of publishing activity in Minnesota. Newspapers represent the majority of jobs statewide,

with the distribution of newspapers largely following population density patterns. Periodical publishing

is mostly clustered in Duluth, Mankato and Twin Cities. Periodical publishers in MN tend to produce

extremely specialized magazines dedicated to niche interests, like powersports, boating and horse

training.1 The Minneapolis-St. Paul region claims the lion’s share of jobs in book publishing. National

brands like Lerner, Llewellyn and Cengage are headquartered in the Twin Cities, as well as smaller

nonprofit publishers like Milkweed and Graywolf Press. The region is also home to a few newer “DIY”

book publishers, like Beaver’s Pond Press, that help authors self-publish their work.

Table 9: Regional Specialization of Publishing Employment vs. National Employment per Industry, 2008

Region EDR All Publishing Book Publishing Newspaper Publishing

Periodical Publishing

Jobs LQ Jobs LQ Jobs LQ Jobs LQ

Northwest 1 205 0.86 0 0.00 117 1.34 68 1.79

Headwaters 2 260 1.37 0 0.00 159 2.27 18 0.59

Arrowhead 3 948 1.00 9 0.10 516 1.48 284 1.87

West Central 4

251 0.42 9 0.17 217 0.99 59 0.62

North Central 5

334 0.81 9 0.24 293 1.93 18 0.27

SW Central 6E 236 0.64 0 0.00 152 1.11 50 0.84

Upper MN Valley 6W

60 0.43 0 0.00 60 1.16 0 0.00

East Central 7E 127 0.41 0 0.00 118 1.04 18 0.36

Central 7W 611 0.53 50 0.48 503 1.18 27 0.15

Southwest 8 444 1.19 0 0.00 401 2.91 18 0.30

South Central 9

1,203 1.66 259 3.94 515 1.93 77 0.66

Southeast 10 1,297 0.74 68 0.43 841 1.30 186 0.66

Metro 11 23,648 1.94 7,923 7.17 3,243 0.72 1,320 0.68

Data Source: U.S. Census

1 See, for example, the membership directory of the MN Magazine and Publishers Association:

http://www.mmpa.net/directory.html

20

The publishing industry in Minnesota is largely broken into three specializations, each operating

independently from the others: books, newspapers and periodicals. Software publishers also have a

presence in the state, though to a lesser degree. Additionally, within each sub-field, publishers are

highly specialized within distinct niches (Schiffman). As a result, publishers find they have more in

common with their vendors and customers than with fellow publishers. Unlike printing, which is unified

under a single strong industry organization (PIM), the publishing industry in Minnesota has developed

multiple industry organizations, including three separate organizations for book publishers. Periodical

publishers are mainly unified through the MN Magazine and Publishing Association, while the MN

Newspaper Association is the main newspaper publishing organization.

Publishing has been impacted by new technologies, but not to the severe degree witnessed in printing.

There has been a 10% contraction in the number of publishing firms in MN since 2001, compared to a

contraction rate of 14% in printing (BLS). Most of the publishers that went out of business were

newspaper and software publishers (BLS). The new technologies causing the most disruption in

publishing are e-readers and various social media applications. Many publishers are embracing the new

technologies, however, and rushing to adapt their content delivery modes. Mary Hennessy, with the

Industrial Fabrics Association International (IFAI) described their transition into digital products, and she

noted that the use of digital applications, such as PDFs, offers IFAI the potential for greater profitability

due to quicker turnaround times. Looking ahead, Hennessy notes that social media technologies should

not to be ignored and is likely the key to the future of the industry.

Publishing firms seem to be embracing the winds of change and continue to look ahead to the future to

see how they will fit in. Innovation tends to be driven by introduction of new devices (iPad, Kindle,

Nook, etc) or by updates to a key software program, like Adobe (Wallek, Schiffman). However, the

publishing industry in Minnesota is typified by a variety of niche firms, from children’s books to online

higher education publications. Competition within these niches appears to be less fierce than what is

experienced by companies seeking to meet a broader readership market. Kevin Coghlan, President of

The Coghlan Group, notes that his firm specializes in the marketing and production of local higher

education publications, a niche that few other periodical publishers pursue. Mary Hennessy, Vice

President of Communications for the Industrial Fabrics Association International (IFAI) also describes a

niche in the business-to-business publications produced for their members. Because of the lack of direct

competition, IFAI demonstrates a willingness to collaborate with other firms within the publishing

industry.

