3.2.1. Innovative financing for renewable energy ... · Innovative financing for renewable energy...

59

25 3.2.1. Innovative financing for renewable energy development 3.2.1.1. Overall summary Background and objectives Energy demand and consumption have increased alongside economic development in the Asia- Pacific region, resulting in a large gap between demand and supply. The total APEC final energy consumption is projected to increase to 5,948 Mtoe (million tonnes of oil equivalent) in 2020, from 3,760 Mtoe in 1999. This represents a rise of 58.2 percent or an annual growth rate of 2.2 percent 1 . Within the current technological paradigm, this will have major environmental implications, especially in relation to climate change and global warming, unless new and sustainable sources of energy are developed. In addition, there are an estimated 2 billion people lacking access to modern energy services world-wide, of which 1.2 billion live in Asia. For many of the non-electrified rural areas, decentralised energy systems have proved more financially viable than connection to the grid. Developing new and sustainable sources of energy provide an opportunity to meet the future growth in energy consumption, provide electricity to those who presently lack it while at the same time preventing further environmental degradation. Renewable energy sources present a huge potential for contributing to the provision of clean energy, but also raise a range of challenges related to technology, resource availability and high investment and capital costs. Meeting the challenge of large scale commercialisation of renewable energy (RE) products and services will require 1) mitigating the initial high costs of RE systems; 2) improving competitiveness against traditional fossil fuels including the removal or redirection of subsidies; 3) ensuring access to affordable consumer financing; 4) enhancing access to credit for the RE industry; and 5) ensuring sustainability without public aid and subsidy. This research has explored innovative modes of delivery in four areas of financing likely to be the primary sources for financing the development and commercialisation of RE in the mid-long term period: government finance, international funding mechanisms (including clean climate initiatives), private sector finance (including financing through energy service companies), and micro-credit and community-based financing. Research activities in FY 2003 In line with the research framework designed in the first year of the project, activities in the second year consisted of: Collection of good practices in new technologies Further field studies were conducted and innovative practices in the financing of renewable energy were collected grouped into the four categories of financing. While the technology covered during the first year was limited to grid-connected wind power applications and decentralised solar power applications, activities in the second year were expanded so as to collect innovative practices in the areas of grid-connected biomass, integrated water heating systems and landfill gas. Finalisation of the framework for strategic policy options The framework for strategic policy options was further developed and discussed at research team meetings (see section on SPO for details). 1 Asia-Pacific Energy Research Centre (2002) APEC Energy Demand and Supply Outlook 2002, Asia-Pacific Energy Research Centre, Institute of Energy Economics, Tokyo: Japan. Available at: http://www.ieej.or.jp/aperc/pdf/APEC- EDSO2002.pdf

Transcript of 3.2.1. Innovative financing for renewable energy ... · Innovative financing for renewable energy...

25

3.2.1. Innovative financing for renewable energy development 3.2.1.1. Overall summary Background and objectives

Energy demand and consumption have increased alongside economic development in the Asia-Pacific region, resulting in a large gap between demand and supply. The total APEC final energy consumption is projected to increase to 5,948 Mtoe (million tonnes of oil equivalent) in 2020, from 3,760 Mtoe in 1999. This represents a rise of 58.2 percent or an annual growth rate of 2.2 percent1. Within the current technological paradigm, this will have major environmental implications, especially in relation to climate change and global warming, unless new and sustainable sources of energy are developed. In addition, there are an estimated 2 billion people lacking access to modern energy services world-wide, of which 1.2 billion live in Asia. For many of the non-electrified rural areas, decentralised energy systems have proved more financially viable than connection to the grid. Developing new and sustainable sources of energy provide an opportunity to meet the future growth in energy consumption, provide electricity to those who presently lack it while at the same time preventing further environmental degradation. Renewable energy sources present a huge potential for contributing to the provision of clean energy, but also raise a range of challenges related to technology, resource availability and high investment and capital costs.

Meeting the challenge of large scale commercialisation of renewable energy (RE) products and

services will require 1) mitigating the initial high costs of RE systems; 2) improving competitiveness against traditional fossil fuels including the removal or redirection of subsidies; 3) ensuring access to affordable consumer financing; 4) enhancing access to credit for the RE industry; and 5) ensuring sustainability without public aid and subsidy. This research has explored innovative modes of delivery in four areas of financing likely to be the primary sources for financing the development and commercialisation of RE in the mid-long term period: government finance, international funding mechanisms (including clean climate initiatives), private sector finance (including financing through energy service companies), and micro-credit and community-based financing. Research activities in FY 2003

In line with the research framework designed in the first year of the project, activities in the second year consisted of: Collection of good practices in new technologies

Further field studies were conducted and innovative practices in the financing of renewable energy were collected grouped into the four categories of financing. While the technology covered during the first year was limited to grid-connected wind power applications and decentralised solar power applications, activities in the second year were expanded so as to collect innovative practices in the areas of grid-connected biomass, integrated water heating systems and landfill gas.

Finalisation of the framework for strategic policy options

The framework for strategic policy options was further developed and discussed at research team meetings (see section on SPO for details).

1 Asia-Pacific Energy Research Centre (2002) APEC Energy Demand and Supply Outlook 2002, Asia-Pacific Energy Research Centre, Institute of Energy Economics, Tokyo: Japan. Available at: http://www.ieej.or.jp/aperc/pdf/APEC-EDSO2002.pdf

26

Research team meetings A mid-term research team meeting was held in New Delhi, India in July 2003, hosted by the

Energy and Resources Institute, and a further meeting was held in Bangkok in November 2003, in conjunction with the first RISPO plenary workshop. Finally, a research team meeting was held in February 2004 in Japan, in conjunction with the second RISPO Plenary Workshop. Publication of research findings and presentation at international conferences

On the basis of the research outputs of the first year, a number of activities were initiated in order to disseminate the research findings so far. This included writing and publishing a research note entitled “Financing Renewable Energy in India: A Review of Mechanisms in Wind and Solar Applications” in the International Review of Environmental Strategies by research team members from IGES and TERI. Another paper titled “Developments with Photovoltaic Research and Applications in India” was presented by research team members from India at the 14th International Photovoltaic Science and Engineering Conference in Bangkok, in January 2004.

Contribution to the policy-making process

Research team members from the Energy Research Institute, China prepared and made arrangements for the “European Union - China High Level Conference on Renewable Energy Policy and Project Financing”, held on April 6, 2004 in Beijing, China. Members also participated in development activities of the China wind power and small hydro program under the Clean Development Mechanism (CDM), as well as preparing the draft of the “Renewable Energy Promotion Law of the People’s Republic of China”. Good practices

Seventeen good practices have been collected from China and India, in collaboration with the Energy Research Institute of China and The Energy and Resources Institute of India. The practices cover various innovative financing mechanisms including: mechanisms that combine government

and community financing (India); development of a market-oriented institutional and financial model for decentralised solar systems (India); wind-power development through combination of the Clean Development Mechanism CDM and public sector financing (India); scaling-up of renewable village power through governmental finance and bidding based on market regulation (China); experience of the first CDM project in renewable energy financing in China (China); financing the utilisation of landfill gas through economic incentives (China); commercialisation of solar hot water systems through a ‘financial intermediary (FI) scheme’ (India); market development for solar lanterns in a post-subsidy regime (India); developing a sustainable financial

model for solar pumping systems (India). Economic instruments, awareness raising, partnerships, technologies, design, planning and management were among critical instruments in these successful practices.

Solar water pumping in Chandigarh, India Photo by Gueye Kamal, IGES

27

Strategic Policy Options

Based on the provisional framework developed in the first year, work continued towards finalising the SPO framework following the life-cycle approach. The results of the policy and literature review, and the collection and analysis of good practices indicate that there is a relation of interdependence between the deployment of RE products and technologies and their market demand with regard to financing. The availability of financing for research and development as well as for manufacturing is crucial for reducing the high costs of the systems. Similarly, adequate consumer finance enhances affordability and stimulates further demand, which in turn leads to further development of the RE industry. Given this inter-linkage between industry and market growth on the one hand and price reduction on the other, the challenge of financing is addressed under a life-cycle approach (LCA), which examines financing mechanisms during the stages of: 1) research and development; 2) demonstration; 3) early commercialisation; and 4) demand-driven commercialisation.

