5Ed CCH Forensic Investigative Accounting Ch03

36

Forensic and Investigative Forensic and Investigative Accounting Accounting Chapter 3 Fraudulent Financial Reporting © 2011 CCH. All Rights © 2011 CCH. All Rights Reserved. Reserved. 4025 W. Peterson Ave. 4025 W. Peterson Ave. Chicago, IL 60646-6085 Chicago, IL 60646-6085 1 800 248 3248 1 800 248 3248 www.CCHGroup.com www.CCHGroup.com

-

Upload

alysha-liloprah-pruitt -

Category

Documents

-

view

30 -

download

7

description

5Ed CCH Forensic Investigative Accounting Ch03

Transcript of 5Ed CCH Forensic Investigative Accounting Ch03

Forensic and Investigative AccountingForensic and Investigative Accounting

Chapter 3

Fraudulent Financial Reporting

© 2011 CCH. All Rights © 2011 CCH. All Rights Reserved.Reserved.

4025 W. Peterson Ave.4025 W. Peterson Ave.

Chicago, IL 60646-6085Chicago, IL 60646-6085

1 800 248 32481 800 248 3248

www.CCHGroup.comwww.CCHGroup.com

Chapter 3 Forensic and Investigative Accounting 2

An International ProblemAn International Problem

Fraud Fraud is an international phenomenon touching all countries. Transparency International (TI) is a global network including more than 90 locally established national chapters and chapters-in-formation, whose goal is to fight corruption in the national arena. TI produces a Transparency International Corruption Perception Index (CPI), which ranks more than 150 countries by their perceived levels of corruption, as determined by expert assessments and opinion surveys.

Chapter 3 Forensic and Investigative Accounting 3

Michael Comer’s Types of FraudMichael Comer’s Types of Fraud1.1. Corruptions (e.g., kickbacks).Corruptions (e.g., kickbacks).

2.2. Conflicts of interest (e.g., drug/alcohol abuse, part-time Conflicts of interest (e.g., drug/alcohol abuse, part-time work).work).

3.3. Theft of assets.Theft of assets.

4.4. False reporting or falsifying performance (e.g., false False reporting or falsifying performance (e.g., false accounts, manipulating financial results).accounts, manipulating financial results).

5.5. Technological abuse (e.g., computer related fraud, Technological abuse (e.g., computer related fraud, unauthorized Internet browsing).unauthorized Internet browsing).

Comer’s Rule: Fraud can happen to anyone at anytime.Comer’s Rule: Fraud can happen to anyone at anytime.

Source: M.J. Comer, Source: M.J. Comer, Investigating Corporate FraudInvestigating Corporate Fraud, Burlington, Vt.: Gower Publishing Co., , Burlington, Vt.: Gower Publishing Co., 2003, pp. 4-5.2003, pp. 4-5.

Chapter 3 Forensic and Investigative Accounting 4

The Cost of FraudThe Cost of Fraud Organizations lose Organizations lose 5 percent5 percent of annual revenue of annual revenue

to fraud and abuse.to fraud and abuse. Fraud and abuse costs organizations more than Fraud and abuse costs organizations more than

$2.9* $2.9* trilliontrillion annually. annually.

* $994 billion in 2008 in U.S. * $994 billion in 2008 in U.S. $652 billion in 2006. $660 $652 billion in 2006. $660 billion in 2004.billion in 2004.

Source: 2010 Wells Report

Chapter 3 Forensic and Investigative Accounting 5

Advantage of Compliance SpendingAdvantage of Compliance Spending

General Counsel Roundtable says that General Counsel Roundtable says that each each $1$1 of compliance spending of compliance spending savessaves organizations, on the average, organizations, on the average, $5.21$5.21 in in heightened avoidance of legal liabilities, harm heightened avoidance of legal liabilities, harm to the organization’s reputation, and lost to the organization’s reputation, and lost productivity.productivity.

Source: Jonny Frank, “Fraud Risk Assessments,” Source: Jonny Frank, “Fraud Risk Assessments,” Internal AuditorInternal Auditor, April 2004, p. 47., April 2004, p. 47.

