Methodist Healthcare Ministries Medicaid Extension Presentation

Methodist Healthcare Ministries of South Texas, Inc.

Consolidated Financial Statements

December 31, 2014 and 2013

Methodist Healthcare Ministries of South Texas, Inc. Table of Contents Page

Independent Auditor’s Report 1

Consolidated Statements of Financial Position 3

Consolidated Statements of Activities 4

Consolidated Statements of Cash Flows 5

Notes to the Consolidated Financial Statements 6

AUSTIN HOUSTON SAN ANTONIO 811 BARTON SPRINGS ROAD, SUITE 550 1980 POST OAK BOULEVARD, SUITE 1500 100 N.E. LOOP 410, SUITE 1100 TOLL FREE: 800 879 4966

AUSTIN, TEXAS 78704 HOUSTON, TEXAS 77056 SAN ANTONIO, TEXAS 78216 WEB: PADGETT‐CPA.COM

512 476 0717 800 879 4966 210 828 6281

Independent Auditor’s Report To the Board of Directors Methodist Healthcare Ministries of South Texas, Inc. San Antonio, Texas Report on the Financial Statements We have audited the accompanying consolidated financial statements of Methodist Healthcare Ministries of South Texas, Inc. (“MHM”), which comprise the consolidated statements of financial position as of December 31, 2014 and 2013, and the related consolidated statements of activities and cash flows for the years then ended and the related notes to the consolidated financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We did not audit the consolidated financial statements of Methodist Healthcare System of San Antonio, Ltd., LLP, a partnership, and as discussed in Note 1 to the consolidated financial statements, an investment which is accounted for using the equity method of accounting. The investment in Methodist Healthcare System of San Antonio, Ltd., LLP totaled $390,206,237 and $361,043,862 as of December 31, 2014 and 2013, respectively, and the equity in earnings totaled $137,662,375 and $114,815,335, respectively, for the years then ended. The consolidated financial statements of Methodist Healthcare System of San Antonio, Ltd., LLP were audited by other auditors, whose report has been furnished to us, and our opinion, insofar as it relates to the amounts included for MHM, is based solely on the report of the other auditors. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements,

Page 2

whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to MHM’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of MHM’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, based on our audits and the reports of the other auditors, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of Methodist Healthcare Ministries of South Texas, Inc. as of December 31, 2014 and 2013, and the changes in its net assets and its cash flows for the years then ended, in accordance with accounting principles generally accepted in the United States of America.

San Antonio, Texas June 8, 2015

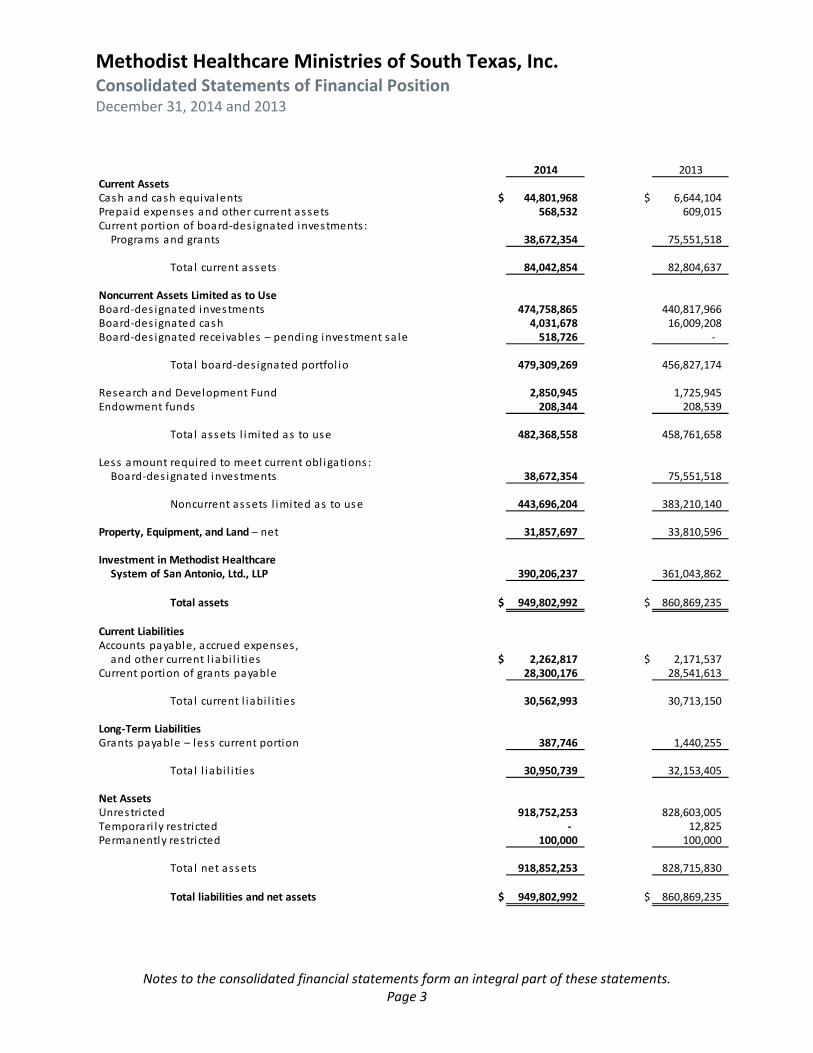

Methodist Healthcare Ministries of South Texas, Inc. Consolidated Statements of Financial Position December 31, 2014 and 2013

Notes to the consolidated financial statements form an integral part of these statements. Page 3

2014 2013Current AssetsCash and cash equiva lents $ 44,801,968 $ 6,644,104Prepaid expenses and other current assets 568,532 609,015Current portion of board‐des ignated investments :Programs and grants 38,672,354 75,551,518

Tota l current assets 84,042,854 82,804,637

Noncurrent Assets Limited as to UseBoard‐des ignated investments 474,758,865 440,817,966Board‐des ignated cash 4,031,678 16,009,208 Board‐des ignated receivables – pending investment sa le 518,726 ‐

Tota l board‐des ignated portfol io 479,309,269 456,827,174

Research and Development Fund 2,850,945 1,725,945Endowment funds 208,344 208,539

Tota l assets l imited as to use 482,368,558 458,761,658

Less amount required to meet current obl igations :Board‐des ignated investments 38,672,354 75,551,518

Noncurrent assets l imited as to use 443,696,204 383,210,140

Property, Equipment, and Land – net 31,857,697 33,810,596

Investment in Methodist Healthcare System of San Antonio, Ltd., LLP 390,206,237 361,043,862

Total assets $ 949,802,992 $ 860,869,235

Current LiabilitiesAccounts payable, accrued expenses , and other current l iabi l i ties $ 2,262,817 $ 2,171,537

Current portion of grants payable 28,300,176 28,541,613

Tota l current l iabi l i ties 30,562,993 30,713,150

Long‐Term LiabilitiesGrants payable – less current portion 387,746 1,440,255

Tota l l iabi l i ties 30,950,739 32,153,405

Net AssetsUnrestricted 918,752,253 828,603,005Temporari ly restricted ‐ 12,825Permanently restricted 100,000 100,000

Tota l net assets 918,852,253 828,715,830

Total liabilities and net assets $ 949,802,992 $ 860,869,235

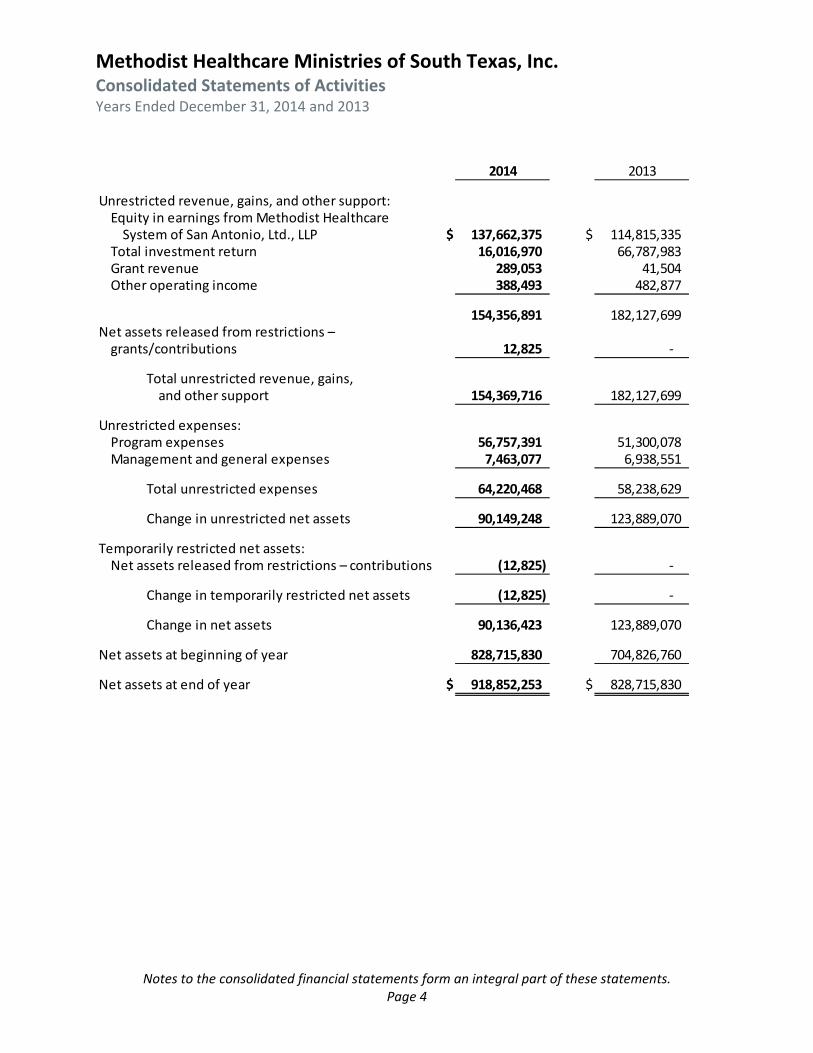

Methodist Healthcare Ministries of South Texas, Inc. Consolidated Statements of Activities Years Ended December 31, 2014 and 2013

Notes to the consolidated financial statements form an integral part of these statements. Page 4

2014 2013

Unrestricted revenue, gains, and other support:Equity in earnings from Methodist HealthcareSystem of San Antonio, Ltd., LLP $ 137,662,375 $ 114,815,335

Total investment return 16,016,970 66,787,983Grant revenue 289,053 41,504Other operating income 388,493 482,877

154,356,891 182,127,699Net assets released from restrictions –grants/contributions 12,825 ‐

Total unrestricted revenue, gains,and other support 154,369,716 182,127,699

Unrestricted expenses:Program expenses 56,757,391 51,300,078Management and general expenses 7,463,077 6,938,551

Total unrestricted expenses 64,220,468 58,238,629

Change in unrestricted net assets 90,149,248 123,889,070

Temporarily restricted net assets:Net assets released from restrictions – contributions (12,825) ‐

Change in temporarily restricted net assets (12,825) ‐

Change in net assets 90,136,423 123,889,070

Net assets at beginning of year 828,715,830 704,826,760

Net assets at end of year $ 918,852,253 $ 828,715,830

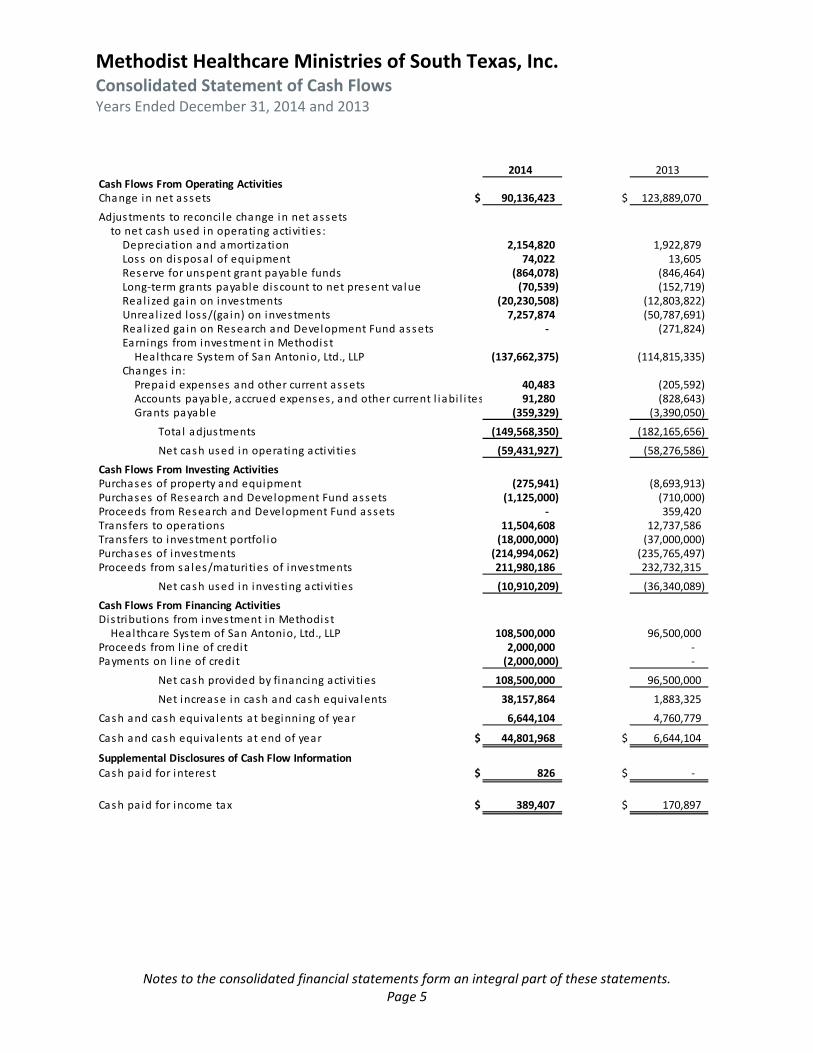

Methodist Healthcare Ministries of South Texas, Inc. Consolidated Statement of Cash Flows Years Ended December 31, 2014 and 2013