- Government finance - International funding

mechanisms - Private-sector finance - Micro-credit and community-

based finance

Early commercialisation

Demand-driven

Research and development

Demonstration

Figure 3-1. Life Cycle Approach

28

Framework

The framework and proposal of strategic policy options were developed to provide research-based answers to the following questions:

1. Which particular types of barriers are best addressed by governments, international financing mechanisms, private finance and micro-credit/community-based financing respectively?

2. Who can best address the financial requirements at each specific stage of the LCA? 3. To what extent is the role of the different financing instruments technology-specific (i.e.

does this vary between solar, wind, biomass etc.)? 4. What would be the optimal combination of financing sources for the respective

technologies? 5. How can policy options be replicated in other countries?

The following key principles were identified as driving forces behind sustainable financing

strategy: Financing should be an instrument that drives market development. Financing mechanisms should not be a one-time delivery initiative but should involve a

package of services for acquisition and maintenance of RE products. Financing should increasingly move away from subsidy-driven schemes and rely on private

finance and market-driven demand.

29

Table 3-1. Framework of Strategies and Strategic Policy Options Strategy Strategic Policy Options

(Source of finance) Financing Instruments (Modality of delivery)

R&D funds/development funds Optimal use of government funds Technology Commercialisation/incubation

funds

Incubation funds/venture capital

Joint venture and technology transfer

Attracting International development funding mechanisms Collaborative R&D

Increasing financing by public/private financing institutions

Risk capital and technology finance

SSuuppppoorrtt ffoorr tteecchhnnoollooggyy aanndd pprroodduucctt ddeevveellooppmmeenntt.. ((RReesseeaarrcchh,, DDeevveellooppmmeenntt aanndd DDeemmoonnssttrraattiioonn ssttaaggee))

Enhancing private sector financing

Corporate-funded R&D Combining subsidy with loans in the ownership model Competitive biding for minimum subsidy Redirecting subsidies away from fossil fuel based energy Environmental cost of fossil fuel projects

Greening of GDP

Optimum use of government funds

Increasing share of RE Refinancing: Two-step loans Buying down interest rate of commercial lending

Attracting international funding mechanisms Creating Special Purpose Vehicles for Clean

climate mechanisms (CDM, FCP, carbon trading)

Renewable portfolio lending Increasing financing by private/public financial institutions Market-based institutional finance

Micro-credit and self help group-based financing Carbon Cess, Preferential tariff, Concession tariff / Tariff rebate

Leveraging consumer financing

Community-based green funds

Development of energy service companies Fee for service model Vendor credits Leasing

IImmpprroovviinngg tthhee ccoommppeettiittiivveenneessss ooff rreenneewwaabbllee eenneerrggyy mmaarrkkeettss.. ((CCoommmmeerrcciiaalliissaattiioonn ssttaaggee))

Enhancing private sector financing

Renewable energy processing zones (concessions, tax holidays etc.)

30

Preliminary proposal

Research on the basis of the life cycle approach led to the identification of two key strategies that aim to 1) support technology and product deployment (at the research, development and demonstration stages) and 2) improve the competitiveness of RE markets (at the commercialisation stage). Based on these strategies, five strategic policy options have been developed. The indication from the policy options identified is that innovation was related more closely to innovative modes of delivery than to new sources and mechanisms of financing. Accordingly, the strategic policy options (SPO) place emphasis on modes of delivery (financing instruments) that involve new combinations of different sources of finance, optimising the aggregate effect in reducing the financing barrier. In other words, each SPO incorporates a combination of financing instruments. There are five SPOs presented in detail under the country sections: • Optimum use of government funds • International funding mechanisms • Increasing financing by private/public financial institutions • Leveraging consumer financing • Enhancing private sector financing Research plan in FY 2004 SPO development - Completion of country-specific SPO (August 2004) - Developing SPO applicable to Asian countries (September – December 2004) - Completion of SPO and draft final report (December 2004) - Review of draft final report (January 2005) - Finalisation of SPO and final report (February 2005) SPO review meetings - Review meeting, China (August 2004) - Review meeting, India (September 2004) Dissemination of research results - Renewable energy workshop, India (April 2004) - Renewable energy workshop, China (April 2004) - Policy paper on SPO (February 2005)

31

Research collaborators Energy Research Institute (ERI), China Ms. Hu Xiulian Ms. Jingli Shi Dr. Kejung Jiang The Energy and Resources Institute (TERI), India Ms. Akanksha Chaurey Mr.Yuvaraj Dinesh Babu Mr. Shirish Garud Institute for Global Environmental Strategies (IGES), Japan Dr. Gueye Kamal

32

3.2.1.2. Summary of research progress in selected countries A. China Summary of research progress in FY 2003 Literature, information and policy survey

A review was conducted of the various publications released by the government, research and financial institutions, public and private companies including renewable energy users and manufacturers; internet sites, international collaborative projects etc. Site visit, group discussion, expert meetings and telephone interviews

Wind energy site-visits were conducted in order to meet with the major wind manufacturers and user groups; expert meetings were organised with various representatives of financial institutions; and solar energy site-visits were conducted in order to interact with the supplier’s network of dealers and technicians, individual households, and rural banks. Research team meeting and electronic discussion

The first meeting of the research team on March 27-28, 2003 in Bangkok, Thailand, the second on July 22-23, 2003 in New Delhi, India, the third on November 22-23, 2003 in Bangkok, Thailand, and the fourth on February 10-12, 2004 in Japan, were held to review the research framework, identify financing mechanisms potentially innovative in the collection of good practices, and adopt the basic framework for Strategic Policy Options. Follow up activities were conducted through electronic discussions. Activities related to the project

Members of the team prepared and made arrangements for the “EU-China High Level Conference on Renewable Energy Policy and Project Financing”, held on April 6, 2004 in Beijing. Members also participated in development activities of the China wind power and small hydro CDM program, as well as drafting “the Renewable Energy Promotion Law of the People’s Republic of China (Draft version) Background information in China Renewable energy resources potentials in China

According to the initial assessment, China has great potential for renewable energy resources development, including wind power, hydro energy, solar and biomass. According to the estimates made by the China Academy of Meteorology, exploitable on-shore wind power is about 253 GW, and offshore wind power is 750 GW, totalling 1 TW. According to the results of re-investigation released from the latest hydro resources, exploitable small hydro resource is 125 GW, and 65% of this is located in the western region. According to this estimation, the amount of solar radiation received at the ground surface is about 170 billion tce each year in China. Solar energy is potentially highly valuable in most of areas of China. Driving force behind the development of renewable energy in China

20 thousand villages and more than 800 rural households, over 30 million rural people, as yet have no access to electric power in China, and 50% of domestic energy use still relies on non-commercial energy in China’s rural areas. This not only influences the quality of living in rural areas, but also has a great impact on the environment. Therefore, China urgently needs to improve its energy structure that is dominated by coal use, and increase energy efficiency and benefits. Environmental protection and GHGs emission mitigation will influence sustainable development in China. Commercialisation, industrialisation and market-oriented development of renewable energy will definitely provide an opportunity for China to create a new economic growth area.

