2018 Business Apps Report - documents.chitra.live

11

Business Applications Reseller Report

Transcript of 2018 Business Apps Report - documents.chitra.live

Business Applications Reseller Report

BUSINESS APPLICATIONS RESELLER REPORT

below the 3.9 per cent of the wider Top 250. They are also below the average margins posted by the 20 specialist print VARs (5.8 per cent) and 35 comms VARs (3.9 per cent) covered in CRN Essential’s mini-reports, but higher than those clocked up by the 20 audiovisual (3.4 per cent) and 13 cybersecurity specialists (2.6 per cent) examined.

Despite this, some of the firms featured in this report are among the most profitable in the entire Top 250, with seven of the 30 posting double-digit operating profit margins in their most recent financial years. One, SAP partner Edenhouse, boasts profit margins verging on an impressive 25 per cent.

Laser focusBringing together solutions from multiple vendors is seen by some as a hallmark of VARs, resellers and other forms of channel firms.

However, many ERP, CRM, BI or CAD specialists diverge from this rule by focusing on a single vendor.

Among the 30 firms profiled, six have a clear focus on SAP, six on Microsoft Dynamics, four on Oracle, four on Autodesk and one on Sage. Arguably, a single-vendor approach has become even more necessary for many boutique software VARs in recent years due to the accelerated speed of change in technology brought about by cloud (see interview with QUANTIQ’s Stuart Fenton, p6).

These are highly specialised firms that are more people-intensive than any other flavour of VAR CRN Essential has examined this year. Many also double up as ISVs. The average revenue generated per employee across the 30 stands at £180,000, compared with £412,000 for the wider Top 250.

Collectively, the top 30 had an average of 4,817 staff in their last financial years, a net rise of 174 on the previous year.

Wages (see p10) are also generally higher than the wider Top 250, with figures harvested from their last annual accounts showing the average (mean) wage rising by 2.3 per cent year on year to £53,853.

‘Short-term pain for long-term gain’ is the bargain many of the firms featured in our inaugural Business Applications Reseller Report struck in their last financial years.

This study – the last of five sector-specific reports from CRN Essential in 2018 – profiles 30 boutique VARs and consultancies with a laser focus on business software including ERP, CRM, business intelligence and CAD. Together they employ nearly 5,000 staff.

For many of them, 2017 was a year of transition as the impact of shifting more business to cloud left a short-term hole in their balance sheets.

Collectively, their revenues rose by a modest six per cent to £676m, while average operating profit margins across the group lurched downwards – from 4.1 to 3.7 per cent.

Despite this, some are among the most profitable in the entire Top 250 UK VARs, with double-digit margins a common sight.

Unlike the wider Top 250, the 30 firms profiled here often practise vendor monogamy, with many focused solely on a single brand such as SAP, Oracle or Autodesk.

They tend to be much more specialised than their Top 250 brethren are, with higher salaries to boot – average wages across the 30 stood at close to £54,000 in their last financial years, compared with £46,140 for the wider Top 250.

Painful transitionUsing CRN’s Top 250 resellers as a starting point, we were able to identify 30 boutique resellers and consultancies focused primarily on business applications, whether that be ERP, CRM, business intelligence, SCM software, CAD or other niches. Despite seeing collective revenues rise by six per cent to £676.2m, many of the 30 endured mixed years as they and their key vendors embarked on the often painful transition to the cloud.

Those that have built practices around Autodesk have been particularly badly hit by the vendor’s decision to switch lock, stock to a subscription model, with the CAD vendor’s largest UK partner – Excitech – suffering a contraction in both sales and profits. However, rival Graitech – whose last set of financial results cover a more recent period – claimed in its directors’ report that the switchover is having a “positive effect” on its business now it has ported all its customers to the new model (see p5).

eBECS – a Microsoft Dynamics specialist ranked sixth in this report – also admitted its fiscal numbers were dented by customers migrating from traditional on-premise software to SaaS contracts where revenue is recognised on a monthly basis. Like many others in this report, eBECS is, however, betting on SaaS to boost its business in the long term.

“This change, although affecting the business in the short term, is beneficial both to eBECS and the industry as it increases certainty of cashflows and requires customers to be properly serviced by its chosen partner,” its directors’ report stated.

The pain of this cloudy transition was written across the most recent financial results of many of the 30. Average (mean) operating profit margins fell from 4.1 to 3.7 year on year, with seven – or 23 per cent – of the 30 making an operating loss. That compares with just 11 per cent of the wider Top 250 UK resellers who made an operating loss.

Average operating profit margins are also a shade

2

Business Applications Reseller Report

0

3

6

9

12

15

Print Audiovisual Comms Cybersecurity Wider top 250

15

12

9

6

3

0%

Average VAR operating profit margins and growth by niche

Operating profit marginGrowth

Business applications

3

BUSINESS APPLICATIONS RESELLER REPORT

After a year to forget, this retail-focused Microsoft Dynamics and Sage partner appears to be getting back on track under new chief executive Adalsteinn Valdimarsson.

Its interim results for the six months ending 31 March 2018 showed a significant improvement in underlying profitability, with revenues also rebounding by three per cent to £40.3m following efforts to restructure and refocus.