Analysis of Advertising

Like the printing and publishing industry sectors, the advertising industry has changed significantly in

recent years. Since we incorporated advertising into the study fairly late in the game, we have less

analysis pertaining to this industry. Like publishing, the advertising industry is difficult to pin down and

fit neatly into a box. The U.S. Department of Labor defines advertising as “creating an advertising

campaign.” (NAICS). For the purposes of this report, we will use the definition of “messaging intended

21

to sell something.” Advertising firms are diverse and broadly work to satisfy the needs of their clients.

This means that advertising work tends to be both digital and print, depending on the audience that is

targeted for the product promotion. Advertising agencies provide a range of services to their clients,

including: “advice, creative services, account management, production of advertising material, media

planning, and buying (i.e., placing advertising) (NAICS).”

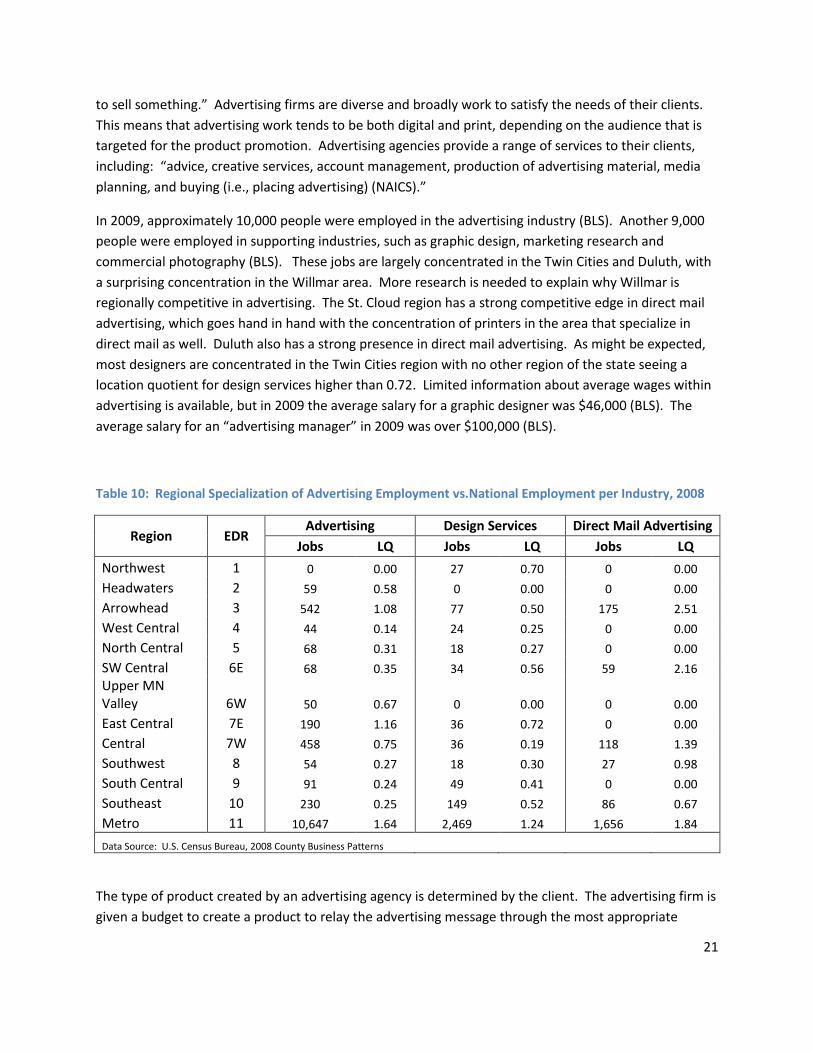

In 2009, approximately 10,000 people were employed in the advertising industry (BLS). Another 9,000

people were employed in supporting industries, such as graphic design, marketing research and

commercial photography (BLS). These jobs are largely concentrated in the Twin Cities and Duluth, with