33

Current status of renewable energy industry With advances in science and technology, China's renewable energy industry has witnessed

steady growth. In some technologies, most notably solar water heating, China has a well-established industry with decent sized export markets, and a number of other technologies are rapidly moving towards commercialisation. Chinese advances in renewable energy technologies include: – development of practical and commercialised units – basic design/manufacturing capacity for modern and large-scale units – establishment of national testing centres – training of technical personnel – new innovative technologies for development and application – continuous improvement of equipment performance, which is approaching international

standards for many technologies

34

Table 3-2 . Current status of China's renewable energy technologies Maturity and Development Phase Types of Technologies

R&D Demonstration Early-commercialisation

Demand-driven commercialisation

Solar water heater •

Passive solar house •

Solar stove •

Solar drier •

Solar cell •

Grid connected wind turbines •

Small and mini wind turbines •

Geothermal power generation •

Geothermal heating •

Traditional bioenergy technology •

Small methane tank •

Large-medium methane technology •

Municipal organic waste power generation •

Biomass gasification •

Other modern bioenergy technologies •

Wave power generation •

Tidal power generation •

Ocean thermal energy conservation •

New hydrogen manufacturing technology •

Hydrogen storage techniques •

Small hydropower •

35

China’s Current Policies on Renewable Energy National legislation, policies and programmes

The Government of China has made a substantial effort to develop renewable energy. The primary energy policies published by the central government are as follows (Policies, laws and regulations associated with renewable energy in China are detailed in Appendix A): (1) People's Republic of China (PRC) Law on Electricity

This was China's first energy-related law. The legislation states that the state encourages and supports renewable energy and clean energy based power generation; promotes the development of hydropower resources in rural areas, including construction of medium and small-sized hydropower stations; and encourages and supports rural power supply including solar, wind, geothermal and biomass energies. (2) Energy Conservation Law

The 1998 Law on Energy Conservation described the important strategic role and position of energy efficiency and renewable energy in bringing about emission reductions and environmental improvement. The legislation requires government at each level to enhance the rural energy supply, including the development and utilisation of biogas, solar energy, wind, hydro and geothermal energies. (3) Regulation on Grid-connected Wind Power Generation Management

Promulgated in 1994, the Regulation on Grid-connected Wind Power Generation Management is one of the most concrete regulations focusing on renewable energy. This document stipulates that wind power shall be allowed access to the nearby grid and that the network shall purchase all output. The wind power tariff shall be determined based on the cost (both principal and interest repayment) plus a reasonable profit. The incremental cost of wind power above the average electricity tariff should be shared by the whole grid. (4) Ninth Five-Year-Plan and 2010 Objectives for National Social and Economic Development

In the 9th five-year-plan for China's national economic and social development, the energy development strategy was defined as “centred around coal based electric power with enhanced survey and development of petroleum and natural gas resources” The policy also stressed the necessity of developing small hydro power, wind energy, solar energy, geothermal energy and biomass energy compatible with local conditions. (5) Notification on Further Support for Renewable Energy Development

In 1999, the former SDPC and Ministry of Science and Technology issued the Notification on Further Support for Renewable Energy Development. This document presents a series of concrete economic incentive policies for promoting renewable energy. (6) National programmes

The "Riding the Wind Program" was initiated by the former SDPC in 1996. The programme selected domestic WTG manufacturers through a bidding process, and formed joint venture enterprises with foreign companies for production. A joint venture company Xi'an NORDEX Wind Turbine Co. Ltd. was established with Xi'an Aero-Engine (XAE) and NORDEX of Germany, where manufacturing technology of 600kW WTG was imported. Another joint venture company Y1TUO-MADE (Luoyang) Wind Turbine Ct). Ltd. was established by China YITUO Group Co. Ltd. and MADE Technologies Renewable, S.A. Spain, where manufacturing technology of 660kW WTG was imported. Both companies have the capability of batch production and their products have been installed in wind farms, totalling more than 20.

The "National Debt Wind Power Program" of the former State Economy & Trade Commission

36

(SETC) has been in place since 1998. The program uses national debt with favourable condition of interest subsidy to build wind farms, and the planned total installed capacity will be 73MW. It is expected to accelerate the development of domestic wind power equipment manufacture. The China Classification Society (CCS) is preparing to establish a type certification scheme for locally manufactured WTGs, to implement tests and measurements according to international standards.

The "Brightness Program", sponsored by the former SDPC from 1996 onwards, aims to provide electricity to off-grid villages and households in the western part of China, 23 million people in total. The first phase of this program (projects in Inner-Mongolia, Gansu and Tibet) was completed in 2000. The Central Government intends to invest RMB 2 billion in the next few years to supply PV power to the off-grid villages in western China. The program will drive the PV market forward. (7) Strategic planning for renewable energy development in 2020

Part way through 2003, the National Development and Reform Commission (NDRC) initiated the formulation of Strategic planning for renewable energy development in 2020, to promote renewable energy technology development in China and keep up with world trends. The strategy is based on renewable energy resources and technology characteristics in China to meet the social and economic development requirement, and it draws on foreign experience and lessons learned. The strategy presents the objectives, layout and policy measures for renewable energy development in China in the next 20 years, guiding the path of development and construction of key projects in the renewable energy field. Economic incentives (1) Tax exception and reduction

Customs Tariff Relief. With the gradual opening of Chinese markets, customs duties for many imports have been reduced, and duties on renewable energy equipment are lower than the average. For example, customs duty is not applied to imported wind turbines. Ironically, this damages the overall objective of promoting local manufacturing considering wind turbine components are subject to a three-percent customs tax. This policy provides an incentive to import complete turbine units from abroad and not to use as much local equipment as possible. Since local equipment is cheaper, the overall effect is to raise the cost of wind generation equipment unnecessarily. (2) VAT reduction

Value Added Tax Relief. At present, most renewable energy products are taxed at the full value added tax (VAT) level. The two exceptions are the VAT on biogas at 13 percent (current standard VAT is 17%) and that on small hydropower generation at 6 percent. (3) Income tax reduction

Income Tax Relief. China’s income tax system has greatly improved in recent years. At present, the standard income tax paid by enterprises is 33 percent. Local authorities collect income tax from local enterprises, and some regions, such as Inner Mongolia and Xinjiang, have developed preferential policies to support the development of renewable energy. (4) Pricing

Discount price. Local authorities have various measures for pricing certain renewable energy applications. For example, Shanghai authorities have defined a higher price for biogas based cooking gas at Rmb 1.20 Yuan/m3 while other provinces such as Sichuan and Guandong have offered discount prices for the cement used in biogas tank construction.

37

(5) Discounted loan interest rate Discount loans. In 1987, the Chinese Government created discount loans specifically for rural

energy development. These loans support biogas projects, solar thermal applications and wind power generation technology. In 1996 the fund totalled Rmb 130 million. The government offered a 50 percent discount on regular commercial bank loan interest. In addition, the government has made a limited number of low interest loans available for small hydro projects.

In 1999, the State Council, SDPC, and the Ministry of Science and Technology issued the

Notification on Further Supporting the Development of Renewable Energy. The statement stressed that renewable power projects would enjoy priority in state bank loans. The National Development Bank is the lead institution providing such loans and encourages the involvement of other commercial banks. The SDPC assists the developer in acquiring bank loans for projects above 3MW. These types of loans are subject to an interest rate reduction of two percent below the commercial rate, a discount subsidised by the national or local government. (6) Subsidy

Subsidies. The central authorities’ subsidies for renewable energy are usually offered for research or development and there are also some local subsidies for solar energy and wind power. Subsidies paid to investors are used in China for investing in the construction of local small hydropower stations. Consumer subsidy is also a widely used incentive. In addition to its extensive application in extending solar energy equipment and mini wind generators, these subsidies are used widely for efficient firewood stoves and other biomass energy technologies. The objective is to spur on the expansion of production capacity and thus reach the goal of cost reduction.

As an example of local policy, the Shanghai municipal government allocated a financial appropriation of Rmb 10 million yuan for a fund dedicated to the promotion of biogas projects using a market mechanism based on demand growth. Some local authorities such as those in Liaoning and Dalian provided an Rmb 700 yuan subsidy for farmers using methane to heat greenhouses or nurseries. This is in addition to low interest loans of up to Rmb 2, 000 yuan for each system.