Notes to the consolidated financial statements form an integral part of these statements. Page 5

2014 2013Cash Flows From Operating ActivitiesChange in net assets $ 90,136,423 $ 123,889,070

Adjustments to reconci le change in net assets to net cash used in operating activi ties :Depreciation and amortization 2,154,820 1,922,879Loss on disposal of equipment 74,022 13,605Reserve for unspent grant payable funds (864,078) (846,464)Long‐term grants payable discount to net present value (70,539) (152,719)Real i zed gain on investments (20,230,508) (12,803,822)Unrea l ized loss/(ga in) on investments 7,257,874 (50,787,691)Real i zed gain on Research and Development Fund assets ‐ (271,824)Earnings from investment in Methodist Healthcare System of San Antonio, Ltd., LLP (137,662,375) (114,815,335)

Changes in:Prepaid expenses and other current assets 40,483 (205,592)Accounts payable, accrued expenses , and other current l iabi l i tes 91,280 (828,643)Grants payable (359,329) (3,390,050)

Tota l adjustments (149,568,350) (182,165,656)

Net cash used in operating activi ties (59,431,927) (58,276,586)

Cash Flows From Investing ActivitiesPurchases of property and equipment (275,941) (8,693,913)Purchases of Research and Development Fund assets (1,125,000) (710,000)Proceeds from Research and Development Fund assets ‐ 359,420Transfers to operations 11,504,608 12,737,586Transfers to investment portfol io (18,000,000) (37,000,000)Purchases of investments (214,994,062) (235,765,497)Proceeds from sa les/maturi ties of investments 211,980,186 232,732,315

Net cash used in investing activi ties (10,910,209) (36,340,089)

Cash Flows From Financing ActivitiesDistributions from investment in Methodis t Healthcare System of San Antonio, Ltd., LLP 108,500,000 96,500,000

Proceeds from l ine of credi t 2,000,000 ‐ Payments on l ine of credi t (2,000,000) ‐

Net cash provided by financing activi ties 108,500,000 96,500,000

Net increase in cash and cash equiva lents 38,157,864 1,883,325

Cash and cash equiva lents at beginning of year 6,644,104 4,760,779

Cash and cash equiva lents at end of year $ 44,801,968 $ 6,644,104

Supplemental Disclosures of Cash Flow Information

Cash paid for interest $ 826 $ ‐

Cash paid for income tax $ 389,407 $ 170,897

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 6

1. Organization and Significant Accounting Policies Organization Methodist Healthcare Ministries of South Texas, Inc. (“MHM”), a faith‐based, tax‐exempt nonprofit corporation incorporated under the laws of the state of Texas, was originally chartered in 1955 by the Rio Texas Conference (the “Conference”), formerly known as the Southwest Texas Conference of The United Methodist Church. The members of the Board of Directors (the “Board”) are approved annually by the Conference and represent a variety of community leaders, including a number of local United Methodist Church officials. At all times, at least 60% of the Board must be members of The United Methodist Church. MHM was formerly known as Southwest Texas Methodist Hospital (the “Hospital”), a hospital operated for charitable, scientific, educational, and religious purposes. On January 11, 1995, MHM entered into a partnership agreement with Columbia/HCA Healthcare Corporation of Central Texas (“HCA‐Central”), an indirect wholly owned subsidiary of HCA Inc. (HCA Inc. was acquired effective November 17, 2006 by Hercules Holding II, LLC), to form a Texas limited partnership, Methodist Healthcare System of San Antonio, Ltd., LLP (the “Partnership”), to provide healthcare services to San Antonio and the surrounding areas. The Partnership filed a certificate to add the designation of limited liability partnership effective June 5, 2003. HCA Inc. is a holding company whose affiliates own and operate hospitals and related healthcare entities. The Partnership is structured with two general partners, MHM and HCA‐Central, each with a 20% general partnership interest. The two general partners also hold limited partnership interests, with MHM holding 30% and HCA‐Central and other wholly owned subsidiaries of HCA Inc. holding a combined 30%. Each partner, in exchange for its partnership interest, contributed substantially all its hospital‐related assets and liabilities located in the San Antonio area. All distributions shall be in proportion to each partner’s sharing percentage. Under the partnership agreement, as amended, the partners’ sharing percentages for allocation of partnership income or loss were 20% to each general partner and 30% to each limited partner. As a nonprofit corporation, MHM has the responsibility to ensure quality care is available to everyone at Methodist Healthcare System facilities, including those without financial means to pay for hospital services, in accordance with its eligibility policy for charity care. Since MHM owns 50% of the Partnership and appoints 50% of the Partnership’s Board of Governors, including the chair, the investment in the Partnership is accounted for using the equity method of accounting. Under the equity method of accounting, the Partnership’s accounts are not reflected within MHM’s consolidated statements of financial position and consolidated statements of activities; however, MHM’s share of the earnings or losses of the Partnership is reflected in the caption “equity in earnings from Methodist Healthcare System of San Antonio, Ltd., LLP” in the consolidated statements of activities. On April 10, 1996, Wesley Primary Care Clinic (”WPCC”) was originally incorporated as a not‐for‐profit corporation under the Texas Non‐Profit Corporation Act. WPCC is currently certified as a not‐for‐profit health organization under Chapter 177 of the Texas Medical Board Rules and Regulations and Section 162.001(b) of the Texas Occupation Code. MHM is the sole member of WPCC, which was created for the purpose of hiring physicians, dentists, and advanced practice professionals to provide medical and dental services at MHM’s clinics.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 7

WPCC has responsibility for all medical and dental practice issues, including salaries and benefits for physicians, dentists, and advanced practice professionals. All other activities and expenses of WPCC are managed by MHM and are reflected as direct program expenses of MHM. The consolidated financial statements of MHM include the accounts of MHM and WPCC. All significant intercompany accounts and transactions have been eliminated in consolidation. Mission Statement “Serving Humanity to Honor God” To serve by improving the physical, mental, and spiritual health of those least served in the Rio Texas Conference area of The United Methodist Church. Charity Program Spending MHM is committed to nurturing the health and well‐being of the whole individual – physically, mentally, and spiritually. It is also committed to the concept of empowering others – existing agencies, programs, and people – by providing resources so specific needs of the local communities are identified and met. Strict policies of review, selection, and oversight in resource allocation are maintained by the Board and staff of MHM to ensure the greatest results are achieved and existing services are not duplicated, but enhanced. MHM incurred $56,757,391 in 2014 and $51,300,078 in 2013 for program expenses for operating programs and grants, and $275,941 in 2014 and $8,693,913 in 2013 for all capital expenditures, including construction in progress and related to programs to improve individual and family health in South Texas for the least‐served. In an effort to expand services to the underserved in the community served by Wesley Health & Wellness Center (“WHWC”), the Board approved an expansion of the WHWC building and the construction of a new Child Care Center building (to be operated by another entity) on the property. The total cost of the project was approximately $11,846,000.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 8

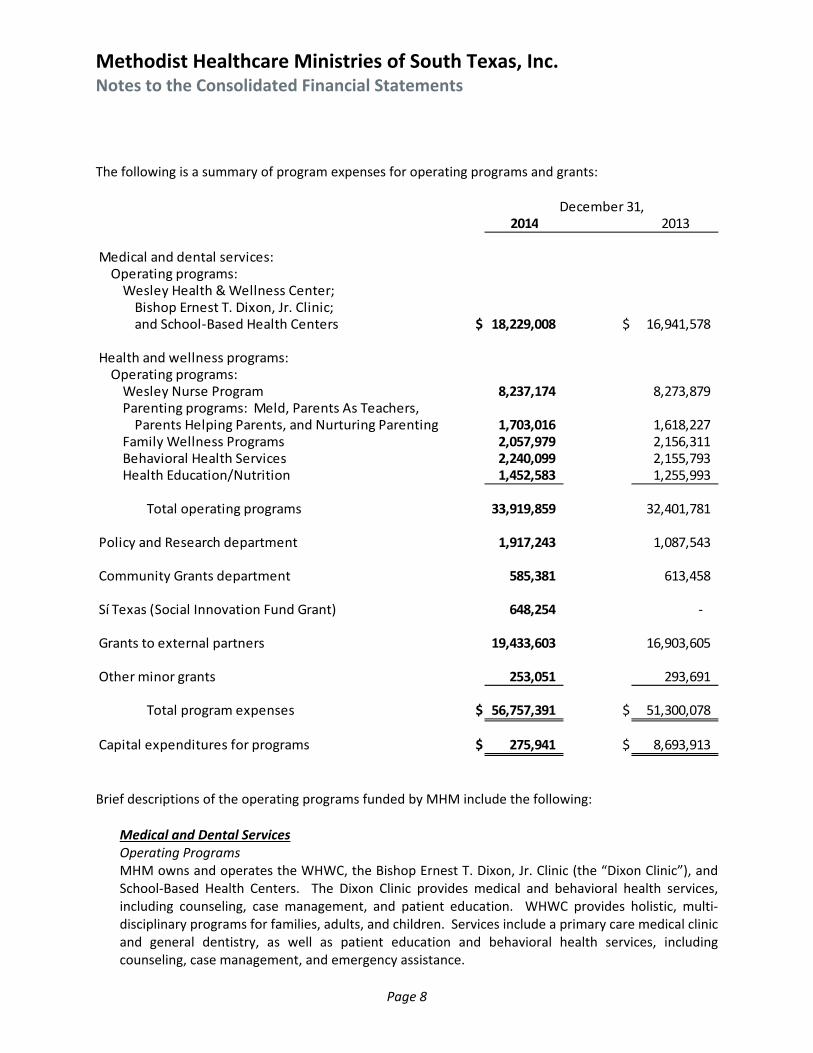

The following is a summary of program expenses for operating programs and grants:

2014 2013

Medical and dental services:Operating programs:Wesley Health & Wellness Center;Bishop Ernest T. Dixon, Jr. Clinic;and School‐Based Health Centers $ 18,229,008 $ 16,941,578

Health and wellness programs:Operating programs:Wesley Nurse Program 8,237,174 8,273,879Parenting programs: Meld, Parents As Teachers,Parents Helping Parents, and Nurturing Parenting 1,703,016 1,618,227

Family Wellness Programs 2,057,979 2,156,311Behavioral Health Services 2,240,099 2,155,793Health Education/Nutrition 1,452,583 1,255,993

Total operating programs 33,919,859 32,401,781

Policy and Research department 1,917,243 1,087,543

Community Grants department 585,381 613,458

Sí Texas (Social Innovation Fund Grant) 648,254 ‐

Grants to external partners 19,433,603 16,903,605

Other minor grants 253,051 293,691

Total program expenses $ 56,757,391 $ 51,300,078

Capital expenditures for programs $ 275,941 $ 8,693,913

December 31,

Brief descriptions of the operating programs funded by MHM include the following:

Medical and Dental Services Operating Programs MHM owns and operates the WHWC, the Bishop Ernest T. Dixon, Jr. Clinic (the “Dixon Clinic”), and School‐Based Health Centers. The Dixon Clinic provides medical and behavioral health services, including counseling, case management, and patient education. WHWC provides holistic, multi‐disciplinary programs for families, adults, and children. Services include a primary care medical clinic and general dentistry, as well as patient education and behavioral health services, including counseling, case management, and emergency assistance.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 9

Health, dental, and counseling services are provided by MHM through School‐Based Health Centers that provide primary medical and dental care to school‐age children and their siblings up to age 21 who live in the Schertz‐Cibolo‐Universal City Independent School District and Marion Independent School District, where such services are not readily available. The sites currently are at Krueger Elementary in Marion, Texas and Schertz Elementary in Schertz, Texas. Health and Wellness Programs Operating Programs The Wesley Nurse Program (“WNP”) is a faith‐based, holistic program committed to serving the least served through education, health promotion, and collaboration. The majority of the WNP sites are in churches in rural communities. Some are in larger cities, including a site at the historic San Fernando Cathedral in downtown San Antonio. All nurses in the program are specially trained registered nurses. Family wellness programs are available for youth, adults, and seniors to promote health and wellness through social interaction, building family unity, and education. Activities include exercise classes, parent and family trainings, support groups, and a community justice program. Parenting programs include Meld, Parents As Teachers, Nurturing Parenting Programs, and Parents Helping Parents (“PHP”) – parent education programs designed to inform parents about the importance of early education in the development of their children. MHM is a licensed network affiliate of the Parents As Teachers’ Meld program. MHM offers Meld programs for young mothers, young fathers, growing families, and parents of children with special needs. MHM conducts personal home visits with parents of children ages 0‐5, including prenatal visits. PHP is a program developed by MHM in partnership with the Texas Cooperative Extension in 1999. PHP provides training and technical assistance for volunteers to implement parent support groups in the rural areas of South Texas. MHM behavioral health services have been extended into the Coastal Bend Area, Rio Grande Valley, and Laredo through Church‐Based Community Counseling programs. Counseling is provided by licensed professional counselors and licensed clinical social workers. Nutrition and Health Education is a vital component of MHM. The primary focus is to provide educational support through MHM clinics by offering health education programs to clinic patients on an individual and group basis and to the general community.