a surprising concentration in the Willmar area. More research is needed to explain why Willmar is

regionally competitive in advertising. The St. Cloud region has a strong competitive edge in direct mail

advertising, which goes hand in hand with the concentration of printers in the area that specialize in

direct mail as well. Duluth also has a strong presence in direct mail advertising. As might be expected,

most designers are concentrated in the Twin Cities region with no other region of the state seeing a

location quotient for design services higher than 0.72. Limited information about average wages within

advertising is available, but in 2009 the average salary for a graphic designer was $46,000 (BLS). The

average salary for an “advertising manager” in 2009 was over $100,000 (BLS).

Table 10: Regional Specialization of Advertising Employment vs.National Employment per Industry, 2008

Region EDR Advertising Design Services Direct Mail Advertising

Jobs LQ Jobs LQ Jobs LQ

Northwest 1 0 0.00 27 0.70 0 0.00

Headwaters 2 59 0.58 0 0.00 0 0.00

Arrowhead 3 542 1.08 77 0.50 175 2.51

West Central 4 44 0.14 24 0.25 0 0.00

North Central 5 68 0.31 18 0.27 0 0.00

SW Central 6E 68 0.35 34 0.56 59 2.16

Upper MN Valley 6W 50 0.67 0 0.00 0 0.00

East Central 7E 190 1.16 36 0.72 0 0.00

Central 7W 458 0.75 36 0.19 118 1.39

Southwest 8 54 0.27 18 0.30 27 0.98

South Central 9 91 0.24 49 0.41 0 0.00

Southeast 10 230 0.25 149 0.52 86 0.67

Metro 11 10,647 1.64 2,469 1.24 1,656 1.84

Data Source: U.S. Census Bureau, 2008 County Business Patterns

The type of product created by an advertising agency is determined by the client. The advertising firm is

given a budget to create a product to relay the advertising message through the most appropriate

22

medium that will allow the advertisement to reach its targeted audience (Olson, Yantes). There has been

a shift over the years in the types of advertising products being produced due to the social networking

and technological shifts over time. Entire positions have been eliminated over time due to the improved

technology and software, decreasing the need for an actual human to complete a task (Walker).

Advertising firms face different challenges related to new technologies than printers and publishers do.

For some businesses, the increased use of technologies like GoogleMaps and consumer-level GPS

systems draw viewers away from traditional advertising venues. Multiple advertising interview sources

see a continued need for printed products, however, particularly for the tourism and hospitality sectors.

Hedberg Maps specializes in creating customized promotional maps for events like Holidazzle, industry

conventions, and key destination corridors like the Midtown Greenway (Jordan). Companies see value

in Hedberg’s products because a customized printed map allows companies the opportunity to put their

branding front and center. Given the fickle nature of technology trends, the challenge for the

advertising industry lies in anticipating which technology trends are fads and which trends will become

permanent features of the new advertising landscape. Some advertising sources remembered the

“multi-media” fad of the 1990s when providing promotional CDs and DVDs was projected to remake the

industry. Those efforts did not have nearly the impact with consumers that advertisers hoped.

Underlying Economic Activity within the Cluster The connections within the cluster remained obtuse until we considered the basic economic activity

underlying printing, publishing and advertising. Each industry responds to this chain of activity. There is

an idea that goes through a design phase and then distributed by an entity in a specific product form.

When considering the roles that publishing and advertising play in the economy, this basic chain of

activity takes on different characteristics. Figure 2 below identifies some of the interconnected

processes involved in the value chain for printing, publishing and advertising. Interview sources

identified three economic drivers that stimulate activity in the PPA cluster: the knowledge creation

sector, as in research generated by the University system; the arts and creative sector, as in the

Minneapolis College of Art and Design (MCAD); and general business needs, as in demand for products

that fluctuates with the standard business cycle. The top chain of activity relates mostly to publishing,

while the bottom row relates mostly to advertising. At the top, an idea is developed by an author or

IDEA DESIGN PHASEDISTRIBUTION

AGENTPRODUCT

FORM

23

journalist, which then goes through an editing phase, and is then distributed in print or online by a

publisher. A similar process happens with advertising. A product generates need for an advertisement

or packaging, which goes through a graphic design phase and is distributed through various print and

online platforms. In reality, this process is much more complicated, but this concept map helps

elucidate some of the basic activities involved in this cluster.

