22_schedule_vi

35

1 SCHEDULE VI OF COMPANIES ACT,1956 CUM SCHEDULE VI OF COMPANIES ACT,1956 CUM ANNUAL REPORT ANALYSIS ANNUAL REPORT ANALYSIS BY SUMAT SINGHAL BY SUMAT SINGHAL INTRODUCES A SEMINAR ON INTRODUCES A SEMINAR ON

-

Upload

sumatrhtdm -

Category

Documents

-

view

219 -

download

0

Transcript of 22_schedule_vi

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 1/35

11

SCHEDULE VI OF COMPANIES ACT,1956 CUMSCHEDULE VI OF COMPANIES ACT,1956 CUMANNUAL REPORT ANALYSISANNUAL REPORT ANALYSIS

BY SUMAT SINGHALBY SUMAT SINGHAL

INTRODUCES A SEMINAR ONINTRODUCES A SEMINAR ON

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 2/35

22

ObjectiveObjective

To Understand:To Understand:General Requirements of the Company Act General Requirements of the Company Act

SCHEDULE VI with respect toSCHEDULE VI with respect toRequirements of the Company Act with respect to theRequirements of the Company Act with respect to theProfit and loss account Profit and loss account Requirements of the Company Act with respect to theRequirements of the Company Act with respect to the

Balance sheet Balance sheet Part IIIPart IIIPart IVPart IV

Accounting Treatment of Special Items in the financial Accounting Treatment of Special Items in the financialStatements of a Limited CompanyStatements of a Limited Company

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 3/35

33

Books of AccountsBooks of Accounts

SectionSection 209209 of of thethe CompaniesCompanies Act Act specifiesspecifies thethe booksbooksof of accountsaccounts toto bebe maintainedmaintained byby aa companycompany. .

According According toto thisthis Section,Section, everyevery companycompany shouldshould keepkeepat at itsits registeredregistered officeoffice properproper booksbooks of of accountsaccounts. .

CompaniesCompanies whichwhich areare engagedengaged inin manufacturing,manufacturing,

production,production, processingprocessing oror miningmining activities,activities, shouldshouldprepareprepare aa set set of of cost cost accountsaccounts inin additionaddition toto thethefinancialfinancial accountsaccounts. .

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 4/35

44

Legal Requirements RegardingLegal Requirements Regarding Annual Accounts Annual Accounts

At At everyevery annualannual generalgeneral meetingmeeting of of thethe shareholders,shareholders, thethe BoardBoard of of DirectorsDirectorsof of thethe companycompany shouldshould laylay beforebefore thethe shareholders,shareholders, a a balancebalance sheet sheet andandprofit profit andand lossloss account account asas at at thethe endend of of thethe accountingaccounting periodperiod..

TheThe annualannual accountsaccounts of of thethe companycompany must must bebe submittedsubmitted inin anan annualannualgeneralgeneral meetingmeeting withinwithin sixsix monthsmonths countedcounted fromfrom thethe last last dayday of of thetheaccountingaccounting periodperiod toto whichwhich thethe accountsaccounts relaterelate..

TheThe periodperiod toto whichwhich thethe accountsaccounts relaterelate isis knownknown asas thethe financialfinancial yearyear andand it it maymay bebe lessless than,than, equalequal toto oror greatergreater thanthan 1212 monthsmonths but but cannot cannot exceedexceed 1515

monthsmonths. .TheThe CompaniesCompanies Act Act providesprovides that that aa statement statement of of allall significant significant accountingaccountingpoliciespolicies adoptedadopted inin thethe preparationpreparation andand thethe presentationpresentation of of thethe BalanceBalanceSheet Sheet andand Profit Profit andand LossLoss account account shallshall bebe discloseddisclosed inin thethe company scompany sBalanceBalance Sheet Sheet..

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 5/35

55

Part Part IIII of of ScheduleSchedule VI VI of of thethe CompaniesCompanies Act Act 19561956,, doesdoes not not prescribeprescribe anyanyformat format forfor thethe profit profit andand lossloss account account but but onlyonly outlinesoutlines thethe informationinformation toto bebeincludedincluded..

TheThe variousvarious itemsitems of of receiptsreceipts andand expensesexpenses shouldshould bebe arrangedarranged underunder most most convenient convenient headsheads. .

SecSec 211211 requirement requirement

According According toto Part Part IIII of of Schedule,Schedule, certaincertain informationinformation hashas toto bebe providedprovided bybywayway of of notesnotes toto profit profit andand lossloss account account. .

TheThe profit profit andand lossloss appropriationappropriation showsshows inin detaildetail thethe appropriationsappropriations mademadefromfrom thethe profitsprofits inin respect respect of of dividendsdividends andand transfertransfer toto reserves,reserves, etcetc..

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 6/35

66

Legal Requirements with Respect to BalanceLegal Requirements with Respect to BalanceSheetSheet

Part Part II of of ScheduleSchedule VI VI of of thethe CompaniesCompanies Act Act specifiesspecifies bothboth thethe formform andandcontent content of of thethe balancebalance sheet sheet of of aa companycompany. .