London-listed K3 is placing an increased emphasis on its own intellectual property, which now generates about a fifth of revenue. This includes its flagship product, Imagine IP, a cloud-native delivery platform that is embedded with software from Microsoft.

Its last annual results, covering an elongated 17-month period ending on 30 November 2017, showed an eye-watering £14.8m operating loss on revenues that fell six per cent to £118m in the 17 months to 30 November 2017.

With revenues approaching €900m and 7,000 employees, Germany-based Itelligence is one of SAP’s largest partners globally. Its UK arm hit £65.7m revenues in its year to 31 December 2017, a 10 per cent rise, with cloud and hosting sales almost doubling to £6m. UK operating profits inched up from £5.1m to £5.2m. Offering a range of services including consulting, managed services and training, NTT Data-owned Itelligence claims it leads the way in new SAP technologies, including S/4HANA digital core.

Billing itself as the UK’s largest independent SAP consultancy, Edenhouse has nearly doubled in size in the last two years, with revenues for its year to 31 March 2017 hiking an impressive 30 per cent. Operating profits of £9.5m also make it the most

Revenue: £83.4m (pro rata)Operating loss: £10.4m (pro rata)Operating profit margin: -12.5%

1 K3 Business Technology it blamed partly on the short-term pain associated with the industry shift from on-premise to SaaS.

Demand for Dynamics remained strong during the year, eBECS said, although it claimed that delays to the launch of Dynamics 365 hit its sales. It draws 13 per cent of sales from Saudi Arabia, where it claims to be Microsoft’s largest partner.

A string of acquisitions on this side of the Irish Sea have super-charged this Dublin-based Oracle, Microsoft and AWS’ UK business. Despite it having entered the UK only in 2013, Version 1’s sales from this country hit £33.5m in calendar 2017 – a 51 per cent hike – with operating profits rising at a similar rate to £2.25m.

Backed by Volpi Capital, Version 1 enlisted its 1,000th member of staff in March 2018. In June it added another 80 workers when it acquired London-based Oracle HCM specialist Cedar Consulting – its sixth UK purchase in quick succession. The firm’s group revenue run rate currently stands at around €120m.

Owned by Sage founder Graham Wylie, this Microsoft, Sage, Pegasus and Qlik Sense partner blamed a revenue rollback of five per cent in its year to 31 March 2017 on the shift to customers consuming software on a subscription basis. But a decision to focus more on recurring revenues – which now stand at 66.3 per cent of the total – propelled the firm into the black after two years of losses. TSG continues to push into developing its own IP, investing £672,000 into its Tribe and Traveller products during the year.

It’s now a misnomer to refer to this Oracle partner as ‘Red Stack’, the Chelmsford-based firm’s brand having now been fully subsumed by US owner

profitable firm in this report. During the year Edenhouse claims that it made a “significant investment” in SAP’s Digital Suite, S/4HANA and in its cloud capabilities.

The UK arm of this Oracle, SAP and Salesforce partner, which is headquartered in Pune, India, bagged eight new orders in its last fiscal year, including a seven-year deal with an unnamed bank. Revenues for its year to 31 March 2017 bounced 20 per cent to £36.6m, with operating profit following suit, pogoing from £3.3m to £5.7m. During the year it acquired London-based experience design company Foolproof.

Headquartered in the UK’s tallest building, The Shard, this SAP Business One and Infor Sunsystems specialist has lofty international ambitions to match, acquiring an Argentinian software developer and opening offices in the Philippines and Mexico in its last financial year.

Sapphire’s latest numbers covered a nine-month period ending 31 December 2017 following a change to its year end. Annualised, revenues rose 14 per cent to £35.7m, with operating profits vaulting from £2.6m to £3.6m. Although its US and rest-of-world sales grew 46 and 32 per cent, respectively, the UK still generates nearly two thirds of the total.

This Chesterfield-based Microsoft Dynamics partner branded its fiscal 2017 ending 31 March 2017 a “challenging year”, claiming “considerable management time” was invested into forming its strategic partnership with global services giant CSC. The association was a prelude to eBECS’ acquisition by CSC – or DXC Technology as it is now known – in its entirety in April 2018. Revenue growth slowed from 17 to six per cent, which

Revenue: £65.7mOperating profit: £5.2mOperating margin: 8.1%

2 Itelligence

Revenue: £39.5mOperating profit: £9.5mOperating margin: 24%

3 Edenhouse Solutions

Revenue: £36.6mOperating profit: £5.7m

Operating margin: 15.6%

4 Zensar Technologies

Revenue: £35.7m (pro rata)Operating profit: £3.6m (pro rata)

Operating margin: 10.1%

5 Sapphire Systems

Revenue: £34.8mOperating loss: £415,000Operating margin: -1.2%

6 eBECS

Revenue: £33.5mOperating profit: £2.3mOperating margin: 6.7%

7 Version 1

Revenue: £32.8mOperating profit: £32,000Operating margin: 0.1%

8 TSG

Revenue: £32.3mOperating profit: £1.3mOperating margin: 3.9%

9 Red Stack Tech

BUSINESS APPLICATIONS RESELLER REPORT

4

Oracle of wisdomIan Thomason, chief executive of £10m-revenue Oracle partner Explorer UK, gives an overview of life in Big Red’s channel

