5-Special Financing Models for Energy Management...

56

Energy Finance Glenn Barnes Environmental Finance Center University of North Carolina at Chapel Hill 919-962-2789 [email protected]

Transcript of 5-Special Financing Models for Energy Management...

Energy Finance

Glenn BarnesEnvironmental Finance CenterUniversity of North Carolina at Chapel [email protected]

www.efcnetwork.org

Smart Management for Small Water Systems

www.efcnetwork.org

www.efcnetwork.org

Session Objectives

• To discuss ways you might pay for energy management projects at your water system / organization, focusing on energy-specific financing models.

www.efcnetwork.org

Ways to Pay

• Pay as you go (current receipts)

• Save in advance and pay (fund balance, capital reserve fund)

• Pay later (someone loans you money)

• Grants (let someone else pay)

www.efcnetwork.org

The Best Way to Pay? It Depends

• Pay as you go

• Fund balance

• Pay later

• Grants

} Best for small energy improvements

Best for large energy improvements

www.efcnetwork.org

What is an Energy Upgrade?

• An energy upgrade to water or wastewater system is really just a capital improvement

• You can treat energy upgrades just like any other capital improvement

www.efcnetwork.org

Where Capital Funding Comes From

• Rates / Monthly bills• Special assessments to current customers• Impact fees to new customers• Debt Market, including State Revolving

Funds• Grants• Or any way that your system gets revenue

www.efcnetwork.org

What is an Energy Upgrade?

• An energy upgrade to a water or wastewater system is also a specialcapital improvement

• As a result, there are special financing options available for energy upgrades

www.efcnetwork.org

Special Financing Models for Energy Management

1. Internal revolving energy funds (“virtuous cycle”)

2. Performance Contracting (ESCOs)3. PPA: Power Purchase Agreements4. QECB’s: Qualified Energy Conservation

Bonds

www.efcnetwork.org

Internal Revolving Energy Funds

www.efcnetwork.org

Funding a Plan: Energy Revolving Funds

• Capitalized as a “bank” from which departments and divisions can borrow to fund energy efficiency, renewable energy or energy conservation projects.

• Allows systems to provide a continual stream of funds for energy efficiency improvements without tapping into existing capital cycles.

www.efcnetwork.orgSource: Ann Arbor Energy Fund

www.efcnetwork.org

• Based on audits of facilities or other pre-determined criteria

• Energy efficiency tied to other capital improvements

• “Spreading the wealth”

Choosing Projects

www.efcnetwork.org

• Issues to consider– It may depend on your systelm’s internal policies

and/or how your energy bills are paid– A clear, consistent policy is key for the long-term

success of the revolving fund

• Ways for the money to be handled– Within your finance office– Each department repays the fund– The budget includes a certain amount of money

to be re-appropriated into the fund each year

How the Money Is Handled

www.efcnetwork.org

• Actual Savings

• Estimated Savings (Defined repayment schedule)

• Upfront Agreements

• Determining Loan Terms

Repayment Methods

www.efcnetwork.org

• From a finance and management perspective, the issue is how to determine repayments into the fund– Actual savings– Estimated savings

• If repayments are tied to actual savings (note: actual energy savings ≠ actual dollar savings), you need a pre-determined M&V system

• If repayments are on a fixed schedule based on estimated savings, M&V is not relevant for repayments

M&V of Projects

www.efcnetwork.org

Establishment: Seed money• Appropriating funds

• Maintaining an expired budget line item

• Capitalizing on existing energy savings and other cost reductions

• Cost reductions from competitive bidding

• Private foundations and grants

• Bonds

www.efcnetwork.org

Fund maintenance• Avoided costs and

+ Interest from borrowers

+ Appropriated funds

+ Renewable energy credits/Green tags

+ Energy sales

www.efcnetwork.org

Chapel Hill’s Energy Bank• Established: 2006

• Seed money amount: $500,000

• Seed money source: Bond

• Fund maintenance: 100% of energy savings

www.efcnetwork.org

Revolving Energy Funds

• Have any of you already set up an internal revolving energy fund at your system?

www.efcnetwork.org

Performance Contracting

www.efcnetwork.org

What is Performance Contracting• An ESCO proposes and designs a

package of energy cost reduction measures, installs or implements those cost reduction measures, and guarantees the savings of the cost reductions.

• The ESCO may put up all of the capital for the energy projects.