Research and development policy (1) Proving funds for renewable energy R&D

Funding from the central authorities for research, development and demonstration are made for the following purposes:

– Providing administrative expenses and research budgets for scientific research institutions.

– Supporting major scientific studies and related training: as shown by the incomplete statistics,

the total budget used in the 9th five-year-plan period for this purpose exceeded Rmb 100 million yuan.

– Offering project subsidies: in the early 1990s, for example, the central authorities invested Rmb 7 million in the construction 4 PV stations in Tibet as a demonstration project.

– Providing assistance in the planning process: for example, in 1996, the State Planning Commission, State Science and Technology Commission and State Economic Commission jointly published “Development Outlines for China's Energy and Renewable Energy Development in 1996-2010."

38

(2) Supporting renewable energy technology demonstration In line with the energy, environment and sustainable development strategy, the government of

China pays much attention to the development and demonstration of renewable energy technologies. For example, two demonstrations on solar cooling were completed in the state R&D Program for 9th Five-year-plan. – The Shangdong project

This integrated solar system was built in Rushan, Shangdong in 1999. It functions as a cooling, heating and hot water system for a gymnasium with a space of 1000m2. This system has 2160 pieces of heat-pipe evacuated tubular collector with a net absorber area of 364m2 and is equipped with a LiBr absorption chiller. Typically in summer the system provides 1777.4M J/day of refrigeration capacity with a COP of around 0.5, while in winter it supplies 2175.3MJ/day of heat. Beside the cooling and heating system, it supplies 32000 litres of hot water. – The Guangdong project

This integrated system was constructed in Jiangmen, Guangdong in 1996. It serves as a cooling system for one floor of a plaza (600m2) and heats 30 tons of hot water for the whole building. The system is equipped with 500 m2 of flat plate collectors and a 100kW LiBr absorption chiller with COP around 0.44. Priority areas for developing the renewable energy and development goal in China

Materials from the relevant government agencies and reports from research institutes have shown that the priority areas of renewable energy development in the coming 20 years will be renewable energy power generation, renewable energy gas supply, renewable energy heat supply, liquefied fuel from renewable energy and new energy technology (fuel cells and hydrogen energy).

The key areas for development of renewable energy power generation include small hydro power, wind power, solar power and biomass power. The total installation capacity of renewable energy power generation will reach about 600 TW in 2010, accounting for about 10% of the national total. Amongst these, small hydro will hold a share of 80%, wind power 7% and solar and biomass power 31% . In 2020, the total installation capacity of renewable energy power generation will reach about 1150 TW, about 12% of national total. Small hydro will hold a share of 65%, wind power 17% and solar and biomass power 18% .

Heating supplied by renewable energy (heating supplied by solar heaters and geothermal energy) will replace 22 Mtce (million tonnes of coal equivalent) energy by 2010, which will increase to 45 Mtce of renewable energy by 2020. Liquefied fuels made from renewable energy (bio-ethyl alcohol, bio-oil) will replace 11.43 Mtce or 8 Mtoe (million tonnes of oil equivalent) by 2020. Barriers and issues of renewable energy development in China

In general, renewable energy in China suffers from a lack of a well-articulated policy framework and an independent industry that can attract investment capital. Though there certainly is progress, most renewable technologies would benefit from a comprehensive set of policies, tailored to address the phase of development of the individual technology. There are numerous renewable energy technologies in different stages of development in China, and therefore there are various barriers and problems. The following is a summary of the barriers common to all technology fields, and Annex 2 gives a detailed analysis of wind power. – The role of renewable energy in the national energy development general strategy is weak,

showing a lack of long-term objectives, development planning and concrete implementation measures. The omission of renewable energy utilisation in national energy statistics effects energy policymaking.

39

– There are no supporting policies or incentive mechanisms formulated by the legislative requirements. The existing policies are not integrated, lacking power, stability and consistency.

– There are no effective supporting investment and financing mechanisms available. Many

renewable projects are funded by the government, and international assistance or large scale commercial development is not possible.

– There is lack of input in R&D and industrialisation. An integrated renewable technology

industry base and quality control system including standards and certifications have not yet been established. Technology and equipment still rely on imports.

– There is lack of resource surveys, assessments and management systems. Resource surveys fail

to provide detailed information for project planning and development, therefore increasing the investment risks.

– There is lack of a scientific, accurate and complete assessment system. As a result, the

environmental and social benefits of renewable energy are undocumented and renewable technologies are disadvantaged in market competition.

– Common barriers to the financing for renewable energy are: high up-front capital costs and low

affordability of renewable energy (RE) products and technologies by consumers; inadequate accessibility to credit by RE industry and consumers; and subsidies for fossil fuels that hinder the RE market development and reduce competitiveness

Paths to be taken to solve the problem of financial capital needed to develop renewable energy in China – Establish a fund guarantee system for renewable energy construction, involving the government,

social benefits organisations, renewable energy special capital and renewable energy development funds.

– The main solutions to solving the problem of gaining the financial capital needed for renewable

energy development are to combine: state guidance investment with social multi-channel investment; poverty shake-off with ecologic protection project, in which state investment plays the leading role; state investment with subsidiaries, such as those based on total investment, giving 5% financial support for small hydro power, and 1% financial support for wind power. The state should be responsible for investment in wind power resource exploration and assessment, project planning, and standards and regulations formulation. As for waste biomass utilisation project, the government should subsidise 3% of the total investment.

– Cultivate the space needed for renewable energy development. Before 2010, policies of

government bidding, MMS and law binding power purchase price should be adopted, and after 2010, a competitive renewable energy market should be developed gradually.

40

Good practices identified

In this research, the current focus in renewable energy technologies are solar and wind energy . According to the analysis of existing policies in China, the research group prepared a draft list of good practices, which was submitted for discussion at the working meeting held on July 22- 23, 2003 in New Delhi, India. Based on the results of this discussion, the research group determined a list of the first four good practices that have been conducted. These were:

Demonstration of a wind power concession policy to reduce the large-scale wind power price.

Location; Dongfeng Wind Farm, Jiangsu Province, China, and Huilai Wind Farm, Guangdong Province, China.

Establishment of a Renewable Energy Service Company (RESCOs) for the Renewable Village

Power System. Location; Bulunkou Xiang, Xinjiang Province, China.

Utilising Landfill Gas for Power Generation. Location; ShuiGe Landfill Site, Nanjing City, Jiangsu Province, China.

Solar Water Heater Integrated Building. Location; Qingdao, Shandong Province, China.