You specialise in Oracle (specifically Oracle’s Core Technology software products, Engineered Systems and Oracle Cloud for PaaS and IaaS). What are the advantages – and drawbacks – of having a single-vendor focus, and do you ever see this changing?Although Explorer is now single vendor, we were previously multi-vendor. Four years ago, we saw a change coming in the Oracle partner landscape and having already put almost 20 years into building an Oracle practice, we took the decision to go all in. It’s obvious to see there are only two main choices in the IT channel landscape. Either do everything a customer wants (single source of supply with no in-depth knowledge) or become specialised deep and wide in a single vendor.

The only disadvantage I can see is if Oracle stops producing new products and new versions of existing products that are innovative and/or market driven. I just can’t see this happening. In all the years I’ve known Oracle, they’ve either built or bought best-of-breed in all areas. What’s the mega-trend defining 2018 for Oracle partners like Explorer?Oracle licence compliance has always been a concern for most Oracle customers but it’s now increasing since Oracle has used it to get customers to invest in Oracle Cloud. Oracle License Management Services

(LMS) is only increasing the number of audits it does with customers. The only way to mitigate this risk is to do a SAM assessment and architecture review with an authorative specialist Oracle Partner, like Explorer. If a customer leaves this until Oracle LMS drops them a letter, it’s probably too late. You’ve just started your fiscal 2019. In terms of the KPIs and goals you’re focused on, what would a successful year look like?For fiscal 2018, ending in August, we reached the £10m-turnover milestone. We maintained profit, less the amount we are re-investing. For fiscal 2019, we want more of the same, increasing the number of customers and partners for our services and at the same time providing the same high level of services to our existing and very loyal customer base.

We are going though IS0 27001 accreditation and looking to implement an increasing number of new and unique offerings with strong marketing investment to get the message out. As an Oracle-specialised partner, how closely do your fortunes mirror those of Oracle, and what is the best way to maximise returns in the Oracle channel right now?Oracle is going through a difficult period of change at the moment and trying to convert every customer on-premise to the Oracle Cloud. We have never taken this stance and do not believe it is the correct approach. Oracle Cloud might be relatively new, but hosting and managed datacentres have been around for years.

At Explorer, we always put the customer first, in terms of what they want from their Oracle environments for their business, today and in the future, in line with their plans.

What keeps you awake at night?Recruitment! We need to ensure we keep high levels of service for our customers, as well as the partners that use our services. We are only able to do this with the stellar staff that we have. This comes by investing in people and their skills as well as providing them with great opportunities to be proud of what they do for our customers. We recruit from the UK and the EU. The lack of clarity on Brexit is a constant bugbear. Many resellers and consultancies in this report referenced the move they and their vendor partners are making to cloud and SaaS. In the long term, will the shift to cloud have a margin-enriching, or margin-sapping effect for you and your peers?

BUSINESS APPLICATIONS RESELLER REPORT

5

Revenue: £26m (pro rata)Operating profit: £45,000 (pro rata)

Operating margin: 0.2%

10 Excitech

In our experience, Oracle Cloud is not a threat to our business; it enhances it. If customers asked us about hosting before, we’d have to construct something with a hosting company and the customer would need to buy the Oracle Term licences required. Oracle Cloud makes it much easier with Universal Credits that can be used for many cloud services, not just the database, without the need to buy any Oracle licences. They can start with a small investment and “pay as they grow”.

With these customers, there is just a shift in the deal. Instead of making margin from on-premise licences, there is a small margin for Oracle Cloud Credits. This will hurt a product-only Oracle partner, but as we provide all the consulting and development services to migrate an existing application or build a new

application (with APEX) in the Oracle Cloud, then we are making more on services so for us it balances out and it is the reason why our services business is growing so quickly.

Who do you consider as your closest competitors?Our single biggest competitor is Oracle itself, especially when it gets a new sales rep who does not realise or understand all the work a specialist Oracle-only partner like Explorer puts in and then decides to approach our customer directly. Fortunately, we are seasoned and wise enough to counter this with our Oracle exec relationships who do know the true value of Explorer to the business.

Data Intensity, which acquired it for $13.9m in September 2016. However, to simplify things, we’re sticking with the status quo until Data Intensity’s 2017 results are published. In its year to 31 December 2016, Red Stack’s operating profits rolled back from £1.9m to £1.3m on revenues that swelled 15 per cent.

Autodesk’s largest UK Platinum partner was still feeling short-term pain from the CAD vendor’s shift to a subscription model at the time it reported its shortened eight-month year ending 31 January 2017. Revenues hit £17.4m, down 17 per cent on a pro-rated basis. Operating profits also thinned from £2.1m to £30,000. In June 2017 Enfield-based Excitech acquired another CAD reseller, CABS, boosting its Autodesk subscriber base by 10 per cent.