Figure 2: Value Chain for Printing, Publishing and Advertising. Source: Author created using information from interview sources.

We showed the above value chain map to a group of graphic designers, and they respectfully disagreed

(Tolsma, Westerlund). They felt that a value chain filled with boxes and arrows wrongly gives equal

weight to all aspects of the production chain. In reality, they argued, the market success of these

products ultimately rests on the strength of the idea. Does that idea have a compelling design? Is it

produced in a quality and affordable way? Only then, they argued, should the distribution method be

worried about. According to the graphic designers we interviewed, the printing industry is primarily

concerned with the production and distribution of products in a physical form, while the advertising and

publishing industries are concerned with the design and production phases. To help illustrate their

argument, the designers crafted a “value pyramid,” included below in Figure 3 (Tolsma, Westerlund).

24

Figure 3: Value Pyramid Proposed by Graphic Designers for Printing, Publishing and Advertising Cluster

We then shared this value pyramid with a group of printers, who respectfully disagreed with the graphic

designers (PIM). Printers often have to adjust designs because they are not aligned with production

standards. The printers argued that consideration should first be given to the production process, and

only then should the design be finalized. Figure 4 below illustrates the value chain proposed by printers.

Figure 4: Value Pyramid Proposed by Printers

The purpose of this report is not to declare a winner or loser in this friendly debate, but the

disagreement between printers and graphic designers perhaps highlights an opportunity for

collaboration within the industry. If the local companies involved in this cluster found a way to

Distribution

Design Execution

Production Process

Idea

25

strengthen the institutional linkages between designers and printers, our region could create a

competitive advantage that perhaps does not exist in other locations. The printers, publishers and

advertisers interviewed for this study identified time as a crucial element for competitive success.

Nationally, companies are competing on turn-around time. Eliminating the need for printers to

reconfigure design could help speed up the production process, helping our local cluster distinguish

itself from other regions.

The intersection of these three industries highlights an unusual inter-dependency between the creative

sector and manufacturing. Without a comprehensive evaluation of these industries together, policy

makers may not recognize the state’s mutual reliance on fine and industrial arts.