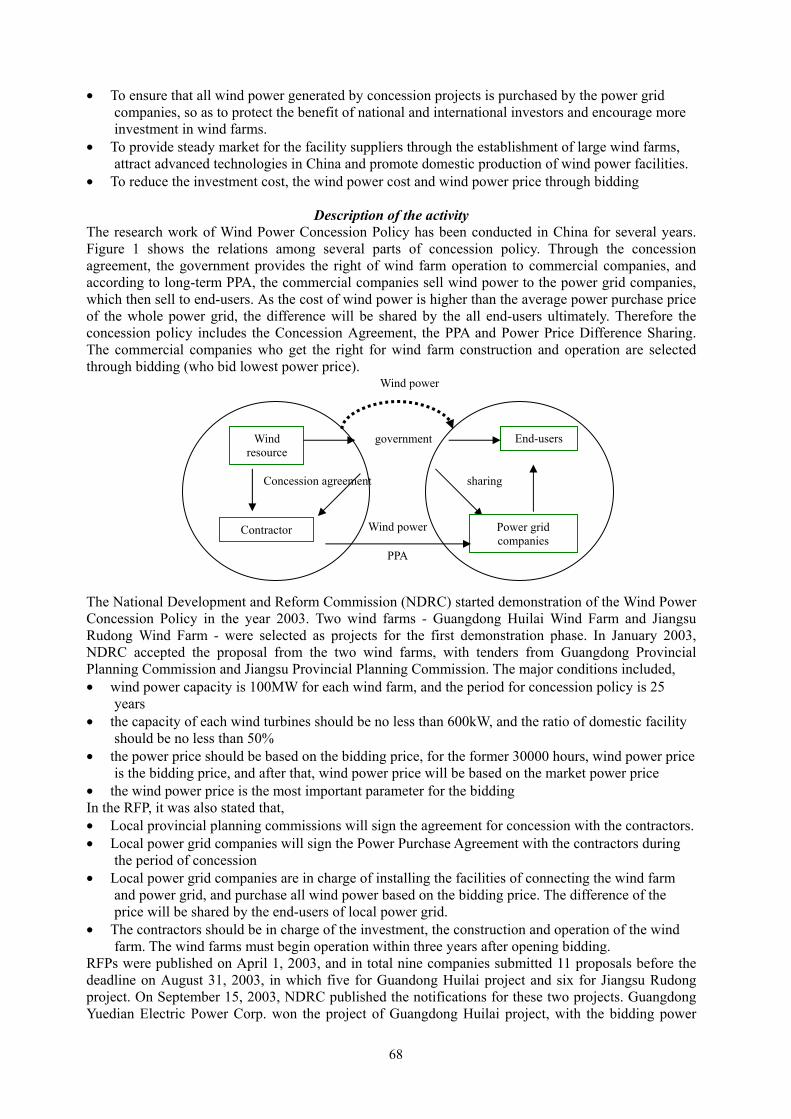

a. Demonstration of wind power concession policy to reduce the large-scale wind power price Location: Dongfeng Wind Farm, Jiangsu Province, China, and Huilai Wind Farm, Guangdong Province, China Background: Research into Wind Power Concession Policies has been conducted in China for several years. Chinese wind power has also developed rapidly in recent years, reaching 468MW by the end of 2002, which was three times that of 1997. At present, the major problems facing wind power in China are the Power Purchase Agreement and Wind Power Price. In order to stimulate the development of wind power, the National Development and Reform Commission initiated the Wind Power Concession Policy in 2003. Objective: The objectives of the demonstration of wind power concession are: (i) to provide guarantees to the wind farm developer when signing a long-term Power Purchase Agreement with the power-grid company; (ii) to reduce the wind power price through international bidding. Activity: The Energy Bureau of National Development and Reform Commission is in charge of the demonstration of the wind power concession policy. Two sites were selected in Jiangsu and Guangdong and international bidding was adopted. The first bidding was conducted by the Jiangsu Planning Commission and Guangdong Planning Commission. A total of 11 international and national wind farm developers were involved in the bidding. Ultimately, the Huarui Corp. won the Jiangsu Dongfeng project, and Guangdong Yuedian Electric Power Corp. won the Guangdong Huilai project. The results of the bidding were that,

The wind farm concession period is 25 years During these 25 years, the power-grid company must purchase all wind power from the wind

farms The power price of the first 30000 hours is determined by the bidding; for the Jiangsu project,

0.436yuan/kWh, for the Guangdong project, 0.51yuan/kWh

41

Impact: The price of wind power is greatly reduced through the wind concession policy and bidding. The wind power price of the former projects in Jiangsu and Guangdong was over 0.6yuan/kWh (some projects even reached 1yuan/kWh). Potential for application: These two projects comprised the first wind power concession policy demonstration. The National Development and reform Commission is planning for later groups of wind power projects. b. Establishing Renewable Energy Service Companies (RESCOs) for the Renewable Village Power System Location: Bulunkou Xiang, Xinjiang Province of China Background: The Renewable Village Power system is important in solving the residential power supply problem in remote areas. The UNDP/GEF Capacity Building project of rapid Development of Renewable Energy Commercialisation in China supported the establishment of several renewable village power systems for demonstration, including the Bulunkou project, located in Xinjiang province. Apart from providing financial support for investment in the renewable village power system, the UNDP project also supports the set up of RESCOs for the maintenance and operation of the village power system. Objective: To help establish RESCOs. Activity: The UNDP project provided US$600,000 for the initial investment in the Bulukou system. The systems comprised 5 sub-systems. The total installed capacity is 60kW of wind turbines, and 8kW PV and 120kVA diesel generators. The local government provided 1.6 million RMB yuan of investment. A RESCO was registered in the beginning of year 2003, and the company took charge of the system operations in March 2003. The price of power charged to farmers, government buildings and business buildings are 1yuan/kWh, 1.2yuan/kWh and 1.5yuan/kWh respectively. The money collected covers the operation costs at present, including salaries and small maintenance costs. But for maintenance work such as battery changing that necessitates a great deal of money, the income from power cost collection is not sufficient. Impact: This RESCO is the first true RESCO in China, and the company provides the service to keep the village power system in normal operation. Potential for application: In 2002-2003, the National Development and reform Commission implemented the Song-Dian-Dao-Xiang project, to equip 800 villages in remote areas with PV and PV hybrid village power system. But the difficulty of keeping these systems in normal operation in the next 10-15 years is a problem faced by the National Development and Reform Commission. RESCO will be the ideal choice. c. Utilising Landfill Gas for Power Generation Location: ShuiGe Landfill Site, Nanjing City, Jiangsu Province, China Background & Activity: The UNDP/GEF project, “Promoting the Methane Recovery and Utilisation from Mixed Municipal Refuse of Chinese Landfill Sites” was initiated in 1997, One major activity of the project is to construct landfill gas utilisation systems in three Chinese cities. Shuige Landfill Site of Nanjing city is one of the demonstration sites. The landfill sites were owned by local government, but through bidding, the local government and

42

project management office selected an Australian company to take charge of the construction and operation of the landfill gas utilisation system. The local government also helped with negotiations between the Australian company and the local power-grid company. The Power Purchase Agreement was signed in 2001 and the system began operation in 2002. This project was successful in selecting a private company (international) to operate the system, rather than intending the owner of the landfill site to manage the system. d. Solar Water Heater Integrated Building Location: Tianjin or Qingdao (to be determined) Background & Activity: The solar water heater is the single technology in the renewable energy field at the full commercialisation stage in China. In some cities such as Kunming, development is progressing quite well, but in others, especially in tourist-attractive cities such as Dalian, installation was forbidden by the local regulations, which considered solar water heaters to badly influence the appearance of buildings. In recent years, the concept of the solar water heater integrated building was proposed, and a number of solar water heater manufacturers have cooperated with construction companies to install the new solar water heater in solar buildings. A UNF project titled “Improvement and Expansion of Solar Water Heating Technology in China” was implemented in year 2002, and both Tianjin and Qingdao are sites for demonstration. The case study will examine one of the demonstration sites, however as members of the research group have not yet visited the sites, the site for our case study is yet to be decided. Strategic Policy Options developed

Increasing financing by private/public financial institutions

The perception of high risk and high transaction costs of renewable energy transactions, combined with limited affordability by low income consumers are common barriers to commercial banking playing a significant role in financing access to RE products and services. The policy options envisaged aim to: increase the renewable portfolio in total bank lending; increase government intervention that establishes new financial institutions operating on preferential market terms; and introduce mechanisms to reduce the interest rate for commercial lending.

In China, the establishment of a renewable energy development fund has been studied and discussed amongst the relevant governmental departments for some time. The fund will be set up by the government, with the objective of providing funds specifically for the development and utilisation of renewable energy. The renewable energy development fund will use funding from the following sources:

– Sale surcharge of electric power and fuel: in accordance with the target of renewable energy development, the government will calculate the level of surcharge to be imposed on the sale price.

– Financial allocation from China’s central government – Benefits from fund – Grants and others

Once established, the fund will be used for the following purposes: – Subsidies for power tariff gap of renewable generation connecting with the grid – Subsidies for investment and operation costs of off-grid power systems in remote areas – Subsidies for price gap of bio-liquid fuel – Subsidies for renewable energy technology application in rural areas – Subsidies for technology research & development, introduction, demonstration projects – Outreach, education, training, international cooperation and exchange.