Unlike Excitech, this Southampton-based CAD specialist claimed in its latest annual results, covering the 12 months ending 31 December 2017, that it has successfully transitioned to Autodesk’s new subscription-based model, with all its revenues and 60 per cent of its customers successfully moved. “We see this as having a positive effect on the business, with more predictable revenue from existing customers and an easier entry point for new customers,” Graitech’s directors’

Datel claims it consolidated its position as Sage’s largest UK business partner when it acquired fellow Warrington-based business Ensphere Consulting in June 2018. Counting Flybe and Vimto manufacturer Nichols plc among its clients, Datel saw revenue inch up one per cent to £20.3m in its year to 31 May 2017. Operating profit fell slightly to £876,000. The 178-strong firm said it invested in headcount around implementing Sage X3 and in its R&D team during the year.

With 2,000 staff globally and 8,600 ERP implementations under its belt, this Danish firm is a giant of the Microsoft Dynamics channel. Its UK arm – whose MD, Mary Hunter, won a Women in Technology Leadership award at Microsoft Inspire 2018 – posted a slight dip in revenues and profits in its year to 31 December 2017. Fiscal 2018 numbers will be bolstered by the recent acquisition of £5m-revenue Dynamics 365 specialist Cambridge Online Systems, however.

This SAP Gold partner highlights the success of a cricket team it founded with

report said. It also flagged a “contraction in the number of competitors in the Autodesk space”, claiming “only the largest partners will survive”, as full-year revenues and operating profits vaulted 12 and 33 per cent respectively.

The most recent annual results of the last of three £20m-revenue Autodesk Platinum partners featured in this report also bore the hallmarks of the CAD vendor’s transition to a subscription model. Cadline’s operating profits for the year to 31 March 2017 nose-dived from £1.2m to £197,000, while revenues fell two per cent. But the Middlesex-based firm, which also has offices in Gatwick, Cambridge, Manchester, Leeds and Birmingham, maintained that the switch would “benefit business in the long term”.

Inoapps started life in 2006 when founder Andy Bird identified a gap in the market for Oracle applications for the oil and gas industry. Today, it is Oracle’s reigning Cloud-First partner of the year, with 175 staff and offices in Aberdeen, Edinburgh, London, Derby, the USA, Malaysia and Singapore. For its year to 31 July 2017, revenues fell five per cent. Operating losses widened to £1.1m, which it blamed on a £407,000 bad debt and costs associated with overseas expansion.

Revenue: £25mOperating profit: £736,000

Operating margin: 2.9%

11 Graitec

Revenue: £24.4mOperating profit: £197,000

Operating margin: 0.8%

12 CADline

Revenue: £18.7mOperating profit: £3.4m

Operating margin: 18.2%

15 Columbus

Revenue: £20.3mOperating loss: £876,000Operating margin: -4.3%

14 Datel

Revenue: £22mOperating loss: £1.1m

Operating margin: -5.1%

13 Inoapps

Revenue: £16.9mOperating profit: £1.9m

Operating margin: 11.1%

16 Invenio Business Solutions

6

BUSINESS APPLICATIONS RESELLER REPORT

A Dynamic perspectiveStuart Fenton, chief executive of QUANTIQ, opens up on the pros and cons of being a Microsoft Dynamics-specialist partner

What’s the mega-trend defining 2018 for Microsoft Dynamics partners like QUANTIQ?The most significant trend as a partner is the amazing pace of development coming from Microsoft within the Business Applications division. Microsoft is adding new elements, updating features and improving platforms faster than ever. Once clients are on the platforms, they can enjoy modern, mobile business applications that will serve them well into the future. As a Dynamics partner, we have to move at least as fast as Microsoft to ensure our clients enjoy the technology trends as they happen.

At the time you acquired Profile Enterprise Solutions’ Dynamics business in August, you argued that smaller Dynamics partners are struggling to keep up with the pace of innovation within the Dynamics product set. What kind of scale do you need to be successful as a Dynamics partner, and is QUANTIQ itself large enough to survive in the long term?Dynamics is a broad area. Partners that focus on perhaps Business Central or just Customer Engagement (CRM) can probably survive with 25 people or so. However, Dynamics 365 is a very different offering and requires extraordinary depth

and breadth of skills across technologies and functional areas. In addition, each member of the team needs time to learn new technologies and practise with them too. Partners with fewer than 100 experienced staff will struggle to remain on top of the new innovations while providing professional services and ongoing managed services to the clients.

QUANTIQ now has 180 staff including our offshore development team and therefore we are the right size to support mid-sized to large clients. However, we need to continue growth during 2018 to get over 200 heads just to service the business that we have won. I certainly see us reaching 350 heads in the near future.

Which KPIs do you focus on and what would a successful 2018 look like for your business?Service businesses such as ours will have hundreds of metrics but success for us is ultimately profitable growth through happy, engaged staff; more clients and higher client satisfaction levels.

Could you give us an idea of how QUANTIQ’s revenue mix is changing in regards to on-premise versus cloud, and what impact you expect the shift to recurring revenues to have on your profitability long term? Is there short-term pain involved in that transition?One hundred per cent of our growth has come from cloud-based projects and it represents over 100 per cent of our new business. Many of our existing clients use on-premise solutions but will upgrade over the coming years. Three years ago, our business was 90 per cent on-premise. We are now circa 70 per cent cloud for all our business and we expect this to be above 90 per cent by 2020.