Chapter 3 Forensic and Investigative Accounting 6

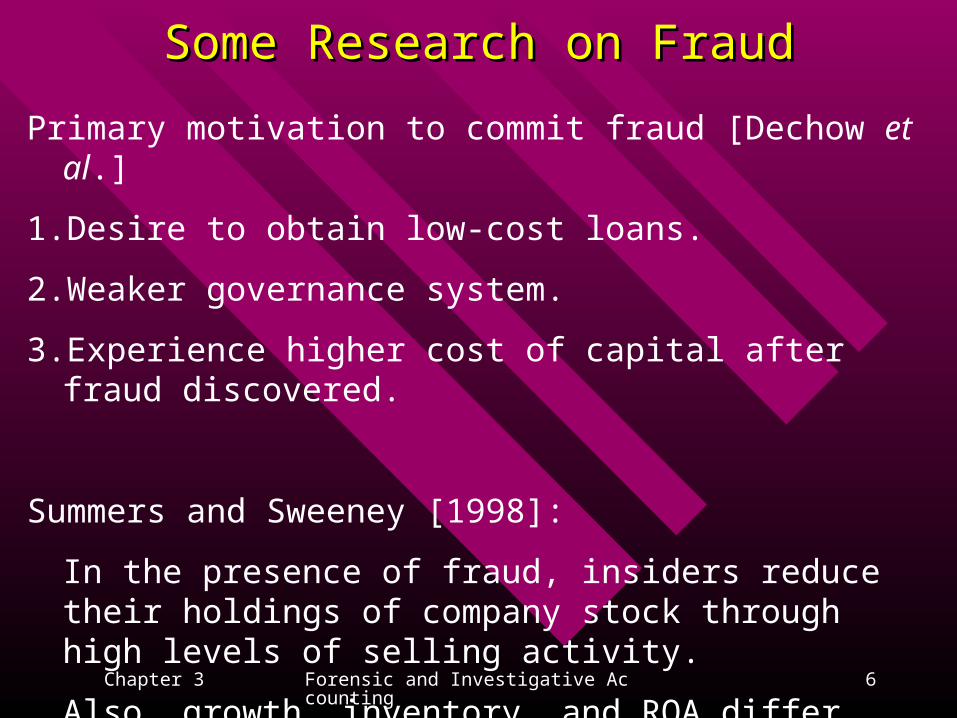

Some Research on FraudSome Research on Fraud

Primary motivation to commit fraud [Dechow et al.]

1. Desire to obtain low-cost loans.

2. Weaker governance system.

3. Experience higher cost of capital after fraud discovered.

Summers and Sweeney [1998]:

In the presence of fraud, insiders reduce their holdings of company stock through high levels of selling activity.

Also, growth, inventory, and ROA differ significantly.

Chapter 3 Forensic and Investigative Accounting 7

The Methods - FrequencyThe Methods - Frequency Asset misappropriation accounted for more than four Asset misappropriation accounted for more than four

out of five offenses or 90% in 2010 (88.7% in 2008) out of five offenses or 90% in 2010 (88.7% in 2008) ((91.5% in 200691.5% in 2006) (92.7% in 2004).) (92.7% in 2004). $135,000$135,000

Bribery and corruption constituted about 30% (27.4% Bribery and corruption constituted about 30% (27.4% in 2008) (in 2008) (30.8% in 2006) 30.8% in 2006) (30.1% in 2004) of (30.1% in 2004) of offenses. $250,000 ($375,000) ($538,000)offenses. $250,000 ($375,000) ($538,000)

Fraudulent statements were the smallest category of Fraudulent statements were the smallest category of offense 5% (10.3% in 2008) (offense 5% (10.3% in 2008) (10.6% in 2006)10.6% in 2006) (7.9% (7.9% in 2004) (in 2004) (most costlymost costly). $4 million per scheme.). $4 million per scheme.

Source: 2010 Global Fraud Study, ACFE.Source: 2010 Global Fraud Study, ACFE.

Chapter 3 Forensic and Investigative Accounting 8

Tra

ns

pa

ren

cy

Inte

rnatio

na

l Co

rrup

tion

P

erce

ptio

ns

Ind

ex

20

10

Chapter 3 Forensic and Investigative Accounting 9

One Small ClueOne Small Clue

A former Scotland Yard scientist tried to create the world’s A former Scotland Yard scientist tried to create the world’s biggest fraud by authenticating biggest fraud by authenticating $2.5 $2.5 trilliontrillion worth of fake worth of fake U.S. Treasury bonds.U.S. Treasury bonds.