Grants to External Partners Beginning in 1996, MHM has partnered with other community health centers and providers with similar missions through grants. This collaborative effort allows MHM to provide healthcare services at a lower cost through partnering with existing organizations in the underserved areas of San Antonio and South Texas.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 10

One of MHM’s strategic goals is to support mental health initiatives in MHM’s area. In 2011, MHM’s Board approved funding of $9,447,089 over a four‐year period to partner with other organizations to provide a much needed higher level of care for the growing population of underserved individuals who suffer from mental illness. These grants will address the mental health professional shortage and provide capital for construction of mental health clinics and funding for services.

All grants to partners are contingent upon performance and the availability of funds. Performance and compliance are reviewed quarterly by the Board and staff.

Basis of Accounting The accompanying consolidated financial statements have been prepared on the accrual basis of accounting applicable to not‐for‐profit organizations in accordance with accounting principles generally accepted in the United States of America (“GAAP”). Support and revenue are reported as an increase in unrestricted net assets unless use of the related assets is limited by donor‐imposed restrictions. Expenses are reported as decreases in unrestricted net assets. Gains and losses on investments and other assets or liabilities are reported as increases or decreases in unrestricted net assets unless their use is restricted by explicit donor stipulation or by law. Expirations of temporary restrictions on net assets (e.g. the donor stipulated purpose has been fulfilled and/or the stipulated time period has elapsed) are reported as reclassifications between the applicable classes of net assets. Use of Estimates The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Basis of Presentation In accordance with Not‐for‐Profit Entities topic of the Accounting Standards Codification (“ASC”), MHM reports information regarding its financial position and activities according to three classes of net assets: unrestricted net assets, temporarily restricted net assets, and permanently restricted net assets. Under these provisions, net assets and revenue, expenses, gains, and losses are classified as unrestricted, temporarily, and permanently restricted, based on the following criteria: Unrestricted Net Assets – Unrestricted net assets represent expendable funds available for operations which are not otherwise limited by donor restrictions. Unrestricted net assets may be designated for specific purposes by actions of the Board. The Board designated funds in 2013 for the Roy Campbell III Endowment Fund. The balance at December 31, 2014 is $108,344 ($108,539 in 2013).

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 11

Temporarily Restricted Net Assets – Temporarily restricted net assets consist of contributed funds subject to donor‐imposed restrictions contingent upon specific performance of a future event or passage of time before MHM may spend the funds. As of December 31, 2014 there were no temporarily restricted net assets and $12,825 as of December 31, 2013 for children’s healthcare services. Permanently Restricted Net Assets – Permanently restricted net assets are subject to irrevocable donor restrictions requiring that assets be maintained in perpetuity, usually for the purpose of generating investment income to fund annual operations or to be used for a charitable purpose. Cash and Cash Equivalents Highly liquid investments with original maturities of three months or less are reported as cash equivalents, excluding amounts whose use is limited by Board designation. MHM routinely invests its surplus operating funds in investments, such as money market funds, interest‐earning and noninterest‐earning bank accounts, and other short‐term investments. The carrying amount reported in the consolidated statements of financial position approximates the fair value of all short‐term cash positions. Investments Managed Accounts and Mutual funds are reported at fair value based on readily available quoted market prices. Private, alternative investments, such as hedge funds, are carried at fair value based on net asset values disclosed in the respective audited financial statements. The estimated fair value of securities for which there are no quoted market prices are based on similar types of securities that are traded in the market or values provided in audited financial statements of the funds. Unrealized gains and losses are included in the consolidated statements of activities. MHM has an investment policy that sets guidelines and constraints to ensure the portfolio is appropriately diversified. Assets Limited as to Use Assets limited as to use consisting of cash, money market funds, mutual funds, endowments, and debt and equity positions are carried at fair value. The research and development funds are carried at cost. Investments in partnerships are recorded based on MHM’s share of the partnership’s underlying value of portfolio securities, as reported to MHM by the related investment managers. Gains and losses and investment income/losses are reported as unrestricted or temporarily/permanently restricted net assets, as appropriate. Any changes in the net asset value of the partnerships are reflected as unrealized gains or losses. Property, Equipment, and Land Property and equipment acquisitions are recorded at cost. Depreciation is calculated on the straight‐line method over the estimated useful life of the depreciable assets. Leasehold improvements are amortized over the lease term.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 12

The estimated life used in computing depreciation and amortization is as follows: Buildings 30 yearsBuilding improvements 10‐15 yearsLeasehold improvements 3‐5 yearsMajor moveable equipment/office furnishings 3‐15 years Impairment of Long‐Lived Assets MHM reviews the carrying value of property and equipment for impairment whenever events and circumstances indicate the carrying value of an asset may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. In cases where undiscounted expected future cash flows are less than the carrying value, an impairment loss is recognized equal to an amount by which the carrying value exceeds the fair value of assets. The factors considered by management in performing this assessment include current operating results, trends and prospects, and the effects of obsolescence, demand, competition, and other economic factors. MHM did not recognize an impairment loss during the years ended December 31, 2014 and 2013. Medical Malpractice Self‐Insurance Prior to January 11, 1995, the Hospital self‐insured against malpractice claims. The Hospital established a trust for the purpose of setting aside assets based on actuarial funding recommendations. All assets and contingent liabilities for claims occurring prior to January 11, 1995, related to the trust, were transferred to MHM. Various levels of self‐insurance and excess coverage were in effect from July 1977 through January 10, 1995. As of December 31, 2003, all trust assets have been expended for malpractice claims, and all known claims have been resolved. If necessary, any future settlements or claims, which are not covered by insurance, would be paid out of Board‐designated assets. MHM obtained a tail policy on January 11, 1995, in the amount of $10,000,000 per claim and $10,000,000 annual aggregate above $3,000,000 per occurrence and $6,000,000 aggregate, retroactive to November 30, 1989. Any future settlements or claims would have to be paid out of other Board‐designated assets. Currently, MHM maintains a professional liability policy for nurses and other ancillary staff with a $1,000,000 per claim and $3,000,000 aggregate per year limit with a $5,000 deductible. An excess liability umbrella policy covering both general liability and professional liability claims is also in effect with a $15,000,000 limit per claim. Grants MHM considers all government grants and contracts as exchange transactions rather than contributions. MHM recognizes revenue from fee‐for‐service transactions as services are rendered and, for grants, as eligible expenditures are incurred. Advances from government agencies are recorded as refundable advances. Eligible expenditures incurred in excess of grant fund reimbursements are recorded as receivables. Any of the funding sources may, at their discretion, request reimbursement for expenses or return of funds, or both, as a result of any noncompliance with the terms of the grant or contract.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 13

In 2014, MHM was awarded a federal grant by the Social Innovation Fund (“SIF”) which is a key White House initiative and program of the Corporation for National and Community Service (“CNCS”) that combines public and private resources to grow the impact of innovative, community‐based solutions that have compelling evidence of improving the lives of people in low‐income communities throughout the United States. Thru this grant MHM developed the Sí Texas: Social Innovation for a Healthy South Texas project, focusing on integrated behavioral health models that are effectively improving health outcomes in South Texas communities with high rates of poverty, depression, diabetes, obesity and associated risk factors. The project leverages both federal and nonfederal dollars. The amount awarded is $5,000,000 per year from September 1, 2014 to August 31, 2019. Currently federal funds have only been appropriated for the first two years. As of December 31, 2014 MHM incurred $648,254 in matching expenses (nonfederal) associated with this grant. Contributions All contributions are considered to be available for unrestricted use unless specifically restricted by the donor. Amounts received that are designated for future periods or restricted by the donor for specific purposes are reported as temporarily restricted or permanently restricted support that increases those net asset classes. However, if a restriction is fulfilled in the same time period in which the contribution is received, MHM reports the support as unrestricted income. In‐Kind Support and Donated Personal Services of Volunteers In‐kind support is recorded as revenue and expense in the accompanying consolidated statements of activities only if the contribution meets the requirements of Not‐for‐Profit Entities of the ASC. In accordance with the ASC, for contributed services to be recognized as revenue, services must be those that would normally be paid for, the same as those normally provided by the donor, and clearly measurable. Volunteers at WHWC donate their time to support the various programs. Donated volunteer hours, for which no value has been assigned, totaled 6,415 hours and 5,654 hours at December 31, 2014 and 2013, respectively. MHM receives rental space, for a nominal amount, for the medical and dental operating sites at the Marion and Schertz‐Cibolo‐Universal City Independent School Districts. No amounts have been recognized for this rental space in the consolidated statements of activities. Functional Allocation of Costs The costs of providing the program and other activities have been summarized on a functional basis in the consolidated statements of activities. Accordingly, costs are allocated to the programs and management and general expenses based on actual use or estimated use, if actual use is not readily determinable. Concentrations of Credit Risk MHM maintains its cash in bank deposit accounts which, at times, may exceed federally insured limits. Accounts are guaranteed by the Federal Deposit Insurance Corporation up to a maximum of $250,000. MHM has not experienced any losses in such accounts.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 14

Reclassification Certain reclassifications have been made in the prior year’s financial statements to conform to the current year’s presentation. Recent Accounting Pronouncement Revenue – In May 2014, FASB issued ASU No. 2014‐09, Revenue From Contracts With Customers, requiring an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. The updated standard will replace most existing revenue recognition guidance in accounting principles generally accepted in the United States of America when it becomes effective and permits the use of either a full retrospective or retrospective with cumulative effect transition method. The updated standard will be effective for annual reporting periods beginning after December 15, 2017 and for interim periods within annual periods beginning after December 15, 2018. MHM has not yet selected a transition method and is currently evaluating the effect the updated standard will have on the financial statements. Effective April 1, 2015, FASB voted for a one‐year deferral of the effective date of the new revenue recognition standard. 2. Fair Value Measurements and Disclosures The requirements of Fair Value Measurements and Disclosures of the ASC apply to all financial instruments and all nonfinancial assets and nonfinancial liabilities that are being measured and reported on a fair value basis. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Fair Value Measurements and Disclosures also establishes a fair value hierarchy that prioritizes the inputs used in valuation methodologies into the following three levels:

Level 1 Inputs – Unadjusted quoted prices in active markets for identical assets or liabilities.

Level 2 Inputs – Observable inputs other than Level 1 prices, such as quoted prices for similar assets or liabilities, or other inputs that can be corroborated by observable market data for substantially the full term of the assets or liabilities.

Level 3 Inputs – Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities. Level 3 assets and liabilities include financial instruments whose value is determined using pricing models, discounted cash flow methodologies, or other valuation techniques, as well as instruments for which the determination of fair value requires significant management judgment or estimation.