Is the ERP market growing, and where are the biggest growth hotspots?The overall ERP market is growing at around 10 per cent, with some players such as Microsoft far exceeding that, and others struggling. Most industry sectors are seeing growth, but professional services organisations are a particular hot-spot. From a technology perspective, business intelligence and HCM are driving a great deal of new business across all industry sectors.

You specialise in Microsoft Dynamics. What are the advantages – and drawbacks – of having a single-vendor focus, and do you ever see this changing?To be successful, we believe that a 100 per cent focus on being the best in Dynamics outweighs the risks of a single-vendor focus. I see competitors that

7

BUSINESS APPLICATIONS RESELLER REPORT

This Poole-based SAP partner claims it was the first to take SAP Business One to market after its launch in 2003, the first to achieve SAP Gold status, and one of only two Master SAP VARs. It also partners with Citrix, VMware and Microsoft. Revenues for its year to 30 September 2017 rose by six per cent to £11.2m, but operating profits fell slightly to £454,000.

This Stockport-based business intelligence specialist’s “aggressive pursuits” in the public sector helped fuel a 10 per cent hike in revenues for its year to 31 March 2018. Despite this, it logged an operating loss of £537,000. Owned by Indian company Saksoft, Acuma bills itself as a digital transformation specialist, partnering with the likes of SAP, Birst, Jaspersoft, Microsoft, LogiAnalytics, SAS, Talend and Tibco Spotfire.

An arm of €160m-revenue German CAD giant Mensch und Maschine Group, this Oxfordshire-based Autodesk partner said it continued to offer a wider set of software solutions from multiple vendors in its year to 31 December 2016. Revenues rose 12 per cent to £8.5m, with operating losses narrowing from £517,000 to £383,000. Offering its own Mensch und Maschine Group products and providing customised software solutions to its clients is also part of the gameplan.

Dynamics business of Profile Enterprise Solutions this August, chief executive Stuart Fenton claimed that smaller Dynamics partners are struggling to keep up with the rising pace of change in the product set (go to p6 to read our interview with Fenton).

This London- and Stockport-based Microsoft Dynamics 365 and GP specialist counts charities Oxfam and Solent Mind among its customers. Revenues for its year to 31 December 2016 dropped 10 per cent, which it said reflected its transition to recurring, cloud-based revenues, together with the disposal of its small Sage business unit in June 2016. Operating losses narrowed from £1.1m to £750,000.

Despite grumbling about “challenging” economic conditions, this CAD consultancy posted top-line and bottom-line growth in its year to 31 December 2016, with sales shooting up 29 per cent and operating profits trebling to £262,000. The firm partners with Autodesk and Dassault Systemes, selling to clients in the manufacturing, construction and automotive industries.

one of its marquee clients, Universal Music Group, on the Key Facts section of its website. Revenues in its year to 31 March 2017 rose 32 per cent to £16.9m, with £5.3m of the total coming from abroad. Despite operating profits doubling to £1.8m, Reading-based Invenio ploughed the entire return back into its business, rather than declaring a dividend.

This Microsoft partner, whose focus areas include Dynamics and Sharepoint, was hit by a bad debt of £296,000 stemming from the collapse of a retail client in its most recent, elongated, financial year, which covered the 18 months to 31 October 2017. On a pro-rated basis, revenues fell 14 per cent, with operating profit dropping by around three quarters. In October 2017 it acquired Just Computing, a move the West Sussex-based outfit said would allow its customers to choose between the Microsoft cloud stack and private cloud.

With 185 employees and 950 deployments under its belt, QUANTIQ is one of Microsoft’s top UK ERP and CRM partners. The London-based firm posted an operating loss of £471,000 on revenues that rose 13 per cent in its year to 31 December 2017 (although its net profits hit a healthy £704,000).

Talking to CRN at the time that QUANTIQ acquired the 40-person

try to do what we do with multiple vendors and are simply average in each practice. Focused firms like ours provide clients with the greatest likelihood of outstanding outcomes. Naturally, any relationship can have its ups and downs, but having worked with Microsoft since 1990, I am confident of its commitment to the channel, channel health and the Dynamics technology.

I can’t see us adding additional vendors to the business without diluting our focus. The only possibility would be to add an entirely new, but separate business to the group – but I don’t really want to.

What is the biggest challenge facing your business today?Recruiting great people with talent, energy, resilience and passion. I’m a big believer in the Success formula by Angela Duckworth: Talent x Effort = Skills. Skills x Effort = Success.

Talent alone is not enough – it’s people who are passionate about themselves and their clients and are willing to break moulds. We recruit through a number of routes, but we are very picky. Many people we reject end up at competitors. We just don’t want mediocre people with the wrong focus or behaviour.