When two men tried to pass off $25 million worth of the When two men tried to pass off $25 million worth of the bonds in Toronto in 2001, a Mountie noticed the bonds bore bonds in Toronto in 2001, a Mountie noticed the bonds bore the word the word “dollar”“dollar” rather rather “dollars.”“dollars.”

Police later raided a London bank vault and discovered that Police later raided a London bank vault and discovered that the bonds had been printed with an ink jet printer that had not the bonds had been printed with an ink jet printer that had not been invented when the bonds were allegedly produced.been invented when the bonds were allegedly produced.

Zip codes were used even though they were not introduced Zip codes were used even though they were not introduced until 1963.until 1963.Sue Clough, “Bungling Scientist Is Jailed for Plotting World's Biggest Fraud,” Sue Clough, “Bungling Scientist Is Jailed for Plotting World's Biggest Fraud,” News.telegraph.co.uk, January 11, 2003.News.telegraph.co.uk, January 11, 2003.

Chapter 3 Forensic and Investigative Accounting 10

Catch Me If You CanCatch Me If You Can

Numbers Don’t Lie.

Criminals are another story.

Money talks. But more often it whispers. When shady characters are up to no good, they often leave a trail of questionable financial transactions.

Chapter 3 Forensic and Investigative Accounting 11

Three M’s of Financial Reporting FraudThree M’s of Financial Reporting Fraud ManipulationManipulation, falsification, or alteration of , falsification, or alteration of

accounting records or supporting documents accounting records or supporting documents from which financial statements are prepared.from which financial statements are prepared.

MisrepresentationMisrepresentation in or intentional omission in or intentional omission from the financial statements of events, from the financial statements of events, transactions, or other significant information.transactions, or other significant information.

Intentional Intentional misapplicationmisapplication of accounting of accounting principles relating to amounts, classification, principles relating to amounts, classification, manner of presentation, or disclosure.manner of presentation, or disclosure.

Source: D.S. Hilzenrath, “Forensic Auditors Find What Some Companies Try to Hide,” The Washington Post, November 23, 2002, p.19.

Chapter 3 Forensic and Investigative Accounting 12

Fraud Schemes Based on Fraud Schemes Based on SEC ReleasesSEC Releases

1.1. Fictitious and/or overstated revenues and Fictitious and/or overstated revenues and assets.assets.

2.2. Fictitious reductions of expenses and liabilities.Fictitious reductions of expenses and liabilities.

3.3. Premature revenue recognition.Premature revenue recognition.

4.4. Misclassified revenues and assets.Misclassified revenues and assets.

5.5. Overvalued assets or undervalued expenses and Overvalued assets or undervalued expenses and liabilities.liabilities.

(continued on next slide)(continued on next slide)

Chapter 3 Forensic and Investigative Accounting 13

Fraud Schemes Based on Fraud Schemes Based on SEC ReleasesSEC Releases

6.6. Omitted liabilities.Omitted liabilities.

7.7. Omitted or improper disclosures.Omitted or improper disclosures.

8.8. Equity fraud.Equity fraud.

9.9. Related-party transactions.Related-party transactions.

10.10. Alter ego.Alter ego.

11.11. Minimizing income or inflating expenses to Minimizing income or inflating expenses to reduce tax liabilities.reduce tax liabilities.

Chapter 3 Forensic and Investigative Accounting 14

Shenanigans to Boost EarningsShenanigans to Boost Earnings

Recording revenue before it is earned.Recording revenue before it is earned. Creating fictitious revenue.Creating fictitious revenue. Boosting profits with nonrecurring Boosting profits with nonrecurring

transactions.transactions. Shifting current expenses to a later period.Shifting current expenses to a later period. Failing to record or disclose liabilities.Failing to record or disclose liabilities. Shifting current income to a later period.Shifting current income to a later period. Shifting future expenses to an earlier period.Shifting future expenses to an earlier period.