So a company may prepare its balance sheet either in the horizontalSo a company may prepare its balance sheet either in the horizontal

specified in part I Schedule VI or may prepare it in a statement form, statingspecified in part I Schedule VI or may prepare it in a statement form, statingthe liabilities as sources of funds in the first part and listing the assets asthe liabilities as sources of funds in the first part and listing the assets asapplications of funds in the second part.applications of funds in the second part.

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 7/35

77J OURNEY BEGINS NOW .J OURNEY BEGINS NOW .

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 8/35

88

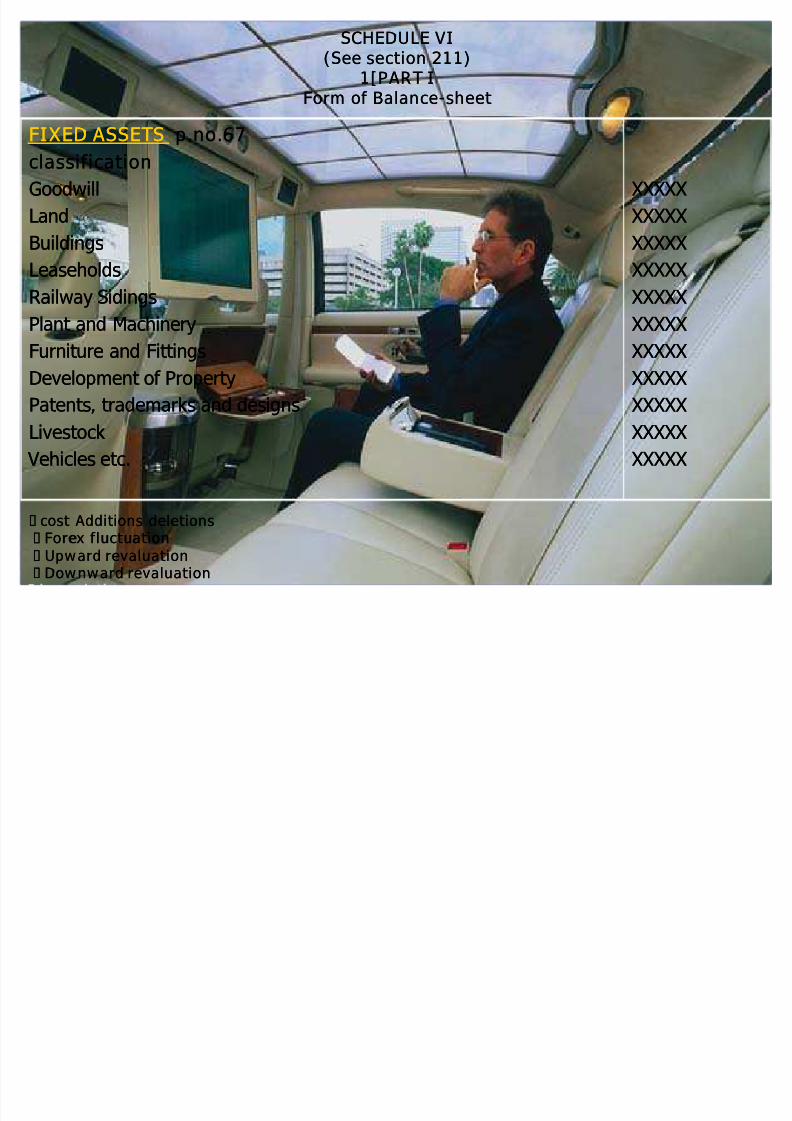

FIXED ASSETSFIXED ASSETS p.no.67p.no.67classificationclassificationGoodwillGoodwillLandLandBuildingsBuildings

LeaseholdsLeaseholdsRailway SidingsRailway SidingsPlant and MachineryPlant and MachineryFurniture and FittingsFurniture and FittingsDevelopment of PropertyDevelopment of Property

Patents, trademarks and designsPatents, trademarks and designs

LivestockLivestock Vehicles etc. Vehicles etc.

XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX

XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX

XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX

SCHEDU LE VISCHEDU LE VI(See section 211)(See section 211)

1[PART I1[PART IForm of BalanceForm of Balance- -sheetsheet

cost Additions deletionscost Additions deletionsForexForex fluctuationfluctuationUpward revaluationUpward revaluationDownward revaluationDownward revaluation

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 9/35

99

INVESTMENTSINVESTMENTS p.nop.no. 79. 79Investments in Govt. or Trust SecuritiesInvestments in Govt. or Trust Securities

Investments in shares, debentures or bondsInvestments in shares, debentures or bonds

Immovable propertiesImmovable properties

Investments in the capital of partnership firmsInvestments in the capital of partnership firms

Balance of Balance of unutilisedunutilised monies raised by Issuemonies raised by Issue

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

valuationsvaluationsShares market value of quoted and unquotedShares market value of quoted and unquotedinvestment details : a statement of investments in body corporateinvestment details : a statement of investments in body corporate