Revenue: £16.7m (pro rata)Operating profit: £165,000 (pro rata)

Operating margin: 1%

17 Acora

Revenue: £15.7mOperating loss: £471,000

Operating margin: -3%

18 QUANTIQ

Revenue: £12.6mOperating loss: £763,000Operating margin: -6.1%

19 m-hance

Revenue: £12.1mOperating profit: £262,000

Operating margin: 2.2%

20 Majenta Solutions

Revenue: £11.2mOperating profit: £454,000

Operating margin: 4%

21 Codestone Group

Revenue: £10.5mOperating loss: £537,000Operating margin: -5.1%

22 Acuma Solutions

Revenue: £8.5mOperating loss: £383,000Operating margin: -4.5%

23 Man and Machine

Centiq claims to have deployed SAP HANA for over 50 organisations. It admitted its fiscal 2018 ending 31 March was “a year of transition and development” as it posted an operating loss of £1.1m on revenues that fell 24 per cent to £6m. Major shareholder Lloyds Development Capital has been “very supportive”, providing additional investment in October 2017 to help fund the restructuring activity as Centiq pushes into cloud.

This SAP Silver partner claims to be seeing the fruits of a recent restructuring drive after returning to profit in its year to 30 April 2017. But revenue for the period fell nine per cent, unaudited figures show. Based in Aberdeen, Absoft showcases numerous oil and gas references on its website, but stressed that its “previous dependence in any one sector has significantly been reduced”. It has built an ERP solution, Absoft Adima, tailored to SME manufacturers.

Despite turning 30 this year, this Netsuite and Microsoft Dynamics partner is to this day run by its founder, Tim Nolan. In its year to 30 June 2017, Nolan saw revenues swell nine per cent. Operating profits thinned from £264,000 to £224,000 as it complained of increased staff costs. The Fleet-based firm, which also has offices in Edinburgh, Birmingham, Colorado and Sydney, claims to have more than 15 custom-developed applications.

Global Microsoft Dynamics partner SAGlobal bolstered its UK business last year when it acquired Cardiff-based M4 Systems. Although SAGlobal told us at the time the move created a £7m player in the UK, as it doesn’t report UK numbers we’ve used M4’s last set of accounts – for its year to 31 December 2016 – to form the basis of this profile. Globally SAGlobal has 600 staff.

This SAP Business One and Sage X3 consultancy was founded by its CEO and chairman, Bill Milligan, in 1991. Today it employs nearly 100 staff, turning over £8.2m in its year to 31 December 2016, a two per cent annual decline. Operating profits for the year stood at £483,000, up from £341,000 in 2015. Its head office and primary datacentre is in Cheshire.

Explorer UK claims it is the only remaining independent, single-vendor Oracle partner for its Core Technology, engineered systems and Oracle cloud. Managing director Ian Thomason told us it is gearing up to double the size of its Leeds headquarters as it continues to reinvest its profits back into the business. Revenues and operating profits for its shortened, 11-month year to 31 August 2017 fell a respective 13 per cent and 24 per cent on a pro-rated basis, according to numbers Explorer shared with us (see interview with Ian Thomason on p4).

Incremental Group claimed that its June 2018 acquisition of CRM specialist Gap Consulting makes it one of the largest Microsoft Dynamics partners in the UK, with 125 staff. This follows on from its purchase of eBusiness in 2016. Accounts for its year to 31 March 2018 show revenue vaulting 60 per cent to £6.6m and operating profits trebling to £690,000. Despite having only been born in 2015, Incremental Group now boasts offices in Glasgow, Aberdeen, Cheshire, Manchester and London.

Counting M&S, Unilever and Prudential among its clients, Nottingham-based

BUSINESS APPLICATIONS RESELLER REPORT

8

Revenue: £8.2mOperating profit: £483,000

Operating margin: 5.9%

24 Frontline Consultancy

Revenue: £8m (pro rata)Operating profit: £791,000 (pro rata)