Chapter 3 Forensic and Investigative Accounting 15

RationalizationRationalization

Sherron Watkins provides an excellent Sherron Watkins provides an excellent comment about comment about rationalizationrationalization with respect to with respect to Enron’s Jeff Skilling and Andy Fastow. Enron’s Jeff Skilling and Andy Fastow.

At what point did they turn crooked? “But At what point did they turn crooked? “But there is not a defining point where they became there is not a defining point where they became corrupt. It was one small step after another, with corrupt. It was one small step after another, with more and more rationalizations. There was a more and more rationalizations. There was a slow erosion of values over timeslow erosion of values over time.”.”

Source: Source: Pamela Colloff, “The Whistle-Blower,” Pamela Colloff, “The Whistle-Blower,” Texas MonthlyTexas Monthly, , April 2003, p. 141.April 2003, p. 141.

Chapter 3 Forensic and Investigative Accounting 16

ReframingReframing

Behavioral psychologists call this rationalization Behavioral psychologists call this rationalization “reframing,” where someone who is about to cheat will “reframing,” where someone who is about to cheat will adjust the definition of cheating to exclude his or her adjust the definition of cheating to exclude his or her actions. Dan Ariely says “people who would never take $5 actions. Dan Ariely says “people who would never take $5 from petty cash have no problem paying for a drink for a from petty cash have no problem paying for a drink for a stranger and putting it on a company tab.”stranger and putting it on a company tab.”

Source: Source: S.L. Mintz, “The Gauge of Innocence,” S.L. Mintz, “The Gauge of Innocence,” CFOCFO, April 2009, p. 56., April 2009, p. 56.

Chapter 3 Forensic and Investigative Accounting 17

Internal vs. External FraudInternal vs. External Fraud

InternalInternal ExternalExternal

EmployeeEmployee ManagementManagement

Stock theftStock theft LappingLapping Check forgeryCheck forgery

Misappropriation Misappropriation of cash assetsof cash assets

Expense accountsExpense accounts False insurance False insurance claimsclaims

LappingLapping False financial False financial statementsstatements

Credit card fraudCredit card fraud

Check forgeryCheck forgery Misappropriation Misappropriation of cash/assetsof cash/assets

False invoicesFalse invoices

Expense accountsExpense accounts Unnecessary Unnecessary purchasespurchases

Product Product substitutionsubstitution

Chapter 3 Forensic and Investigative Accounting 18

Internal vs. External Fraud (contd.)Internal vs. External Fraud (contd.)

InternalInternal ExternalExternal

EmployeeEmployee ManagementManagement

Petty cashPetty cash Check forgeryCheck forgery Bribes/secret Bribes/secret commissioncommission

KickbacksKickbacks KickbacksKickbacks Bid rigging/price Bid rigging/price fixingfixing

Loans/Loans/

investmentsinvestments

Ghost vendorsGhost vendors False representation False representation of fundsof funds

Ghost Ghost employeesemployees

Diversion of salesDiversion of sales

Source: KPMG, Fraud Awareness Survey, Dublin: KPMG, 1995, pp. 10-12.

Chapter 3 Forensic and Investigative Accounting 19

Four Factors Contributing to Four Factors Contributing to Business FraudBusiness Fraud

1.1. MotiveMotive2.2. OpportunityOpportunity3.3. Lack of integrity (or rationalization)Lack of integrity (or rationalization)4.4. Capacity—the person must have the Capacity—the person must have the

necessary traits, abilities, or positional necessary traits, abilities, or positional authority to commit the crimeauthority to commit the crime

Source: Wolfe and Hermanson, “The Fraud Diamond,” Source: Wolfe and Hermanson, “The Fraud Diamond,” The CPA J.,The CPA J., December 2004, pp. 38-42. December 2004, pp. 38-42.

Chapter 3 Forensic and Investigative Accounting 20

Components of Internal ControlsComponents of Internal Controls

Control environmentControl environment Risk assessmentRisk assessment Control activities or control proceduresControl activities or control procedures Information and communication systems Information and communication systems

supportsupport MonitoringMonitoring

Source: SAS No. 94, The Effect of Information Technology on the Auditor’s Consideration of Internal Control in a Financial Statement Audit, New York: AICPA.