Investment in partnership firmsInvestment in partnership firmsunutilisedunutilised money raised by issuemoney raised by issue

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 10/35

Some brain exerciseSome brain exerciseWhat about What about

Investment of reserve fundInvestment of reserve fund

Investment in subsidiary co. for trade purposeInvestment in subsidiary co. for trade purpose

Temporary investment of idle working capitalTemporary investment of idle working capital

Investment pledged with bank as securities forInvestment pledged with bank as securities forloanloan

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 11/35

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 12/35

1212

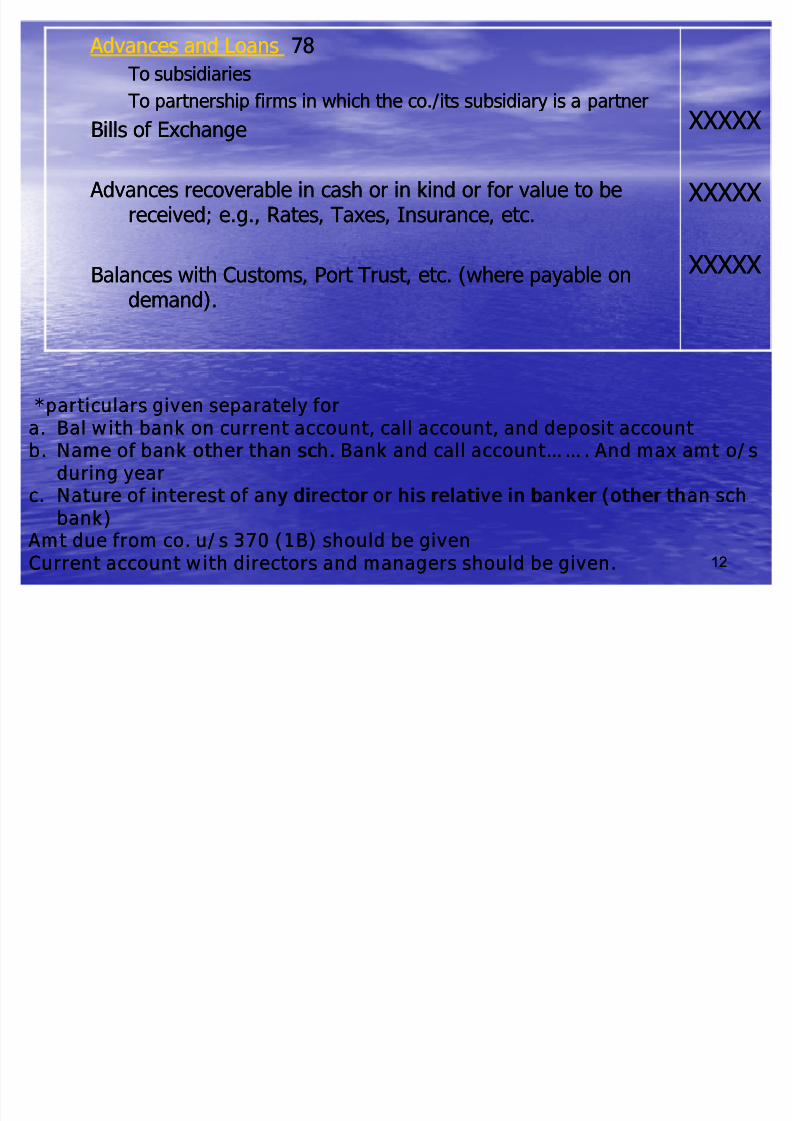

Advances and Loans Advances and Loans 7878To subsidiariesTo subsidiariesTo partnership firms in which the co./its subsidiary is a partnerTo partnership firms in which the co./its subsidiary is a partner

Bills of ExchangeBills of Exchange

Advances recoverable in cash or in kind or for value to be Advances recoverable in cash or in kind or for value to bereceived; e.g., Rates, Taxes, Insurance, etc.received; e.g., Rates, Taxes, Insurance, etc.

Balances with Customs, Port Trust, etc. (where payable onBalances with Customs, Port Trust, etc. (where payable ondemand).demand).

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

*particulars given separately for

*particulars given separately fora.a. Bal with bank on current account, call account, and deposit accountBal with bank on current account, call account, and deposit account

b.b. Name of bank other than sch. Bank and call account . And max amt o/sName of bank other than sch. Bank and call account . And max amt o/sduring yearduring year

c.c. Nature of interest of any director or his relative in banker (other thanNature of interest of any director or his relative in banker (other than sch schbank)bank)

Amt due from co. u/s 370 (1 B) should be given Amt due from co. u/s 370 (1 B) should be givenCurrent account with directors and managers should be given.Current account with directors and managers should be given.