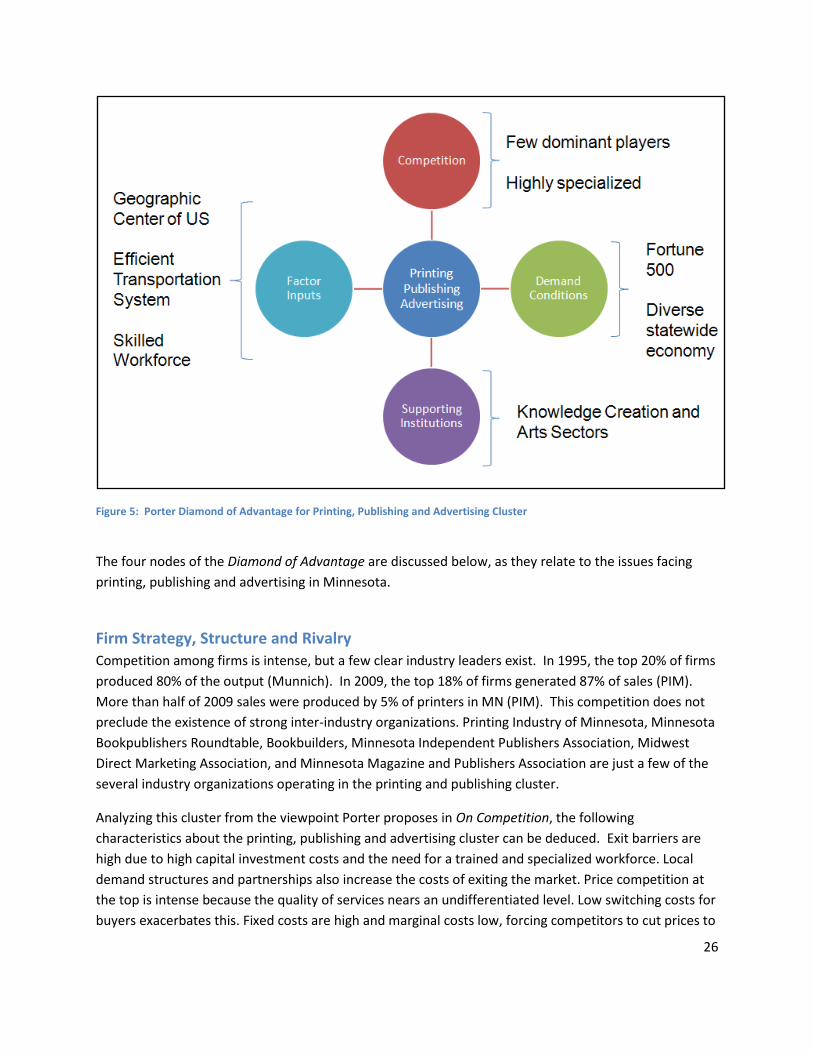

Analysis of Diamond of Advantage

Using the Porter Diamond, an assessment tool for cluster analysis to evaluate the interplay among four

“broad attributes” that Porter argues are key determinants of competitive advantage (Porter: 227).

1. Factor Inputs: factor (input) quantity, costs, quality and specialization – natural resources,

human resources, capital resources, physical infrastructure, administrative infrastructure,

information infrastructure, scientific and technological infrastructure.

2. Competition: a local context that encourages appropriate forms of investment and

sustained upgrading. Also includes competition among locally-based rivals.

3. Demand Conditions: sophisticated and demanding local customers who have needs that

anticipate those elsewhere. Could also include unusual local demand in specialized

segments that can be served globally.

4. Supporting Institutions: presence of capable, locally-based suppliers, as well as the presence

of competitive related industries.

A notable feature of the Diamond of Advantage is that it focuses on the characteristics of the business

environment. The role of government is deemphasized, but evident on the margins. The schematics of

the Diamond serve to emphasize that many of the issues related to competitive advantage are best

solved by the private sector, yet government has an important role to play in promoting policies that

support broad needs, such as workforce and infrastructure development.

26

Figure 5: Porter Diamond of Advantage for Printing, Publishing and Advertising Cluster

The four nodes of the Diamond of Advantage are discussed below, as they relate to the issues facing

printing, publishing and advertising in Minnesota.

Firm Strategy, Structure and Rivalry

Competition among firms is intense, but a few clear industry leaders exist. In 1995, the top 20% of firms

produced 80% of the output (Munnich). In 2009, the top 18% of firms generated 87% of sales (PIM).

More than half of 2009 sales were produced by 5% of printers in MN (PIM). This competition does not

preclude the existence of strong inter-industry organizations. Printing Industry of Minnesota, Minnesota

Bookpublishers Roundtable, Bookbuilders, Minnesota Independent Publishers Association, Midwest

Direct Marketing Association, and Minnesota Magazine and Publishers Association are just a few of the

several industry organizations operating in the printing and publishing cluster.

Analyzing this cluster from the viewpoint Porter proposes in On Competition, the following

characteristics about the printing, publishing and advertising cluster can be deduced. Exit barriers are

high due to high capital investment costs and the need for a trained and specialized workforce. Local

demand structures and partnerships also increase the costs of exiting the market. Price competition at

the top is intense because the quality of services nears an undifferentiated level. Low switching costs for

buyers exacerbates this. Fixed costs are high and marginal costs low, forcing competitors to cut prices to

27

steal incremental customers. Larger firms exhibit economies of scale and require new entrants to enter

the industry on a large scale, which is complicated by the capital requirements of the industry. Supply-

side economies of scale can exist anywhere in the value chain: the most vital value chain links in Printing

and Publishing are transportation and logistics, telecommunications and IT, and manufacturing facilities

(Munnich). According to Porter, supply side economies of scale greatly reduce the threat of new

entrants.

