A Brief History of Macro - Central European University

21

A Brief History of Macro IstvÆn Knya MNB and CEU September 2008 IstvÆn Knya A Brief History of Macro

Transcript of A Brief History of Macro - Central European University

A Brief History of Macro

István Kónya

MNB and CEU

September 2008

István Kónya A Brief History of Macro

The beginnings of macro

Macroeconomics did not exist as a separate �eld until the20th century

Before WWI, macro policy in most industrial countriesconcentrated only on the maintanance of the gold standardexchange rate system

The gold standard is an example of commodity money, whereone good (gold) is chosen to be the numeraireThis is di¤erent from the current systems, where the centralbank issues �at (paper) moneyExchange rates were �xed to gold, and hence to each otherPrices were just as likely to go up as down, there was nogeneral problem of in�ation

The rigidity and arbitrariness of the money supply led toswings in real economic activity

Limited franchise allowed policymakers to discount publicopinion

István Kónya A Brief History of Macro

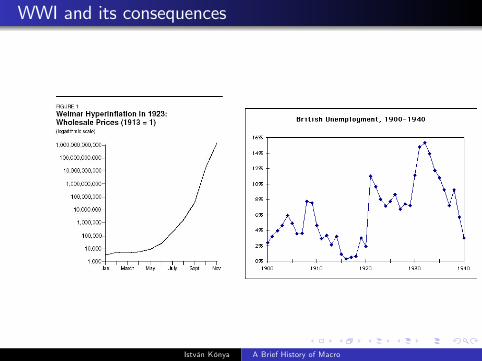

War, in�ation and stabilization

Financing WWI was eventually done by monetizinggovernment debt (printing money) and suspendingconvertability

In continental Europe, this led to hyperin�ation during theaftermath of the war

Most industrial countries eventually re-entered the goldstandard as part of their stabilization e¤ortThe British pound, the central currency of the pre-WWI goldstandard, depreciated against the USD during the war (Britaindid not su¤er hyperin�ation)

For reasons of perceived credibility and perhaps some vanity,Britain chose to restore the pre-war parity

A good laboratory for the short-run non-neutrality of money

István Kónya A Brief History of Macro

WWI and its consequences

István Kónya A Brief History of Macro

The Great Depression

The Great Depression convinced economists that theself-correcting mechanisms, in particular the �exibility ofwages and the price level, need not work fast enough

Keynes developed a coherent system (a general equilibriummodel) to examine the e¤ect of rigid wages and prices on theinterdependent markets for labor, goods and money

He showed that in the absence of price adjustment, �scalpolicy can help an economy when output is below potentialMonetary policy can also help by increasing the moneysupply, altough Keynes was sceptical about its practical use

István Kónya A Brief History of Macro

The Great Depression and its aftermath

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

1600.0

1800.0

2000.0

1929 1930 1931 1932 1933 1934 1935 1936 1937 1938 1939 1940 1941 1942 1943 1944 1945

Real GDP

István Kónya A Brief History of Macro

The Keynesian "Revolution"

Keynesian thinking dominated macro until the 1960�s, bothbecause of its appeal to activist policymakers and economists,and also because of its apparent success

Hicks developed the IS-LM model, a mathematical version ofKeynes�thinking which is still widely used in undergraduateeducation and (less fortunately) in policy discussions.

For 20-30 years, most macro was about measuring the gapbetween demand and potential output and stimulatingdemand su¢ ciently to reach potential.

István Kónya A Brief History of Macro

The "Golden Age"

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

4000.0

4500.0

5000.0

1948

1949

1950

1951

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

Real GDP

István Kónya A Brief History of Macro

Neoclassical Synthesis

Growing prominence of optimization theory and marginalanalysis in microeconomics led to incorporation intomacroeconomic models.

Optimal models of saving, investment and demand forliquidity were used to describe a medium term equilibriumaround which the economy would �uctuate in the short-run.

During the 1950�s, macro conceptually split changes in outputinto two parts:

Long-term growth: models in which prices adjust perfectly toeconomic conditions.Business cycles: models in which they would not.Large empirical models were constructed and estimated, basedon advances in econometrics.

István Kónya A Brief History of Macro

Trend growth and business cycle

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

4000.0

4500.0

5000.0

1948

1949

1950

1951

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

Real GDPLinear (Real GDP)

István Kónya A Brief History of Macro

Monetarism

In 1960�s, monetarists led by Milton Friedman began toemphasize the role of the money supply (as opposed to realdemand factors) as determinants of �uctuations in output andespecially in�ation.