Operating margin: 9.8%

25 Explorer UK

Revenue: £6.6mOperating profit: £690,000Operating margin: 10.5%

26 Incremental Group

Revenue: £6mOperating loss: £1.1m

Operating margin: -19.1%

27 Centiq

Revenue: £5.2mOperating profit: £191,000

Operating margin: 3.7%

28 Absoft

Revenue: £4.1mOperating profit: £224,000

Operating margin: 5.5%

29 Nolan Business Solutions

Revenue: £3mOperating profit: £521,000Operating margin: 17.3%

30 M4 Systems

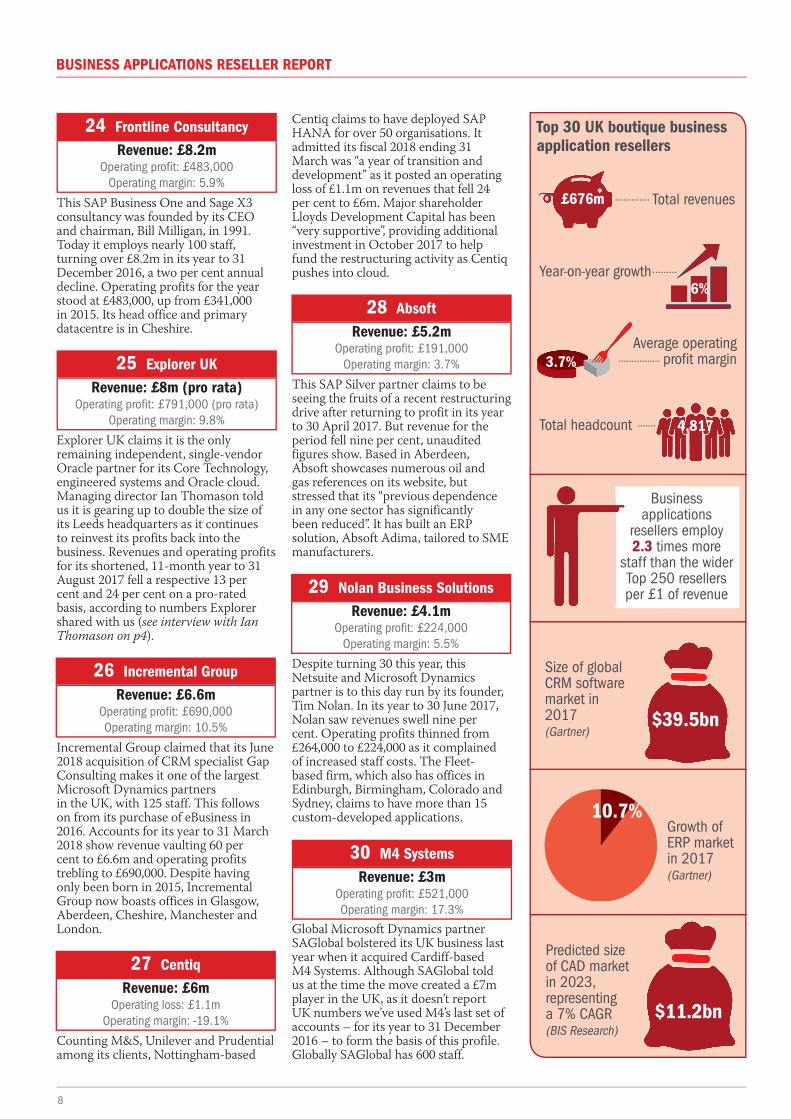

$39.5bn

$11.2bn

Business applications

resellers employ 2.3 times more

staff than the wider Top 250 resellers per £1 of revenue

Size of global CRM software market in 2017 (Gartner)

Predicted size of CAD market in 2023, representing a 7% CAGR (BIS Research)

Growth of ERP market in 2017 (Gartner)