Factor (Input) Conditions

Favorable factor conditions for the Printing and Publishing cluster are due in large part to geographic

location, strong infrastructure, natural resource endowments, and human capital. Minnesota is very

near to the center of the North American continent, linked to the east, west, and gulf coasts by major

interstate highways and rail lines. The Twin Cities also have exceptional telecommunications

infrastructure, which has created a very favorable environment for several of Printing’s biggest

customers, including the computer software industry and the advertising and design industry (Hackler).

The Printing and Publishing cluster benefits greatly from Minnesota’s extensive natural resources and

from its legacy industries. Minneapolis was at one time a premier mill-city and its acquisition of capital

and industrial investment lead to diversification in manufacturing and production. Access to timber, iron

ore, and water prompted expansion into metalworking and production technology (Munnich).

Having a skilled and highly educated workforce is typically seen as an advantage to the printing and

publishing cluster, but this disproportionately benefits publishing. The printing industry depends on a

stream of skilled factory and shop floor workers, usually in positions that require 2-year technical

degrees. The number of degree programs has been shrinking in recent years due to a lack of student

interest and the high costs associated with acquiring up-to-date training equipment. Hennepin Technical

College has the largest program in the MNSCU system, but staff with the program admits that it does

not train enough students to fulfill even local employer demand.

Demand Conditions

Minnesota has considerable regional markets for printing and publishing services. Several of Printing

and Publishing’s biggest customers have a heavy presence in the Twin Cities region: ad agencies, graphic

design firms, IT software, and machine and metalworking to name a few (Munnich). The Twin Cities are

one of a select few national hubs for direct mail advertising and magazine distribution, both of which

benefit from Minnesota’s central location (Bijnagte, Hennessey). Network effects exist across industries

for the services provided by Thomson Reuters, which is both a major publisher and provider of legal

services. Major local purchasers include: accounting and financials, universities, machinery and

metalworking, corporate headquarters, hospitality businesses, advertising and graphic design firms,

telecommunications and the IT industry (Munnich). The Twin Cities has one of the 10 highest

28

concentrations of advertising agencies in the nation, and local demand is anchored by a diverse base of

customers, but the printing and publishing cluster still manages to sell 50% of total sales outside of the

Twin Cities (Munnich).

The existence of several printing and publishing rivals creates cost savings opportunities for buyers.

Several large-volume buyers exist in the local market, and printing and publishing has high-fixed costs

(Munnich). High costs and low marginal costs amplify the pressure on rivals to keep capacity filled

through discounting (Munnich). High levels of competition over time have created a sector that has

consistently high quality. This means that the industry’s products are at least somewhat standardized. If

buyers believe they can find equivalent products across providers they can play rivals against one

another (Munnich). Buyers also most likely do not face high switching costs, and so prices are held down

(Munnich).

Related and Supporting Industries

Printing and Publishing take advantage of several strong supporting industries and institutions.

Minneapolis is a central transportation hub for the region, and so logistics and transportation industries

are very strong (Munnich). Printing especially depends on these companies, and Minneapolis’ position

as a national hub for direct mail and magazine distribution is evidence of the strength of these

companies. Direct inputs like timber and paper are also strong industries in Minnesota, both of which

benefit from the state’s plentiful natural resources and historical economy (Munnich). The existence of

several large law firms and financial firms has also lead to horizontal diversification: Thomson Reuters

purchased WESTLAS in the 1990s, and has established that division as both a legal publisher and as a

legal services provider (Munnich). Along with major finance companies comes availability and access to

financing opportunities (Munnich). Because of the capital intensive nature of printing, local companies

benefit from the existence of multiple potential funding sources (Munnich).

Minnesota also has the second highest recycling rate in the nation, and the recycling industry employs

over 20,000 people (MPCA).2 Linkages between timber harvesting, paper production, printing, and

recycling, all lead to greater efficiency and mitigate possible negative environmental externalities of the

printing and publishing industry (Munnich). Suppliers of other production inputs are found throughout

the state. Specialty ink and paper companies have strong ties to the printing industry, and a few have

members on the board of PIMN.