This and next several slides courtesy of Len Hoey, N.C. State Energy Office.

www.efcnetwork.org

What is Performance Contracting• The ESCO pays itself back for the

package over time using the stream of revenue provided by the energy reduction measures.

• Third party verifies ESCO reconciliation report.

This and next several slides courtesy of Len Hoey, N.C. State Energy Office.

www.efcnetwork.org

Why not do it yourself?

• Often opportunities to reduce energy costs are well known but owners are unable to take advantage of them

• Capital

• Expertise

• Manpower

• Can you guarantee the savings?

www.efcnetwork.org

Performance Contracting Advantages

• A process with a single point of responsibility (rather than multiple contractors for various projects).

• Provides you with the ESCO’s capital.• Provides you with the engineering and

project management expertise of the ESCO.• Guaranteed performance / savings.

www.efcnetwork.org

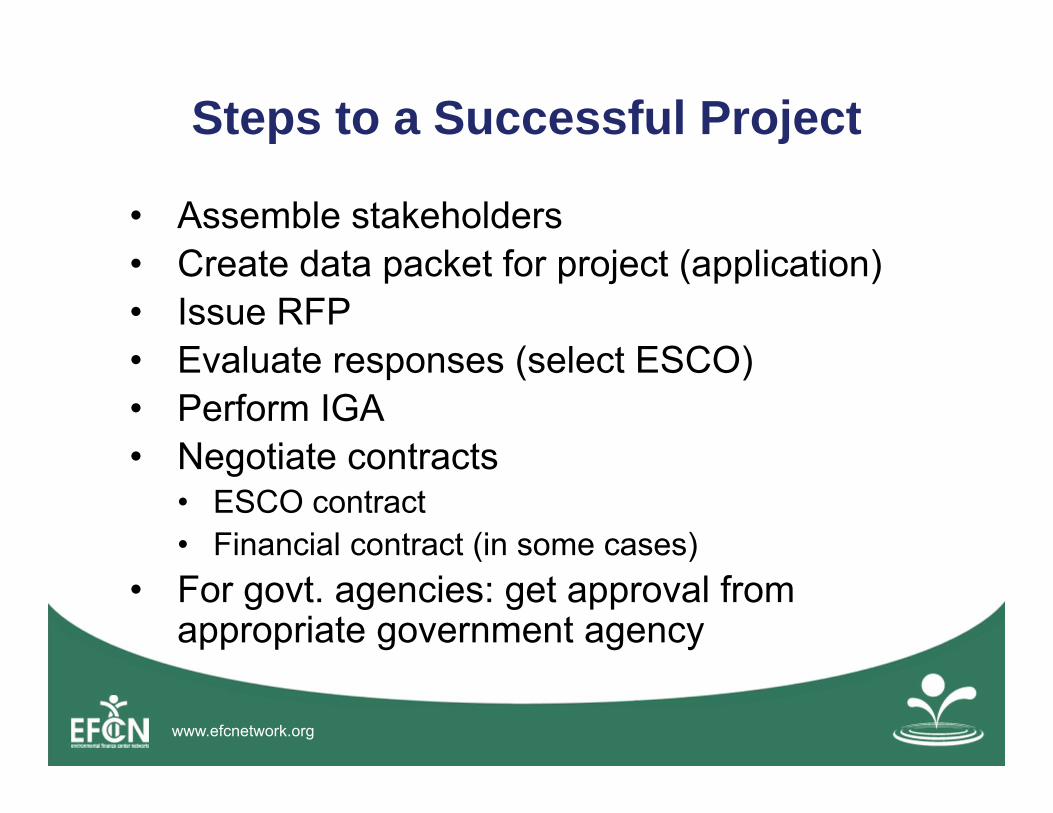

Steps to a Successful Project

• Assemble stakeholders• Create data packet for project (application)• Issue RFP• Evaluate responses (select ESCO)• Perform IGA• Negotiate contracts

• ESCO contract• Financial contract (in some cases)

• For govt. agencies: get approval from appropriate government agency

www.efcnetwork.org

Measurement & Verification

• Actual savings measured are compared to guaranteed savings by third party.

• If actual savings less than guaranteed savings, ESCO pays the difference to the governmental unit.