43

A special account for the renewable energy development fund will be established to be located in China’s central financial agency. The government agencies responsible for energy management will develop an annual budget so as to realise the target of “a special fund for a special purpose”. On examination and approval of the subsidies for renewable generation and bio-liquid fuel by the government departments concerned, the enterprises can deduct this directly from the sale surcharge on behalf of the relevant agencies. Suggestions on research plan in Year 3 April: – “EU-China High Level Conference on Renewable Energy policy and Project Financing” in

Beijing. – Study of SPO analysis evaluation model methodology May – June – Develop SPOs – Participate in the renewable energy international conference to be held in Born, Germany – Compile SPO background report – Study of model analysis scenarios August – October – Apply the model to the development of scenarios analysis – Prepare initial SPOs national report September – December – Review and discussion of SPOs national initial report – Meeting of capacity building January – February – Complete and revise SPOs national report – Finalise SPO report

44

B. India Summary of research activities in FY 2003

Year 2 of the IFRED sub-theme focussed on four activities:

1. Finalising the framework for SPOs 2. Writing the research note/background paper 3. Presenting the research outcome at an International Conference 4. Collecting four more GPIs

Based on the provisional framework developed in year 1 of the sub-theme, work continued

towards finalising the SPO framework following the life-cycle approach. The results of the policy and literature review, and the first four GPIs indicated that there is a relation of interdependence between the deployment of RE products and technologies and their market demand with regard to financing. The availability of financing for research and development as well as for manufacturing is crucial for reducing the high costs of the systems. Similarly, adequate consumer finance enhances affordability and stimulates further demand, which in turn leads to further development of the RE industry.

Given this inter-linkage between industry and market growth on the one hand and price

reduction on the other, the challenge of financing is addressed under a life-cycle approach, which examines financing mechanisms during the stages of: 1) research and development; 2) demonstration; 3) early commercialisation; and 4) demand-driven commercialisation. The above framework was finalised through the following steps:

- Team meeting in Delhi, India in August 2003, attended by IGES, ERI and TERI - Electronic discussion and e-mails - Group meeting during RISPO research meeting in Bangkok in November 2003, attended by

IGES, ERI, Department of Energy, Fiji and TERI - Group meeting during 2nd RISPO plenary workshop in Hayama, Japan in February 2004,

attended by IGES, ERI, Department of Energy, Fiji and TERI - Writing the research note/background paper

Based on the research completed in Year 1, a research note “Financing Renewable Energy in India: A Review of Mechanisms in Wind and Solar Applications” was written by the team members from IGES and TERI. This note, after undergoing the peer review process, is now being published in the International Review of Environmental Strategies.

Collecting four more GPIs The following four GPIs were collected in Year 2. They are summarised in section 4 of this

report: - Developing a sustainable financing model for SPV pumping - 7.8 MW biomass grid connected power - CDM project - Market development for Solar lantern in a post-subsidy regime - Commercialisation of Solar hot water systems Presenting the research outcome at an International Conference

Based on the research of Year 1, a paper entitled “Developments with Photovoltaic Research and Applications in India” was presented at the 14th International PV Science and Engineering Conference in Bangkok, in January 2004.

45

Background information in India As of March 2003, the achievements in grid connected wind energy systems and Solar PV stand

at 1807 MW and 121 MWp respectively. Further, the government is keen to increase the share of RE in the country’s installed power generation capacity by an additional 10,000 MW by the year 2012. A draft of the RE policy statement has been submitted by MNES for approval. Within the long-term vision, this Policy Statement seeks to set out the major application areas and near term targets for the period up to the end of the Eleventh Five Year Plan, the year 2012. One of the major application areas is the village electrification of 18,000 remote villages. In another initiative, the Ministry of Power (MoP) has set up a mission called REST – Rural Electrification Supply Technology Mission— whose basic objective is to accelerate the completion of all villages progressively by the year 2012 using local RE sources and decentralised technologies (as of March 31st 2003, 72715 villages were yet to be electrified). Such target oriented programmes and the introduction of the Electricity Act 2003 (EA 2003), which came into effect on June 2nd 2003 are expected to facilitate the development of the RE market in India.

The Electricity Act 2003 contains several provisions favourable to RE power, including rural

electrification. It provides for local generation and distribution of electricity by Panchayats (legally elected village level governing bodies), rural franchisees, NGOs and user associations by involving local communities in managing electricity distribution. Under the open access scheme expected to be in place by mid 2004, the Independent Power Producers (IPP) can establish RE power plants for captive use, third party sale, power trading companies and for own transmission and distribution both in rural and urban areas. The act also directs the Central Government to prepare national electricity and tariff policies including RE based power. The most important feature of the act is that it empowers state electricity regulators to promote RE specifically by purchasing electricity from RE sources from distribution licensees. This is considered to be a major boost in the promotion of the RE sector in India. In other words, once it is implemented, the utilities in the state will be given a target for RE based power, a certain percentage as specified by the regulator. In this liberalised electricity market, the financing mix for RE is likely to change as new financing institutions and mechanisms are developed. Good practices identified

This section gives a summary of the four good practices reviewed in this report

a. Developing a sustainable financing model for solar pumping systems

The scheme was designed to promote the use of solar photovoltaic pumping systems as an alternative to diesel powered pump sets. This was to reduce diesel consumption, which in turn can reduce environmental pollution and hardship faced by farmers in fetching diesel from far of places.

The scheme has been one of the most successful schemes in the renewable energy sector in the

country. Under the scheme so far 1700 pumps have been installed in the state of Punjab in the last three years. The total number of pumps installed in the country stands at 5113. It is estimated that an individual farmer is able to save INR 40000 to 60,000.00 in diesel expenses per year. Additionally, employment is generated in the state since each manufacturer provides service facilities at the district level. An appropriate financial scheme is the critical tool for the success of this project. The innovative approach of combining soft loans, user contribution, government assistance in terms of capital subsidy and users contribution and enhancing the advantage of depreciation tax benefit to the beneficiary is key to success of the scheme. A judicious mix of these financial instruments resulted in a net contribution of beneficiary to Rs. 55,000.00, which is close to the investment required for a conventional diesel pump set. Thus the main barrier, high capital investment, was removed.

46

b. Market development for Solar Photovoltaic lantern in post-subsidy regime

Solar Lanterns were first developed in India almost a decade ago to provide a cost effective, affordable solution to meet the challenge of providing adequate light to the rural population of India. Solar lanterns were first developed to replace the candles, kerosene lights and hurricane lanterns commonly used by villagers. Besides this, portable light is used in agricultural fields during irrigation, harvesting, during fishing at night, and for many other activities. The portable solar lantern is an ideal solution for these applications. The Ministry of Non Conventional Energy Sources, Government of India, initially developed the specifications for lantern that can give adequate illumination for 4 hours per day. In the initial stages of development, the lantern cost was approximately, Rs 5500, a subsidy of Rs 3500 was available from the central government and some states provided additional subsidy. The lantern programme became quite successful and 441481 lanterns were distributed by 31st March 2003. The main barrier identified was the limited funding available for subsidy. Market feedback from users gave new ideas for product development and marketing to manufacturers. However, MNES approved just one lantern design under the subsidy scheme. The limited funds available for subsidy and the high price of non-subsidised lanterns when compared with the subsidised lanterns, was identified as a major barrier to the large-scale penetration of lanterns into the Indian market. A number of manufacturers identified the market potential and developed various new designs. The cost of these smaller design models was reduced to Rs.1500. In the year 2003, the subsidy for solar lanterns was removed on the understanding that the product was now mature and capable of being sold in the open market on its own merits. In the post-subsidy regime, manufacturers developed various innovative schemes such as the salary deduction scheme to enhance the market for the new product. c. Commercialisation of Solar hot water systems through financial intermediary scheme

The objective of this case study was to assess the effectiveness and impact of an innovative financing instrument, namely ‘financial intermediary scheme’, on the solar thermal market. The use of solar water heating systems has increased rapidly in the domestic market in India, particularly in the state of Maharashtra, in the last few years. The typical solar water heating system consists of a solar collector, insulated storage tank, cold water supply tank and insulated piping. The collectors are manufactured and certified as per Indian standards (IS12933) and there are 58 approved manufacturers in the country. The total installed capacity in the state of Maharashtra is above 3.5 Millions lit per day (70,000 Sq m. area). The Ministry of Non Conventional Energy Sources (MNES) removed the direct capital subsidy on solar water heating systems in 1993 and the demand for solar water heating systems subsequently decreased. MNES then introduced two schemes: i) direct soft loan through nationalised banks and, ii) soft loan scheme through financial intermediaries. The financial intermediaries (FI) can be any company meeting the criteria of eligibility for channelling the credit from IREDA to the customer. This approach opened new markets for manufacturers who themselves became financial intermediaries or created links between themselves and the financial institutions participating in the scheme. This study was carried out to assess the impact of the scheme on the market and manufacturers.