A description of the valuation methodologies used for instruments measured at fair value, as well as the general classification of such instruments pursuant to the valuation hierarchy, is set forth on the following page.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 15

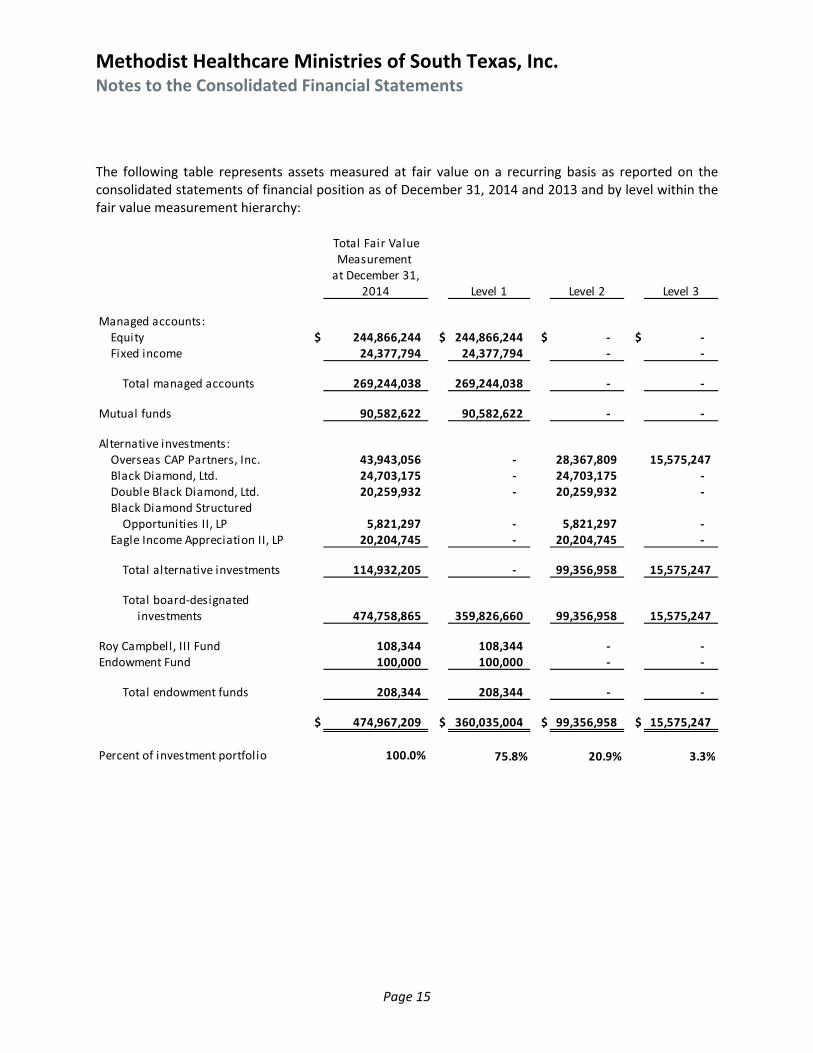

The following table represents assets measured at fair value on a recurring basis as reported on the consolidated statements of financial position as of December 31, 2014 and 2013 and by level within the fair value measurement hierarchy:

Total Fair ValueMeasurement at December 31,

2014 Level 1 Level 2 Level 3

Managed accounts:Equity $ 244,866,244 $ 244,866,244 $ ‐ $ ‐ Fixed income 24,377,794 24,377,794 ‐ ‐

Total managed accounts 269,244,038 269,244,038 ‐ ‐

Mutual funds 90,582,622 90,582,622 ‐ ‐

Alternative investments:Overseas CAP Partners, Inc. 43,943,056 ‐ 28,367,809 15,575,247Black Diamond, Ltd. 24,703,175 ‐ 24,703,175 ‐ Double Black Diamond, Ltd. 20,259,932 ‐ 20,259,932 ‐ Black Diamond Structured Opportunities II, LP 5,821,297 ‐ 5,821,297 ‐

Eagle Income Appreciation II, LP 20,204,745 ‐ 20,204,745 ‐

Total alternative investments 114,932,205 ‐ 99,356,958 15,575,247

Total board‐designated investments 474,758,865 359,826,660 99,356,958 15,575,247

Roy Campbell, III Fund 108,344 108,344 ‐ ‐ Endowment Fund 100,000 100,000 ‐ ‐

Total endowment funds 208,344 208,344 ‐ ‐

$ 474,967,209 $ 360,035,004 $ 99,356,958 $ 15,575,247

Percent of investment portfolio 100.0% 75.8% 20.9% 3.3%

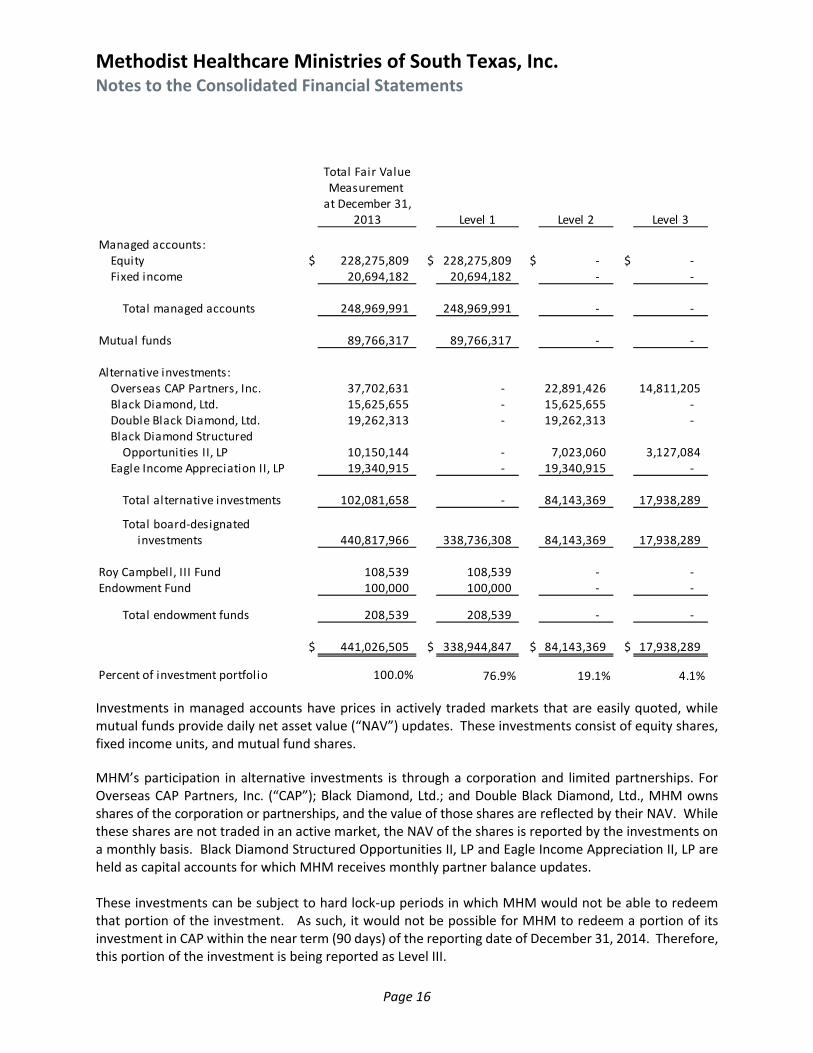

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 16

Total Fair ValueMeasurement at December 31,

2013 Level 1 Level 2 Level 3

Managed accounts:Equity $ 228,275,809 $ 228,275,809 $ ‐ $ ‐ Fixed income 20,694,182 20,694,182 ‐ ‐

Total managed accounts 248,969,991 248,969,991 ‐ ‐

Mutual funds 89,766,317 89,766,317 ‐ ‐

Alternative investments:Overseas CAP Partners, Inc. 37,702,631 ‐ 22,891,426 14,811,205Black Diamond, Ltd. 15,625,655 ‐ 15,625,655 ‐ Double Black Diamond, Ltd. 19,262,313 ‐ 19,262,313 ‐ Black Diamond Structured Opportunities II, LP 10,150,144 ‐ 7,023,060 3,127,084

Eagle Income Appreciation II, LP 19,340,915 ‐ 19,340,915 ‐

Total alternative investments 102,081,658 ‐ 84,143,369 17,938,289

Total board‐designated investments 440,817,966 338,736,308 84,143,369 17,938,289

Roy Campbell, III Fund 108,539 108,539 ‐ ‐ Endowment Fund 100,000 100,000 ‐ ‐

Total endowment funds 208,539 208,539 ‐ ‐

$ 441,026,505 $ 338,944,847 $ 84,143,369 $ 17,938,289

Percent of investment portfolio 100.0% 76.9% 19.1% 4.1%

Investments in managed accounts have prices in actively traded markets that are easily quoted, while mutual funds provide daily net asset value (“NAV”) updates. These investments consist of equity shares, fixed income units, and mutual fund shares.

MHM’s participation in alternative investments is through a corporation and limited partnerships. For Overseas CAP Partners, Inc. (“CAP”); Black Diamond, Ltd.; and Double Black Diamond, Ltd., MHM owns shares of the corporation or partnerships, and the value of those shares are reflected by their NAV. While these shares are not traded in an active market, the NAV of the shares is reported by the investments on a monthly basis. Black Diamond Structured Opportunities II, LP and Eagle Income Appreciation II, LP are held as capital accounts for which MHM receives monthly partner balance updates. These investments can be subject to hard lock‐up periods in which MHM would not be able to redeem that portion of the investment. As such, it would not be possible for MHM to redeem a portion of its investment in CAP within the near term (90 days) of the reporting date of December 31, 2014. Therefore, this portion of the investment is being reported as Level III.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 17

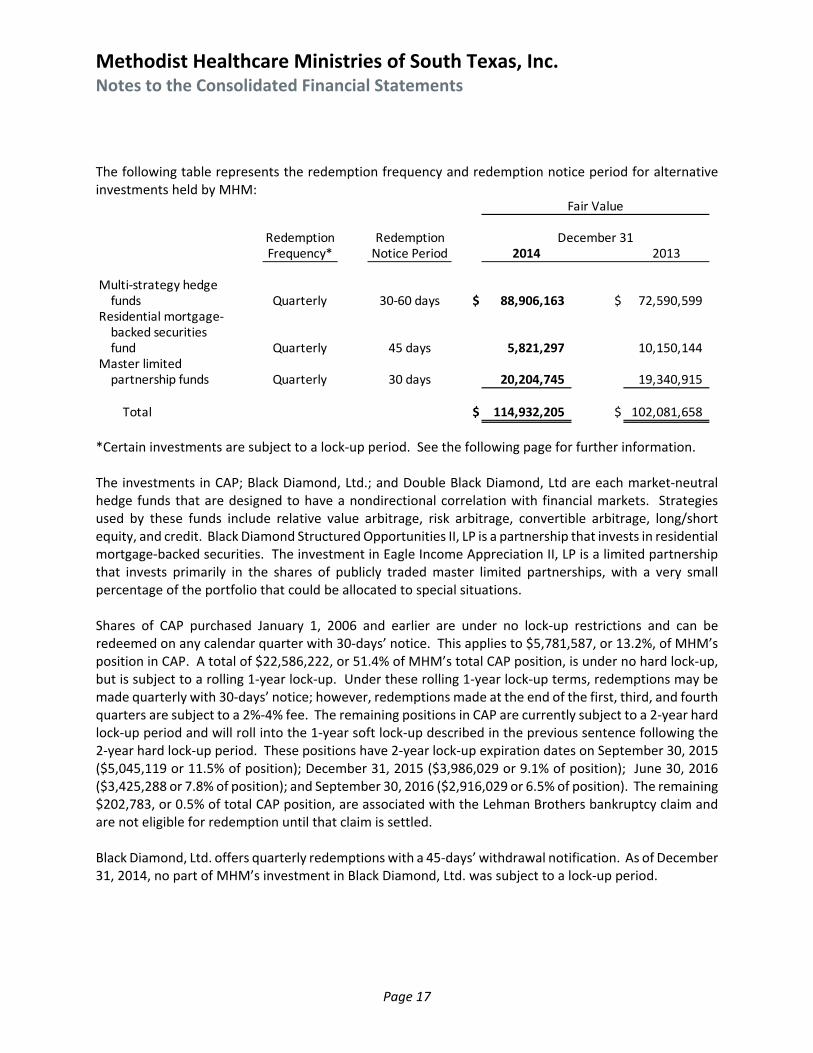

The following table represents the redemption frequency and redemption notice period for alternative investments held by MHM:

Redemption RedemptionFrequency* Notice Period 2014 2013

Multi‐strategy hedgefunds Quarterly 30‐60 days $ 88,906,163 $ 72,590,599

Residential mortgage‐backed securities fund Quarterly 45 days 5,821,297 10,150,144

Master limited partnership funds Quarterly 30 days 20,204,745 19,340,915

Total $ 114,932,205 $ 102,081,658

Fair Value

December 31

*Certain investments are subject to a lock‐up period. See the following page for further information. The investments in CAP; Black Diamond, Ltd.; and Double Black Diamond, Ltd are each market‐neutral hedge funds that are designed to have a nondirectional correlation with financial markets. Strategies used by these funds include relative value arbitrage, risk arbitrage, convertible arbitrage, long/short equity, and credit. Black Diamond Structured Opportunities II, LP is a partnership that invests in residential mortgage‐backed securities. The investment in Eagle Income Appreciation II, LP is a limited partnership that invests primarily in the shares of publicly traded master limited partnerships, with a very small percentage of the portfolio that could be allocated to special situations. Shares of CAP purchased January 1, 2006 and earlier are under no lock‐up restrictions and can be redeemed on any calendar quarter with 30‐days’ notice. This applies to $5,781,587, or 13.2%, of MHM’s position in CAP. A total of $22,586,222, or 51.4% of MHM’s total CAP position, is under no hard lock‐up, but is subject to a rolling 1‐year lock‐up. Under these rolling 1‐year lock‐up terms, redemptions may be made quarterly with 30‐days’ notice; however, redemptions made at the end of the first, third, and fourth quarters are subject to a 2%‐4% fee. The remaining positions in CAP are currently subject to a 2‐year hard lock‐up period and will roll into the 1‐year soft lock‐up described in the previous sentence following the 2‐year hard lock‐up period. These positions have 2‐year lock‐up expiration dates on September 30, 2015 ($5,045,119 or 11.5% of position); December 31, 2015 ($3,986,029 or 9.1% of position); June 30, 2016 ($3,425,288 or 7.8% of position); and September 30, 2016 ($2,916,029 or 6.5% of position). The remaining $202,783, or 0.5% of total CAP position, are associated with the Lehman Brothers bankruptcy claim and are not eligible for redemption until that claim is settled. Black Diamond, Ltd. offers quarterly redemptions with a 45‐days’ withdrawal notification. As of December 31, 2014, no part of MHM’s investment in Black Diamond, Ltd. was subject to a lock‐up period.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 18