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 13/35

1313

MISCE LL ANEOUS EXPENDITUREMISCE LL ANEOUS EXPENDITURE(to(to the extent not written off or adjusted)the extent not written off or adjusted)

Preliminary ExpensesPreliminary Expenses

Expenses including commission/ brokerage on underwriting orExpenses including commission/ brokerage on underwriting orsubscription of shares or debenturessubscription of shares or debentures

Discount allowed on issue of shares or debenturesDiscount allowed on issue of shares or debentures

Interest paid out of capital during constructionInterest paid out of capital during construction

Development expenditure not adjustedDevelopment expenditure not adjusted

Other items (Specifying nature)Other items (Specifying nature)

PRO FIT AND LOSS ACCOUNTPRO FIT AND LOSS ACCOUNT(Debit Balance)(Debit Balance)

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

FAST FAST

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 14/35

1414

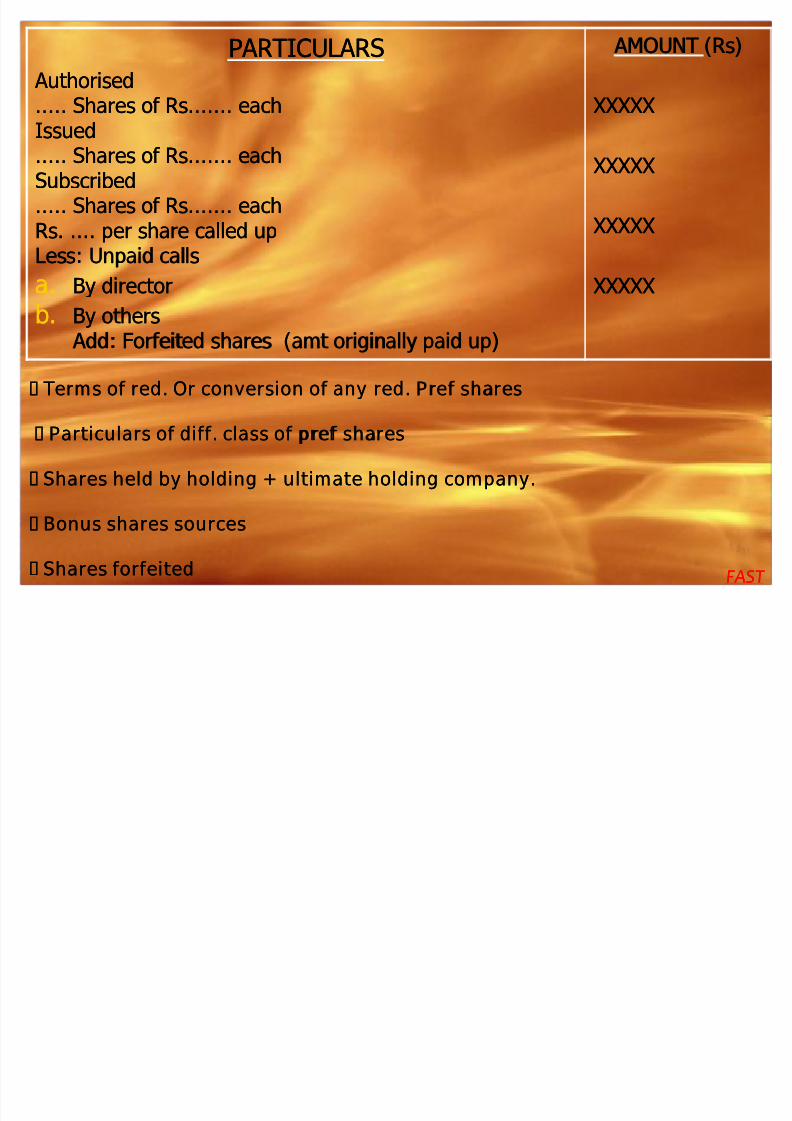

PARTICULARSPARTICULARS Authorised Authorised..... Shares of Rs....... each..... Shares of Rs....... each

IssuedIssued..... Shares of Rs....... each..... Shares of Rs....... eachSubscribedSubscribed..... Shares of Rs....... each..... Shares of Rs....... eachRs. .... per share called upRs. .... per share called upLess:Less: Unpaid callsUnpaid calls

a.a. By directorBy directorb.b. By othersBy others

Add: Add: Forfeited shares (amt originally paid up)Forfeited shares (amt originally paid up)

AMOUNT AMOUNT (Rs)(Rs)

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

Terms of red. Or conversion of any red.Terms of red. Or conversion of any red. Pref Pref sharesshares

Particulars of diff. class ofParticulars of diff. class of pref pref sharesshares

Shares held by holding + ultimate holding company.Shares held by holding + ultimate holding company.