• The cost of the required third party M&V review is to be included in the contract.

www.efcnetwork.org

ESPC ConceptQuick Payback Long Payback

Cost Savings Cost Savings

Energy Conservation Measures

• Lighting retrofits

• EMS

Major Building Improvements

• HVAC Upgrades

• Pumps

•Solar thermal/PV

Comprehensive Facility Improvement Project

www.efcnetwork.org

Funding

Before Improvements After Improvements

Annual Operating Budget

Utility Costs(Gas, Electric, Water)

MaintenanceCosts

MaintenanceCosts

Utility CostsSavingsRepayImprovements

Savings generated fund the project!

www.efcnetwork.org

Savi

ngs

Debt Service

Cash Flow to Owner/Savings

Before Performance Contract

During Performance Contract

After Performance Contract

$Pr

ojec

t Im

plem

enta

tion

Operations Budget

or

Utility Bill

Debt Service

Cash FlowM&V Costs

Gua

rant

eed

Savi

ngs

Operations Budget

or

Utility Bill

Operations Budget

or

Utility Bill

PC Funding – Your Utility’s Budget

www.efcnetwork.org

Discussion

• Have any of you already done an energy management performance contract?

• If so, what was your experience like? For how many years was the contract term?

• Would you use this process again?• If you have not done so before, are you

interested in trying a performance contract?

www.efcnetwork.org

Power Purchase Agreement

www.efcnetwork.org

Power Purchase Agreement• A company such as FLS Energy, Inc., finances

some of, or all of, a renewable energy project. You may not have to put up any capital at all.

• For example, Hawaii PPA contract for large solar hot water project (1,400 homes). FLS has also done Camp Lejeune marine base.

• Sell electricity under long term sales contract – possibly lock in much lower electric rates than today.

www.efcnetwork.org

PPAs and Tax Equity• If a company from the mainland comes to

contract a PPA with you, they can still qualify for the 30% federal investment tax credit for renewable energy.

• This may allow them to put up 100% of the necessary capital. And you may get much lower electric rates.

www.efcnetwork.org

PPA Example

• Going back to the case of Hawaii and FLS Energy, base electric price is about 28-29 cents per kWh.

• Selling BTU thermal equivalent of hot water in kWh terms may reduce this rate sharply (e.g. down to 20 cents per kWh), saving significant money across the long term (e.g. 10-15 years).

www.efcnetwork.org

www.efcnetwork.org

Pros of a PPP May Include:- An additional funding source- Private partner can take advantage of tax credits- Private entities have access to different dollars- Cost-savings derived from management,

technical, operational, or other efficiency of the private partner

- Reduce public partner’s role from day-to-day operational management to contract management, to allocate scarce staff or other limited public resources

www.efcnetwork.org

PPP Example

www.efcnetwork.org

Qualified Energy Conservation Bonds

www.efcnetwork.org

Bonds

• In general, a bond is a written promise to repay borrowed money

• On a definite schedule and usually at a fixed rate of interest for the life of the bond