2 MN Pollution Control Agency. Retrieved from: http://www.pca.state.mn.us/index.php/living-green/living-green-

citizen/reduce-reuse-recycle/recycling-more-ways.html

29

SWOT Analysis A common way to summarize the business environment of a firm, or in this case the printing and

publishing cluster, is to utilize a SWOT (strengths, weaknesses, opportunities, and threats) analysis

approach. For this analysis strengths and weaknesses are defined as the internal characteristics that

place the firm, relative to others, at an advantage or disadvantage, respectively. Opportunities and

threats are then the external factors. Opportunities are chances to grow or become more profitable

within the environment while threats are potential obstacles to success. The SWOT tool can be

beneficial for decision makers within a cluster as it presents the current environment in a manner

conducive to identifying areas for improvement and advantages to build upon.

Strengths:

To reiterate from above, Minnesota’s printing and publishing cluster has a number of local advantages

that help maintain its national competitiveness. Minnesota’s emphasis on the value of education has

created a reputation for productivity that draws companies to the region, which is not unique to the

printing industry. Our interview subjects commented repeatedly that despite the challenges facing the

printing industry, the strong work ethic of employees has helped keep local companies afloat.

The natural endowments of lumber in the area coupled with very efficient paper producing firms afford

local printers easy access to a key input. Having this resource locally available provides Minnesota

printers with the ability to make last minute changes to paper orders which can be….

Minnesota’s central location and well developed infrastructure provide an additional edge to local

manufacturers. Despite rush-hour congestion, our extensive network of highways is cited as one of the

prime reasons the local printing industry is more efficient than places like New York City or Los Angeles,

where nearly constant gridlock prevents easy movement of inputs through the production process

(Radzeij). When time is of the essence, being able to print and deliver material to a mail house within

the same day gives Minnesota printers a competitive advantage. The central location has also been

historically beneficial for timely shipping to customers on both coasts. For this reason Minnesota has

developed a niche specialization in direct mail advertising because national corporations are able to

time the delivery of direct mail promotions so that they arrive on both coasts on the same day. The

promotions are designed and printed here in Minnesota, then delivered to households across the

country. Minnesota has also developed a specialization in magazine publishing and printing for similar

reasons.

The local industries have also differentiated themselves from others nationally both with their more

holistic approaches and specialized customer bases. In general, Minnesota printers and publishers have

both claimed to take on more responsibilities and a larger role in total production to differentiate

themselves from the competition. Many of the publishers have also found more specific niches and

which may be isolating from much of the competition.

30

Weaknesses:

Although Minnesota’s printing and publishing cluster has many tangible advantages, in some ways these

differentiating characteristics have also put the cluster at a disadvantage. For example, the central

location and ability to serve large demand on both coasts has always been an advantage, but our

location makes it tougher to attract talent to the area from other areas with strong printing and

publishing labor supplies such as New York or Los Angeles. This inability to bring in qualified workers

would not be such a big issue if as a state Minnesota was training its own labor force to fill these

positions, but unfortunately there are areas in which it comes up short.

At a time when the strong education system is cited as one of the prime reasons for our regional

competitive edge, its limited specialization in printing and publishing also poses problems for the

cluster. Within Minnesota there in an absence of publishing degrees, so many firms are content with

Journalism and English majors to fill roles. However, others admit that finding workers prolific in writing,

design, and newer technologies can be difficult with recent graduates and they are forced to contract

out to freelance workers more familiar with cutting edge technologies from places like New York.

For printing, only three public higher education institutions in Minnesota provide training on using the

printing press and other shop floor equipment (Mesabi, Mankato and Anoka-Hennepin technical

colleges). Budget shortfalls in the MNSCU system has led to a redirection of course offerings towards

computer-based skills for desk-top publishing rather than skills associated with printing equipment, such

as robotics programming. Rumors abound that Mankato is considering closing the doors on its printing

program, despite the large philanthropic support over the years from printers like Glen Taylor (Kenney-

Fine). Public technical colleges have not had the resources in recent years to invest in new capital

equipment. Dunwoody Institute, a private technical education school, has helped fill the gap to some

extent.

A related concern expressed by the printing industry is the lack of emphasis on printing as a vocation in

the K-12 education system in Minnesota. Davis notes that there may be only two high schools in the

state that are actively introducing students to careers in print. This trend follows a shift away from

vocational training in general, as the state has placed greater emphasis on preparing students to attend

a 4-year college (Kenney-Fine).