Bonus shares sourcesBonus shares sources

Shares forfeitedShares forfeited FAST FAST

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 15/35

1515

RESERVES AND SURP LUSRESERVES AND SURP LUS

Capital ReservesCapital ReservesCapital Redemption ReserveCapital Redemption Reserve

Share Premium Account Share Premium Account Other ReservesOther ReservesLess:Less: Debit balance in profit and loss account, if anyDebit balance in profit and loss account, if any

Balance in the profit and loss accounts after providing forBalance in the profit and loss accounts after providing forproposed allocation namely Dividend Bonus orproposed allocation namely Dividend Bonus orReservesReserves

Prop osed additions to ReservesProposed additions to ReservesSinking FundsSinking Funds

XXXXX XXXXX XXXXX XXXXX

XXXXX XXXXX XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX XXXXX XXXXX

Additions and deductions Additions and deductions

Reserve and fundReserve and fund

Details of utilizations of securities premiumDetails of utilizations of securities premium

Debit bal of P & L deduct fromDebit bal of P & L deduct from uncommiteeduncommiteed reservereserve

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 16/35

1616

SECURED LOANSSECURED LOANSDebenturesDebenturesLoans and Advances from BanksLoans and Advances from Banks

Loans and Advances from SubsidiariesLoans and Advances from SubsidiariesOther Loans and AdvancesOther Loans and AdvancesUNSECURED LOANSUNSECURED LOANS

Fixed DepositsFixed DepositsLoans and Advances from SubsidiariesLoans and Advances from SubsidiariesShort Short--term Loans and Advances:term Loans and Advances:

from Banksfrom Banksfrom othersfrom others

XXXXX XXXXX XXXXX XXXXX

XXXXX XXXXX XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX XXXXX XXXXX

terms of red ofterms of red of debenturestdebenturestdebdeb held by nominee or trusteeheld by nominee or trusteeinterestinterest accuredaccured and dueand duefor secured loanfor secured loan nature of securitynature of securityloans from director , managers separatelyloans from director , managers separately

details of loan guaranteed bydetails of loan guaranteed by dorector dorector managermanager

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 17/35

1717

Other Loans and AdvancesOther Loans and Advancesfrom Banksfrom Banksfrom othersfrom others

CURRENT LIA BI LITIES & PROVISIONSCURRENT LIA BI LITIES & PROVISIONSCurrent LiabilitiesCurrent Liabilities

Acceptances AcceptancesSundry CreditorsSundry Creditors

Total outstanding dues of small scale industrialTotal outstanding dues of small scale industrialundertaking(s).undertaking(s).

Total outstanding dues of creditors other than small scaleTotal outstanding dues of creditors other than small scaleindustrial undertaking(s).industrial undertaking(s).

Subsidiary companiesSubsidiary companies Advance payments and unexpired discounts Advance payments and unexpired discountsUnclaimed DividendsUnclaimed Dividends

Other Liabilities (if any)Other Liabilities (if any)Interest accrued but not due on loansInterest accrued but not due on loans

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

XXXXX XXXXX

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 18/35

1818

ProvisionsProvisionsProvision for TaxationProvision for TaxationProposed DividendsProposed DividendsFor contingenciesFor contingenciesFor Provident Fund SchemeFor Provident Fund SchemeFor Insurance, pension and similar staff For Insurance, pension and similar staff benefit schemesbenefit schemesOther provisionsOther provisions

XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX XXXXX

Name of SSI or MSME amount due more than 30 daysName of SSI or MSME amount due more than 30 days

current a/c with directors or managerscurrent a/c with directors or managers

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 19/35

Contingent liabilities (Foot note)Contingent liabilities (Foot note)Claims against the company not acknowledged as debtsClaims against the company not acknowledged as debts

Uncalled liability on shares partly paidUncalled liability on shares partly paid

Arrears of fixed cumulative dividends on preference shares or Arrears of fixed cumulative dividends on preference shares orothersothers

Estimated amount of contracts remaining to be executed on capitalEstimated amount of contracts remaining to be executed on capitalaccount and not provided foraccount and not provided for

Other money for which the company is contingently liableOther money for which the company is contingently liable

Bills discounted not yet maturedBills discounted not yet matured

1919

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 20/35

2020

Accounting Treatment of Accounting Treatment of Special ItemsSpecial Items in the Financialin the FinancialStatements of a Limited CompanyStatements of a Limited Company

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 21/35

TheThe profit profit andand lossloss account account shouldshould disclosedisclose::((a)a) thethe result result of of thethe workingworking of of thethe companycompany duringduring thethe periodperiodcoveredcovered byby thethe account account; ; andand

(b)(b) creditscredits oror receiptsreceipts andand debitsdebits oror expensesexpenses inin respect respect of of nonnon--recurringrecurring transactionstransactions oror transactionstransactions of of exceptionalexceptional naturenature. .

ItemsItems relatingrelating toto thethe IncomeIncome && ExpenditureExpenditure of of thethe CompanyCompany arrangedarrangedunderunder thethe most most convenient convenient headsheads andand

shouldshould disclosedisclose thethe followingfollowing informationinformation inin respect respect of of thethe periodperiod coveredcovered underunder audit audit::

2121

PROFIT & LOSS ACCOUNT

DISCLOSURE REQUIREMENTS AS PER SCHEDULE VI (PART II) OF THECOMPANIES ACT, 1956

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 22/35

Clause 1.3 disclosure of the name of the CompanyClause 1.3 disclosure of the name of the Companythe corresponding amounts for the immediately preceding financialthe corresponding amounts for the immediately preceding financial

yearyearIn case of companies preparing quarterly or half In case of companies preparing quarterly or half- -yearly accountsyearly accountsNote:Note:·· Where the period covered by the previous accounts does not Where the period covered by the previous accounts does not comprise the same period as covered by current period a note thereof comprise the same period as covered by current period a note thereof should be given.should be given.·· In case of first accounts, a note thereof should be given.In case of first accounts, a note thereof should be given.