www.efcnetwork.org

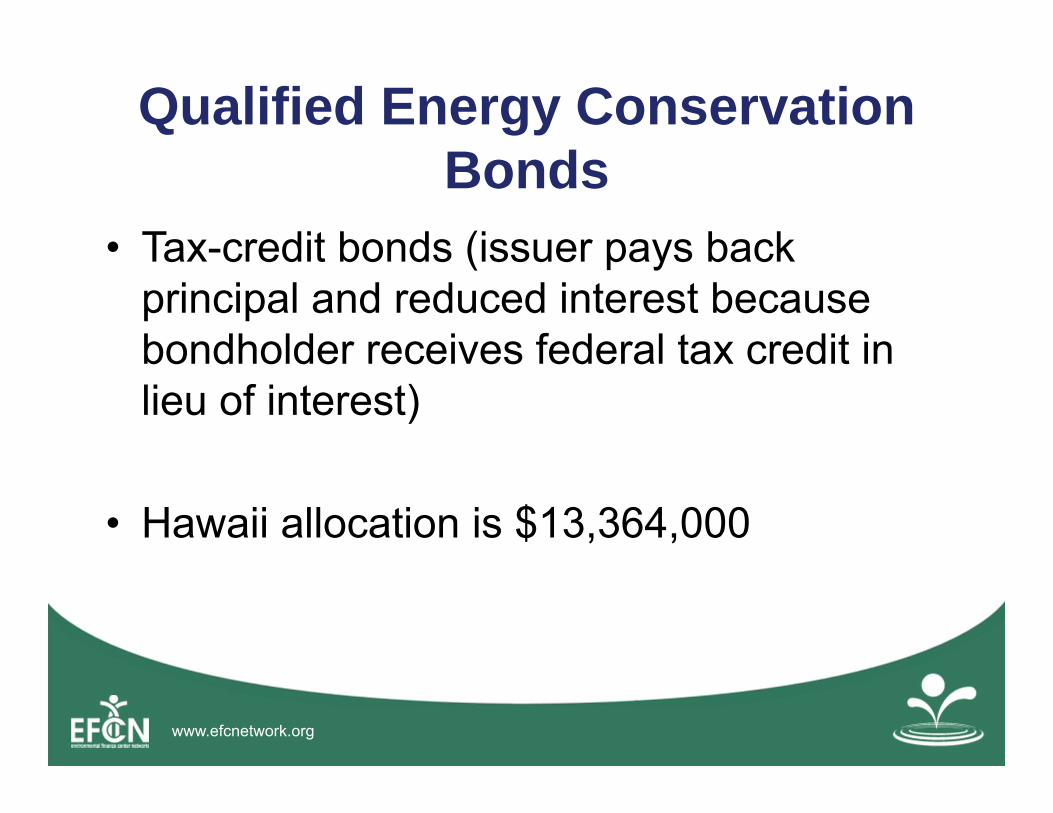

Qualified Energy Conservation Bonds

• Tax-credit bonds (issuer pays back principal and reduced interest because bondholder receives federal tax credit in lieu of interest)

• Hawaii allocation is $13,364,000

www.efcnetwork.org

Qualified Energy Conservation Bonds

• 1%-5% effective interest rate for issuer

– Issuer gets 3%-4% subsidy from Treasury

– 15 to 20-year term

• Qualified projects are broadly defined, including 20 percent reduction of energy use in public facilities

www.efcnetwork.org

• https://www.treasurydirect.gov/GA-SL/SLGS/selectQTCDate.htm

Qualified Tax Credit Rate

www.efcnetwork.org

• Capital expenditures incurred for purposes of--(i) reducing energy consumption in

publicly-owned buildings by at least 20 percent,(ii) implementing green community

programs (including the use of loans, grants, or other repayment mechanisms to implement such programs),

(iii) rural development involving the production of electricity from renewable energy resources

Qualified Projects

Source: 26 USC § 54D

www.efcnetwork.org

• IRS is the ultimate judge of whether or not an issuance is a “qualified project”

• As of yet, IRS is not pre-approving projects

• IRS can audit any QECB issuance for the term of the bond plus three years. Surviving this audit is the only way IRS will indicate if a project is a “qualified project”

• New important guidance, IRS Notice 2012-44:http://www.irs.gov/pub/irs-drop/n-12-44.pdf

Who decides what constitutes a “qualified project?”

www.efcnetwork.org

• The term “publicly-owned buildings” under §54D(f)(1)(A)(i) means a building or buildings that are owned by a State or local government

• For purposes of the 20 percent test, the issuer may measure the reduction in energy consumption using one of the following measurement units: (i) a single publicly-owned building, (ii) multiple publicly-owned buildings; (iii) one or more building system components of one or more publicly-owned buildings, or (iv) a combination of (i) or (ii) and (iii) above

20 Percent Test

Source: IRS Notice 2012‐44

www.efcnetwork.org

• A reasonable and consistently applied method must be used to measure energy savings attributable to capital expenditures with respect to a measurement unit for purposes of the 20 percent test

• For purposes of the 20 percent test, the issuer may consider actual and expected energy consumption in the measurement unit during any reasonable and consistent time periods of not less than one year (the measurement time periods), with one such period ending immediately before, and one such period beginning immediately after...

20 Percent Test

Source: IRS Notice 2012‐44

www.efcnetwork.org

• The purpose of a green community program is to promote one or more of the purposes of energy conservation, energy efficiency, or environmental conservation initiatives relating to energy consumption, broadly construed

• A green community program must: (i) involve property that is available for general public use... or (ii) involve a loan (or other repayment mechanism) or grant program that is broadly available to members of the general public, including individuals or businesses

Green Community Programs

Source: IRS Notice 2012‐44

www.efcnetwork.org

• No more than 30 percent of a Large Local Government’s allocation

• Large Local Government must act as the conduit issuer of the bonds

• In the case of any private activity bond, the term “qualified conservation purposes” shall not include any expenditure that is not a capital expenditure– Source: IRS Notice 2009-29

Private Activity

www.efcnetwork.org

Colorado School of the Mines

• This was a performance contract paid with QECB proceeds (at ~1 percent interest)