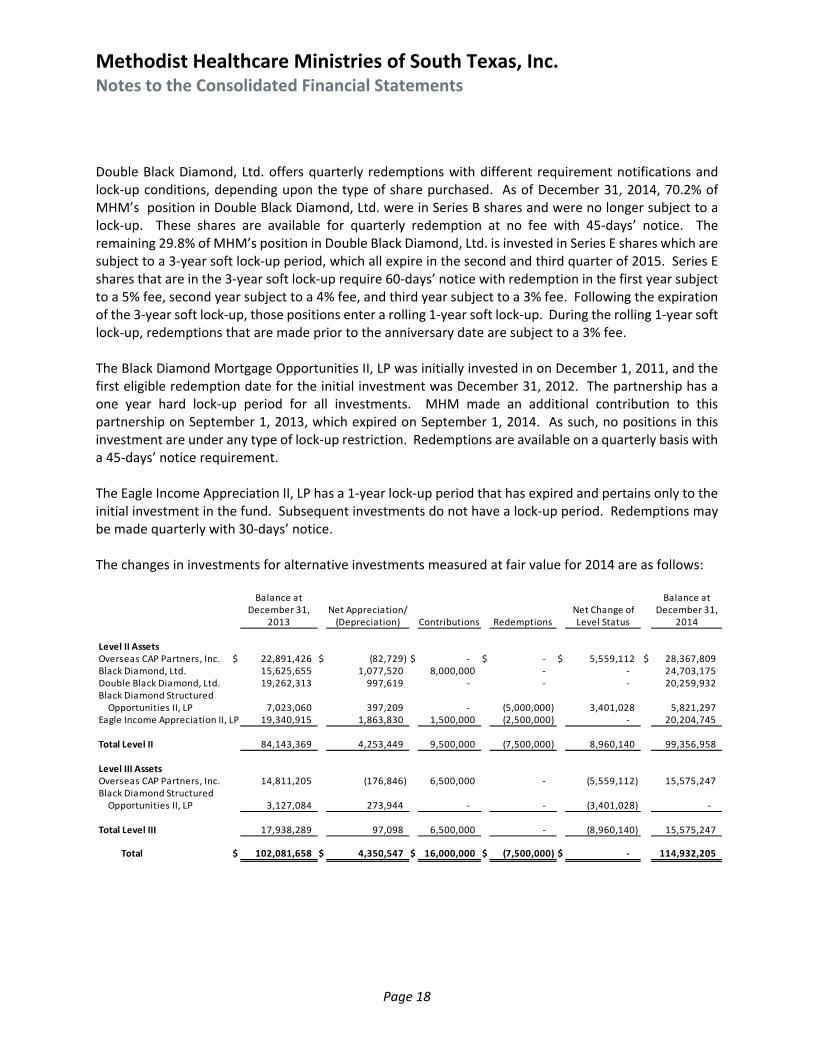

Double Black Diamond, Ltd. offers quarterly redemptions with different requirement notifications and lock‐up conditions, depending upon the type of share purchased. As of December 31, 2014, 70.2% of MHM’s position in Double Black Diamond, Ltd. were in Series B shares and were no longer subject to a lock‐up. These shares are available for quarterly redemption at no fee with 45‐days’ notice. The remaining 29.8% of MHM’s position in Double Black Diamond, Ltd. is invested in Series E shares which are subject to a 3‐year soft lock‐up period, which all expire in the second and third quarter of 2015. Series E shares that are in the 3‐year soft lock‐up require 60‐days’ notice with redemption in the first year subject to a 5% fee, second year subject to a 4% fee, and third year subject to a 3% fee. Following the expiration of the 3‐year soft lock‐up, those positions enter a rolling 1‐year soft lock‐up. During the rolling 1‐year soft lock‐up, redemptions that are made prior to the anniversary date are subject to a 3% fee. The Black Diamond Mortgage Opportunities II, LP was initially invested in on December 1, 2011, and the first eligible redemption date for the initial investment was December 31, 2012. The partnership has a one year hard lock‐up period for all investments. MHM made an additional contribution to this partnership on September 1, 2013, which expired on September 1, 2014. As such, no positions in this investment are under any type of lock‐up restriction. Redemptions are available on a quarterly basis with a 45‐days’ notice requirement. The Eagle Income Appreciation II, LP has a 1‐year lock‐up period that has expired and pertains only to the initial investment in the fund. Subsequent investments do not have a lock‐up period. Redemptions may be made quarterly with 30‐days’ notice. The changes in investments for alternative investments measured at fair value for 2014 are as follows:

Balance at Balance atDecember 31, Net Appreciation/ Net Change of December 31,

2013 (Depreciation) Contributions Redemptions Level Status 2014

Level II AssetsOverseas CAP Partners, Inc. $ 22,891,426 $ (82,729) $ ‐ $ ‐ $ 5,559,112 $ 28,367,809Black Diamond, Ltd. 15,625,655 1,077,520 8,000,000 ‐ ‐ 24,703,175Double Black Diamond, Ltd. 19,262,313 997,619 ‐ ‐ ‐ 20,259,932Black Diamond Structured Opportunities II, LP 7,023,060 397,209 ‐ (5,000,000) 3,401,028 5,821,297Eagle Income Appreciation II, LP 19,340,915 1,863,830 1,500,000 (2,500,000) ‐ 20,204,745

Total Level II 84,143,369 4,253,449 9,500,000 (7,500,000) 8,960,140 99,356,958

Level III AssetsOverseas CAP Partners, Inc. 14,811,205 (176,846) 6,500,000 ‐ (5,559,112) 15,575,247Black Diamond Structured Opportunities II, LP 3,127,084 273,944 ‐ ‐ (3,401,028) ‐

Total Level III 17,938,289 97,098 6,500,000 ‐ (8,960,140) 15,575,247

Total $ 102,081,658 $ 4,350,547 $ 16,000,000 $ (7,500,000) $ ‐ 114,932,205

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 19

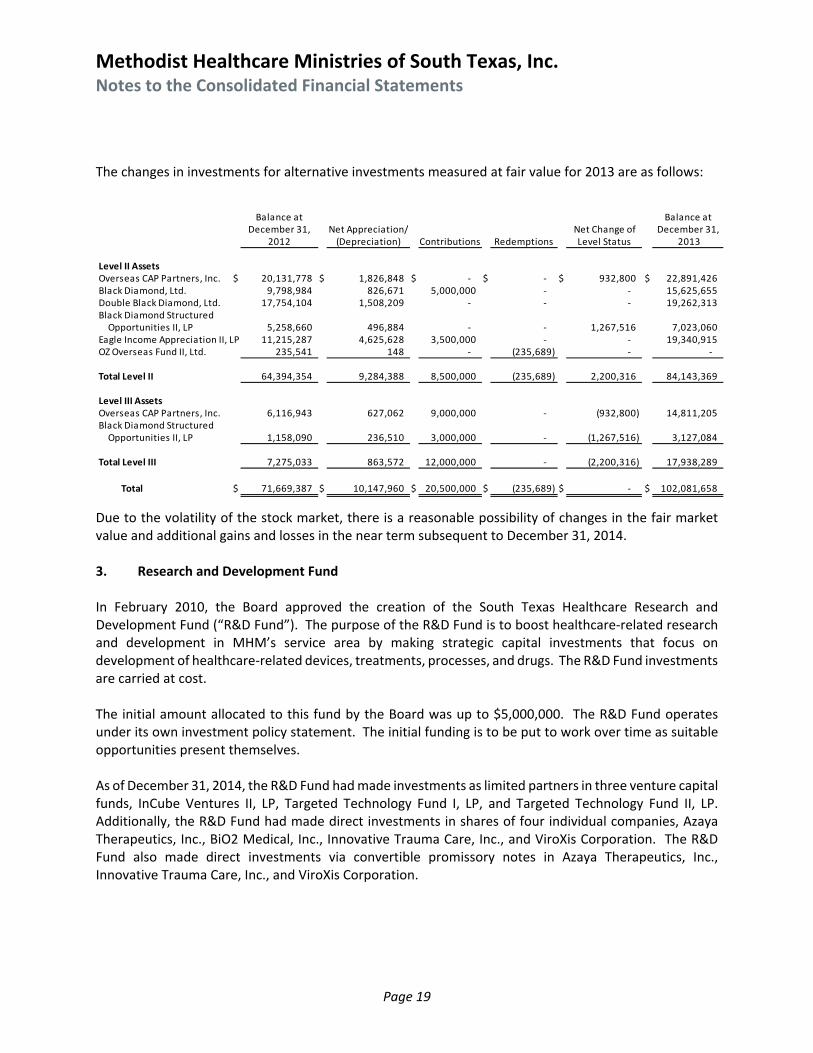

The changes in investments for alternative investments measured at fair value for 2013 are as follows:

Balance at Balance atDecember 31, Net Appreciation/ Net Change of December 31,

2012 (Depreciation) Contributions Redemptions Level Status 2013

Level II AssetsOverseas CAP Partners, Inc. $ 20,131,778 $ 1,826,848 $ ‐ $ ‐ $ 932,800 $ 22,891,426Black Diamond, Ltd. 9,798,984 826,671 5,000,000 ‐ ‐ 15,625,655Double Black Diamond, Ltd. 17,754,104 1,508,209 ‐ ‐ ‐ 19,262,313Black Diamond Structured Opportunities II, LP 5,258,660 496,884 ‐ ‐ 1,267,516 7,023,060Eagle Income Appreciation II, LP 11,215,287 4,625,628 3,500,000 ‐ ‐ 19,340,915OZ Overseas Fund II, Ltd. 235,541 148 ‐ (235,689) ‐ ‐

Total Level II 64,394,354 9,284,388 8,500,000 (235,689) 2,200,316 84,143,369

Level III AssetsOverseas CAP Partners, Inc. 6,116,943 627,062 9,000,000 ‐ (932,800) 14,811,205Black Diamond Structured Opportunities II, LP 1,158,090 236,510 3,000,000 ‐ (1,267,516) 3,127,084

Total Level III 7,275,033 863,572 12,000,000 ‐ (2,200,316) 17,938,289

Total $ 71,669,387 $ 10,147,960 $ 20,500,000 $ (235,689) $ ‐ $ 102,081,658

Due to the volatility of the stock market, there is a reasonable possibility of changes in the fair market value and additional gains and losses in the near term subsequent to December 31, 2014. 3. Research and Development Fund In February 2010, the Board approved the creation of the South Texas Healthcare Research and Development Fund (“R&D Fund”). The purpose of the R&D Fund is to boost healthcare‐related research and development in MHM’s service area by making strategic capital investments that focus on development of healthcare‐related devices, treatments, processes, and drugs. The R&D Fund investments are carried at cost. The initial amount allocated to this fund by the Board was up to $5,000,000. The R&D Fund operates under its own investment policy statement. The initial funding is to be put to work over time as suitable opportunities present themselves. As of December 31, 2014, the R&D Fund had made investments as limited partners in three venture capital funds, InCube Ventures II, LP, Targeted Technology Fund I, LP, and Targeted Technology Fund II, LP. Additionally, the R&D Fund had made direct investments in shares of four individual companies, Azaya Therapeutics, Inc., BiO2 Medical, Inc., Innovative Trauma Care, Inc., and ViroXis Corporation. The R&D Fund also made direct investments via convertible promissory notes in Azaya Therapeutics, Inc., Innovative Trauma Care, Inc., and ViroXis Corporation.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 20