Clause 1.4 The Central Government may direct that a company shallClause 1.4 The Central Government may direct that a company shallnot be obliged to show the amount set aside to provisions other thannot be obliged to show the amount set aside to provisions other thanthose relating to depreciation, renewal or diminution in value of assets,those relating to depreciation, renewal or diminution in value of assets,

Additional Information Additional Information> Statement on the Amendments to Schedule VI to the Companies> Statement on the Amendments to Schedule VI to the Companies

Act, 1956 Act, 1956

2222

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 23/35

clause 2 Expenditureclause 2 Expenditure : :The expenditure incurred on each of the following items should be disclosedThe expenditure incurred on each of the following items should be disclosedseparately for each item :separately for each item :- ->Consumption>Consumption of stores and spare parts.of stores and spare parts.>Power>Power and Fueland Fuel>Rent >Rent >Repairs>Repairs to Buildingsto Buildings>Repairs>Repairs to Machineryto Machinery

>Salaries>Salaries, Wages and Bonus, Wages and Bonus>Contribution>Contribution to Provident and other Fundsto Provident and other Funds>Workmen>Workmen and Staff Welfare Expenses ( to the extent not adjusted from anyand Staff Welfare Expenses ( to the extent not adjusted from anyprevious provision or reserve )previous provision or reserve )Note : Information in respect of this item should also be given in the balanceNote : Information in respect of this item should also be given in the balancesheet under the relevant provision or reserve account.)sheet under the relevant provision or reserve account.)>Insurance>Insurance>Rates>Rates and Taxes, excluding taxes onand Taxes, excluding taxes on incomeincome

clause 2.12 Miscellaneousclause 2.12 Miscellaneous expensesexpensesNoteNote:: Any Any item under which the expenses are exceeding 1% of the totalitem under which the expenses are exceeding 1% of the total

revenue of the company or Rs. 5,000,revenue of the company or Rs. 5,000, which ever is higher, should be shown aswhich ever is higher, should be shown asa separate and distinct a separate and distinct item.item.2323

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 24/35

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 25/35

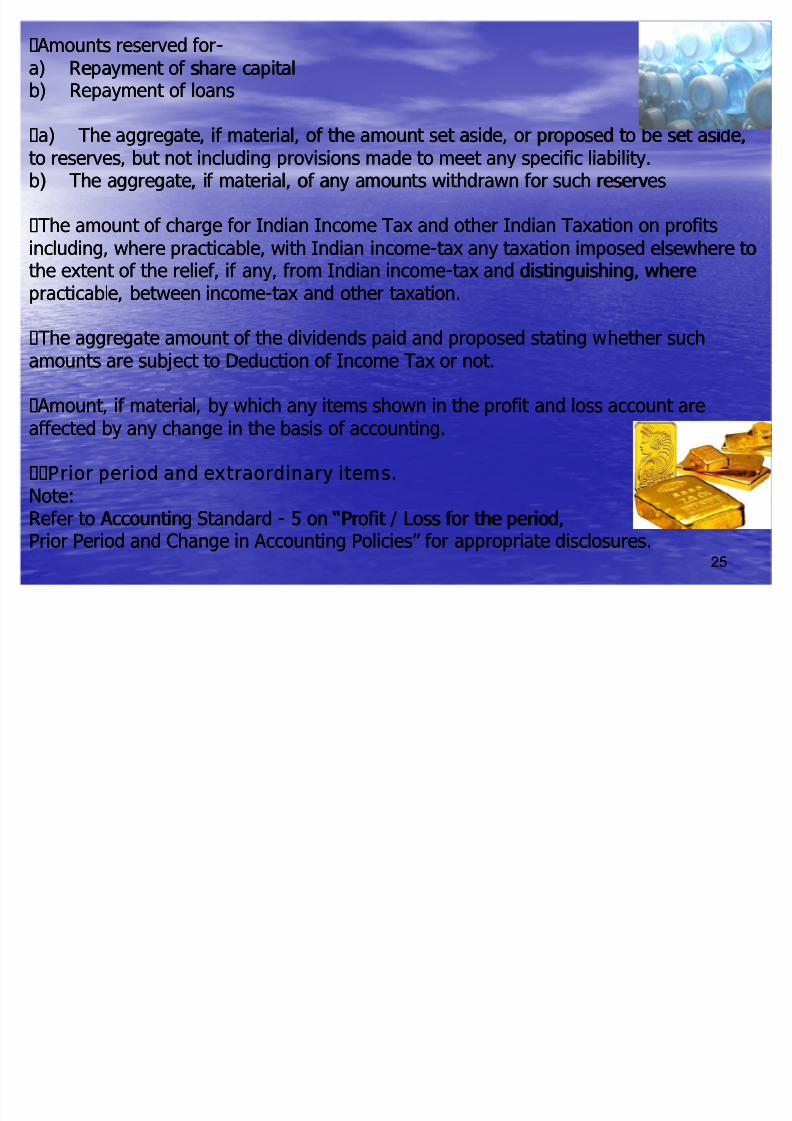

Amounts reserved for Amounts reserved for- -a)a) Repayment of share capitalRepayment of share capitalb)b) Repayment of loansRepayment of loans