47

d. Biomass power development by the private sector - a combination of international funding mechanism and public sector financing

The 7.8 MW biomass power plant in Rajasthan is one of the six projects short listed by the Government of The Netherlands under their Carbon Emission Reduction Units Procurement Tender (CERUPT). This is the first biomass power project to be commissioned under the CDM in India. The project utilises mustard stalk as a major biomass fuel for generating steam for power generation, which is abundantly available in the vicinity of the site. A portion of the electricity generated is sold to the State grid, namely Rajasthan State Electricity Board (RSEB). Kalpataru Energy Venture Private Ltd., has implemented this project near the village of Kawai in the Bharatpur District, in the state of Rajasthan in India, based on CDM. The CDM project Design Document (PDD) is presently under validation by the Accredited Operational Entity (AOE). The total investment in the project is USD 7 Million and the expected revenue from CERs is USD 1.3 million over 10 years, with a total CERs generation of 0.3 million over 10 years. The project achieved financial closure from a nationalised bank, namely the Oriental Bank of Commerce. The project also envisages an advance payment from CERs revenue totalling 50 % of the total revenue from CERs on a discounted basis.

The combustion technology used is totally indigenous, whereas the turbine is imported from Japan. The power generated is sold to the state utility, namely the Rajasthan Vidyut Prasaran Nigam (RVPN). The Power Wheeling and Banking Agreement (WBA) has also been signed with RVPN and the Vidyut Vitran Nigams (VVNs) for the sale of power to third parties. The electricity generated will replace the mixture of lignite and coal-based power generation. The project generates substantial direct employment and contributes to the economic development of the region. Strategic Policy Options developed a. Optimum use of government funds

There is a clear indication that public finance, either through subsidy, fiscal incentives or other forms of governmental financial support, is crucial in the initial stages of technology and market development. In both developing (India’s RE programme) and developed countries (Japan’s Sunshine project), government support in terms of technology development funds, performance linked incentives etc. have helped the growth of the RE sector. However, at the commercialisation stage, sustainable market development is illusionary so long as it depends solely on subsidy. Nevertheless, the removal of subsidy can only be envisaged in terms of gradual policy change. This involves a competitive approach to the provision of subsidy with the objective of optimal use, as well as a stable and long-term commitment to selective subsidy to ensure long-term private investment commitments, and a combination of subsidy with loan ownership models. The approach taken under this SPO includes: a) the choice of government funding at the demonstration stage, subsidy support at the market initiation stage and soft loans at the commercialisation stage, b) the use of a fee-for-service model that matches the user ‘s financial capacity with the level of services provided and the effective use of various developmental funding in setting up the utility. Related good practices

Market development of Solar lanterns in post-subsidy regime Developing a sustainable financial model for solar pumping systems Commercialisation of Solar hot water systems through the ‘financial intermediary (FI)

scheme’ implemented by MNES/IREDA Solar PV minigrids in Sunderbans- a combination of government and community financing Public sector financing for wind power development

48

b. International funding mechanisms

Bilateral and multilateral financing sources have played a major role as incubation funds for RE development. However, the traditional method of one-time delivery of aid either through direct financing or provision of equipment has serious limitations. This strategy option identifies new forms of delivery of external aid within the national policy framework, taking into consideration barriers that can best be addressed by external aid and international funding mechanisms, such as the Global Environment Facility and the clean climate initiatives. The analytical work under the SPO has focused on the Clean Development Mechanism (CDM) taking into consideration international developments in the CDM process as well as those at the national level in India. At the international level, the modalities and procedures (M&P) for operationalising CDM have progressed satisfactorily. This has been accompanied by similar progress at the national level, in terms of establishing the DNA (Designated National Authority), a number of project design documents in response to CDM tenders, scores of capacity building events, country CDM studies etc., In India, the DNA, established in December 2003, had cleared around 17 projects as of February 2004 out of a total submission of 47 projects. The CDM project development has peaked in India and there are more than 100 PINs (Project Information Notes) currently seeking sources for development PDDs (Project Design Documents). Under various donors of the CDM capacity-building programme in India (8 so far) and in response to various CDM tenders, a total of around 50 PDDs are in various stages of completion, while many other PDDs have already been completed. These donors and tendering countries include GTZ, CIDA, The World Bank, Sweden, The Netherlands, the Prototype Carbon Fund, Austria, Foreign Commonwealth Office, U.K. Additionally, at least 75 PDDs are at various stage of completion under private sector initiatives,. Most of the PDDs are being developed in the energy sector, with renewable energy the most frequent. Related good practices

Wind power development by the private sector - a combination of international funding mechanism and public sector financing

Biomass power development by the private sector - a combination of international funding mechanism and public sector financing

49

Suggestions on research plan in Year 3 April: – Renewable energy conference in New Delhi – Revising good practices May – June – Developing SPOs – Drafting background papers August – October – Prepare initial SPOs national report September – December – Organising two workshops to disseminate the research findings January – February – Revising SPOs national report – Finalise SPO report

50

3.2.1.3. Good Practices collected in FY 2003

1. Commercialisation of Solar hot water systems through financial intermediary scheme, India.

2. Developing a sustainable financing model for solar pumping systems, India.

3. Market development for Solar Photovoltaic lantern in post-subsidy regime, India.

4. Biomass power development by the private sector - a combination of international funding mechanism and public sector financing, India.

5. Demonstration of wind power concession policy to reduce the large-scale wind power price, China.

6. Encouraging Various Finance Sources for the Utilisation of Landfill Gas Through Economic Incentive Policies, China

51

Asia-Pacific Environmental Innovation Strategies (APEIS) Research on Innovative and Strategic Policy Options (RISPO)

Good Practices Inventory

Commercialisation of Solar hot water systems through ‘financial intermediary (FI) scheme’ implemented by MNES/IREDA

Keywords: Solar water heating systems, Financial Intermediary (FI) scheme, IREDA, MNES Strategy: Innovative financing for renewable energy development Environmental areas: Urban environment Critical instruments: Economic instruments, Organisational arrangements Country: India Location: State of Maharashtra, India Participants: Solar thermal manufacturers, Indian Renewable Energy Development Agency (IREDA), Individual customers, Ministry of Non-Conventional Energy Sources (MNES) Duration: 1995-onwards Funding: Community, IREDA and private financial institutes

Background: The use of solar water heating systems is increasing rapidly in domestic market in India and particularly in the state of Maharashtra in last few years. The typical solar water heating system consists of a solar collector, insulated storage tank, cold water supply tank and insulated piping. The collectors are manufactured and certified as per Indian standards (IS12933). There are 58 approved manufacturers in the country. Total installed capacity in the state of Maharashtra is above 3.5 Millions lit per day (70,000 Sq m. area). The Ministry of Non Conventional Energy Sources (MNES) removed the direct capital subsidy on solar water heating systems in 1993. Subsequently the demand for solar water heating systems reduced. MNES then introduced two schemes- i) direct soft loan through nationalised banks and, ii) soft loan scheme through financial intermediaries. The financial intermediaries (FI) can be any company meeting the criteria of eligibility for channelling the credit from IREDA to the customer. This approach opened new markets for manufacturers who themselves became financial intermediaries or who tied up with financial institutions for participating in the scheme. This study was carried out to assess the impact of the scheme on market and on manufacturers.