10.7%

Top 30 UK boutique business application resellers

Total headcount

Year-on-year growth

Total revenues

Average operating profit margin

4,817

6%

£676m

3.7%

BUSINESS APPLICATIONS RESELLER REPORT

9

Revenue YoY growth Operating profit Operating profit margin

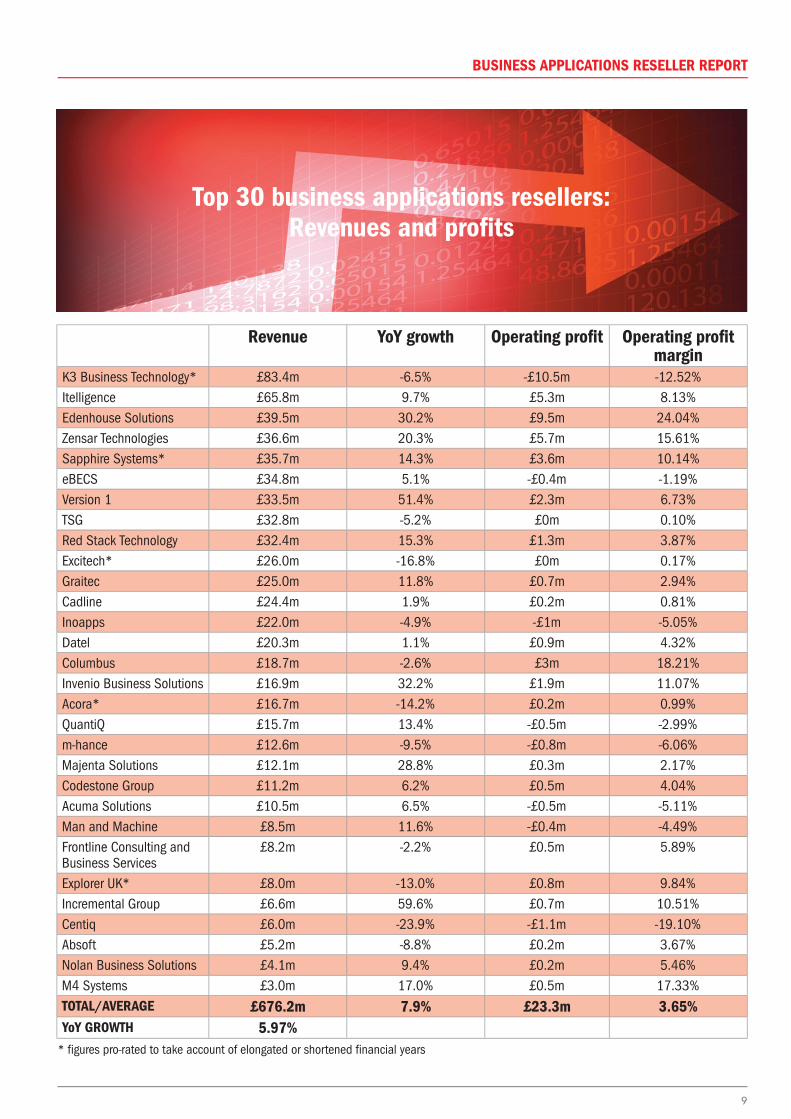

K3 Business Technology* £83.4m -6.5% -£10.5m -12.52%Itelligence £65.8m 9.7% £5.3m 8.13%Edenhouse Solutions £39.5m 30.2% £9.5m 24.04%Zensar Technologies £36.6m 20.3% £5.7m 15.61%Sapphire Systems* £35.7m 14.3% £3.6m 10.14%eBECS £34.8m 5.1% -£0.4m -1.19%Version 1 £33.5m 51.4% £2.3m 6.73%TSG £32.8m -5.2% £0m 0.10%Red Stack Technology £32.4m 15.3% £1.3m 3.87%Excitech* £26.0m -16.8% £0m 0.17%Graitec £25.0m 11.8% £0.7m 2.94%Cadline £24.4m 1.9% £0.2m 0.81%Inoapps £22.0m -4.9% -£1m -5.05%Datel £20.3m 1.1% £0.9m 4.32%Columbus £18.7m -2.6% £3m 18.21%Invenio Business Solutions £16.9m 32.2% £1.9m 11.07%Acora* £16.7m -14.2% £0.2m 0.99%QuantiQ £15.7m 13.4% -£0.5m -2.99%m-hance £12.6m -9.5% -£0.8m -6.06%Majenta Solutions £12.1m 28.8% £0.3m 2.17%Codestone Group £11.2m 6.2% £0.5m 4.04%Acuma Solutions £10.5m 6.5% -£0.5m -5.11%Man and Machine £8.5m 11.6% -£0.4m -4.49%Frontline Consulting and Business Services

£8.2m -2.2% £0.5m 5.89%

Explorer UK* £8.0m -13.0% £0.8m 9.84%Incremental Group £6.6m 59.6% £0.7m 10.51%Centiq £6.0m -23.9% -£1.1m -19.10%Absoft £5.2m -8.8% £0.2m 3.67%Nolan Business Solutions £4.1m 9.4% £0.2m 5.46%M4 Systems £3.0m 17.0% £0.5m 17.33% TOTAL/AVERAGE £676.2m 7.9% £23.3m 3.65%YoY GROWTH 5.97%

Top 30 business applications resellers: Revenues and profits

* figures pro-rated to take account of elongated or shortened financial years

BUSINESS APPLICATIONS RESELLER REPORT

10

Top 30 business application resellers: Headcount and average (mean) wages

Incisive Media, New London House, 172 Drury Lane, London WC2B 5QR Tel: (020) 7484 9000Editor Doug Woodburn 9817 Senior reporter Tom Wright 9797 Reporter Marian McHugh 9883 Content editor Josh Budd 9854 Reporter Nima Green 9781 Senior production editor Amy MicklewrightCommercial director Matt Dalton 9896 Head of global sales Nina Patel 9943

Account director Jessica Feldman 9839 Account manager Jessica Richards 9923 Group publishing director Alan Loader Managing director, Incisive Media Jonathon Whiteley © 2018 Incisive Media

Headcount Previous year Average (mean) salary

Previous year

K3 765 762 £49,130 £47,768 Itelligence 254 225 £78,500 £82,649 Edenhouse Solutions 234 195 £55,897 £55,144 Zensar Technologies 207 195 £49,188 £44,744 Sapphire Systems 231 210 £57,160 £57,329 eBECS 311 297 £55,627 £52,189 Version 1 223 150 £65,457 £64,640 TSG 358 378 £38,547 £37,302 Red Stack Technology 97 100 £66,361 £57,690 Excitech 122 123 £49,586 £46,553 Graitec 77 69 £43,156 £46,391 Cadline 86 81 £51,442 £47,457 Inoapps 175 148 £56,480 £66,358 Datel 178 174 £43,899 £43,385 Columbus 127 127 £59,992 £60,126 Invenio Business Solutions 413 455 N/A N/A Acora 165 185 £42,954 £40,335 QuantiQ 121 105 £74,926 £73,552 m-hance 138 146 £53,435 £49,582 Majenta Solutions 43 37 £53,581 £53,946 Codestone Group 100 99 £52,570 £47,394 Acuma Solutions 16 18 £68,250 £67,000 Man and Machine 27 23 £45,000 £51,696 Frontline Consulting and Business Services

85 90 N/A N/A

Explorer UK 29 25 N/A N/A

Incremental Group 52 34 N/A N/A Centiq 39 46 N/A N/A Absoft 55 62 N/A N/A Nolan Business Solutions 50 48 £45,020 £38,375 M4 Systems 39 36 £36,308 £31,917

TOTAL 4,817 4,643 AVERAGE £54,238 £52,688

Data based on ‘average monthly number of employees’ and ‘wages and salaries’ figures displayed in most-recent accounts