a)a) The aggregate, if material, of the amount set aside, or proposed to be set aside,The aggregate, if material, of the amount set aside, or proposed to be set aside,to reserves, but not including provisions made to meet any specific liability.to reserves, but not including provisions made to meet any specific liability.b)b) The aggregate, if material, of any amountsThe aggregate, if material, of any amounts withdrawn for such reserveswithdrawn for such reserves

The amount of charge for Indian Income Tax and other Indian Taxation on profitsThe amount of charge for Indian Income Tax and other Indian Taxation on profitsincluding, where practicable, with Indian incomeincluding, where practicable, with Indian income- -tax any taxation imposed elsewhere totax any taxation imposed elsewhere to

the extent of the relief, if any, from Indian incomethe extent of the relief, if any, from Indian income- -tax and distinguishing, wheretax and distinguishing, wherepracticable, between incomepracticable, between income- -tax and other taxation.tax and other taxation.

The aggregate amount of the dividends paid and proposed stating whether suchThe aggregate amount of the dividends paid and proposed stating whether suchamounts are subject to Deduction of Income Tax or not.amounts are subject to Deduction of Income Tax or not.

Amount, if material, by which any items shown in the profit and loss account are Amount, if material, by which any items shown in the profit and loss account areaffected by any change in the basis of accounting.affected by any change in the basis of accounting.

Prior period and extraordinary items.Prior period and extraordinary items.Note:Note:Refer to Accounting StandardRefer to Accounting Standard - - 5 on Profit / Loss for the period,5 on Profit / Loss for the period,Prior Period and Change in Accounting Policies for appropriate disclosures.Prior Period and Change in Accounting Policies for appropriate disclosures.

2525

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 26/35

Income :Income : Aggregate amount of sales (turnover) Aggregate amount of sales (turnover)Note: Breakup to be given in respect of each class of goods dealt with by theNote: Breakup to be given in respect of each class of goods dealt with by thecompany indicating amount of sales and quantities of such sales for each classcompany indicating amount of sales and quantities of such sales for each classseperatelyseperately. .

Amount of income from investments, distinguishing between trade and other Amount of income from investments, distinguishing between trade and otherinvestments.investments.

Other Income by way of interest, specifying the nature of the income.Other Income by way of interest, specifying the nature of the income.

The amount of Income Tax DeductedThe amount of Income Tax Deducteda)a) Dividends from subsidiary companies.Dividends from subsidiary companies.b)b) Provisions for loss of subsidiary companies.Provisions for loss of subsidiary companies.

Profits or Losses on investment (showing separately the extent of profits orProfits or Losses on investment (showing separately the extent of profits orlosses earned or incurred on account of membership of a partnership firm)( tolosses earned or incurred on account of membership of a partnership firm)( tothe extent not adjusted from any previous reserve or provision)the extent not adjusted from any previous reserve or provision)Note : Information in respect of this item should also be given in the balanceNote : Information in respect of this item should also be given in the balancesheet under the relevant provision or reserve account.)sheet under the relevant provision or reserve account.)

2626

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 27/35

Profits or losses in respect of transactions of a kind, not usually undertakenProfits or losses in respect of transactions of a kind, not usually undertakenby the company or undertaken in circumstances of an exceptional or nonby the company or undertaken in circumstances of an exceptional or non- -recurring nature, if material in amount.recurring nature, if material in amount.

Miscellaneous Income.Miscellaneous Income.

(xv) Amount, if material, by which any items shown in the profit and loss(xv) Amount, if material, by which any items shown in the profit and lossaccount are affected by any change in the basis of accountingaccount are affected by any change in the basis of accounting. .

[[4. The profit and loss account shall also contain or give by way of a note4. The profit and loss account shall also contain or give by way of a notedetailed information, showing separately the following payments provided ordetailed information, showing separately the following payments provided ormade during the financial year to the directors (including managing directors),made during the financial year to the directors (including managing directors),oror manager, if any, by the company, the subsidiaries of the company and anymanager, if any, by the company, the subsidiaries of the company and anyother personother person: :--((ii) managerial remuneration under section 198 of the Act paid or payable) managerial remuneration under section 198 of the Act paid or payableduring the financial year to the directors (including managing directors),during the financial year to the directors (including managing directors),managermanager, if any, if any;;

((vi) other allowances and commission including guarantee commission (detailsvi) other allowances and commission including guarantee commission (detailsto be given)];to be given)];

2727

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 28/35

(vii) any other perquisites or benefits in cash or in kind (stating approximate money(vii) any other perquisites or benefits in cash or in kind (stating approximate moneyvalue where practicable);value where practicable);

(viii) pensions, etc.,(viii) pensions, etc.,- -

(a) pensions,(a) pensions,(b) gratuities,(b) gratuities,(c) payments from provident funds,(c) payments from provident funds,(d) compensation for loss of office,(d) compensation for loss of office,(e) consideration in connection with retirement from office.(e) consideration in connection with retirement from office.