In particular, Friedman pointed out the way that demandstimulus, once it becomes expected may lose its e¤ectiveness.

The Phillips curve debate

Based on statistical observations, many Keynesian economistsconcluded that there is an exploitable trade-o¤ betweenin�ation and unemploymentFriedman, Phelps and others argued that because in�ationexpectations adjust, the trade-o¤ cannot hold in the long run

István Kónya A Brief History of Macro

Stag�ation

2000.0

2500.0

3000.0

3500.0

4000.0

4500.0

5000.0

5500.0

6000.0

6500.0

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

Rea

l GD

P

0

2

4

6

8

10

12

14

16

18

Infla

tion

István Kónya A Brief History of Macro

The turbulent 70s

During the 1970�s, oil price shocks led to a period of rapidprice rises and low growth, called stag�ation.In many countries, in�ationary expectations led to wage-pricespirals and historically high in�ation rates.

This con�rmed the importance of expectations and theinstability of the Phillips curve

Developed economies begin 20 year slowdown in productivitygrowth rates.

In the early 1970�s, the US abandons the Bretton Woodssystem of �xed exchange rates, and exchange rates start to�oat.

After a few years of relative stability, exchange rates becomeone of the most volatile variables.Many new challenges emerge for international economics

István Kónya A Brief History of Macro

Rational expectations

Lucas develops economic theories which rigorously incorporatethe formation of expectations of future in economic models.

Calls for building models with explicit microfoundations,based on dynamic optimization by economic agents(households, �rms and possibly governments) in a stochasticenvironmentThe Lucas Critique states that empirical regularities that arenot derived from optimizing behavior are not invariant topolicy changes

Rational expectations models became widely accepted:They incorporate expectations in a way that is entirelyconsistent with rationality and optimizing behavior (i.e.microeconomics)They provided explanations for the rise of in�ationary spiralsand the seeming ine¤ectiveness of monetary policy.They provided the intellectual background for central bankindependence, pointing out time inconsistency problems

István Kónya A Brief History of Macro

Real Business Cycles

Early versions of microfounded rational expectations modelabandoned the Keynesian assumptions completely, andassumed that prices adjust �exibly and instantenously

The most in�uential work in this direction is the RealBusiness Cycle school

Showed that a large part of observed �uctuations may be dueto the e¢ cient response of economies to random disturbancesin production opportunities (productivity shocks)

The most important contribution of the RBC literature ismethodological: today most macroeconomic models are builton RBC foundations, and are subjected to rigorousquantitative evaluation

István Kónya A Brief History of Macro

The Volcker disin�ation

0.0

1000.0

2000.0

3000.0

4000.0

5000.0

6000.0

7000.0

1978 1979 1980 1981 1982 1983 1984 1985 1986

Rea

l GD

P

0

2

4

6

8

10

12

14

16

18

Infla

tion

István Kónya A Brief History of Macro

New Keynesians

RBC models cannot explain why monetary policy has a strongand lasting impact on economic activity

Using micro models of monopoly, a number of economistsdevelop rigorous models in which prices are sticky because ofadjustment costs.

Unlike RBC models, these models can explain why monetarypolicy has signi�cant e¤ects on output.

These models are typically static and cannot explain dynamicsor long-run at all.

István Kónya A Brief History of Macro

The Great Moderation

0.0

2000.0

4000.0

6000.0

8000.0

10000.0

12000.0

14000.0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Rea

l GD

P

0

1

2

3

4

5

6

Infla

tion

István Kónya A Brief History of Macro

The New Neoclassical Synthesis

Economists begin to incorporate New Keynesian models ofprice stickiness into uni�ed RBC framework.

These models explain which type of policies can o¤set e¤ectsof price-stickiness which might lead to underemploymentwithout leading to wage-price spirals.

Central banks have been relying extensively on insightsprovided by the insights of this literature.

The results of this e¤ort are the development and increasinguse of estimated DSGE (Dynamic Stochastic GeneralEquilibrium) models.

István Kónya A Brief History of Macro

What about growth?

Economists generally acknowledge that explaining sustainedgrowth is the "real thing"

There were two important waves of progress in growth theory

Late 50s to early 60s: the development of the neoclassicalmodel of "exogenous growth"Late 80s to early 90s: the development of "endogenousgrowth" models

No big dramatic events as in business cycle macro, but manyopen questions

Role of institutions, policy, openness, missing and incompletemarkets ...

István Kónya A Brief History of Macro

The end of the business cycle?

István Kónya A Brief History of Macro