Chapter 3 Forensic and Investigative Accounting 21

Types of ControlsTypes of Controls

Preventive ControlsPreventive Controls

Segregation of duties Required approvals Securing assets Passwords Using document control numbers Drug testing Job rotation Computer backup

Chapter 3 Forensic and Investigative Accounting 22

Types of ControlsTypes of Controls

Detective ControlsDetective Controls

Reconciliations Reviews Event notifications Surprise cash count Counting inventory

Chapter 3 Forensic and Investigative Accounting 23

Types of ControlsTypes of Controls

Corrective ControlsCorrective Controls

Training Process redesign Additional technology Quality circle teams Budget variance reports

Chapter 3 Forensic and Investigative Accounting 24

Earnings ManagementEarnings Management

Earnings management may be defined as the Earnings management may be defined as the “purposeful intervention in the external “purposeful intervention in the external financial reporting process, with the intent of financial reporting process, with the intent of obtaining some private gain.”obtaining some private gain.”

– – Katherine Schipper, “Commentary on Earnings Management,” Accounting Horizon, Katherine Schipper, “Commentary on Earnings Management,” Accounting Horizon, December 1989, p. 92.December 1989, p. 92.

Chapter 3 Forensic and Investigative Accounting 25

Richard Davis says there is no psychometric way to Richard Davis says there is no psychometric way to measure integrity, so forget about personality tests measure integrity, so forget about personality tests to pick the fraudsters. They are easily faked. to pick the fraudsters. They are easily faked.

He is more hopeful about new methods involving He is more hopeful about new methods involving microexpressions, or those brief facial expressions microexpressions, or those brief facial expressions that may reveal a person’s predisposition to fraud.that may reveal a person’s predisposition to fraud.

Source: Source: S.L. Mintz, “The Gauge of Innocence,” S.L. Mintz, “The Gauge of Innocence,” CFOCFO, April 2009, p. 57., April 2009, p. 57.

Difficult to Measure IntegrityDifficult to Measure Integrity

Chapter 3 Forensic and Investigative Accounting 26

Fraud can be explained by three factors:Fraud can be explained by three factors:• Supply of motivated offenders.Supply of motivated offenders.

• Availability of suitable targets.Availability of suitable targets.

• Absence of capable guardians (e.g., internal controls).Absence of capable guardians (e.g., internal controls).

The three B’s -- babes, booze, and bets.The three B’s -- babes, booze, and bets.

Some fraudsters wish to make fools of their victims. They Some fraudsters wish to make fools of their victims. They take delight in the act itself.take delight in the act itself.

Risk of fraud is a product of both personality and Risk of fraud is a product of both personality and environmental (or situational) variables.environmental (or situational) variables.

Grace Duffield and Peter Grabosky, “The Psychology of Fraud,” Australian Institute of Criminology, Grace Duffield and Peter Grabosky, “The Psychology of Fraud,” Australian Institute of Criminology, No. 19.No. 19.

Psychology of FraudPsychology of Fraud

Chapter 3 Forensic and Investigative Accounting 27

Parallel Universe: Two OpinionsParallel Universe: Two OpinionsExternal auditors must do a External auditors must do a regularregular auditaudit of a of a

company (e.g., financial statements are fairly stated) and must company (e.g., financial statements are fairly stated) and must alsoalso audit the internal controlsaudit the internal controls to ensure that the financial to ensure that the financial statements are accurate (e.g., issue two opinions).statements are accurate (e.g., issue two opinions).

Prior to the external auditors’ arrival, the company Prior to the external auditors’ arrival, the company itself itself must reviewmust review its internal controls and its internal controls and issue a reportissue a report on on the effectiveness of these controls.the effectiveness of these controls.

There will be There will be two external opinionstwo external opinions: on : on management’s assessment of the internal controls over management’s assessment of the internal controls over financial reporting and another one on the effectiveness of the financial reporting and another one on the effectiveness of the internal controls themselves (e.g., statements are fairly internal controls themselves (e.g., statements are fairly stated).stated).PCAOB Release 2004-001.PCAOB Release 2004-001.