Objectives: The objective of this case study was to assess the effectiveness and impact of the innovative financing instrument namely ‘financial intermediary scheme’ on the solar thermal market

Description of the activity: The scheme of soft loan through financial intermediaries was formulated to open the market for solar water heating systems. It was observed that there is a huge market potential for solar water heating systems as the technology is proven and accepted by the market. However, the main barriers were i) limited funds available under subsidy schemes and, ii) lengthy and time consuming procedures to get the subsidy sanctioned. The soft loan through intermediaries removed these two barriers effectively. Under the scheme, financial intermediary can get a line of credit approved from IREDA for providing loans to customers based on the projected sales. The loan is available for onward financing the customer for purchase of solar water heating systems. The FI can avail loan at an interest rate of 2.5 % per annum and can extend loan to consumer at an interest rate of up to 5% (spread of 2.5%). the loan is available upto 80% of the system cost. The FI is responsible for the recovery of the loan amount from the customer and is also responsible to return the loan to IREDA, which provided the finance. The funds are revolving type and FI based on its business plan can avail further loans. Any legal company that can satisfy eligibility criteria and terms and conditions of the loan scheme can become the FI. The

Summary of the Practice

52

scheme was specifically designed to help individual customers and customers of domestic hot water systems.

Overview Economic instruments, in particular the combination of various financing instruments, and an organisational arrangement whereby a one-stop service takes care of product delivery, financing and after sales services were critical to the success of the scheme.

Economic instruments Choice of government funding at demonstration stage, subsidy support at market initiation stage and

soft loan at commercialisation stage The product has seen the support of various financing instruments at different stages of its life-cycle. The sector has witnessed a tremendous growth even after the removal of subsidy, indicating that appropriate financing instruments at appropriate developmental stage help the sector grow.

Organisational arrangements One-stop service regarding product, finance and after-sales service.

The financing intermediary scheme provided means for financing proven renewable energy technology on wider scale. It helped consumers to get guaranteed service from one point. It also increased the consumer confidence in manufacturer, product and after sales service. The scheme also helped increasing the credibility of the products since the supplier/ manufacturing company offered loan too.

The scheme helped manufacturer to provide financial assistance to prospective customer directly. This improved the market as customers from small towns, rural and semi urban areas could also take loan easily. Same supplier providing loan, also gave the customer a confidence about his credibility, as well as quality and durability of the product. This improved the market response and trust in technology. The sales for solar water heating system are rising steadily and total installed capacity is now well over 0.7 million Sq. m as on March 2003. Following graph shows the year wise installations.

Source - MNES annual reports from 1988 to 2000

1. Appropriate financial schemes are a must to cater to the needs of the consumers for proven RE technologies that are on the verge of commercialisation.

Impacts

Lessons Learned

100

150

200

250

300

350

400

450

500

550

1988 1990 1992 1994 1996 1998 2000Year

X100

0 sq

. m

Critical Instruments

53

2. Adequate availability of working capital and funds for providing loan helps during early commercialisation. Shortage of funds for loan scheme, subsidy etc. act as barrier for people to run away from RE technology.

3. Timely change in policies responding to changing market needs both in term of finance and product up-gradation is important.

4. The capital investment in the case of solar water heating system is 4 times more than that for the conventional electric geyser however; the savings in electricity consumption are equal to or in some cases, more than the monthly repayment of the loan. However, as market increased, the manufacturers, particularly small and medium ones with their limited resources faced difficulty in providing guarantees required for loan security. Also, their locked up capital in loan for five years became barriers. However, by that time the bank loan schemes came in to place in a big way and thus the transaction was smoother. The customer now has choice of loan schemes or for cheaper price for 100% down payment purchase.

The success of the intermediary finance scheme implemented through manufacturers and other eligible agencies can be effectively used for other products and technologies in other countries. In the case of solar hot water system alone, apart from domestic sector, the process heat requirements in the small and medium enterprises can economically be met by this technology. Mr. Shirish Garud, Fellow, The Energy and Resources Institute (TERI) Darbari Seth Block, Habitat Place, Lodhi Road, New Delhi 110003, India. [email protected] Ph 0091-11-24682111 Fax 0091-11-24682144 Case reviewer: Shirish Garud, Fellow, The Energy and Resources Institute (TERI), E-mail: [email protected] Information date: 20 March 2004

Potential for Application

Contact

54

Asia-Pacific Environmental Innovation Strategies (APEIS) Research on Innovative and Strategic Policy Options (RISPO)

Good Practices Inventory

DEVELOPING A SUSTAINABLE FINACIAL MODEL FOR SOLAR PUMPING SYSTEMS

Keywords: Solar photovoltaic, Solar water pumping, Soft loan, Subsidy, IREDA Strategy: Innovative financing for renewable energy development Environmental areas: Water resource management, Rural Environment Critical instruments: Economic instruments, Awareness capacity building Country: India Location: State of Punjab, India Participants: Punjab Energy Development Agency, PV industry, Individual farmers (Village community), local enterprise, Indian Renewable Energy Development Agency (IREDA), Ministry of Non-Conventional Energy Sources (MNES) Duration: 1999-onwards Funding: Central subsidy, sate subsidy, community, IREDA, private financial institutions

Background: Punjab is the largest surplus state in food grains in India. The state is also called as the ‘food bowl’ of India. Located in North West of the country, Punjab has an area of 50362 Sq. km comprising of plain and fertile land. At present, over 84% of the total geographical area of the state is under cultivation. The state has four major rivers and a vast network of canals and tube wells for irrigation purpose. As per State government Statistics, in 1997-98 the state had a total of 9,75,000 tube wells out of which 7,50,000 are having electrical pumps and 1,25,000 are powered by diesel generators. Due to the shortage of electricity, many tube wells, which are powered by electricity, have alternative diesel powered pumps installed with it. The water table available in most parts of the state is @ 5 m. Solar Photovoltaic based water pumping systems, though found suitable, are beyond the reach of the farmers. The solar PV pumping project of MNES/IREDA as implemented in the state of Punjab, has introduced innovations in original scheme to not only match the technology services to the needs of the farmers, but also to make these services affordable to them.

Objectives: The scheme was designed to promote the use of solar photovoltaic pumping systems as an alternative to diesel powered pump sets. This was to reduce the diesel consumption, which in turn can reduce the environmental pollution and hardship of farmers who have difficulties in fetching diesel from far off places.

Description of the activity: Under the Solar Photovoltaic Water Pumping Programme of the MNES, the Punjab Energy Development Agency (PEDA) has completed installation of 500 solar pumps in Punjab for agricultural uses. When the subsidy scheme for solar photovoltaic pumping was launched in India, only 900 Wp (1 Hp) system at roughly Rs. 200,000 with 50% capital subsidy on the complete system was approved. There were few takers of this scheme in Punjab as the 1 Hp system was not sufficient to meet irrigation requirement of the farmers, and the expected contribution from the farmer (Rs. 100,000) was very high. Realising that the farmers needed a minimum 2 Hp (1800 W) capacity pump and a suitable finance scheme (as this pump costs Rs. 350,000), the Punjab State Government through its agency- Punjab Energy Development Agency (PEDA) took following initiatives:

Summary of the Practice

55

1. Got the 1800 W (2 Hp) capacity solar photovoltaic pumping system approved by the MNES for

distribution under the scheme 2. Helped manufacturers to tie up with financial institutions to take soft loan from IREDA and

offer pumps under lease-finance scheme. (In this scheme, the financial institution takes advantage of the financial incentive in terms of 100% accelerated depreciation in the first year available under Income tax rules and passes on this incentive to the user by offering him a one-time lump-sum payment instead of the regular rentals)