The promissory note which MHM holds for Azaya Therapeutics, Inc. has a principal amount of $335,000, is dated February 15, 2013 and was scheduled to mature on December 31, 2014. The note has an interest rate of five percent (5.0%) and is convertible to shares of the company per the following conditions: (1) if Azaya enters into a subsequent equity financing round then the principal and unpaid accrued interest of the promissory note converts into the shares of stated financing round at a conversion price of $2.00 per share, or (2) in the event that no financing round occurs prior to the maturity date, principal and unpaid accrued interest may be converted into Preferred Stock of the company at a conversion price of $2.00 per share. In November 2014, MHM submitted formal paperwork to Azaya Therapeutics, Inc. pertaining to the conversion of their promissory note to common shares of the company. This was related to terms of the newly initiated Series A Preferred Shares financing round that Azaya started in late 2014. The actual conversion will not occur until this Series A round has been completed, which is expected to be a mid‐2015 event, at which time MHM will receive the common shares in Azaya at a price of $2.00 per share. The promissory note which MHM holds for ViroXis Corporation has a principal amount of $250,000 and is dated May 2, 2014 and cannot be redeemed prior to September 30, 2015. The note has an interest rate of seven percent (7.0%) per annum and is subject to automatic conversion per the following: (1) conversion into shares of the next round of financing at a 20% discount to the per share purchase price of that next financing round, or (2) if a change of control occurs prior to the initial closing of the next financing, conversion into shares of Series Preferred B Stock immediately at a price of $5.00 per share (as adjusted for any stock dividend, stock split or combination with respect to the Series B Preferred Stock after the date of the promissory noted but prior to the date the note converts into Series B Preferred Stock). The promissory note which MHM holds for Innovative Trauma Care, Inc. has a principal amount of $150,000 and is dated August 29, 2014 with a maturity date of December 31, 2014. The note has an interest rate of eight percent (8.0%) and is subject to automatic conversion per the following: (1) conversion into shares of the next round of financing at a 20% discount to the per share purchase price, or (2) if a change of control occurs prior to the initial closing of the next financing, shares of Class B Preferred Shares immediately at a rate of $1.50 (as adjusted for stock splits, stock dividends, combinations and the like with respect to the Company’s Class B Preferred Shares). As of December 31, 2014, Innovative Trauma Care is proceeding with their next round of financing which is expected to close in the second quarter of 2015. Upon the successful completion of that financing round, the note that MHM holds will be converted to shares of that round at the 20% discount to per share price. As of December 31, 2014, the total committed capital for these partnerships and direct investments was $3,585,000 ($2,835,000 in 2013). As of December 31, 2014, $3,010,000 of that had been called ($1,885,000 in 2013).

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 21

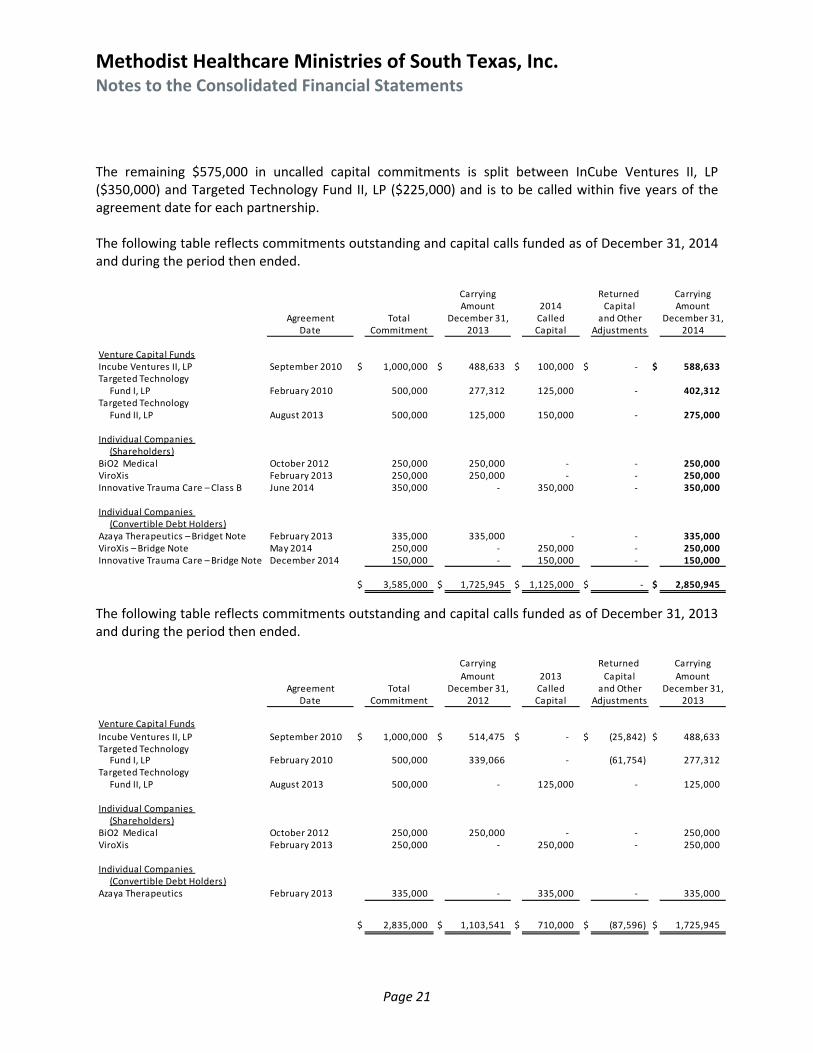

The remaining $575,000 in uncalled capital commitments is split between InCube Ventures II, LP ($350,000) and Targeted Technology Fund II, LP ($225,000) and is to be called within five years of the agreement date for each partnership. The following table reflects commitments outstanding and capital calls funded as of December 31, 2014 and during the period then ended.

Carrying Returned CarryingAmount 2014 Capital Amount

Agreement Total December 31, Called and Other December 31,Date Commitment 2013 Capital Adjustments 2014

Venture Capital FundsIncube Ventures II, LP September 2010 $ 1,000,000 $ 488,633 $ 100,000 $ ‐ $ 588,633 Targeted Technology

Fund I, LP February 2010 500,000 277,312 125,000 ‐ 402,312 Targeted Technology

Fund II, LP August 2013 500,000 125,000 150,000 ‐ 275,000

Individual Companies (Shareholders)

BiO2 Medical October 2012 250,000 250,000 ‐ ‐ 250,000 ViroXis February 2013 250,000 250,000 ‐ ‐ 250,000 Innovative Trauma Care – Class B June 2014 350,000 ‐ 350,000 ‐ 350,000

Individual Companies (Convertible Debt Holders)

Azaya Therapeutics – Bridget Note February 2013 335,000 335,000 ‐ ‐ 335,000 ViroXis – Bridge Note May 2014 250,000 ‐ 250,000 ‐ 250,000 Innovative Trauma Care – Bridge Note December 2014 150,000 ‐ 150,000 ‐ 150,000

$ 3,585,000 $ 1,725,945 $ 1,125,000 $ ‐ $ 2,850,945

The following table reflects commitments outstanding and capital calls funded as of December 31, 2013 and during the period then ended.

Carrying Returned Carrying

Amount 2013 Capital AmountAgreement Total December 31, Called and Other December 31,

Date Commitment 2012 Capital Adjustments 2013

Venture Capital Funds

Incube Ventures II, LP September 2010 $ 1,000,000 $ 514,475 $ ‐ $ (25,842) $ 488,633 Targeted Technology

Fund I, LP February 2010 500,000 339,066 ‐ (61,754) 277,312 Targeted Technology

Fund II, LP August 2013 500,000 ‐ 125,000 ‐ 125,000

Individual Companies (Shareholders)

BiO2 Medical October 2012 250,000 250,000 ‐ ‐ 250,000 ViroXis February 2013 250,000 ‐ 250,000 ‐ 250,000

Individual Companies (Convertible Debt Holders)

Azaya Therapeutics February 2013 335,000 ‐ 335,000 ‐ 335,000

$ 2,835,000 $ 1,103,541 $ 710,000 $ (87,596) $ 1,725,945

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 22

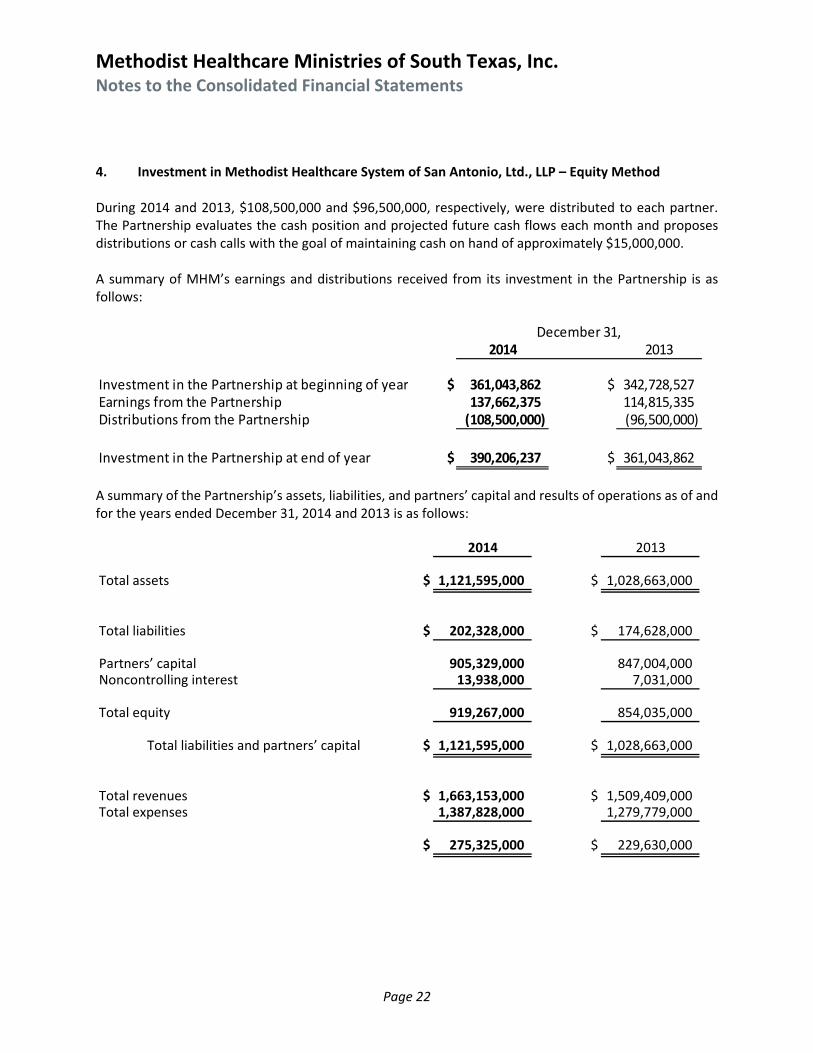

4. Investment in Methodist Healthcare System of San Antonio, Ltd., LLP – Equity Method During 2014 and 2013, $108,500,000 and $96,500,000, respectively, were distributed to each partner. The Partnership evaluates the cash position and projected future cash flows each month and proposes distributions or cash calls with the goal of maintaining cash on hand of approximately $15,000,000. A summary of MHM’s earnings and distributions received from its investment in the Partnership is as follows:

2014 2013

Investment in the Partnership at beginning of year $ 361,043,862 $ 342,728,527Earnings from the Partnership 137,662,375 114,815,335Distributions from the Partnership (108,500,000) (96,500,000)

Investment in the Partnership at end of year $ 390,206,237 $ 361,043,862

December 31,

A summary of the Partnership’s assets, liabilities, and partners’ capital and results of operations as of and for the years ended December 31, 2014 and 2013 is as follows:

2014 2013

Total assets $ 1,121,595,000 $ 1,028,663,000

Total liabilities $ 202,328,000 $ 174,628,000

Partners’ capital 905,329,000 847,004,000Noncontrolling interest 13,938,000 7,031,000

Total equity 919,267,000 854,035,000

Total liabilities and partners’ capital $ 1,121,595,000 $ 1,028,663,000

Total revenues $ 1,663,153,000 $ 1,509,409,000Total expenses 1,387,828,000 1,279,779,000