Chapter 3 Forensic and Investigative Accounting 28

Anti-Fraud ProgramAnti-Fraud Program

An auditor must perform “company-wide anti-fraud An auditor must perform “company-wide anti-fraud programs and controls and work related to other programs and controls and work related to other controls that have a pervasive effect on the company, controls that have a pervasive effect on the company, such as general controls over the company’s electronic such as general controls over the company’s electronic data processing.” data processing.”

Further, the auditor must “obtain directly the ‘Further, the auditor must “obtain directly the ‘principal principal evidenceevidence’ about the effectiveness of internal controls.”’ about the effectiveness of internal controls.”

PCAOB endorses the COSO Cube.PCAOB endorses the COSO Cube.

Source: PCAOB Release 2004-001.Source: PCAOB Release 2004-001.

Chapter 3 Forensic and Investigative Accounting 29

Source: 2008 Wells Report, ACFE.

Chapter 3 Forensic and Investigative Accounting 30

Fraud’s Fatal FailingsFraud’s Fatal Failings

85%85% of fraud victims of fraud victims never getnever get their money their money or property back.or property back.

Most investigations flounder, leaving the Most investigations flounder, leaving the victims to defend for themselves against victims to defend for themselves against counter-attacks by hostile parties.counter-attacks by hostile parties.

30%30% of companies that fail do so because of of companies that fail do so because of fraudfraud..

Source: Michael J. Comer, Source: Michael J. Comer, Investigating Corporate FraudInvestigating Corporate Fraud, , Burlington, VT: Gower Publishing, 2003, p. 9.Burlington, VT: Gower Publishing, 2003, p. 9.

Chapter 3 Forensic and Investigative Accounting 31

COSO Study FindingsCOSO Study Findings Financial fraud affects companies of all sizes, with the Financial fraud affects companies of all sizes, with the

median company having assets and revenues just under $100 median company having assets and revenues just under $100 million.million.

The median fraud was $12.1 million. More than 30 of the The median fraud was $12.1 million. More than 30 of the fraud cases each involved misstatements/misappropriations fraud cases each involved misstatements/misappropriations of $500 million or more.of $500 million or more.

The SEC names the CEO and/or CFO for involvement in 89 The SEC names the CEO and/or CFO for involvement in 89 percent of the fraud cases. Within two years of the percent of the fraud cases. Within two years of the completion of the SEC investigation, about 20 percent of the completion of the SEC investigation, about 20 percent of the CEOs/CFOs had been indicted. Over 60 percent of those CEOs/CFOs had been indicted. Over 60 percent of those indicted were convicted.indicted were convicted.

Motivations include meeting expectations, concealing Motivations include meeting expectations, concealing deteriorating financial conditions, and preparing for deteriorating financial conditions, and preparing for debt/equity offerings.debt/equity offerings.

Chapter 3 Forensic and Investigative Accounting 32

COSO Study FindingsCOSO Study Findings Revenue frauds accounted for over 60 percent of the cases. Revenue frauds accounted for over 60 percent of the cases.

Overstated assets, 51%. Understatement of expenses/ Overstated assets, 51%. Understatement of expenses/ liabilities (31%). Misappropriation of assets, 14%.liabilities (31%). Misappropriation of assets, 14%.

Many of the commonly observed board of director and audit Many of the commonly observed board of director and audit committee characteristics such as size, meeting frequency, committee characteristics such as size, meeting frequency, composition, and experience do not differ meaningfully composition, and experience do not differ meaningfully between fraud and no-fraud companies. Recent corporate between fraud and no-fraud companies. Recent corporate governance regulatory efforts appear to have reduced governance regulatory efforts appear to have reduced variation in observable board-related governance variation in observable board-related governance characteristics.characteristics.

Twenty-six percent of the firms engaged in fraud changed Twenty-six percent of the firms engaged in fraud changed auditors during the period examined compared to a 12 auditors during the period examined compared to a 12 percent rate for no-fraud firms.percent rate for no-fraud firms.

Chapter 3 Forensic and Investigative Accounting 33

COSO Study FindingsCOSO Study Findings Initial news in the press of an alleged fraud resulted in an Initial news in the press of an alleged fraud resulted in an

average 16.7 percent abnormal stock price decline for the average 16.7 percent abnormal stock price decline for the fraud company in the two days surrounding the fraud company in the two days surrounding the announcement. announcement.