4A. The profit and loss account shall contain or give by way of a note a statement 4A. The profit and loss account shall contain or give by way of a note a statement showing the computation of net profits in accordance with section 349 of the Act showing the computation of net profits in accordance with section 349 of the Act . .

4B. The profit and loss account shall further contain or give by way of a note detailed4B. The profit and loss account shall further contain or give by way of a note detailedinformation in regard to amounts paid to the auditor,information in regard to amounts paid to the auditor, [ [whether as fees, expenses orwhether as fees, expenses orotherwise for servicesotherwise for services renderedrendered- -(a) as auditor;(a) as auditor;

((b) as adviser, or in any other capacity, in respect of b) as adviser, or in any other capacity, in respect of- -((ii) taxation matters) taxation matters; ;(ii) company law matters(ii) company law matters; ;(iii) management services; and(iii) management services; and(c) in any other manner].](c) in any other manner].]

2828

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 29/35

[[4C. In the case of a manufacturing companies, the profit and loss account 4C. In the case of a manufacturing companies, the profit and loss account shall also contain, by way of a note in respect of each class of goodsshall also contain, by way of a note in respect of each class of goodsmanufactured, detailed quantitative information in regard to the following,manufactured, detailed quantitative information in regard to the following,namely:namely:--(a) the licensed capacity (where(a) the licensed capacity (where licencelicence is in force);is in force);

((b) the installed capacity; andb) the installed capacity; and

((c) the actual production.c) the actual production.

4D4D. The profit and loss account shall also contain by way of a note the. The profit and loss account shall also contain by way of a note thefollowing information, namely:following information, namely:- -(a) value of imports calculated on C.I.F. basis by the company during the(a) value of imports calculated on C.I.F. basis by the company during thefinancial year in respect of:financial year in respect of:- -((ii) raw materials;) raw materials;

(ii) components and spare parts;(ii) components and spare parts;

(iii) capital goods;(iii) capital goods;

2929

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 30/35

(b) expenditure in foreign currency during the financial year on account of (b) expenditure in foreign currency during the financial year on account of royalty, knowroyalty, know- -how, professional, consultation fees, interest, and otherhow, professional, consultation fees, interest, and othermatters;matters;

(c) value of all imported raw materials, spare parts and components(c) value of all imported raw materials, spare parts and componentsconsumed during the financial year and the value of all indigenous rawconsumed during the financial year and the value of all indigenous rawmaterials, spare parts and components similarly consumed and thematerials, spare parts and components similarly consumed and thepercentage of each to the total consumption;percentage of each to the total consumption;

(d) the amount remitted during the year in foreign currencies on account of (d) the amount remitted during the year in foreign currencies on account of dividends, with a specific mention of the number of nondividends, with a specific mention of the number of non- -resident resident shareholders, the number of shares held by them on which the dividendsshareholders, the number of shares held by them on which the dividendsrelated;related;

(e) earnings in foreign exchange classified under the following heads,(e) earnings in foreign exchange classified under the following heads,namely:namely:--((ii) export of goods calculated on F.O.B. basis;) export of goods calculated on F.O.B. basis;(ii) royalty, know(ii) royalty, know- -how, professional and consultation fees;how, professional and consultation fees;(iii) interest and dividend;(iii) interest and dividend;(iv) other income, indicating the nature thereof.](iv) other income, indicating the nature thereof.]

3030

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 31/35

3131

PART III P.NO. 84PART III P.NO. 84InterpretationInterpretation

PART IVPART IVBalance Sheet Abstract and Company's GeneralBalance Sheet Abstract and Company's General

Business ProfileBusiness Profile

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 32/35

3232

SO LUTIONSSO LUTIONSRequirements as to Part IV p.no. 84

A.Company registration details

a.Registration No.b.State Codec.Balance sheet date

B.Capital Raised during the yeara.Public issueb.Rights issuec.Bonus issued.Private placement

C.Details of mobilization and deployment of funds (amountsin Rs. Thousands)

a.Total Liabilitiesb.Total Assets

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 33/35

Some brain exerciseSome brain exercise

33333333

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 34/35

3434

Please feel free to contact us on atPlease feel free to contact us on atSUMAT foundation: bySUMAT foundation: by SUMAT SINGHALSUMAT SINGHAL

+8103620466+8103620466

POWERED BY :POWERED BY : sumatsumat foundationfoundation

Thank you for attending

8/7/2019 22_schedule_vi

http://slidepdf.com/reader/full/22schedulevi 35/35

3535