$ 275,325,000 $ 229,630,000

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 23

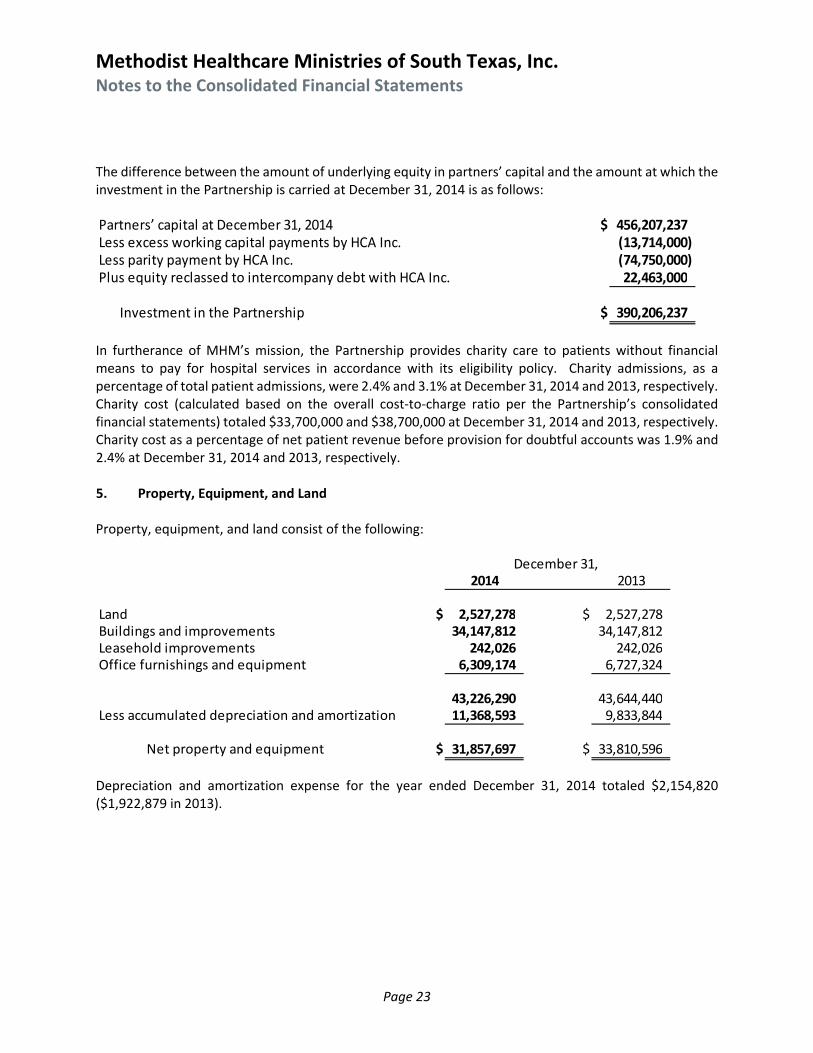

The difference between the amount of underlying equity in partners’ capital and the amount at which the investment in the Partnership is carried at December 31, 2014 is as follows: Partners’ capital at December 31, 2014 $ 456,207,237Less excess working capital payments by HCA Inc. (13,714,000)Less parity payment by HCA Inc. (74,750,000)Plus equity reclassed to intercompany debt with HCA Inc. 22,463,000

Investment in the Partnership $ 390,206,237

In furtherance of MHM’s mission, the Partnership provides charity care to patients without financial means to pay for hospital services in accordance with its eligibility policy. Charity admissions, as a percentage of total patient admissions, were 2.4% and 3.1% at December 31, 2014 and 2013, respectively. Charity cost (calculated based on the overall cost‐to‐charge ratio per the Partnership’s consolidated financial statements) totaled $33,700,000 and $38,700,000 at December 31, 2014 and 2013, respectively. Charity cost as a percentage of net patient revenue before provision for doubtful accounts was 1.9% and 2.4% at December 31, 2014 and 2013, respectively. 5. Property, Equipment, and Land Property, equipment, and land consist of the following:

2014 2013

Land $ 2,527,278 $ 2,527,278Buildings and improvements 34,147,812 34,147,812Leasehold improvements 242,026 242,026Office furnishings and equipment 6,309,174 6,727,324

43,226,290 43,644,440Less accumulated depreciation and amortization 11,368,593 9,833,844

Net property and equipment $ 31,857,697 $ 33,810,596

December 31,

Depreciation and amortization expense for the year ended December 31, 2014 totaled $2,154,820 ($1,922,879 in 2013).

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 24

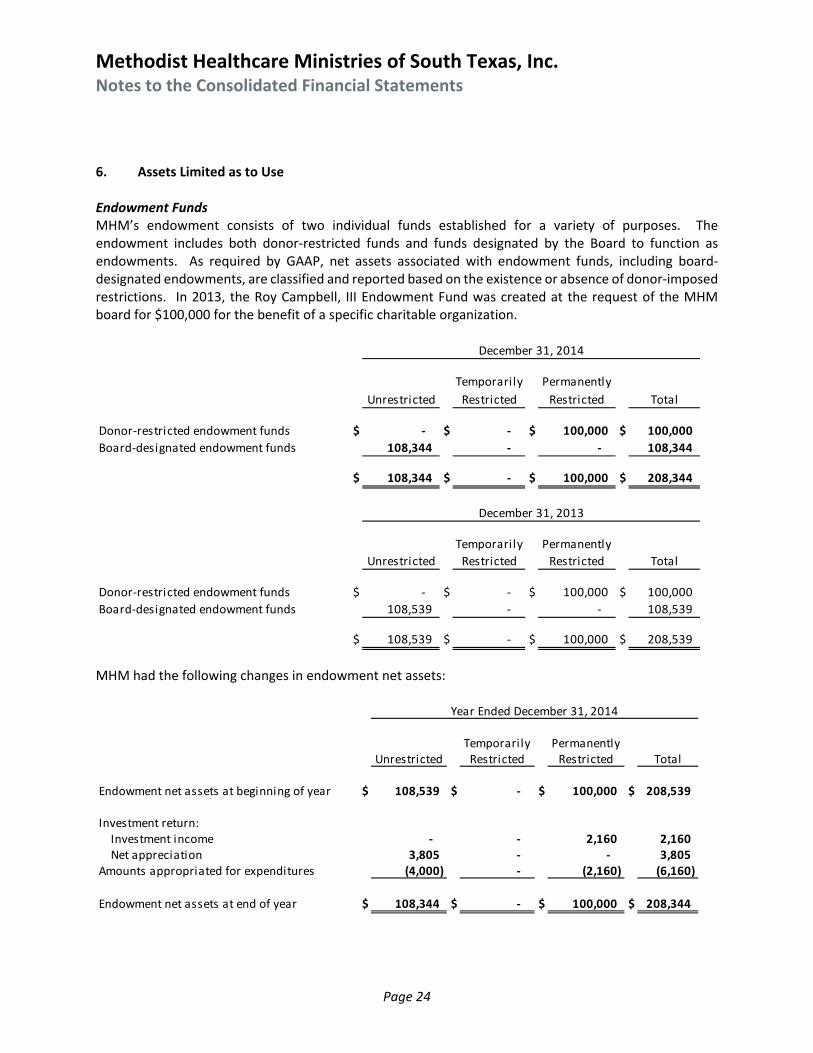

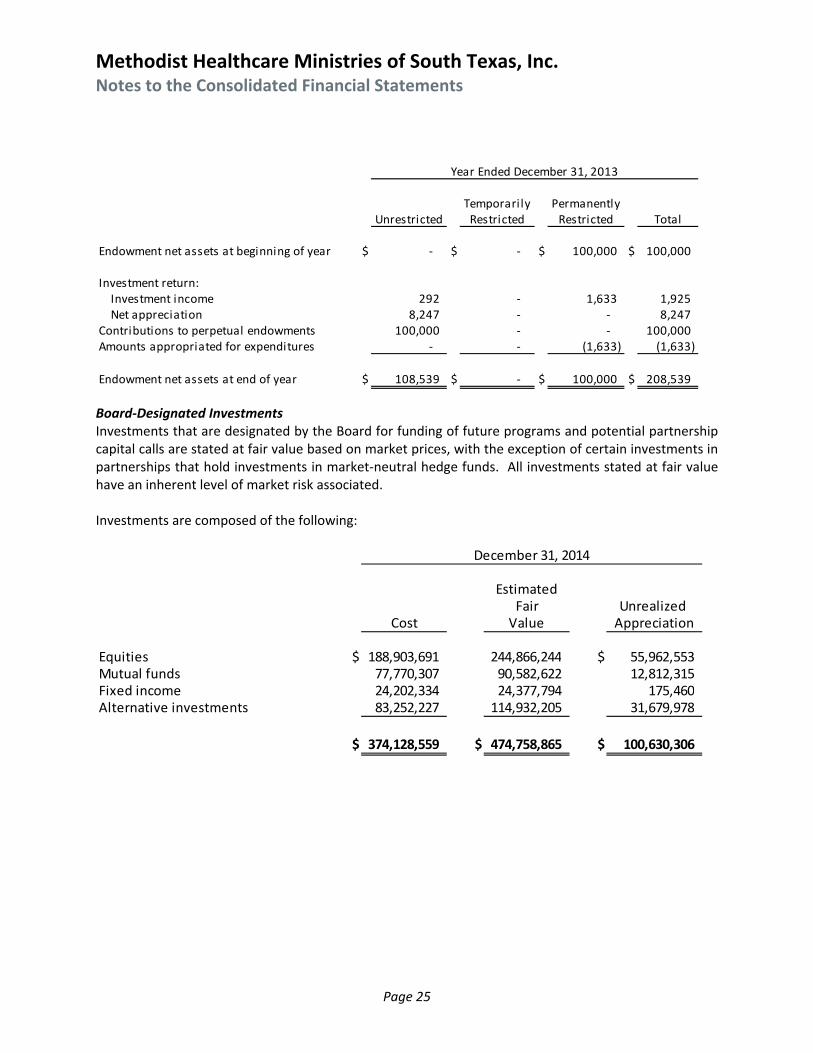

6. Assets Limited as to Use Endowment Funds MHM’s endowment consists of two individual funds established for a variety of purposes. The endowment includes both donor‐restricted funds and funds designated by the Board to function as endowments. As required by GAAP, net assets associated with endowment funds, including board‐designated endowments, are classified and reported based on the existence or absence of donor‐imposed restrictions. In 2013, the Roy Campbell, III Endowment Fund was created at the request of the MHM board for $100,000 for the benefit of a specific charitable organization.

Temporarily Permanently

Unrestricted Restricted Restricted Total

Donor‐restricted endowment funds $ ‐ $ ‐ $ 100,000 $ 100,000

Board‐designated endowment funds 108,344 ‐ ‐ 108,344

$ 108,344 $ ‐ $ 100,000 $ 208,344

Temporarily Permanently

Unrestricted Restricted Restricted Total

Donor‐restricted endowment funds $ ‐ $ ‐ $ 100,000 $ 100,000

Board‐designated endowment funds 108,539 ‐ ‐ 108,539

$ 108,539 $ ‐ $ 100,000 $ 208,539

December 31, 2014

December 31, 2013

MHM had the following changes in endowment net assets:

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Endowment net assets at beginning of year $ 108,539 $ ‐ $ 100,000 $ 208,539

Investment return:Investment income ‐ ‐ 2,160 2,160 Net appreciation 3,805 ‐ ‐ 3,805

Amounts appropriated for expenditures (4,000) ‐ (2,160) (6,160)

Endowment net assets at end of year $ 108,344 $ ‐ $ 100,000 $ 208,344

Year Ended December 31, 2014

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 25

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Endowment net assets at beginning of year $ ‐ $ ‐ $ 100,000 $ 100,000

Investment return:Investment income 292 ‐ 1,633 1,925 Net appreciation 8,247 ‐ ‐ 8,247

Contributions to perpetual endowments 100,000 ‐ ‐ 100,000 Amounts appropriated for expenditures ‐ ‐ (1,633) (1,633)

Endowment net assets at end of year $ 108,539 $ ‐ $ 100,000 $ 208,539

Year Ended December 31, 2013

Board‐Designated Investments Investments that are designated by the Board for funding of future programs and potential partnership capital calls are stated at fair value based on market prices, with the exception of certain investments in partnerships that hold investments in market‐neutral hedge funds. All investments stated at fair value have an inherent level of market risk associated. Investments are composed of the following:

EstimatedFair Unrealized

Cost Value Appreciation

Equities $ 188,903,691 244,866,244 $ 55,962,553Mutual funds 77,770,307 90,582,622 12,812,315Fixed income 24,202,334 24,377,794 175,460Alternative investments 83,252,227 114,932,205 31,679,978