News of an SEC or Department of Justice investigation News of an SEC or Department of Justice investigation resulted in an average 7.3 percent abnormal stock price resulted in an average 7.3 percent abnormal stock price decline.decline.

Companies engaged in fraud often experienced bankruptcy, Companies engaged in fraud often experienced bankruptcy, delisting from a stock exchange, or material asset sales at delisting from a stock exchange, or material asset sales at rates much higher than those experienced by no-fraud firms. rates much higher than those experienced by no-fraud firms.

50% of the stock traded on NASDAQ over a variety of 50% of the stock traded on NASDAQ over a variety of industries.industries.

Chapter 3 Forensic and Investigative Accounting 34

COSO Study FindingsCOSO Study Findings 20% of the fraud companies were in the computer 20% of the fraud companies were in the computer

hardware/software industry and 20% were in financial hardware/software industry and 20% were in financial service providers. 11% were in health care and health service providers. 11% were in health care and health products. products.

45% of the Section 404 opinions indicated effective controls 45% of the Section 404 opinions indicated effective controls and 45% indicated ineffective controls.and 45% indicated ineffective controls.

Source:Source: COSO News Release, Alamonte Springs, May 20, 2010, COSO News Release, Alamonte Springs, May 20, 2010, www.coso.org/documents.www.coso.org/documents.

Chapter 3 Forensic and Investigative Accounting 35

Fraud PentagonFraud Pentagon

Source: P.D. Goldman, Fraud in the Markets (John Wiley & Sons: 2010), pp. 24-25.

Chapter 3 Forensic and Investigative Accounting 36

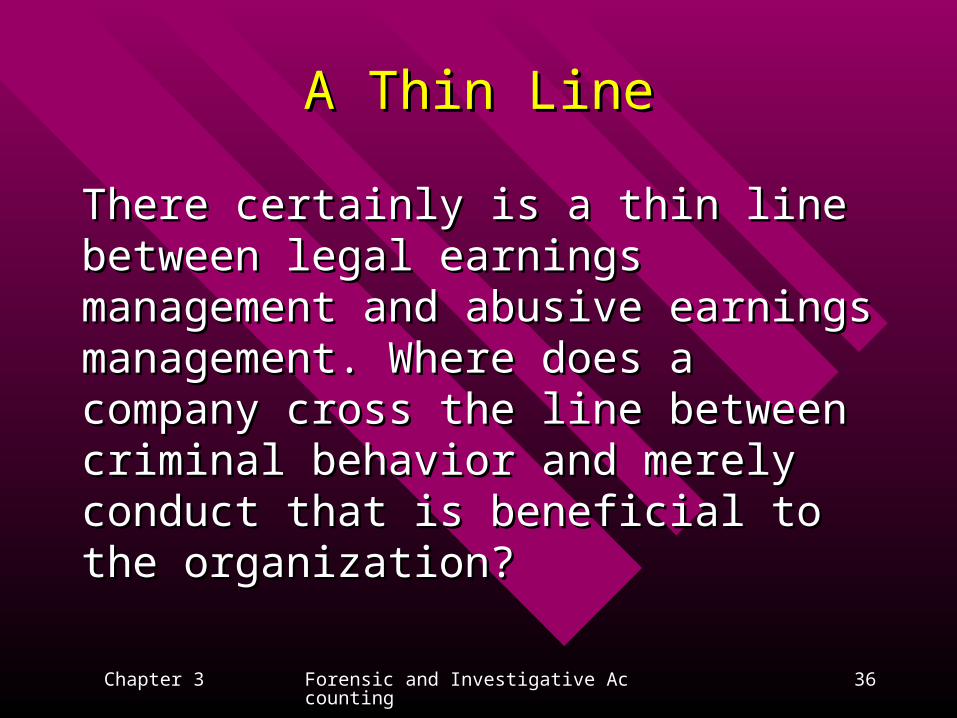

A Thin LineA Thin Line

There certainly is a thin line between legal There certainly is a thin line between legal earnings management and abusive earnings earnings management and abusive earnings management. Where does a company cross management. Where does a company cross the line between criminal behavior and merely the line between criminal behavior and merely conduct that is beneficial to the organization? conduct that is beneficial to the organization?