• Audit done of energy and water use on the campus

www.efcnetwork.org

Colorado School of the Mines

• Phase I included:– Campus irrigation controls retrofit– Domestic water conservation– HVAC exhaust energy

recovery– Partial campus

lighting retrofit

www.efcnetwork.org

• Deerfield, IL has a population of 18,225 and an MHI of about $107,000

• Issued an 18-year QECB bond of $12.5 million with an effective interest rate of 1.12% (AAA bond rating)– General Obligation bond—no voter approval required

in IL• Funded equipment replacement that is expected

to realize a 21-22 percent energy savings• Part of a larger bond issuance

Wastewater Treatment in Deerfield, IL

www.efcnetwork.org

Smart Management for Small Water Systems

www.efcnetwork.org

A Few More Thoughts on Debt

www.efcnetwork.org

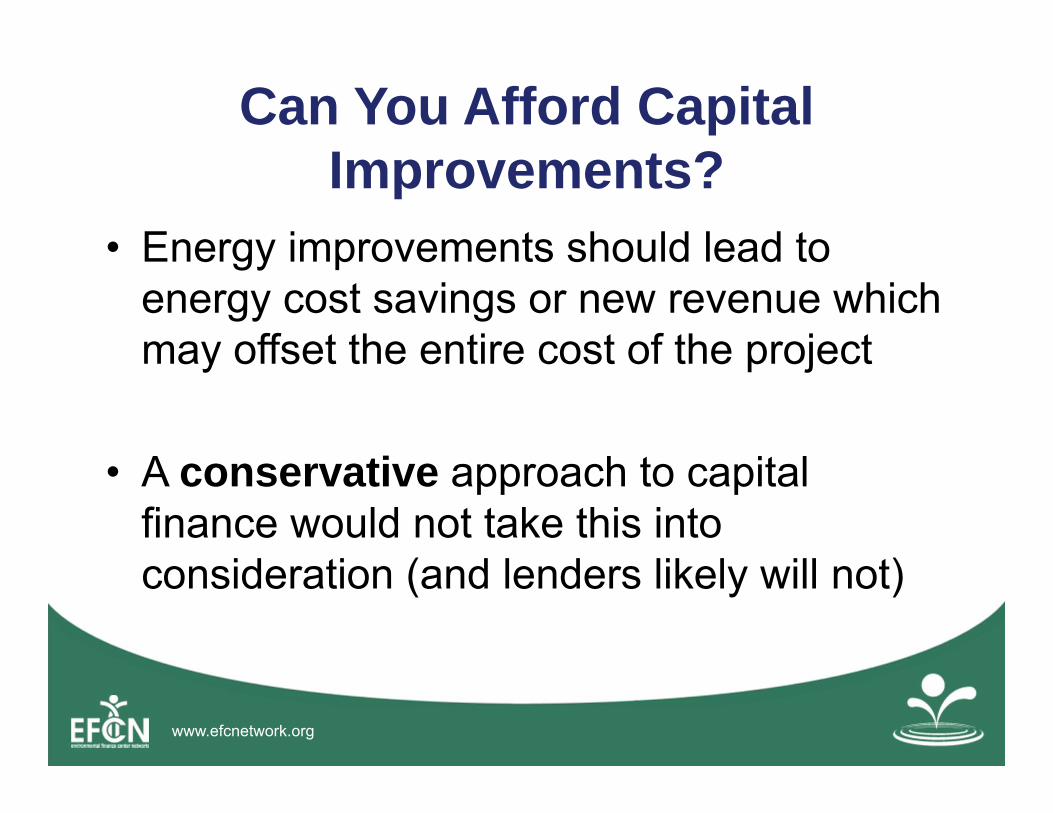

Can You Afford Capital Improvements?

• Energy improvements should lead to energy cost savings or new revenue which may offset the entire cost of the project

• A conservative approach to capital finance would not take this into consideration (and lenders likely will not)

www.efcnetwork.org

The Lender View

• Lenders generally are not swayed by the potential energy cost savings of projects (though the guarantees of performance contracts help)

• Instead, lenders look at the credit worthiness of the system/business as a whole

www.efcnetwork.org

Take Away• It is tempting to think only about energy

improvements paying for themselves

• It is better to think about energy improvements as an investment in your system or business to reduce future operating expenses– Savings can then be applied to future capital

projects, mitigating rate increases, etc.