$ 374,128,559 $ 474,758,865 $ 100,630,306

December 31, 2014

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 26

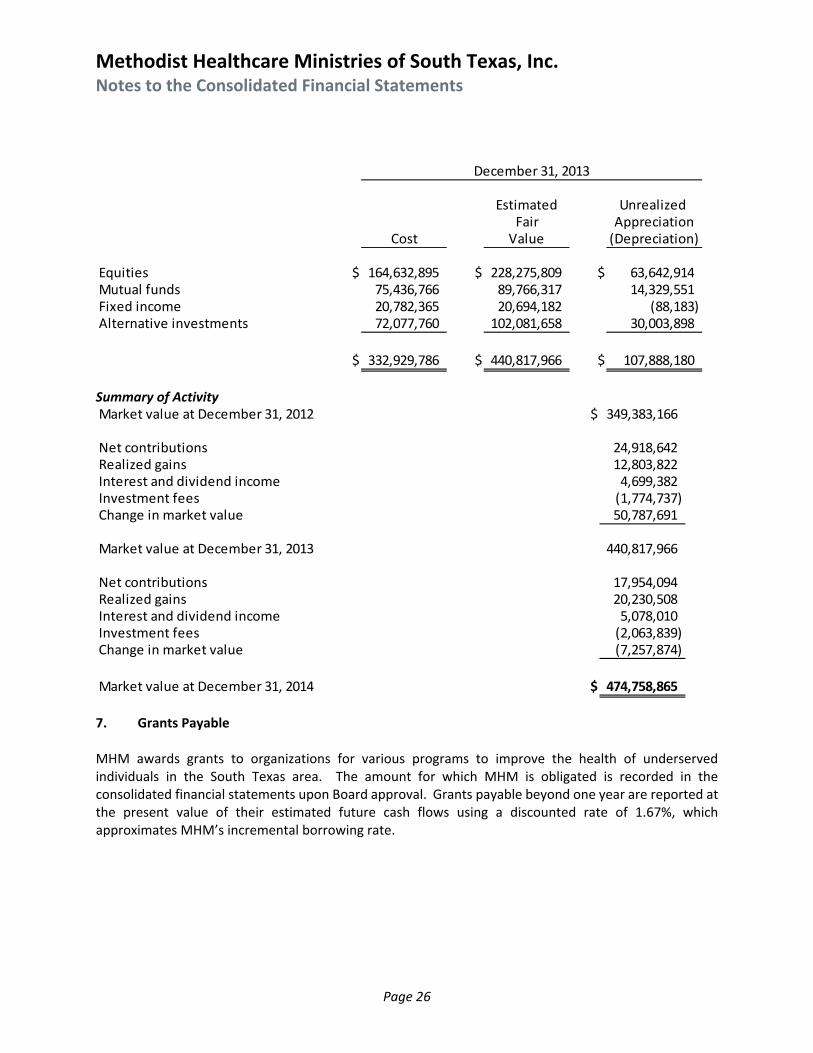

Estimated Unrealized Fair Appreciation

Cost Value (Depreciation)

Equities $ 164,632,895 $ 228,275,809 $ 63,642,914Mutual funds 75,436,766 89,766,317 14,329,551Fixed income 20,782,365 20,694,182 (88,183)Alternative investments 72,077,760 102,081,658 30,003,898

$ 332,929,786 $ 440,817,966 $ 107,888,180

December 31, 2013

Summary of Activity Market value at December 31, 2012 $ 349,383,166

Net contributions 24,918,642Realized gains 12,803,822Interest and dividend income 4,699,382Investment fees (1,774,737)Change in market value 50,787,691

Market value at December 31, 2013 440,817,966

Net contributions 17,954,094Realized gains 20,230,508Interest and dividend income 5,078,010Investment fees (2,063,839)Change in market value (7,257,874)

Market value at December 31, 2014 $ 474,758,865

7. Grants Payable MHM awards grants to organizations for various programs to improve the health of underserved individuals in the South Texas area. The amount for which MHM is obligated is recorded in the consolidated financial statements upon Board approval. Grants payable beyond one year are reported at the present value of their estimated future cash flows using a discounted rate of 1.67%, which approximates MHM’s incremental borrowing rate.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 27

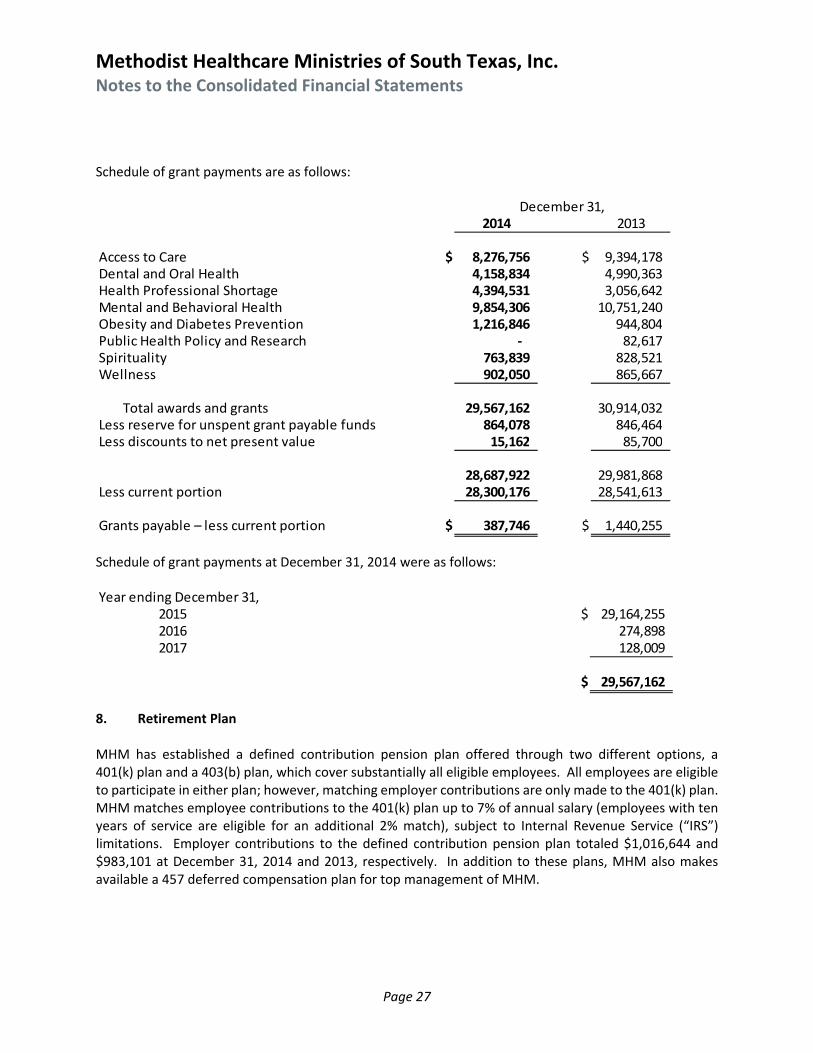

Schedule of grant payments are as follows:

2014 2013

Access to Care $ 8,276,756 $ 9,394,178Dental and Oral Health 4,158,834 4,990,363Health Professional Shortage 4,394,531 3,056,642Mental and Behavioral Health 9,854,306 10,751,240Obesity and Diabetes Prevention 1,216,846 944,804Public Health Policy and Research ‐ 82,617Spirituality 763,839 828,521Wellness 902,050 865,667

Total awards and grants 29,567,162 30,914,032Less reserve for unspent grant payable funds 864,078 846,464Less discounts to net present value 15,162 85,700

28,687,922 29,981,868Less current portion 28,300,176 28,541,613

Grants payable – less current portion $ 387,746 $ 1,440,255

December 31,

Schedule of grant payments at December 31, 2014 were as follows: Year ending December 31,

2015 $ 29,164,2552016 274,8982017 128,009

$ 29,567,162

8. Retirement Plan MHM has established a defined contribution pension plan offered through two different options, a 401(k) plan and a 403(b) plan, which cover substantially all eligible employees. All employees are eligible to participate in either plan; however, matching employer contributions are only made to the 401(k) plan. MHM matches employee contributions to the 401(k) plan up to 7% of annual salary (employees with ten years of service are eligible for an additional 2% match), subject to Internal Revenue Service (“IRS”) limitations. Employer contributions to the defined contribution pension plan totaled $1,016,644 and $983,101 at December 31, 2014 and 2013, respectively. In addition to these plans, MHM also makes available a 457 deferred compensation plan for top management of MHM.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 28

9. Commitments and Contingencies Certain conditions may exist as of the date the consolidated financial statements are issued, which may result in a loss to MHM, but which will only be resolved when one or more future events occur or fail to occur. MHM’s management and its legal counsel assess such contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to legal proceedings that are pending against MHM or unasserted claims that may result in such proceedings, MHM’s legal counsel evaluates the perceived merits of any legal proceedings or unasserted claims, as well as the perceived merits of the amount of relief sought or expected to be sought therein. If the assessment of a contingency indicates it is probable that a material loss has been incurred and the amount of the liability can be estimated, then the estimated liability would be accrued in MHM’s consolidated financial statements. If the assessment indicates a potentially material loss contingency is not probable, but is reasonably possible, or is probable, but cannot be estimated, then the nature of the contingent liability, together with an estimate of the range of possible loss, if determinable and material, would be disclosed. Loss contingencies considered remote are generally not disclosed unless they involve guarantees, in which case the guarantees would be disclosed. MHM is involved in claims and litigation in the normal course of business. Management believes the applicable insurance coverage is adequate to cover costs of settlement and defense of such claims and litigation. Malpractice claims that fall within the Hospital/MHM’s adopted policy of self‐insurance (see Note 1) could be asserted against the Hospital/MHM. There could be additional incidents that could have occurred through January 10, 1995, which may result in the assertion of additional claims. Management has no knowledge of potential claims. In July 2014, MHM renewed its agreement with Frost Bank for a $50,000,000 revolving line of credit with a variable rate at one month LIBOR plus 1.5% and a maturity date of September 2015. The line imposes certain minimum investment balance restrictions. There was no amount outstanding on this line of credit as of December 31, 2014 and 2013.

Methodist Healthcare Ministries of South Texas, Inc. Notes to the Consolidated Financial Statements

Page 29

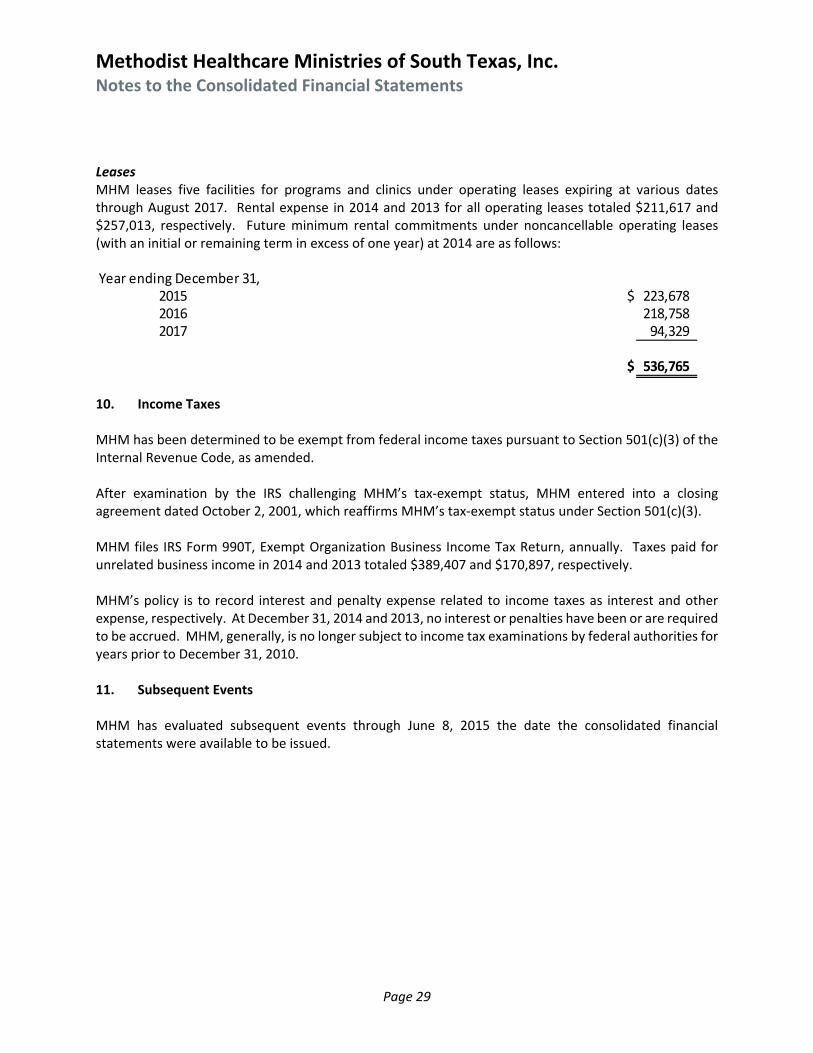

Leases MHM leases five facilities for programs and clinics under operating leases expiring at various dates through August 2017. Rental expense in 2014 and 2013 for all operating leases totaled $211,617 and $257,013, respectively. Future minimum rental commitments under noncancellable operating leases (with an initial or remaining term in excess of one year) at 2014 are as follows: Year ending December 31,

2015 $ 223,6782016 218,7582017 94,329

$ 536,765

10. Income Taxes MHM has been determined to be exempt from federal income taxes pursuant to Section 501(c)(3) of the Internal Revenue Code, as amended. After examination by the IRS challenging MHM’s tax‐exempt status, MHM entered into a closing agreement dated October 2, 2001, which reaffirms MHM’s tax‐exempt status under Section 501(c)(3). MHM files IRS Form 990T, Exempt Organization Business Income Tax Return, annually. Taxes paid for unrelated business income in 2014 and 2013 totaled $389,407 and $170,897, respectively. MHM’s policy is to record interest and penalty expense related to income taxes as interest and other expense, respectively. At December 31, 2014 and 2013, no interest or penalties have been or are required to be accrued. MHM, generally, is no longer subject to income tax examinations by federal authorities for years prior to December 31, 2010. 11. Subsequent Events MHM has evaluated subsequent events through June 8, 2015 the date the consolidated financial statements were available to be issued.